Macy's Inc.: The Rise, Fall, and Fight for Survival of America's Department Store Icon

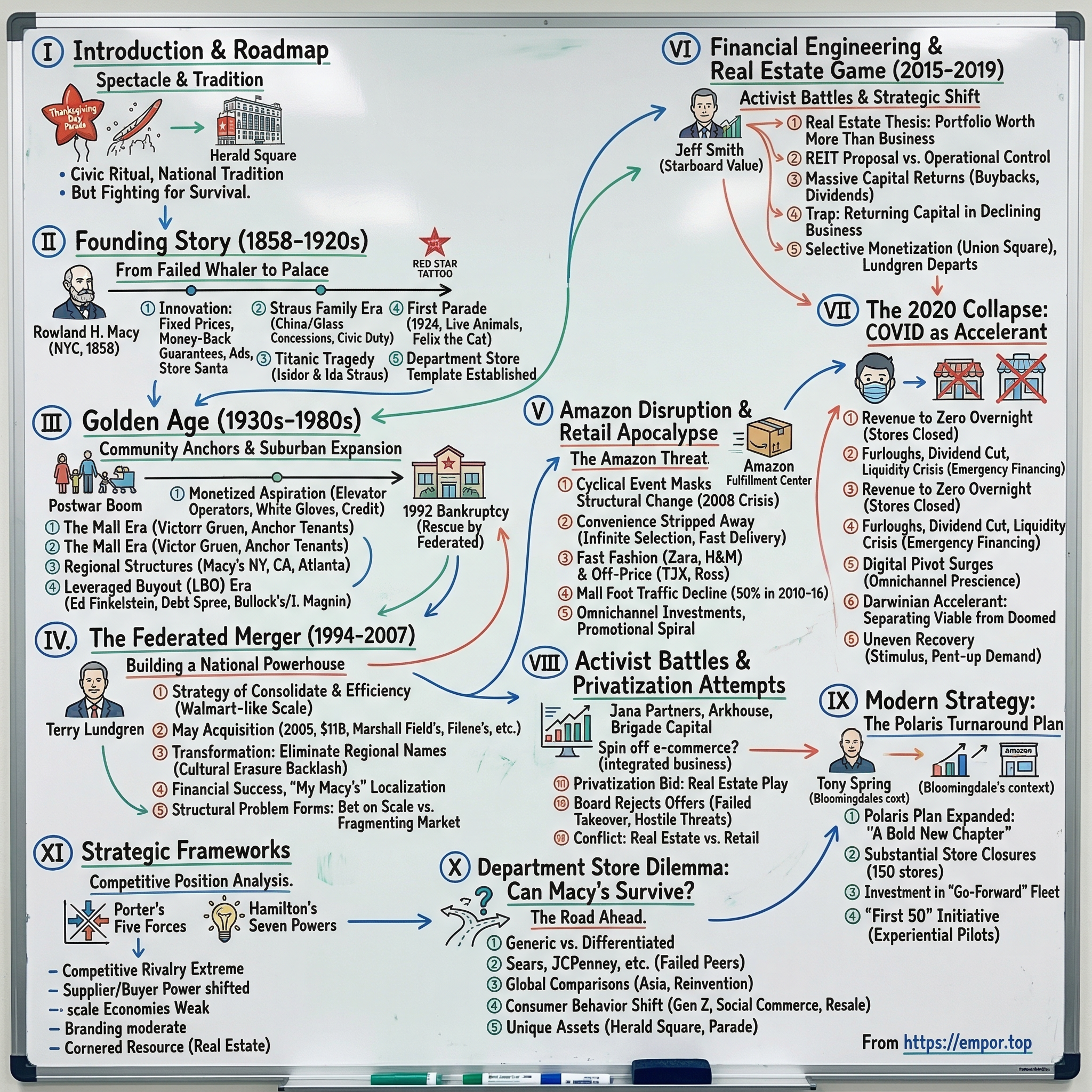

I. Introduction & Episode Roadmap

Picture this: every Thanksgiving morning, roughly fifty million Americans tune in to watch giant helium balloons float down Sixth Avenue past a building that has defined American retail for over a century. The Macy's Thanksgiving Day Parade is not just a marketing event. It is a civic ritual, a national tradition so embedded in the cultural fabric that most people cannot imagine a holiday season without it. That building at Herald Square, spanning an entire city block at 34th Street and Broadway, is more than a store. It is a monument to a particular idea of American commerce: the department store as palace, as community anchor, as aspiration engine for the middle class.

But behind the balloons and the spectacle, Macy's Inc. is fighting for its life.

How did a retail institution that defined American consumer culture for over a century end up battling activist investors, fending off take-private bids, and closing hundreds of stores while its stock trades at a fraction of its peak? How did the company that invented modern retailing become a case study in disruption, financial engineering, and the brutal economics of structural decline?

This is the story of Macy's: from a failed whaler's son who opened a tiny dry goods shop in 1858 to a $28 billion national powerhouse that is now racing to reinvent itself before the clock runs out.

Along the way, we will trace five key inflection points that made Macy's what it is today. First, the audacious Federated merger and $11 billion May Department Stores acquisition that created a national brand but killed beloved regional identities like Marshall Field's and Filene's. Second, the financial engineering era when billions flowed to shareholders through buybacks and dividends instead of into the digital transformation the business desperately needed. Third, the Amazon-driven retail apocalypse that hollowed out the American mall and exposed the structural vulnerabilities of the department store format. Fourth, the COVID collapse that took revenue to zero overnight and nearly killed the company. And fifth, the ongoing activist battles and privatization attempts that continue to define the present, with private equity circling a company whose real estate may be worth more than its enterprise value.

Along the way, we will examine the strategic frameworks that explain why Macy's is in the position it is in, the bull and bear cases for the stock, and the lessons that founders, operators, and investors can extract from one of the most dramatic case studies in American business history.

Every section of this story carries a lesson for anyone trying to understand what happens when an incumbent institution meets a world that no longer needs it in the same way.

II. Founding Story: From Peddler to Palace (1858–1920s)

Rowland Hussey Macy was born on August 30, 1822, on Nantucket Island, Massachusetts, into a Quaker family with deep roots in the whaling trade. At fifteen, he did what Nantucket boys did: he signed aboard the whaleship Emily Morgan and spent four years at sea chasing leviathans across the Pacific. The whaling life was brutal: months of boredom punctuated by hours of violent, dangerous work hauling in creatures the size of buses. Somewhere during those years on the ocean, Macy acquired a tattoo. A red star, inked on his forearm or hand, the kind of mark sailors carried as talismans against the vast indifference of the sea. He could not have known that this piece of sailor's ink would become one of the most recognized logos in retail history.

Whaling did not suit Macy long-term. He came ashore and tried his hand at shopkeeping, which, it turned out, did not suit him either. Between 1843 and 1855, he opened and closed four separate dry goods stores in Massachusetts, California during the Gold Rush, and Wisconsin. Every single one failed. He went bankrupt in 1855. Consider that track record: four ventures, four failures, in four different states over twelve years. Most people would have found another line of work. Macy was not most people. He possessed that particular stubbornness that separates entrepreneurs who eventually succeed from those who simply try.

In 1858, at age thirty-six, carrying the lessons of four failures, he moved to New York City and opened R.H. Macy Dry Goods at the corner of Sixth Avenue and 14th Street. On October 28, 1858, opening day, total sales came to $11.08. It was not an auspicious start. But what happened next reveals why the previous failures mattered. Macy brought to this fifth attempt something his competitors lacked: a relentless, almost compulsive instinct for innovation. He had failed enough times to understand what customers actually wanted.

He instituted fixed prices at a time when haggling was universal in retail. Think about how radical this was: every other merchant in New York expected a negotiation on every sale, which made the shopping experience adversarial and unpredictable. Macy posted his prices and stuck to them. He offered money-back guarantees when most merchants operated on a buyer-beware basis. He placed newspaper advertisements, which was considered vulgar by many established merchants, and illuminated his storefront with gaslight to attract evening passersby. He put a store Santa Claus in the window during the holidays and created themed merchandise displays that turned shopping from an errand into an experience. By the time he replaced his Massachusetts rooster logo with the red star from his whaling tattoo around 1862, the store was already becoming a destination.

The first year's revenues were roughly $85,000. By 1870, the store was doing $1 million in annual sales. Macy expanded aggressively into adjoining buildings, adding department after department: shoes, hats, home goods, toys, eventually food. He was, without using the term, inventing the department store concept, the idea that a single retail establishment could serve every need of a household.

Macy died in Paris on March 29, 1877, from kidney disease, before his creation became a true institution. Ownership passed through family hands until 1888, when two brothers who had been running a china and glassware concession inside the store began buying in. Isidor and Nathan Straus, German-Jewish immigrants with a gift for both commerce and philanthropy, gained full ownership of R.H. Macy & Co. by 1896 and transformed it into something grander than a dry goods shop.

The Strauses understood that a department store could be more than a place to buy things. It could be a civic institution, a gathering place, a symbol of urban sophistication and middle-class possibility. Nathan Straus became famous for his philanthropy, spending much of his fortune providing pasteurized milk to New York's poor and funding tuberculosis prevention. Isidor served briefly in Congress and became a respected voice in New York civic life. Their combined reputation lent the Macy's name a credibility that went beyond commerce.

Under their leadership, Macy's outgrew its 14th Street home. In 1902, they made the bold decision to relocate uptown to Herald Square, at 34th Street and Broadway, so far north of the established shopping district that management initially ran a steam wagonette to shuttle bewildered customers from the old location. The move was considered a gamble: 34th Street was not yet the commercial center it would become. The Herald Square flagship would grow to encompass roughly 2.2 million square feet, making it one of the largest department stores on the planet. It remains there today, an anchor of Midtown Manhattan, its entrance still bearing the brass memorial plaques that tell one of the most poignant stories in American business history.

On April 15, 1912, Isidor and Ida Straus were passengers aboard the RMS Titanic. When the ship began to sink, Isidor refused to board a lifeboat ahead of women and children who were still waiting. Ida refused to leave her husband's side. "I will not be separated from my husband," she told a crew member. "As we have lived, so we will die, together." She gave her fur coat to her maid, told her to get into the lifeboat, and the couple was last seen sitting together on deck chairs, holding hands. The story, confirmed by multiple survivors, became one of the most famous love stories of the Titanic tragedy and cemented a human dimension into the Macy's brand that no amount of advertising could replicate. It was the kind of association that money cannot buy: not a transaction, but a story about love, duty, and sacrifice, permanently fused to the company's identity.

A dozen years later, on Thanksgiving Day 1924, Macy's staged what it called the Macy's Christmas Parade. The inspiration came partly from immigrant employees who wanted to recreate the festive street parades of their European homelands, and partly from the store's desire to declare the official start of the holiday shopping season. The first parade featured four floats, four bands, live animals borrowed from the Central Park Zoo, hundreds of costumed employees, and Santa Claus, who was enthroned on the store balcony as the "King of the Kiddies." Over 250,000 people showed up on that first day. Macy's declared it an annual event on the spot.

The parade evolved rapidly. By 1927, the live animals were replaced with the giant helium balloons that would become the parade's signature. Felix the Cat was the first character balloon that year. Over the following decades, the parade grew into a television spectacle, eventually becoming the second-most-watched event on American TV after the Super Bowl. It has run every Thanksgiving since 1924, pausing only during World War II when rubber and helium were rationed for the war effort. What began as a marketing stunt became a genuine American institution, and the brand that staged it became synonymous with the holidays themselves.

By the late 1920s, Macy's had established the template that would define department store retailing for the next half century: one-stop shopping under one roof, fixed prices, generous return policies, spectacular displays, and an emotional connection to community life that went far beyond transactions. The question was whether that template could survive as America itself transformed.

III. Golden Age: Department Stores as Community Anchors (1930s–1980s)

Walk into a major American department store in 1955 and you entered a world designed to make you feel like someone important. White-gloved elevator operators announced each floor's offerings in measured tones. Perfume counter attendants greeted regulars by name. A restaurant on the upper floors served lunch on real china with cloth napkins. The store extended credit to families who had never had a bank account, introduced them to brands they had only seen in magazines, and offered a curated, aspirational version of American life under one roof. For millions of postwar families moving to the suburbs for the first time, the department store was not just a shop. It was a social institution, a place where you took your children to see Santa, where you registered for your wedding, where the changing of the window displays marked the turning of the seasons.

This was the genius of the department store model at its peak: it monetized aspiration. The store told you who you could become, showed you the products that would get you there, and extended you the credit to buy them. In an era before mass media fragmented attention and before e-commerce provided infinite alternatives, the department store was the place where American consumer culture was staged, curated, and sold.

The postwar economic boom supercharged this model. As the American middle class expanded and migrated to the suburbs, the department store followed. The enclosed shopping mall, pioneered by Victor Gruen at Southdale Center in Edina, Minnesota in 1956, was designed around the department store as its anchor tenant, the gravitational force that pulled foot traffic through the corridors of smaller shops. The symbiosis was elegant: the department store drew customers to the mall, the mall's smaller shops benefited from the traffic, and rent from those shops subsidized the favorable lease terms that anchors received. By the 1970s, there were roughly 1,500 enclosed malls in America. By 1990, there were over 2,500.

Macy's, along with competitors like Bloomingdale's, Nordstrom, Marshall Field's, and regional chains stretching from coast to coast, rode this wave of suburban expansion aggressively. Through the 1950s, 1960s, and 1970s, Macy's opened mall anchor stores across the country, operating as a collection of regional divisions: Macy's New York, Macy's California, Macy's Atlanta, each tailored to local tastes but unified under the red star. The regional structure was important: each division had a president who understood local fashion preferences, weather patterns, demographics, and competitive dynamics. A dress that sold well in Atlanta might gather dust in San Francisco. The best department store operators understood this and merchandised accordingly.

Competition was fierce but the industry was large enough for multiple players to prosper. Bloomingdale's occupied the upscale, fashion-forward niche, positioning itself as the cool, urbane alternative for affluent shoppers. Nordstrom was building its reputation for fanatical customer service on the West Coast, where legends circulated about salespeople who would accept returns of tires even though the store never sold tires. Sears and JCPenney dominated the mass market and middle America. Regional chains like Marshall Field's in Chicago, Filene's in Boston, and Kaufmann's in Pittsburgh had deep community roots that made them almost civic institutions. The department store industry was not a monolith but an ecosystem, each player occupying a slightly different position in the market, each serving a distinct customer segment or geography.

Then came the leveraged buyout era, and Macy's nearly destroyed itself.

Edward Finkelstein had joined Macy's in 1948 as a trainee and risen over four decades to become Chairman and CEO. He was a true merchant, the kind of retailer who could walk a sales floor and spot what was wrong with the merchandise mix in minutes. He modernized the stores' presentation in the 1970s and early 1980s, shifting toward fashion-forward product, introducing celebrity designer partnerships, and making Macy's feel more contemporary and exciting. Under his leadership, Macy's was widely regarded as the best-run department store chain in the country.

But in 1986, fearing a hostile takeover in an era when corporate raiders like Carl Icahn and Ronald Perelman were picking off companies like fruit from a tree, Finkelstein made a fateful decision. He engineered a management-led leveraged buyout, persuading nearly four hundred executives to participate in taking the company private for approximately $3.5 billion. The transaction was financed almost entirely with debt. Finkelstein personally sold his existing stock and options for roughly $10 million, reinvested $4.4 million into the LBO, and pocketed the difference. The executives who participated were betting their personal wealth on the proposition that a private Macy's, free from public market scrutiny, could grow fast enough to service the enormous debt.

Then Finkelstein doubled down. In 1988, riding the wave of LBO-fueled expansion, he acquired the Bullock's and I. Magnin chains from Canadian retailer Robert Campeau for approximately $1.1 billion, expanding Macy's into new markets but strapping even more debt onto an already leveraged balance sheet. The timing was catastrophic. The 1990-91 recession hit consumer spending hard, particularly in the discretionary categories that department stores depended on. Debt service consumed operating cash flows, and the expansion debt from Bullock's and I. Magnin added weight to a structure that was already sagging.

On January 27, 1992, R.H. Macy & Co., 133 years old, filed for Chapter 11 bankruptcy protection with $5.3 billion in liabilities. The filing sent shockwaves through the retail world. Finkelstein, who had given four decades of his life to Macy's, departed within months. The man who was arguably the best department store merchant of his generation was brought down not by his retailing skills but by his financial ambition. It was a cautionary tale that would echo through every subsequent chapter of the company's history: financial engineering can amplify success, but it can accelerate destruction when the underlying business stumbles.

The rescue came from an unlikely quarter. Federated Department Stores, which had itself emerged from its own Chapter 11 bankruptcy in 1992 after being taken down by Robert Campeau's overleveraged acquisition spree, saw the Macy's nameplate as an asset too valuable to let die. In December 1994, Federated acquired R.H. Macy & Co., merging two battered department store empires into a single entity. Federated operated Bloomingdale's, Burdines, Lazarus, Rich's, and other regional chains. Adding the Macy's name, with its national recognition, its parade, its Herald Square flagship, and its emotional resonance with the American consumer, gave Federated something none of its other nameplates could provide. The stage was set for the most aggressive consolidation play in American department store history.

IV. The Federated Merger: Building a National Powerhouse (1994–2007)

Terry Lundgren grew up in Long Beach, California, the son of a produce manager at a local grocery store. He worked his way through the University of Arizona and joined Bullock's department store in Los Angeles after graduation, starting on the sales floor. He moved to Neiman Marcus, then to Federated, where he climbed through the merchant ranks with a combination of charm, competitive intensity, and an unerring eye for what would sell. Colleagues described him as a natural leader: tall, charismatic, and possessed of a confidence that could shade into stubbornness when he believed in a strategy. He became CEO of Federated in 2003 and Chairman in 2004, and from that perch, he executed a strategy of such breathtaking ambition that it would define Macy's for a generation, for better and for worse.

Lundgren's central insight was that the American department store industry was fragmented into dozens of regional operators, each with its own brand, advertising budget, merchandising team, and supply chain. This fragmentation was expensive. Every regional chain ran its own television campaigns, negotiated separately with the same vendors, and operated independent distribution networks. In an era when Walmart was proving that relentless scale could crush competitors, Lundgren believed the same logic applied to department stores. His plan was audacious: consolidate the industry under one national brand and capture the efficiency gains.

The centerpiece was the acquisition of The May Department Stores Company, announced on February 28, 2005, for $11 billion, the largest retail transaction in American history at the time. May operated a sprawling portfolio of regional department store brands: Marshall Field's in Chicago, Filene's in Boston, Kaufmann's in Pittsburgh, Famous-Barr in St. Louis, Hecht's in Washington, Robinsons-May in California, Meier & Frank in Portland, and several others. In a single transaction, Federated nearly doubled in size, becoming the third-largest general merchandise retailer in the United States.

The deal was transformative in ways that went beyond simple revenue addition. May's stores filled geographic gaps in Federated's footprint, creating a truly national department store operator for the first time. The combined company would operate in virtually every major metropolitan area in America, reaching consumers from Boston to Los Angeles, from Chicago to Miami. Lundgren believed this geographic completeness was essential for a simple reason: national advertising.

Consider the economics. Before the merger, if Macy's wanted to run a television commercial during a primetime network broadcast, it was paying for eyeballs in every market but only benefiting from those where it had stores. After the merger, every impression counted. National advertising was cheaper per impression than regional campaigns. A single national brand could negotiate harder with vendors, demanding better terms and exclusive products by offering guaranteed distribution in every major market. Consolidated operations meant fewer distribution centers, fewer regional management teams, fewer duplicated functions. In an era when Walmart was proving that scale economics could crush smaller competitors, Lundgren bet that the same principle applied to department stores. If you could not beat Walmart on price, you could at least match them on efficiency.

But the execution of this strategy required a decision that would haunt Macy's for years: every regional nameplate had to go. On September 9, 2006, more than four hundred stores simultaneously converted to the Macy's name. In a single day, Marshall Field's, Filene's, Hecht's, Famous-Barr, Kaufmann's, Robinsons-May, Meier & Frank, L.S. Ayres, and others ceased to exist. Federated formally renamed itself Macy's, Inc. in June 2007.

The backlash was fierce. In Chicago, where Marshall Field's had been a civic institution since 1852, hundreds of protesters gathered beneath the famous clock at State and Washington on conversion day. They returned on the one-year anniversary. Boycott groups formed online. Local politicians issued statements of regret. The anger was not merely nostalgic. These were brands that had spent decades building trust, community identity, and local relevance. Replacing them with a single national name felt like an act of cultural erasure, and the numbers bore this out. In December 2006, same-store sales at former Marshall Field's locations ran thirty percent below comparable Macy's stores. Internal post-mortems acknowledged that between ten and twenty percent of former May customers simply walked away. Similar patterns played out in Boston, Pittsburgh, and Portland.

Lundgren's team responded with a localization initiative called "My Macy's," launched in 2008, which attempted to tailor merchandise assortments to local tastes within the national brand framework. It was an implicit admission that homogenization had gone too far, a billion-dollar fix for a problem the rebranding had created.

And yet, despite the cultural backlash, the strategy ultimately delivered on its financial promises. Scale economies in purchasing, advertising, and operations drove meaningful efficiency gains. Macy's reached peak revenue of approximately $28.1 billion in fiscal year 2014, operating over eight hundred stores under the Macy's and Bloomingdale's nameplates with approximately 175,000 employees. The company was widely regarded as one of the most competently managed traditional retailers in America. Its private-label merchandise generated higher margins than national brands. Its omnichannel investments were ahead of most peers. Analysts praised Lundgren's vision.

But beneath the impressive top-line numbers, a structural problem was forming. Macy's had bet on scale at precisely the moment when the retail market was fragmenting. The logic of consolidation assumed that bigger was better, that national scale would create insurmountable advantages in purchasing, advertising, and operations. And in the short term, it did. But the world was moving in the opposite direction. Consumers were not looking for one giant store that sold everything adequately. They were seeking specialized retailers that sold specific things brilliantly: lululemon for yoga pants, Sephora for cosmetics, Warby Parker for eyeglasses, and a thousand direct-to-consumer brands for everything else. Alternatively, they were seeking online platforms that offered infinite selection with one-click convenience.

The irony was profound. Macy's had achieved national scale just as scale ceased to be the primary competitive advantage in retail. The consolidation strategy had created a national powerhouse, but it had also created a national target, a single brand that every competitor, from Amazon to a niche Shopify store, could position against. And the forces gathering against it were about to become overwhelming.

V. The Amazon Disruption & Retail Apocalypse (2007–2016)

The 2008 financial crisis hit department stores with particular brutality. Their core customer, the American middle class, pulled back spending with a ferocity not seen since the Depression. But the recession was not the real story. It was a cyclical event that masked a structural transformation. The real story was happening in a fulfillment center in Seattle, where a company called Amazon was building the infrastructure to make the department store model obsolete.

To understand why Amazon was so devastating to Macy's, you have to understand what a department store actually is. It is a curated, general-purpose retailer that makes money by aggregating demand across dozens of product categories under one physical roof. The department store's value proposition was convenience: you could buy a suit, a blender, perfume, and children's shoes in one trip. But Amazon offered the same aggregation with infinite selection, lower prices, no parking hassle, and increasingly fast delivery. The convenience advantage that had sustained department stores since the 1850s was being stripped away, category by category, year by year.

Simultaneously, the fast fashion revolution was attacking from below. Zara, H&M, and Forever 21 offered trendy apparel at a fraction of department store prices, with new styles arriving weekly instead of seasonally. Zara's parent, Inditex, had built a supply chain that could take a design from concept to store shelf in two weeks. Department stores, by contrast, placed orders months in advance and took markdowns on whatever did not sell. The speed differential was devastating: by the time a trend hit Macy's shelves at full price, it was already available at Zara for less.

And off-price retailers like TJX (parent of TJ Maxx and Marshalls) and Ross Stores were siphoning away the bargain-hunting customers who used to wait for Macy's sales. These off-price chains operated on a fundamentally different model: they bought excess inventory from brands and sold it at deep discounts in no-frills stores with low overhead. Their growth was double-digit while department stores were contracting. TJX alone grew from $25 billion in revenue in 2013 to over $50 billion by 2023, essentially building a second Macy's-sized business in a decade on the exact customer segment that Macy's was losing. The middle of the market was hollowing out, and Macy's was standing squarely in it.

Mall foot traffic began its long secular decline. The statistics were grim: between 2010 and 2016, foot traffic to enclosed malls fell by roughly fifty percent according to industry tracking firms. The reasons went beyond e-commerce. The smartphone revolution meant consumers could browse, compare prices, and read reviews without leaving their couch. Social media replaced the mall as the place where teenagers gathered. Streaming entertainment replaced the mall multiplex as the evening's activity. The enclosed shopping mall, which had been the center of American suburban social life for half a century, was losing its relevance as a gathering place, not just as a shopping destination.

Anchor department stores, which depended on mall traffic for a significant share of their customers, felt the decline acutely. The "retail apocalypse" narrative, amplified by media coverage of empty parking lots and shuttered storefronts, became a self-reinforcing cycle: declining traffic led to declining sales, which led to store closures, which reduced traffic further, which led to more closures.

Macy's was not standing still. The company invested heavily in omnichannel capabilities: mobile apps, same-day delivery, buy-online-pickup-in-store functionality, and upgraded e-commerce infrastructure. These were not token efforts. Macy's was one of the first traditional retailers to integrate its inventory systems so that online orders could be fulfilled from any store, effectively turning eight hundred locations into mini distribution centers. It was smart, and it was not enough.

The fundamental problem was that Macy's could not outspend Amazon on technology, could not out-convenience Amazon on delivery, and could not match the selection of a platform with effectively unlimited shelf space. Every dollar spent on digital transformation was a dollar not spent on store experience or merchandise. The company was caught in what strategists call the "stuck in the middle" trap: not cheap enough to compete with off-price, not differentiated enough to compete with specialty retailers, and not digital enough to compete with Amazon.

And then there was the promotional spiral, one of the most corrosive dynamics in department store economics. Here is how it works: as traffic declines, the store runs more sales and promotions to lure customers back. The promotions train customers to wait for discounts rather than pay full price. Full-price sales decline further, so the store runs even more promotions to hit its revenue targets. Gross margins compress. To offset the margin compression, the store cuts staff, reduces service quality, and defers store maintenance. The shopping experience deteriorates, driving more customers to competitors. Which triggers more promotions. It is a death spiral, and every department store in America was caught in some version of it. Macy's, because of its massive scale, was caught in it more visibly than most. The company's "Friends and Family" sale, its "One Day Sale," its "Black Friday Preview" events — they all ran so frequently that the only remarkable thing would have been a week without a sale.

After peaking at $28.1 billion in fiscal 2014, Macy's revenue began to decline. Holiday 2015 same-store sales fell 5.2 percent, a particularly alarming signal during the most important quarter of the year. In January 2016, the company laid off 4,800 employees and targeted $400 million in annual savings. By August 2016, it announced another one hundred store closures and 10,000 additional job cuts, targeting $550 million in savings. The store count began its long march downward: from roughly 850 at peak to 775, then 737, then 673. Each closure announcement made headlines, and each headline reinforced the narrative that department stores were dying.

The human cost was enormous. Tens of thousands of Macy's employees lost their jobs. Communities that depended on Macy's as a major local employer watched those positions disappear. And the retail workers who remained faced an increasingly difficult labor market: fewer hours, more pressure to sell, and the constant background hum of whether their store would be next on the closure list.

Into this difficult environment stepped an activist investor who saw something Macy's management was trying to ignore: the buildings themselves might be worth more than the business inside them.

VI. Financial Engineering & The Real Estate Game (2015–2019)

Jeff Smith, the founder and CEO of activist hedge fund Starboard Value, disclosed a stake in Macy's in July 2015 and immediately began pressing a thesis that would define the company's strategic debate for years.

Starboard's approach was data-driven and detailed. In a presentation released on January 11, 2016, Smith and his team argued that Macy's real estate portfolio was worth approximately $21 billion, a figure that dwarfed the company's market capitalization of roughly $10 billion at the time. The math was seductive: Herald Square alone, sitting on one of the most valuable blocks of commercial real estate in the world, was estimated to be worth several billion dollars. The building's upper floors had been partially converted to office space, and the retail portion occupied prime Manhattan frontage that was essentially irreplaceable. Dozens of other owned properties in prime locations across the country — from Union Square in San Francisco to locations in suburban malls with strong demographics — added up to a massive portfolio of undervalued assets.

Starboard's proposal was straightforward: spin the real estate into a REIT (Real Estate Investment Trust) structure, separating the property assets from the retail operations. For those unfamiliar with the structure, a REIT is a company that owns income-producing real estate and is required by law to distribute at least ninety percent of its taxable income to shareholders as dividends, in exchange for favorable tax treatment. The retail business would then lease back the space from the REIT, and shareholders would own both a real estate company and a retail company, with the combined value exceeding the current market cap. It was the same playbook that had been run at other asset-heavy companies, from Darden Restaurants to Sears, and on paper, it made sense.

Macy's management pushed back, and their argument deserves careful consideration because it remains relevant to every real-estate-intensive business facing similar activist pressure today.

Their argument was operational: owning your own real estate gives you control over your most important physical asset. You can renovate, reconfigure, sublease, or redevelop without a landlord's permission. If you spin the real estate into a REIT and lease it back, you have converted an owned asset into a fixed cost obligation. In a growing business, that fixed cost is manageable. In a declining business, where revenue is falling while rent stays constant, the fixed cost can become a death sentence. The company pointed to Sears, where Eddie Lampert had executed a version of this playbook by spinning off Seritage Growth Properties, and where the result was a hollow retail operation paying rent to its own former real estate while the stores deteriorated from chronic underinvestment.

Instead of a full spin-off, Macy's pursued selective monetization. It sold the upper floors of its Union Square San Francisco location to a hotel developer. It engaged Brookfield Asset Management to analyze roughly fifty properties for mixed-use development potential, adding residential, office, or hotel space above retail floors. These were incremental moves, not the dramatic restructuring Starboard demanded. Frustrated by the pace, Starboard exited its entire Macy's position in May 2017. Jeff Smith publicly acknowledged he had "bought too early," a polite way of saying the thesis was right but the timing was wrong.

Meanwhile, the company was pursuing a different form of financial engineering that would prove equally controversial: returning massive amounts of capital to shareholders. Between roughly 2011 and 2016, Macy's spent approximately $7.7 billion buying back its own shares, a figure representing nearly seventy percent of the company's eventual market capitalization at its trough. Shares outstanding fell from about 421 million to roughly 311 million. The buybacks were executed at prices ranging from the mid-twenties to the high sixties, meaning that enormous sums were spent repurchasing shares near the peak, destroying value that could have been invested in transformation. The quarterly dividend, which grew steadily through the mid-2010s to reach $1.51 per share annually, consumed additional billions.

This was the classic financial engineering trap. In a stable or growing business, buybacks and dividends are excellent ways to return excess capital. But Macy's was not a stable business. It was a declining one, and every dollar returned to shareholders was a dollar not spent on the digital transformation, store renovation, or new format development that might have slowed the decline. The parallel to Sears was uncomfortable: Eddie Lampert had similarly channeled Sears' cash flows into buybacks and financial maneuvers rather than reinvesting in the stores, and by 2018, Sears was bankrupt.

Terry Lundgren stepped down as CEO in the first quarter of 2017, handing the reins to Jeff Gennette, a company lifer who had joined Macy's in 1983 and served as President since 2014. Lundgren remained as Executive Chairman until January 31, 2018, when he fully retired from the board, ending an era in which he had been the architect of Macy's national consolidation strategy. The strategy had achieved its financial objectives in the short term but had left the company vulnerable to the structural shifts that were now accelerating.

Gennette moved to diversify the portfolio. Macy's Backstage, an off-price format launched in fall 2015 to compete with TJX and Ross, expanded from six pilot stores into a broader network of store-within-store locations nested inside full-line Macy's. In February 2015, Macy's had acquired Bluemercury, a luxury beauty and skincare spa chain with sixty stores, for $210 million, adding a small but fast-growing luxury vertical. And Bloomingdale's, always the premium banner in the portfolio, was positioned as a growth engine separate from the Macy's nameplate's challenges.

These were sensible moves, but they were incremental when the situation called for something more dramatic. The company was spending billions on share buybacks while the core business eroded. It was investing in off-price and beauty while the flagship department store format continued to lose relevance. The real estate was valuable, but extracting that value without destroying the operations required a level of strategic creativity that neither management nor its critics had fully articulated. And then came a crisis that made all previous challenges look manageable.

VII. The 2020 Collapse: COVID as Accelerant

On March 18, 2020, Macy's closed all 775 of its stores across the United States. Not some of them. Not temporarily reduced hours. All of them, simultaneously, as the COVID-19 pandemic shut down non-essential businesses across the country. Revenue went to zero overnight. Think about what that means for a company with roughly $24 billion in annual sales: approximately $65 million in revenue disappearing every single day, while costs — rent, insurance, debt service, utilities, security — continued to accrue.

The speed of the crisis was unlike anything the company had experienced, even during the 1992 bankruptcy. In the LBO collapse, the business deteriorated over years. COVID compressed that same destruction into weeks. The stock, which had traded above $17 in mid-February, collapsed to below $5 by late March. At its trough, Macy's market capitalization was less than $1.5 billion — a staggering figure for a company that had been valued at over $25 billion just five years earlier.

Twelve days after the closures, on March 30, the company announced it was furloughing the majority of its 125,000 employees. The term "furlough" was doing a lot of work in that sentence: it meant that roughly 130,000 people suddenly had no income, though Macy's maintained company-funded health benefits through at least May. CEO Jeff Gennette and the board suspended their own salaries. The dividend, which had been a pillar of the shareholder return story for years, was eliminated. Share buybacks, already reduced, stopped entirely.

The liquidity crisis was existential. Macy's was burning cash with no revenue coming in and hundreds of millions in fixed costs, from leases to insurance to the minimum staffing needed to maintain physical assets. The company scrambled to secure approximately $4.5 billion in emergency financing, assembled through a combination of instruments: $1.5 billion drawn from existing revolving credit facilities, approximately $1.3 billion in new bonds secured against real estate assets, and additional arrangements to reach the total. S&P downgraded Macy's credit rating by four notches, landing at B+, just above the lowest speculative-grade category. For a company that had maintained investment-grade ratings for years, this was a marker of how close to the edge it had come.

The speed of the digital pivot was remarkable. With physical stores shuttered, e-commerce became the only revenue channel. Digital sales surged fifty-three percent year-over-year in the second quarter of 2020, during peak store closures. For the full year, e-commerce grew approximately twenty percent, reaching roughly $7.6 billion, and digital penetration jumped from about twenty-five percent of total revenue in 2019 to approximately forty-four percent at its peak. Customers who had never ordered from Macy's online were suddenly doing it regularly. The company's prior investments in omnichannel infrastructure, including the ability to fulfill online orders from store inventory, proved prescient, even though stores were closed, the inventory sitting in them could be shipped to customers.

In June 2020, Macy's announced a formal restructuring plan that included additional corporate layoffs and the acceleration of planned store closures. Roughly 125 stores were marked for closure, reducing the fleet by about one-fifth. The closures were not random: they targeted underperforming mall locations where traffic had been declining for years and where COVID had simply accelerated an inevitable end. Many of these stores were in so-called "C" and "D" grade malls — properties in secondary and tertiary markets where co-tenancy clauses were being triggered by the departure of other anchor tenants. When Sears or JCPenney closed in a given mall, the remaining anchors including Macy's often gained the right to break their leases or renegotiate terms, creating a domino effect that further destabilized already struggling properties.

But COVID did more than force temporary closures. It exposed and accelerated every structural weakness in the department store model. Malls, already struggling, saw their anchor tenants disappear for months. The so-called "mall death spiral" entered a new phase: without anchor tenants, smaller in-line retailers lost the foot traffic they depended on and closed their own stores, which reduced the mall's attractiveness further, which made it harder to replace the departed anchors. When stores reopened, foot traffic recovered only partially. Industry data suggested that by late 2021, mall foot traffic remained fifteen to twenty percent below 2019 levels, a shortfall that represented a permanent shift in consumer behavior rather than a temporary pandemic effect. Consumers who had learned to shop online during lockdowns did not fully return to physical stores. The pandemic compressed years of gradual digital migration into months.

The surprising element was the recovery. Stimulus checks, pent-up consumer demand, and inventory shortages across the retail industry drove a snap-back in spending that benefited survivors. Full-year 2020 revenue bottomed at approximately $17.3 billion. By fiscal 2021, revenue recovered to roughly $24.4 billion, nearly matching pre-pandemic levels.

The recovery, however, was uneven in ways that told a deeper story. The stores that came back strongest were the ones in the best locations with the most invested footprints. The stores that struggled to recover were the ones in dying malls with deferred maintenance and declining foot traffic — precisely the stores COVID would have closed eventually anyway. The pandemic functioned as a Darwinian accelerant, separating the viable from the doomed with brutal efficiency. Management recognized this pattern and used it to justify faster closure of the weakest locations.

But the recovery also masked a permanent change in the competitive landscape: the strong had gotten stronger (Amazon, Walmart, Target, TJX), and the weak had been culled (JCPenney filed for bankruptcy in May 2020; hundreds of smaller retailers closed permanently). The customers Macy's lost during lockdowns did not all come back. Some discovered they did not need a department store at all. Some shifted permanently to online shopping. Some found that off-price retailers offered better value. The pre-pandemic customer base was simply not going to reconstitute itself, and the company would need to earn every shopper's attention in a way it never had before.

Macy's survived. But it emerged into a world where the case for radical transformation was no longer debatable.

VIII. The Activist Battles & Privatization Attempts (2020–2024)

The post-COVID environment attracted activist investors like blood in the water. With Macy's stock battered, its real estate still valuable, and its operating model under existential pressure, the stage was set for a series of confrontations that would test whether the company's board could maintain control of its own destiny. In the world of activist investing, a beaten-down stock with hard assets trading below replacement value is the equivalent of a neon sign reading "opportunity." Multiple parties saw that sign and came running.

In October 2021, Jana Partners, a well-known activist hedge fund, took a stake in Macy's and publicly urged the company to spin off its e-commerce business from its physical stores. Jana's thesis was inspired by Saks Fifth Avenue, which had separated its online operation from its stores earlier that year, attracting a minority investment that valued the digital business at $2 billion, roughly two times sales. Jana portfolio manager Scott Ostfeld estimated that Macy's digital operations could be worth $16.8 billion on a standalone basis, far exceeding the company's total market capitalization.

The proposal had a certain logic: if digital is growing and physical is shrinking, why not separate them and let the market value each independently? Macy's took the idea seriously enough to hire AlixPartners, the consulting firm, to evaluate the concept. CEO Jeff Gennette addressed it directly at an investor day in November 2021. But after analysis, the company concluded that its digital and physical businesses were too deeply integrated to separate profitably. Online orders fulfilled from stores, in-store returns of online purchases, the shared inventory system that turned every location into a distribution node: cutting these connections would destroy value, not create it. Jana exited its position within months, and the e-commerce spinoff died.

The more dramatic battle came from a different direction entirely, and it went to the heart of the question that had hung over Macy's for a decade: is this a retail company or a real estate company?

On December 1, 2023, Arkhouse Management, a real estate-focused investment firm led by Gavriel Kahane, together with Brigade Capital Management, a fixed-income specialist, offered $21 per share to take Macy's private. The bid valued the company at approximately $5.8 billion, representing a thirty-two percent premium to the prior day's closing price. Arkhouse's background was telling: Kahane had experience in real estate development and property monetization, not retail operations. The thesis was familiar: the real estate was worth more than the market was giving the company credit for, and private ownership would allow for patient restructuring without the pressure of quarterly earnings reports and public market scrutiny. But the subtext was clear to every analyst who examined the proposal: the bidders were primarily interested in the buildings, not the business inside them.

Macy's board rejected the offer unanimously in January 2024, citing the bidders' failure to present a viable, fully financed acquisition plan. This was not merely posturing: in the parlance of deal-making, "highly conditional" financing is the polite way of saying the money is not actually there. A serious take-private bid comes with committed financing letters from major banks, demonstrating that the capital to complete the transaction has been arranged. What Arkhouse and Brigade presented, according to the board's assessment, fell well short of that standard.

Arkhouse and Brigade responded with escalating pressure, threatening to take their case directly to shareholders and launch a hostile campaign. They nominated a slate of directors for the board, a standard activist playbook move designed to gain leverage in negotiations.

The next several months played out as a slow-motion chess match. In March 2024, the bidders raised their offer to $6.6 billion, or $24 per share. In June, they bumped it again to $24.80. The board engaged in negotiations, evaluated the proposals, and in July 2024 voted unanimously to end all discussions. The stated reason was the same: the bidders had "failed to deliver a definitive, fully financed and actionable proposal." Reading between the lines, the board believed the company was worth more than the offered price and that the bidders were trying to acquire irreplaceable real estate assets on the cheap.

The failed takeover bid had consequences beyond its immediate outcome. It focused intense investor attention on the gap between Macy's market value and the estimated worth of its real estate portfolio. It accelerated pressure on new CEO Tony Spring, who had taken the helm on February 4, 2024, to demonstrate that organic value creation could exceed what a take-private transaction would deliver. And it raised uncomfortable questions about corporate governance: were the directors protecting shareholder interests by rejecting the bids, or were they protecting their own positions?

For investors watching from the sidelines, the privatization debate crystallized the central tension in the Macy's story. Private equity sees a real estate portfolio worth more than the enterprise value, a cost structure ripe for cutting, and the freedom to execute a multi-year transformation without quarterly earnings pressure. The bears see a declining retail business with demographic headwinds, trapped real estate value that cannot be extracted without destroying operations, and the risk that privatization is just a slow-motion liquidation dressed in strategic language. The bulls counter that the death of department stores has been overstated, that the market is still worth over $150 billion in the United States alone, and that a smaller, better-executed Macy's can thrive. Neither side has been definitively proven right.

IX. Modern Strategy: The Polaris Turnaround Plan (2021–Present)

Jeff Gennette unveiled the Polaris transformation plan in February 2020, literally weeks before COVID-19 rendered its original assumptions obsolete. The plan's core elements survived the pandemic, albeit in modified form: close approximately 125 underperforming stores within three years, invest in roughly four hundred "go-forward" locations, expand Backstage off-price shops, grow off-mall formats, and accelerate digital and omnichannel capabilities.

When Tony Spring succeeded Gennette as CEO on February 4, 2024, he brought a fundamentally different perspective to the turnaround. Spring had spent his entire career at Macy's Inc., joining the company in 1987 and rising through the Bloomingdale's organization. He served as CEO of Bloomingdale's from 2014, overseeing a decade in which the luxury banner maintained its brand cachet and grew its digital business while the Macy's nameplate struggled. Where Gennette was an operations-oriented executive who thought in terms of efficiency and process improvement, Spring was a merchant who thought in terms of brand, experience, and customer emotion. He understood intuitively what made Bloomingdale's work — the sense that walking into the store was an event, not an errand — and his mandate was to bring some of that philosophy to the larger enterprise.

On February 27, 2024, Spring announced "A Bold New Chapter," an expansion and evolution of Gennette's Polaris framework.

The plan was aggressive and specific in a way that previous strategic announcements had not been. Approximately 150 underperforming Macy's-nameplate stores would close by end of 2026, up from Gennette's target of 125. The company initially targeted fifty closures by the end of fiscal 2024, subsequently increased to sixty-five. The surviving fleet of approximately 350 "go-forward" locations would receive meaningful investment in staffing, merchandising, visual presentation, and community engagement. CFO Adrian Mitchell, who also received the title of Chief Operating Officer as part of the leadership transition, provided clear financial guardrails: savings from closures would fund investment in go-forward stores, with the net effect expected to be margin-accretive within two years.

The closure math was straightforward. The 150 stores targeted for elimination were the worst performers in the fleet, generating below-average revenue per square foot and, in many cases, operating at a loss when fully loaded costs including occupancy and depreciation were accounted for. Removing them from the portfolio would mechanically improve average store productivity, average margins, and average customer satisfaction scores, even if total revenue declined. It was subtraction by addition: making the whole healthier by removing the weakest parts.

The most closely watched element of the Bold New Chapter was the "First 50" initiative: fifty go-forward stores designated as elevated experiential pilots. These locations received disproportionate investment in sales associates per square foot, in-store events, localized merchandise assortments, and enhanced visual displays. The concept was essentially a test of whether the department store format could thrive if you spent enough on the experience. The answer, at least in early results, was encouraging. The First 50 stores delivered four consecutive quarters of comparable sales growth and the highest customer satisfaction scores for the Macy's nameplate in years. By the third quarter of fiscal 2024, these locations were outperforming the rest of the fleet by 3.4 percentage points on comparable sales. Spring reported that the fourth quarter performance was "our highest comparable sales of the year, our best performance in 11 quarters" within the pilot stores.

The luxury portfolio remained the brightest spot. Bloomingdale's, operating approximately thirty-three full-line stores, continued to hold its position as a premium destination, and the "Bloomie's" small-format concept, first opened in Fairfax, Virginia in 2021, offered a template for expansion into affluent suburban markets without the overhead of a full-scale department store. Bluemercury, with approximately 158 standalone stores, operated in the fast-growing prestige beauty segment, a category that has proven relatively resistant to online disruption because consumers want to touch, smell, and try products before buying.

Omnichannel integration deepened. Buy-online-pickup-in-store (commonly known as BOPIS), curbside pickup, and same-day delivery became standard offerings across the go-forward fleet. These capabilities matter because they represent the one area where physical retailers have a genuine advantage over pure e-commerce: immediacy. A customer who needs a gift today, or who wants to try something on before committing, or who wants the instant gratification of walking out with a purchase, cannot get that from Amazon.

A nascent digital marketplace strategy, adding third-party sellers to expand online assortment without inventory risk, signaled Macy's awareness that its digital platform needed broader selection to compete. The marketplace model, pioneered by Amazon, allows a retailer to offer millions of products without holding inventory, collecting a commission on each sale. It is capital-light and margin-additive, but it requires significant traffic to attract sellers and significant curation to maintain brand integrity.

On the merchandise front, the company invested in private-label brands, which carry higher margins than national brands, and pursued exclusive partnerships to differentiate its offering. These moves were designed to address the "stuck in the middle" problem: if Macy's could offer products available nowhere else, customers had a reason to visit that Amazon could not replicate.

The workforce dimension deserves attention. With approximately 85,000 to 95,000 employees depending on seasonal cycles, Macy's remained one of the largest private employers in American retail. Labor costs were rising, retention in hourly retail roles was challenging, and the First 50 initiative's emphasis on more and better-trained associates per store represented a significant ongoing investment. The company needed its people to deliver the elevated experience that would justify the store's existence.

The headline financial results told a story of managed decline with pockets of genuine improvement. Fiscal year 2024 net sales came in at $22.3 billion, down 3.5 percent from $23.1 billion the prior year, reflecting ongoing store closures and soft consumer spending. Full-year adjusted diluted earnings per share were $2.64, down from $3.28 the prior year. Fourth quarter net income was $342 million, a meaningful improvement from the net loss of $128 million in the year-ago quarter, suggesting that the cost rationalization from store closures was beginning to flow through to profitability.

The company guided fiscal 2025 to $21.0 to $21.4 billion in net sales, a further decline as the 150-store closure program works through the system. Cash and cash equivalents stood at $1.3 billion, and total debt was approximately $2.8 billion, with no material maturities until 2027. That debt maturity profile provides crucial breathing room: the company does not face a refinancing wall in the near term, which means it can focus management attention on operational transformation rather than balance sheet triage.

The central strategic question is whether the "Bold New Chapter" represents a genuine inflection point or simply a more graceful, better-managed version of the same decline. The First 50 results suggest that the department store format can still work if sufficiently invested in. But scaling that investment across 350 stores while revenue is declining requires a delicate balance between spending enough to drive improvement and maintaining the financial discipline that keeps creditors comfortable. It is a high-wire act with no safety net.

X. The Department Store Dilemma: Can Macy's Survive?

The fundamental question hanging over Macy's is not whether the company will exist in five years. It almost certainly will. The question is whether it will exist as a vital, growing retail enterprise or as a slow-motion real estate liquidation.

The roster of the fallen provides sobering context. Sears, once the largest retailer in America with over 3,500 stores and $55 billion in annual sales at its peak, is effectively extinct, reduced to approximately five remaining locations and a single Kmart. Sears' collapse was not merely a failure of management, though Eddie Lampert's financial engineering and chronic underinvestment certainly accelerated the decline. It was a failure to recognize that the business model itself was obsolete. JCPenney, which filed for bankruptcy in May 2020 after years of declining sales and failed turnaround attempts, survived only because mall operators Brookfield and Simon Property Group paid roughly $800 million to keep it alive as an anchor tenant for their properties. The fact that JCPenney's saviors were mall owners rather than retailers tells you everything about the economic dynamics at work: the stores were worth more as traffic generators for surrounding tenants than as standalone retail operations. Lord & Taylor, once the oldest department store chain in America, closed its doors permanently in 2020. Barneys New York, the beloved high-fashion institution, shut down the same year. Century 21, the New York off-price institution, also succumbed. The graveyard of American department stores is large and growing.

Among the survivors, the strategies vary instructively.

Nordstrom, facing many of the same pressures as Macy's, went private in a $6.25 billion deal completed in May 2025, with the founding family and Mexican retail group El Puerto de Liverpool splitting ownership roughly fifty-fifty. The Nordstrom family bet that private ownership would provide the patience to invest in long-term transformation without quarterly earnings pressure. It is the clearest test case for whether the department store's problem is the format itself or the public market's inability to give management the time and capital to fix it.

Dillard's, controlled by the founding family in Little Rock, Arkansas, has arguably been the best-managed survivor and offers a masterclass in disciplined retail operations. The Dillard family kept the company focused on Sun Belt and secondary markets where competition was less intense, invested heavily in own-brand merchandise that carried higher margins, maintained stores in excellent condition, and returned massive amounts of capital through buybacks that dramatically reduced the share count. Dillard's fiscal 2024 revenue was approximately $6.6 billion, a fraction of Macy's, but its stock performance over the past five years has been extraordinary, driven by a combination of stable operations and aggressive capital return.

Kohl's, operating in the off-mall value segment, has struggled with declining sales and strategic missteps, including a high-profile partnership with Sephora shop-in-shops that generated buzz but failed to reverse the fundamental revenue decline. Kohl's announced 27 store closures in January 2025.

Internationally, the picture is more nuanced, and instructive for anyone trying to predict Macy's future. Department stores continue to thrive in parts of Asia, where dense urban populations, public transit-oriented shopping patterns, and cultural preferences for in-person retail maintain foot traffic. In Japan, department store operators like Isetan Mitsukoshi have reinvented themselves as curators of luxury and experience, with food halls, art exhibitions, and personal shopping services that draw customers for reasons beyond mere transaction. In South Korea, Shinsegae and Lotte department stores operate as destinations, combining retail with entertainment, dining, and cultural programming. In China, luxury-oriented department stores remain key distribution channels for premium brands, with the physical store serving as a brand-building venue as much as a sales channel.

The Western model's decline is not a universal law of retail evolution. It is a reflection of specific structural changes in American and European consumer behavior: suburbanization, car dependence, the shift to online shopping, and the rise of off-price and fast fashion alternatives. The Asian examples suggest that the department store format can survive and even thrive when it reinvents itself as an experiential destination rather than a transactional one. The question is whether American consumers, with their car-dependent lifestyles and delivery-everything expectations, will ever value that kind of physical retail experience in the way their Asian counterparts do.

The consumer behavior shifts are perhaps the most concerning long-term challenge, and they deserve careful examination because they strike at the heart of whether Macy's can attract the next generation of shoppers.

Younger consumers, particularly Gen Z, shop differently than the Baby Boomers who built Macy's into a powerhouse. They discover brands on TikTok and Instagram, not in department store aisles. They buy directly from brands' websites, valuing the authentic connection that a DTC relationship provides. They care about sustainability and are increasingly skeptical of the mass-consumption model that department stores represent. They prefer experiences over possessions: travel, dining, concerts, and events compete directly with discretionary retail spending for their wallets.

The resale market, led by platforms like ThredUp and The RealReal, is growing rapidly, driven by both economic and environmental motivations. Rental models like Rent the Runway offer access without ownership. These are not temporary trends or pandemic-era anomalies. They represent a generational recalibration of the relationship between consumers and physical retail. The challenge for Macy's is existential: if the next generation of consumers does not develop the department store habit, no amount of operational improvement will prevent a slow fade.

Macy's unique assets should not be dismissed. Herald Square remains one of the most iconic retail locations in the world. The Thanksgiving Day Parade generates billions of media impressions annually. Brand recognition, while strongest among older demographics, is nearly universal. The real estate portfolio, while complicated to monetize, represents genuine embedded value. Bloomingdale's and Bluemercury provide exposure to luxury and beauty segments that continue to grow.

The myth that department stores are dead deserves careful examination. The reality is more nuanced. What is dying is the generic, mid-market, mall-anchored department store that offers nothing you cannot get better somewhere else. What survives, and in some cases thrives, are stores that offer genuine differentiation: extraordinary service (Nordstrom), disciplined value (Dillard's), luxury curation (Neiman Marcus under new ownership), or irreplaceable location and cultural significance (Herald Square). The question for Macy's is whether it can migrate from the dying category to the surviving one, and whether it can do so fast enough with a fleet of 350 stores rather than a boutique portfolio of twenty.

Whether these assets add up to a viable future or merely a more interesting liquidation story depends entirely on execution.

XI. Strategic Frameworks: Porter's Five Forces & Hamilton's Seven Powers

Understanding Macy's competitive position requires looking beyond the company's own strategy to the structural forces shaping the industry and the sources of durable competitive advantage, or lack thereof. Two frameworks — Michael Porter's Five Forces and Hamilton Helmer's Seven Powers — provide complementary lenses for this analysis. Porter tells us about the attractiveness of the industry Macy's operates in: how profitable the average participant can expect to be. Helmer tells us about Macy's specific competitive advantages: whether the company possesses durable powers that can sustain above-average returns. The picture from both frameworks is challenging, but not without nuance.

Competitive Rivalry is extreme. Macy's competes not against a handful of similar department stores, as it did in the 1980s, but against essentially the entire retail universe. Amazon dominates online, offering unlimited selection with next-day delivery. Walmart and Target offer everyday low prices with improving merchandise. TJX Companies and Ross Stores have built formidable off-price businesses that intercept the bargain-hunting customer who used to shop Macy's sales events. Specialty retailers from lululemon to Sephora dominate individual categories. Direct-to-consumer brands bypass traditional retail entirely. And within the remaining department store segment, differentiation has eroded to the point where one mid-tier store is largely interchangeable with another. The promotional intensity is punishing: Macy's runs near-constant sales events, training customers to never pay full price, which compresses margins and devalues the brand.

The threat from new entrants is high and getting higher. Digital-native brands can launch with a Shopify store and an Instagram account, reaching consumers at a fraction of the cost that a physical retailer incurs. Pop-up and experiential retail models allow brands to create physical presences without the permanent cost structure of a department store. The barriers that once protected incumbents, primarily the capital required to build and operate hundreds of physical stores, have become liabilities rather than moats.

Supplier bargaining power has shifted meaningfully. Brand vendors, which used to depend on department stores as their primary distribution channel, now operate their own direct-to-consumer stores, sell through Amazon, and run e-commerce sites. A brand like Nike does not need Macy's to reach consumers in the way it did twenty years ago. Luxury brands are increasingly selective about their retail partners, preferring to control their distribution and maintain brand image. Macy's private-label brands provide some leverage, since those products are available nowhere else, but private label remains a partial solution.

Buyer power is at historic highs. Consumers have infinite choice, total price transparency through comparison shopping apps, and zero switching costs. Loyalty programs exist, and Macy's Star Rewards program offers benefits tied to the Macy's credit card, but these create marginal rather than meaningful switching costs. A customer dissatisfied with Macy's experience can be shopping at Nordstrom, Target, or Amazon within seconds. The core Macy's customer demographic, middle-income consumers aged forty-five and above, is not growing, while younger cohorts show less affinity for the department store format.

The threat of substitutes encompasses almost every alternative form of retail. E-commerce substitutes for convenience. Off-price stores substitute for value. Fast fashion substitutes for trend. Rental and resale platforms substitute for ownership. Experiential spending, from travel to dining to entertainment, substitutes for material goods. Every category that Macy's serves faces a category killer that does that one thing better.

Through the lens of Hamilton Helmer's Seven Powers framework, the picture is equally challenging.

Scale Economies are weak. While Macy's size provides some purchasing leverage and advertising efficiency, these advantages have eroded as digital platforms achieve scale effects that dwarf physical retail. Amazon's scale in logistics, data, and vendor negotiation surpasses anything Macy's can match. Walmart's scale in procurement is unassailable. And Macy's fixed cost base, heavily weighted toward physical real estate, means that declining sales directly erode unit economics. Scale is a liability when the business is shrinking.

Network Effects are essentially absent. A department store does not become more valuable to each customer as more customers use it. There is no flywheel dynamic of the kind that powers Amazon's marketplace. Macy's nascent digital marketplace strategy could theoretically create network effects if it achieves scale, but it is far too early and too small to constitute a power.

Counter-Positioning works against Macy's, not for it. Digital-native and direct-to-consumer brands have successfully counter-positioned against traditional department stores. These brands offer lower prices (by eliminating the retail middleman), more authentic brand stories, and a shopping experience designed for how people actually live today. Macy's cannot easily adopt these models without cannibalizing its existing business, which is the classic counter-positioning trap for incumbents.

Switching Costs are very weak. The Macy's credit card creates some financial incentive to continue shopping, but the rewards are modest relative to the switching costs created by, say, an enterprise software platform or an integrated operating system. Customers face no meaningful penalty for shopping elsewhere.

Branding is the one area where Macy's retains moderate power. The Macy's name is among the most recognized retail brands in America. The Thanksgiving Day Parade generates enormous annual awareness. Herald Square is an iconic destination. But brand associations are aging with the customer base, and among younger consumers, the Macy's brand connotes neither aspiration nor relevance. Bloomingdale's retains stronger brand cachet, particularly in the luxury segment, but it operates at a much smaller scale.

Cornered Resource is arguably Macy's strongest power, and it resides in its real estate portfolio. Locations like Herald Square are irreplaceable. Prime mall and urban locations in major markets represent assets that cannot be replicated. But this power is complicated: the resource is underutilized, potentially trapped, and difficult to monetize without undermining operations. A cornered resource that you cannot effectively deploy is more of an option than a power.

Process Power is weak. Macy's does not possess proprietary processes or capabilities that competitors cannot replicate. Its omnichannel technology is good but not differentiated. Its merchandising processes are standard for the industry. Legacy systems and organizational culture make adaptation slower than necessary.

The synthesis is sobering but clarifying. Macy's possesses one meaningful competitive power: its real estate portfolio as a cornered resource. Every other power is weak or absent, and all five of Porter's competitive forces are working against the business model.

This does not mean Macy's will fail. Companies can survive and even thrive in structurally disadvantaged positions through superior execution, niche focus, and creative strategy. Dillard's has proven this in the department store sector specifically. But it means that survival requires something approaching a fundamental reinvention of the format, not merely better management of the existing one. The First 50 initiative is the first genuine attempt at such reinvention: not just operating the same department store more efficiently, but reimagining what the department store experience means in an age of infinite online alternatives. Whether fifty pilot stores can become a blueprint for 350 is the central strategic question facing the company today.

XII. Bull vs. Bear Case & Investment Perspective

The Bull Case

Every investment debate begins with a question: what does the market already know, and what might it be missing? With Macy's trading at a market capitalization of approximately $5.3 billion as of early 2026, the market is pricing in continued decline. The bull case rests on the proposition that the market is pricing in too much decline and not enough transformation.

The optimistic view begins with arithmetic. The company's real estate portfolio, even after years of closures and monetization, is estimated to be worth a substantial multiple of the current enterprise value. Herald Square alone, sitting on some of the most valuable real estate in Manhattan, represents enormous embedded value. The Arkhouse and Brigade take-private attempts validated this thesis: sophisticated real estate investors were willing to pay a significant premium to current market prices to gain control of these assets.

Beyond real estate, the bulls point to operational improvement. The First 50 stores are delivering four consecutive quarters of comparable sales growth and materially outperforming the rest of the fleet. If the elevated experience model can be scaled across the 350 go-forward locations, the comparable sales trajectory for the remaining business could inflect positively even as total revenue declines from store closures. The luxury portfolio, Bloomingdale's and Bluemercury, is growing and profitable in segments that have shown resilience through retail cycles.

Tony Spring's leadership brings a merchant's eye developed over a decade running the most successful banner in the portfolio. The "Bold New Chapter" strategy is coherent and actionable. Digital penetration continues to grow. The balance sheet is manageable, with $1.3 billion in cash and no major debt maturities until 2027. The death of department stores has been overstated: the American department store market still represents over $150 billion in annual spending, and a well-run player can capture a profitable share.

There is also a contrarian argument about the real estate: rather than viewing it as trapped value, the bulls argue that the physical store network, when properly invested in, is itself a competitive advantage that pure e-commerce players cannot replicate. Customers can touch and try products, receive personalized service, and take items home immediately. The stores function as distribution nodes for e-commerce fulfillment, reducing last-mile delivery costs. And the physical presence creates brand visibility and trust that digital advertising cannot fully replace. If Spring can demonstrate that a well-run Macy's store generates attractive four-wall economics, the narrative shifts from "trapped real estate" to "productive retail infrastructure."

The Bear Case

The pessimistic view starts with the same arithmetic and reaches a starkly different conclusion. Real estate value is real, but it is trapped. You cannot sell the building without closing the store, and closing the store without a replacement tenant destroys the value of the surrounding mall. Sale-leaseback transactions convert an owned asset into a fixed cost obligation, adding rent to a declining revenue base. The real estate is valuable in theory but extraordinarily difficult to monetize in practice without accelerating the operational decline.

The secular trends are relentless. Department store spending as a share of total retail continues to decline. The core Macy's customer demographic is aging out, and younger consumers show no signs of gravitating toward the format. Amazon, Walmart, and the DTC ecosystem have structural advantages in cost, selection, and convenience that Macy's cannot match. The promotional intensity required to drive traffic compresses margins to unsustainable levels.

The competitive position analysis is damning: weak or absent advantages across nearly every dimension of strategic power. The company is caught in the middle, not cheap enough to compete on value, not differentiated enough to compete on experience, and not digital enough to compete on convenience. The First 50 results are encouraging but may simply prove that you can generate growth by overspending on a handful of stores, which is not a scalable or profitable model.

Debt and pension obligations further constrain strategic flexibility. While the current debt load of approximately $2.8 billion is manageable at current cash flow levels, any significant revenue decline or margin compression could push leverage ratios into uncomfortable territory. The company also carries pension and post-retirement benefit obligations that represent ongoing cash commitments. In a rising-interest-rate environment, the cost of refinancing debt increases, and in a declining-revenue business, the capacity to service that debt shrinks. The balance sheet is not in crisis, but it leaves limited room for error.