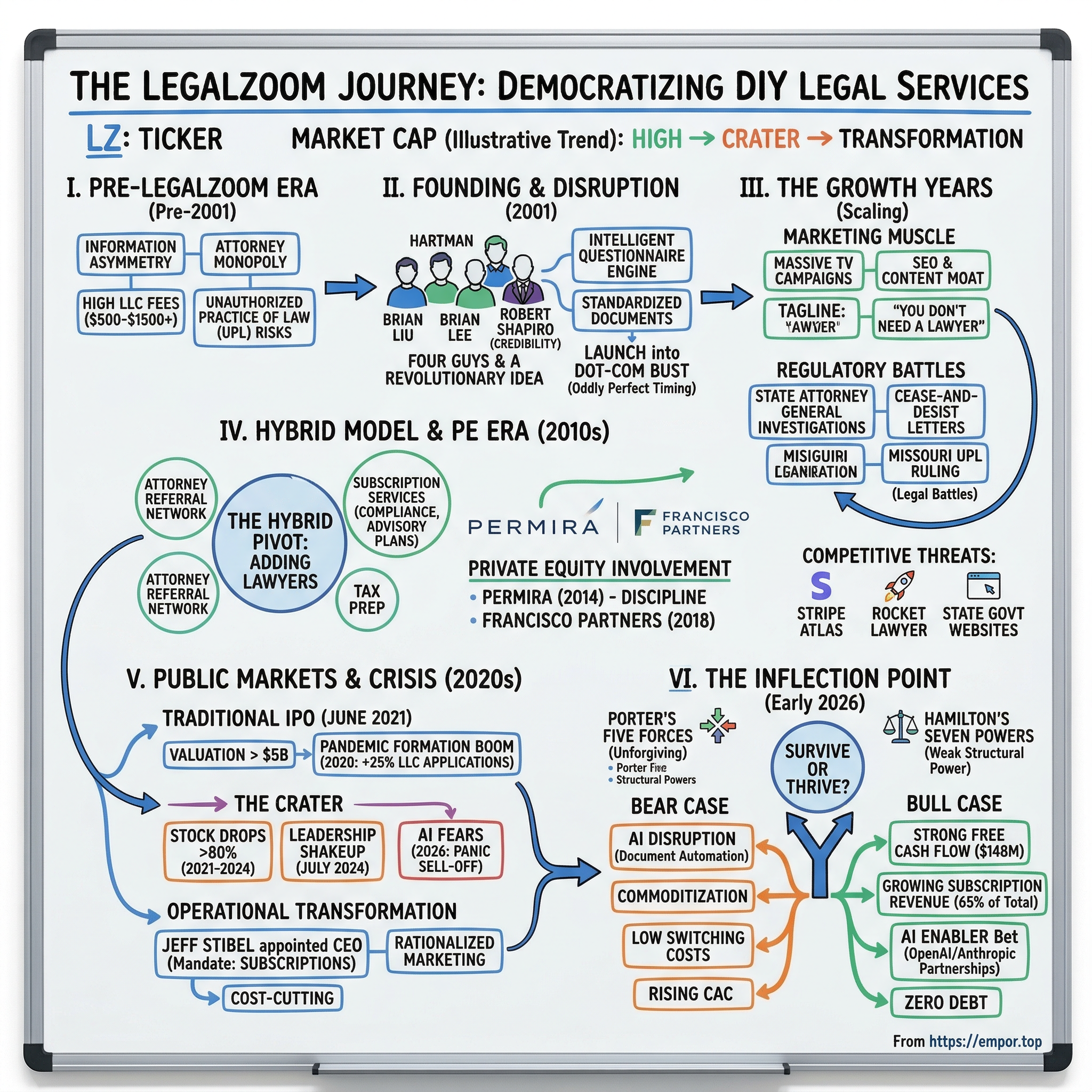

LegalZoom: The Story of DIY Legal Services

I. Introduction & Episode Roadmap

Picture this: a twenty-six-year-old entrepreneur sits in her apartment in Austin, Texas, laptop open, a half-eaten burrito growing cold beside her. She has an idea for a business—a mobile dog grooming service—and she knows she needs an LLC. Her father tells her to call a lawyer. She Googles it instead and within forty-five minutes, for seventy-nine dollars plus state filing fees, LegalZoom has generated her articles of organization, her operating agreement, and an EIN application. No office visit. No billable hour. No three-week waiting period. She clicks submit and goes back to her burrito.

That scene has played out millions of times since 2001. LegalZoom has helped form more businesses in America than any other platform, processing nearly half a million formations in 2021 alone—roughly one every single minute. The company generated $756 million in revenue in fiscal 2025, employs thousands of people, and has built a subscriber base of approximately two million compliance customers. By any measure, it changed the way ordinary Americans interact with the legal system.

But here is the paradox at the heart of the LegalZoom story: the company that democratized legal services for millions of small businesses has struggled mightily to build the kind of durable competitive advantage that rewards long-term shareholders. LegalZoom went public in June 2021 at a valuation exceeding five billion dollars. Within three years, the stock had cratered more than eighty percent. A leadership shakeup in mid-2024 sent shares to their all-time low. And as of early 2026, the specter of artificial intelligence—the very technology that could supercharge LegalZoom's platform—has instead terrified investors into pricing the stock near its lowest levels ever.

The central question is deceptively simple: How did a website that lets you create an LLC for seventy-nine dollars disrupt a centuries-old profession—and why has building a lasting business around that disruption proven so difficult?

This is a story about democratization and its limits. About the difference between breaking open a market and owning it. About what happens when you lower barriers for customers and simultaneously lower them for competitors.

It is a cautionary tale of capital markets timing, a case study in operational discipline forced by crisis, and increasingly, a test of whether incumbents can ride the AI wave rather than drown in it. The narrative arc runs from dot-com era origins through a turbulent IPO, a stock price collapse, forced leadership change, and a financial turnaround that is still unfolding.

Along the way, it raises questions that matter far beyond legal services: Can professional services ever be fully commoditized? What does a moat look like in a regulated industry? And when does brand awareness stop being a competitive advantage and start being merely an expensive habit?

II. The Legal Industry Before LegalZoom

To understand what LegalZoom disrupted, you have to understand what existed before it—and why the American legal system was practically designed to resist disruption.

In the 1990s, forming a simple limited liability company required, for most people, hiring an attorney. The process was not complicated—an LLC formation involves filling out a standardized state form, paying a filing fee, and drafting a basic operating agreement. The legal work itself might take an experienced attorney thirty minutes. But the bill would routinely run five hundred to fifteen hundred dollars, and in major metropolitan areas, significantly more. Trademark filings, simple wills, and business contracts followed the same pattern: standardized documents, minimal customization, and pricing that reflected the lawyer's hourly rate rather than the complexity of the task.

The reason for this pricing power was structural, not technical. American bar associations had spent more than a century constructing what amounted to a professional monopoly. The doctrine of "unauthorized practice of law"—UPL—made it illegal for non-lawyers to provide legal advice or prepare legal documents for others. The definition of what constituted "legal advice" versus "information" was deliberately vague and varied wildly from state to state. A company that helped customers fill out forms could be accused of practicing law without a license. The penalties were real: fines, injunctions, even criminal prosecution.

This created an information asymmetry that was almost comically extreme. Customers had no way to know what a legal service should cost, how long it should take, or whether the document they received was any different from a template available for free at the county clerk's office. Law firms had zero incentive to educate them. The entire system functioned as a black box: you put money in one end and legal documents came out the other, with no transparency about what happened in between.

There were early challengers. Nolo Press, founded in Berkeley in 1971, published self-help legal books and fill-in-the-blank forms that let consumers handle simple legal matters themselves. By the 1990s, Nolo had built a modest business selling books like "Incorporate Your Business" and "Nolo's Simple Will Book." But the products were inherently limited—a book could provide information, but it could not interact with the customer, check for errors, or file documents with state agencies. The UPL doctrine also constrained what Nolo could offer: the moment a product crossed from "information" to "advice," it entered legally dangerous territory.

Then came the internet, and with it, the tantalizing possibility that technology could do what books could not. The dot-com boom of the late 1990s spawned a wave of startups attempting to disintermediate professional services: travel agents, stockbrokers, insurance agents, real estate agents. The thesis was elegant—information technology could eliminate middlemen, reduce costs, and give consumers direct access to products and services that had previously required professional gatekeepers. In most of these verticals, the thesis proved at least partially correct. Expedia gutted the travel agency business. E*Trade and its ilk democratized stock trading. Lending Tree changed mortgage shopping.

But legal services were different, and not just because of UPL restrictions. Lawyers occupied a unique cultural position—part trusted advisor, part fiduciary, part officer of the court. The emotional stakes of legal transactions felt higher than booking a flight or opening a brokerage account. A badly formed LLC could mean personal liability. A flawed will could mean family litigation. Customers needed not just information but reassurance, and that reassurance had traditionally come from a human being with a law degree and a framed diploma on the wall.

Consider the economics from the consumer side. A small business owner in 1998 who wanted to form an LLC in California faced a state filing fee of around seventy dollars—plus an attorney fee of anywhere from five hundred to two thousand dollars. The attorney's work consisted primarily of asking the client a series of standard questions (What is the business name? Who are the members? How will profits be distributed?), typing the answers into a template, and filing the result with the Secretary of State. The information asymmetry was so extreme that most clients had no idea they were paying fifteen hundred dollars for what amounted to thirty minutes of work and a form that was ninety-five percent identical to every other LLC filing in the state.

The question hanging over the legal industry at the turn of the millennium was whether technology could provide that reassurance at scale—and whether the bar associations would allow it to try.

III. Founding Story: Four Guys and a Revolutionary Idea

The origin of LegalZoom reads like a Hollywood pitch, which is fitting because two of its founders came from the entertainment world and one was among the most famous lawyers in American history.

In the late 1990s, Brian Liu and Brian Lee were working together in Los Angeles's entrepreneurial scene. Liu, a Yale Law School graduate, had practiced briefly at the powerhouse firm O'Melveny & Myers before pivoting to business. Lee, a serial entrepreneur with a background in e-commerce, would later co-found ShoeDazzle with Kim Kardashian and The Honest Company with Jessica Alba. The third co-founder, Edward Hartman, brought technology chops and operational experience. But the fourth name on the founding documents was the one that turned heads: Robert Shapiro.

Yes, that Robert Shapiro. The criminal defense attorney who had represented O.J. Simpson in the 1995 murder trial was, by the late 1990s, one of the most recognizable lawyers in America. Shapiro brought something the other three founders lacked: instant credibility in the legal world and a Rolodex that could open doors in Hollywood, media, and corporate America. He also brought something more subtle—a deep understanding of how ordinary Americans perceived the legal profession. Shapiro had seen both sides: the rarefied world of high-profile litigation and the far more common experience of small business owners and families who needed simple legal documents but found the process intimidating and expensive.

The founding insight was straightforward but powerful: most legal documents are standardized. An LLC operating agreement in California follows the same basic structure whether you are forming a dog grooming business or a technology consultancy. The articles of incorporation in Delaware are virtually identical from company to company—the differences come down to a handful of variables like the company name, the number of authorized shares, and the name of the registered agent. The customization that lawyers provided—and charged handsomely for—was largely a matter of asking the right questions and plugging answers into the right template. What if software could ask those questions?

It was a question that seems obvious in retrospect but was genuinely radical at the time. The legal profession had operated for centuries on the premise that legal work required legal judgment—that even routine documents demanded the expertise of a licensed attorney. LegalZoom's founders looked at the actual documents being produced and saw a different reality: in the vast majority of cases, the "judgment" consisted of choosing between two or three standard options based on the client's straightforward answers to straightforward questions.

The team built what amounted to an intelligent questionnaire engine. Customers would answer a series of guided questions about their business, family situation, or intellectual property needs, and the software would assemble a customized legal document based on their responses. The technology was not artificial intelligence in any modern sense—it was decision-tree logic, essentially a sophisticated choose-your-own-adventure for legal forms. But it was powerful enough to produce documents that were functionally equivalent to what a junior associate at a law firm would draft for the same purpose.

The critical legal and strategic question was existential from day one: Was LegalZoom a legal service or a technology company? If it was a legal service, it was arguably engaging in the unauthorized practice of law. If it was a technology company—a "document preparation service"—it was merely helping customers create their own documents, no different in principle from selling them a typewriter and a form book.

LegalZoom launched in 2001, squarely into the teeth of the dot-com bust. The timing was terrible for fundraising but oddly perfect for their product. The economic slowdown meant that small business owners were even more cost-conscious than usual, and the idea of paying a lawyer a thousand dollars to file a form that LegalZoom could help you complete for a fraction of the cost had obvious appeal.

The early product lineup was focused and practical: LLC formations, incorporations, trademark filings, and basic estate planning documents like wills and living trusts. These were the bread-and-butter transactions that generated the bulk of revenue at small law firms across the country—and the ones where the gap between what lawyers charged and the actual complexity of the work was widest.

The lawyer pushback was immediate and fierce. Bar associations across the country received complaints. Cease-and-desist letters arrived. State attorneys general opened investigations. In Missouri, a state court found that LegalZoom had engaged in the unauthorized practice of law and ordered the company to stop operating in the state. Similar actions were threatened or initiated in several other jurisdictions. The company spent years in courtrooms defending its right to exist—a grimly ironic situation for a company whose mission was to reduce its customers' need for lawyers.

But customers kept coming. The product-market fit was undeniable. LegalZoom was not selling a luxury or a nice-to-have; it was selling access to a basic business necessity that had been artificially overpriced for decades. Every LLC formation was a small act of economic empowerment, and word-of-mouth spread fast among the small business community.

What made the early LegalZoom product work was something that looks obvious in hindsight but was genuinely innovative at the time: the guided questionnaire. Rather than presenting customers with a blank form and legal jargon, the software walked them through a conversational series of questions—"What will your business be called? Where will it operate? Who are the owners?"—and assembled the answers into a properly formatted legal document. Think of it like TurboTax for legal forms: the underlying document was standardized, but the customer experience felt personalized and accessible. The technology was not sophisticated by modern standards—it was essentially a series of if-then decision trees with template insertion—but it solved the core problem of making legal document preparation feel approachable to people who had never interacted with the legal system before. For the first time, a person with no legal knowledge could produce a document that was functionally identical to what a lawyer would have created, at a fraction of the cost and time.

The early revenue model was simple: charge a flat fee for document preparation, significantly below what an attorney would charge but high enough to generate attractive gross margins. Formation fees started at ninety-nine dollars (later reduced to seventy-nine dollars as competition intensified), trademark filings were in the same range, and estate planning documents like wills and trusts carried modestly higher price points. The beauty of the model was its scalability—the same questionnaire and template system could serve a hundred customers or a hundred thousand with minimal incremental cost.

The company had found its flywheel—though, as we will see, keeping it spinning would prove far more challenging than starting it.

IV. The Growth Years: Scaling Through Marketing

If LegalZoom's founding was a story of product innovation, its growth phase was a story of marketing muscle. And the company developed an appetite for advertising that would ultimately become both its greatest strength and most persistent vulnerability.

By the mid-2000s, LegalZoom had figured out its playbook. The product was working—customers were successfully forming LLCs, filing trademarks, and creating wills through the platform. The question was how to reach the millions of potential customers who did not yet know the service existed. The answer was blunt-force marketing: search engine optimization, paid search advertising, and eventually, a massive television campaign that made LegalZoom a household name.

The SEO strategy was particularly effective in the early days. When someone Googled "how to form an LLC" or "do I need a lawyer to incorporate," LegalZoom wanted to be the first result. The company invested heavily in content marketing, building an enormous library of educational articles about business formation, intellectual property, estate planning, and small business compliance. This content served a dual purpose: it drove organic search traffic and it established LegalZoom as a trusted authority—a brand that knew legal topics even if it was not, strictly speaking, a law firm.

The scale of this content operation deserves appreciation. Over the years, LegalZoom built out thousands of pages covering topics from "What is a registered agent?" to "How to trademark a name" to "Differences between an LLC and an S-Corp." Each article was optimized for specific search queries, creating a web of content that captured potential customers at the moment they were beginning to think about forming a business or handling a legal matter. This SEO moat—while not impregnable—represented millions of dollars of invested content creation and years of domain authority building that a new competitor could not easily replicate.

The television advertising, which ramped up significantly in the latter half of the decade, carried a message that was simultaneously empowering and provocative: "You don't need a lawyer for this." The tagline was genius—five words that crystallized the value proposition while implicitly challenging the entire legal establishment. The ads featured testimonials from satisfied customers—real small business owners who had formed their companies through LegalZoom—and emphasized affordability, simplicity, and speed.

Robert Shapiro appeared in early campaigns, lending his celebrity and legal credibility to the brand. Here was a man who had defended O.J. Simpson in the trial of the century, telling America that simple legal documents did not require expensive lawyers. The implicit message was clear: if one of America's most famous lawyers was endorsing this service, it must be legitimate. The Shapiro endorsement was worth far more than any paid celebrity spokesperson could provide—it was an insider validating an outsider's thesis about his own industry.

The marketing spend worked. LegalZoom grew rapidly, reaching millions of customers and establishing itself as the dominant brand in online legal services. But the strategy had a structural problem that would haunt the company for years: customer acquisition costs were high, and there was limited natural retention. A customer who formed an LLC in 2007 might not need another legal document for years—or ever. Each new customer had to be acquired from scratch, and as competition for search keywords intensified, the cost of acquisition kept climbing.

Meanwhile, LegalZoom was fighting regulatory battles on fifty fronts simultaneously. Each state had its own rules about unauthorized practice of law, and what was legal in California might be prohibited in North Carolina. The company hired armies of compliance lawyers—another irony—and developed state-specific versions of its products and disclosures. Some states required LegalZoom to register as a "legal document preparation service." Others required specific disclaimers. A few attempted to ban the company outright. This regulatory patchwork created real operating costs and complexity, but it also served as a barrier to entry: any competitor wanting to replicate LegalZoom's national footprint would need to navigate the same minefield.

The fundamental business model during this period had two pillars. The first was transactional revenue from document preparation—formation fees, trademark filings, will creation. These transactions carried attractive gross margins because the marginal cost of generating an additional document was negligible once the template and questionnaire system had been built. The second pillar, which would grow in importance over time, was compliance and subscription services: registered agent services, annual report filings, compliance alerts, and other ongoing obligations that small businesses needed to maintain their legal standing. These subscriptions were lower-margin but recurring, providing a revenue stream that did not depend on acquiring new customers each quarter.

The lawyer resistance during this period deserves a closer look, because it reveals the structural dynamics that both protected and constrained LegalZoom. Bar associations in multiple states filed complaints alleging unauthorized practice of law. In North Carolina, the state bar issued a cease-and-desist. In Connecticut, an investigation was opened. The most consequential action came in Missouri, where a court ruled that LegalZoom had indeed engaged in the unauthorized practice of law by selecting and assembling legal documents for customers—activities that crossed the line from "information" to "advice." LegalZoom fought these battles with a simple but powerful argument: the company was not providing legal advice; it was providing a technology tool that helped customers create their own documents. The distinction was legally meaningful, and LegalZoom eventually prevailed or settled in most jurisdictions. But the legal expenses were significant, and the uncertainty hung over the company like a persistent fog.

Institutional investors noticed the underlying strength despite the regulatory noise. In 2011, LegalZoom attracted venture capital from heavyweights IVP (Institutional Venture Partners) and Kleiner Perkins Caufield & Byers—firms more commonly associated with high-growth software companies than legal services businesses. The investment validated LegalZoom's positioning as a technology company, at least in the eyes of Silicon Valley. It also raised the stakes: with blue-chip VCs on the cap table, the expectations for growth, scalability, and an eventual exit intensified considerably. The company was no longer a scrappy startup fighting bar associations; it was a venture-backed growth company with institutional pressure to deliver returns.

Then came the private equity heavyweights. In February 2014, European buyout firm Permira acquired between forty-seven and fifty percent of LegalZoom for two hundred million dollars, valuing the company at approximately four hundred twenty-five million dollars. The investment brought not just capital but governance discipline and a push toward operational efficiency. Bryant Stibel, the investment firm of future CEO Jeff Stibel, also participated in this round. Permira took majority board control, installing directors who would shape the company's strategic direction for the next decade.

For investors tracking the LegalZoom story, this growth era established the central tension that persists today: the company built a powerful brand and massive customer acquisition engine, but neither translated into the kind of pricing power or customer lock-in that characterizes truly great businesses. LegalZoom could get customers in the door cheaply enough to generate solid revenue growth, but it could not keep them there without spending again, and again, and again.

V. The Attorney Network and the Hybrid Model

By 2010, LegalZoom faced an uncomfortable strategic reality. The pure DIY model had taken the company far, but it was bumping against ceilings—regulatory, competitive, and economic—that threatened to cap its growth.

The regulatory pressure was the most immediate concern. Bar associations had not given up their fight against online legal services, and some of the legal challenges were gaining traction. The Missouri ruling had been a wake-up call, and while LegalZoom ultimately prevailed or reached settlements in most jurisdictions, the constant litigation was expensive, distracting, and created genuine uncertainty about the company's long-term legal standing.

The strategic response was counterintuitive but shrewd: if the bar associations' primary objection was that LegalZoom was practicing law without lawyers, then add lawyers. Starting around 2010, the company began building an attorney referral network—a marketplace that connected LegalZoom customers with licensed attorneys who could review documents, provide legal advice, and handle matters too complex for automated document assembly. The model was similar to what companies like Avvo and later UpCounsel were building, but with one critical advantage: LegalZoom already had the customers.

Think of it as a two-lane highway. In the fast lane, customers who needed simple, standardized documents—LLC formations, basic trademarks, straightforward wills—could use the automated platform and be done in minutes. In the slow lane, customers with more complex needs—business disputes, estate planning for blended families, trademark oppositions—could be matched with an attorney through the LegalZoom network. The genius of the model, in theory, was that every customer started in the fast lane, generating transactional revenue, and some percentage migrated to the slow lane, generating referral and subscription revenue.

This hybrid approach served multiple strategic purposes. It defused some of the UPL criticism by positioning LegalZoom as a complement to traditional legal services rather than a replacement. It opened new revenue streams through attorney referral fees and subscription-based legal plans. And it began to address the customer retention problem: a small business that formed its LLC through LegalZoom could now also get its contracts reviewed, its trademark disputes handled, and its tax questions answered through the same platform.

The business model evolution was reflected in the revenue mix. Subscription and compliance revenue grew as a share of total sales, reducing the company's dependence on one-time transactional fees. LegalZoom introduced a "Business Advisory Plan" that bundled compliance monitoring, registered agent services, and attorney consultations into a monthly subscription. Tax preparation services were added. Estate planning expanded beyond simple wills into more complex instruments like living trusts.

But the hybrid model introduced its own complications. Each layer of service added operational complexity and organizational confusion. Managing a network of independent attorneys—ensuring quality control, handling customer complaints when an attorney underperformed, maintaining compliance with each state's bar rules about referral fees and advertising—was fundamentally different from running a software platform. The attorneys were not LegalZoom employees; they were independent professionals with their own practices, their own schedules, and their own quality standards. The company was caught between identities: Was it a marketplace connecting customers with lawyers? A SaaS platform for small business compliance? A service business with technology on top? The answer, frustratingly, was "a little of each"—and none of them neatly.

Competition was also intensifying. Rocket Lawyer, launched in 2008, offered a similar combination of document automation and attorney access with a subscription-first business model. IncFile—which would later rebrand as Bizee—undercut LegalZoom on price, offering free LLC formations (exclusive of state fees) and attracting budget-conscious entrepreneurs. State governments were also improving their own filing websites, making it easier for customers to bypass intermediaries entirely. And a new wave of fintech companies, led by Stripe Atlas, began offering business formation as a feature bundled with payment processing—threatening to commoditize the very service at the core of LegalZoom's business.

The revenue impact of the hybrid model was meaningful. By the mid-2010s, subscription and compliance revenue was growing as a percentage of total sales, smoothing out the lumpy nature of transactional revenue and providing better visibility into future earnings. The company introduced tiered subscription plans—basic compliance packages, premium business advisory plans, and full-service legal plans that included attorney consultations. Each tier carried different margins and retention characteristics, creating a layered business model that was more resilient but also more complex to manage and communicate to investors.

The internal strategic debate during this period was intense: How much should the company invest in technology versus services? Should it compete on price or move upmarket? Could it build network effects by deepening relationships with both small businesses and attorneys, or would it forever be stuck in the no-man's-land between a tech platform and a professional services firm? The tension between "marketplace" (connecting customers and lawyers), "SaaS" (selling software subscriptions), and "service business" (providing hands-on assistance) was never cleanly resolved—and arguably remains unresolved today. Each identity implies different growth strategies, different margin profiles, and different valuation frameworks. The inability to clearly answer "what kind of company are we?" would prove to be a persistent challenge in the public markets. These questions remained largely unsettled as LegalZoom entered the next phase of its story—the long and winding road to the public markets.

VI. The First IPO Attempt and the Private Equity Era

In May 2012, LegalZoom filed a registration statement with the SEC, signaling its intention to go public. The S-1 filing pulled back the curtain on a business that was growing nicely but carried significant question marks. Revenue was approaching four hundred million dollars. The customer base numbered in the millions. But the filing also revealed dependence on marketing spend, regulatory risks that filled pages of risk factors, and a business model that Wall Street struggled to categorize.

Was LegalZoom a technology company deserving of a high-growth multiple? Or was it a legal services business with a website—a glorified document preparation shop that happened to operate online? The distinction mattered enormously for valuation. Tech companies in 2012 were commanding revenue multiples of five to ten times or more. Legal services businesses traded at two to three times revenue, if they were public at all.

The IPO never happened. LegalZoom withdrew its filing in the fall of 2012, citing market conditions—the Facebook IPO debacle in May 2012 had briefly chilled the tech IPO market, and investor appetite for consumer-facing internet companies had soured. But insiders acknowledged that the company also struggled to find the right investor narrative. The withdrawn IPO was not a crisis, but it was a telling signal: LegalZoom had a product customers loved, a brand everyone recognized, and a business model that did not quite fit any of the boxes that public market investors wanted to check.

What followed was nearly a decade in private equity's embrace—a period that would fundamentally reshape the company's operations and strategic ambitions. Permira had already taken its large stake in 2014, and in July 2018, LegalZoom announced a five hundred million dollar secondary investment led by Francisco Partners and GPI Capital, with participation from Franklin Templeton and Neuberger Berman. That transaction valued the company at approximately two billion dollars—nearly five times what Permira's 2014 investment had implied. The capital was used partly for secondary transactions, allowing early investors and employees to cash out some of their holdings, and partly to fund continued growth investments.

The PE era brought a focus on operational metrics and a push to diversify revenue. LegalZoom invested in its technology infrastructure, improving the customer experience and building mobile capabilities. Subscription products were refined and expanded. The company experimented with AI-powered tools for document review and customer service automation—early-stage efforts that would later become central to the company's strategy. Dan Wernikoff, a former executive at Intuit—the company behind TurboTax—was recruited as CEO in October 2019, signaling a strategic orientation toward the kind of subscription-based, technology-enabled business model that Intuit had perfected in tax preparation.

Wernikoff's arrival was significant for another reason: he understood how to build a subscription business in a category where the core transaction was episodic. At Intuit, he had been senior vice president and general manager of the TurboTax business, where the foundational insight had been that customers who filed their taxes once through the software would come back year after year, creating a powerful retention loop. The TurboTax model showed that even in a category with an inherently annual transaction, you could build a subscription-like business with high retention rates if the product was good enough and the switching costs were high enough.

Wernikoff saw a similar opportunity at LegalZoom: form an LLC once, then stay for compliance monitoring, registered agent services, tax filing, and ongoing legal guidance. The critical difference, however, was that tax filing is mandatory and annual—customers must do it every year—while many of LegalZoom's compliance services felt optional to small business owners who were cutting costs. The challenge was converting one-time customers into subscribers, and on that metric, progress was steady but slow.

The competitive landscape during the PE era was evolving in ways that would become problematic. Stripe Atlas launched in 2016, offering Delaware C-Corp formation bundled with a Stripe merchant account, a bank account at Silicon Valley Bank, and legal templates from Orrick—essentially giving startups everything they needed to incorporate and start processing payments in a single package. The strategic implication was alarming for LegalZoom: formation was becoming a loss leader for companies with more valuable products to sell downstream. If Stripe could give away formation to acquire payment processing customers, what did that say about the standalone value of the formation business?

Then came the pandemic. COVID-19 hit the American economy like a wrecking ball in March 2020, shuttering businesses and throwing millions out of work. But an unexpected thing happened alongside the destruction: business formations surged. In 2020, approximately 4.3 million new business applications were filed with the IRS, a twenty-five percent increase over the prior year. Laid-off workers became freelancers, side hustles became businesses, and the great resignation was already underway before anyone coined the term. LegalZoom was the direct beneficiary. In 2020, the company claimed that ten percent of all new LLCs and five percent of all new corporations in America were formed through its platform. Revenue jumped from roughly four hundred eight million in 2019 to four hundred seventy-one million in 2020—a fifteen percent increase during a year when much of the economy was contracting.

The pandemic boom did more than juice the numbers. It validated the thesis that online legal services were not a niche but a default—that the shift from lawyers' offices to websites was permanent and accelerating. When physical law offices closed during lockdowns, even customers who might have preferred the traditional route were forced online. Many discovered that the experience was faster, cheaper, and perfectly adequate for their needs. The behavioral shift was real, and it persisted even after lockdowns ended.

But the boom also masked underlying weaknesses that would become painfully apparent once the tailwind faded. Customer acquisition costs were rising, competition was intensifying, and the per-customer economics were not improving at scale. The strong revenue growth numbers of 2020 and 2021 created an illusion of operating leverage that did not actually exist. It also created the conditions for what came next: a return to the public markets, this time with wind at the company's back and a capital markets environment that was, for a brief and extraordinary moment, willing to pay almost any price for growth.

VII. Going Public: The IPO and the Euphoria

On June 30, 2021, LegalZoom finally achieved what it had attempted and abandoned nine years earlier: it went public. But the company that listed on the Nasdaq was a very different animal from the one that had filed its S-1 in 2012.

A common misconception—fueled partly by the timing—is that LegalZoom went public via a SPAC merger. It did not. The company executed a traditional initial public offering, pricing shares at twenty-eight dollars apiece and raising approximately seven hundred six million dollars in gross proceeds. The deal was underwritten by a blue-chip syndicate led by J.P. Morgan and Morgan Stanley, with Barclays, Bank of America Securities, Citigroup, Credit Suisse, and Jefferies filling out the book. A concurrent private placement accompanied the offering. The IPO implied a fully diluted valuation in the range of five to seven billion dollars, depending on which share count methodology investors used—a remarkable number for a company that had been valued at two billion just three years earlier.

The pitch to investors was compelling: LegalZoom had recurring revenue through its subscription products, a massive total addressable market in small business services, and the tailwind of a secular shift from offline to online legal services. The pandemic formations boom made the growth story tangible. Management talked about a fifty-one billion dollar serviceable addressable market and single-digit market share—the implication being that the company had decades of runway ahead.

The market responded with enthusiasm. Shares opened above the IPO price and surged in the weeks that followed, reaching an all-time high of $39.85 on August 10, 2021—just six weeks after the debut. At that peak, LegalZoom was valued at roughly seven and a half billion dollars—more than seventeen times the valuation Permira had paid in 2014 and nearly four times the 2018 secondary round valuation. For the private equity sponsors, the founders, and the early employees, it was a triumphant moment. The long road from a withdrawn 2012 filing to a successful 2021 listing had finally delivered a public market exit.

Robert Shapiro, the co-founder whose name and celebrity had helped legitimize the company two decades earlier, watched from a board seat he would eventually relinquish. Brian Liu, who had served as CEO through the growth years before stepping back, saw his founding vision validated by one of the largest legal technology IPOs in history. Brian Lee, who had gone on to co-found multiple successful consumer companies, added another notch to his entrepreneurial record.

But euphoria has a short half-life in the stock market, and the forces that would unravel LegalZoom's valuation were already in motion. The IPO came during a period of extraordinary exuberance in the public markets—the same window that saw companies like Robinhood, Coinbase, and dozens of SPAC-merged businesses debut at valuations that would prove wildly unsustainable. Interest rates were near zero. Speculative capital was abundant. And investors were willing to pay premium multiples for "tech-enabled" businesses with recurring revenue, regardless of whether the underlying economics justified the valuation.

For LegalZoom specifically, the numbers beneath the headline growth told a more complicated story. Revenue was growing, but customer acquisition costs were not falling with scale. The subscription business was building, but churn rates suggested that converting one-time formation customers into long-term subscribers was harder than the investor presentation implied. Gross margins were healthy, but operating margins were compressed by the relentless marketing spend required to maintain growth. And the competitive landscape was not standing still: Bizee, ZenBusiness, Northwest Registered Agent, and others were gaining share with aggressive pricing and modern user experiences.

In the second half of 2021, the stock began a decline that would continue, with intermittent rallies, for nearly three years. Lockup expirations flooded the market with insider shares. The broader rotation away from growth stocks accelerated as the Federal Reserve signaled interest rate increases. And LegalZoom's quarterly results, while not disastrous, consistently failed to demonstrate the kind of operating leverage that would justify a multi-billion-dollar valuation. Each earnings report seemed to tell the same story: revenue growing in the high single digits, marketing spend stubbornly high, and profitability just around the corner but never quite arriving.

The IPO had given LegalZoom the capital and public market currency it needed. What it had not given the company was time—the market's patience for the growth-to-profitability transition was running out faster than anyone expected.

There is a subtle but important distinction between LegalZoom and the SPAC-merged companies that went public during the same window. Unlike Lucid Motors, Joby Aviation, and dozens of other businesses that used blank-check companies to reach the public markets, LegalZoom went through the rigorous underwriting process of a traditional IPO, with full SEC review and institutional investor due diligence. The company's prospectus was scrutinized by analysts at J.P. Morgan, Morgan Stanley, and a half-dozen other investment banks. This should have provided a valuation reality check—and perhaps it did, relative to the even more extreme valuations that some SPAC mergers achieved. But the broader market euphoria of mid-2021 was powerful enough to overwhelm even traditional gatekeeping, and LegalZoom's IPO valuation reflected the mood of the moment more than the economics of the business.

VIII. Crisis and Transformation: The Pressure Cooker

The speed of the decline was breathtaking. From its August 2021 high near forty dollars, LegalZoom's stock fell to the mid-twenties by the end of 2021, then to the mid-teens by the end of 2022, and then into single digits by late 2023 and into 2024. The chart looked like a ski slope—a brief peak followed by a long, relentless descent with only occasional bumps of relief. An investor who bought a thousand dollars' worth at the IPO price held roughly two hundred forty-three dollars' worth by mid-2024—a seventy-six percent loss in three years. For those who bought near the August peak, the losses were even more severe.

What went wrong? The answer is a combination of macro headwinds, operational challenges, and a market that reassessed what LegalZoom's business was actually worth. To understand the scale of the destruction: LegalZoom's peak market capitalization of roughly seven and a half billion dollars had shrunk to barely one billion by mid-2024. In dollar terms, more than six billion dollars of shareholder value had evaporated. The Permira investors who had been involved since 2014 watched their triumphant public exit turn into a paper loss relative to the IPO price.

The macro story was straightforward and painful: the pandemic-era business formation boom was normalizing. After the surge to 4.3 million new business applications in 2020, followed by even higher numbers in 2021—the highest levels in American history—the pace of new formations began to moderate. The great resignation was cooling. The stimulus checks that had funded thousands of entrepreneurial experiments had been spent. Many of the pandemic-era businesses—the Etsy shops, the DoorDash side hustles, the consulting LLCs—had quietly dissolved. This was not a collapse—business formation rates remained elevated relative to pre-pandemic levels—but the deceleration hit LegalZoom's transactional revenue directly. Meanwhile, the Federal Reserve's aggressive interest rate increases in 2022 and 2023 hammered growth-stock valuations across the market, and LegalZoom was caught in the undertow.

Operationally, the company was struggling with the core tension that had defined it since its founding: customer acquisition was expensive, competition was intensifying, and the path to meaningful profitability required either dramatically improving unit economics or dramatically cutting costs. Revenue growth decelerated from over twenty percent in 2021 to eight percent in 2022 and about six and a half percent in 2023. These were not terrible numbers, but they were a far cry from the growth trajectory that the IPO valuation had priced in.

A particularly painful moment came on May 7, 2024, when first-quarter results disappointed on nearly every key metric: average revenue per subscriber, average order value, and new business formation counts all came in below expectations. The stock plummeted roughly twenty-four percent in a single trading session. Investors who had believed the turnaround story was working suddenly questioned whether the problems were deeper than management had let on.

Then came the most dramatic moment. On July 9, 2024, LegalZoom announced that CEO Dan Wernikoff was departing and would be replaced by Jeff Stibel, who had been serving as Board Chairman since 2018 and whose investment firm had been involved with the company since the 2014 Permira transaction. The announcement was abrupt and unexpected. The stock fell approximately twenty-five percent in a single day, closing at $5.86 and briefly touching $5.33—its all-time low. The Rosen Law Firm launched a securities class-action investigation on behalf of shareholders, alleging that the company may have made misleading statements about its business prospects.

Stibel's appointment carried a specific mandate: accelerate the transition to a subscription-centric business model. The choice of Stibel was itself revealing. He was not a legal industry executive or a consumer technology visionary; he was a subscription business operator. His background at companies like Dun & Bradstreet and in digital media had given him deep experience in the mechanics of recurring revenue: how to reduce churn, how to optimize pricing tiers, how to maximize customer lifetime value. The board was sending a clear signal about where it wanted the company to go.

The board's theory was that LegalZoom's transactional revenue—dependent on new customer acquisition each quarter—was inherently volatile and expensive to maintain, while subscription revenue was more predictable and carried better long-term economics. Stibel, who had built his career around subscription and digital media businesses, was positioned as the right leader for this pivot.

The operational overhaul that followed was aggressive. Marketing spend was rationalized, with the company shifting from brand-building television campaigns to more targeted, higher-ROI digital channels. The product organization was restructured around subscriber retention and lifetime value rather than pure customer acquisition volume. Cost-cutting initiatives hit non-core activities. And the company began investing more deliberately in technology—particularly AI—as a means of improving both customer experience and operating efficiency.

The strategic review that followed Stibel's appointment was comprehensive. Management assessed each product line, each marketing channel, and each customer segment through the lens of lifetime value relative to acquisition cost. Products and channels that could not justify their cost were cut or restructured. The registered agent business—where LegalZoom serves as a company's official agent for receiving legal documents—was identified as a particularly attractive subscription product because of its high retention rates and low marginal cost. Compliance monitoring services were bundled and simplified. The attorney network was restructured to improve quality and reduce management overhead.

The results were slow to show but real. By fiscal 2024, revenue had grown to approximately six hundred eighty-two million dollars, and the company was generating meaningful adjusted EBITDA. More importantly, the subscription business was growing faster than the transactional business—a structural shift that, if sustained, would improve the quality and predictability of earnings over time. The company added over a hundred thousand net new subscription units in 2023 alone.

The revenue numbers during this transformation period tell the story of a company in transition. After growing over twenty percent in 2021 on the back of the pandemic boom, revenue growth decelerated to eight percent in 2022 and about six and a half percent in 2023, before recovering to three percent in 2024 as the subscription pivot took hold. The absolute revenue numbers continued to grow—from roughly $574 million in 2021 to $682 million in 2024—but the deceleration spooked growth investors who had bought the stock at multiples that assumed much faster expansion.

For investors, the crisis period established a critical lesson about LegalZoom's business model: growth-at-all-costs was not viable in a business with high customer acquisition costs and limited pricing power. The activist pressure—whether from institutional shareholders, the securities investigation, or the board itself—forced a necessary reckoning with unit economics. The question going forward was whether the pivot to profitability could coexist with enough growth to justify a premium valuation, or whether LegalZoom was simply managing a controlled decline into a smaller, more profitable business.

IX. The Inflection Point: Survive or Thrive?

In February 2026, LegalZoom reported its fiscal 2025 results, and the numbers told a story of genuine financial improvement. Revenue reached $756 million, an eleven percent increase over the prior year—the strongest growth rate since the pandemic era. Subscription revenue hit $492.5 million, growing thirteen percent and now accounting for roughly sixty-five percent of total sales. Net income was $15.4 million—modest in absolute terms but significant as a proof point that the company could be profitable on a GAAP basis. Adjusted EBITDA came in at $172.2 million, a twenty-three percent margin. Most impressively, free cash flow reached a record $147.9 million, up forty-eight percent year over year.

The balance sheet looked healthy: $203 million in cash and zero debt as of year-end 2025. The company had roughly two million subscription units, growing fourteen percent annually, and had announced a hundred-million-dollar increase to its share repurchase authorization—a signal that management believed the stock was undervalued and that returning capital to shareholders was a better use of cash than incremental marketing spend. On a pure cash-flow basis, LegalZoom was beginning to look like a real business rather than a growth experiment.

For the first quarter of 2026, management guided to revenue of $200 to $203 million—implying roughly ten percent year-over-year growth—and adjusted EBITDA of $34 to $36 million. The EBITDA guidance represented a slight year-over-year decrease, which management attributed to a timing shift in marketing spend toward the peak business formation season. These numbers suggested stability and continued momentum, if not acceleration.

But the stock market was not impressed. As of early March 2026, LegalZoom shares traded near $6.67—roughly seventy-six percent below the IPO price and eighty-three percent below the all-time high. The market capitalization hovered around $1.2 billion. On an enterprise value to free cash flow basis, the stock was trading at single-digit multiples—a valuation typically reserved for businesses with serious structural problems or no growth prospects.

The culprit, at least in early 2026, was artificial intelligence. In late January 2026, when Anthropic released enhanced agentic AI capabilities for its Claude platform, a wave of panic swept through software and services stocks that were perceived as vulnerable to AI disruption. LegalZoom's stock fell nearly twenty percent in a single day and continued declining to a fifty-two-week low of $6.14 on February 24, 2026. The logic was blunt: if AI could automate legal document preparation, what was LegalZoom's reason to exist?

The company's response to the AI threat has been to embrace it rather than run from it. In February 2025, LegalZoom announced a "Connector" integration built directly into Anthropic's Claude ecosystem, allowing users to move from AI-powered legal analysis to real attorney guidance on the same platform. Later in 2025, the company announced a collaboration with OpenAI's ChatGPT, integrating LegalZoom's products and services directly into ChatGPT's agent capabilities—a partnership that drove a twelve percent single-day stock surge on the day of the announcement. In March 2025, Pratik Savai was hired as Chief Technology Officer specifically to lead AI integration and platform scalability. Savai came from Elation Health and had previously spent sixteen years at Cornerstone OnDemand, where he helped scale the company to over eight hundred forty million dollars in recurring subscription revenue.

LegalZoom's AI strategy rests on a specific bet: that the "last mile" of legal services—the compliance requirements, regulatory filings, attorney review, and ongoing maintenance that follow initial document creation—cannot be fully automated by generalist AI tools. In management's framing, AI makes the top of the funnel larger and cheaper (more people can draft initial documents) while increasing the value of the middle and bottom of the funnel (compliance, review, and ongoing advisory services). The company has positioned itself as "human-in-the-loop"—using AI to improve efficiency and customer experience while maintaining the attorney network and compliance infrastructure that AI alone cannot replicate.

On the competitive front, LegalZoom made a significant acquisition in February 2025, purchasing Formation Nation—the parent company of Inc Authority and Nevada Corporate Headquarters—for $49.3 million in cash plus approximately 2.2 million shares of restricted stock. The deal brought over a hundred forty experienced small business service professionals and two distinct brands: Inc Authority, a low-cost formation service, and NCH, a premium consultative service. The acquisition was designed to expand LegalZoom's go-to-market strategy by adding a high-touch, consultative channel alongside its self-service platform.

The competitive landscape remains intense and increasingly segmented. Bizee (the rebranded IncFile) continues to attract budget-conscious customers with free LLC formations, essentially using formation as a loss leader to sell registered agent services and compliance packages. ZenBusiness has emerged as a credible challenger with strong customer reviews, modern technology, and aggressive pricing. Northwest Registered Agent competes on privacy and simplicity, appealing to customers who want a low-profile formation experience. Rocket Lawyer maintains its subscription-first approach, offering unlimited legal documents for a monthly fee.

And state government websites continue to improve, making it easier for savvy entrepreneurs to file their own documents directly—eliminating the intermediary entirely. Wyoming, Delaware, and several other formation-popular states have built online filing systems that are increasingly user-friendly, with step-by-step guidance that mimics (on a basic level) what LegalZoom's own questionnaire engine provides.

The myth versus reality check on LegalZoom's AI positioning is worth pausing on. The consensus narrative in early 2026 is that AI will destroy companies like LegalZoom by automating document preparation—the very service that built the business. The reality is more nuanced. AI tools can indeed generate a first draft of an LLC operating agreement or a basic will. But they cannot file documents with state agencies, serve as a registered agent, monitor compliance deadlines, or provide the accountability and quality assurance that small business owners need for documents with legal consequences. The real question is not whether AI can replace LegalZoom's document preparation—it probably can—but whether LegalZoom can position itself as the execution layer that sits on top of AI-generated documents. That is the bet management is making with its Anthropic and OpenAI partnerships.

For investors evaluating LegalZoom today, the critical question is whether the financial turnaround—strong free cash flow, growing subscriptions, improving margins—represents a genuine inflection point toward sustainable value creation, or whether it is simply the result of cost-cutting that has temporarily boosted profitability while undermining long-term growth.

X. Business Model Deep Dive and Unit Economics

To understand LegalZoom's investment case, you need to understand how it actually makes money—and why the economics of each revenue stream tell very different stories.

The business has three primary revenue categories. First is transactional revenue: the fees customers pay for one-time document preparation services like LLC formations, trademark filings, and estate planning documents. This is the original LegalZoom product—the seventy-nine-dollar LLC formation. Second is subscription revenue: recurring payments for services like registered agent, compliance monitoring, annual report filing, and business advisory plans. Third, and smallest, is partnership and referral revenue: fees earned from connecting customers with attorneys, tax professionals, and other service providers.

The transactional business is straightforward but structurally challenged. Gross margins are high because the marginal cost of producing an additional legal document is near zero once the template and questionnaire system has been built. But customer acquisition costs eat into those margins significantly. Each new formation customer must be acquired through paid search, SEO content, television advertising, or partnerships—and the cost of acquiring that customer has been rising steadily as competition for search keywords intensifies and digital advertising costs inflate across the ecosystem.

The subscription business is where management has been placing its bets. Subscription revenue grew to $492.5 million in fiscal 2025, representing roughly sixty-five percent of total revenue. The value proposition is tangible: small businesses have ongoing compliance obligations—registered agent requirements, annual report filings, franchise tax deadlines—and LegalZoom bundles these into a monthly or annual subscription. The churn dynamics are the critical variable. If customers stay for multiple years, the lifetime value of a subscriber can be quite attractive relative to the acquisition cost. If they churn after one year—which many do, particularly if they formed a business that failed or never got off the ground—the economics are much less compelling.

LegalZoom does not disclose detailed cohort-level retention data, which makes it difficult for outside investors to precisely model customer lifetime value. This is a significant analytical limitation. Without knowing how many customers churn after one year versus three years versus five years, and without knowing the revenue per subscriber at each tenure level, the range of reasonable lifetime value estimates is wide. The company has disclosed that it had approximately two million subscription units as of mid-2025, growing fourteen percent annually. The growth rate is encouraging, but the absolute number of net additions—roughly a hundred thousand per year—suggests that gross additions are significantly offset by churn. In other words, a lot of customers are coming in the front door, but a meaningful number are also leaving through the back door. The net growth figure obscures what may be a very active—and expensive—subscriber replacement cycle.

The marketing efficiency question is perhaps the most important variable for long-term investors. LegalZoom spends heavily on search engine marketing, where it bids on keywords like "LLC formation" and "register a business." In the paid search world, these are competitive keywords—dozens of companies bid on the same terms, driving up the cost per click and requiring constant optimization to maintain profitable acquisition economics. The company also maintains a significant SEO footprint, with educational content ranking for thousands of legal and business-related search terms. Television advertising, once a dominant channel, has been scaled back under the current management's focus on ROI-driven spending.

The shift toward digital and subscription-focused marketing has improved efficiency, but customer acquisition costs remain a significant line item. Here is the fundamental challenge: unlike a SaaS product where the customer's data lives in the platform (creating switching costs), or a marketplace where network effects lower acquisition costs over time, LegalZoom must essentially re-earn each customer's business. The marketing spend is not building a flywheel—it is running on a treadmill.

Gross margins are healthy—in the neighborhood of sixty-five to seventy percent—reflecting the high-margin nature of both document preparation and software-delivered subscription services. But operating margins have historically been compressed by the combination of marketing spend, technology investment, and the operational costs of managing compliance across fifty states. The fiscal 2025 adjusted EBITDA margin of twenty-three percent represented meaningful improvement, and the company's record free cash flow of $147.9 million showed that the business can generate real cash when marketing spend is disciplined.

The cross-sell opportunity remains the central strategic question. LegalZoom touches a small business at its moment of creation—the LLC formation is the first interaction. In theory, the company should be able to sell that customer a bundle of ongoing services: compliance, tax preparation, legal plans, insurance, banking referrals, and more. In practice, the cross-sell conversion rates have been lower than management (and investors) hoped. Many customers form their LLC and never return. Those who do subscribe often choose the most basic compliance package and resist upselling into higher-value plans.

Technology investment has been a growing priority. The AI partnerships with Anthropic and OpenAI are the most visible recent initiatives, but the company has also been investing in its core platform—improving the customer experience, streamlining document assembly workflows, and building tools that help subscribers manage their compliance obligations more efficiently. The question is whether these investments will create genuine competitive differentiation or simply maintain parity with a field of well-funded competitors.

With all of this complexity, investors need a simple framework for tracking whether LegalZoom's strategy is working. The two KPIs that matter most are subscription unit growth rate and free cash flow conversion. Subscription units reveal whether the company is successfully shifting from episodic transactional revenue to recurring relationships—the foundation of its entire strategic pivot. Free cash flow conversion tells you whether the profitability improvements are real or merely accounting artifacts of adjusted metrics. If subscription growth stays in the low-to-mid teens and free cash flow continues expanding, the business thesis works. If either falters, the story gets much harder to believe.

XI. Porter's Five Forces

Every business operates within a competitive structure, and LegalZoom's structure is, to put it bluntly, unforgiving.

A Porter's Five Forces analysis reveals why this is a company that has struggled to translate market leadership into pricing power and durable returns.

The threat of new entrants is high. Building a basic document preparation platform requires modest technology investment—the core product is a questionnaire engine and a template library, not a Mars rover. Any well-funded startup can build a functional LLC formation tool in a matter of months. The barriers that do exist—brand recognition, SEO authority, regulatory expertise across fifty states—are meaningful but not insurmountable. ZenBusiness, Northwest, and Bizee all entered after LegalZoom and built credible competitive positions relatively quickly. And the ultimate low-cost competitor—state government websites that allow direct filing for nothing more than the filing fee—keeps getting better.

Supplier power is low, which is one of the few structural advantages in LegalZoom's favor. The company's primary inputs are technology infrastructure (commoditized and available from multiple cloud providers), a network of independent attorneys (fragmented and plentiful), and labor for customer service and operations (available at market rates). No single supplier has meaningful leverage over the business.

Buyer power is high. LegalZoom's customers are predominantly small business owners and entrepreneurs—a population that is inherently price-sensitive, comparison-shops aggressively online, and faces minimal switching costs. Moving from LegalZoom to a competitor for your next legal document requires nothing more than typing a different URL. The one mitigating factor is trust: legal services involve a degree of emotional stakes that makes some customers willing to pay a modest premium for a brand they recognize and trust. But "modest premium" is the operative phrase—LegalZoom cannot charge dramatically more than alternatives without losing customers.

The threat of substitutes is very high and growing. Customers can file directly with state agencies, often for free. They can hire a local attorney for personal attention. Accountants and banks increasingly offer formation services as loss leaders to acquire financial services customers. And now, AI-powered tools—from ChatGPT to specialized legal AI startups—can generate legal documents with startling speed and quality. Each of these substitutes addresses a different segment of the market, but collectively they ensure that LegalZoom faces competitive pressure from every direction.

Competitive rivalry is intense and getting more so. The online legal services market is fragmented, with no player commanding more than low-double-digit market share. Price competition is fierce, particularly at the entry level where free or near-free formation services are used as customer acquisition tools. Bizee's free LLC formation offer, for example, positions formation itself as a loss leader for selling registered agent services and compliance packages—a pricing strategy that puts direct pressure on LegalZoom's transactional revenue.

Differentiation is difficult because the core product—a correctly filed state form—is fundamentally the same regardless of which platform generates it. An LLC formed through LegalZoom is legally identical to one formed through ZenBusiness, Northwest, or the state's own website. The result is a marketing arms race that consumes a disproportionate share of revenue and puts constant pressure on operating margins. Companies compete on speed of processing, customer service quality, and bundle pricing rather than on any inherent product superiority.

The overall picture is a company operating in a structurally difficult industry where the forces of competition consistently work against pricing power, margin expansion, and durable returns on invested capital.

For investors familiar with Michael Porter's work, this configuration—high threat of substitutes, high buyer power, high rivalry, high entry threat—is the recipe for an industry where even the best operators struggle to earn returns above their cost of capital. The only structural positive—low supplier power—is necessary but not sufficient to build a great business.

The critical implication is that LegalZoom needs to find ways to change the competitive dynamics, not merely to operate more efficiently within them. Efficiency improvements can boost margins temporarily, but they do not alter the fundamental forces that constrain pricing power and invite competition. The AI partnerships and subscription pivot are attempts to reshape the playing field, but whether they succeed depends on execution more than strategy.

XII. Hamilton's Seven Powers

If Porter's Five Forces describe the industry structure, Hamilton Helmer's Seven Powers framework asks a more pointed question: Does LegalZoom have any source of durable competitive advantage—any "power" that can sustain returns above the cost of capital over the long term?

Scale economies are weak. In most technology businesses, scale creates a virtuous cycle: as you grow, your per-unit costs fall, allowing you to invest more in product and customer acquisition, which drives further growth. LegalZoom benefits from scale in its technology costs—the platform serves two million subscribers without proportionally increasing engineering headcount. But the most important cost—customer acquisition—does not improve meaningfully with scale. The company still has to bid for the same search keywords, still has to run advertisements, still has to compete for every marginal customer. There is operational leverage in compliance services, but it has not been enough to drive the kind of margin expansion that scale-advantaged businesses typically deliver.

Network effects are minimal. This is perhaps the most damning assessment in the framework. In the best technology businesses—marketplaces, social networks, communication platforms—each new user makes the product more valuable for all other users. LegalZoom has none of this dynamic. A customer forming an LLC gains nothing from the fact that millions of other customers have also used the platform. The attorney network is a two-sided marketplace in theory, but it lacks the liquidity and matching efficiency that create real network effects. There is no viral growth, no user-generated content flywheel, no data advantage that compounds with scale.

Counter-positioning was once LegalZoom's most powerful advantage, and it has eroded significantly. When the company launched, traditional law firms could not replicate its model without cannibalizing their own billable-hour revenue. Offering automated document preparation at seventy-nine dollars would have meant admitting that the work lawyers were charging a thousand dollars for was not actually worth a thousand dollars. This asymmetry gave LegalZoom a window of protection. But two decades later, the counter-positioning advantage has faded. Lawyers have adapted—many now use their own document automation tools, offer flat-fee services, or partner with legal technology platforms. And non-traditional competitors (fintech companies, accounting firms, banks) entered the market without the same cannibalization concern.

Switching costs are low to moderate. For transactional services—LLC formations, trademark filings—switching costs are effectively zero. A customer can use LegalZoom for their first LLC and Bizee for their second without any friction. Subscription services create some switching costs: transferring a registered agent, migrating compliance records, and setting up new monitoring services all involve hassle that many customers would prefer to avoid. But these are convenience costs, not structural lock-in, and they can be overcome by a competitor willing to offer a smoother migration process or a lower price.

Brand power is moderate—meaningful but insufficient to drive pricing power. LegalZoom is the most recognized name in online legal services, and brand matters in a category where customers are entrusting sensitive business and personal information to a platform. Trust is a genuine differentiator, particularly for first-time entrepreneurs who are unfamiliar with the formation process. But brand awareness has not translated into the kind of pricing premium that brands like Apple or Nike command. LegalZoom's prices are competitive with, not materially above, its main rivals.

Cornered resources are weak. The company does not possess proprietary technology, exclusive data sets, or irreplaceable talent that competitors cannot access. Its attorney network is not exclusive—the same attorneys work with multiple platforms. The closest thing to a cornered resource is the company's SEO authority—decades of content investment have built a domain authority that would be expensive and time-consuming for a new entrant to replicate. But SEO authority is not permanent; algorithm changes, competitor investment, and shifting user behavior can erode it over time.

Process power is moderate. LegalZoom has accumulated deep expertise in navigating the regulatory complexity of fifty different state legal systems, and its document assembly workflows have been refined over two decades of operation. This institutional knowledge is real and creates some competitive advantage—a new entrant would need years to build equivalent regulatory expertise. The company knows which states require operating agreements to be filed, which require annual reports by specific dates, how to handle name availability searches, and how to structure its services to comply with UPL regulations in every jurisdiction.

But process power is replicable by well-funded competitors willing to invest the time, and it does not prevent disruption by technologies (like AI) that may make regulatory navigation fundamentally easier. If AI can parse and interpret state-specific legal requirements in real time, the value of two decades of accumulated human expertise diminishes considerably.

The overall assessment is sobering: LegalZoom has weak structural power. The business relies primarily on brand recognition and operational execution rather than durable competitive advantages. The absence of meaningful network effects, low switching costs, and erosion of counter-positioning create a business that must continuously earn its customers rather than capturing them in a defensible ecosystem.

Compare this to businesses that score well on the Seven Powers framework. Intuit's TurboTax, for instance, benefits from strong switching costs (customers store years of tax data and return annually), brand power that drives pricing premium, and scale economies in product development. Netflix benefited from early counter-positioning against Blockbuster and built scale economies that funded content investment. LegalZoom has none of these dynamics in sufficient strength. This does not mean the business cannot be profitable—it clearly can, as fiscal 2025 demonstrated—but it does mean that the profitability is fragile and must be defended through continuous operational excellence rather than structural advantage. That distinction matters enormously for long-term investors, because operational excellence can erode with management changes, competitive shifts, or technological disruption in ways that structural advantages typically do not.

XIII. Bear Case vs. Bull Case

The investment debate around LegalZoom at its current valuation comes down to a fundamental disagreement about the nature of the business: Is this a structurally challenged company in a commoditizing market, or an undervalued franchise with improving economics and optionality on AI?

The bear case begins with industry structure.

As the Porter's and Seven Powers analyses suggest, LegalZoom operates in a market with high competitive intensity, low switching costs, and minimal network effects. The core product—legal document preparation—is being commoditized from multiple directions: free state government websites, low-cost competitors like Bizee and ZenBusiness, and increasingly capable AI tools that can generate legal documents in seconds. The bear asks: What is LegalZoom's moat? If the answer is "brand," the follow-up is: When has brand alone been sufficient to sustain above-market returns in a commodity industry?

AI is the bear's most potent weapon. If generalist AI tools like ChatGPT and Claude can generate LLC operating agreements, trademark applications, and basic wills with high accuracy and minimal cost, then the entire foundation of LegalZoom's business—automated document preparation at a fraction of what lawyers charge—is threatened by tools that are even cheaper and more automated. The company's AI partnerships may provide some defense, but they also raise a troubling question: Why would a customer use LegalZoom's ChatGPT integration to form an LLC when they could use ChatGPT directly?

The bear also points to customer acquisition economics that remain structurally challenged. Despite the pivot to subscription-focused marketing, LegalZoom still spends heavily to acquire each new customer, and the competitive dynamics of paid search ensure that this cost is unlikely to decline materially. Growth has been moderate—eleven percent in fiscal 2025, but from a base that was itself depressed by normalization of pandemic-era formation volumes.

Management credibility, while improving under Stibel, is still being rebuilt. The abrupt CEO transition in July 2024—announced without warning and accompanied by a guidance cut—damaged institutional investor confidence. The securities class-action investigation, while not unusual for companies with sharp stock declines, adds a layer of legal risk and governance concern. And the company's analyst coverage tells its own story: as of early March 2026, Barclays had downgraded the stock to Underweight, UBS maintained a Neutral rating, and the consensus price target—while above the current stock price—reflects limited conviction in a near-term re-rating.

The bull case starts with a simple observation: the market may have overcorrected.

At a market capitalization of roughly $1.2 billion, LegalZoom trades at approximately eight times its fiscal 2025 free cash flow of $148 million—a multiple that implies the market expects the business to shrink or that the cash flows are unsustainable. The bull argues that neither is the case: subscription revenue is growing at thirteen percent, the subscriber base is expanding, and the company has zero debt and over two hundred million dollars in cash. The balance sheet provides a margin of safety, and the shareholder return program (including the expanded buyback authorization) suggests management confidence in the sustainability of cash flows.

On the competitive front, the bull notes that LegalZoom has actually been gaining market share. The Formation Nation acquisition in February 2025 added two complementary brands—a low-cost option (Inc Authority) and a premium consultative option (NCH)—giving LegalZoom a multi-brand strategy similar to what hotel chains and auto companies use to cover different market segments without diluting the flagship brand. The company estimates its market share at approximately nine percent of a fifty-one billion dollar serviceable addressable market, which means even modest share gains represent meaningful revenue growth in absolute terms.