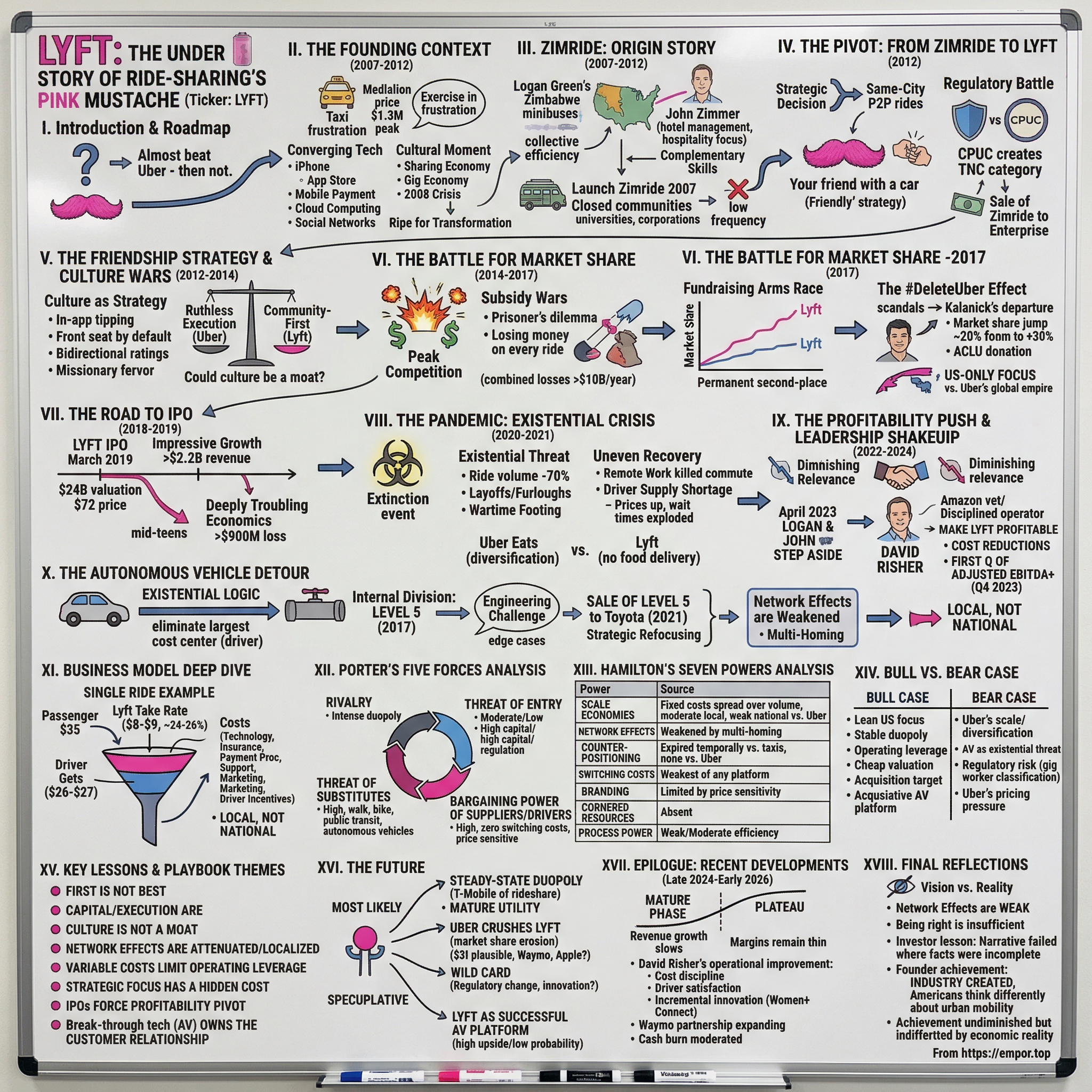

Lyft: The Underdog Story of Ride-Sharing's Pink Mustache

I. Introduction & Episode Roadmap

How did two scrappy founders with pink fuzzy mustaches strapped to the grills of their cars almost beat Uber — and then, quite clearly, not?

That question contains more lessons about platform economics, capital intensity, and the brutal mathematics of being number two than perhaps any other startup story of the last decade. Lyft is not a failure. It is not defunct. It carries over thirty million active riders in the United States, generates more than five billion dollars in gross bookings annually, and has finally — after years of hemorrhaging cash — begun to produce adjusted profits. But it is also a company that went public at a valuation of twenty-four billion dollars, saw its stock briefly touch eighty-seven dollars per share on its first day of trading, and now sits in the mid-teens, having destroyed roughly eighty percent of its IPO investors' capital. It holds approximately thirty percent of the American ride-hailing market, while its rival Uber commands essentially all the rest — plus a global empire spanning food delivery, freight logistics, and autonomous vehicle partnerships.

The Lyft story matters because it is the cleanest case study in modern business of what happens when you have the right idea at the right time, build genuine cultural differentiation, earn the love of the media and the public, and still lose. It tests every assumption venture capitalists hold dear about network effects, winner-take-most markets, and the power of narrative. And it forces a reckoning with an uncomfortable truth: in platform businesses with contested supply, being beloved is not the same as being durable.

The themes running through this story are timing versus execution, culture as strategy versus culture as moat, the compounding advantages of incumbency, and the irreducible tension between growth and profitability in a capital-intensive marketplace. To understand how Lyft arrived at its current crossroads, the story begins not in San Francisco, not with a pink mustache, and not even in the United States — but in a crowded minibus in Zimbabwe.

II. The Founding Context: Why 2007–2012 Was Ripe for Ride-Sharing

Before Uber and Lyft existed, getting a ride in an American city was an exercise in frustration that most people simply accepted as a fact of life. The taxi industry in major metropolitan areas operated under a medallion system that had, in many cities, remained fundamentally unchanged since the 1930s. In New York, a single taxi medallion sold for over one million dollars at its peak — a government-granted monopoly right that enriched medallion owners and fleet operators while keeping the supply of taxis artificially constrained. Passengers stood on street corners waving their arms. They called dispatch numbers and waited thirty minutes for a car that might or might not show up. They had no way to track their ride, no way to pay without cash or a clunky credit card swiper mounted on the back of the seat, and no meaningful recourse if the driver took a circuitous route or treated them poorly.

The experience was bad in New York, where at least you could hail a cab on most major streets. In cities like Los Angeles, San Francisco, or Houston, it was nearly nonfunctional. Taxi density was too low, public transit was underfunded, and car ownership was essentially mandatory. For a sense of how broken the system was, consider that a single taxi medallion in New York City sold for 1.3 million dollars in 2013 — a price that reflected not the value of the service being provided to consumers, but the artificial scarcity created by a government-enforced supply cap. The medallion system enriched a small class of fleet operators while providing terrible service to millions of riders. The gap between the transportation experience that technology made possible and the transportation experience that actually existed was enormous — and widening.

Several converging technologies finally created the conditions for someone to close that gap. The iPhone launched in 2007 and the App Store opened in 2008, putting a GPS-enabled, internet-connected computer in every pocket. Mobile payment infrastructure matured through services like PayPal and eventually Stripe, making it possible to charge a credit card without hardware. Cloud computing — Amazon Web Services launched its core services in 2006 — meant that a startup could build real-time geolocation matching systems without owning a single server. And social networks, particularly Facebook, created identity verification and trust layers that made it psychologically safer to get into a stranger's car.

To understand what these enabling technologies meant in practical terms, imagine a rider in 2012 versus 2006. In 2006, you could not hail a car from your phone because smartphones barely existed. You could not pay without cash because mobile payments did not work reliably. You could not track your car's arrival because consumer GPS was too imprecise and too expensive to deploy at scale. And even if all of those problems were solved, the server infrastructure required to run a real-time matching algorithm across thousands of simultaneous requests would have cost millions of dollars to build and maintain. By 2012, every one of those barriers had fallen. The technology stack that ride-sharing required had gone from prohibitively expensive to essentially free.

The cultural moment mattered as much as the technology. The sharing economy was emerging as both a movement and a buzzword. Airbnb, founded in 2008, had proven that people would open their homes to strangers if the platform created enough trust and convenience. TaskRabbit and a dozen other startups were demonstrating that the gig economy could match supply and demand for services ranging from furniture assembly to dog walking. The financial crisis of 2008 had left millions of Americans looking for supplemental income, and the idea of monetizing assets you already owned — a spare bedroom, a car sitting in your driveway — resonated deeply in an economy where traditional employment felt precarious.

San Francisco served as the perfect incubator for this transformation. The city was dense enough to generate ride demand, wealthy enough to support early adopters willing to try something new, and technologically literate enough to download a new app and trust it. Crucially, California's regulatory environment — messy, politicized, but ultimately permissive — allowed companies to operate in legal gray areas long enough to build consumer demand before regulators could shut them down. Previous attempts at technology-enabled taxi services had launched and died in the 2000s because neither the smartphone ecosystem nor the cultural willingness to share existed yet. By 2010, both had arrived simultaneously, and the stage was set for a revolution that would ultimately be led by two very different companies with two very different philosophies.

III. Zimride: The Unexpected Origin Story (2007–2012)

In 2005, a twenty-one-year-old UC Santa Barbara student named Logan Green spent a semester studying abroad in Zimbabwe. What he saw there rewired his understanding of transportation. In Harare, there were no Ubers, no well-organized bus systems, and very few private vehicles. Instead, people moved around the city in collective minibuses — informal, community-organized transportation where strangers shared rides going in roughly the same direction. Drivers would fill their vehicles before departing, passengers would negotiate fares, and the whole system operated on a kind of organic, trust-based efficiency that stood in stark contrast to the car-centric, single-occupancy commute culture Green had grown up with in Los Angeles.

Green returned to California with a conviction that would shape his entire career: most cars on American roads were essentially empty. The average private vehicle carries 1.1 people. Highways are clogged with four-seat and five-seat cars carrying a single human being. If you could match people going the same direction — if you could replicate Zimbabwe's collective transportation ethic using American technology — you could solve congestion, reduce emissions, and save money for everyone involved.

He started tinkering with a ride-matching website while still at UCSB, experimenting with Craigslist postings and crude digital tools to connect people heading in the same direction. Around this time, he connected with John Zimmer, a hotel management student at Cornell University's School of Hotel Administration. Zimmer was a different personality from Green — more polished, more business-oriented, steeped in the hospitality industry's obsession with customer experience. Where Green was the quiet, systems-thinking environmentalist, Zimmer was the gregarious operator who understood how to build products that made people feel good. They bonded over a shared frustration with American transportation and a shared belief that technology could unlock the massive latent capacity sitting idle in America's two hundred fifty million registered vehicles.

Their complementary skills were obvious from the start: Green was the visionary who could see the systemic opportunity in transportation, and Zimmer was the builder who could translate that vision into a product people would actually use.

In 2007, they co-founded Zimride — named, naturally, after Zimbabwe. The concept was straightforward: a ride-matching platform that connected people traveling the same long-distance routes. Think of it as a digital hitchhiking board. A student driving from Berkeley to Los Angeles for Thanksgiving could post their trip, and other students heading the same way could claim a seat and split gas money. The platform integrated with Facebook, using social graph data to create trust between riders and drivers. You were not getting into a stranger's car; you were getting into the car of someone who shared fourteen mutual friends and attended the same university.

Zimride's go-to-market strategy was clever and targeted. Rather than trying to build a consumer marketplace from scratch — a cold-start problem that kills most two-sided platforms — Green and Zimmer focused on closed communities: college campuses and corporations. They signed deals with universities like Cornell, UC Berkeley, and Stanford, embedding Zimride as the official ride-matching tool for campus communities. They then expanded into enterprise sales, signing contracts with companies like Walmart and the U.S. military, which wanted to help employees carpool to reduce parking demand and carbon emissions.

The business model worked. Revenue grew steadily. The platform processed hundreds of thousands of ride matches. But Zimride hit a ceiling that its founders found deeply frustrating. Long-distance carpooling was a fundamentally low-frequency use case. A student might carpool home for Thanksgiving and spring break — maybe four or five times a year. There was no habit formation, no daily engagement, no opportunity to build the kind of dense marketplace liquidity that creates compounding network effects. The economics of long-distance ride-matching were functional but flatly uninspiring. Green and Zimmer had built a solid small business. What they wanted to build was a transformative platform.

Meanwhile, something was happening in their own backyard that demanded their attention. Travis Kalanick and Garrett Camp had launched UberCab in San Francisco in 2010, initially as a black-car service for people willing to pay a premium for a reliable, app-hailed town car. And in mid-2012, a smaller company called SideCar had quietly launched a peer-to-peer ride service that allowed ordinary people to use their personal cars to give rides to strangers — the first true transportation network company, though the regulatory category did not yet exist. Green and Zimmer watched these developments with a mixture of fascination and dread. Fascination because the same-city, short-distance, peer-to-peer model was exactly the high-frequency use case Zimride needed. Dread because if they did not act fast, someone else would own the future they had been building toward for five years.

IV. The Pivot: From Zimride to Lyft (2012)

Inside Zimride's small San Francisco office in the summer of 2012, Logan Green and John Zimmer faced the most consequential strategic decision of their careers. They could see that same-city, peer-to-peer rides were going to be enormous — Uber was growing explosively, SideCar was proving the peer-to-peer model, and the regulatory environment in California was beginning to crack open. But pursuing this market meant cannibalizing their existing business. Every resource poured into a new short-distance product was a resource taken away from the Zimride platform that was generating their revenue and supporting their employees.

The internal debate was intense, and it played out over weeks of heated discussions in Zimride's cramped office. Zimride was working. It had customers, it had revenue, it had contracts with major universities and corporations. Walking away from that to chase a market already being contested by Uber — which had raised over three hundred million dollars by this point and was led by Travis Kalanick, one of the most aggressive operators in Silicon Valley history — felt like bringing a knife to a gunfight. But Green and Zimmer kept returning to a fundamental conviction: they had spent five years learning how to match riders and drivers. They understood marketplace dynamics, trust mechanics, and community building better than anyone. If they did not apply that knowledge to the massive opportunity in front of them, they would spend the rest of their lives watching someone else build what they should have built.

In the summer of 2012, they launched a new product within Zimride called Lyft. The name was deliberately casual — a "lift" with a twist, evoking friendliness and informality. But the truly iconic decision was the pink mustache. Green and Zimmer decided that every Lyft driver would attach a large, furry, hot-pink mustache to the front grill of their car. The effect was absurd, attention-grabbing, and deeply intentional. In a market where Uber positioned itself as "everyone's private driver" — sleek, professional, aspirational — Lyft wanted to be "your friend with a car." The pink mustache was ridiculous on purpose. It was a visual manifesto: this is not a taxi service, this is a community. You could spot a Lyft car from a block away, which made the pickup effortless, and the absurdity of the mustache made both rider and driver laugh, immediately breaking the social awkwardness of getting into a stranger's vehicle.

Riders were encouraged to sit in the front seat. They were expected to fist-bump their driver. Conversations were part of the experience. The entire interaction was designed to feel like catching a ride with someone you knew, not hiring a chauffeur. This was not mere marketing whimsy. It was a deliberate counter-positioning strategy against Uber's luxury-and-efficiency brand, and it tapped into the same sharing-economy ethos that had made Airbnb feel like a movement rather than a hotel alternative.

The regulatory challenge was enormous. When Lyft launched, there was no legal framework for what it was doing. Taxis were regulated. Limousines were regulated. But the idea that an ordinary person could use a personal vehicle to give rides to strangers for money existed in a regulatory void. The California Public Utilities Commission had no category for it. Taxi companies were furious. City officials were confused. Lyft, along with SideCar and Uber (which launched its own peer-to-peer service, UberX, shortly after), essentially created facts on the ground — building so much consumer demand and driver supply that regulators were forced to accommodate rather than prohibit.

The regulatory battle was as much a lobbying effort as a legal one. Lyft, SideCar, and Uber mobilized their rider bases to write to regulators, attend public hearings, and advocate for the right to choose how they got around. It was grassroots advocacy powered by technology companies with marketing budgets, and it worked. In September 2013, the CPUC created the Transportation Network Company category — the first regulatory framework in the world designed specifically for app-based ride-hailing. The new rules required background checks, insurance coverage, and vehicle inspections but otherwise allowed TNCs to operate legally. It was a landmark moment that legitimized the entire industry, and Lyft had been at the forefront of pushing for it. That same year, Green and Zimmer made the final, irreversible commitment to their new direction. They sold Zimride to Enterprise Rent-A-Car, divesting the long-distance carpooling platform that had started it all in order to focus every dollar and every employee on Lyft's growth.

That same year, Green and Zimmer made the final, irreversible commitment to their new direction. The sale of Zimride to Enterprise was a pivotal moment that deserves more attention than it typically receives. Enterprise Rent-A-Car, the privately held rental car giant, saw Zimride's campus ride-matching technology as a complement to its existing car-sharing service, WeCar, which it had deployed at universities. For Enterprise, the acquisition was a modest bet on campus mobility. For Lyft, it was liberation.

Selling Zimride was both a financial necessity and a psychological liberation. The sale price was not publicly disclosed but was reportedly modest — enough to provide some runway but hardly a windfall. What it gave Green and Zimmer was clarity. They were no longer hedging. They were no longer maintaining a legacy business while incubating a new one. They were all in on peer-to-peer ride-sharing in American cities, competing head-to-head against the most aggressive and best-funded startup in Silicon Valley history. The pink mustache was no longer an experiment. It was the company.

V. The Friendship Strategy & Culture Wars (2012–2014)

If you had walked into Lyft's early San Francisco office, you would have found beanbag chairs, a mural of the pink mustache on the wall, and employees who genuinely believed they were building something different — not just a better taxi service, but a movement. From its earliest days, Lyft made a strategic bet that culture could function as a competitive weapon. In a market where the underlying product — getting from point A to point B in someone else's car — was fundamentally interchangeable, Lyft believed that how the experience felt would determine who won. And the experience Lyft wanted to create was the antithesis of everything Uber represented.

Uber, under Travis Kalanick, had built a corporate identity around ruthless execution, disruption, and a certain swagger that Silicon Valley admired and the public increasingly distrusted. Kalanick talked openly about crushing competitors, his company deployed ethically questionable tactics like "Operation SLOG" — a campaign to recruit Uber drivers at Lyft pickup locations — and the internal culture celebrated a win-at-all-costs mentality. The media, hungry for narrative contrast, found its perfect foil in Lyft. Here was the friendly ride-sharing company with pink mustaches and fist bumps, run by two founders who talked about community and sustainability rather than domination and disruption.

Lyft leaned into this positioning with missionary fervor. The company invested heavily in driver experience, offering features that Uber resisted: in-app tipping, transparent fare breakdowns, and a driver-friendly rating system that did not punish small infractions. While Uber treated drivers as interchangeable commodities in a supply chain, Lyft publicly celebrated its drivers as community members. This was not entirely altruistic — happy drivers provided better service and were less likely to defect to Uber — but it reflected a genuine philosophical difference between the two companies.

The passenger experience was similarly differentiated. Lyft riders sat in the front seat by default, a simple design choice that fundamentally changed the dynamic. You were not in the back of a taxi being driven by a stranger. You were sitting next to a person, and social norms compelled conversation. Lyft's rating system was bidirectional from the start — drivers rated passengers and passengers rated drivers — creating a sense of mutual accountability that mitigated bad behavior on both sides.

On the product side, Lyft introduced several innovations that reflected its community-first philosophy. Lyft Line, launched in 2014, was a shared-ride product that matched multiple passengers heading in similar directions — a digital version of the Zimbabwean minibus that had inspired Logan Green nearly a decade earlier. In-app tipping, which Uber would not add for years, generated goodwill with drivers and differentiated the economic proposition. Safety features, including in-app emergency buttons and ride tracking shared with trusted contacts, addressed the fundamental anxiety of getting into a stranger's car.

But there was an uncomfortable question lurking beneath Lyft's cultural strategy: could culture actually function as a competitive moat? The answer, as the next several years would demonstrate, was more complicated than Lyft's founding narrative suggested. Culture attracted media coverage and rider affinity, but it did not prevent drivers from switching to Uber when Uber offered better incentives. It did not prevent riders from opening the Uber app when Lyft's estimated time of arrival was three minutes longer. And it did not generate the kind of structural lock-in — switching costs, proprietary data, embedded workflows — that sustains durable competitive advantages in platform businesses.

Lyft began its national expansion in 2013 and 2014, rolling out market by market across the United States. The playbook was straightforward: recruit drivers, onboard them with the friendly Lyft ethos, launch with promotions and free rides for passengers, and grow liquidity until the market became self-sustaining. It worked. Lyft expanded into dozens of cities, building meaningful market presence everywhere it launched. But Uber was expanding faster, with more capital, and in every market Lyft entered, Uber was already there — or arrived within weeks.

The expansion strategy itself was methodical. Lyft would identify a target city, recruit a local team, begin signing up drivers weeks before launch, and then flood the market with free-ride promotions to generate initial demand. Once a city reached a critical mass of riders and drivers, the subsidies could be dialed back and the marketplace would approach self-sustaining liquidity. The problem was that Uber used an identical playbook with more money. In many markets, Uber would observe Lyft's launch preparations and preemptively increase driver incentives in that city, effectively making it more expensive for Lyft to achieve critical mass. It was a war of attrition fought city by city, block by block, ride by ride.

The cultural narrative bought Lyft time and attention. But the clock was ticking on whether it could convert that narrative into the kind of scale and economic performance that would make it a durable business.

VI. The Battle for Market Share: Peak Competition (2014–2017)

The years between 2014 and 2017 were the most expensive, chaotic, and consequential period in ride-sharing history. Two companies armed with billions of dollars in venture capital spent money at rates that made the dot-com bubble look restrained, all in pursuit of a simple but merciless goal: achieving enough marketplace liquidity to make the other side irrelevant. It was, by any measure, one of the most capital-intensive competitions in the history of American business.

The subsidy wars began in earnest in 2014. Both Uber and Lyft realized that the key to winning a two-sided marketplace was liquidity — the number of available drivers within a short pickup time of any given rider. More drivers meant shorter wait times. Shorter wait times meant more riders. More riders meant more money for drivers, which attracted more drivers. This virtuous cycle was the theoretical promise of network effects in ride-sharing, and both companies believed that whoever achieved critical liquidity first would lock in a self-reinforcing advantage that the other could never overcome.

The problem was that achieving liquidity required subsidizing both sides of the market simultaneously. Drivers were offered guaranteed minimum earnings: drive for a certain number of hours and earn at least a certain amount, regardless of how many rides you completed. Riders were offered promotional credits, discounted fares, and free rides for referrals. The result was that for much of this period, both companies were losing money on every single ride — paying drivers more than what riders paid, and lighting the difference on fire. Industry analysts estimated that at the peak of the subsidy wars, the combined losses of Uber and Lyft on rider and driver incentives exceeded ten billion dollars annually.

The economics were insane, but neither company could afford to stop. If Lyft reduced subsidies, drivers would switch to Uber. If Uber reduced subsidies, riders would try Lyft. It was a classic prisoner's dilemma, and both players chose the maximally aggressive strategy.

The fundraising arms race that fueled these subsidies was breathtaking. Lyft raised a two hundred fifty million dollar Series D round led by Andreessen Horowitz in 2014. In 2016, General Motors invested five hundred million dollars in Lyft as part of a strategic partnership focused on autonomous vehicles — a vote of confidence from one of America's largest corporations that gave Lyft both capital and credibility. But for every dollar Lyft raised, Uber raised ten. By 2017, Uber had raised a cumulative total exceeding twenty billion dollars, giving it a war chest that Lyft could never match. The disparity was not just financial; it was psychological. Lyft's fundraising was always framed as keeping pace with Uber, never as leading the market. This permanent second-place positioning affected everything from hiring to driver recruitment to media coverage.

Then, in late January 2017, something extraordinary happened. President Donald Trump signed an executive order restricting travel from seven Muslim-majority countries. Protests erupted at airports across the country. The New York Taxi Workers Alliance, in solidarity with the protesters, called a work stoppage at John F. Kennedy International Airport. Uber, whether through incompetence or indifference, appeared to break the strike by continuing to operate at JFK and disabling surge pricing — a move widely interpreted as profiting from a political crisis. The hashtag #DeleteUber went viral. Over five hundred thousand people deleted the Uber app in a matter of days.

And where did they go? Straight to Lyft. Downloads surged. Market share, which had been hovering around twenty percent, jumped past thirty percent almost overnight. It was the single largest competitive gift in ride-sharing history, and Lyft received it not because of anything it did, but because of what Uber was. Adding fuel to the fire, former Uber engineer Susan Fowler published a devastating blog post in February 2017 detailing a culture of systemic sexual harassment, HR indifference, and retaliatory management at Uber. The post went viral, triggering an internal investigation that would ultimately lead to the departure of more than twenty senior executives and, in June 2017, the resignation of CEO Travis Kalanick himself.

Lyft's positioning during this period was pitch-perfect. The company donated a million dollars to the ACLU, publicly championed diversity and inclusion, and positioned itself as the ethical alternative to Uber's toxic culture. The media narrative was irresistible: virtuous underdog versus corrupt giant. Lyft's brand sentiment soared.

But here is where the story turns instructive for investors. Despite #DeleteUber, despite Uber's cascading scandals, despite Lyft's surge in market share and brand favorability, Lyft could not convert the moment into a permanent structural advantage. Within a year, Uber had replaced Kalanick with Dara Khosrowshahi — a measured, diplomatic operator who systematically repaired the company's culture and public image. Uber's market share stabilized. Many riders who had deleted Uber redownloaded it when prices or wait times on Lyft proved less competitive. The episode revealed a painful truth about ride-sharing: in a commodity market where switching costs are zero, even massive brand advantages are transient.

Lyft made another consequential strategic decision during this period: it chose to remain exclusively focused on the United States. Uber, by contrast, was expanding aggressively into Europe, Asia, Latin America, and Africa — spending billions to build or acquire operations in dozens of countries. Lyft's decision to stay domestic was framed as disciplined capital allocation. Why burn money fighting regulatory battles and local competitors in markets you do not understand when the American market alone is worth tens of billions of dollars? In hindsight, this was probably the right call — Uber ultimately lost billions on international expansion and retreated from markets like China, Russia, and Southeast Asia. But Uber's global diversification also gave it something Lyft would never have: a portfolio of businesses — Uber Eats, Uber Freight, Uber's advertising division — that could cross-subsidize its rides business and insulate it from the brutal unit economics of any single market.

VII. The Road to IPO: Growing Up in Public (2018–2019)

By 2018, both Lyft and Uber had been private for nearly a decade. Their investors — Andreessen Horowitz, Fidelity, General Motors, and dozens of others — wanted liquidity. The companies themselves needed to demonstrate that the billions of dollars they had consumed could produce an actual public-market business. The race to IPO became its own competition, and Lyft chose to sprint.

On March 29, 2019, Lyft went public on the NASDAQ exchange, becoming the first major ride-hailing company to list in the United States. It was a deliberate strategic decision: by going first, Lyft could capture investor attention before Uber's much larger offering sucked up all the oxygen. The timing also reflected a certain bravado — Lyft wanted to prove it could stand on its own, not just as Uber's shadow.

The S-1 filing painted a portrait of a company with impressive growth and deeply troubling economics. Revenue for 2018 was approximately 2.2 billion dollars, representing growth of over one hundred percent year-over-year. Active riders exceeded eighteen million. The company claimed thirty-nine percent of the U.S. ride-sharing market — a number that competitors and analysts immediately contested, arguing it was inflated by how Lyft defined the market. But the losses were staggering: Lyft had posted a net loss of over nine hundred million dollars in 2018, with no clear timeline to profitability.

The IPO priced at seventy-two dollars per share, valuing the company at approximately twenty-four billion dollars. On the first day of trading, shares surged to nearly eighty-eight dollars, a euphoric opening that briefly made Lyft worth more than many established Fortune 500 companies. Then reality intervened. Within a week, the stock had fallen below the IPO price. Within months, it had crashed into the forties. By the end of 2019, shares were trading in the low forties, having lost roughly half their value from the first-day peak.

The collapse reflected a rapid repricing of expectations. Public market investors, unlike venture capitalists, demanded a path to profitability — not just growth narratives and addressable market slides. Lyft's unit economics were still fundamentally broken: the company was spending more to acquire and retain riders and drivers than it earned from each ride. The only path to profitability required either raising prices — which would drive riders to Uber — or cutting subsidies — which would drive drivers to Uber. This circular trap defined Lyft's economic reality, and public investors understood it immediately.

Making matters worse, Uber IPO'd just six weeks later, in May 2019, raising 8.1 billion dollars in the largest technology IPO since Alibaba. Uber's offering was forty times the size of Lyft's and attracted a different class of institutional investor. The comparison was unflattering: Uber had four times Lyft's revenue, a global footprint spanning sixty-three countries, and a diversified business including food delivery and freight. Lyft looked provincial by comparison — a single-product, single-market company trading at a premium to a more diversified competitor.

The IPO experience forced Lyft into a painful but necessary transformation. The growth-at-all-costs playbook that had defined the private years was no longer viable under the scrutiny of quarterly earnings calls and public market analysts. Logan Green and John Zimmer began pivoting toward efficiency, cutting costs, and promising a path to profitability. But the damage to investor confidence was profound. Lyft had entered the public markets with a story about transforming American transportation and the promise of network effects that would eventually produce monopoly-like returns. What investors got instead was a commoditized marketplace with thin margins and no visible moat.

The stock's relentless decline was a slow-motion repricing of what Lyft actually was: not a technology platform with winner-take-most dynamics, but a two-sided marketplace in a structurally challenging industry where switching costs were zero, competition was brutal, and profitability required operating discipline rather than visionary ambition. It was a harsh education, both for Lyft and for the venture capital ecosystem that had funded it.

There was also a deeper structural irony at play. By going public first, Lyft had intended to set the narrative for ride-sharing valuations. Instead, it set a cautionary template. When Uber IPO'd weeks later, its own stock also fell immediately and continued declining for months — but Uber's larger scale, diversified business, and global ambitions gave institutional investors a reason to hold through the pain. Lyft had no such cushion. It was a pure-play on a single product in a single market, and when that product's unit economics disappointed, there was no secondary thesis to fall back on. The lesson was painfully clear: in a commodity marketplace, the luxury of being a public company comes at a high price.

VIII. The Pandemic: Existential Crisis & Resilience (2020–2021)

On March 11, 2020, the World Health Organization declared COVID-19 a global pandemic. Within days, cities across the United States locked down, offices emptied, and Americans stopped moving. For most technology companies, the pandemic was a disruption that accelerated existing digital trends. For Lyft — a company whose entire value proposition required two strangers to sit in an enclosed space together, breathing the same air — it was something closer to an extinction event. For a company whose entire revenue depended on people getting into cars with strangers, the pandemic was an existential threat of the most literal kind.

Lyft's ride volume dropped by more than seventy percent almost overnight. Revenue, which had been growing steadily, collapsed. The company was burning cash at an alarming rate, with no visibility into when — or whether — demand would return. The magnitude of the crisis was unlike anything Lyft had faced, even during the brutal subsidy wars with Uber. Those fights had been about market share; this was about survival.

The company's market capitalization, already battered from its post-IPO decline, cratered further as investors contemplated the possibility that ride-sharing demand might never fully recover. Logan Green and John Zimmer acted with a speed that surprised even their critics. In April 2020, Lyft laid off approximately seventeen percent of its workforce — nearly one thousand employees — and furloughed hundreds more. Executive salaries were slashed. Marketing budgets were gutted. Every discretionary expense was eliminated. The company entered what was essentially wartime footing, prioritizing cash conservation above all else.

One decision during this period revealed something genuine about Lyft's mission-driven identity. The company launched a program offering free and discounted rides to healthcare workers, enabling nurses, doctors, and hospital staff to commute safely during a period when public transit felt dangerous and Uber and Lyft rides were scarce. It was a small initiative in the grand scheme of the pandemic, but it generated meaningful goodwill and media coverage, and it aligned with the values-driven brand that Lyft had cultivated since the pink mustache days.

Lyft survived the pandemic for two reasons that were somewhat ironic in retrospect. First, the IPO that investors cursed had actually left the company with a strong balance sheet — enough cash to endure months of dramatically reduced revenue without raising emergency capital. The public markets had funded Lyft's survival. Second, the US-only strategy that critics called unambitious meant Lyft had no exposure to the devastating international shutdowns that ravaged Uber's operations in Europe, Latin America, and Asia. Uber, with its global complexity and multiple business lines, faced a far more complicated crisis than Lyft's relatively focused American operation.

The recovery, when it came, was uneven and frustrating. By mid-2021, vaccine distribution was accelerating and Americans were beginning to move again. But the pandemic had permanently altered mobility patterns in ways that hurt ride-sharing. Remote work killed the daily commute — historically one of ride-sharing's most reliable demand drivers. Morning and evening rush-hour rides, which had been a substantial portion of Lyft's volume, never fully recovered. What did recover — and in some cases surged past pre-pandemic levels — was leisure and social travel: airport rides, weekend nights out, concert and event transportation.

The more acute problem — and the one that would haunt Lyft for the next two years — was driver supply. During the pandemic, many Lyft and Uber drivers had found other employment, received stimulus checks that reduced the urgency of gig income, or simply decided that driving strangers around during a respiratory pandemic was not worth the risk. When demand returned, drivers did not. The supply shortage was devastating. Wait times exploded from the pre-pandemic norm of three to five minutes to fifteen, twenty, even thirty minutes in some markets. Prices surged as algorithms attempted to balance thin supply against recovering demand. The customer experience degraded badly, and riders who had formed a Lyft habit during the #DeleteUber era found themselves reluctantly returning to Uber, which generally had better driver supply thanks to the drawing power of Uber Eats — a business that kept drivers active and on the road even when ride demand was low.

Lyft did not have a food delivery business. This was not an oversight; the company had deliberately chosen to remain focused on ride-sharing rather than diversify into delivery. But the pandemic exposed the strategic cost of that focus. Uber drivers could seamlessly switch between giving rides and delivering food, staying busy and earning money throughout the day regardless of ride demand. Lyft drivers could only give rides, and when rides were scarce, they left the platform entirely. The multi-product flywheel that Uber had built turned out to be not just a diversification strategy but a driver retention strategy, and its absence at Lyft was acutely felt.

The meme stock era of early 2021 briefly turned Lyft into a speculative trading vehicle, with the stock experiencing sharp volatility as retail traders on Reddit and other platforms identified it as a potential short squeeze candidate. The stock spiked above sixty dollars in March 2021, driven more by momentum and short interest than by any fundamental change in the business. For a moment, it looked like the pandemic might perversely benefit Lyft by resetting the cost structure, eliminating marginal competitors, and allowing the company to restart with a leaner operation. But the driver supply crisis that followed the demand recovery quickly demonstrated that Lyft's fundamental challenges — contested supply, intense competition, thin margins — had not been solved by the pandemic. They had merely been temporarily obscured by it.

IX. The Profitability Push & Leadership Shakeup (2022–2024)

By 2022, the pandemic recovery was well underway, but Lyft found itself in an uncomfortable position — profitable on a path that management had outlined, yet still losing money on a GAAP basis, and watching its stock price tell a story of diminishing relevance. Ride volumes were recovering but had not returned to pre-pandemic peaks. The stock had cratered from its IPO high of eighty-eight dollars to the low teens, a decline so severe that it raised questions about whether the company could survive as an independent public entity. Losses were still mounting. Activist investors were beginning to circle, pressing management for a credible plan to reach profitability.

The pressure was compounded by a contrast that grew more painful by the quarter: Uber, under Dara Khosrowshahi's leadership, had executed a dramatic turnaround. Uber was approaching profitability, its Eats business was thriving, and the stock was recovering. Every piece of positive Uber news was implicitly a rebuke of Lyft's strategy. If the ride-sharing model could work, why was it working for Uber and not for Lyft?

Logan Green and John Zimmer responded with a profitability plan that promised adjusted EBITDA breakeven by the fourth quarter of 2023. The plan involved massive cost reductions: killing the bike and scooter programs that had consumed capital without generating meaningful returns, reducing headcount through multiple rounds of layoffs, streamlining the technology organization, and focusing maniacally on core ride-sharing operations. Take rates — the percentage of each ride that Lyft kept as revenue — were pushed higher through better matching algorithms and reduced incentive spending. The company began acting less like a growth-stage startup and more like a mature operating business.

But the founders' credibility had been eroded by years of missed targets and unfulfilled promises. In April 2023, Green and Zimmer made the decision — or had it made for them — to step aside. Green resigned as CEO and Zimmer stepped down as president, though both remained on the board. Their replacement was David Risher, a veteran operator whose resume could not have been more different from the ride-sharing-native founders. Risher had spent thirteen years at Amazon in its early days, where he had risen to senior vice president overseeing the retail business. He subsequently became CEO of Worldreader, a nonprofit focused on digital literacy, and served on the board of Chegg, the education technology company. He was not a ride-sharing visionary. He was not a mobility evangelist. He was a disciplined operator who understood how to build efficient, scalable businesses.

Risher's background at Amazon was particularly relevant. He had spent his formative professional years in a company obsessed with operational efficiency, customer experience metrics, and relentless cost management — exactly the skills Lyft needed. His first weeks on the job reportedly included riding in dozens of Lyft vehicles incognito, speaking with drivers about their frustrations, and auditing the company's cost structure line by line.

Risher's mandate was blunt: make Lyft profitable. No more grand narratives about transforming transportation. No more experiments with autonomous vehicles, bikes, scooters, or adjacent business lines. Just make the core ride-sharing business work — generate more revenue per ride, spend less to acquire each rider and driver, and produce enough cash flow to justify the company's existence as a publicly traded entity.

Green and Zimmer's departure was handled with grace, but there was an unmistakable finality to it. The founders who had started with pink mustaches and fist bumps were giving way to a professional manager who had helped build Amazon's ruthlessly efficient retail machine. It was the corporate equivalent of a band's lead singers stepping aside for a session musician who could actually read the sheet music.

The transition was more than a change in personnel; it was a philosophical break with Lyft's founding identity. Green and Zimmer had built Lyft as a mission-driven company that happened to operate in ride-sharing. Risher ran it as a ride-sharing company that needed to make money. The distinction mattered. Under Risher, Lyft stopped talking about changing the world and started talking about reducing cost per ride. The pink mustache era was definitively over.

The results came faster than most observers expected. In the fourth quarter of 2023, Lyft reported its first quarter of positive adjusted EBITDA — a milestone that validated the turnaround thesis and sent the stock rallying from around ten dollars to over twenty dollars per share. The profitability was thin — generated more by aggressive cost-cutting than by revenue expansion — but it was real, and it demonstrated that the ride-sharing business model could produce positive unit economics when managed with discipline.

Through 2024 and into early 2025, Lyft maintained this trajectory. Profitability improved modestly quarter by quarter. Market share stabilized at roughly thirty percent — lower than the thirty-nine percent the company had claimed at IPO, but steady enough to sustain a functioning marketplace. The stock settled into a trading range of roughly thirteen to eighteen dollars, representing a market capitalization of six to eight billion dollars. This was a far cry from the twenty-four billion dollar IPO valuation, but it reflected something that the IPO valuation never did: the reality of what Lyft actually earned.

Risher introduced several product initiatives focused on differentiation within the constraints of a mature market. Women+ Connect, launched in 2024, allowed women and nonbinary riders to be matched preferentially with women and nonbinary drivers — a safety-focused feature that addressed a genuine pain point in ride-sharing and that Uber had not replicated. Price transparency improvements gave riders more predictable fare estimates. Driver experience investments, including more flexible scheduling tools and improved earnings visibility, aimed to stabilize the supply side of the marketplace. These were incremental improvements, not transformative innovations, but they reflected a company that had accepted its competitive position and was working to optimize within it.

X. The Autonomous Vehicle Detour & Strategic Bets

Few strategic pivots in recent startup history have been as expensive and ultimately futile as Lyft's pursuit of autonomous vehicle technology. It is a cautionary tale about the seductive logic of eliminating your biggest cost center — and the hubris of believing you can solve a problem that has defeated some of the world's best-funded engineering organizations. To understand why Lyft invested so heavily in self-driving cars — and why it eventually retreated — requires understanding the existential logic that drove the bet.

In ride-sharing, roughly seventy to eighty percent of the cost of every ride goes to the driver. The driver is not just the largest expense; the driver is the product. Without drivers, there are no rides, no revenue, no business. Autonomous vehicles represented the theoretical possibility of eliminating that cost entirely — turning a low-margin, labor-intensive marketplace into a high-margin technology platform. If self-driving cars worked, the company that controlled them would own the most profitable transportation business in history. And if they worked and you did not have them, you were dead.

This existential framing drove Lyft's AV investments. The 2016 strategic partnership with General Motors, which included GM's five-hundred-million-dollar investment, was partly about capital but mostly about positioning Lyft as a platform for autonomous vehicle deployment. The vision was that GM (and later other manufacturers) would build the self-driving cars, and Lyft would provide the network — the riders, the routes, the demand — on which those cars would operate. Lyft would become the operating system of autonomous mobility, not the manufacturer of the hardware.

In 2017, Lyft went further, establishing its own internal autonomous vehicle division called Level 5, headquartered in Palo Alto. The team grew to several hundred engineers working on perception, planning, and vehicle systems. It was a massive investment for a company that was already losing hundreds of millions of dollars annually on its core business.

But the autonomous vehicle industry was learning a painful lesson that outsiders had not yet absorbed: self-driving at scale was not an engineering problem that could be solved with enough money and enough PhDs. It was a nearly intractable challenge involving edge cases — the unusual, unpredictable situations that human drivers handle intuitively but that confound even the most sophisticated AI systems. A child chasing a ball into the street. A construction worker waving traffic through with ambiguous hand signals. A car door opening unexpectedly. Each of these scenarios represented a potential failure mode that had to be solved with near-perfect reliability before autonomous vehicles could operate safely in the real world. And there were millions of such scenarios.

By 2021, Lyft's leadership recognized what the industry was slowly acknowledging: full self-driving was not five years away, as optimists had claimed in 2016. It was possibly decades away from the kind of ubiquitous deployment that would transform ride-sharing economics. And Lyft — bleeding money on its core business, under pressure from public markets, and competing against companies like Waymo (backed by Alphabet's effectively infinite resources) and Cruise (backed by General Motors) — simply could not afford the R&D spending required to stay in the race.

In April 2021, Lyft sold its Level 5 autonomous vehicle division to Woven Planet Holdings, a subsidiary of Toyota, for approximately five hundred fifty million dollars. The sale was framed as strategic refocusing: Lyft would not build its own self-driving technology but would instead position itself as an open platform that any autonomous vehicle provider could plug into. Waymo, Motional (a joint venture between Hyundai and Aptiv), and others would build the cars; Lyft would provide the rides.

The sale price — five hundred fifty million dollars — was meaningful but modest relative to the billions that companies like Waymo and Cruise had spent on autonomous development. It roughly recouped what Lyft had invested in Level 5 but did not compensate for the opportunity cost of management attention and engineering talent that had been diverted from the core business.

Whether this was strategic wisdom or capitulation depends on one's time horizon and assumptions. The optimistic interpretation is that Lyft correctly identified that it could not win the AV manufacturing race and chose to compete where it had a natural advantage: demand aggregation and network operations. The pessimistic interpretation is that Lyft surrendered its only path to structural differentiation and is now entirely dependent on AV companies that have no particular reason to share their economics with a ride-hailing middleman.

The AV question was not the only strategic detour that proved costly. In 2018, Lyft acquired Motivate, the largest bike-share operator in the United States, which operated systems including Citi Bike in New York and Ford GoBike in San Francisco. The acquisition was part of a broader "multimodal transportation" thesis — the idea that Lyft should offer riders not just car rides but bikes, scooters, and eventually autonomous vehicles, all through a single app. The reality was less elegant. Bike and scooter operations were capital-intensive, low-margin, weather-dependent, and plagued by vandalism and regulatory challenges. Under Risher's leadership, these programs were scaled back dramatically as part of the broader profitability push.

The pattern across Lyft's strategic bets was consistent: ambitious thesis, significant investment, eventual retreat. Each detour consumed capital and management attention that might have been better spent strengthening the core ride-sharing business. The lesson was not that these bets were irrational — any of them could have worked in a different capital environment — but that a company perpetually fighting for survival against a better-funded competitor cannot afford the luxury of multiple strategic experiments.

The contrast with Uber's strategic approach is instructive. Uber also invested heavily in autonomous vehicles, bikes, and scooters. But Uber's diversification into food delivery — initially dismissed as a distraction — proved to be the company's most consequential strategic decision. Uber Eats transformed Uber from a single-product rides company into a multi-sided logistics platform, creating cross-selling opportunities, driver retention advantages, and a revenue diversification that insulated the company from the ride-sharing market's cyclicality. Lyft's decision not to enter food delivery was defensible on capital discipline grounds at the time, but it left the company strategically naked when the pandemic demonstrated the value of having multiple demand sources for the same driver network.

XI. Business Model Deep Dive & Unit Economics

To understand Lyft's business at its most fundamental level, consider a single ride. A passenger opens the Lyft app, requests a ride from downtown San Francisco to the airport, and is matched with a driver five minutes away. The ride takes twenty-five minutes and the passenger pays thirty-five dollars. Of that thirty-five dollars, Lyft keeps approximately eight to nine dollars — the "take rate" of roughly twenty-four to twenty-six percent. The remaining twenty-six to twenty-seven dollars goes to the driver.

Out of Lyft's eight to nine dollars, the company must fund the technology platform (servers, engineers, app development), insurance (Lyft carries a commercial insurance policy for every ride), payment processing fees (roughly two to three percent of the fare), customer support, marketing and rider acquisition, driver bonuses and incentives, and corporate overhead. When Lyft was growing aggressively, the cost of incentives alone — promotional credits for riders, guaranteed minimums for drivers — consumed more than the company earned on many rides. The unit economics were negative: Lyft was paying for the privilege of providing transportation.

The path to profitability required improving multiple variables simultaneously. Take rates needed to increase, meaning Lyft needed to capture a larger percentage of each fare — achieved through reduced incentive spending and algorithmic improvements in pricing. Driver utilization needed to improve, meaning each driver should spend less time waiting for rides and more time carrying passengers — achieved through better matching algorithms that predict demand and position drivers closer to likely pickup locations. And the cost structure needed to shrink, meaning fewer employees, less marketing spend, and more efficient operations.

Understanding how Lyft generates revenue requires looking beyond the headline ride-matching service to the full suite of monetization mechanisms the company has developed. Lyft's revenue model has four components, though ride-sharing dominates overwhelmingly. The primary revenue stream is the take rate on rides — the service fee that Lyft charges on every completed trip. A secondary and growing stream is advertising: Lyft sells ad placements within the app and on the screens mounted in some vehicles. A third stream is subscriptions: Lyft Pink (now called Lyft+) offers riders a monthly membership that provides discounted rides, priority pickups, and other perks. And a fourth stream is driver services: Lyft earns fees from the Express Drive vehicle rental program that provides cars to drivers who do not own suitable vehicles.

The marketplace dynamics of ride-sharing are theoretically powerful but practically limited. In a classic two-sided network effect, more riders attract more drivers (because there is more earning opportunity), and more drivers attract more riders (because wait times are shorter and coverage is better). This flywheel should, in theory, create a winner-take-all dynamic where one platform achieves such overwhelming liquidity that competitors cannot attract either side of the market.

In practice, ride-sharing network effects are far weaker than this theory suggests, for one fundamental reason: multi-homing. Both drivers and riders routinely use both Lyft and Uber. Most drivers have both apps open simultaneously and accept whichever ride request comes first. Most frequent riders have both apps installed and check prices and wait times on each before choosing. There is no cost to switching, no data to migrate, no workflow to rebuild. Multi-homing is frictionless, and it fundamentally undermines the winner-take-all dynamic that network-effects theory predicts.

Network effects in ride-sharing are also intensely local rather than national. Having abundant driver supply in Chicago does nothing for a rider in Miami. Each city is essentially its own marketplace with its own liquidity dynamics. This means that national scale provides limited competitive advantage beyond shared technology and brand recognition — and it explains why Lyft can maintain meaningful market share in many cities despite being dramatically smaller than Uber at the national level.

The capital intensity problem has diminished but not disappeared. Lyft no longer burns money at the rates it did during the subsidy wars, but maintaining marketplace liquidity still requires ongoing investment in driver incentives, particularly during supply-constrained periods. Every holiday weekend, every concert surge, every airport rush requires Lyft to offer bonuses that attract enough drivers to serve demand. This is not a one-time cost; it is a perpetual operating expense that compresses margins and limits the operating leverage that pure software businesses enjoy.

XII. Porter's Five Forces Analysis

The ride-sharing industry's structural dynamics explain why Lyft — and frankly even Uber — have struggled to generate the kind of returns that their early investors envisioned. Applying Michael Porter's framework to Lyft's competitive position reveals an industry with unfavorable economics across nearly every dimension.

Competitive rivalry between Lyft and Uber is intense by any measure. The United States ride-sharing market is effectively a duopoly, with Uber commanding roughly seventy percent share and Lyft holding the remaining thirty. But duopoly does not mean comfortable. Both companies compete aggressively on price, driver incentives, feature development, and brand perception. The products are functionally interchangeable — a Lyft ride from the airport and an Uber ride from the airport deliver identical outcomes. This commodity-like substitutability means that competition defaults to price, which compresses margins for both players. Neither company has been able to establish sustained pricing power, because any price increase by one simply drives volume to the other.

The threat of new entrants is moderate to low, which is actually one of the few structural advantages the industry offers its incumbents. Building a ride-sharing platform requires substantial capital investment in technology, insurance, regulatory compliance, and driver-rider acquisition. The cold-start problem — needing both drivers and riders to be present simultaneously in every geography — creates a meaningful barrier. Regulatory frameworks, once they were established, created another hurdle: new entrants must navigate licensing, insurance mandates, and background check requirements that incumbents have already satisfied. Regional competitors can and do succeed in specific markets, but building a national platform to challenge Lyft or Uber would require billions of dollars and years of sustained investment with no guarantee of success.

The bargaining power of suppliers — in this case, drivers — is moderate to high and represents one of the industry's most significant structural challenges. Drivers are not employees; they are independent contractors who can switch platforms instantaneously. Most active drivers maintain accounts on both Lyft and Uber and allocate their time to whichever platform offers better economics at any given moment. This multi-homing behavior means that neither company can count on driver loyalty, and both must continuously invest in incentives to maintain adequate supply. The gig economy regulatory environment adds additional pressure: California's AB5 legislation, various municipal regulations, and ongoing legal challenges over worker classification threaten to reclassify drivers as employees, which would dramatically increase costs. However, the atomized nature of the driver workforce — millions of individuals without collective bargaining power — limits their ability to extract concessions beyond what market dynamics provide.

The bargaining power of buyers — riders — is high, and this is arguably the most damaging of the five forces for Lyft's economics. Switching costs are functionally zero. Most frequent riders have both apps installed and comparison-shop in real time. Loyalty programs like Lyft Pink provide modest incentives to consolidate rides on one platform, but the savings are not large enough to prevent riders from checking Uber when Lyft's price or wait time is unfavorable. Riders are also highly price-sensitive: numerous studies have shown that the majority of ride-sharing customers will choose the cheaper option regardless of brand preference. This price sensitivity, combined with zero switching costs, means that Lyft has almost no ability to raise prices without losing volume.

The threat of substitutes is high and multifaceted. For shorter trips, riders can walk, bike, or take a scooter. For commutes, public transit competes directly in cities with adequate systems. For longer trips, personal car ownership remains the dominant mode of transportation in America, and the post-pandemic rise of remote work has permanently reduced the commuting occasions that drove ride-sharing demand. Looking further ahead, autonomous vehicles represent the most significant substitute threat — not because they replace ride-sharing, but because they could fundamentally restructure who provides and profits from it.

The aggregate picture is sobering. Lyft operates in an industry with intense rivalry, powerful suppliers and buyers, significant substitutes, and only modest barriers to entry. This structural reality explains why ride-sharing has proven so resistant to the kind of profitability that technology investors expect: the industry's competitive dynamics compress margins from every direction.

For investors trying to compare ride-sharing to other platform businesses, the Porter's analysis reveals a critical distinction. Search engines have a near-monopoly with massive switching costs (data lock-in, habit, and ecosystem integration). Social networks benefit from direct network effects where the product itself becomes more valuable with every user. Ride-sharing has neither. It is a marketplace business where the product — transportation — is a commodity, the supply is contested, and the customer has near-perfect information on pricing from competing platforms. This structural profile more closely resembles the airline industry or the restaurant industry than it does Google or Facebook, and the valuation implications are correspondingly different.

XIII. Hamilton's Seven Powers Analysis

Hamilton Helmer's Seven Powers framework asks a more pointed question than Porter's: not just what are the competitive dynamics of an industry, but what durable competitive advantages — "powers" — does a specific company possess? Applied to Lyft, the analysis is revealing and, for investors, somewhat discouraging.

Scale economies in ride-sharing are moderate and less impactful than they initially appear. Lyft's fixed technology costs — the engineering team, the servers, the app infrastructure — can be amortized across a larger ride volume, which theoretically creates cost advantages over smaller competitors. But Lyft is not competing against smaller competitors; it is competing against Uber, which has far greater scale. And the operational costs of ride-sharing are largely variable: each ride requires a driver, insurance, and payment processing. Unlike software, where marginal cost approaches zero, ride-sharing has a stubbornly high marginal cost floor. Furthermore, scale in ride-sharing is local, not national. Having millions of rides in New York does not reduce the cost of providing rides in Denver.

Network effects, the power most frequently cited in Lyft's favor, are weak to moderate in practice. The two-sided marketplace creates a theoretical flywheel: more drivers reduce wait times, attracting more riders, generating more income for drivers, attracting more drivers. But multi-homing — the ability of both drivers and riders to use competing platforms simultaneously — severely undermines this dynamic. In a market where both sides regularly participate on multiple platforms, the self-reinforcing advantages that network effects are supposed to provide are dramatically diluted. Uber's larger network provides a real advantage in driver availability and geographic coverage, but Lyft's thirty percent share demonstrates that network effects have not produced the winner-take-all outcome that theory predicted.

Counter-positioning — the ability to adopt a strategy that incumbents cannot copy without damaging their own business — was Lyft's most potent power in its early years, but it has expired. When Lyft launched, its community-focused, peer-to-peer positioning was genuinely counter-positioned against taxis, which could not adopt a technology-forward, gig-economy model without destroying their existing medallion-based businesses. But that counter-positioning was against taxis, not against Uber. And even against taxis, the advantage was temporal: once the regulatory frameworks for TNCs were established, there was nothing preventing anyone from copying the model. Today, Lyft has no meaningful counter-positioning against any competitor.

Switching costs are among the weakest of any technology platform in existence. A rider can switch from Lyft to Uber in approximately five seconds: open a different app, enter the same destination, and tap a button. There is no data to migrate, no history that matters, no workflow to rebuild, no integration to disconnect. Drivers can switch even faster — they literally toggle between apps ride to ride. The absence of switching costs means that Lyft must re-earn every customer's business on every ride, competing on price and availability rather than on lock-in.

Branding provides Lyft with some power, but far less than its cultural narrative would suggest. The Lyft brand has high awareness and generally positive associations — friendlier, more community-oriented, more socially conscious than Uber. But in ride-sharing, brand does not drive purchase decisions the way it does in luxury goods, consumer packaged goods, or even in adjacent categories like hotels. When a rider needs to get somewhere, the decision is overwhelmingly driven by price and estimated time of arrival, not by brand sentiment. Lyft's mission-driven positioning resonates with certain demographics, but surveys consistently show that the majority of riders will switch platforms for a two-dollar price difference or a three-minute wait time difference.

Cornered resources — proprietary assets that competitors cannot replicate — are essentially absent from Lyft's arsenal. The company does not possess unique data that competitors lack (both companies have similar rider and driver data), proprietary technology (the matching algorithms are similar in concept and execution), or exclusive partnerships (AV partnerships are non-exclusive, and driver supply is shared). The sale of the Level 5 AV division removed what might have become a cornered resource, though the billions of dollars required to develop it may not have been worth the investment. This is perhaps the starkest assessment in the entire framework: Lyft simply does not own anything that a well-funded competitor could not replicate.

Process power — the ability to execute operational tasks with consistently superior efficiency — is Lyft's most plausible competitive advantage, but it is weak to moderate at best. Under David Risher's leadership, Lyft has improved its matching algorithms, streamlined its cost structure, and developed operational processes that generate incrementally better unit economics. But these improvements are not proprietary: they are replicable by any well-managed competitor with sufficient engineering talent, and Uber has both more engineers and more data with which to train its algorithms.

The aggregate assessment is stark: Lyft possesses very limited durable competitive advantages under Helmer's framework. No single power is strong, and several are effectively absent. This explains the company's persistent difficulty in generating the kind of returns that justify its public market valuation — and it raises fundamental questions about the long-term investment case.

If one compares Lyft's Seven Powers profile to that of a truly dominant platform like Visa or Mastercard — which benefit from massive scale economies, powerful network effects, extremely high switching costs, and strong branding — the contrast is stark. Even compared to Uber, which at least benefits from greater scale, a broader product portfolio that strengthens driver supply (a form of cornered resource), and somewhat stronger process power through its larger engineering organization, Lyft's competitive position looks structurally disadvantaged. The Seven Powers framework does not predict that Lyft will fail. But it does predict that Lyft will struggle to generate the kind of excess returns that create substantial shareholder value, and seventeen years of corporate history have borne that prediction out.

XIV. The Bull vs. Bear Case

The investment debate around Lyft reduces to a fundamental question: can a number-two player in a commodity marketplace with zero switching costs and moderate network effects generate attractive returns for shareholders? The answer depends on which assumptions one makes about market structure, competitive dynamics, and the long-term evolution of autonomous transportation.

The bull case rests on several pillars. First, Lyft's US-focused strategy, long derided as unambitious, has produced a leaner, more disciplined business than Uber's sprawling global operation. Every dollar of revenue comes from a single market that Lyft understands intimately, and the absence of international complexity means fewer regulatory risks, no currency exposure, and simpler operations. Second, the duopoly structure of the American market, while not comfortable, appears stable: no new entrant has gained meaningful share in years, and the capital requirements to challenge either incumbent are prohibitive. Third, operating leverage is beginning to emerge as Lyft grows rides on a relatively fixed technology cost base — each incremental ride is increasingly profitable. Fourth, the stock's valuation, at less than one times revenue and a single-digit multiple of adjusted EBITDA, is objectively cheap relative to Uber and to most technology companies, offering meaningful upside if profitability continues to improve. Fifth, Risher's operational discipline has restored credibility with investors and created a more predictable, manageable business.

The management argument under Risher has become quietly compelling: Lyft does not need to beat Uber. It needs to earn a sufficient return on its thirty percent of a very large market. If the U.S. ride-sharing market is worth fifty to sixty billion dollars in gross bookings annually, thirty percent of that is fifteen to eighteen billion dollars in bookings, generating roughly four billion in revenue at current take rates. On a lean cost structure, that revenue base can produce meaningful cash flow.

The potential for an acquisition provides an additional source of optionality. Lyft's rider network, demand data, and geographic coverage could be valuable to a strategic buyer. Google, which is building Waymo's autonomous ride-hailing service, might value Lyft's demand aggregation capabilities. Amazon, which has invested in autonomous vehicles through Zoox, might see Lyft as a distribution channel. Apple, which has explored both car manufacturing and ride-hailing, could view Lyft as a faster path to market than building from scratch. At a six to eight billion dollar market capitalization, Lyft is acquirable by any of these companies without material financial strain.

The bull case also includes the autonomous vehicle platform thesis: as AV technology matures, multiple providers will need a ride-hailing network on which to deploy their vehicles. If Lyft can position itself as a neutral platform — available to Waymo, Motional, and other AV developers — it could evolve from a low-margin marketplace into a high-margin technology layer. This is speculative but not unreasonable, and it would represent the most transformative upside scenario for current shareholders.

The bear case is equally compelling and perhaps more grounded in structural reality. Uber's scale advantage is not merely quantitative; it is qualitative. Uber's diversified business — Eats, Freight, advertising, global rides — generates cross-subsidy opportunities that Lyft cannot match. When Uber wants to acquire or retain drivers, it can offer them earning opportunities across rides and deliveries. When Uber wants to acquire riders, it can bundle ride credits with Uber One memberships that also include Eats discounts. Lyft has no equivalent multi-product strategy, and building one from scratch at this stage would require precisely the kind of capital-intensive investment that the company can no longer afford.

The AV future, rather than being an opportunity, may represent an existential threat. If Waymo or Tesla or another company achieves fully autonomous ride-hailing at scale, the question becomes: why would they need Lyft at all? Waymo already operates its own consumer-facing ride-hailing app. Tesla has stated its intention to operate a robotaxi network directly. These companies would be building both the supply (autonomous vehicles) and the demand (consumer apps), leaving no role for a middleman. Lyft's platform thesis assumes that AV providers will want to outsource demand aggregation, but the history of technology suggests that companies with breakthrough technology prefer to own the entire customer relationship.

The regulatory environment also presents an underappreciated risk. Ongoing debates about gig worker classification — most notably California's AB5 legislation and similar proposals in other states and at the federal level — threaten to reclassify drivers as employees, which would dramatically increase Lyft's labor costs and potentially make the business model unworkable in its current form. While both Lyft and Uber face this risk equally, Uber's greater scale and diversification provide more capacity to absorb regulatory cost increases.

Market share erosion is another risk that the bull case underestimates. Uber's superior unit economics, driven by its larger scale and diversified revenue, give it the ability to subsidize rides at levels Lyft cannot match. If Uber chose to sacrifice short-term profitability to buy market share — as it has done multiple times in its history — Lyft's thirty percent share could decline toward a level where marketplace liquidity becomes challenged. Below some critical threshold of driver availability, wait times become uncompetitive, riders leave, drivers follow, and the marketplace enters a death spiral.

For investors evaluating Lyft on an ongoing basis, the noise of quarterly earnings calls and market commentary can obscure what truly matters. Two key performance indicators cut through that noise and tell investors whether the fundamental business is improving or deteriorating.

The first is take rate — the percentage of gross bookings that Lyft retains as revenue. The second is rides per active rider per quarter, which measures both customer engagement frequency and the company's ability to maintain habitual usage patterns. Take rate captures Lyft's pricing power and cost discipline in a single number: rising take rates signal improving unit economics, while declining take rates suggest competitive pressure or increased subsidization. Rides per active rider reveals whether Lyft is deepening relationships with existing customers or merely maintaining a base of infrequent users. Together, these two metrics tell the story of whether Lyft's business is improving or deteriorating at the most fundamental level.

XV. Key Lessons & Playbook Themes

The Lyft story, now spanning nearly two decades from Zimride's founding to the present, offers a series of lessons that transcend ride-sharing and speak to broader truths about platform competition, capital allocation, and the limits of narrative in business.

These lessons are not just relevant to ride-sharing. They apply broadly to any venture-backed platform business competing in a market with contested supply, zero switching costs, and capital-intensive operations. The parallels to food delivery, cloud kitchens, and other marketplace businesses are direct and instructive.