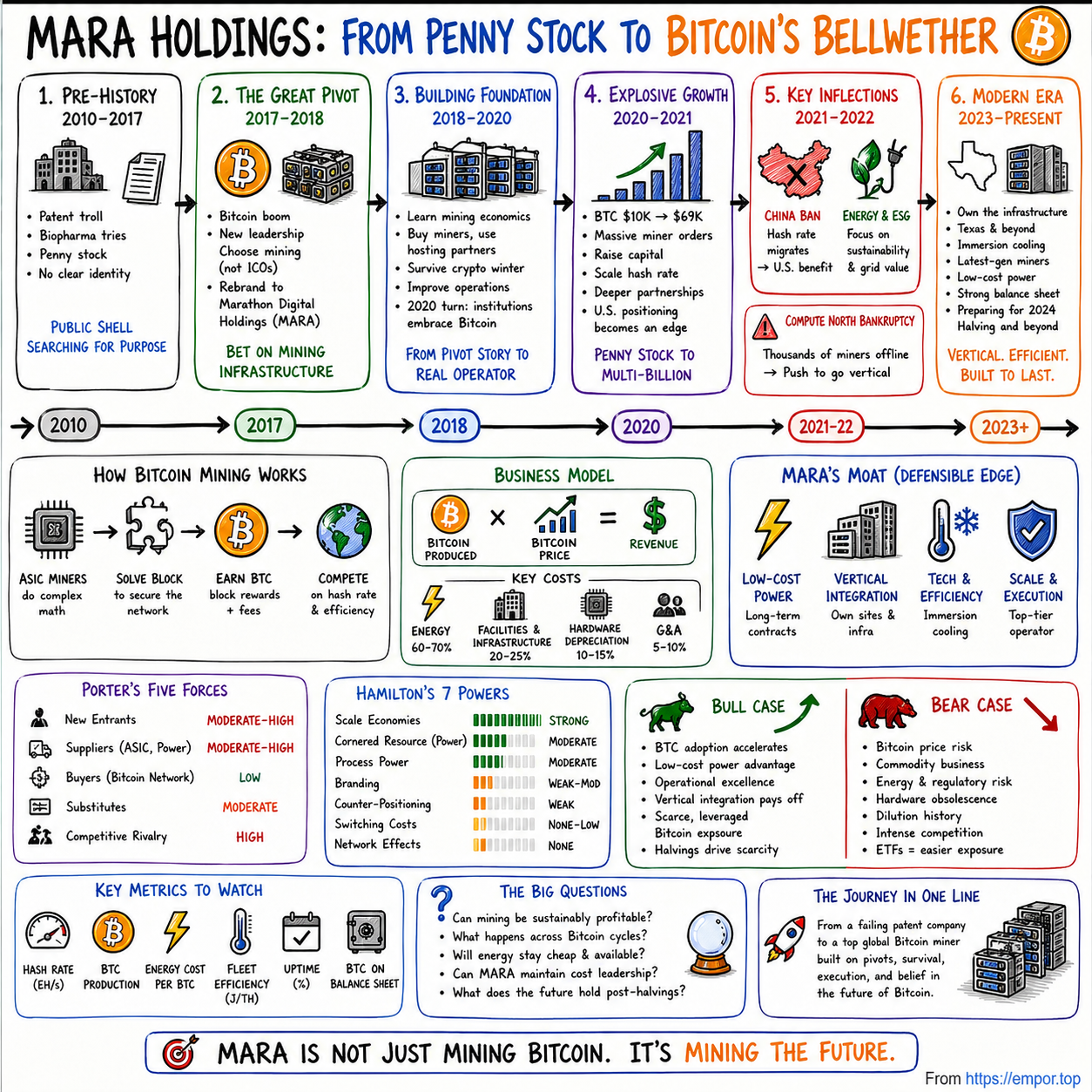

MARA Holdings: From Penny Stock to Bitcoin's Bellwether

Introduction and Episode Roadmap

Picture this: it is late 2017, and a tiny company trading on the NASDAQ for less than a dollar per share is about to make the most audacious corporate pivot in recent American business history. Marathon Patent Group — a failing patent licensing firm with no viable future, bleeding cash, and running out of ideas — is preparing to transform itself into one of the world's largest Bitcoin mining operations.

Within four years, the stock would soar past seventy-six dollars. Within five, it would crash back below four. And through it all, the company would survive, reinvent itself multiple times, and emerge as a bellwether for the entire cryptocurrency mining industry.

How did a struggling patent troll become one of the world's largest Bitcoin miners? That is the question at the heart of this story, and the answer reveals as much about the nature of corporate reinvention as it does about the volatile, unpredictable world of digital assets.

The central tension running through every chapter is deceptively simple: is Bitcoin mining a real business, or is it just speculation dressed up in industrial clothing? MARA has navigated at least three near-death experiences, pivoted its entire business model multiple times, survived a ninety-six percent stock decline, weathered SEC investigations, and emerged with a market capitalization exceeding seven billion dollars.

The themes are universal: corporate transformation under duress, the fine line between timing and vision, and the question of whether building infrastructure around a volatile asset creates lasting value or just amplifies the volatility.

Along the way, MARA has forced the market to grapple with questions that extend far beyond cryptocurrency: What is the relationship between energy infrastructure and digital assets? Can a commodity business build durable competitive advantages? And what does it mean for a company to survive when its stock drops ninety-six percent and comes back?

We will trace this story from the company's origins as a uranium exploration venture in 2010, through its years as a patent troll, into the great crypto pivot of 2017, through bull markets and bear markets, through the China mining ban and the Compute North bankruptcy, all the way to its current incarnation as a vertically integrated energy and digital infrastructure company with operations on four continents. The ride has been anything but boring.

The Pre-History: Marathon Patent Group (2010-2017)

The corporate entity that would eventually become MARA Holdings was incorporated on February 23, 2010, in Nevada under a name that reveals absolutely nothing about its future trajectory: Verve Ventures Inc. The original business plan involved uranium and vanadium exploration and mineral rights — about as far from Bitcoin mining as a company can get while still technically being in the extraction business.

By December 2011, the company had already pivoted once, renaming itself American Strategic Minerals Corporation. But the minerals business was going nowhere.

By 2013, the company had executed its second reinvention, this time emerging as Marathon Patent Group, Inc. The new business model was straightforward and controversial: buy portfolios of distressed patents, then extract licensing fees from companies that were allegedly infringing on those patents. Through its subsidiary Uniloc, Marathon became one of the more active non-practicing entities in the country, filing numerous patent infringement suits against major technology companies.

The polite term for this was "IP monetization." The less polite term, widely used in tech circles, was "patent trolling."

For a few years, this model generated some revenue. But the patent assertion business was becoming increasingly hostile territory. Courts were tightening standards for patent infringement claims. The America Invents Act of 2011 had created new mechanisms for challenging weak patents. Large technology companies were banding together to fight back. And the public perception of patent trolls had turned decisively negative.

By 2016 and 2017, Marathon Patent Group was a penny stock searching for an identity, bleeding cash, with a business model that was becoming less viable with each passing quarter. The company attempted various reinventions — exploring biopharmaceuticals, real estate IP — but nothing gained traction.

Here is the detail that matters most for understanding what happened next: Marathon was still a public company. It had a NASDAQ listing, corporate infrastructure, and a management team that understood capital markets. In the world of corporate reinvention, being a public shell company with an active listing is not a liability — it is an asset. Taking a company public from scratch is expensive, time-consuming, and uncertain.

Marathon's management recognized that their patent business was dying, but their public listing was very much alive. What they needed was a new story to tell.

The company's financial position by this point was dire. Revenue was negligible, the share price hovered around a dollar, and the market capitalization had dwindled to the tens of millions. For investors, Marathon Patent Group was essentially a call option on management's ability to find something — anything — worth doing with a public company shell. The board knew that without a radical reinvention, delisting from NASDAQ was a real possibility. Penny stocks that fail to maintain minimum listing requirements get relegated to the OTC markets, where liquidity dries up and institutional investors cannot follow.

And in the fall of 2017, the story found them.

The Great Pivot: Discovering Bitcoin Mining (2017-2018)

To understand why Marathon's pivot made sense in context, you have to remember what the world looked like in late 2017. Bitcoin had gone from roughly a thousand dollars at the start of the year to nearly twenty thousand dollars by December. Initial coin offerings were raising billions. Blockchain was the most searched buzzword in corporate America. Every public company that could plausibly attach the word "blockchain" to its name was doing so — Long Island Iced Tea Corp. famously renamed itself Long Blockchain Corp. and saw its stock price triple overnight.

The cynics had plenty of ammunition. But Marathon's pivot was not a name-change stunt.

On November 2, 2017, the company announced a definitive purchase agreement to acquire one hundred percent of Global Bit Ventures Inc., a digital asset technology company that was actually mining cryptocurrencies. This was the decisive moment. Marathon was not creating a token, launching an ICO, or slapping "blockchain" on a press release. It was acquiring real mining hardware and operational expertise.

The strategic logic was clear: Bitcoin mining is an infrastructure business. Miners provide the computational work that secures the Bitcoin network and, in return, receive newly minted Bitcoin as block rewards. It is an industrial process with measurable inputs — electricity and hardware — and measurable outputs — Bitcoin.

The leadership transition during this period shaped everything that followed. Merrick Okamoto served as acting Chairman and CEO from August 2017, overseeing the initial pivot to crypto mining. Fred Thiel, who would become the defining executive of the company's modern era, joined the board of directors in April 2018.

Thiel brought a very different profile to the table. Born in France, educated at the Stockholm School of Economics with executive courses at Harvard Business School, fluent in four languages, Thiel had spent over thirty-five years in the technology sector. His resume included stints as CEO of Lantronix and Local Corporation, and running his own advisory firm, Thiel Advisors, where he counseled firms like EQT AB and Graham Partners on value creation strategies. He was not a crypto ideologue. He was a technology operator who saw an industrial opportunity.

The financing challenge was real. How do you fund a complete business transformation when your existing business generates almost no revenue? Marathon turned to what would become its signature capital markets move: equity issuance. In a bull market, the narrative was powerful enough to attract capital. In a bear market, it would become the source of enormous shareholder dilution.

What distinguished Marathon's approach from the worst of the blockchain pivots was the focus on physical infrastructure. The company was buying ASIC miners — specialized computer chips designed solely for Bitcoin mining. It was securing hosting arrangements at data centers. It was learning the operational complexities of running industrial-scale computing operations. This was not a paper pivot. It was the beginning of an industrial operation.

The name change came later — Marathon Patent became Marathon Digital Holdings in March 2021, and eventually MARA Holdings in August 2024. But the real transformation began here, in late 2017, with the bet that Bitcoin is infrastructure, mining is a business, and building the physical backbone of this network would create value that speculation alone could not.

It is worth pausing to acknowledge the skepticism this move generated. The crypto boom of 2017 was full of opportunistic rebranding — companies with no blockchain expertise slapping new names on old shells to ride the hype cycle. Many of these companies would be worthless within two years. The critics who lumped Marathon into this category were not unreasonable. But Marathon's acquisition of actual mining hardware and operational know-how, rather than just a whitepaper and a token, was a meaningful distinction. Whether it was enough to justify the pivot would take years to determine.

Building the Foundation: Early Mining Operations (2018-2020)

Before diving into Marathon's early operational story, a quick primer on Bitcoin mining economics is essential. Bitcoin mining is the process by which new transactions are verified and added to the blockchain. Miners compete to solve a complex mathematical puzzle — think of it like a global lottery where buying more tickets improves your odds, but each ticket costs electricity to generate. The first miner to solve the puzzle gets to add the next "block" of transactions to the chain and receives a block reward in newly created Bitcoin.

Two features of Bitcoin's design make mining economics uniquely volatile.

First, the network automatically adjusts the difficulty of the puzzle every two weeks. If more miners join, the puzzle gets harder and each miner's share of rewards shrinks. It is a self-correcting system that prevents any single participant from dominating the network.

Second, the block reward gets cut in half approximately every four years in an event called "the halving." This means miners are on a perpetual treadmill: their revenue per unit of computing power declines over time, and they must continuously find cheaper energy, more efficient hardware, or both just to stay competitive. It is a Darwinian system by design.

Marathon's early operations relied heavily on third-party hosting arrangements. The company did not own data centers. Instead, it procured ASIC miners, primarily from Bitmain, the dominant Chinese manufacturer, and placed them in facilities operated by hosting partners. The most significant early relationship was with Compute North, which would later become both Marathon's lifeline and its biggest operational crisis.

The hosting model had clear advantages: lower upfront capital, faster deployment, and the ability to scale without building physical infrastructure from scratch. It also had a devastating weakness that was not yet apparent: Marathon's entire business depended on the reliability and financial stability of partners it did not control.

The 2018-2019 crypto winter tested everyone in the industry. Bitcoin crashed from nearly twenty thousand dollars to below four thousand — an eighty-plus percent decline. For a company like Marathon, which had pivoted into mining at the peak of the previous cycle, this was existential. Revenue collapsed. The economics of mining at those Bitcoin prices were brutal for anyone without extremely cheap electricity.

Marathon survived through a combination of aggressive cost management, further equity dilution, and what can only be described as institutional stubbornness. The company issued additional shares to stay funded, diluting existing shareholders but keeping the lights on — literally. Many crypto miners went bankrupt during this period. Others simply shut down their machines and walked away. Marathon did not.

This period is crucial for understanding the company's DNA. The management team that survived the 2018-2019 winter internalized a lesson that would shape every subsequent decision: in this industry, survival is the strategy. If you can stay alive through the downturn, the next upturn rewards survivors disproportionately. It is a philosophy that would prove prescient — but also one that sometimes substituted endurance for wisdom.

The turning point came in 2020, and it came from outside the crypto industry. The COVID-19 pandemic triggered unprecedented monetary policy responses from central banks worldwide. The Federal Reserve slashed interest rates to zero and began purchasing assets at a pace never before seen. Governments distributed trillions in stimulus payments.

The narrative around Bitcoin shifted dramatically. Suddenly, the digital scarcity argument had teeth: in a world where central banks were printing money with abandon, a fixed-supply digital asset started looking less like speculative mania and more like prudent hedging.

MicroStrategy, led by Michael Saylor, announced in August 2020 that it had purchased two hundred fifty million dollars worth of Bitcoin as a treasury reserve asset. Tesla followed in early 2021 with a one and a half billion dollar purchase. PayPal began allowing users to buy and sell Bitcoin. Fidelity launched digital asset custody services. Square (now Block) put Bitcoin on its corporate balance sheet.

The institutional awakening had begun, and it fundamentally changed the calculus for companies like Marathon. When only retail speculators cared about Bitcoin, mining was a fringe activity. When the world's largest corporations and asset managers began treating Bitcoin as a legitimate asset class, the miners producing it became infrastructure providers for a maturing financial system. Marathon was positioned to ride the wave.

But the company also made a move in October 2020 that would later generate significant controversy — one involving a retired coal plant in Montana.

The Explosive Growth Phase (2020-2021)

The 2020-2021 bull market was unlike anything the crypto industry had experienced. Bitcoin went from roughly ten thousand dollars in the summer of 2020 to an all-time high near sixty-nine thousand dollars in November 2021. For Bitcoin miners, this was the equivalent of striking oil during a price boom.

Marathon pursued what can only be described as a maximum aggression strategy.

The company placed massive orders for ASIC miners from Bitmain, eventually committing to purchase over one hundred thousand machines. To put that number in context: each of these miners is a specialized computer roughly the size of a shoebox that consumes two to three kilowatts of electricity and generates significant heat. One hundred thousand of them require hundreds of megawatts of power, enormous cooling infrastructure, and sophisticated monitoring systems. Marathon was building one of the largest mining fleets in the world.

The capital to fund this expansion came from the equity markets. Marathon executed multiple equity raises at increasingly favorable prices, taking advantage of investor enthusiasm for Bitcoin infrastructure. The virtuous cycle was powerful: higher Bitcoin prices drove higher stock prices, which allowed Marathon to raise more capital, which funded more miners, which increased hash rate. Shares that had traded below a dollar climbed past seventy-six dollars by November 2021.

In early 2021, Marathon also purchased approximately forty-eight hundred Bitcoin for roughly one hundred fifty million dollars. This was early adoption of what would later become the company's defining treasury strategy: HODL rather than sell. The logic was straightforward — if you believe Bitcoin's price will appreciate over time, selling mined Bitcoin to cover operating expenses is like selling an appreciating asset at today's price to fund today's costs.

But risks were accumulating beneath the surface. The Compute North hosting relationship was becoming a dangerous concentration of operational dependency. Supply chain delays plagued the entire mining industry, with ASIC deliveries from China facing months-long backlogs.

The company also stumbled into a controversy that revealed deep tensions between Bitcoin's ideological community and the realities of operating in a regulated environment. In March 2021, Marathon launched what it called the first OFAC-compliant Bitcoin mining pool in North America, using technology to filter transactions and exclude those from the Treasury Department's Specially Designated Nationals list.

The Bitcoin community erupted. This was, in their view, transaction censorship — a fundamental violation of Bitcoin's censorship-resistant design. Marathon reversed the policy later that year, updating to standard Bitcoin Core software and signaling support for the Taproot upgrade. But the episode left a mark on the company's credibility within the crypto-native community.

And underneath all of this was the most fundamental risk of all: Bitcoin price correlation. Marathon's stock, at its core, was a leveraged bet on Bitcoin's price. When Bitcoin went up, Marathon went up more. The problem, which would become painfully apparent in 2022, was that leverage works in both directions. The stock that hit seventy-six dollars would eventually trade below four — a decline of approximately ninety-six percent, wiping out billions of dollars in market capitalization. Anyone who bought at the top and held through the crash would need the stock to increase roughly twenty-fold just to break even. This kind of volatility is not a bug of mining stocks — it is the defining feature.

Inflection Point: The China Mining Ban (Mid-2021)

In the spring of 2021, the Chinese government did something that nobody in the Bitcoin mining industry thought was possible: it shut down the entire operation. In a series of escalating crackdowns between May and July 2021, Chinese authorities banned Bitcoin mining across the country.

The impact was staggering. At the time, China hosted an estimated fifty percent or more of the global Bitcoin hash rate. Overnight, that capacity went dark.

For the Bitcoin network itself, this was a stress test of unprecedented magnitude. The hash rate collapsed, which meant blocks were being produced more slowly. But Bitcoin's self-correcting difficulty adjustment mechanism kicked in — within weeks, the difficulty dropped to match the reduced hash rate, and the network stabilized. For existing non-Chinese miners, the economics suddenly improved dramatically: with half the competition gone, each remaining miner's share of block rewards roughly doubled.

For Marathon, which was entirely U.S.-based, the China ban was a transformational event. What had been a geographic limitation — being confined to American operations — was suddenly a strategic advantage.

The narrative shifted almost instantly. Bitcoin mining was no longer just a business. It was an American infrastructure play, a matter of financial sovereignty, and a strategic asset in the geopolitical competition between the United States and China. Marathon capitalized aggressively on this framing, accelerating expansion plans and positioning itself as the leader of America's Bitcoin mining industry.

But the China ban also set in motion competitive dynamics that would make Marathon's life harder in the long run. The displaced Chinese miners did not simply disappear. Many relocated to Kazakhstan, Russia, and other jurisdictions. Others sold their machines at discount prices, flooding the secondary market with used ASICs and making it easier for new entrants. The hash rate recovered within roughly six months, and by early 2022, global competition was more intense than ever.

The window of easy profits from reduced competition had been brief. But the strategic implications of the China ban were permanent. The United States had become the world's largest Bitcoin mining hub, a position it maintains to this day. States like Texas, Wyoming, Kentucky, and Georgia began actively competing for mining investment, offering tax incentives, streamlined permitting, and political support.

For Marathon, the China ban validated the domestic strategy and provided an invaluable geopolitical narrative for conversations with regulators and lawmakers. But geographic advantage alone would not be enough — the industry needed a more sustainable competitive edge, and Marathon's challenge was to build one. That challenge was about to become dramatically more urgent as the energy conversation exploded into public consciousness.

Inflection Point: The Energy and ESG Crisis (2021-2022)

If the China ban was an unexpected gift, the energy and ESG crisis that engulfed Bitcoin mining in 2021-2022 was a threat that Marathon had partially brought upon itself.

In October 2020, Marathon had entered a joint venture with Beowulf Energy LLC to build a data center at the Hardin Generating Station in Hardin, Montana — a coal-fired power plant that had been slated for retirement. Marathon issued six million shares to parties in the deal, and the facility operated at approximately fifty-seven megawatts. The economics were attractive: retired power plants offered cheap electricity. The optics were terrible.

When investigative journalists and environmental organizations examined the operation, they discovered that CO2 emissions at the Hardin facility had increased approximately tenfold — from 79,516 tons in 2020 to 755,670 tons in 2021 — directly attributable to Bitcoin mining operations. The New York Times, the Los Angeles Times, Mother Jones, and The Guardian all published critical coverage. Marathon had revived a dead coal plant to mine cryptocurrency, and the environmental cost was enormous.

The broader industry was under similar pressure. In May 2021, Elon Musk announced that Tesla would stop accepting Bitcoin payments, citing environmental concerns about mining's energy intensity. The tweet sent Bitcoin's price tumbling and galvanized a wave of ESG-focused criticism.

Marathon's response was a multi-year strategic pivot. In April 2022, the company announced plans to relocate mining operations away from the Hardin coal plant and pursue carbon neutrality by year-end 2022. It joined the Bitcoin Mining Council, an industry group promoting transparency about energy consumption.

The Texas strategy emerged as the centerpiece of transformation. Texas offered a unique combination: a deregulated electricity grid managed by ERCOT, abundant renewable energy from wind and solar, and a state government actively courting the crypto industry.

Perhaps most importantly, Texas's grid offered something no other state could match at scale: the economics of curtailment. During periods of extreme grid stress — summer heatwaves, for instance — miners could shut down their operations and effectively sell their electricity allocation back to the grid. They got paid not to mine.

This turned Bitcoin mining from a grid burden into a grid resource — a flexible load that could be dispatched during emergencies. The economic logic was genuinely compelling: Bitcoin mining is one of the few industrial processes that can operate twenty-four-seven, be located anywhere with cheap electricity, and shut down on short notice without damaging equipment or products. These characteristics make miners ideal customers for intermittent renewable energy sources like wind and solar.

In November 2021, Marathon also disclosed an SEC subpoena related to the Hardin data center and the Beowulf Energy joint venture, investigating potential violations of federal securities laws related to the share issuance. Multiple class action lawsuits followed. While the class actions were voluntarily dismissed in October 2022, the SEC investigation represented yet another crisis layered on top of the company's environmental and financial challenges.

The narrative evolution was remarkable. Within two years, Marathon went from being pilloried as a coal-burning environmental pariah to positioning itself as a grid-stabilizing partner for renewable energy. The company began actively seeking wind, solar, and flared natural gas sources for its operations. A partnership with NGON focused on monetizing flare gas at oil and gas fields — methane that would otherwise be vented into the atmosphere. By converting this waste gas into electricity for Bitcoin mining, Marathon could argue it was actually reducing emissions compared to the status quo.

Whether this repositioning represented genuine environmental commitment or clever corporate marketing is debatable. The pragmatic answer is probably: both. Marathon needed to solve its ESG problem to maintain access to institutional capital, and it found solutions that also happened to improve its economics. In the world of corporate sustainability, outcomes often matter more than motivations.

That transformation was not yet complete when the next crisis hit — and this one would strike at the very foundation of Marathon's operating model.

Inflection Point: Compute North Bankruptcy and Vertical Integration (2022-2023)

On September 22, 2022, Compute North LLC filed for Chapter 11 bankruptcy protection. For Marathon, this was the moment when the weaknesses of the asset-light hosting model became devastatingly clear.

The timing could not have been worse. Bitcoin had already crashed from sixty-nine thousand dollars to below twenty thousand. The broader crypto industry was reeling from the Terra-Luna collapse and the FTX implosion. Marathon's stock had declined approximately ninety-six percent from its November 2021 high.

Marathon's total exposure to Compute North was approximately eighty million dollars: ten million in convertible preferred stock, twenty-one point three million in an unsecured senior promissory note, and roughly fifty million in operating deposits and prepayments. The company ultimately expected to recover less than half.

Thousands of miners were suddenly at risk of going offline. The company's mining operations at the King Mountain facility in Texas, along with operations at Wolf Hollow, Nebraska, and South Dakota, were all dependent on Compute North's infrastructure.

But crises, as the saying goes, are terrible things to waste.

The Compute North bankruptcy forced Marathon to confront a fundamental strategic question: continue relying on third-party hosting, or own and operate its own infrastructure? The answer was emphatic. Marathon launched the most aggressive vertical integration push in the company's history.

At King Mountain, the largest site, operations continued largely uninterrupted thanks to the NextEra Energy joint venture structure that partially insulated Marathon from Compute North's financial problems. But the lesson was permanent: counterparty risk in hosting arrangements was an existential threat.

In December 2023, Marathon made its first major acquisition of owned infrastructure, purchasing two operational Bitcoin mining facilities from subsidiaries of Generate Capital for 178.6 million dollars. At the beginning of 2023, Marathon owned zero percent of its mining capacity. Everything was hosted.

The Generate Capital acquisition marked the beginning of a fundamental transformation: from renter to owner, from asset-light to asset-heavy, from dependent on hosting partners to controlling its own destiny.

The economics of the shift were significant. Hosting arrangements typically involved paying a fixed rate per kilowatt-hour plus a percentage of mining revenue or a management fee. By owning facilities outright, Marathon could negotiate directly with utilities, control its own maintenance, and capture the full economic benefit of efficiency improvements. The trade-off was obvious: much higher capital expenditure and operational complexity.

The company also invested heavily in immersion cooling technology — a technique where mining machines are submerged in a specialized non-conductive fluid rather than air-cooled. The advantages compound over time: hardware lasts longer, operates at lower temperatures, runs at higher performance settings, and produces less noise. Marathon positioned immersion cooling as a technology differentiator in its marketing to investors.

By the end of 2024, owned-and-operated capacity had grown from three percent to sixty-five percent. The Compute North crisis, in retrospect, was the catalyst that forced Marathon to become a real infrastructure company rather than a hardware owner renting space in someone else's data centers. The company also began mining Kaspa, an alternative proof-of-work cryptocurrency, deploying its first Kaspa ASICs in September 2023 after evaluation beginning in May. By mid-2024, Marathon had mined approximately 93 million KAS tokens valued at roughly fifteen million dollars, with about sixty petahashes of Kaspa mining power deployed. This diversification into alternative proof-of-work coins was a first for a major public miner and signaled Marathon's willingness to apply its infrastructure capabilities beyond Bitcoin.

Out of the ashes of its worst operational crisis came its most important strategic transformation.

The Modern Era: Scale, Strategy, and the 2024 Halving

By the time Bitcoin's fourth halving arrived in April 2024, Marathon had repositioned itself as a fundamentally different company. The halving cut block rewards from 6.25 to 3.125 Bitcoin per block — in practical terms, every miner on the network would produce roughly half as much Bitcoin as before, unless they increased their hash rate proportionally.

For inefficient miners with high electricity costs, halvings are extinction events. For well-positioned operators, they are competitive shakeouts that clear out the weak hands.

Fred Thiel, who had become CEO in April 2021, had spent the preceding year preparing. The strategy centered on three pillars: maximize efficiency, reduce costs, and continue accumulating Bitcoin on the balance sheet.

Marathon upgraded its mining fleet to the latest-generation ASIC miners, achieving a fleet efficiency of twenty joules per terahash by year-end 2024. To translate: efficiency in mining is measured by how much energy it takes to produce a unit of computational work. Lower is better. Twenty joules per terahash represented a significant improvement from earlier-generation hardware that consumed thirty or forty joules per terahash. Each efficiency improvement directly reduces the cost to mine each Bitcoin.

The hash rate reached 53.2 exahashes per second by December 2024, surpassing the company's year-end target. An exahash is a quintillion hash computations per second — a number so large it defies intuition. What matters is relative scale: Marathon was consistently among the top three to five largest miners globally.

The HODL strategy became increasingly central to Marathon's identity. Rather than selling mined Bitcoin to fund operations, Marathon accumulated Bitcoin on its balance sheet while funding operations through convertible debt issuances. In 2024 alone, the company purchased an additional 22,065 Bitcoin at an average price of approximately eighty-seven thousand dollars per coin. By September 2025, holdings had grown to approximately 52,850 Bitcoin — making Marathon the second-largest corporate holder of Bitcoin behind MicroStrategy.

To fund these purchases, Marathon turned to the convertible debt market with remarkable aggressiveness. In November 2024: one billion dollars in zero-coupon convertible notes due 2030. December 2024: another 850 million at zero-coupon due 2031. July 2025: a further 950 million at zero-coupon due 2032. Total convertible debt issued in roughly nine months: approximately 2.8 billion dollars, all at zero percent interest.

Zero-coupon convertibles are elegant financial instruments from the issuer's perspective — no cash interest payments required. Investors accept zero coupon because they receive the option to convert notes into equity if the stock rises. The risk is dilution: when notes convert, existing shareholders' percentage ownership decreases proportionally.

The financial results reflected the inherent volatility of a business whose primary asset fluctuates wildly. Fiscal year 2024 was a banner year: revenue of 656.4 million dollars, up sixty-nine percent. But fiscal year 2025 told a different story: revenue grew thirty-eight percent to 907.1 million dollars, while the company posted a net loss of 1.3 billion dollars for the full year, including a 1.7 billion dollar loss in the fourth quarter. The culprit was a 1.5 billion dollar negative change in fair value of digital assets under new accounting rules requiring quarterly mark-to-market.

The cost per Bitcoin mined rose from about thirty-two thousand dollars in the fourth quarter of 2024 to nearly forty-nine thousand dollars in the same quarter of 2025. Daily Bitcoin production declined from an average of 27.1 to 21.9 coins. Marathon was mining less Bitcoin at a higher cost — and the only way to make the economics work was for Bitcoin's price to keep climbing.

The strategic diversification into AI and HPC infrastructure marked perhaps the most significant new chapter. In February 2026, Marathon announced a joint venture with Starwood Digital Ventures to develop an initial 1.0 gigawatt of IT capacity, scalable to 2.5 gigawatts, for hyperscale and AI workloads. The stock surged seventeen percent. In April 2025, the company acquired a sixty-four percent stake in Exaion, a subsidiary of Electricite de France, for approximately 168 million dollars, gaining a foothold in European HPC markets. And the MPLX LP partnership added integrated gas-fired power generation in West Texas.

In February 2025, Marathon acquired a wind farm in Texas with 240 megawatts of interconnection capacity and 114 megawatts of nameplate wind capacity, expected to be operational in the second half of 2025. This was a remarkable milestone — a Bitcoin mining company now owned its own power generation assets. The MPLX LP partnership would add integrated gas-fired power generation, effectively making Marathon its own utility.

Marathon now operates eighteen data centers across four continents with approximately 1.8 gigawatts of controlled energy capacity — enough to power roughly 1.3 million homes. The pathway to scale through the Starwood partnership and MPLX deal could take that total to approximately 3.3 gigawatts. Whether this diversification proves visionary or a distraction from the core business remains one of the key questions for the company going forward.

Technology and Operations Deep Dive

At the heart of Marathon's operation is a surprisingly elegant industrial process. Tens of thousands of ASIC miners — each a specialized computer containing chips that do one thing and one thing only: compute SHA-256 hash functions as fast as possible — sit in rows inside data centers that look less like traditional server rooms and more like high-tech warehouses.

Think of an ASIC miner as a single-purpose calculator that can only do one type of math, but does it billions of times per second. Each machine generates enormous heat, roughly equivalent to a small space heater running at full blast, which must be removed continuously to prevent failure.

Traditional air cooling, where massive fans blow air across the miners and exhaust hot air from the building, is the simplest approach. But Marathon's investment in immersion cooling represents a bet on the next generation of mining. In immersion-cooled setups, miners are submerged in tanks filled with a specialized dielectric fluid — a non-conductive liquid that absorbs heat far more efficiently than air. The fluid circulates through heat exchangers that dissipate the heat externally.

The advantages compound over time: hardware lasts longer at lower temperatures, miners can be "overclocked" to run harder because superior cooling prevents thermal throttling, and the entire operation runs quieter — important when siting data centers near communities.

The supply chain for mining hardware remains concentrated. Bitmain and MicroBT, both Chinese companies, dominate the ASIC manufacturing market. This creates a geopolitical irony: companies positioning themselves as pillars of U.S. digital infrastructure remain dependent on Chinese hardware suppliers. Marathon's scale provides some negotiating leverage — priority access to new hardware and volume discounts — but the fundamental supply chain risk persists.

Fleet management at this scale requires sophisticated software systems. Monitoring tens of thousands of individual machines, each with potential to fail, overheat, or underperform, demands real-time dashboards, automated alerting, and skilled technical teams. Even a few percentage points of uptime difference across a fleet this size translates into millions of dollars of production annually.

The talent challenge is often overlooked. Mining operations are frequently located in remote areas where cheap electricity is available — places like Garden City, Texas, or rural Nebraska — which means recruiting and retaining skilled technicians requires competitive compensation, housing support, and a genuine operational culture. Building a world-class operations team in a town of twenty-five thousand people is not the same as hiring engineers in Austin or San Francisco.

Marathon's operations team, led by COO Sash Jain, has had to build expertise in an industry that barely existed a decade ago. There are no university programs in "Bitcoin mining operations management." The knowledge has been built through trial and error, borrowing practices from traditional data center operations, oil and gas field management, and power plant engineering. It is a hybrid discipline that requires understanding computing, electrical engineering, thermodynamics, and logistics simultaneously.

Security considerations span both physical and cyber domains. The physical assets — millions of dollars of mining hardware in sometimes remote locations — need protection. And the digital operations — pool connections, wallet management, monitoring systems — present cyber attack surfaces that must be defended. A security breach at a mining facility could result in stolen hardware, redirected mining rewards, or operational sabotage.

Business Model and Unit Economics

Marathon's revenue formula is deceptively simple: Bitcoin produced multiplied by Bitcoin price. Everything else is cost management.

The cost structure breaks down with energy dominating at approximately sixty to seventy percent of total operating costs. After energy, the next largest components are hardware depreciation, facilities overhead, and corporate expenses. This is why energy procurement is not just an operational detail at Marathon — it is the single most important strategic decision the company makes.

Consider the math. The difference between paying three cents per kilowatt-hour and six cents per kilowatt-hour for electricity is not a rounding error. It is the difference between a profitable mining operation and a money-losing one. At three cents, Marathon can mine Bitcoin profitably even during moderate price dips. At six cents, the break-even point rises dramatically, and any extended period of low Bitcoin prices turns mining into a cash incinerator.

ASIC miners have a useful life of roughly three to five years, depending on how aggressively they are run and how quickly newer models make them obsolete. This creates a perpetual capital expenditure treadmill: Marathon must continuously invest in new hardware just to maintain its competitive position, let alone grow. Mining is a capital-intensive business with rapid technology depreciation — imagine running an airline where your planes lose half their value every two years.

The treasury strategy debate is fundamental to understanding Marathon's investment thesis. The HODL approach — accumulating Bitcoin rather than selling it — has been enormously rewarded during bull markets. But during bear markets, the unrealized gains evaporate, and the company still needs cash for operations. The 2025 annual results illustrated this tension starkly: revenue was strong, but the net loss driven by digital asset fair value declines was enormous.

The correlation question haunts every public Bitcoin miner. Is Marathon a mining company, or is it a Bitcoin ETF with operations? The honest answer: both. Marathon's stock tracks Bitcoin's price with high correlation, typically with a leverage factor — moving more than Bitcoin in both directions. Since the launch of spot Bitcoin ETFs in 2024, investors now have a simpler, cleaner way to gain Bitcoin exposure without operational risks, dilution, and management overhead.

Marathon's management argues that mining provides leveraged exposure with operational upside: if you can mine Bitcoin for forty thousand dollars and the market price is ninety thousand, the mining operation creates fifty thousand dollars of value per Bitcoin that passive ownership cannot. But this argument depends entirely on Marathon maintaining mining costs below market price — far from guaranteed as network difficulty rises and halvings continue.

There is also the dilution dimension. Marathon has funded its growth primarily through equity issuance and convertible debt. Every share issued or convertible note sold represents future dilution to existing shareholders. Even if Marathon mines Bitcoin profitably, shareholders only benefit to the extent that the per-share value of the company's assets grows faster than the share count. If the share count doubles while Bitcoin's price also doubles, shareholders are running in place. This is the silent tax that capital-intensive growth companies impose on their investors, and it is one of the most important dynamics to understand about Marathon's business model.

CFO Salman Khan and the finance team have navigated this tension by favoring zero-coupon convertibles over straight equity issuance where possible — minimizing ongoing cash costs while deferring the dilution question to the future. It is a bet that the future will be kind enough to absorb the dilution without destroying per-share value.

Strategy and Competitive Positioning

Marathon's strategic evolution in 2025 and 2026 represents perhaps its most significant transformation since the original crypto pivot. The August 2024 rebranding from Marathon Digital Holdings to MARA Holdings was not cosmetic — it signaled expansion beyond pure Bitcoin mining into AI infrastructure, high-performance computing, and energy generation.

The Starwood Digital Ventures joint venture, announced in February 2026, was the clearest expression of this strategy: 1.0 gigawatt of initial AI-ready data center capacity, scalable to 2.5 gigawatts. Marathon brings energy assets and site infrastructure; Starwood provides institutional capital and management expertise to attract hyperscale tenants. The Exaion acquisition gave Marathon a foothold in European HPC markets backed by France's state-owned EDF.

Against this backdrop, Marathon's competitors have evolved significantly.

Riot Platforms, historically Marathon's closest competitor, has pursued a similar AI/HPC pivot, pausing construction at its Corsicana facility to evaluate AI opportunities. Core Scientific emerged from Chapter 11 bankruptcy in 2024 and secured a major partnership with CoreWeave to provide AI infrastructure for Microsoft and OpenAI. CleanSpark has focused on scaling its exclusively U.S.-based Bitcoin mining operations, achieving fifty exahashes per second.

All major public miners are grappling with the same fundamental question: is the future Bitcoin mining, AI infrastructure, or a hybrid? The pivot to AI is attractive because workloads are growing exponentially and data center capacity is in short supply. But AI data centers require different capabilities: higher-quality power delivery, more sophisticated networking, and long-term contracts with creditworthy enterprise tenants rather than the spot-market economics of Bitcoin mining.

Marathon's competitive advantages in this transition are real but not insurmountable. The company has scale, operational expertise in power-intensive computing, financial resources from convertible debt issuances, and first-mover advantage in certain locations. But competition for AI data center capacity is intense, and well-capitalized players from the traditional data center industry bring decades of relevant experience.

The geographic concentration in Texas, while strategically sound, creates risk: a single adverse regulatory action by the state legislature or ERCOT could disrupt significant operations. The February 2021 Texas winter storm — which caused widespread grid failures and rolling blackouts — demonstrated that even the most miner-friendly jurisdiction carries infrastructure risk. The international diversification — operations on four continents — is partly a hedge against this concentration.

Marathon has also invested in building versus buying capabilities. The two Ohio data centers with 222 megawatts of approved capacity, acquired during the vertical integration push, gave Marathon turnkey facilities that could be repurposed between Bitcoin mining and other workloads. The Nebraska data center acquisition, at 42 megawatts, provided geographic diversification away from Texas dependency. Each acquisition added to Marathon's mosaic of power sources and locations, reducing the company's vulnerability to any single point of failure.

The Regulatory and Political Environment

Marathon operates at the intersection of two politically charged industries: cryptocurrency and energy. The regulatory landscape is complex, evolving, and varies dramatically by jurisdiction.

Texas has emerged as the most important domestic jurisdiction, having actively courted the mining industry through deregulated electricity markets, favorable tax treatment, and explicit political support. The ERCOT grid relationship is central: miners participate in demand response programs, reducing consumption during grid stress in exchange for financial compensation.

At the federal level, the picture has been more uncertain. The SEC investigation into Marathon's Hardin data center deal was a reminder that public crypto companies operate under the same securities laws as everyone else. The bipartisan infrastructure bill included reporting requirements that created compliance burdens. Debates about mining's environmental impact have kept the industry on the defensive with certain regulators and lawmakers.

Marathon has invested in political and regulatory engagement — participating in industry associations, engaging with lawmakers, and positioning itself as a responsible operator. The shift away from coal and toward renewables was as much a regulatory strategy as an environmental one. In a world where a single hostile regulatory action could devastate the business, political capital is as important as financial capital.

The international expansion to four continents serves as both a growth strategy and a hedge against regulatory concentration risk. The Exaion acquisition, backed by France's state-owned EDF, provides geopolitical diversification that few crypto-native companies can match.

Future regulatory risks include potential carbon taxes, mining restrictions, energy consumption caps, and changes to how digital assets are treated for tax and accounting purposes. The new FASB rules requiring quarterly mark-to-market accounting for digital assets, which took effect recently, already demonstrated their impact through Marathon's 2025 financial results — the 1.5 billion dollar negative fair value swing in a single quarter illustrates how profoundly accounting rules can affect reported earnings for a company holding tens of thousands of Bitcoin.

The political dynamics around cryptocurrency have become increasingly partisan and increasingly relevant. Some lawmakers view Bitcoin mining as innovation and job creation; others see it as environmental damage and energy waste. Marathon's ability to navigate this divide — building relationships across the political spectrum, demonstrating tangible economic benefits to local communities, and positioning mining as a grid resource — may prove as important to its long-term success as any technological or operational improvement.

States are actively competing for mining investment, creating a patchwork of regulatory environments that Marathon must navigate. Wyoming has enacted some of the most crypto-friendly legislation in the country. Kentucky offers tax incentives. Georgia and North Carolina have attracted significant mining investment. Each jurisdiction brings different energy economics, regulatory requirements, and political dynamics.

Porter's Five Forces and Hamilton's Seven Powers

The threat of new entrants into Bitcoin mining is deceptively high. The concept is simple: buy mining hardware, find cheap electricity, start earning Bitcoin. But competitive entry at scale is a very different proposition — capital requirements run into the hundreds of millions, securing competitive power contracts requires relationships and scale that new entrants lack, and operational expertise cannot be acquired overnight. Bull markets attract new entrants; bear markets crush inefficient operators. It is a natural selection machine.

Supplier power is significant. The ASIC hardware market is effectively an oligopoly dominated by Bitmain and MicroBT. During bull markets, demand far exceeds supply, giving manufacturers enormous pricing power. Marathon's scale provides some negotiating leverage, but the fundamental dependency on two Chinese companies is a structural vulnerability.

Buyer power is essentially nonexistent, which is both blessing and curse. The "buyer" is the Bitcoin network itself — a decentralized protocol that pays block rewards based on hash rate contribution. No customer to negotiate with, no sales team needed. But also no ability to charge a premium or differentiate your product.

The threat of substitutes has increased meaningfully since spot Bitcoin ETFs launched. Investors seeking Bitcoin exposure now have a cleaner, simpler alternative without operational risk, dilution, or management overhead. Ethereum's transition to proof-of-stake demonstrated that major blockchains can abandon mining entirely, though Bitcoin's community makes a similar transition extraordinarily unlikely.

Competitive rivalry among public miners is intense and zero-sum. The total Bitcoin created per block is fixed. When Marathon adds hash rate, it takes market share from other miners by definition. Competition centers almost entirely on cost.

Through the lens of Hamilton Helmer's Seven Powers framework, the picture is nuanced.

Scale economies are Marathon's strongest power source, though moderate rather than dominant. Fixed costs spread across larger hash rate, bulk hardware purchasing yields discounts, and bigger energy offtake agreements command better rates. But returns diminish at the margins — cooling complexity, logistics, and management challenges grow with scale.

Network effects are entirely absent. Marathon does not benefit from having more users or participants. The Bitcoin network has network effects; individual miners do not capture them.

Counter-positioning is weak but present. Traditional energy companies could theoretically enter Bitcoin mining, but cultural aversion, reputational concerns, and regulatory uncertainty have kept most on the sidelines. Large tech companies have the capability but allocate resources to cloud and AI instead.

Switching costs are zero. The Bitcoin network is permissionless. If Marathon went offline tomorrow, the network would adjust difficulty and continue producing blocks. Marathon must remain cost-competitive every single day.

Cornered resource — specifically, long-term cheap power contracts — is Marathon's second-strongest power. Sub-four-cent-per-kilowatt-hour power at its best locations represents a genuine competitive advantage. The Texas wind farm acquisition, Ohio data centers, and MPLX gas generation partnership are investments in cornered energy resources. But cheap power is not truly cornered in the long run: other operators can and do find competitive rates elsewhere.

Process power is moderate. Operational expertise in fleet management, immersion cooling, and facility operations has been built over years. But these processes are not patent-protected or fundamentally impossible to copy.

The overall assessment is sobering but honest: Marathon has moderate moats, primarily from scale and cornered power resources. This is fundamentally a commodity business with thin differentiation, where success depends on relentless operational execution and the ability to survive Bitcoin's legendary volatility.

The comparison to other commodity businesses is instructive. Gold miners face similar dynamics — they produce a commodity whose price they cannot control, compete primarily on cost, and depend on geological resources analogous to power contracts. But gold miners at least have the advantage of a multi-thousand-year track record for their underlying commodity. Bitcoin miners are building infrastructure for an asset class that is less than two decades old and still debated as to whether it represents a genuine store of value or a speculative phenomenon. This additional layer of uncertainty makes the mining business even more challenging to analyze through traditional frameworks.

Bull vs. Bear Case

The bull case for Marathon rests on several reinforcing premises.

If Bitcoin adoption continues to accelerate — institutional, sovereign, global retail — then the price rises, and Marathon's economics improve dramatically. The 52,850-plus Bitcoin treasury becomes more valuable, mining margins expand, and the stock re-rates. The diversification into AI and HPC infrastructure creates revenue streams not directly tied to Bitcoin's price, reducing cyclicality. The vertical integration completed over 2023-2024 provides cost advantages that hosted competitors lack.

The energy infrastructure narrative is compelling: if Marathon successfully transitions from "Bitcoin miner that happens to own data centers" to "energy infrastructure company that happens to mine Bitcoin," the valuation framework changes entirely. Infrastructure companies trade at higher multiples than commodity producers. The 2.5-gigawatt AI data center pipeline, if executed, would represent enormous scale largely independent of cryptocurrency markets.

The 2028 halving, while reducing mining rewards further, will force out inefficient operators and increase Marathon's relative market share. And Marathon's unique combination of energy expertise, data center operations, and existing infrastructure positions it well for the AI-driven buildout reshaping the technology landscape.

The bear case is equally compelling.

If Bitcoin's price does not appreciate, Marathon's economics are brutal. The cost to mine Bitcoin reached nearly forty-nine thousand dollars per coin in the fourth quarter of 2025 and continues rising with network difficulty. If Bitcoin trades sideways or declines for an extended period, Marathon burns cash, its treasury loses value, and the 2.8 billion dollars in convertible notes become dilution bombs for shareholders.

The commodity nature of the business is a structural bear argument. No brand loyalty, no product differentiation, no customer relationships. Marathon is in a perpetual race to be the lowest-cost producer, and that race never ends. Hardware depreciates rapidly, requiring constant reinvestment.

The AI pivot, while strategically sound, is unproven and entering a fiercely competitive market where established players like Equinix and Digital Realty have decades of experience. The Starwood joint venture is promising but embryonic.

Regulatory risk remains a wildcard — carbon taxes, mining restrictions, or energy policy changes could dramatically increase costs. The geographic concentration in Texas creates single-point-of-failure risk. And the existential risk, remote but real, is that Bitcoin itself could fail or transition away from proof-of-work, rendering Marathon's business model obsolete overnight.

The dilution history demands honest examination. Marathon has repeatedly issued equity and convertible debt to fund growth, significantly reducing early shareholders' percentage ownership. Merrick Okamoto, the early CEO who oversaw the initial crypto pivot, was reported to have sold shares worth tens of millions of dollars during his tenure — a fact that some investors view as management enrichment at shareholder expense rather than genuine value creation. The zero-coupon convertible strategy is clever financial engineering, but it is also a bet: if Bitcoin rises enough, the dilution is forgiven. If it does not, shareholders bear the cost.

The substitution risk from Bitcoin ETFs deserves particular emphasis. When the first spot Bitcoin ETFs were approved in January 2024, they attracted tens of billions of dollars in inflows within months. These products offer pure Bitcoin exposure at low fees, with no operational risk, no dilution, no management overhead, and no counterparty risk. For an investor whose primary thesis is "Bitcoin will appreciate," an ETF is objectively a simpler and likely superior vehicle. Marathon's value proposition must therefore rest on something beyond mere Bitcoin exposure — it must demonstrate that mining creates value above and beyond what passive Bitcoin ownership provides.

Key Metrics: What to Watch

For investors tracking Marathon's ongoing performance, two metrics matter most.

First: energy cost per Bitcoin mined. This single number captures the combined effect of energy procurement, fleet efficiency, network difficulty, and operational execution. If Marathon keeps this well below Bitcoin's market price, the business generates positive economics. If the spread narrows, the business is in trouble. The trend from roughly thirty-two thousand dollars in the fourth quarter of 2024 to nearly forty-nine thousand in the fourth quarter of 2025 is concerning and deserves close monitoring.

Second: Bitcoin holdings on the balance sheet relative to total convertible debt outstanding. Marathon's treasury strategy is core to the investment thesis, and this ratio measures balance sheet health. As of late 2025, Marathon held approximately 52,850 Bitcoin against roughly 2.8 billion in convertible notes. If Bitcoin prices rise, this ratio improves. If they fall, it deteriorates, and the convertible notes become an increasingly heavy burden.

A supplementary metric worth tracking is fleet efficiency measured in joules per terahash. This indicates whether Marathon is staying on the technology curve — lower numbers mean more Bitcoin produced per unit of energy consumed, which directly supports the first metric.

The Big Questions and Future Scenarios

The fundamental question about Marathon is whether Bitcoin mining is infrastructure or speculation. The honest answer: it is both, and the ratio shifts with the market cycle. During bull markets, the infrastructure narrative is compelling — Marathon is building the physical backbone of a new monetary system. During bear markets, the speculation narrative dominates — Marathon is a leveraged bet on a volatile digital asset with no fundamental floor.

If Bitcoin reaches two hundred thousand dollars, Marathon's balance sheet becomes enormously valuable, mining margins expand dramatically, and the stock likely re-rates to a much higher level. If Bitcoin falls to twenty thousand dollars, Marathon faces an existential cost squeeze, its treasury loses most of its value, and the convertible notes become crippling. The wide range of these scenarios tells you everything about the risk profile.

The 2028 halving looms as the next major test. Block rewards will fall to 1.5625 Bitcoin — half the current level. At that rate, only the most efficient miners with the cheapest power will be profitable. Marathon's vertical integration, efficiency investments, and energy infrastructure are all preparing for that moment.

The consolidation endgame for the mining industry is another key question. As weaker operators exit and competitive entry costs rise, the industry will likely consolidate around a handful of well-capitalized survivors. Marathon, given its scale and resources, is more likely to be an acquirer than a target.

Technology disruption is another factor that sophisticated investors must weigh. Quantum computing, while still years away from practical deployment at scale, could theoretically break the SHA-256 cryptographic function that underpins Bitcoin mining. More immediately, advances in ASIC chip design could suddenly obsolete Marathon's current fleet, requiring massive reinvestment to stay competitive. The treadmill never stops.

And the diversification question: does the AI/HPC pivot represent Marathon's future, or is it a distraction? If the Starwood venture, Exaion, and MPLX partnerships deliver, Marathon could eventually generate significant revenue from workloads unrelated to cryptocurrency. This would be genuinely transformational — converting a single-commodity business into a diversified infrastructure platform. But execution risk is substantial, the competition is fierce, and the transformation is just beginning. Core Scientific has already secured a major AI hosting deal with CoreWeave. Riot Platforms is reorienting toward HPC. The race to diversify is industrywide, and being first does not guarantee being best.

Lessons for Founders and Investors

Marathon's story offers several lessons that extend beyond Bitcoin mining.

The most obvious: sometimes the best path forward is to completely abandon what you are doing and become something entirely different. Marathon's pivot from patent trolling to crypto mining was not incremental. It was a complete reinvention, and it worked because management recognized their existing business was dying and had the courage to bet everything on a new direction. The lesson is not that all pivots succeed — most fail. The lesson is that when your existing business is terminally impaired, the risk of inaction exceeds the risk of radical change.

Timing matters enormously, and Marathon was lucky. The pivot happened during the 2017 boom, which provided market enthusiasm to raise capital. Had it occurred two years later, during the 2019 crypto winter, financing might have been impossible. But timing alone is insufficient — Marathon had to execute through years of operational challenges, bear markets, and crises.

The capital markets strategy is worth studying. Marathon has been masterful at using public equity and convertible debt to fund growth during boom times. The zero-coupon convertibles are clever instruments: capital without cash interest payments. But every dollar raised is a claim on future value that existing shareholders must share.

Vertical integration becomes inevitable when supply chain partners fail. The Compute North bankruptcy forced the shift from hosted to owned infrastructure, which turned out to be the right strategic move regardless. The lesson: own your infrastructure when your core operations depend on assets you cannot afford to lose control of.

The narrative-then-reality sequence is worth studying in its own right. Marathon sold the story of Bitcoin infrastructure to investors long before the actual infrastructure was built. This is not uncommon in high-growth industries — Amazon sold the story of e-commerce dominance years before it became profitable. But the gap between narrative and reality creates risk for investors who buy the story and then must wait through years of execution, dilution, and volatility for the reality to catch up.

And finally: in commodity businesses, the lowest-cost producer wins. There is no brand premium in Bitcoin mining. No customer loyalty. No product differentiation. The only sustainable advantage is producing the commodity more cheaply than your competitors — and that competition includes every miner on earth. Marathon's leadership understands this deeply — every strategic decision, from the vertical integration push to the wind farm acquisition to the immersion cooling investments, is ultimately aimed at driving down the cost per Bitcoin mined. In a business where the price of your product is determined by a global, decentralized market that you cannot influence, cost control is not just important. It is everything.

The Verdict

Marathon's transformation from a failing patent troll to a legitimate Bitcoin mining and infrastructure operator is one of the most remarkable corporate reinventions of the past decade. A company worth less than thirty million dollars and searching for a reason to exist has become a multi-billion dollar enterprise with operations on four continents and more than fifty thousand Bitcoin on its balance sheet.

But the question of value creation is more nuanced than the headlines suggest. The answer depends entirely on when you bought and when you sold. Someone who purchased at thirty-five cents in March 2020 and sold at seventy-six dollars in November 2021 earned a life-changing return. Someone who bought at the peak and held through the crash experienced devastating losses. As of March 2026, the stock trades around eight dollars and sixty-six cents, with a fifty-two-week range of 6.66 to 23.45.

The comparison to simply buying and holding Bitcoin is instructive and humbling. A spot Bitcoin ETF provides cleaner exposure to the same underlying theme without operational risk, management risk, dilution risk, regulatory risk, and technology risk.

What makes Marathon genuinely interesting is the strategic optionality embedded in its infrastructure assets. If the AI data center buildout proceeds as planned, Marathon could evolve into something that no longer depends primarily on Bitcoin's price. The 2.5-gigawatt pipeline, the Exaion business in Europe, and the owned power generation assets represent potential value streams independent of cryptocurrency markets. Whether this optionality is worth the premium over a Bitcoin ETF is the question investors must answer for themselves.

Marathon's story is, in the end, Bitcoin's story: one of extreme volatility, radical transformation, and profound uncertainty about what the future holds. The company has survived challenges that would have killed most businesses. Whether this adaptability represents genuine strategic capability or simply the stubborn survival instinct of a public company that refuses to die is a question that only the next cycle will answer.

Further Reading and Resources

Books: "The Blocksize War" by Jonathan Bier provides essential context for Bitcoin's governance and the ideological tensions that shaped the mining industry. "Layered Money" by Nik Bhatia places Bitcoin within the broader framework of monetary infrastructure. "The Bitcoin Standard" by Saifedean Ammous presents the economic theory behind Bitcoin's design. "Digital Gold" by Nathaniel Popper chronicles Bitcoin's early history and the colorful characters who built its ecosystem.

Data and Industry Resources: The Cambridge Bitcoin Electricity Consumption Index remains the authoritative source for global mining energy data. The Bitcoin Mining Council publishes quarterly reports on energy mix and sustainability. Hashrate Index provides comprehensive coverage of mining economics, hardware pricing, and industry trends. Marathon's SEC filings — 10-K annual reports and quarterly 10-Qs — are essential reading for serious evaluation. Riot Platforms and Core Scientific investor materials offer valuable competitive benchmarks.

Podcasts: What Bitcoin Did, hosted by Peter McCormack, features in-depth interviews with mining CEOs and industry leaders. The Investor's Podcast Network covers Bitcoin mining economics. TFTC with Marty Bent provides regular mining industry coverage. The Texas Blockchain Council publishes reports on state-level mining dynamics and the ERCOT grid relationship central to Marathon's strategy.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube