MAIA Biotechnology: The Trojan Horse for Cancer's Immortal Engine

I. Introduction: The "Eternal" Life of a Cancer Cell

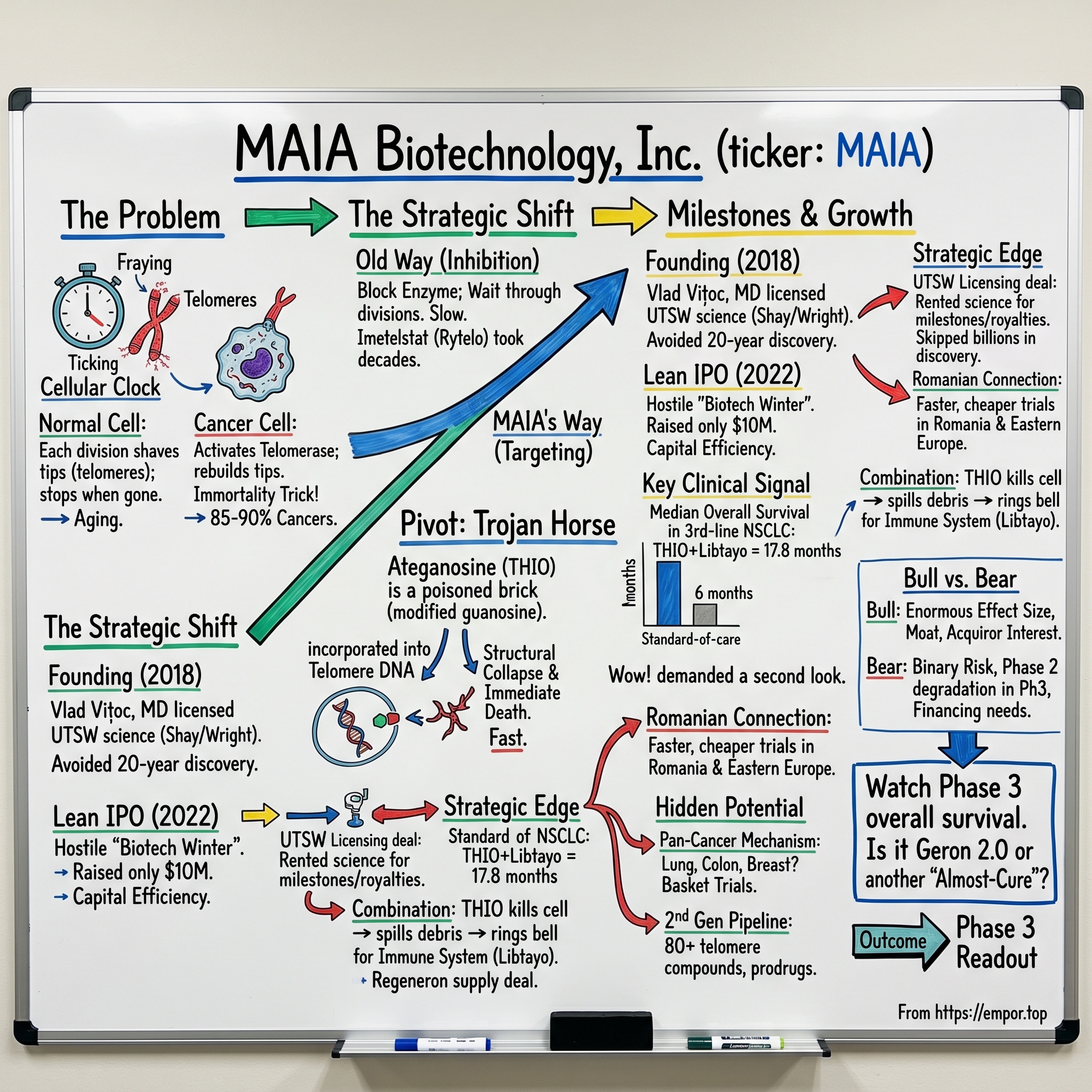

Picture a single cell dividing. Each time it splits, something almost imperceptible happens at the tips of its chromosomes. Those tips—called telomeres—are like the plastic caps on the ends of shoelaces, the little aglets that keep the lace from fraying. Every division shaves a sliver off the cap. Do this enough times and the cap is gone, the chromosome frays, and the cell does the responsible thing: it stops dividing and quietly retires. This is, in a very real sense, why we age. It is the molecular clock ticking inside almost every cell in your body.

Cancer cells cheat the clock. They switch back on an enzyme called telomerase—a kind of cellular repair crew that rebuilds the caps as fast as they wear down. With telomerase running, the clock never reaches zero. The cell becomes, for all practical purposes, immortal. It divides forever. This single trick is so central to cancer that the discovery of telomeres and telomerase earned Elizabeth Blackburn, Carol Greider, and Jack Szostak the 2009 Nobel Prize in Physiology or Medicine. Roughly 85 to 90 percent of all human cancers reactivate telomerase to achieve this immortality.

Here is the strategic question that has haunted oncology for three decades. If telomerase is the engine of cancer's immortality, why not just turn it off? Block the enzyme, the caps erode, the cells die. Simple. Except it isn't simple at all—and the company at the center of this story figured out that the obvious approach may have been the wrong one all along.

Most cancer drugs are, in essence, attempts to slow a fire. Chemotherapy poisons fast-dividing cells. Immunotherapy recruits your immune system to hunt tumors. Targeted therapies jam specific signaling pathways. All of them are fighting the flames. MAIA Biotechnology, Inc.—the AMEX-listed microcap at the heart of this episode—is doing something stranger. It is not trying to slow the fire. It is trying to dismantle the fuel tank, and to do it by feeding the tank a poison disguised as fuel.

That poison is a molecule called THIO, now carrying the generic name ateganosine. And the headline number that put MAIA on the map is almost difficult to believe for a company most investors had never heard of. In its Phase 2 lung cancer trial, in patients who had already failed two or more prior treatments—the kind of heavily pre-treated population where standard chemotherapy buys maybe six months of life—THIO produced a median overall survival of 17.8 months.1 Roughly three times the benchmark. In a corner of medicine where new drugs fight for incremental weeks, this was a number that demanded a second look.

So how did a tiny clinical-stage biotech, born out of a Dallas laboratory and floated onto a public exchange during the worst biotech bear market in a generation, end up holding survival data that towers over the standard of care? This is the story of a Trojan horse—a molecule that doesn't break down the gates of cancer's fortress, but gets waved inside by the enemy's own guards. It runs from the lab benches of UT Southwestern, through a $10 million IPO that almost nobody wanted, across clinical trial sites in Romania and Hungary and Taiwan, and into a pivotal Phase 3 trial that will determine whether this is the next standard of care or just another beautiful idea that didn't survive contact with reality.

Let's start where every great drug story starts: with two scientists who spent their careers staring at the ends of chromosomes.

II. Founding & The "Trojan Horse" Pivot

For most of the late twentieth century, the study of telomeres was a quiet, almost monastic corner of biology. And at the University of Texas Southwestern Medical Center in Dallas, two researchers made it their life's work: Dr. Jerry Shay and Dr. Woodring Wright. They were a partnership in the truest sense—Shay the cell biologist, Wright the cell biologist and physician, collaborators for decades, names that appear together on a long string of foundational papers about how cells age and how cancer escapes aging. If you wanted to understand telomerase, you read Shay and Wright. They were not building a company. They were building a field.

The conventional wisdom that emerged from that field was logical and, as it turned out, painfully slow to execute. If cancer needs telomerase, then inhibit telomerase. Starve the enzyme. Let the caps wear down naturally and let the cancer cells age themselves to death. This was the path taken most famously by Geron Corporation, a California company incorporated back in 1990 that bet its entire existence on telomerase inhibition.2 Its drug, imetelstat, was designed to gum up the enzyme directly.

The trouble with the inhibition approach is a matter of arithmetic and patience. If you block telomerase, the telomeres only shorten a little with each cell division. You have to wait through many, many divisions before the caps get short enough to actually kill the cancer cell. That's slow. In an aggressive tumor that is doubling rapidly, "slow" can mean the patient runs out of time before the drug runs out the clock. Geron's journey is the cautionary tale here: the company spent more than three decades and an enormous amount of capital before its telomerase inhibitor finally won FDA approval—and not in a solid tumor like lung cancer at all, but in a blood disorder. Rytelo (imetelstat) was approved in June 2024, some 34 years after the company was founded.2 Thirty-four years. That is the timeline that telomere science had earned itself a reputation for.

Now here is the pivot that changed everything—the conceptual leap that turned a slow strategy into a fast one. What if you didn't block telomerase at all? What if, instead, you let the enzyme run at full speed—and handed it a poisoned brick to build with?

That is THIO. Its full chemical name is 6-thio-2'-deoxyguanosine, or 6-thio-dG, and the trick is elegant to the point of being almost mischievous. THIO is a modified version of one of the four natural building blocks of DNA, guanosine. It looks, to the cell's machinery, like a perfectly normal nucleotide. Telomerase—busily rebuilding those telomere caps in a cancer cell—grabs THIO and incorporates it into the telomeric DNA, mistaking the poison for raw material. But THIO doesn't fit. Once embedded in the telomere, it triggers an immediate structural collapse: the cell reads it as catastrophic DNA damage, alarm bells ring, and the cell dies—fast. Not after dozens of divisions. After the very next time telomerase tries to do its job.3

This is the Trojan horse. Geron tried to break down the gates. MAIA's molecule gets carried through the gates by the enemy's own guards—because the only cells with telomerase running hot enough to take up THIO are the cancer cells. Healthy cells, with telomerase mostly switched off, largely ignore it. The selectivity is built into the mechanism. And crucially, the collapse is fast, which is exactly what the inhibition approach could never deliver.

The science was Shay and Wright's. The vision to turn it into a clinical drug company belonged to a different kind of person—not a bench scientist but a physician-executive with a builder's instinct. In 2018, Vlad Vițoc, an M.D. by training, founded MAIA Biotechnology around the THIO molecule, licensing the underlying patents out of UT Southwestern.3 Vițoc's bet was a classic "fast-follow the science, lead the execution" play. He wasn't going to spend twenty years in discovery. The discovery was done; it was sitting in a Dallas lab. The job was to take a validated mechanism and drive it through the clinic faster and leaner than a company like Geron ever could—and to avoid Geron's central mistake of choosing a slow mechanism and a hard indication.

It's worth pausing on the name. MAIA. In Greek mythology, Maia was the eldest of the Pleiades and, in some tellings, a goddess associated with rebirth and the renewal of life. For a company whose entire thesis is about manipulating the machinery of cellular immortality, it's a fitting bit of branding. But mythology doesn't enroll patients or raise capital. For that, Vițoc was going to have to take this thing public—and the timing he drew was about as bad as it gets.

III. Inflection Points: The 2022 IPO and the "17.8 Month" Miracle

Imagine trying to sell the world's investors on a speculative, pre-revenue, clinical-stage cancer biotech in the summer of 2022. The Nasdaq Biotechnology Index had been in freefall. The era of cheap money that had floated hundreds of biotechs to the public markets in 2020 and 2021 had slammed shut. The phrase on every healthcare banker's lips was "biotech winter." IPOs were being pulled, not priced. Crossover funds were nursing losses and hoarding cash. This was the market into which MAIA chose to walk.

And walk it did. On July 27, 2022, MAIA priced its initial public offering: two million shares of common stock at $5.00 per share, for aggregate gross proceeds of just $10 million.4 The stock began trading on the NYSE American the next day under the ticker MAIA.4 Ten million dollars. To put that in perspective, in the boom of the prior eighteen months it was not unusual for a biotech to raise ten or fifteen times that amount in a single offering. MAIA went public with what a fashionable Boston biotech might have spent on office build-out.

Why do it at all? Why go public for so little, in so hostile a market? The answer reveals something about MAIA's whole philosophy. A public listing, even a small one, gave the company a currency—a tradable stock—and a platform to raise more capital as clinical milestones arrived. It was a beachhead, not a war chest. In a winter, you don't need to be the biggest army; you need to still be alive when spring comes. The $10 million was survival capital, deliberately matched to a plan of extreme capital efficiency. Most biotechs that raised hundreds of millions in 2021 would spend the next three years cutting staff and writing down pipelines. MAIA, having never gorged, had less to purge.

Then came the data—and the data is the whole reason we're talking about this company.

The pivotal readout came from the THIO-101 trial, a Phase 2 study in non-small cell lung cancer, or NSCLC, by far the most common form of lung cancer. The patients in this trial were not newly diagnosed. They were third-line and later: people whose cancer had already chewed through a checkpoint-inhibitor immunotherapy regimen and then chemotherapy, and kept growing. For this population, the medical cupboard is nearly bare. Standard salvage chemotherapy in third-line NSCLC offers a median progression-free survival of roughly 2.5 months and an overall survival measured in single-digit months.1 These are patients running out of options and time.

In May 2024, MAIA reported its first significant survival signal from THIO-101, and the market began to pay attention.5 But it was the matured data, reported through 2025, that turned heads across oncology. As of a June 30, 2025 data cutoff, THIO—dosed at 180 mg and sequenced with the immunotherapy cemiplimab—delivered a median progression-free survival of 5.6 months, more than double the 2.5-month standard-of-care benchmark.1 And the overall survival figure was the showstopper: a median of 17.8 months.1 Two patients had completed 33 cycles of therapy—meaning they were still alive and on treatment far longer than anyone in this setting has any right to expect.1

Let's translate that 17.8 months into plain language, because the magnitude is easy to under-feel when it's just a number. In a patient group where chemotherapy historically buys roughly half a year, THIO was associated with nearly three times the survival. In oncology, where regulators and journals celebrate drugs that extend life by six or eight weeks, a tripling is not an incremental improvement. It is the kind of separation that, if it holds up, rewrites a treatment paradigm. The appropriate caveat—and we'll hammer it again later—is that this was a single-arm Phase 2 study with a small number of patients, not a randomized head-to-head trial. Phase 2 miracles have a way of regressing toward the mean in Phase 3. But even skeptical oncologists conceded the signal was unusually strong.

The second inflection point was a relationship, not a result. From the very beginning, THIO was never meant to work alone. The design pairs it with a checkpoint inhibitor—a drug that releases the brakes on the immune system. The logic is beautiful: THIO kills cancer cells by blowing up their telomeres, and that violent death spills tumor debris into the surroundings, effectively ringing a dinner bell for the immune system. The checkpoint inhibitor then makes sure the immune system actually answers the call. Kill the cells, and alert the cavalry. The checkpoint inhibitor MAIA chose was cemiplimab, sold as Libtayo, which is made by Regeneron. As early as February 2021—before the IPO—MAIA had signed a clinical supply and non-exclusive license agreement with Regeneron, under which Regeneron supplies Libtayo for the trials while MAIA sponsors and funds them and keeps global development and commercial rights to THIO.6 It was a low-cost way for a tiny company to run a combination study with a marketed blockbuster immunotherapy.

By late 2024, the interim survival numbers were maturing and being presented at major scientific meetings, including a late-breaking presentation at the Society for Immunotherapy of Cancer conference in November 2024.7 And in 2025, the regulatory momentum arrived. On July 28, 2025, the FDA granted THIO Fast Track designation for third-line NSCLC—a status that smooths and speeds the path to potential approval for drugs addressing serious unmet need.8 With Fast Track in hand and a survival signal that wouldn't quit, MAIA moved to initiate its pivotal Phase 3 trial, THIO-104. The microcap that nobody wanted in the winter of 2022 suddenly had the one thing money can't buy in biotech: a differentiated clinical result. The question now became how to pay for the expensive part—and that takes us into the company's capital allocation.

IV. Capital Allocation & Benchmarking: The UTSW Licensing Deal

Every biotech is, at its foundation, a financial structure wrapped around a molecule. And MAIA's foundation was a piece of paper signed with the Board of Regents of the University of Texas System, on behalf of UT Southwestern Medical Center—the patent and technology license agreement that gave the company the legal right to the THIO molecule and the family of patents around it.9 Understanding this deal is understanding the company's entire economic engine, because MAIA does not own its science the way a discovery-driven biotech does. It rents it from a university, and the rent is paid in milestones and royalties.

The structure of these academic licenses follows a familiar template. There's typically an upfront fee, often a slug of equity granted to the university, annual maintenance payments, a ladder of milestone payments triggered as the drug advances through clinical phases and toward approval, and then a royalty on eventual sales. The specific dollar figures in MAIA's UTSW agreement were largely redacted in the public SEC filings—a common practice for confidential commercial terms—so the precise upfront fee and exact milestone schedule are not fully disclosed in the primary documents.9 What we can say with confidence is the shape of the deal: MAIA acquired the inventions of Shay, Wright, and their colleagues for a fraction of what it would cost to discover them from scratch, in exchange for a tail of payments that only come due if and as the drug succeeds.

And that shape is the entire point. Think about the alternative. The discovery-and-validation work that produced THIO—decades of telomere biology, the insight that a modified nucleotide could be weaponized, the preclinical proof that it selectively kills telomerase-positive cancer cells—represents the most expensive and most failure-prone part of the entire drug development process. Most molecules die here, in obscurity, having consumed years and millions. By licensing a validated mechanism out of a university, MAIA effectively bought past the highest-mortality stretch of the journey. It paid not in cash up front but in a promise to share the upside. For a company that went public on $10 million, this is the only model that makes any arithmetic sense.

Now, the benchmarking question the bears like to raise: did MAIA overpay? Royalties of a few percent on a potential blockbuster, plus a milestone ladder, can add up to real money over a drug's commercial life. But compare the capital efficiency. Geron spent more than three decades and, by the industry's own rough yardstick—the oft-cited figure that a new drug costs on the order of $2.6 billion and 10 to 15 years to develop—a fortune to bring a telomerase drug to market through in-house discovery.2 MAIA's licensing model trades a sliver of future sales for the ability to skip most of that cost and most of that time. In capital-efficiency terms, paying low-single-digit royalties to avoid a multi-decade, multi-hundred-million-dollar discovery slog isn't overpaying. It's arbitrage. The risk MAIA took on wasn't discovery risk; it was clinical and financing risk—will the drug work in larger trials, and can a small company fund those trials to readout?

Which brings us to the financing side of capital allocation, and a very deliberate number. In March 2026, MAIA raised approximately $33 million in a public offering of common stock.10 On the surface, $33 million for a Phase 3 oncology program sounds almost comically thin—large pharma can spend that on a single Phase 3 trial's monitoring costs. But MAIA framed it precisely: management stated the net proceeds were expected to fully fund the company's ongoing pivotal Phase 3 THIO-104 trial through its readout.10 That is the tell. This wasn't a "raise as much as the market will bear" offering. It was a "raise exactly what we need to get to the next value-inflection point" offering—the data readout that either validates the whole thesis or breaks it.

The discipline here is strategic, not just frugal. Every dollar a microcap raises dilutes existing holders, and raising at a depressed share price—MAIA traded around a dollar in late 2025—is especially painful, because you sell a lot of shares for a little money.11 By sizing the raise to a specific milestone rather than to a multi-year runway, management is making a bet that the next data readout will re-rate the stock, allowing future capital to be raised on far better terms. It's the financing equivalent of refusing to sell your house in a down market when you only need enough cash to get through the month. The whole approach—lean IPO, milestone-sized raises, a licensed rather than self-discovered asset—paints a picture of a management team obsessed with capital efficiency. And that obsession traces directly back to the people running the company, and to one of the more unusual geographic strategies in small-cap biotech.

V. Management: "Skin in the Game" & The Romanian Connection

In late November 2025, with MAIA's stock languishing around a dollar, something happened that tends to make professional investors sit up. The CEO started buying. Not a token, press-release purchase, but a sustained series of open-market buys. Over the span of a single week, between November 21 and 28, 2025, MAIA's CEO and board members acquired roughly 182,445 shares of company stock.11 Vlad Vițoc himself bought across multiple days: 10,500 shares on November 25 at around $0.97, another 22,000 on November 26 at just over a dollar, and 50,000 more on November 28 at around $1.14.11 After the buying, his direct holding stood at 881,421 shares, and he is classified in SEC filings as a 10% owner of the company.11

Why does this matter? Because of all the signals a management team can send, open-market insider buying is among the hardest to fake. Executives can talk up a stock for free. Stock options cost them nothing to receive. But reaching into your own pocket, in the open market, to buy more of a thing you already own a great deal of—at a moment when the stock is beaten down—is the costliest and therefore most credible signal of conviction there is. The CEO is voluntarily increasing his exposure to a binary clinical outcome with his personal capital. He eats his own cooking. For a clinical-stage biotech, where so much depends on whether you trust management's read of the science, that alignment is not a footnote. It's central to the investment case.

The man at the center is Vlad Vițoc—and the spelling matters, because it points to the company's hidden geographic edge. Vițoc is Romanian by origin, a physician (M.D.) turned biotech executive who founded MAIA in 2018 and has run it as Chairman, President, and CEO ever since. His background as a doctor rather than a pure financier shapes the company's posture: clinically literate, focused relentlessly on the survival data as the thing that matters, and willing to design trials around mechanism rather than marketing. The incentive structure across the leadership is heavily milestone-weighted, tied to advancing the program toward Phase 3 success rather than to short-term stock performance—the kind of compensation design that makes sense when the entire value of the enterprise is locked behind a small number of future clinical events.

And then there is the Romanian connection itself, which is one of the quietly brilliant operational moves in this story. In its early build-out, MAIA established wholly owned subsidiaries in Romania and Australia to support the global development of THIO.12 The Romanian entity, MAIA Biotechnology Romania S.R.L., anchors a clinical strategy that leans heavily on Eastern Europe. The THIO-101 trial enrolled patients not just in the United States and Australia but across Hungary, Poland, Turkey, Taiwan, and Romania.13 Romania, in particular, became a focal point: the company identified clinical sites across multiple European countries and pushed enrollment hard through Eastern Europe, working with a leading Romanian oncologist, Dr. Tudor Ciuleanu—a professor at the Iuliu Hațieganu University of Medicine and Pharmacy and the Ion Chiricuța Institute of Oncology, two of the country's premier cancer centers—as a member of its scientific advisory board and a key investigator.13

Why does running trials in Cluj-Napoca and Budapest rather than Boston and Houston matter so much? Two reasons, both of which compound the capital-efficiency thesis. First, speed of enrollment. Eastern European oncology centers often have large numbers of patients and fewer competing trials, which means a small biotech can fill its trial cohorts faster than it could in the hyper-competitive American academic centers where every patient is being courted by a dozen studies. In clinical development, time is the most expensive resource of all; a trial that enrolls a year faster is a year of cash burn saved and a year of patent life gained. Second, cost. Running a clinical site in Romania is dramatically cheaper than running one in the United States—lower per-patient costs, lower overhead. For a company that funds its pivotal trial with a $33 million raise, the difference between a $50 million trial and a $100 million trial is the difference between existing and not existing.

So the "Romanian connection" is not a sentimental quirk of a founder's heritage. It is a deliberate arbitrage on the geography of clinical research—using the founder's home-region networks to enroll faster and cheaper than rivals burning Silicon Valley money in Silicon Valley clinics. It is the human and operational expression of the same instinct that produced the lean IPO and the milestone-sized raise. And it sets up the question of what, exactly, all this efficiency is being deployed to build—because THIO, it turns out, may be just the first molecule out of a much larger machine.

VI. "Hidden" Growth: The 2nd Gen Pipeline & Basket Trials

When investors look at MAIA, they see a one-drug company: THIO for lung cancer, binary outcome, sink or swim. That view is incomplete, and the incompleteness is where the optionality hides. Because what UT Southwestern licensed to MAIA was not really one molecule. It was a mechanism—and a mechanism can spawn a library.

That library is the second-generation program, and it is larger than most people realize. MAIA has developed more than 80 THIO-like compounds as part of its next-generation telomere-targeting effort.14 These belong to a new chemical class the company calls telomere-targeting divalent dinucleotides—molecules engineered to be more selective for cancer cells over normal cells and, in some designs, more potent than THIO itself.14 In January 2023, the company nominated a lead next-generation candidate, designated MAIA-2021-20, for advancement into the formal preclinical toxicity studies that precede human trials, along with a back-up candidate.14

Here is the layman's version of why a "second generation" matters. THIO is the proof of concept—the first molecule to demonstrate that the Trojan-horse mechanism works in patients. But first-generation drugs almost always have limitations: maybe they can't reach certain tissues, maybe they cause off-target effects, maybe they can't be formulated as a convenient pill. The second-generation compounds are attempts to fix those limitations. One important design is the lipid-modified prodrug—a version of the molecule wrapped in a fatty coating so it can slip into cells or tissues that the original couldn't reach, then shed the coating once inside to release the active drug.14 If THIO is a key that opens some doors, the prodrugs are attempts to cut keys for the locks THIO can't currently turn—potentially expanding the mechanism into cancers where the parent molecule falls short. That's a hidden pipeline sitting behind the lead asset, and it costs the market nothing today because nobody is pricing it in.

But the most expansive piece of the "hidden growth" thesis isn't the chemistry. It's the biology of the mechanism itself, and what it implies for the addressable market. Recall the number from the top of this episode: roughly 85 to 90 percent of all human cancers reactivate telomerase. THIO's killing mechanism depends on telomerase being active. Which means—in theory—THIO should work not just in lung cancer, but in any telomerase-positive tumor. Lung, colon, breast, pancreatic, liver, brain. The mechanism doesn't care what organ the cancer started in; it cares whether telomerase is running. THIO was originally granted orphan drug designation in small cell lung cancer, and the broader telomere-targeting concept has been explored preclinically in cancers as varied as hepatocellular carcinoma.15

This is the logic behind a "basket" strategy. Rather than treating MAIA as a lung cancer company, the more accurate framing is a pan-cancer infrastructure play—a platform built on a mechanism that, if it works in one telomerase-positive tumor, has a strong biological rationale to work across many. The THIO-102 study and the broader development plan reflect this ambition to extend beyond the initial NSCLC indication. The lung cancer trial is the wedge; the mechanism is the market.

Now, the sober counterweight, because basket logic is seductive and frequently wrong. "It should work everywhere" is a sentence that has preceded countless oncology disappointments. Tumors differ enormously in their biology, their microenvironments, and their resistance mechanisms; a drug that shines in one cancer can do nothing in another for reasons that only become clear in hindsight. The breadth of telomerase positivity is a real and unusual asset—it's rare to have a mechanistic target present in nine of ten cancers—but breadth of theoretical applicability is not the same as proven efficacy. The honest way to hold this is as optionality: a portfolio of shots on goal, each cheap to take given the licensed platform, any one of which could matter enormously, none of which is guaranteed. For investors, the second-generation library and the basket potential are not the base case. They are the free call options stapled to the lead asset. And whether those options have any value at all depends entirely on whether the core mechanism gives MAIA a defensible position—which is a question of competitive strategy.

VII. The Playbook: Porter's 5 Forces & Hamilton's 7 Powers

Strip away the biology for a moment and ask the question a strategist would ask: if THIO works, what stops someone bigger, richer, and faster from simply doing the same thing and crushing this $10-million-IPO upstart? This is where MAIA's position gets genuinely interesting, and where the frameworks of competitive strategy—Hamilton Helmer's 7 Powers and Michael Porter's Five Forces—earn their keep.

Start with what Helmer would call a Cornered Resource. MAIA's right to the foundational telomere-targeting patents, licensed exclusively out of UT Southwestern, is the closest thing a clinical-stage biotech has to an unbreachable moat.9 If telomere targeting via the Trojan-horse mechanism turns out to be the next frontier in oncology, MAIA owns the toll booth on the road into it. A competitor can't simply copy THIO; the composition-of-matter and method patents stand in the way. They would have to invent around the mechanism—which is precisely what the second-generation library is designed to make harder, by populating the surrounding chemical space with MAIA's own patented compounds. The cornered resource isn't just one molecule; it's an attempt to fence off an entire approach.

The more subtle power is Counter-Positioning, and it's the heart of MAIA's strategic elegance. The entire oncology industry has spent the last decade in a frenzy around immuno-oncology—PD-1 and PD-L1 checkpoint inhibitors, the Keytrudas and Opdivos and Libtayos of the world. Dozens of companies fight over the same crowded mechanism. MAIA did not try to build a better checkpoint inhibitor and join that bloody scrum. Instead, it positioned THIO as the primer—the drug that makes the existing checkpoint inhibitors work better. By killing cancer cells in a way that alerts the immune system, THIO is designed to turn "cold" tumors that don't respond to immunotherapy into "hot" tumors that do. That's counter-positioning: rather than competing with the incumbents' franchises, MAIA positions itself as the thing that rescues and extends those franchises. A big pharma company with a checkpoint inhibitor losing patients to resistance has every incentive to want THIO to exist, not to kill it.

Run the Porter's Five Forces and the picture sharpens further. The threat of substitutes is unusually low: the only close conceptual rival is telomerase inhibition, and we've already seen how that approach is slower-acting and took Geron three decades to bring to market in a different indication entirely.2 MAIA's faster, structural-collapse mechanism is a genuinely differentiated substitute, not a me-too. Bargaining power of buyers—in this case, patients and the physicians prescribing for them—is, bluntly, low in the setting MAIA targets first. A patient with third-line NSCLC who has exhausted immunotherapy and chemotherapy has almost no alternatives; a drug that triples survival in that desperate setting commands enormous pricing and adoption leverage precisely because the alternatives are so poor. Bargaining power of suppliers is interesting: MAIA depends on Regeneron to supply Libtayo for the combination, which is a real dependency, but the clinical supply arrangement and MAIA's retention of global rights to THIO keep the relationship more partnership than hostage situation.6

The two forces that don't favor MAIA are the ones investors must respect. The threat of new entrants is never zero in biotech—the patents raise the wall, but a determined big pharma with a different telomere-targeting chemistry could eventually climb it. And competitive rivalry in oncology broadly is ferocious; even if MAIA owns its niche, it competes for the same patients, the same trial sites, and the same investor dollars as a thousand other cancer programs. The strategic conclusion is that MAIA's powers are real but conditional. The moat exists if the drug works. The counter-positioning is brilliant if the survival data holds. Every Helmer power and every favorable Porter force is downstream of a single binary event—the Phase 3 readout. Which is exactly the tension we have to weigh in the bull and bear cases.

VIII. Bull vs. Bear: The Analysis

Every microcap biotech is an argument with itself, and MAIA is an unusually sharp one. Let's wargame both sides honestly, because the gap between them is enormous and the resolution is, frankly, unknowable in advance.

The bear case begins with the brutal arithmetic of small-cap clinical biotech. This is a company with a stock that traded around a dollar in late 2025, a market capitalization that makes it a true microcap, and a future that hinges almost entirely on a single drug in a single pivotal trial.11 That is the definition of binary risk. If THIO-104 fails—if the spectacular Phase 2 survival signal melts in the heat of a larger, randomized, controlled trial—there is no diversified revenue base to cushion the fall, no second approved product, just a licensed molecule that didn't pan out and a balance sheet that will need refilling. And Phase 2-to-Phase 3 attrition is the graveyard of biotech; single-arm Phase 2 results in small patient numbers regress toward the mean with grim regularity, because the controlled comparison and the larger sample have a way of revealing that some of the magic was patient selection and chance.

The bear has more ammunition. There's the Regeneron dependency: THIO's lead program is built around sequencing with Libtayo, a drug MAIA does not own. The relationship is contractual and, so far, cooperative, but a strategic shift at Regeneron, or a decision to deprioritize the combination, would be a real shock to a company without the resources to easily pivot.6 There's financing risk: even with the milestone-sized March 2026 raise funding the Phase 3 through readout, a microcap that perpetually returns to the market for capital dilutes its holders, and does so most painfully when the stock is cheap.10 And there's the uncomfortable reality that the most credible validation—the open-market insider buying—while genuinely reassuring, is also exactly what you'd expect from a true believer who may simply be wrong. Conviction is not the same as correctness.

Now the bull case, and it rests on one extraordinary feature of the data: the sheer size of the effect. When a drug beats the standard of care by a few weeks, even a modest degradation in a larger trial can erase the benefit entirely. But when a drug is associated with roughly three times the survival benchmark—17.8 months against a single-digit standard—the margin of safety in the effect size itself is enormous.1 The bull's sharpest formulation is this: even if the Phase 3 results degraded substantially from the Phase 2 signal, what remained could still be a clinically meaningful, even practice-changing, improvement over chemotherapy. You don't need the miracle to fully hold. You need it to half-hold. That asymmetry—a beaten-down microcap valuation against a drug whose efficacy signal has room to shrink and still matter—is the entire bull thesis in one sentence.

Layer on the strategic optionality we've already walked through: the FDA Fast Track designation that could accelerate approval, the pan-cancer breadth of a telomerase-dependent mechanism, the 80-plus compound second-generation library, and the counter-positioning that makes THIO complementary to—rather than competitive with—the immuno-oncology giants.814 Each is a call option that the depressed valuation arguably gives away for free.

And that complementarity feeds the most tantalizing bull scenario of all: the acquisition play. Consider the position of a large pharmaceutical company with a multi-billion-dollar checkpoint-inhibitor franchise that is slowly eroding as patients develop resistance. A drug that demonstrably extends the usefulness of checkpoint inhibitors—that turns non-responders into responders—is not just a nice asset to such a company. It is a defensive necessity. MAIA, with its tidy market cap and its single high-value mechanism, is precisely the kind of bite-sized, strategically coherent acquisition a big player makes to protect an existing immunotherapy empire. The counter-positioning that makes MAIA a good partner also makes it a logical takeover target. The bear says "one trial from zero." The bull says "one data readout from being someone's must-have acquisition." Both are true at once, which is what makes the stock what it is.

So where should a long-term, fundamentals-minded observer actually point their attention amid all this? Not at the daily stock chart, which for a binary microcap is mostly noise. The signal lives in a very small number of things.

IX. Conclusion & Final Reflections

Step back from the ticker and the survival curves, and the MAIA story resolves into something larger than one molecule. It is a case study in how a high-impact biotechnology company can be built on a fraction of the capital the industry assumes is required. The conventional model—the one that produced Geron's thirty-four-year, fortune-consuming march—is in-house discovery, enormous raises, and patient decades. MAIA inverted nearly every part of it. It licensed a validated mechanism out of a university rather than discovering one. It went public on $10 million in the teeth of a bear market rather than gorging in a boom. It raised capital in milestone-sized bites tuned to specific value inflections. And it ran its pivotal trials through Romania and Hungary and Taiwan rather than the most expensive zip codes in American medicine. The lesson for founders is not that THIO will work—we don't yet know that. The lesson is that capital efficiency is itself a strategy, and that in a winter, the lean survive to see the spring.

If there is a single discipline this episode should leave with a long-term investor, it is to watch the few things that actually determine the outcome and ignore the thousand that don't. For MAIA, the key performance indicators are unusually clean. The first and overwhelmingly most important is the overall survival data in the pivotal Phase 3 THIO-104 trial—the randomized, controlled readout that will either confirm or shatter the 17.8-month Phase 2 signal. Everything else is secondary to whether that number holds in a head-to-head comparison against chemotherapy.110 The second is trial enrollment pace, the operational heartbeat that tells you whether the Eastern European site strategy is delivering the speed and cost advantage it promises, and therefore whether the company can reach readout on the capital it has. And the third, quieter signal is insider behavior and the cadence of financing—whether management continues to buy, and whether the next raise comes at a higher or lower price, which together reveal how the people closest to the data are reading it.11

Which returns us to the question this whole episode has been circling. Is MAIA the "Geron 2.0" that finally delivers on the decades-old promise of telomere science—taking the same Nobel-winning biology that defeated the inhibition approach and cracking it open with a Trojan horse? Or is it one more beautiful mechanism that dazzles in Phase 2 and disappoints in Phase 3, joining the long, quiet graveyard of oncology's almost-cures?

The honest answer is that the company has done something genuinely rare: it has produced a survival signal large enough that even a skeptic has to take the bull case seriously, while remaining small and unproven enough that even a believer has to respect the bear. It has built, on a shoestring, a piece of pan-cancer infrastructure around a mechanism present in the overwhelming majority of human tumors—and it has wrapped that infrastructure in patents, partnerships, and a counter-positioning that would make it valuable to an acquirer the moment the data clears. From a Dallas lab bench to the AMEX floor, MAIA has turned a poisoned brick handed to cancer's own repair crew into one of the more asymmetric bets in small-cap biotechnology. Whether the immortal engine of the cancer cell finally meets its match in that brick is a question only the Phase 3 readout can answer—and that, for once, is a cliffhanger worth watching.

References

-

MAIA Biotechnology Highlights Positive Efficacy Data from THIO-101 Phase 2 Clinical Trial in Non-Small Cell Lung Cancer — MAIA Biotechnology, Inc., 2025-09-11 ↩↩↩↩↩↩↩

-

After 33 years, Geron's first approval marks a turn in Nobel-winning science — PharmaVoice, 2024 ↩↩↩↩

-

Telomere Targeting: A New Frontier in Oncology / Lung cancer treatment shows promise in tumor models — UT Southwestern Medical Center Newsroom, 2024 ↩↩

-

MAIA Biotechnology Announces Pricing of Initial Public Offering — Business Wire, 2022-07-27 ↩↩

-

MAIA Biotechnology Reports Positive Efficacy and Safety Data from Phase 2 THIO-101 Clinical Trial — GlobeNewswire, 2024-05-14 ↩

-

MAIA Biotechnology Announces Clinical Supply Agreement with Regeneron for Phase 1/2 Clinical Trial Evaluating THIO with Libtayo (cemiplimab) — Business Wire, 2021-02-02 ↩↩↩

-

MAIA Biotechnology Announces Positive Efficacy Updates for Phase 2 THIO-101 Trial in Advanced Non-Small Cell Lung Cancer — MAIA Biotechnology, Inc., 2024 ↩

-

MAIA Biotechnology Receives FDA's Fast Track Designation for Ateganosine as a Treatment for Non-Small Cell Lung Cancer — Business Wire, 2025-07-28 ↩↩

-

Patent & Technology License Agreement between MAIA Biotechnology and the Board of Regents of the University of Texas System (UT Southwestern) — Justia Business Contracts / SEC ↩↩↩

-

MAIA Biotechnology Expects Recent $33 Million Capital Raise to Fully Fund Ongoing Pivotal Phase 3 Trial — GlobeNewswire, 2026-04-08 ↩↩↩↩

-

MAIA Leadership Continues Insider Buying in 2025 and Trial Data Signals Breakout Potential — GlobeNewswire, 2025-12-11 ↩↩↩↩↩↩

-

MAIA Biotechnology, Inc. Establishes Wholly Owned Subsidiaries in Romania and Australia to Support Global Development of THIO — MAIA Biotechnology, Inc. ↩

-

MAIA Biotechnology CEO Presents Telomere Targeting Efficacy at Romania's 2025 Smart Diaspora Conference on Oncology Research and Innovation — BioSpace, 2025 ↩↩

-

MAIA Biotechnology Announces Publication of Peer-Reviewed Study Featuring Potency and Potential of Novel THIO Prodrug — Business Wire, 2025-03-20 ↩↩↩↩↩

-

Activating an Adaptive Immune Response with a Telomerase-Mediated Telomere Targeting Therapeutic in Hepatocellular Carcinoma — Molecular Cancer Therapeutics (AACR), 2023 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube