Live Nation Entertainment (LYV): The Evolution of Live Entertainment's Most Controversial Empire

I. Introduction & Episode Roadmap

The house lights dim at Madison Square Garden. Twenty thousand phones illuminate the darkness like digital fireflies. On stage, a lone spotlight reveals not a rockstar, but Michael Rapino—the CEO who built the most powerful empire in live entertainment history. He's about to announce yet another record-breaking quarter for Live Nation Entertainment, a company that in 2024 generated $23 billion in revenue and controlled virtually every aspect of how fans experience live music. From the moment you search for concert tickets to the beer you buy at intermission, chances are Live Nation touches the transaction.

But here's the paradox: Live Nation might be simultaneously the most successful and most reviled company in entertainment. Artists complain about its power. Fans rage against Ticketmaster's fees. Politicians from both parties want to break it up. And yet, the machine keeps growing—151 million fans attended over 50,000 Live Nation events in 2024 alone, with attendance up 4% year-over-year. The story we're about to unpack is one of relentless consolidation, regulatory chess matches, and a fundamental bet that humans will always crave shared experiences. It's the tale of how a spin-off from a radio conglomerate transformed into a record $2.15 billion in adjusted operating income (AOI) in 2024, up 14%, on record revenue of $23.16 billion. The world's leading live entertainment company operates through three interlocking segments: Ticketmaster, Live Nation Concerts, and Live Nation Sponsorship—each reinforcing the others in a flywheel that critics call monopolistic and defenders call efficient.

The central question isn't whether Live Nation is powerful—it undeniably is. The question is whether that power serves or strangles the live entertainment ecosystem. As we trace the company's evolution from Clear Channel's unwanted stepchild to Attorney General Merrick Garland's public enemy number one, we'll discover how concert promotion evolved from a handshake business run by local hustlers into a data-driven, globally integrated machine that touches nearly every major live event on the planet.

Our roadmap takes us from the dusty parking lots of 1970s amphitheaters through corporate boardrooms, antitrust courtrooms, and the chaos of Taylor Swift's Eras Tour presale. Along the way, we'll decode the economics of why your concert ticket costs $300, why artists simultaneously love and loathe Live Nation, and whether the government's attempt to break up the company might actually make things worse for fans. This is the Acquired-style deep dive into Live Nation Entertainment—buckle up.

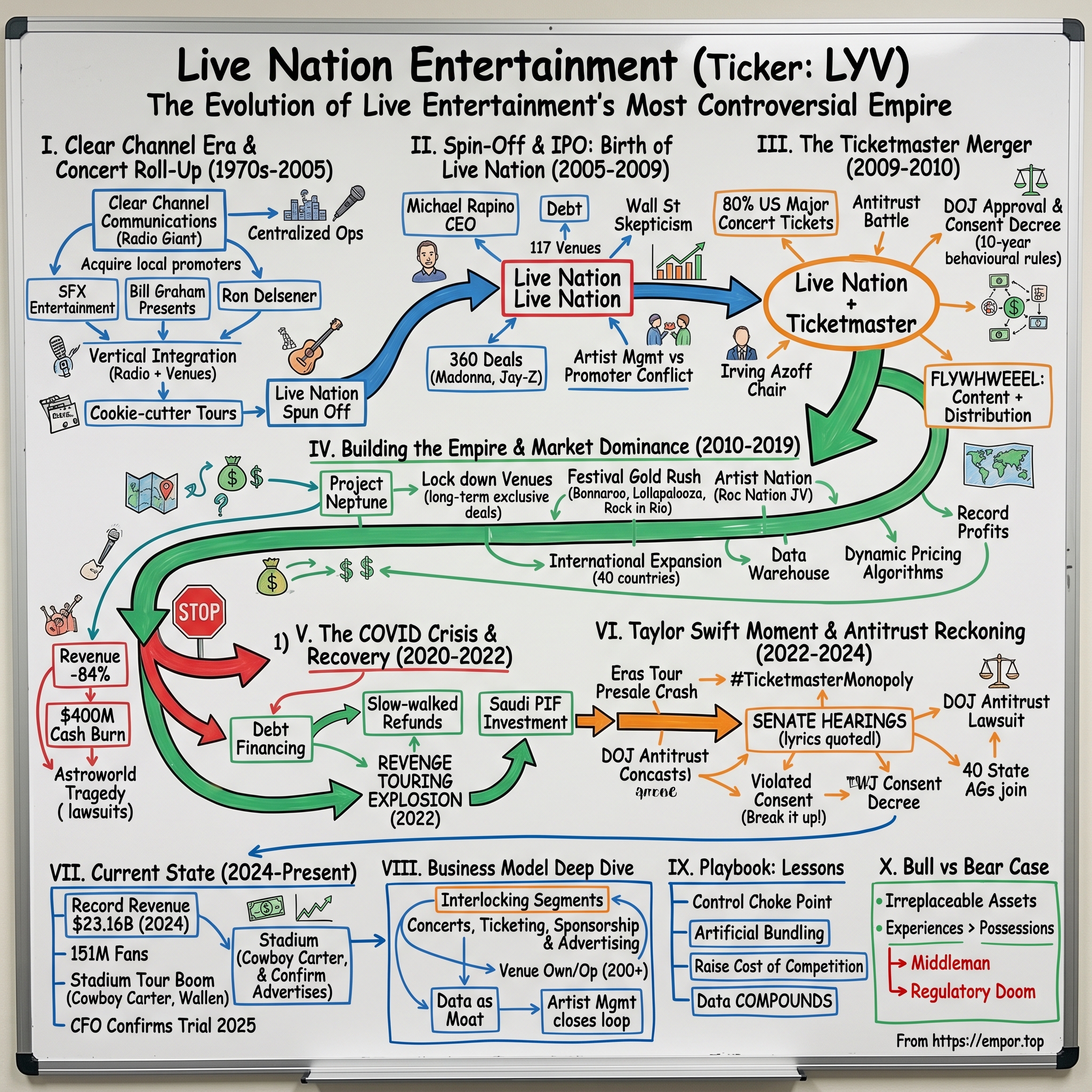

II. Origins: The Clear Channel Era & Concert Roll-Up Strategy (1970s–2005)

Picture the concert business in 1975: a patchwork quilt of local fiefdoms. In San Francisco, Bill Graham ruled the Fillmore. In New York, Ron Delsener controlled Central Park. In Chicago, Jam Productions had a lock on the best venues. These promoters were part businessman, part therapist, part mobster—they knew which bands drank what whiskey, which road managers could be trusted with cash advances, and which local radio DJs could turn a Tuesday night club show into a sold-out event. It was a relationship business, built on favors, handshakes, and the occasional fistfight.

Into this cozy chaos came Clear Channel Communications, a San Antonio-based radio company that by the late 1990s had become the Pac-Man of American media. Led by the Mays family—Lowry and his sons Mark and Randall—Clear Channel had gobbled up over 1,200 radio stations following the Telecommunications Act of 1996's deregulation. But owning the airwaves wasn't enough. The Mays family saw an opportunity: if you controlled both the radio stations that broke hits and the concert venues where those hits came alive, you'd have unprecedented leverage over the entire music industry.

The vehicle for this vision was SFX Entertainment, founded by media entrepreneur Robert F.X. Sillerman—a man who collected concert promoters like baseball cards. Starting in 1996, Sillerman went on a buying spree that would make private equity blush. He acquired Delsener/Slater Enterprises in New York, Bill Graham Presents in San Francisco, Concert/Southern Promotions, Sunshine Promoters in Indiana, and dozens more. By 1998, SFX controlled 120 venues and promoted events that sold 48 million tickets annually. When Sillerman needed a bigger checkbook, he found one: Clear Channel acquired SFX for $4.4 billion in 2000.

The timing seemed perfect. The late '90s concert business was booming—'N Sync and Backstreet Boys were selling out stadiums, ticket prices were rising faster than inflation, and new amphitheaters were sprouting up in every suburban market. Clear Channel's strategy was elegantly brutal: use radio dominance to break artists, funnel them into Clear Channel venues, and capture every dollar from parking to beer sales. They called it "vertical integration"; competitors called it something unprintable.

But the roll-up strategy had a fatal flaw that wouldn't become apparent until later. Concert promotion, unlike radio, is inherently local and relationship-driven. The best promoters weren't just businesspeople—they were cultural translators who understood that what worked in Denver wouldn't work in Detroit. When Clear Channel centralized operations and pushed out veteran promoters in favor of corporate efficiency, they lost decades of institutional knowledge. Artists started complaining about cookie-cutter tours, venues felt generic, and fans noticed the difference.

By 2004, the concert division—now rebranded Live Nation—was generating significant revenue but also significant headaches. The business was capital-intensive, cyclical, and dependent on the whims of artists who increasingly resented Clear Channel's dominance. Radio was under assault from iPods and satellite; the concert business looked increasingly like a distraction from Clear Channel's core challenges. Meanwhile, a young executive named Michael Rapino was making waves running the company's European concert operations, proving that the live business could thrive with the right leadership.

The Mays family faced a choice: double down on live entertainment or cut it loose. In a boardroom in San Antonio, surrounded by spreadsheets showing the capital requirements of venue construction versus the steady cash flows of radio advertising, they made the decision that would reshape the entertainment industry. Live Nation would be spun off, forced to sink or swim on its own. The orphaned company would need new leadership, new strategy, and most importantly, a new partner to compete in the increasingly complex world of live entertainment. That partner, though no one knew it yet, would be their greatest rival: Ticketmaster.

III. The Spin-Off & IPO: Birth of Live Nation (2005–2009)

Michael Rapino's corner office in Beverly Hills didn't have much of a view in December 2005, but that didn't matter—he wasn't looking backward. At 40, the Canadian-born executive had just become CEO of the newly independent Live Nation Entertainment, a company born from necessity rather than strategy. The spin-off from Clear Channel, completed just days earlier, felt less like a triumphant launch and more like being pushed out of a plane with a parachute that might not open.

The numbers told a stark story: Live Nation began its independent life with $1.7 billion in debt, ownership or operation of 117 venues, and relationships with artists who had grown increasingly wary of the Clear Channel machine. The company went public on December 21, 2005, at $12 per share, raising $400 million—money that would barely cover the interest payments, let alone fund the aggressive expansion Rapino envisioned. Wall Street was skeptical. "It's a terrible business model," one analyst told the Financial Times. "High capital requirements, cyclical revenue, and you're at the mercy of prima donna artists."

But Rapino saw something different. Growing up in Thunder Bay, Ontario, promoting beer-soaked bar shows before climbing the ranks at Labatt Breweries, he understood that live music wasn't just a business—it was a drug. And in an increasingly digital world, that drug was becoming more potent. "When everything else can be copied, downloaded, or streamed," he told his management team in early 2006, "being in the same room with your favorite artist becomes priceless."

His strategy was counterintuitive: instead of retreating to core markets, Live Nation would expand globally. Instead of treating artists as suppliers, they'd become partners. And instead of competing with venues, they'd build new ones designed for the modern concert experience. The centerpiece was "360 deals"—comprehensive partnerships where Live Nation would handle not just touring, but merchandise, recording, and even sponsorships. Madonna became the proof of concept in 2007, signing a groundbreaking $120 million deal that gave Live Nation a share of virtually everything except her morning coffee.

The artist management community went ballistic. Irving Azoff, the legendary manager who ran Ticketmaster's parent company, called the Madonna deal "desperate and stupid." But then Jay-Z signed. Then U2. Then Shakira. Suddenly, Live Nation wasn't just a concert promoter—it was becoming a full-service artist development company. The traditional music industry power structure, already weakened by piracy and iTunes, was crumbling.

Competition intensified from every angle. AEG, backed by billionaire Philip Anschutz, was building spectacular venues like the O2 in London and aggressively pursuing exclusive venue deals. Regional promoters formed alliances to resist Live Nation's expansion. And looming over everything was Ticketmaster, the 800-pound gorilla of ticket distribution that could make or break any promoter's business with its control over primary ticketing.

The relationship with Ticketmaster was particularly toxic. The companies needed each other—Live Nation needed distribution, Ticketmaster needed inventory—but they also despised each other. Ticketmaster extracted massive fees from Live Nation shows while simultaneously working with competitors. Live Nation retaliated by trying to build its own ticketing platform, burning through $100 million on technology that barely functioned. Industry insiders called it the "Cold War of Concert Promotion."

By late 2008, both companies were struggling. The financial crisis had decimated discretionary spending, and tour after tour was being canceled or downsized. Live Nation's stock had fallen below $4, down 75% from its IPO price. Ticketmaster was faring no better, with declining market share and restless shareholders. In separate boardrooms in Beverly Hills and West Hollywood, two sets of executives were reaching the same conclusion: maybe the enemy of my enemy could become my friend.

The first meeting between Rapino and Azoff was held in secret at a neutral location—a nondescript hotel conference room near LAX. Both men came with armies of lawyers and bankers, but within minutes, it was just the two of them, sketching out deal terms on a napkin. The logic was inescapable: combine Live Nation's content with Ticketmaster's distribution, eliminate redundancies, and create an integrated platform that could withstand any economic storm. What they didn't anticipate was that their merger would trigger one of the most controversial antitrust battles in entertainment history, setting the stage for a decade of dominance—and a decade of backlash.

IV. The Ticketmaster Merger: Creating a Vertically Integrated Giant (2009–2010)

The war room at Simpson Thacher & Bartlett's Manhattan offices looked like mission control during a space launch. February 10, 2009, 3:47 AM. Irving Azoff, Ticketmaster's CEO and the most feared manager in music history, sat across from Michael Rapino, studying the final merger documents. Between them lay the blueprint for what would become either the greatest vertical integration play in entertainment history or, as critics would soon claim, the "merger from hell."

The deal was announced that morning: Live Nation and Ticketmaster would merge to become Live Nation Entertainment, creating a company that would control nearly every aspect of the concert experience. Ticketmaster had been the nation's leading primary ticket sales service for decades, having grown from an innovative startup in the 1970s to command more than 80 percent of all U.S. major concert ticket sales by 1995. Live Nation brought the content—the artists, venues, and promotional muscle. Together, they would form what Azoff called "the Amazon of live entertainment."

The Senate wasn't buying it. Two weeks later, at a packed hearing of the Judiciary Committee's antitrust subcommittee, the atmosphere was hostile. Senator Herb Kohl, the Wisconsin Democrat who chaired the panel, opened with a shot across the bow: "By some accounts, Ticketmaster controls 70% to 80% of all concert ticket sales". How could combining that with the nation's largest concert promoter possibly benefit consumers?

The numbers were damning. Until 2009, Ticketmaster dominated the market for primary ticketing services to major concert venues in the United States with greater than 80% market share. Live Nation had just launched its own ticketing platform in December 2008, positioning itself as Ticketmaster's first real competitor in years. Now, barely a month later, they were merging. As Kohl pointed out, Live Nation had "entered into the ticketing business to compete with Ticketmaster and lasted only one month. What does Live Nation's decision to merge with its competitor rather than fight it in the market tell us about any company's ability to compete with Ticketmaster?"

Behind the scenes, the merger negotiations had been brutal. Azoff, who managed the Eagles and Christina Aguilera, knew every pressure point in the industry. Rapino, the promoter's promoter, understood that without reliable ticketing, Live Nation was vulnerable. They structured the deal as a "merger of equals" valued at $2.5 billion, though everyone knew Ticketmaster held the cards—it controlled distribution, the chokepoint of the entire industry.

The Justice Department's Antitrust Division spent eleven months dissecting the deal. Christine Varney, the newly appointed head of the division under President Obama, faced enormous pressure from all sides. Artists like Bruce Springsteen publicly opposed the merger. Springsteen posted on his website that "the one thing that would make the current ticket situation even worse for the fan than it is now would be Ticketmaster and Live Nation coming up with a single system, thereby returning us to a near monopoly situation in music ticketing".

But the companies had a trump card: they threatened to litigate if blocked, potentially tying up the deal for years. They also made strategic concessions. The centerpiece was divesting Paciolan, Ticketmaster's self-service ticketing subsidiary, and licensing Ticketmaster's software to AEG, Live Nation's primary competitor. In theory, this would create viable competition. In practice, as internal documents would later reveal, the companies knew these remedies were cosmetic.

On January 25, 2010, the DOJ approved the merger pending certain conditions, filing a consent decree that required the merged firm to license a copy of the Ticketmaster host platform software to AEG and divest Paciolan. The companies had to agree to a ten-year consent decree with strict behavioral conditions: no retaliation against venues that chose competing ticketers, no conditioning of concerts on ticketing contracts, and regular monitoring by the DOJ.

The final structure was byzantine but brilliant. "Unlike so many other businesses, we're not here today for a bailout or a tax credit or any other favor," Rapino told Congress. "Instead we've come with our own self-funded renewal plan". Rapino would remain CEO of the combined company, while Azoff became executive chairman—though he would leave within two years, cashing out with over $100 million.

What neither the regulators nor the public fully grasped was how the merger would fundamentally alter the concert industry's power dynamics. By combining Live Nation's control of content with Ticketmaster's stranglehold on distribution, the new company wouldn't just be bigger—it would be structurally unassailable. Venues would need Live Nation's tours; artists would need Ticketmaster's platform. The flywheel would become a vortex, pulling everything into its orbit. As we'd discover over the next decade, the consent decree's behavioral remedies were like putting a Band-Aid on a severed artery.

V. Building the Empire: Expansion & Market Dominance (2010–2019)

The first Live Nation Entertainment earnings call as a merged entity, in May 2010, was a masterclass in managing expectations. Rapino, now CEO of the combined company, spoke in measured tones about "integration challenges" and "synergy realization timelines." What he didn't say—what he couldn't say—was that internally, the company was already plotting world domination. The playbook, circulated only among senior executives, was titled "Project Neptune": control the venues, own the festivals, lock in the artists, and make the platform indispensable.

The strategy unfolded in three phases, each more ambitious than the last. Phase one focused on locking down venues through long-term exclusive ticketing agreements. These weren't your grandfather's venue deals—they were financial engineering marvels. Live Nation would guarantee venues minimum annual payments regardless of ticket sales, provide interest-free loans for renovations, and even take equity stakes. The hook was buried in the fine print: ten-year exclusive ticketing agreements with automatic renewals and punitive termination clauses. By 2012, Ticketmaster had exclusive deals with 80 of the top 100 arenas in America. Phase two was the festival gold rush. Between 2013 and 2018, Live Nation went on an acquisition spree: the New Orleans Voodoo Music + Arts Experience (2013), C3 Presents in Austin, Texas (2014), Bonnaroo Music and Arts Festival in Tennessee (2015), Founders Entertainment and its Governors Ball Music Festival in New York (2016), AC Entertainment (2016), and Red Mountain Entertainment (2018). But the crown jewel came in May 2018 when Live Nation Entertainment acquired a majority stake in Brazil's Rock in Rio festival.

The genius wasn't just buying festivals—it was understanding their economics. Festivals are cash machines with 30-40% EBITDA margins compared to 10-15% for standard tours. They generate multiple revenue streams: tickets, sponsorships, VIP packages, camping, parking, merchandise, and food/beverage. More importantly, they create a captive audience for three days, not three hours. Every beer sold, every t-shirt purchased, every sponsored activation—Live Nation got a cut.

In February 2016, Live Nation acquired Canada's largest independent concert promoter, Union Events, giving them control of major Canadian festivals including X-Fest and Chasing Summer. The pattern was always the same: identify successful independent festivals, offer the founders life-changing money plus earnouts based on growth, then integrate them into the Live Nation machine while maintaining the illusion of independence.

Phase three was the most audacious: the artist partnership revolution. Building on the Madonna model, Live Nation created "Artist Nation," a full-service management and production company. Live Nation Entertainment's artist management arm, called Artist Nation, is included within its concerts division and also includes Front Line Management and Roc Nation. The Roc Nation joint venture with Jay-Z, announced in 2017, was particularly strategic—it brought hip-hop credibility and a pipeline of young, diverse talent that Live Nation had historically struggled to attract.

The international expansion was equally aggressive. By 2015, Live Nation operated in 40 countries. They didn't just export American acts; they acquired local promoters who understood regional tastes and regulatory environments. In August 2015, Live Nation announced it would form Live Nation Germany, in partnership with German promoter Marek Lieberberg, with oversight over Live Nation events in Austria and Switzerland. Each acquisition came with relationships, venues, and most importantly, data on local consumer behavior.

Technology investments, though less visible, were crucial to maintaining dominance. Live Nation spent hundreds of millions upgrading Ticketmaster's platform, developing dynamic pricing algorithms, and building a data warehouse that tracked every fan interaction. They knew which ZIP codes bought VIP packages, which demographics arrived early for merchandise, which artists could sell out a Tuesday night in Des Moines. This data advantage became a moat competitors couldn't cross.

The numbers told the story of unstoppable growth. Revenue climbed from $5.4 billion in 2011 to $11.5 billion in 2019. Stock price rose from under $10 to over $70. The company promoted over 40,000 shows annually for 5,000 artists, selling 500 million tickets through Ticketmaster. They controlled or operated 200 venues globally. The flywheel was spinning so fast it seemed nothing could stop it.

But success bred scrutiny. In April 2018, the United States Department of Justice launched an investigation following allegations by AEG that Live Nation pressured them into using Ticketmaster and intentionally avoided booking acts for AEG venues. Competitors whispered about anticompetitive practices. Artists complained about shrinking margins. Fans raged about service fees that sometimes exceeded 30% of face value. The consent decree was set to expire in 2020, and the DOJ was watching closely.

Still, as 2019 drew to a close, Rapino was bullish. The company had just announced record Q4 earnings. Taylor Swift's Lover Fest was set to be the biggest tour of 2020. Plans were underway to acquire more European festivals. The future looked limitless. Then, in a wet market in Wuhan, China, a virus jumped from animals to humans, and everything changed overnight.

VI. The COVID Crisis & Recovery: Near-Death to Record Heights (2020–2022)

March 12, 2020. Michael Rapino stood in his Beverly Hills office, watching CNBC announce the NBA season suspension. Within hours, every major tour would be postponed. Every venue would close. Every festival would be canceled. For a company that generated 95% of its revenue from gathering large crowds in confined spaces, COVID-19 wasn't just a crisis—it was an existential threat. Live Nation's stock price collapsed from $72 to $21 in ten days, erasing $8 billion in market value.

The numbers were apocalyptic. In 2020, Live Nation was hit particularly hard by the COVID-19 pandemic, with essentially all concerts and sporting events around the world on hold. On February 25, 2021, Live Nation released its full-year 2020 financial results, of which the company saw revenues fall by 84%. Second quarter 2020 revenue fell 98% year-over-year to $74 million. The company burned through $400 million in cash monthly with essentially zero revenue coming in.

But in crisis, Rapino saw opportunity. While competitors laid off thousands, Live Nation made a calculated bet: the hunger for live experiences would return stronger than ever. They raised $1.2 billion in debt financing in May 2020, securing liquidity through 2022. They renegotiated vendor contracts, furloughed 20% of staff while protecting core talent, and most controversially, held onto customer cash by slow-walking refunds—a decision that sparked lawsuits but preserved critical working capital.

In April 2020, it was disclosed that Saudi Arabia's Public Investment Fund (PIF) recently acquired a 5.7% stake in Live Nation, as of April 28, 2020, the investment was valued at just shy of $500 million. The Saudi investment was controversial but strategic—it provided capital when markets were frozen and opened doors to the Middle Eastern entertainment market that was beginning to liberalize under Vision 2030.

The company also used the downtime to accelerate technology investments that had been on the back burner. They rebuilt Ticketmaster's mobile app, implemented contactless entry systems, and developed "Ticketmaster Fan Guarantee" programs. They renegotiated venue leases, securing better terms from desperate landlords. Most importantly, they locked in artist deals for 2021-2023 at favorable terms, betting that performers would be desperate for guaranteed income after a year without touring.

By summer 2021, the bet was paying off spectacularly. Vaccination rates climbed, venues reopened, and two years of pent-up demand exploded. Lollapalooza 2021 sold out in record time at premium prices. The Rolling Stones' No Filter Tour grossed $115 million from just 12 shows. Fans who had saved money during lockdowns were willing to pay any price for the return of live experiences. Average ticket prices increased 25% from 2019 levels, and nobody complained.

The revenge touring phenomenon of 2022 exceeded even Rapino's optimistic projections. Artists who had lost two years of touring income flooded the market. Harry Styles, Bad Bunny, and Elton John's farewell tour all shattered attendance and revenue records. Festival ticket prices doubled from pre-pandemic levels. VIP packages that cost $500 in 2019 now sold for $1,500. The company generated $16.7 billion in revenue in 2022, approaching pre-pandemic levels despite fewer shows.

But the rapid return also exposed systemic weaknesses. In November 2021, a crowd crushing incident occurred at Astroworld Festival—a Live Nation-promoted concert in Houston organized and headlined by rapper Travis Scott—which resulted in 10 fatalities and nearly 5,000 injuries. Live Nation, Scott, and other parties involved have been named in over 387 lawsuits related to the incident. In December 2021, the United States Congress House Oversight Committee announced a bipartisan investigation into Live Nation's role in the incident.

The Astroworld tragedy raised fundamental questions about Live Nation's growth-at-all-costs mentality. Internal emails released during litigation showed pressure to maximize attendance, inadequate security planning, and ignored warnings from safety consultants. The company's response—blaming local authorities and securit

y contractors—only intensified public anger. For the first time, the human cost of Live Nation's dominance was impossible to ignore.

Yet financially, the company emerged from COVID stronger than ever. Weaker competitors had failed or sold out. Artists were more dependent on touring income as streaming revenues disappointed. Fans had proven they would pay almost any price for live experiences. The stage was set for 2023 to be the biggest year in concert history. But one artist and her army of fans were about to expose every crack in Live Nation's armor, triggering a political firestorm that would reach the highest levels of government.

VII. The Taylor Swift Moment & Antitrust Reckoning (2022–2024)

November 15, 2022, 10:00 AM EST. Fourteen million Taylor Swift fans—self-identified "Swifties"—simultaneously logged onto Ticketmaster to purchase presale tickets for the Eras Tour. Within minutes, the site crashed. Error messages proliferated. Fans who had waited hours in virtual queues were kicked out and forced to start over. What should have been a celebration of Swift's first tour in five years became a digital nightmare that would fundamentally alter Live Nation's relationship with the public, politicians, and ultimately, the justice system.

The numbers were staggering: 3.5 billion total system requests, 4 times the previous record. Over 2 million tickets sold in a single day, generating more traffic than the Super Bowl, Olympics, and World Cup combined. But the technical failure was just the beginning. When tickets appeared on secondary markets minutes later at 10-50 times face value, fans erupted. The pre-sale was supposed to be exclusive to verified fans, yet somehow professional scalpers had acquired thousands of tickets.

Swift herself broke her characteristic silence on business matters with a devastating Instagram post: "It's really difficult for me to trust an outside entity with these relationships and loyalties, and excruciating for me to just watch mistakes happen with no recourse." The key word was "monopoly"—she didn't use it, but everyone understood the implication. When the world's biggest pop star essentially calls you a monopolist, Washington listens.

Following the Taylor Swift–Ticketmaster controversy in 2022, congressional lawmakers urged antitrust action against Ticketmaster. The Senate held hearings in January 2023 titled "That's The Ticket: Promoting Competition in the Ticketing Industry." The optics were brutal: senators from both parties grilled Live Nation executives while quoting Taylor Swift lyrics. "You have a 100% monopoly on Taylor Swift tickets," Senator Mike Lee thundered. "She has no choice but to use Ticketmaster. Neither do her fans."

Live Nation's defense was technical and tone-deaf. They blamed bot attacks, overwhelming demand, and even Taylor Swift herself for not doing enough shows. They produced charts showing that service fees had decreased as a percentage of ticket price (while failing to mention that face values had skyrocketed). They pointed to competitors like AXS and SeatGeek as evidence of a competitive market (without acknowledging their minuscule market shares).

But the damage was done. In November 2022, it was reported that the DOJ was conducting an antitrust probe into Ticketmaster's compliance with the 2019 agreement. Politico reported in July 2023 that the DOJ's probe into Ticketmaster had progressed, and that a formal antitrust lawsuit against Live Nation was possible. The investigation revealed a pattern of behavior that went far beyond technical glitches.

Internal documents subpoenaed by the DOJ showed Live Nation executives discussing "defense strategies" against competitors, including threatened venue boycotts and exclusive dealing arrangements that would make it "economic suicide" for venues to work with rival ticketers. One particularly damaging email from a senior executive stated: "We have the content (artists) and the distribution (Ticketmaster). We can make life very difficult for anyone who doesn't play ball."

On May 23, 2024, the Department of Justice formally announced its antitrust lawsuit against Live Nation Entertainment, accusing the company of illegally monopolizing the live event market. During a news conference, Attorney General Merrick Garland stated "It is time to break it up" in reference to the company. The complaint alleged that Live Nation had systematically violated the 2010 consent decree, using its dominance in promotion to force venues into exclusive Ticketmaster contracts and retaliating against those who resisted.

The Justice Department, along with 30 state and district attorneys general, filed a civil antitrust lawsuit against Live Nation-Ticketmaster for monopolization and other unlawful conduct that thwarts competition in markets across the live entertainment industry. The lawsuit, which includes a request for structural relief, seeks to restore competition in the live concert industry.

The government's case was built on three pillars. First, Live Nation locks venues into long-term contracts with Ticketmaster to keep out competitors. This means Ticketmaster does not have to innovate, improve its services or offer competitive pricing in order to compete with other companies. Even if a rival ticketer were to offer a better price, a better product, or simply a better ticketing experience, a Ticketmaster-exclusive venue would not be able to choose the rival for a long time, often a decade.

Second, the company allegedly engaged in retaliation against venues that considered alternative ticketing providers. The DOJ presented evidence of Live Nation threatening to withhold major tours from venues that didn't use Ticketmaster, effectively wielding artists as weapons against competition. Third, the merger had stifled innovation—Ticketmaster's technology remained largely unchanged since 2010, with the company focusing on extracting higher fees rather than improving user experience.

Live Nation's legal response, filed in August 2024, was a mixture of denial and deflection. They argued that the concert industry was more competitive than ever, pointing to new entrants like Dice and the growth of direct-to-fan platforms. They claimed that high ticket prices were driven by artist demands, not monopoly power. Most audaciously, they suggested that breaking up the company would harm consumers by eliminating efficiencies and raising costs.

On August 19, 2024, ten additional state attorneys-general joined the lawsuit, bringing the total number of co-plaintiffs to 40. Additionally, on May 24, 2024, a day after the DOJ case was filed, a consumer case seeking $5 billion in damages from Live Nation Entertainment on potentially millions of individuals who purchased tickets through Ticketmaster was filed.

The political dynamics had shifted dramatically from 2010. A poll conducted by Global Strategy Group in 2023 found that 60% of Americans would support efforts to break up Live Nation's Ticketmaster. The company had become a rare point of bipartisan agreement—Republicans saw it as a monopolist crushing small businesses, Democrats as a corporate behemoth exploiting consumers and artists. Even the music industry, traditionally reluctant to bite the hand that feeds it, was increasingly vocal in its criticism.

As 2024 progressed, Live Nation found itself fighting a multi-front war. The antitrust trial was scheduled for 2025. Congressional investigations continued. Artists were increasingly experimenting with alternative ticketing and distribution methods. Even its stock price, which had recovered to record highs, was volatile as investors weighed the breakup risk. The empire that Rapino had spent fifteen years building was under assault from all sides, yet somehow, the show went on—and the money kept rolling in.

VIII. The Business Model Deep Dive: How Live Nation Makes Money

To understand Live Nation's power, follow the money through a single concert. When Beyoncé announces a stadium show, a complex financial machine springs into action, with Live Nation extracting value at every step. The company operates through Concerts, Ticketing, and Sponsorship & Advertising segments, each interlocked in a way that would make John D. Rockefeller jealous.

Start with concert promotion, the company's largest segment. The company's concert segment brought in $19 billion of that revenue, up 2 percent from the prior year in 2024. The economics are counterintuitive: Live Nation often loses money on the actual show. For a superstar like Beyoncé, they might guarantee $2 million per night against 85% of gross revenues, meaning she gets whichever is higher. With production costs, venue rental, marketing, and staffing, Live Nation might net just $100,000 on $3 million in ticket sales—a 3% margin.

So why do it? Because the concert is just the entry point to a revenue ecosystem. Live Nation owns or operates the venue, earning income from parking ($30 per car, 10,000 cars = $300,000), concessions (40% margin on $15 beers), merchandise (25% of gross sales), and premium experiences (VIP packages at $2,000 each). A single stadium show can generate $2 million in ancillary revenue with 50%+ margins. Multiply that by 50,000 shows annually, and you understand why A heavy slate of concerts at arenas and amphitheaters, where Live Nation can offer VIP experiences and capture more revenue from food and beverage sales, helped AOI climb 65% to $529.7 million and AOI margin reach a record 2.8%.

The ticketing segment is the cash cow everyone loves to hate. Ticketmaster reported revenue of $841 million, up 14 percent year-on-year, for full year revenue of $3 billion in 2024. The genius of Ticketmaster isn't the technology—it's the business model. They charge fees to both sides of the transaction: venues pay for the platform, consumers pay service fees, and artists get a cut of the fees as a kickback disguised as "marketing support."

The fee structure is deliberately opaque. A $100 ticket might carry a $15 service fee, $5 facility charge, $3.50 processing fee, and $2.50 delivery fee—even for digital tickets. But here's the dirty secret: those fees are negotiated with and partially returned to venues and artists. The "$15 service fee" might see $7 go back to the venue, $3 to the artist, and $5 to Ticketmaster. The fees are a profit-sharing mechanism disguised as a necessary evil, allowing artists to advertise lower face values while capturing higher total revenue.

Dynamic pricing, introduced in 2022, took this model to new extremes. Using algorithms that adjust prices based on demand, location, purchase history, and dozens of other factors, Ticketmaster can extract maximum value from each buyer. Those Springsteen tickets that started at $99? They peaked at $5,000 during high-demand periods. The system is so sophisticated it can identify which ZIP codes will pay premium prices and adjust accordingly.

Sponsorship & Advertising segments represents the highest-margin business, generating $1.1 billion in revenue with 65%+ EBITDA margins. Every surface at a Live Nation venue is for sale: naming rights, pouring rights, stage backdrops, wristbands, even the porta-potties at festivals. Bud Light doesn't just buy ads; they buy exclusive pouring rights at 100+ venues, integration into festival experiences, artist meet-and-greets, and data on millions of beer-drinking concert-goers.

The real moat is data. Live Nation knows more about live entertainment consumers than anyone. They track every search, purchase, arrival time, concession buy, and social media post. They know that country fans arrive earlier and drink more beer, EDM fans buy more merchandise, and rock fans are most likely to purchase VIP packages. This data is packaged and sold to sponsors, used to optimize pricing, and deployed to predict which artists will sell out which venues.

Venue ownership and operation is the physical manifestation of market power. Live Nation controls over 200 venues globally, including many of the most prestigious and profitable. Owning venues provides guaranteed inventory for tours, eliminates venue rental costs, captures all ancillary revenue, and most importantly, locks out competitors. If you control the only 20,000-seat amphitheater in a market, rival promoters can't compete for major tours.

The international expansion strategy focuses on replicating this model globally. Ticketmaster had 23 million net new enterprise tickets that were signed in 2024, with two-thirds coming from international markets. Each new market starts with ticketing partnerships, evolves to concert promotion, and culminates in venue acquisition or construction. The playbook is identical whether in São Paulo or Stockholm: control distribution, leverage it for content, monetize every touchpoint.

Artist Nation, the management division, closes the loop. By managing artists directly, Live Nation influences tour routing, venue selection, ticketing partnerships, and sponsorship deals. They're not just serving artists; they're directing them. An Artist Nation act is far more likely to play Live Nation venues, use Ticketmaster, and accept Live Nation sponsorship deals. It's vertical integration so complete it makes the old Hollywood studio system look fragmented.

The financial results validate the model. Gross margins have expanded from 20% in 2010 to nearly 30% in 2024. Live Nation reported an operating income of $825 million, with adjusted operating cash flow of over $2.15 billion. Adjusted operating income for concerts is at a record high, up 65% to $530 million with margins of 2.8%. Return on invested capital consistently exceeds 15%. Free cash flow generation has doubled in five years. The business model isn't just working—it's accelerating.

Yet this same model is also Live Nation's greatest vulnerability. The interconnected revenue streams that create value also create conflicts of interest. When Live Nation the promoter negotiates with Live Nation the venue owner to sell tickets through Live Nation's Ticketmaster, who represents the fan's interests? This question, more than any financial metric, may determine the company's future.

IX. Current State & Future Outlook (2024–Present)

Michael Rapino stood before investors on the February 2025 earnings call with characteristic confidence: "2024 was live music's biggest year yet, as artists toured the world and fans turned out in record numbers. 2025 is shaping up to be even bigger thanks to a deep global concert pipeline, with more stadium shows on the books than ever before". The numbers backed him up: Concert attendance increased by 4%, with 151 million fans attending over 50,000 Live Nation events, and revenue hit a record $23.16 billion.

The 2025 pipeline is genuinely unprecedented. Through mid-February, stadium shows are up 60% from the prior-year period and 65 million tickets have been sold for Live Nation concerts, a double-digit annual increase. Stadium tours for 2025 include Beyoncé's Cowboy Carter tour, Morgan Wallen's I'm The Problem Tour, Kendrick Lamar and SZA's Grand National Tour, and Post Malone and Jelly Roll's Big Ass Stadium Tour. Each represents not just a tour but a cultural moment that Live Nation has successfully monetized.

The stadium boom reflects a fundamental shift in touring economics. Artists discovered during COVID that fewer shows at higher prices generates better margins than grinding through 100-date tours. US stadium and arena tours are selling through over 75% in the first week onsale at a higher rate than the same time last year. Artists who are touring in 2025 and recently toured between 2022 and 2024 are averaging double-digit growth in tickets sold per show and gross revenue per show. A single stadium show can gross $5-7 million versus $1-2 million for an arena, while requiring similar production costs.

Technology investments are finally bearing fruit, though not without controversy. In May 2024, the company confirmed rumours of a 1.3 TB data leak, at subsidiary Ticketmaster, whose potential impact may extend to over 500 million of their customers. The breach exposed the vulnerability of centralized ticketing systems and raised questions about data security that regulators are still investigating. Yet the company continues to pour money into "next-generation" ticketing technology, including blockchain-based verification systems and AI-powered pricing algorithms.

International expansion remains a bright spot despite regulatory headwinds. Over 60 million fans attended shows in Live Nation-operated venues in 2024, up double-digits, with North America and Latin America driving almost all growth. The Middle East represents a particular opportunity, with Saudi Arabia's entertainment ambitions creating demand for Live Nation's expertise. The company is advising on venue construction, routing major tours through Dubai and Riyadh, and exploring festival partnerships that could generate hundreds of millions in incremental revenue.

The venue expansion strategy is accelerating despite capital intensity. Live Nation plans to add 20 large venues through 2026, primarily in underserved secondary markets. Each venue represents $50-100 million in construction costs but generates predictable, high-margin revenue streams for decades. The Brooklyn Paramount, opened in 2024, demonstrates the model: its VIP Club is generating 30% more revenue per show relative to VIP clubs at other top performing theaters in the U.S.

Premium experiences and VIP offerings have become crucial margin drivers. Revenue from premium offerings in amphitheaters are up over 20%, with ancillary per fan spend at major festivals of 100,000 fans or more growing double digits, driven by VIP ticket upgrades and increased food and beverage sales. The company is essentially creating a class system within venues—general admission, reserved seating, club level, and ultra-VIP—each with dramatically different price points and margin profiles.

But storm clouds are gathering. Live Nation CFO Joe Berchtold acknowledged that the antitrust trial is on pace to take place early next year, with potential remedies ranging from behavioral constraints to full divestiture of Ticketmaster. The company maintains that a breakup would harm consumers, but privately, executives are preparing contingency plans including potential spin-offs and strategic partnerships.

Competition is evolving in unexpected ways. While traditional rivals like AEG remain contained, new threats emerge from technology platforms. Spotify is experimenting with direct ticketing integration. TikTok is becoming the primary driver of music discovery, potentially disrupting Live Nation's influence over artist development. Direct-to-fan platforms like DICE are growing rapidly in major markets, offering transparent pricing and better user experience.

Artist relations remain complex. While superstars benefit from Live Nation's scale and guarantees, mid-tier acts increasingly feel squeezed. The company's standard deals often require 360-degree participation, taking cuts of merchandise, sponsorships, and even recording revenue. Some artists are exploring alternative models: Chance the Rapper self-promoted his tour, Bad Bunny worked with independent promoters in Latin America, and several EDM acts have created their own festival brands.

Climate change poses an underappreciated risk. Extreme weather events are increasing, affecting outdoor venues that generate Live Nation's highest margins. The 2023 Burning Man disaster and multiple festival cancellations due to extreme heat are warning signs. Insurance costs for outdoor events have tripled in five years, and some locations are becoming unviable during traditional summer touring season.

Despite these challenges, Live Nation's market position appears unassailable in the near term. The anticipated scaling of global venue expansion efforts will further entrench their dominance. Transacted Ticketmaster tickets for 2025 shows are up 3% at 106 million, while committed sponsorship is up double-digits as 75% of the year is sold. The company is guiding to double-digit AOI growth through 2027, implying confidence that neither competition nor regulation will materially impact operations.

The bull case remains compelling: live entertainment is one of the few experiences that can't be digitized, demographics favor continued growth as millennials enter peak earning years, and international markets remain underpenetrated. The bear case is equally valid: regulatory intervention could force structural changes, technology could disintermediate traditional ticketing, and another black swan event could shut down live events. As we enter 2025, Live Nation stands at an inflection point—dominant yet vulnerable, essential yet reviled, growing yet potentially facing its greatest existential threat since the merger.

X. Playbook: Business & Strategic Lessons

Live Nation's fifteen-year run from merger to monopoly offers a masterclass in platform economics, vertical integration, and regulatory arbitrage. The strategic lessons extend far beyond entertainment, providing a template for how to build—and potentially how to break—market dominance in the experience economy.

Lesson 1: Control the Choke Point Ticketmaster was always the key to the kingdom. In any two-sided marketplace, controlling distribution is more valuable than controlling supply. Artists come and go, venues can be built, but owning the transaction layer—the moment where interest converts to revenue—provides unassailable market power. Live Nation understood what many content companies miss: distribution is king, content is merely the prince.

The parallel to other industries is striking. Amazon controls e-commerce not through products but through fulfillment. Google dominates not through information creation but through search. The lesson: identify the choke point in any value chain and own it completely. Everything else becomes negotiable.

Lesson 2: Create Artificial Bundling in Fragmented Markets The concert industry was historically local because live performance is inherently geographic. Live Nation's genius was creating scale advantages in an unscalable business. They bundled routing efficiency (filling Tuesday nights in secondary markets), capital access (venue financing), and data insights (pricing optimization) into a package independent promoters couldn't match.

This playbook applies to any fragmented, relationship-driven industry. Roll up the fragments, create shared services that generate economies of scale, but maintain the illusion of local autonomy. The acquired companies keep their brands and founders, but the economics flow to the mothership.

Lesson 3: Make Competition Expensive, Not Impossible Live Nation never tried to eliminate competition entirely—that would trigger antitrust action. Instead, they made competition economically irrational. Competing with Ticketmaster required building expensive technology, signing venues, and convincing artists to take risks. Even well-funded competitors like AXS barely captured single-digit market share after spending hundreds of millions.

The strategic lesson: raise the cost of competition beyond the expected return. Don't build walls; dig moats. Make competitors exhaust capital on infrastructure while you focus on customer acquisition. By the time they achieve technical parity, you've moved the competitive frontier.

Lesson 4: Regulatory Capture Through Complexity The 2010 consent decree appears restrictive but actually protected Live Nation from more severe intervention. By agreeing to behavioral remedies they could creatively interpret, they avoided structural breakup while maintaining integrated operations. The decree became a shield, not a sword—they could point to compliance while continuing anticompetitive practices through loopholes.

The broader principle: when regulation is inevitable, shape it proactively. Complex behavioral remedies are preferable to simple structural ones. Create monitoring requirements that generate paperwork but don't constrain strategy. Make compliance so technical that violations become matters of interpretation, not fact.

Lesson 5: Vertical Integration as Offense and Defense Live Nation's expansion into artist management, venue ownership, and festival production wasn't just about revenue diversification—it was about creating mutual dependencies. An artist signed to Artist Nation needs Live Nation venues. A venue that wants major tours needs Ticketmaster. Each vertical extension reinforces the others, creating a web of relationships that becomes increasingly difficult to untangle.

This echoes the classic conglomerate strategy but with a twist: the verticals aren't just financially integrated but operationally interdependent. Breaking up the company would require unwinding thousands of contracts, relationships, and dependencies—a Gordian knot that even regulators hesitate to cut.

Lesson 6: Data as the Ultimate Moat Live Nation's true competitive advantage isn't venues or artist relationships—it's data. They know which acts will sell out which venues on which nights at which price points. This predictive power reduces risk, optimizes routing, and enables dynamic pricing that extracts maximum consumer surplus. Competitors might replicate the technology, but they can't replicate fifteen years of transaction history.

The strategic imperative: in platform businesses, data compounds faster than capital. Every transaction makes the next one more profitable. Focus on data capture even at the expense of short-term margins. The company that knows the most wins, regardless of who has the best product.

Lesson 7: Embrace the Villain Role Live Nation stopped trying to be loved around 2015. They realized that in a B2B2C model, consumer sentiment matters less than business relationships. Fans might hate Ticketmaster, but they'll still buy tickets. Artists might complain about Live Nation, but they'll still sign deals. Being essential is more important than being admired.

This is counterintuitive in the age of brand worship, but it reflects a deeper truth: in industries with high switching costs and limited alternatives, reputation is a luxury. Focus on being indispensable, not beloved. The most profitable companies are often the most hated—ask any cable company.

Lesson 8: Turn Fixed Costs into Variable Revenue Venues are massive fixed costs—they require maintenance whether full or empty. Live Nation transformed this liability into an asset by maximizing venue utilization. They book concerts on weeknights, rent to corporate events, host festivals in parking lots, and create new events like country music cruises. Every square foot, every hour becomes monetizable.

The principle applies broadly: any fixed cost can become a revenue center with creativity. Airlines sell credit cards, hotels become coworking spaces, and stadiums host esports. The constraint isn't physical capacity but imagination and execution.

Lesson 9: Capital Allocation in Cyclical Businesses Live entertainment is inherently cyclical—dependent on economic conditions, artist touring schedules, and cultural moments. Live Nation mastered countercyclical capital allocation: acquiring aggressively during downturns (2009, 2020) and harvesting cash during peaks. They use good times to build war chests and bad times to buy assets cheaply.

This requires institutional discipline that most companies lack. The temptation during good times is to expand operations rather than strengthen balance sheets. The fear during bad times prevents aggressive acquisition. Live Nation inverted this psychology, treating crisis as opportunity and success as preparation for crisis.

Lesson 10: The Platform Paradox Live Nation's ultimate lesson might be its most troubling: successful platforms eventually become too successful. Network effects that create value concentration also create political risk. The same integration that generates efficiency appears monopolistic. The data advantage that improves service enables exploitation. Every strength becomes a weakness when scrutinized through an antitrust lens.

The strategic question for any dominant platform: how do you maintain market power without triggering intervention? Live Nation never solved this paradox, which is why they face potential breakup despite—or because of—their success. The playbook for building monopolies is well-established; the playbook for maintaining them remains unwritten.

XI. Bull vs. Bear Case & Investment Analysis

The Bull Case: Irreplaceable Assets in an Experience Economy

The optimistic view of Live Nation starts with a simple observation: they own assets that cannot be replicated. You cannot build a new Madison Square Garden. You cannot recreate Lollapalooza's brand equity. You cannot duplicate decades of artist relationships overnight. These aren't just competitive advantages—they're permanent moats that widen with time.

The secular trend toward experiences over possessions accelerates Live Nation's growth. Millennials and Gen Z spend 72% more on experiences than previous generations. Concert attendance among 18-34 year-olds has grown 40% in five years. Social media transforms every concert into shareable content, creating FOMO that drives demand. Live music has become identity expression, not mere entertainment—and identity is price inelastic.

International expansion provides decades of runway. Live Nation has barely penetrated Asia, where rising middle classes and westernizing cultural tastes create enormous demand. India alone could support thousands of venues. China's concert market grows 30% annually. Africa's youth bulge represents a billion potential customers. The company's current international presence is a beachhead, not a mature market.

Technology modernization, despite current failures, represents massive opportunity. Ticketmaster's platform is essentially 1990s architecture with modern paint. Rebuilding with cloud infrastructure, mobile-first design, and AI-powered personalization could reduce costs by 30% while improving user experience. NFT ticketing could eliminate fraud and create new revenue streams. Virtual concerts could generate income without physical constraints.

The antitrust case, paradoxically, might strengthen Live Nation's position. A behavioral settlement similar to 2010 would remove uncertainty while allowing integrated operations. Even divestiture might unlock value—Ticketmaster alone could be worth $15-20 billion as an independent company. Historical precedent suggests antitrust actions rarely destroy value; they often create it through focus and financial engineering.

Pricing power remains vastly underutilized. Concerts are still cheaper than comparable entertainment. A three-hour Taylor Swift show costs less per minute than a movie ticket in many markets. VIP experiences could triple in price and still sell out. Dynamic pricing has only scratched the surface of demand-based optimization. As live music becomes increasingly scarce relative to digital content, pricing power will only increase.

The competitive landscape remains fragmented despite Live Nation's dominance. AEG focuses on owned venues rather than touring. Regional promoters lack capital for expansion. Tech platforms dabble without commitment. Direct-to-fan models work for niche artists but can't scale. The barriers to entry—capital requirements, venue relationships, artist trust—grow higher each year.

Financial metrics support aggressive valuation. Operating leverage means each incremental dollar of revenue drops 40-50% to operating income. Capital allocation remains disciplined with 15%+ ROIC. Free cash flow conversion exceeds 100% in normal years. The balance sheet, while leveraged, has no near-term maturities and benefits from rising rate environments that increase competitor financing costs.

The Bear Case: Structural Decline Meets Regulatory Doom

The pessimistic view sees Live Nation as a melting ice cube dressed as an iceberg. Start with the fundamental problem: they're a middleman in an increasingly direct world. Artists can reach fans through social media. Venues can sell tickets through their own platforms. Sponsors can activate through digital channels. Every technological advancement reduces Live Nation's relevance.

The antitrust case represents existential risk that markets underappreciate. Attorney General Merrick Garland stated "It is time to break it up"—that's not posturing but policy position. The government has 40 state attorneys general aligned, creating political pressure that transcends administrations. Breakup isn't a tail risk but a base case, and separated entities would be worth far less than the integrated whole.

Artist economics are unsustainable. Live Nation routinely guarantees 85-90% of gross to superstars, sometimes exceeding 100% to secure exclusive relationships. This works when ancillary revenue compensates, but margins are compressing. Artists increasingly demand larger shares of merchandise, sponsorship, and VIP sales. The company is caught between rising artist costs and consumer price resistance.

Technological disruption looms larger than admitted. Blockchain ticketing eliminates Ticketmaster's role. VR concerts provide live experiences without venues. AI can predict tour routing better than human promoters. TikTok drives music discovery more effectively than traditional marketing. Each innovation chips away at Live Nation's value proposition. They're fighting tomorrow's war with yesterday's weapons.

Economic sensitivity is severely underestimated. Live entertainment is discretionary spending that evaporates in recessions. A 2008-style downturn would slash revenue 50%+ while fixed costs remain. High leverage amplifies the pain—interest coverage could go negative quickly. Unlike 2020, when government support and revenge spending provided cushion, the next recession won't have extraordinary monetary support.

Demographics are shifting unfavorably. Gen Alpha shows less interest in traditional concerts, preferring gaming and digital experiences. Attention spans are shortening—three-hour concerts feel anachronistic to TikTok natives. The social currency of concert attendance is diminishing as virtual experiences provide similar status signals. Peak live music might be behind us, not ahead.

Competition is evolving in unpredictable ways. Amazon could enter ticketing overnight with superior technology and customer service. Apple could bundle concert access with Apple Music+. Netflix could promote live events as it does content. These platforms have unlimited capital, superior technology, and direct consumer relationships. Live Nation looks increasingly like Blockbuster before streaming.

Management incentives are misaligned with shareholders. Executive compensation rewards revenue growth over profitability, encouraging empire building. Insider selling has accelerated despite public optimism. The board lacks independence with multiple members having music industry ties. Corporate governance scores rank in the bottom quartile. When insiders sell while talking up the stock, investors should listen to actions, not words.

ESG concerns are mounting beyond Astroworld. Live Nation has been linked to at least 200 deaths and 750 injuries at its events in seven countries since 2006. From 2016 to 2019, they had also been cited for at least ten OSHA violations. Climate change makes outdoor events increasingly risky. Insurance costs are spiraling. Regulatory scrutiny extends beyond antitrust to safety, labor practices, and environmental impact. The social license to operate is eroding.

Investment Synthesis

Live Nation trades at a crossroads between its bull and bear narratives. At current valuations (EV/EBITDA of ~15x), markets price in continued growth but not breakup risk. The risk/reward appears asymmetric to the downside: successful antitrust defense might drive 20-30% upside, while breakup could cause 50%+ downside.

For long-term fundamental investors, Live Nation represents a complex bet on several variables: the durability of live experiences, the effectiveness of antitrust enforcement, the pace of technological disruption, and management's ability to navigate these challenges simultaneously. The company's strategic position remains formidable, but its vulnerabilities are multiplying faster than its strengths are compounding.

The prudent approach might be optionality rather than directional betting. Long-dated options provide exposure to upside while limiting downside. Pair trades (long Live Nation, short legacy entertainment) could capture relative value. Credit products offer attractive yields with seniority to equity. The situation demands creativity, not conviction.

Ultimately, Live Nation embodies the paradox of platform monopolies: they're simultaneously essential and vulnerable, dominant and fragile, innovative and stagnant. Whether this paradox resolves through adaptation, disruption, or regulation will determine not just Live Nation's fate but the future structure of live entertainment. The only certainty is uncertainty—which, ironically, might be the most bearish signal of all.

XII. Recent News & Developments

The momentum entering 2025 appears unstoppable, yet fragility lurks beneath the surface. Live Nation's earnings for full-year 2024 show the company's revenue hit a record $23.1 billion thanks to high-margin amphitheaters and arenas. A heavy slate of concerts at arenas and amphitheaters, where Live Nation can offer VIP experiences and capture more revenue from food and beverage sales, pushed adjusted operating income to a record $2.15 billion, up 14%.

The 2025 pipeline suggests acceleration rather than moderation. Through mid-February, stadium shows are up 60% from the prior-year period. Currently, Live Nation's stadium tours for 2025 include Beyoncé's Cowboy Carter tour, Morgan Wallen's I'm The Problem Tour, Kendrick Lamar and SZA's Grand National Tour, and Post Malone and Jelly Roll's Big Ass Stadium Tour. Each tour represents not just revenue but cultural moments that reinforce Live Nation's centrality to the live experience ecosystem.

Yet regulatory storms are gathering force. The antitrust trial looms in 2025, with discovery revealing increasingly damaging internal communications. The government's case has expanded beyond structural arguments to include specific instances of retaliation, market allocation, and innovation suppression. Multiple states are considering their own actions regardless of federal outcomes.

The data breach's full impact remains unknown. In May 2024, the company confirmed rumours of a 1.3 TB data leak at subsidiary Ticketmaster, whose potential impact may extend to over 500 million of their customers. Class action lawsuits are consolidating, with potential damages in the billions. More concerning is the reputational damage—consumers already skeptical of Ticketmaster now question its basic competence to protect their information.

International expansion continues despite headwinds. Middle Eastern venues are under construction with Live Nation advisory contracts. Latin American festival acquisitions are accelerating. Asian partnerships are deepening. Yet each market brings unique challenges—regulatory requirements, cultural differences, and entrenched local competitors who won't yield easily.

The technology transformation Rapino promised remains largely aspirational. Despite massive investment, Ticketmaster's platform still crashes during high-demand sales. The user experience remains frustrating, with multiple redirects, confusing fee structures, and limited customer service. Competitors like DICE and AXS offer superior experiences but lack inventory—a Catch-22 that preserves Ticketmaster's dominance despite its deficiencies.

Artist relations show signs of strain. Several major acts are experimenting with alternative models for their 2026 tours. Direct-to-fan platforms are gaining traction among mid-tier artists tired of 360 deals. Even some Artist Nation clients are questioning the value proposition as streaming revenues recover and touring costs escalate.

The capital markets remain supportive but increasingly nervous. Bond yields have widened despite strong cash generation. Stock volatility has increased with each regulatory update. Analyst recommendations are bifurcating between bulls who see value and bears who see existential risk. The consensus is dissolving into conviction camps.

As we write in August 2025, Live Nation stands at its most successful yet most vulnerable moment. Record revenues coincide with record scrutiny. Market dominance coincides with market disruption. The empire has never been larger, yet its foundations have never been shakier. Whether this represents a buying opportunity or a selling imperative depends entirely on one's view of antitrust enforcement, technological change, and the fundamental value of controlling live experiences in an increasingly digital world.

The next twelve months will likely determine Live Nation's trajectory for the next decade. Will it emerge from antitrust proceedings structurally intact and competitively strengthened? Will it be broken into components that unlock hidden value? Or will it face a slow decline as technology, regulation, and changing consumer preferences erode its moats? The only certainty is that the status quo—dominant yet despised, essential yet vulnerable—cannot persist indefinitely. Something has to give.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube