Lululemon Athletica Inc.: The Science of Feel and the Battle for the Athleisure Throne

I. Introduction & Episode Roadmap

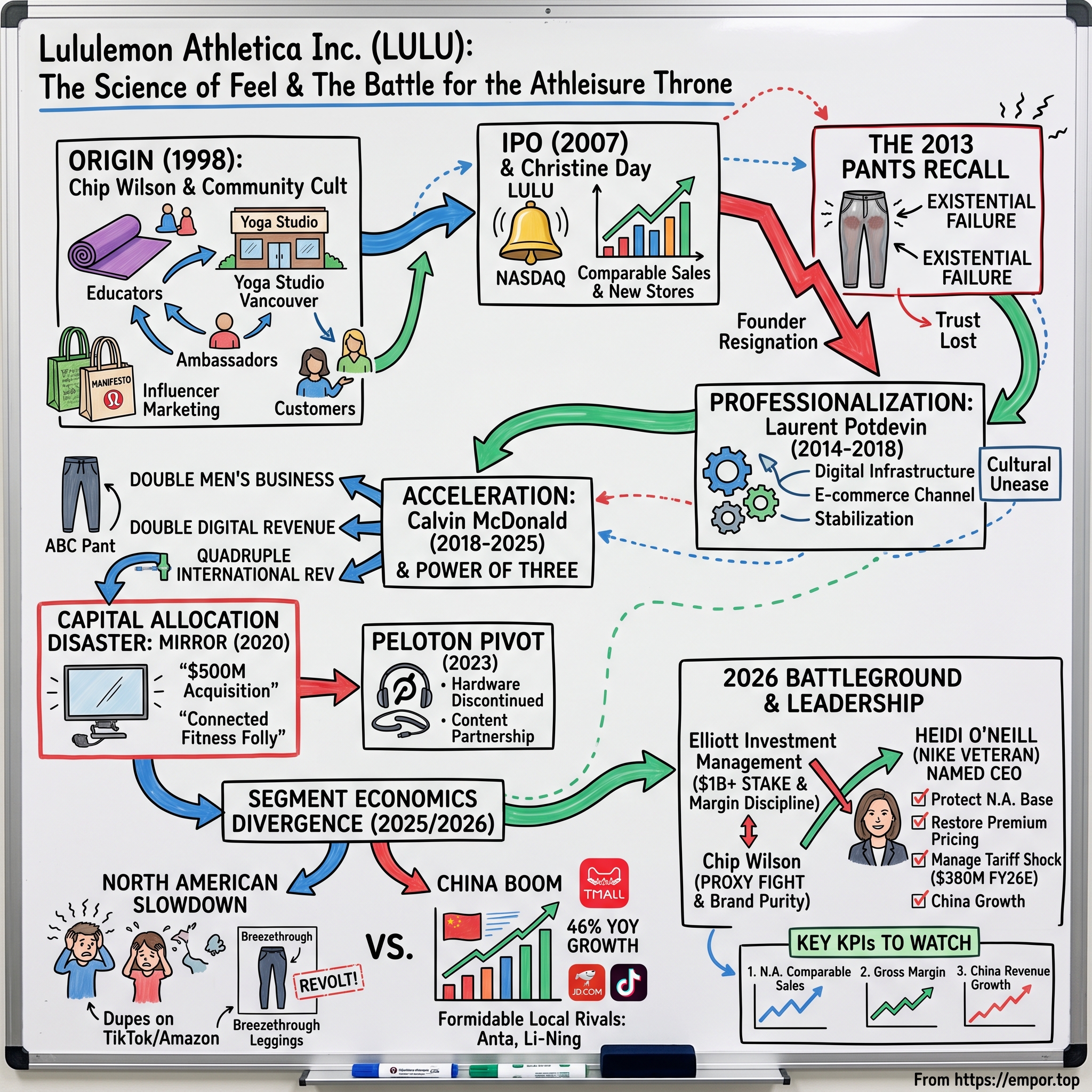

Walk into any Lululemon store on a Saturday morning and you will see something that looks nothing like retail. There is no hard-sell. There are no doorbuster signs. Instead, a rolled-up rack of yoga mats sits by the window, a chalkboard advertises a free community class at 8 a.m., and the staff — the company insists on calling them "educators," never salespeople — talk to you about your hip mobility before they talk to you about a pair of $128 leggings. For the better part of two decades, this was one of the most productive square footage in all of physical retail: a store that felt like a wellness clinic and printed money like a software company.

That is the first paradox worth sitting with. Lululemon built a roughly $11 billion revenue business selling stretchy black pants, and it did so while earning gross margins north of 56% — the kind of number you associate with branded pharmaceuticals or enterprise software, not apparel, where 40% is respectable and 50% is elite.1 It invented, or at least commercialized and named, an entire category: "athleisure," the idea that the clothes you sweat in and the clothes you live in could be the same clothes, and that you would happily pay a premium for the privilege.

But this is not a victory-lap story. This is a story caught at its most dangerous inflection point. By late 2025 and into 2026, the ultimate direct-to-consumer darling had become a corporate battleground. North American growth — the home market that made the brand — stalled. A blockbuster product launch was yanked from shelves within weeks after customers mocked its design. Longtime CEO Calvin McDonald announced his departure. The activist hedge fund Elliott Investment Management amassed a stake worth more than $1 billion and started agitating for change.2 Founder Chip Wilson, exiled from the boardroom a decade earlier, saw his opening and launched a proxy fight to reclaim influence over the company he built. And the board reached for an outsider — a Nike veteran named Heidi O'Neill — to steady the ship.3

So how did we get from that yoga studio in Vancouver to a boardroom knife fight? Over the next several sections, we will trace the arc: the community-led retail playbook that bypassed the entire advertising-industrial complex; the unit economics that made small stores absurdly productive; the $500 million capital-allocation disaster called Mirror; the China engine now doing much of the heavy lifting; and the 2026 activist showdown that will determine whether Lululemon's magic was durable or merely a moment. Let's start where every good origin myth starts — with a founder convinced everyone else was doing it wrong.

II. The Origin Story & Chip Wilson's Cult of Community (1998–2007)

Chip Wilson was already a veteran of the apparel wars when he wandered into a yoga class in Vancouver in the late 1990s. He had spent the 1980s and early 1990s building and eventually selling Westbeach, a surf-skate-snowboard streetwear brand, which meant he understood two things most retail founders don't: technical performance fabric, and youth subculture. What he noticed in that yoga class was a gap sitting at the intersection of both. The room was suddenly full — yoga participation was exploding — and yet the women practicing were wearing cotton dance attire and generic gym gear that went sheer when they bent over, held sweat, and sagged out of shape within weeks.

Wilson's instinct was not "let's make cuter workout clothes." It was closer to an engineering problem. He began experimenting with fabrics built around a high proportion of Lycra spandex, eventually landing on the blend he branded Luon — a material engineered to stretch four ways, wick moisture, resist odor, and hold a flattering shape under load. This was the seed of what the company would later brand, with characteristic swagger, the "Science of Feel." The pitch was that these were not clothes; they were technical equipment. You did not buy Lululemon the way you bought a T-shirt. You bought it the way a cyclist buys a helmet or a runner buys shoes — as performance gear where the specification actually mattered.

Whether the engineering was genuinely irreplicable or merely well-marketed is a question worth flagging early, because the entire premium pricing model rests on the answer. What's undeniable is that Wilson wrapped the product in a go-to-market strategy that was, for its time, radical. The dominant playbook in athletic apparel belonged to Nike: sign the world's greatest athletes to enormous endorsement contracts, buy Super Bowl ad inventory, and let aspiration trickle down from Michael Jordan to the weekend jogger. That model required hundreds of millions of dollars and a globally recognized logo before you sold a single shoe.

Wilson did the opposite. He had no money for LeBron, so he inverted the funnel. The first Lululemon location, which opened in Vancouver's Kitsilano neighborhood in 1998–2000, was designed as a shared space: a retail store by day, a yoga and community studio by night. Rather than pay celebrities, the company recruited local yoga instructors and fitness trainers as "ambassadors" — giving them free product in exchange for wearing it in front of their classes and feeding back detailed notes on fit and performance. The instructor, standing at the front of a room full of exactly the customer Lululemon wanted, became a walking, sweating, credible billboard. It was influencer marketing a decade before Instagram existed, and it cost almost nothing.

Then there were the bags. Lululemon printed its reusable shopping bags with a manifesto — cheerful, self-help-inflected, occasionally eyebrow-raising aphorisms about breathing, sunscreen, mediocrity, and living your best life. Customers carried these bags everywhere, turning grocery runs into brand impressions and seeding a slightly cult-like in-group identity. You either found the mantras inspiring or insufferable, and that polarization was the point: strong brands are built by the people who love them intensely, not by the people who are mildly okay with them.

The result was a company that grew through community density rather than advertising spend — building a fanatical base in one studio, one city, one ambassador at a time. It was slower than buying reach, but it was far stickier and far cheaper, and it produced customers who felt like members rather than shoppers. By the mid-2000s, with dozens of stores and a rabid following, Lululemon had proven the model worked. The obvious next question was whether it could survive contact with the public markets — and with the scrutiny that comes when a founder's personality is inseparable from the brand.

III. IPO to the Great Sheer Pants Recall & Founder Exit (2007–2013)

By 2007, Lululemon was ready to go public, and the leadership pairing that took it there is worth noting: Chip Wilson the visionary founder, and Christine Day the operator. Day had come from Starbucks, where she had spent years scaling a company that also sold an experience wrapped around a premium everyday product, and she was brought in to bring adult supervision to Wilson's creative chaos. In the summer of 2007, Lululemon listed on the NASDAQ under the ticker LULU, raising roughly $327 million in an offering that valued the still-small chain richly and gave it the capital to blanket North America with stores.4 The IPO was a coming-out party for the entire athleisure thesis, and for several years the stock did what the story promised — comparable sales ripped, new stores hit productivity targets fast, and Lululemon became a Wall Street darling.

Then came March 2013, and the single most on-the-nose product failure in the company's history.

Lululemon discovered that a substantial run of its signature black Luon yoga pants was defective in the most humiliating way imaginable: the fabric turned sheer when the wearer bent over, effectively becoming see-through under the exact conditions the pants existed to handle. The company pulled the affected products — around 17% of all women's bottoms in its stores — and issued a recall.5 For a brand whose entire premium was built on the promise that the fabric was superior, this was existential. It was not a fashion miss; it was a failure of the core technical claim. The financial damage ran to tens of millions of dollars in lost revenue and inventory write-offs, and management slashed its outlook.5 But the reputational damage was worse, because it invited a question the brand could not afford: if we're paying triple the price for the technology, and the technology fails, what exactly are we paying for?

Management might have survived the fabric problem with a clean apology. Instead, the crisis metastasized because of Chip Wilson himself. In a November 2013 television interview, asked about complaints that the pants pilled and went sheer, Wilson suggested the problem was not the product but the customers — remarking that "some women's bodies just actually don't work" for the pants, and pointing to thigh friction as the culprit.6 The comment detonated. It read as the founder blaming women's bodies for his company's manufacturing defect, and it violated the intimate, aspirational trust the brand had spent fifteen years cultivating with exactly those women.

The fallout was swift and structural. Christine Day, who had already signaled her intent to step down amid the recall fallout, exited as CEO. And in December 2013, Chip Wilson resigned as non-executive chairman of the board, apologizing for his remarks.6 The founder whose personality was the brand had become a liability to it. He retained a large ownership stake — which would matter enormously more than a decade later — but his operational grip was broken.

The episode revealed something durable about Lululemon's risk profile that still applies today. The brand's greatest strength, an almost religious customer trust in product superiority, is also its greatest fragility: a single visible defect or tone-deaf message can inflict damage far out of proportion to the immediate financial cost, because the entire premium depends on the customer's faith that Lululemon simply does not get this wrong. Keep that dynamic in mind, because the company was about to spend the next decade learning it over and over. First, though, it needed a leader who could professionalize the business without a founder looking over his shoulder.

IV. The Laurent Potdevin Era: Growth and Cultural Misalignment (2014–2018)

In January 2014, with the founder freshly gone from the chairmanship and the brand still nursing its wounds, the board turned to Laurent Potdevin. A French-born executive who had run the snowboard brand Burton and served as president of Toms Shoes, Potdevin was hired to do the unglamorous work: build out digital infrastructure, professionalize supply chain and merchandising, expand internationally, and generally turn a founder-led cult brand into a scalable global corporation.7

On the numbers, the Potdevin era delivered. E-commerce, which had been an afterthought, became a genuine channel. The store base expanded steadily across North America and pushed further into international markets. Revenue and profitability climbed through the mid-2010s, and the sheer-pants trauma faded from the headlines as new product and new stores did their work. If you judged the period purely by the financial statements, it looked like a successful stabilization — proof that the brand equity Wilson built could survive its founder's departure and keep compounding under professional management.

But underneath the growth ran a current of unease. The grassroots, community-first ethos — the ambassador dinners, the studio-in-the-store intimacy, the sense that Lululemon was run by yoga people rather than apparel executives — was harder to preserve at scale, and longtime devotees sensed a dilution of the culture that had made the brand feel special. That tension between financial scaling and cultural authenticity is a recurring theme in premium consumer brands, and Lululemon was not immune.

Then, in February 2018, the Potdevin era ended as abruptly as it began. The board announced his immediate resignation, stating plainly that he had fallen short of the company's standards of conduct — reporting related to relationships and behavior deemed inappropriate for the workplace.8 There was no long goodbye and no face-saving transition. It was the second time in five years that a Lululemon CEO had exited under a cloud, and the second time the company had to prove that its brand was bigger than the person running it.

What's notable — and genuinely says something about the durability of the underlying business — is how little the stock and the operations flinched. The board installed executive chairman Glenn Murphy, the former Gap chief, to steady governance, and the machine kept running while the search for a permanent CEO proceeded.8 A brand that could lose two chief executives to scandal within five years and still compound suggested the asset itself — the customer relationship, the product, the store economics — was more resilient than any individual leader. The next CEO would take that resilient asset and, for a while, make it look unstoppable.

V. The Calvin McDonald Era: "Power of Three" and Global Domination (2018–2025)

Calvin McDonald arrived in August 2018 carrying a résumé purpose-built for the moment. A Canadian who had run Sephora Americas and, before that, Sears Canada, he understood both the theater of premium specialty retail and the discipline of operating at scale.9 Where Potdevin's mandate had been stabilization, McDonald's was acceleration — and within months he gave Wall Street a framework crisp enough to fit on a slide and ambitious enough to move the stock.

He called it the "Power of Three." The plan set three concrete five-year targets by 2023: double the men's business, double the digital (e-commerce) business, and quadruple international revenue.9 The genius of the framework was that it converted a vague "we'll grow" into three specific, testable promises against which management could be held accountable — a discipline that, as we'll see, matters enormously when judging management credibility.

The men's story is the cleanest proof point, because it required solving a real problem: men associated Lululemon with women's yoga pants and largely stayed away. The company's answer was to re-engineer its fabric technology into products men would actually buy without embarrassment. The centerpiece was the ABC pant — the acronym cheekily stands for "Anti-Ball Crushing," a piece of copywriting that told male customers, in language they'd remember, that the pants were engineered for comfort in a specific and personal way. Paired with the Commission trouser and a growing base of technical shirts, Lululemon cracked a demographic that had resisted it for two decades, turning menswear from a rounding error into a genuine growth vector.

The digital story got an enormous, unearned assist. When COVID-19 shuttered stores in 2020, Lululemon's direct-to-consumer engine — already built out under Potdevin and supercharged under McDonald — absorbed demand that would otherwise have walked into locked stores. More importantly, the pandemic was a structural tailwind for the entire product category: a world working from home and exercising at home wanted exactly what Lululemon sold — comfortable, functional, presentable clothing you could take a Zoom call in and then go for a run. Direct-to-consumer sales, which management had targeted merely doubling, came to represent well over 40% of total revenue in the early 2020s, and the brand rode the athleisure wave to record results.10

By 2022, with the first Power of Three essentially achieved ahead of schedule, McDonald doubled down — literally. He unveiled "Power of Three x2," a plan to double the company's 2021 revenue of roughly $6.25 billion to $12.5 billion by 2026, again anchored on doubling men's, doubling digital, and quadrupling international off the new, higher base.10 It was a bold, specific, public commitment, and for a couple of years the trajectory looked plausible. Holding it up against reality in 2026 — where revenue reached about $11.1 billion, growth had slowed to mid-single digits, and North America had stalled — tells you a great deal about how the story curdled.1 The target wasn't reckless when set; it was extrapolation from a genuine boom. But it locked management into a growth narrative just as the tailwinds that produced the boom were about to reverse.

The clearest early sign that McDonald's team could confuse a pandemic sugar high for permanent demand came not from apparel at all. It came from a mirror.

VI. Capital Deployment & M&A Blunder: The Mirror Fiasco and Peloton Pivot (2020–2023)

In June 2020, three months into the pandemic, with connected-fitness stocks soaring and Peloton the hottest name in consumer hardware, Lululemon announced it would acquire Mirror — a startup that sold a $1,495 wall-mounted screen streaming live and on-demand workout classes — for $500 million.11 The logic, articulated with real conviction at the time, was seductive. Lululemon had the customer, the sweat, and the community; Mirror had the hardware and the content platform. Bolt them together and Lululemon could own the customer's entire fitness life — sell them the leggings, the class, and the subscription — building a recurring-revenue digital ecosystem that would justify a higher valuation multiple.

It was, in retrospect, a textbook case of buying the top. The entire thesis rested on the assumption that the pandemic's shift toward at-home connected fitness was permanent rather than a temporary artifact of locked gyms. It was not. As vaccines rolled out and gyms and studios reopened, consumer appetite for expensive fitness hardware collapsed. Peloton — the far larger, far better-funded incumbent Lululemon was implicitly betting against — cratered spectacularly, taking the credibility of the whole category down with it. Mirror faced brutal customer-acquisition costs, a saturated market, and a product that looked increasingly like a pandemic novelty.

The pattern was not unique to Lululemon, which is worth stating because it tempers the temptation to call this a singular act of folly. Under Armour had paid roughly $475 million for the calorie-tracking app MyFitnessPal in 2015, struggled to monetize it, and eventually sold it in 2020 for a fraction of that price.12 Nike had launched, then quietly shuttered, its FuelBand wearable-hardware effort years earlier. The connected-fitness and wearables graveyard was already well populated by the time Lululemon walked in. The recurring lesson: apparel and footwear brands repeatedly overestimate their ability to translate brand love into stickiness in consumer technology, a fundamentally different business with different competencies, cost structures, and competitive dynamics.

The reckoning came in stages. In its results for the fiscal year ended January 2023, Lululemon recorded a $442.7 million post-tax impairment charge against Mirror, writing down essentially the entire value of the acquisition — an admission, in accounting terms, that $500 million of shareholder capital had largely evaporated in under three years.13 Then, in September 2023, the company engineered its exit with a face-saving pivot: rather than keep bleeding on hardware, Lululemon struck a five-year partnership with — of all companies — Peloton. Lululemon would discontinue Mirror hardware sales and migrate its digital subscribers onto Peloton's content platform, while Peloton became the exclusive digital fitness-content partner for Lululemon and Lululemon became Peloton's primary athletic-apparel partner.14 The one-time rivals essentially agreed to swim in their own lanes: Peloton would handle content, Lululemon would handle clothes.

For investors, the Mirror episode is the single most important test of management's capital-allocation judgment in this era, and it should be weighed honestly against the operational wins of the Power of Three. It demonstrated a willingness to chase a hot narrative with a large check at precisely the wrong moment, and to conflate a temporary demand spike with a durable structural shift — the same error, arguably, embedded in the aggressive x2 revenue target. To management's credit, it cut its losses relatively quickly rather than throwing good money after bad, and the Peloton deal was a reasonably graceful surrender. But the affair left a lasting question about whether the discipline the brand showed in product would extend to the balance sheet. That question would return with a vengeance when an activist showed up. First, though, the growth story had shifted decisively to the other side of the Pacific.

VII. Segment Economics: China Boom vs. North American Slowdown

To understand Lululemon in 2026, you have to hold two opposing pictures in your head at once. In the fiscal year ended February 1, 2026 — FY2025 in the company's calendar — Lululemon generated about $11.1 billion in net revenue, up roughly 5% year over year, at a full-year gross margin of 56.6% and an operating margin near 20%.1 Those remain, in absolute terms, exceptional numbers for an apparel company. But the headline growth rate — mid-single digits for a business that not long ago promised to compound its way to $12.5 billion — masks a violent divergence beneath the surface. One geography is stalling; another is on fire.

Start with the trouble at home. North America, the market that made Lululemon and still supplies the majority of its revenue, slowed sharply. Part of the cause was macro — a value-conscious consumer trading down. But part was self-inflicted, and management largely admitted as much on earnings calls: misjudged color and fashion assortments, gaps in newness, and a sense that the brand had lost a step in giving core customers reasons to keep buying. Into that opening rushed a new generation of well-funded premium rivals — Vuori with its softer, more casual aesthetic, and Alo Yoga with its fashion-forward studio-to-street positioning — alongside a flood of cheap "dupes" on TikTok and Amazon offering leggings that looked identical for a quarter of the price.

The most vivid symbol of the North American stumble arrived in July 2024, with the Breezethrough leggings. Lululemon launched the line with fanfare as a hot-weather performance product, featuring a distinctive back seam and cutout design meant to improve ventilation. Customers took one look and revolted, mocking the seam placement online — the widely circulated complaint was that it created an unflattering "whale-tail" effect — and within weeks Lululemon pulled the entire line from stores and its website.15 Management characterized it on its earnings call as a "test-and-learn" moment, a phrase that landed as a euphemism for a self-inflicted wound. Coming from a company whose whole premium rests on never getting the product wrong, it echoed the sheer-pants trauma of 2013: a reminder that the brand's fragility to visible product missteps is not a historical footnote but a live, recurring risk.

Now flip to the other picture. While North America wobbled, Mainland China accelerated at a pace that would make a startup blush. In the third quarter of fiscal 2025, Lululemon's China Mainland net revenue grew roughly 46% year over year, reaching about $465 million and representing on the order of 18% of total net revenue — up from a rounding error a few years earlier.16 The Chinese premium consumer, it turned out, was exactly the customer Lululemon was built for: aspirational, wellness-oriented, willing to pay for status-signaling technical apparel, and reachable through a sophisticated digital ecosystem. The company built premium flagship presences on native platforms — 天猫 Tmall and 京东 JD.com for e-commerce — and leaned into social commerce through 抖音 Douyin, the domestic sibling of TikTok, to drive discovery and demand.

But China is not a free lunch, and the bull case there requires a clear-eyed look at the competition. Lululemon is expanding into the home turf of formidable, well-capitalized local champions — 安踏体育 Anta Sports, which owns a portfolio of sportswear brands and out-earns Nike in China, and 李宁 Li-Ning, the homegrown brand with deep cultural resonance and aggressive premium ambitions. These players understand Chinese consumers, distribution, and 国潮 guochao (national-pride) branding better than any foreign entrant. Layer on the ever-present risk of shifting consumer sentiment toward domestic brands, regulatory unpredictability, and macro softness, and the 46% growth rate is best read as spectacular but not guaranteed to persist.

The investment takeaway from the segment split is stark. Lululemon is increasingly a story of one mature, high-margin, and now-vulnerable home market being propped up by one fast-growing but geopolitically exposed foreign one. That is a very different, and riskier, business than the all-conquering North American juggernaut of 2021 — and it is precisely the vulnerability that drew a $1 billion predator to the door.

VIII. The 2025/2026 Battleground: Elliott's $1B Stake, CEO Sudden Exit, & the Rise of Heidi O'Neill

For most of 2025, the pressure built quietly — a soft quarter here, a margin miss there, a stock sliding from its 2023 highs. Then, in a matter of weeks around the turn of 2026, it all broke at once, and Lululemon went from a slowing growth story to a full-blown corporate control drama.

The first shock was the CEO. Calvin McDonald, the architect of the Power of Three and the face of Lululemon's global ascent, announced in December 2025 that he would step down, effective January 2026 — an abrupt end after seven years, against a backdrop of stalled North American execution and compressing margins.2 For a company that had already lost two CEOs to scandal, this was a different kind of departure — not misconduct, but a growth story that had run out of road — yet it opened the same kind of leadership vacuum.

Into that vacuum stepped Elliott Investment Management, one of the world's most feared activist funds. In mid-December 2025, reports confirmed Elliott had built a stake worth more than $1 billion, instantly making it one of Lululemon's largest shareholders.2 Elliott's playbook and thesis were legible: here was a world-class brand — a genuine moat — that had been mismanaged operationally, with sloppy product execution, an over-reliance on markdowns that was corroding the premium positioning, and insufficient margin discipline in the face of mounting tariff costs. Crucially, Elliott did not just criticize; it came with a candidate, reportedly favoring veteran retail executive Jane Nielsen, the former CFO and COO of Ralph Lauren, as a potential CEO.2 The message to the board was unmistakable: you have a broken engine bolted to a beautiful chassis, and we intend to have a say in who fixes it.

Then came the ghost of the founding. Chip Wilson, still one of the company's largest individual shareholders more than a decade after his boardroom exile, seized the moment of maximum instability to launch his own campaign — nominating a slate of directors and pressing publicly for a return to the brand's hardcore technical-performance roots, his long-standing critique that the company had drifted toward fashion and away from the elite athletic identity he built.17 Suddenly the board faced a two-front war: a professional activist demanding operational rigor on one flank, and an aggrieved founder demanding a cultural restoration on the other, with the two agendas overlapping in their criticism of the incumbent regime but pointing in different strategic directions.

The board's answer came on April 22, 2026. Rather than hand the keys to Elliott's candidate or Wilson's vision, it reached across the industry's biggest rival and hired Heidi O'Neill, who had spent more than 25 years at Nike, most recently as President of Consumer, Product and Brand — arguably the second-most-powerful operating role at the world's largest athletic brand.3 O'Neill would take office on September 8, 2026, and join the board, while CFO Meghan Frank and executive André Maestrini steered the company as interim co-CEOs through the transition.3 The market's initial reaction was notably cool — the stock sold off on the news, a "vote of no confidence" in the sense that investors had hoped for a cleaner, faster resolution rather than a five-month gap before a Nike insider took the wheel.3

O'Neill's mandate is brutally clear and internally somewhat contradictory. She must protect and reignite the core North American retail base; restore premium pricing power by weaning the company off the promotional markdowns that Elliott blames for eroding margins; navigate a tariff shock that hammered Q4 FY25 gross margin by roughly 520 basis points and threatens to push gross tariff costs from about $275 million in fiscal 2025 toward $380 million in fiscal 2026; and keep the China engine humming — all while satisfying an activist demanding margin discipline and a founder demanding brand purity.18 Whether a lifelong Nike executive can restore a brand whose entire identity was built as the anti-Nike is the central bet of the next chapter, and the market is right to withhold judgment until the results arrive.

IX. Playbook: Durable Business & Investing Lessons

Step back from the drama, and Lululemon offers a genuinely instructive set of business lessons — some about what built the moat, and some cautionary tales about how a great business gets itself into trouble.

The first and most durable lesson is the anti-Nike marketing model. Lululemon proved that in the right category, an organic, local, ambassador-driven marketing funnel could out-leverage hundreds of millions in celebrity endorsement spend. By seeding product with the trusted authority figures in a customer's own life — the yoga instructor, the studio owner, the run-club leader — the company generated credibility that no televised ad could buy, at a fraction of the cost. This kept marketing expense low relative to revenue and, more importantly, produced customers who arrived pre-sold by someone they trusted. The catch, visible in 2026, is that this model works best when the brand is the insurgent underdog; at $11 billion in revenue and with rivals running the identical playbook, the grassroots edge is harder to sustain.

The second lesson is pricing power through niche technical premium. Lululemon convinced customers that its fabrics — Luon, and later Nulu, Everlux, and Luxtreme — were performance equipment rather than commodity apparel, and that framing supported gross margins roughly 10 to 15 points above traditional apparel peers.1 The strategic insight is that a functional, sensory product benefit ("this feels different, this performs when I train") justifies a durable premium in a way that pure fashion — which is fickle and endlessly copyable — never can. The vulnerability is that the premium is only as real as the customer's belief in the performance gap, which the rise of high-quality dupes is actively testing.

The third lesson is the store-led hub model. Lululemon kept its stores relatively small but extraordinarily productive, and increasingly blended physical and digital by using stores to fulfill online orders and serve as community anchors rather than mere transaction points. Small, dense, high-turnover stores generate strong sales per square foot and low occupancy cost relative to revenue, while doubling as marketing and fulfillment infrastructure — a capital-efficient footprint that traditional big-box apparel retail could never match.

And the fourth lesson is the cautionary one, drawn from the wreckage: the pitfalls of ad-hoc extension beyond the core competency. The Breezethrough leggings showed the danger of chasing fashion novelty at the expense of the product credibility that underwrites the premium. Mirror showed the far more expensive danger of entering an entirely different business — consumer hardware — on the assumption that brand love transfers across categories. Both stem from the same root error: forgetting that the moat is narrow and specific, and that every step away from "technical apparel the customer trusts" is a step onto thinner ice. The best businesses know exactly what they are; Lululemon's troubles have consistently come when it forgot. To judge whether the moat is truly durable, it helps to run it through two rigorous frameworks.

X. Strategic Frameworks: Helmer's 7 Powers & Porter's 5 Forces

Business strategist Hamilton Helmer's "7 Powers" framework asks a simple, brutal question of any company: what, precisely, stops a competitor from replicating your success and competing away your profits? Running Lululemon through it separates the real moat from the marketing.

The primary power is Brand. This is the heart of the case. The red logo functions as a social and psychological badge — a signal of a certain aspirational, health-conscious identity — that creates genuine willingness to pay a premium for what is, at a molecular level, stretchy fabric. Brand power of this kind is real and valuable, but it is also affective and defensible only through relentless consistency; every sheer-pants recall and Breezethrough misfire is a direct assault on it, which is why the company's product missteps are strategically graver than they look.

The second power is a Cornered Resource, and here Lululemon's claim is moderate rather than decisive. The company points to its portfolio of proprietary, engineered fabrics and its tightly integrated supply chain of specialized mills, plus the accumulated network of local brand ambassadors. These are genuine assets, but "proprietary fabric" is a softer moat than a patent on a molecule — the dupe economy exists precisely because competitors can source materials that are good enough to satisfy most customers most of the time.

The third power, Scale Economies, is likewise moderate. Lululemon's sourcing scale gives it real cost advantages with global fabric mills and manufacturing partners, but that same concentrated Asian supply chain is exactly what makes it acutely vulnerable to tariffs and geopolitics — a scale advantage in normal times that becomes a scale liability when trade policy turns hostile, as the FY2025 tariff hit demonstrated.

The fourth power, Switching Costs, is weak in the literal sense — nothing physically stops a customer from buying a competitor's leggings tomorrow — but stronger psychologically. Loyal customers harbor a real fear that a cheaper "dupe" won't perform identically under intense training, or won't fit the way they've come to rely on, and that performance anxiety is a soft but genuine retention mechanism. It is not a contract; it is a habit and a hesitation, and habits erode.

Now Michael Porter's Five Forces, which war-games the competitive landscape. The Threat of New Entrants is high and rising: activewear has low barriers to entry, and the last decade produced a wave of premium, VC-backed challengers — Vuori and Alo Yoga most prominently — plus an effectively infinite supply of low-cost dupes. The Bargaining Power of Buyers is moderate-to-high: consumers face endless alternatives and near-zero cost to defect, which is precisely why Lululemon cannot afford a single high-profile product defect. And the Intensity of Rivalry is high and structural — a permanent innovation arms race against a global titan in Nike on one side and nimble, fashion-forward premium upstarts on the other, all fighting for the same aspirational customer. The Threat of Substitutes and Supplier Power round out the picture as more moderate forces, but the top-line reading is clear: Lululemon sits in an attractive category that its own success has made intensely competitive. Which is the perfect setup for weighing the bull and bear cases directly.

XI. Bull vs. Bear Case and Risk Radar

Every contested stock is an argument, and Lululemon in 2026 is a genuinely two-sided one. Let's steel-man both.

The bull case rests on three pillars. First, the brand moat is real and the core customer remains intensely loyal — even after the stumbles, Lululemon still commands pricing roughly double that of standard athletic apparel, and the gross margins prove customers keep paying it.1 Second, the international frontier, and China specifically, represents a large, highly profitable growth runway that can plausibly offset a maturing North America for years; a business growing a major geography at 46% is not a business out of options.16 Third, the incoming leadership is elite — Heidi O'Neill brings decades of Nike's global scaling, product-engine, and brand-management expertise precisely where Lululemon has been weakest, in operational rigor and disciplined product pipelines.3 The bull's synthesis: this is a world-class brand having an execution problem, not a demand problem, and execution problems are fixable with the right operator and an activist forcing discipline.

The bear case is equally coherent. First, margin erosion is structural, not transitory: the loss of the U.S. de minimis exemption and escalating tariffs hammered Q4 FY25 gross margin by roughly 550 basis points, with tariffs alone accounting for about 520 of them, and those costs are set to climb further in fiscal 2026.18 A company that sources heavily from Asia and sells heavily into a tariff-happy America faces a persistent headwind that no amount of brand love fully offsets. Second, and more corrosive, is the dupe threat to the moat itself: if a generation of Gen Z and younger millennial shoppers concludes that a $30 legging is 90% as good as a $120 one, the premium — the entire business model — deflates, and there is real evidence this erosion is underway. Third is transitional turbulence: a five-month CEO gap, an activist demanding change, and a founder waging a proxy war constitute a genuine distraction tax on an organization that needs to be executing flawlessly precisely when it is least able to.

The activist stress test sharpens the bear view. A skeptic would point directly at capital allocation — the $500 million Mirror write-off as Exhibit A that management chased narratives with shareholder money — and at the markdown creep that traded long-term brand equity for short-term sales, and at a board that presided over a stalling core market while setting a $12.5 billion target it was never going to hit. Elliott's presence is, in effect, the market's judgment that these are real governance and discipline failures, not bad luck.

On the risk radar, the material threats are concrete and mechanical rather than generic. Demand risk: is the North American consumer's cooling cyclical or a permanent brand-relevance problem? Trade/geopolitical risk: tariffs on the supply side, and rising Chinese economic nationalism on the demand side, are twin exposures baked into the business model. Competitive/technology risk: the dupe economy, amplified by social media, is a genuine structural threat to premium positioning. And execution risk: the entire bull case is a bet on a leadership transition landing cleanly, which is far from assured.

Which brings us to what actually matters to watch. Amid all the noise, three KPIs tell the story. First, North American comparable sales — the single cleanest read on whether the core market has stabilized or is still deteriorating. Second, gross margin — the direct gauge of whether pricing power is holding and tariff mitigation is working, or whether the premium is bleeding out through markdowns and trade costs. And third, China Mainland revenue growth — the proof of whether the primary growth engine can keep running without hitting a regulatory, competitive, or consumer speed bump. Track those three, and you will know whether the turnaround is real long before the narrative catches up.

XII. Epilogue & Outro

Lululemon's story is, at bottom, a demonstration that the seemingly unassailable giants of an industry can be disrupted from a yoga studio — that community, a sensory product edge, and a small, dense store footprint could carve out a durable, high-margin position against a Nike that outspent it a hundred to one on marketing. For two decades, the "Science of Feel" and the red logo did something rare in apparel: they made a commodity feel irreplaceable, and they charged for it accordingly.

But the same story, told honestly, is a lesson in how quickly high-margin magic can turn fragile at scale. Past roughly $11 billion in revenue, the tailwinds that built the company — the athleisure boom, an underserved premium customer, an insurgent's underdog energy — have matured or reversed, while the vulnerabilities have compounded: a moat under assault from dupes, a supply chain exposed to a trade war, a core market losing a step, and a governance structure now contested by both an activist and its own estranged founder. The very product perfectionism that made the brand also made it brittle, and the last decade is littered with the evidence — sheer pants, a whale-tail seam, a $500 million mirror.

So the question that hangs over the next chapter is genuinely open, and worth resisting the urge to answer prematurely. Can Heidi O'Neill take the very Nike playbook that Lululemon was founded to reject — operational discipline, global scale, a relentless product engine — and use it to stabilize North America, restore the premium, satisfy Elliott, outlast Chip Wilson, and keep China compounding? If she succeeds, Lululemon reclaims its place as the definitive athleisure franchise and the disruption thesis proves durable. If she fails, it becomes a cautionary tale about a brand that confused a moment for a moat. The evidence to decide between those futures will show up, quarter by quarter, in three numbers — and the market, for now, is right to wait and watch.

References

-

lululemon athletica inc. Announces Fourth Quarter and Full Year Fiscal 2025 Results — Business Wire, 2026-03-17 ↩↩↩↩↩

-

Activist investor Elliott builds over $1 billion stake in Lululemon, puts forth CEO candidate — CNBC, 2025-12-18 ↩↩↩↩

-

Lululemon names former Nike exec Heidi O'Neill as next CEO — BNN Bloomberg, 2026-04-22 ↩↩↩↩↩

-

Lululemon Annual Reports and SEC Filings Archive — Lululemon Athletica Inc. ↩

-

Lululemon SEC EDGAR Filings (CIK 1397187) — SEC EDGAR Database ↩↩

-

Lululemon Investor Relations Portal — Lululemon Athletica Inc. ↩

-

Lululemon Media Press Release Center — Lululemon Athletica Inc. ↩↩

-

Lululemon Results Center (Quarterly Earnings) — Lululemon Athletica Inc. ↩↩

-

Lululemon SEC EDGAR Filings (CIK 1397187) — SEC EDGAR Database ↩↩

-

Lululemon to discontinue Mirror as it teams up with Peloton — Retail Dive, 2023-09-27 ↩

-

Financial Times Retail & Consumer Industries — Financial Times ↩

-

Lululemon's ill-timed Mirror acquisition is now almost worthless — Yahoo Finance, 2023 ↩

-

Peloton shares soar on digital content, apparel partnership with Lululemon — CNBC, 2023-09-27 ↩

-

The Wall Street Journal Business Section — Wall Street Journal ↩

-

Lululemon grows on China market strength — China Daily, 2026-03-26 ↩↩

-

Investor Outlook: Elliott's US$1-billion stake sharpens focus on Lululemon — BNN Bloomberg, 2025-12-18 ↩

-

Lululemon Beats Q4 Estimates on Revenue and EPS, but Margin Erosion and Tariff Costs Cloud the Path Forward — MLQ.ai, 2026-03-17 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube