Masco Corporation: From Auto Parts to Home Improvement Empire

I. Introduction & Episode Roadmap

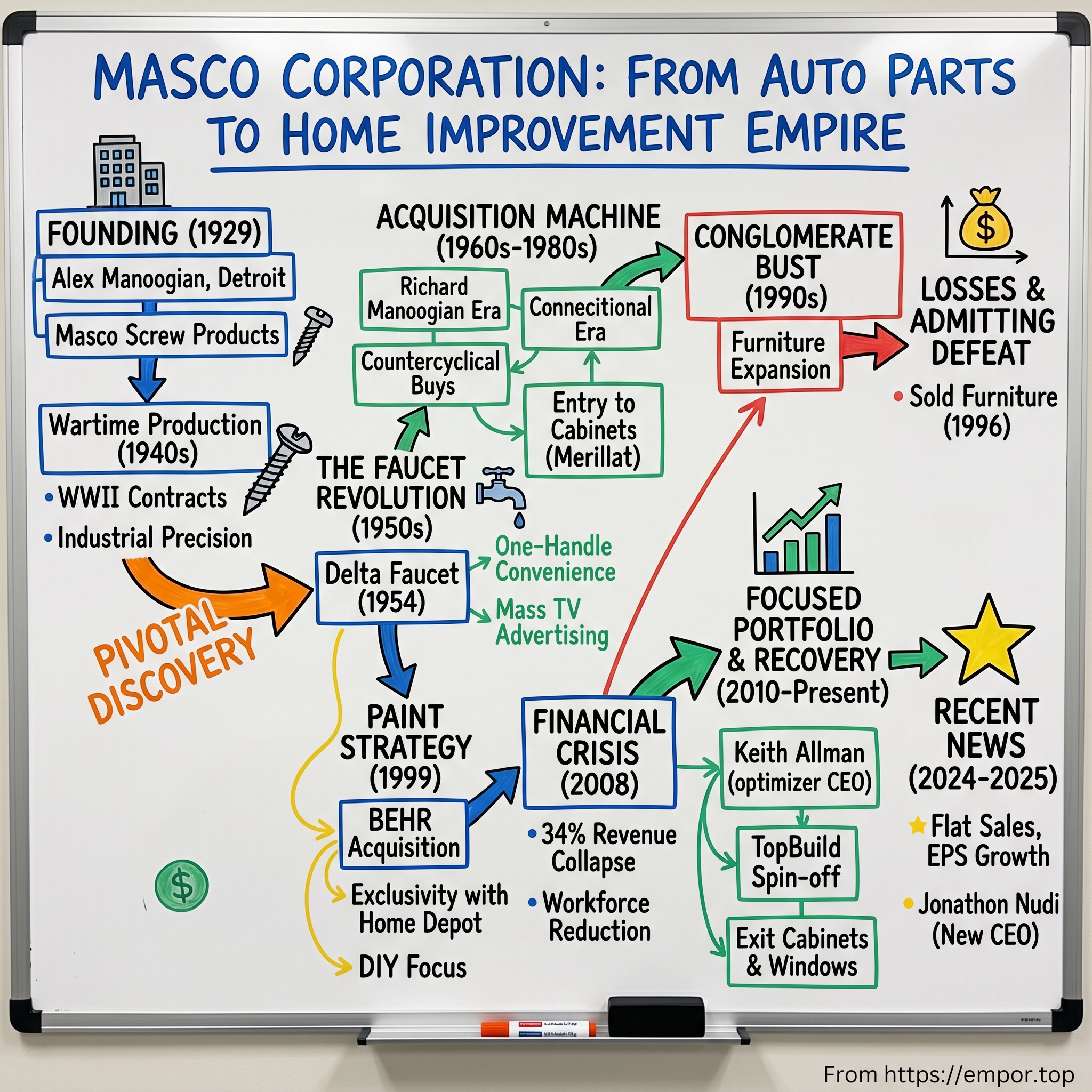

The calendar read December 16, 1929. Six weeks had passed since Black Tuesday sent shockwaves through Wall Street, wiping out fortunes and launching America into the Great Depression. While titans of industry watched their empires crumble, a 28-year-old Armenian immigrant named Alex Manoogian was signing papers to incorporate a tiny screw machine shop in Detroit. The company, Masco Screw Products, would start life on the fourth floor of a decrepit building on Fort Street—directly above the Wayne County Morgue. The symbolism was almost too perfect: while American capitalism lay dying below, Manoogian was birthing what would become a $7.8 billion home improvement colossus.

How does a Depression-era machine shop, founded with $5,000 and a couple of used lathes, transform into one of America's premier building products conglomerates? The answer isn't just about timing or luck—it's about recognizing that every great American housing boom needs its picks and shovels. From the post-war suburban explosion to the DIY revolution, from the housing bubble to today's remote work renovation surge, Masco has been there, quite literally building the American Dream one faucet, one paint can, one cabinet at a time.

This is a story of immigrant grit meeting industrial opportunity. Of a father who fled genocide with $50 in his pocket and built an empire, and a son who transformed that empire through 42 acquisitions worth $10 billion. It's about the serendipitous discovery that turned a failing "one-armed bandit" faucet into the revolutionary Delta brand. About riding macro trends so perfectly that you appear on the Fortune 500 just as America falls in love with home improvement. And yes, it's about surviving when those same trends turn vicious—when the 2008 financial crisis obliterated half your market value and forced you to rethink everything.

The themes we'll explore ripple through American business history: immigrant entrepreneurship that sees opportunity where others see only struggle; product innovation through acquisition rather than pure R&D; the power of channel partnerships that lock in distribution before competitors wake up; and perhaps most importantly, the discipline to know when your conglomerate dreams have become nightmares. Because while Masco's ascent is remarkable, its ability to reinvent itself—to shed businesses worth billions when they no longer fit—might be even more instructive.

From that morgue-adjacent machine shop to today's focused portfolio of premium brands like Delta, Behr, and Hansgrohe, Masco's journey mirrors the evolution of American consumer capitalism itself. It's a masterclass in riding secular trends, managing through cycles, and understanding that sometimes the best acquisition is actually a divestiture. Let's dive into how a company nobody's heard of became the invisible force behind millions of American home improvements.

II. The Alex Manoogian Story & Founding Context

The ship that carried 19-year-old Alex Manoogian to America in 1920 wasn't bearing a future industrialist—it was saving a refugee's life. As a Christian Armenian in Muslim Turkey, Manoogian had witnessed the systematic extermination of his people. The Armenian Genocide had claimed over a million lives, including members of his own family. He arrived at Ellis Island with $50, no English, and the kind of desperation that either breaks you or forges you into steel. For Manoogian, it would be the latter.

Bridgeport, Connecticut became his first American classroom. He took whatever work he could find—dishwasher, factory hand, laborer—but it was a brief stint at a screw machine business that captured his imagination. Here was precision, repetition, quality—concepts that transcended language barriers. The machines spoke in tolerances and measurements, a universal tongue he could master. By 1924, he'd saved enough to move to Detroit, the roaring heart of American industry, where the automobile boom was creating unprecedented demand for precision metal components.

Detroit in the 1920s was America's Silicon Valley—a place where mechanical innovation met entrepreneurial ambition. Manoogian found work in another screw machine shop, but now he wasn't just operating equipment; he was studying the business itself. How contracts were won. How relationships with auto manufacturers developed. How a handful of machines could generate substantial cash flow if you could guarantee quality and delivery. By 1929, after five years of learning and saving, he was ready to bet everything on his own venture.

The timing seemed catastrophic. On October 29, 1929—Black Tuesday—the stock market lost $14 billion in value, equivalent to $200 billion today. Banks failed. Businesses shuttered. Unemployment would soon reach 25%. Yet six weeks later, Manoogian and two partners pooled $5,000 to buy secondhand equipment and incorporate Masco Screw Products Company. The name itself was pragmatic—an acronym from the partners' surnames (Manoogian, Saunders, and Coury) plus "co" for company. No grand vision statements. No delusions of empire. Just three men believing they could make better screws than anyone else, even as the economy collapsed around them.

The company's first headquarters would have discouraged anyone with less determination. The fourth floor of a dilapidated building on Detroit's Fort Street was accessible only by a freight elevator that worked sporadically. The floors below housed the Wayne County Morgue, filling the stairwells with formaldehyde fumes. In summer, the metal equipment turned the space into a furnace. In winter, workers wore gloves to prevent their skin from freezing to the machinery. But Manoogian had fled worse. This wasn't suffering—this was opportunity.

The first breakthrough came from Hudson Motor Car Company, a $7,000 contract for precision parts. But Masco couldn't afford to pay salaries yet, so Manoogian struck a deal with his workers: take IOUs now, get paid when Hudson pays us. It was a trust exercise that would have been impossible without Manoogian's reputation in Detroit's tight-knit manufacturing community. He wasn't just another boss—he was one of them, a machinist who understood the work, who could operate every piece of equipment on the floor.

Depression-era survival required adaptation. When automotive orders dried up, Masco pivoted to whatever industries still had cash: oil field equipment, electrical components, even toy parts. Manoogian instituted a policy that would define the company's culture for decades: no job too small, no specification too demanding. If you needed a custom screw made to aerospace tolerances for a consumer product price, Masco would figure it out. This flexibility—really, this desperation-driven ingenuity—kept the lights on when established competitors were failing weekly.

By 1936, something remarkable had happened. Not only had Masco survived the Depression's worst years, it had grown. Employment reached 35 people. Revenue approached $200,000 annually. The company moved to a proper factory on Detroit's west side. And in 1937, in a move that demonstrated stunning confidence, Masco went public on the Detroit Stock Exchange. A Depression-era startup founded by an immigrant with $50 to his name was now a publicly traded company.

World War II transformed everything. Suddenly, precision metal components weren't just industrial supplies—they were instruments of national survival. Masco's factory ran three shifts, seven days a week, producing parts for tanks, aircraft, and weapons systems. By 1942, revenue exceeded $1 million. The company that had started in a morgue-adjacent loft now employed over 500 people. Manoogian had achieved something remarkable: leadership position in the metalworking sector, recognition from the War Department for production excellence, and enough capital to think beyond mere survival.

But the real transformation was internal. The war had taught Manoogian that Masco's core competency wasn't making screws—it was solving complex metalworking problems under extreme pressure. Whether the customer was Hudson Motor Car or the U.S. Army, the challenge was the same: deliver quality, on time, at scale. This realization would prove crucial when, a decade later, a failing faucet design would land on his desk—a problem that had nothing to do with automobiles but everything to do with precision metalworking.

As the war ended and America pivoted from destroying to building, Manoogian sensed opportunity beyond automotive components. The returning GIs would need homes. Those homes would need fixtures, fittings, and the countless metal components that turn a structure into a dwelling. The question wasn't whether to diversify beyond automotive—it was how and when. The answer would come from an unexpected source: two Armenian friends in California with a revolutionary faucet design that didn't work.

III. The Delta Faucet Revolution (1952–1961)

The meeting that would transform Masco from a parts supplier into a consumer brand powerhouse began, as many pivotal moments do, with a problem nobody else wanted to solve. In 1952, Alex Manoogian received an unusual request from two Armenian friends in California. They'd developed a single-handle faucet—a radical departure from the standard two-handle designs that had dominated American bathrooms since indoor plumbing began. But their innovation had earned a devastating nickname from plumbers: the "one-armed bandit." It leaked. It broke. It was, by most accounts, a disaster.

Manoogian's friends wanted him to manufacture brass components for their troubled faucet. Most suppliers would have run from such a problematic product. But Manoogian saw something others missed: the core concept was brilliant, even if the execution was fatally flawed. Americans were entering an era of push-button convenience—automatic transmissions, electric can openers, TV remote controls. Why should adjusting water temperature require a two-handed juggling act? The single-handle faucet wasn't just an improvement; it was inevitable.

Rather than simply supply parts, Manoogian made a bold proposition: sell him the rights to the entire design. He would fix it. His friends, exhausted from complaints and returns, agreed. What followed was a masterclass in engineering iteration that only someone with Manoogian's decades of metalworking experience could execute. He didn't just tweak the existing design—he reimagined it from the inside out.

The breakthrough was the ball valve principle. Instead of rubber washers that degraded and complex stem assemblies that seized, Manoogian's team developed a stainless steel ball that rotated smoothly within a precisely machined housing. Moving the single lever adjusted both flow rate and temperature mixture simultaneously—engineering elegance that made the previous two-handle standard look prehistoric. The ball valve could handle water pressure variations, mineral deposits, and temperature extremes that destroyed conventional faucets. It was, quite literally, bulletproof plumbing.

But engineering excellence means nothing without market acceptance, and here Manoogian demonstrated marketing genius that rivaled his technical prowess. He named the product Delta—suggesting both change and precision (like the Greek letter's mathematical usage). The name also cleverly avoided any reference to the product's troubled history as the "one-armed bandit." This was a fresh start, a premium product for a modernizing America.

The real innovation, however, came in distribution and marketing. In 1954, when Delta faucets officially launched, the plumbing industry operated like a medieval guild. Plumbers recommended products to wholesalers, who sold to plumbers, who installed for consumers. The end user—the actual homeowner—had virtually no say in faucet selection. Manoogian decided to break this closed loop with a weapon no faucet company had ever deployed: television advertising.

The first Delta television commercials in 1956 were revolutionary not for their production value—they were simple demonstrations—but for their very existence. Here was a faucet company speaking directly to housewives (the primary household decision-makers of the era) about a product they'd never thought to care about. The message was simple: "You don't have to accept what your plumber suggests. Ask for Delta by name." The plumbing establishment was furious. Consumers were delighted.

Sales data tells the story. In 1954, Delta's first year, revenue was negligible—perhaps $100,000. By 1958, annual sales exceeded $1 million. By 1960, they'd reached $5 million. This wasn't just growth; it was market creation. Delta wasn't stealing share from other faucet makers as much as it was convincing Americans that their faucet was a choice worth making, a statement about their home's modernity.

The success attracted someone else's attention: Richard Manoogian, Alex's son. Richard had just graduated from Yale with an economics degree, and his father wanted him to learn the business from the ground up. In 1958, Alex assigned Richard to oversee construction and launch of a new Delta factory in Greensburg, Indiana—a facility that would become the largest faucet manufacturing plant in America.

The choice of Greensburg was strategic. Indiana offered lower labor costs than Detroit, proximity to brass suppliers, and—critically—distance from the automotive industry's boom-bust cycles. Richard's successful launch of the facility demonstrated he had inherited his father's operational excellence. But he brought something else: an economist's understanding of market dynamics and acquisition strategy. While Alex built great products, Richard would build an empire.

By 1961, Delta faucets accounted for more than half of Masco's total revenue. The transformation was complete: a Depression-era auto parts supplier had become a consumer products company. The board recognized this fundamental shift by officially changing the company name from Masco Screw Products Company to simply Masco Corporation. It was more than rebranding—it was a declaration of intent. The screw business had given them capabilities. The faucet business had given them a platform. Now Richard would show them how to use that platform to roll up an entire industry.

The Delta story established a template that Masco would follow for decades: find a fragmented industry with outdated practices, acquire a transformative product or brand, professionalize the operations, and market directly to end consumers. It was a playbook that would generate billions in value. But first, Richard had to convince his father that the family business wasn't about making things—it was about owning the things that make American homes work.

IV. The Acquisition Machine: Richard's Era Begins (1961–1985)

Richard Manoogian didn't ease into leadership—he exploded into it. Where his father had built Masco through patient craftsmanship and engineering excellence, Richard brought a Yale economist's appetite for strategic acquisition and financial engineering. His first major move in 1961, acquiring Peerless Industries, a struggling plumbing products manufacturer, signaled a fundamental shift in Masco's DNA. This wasn't about buying technology or talent. It was about buying market position, distribution relationships, and the inefficiencies Richard knew he could eliminate.

Peerless was a classic Richard target: a family-owned business with decent products, terrible operations, and owners ready to retire. He paid with a combination of cash and Masco stock, keeping the sellers invested in the upside while gaining immediate control. Within eighteen months, Peerless's margins had doubled simply by applying Masco's manufacturing disciplines. But Richard saw something bigger—Peerless's distribution network perfectly complemented Delta's. Suddenly, Masco could offer plumbers and wholesalers a full suite of products, increasing wallet share while reducing sales costs.

By 1962, Delta faucet sales had reached $7 million, validating Richard's thesis that the plumbing industry was ripe for consolidation. But he wasn't content with organic growth. While competitors focused on stealing market share points from each other, Richard was playing a different game entirely: he wanted to own the whole board. His acquisition pace accelerated: Brass Craft Manufacturing (valves and fittings), Brasswind (decorative hardware), Allied Brass (commercial fixtures). Each deal followed the same pattern—identify family businesses with strong brands but weak operations, acquire them at reasonable multiples, then transform them through Masco's operational excellence.

The financial markets took notice. In 1969, Masco achieved a milestone that would have seemed impossible to Alex Manoogian standing in that morgue-adjacent factory: listing on the New York Stock Exchange. The ticker symbol, MAS, began trading at $23 per share, valuing the company at over $100 million. Richard used this currency brilliantly, offering sellers the choice between cash or stock, often convincing them that Masco shares were the better long-term bet. He was usually right—the stock would quadruple over the next five years.

But Richard's true genius lay in recognizing that Masco wasn't really in the faucet or valve business—it was in the "installed products" business. Every acquisition targeted products that required professional installation, created switching costs, and touched consumers' daily lives. This wasn't just diversification; it was ecosystem building. When a plumber recommended Delta faucets, they could also suggest Brasscraft supply lines, Peerless shower systems, and Allied commercial fixtures—all from Masco's portfolio, all generating margins that made pure manufacturing look like charity work.

The 1970s brought challenges that would have crushed a less adaptable company. The oil crisis. Stagflation. Interest rates exceeding 20%. Housing starts collapsed from 2.4 million in 1972 to barely 1 million in 1975. Yet Masco didn't just survive—it thrived through what Richard called "countercyclical acquisition." While competitors conserved cash, Masco went shopping, acquiring distressed assets at fraction of replacement cost. When the economy recovered, Masco owned significantly more market share without having fought for it.

The numbers from this era are staggering. In 1970, Masco's revenue was $118 million. By 1975—despite the worst recession since the 1930s—revenue had nearly tripled to $341 million. That same year, Masco first appeared on the Fortune 500 list at number 460. The immigrant's son running his father's screw machine shop was now CEO of one of America's 500 largest corporations. But Richard was just getting started.

The creation of Masco Industries in 1984 demonstrated Richard's strategic sophistication. Rather than abandon the automotive components business that had sustained the company through the Depression, he spun it into a separately traded entity. This gave automotive suppliers and customers a pure-play investment while allowing Masco Corporation to maintain majority control. It was financial engineering at its finest—creating value through structure rather than operations. The market loved it, pushing Masco's combined market capitalization above $1 billion for the first time.

The year 1984 also marked another milestone: Masco's annual sales exceeded one billion dollars. From $7,000 in Depression-era survival to $1 billion in Reagan-era prosperity—the journey had taken 55 years and hundreds of acquisitions. But Richard's masterstroke came in 1985 with two acquisitions that would define Masco's next chapter: Merillat Industries, America's largest cabinet manufacturer, and Flint and Walling Water Systems, a leader in water pumps and well systems.

Merillat was particularly significant. Cabinets represented a massive adjacent market—larger than faucets, equally fragmented, and perfectly suited to Masco's consolidation playbook. The $136 million acquisition instantly made Masco a major player in kitchen remodeling, opening relationships with contractors and designers who had never specified plumbing products. It was ecosystem expansion at its finest.

That same year, Masco introduced the largest faucet selection in the industry's history—over 2,000 SKUs across multiple brands and price points. This wasn't product proliferation for its own sake; it was market segmentation mathematics. Different brands for different channels, price points for every wallet, styles for every taste. Competitors could compete with one or two Masco brands, but nobody could match the entire portfolio's breadth.

By 1985, Richard had transformed his father's precision manufacturing company into something unprecedented: a home improvement conglomerate built through acquisition rather than internal development. The strategy was so successful that Harvard Business School would later write multiple case studies on the "Masco Model." But Richard wasn't done. If the first phase was about buying companies, the next phase would be about buying entire categories. The furniture industry was about to meet its most ambitious consolidator.

V. The Conglomerate Years: Furniture, Hardware & Global Expansion (1985–1999)

Richard Manoogian stood in the boardroom of Henredon Furniture in 1986, examining handcrafted tables that cost more than most Americans' cars. The contrast with Masco's industrial heritage couldn't have been starker—here was Southern aristocracy meeting Detroit pragmatism. Yet Richard saw past the cultural mismatch to a compelling financial logic: furniture was a $50 billion industry, completely fragmented, with terrible operations and fat margins begging for rationalization. He wrote a check for $298 million, then immediately flew to North Carolina to acquire Drexel Heritage for $356 million more. In six months, Masco had bet over $650 million that it could revolutionize furniture the way it had transformed faucets.

The furniture thesis seemed brilliant on paper. Like plumbing products, furniture touched every American home. Like faucets in the 1950s, the industry was dominated by small family firms with inconsistent quality and antiquated distribution. Richard envisioned applying Masco's operational excellence to furniture manufacturing while leveraging relationships with Home Depot and other retailers to bypass traditional furniture stores' markup-heavy model. What he didn't anticipate was that furniture was fundamentally different from faucets in one crucial way: fashion.

A faucet needs to work. Furniture needs to work and be beautiful, with beauty's definition changing every season. While Masco's engineers could perfect a ball valve that would last decades, they couldn't predict whether consumers would want Colonial, Contemporary, or Country styling next year. Inventory that was perfectly good became perfectly worthless when tastes shifted. The furniture division's warehouses filled with beautiful, well-made pieces that nobody wanted to buy—a problem Masco had never encountered with utilitarian plumbing products.

While wrestling with furniture, Richard didn't slow his acquisition pace elsewhere. The 1988 reorganization that created TriMas Corporation showcased his increasingly complex financial engineering. TriMas combined various specialty industrial products—towing systems, fasteners, precision tools—that didn't fit Masco's consumer focus. Rather than sell these businesses, Richard packaged them into a separate public company, maintaining control while creating a new currency for industrial acquisitions. When TriMas went public in 1991, it added another $500 million to Masco's enterprise value without selling a single asset.

The global expansion accelerated through the 1990s. Masco acquired Hansgrohe, the German luxury faucet manufacturer, for $1.3 billion—a stunning price that made sense only when you understood Richard's strategy. Hansgrohe didn't just bring European engineering and design; it brought entrée to markets where American brands were considered unsophisticated. Suddenly, Masco could sell to luxury hotels in Dubai, apartments in Shanghai, and villas in Monaco. The acquisition also brought something intangible but valuable: European design sensibility that would elevate Masco's entire portfolio.

The numbers from this era reveal both triumph and trouble. Revenue soared from $1 billion in 1984 to over $6 billion by 1996. Masco operated manufacturing facilities in 21 countries, employed over 30,000 people, and controlled leading market positions in dozens of categories. Yet the furniture division was hemorrhaging cash. In 1996, Richard made one of the hardest decisions of his career: admitting defeat. Masco sold most of its Home Furnishings Division to investors for $1.1 billion, creating a new company called LifeStyle Furnishings International. The loss on the investment was staggering—nearly $650 million—but Richard understood sunk cost fallacy better than most CEOs. The furniture adventure was over.

Between 1997 and 2002, freed from furniture's drag, Richard returned to what Masco did best: rolling up fragmented building products categories. The acquisition pace was breathtaking—42 companies valued at $10 billion total. The deals ranged from tiny specialized manufacturers to billion-dollar brands. Arrow Fastener. Vapor Technologies. Tvilum-Scanbirk. Cobra Products. Each brought either technology, market access, or brand equity that enhanced Masco's ecosystem. Richard had learned from furniture: stick to products that improve with engineering, not fashion.

The late 1990s also saw Masco's most successful product launch since Delta: the Peerless pull-out kitchen faucet. It seems simple now—a faucet head that extends on a hose—but it revolutionized kitchen functionality. More importantly, it demonstrated that even in mature categories, innovation could drive premium pricing. The pull-out faucet sold for 40% more than standard models while costing only marginally more to manufacture. It was the kind of margin expansion that made Wall Street swoon.

By 1999, as the millennium approached, Masco looked nothing like the company Alex Manoogian had founded 70 years earlier. Revenue approached $8 billion. The stock had returned over 20% annually for two decades. The company controlled leading positions in faucets, cabinets, locks, and dozens of other categories. But Richard, now 63, had one more transformative acquisition in mind—one that would either crown his legacy or tarnish it. He was about to bet billions on paint, a category Masco had never touched, through a company called Behr that had spent 52 years perfecting one thing: selling paint to do-it-yourselfers.

The furniture debacle had taught Richard that Masco needed to stay within its competency zone. But what exactly was that zone? Not furniture, clearly. But paint? Paint was closer to Masco's core than it initially appeared. It was a consumable home improvement product, sold through the same channels as faucets and cabinets, requiring similar contractor relationships. Most importantly, it was a category where brand, quality, and distribution mattered more than fashion. Richard was about to make his biggest bet yet.

VI. The Behr Acquisition & Paint Strategy (1999)

The meeting between Richard Manoogian and Jeffrey Behr in early 1999 took place not in a boardroom but in a Home Depot store in Orange County, California. Jeffrey, son of founder Otho Behr Jr., walked Richard through the paint aisle, pointing out a remarkable fact: Behr commanded more shelf space than Glidden, Dutch Boy, and Ralph Lauren combined. In this store—and increasingly across Home Depot's thousand-plus locations—Behr wasn't just a paint brand. It was the paint brand. Richard saw immediately what others had missed: Behr had cracked the code on the most important retail partnership in American home improvement.

The Behr story began in 1947 when Otho Behr Jr., a chemist, started selling linseed oil to California furniture manufacturers from his garage. Over five decades, the family had built a regional paint powerhouse through obsessive focus on product quality and customer service. But their masterstroke came in 1983 when they signed an exclusive partnership with a rapidly growing retailer called Home Depot. While established paint giants like Sherwin-Williams and Benjamin Moore dismissed Home Depot as a discounter that would cheapen their brands, Behr went all-in. The genius of the Behr partnership wasn't just exclusivity—it was the alignment of incentives. Behr invested heavily in Home Depot-specific services: computerized color-matching systems, in-store training programs, dedicated merchandising teams. Home Depot, in return, gave Behr unprecedented control over the paint department layout, staffing, and promotion. Competitors could sell through Home Depot's rivals like Lowe's, but they couldn't match the operational integration Behr had achieved. By 1999, this symbiosis had made Behr the fastest-growing paint brand in America.

When Richard announced the acquisition in September 1999, the numbers were staggering: Masco was acquiring five companies with combined annual sales exceeding $1.5 billion for approximately $3.8 billion in cash and stock. Behr was the crown jewel of this package, but the deal also included Tvilum-Scanbirk (European furniture), Mill's Pride (cabinets), and two other building products companies. The acquisition marked the end of Behr's 52-year run as a private company.

The strategic logic was compelling. Paint was a $20 billion annual market in the United States, growing at 3-4% annually, with virtually no cyclicality compared to other building products. Unlike faucets or cabinets, paint was consumable—Americans repainted rooms every 3-7 years, creating recurring revenue streams. The gross margins were exceptional, often exceeding 40%, and brand loyalty was surprisingly strong once consumers found colors and formulations they trusted.

But Richard saw something deeper: paint was the gateway drug of home improvement. A couple deciding to repaint their kitchen would often upgrade their faucet, replace cabinet hardware, maybe even install new lighting. Paint projects triggered cascading renovation decisions. By owning Behr, Masco could influence the beginning of the home improvement journey, positioning its other brands for consideration. It was ecosystem thinking at its most sophisticated.

The integration strategy was counterintuitive. Rather than folding Behr into Masco's existing operations, Richard kept it largely independent. The Behr family's Santa Ana headquarters remained the nerve center. Jeffrey Behr stayed on as president. The company culture—entrepreneurial, fast-moving, obsessed with Home Depot's success—was preserved. Masco provided capital for expansion, acquisition opportunities, and operational best practices, but didn't tamper with the formula that had made Behr successful.

The Home Depot relationship deepened post-acquisition. With Masco's balance sheet behind it, Behr could invest in innovations that smaller competitors couldn't afford: advanced tinting machines that could match any color from a photograph, augmented reality apps that let customers visualize paint colors on their actual walls, premium formulations that justified higher price points. Each innovation strengthened the moat around Behr's Home Depot exclusivity.

The acquisition strategy continued with Masco acquiring Masterchem Industries Inc., the maker of the KILZ brand, expanding the paint portfolio to include primers and specialty coatings. KILZ was to primer what Delta had been to faucets—a category-defining brand with exceptional margins. Together, Behr and KILZ gave Masco a complete architectural coatings platform, from primer to topcoat, from DIY to professional.

The financial impact was immediate and substantial. In 1999, with the Behr acquisition, Masco's annual sales topped five billion dollars for the first time. Paint quickly became one of Masco's most profitable divisions, generating returns on invested capital that exceeded 20% annually. Wall Street rewarded the strategic clarity, pushing Masco's stock to all-time highs.

But perhaps the most important outcome was validation of Richard's evolved strategy. After the furniture debacle, many questioned whether Masco could successfully expand beyond its traditional plumbing and cabinet categories. Behr proved that with the right partner, the right channel strategy, and the right hands-off integration approach, Masco could enter entirely new categories and dominate them. It was a lesson that would prove invaluable when, less than a decade later, the financial crisis would force Masco to completely reimagine its portfolio once again.

VII. Crisis & Transformation: 2008 Financial Meltdown

The numbers from 2006 should have been a warning. Housing starts peaked at 2.3 million units in January, then began a decline so gradual that most executives dismissed it as a healthy cooling after years of unsustainable growth. Richard Manoogian, now 70 and running Masco for four decades, had seen cycles before. The company had survived the 1970s stagflation, the early 1980s recession, the dot-com bust. This felt different, but nobody—not Richard, not Wall Street, not the Federal Reserve—understood they were standing at the edge of an economic cliff.

By December 2007, when the National Bureau of Economic Research officially declared a recession, Masco's stock had already fallen 40% from its 2006 peak. But the real carnage was just beginning. The subprime mortgage crisis wasn't just destroying banks; it was obliterating the entire ecosystem of American home improvement. Foreclosures meant empty houses. Empty houses meant no paint sales, no faucet replacements, no cabinet upgrades. Home Depot, Masco's largest customer, saw same-store sales decline for 13 consecutive quarters. Lowe's fared no better. The professional contractor market—responsible for 40% of Masco's revenue—essentially ceased to exist as construction unemployment reached 27%.

Masco's total revenue collapsed from $11.77 billion in 2007 to $7.8 billion in 2009—a 34% decline that represented the evaporation of $4 billion in annual sales. To put this in perspective, Masco lost more revenue in two years than most Fortune 500 companies generate in a decade. The installation services business, which had seemed so strategic during the housing boom, became an albatross as new construction virtually stopped. Factories that had run three shifts were reduced to one. Some closed entirely.

The human toll was devastating. Masco reduced its workforce from 32,500 to barely 20,000 employees. These weren't just numbers on a spreadsheet—they were skilled craftspeople, many who had spent decades with the company. The cuts went deep into management too. Entire divisions were eliminated. The corporate jet was sold. Executive compensation was slashed. Richard Manoogian, who had built his reputation on growth through acquisition, was now presiding over the controlled demolition of his empire.

But crisis reveals character, and Masco's response demonstrated why great companies survive when good companies disappear. Rather than wait for recovery, the leadership team initiated a transformation program that would fundamentally restructure the company. The first decision was painful but necessary: exit businesses that no longer fit, regardless of sunk costs. The installation services division, which had generated $2 billion in revenue at its peak, was prepared for spin-off. The European furniture operations were sold. Non-core brands were divested or shut down.

The strategic pivot was profound. For decades, Masco had been a conglomerate that happened to focus on home improvement. Now it would become a pure-play branded building products company. The new strategy had three pillars: focus on repair and remodel rather than new construction, prioritize products with replacement cycles rather than discretionary purchases, and invest in brands that commanded pricing power even in downturns. It meant saying goodbye to the empire-building that had defined Richard's era and hello to a leaner, more focused future.

The Windows and doors business became a particular flashpoint. Once seen as a natural extension of Masco's building products portfolio, it had become a capital-intensive nightmare. The business required massive manufacturing facilities, complex logistics, and brutal competition from low-cost imports. In 2009, the division lost over $200 million. The board faced a stark choice: invest hundreds of millions more to achieve competitive scale, or admit defeat and exit. They chose the latter, beginning a multi-year process to divest the division.

Amid the carnage, some divisions showed remarkable resilience. Behr paint, protected by its Home Depot exclusivity, maintained most of its market share even as volumes declined. Delta faucets, now a billion-dollar brand, benefited from the trend toward home improvement as a substitute for moving. The plumbing division's focus on repair and replacement—faucets break regardless of economic conditions—provided some stability. These bright spots validated the new strategic focus: branded, non-discretionary products sold through protected channels.

The financial engineering during this period was equally important. Masco renegotiated credit facilities, extending maturities and loosening covenants before conditions worsened further. The company suspended share buybacks, conserving cash that would prove critical for survival. Most painfully for a company that had increased its dividend for 51 consecutive years, the board cut the quarterly payout by 70%. It was an admission that the old Masco—the reliable dividend aristocrat—was gone.

By 2010, green shoots of recovery were visible. Housing starts, while still depressed at 600,000 units annually, had stopped falling. Home improvement spending showed signs of life as Americans who couldn't sell their homes decided to improve them instead. Masco's restructuring was bearing fruit: despite revenues remaining 35% below peak, profitability was recovering due to the leaner cost structure. The company that emerged from the crisis was smaller but stronger, focused but flexible.

The 2008 financial crisis had done what four decades of competition couldn't: it forced Masco to choose what it wanted to be. The answer was clear: not the biggest home improvement conglomerate, but the best branded building products company. The transition would take another decade to complete, but the direction was set. The age of empire-building was over. The age of optimization had begun.

VIII. Modern Era: Focused Portfolio & Recovery (2010–Present)

Keith Allman stood before Masco's shareholders in May 2015 with a radical proposition: destroy $2 billion in revenue to create value. The installation services business—once Richard Manoogian's vision for integrated home improvement—would be spun off as TopBuild, an independent public company. The decision represented more than strategic restructuring; it was philosophical revolution. The Masco that had spent 70 years acquiring everything was now systematically shedding anything that didn't fit a narrow definition of branded building products excellence.

The TopBuild spinoff, completed in 2015, separated 100% of Masco's Installation and Other Services segment into an independent, publicly-traded company. The market's reaction was telling: both companies' stocks rose. Investors had been begging for this focus for years, frustrated by the complexity of analyzing a company that sold both luxury faucets and installed fiberglass insulation. TopBuild would go on to thrive as a pure-play installation company, while Masco could finally be valued as the branded products company it had become.

But Allman wasn't done. In 2019, he made an even bolder decision: exit the cabinet and windows businesses entirely. These weren't failing divisions—KraftMaid cabinets and Milgard windows were profitable, recognized brands. But they were capital-intensive, cyclical, and lacked the pricing power of Masco's plumbing and paint divisions. The divestitures would remove another $2 billion in revenue, shrinking Masco to roughly half its pre-crisis size. Yet the remaining business would generate higher margins, better returns on capital, and more predictable cash flows.

The windows exit was particularly symbolic. Windows had been Masco's entry into the new construction market, a bet that the company could leverage its manufacturing expertise beyond replacement products. The sale to MI Windows and Doors for $725 million represented admission that manufacturing excellence alone wasn't enough—you needed brands that commanded premium pricing regardless of market conditions. Windows, commoditized by imports and private label competition, would never achieve Delta's or Behr's margins.

The cabinet divestiture was more complex emotionally. Merillat, acquired in 1985, had been one of Richard Manoogian's signature deals. KraftMaid, Quality Cabinets, and Cardell represented decades of investment and integration. But the cabinet market had fundamentally changed. Chinese imports, flat-pack retailers like IKEA, and Home Depot's private label offerings had compressed margins beyond recovery. The sale to ACProducts for $850 million freed Masco from a grinding war of attrition it couldn't win.

What remained was a focused portfolio of two segments: Plumbing Products and Decorative Architectural Products. The plumbing division housed the crown jewels—Delta, Hansgrohe, Peerless, and BrassCraft—brands that dominated their categories with combined market shares exceeding 30% in many segments. The decorative division centered on Behr paint and KILZ primer, supplemented by Liberty Hardware and other accessories. Together, these businesses generated roughly $8 billion in revenue but with EBITDA margins approaching 20%, double what the diversified Masco had achieved. The transformation wasn't just about what to sell, but how to sell it. Digital integration became paramount. Revenue for 2024 reached US$7.83b (down 1.7% from FY 2023), but the company was investing heavily in e-commerce, augmented reality tools, and direct-to-consumer capabilities. Behr's mobile app let consumers virtually paint their rooms. Delta's online configurator helped homeowners design custom faucets. These weren't gimmicks—they were recognitions that the path to purchase had fundamentally changed.

The company also embraced sustainability as both responsibility and opportunity. Water-efficient faucets, low-VOC paints, and recycled packaging weren't just regulatory compliance—they were premium product features that commanded higher prices. Masco's 2023 sustainability report showed 30% reduction in water usage, 25% decrease in greenhouse gas emissions, and 90% of facilities achieving zero waste to landfill. Environmental leadership had become brand differentiation.

Leadership evolution marked this era. Keith Allman, who became CEO in 2014, represented a new generation of Masco executive—less empire builder, more optimizer. His background in operations rather than M&A signaled the shift from growth through acquisition to growth through execution. The management team he assembled shared this philosophy: experts in brand building, digital marketing, and operational excellence rather than deal-making.

For the full year 2024, the company delivered adjusted earnings per share growth of 6% despite a challenging demand environment, expanding adjusted operating margin by 70 basis points to 17.5 percent through focus on cost savings initiatives and operational efficiencies. This performance, achieved despite market headwinds, validated the focused strategy. The company was generating better returns with $8 billion in revenue than it had with $12 billion pre-crisis.

Capital allocation became surgically precise. In 2024, Masco's strong cash flow enabled it to return $1 billion to shareholders through dividends and share repurchases. The dividend, while never recovering to pre-crisis levels in absolute terms, now represented a more sustainable 30% of free cash flow. Share buybacks accelerated, with the company retiring nearly 20% of shares outstanding since 2015. Every dollar was scrutinized for return on invested capital, a discipline that would have been foreign to the acquisition-hungry Masco of the 1990s.

The competitive landscape had also evolved. Fortune Brands had similarly focused its portfolio, spinning off spirits to concentrate on home products. Sherwin-Williams had acquired Valspar, creating a paint giant that dwarfed Behr. Private equity firms were rolling up fragmented categories that Masco once would have dominated. But Masco's focused strategy meant it didn't need to win every battle—just the ones that mattered for its chosen categories.

Looking forward, management expects sales to be approximately flat to up low-single digits when adjusted for divestitures and currency in 2025, anticipating full year adjusted earnings per share to be in the range of $4.20 to $4.45 per share. The guidance reflects confidence not in market growth but in Masco's ability to gain share through superior execution.

The modern Masco bore little resemblance to the conglomerate Richard Manoogian had built. Smaller, simpler, more profitable—it was optimized for the realities of 21st-century capitalism where focus beats diversification, where brand power beats manufacturing scale, where capital efficiency beats empire building. Alex Manoogian's immigrant dream of building something lasting had evolved into Keith Allman's vision of perfecting what remained. The transformation was complete, but the story was far from over.

IX. Playbook: Business & Investing Lessons

The conference room at Harvard Business School fell silent as the professor pulled up Masco's stock chart from 1969 to 2024. "Here," she said, pointing to the massive peak in 2007 and subsequent crash, "is where most case studies would focus. The crisis. The recovery. But the real lesson starts here"—she moved her pointer back to 1954—"with a broken faucet that nobody wanted."

The Delta faucet story exemplifies the power of the single transformative product. Not transformative in the Silicon Valley sense of changing the world, but transformative in recognizing latent demand that even customers don't know exists. Americans in 1954 weren't clamoring for single-handle faucets. They'd accepted two-handle designs as immutable, like accepting that cars needed manual transmissions or phones needed cords. Manoogian's genius wasn't inventing new technology—single-handle designs existed—but perfecting it until it worked reliably, then creating demand through direct-to-consumer marketing. The lesson: sometimes the best innovations are fixing what's broken, not inventing what's new.

The acquisition strategy that built Masco's empire followed a playbook so consistent it became predictable. Target family-owned businesses in the second or third generation, where founders' children wanted liquidity but emotional attachment prevented outright sale. Offer cash for immediate needs plus Masco stock for long-term upside. Keep existing management in place, maintaining the entrepreneurial culture while providing corporate resources. Pay reasonable multiples—typically 8-12x EBITDA—rather than winning bidding wars. Between 1961 and 2002, this formula drove 42 acquisitions worth $10 billion. The discipline was remarkable: walk away from auctions, avoid hostile takeovers, never stretch for "strategic" premiums that couldn't be justified by synergies.

But the real genius was understanding that they weren't buying companies—they were buying positions in fragmented industries ripe for consolidation. Plumbing fixtures, cabinet hardware, paint supplies—industries with hundreds of small players, minimal product differentiation, and relationship-based distribution. Masco would buy the number three or four player, invest in quality and marketing, leverage economies of scale, and emerge as number one or two. It was private equity strategy before private equity existed, generating returns that venture capital would envy through distinctly un-sexy industries.

The channel partnership model, perfected with Behr and Home Depot, demonstrated the power of aligned incentives. Unlike typical supplier relationships where retailers squeeze manufacturers on price, Behr invested in Home Depot's success: training associates, managing inventory, even staffing paint desks during peak periods. Home Depot reciprocated with exclusive shelf space, promotional support, and collaborative product development. The result was a moat that competitors couldn't cross—even with superior products, they couldn't match the operational integration. The lesson extends beyond retail: the best partnerships aren't contracts but ecosystems where both parties' success depends on the other's.

Masco's history illustrates the importance of riding macro trends rather than fighting them. Post-war suburbanization, the 1970s DIY movement, 1990s McMansion boom, 2010s urban renovation surge—each era brought different opportunities that Masco surfed through portfolio evolution. When new construction boomed, focus on builder relationships. When renovation dominated, emphasize retail channels. When sustainability became paramount, lead with water conservation and low-VOC products. The company that sold screws to automotive manufacturers in 1929 was selling smart-home-enabled faucets to millennials in 2024, not through pivots but through patient evolution.

The furniture debacle of the late 1990s provides the starkest lesson about diversification's limits. On paper, furniture seemed logical: home products sold through similar channels with overlapping customers. In reality, furniture was fashion, not function. A faucet needs to work for decades; a sofa needs to look good this season. The $650 million write-off wasn't just financial loss but educational tuition: stick to products where engineering adds value, where brand means quality not style, where replacement cycles are predictable. Warren Buffett calls it "staying within your circle of competence"—Masco learned this lesson expensively but thoroughly.

The 2008 crisis response showcased the importance of managing through cycles rather than timing them. While competitors froze, hoping for quick recovery, Masco restructured radically: divesting entire divisions, cutting costs to match new reality, refocusing on core competencies. They didn't predict the recovery's timing—nobody did—but positioned themselves to thrive regardless. The lesson: in cyclical industries, structure your business to survive the troughs and you'll naturally capture the peaks.

Family control, maintained through super-voting shares and board positions even as the company went public, enabled long-term thinking that pure public companies couldn't match. Richard Manoogian could make decade-long bets on categories like paint because he didn't face quarterly activist pressure. The family's patient capital mentality—accepting lower returns during investment phases—built competitive advantages that impatient capital would have destroyed. This isn't an argument against public markets but recognition that some strategies require time horizons Wall Street won't tolerate.

The capital allocation evolution from empire-building to optimization reflects broader market maturation. In the 1960s-1990s, conglomerates could generate value through financial engineering and professional management. By the 2000s, markets demanded focus, punishing complexity premiums and rewarding pure-plays. Masco's transformation—spinning off TopBuild, divesting cabinets and windows, concentrating on core brands—wasn't admission of failure but recognition of reality. The same company worth 8x EBITDA as a conglomerate trades at 14x as a focused leader.

Finally, Masco's story demonstrates that boring businesses can generate exciting returns. Faucets, paint, cabinet hardware—these aren't products that grace magazine covers or inspire TED talks. But they're purchased repeatedly, generate predictable cash flows, and create genuine brand loyalty. A homeowner might switch smartphone brands annually but will specify Delta faucets for decades. In investing, as in life, the tortoise often beats the hare—not through speed but through consistency, durability, and the compound effect of small advantages sustained over time.

X. Analysis & Bear vs. Bull Case

The investment case for Masco in 2025 hinges on a fundamental question: Is this a cyclical company that happens to own great brands, or a branded goods company that happens to be cyclical? The answer determines whether you're buying at 14x earnings or selling at 14x earnings, whether the 2.5% dividend yield is a floor or a ceiling, whether the focused portfolio represents strength or vulnerability.

The Bull Case: Secular Tailwinds Meet Execution Excellence

Bulls see Masco as perfectly positioned for the next decade of American housing. Start with demographics: 72 million millennials entering prime home-buying years, requiring massive renovation of America's aging housing stock where the median home is now 40 years old. These aren't your parents' renovations—they're Instagram-worthy transformations requiring premium products that photograph well. Delta's Trinsic collection and Behr's designer colors aren't just functional; they're aesthetic statements that command 40% price premiums over basic alternatives.

The repair and remodel focus insulates Masco from new construction volatility. While housing starts might swing 50% peak-to-trough, Americans spend $450 billion annually on home improvement with remarkable consistency. Faucets fail regardless of mortgage rates. Paint fades whether the Fed is hiking or cutting. This non-discretionary demand provides ballast that pure new-construction plays lack. During the 2008 crisis, while new construction collapsed 75%, repair and remodel declined only 20%—painful but survivable.

Brand power in Masco's categories remains underappreciated by markets. Delta commands 30% market share in faucets not through price but through innovation—touchless technology, voice activation, lifetime warranties that actually mean something. Behr owns the DIY paint segment through exclusive Home Depot distribution that competitors can't replicate. These aren't commodities where price determines purchase; they're considered decisions where brand trust drives selection. The pricing power proves it: Masco has pushed through 3-5% annual price increases for a decade while maintaining market share.

The balance sheet provides both defense and offense. Net debt of $2.3 billion against EBITDA of $1.5 billion yields comfortable 1.5x leverage, leaving room for acquisitions or aggressive buybacks if opportunities emerge. Free cash flow conversion exceeding 90% of net income funds both growth investment and shareholder returns without choosing between them. The company could double its dividend and still have ammunition for bolt-on acquisitions.

International expansion remains nascent despite decades of operation. Hansgrohe gives European presence, but Asia-Pacific represents only 8% of revenue despite containing 60% of global construction. As Chinese and Indian middle classes upgrade from basic to premium fixtures, Masco's brands could capture disproportionate share of the premium segment. This isn't speculative—it's already happening in Mexico and Chile where Behr is gaining share rapidly.

The Bear Case: Maturity Meets Disruption

Bears see a mature company in mature categories facing structural headwinds that financial engineering can't overcome. Start with the obvious: housing affordability at 40-year lows, mortgage rates that have tripled from pandemic lows, and existing home sales running 30% below historical averages. Yes, people need faucets, but they can defer replacement, choose repair over replacement, or trade down from Delta to private label. The non-discretionary argument works until consumers become genuinely strapped.

The DIY-to-professional shift threatens Masco's retail-heavy model. During COVID, everyone became a weekend warrior, driving extraordinary retail sales. But complexity is increasing—smart home integration, water efficiency regulations, aesthetic expectations—pushing projects toward professional installation. Professionals buy from wholesalers, not Home Depot, weakening Masco's key channel advantage. Behr's exclusive retail position becomes a liability if pros drive incrementality.

Competition is intensifying from unexpected directions. Amazon Basics launched faucets. Home Depot's Glacier Bay private label gained 5 points of share in three years. Chinese manufacturers like Jomoo and Arrow are moving upmarket with quality that matches established brands at 50% lower prices. The moats that protected Masco for decades—brand recognition, distribution relationships, quality perception—matter less when consumers can read 10,000 reviews on Amazon before purchasing.

The innovation pipeline looks incremental rather than transformative. Smart faucets are interesting but not revolutionary. Paint technology has reached diminishing returns where improvements are imperceptible to consumers. Unlike technology companies where innovation drives replacement cycles, Masco's products last too long for their own good. A Delta faucet installed today might not need replacement until 2040—great for brand reputation, terrible for revenue growth.

ESG pressures could force expensive transitions. California's water restrictions already require faucet flow rates that compromise user experience. Paint VOC regulations get stricter annually, forcing reformulations that increase costs without increasing prices. The sustainability investments Masco touts—while admirable—are table stakes that don't drive revenue, only prevent its loss.

The valuation already reflects successful execution. At 14x forward earnings, Masco trades at a premium to its 10-year average of 12x and substantially above pure-play competitors. Fortune Brands trades at 11x, Kohler (if public) would likely trade at 10x given its cyclicality. The market is pricing in continued share gains and margin expansion that might prove difficult against tough comparisons. Any disappointment could trigger multiple compression that overwhelms operational improvements.

Competitive Reality Check

Masco's true competitors aren't who you'd expect. It's not Kohler in faucets—Delta has already won that battle. It's not Sherwin-Williams in paint—different channels, different customers. The real competition comes from alternative capital allocation: should Home Depot push private label harder, should Amazon enter categories more aggressively, should private equity roll up remaining independents?

Fortune Brands offers the clearest comparison: similar size ($7 billion revenue), similar categories (cabinets, plumbing, doors), similar strategy (divesting non-core, focusing on brands). Yet Fortune trades at a 20% discount to Masco. The difference? Execution consistency. Masco has delivered 28 consecutive quarters meeting or beating earnings expectations. Fortune has missed three times in the same period. In mature industries, execution is everything.

Sherwin-Williams demonstrates what category dominance looks like: 40% market share in professional paint, 4,700 stores, direct relationships with every major contractor. They're the Microsoft to Behr's Apple—less sexy, more profitable. Masco chose the retail/DIY route and executed brilliantly, but ceiling height matters. Behr can't become Sherwin any more than Delta can become Kohler. They're great at what they are, limited by what they're not.

The Verdict: Quality at a Fair Price

Masco isn't a moonshot. It won't double in two years, won't be acquired for a massive premium, won't discover some breakthrough technology that revolutionizes plumbing. It's a high-quality company in slow-growth categories with sustainable competitive advantages trading at a full but fair valuation. For long-term investors seeking ballast rather than thrust, it's compelling. For those seeking the next big thing, look elsewhere.

The bear case is real but manageable. The bull case is credible but capped. The truth, as usual, lies between: a good company in okay industries with excellent execution trading at market prices. In a world of extremes—unprofitable growth stories or declining value traps—Masco's profitable stability might be exactly what portfolios need. Not exciting, but investing isn't entertainment. Sometimes boring is beautiful.

XI. Epilogue & "What Would We Do?"

If Alex Manoogian could see Masco today, what would he recognize? Not the products certainly—touchless faucets and virtual paint selection would seem like magic to someone who started with manual screw machines. Not the scale—$8 billion in revenue would be incomprehensible to someone celebrating their first $7,000 contract. But he'd recognize the essence: a company that solves real problems for real people, that takes pride in quality, that treats customer trust as sacred. The immigrant who fled genocide to build something lasting would understand that legacy transcends any particular product or market.

The journey from auto parts supplier to American Dream enabler wasn't planned—it was evolved. Each generation faced different challenges requiring different responses. Alex's generation needed to survive, to prove that immigrant craftsmen could match anyone's quality. Richard's generation needed to scale, to professionalize family businesses into institutional leaders. Today's generation needs to focus, to choose excellence in few things over adequacy in many. The company that tried to be everything—faucets, furniture, windows, installation—learned that greatness requires saying no more often than yes.

What acquisitions make sense today? The playbook suggests targets that are frustratingly obvious yet difficult to execute. Smart home integration platforms that could unite Masco's products under common control systems. Water treatment companies that complement faucets with whole-home filtration. Premium tool brands that extend the DIY ecosystem. But the discipline must be maintained: only buy what enhances the core, what leverages existing capabilities, what customers already associate with the brands. The furniture disaster's lesson—competency matters more than opportunity—must never be forgotten.

International expansion offers the most tantalizing growth vector. Asia's construction boom makes America's post-war expansion look quaint. Two billion people will enter the global middle class by 2050, most in countries where Masco has minimal presence. But expansion can't mean exporting American products unchanged. It requires local manufacturing, local partnerships, local product adaptation. A Chinese consumer doesn't want an American faucet; they want a faucet that works perfectly in a Chinese home. Hansgrohe provides the template: premium global brand with intense local customization.

Digital and smart home integration isn't optional—it's existential. The generation entering home-buying years doesn't distinguish between physical and digital products. A faucet isn't just hardware; it's software that tracks water usage, prevents leaks, orders replacement filters automatically. Paint isn't just pigment; it's an augmented reality experience that lets you visualize colors before opening a can. Masco must become a technology company that happens to make physical products, not a manufacturing company that bolts on apps.

The capital allocation question looms largest: in a slow-growth industry with limited reinvestment opportunities, what do you do with cash? The current strategy—dividends plus buybacks—is sustainable but uninspiring. The alternative—transformative acquisition—risks another furniture debacle. The middle path might be venture investing: seed funding for startups developing home improvement technologies, option value on disruptions that could threaten or enhance the core business. Imagine Masco Ventures funding the next generation of home improvement innovation, bringing Silicon Valley energy to Detroit discipline.

The cultural challenge might be hardest. How do you maintain entrepreneurial energy in a 95-year-old company? How do you attract talent that could join Google or Goldman Sachs? The answer isn't competing on compensation—Masco will never match tech stock options. It's competing on meaning. The products Masco makes touch billions of lives daily. That faucet delivers clean water to children. That paint transforms houses into homes. That hardware holds together the spaces where life happens. In an economy increasingly disconnected from physical reality, making things that matter matters.

Looking forward, Masco faces a choice that echoes its founding moment. In 1929, Alex Manoogian could have stayed safe, kept his job, avoided the risk of starting a business during the Depression. Instead, he bet everything on the belief that quality products made with integrity would find customers regardless of economic conditions. Today's Masco faces similar uncertainty: housing affordability crisis, demographic shifts, technological disruption, climate change. The safe choice would be to milk existing brands for cash flow, slowly declining into irrelevance.

But what if Masco chose differently? What if it became the platform for reimagining American homes for the next century? Water-recycling faucets for drought-stricken regions. Carbon-negative paints that actively clean air. Modular systems that transform spaces as needs change. The technical capabilities exist. The brand trust exists. The distribution channels exist. What's needed is the same courage Alex showed in 1929: belief that building something better matters, even when—especially when—the future looks uncertain.

The Masco story isn't finished. From a Depression-era machine shop to a Fortune 500 company to a focused brand portfolio, each chapter seemed like an ending but proved to be transition. The next chapter remains unwritten, its authors not yet chosen, its themes not yet clear. But if history is guide, it will be written by immigrants and outsiders, by engineers and entrepreneurs, by people who see problems as opportunities and change as chance.

The American Dream that Alex Manoogian pursued—that hard work and ingenuity could build something lasting—feels fragile today. But maybe that's always how it's felt. Maybe every generation thinks the dream is dying, only to watch the next generation reimagine it. Masco doesn't just serve that dream; it embodies it. Every faucet installed, every room painted, every cabinet mounted is someone improving their life, literally building their future. In that sense, Masco isn't just a company. It's a bet on America itself—that people will keep striving, keep building, keep believing that tomorrow can be better than today.

That bet has paid off for 95 years. There's no reason to think it won't pay off for 95 more.

XII. Recent News**

Leadership Transition Marks New Era**

Masco Corporation announced today that its Board of Directors has appointed Jonathon Nudi as President and Chief Executive Officer, effective July 7, 2025. Nudi will succeed Keith Allman, who will retire as President and Chief Executive Officer and member of the Board of Directors at that time. The transition represents only the sixth CEO in Masco's 95-year history, underscoring the company's culture of long-term leadership stability.

Nudi has extensive strategic, operational and international experience, having served in a variety of leadership positions in the US and Europe over his 30-year career at General Mills. Nudi most recently served as Group President of General Mills' Pet, International and North America Foodservice segments, the company's three largest growth areas, where he drove strong net sales, segment operating profit and market share performance. His consumer goods background and international experience signal potential strategic shifts toward global expansion and enhanced brand building.

"It has been an honor to serve as Masco's President and CEO over the past decade," said Allman. "I am immensely thankful to our employees and proud of the work we've done together to build and refine our core portfolio of leading brands, expand our global footprint and deliver strong results for customers and shareholders. We have proven the strength of Masco's industry-leading brands, service and innovation, and I am confident the team will be in great hands with Jon at the helm.

Q4 2024 Financial Performance

Masco Corporation has reported its fourth quarter and full-year 2024 results. Net sales decreased 2 percent to $7,828 million; in local currency and excluding acquisitions and divestitures, net sales decreased 1 percent. "We delivered another quarter of strong operating results," said Keith Allman, Masco's president and CEO. "Our fourth quarter adjusted operating profit margin expanded 140 basis points, marking the seventh consecutive quarter of year-over-year margin expansion, and our adjusted earnings per share grew by 7 percent. Additionally, we executed on our capital allocation strategy by returning $331 million to shareholders in the quarter through dividends and share repurchases." "For the full year 2024, we expanded adjusted operating margin by 70 basis points to 17.5 percent through our focus on cost savings initiatives and operational efficiencies," continued Allman. "With this strong execution, we delivered adjusted earnings per share growth of 6 percent despite a challenging demand environment. Our strong cash flow also enabled us to return $1 billion to shareholders through dividends and share repurchases."

2025 Outlook and Strategic Priorities

"In 2025, we believe demand across the global repair and remodel markets will be flat to down low single digits. We expect our sales to be approximately flat to up low-single digits when adjusted for divestitures and currency, as we expect to continue to outperform the market in 2025," said Allman. "Based on the market outlook, our expected operating performance, and our capital deployment actions, we anticipate full year adjusted earnings per share to be in the range of $4.20 to $4.45 per share. With our industry leading repair and remodel-oriented product portfolio, strong balance sheet, and disciplined capital allocation, we believe Masco is well positioned to continue to deliver long-term shareholder value."

The guidance suggests management confidence in margin expansion and operational efficiency even in a challenging demand environment, with the company expecting to continue gaining market share through superior execution rather than market growth.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube