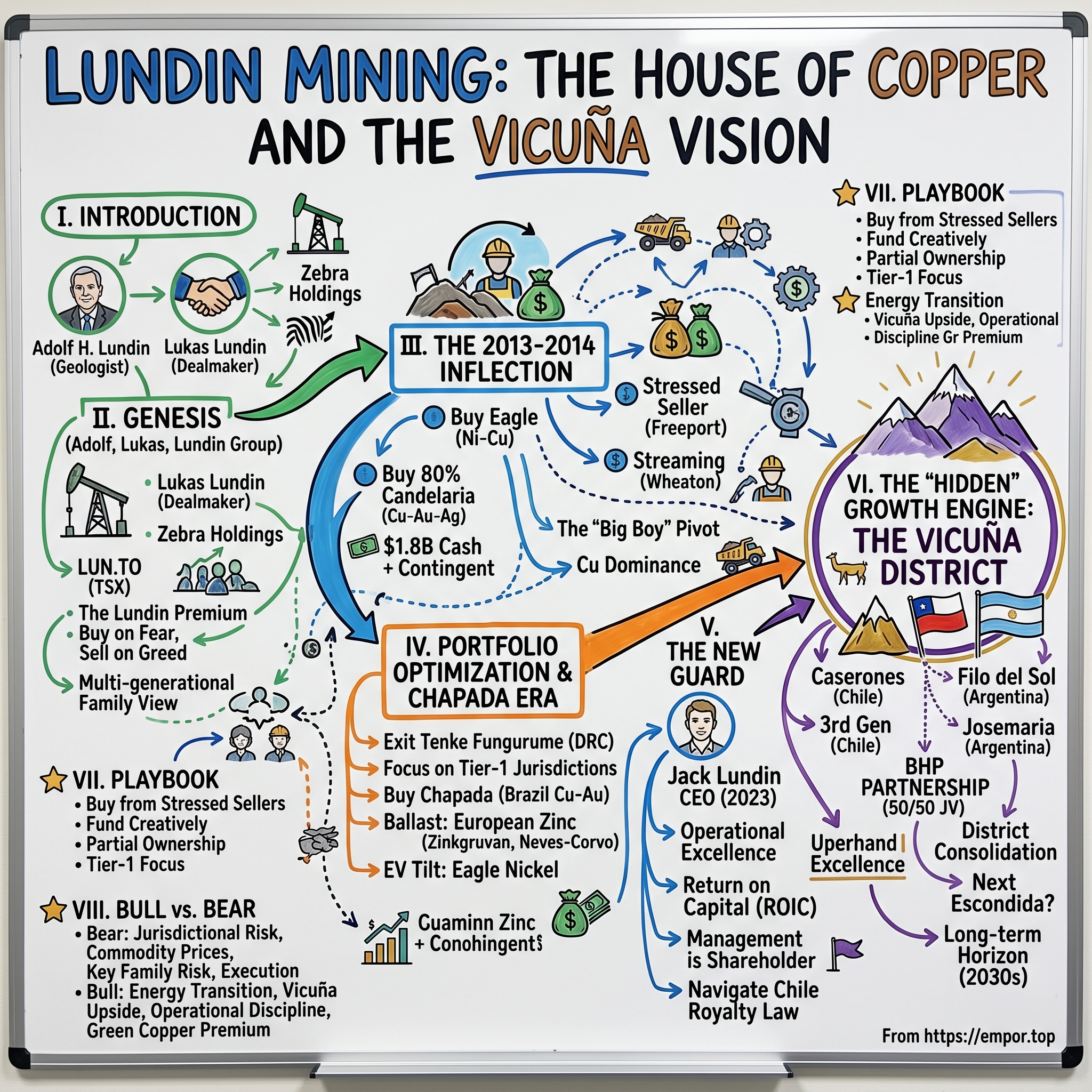

Lundin Mining: The House of Copper and the Vicuña Vision

I. Introduction: The "Lundin Premium"

It is October 2014, and inside a glass-walled conference room in Phoenix, Arizona, two delegations are squaring off across a polished walnut table. On one side sits the executive team of Freeport-McMoRan, North America's largest copper miner, fresh off a balance-sheet-bruising oil and gas misadventure. On the other side sits a comparatively small Canadian outfit run by a Swedish-Canadian family that most mining analysts can still spell only because of the company's distinctive double-O surname. Freeport wants out of a mine in the Atacama Desert called Candelaria. Lundin Mining wants in. By the end of that month, an 80% stake in one of the most profitable copper mines in the Western Hemisphere will have changed hands for $1.8 billion in cash plus contingent consideration1.

For analysts watching from their Bloomberg terminals, the price tag looked aggressive. For the Lundins, it was the natural next move in a playbook that has, over four decades, turned a Stockholm-based oil explorer's family office into one of the most efficient base-metals operators on Earth.

This is the central paradox of Lundin Mining Corporation. From the outside, it looks like just another mid-tier miner with a pleasingly diversified portfolio of copper, zinc, and nickel assets stretched across Chile, Brazil, Portugal, Sweden, and the United States. From the inside, it is something stranger and more interesting: a vehicle for a multi-generational family's specific, high-conviction view on how capital should be deployed inside the most cyclical industry on the planet. They buy when the rest of the sector is licking its wounds. They sell when the narrative is at peak greed. They prefer 80% ownership to 100%. And they treat geology the way Warren Buffett treats balance sheets — as the only thing that ultimately matters.

The thesis we will unpack across this episode is straightforward. Lundin Mining (TSX: LUN, Nasdaq Stockholm: LUMI) is not really a copper miner. It is a capital allocation machine, controlled by the Lundin family and Zebra Holdings, which happens to use the chemistry of Cu, Zn, and Ni as the substrate for its capital decisions. The "Lundin Premium" — the persistent tendency of Lundin-linked companies to trade at slightly richer multiples than their peer set — is not a quirk. It is a payment that the market makes for a specific kind of behavior: counter-cyclical M&A, disciplined divestiture, and an obsessive focus on Tier-1 jurisdictions.

Today we walk through the full arc. We start in the cigar-smoke offices of late-1980s Stockholm, with the family patriarch Adolf Lundin closing oil concessions in places most Western executives could not find on a map. We move through the great 2013-2014 pivot, when Lundin Mining was rebuilt from a zinc-and-nickel novelty into a serious copper house. We benchmark the 2019 Chapada acquisition in Brazil and ask the impolite question: did they overpay? We meet the new CEO, Jack Lundin, grandson of the founder, who took the chair in late 2023 and immediately bet the company on the most ambitious geological play in its history. And we end at the Vicuña District, a wind-scoured plateau on the Chile-Argentina border where Lundin Mining is now partnered with BHP — the largest mining company in the world — on what could become the next Escondida.

By the time the credits roll, you should know whether the so-called "Lundin Way" is really a moat, or just a story the family tells itself on the way to the next deal.

II. The Genesis: Adolf, Lukas, and the Lundin Group

To understand Lundin Mining you must first understand a thin, intense Swedish geologist with a side-parted haircut and an almost mystical belief in the value of being early. Adolf H. Lundin was born in 1932 in Sweden, trained as a petroleum engineer, and spent the early part of his career working for Shell and later for various Middle Eastern oil concerns. By the late 1970s, with the Iranian Revolution remaking the global oil map, he had made a personal decision that would define three generations of his family: he would only work on his own account, and he would only work in places his Anglo-Saxon competitors thought were too dangerous, too political, or too remote. He listed his first vehicle, International Petroleum Corporation, in Vancouver in 1983, and used Canadian capital markets — friendlier to speculative junior issuers than Stockholm — as the launchpad for the rest of his career[^2].

The "Lundin Way" was already visible in those early oil deals. Adolf went to Sudan when others would not. He went to Argentina, Yemen, and the Republic of the Congo. He went to Soviet-era Russia. And he liked to say, in a phrase that has become something of a corporate mantra across the family of companies, that there is "no risk, no reward." It was less a slogan than a license to operate where the competition refused to follow.

By the late 1990s, Adolf had decided that his next act would be metals. The thesis was simple: the late-cycle copper bear market of 1998-2002 had left the world's miners under-invested in new supply just as China's industrialization was about to remake demand. Lundin Mining Corporation in its modern form emerged from a 2007 merger between several Lundin-controlled vehicles — most importantly Lundin Mining and Tenke Mining, which together gave the new entity a portfolio of European base-metals mines plus a stake in the giant Tenke Fungurume copper-cobalt deposit in the Democratic Republic of Congo2. The original idea was to build a globally diversified base-metals house with a Swedish operating culture and a Canadian financing engine.

Then, in October 2006, Adolf died, and the patriarchy passed to his eldest son.

Lukas Lundin was the dealmaker. Where Adolf had been a geologist's geologist, Lukas — born in 1958, educated in Switzerland and at the New Mexico Institute of Mining and Technology — was a financier first and a rock-hound second. He understood that in mining, the deal is half the asset. He spent the 2000s and 2010s spinning out, recombining, and refinancing what came to be called the Lundin-gruppen, or in English, the Lundin Group of Companies — a constellation of separately listed vehicles, each focused on a different commodity but loosely coordinated through family ownership, overlapping boards, and a shared head office in Vancouver and Geneva[^4]. Lundin Petroleum tackled Norwegian crude. Lundin Gold built the Fruta del Norte mine in Ecuador. Filo Corp and NGEx Minerals hunted for new copper-gold in the Andes. Lundin Mining became the cash-generating base-metals flagship.

This is the structural feature that confuses newcomers. Lundin Mining is not the Lundin Group. It is the largest, most operationally mature member of a family of public companies that share genetics, governance overlap, and a roughly common worldview but are legally separate and traded on their own tickers. The family itself owns roughly 15% of Lundin Mining through Zebra Holdings and similar vehicles — not a controlling stake in the strict legal sense, but more than enough, given dispersed institutional ownership, to set strategic direction3.

The other structural feature worth pausing on is the dual listing. Lundin Mining trades on both the Toronto Stock Exchange (LUN) and Nasdaq Stockholm (LUMI), a quirk that reflects the family's transatlantic identity and gives the company a meaningfully broader cost-of-capital surface than a typical Canadian junior. Swedish pension funds, with their long duration profile and structural under-allocation to commodities, are natural holders. Canadian retail and institutional money, with its deep specialist mining coverage, provides the trading depth. The result is a share register that is unusually patient by the standards of the sector.

When Lukas died in July 2022 at the age of 64 after a two-year battle with brain cancer, the obituaries in the mining press described him as the last of the swashbuckling resource entrepreneurs4. The implicit question hanging over Lundin Mining at that moment was whether the deal-making culture would survive the founder's son. As we will see, the answer turned out to be more interesting than either the bulls or the bears expected.

III. The 2013-2014 Inflection: The "Big Boy" Pivot

In the spring of 2013, the global mining industry was in the middle of what insiders called the "super-cycle hangover." Iron ore prices were rolling over. Copper was wobbling on weakening Chinese imports. The major diversified miners — BHP, Rio Tinto, Anglo American — were under furious pressure from shareholders to undo a decade of debt-fueled acquisitions. The CEOs who had championed the bull case were being fired, and their replacements were under one explicit instruction from the boards: sell, simplify, and return capital.

Lukas Lundin saw exactly what was happening, and he understood the implication immediately. When the majors are forced sellers, the mid-tiers eat.

The first course was Eagle Mine. Located in the Upper Peninsula of Michigan, Eagle was a small, high-grade underground nickel-copper mine that Rio Tinto had developed but never really wanted. It was the wrong commodity, the wrong size, and in the wrong jurisdiction for a company of Rio's heft — a curiosity bolted onto a balance sheet that needed to shrink. In June 2013, Lundin Mining agreed to buy Eagle from Rio for $325 million in cash5. It was a textbook orphaned-asset deal: the seller wanted out, the asset was strategically irrelevant to the seller but materially accretive to the buyer, and the price reflected motivation rather than intrinsic value. Within three years, Eagle had paid back the entire purchase price in cumulative free cash flow.

But Eagle was the appetizer. The main course came eighteen months later, in October 2014, and it changed everything about how the market saw Lundin Mining.

Candelaria is an open-pit and underground copper mine in the Atacama region of northern Chile, producing roughly 150,000 tonnes of contained copper per year along with meaningful gold and silver by-product credits. Freeport-McMoRan had inherited it via its 2007 acquisition of Phelps Dodge, and by 2014 the company was scrambling to repair a balance sheet broken by an ill-timed expansion into Gulf of Mexico oil and gas. Freeport needed cash. Lundin had been studying Chilean copper for years.

The deal was announced on October 6, 2014. Lundin Mining agreed to acquire Freeport's 80% stake in Candelaria for $1.8 billion in cash at closing, plus up to $200 million in contingent consideration tied to future copper prices1. The remaining 20% was held — and is still held — by Sumitomo of Japan, a structure we will return to. The price represented roughly 4.5 times consensus next-twelve-months EBITDA for the asset. At the time, the equity research consensus was that Lundin had paid a full price for a mature mine and was taking on too much leverage to do it.

The funding structure is where the Lundin financial mind reveals itself. Rather than blow out the balance sheet, the company funded the acquisition with a stack of debt, a follow-on equity issue, and — most interestingly — a streaming transaction with Wheaton Precious Metals (then Silver Wheaton). In exchange for an upfront payment of roughly $648 million, Lundin sold Wheaton the right to a portion of future gold and silver production from Candelaria at a fixed discount to spot[^8]. Streaming is one of those quietly elegant innovations the mining industry has developed over the past two decades: it lets a base-metals operator monetize a by-product stream that the market does not really value, without giving up control of the asset. For Lundin, the Wheaton stream effectively de-risked something like a third of the purchase price.

What did the deal do to the company? It turned Lundin from a zinc-and-nickel curio with some African upside into a real copper producer. Pro forma for Candelaria, copper went from a minority of revenue to the dominant exposure — and copper, of course, is the metal of electrification, urbanization, and now, the energy transition. The "Big Boy" pivot was less a single transaction than a thesis statement: Lundin Mining was now a copper company, and it would be measured against copper-company benchmarks.

Twelve years on, the numbers vindicate the price. Candelaria has thrown off billions in cumulative free cash flow, repaid the original purchase consideration many times over, and given Lundin both the operating beachhead and the political credibility in Chile that would later enable the Caserones acquisition. The 2014 analysts who called it expensive were technically correct on the spot multiple. They were wrong on the asset.

For investors, the Candelaria lesson is the single most important data point in the Lundin Mining file. It demonstrates the operating model: identify a Tier-1 asset that a stressed seller wants to part with, fund it with a creative capital stack that protects the equity, and then run it for the next decade while the rest of the industry watches the cycle turn.

IV. Portfolio Optimization & The Chapada Era

By 2017, the post-Candelaria Lundin Mining had a new problem, one that successful companies in every industry eventually confront: it had grown out of its old portfolio. Some assets that had made sense for the smaller, scrappier company simply did not fit the new shape.

The most consequential housekeeping move was the exit from Tenke Fungurume. This was the giant copper-cobalt project in the Democratic Republic of Congo that had been one of the founding assets of the modern Lundin Mining via the 2007 Tenke merger. The company held a 24% non-operating interest behind majority owner Freeport-McMoRan. In late 2016, Freeport, again scrambling for cash, agreed to sell its operating stake to China Molybdenum for $2.65 billion. Lundin held a right of first offer over Freeport's interest and, after lengthy negotiations, agreed in November 2016 to sell its own 24% indirect interest into the transaction for $1.136 billion6. The proceeds flowed back into the balance sheet just as the next cycle's M&A window was opening.

The Tenke exit was emblematic of a broader strategic decision: Lundin would, going forward, focus exclusively on what the industry calls Tier-1 jurisdictions. The DRC offered world-class geology but came with chronic political risk, opaque royalty regimes, and operational headaches that did not suit a Vancouver-headquartered mid-tier with European and North American institutional shareholders watching ESG screens. The decision to leave Africa was a deliberate concentration of bet: the Americas and Europe, full stop.

With Tenke proceeds in hand and copper prices rebuilding, the team went hunting. They found their next target in Brazil. In April 2019, Lundin Mining agreed to buy the Chapada copper-gold mine in Goiás state from Yamana Gold for $800 million in cash plus contingent consideration tied to copper prices and silver production7. Chapada was — and is — a long-life, low-cost open-pit operation producing roughly 50,000 tonnes of copper a year, with meaningful gold by-product credits. The seller was a gold-focused company that had inherited a copper mine and never quite known what to do with it. The buyer was, by then, the world's most credentialed mid-tier copper operator.

Did Lundin overpay for Chapada? The enterprise value, including contingent payments and the assumption of certain liabilities, was closer to $1.0 to $1.2 billion depending on how you score the earn-outs. On 2019 numbers, that worked out to roughly 5 times next-twelve-months EBITDA, marginally above the median for Latin American copper transactions of the period. The bull argument is that Chapada has substantial sulfide expansion optionality at depth, plus a regional consolidation thesis through nearby tenure that the seller never funded. The bear argument is that Lundin paid Tier-1 multiples for a Tier-2 asset in a jurisdiction (Goiás, Brazil) where infrastructure, water rights, and labor relations are all more complicated than they look from Vancouver. The truth, six years on, is somewhere in between: Chapada has been a solid contributor but has not produced the kind of step-change cash flows that Candelaria did.

Step back from the individual transactions and look at the shape of the portfolio that emerged by the early 2020s. Copper, almost entirely from Chile and Brazil, made up roughly two-thirds of revenue. Zinc, from two old-world European mines — Zinkgruvan in Sweden, in continuous operation since 1857, and Neves-Corvo in Portugal — provided steady, high-margin, lower-volatility cash flow. Nickel, from Eagle in Michigan, gave the company a small but strategically meaningful tilt toward EV battery chemistries[^11].

The European zinc operations deserve a digression because they reveal something important about the Lundin temperament. Zinkgruvan and Neves-Corvo are not glamorous. They are not in the energy-transition narrative the way copper or nickel are. They are old, deep, technically demanding underground mines staffed by multi-generational mining families in small, cold, remote communities. A pure financial engineer would have sold them years ago. Lundin keeps them because (a) they are consistent free cash flow producers in low-political-risk jurisdictions, (b) they smooth out the volatility of the copper book, and (c) they preserve the company's cultural anchoring in Europe, which matters to a family whose patriarch was Swedish.

For investors, the portfolio shaping of the late 2010s established the modern Lundin formula: a copper-dominant book sized for growth, with European zinc as ballast and North American nickel as optionality. It is a barbell that has held up surprisingly well across every macro regime since.

V. The New Guard: Jack Lundin and Modern Management

In the spring of 2022, with Lukas Lundin entering the final months of his battle with glioblastoma, the family began a deliberate, quiet succession process across the entire Lundin Group. Lundin Mining at that moment was being run by CEO Marie Inkster, a finance executive who had taken the role in 2019 and steered the company competently through the COVID-19 disruption and the post-pandemic copper rally. The question facing the board was not whether Inkster was capable. The question was whether the next chapter of Lundin Mining — a chapter that would clearly involve a generational bet on the Andes — required a different kind of leader.

On October 31, 2023, the company announced that Jack Lundin, grandson of Adolf and son of Lukas, would become CEO effective immediately8. He was 36 years old.

The reaction on the sell side was cautious. Family successions in the mining industry have a famously mixed record, and 36 is young for a job whose typical incumbent has spent two decades wandering through the world's worst weather systems. But for anyone who had actually watched Jack Lundin's career, the appointment was less surprising than it looked. Jack had not been parachuted into the job from a wealth-management perch. He had spent his twenties working in the field — first as a project geologist, then in operations at the Fruta del Norte gold mine in Ecuador, the flagship asset of the family's separate vehicle Lundin Gold, where he eventually rose to the role of project director and helped bring the mine into commercial production in 2019. Among the third-generation Lundins, Jack was the operator.

The shift in tone since the handover has been instructive. Where Lukas's tenure was characterized by big, episodic, headline-grabbing deals — the kind of transactions that get printed on the wall of the deal room — Jack's first eighteen months in the chair have been characterized by a different vocabulary. Operational excellence. Cost discipline. Return on invested capital as the primary management metric, rather than tons produced or reserves added. The company has explicitly told the market that it intends to be measured on cash generation, not growth for growth's sake9.

The incentive structure makes this credible. The Lundin family owns roughly 15% of the company through Zebra Holdings and related vehicles3. That is an order of magnitude more skin-in-the-game than a typical mining major's executive team. When Jack Lundin talks about return on invested capital, he is talking about the family's own checkbook. This is the single most underappreciated structural feature of the entire Lundin Group: management is not a separate cohort of hired professionals whose interests must be aligned via stock options. Management is, in significant part, the largest single shareholder.

Around Jack sits a deep operating bench. The CFO function, the technical services group, and the Latin American country leads are all populated by mining-industry lifers, many of them holdovers from the Candelaria integration. The board includes Adam Lundin (Jack's cousin) as chair and a roster of independent directors with credibility in the Chilean and Brazilian mining communities. The family does not dominate the day-to-day operations of the company, but it sets the tone, picks the targets, and underwrites the long-term horizon.

The political-economic context the new team must navigate is meaningfully harder than the one their predecessors faced. Chile's mining sector has been through a multi-year debate about royalties, tax structure, and the relative shares of national versus regional benefit from mineral wealth. In May 2023, the Chilean Congress passed a new mining royalty law that introduced a hybrid ad valorem and margin-based royalty structure for copper producers, with effective tax rates rising for the largest miners[^14]. The compromise was less punishing than the worst-case scenarios the industry had feared, but it was meaningfully more onerous than the old regime.

Lundin's response was telling. Rather than threaten capital strike or relocate, the company leaned into local relationships. Long-standing community investment programs in the Atacama, formal participation in Chile's mining association consultations, and patient one-on-one engagement with regional governors all paid off in a settlement profile that turned out to be manageable. This is, again, the family-office model showing through: the Lundins have been in Chile long enough — and visibly enough — to be perceived as a permanent member of the community rather than a transient extractor.

For investors watching the leadership transition, the question to keep asking over the next several years is whether Jack Lundin's operator orientation actually shows up in the cash flow statement. Free cash flow conversion, copper cash cost per pound, and capital intensity per tonne of new production are the metrics on which his tenure will ultimately be judged.

VI. The "Hidden" Growth Engine: The Vicuña District

Now we get to the part of the story that is, depending on whom you ask, either the single most exciting district-scale play in the global copper industry or an expensive science project at altitude. The Vicuña District is the future on which Lundin Mining is now wagering its identity.

To picture the place, imagine driving east from the Chilean coastal town of Copiapó, climbing for hours through brown switchbacks into the high Andes, past the snowline, past the vicuña herds that give the district its name, until at roughly 4,000 meters above sea level you cross an invisible line on a rocky plateau where Chile ends and Argentina begins. The air at this altitude is thin enough that workers acclimatize for days before starting shifts. The geology, however, is among the richest copper-gold porphyry systems anyone has identified in the past fifty years.

In March 2023, Lundin Mining announced that it would acquire a 51% interest in the Caserones copper mine, located in Chile's Atacama region near Candelaria, from JX Nippon Mining & Metals for $950 million in cash plus contingent consideration of up to $50 million[^15]. Caserones is a large, conventional copper-molybdenum open-pit operation that had been in production since 2014 but had struggled under its previous owner with operational reliability and capital allocation. Lundin took operational control immediately and, in October 2023, exercised an option to increase its stake to roughly 70%10.

On its face, Caserones is just another mid-life copper mine bought from a tired seller — Candelaria 2.0, with smaller numbers. The deeper logic, however, is geographic. Caserones sits in the same geological neighborhood as Candelaria, allowing Lundin to share roads, water rights, power infrastructure, technical services teams, and government relationships across two assets that, in a different operating model, would each require its own full overhead stack. The synergy math is unglamorous but real: every dollar of shared infrastructure is a dollar that does not have to be financed at the marginal cost of capital.

But the truly interesting move came later. On July 29, 2024, Lundin Mining and BHP — the world's largest mining company by market value — announced that they would jointly acquire Filo Corp, a Lundin Group exploration vehicle that held the Filo del Sol copper-gold-silver discovery on the Argentine side of the border. The total consideration was approximately C$4.1 billion, split equally between the two acquirers11. In parallel, Lundin and BHP announced the formation of a 50/50 joint venture combining Filo del Sol with Lundin's existing Josemaria project across the border — creating a single, contiguous district-scale development asset that the industry has begun to call simply "Vicuña."

Read that again, because it is one of the more significant transactions in the recent history of the copper industry. The largest mining company in the world chose Lundin Mining — not Rio Tinto, not Glencore, not Freeport — as its operating partner on a deposit that BHP's own technical team considers one of the most attractive undeveloped copper-gold systems on the planet. The implicit endorsement of the Lundin platform's South American operating credibility is enormous.

The strategic logic behind the BHP partnership is worth unpacking. From BHP's perspective, Vicuña is too large for any single mid-tier to develop alone — initial capital intensity estimates run into the high single-digit billions of dollars — but too geographically specialized for BHP to want to staff up independently. Partnering with Lundin gives BHP balance-sheet leverage, local credibility, and integration with the broader district. From Lundin's perspective, partnering with BHP de-risks the project from both a financing and a permitting standpoint while keeping Lundin Mining squarely on the cap table of what could be the next Escondida — the BHP-operated mine in northern Chile that is the largest single copper producer in the world.

The "Filo synergy" the outline mentions is also a window into how the Lundin Group really operates as a system. Filo Corp was a separately listed Lundin-family vehicle with its own board and shareholder register. When the asset got hot, it was sold into a joint venture with the family's flagship base-metals operator and the largest miner in the world. NGEx Minerals, another Lundin Group exploration vehicle still active in the same district, plays a similar role: a publicly traded option on additional discoveries that, if successful, will likely find their way back into Lundin Mining through a similar M&A path[^18]. The exploration risk is borne by the public shareholders of the junior vehicles. The development capital, and ultimately the production cash flow, accrue to Lundin Mining. It is, in the most charitable framing, a beautifully efficient division of labor. In the less charitable framing, it is a related-party structure that requires sophisticated minority shareholders to monitor carefully.

The Vicuña bet will not pay off — or, alternatively, will not fully reveal its costs — until the early 2030s, when first production is currently targeted. For investors, the relevant near-term variables are the project's pre-feasibility study, expected to land in the second half of 2026, and the trajectory of permitting on both sides of the Chile-Argentina border.

VII. Playbook: Business and Investing Lessons

Strip away the geology and the family lore, and Lundin Mining is a fascinating case study in what makes a mid-tier mining company structurally interesting. Let us run it through two of the canonical strategy frameworks.

Start with Hamilton Helmer's 7 Powers. The most relevant power for Lundin is what Helmer calls Cornered Resource — the legal or geological ownership of an irreplaceable input. In commodities, this almost always comes down to controlling specific ore bodies. Lundin owns title to specific patches of the Earth's crust in the Atacama and the Vicuña District that no competitor can replicate, no matter how much capital they raise. The Vicuña consolidation is the purest expression of this power, because once you own contiguous district-scale tenure in a productive porphyry belt, future regulatory and infrastructure decisions tend to compound the advantage rather than erode it.

The second relevant power is Scale Economies, but applied at the district rather than the corporate level. Lundin's strategic genius is to recognize that mining-scale economies do not come from being the biggest miner in the world; they come from being the biggest miner in a specific geographic neighborhood. The shared infrastructure between Candelaria and Caserones, and the shared technical services between Josemaria and Filo del Sol, are the operating manifestations of this insight. The corporate parent matters less than the district platform.

Lundin is meaningfully weaker on the other five Helmer powers. Network Economies do not really apply in commodity mining. Switching Costs are minimal — copper buyers are price-takers. Counter-Positioning is hard to claim in an industry where Rio Tinto and BHP have effectively unlimited capital. Branding has some marginal play, but mostly through the energy-transition lens. Process Power exists in pockets — Candelaria's operating culture is genuinely good — but is not dramatic.

Now run it through Porter's Five Forces. Barriers to Entry in primary copper mining are stratospheric: a greenfield porphyry project today requires $3 to $8 billion in development capital, twelve to fifteen years of permitting and construction, and a tolerance for political risk that very few financial sponsors will underwrite. This is the single most important structural feature of the industry, and it is the reason that copper as a commodity is widely expected to enter a multi-decade supply deficit even before you start counting electrification demand. Bargaining Power of Buyers is low; copper sells into a deep global market at LME prices, and individual smelters have negligible leverage over individual mines. Bargaining Power of Suppliers — heavy equipment, mining services, energy — is moderate and rising, particularly for the specialized contractors who can operate at altitude. Rivalry is intense at the corporate level but muted at the district level because of the geographic concentration of productive geology. The Threat of Substitution is the single most important variable to watch, because if copper as the dominant electrical conductor were ever displaced — say, by some combination of aluminum, superconductors, or carbon-based materials — the entire bull case collapses. As of today, the substitution threat is real at the margin (aluminum in power transmission, for example) but not systemic.

The Lundin Playbook itself can be reduced to four operating principles that recur across every major transaction.

First, buy from stressed sellers. Eagle from Rio, Candelaria from Freeport, Chapada from Yamana, Caserones from JX Nippon — every meaningful Lundin acquisition has come from a counterparty whose own balance sheet or strategic situation made them a forced seller. The premium Lundin pays is almost always lower than what an unconstrained seller would extract.

Second, fund creatively. The Wheaton stream that helped finance Candelaria is the archetype. Lundin has consistently been willing to monetize secondary revenue streams (gold by-product, silver by-product, royalties on uncommitted ground) to protect the equity from over-dilution.

Third, prefer partial ownership to total ownership. The Candelaria deal left Sumitomo with 20%. Vicuña is a 50/50 JV with BHP. Caserones still has a JX Nippon residual stake. The principle is that local or strategic partners provide political cover, alternative perspectives, and a sanity check on capital decisions that 100%-owned subsidiaries often lack. The cost is some economic dilution; the benefit is durability.

Fourth, focus on Tier-1 jurisdictions and exit the rest. The Tenke divestiture is the cleanest expression of this principle, but it shows up everywhere in the portfolio.

The deepest investing lesson from the Lundin story is about time horizon. The family thinks in decades. The market thinks in quarters. The premium that long-duration capital can extract in a cyclical industry — when it is willing to buy at the bottom and hold through the cycle — is, empirically, very large.

VIII. Bear vs. Bull Case

Every long-form investing story owes the reader a fair statement of the opposing case. Lundin Mining is no exception.

The bear case starts with jurisdictional risk. Roughly three-quarters of pro-forma production and reserve value sits in South America, primarily Chile but with growing Argentine exposure through Vicuña. Chile is, by Latin American standards, a Tier-1 mining jurisdiction with a sophisticated regulatory system and a long tradition of foreign investment, but it is not Canada or Australia. The 2023 royalty reform passed without crippling the industry, but it did demonstrate that the political consensus around mining-friendly tax policy is no longer unconditional. A future left-of-center government with a worse macro situation could revisit the question. Argentina is materially harder: Vicuña sits on the Argentine side as well, and Argentina's history of capital controls, currency volatility, and unpredictable resource policy is a meaningful overhang on the long-dated cash flows.

The bear case continues with commodity-price exposure. Copper, despite all the energy-transition narrative, remains a cyclical industrial metal whose price can fall 30% in a quarter on a single piece of bad Chinese property-sector data. Lundin's free cash flow is a near-linear function of the copper price above a roughly $3.00 per pound cash cost; below that line, the math gets uglier quickly. Zinc and nickel, the diversifying commodities, have their own cycles that do not always offset the copper cycle.

The third bear point is what mining analysts call "key man" risk — or, in Lundin's case, key family risk. The premium the market pays for the Lundin platform is implicitly a payment for the family's judgment and discipline. If a future generation of Lundins were to dilute that culture — through a bad acquisition, an empire-building tendency, or a softening of the financial conservatism that has defined the past four decades — the premium would compress. There is no contractual protection against this. The market simply has to trust that the family will continue to behave the way the family has historically behaved.

The fourth bear point is execution. Vicuña, when it eventually gets built, will be the largest single capital project in Lundin's history. The mining industry's record on greenfield mega-projects is dismal: cost overruns of 50% or more are the norm, not the exception. Even with BHP as a 50/50 partner, the engineering and permitting risk on a project of this scale is substantial.

Now the bull case. It begins, as all copper bull cases now do, with the structural supply-demand math of the energy transition. Electrification of transportation, build-out of renewable generation capacity, expansion of electrical grids in the developing world, and the new wave of AI-driven data center construction all require enormous quantities of copper, and the industry has not been investing at remotely the level required to meet the projected demand12. The supply gap that the major equity research desks are forecasting for the early 2030s is not a forecast in the conventional sense; it is a mathematical identity, given the lead time of new mine development. Existing producing copper assets are, in this framework, structurally undervalued.

The second bull point is Vicuña as the next Escondida. Escondida, the BHP-operated mine in northern Chile, is the single most valuable copper asset in the world, producing roughly a million tonnes of contained copper per year and generating cash flows that have, over its operating life, dwarfed those of any other single mining asset. The technical case for Vicuña reaching a similar scale is real, although the timeline is long. If Lundin Mining ends up owning 25% of the next Escondida — by virtue of its 50% in the Vicuña JV with BHP — that asset alone would be worth a substantial multiple of the company's current enterprise value.

The third bull point is operational excellence under the Jack Lundin regime. The early signals from the new CEO suggest that the next decade of the company's history will look less like the deal-driven 2010s and more like a disciplined cash-return story, with growth funded internally rather than through frequent equity issuance. If the family's stated discipline on ROIC actually holds — and the 15% inside ownership makes it likely that it will — Lundin Mining could end up being one of the rare mining stocks whose total shareholder return is driven primarily by dividends and buybacks rather than commodity beta.

The fourth bull point is the "green copper" premium. As industrial buyers, particularly European utilities and battery manufacturers, increasingly source according to embedded-carbon criteria, low-emissions producers with European operational anchors will likely capture some pricing premium. Lundin's mix of European zinc operations, Chilean copper assets with progressive electrification of their fleets, and North American nickel positions the company favorably on this axis.

The three KPIs that any long-term investor in Lundin Mining should track are: copper cash cost per pound (the operating performance signal), free cash flow conversion rate (the discipline signal), and progress against the Vicuña pre-feasibility milestones (the optionality signal). Tonnes produced, reserve additions, and headline EBITDA are interesting but secondary.

IX. Conclusion

Step back from the deal histories, the geological maps, and the Helmer frameworks, and what is Lundin Mining, really?

It is a four-decade experiment in whether a family office can run a public mining company better than a professional management cohort can. The hypothesis being tested is that long-duration, owner-aligned capital — patient enough to buy from forced sellers at the bottom of cycles, disciplined enough to walk away from glamorous deals at the top, and culturally rooted enough in specific operating jurisdictions to absorb political shocks that would scatter footloose competitors — produces structurally better returns than the alternative.

The verdict, after forty years, is heavily but not unconditionally favorable. The Candelaria deal alone has justified the family's premium. The Tenke exit demonstrated that the discipline cuts both ways. The Vicuña gambit, partnered with BHP, has elevated the company into a different conversation than it was in even five years ago. None of this proves that the next forty years will look like the past forty. But it does suggest that the structural features of the platform — the dual listing, the family ownership, the operating culture, the geographic concentration in friendly jurisdictions — are not accidents. They are deliberate choices, repeatedly validated by results.

The question of whether Lundin Mining is a Tier-1 major or a super-mid-tier is, in the end, somewhat beside the point. The major diversifieds — BHP, Rio Tinto, Glencore — are vehicles for institutional capital to own broad commodity beta with operational competence. Lundin is something different: a specialized base-metals operator with concentrated geographic and family exposure, designed to compound a specific kind of capital allocation skill over multi-decade time horizons. It will never be as big as BHP, and it does not need to be. It will, however, almost certainly continue to outpunch its market cap in the rooms where the next generation of base-metals deals get done.

There is a final, slightly philosophical observation worth making. The mining industry is one of the few corners of the modern economy where time horizon is still an actual moat. Building a copper mine takes fifteen years. Permitting it takes most of a decade. The development capital is so large that mistakes cannot be unwound. In an investing environment increasingly dominated by quarterly earnings, algorithmic trading, and instant liquidity, the participants who can credibly think in twenty-year windows — and back that thinking with their own capital — have a structural advantage that is essentially impossible to arbitrage away.

The Lundins have been doing this since Adolf put International Petroleum on the Vancouver Stock Exchange in 1983. Their bet is that they will still be doing it, on the same plateau of Andean rock, when the third generation hands off to the fourth.

For investors trying to assess whether the next chapter of that story will look like the last one, the cleanest signal is not in the headline reserves or the next quarterly EBITDA. It is in the cash flow statement of a company that, more than almost any of its peers, has earned the right to be measured on what it does with the money rather than how much of it it can produce.

References

References

-

Lundin Mining to Buy Control of Freeport's Candelaria Mine — Reuters, 2014-10-06 ↩↩

-

Lundin Mining History & The Legacy of Lukas Lundin — The Northern Miner, 2022-07-27 ↩

-

Obituary: Mining Titan Lukas Lundin Dies at 64 — The Northern Miner, 2022-07-27 ↩

-

Lundin Mining to Buy Yamana Gold's Brazilian Mine for Over $1 Billion — Financial Post, 2019-04-15 ↩

-

Lundin Mining Announces CEO Succession — Bloomberg, 2023-10-31 ↩

-

The Lundin Family's Next Big Bet Is a Remote Valley in the Andes — Mining.com, 2024-01-15 ↩

-

Copper Is the New Oil — Goldman Sachs Equity Research, 2024 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube