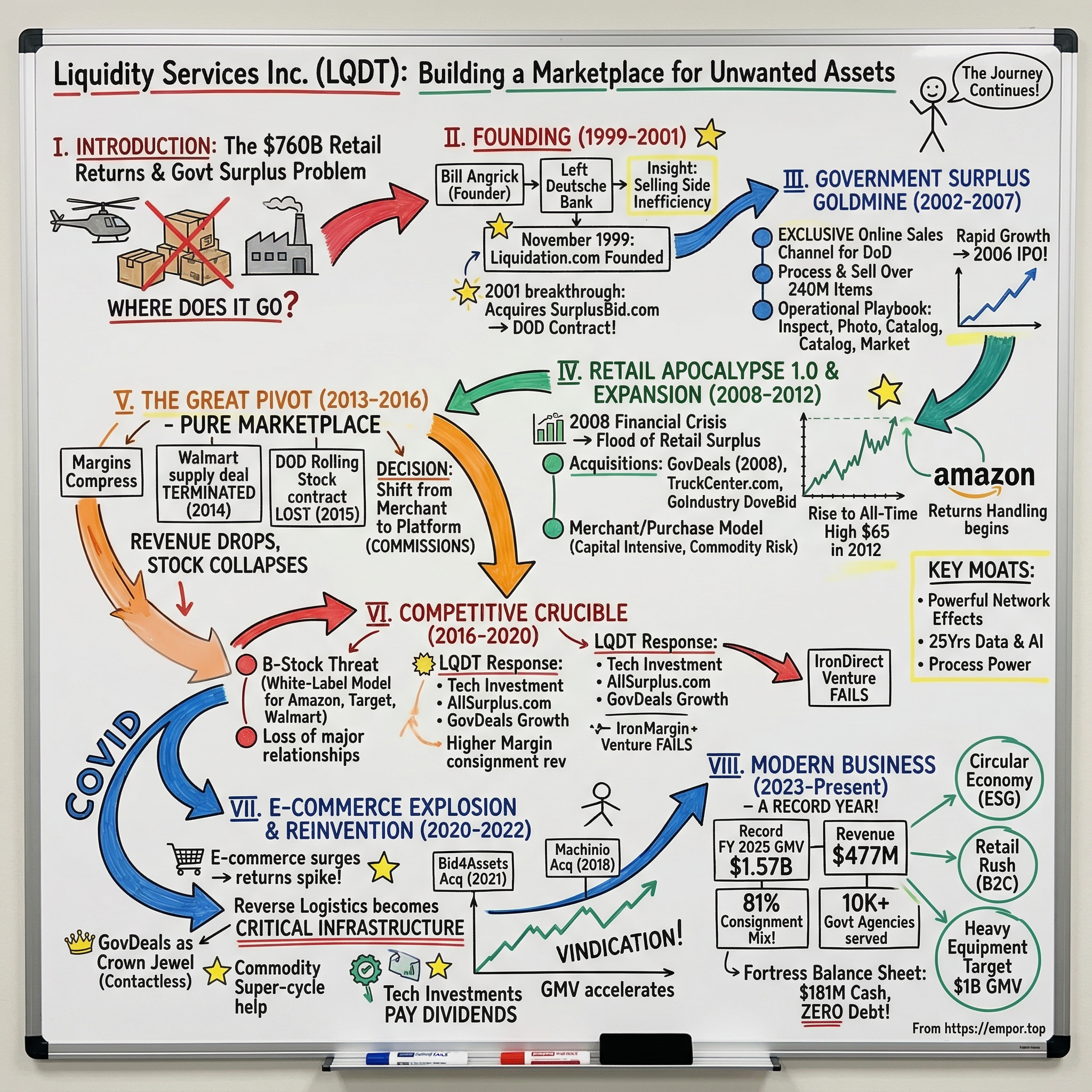

Liquidity Services Inc. (LQDT): The Story of Building a Marketplace for the World's Unwanted Assets

I. Introduction & Episode Roadmap

What do government surplus helicopters, returned Amazon goods, and bankrupt retailer inventory have in common? They all need to go somewhere. And for more than a quarter century, one company has been quietly building the infrastructure to make that happen: Liquidity Services, ticker LQDT on the NASDAQ.

Here is a business that most investors have never heard of, yet it sits at the center of one of the most essential and underappreciated problems in modern commerce: what happens to stuff nobody wants anymore. Every year, American retailers alone deal with roughly $760 billion in returned merchandise. The U.S. Department of Defense generates mountains of surplus equipment, from office chairs to decommissioned vehicles. Bankrupt companies leave behind warehouses full of inventory. Municipalities auction off everything from police cruisers to seized real estate. All of this unwanted, surplus, returned, or obsolete material needs to find a new owner, and doing that efficiently at scale turns out to be an extraordinarily difficult problem.

Liquidity Services, founded in 1999, has been attacking this problem since the earliest days of the commercial internet. The company has survived the dot-com crash, the 2008 financial crisis, the loss of its largest commercial client, a painful multi-year business model transformation, a stock price decline of more than ninety percent from peak, and a global pandemic. Through it all, founder and CEO Bill Angrick has remained at the helm, steering the company through what amounts to one of the longest and most deliberate strategic pivots in recent public company history.

Today, LQDT operates as a marketplace platform generating nearly $1.6 billion in gross merchandise value annually, with close to $480 million in revenue, roughly $60 million in adjusted EBITDA, zero debt, and over $180 million in cash on the balance sheet. The stock trades around $32 per share, giving the company a market capitalization near $950 million. It has recovered more than tenfold from its COVID-era low of $3.06 in March 2020, yet remains roughly half of its all-time high from 2012.

Think about that for a moment. A company that has been publicly traded since 2006, that processes billions of dollars in transactions annually, that serves over ten thousand government agencies and millions of registered buyers worldwide, and that operates the largest online marketplace for surplus and returned goods in the United States, trades at a market cap below a billion dollars. For context, Copart, which operates a similar marketplace model for damaged vehicles, trades at over $50 billion. The difference is not just scale; it is visibility. Copart is covered by dozens of analysts. Liquidity Services is followed by a handful.

The LQDT story is not a tale of explosive hypergrowth or Silicon Valley mythology. It is something arguably more instructive: a case study in building durable infrastructure in an unsexy vertical, making the gut-wrenching decision to sacrifice short-term revenue for long-term positioning, and the compounding power of network effects in a two-sided marketplace. This is a story about patience, about marketplace dynamics, and about what happens when you do one hard thing really well for a very long time.

II. Founding Context & The Surplus.com Origin Story (1999-2001)

In the late 1990s, a young investment banker named William P. Angrick III was sitting in the offices of Deutsche Bank Alex. Brown in Washington, D.C., covering the consumer and business services sector. His job put him at the intersection of two powerful forces: the exploding e-commerce revolution and the staggering inefficiency of how large organizations disposed of assets they no longer needed.

Angrick held an MBA from Northwestern's Kellogg School of Management and a business degree with honors from Notre Dame. He was a CPA. He was methodical, analytical, and deeply interested in marketplace business models. And what he saw from his perch in investment banking was a gap so large it seemed almost absurd.

The B2B marketplace fever of the late 1990s was at full pitch. Companies like Ariba, CommerceOne, and FreeMarkets were attracting billions in market capitalization on the promise of digitizing business-to-business procurement. Everyone was focused on the buying side of the equation. But Angrick's insight was different: what about the selling side? Specifically, what about the trillions of dollars in surplus, obsolete, and returned goods that large organizations desperately needed to move, but had no efficient way to do so?

The U.S. government was the most glaring example. The Department of Defense alone was generating enormous volumes of surplus material, from office equipment to vehicles to industrial machinery. The traditional process for disposing of this stuff involved regional auctions, paper catalogs, and a network of middlemen who bought at deep discounts and resold for profit. The sellers, usually government agencies, captured a tiny fraction of the residual value. The process was slow, opaque, and riddled with inefficiency.

In November 1999, Angrick left Deutsche Bank and founded Liquidation.com with $100,000 of his own savings. He recruited co-founder Jaime Mateus-Tique, a former senior engagement manager at McKinsey & Company, along with co-founder Ben Brown. The thesis was elegant: build an online auction marketplace that could aggregate surplus from large organizations, present it to a global buyer base, and use competitive bidding to maximize recovery value for sellers while giving buyers access to deals they could never find otherwise.

In January 2000, the team opened their first office on K Street in Washington, D.C., in space subleased from Al Gore's presidential campaign headquarters. They had six employees. The combination of backgrounds was deliberate and complementary: Angrick brought investment banking rigor and financial modeling expertise; Mateus-Tique brought McKinsey's structured problem-solving approach and operational discipline. Together, they had both the strategic vision and the execution muscle that most dot-com-era startups lacked.

Their timing seemed terrible: the dot-com bubble was months from popping. But the timing was actually perfect, for a reason that would become clear only in hindsight.

The company's first notable transaction was a $200,000 sale of the George T. Bagby, a marine vessel for Georgia's Natural Resources department. But the real breakthrough came in 2001, when Liquidity Services acquired SurplusBid.com, a small company that happened to hold a contract with the United States Department of Defense. That acquisition was transformative. It gave a tiny startup exclusive access to the single largest generator of surplus property in the world.

Here is why the timing mattered: while hundreds of B2B marketplaces were imploding because they had no real revenue model, no real customers, and no real assets moving through their systems, Liquidity Services had something tangible. It was moving physical goods for the U.S. military. The dot-com crash was devastating for companies built on advertising revenue and page views. But a company that was actually selling things, taking commissions, and serving the federal government had a revenue anchor that most startups could only dream of. Board member Patrick Gross, who joined in 2001, later recalled that revenues were still under $1 million when he came aboard. By 2002, barely three years after founding, the company had reached $72 million in annual sales and achieved profitability.

That trajectory, from sub-million revenue to profitable at $72 million in under three years, is remarkable by any standard. But it also established a pattern that would define the company for decades: Liquidity Services was not flashy, but it was real. It moved real goods, served real customers, and generated real cash flow. And it had stumbled onto a goldmine that would fuel its growth for the next half-decade.

III. The Government Surplus Goldmine (2002-2007)

Picture a sprawling military installation somewhere in the American heartland. Rows of surplus equipment stretch across acres of concrete: communications gear, medical equipment, tools, vehicles, furniture, industrial machinery. Much of it is perfectly functional, just no longer needed by the military. Under the old system, this material would sit in storage for months, sometimes years, slowly depreciating while bureaucrats shuffled paperwork. Eventually, a handful of local dealers might show up at a regional auction and buy everything at pennies on the dollar.

Liquidity Services changed that equation entirely. Through its Government Liquidation marketplace, the company became the exclusive online sales channel for the Defense Logistics Agency's Disposition Services. The scope was staggering: the company would eventually process and sell over 240 million surplus items for the Department of Defense. The contract structure covered everything from usable non-rolling stock surplus property to scrap materials, with a base term of twenty-four months and multiple twelve-month renewal options.

To understand the scale of this opportunity, consider the numbers. The DoD generates surplus across roughly five hundred military installations in the United States and its territories. In any given year, tens of thousands of individual lots need to be disposed of, ranging from a box of used wrenches worth $50 to specialized communications equipment worth hundreds of thousands. Before Liquidity Services, most of this material was sold through live auctions attended by a small group of local dealers who knew the schedule and showed up every month. The prices were low because the competition among buyers was limited. An auction at Fort Hood, Texas might attract twenty bidders. An online auction accessible to anyone in the world might attract two hundred.

What made governments uniquely bad at asset recovery was not incompetence, but structural incentives. Government agencies have no profit motive for maximizing the value of surplus assets. Their budgets are set annually, and the revenue from selling surplus typically flows back to the general fund rather than to the agency that generated it. There is no reward for getting a better price. The traditional disposal process was designed for compliance and accountability, not value maximization. Liquidity Services offered something revolutionary in this context: a technology platform that could photograph, catalog, and market surplus assets to a global buyer base, driving competitive bidding that routinely produced recovery values far above what physical auctions achieved.

The operational playbook was methodical and labor-intensive. The company's teams would inspect surplus items, take detailed photographs, write descriptions, categorize goods, set starting prices, and manage the auction process from listing through payment and shipment. This was not a software-only business. It required warehouses, logistics capabilities, and a deep understanding of the arcane regulations governing the sale of government property. Some items required demilitarization before they could be sold. Others had export restrictions. Navigating this regulatory complexity became its own competitive advantage.

On the buyer side, Liquidity Services cultivated a diverse network: resellers who would refurbish and resell items domestically, exporters who shipped goods to developing countries, scrap dealers who valued the raw materials, and bargain hunters looking for deals. Building liquidity on both sides of the marketplace was the classic chicken-and-egg problem of any two-sided platform, but the government contracts gave the company a massive supply advantage that attracted buyers naturally.

The Government Liquidation marketplace received the Vendor Excellence Award from the Defense Logistics Agency for outstanding performance on multiple occasions, a recognition that underscored the company's operational reliability. In a relationship where compliance failures could mean losing a contract worth hundreds of millions in annual revenue, this kind of track record was invaluable. It was not enough to run good auctions; the company had to navigate complex federal procurement regulations, maintain meticulous records, and manage the physical flow of goods across dozens of military installations.

By 2005, the company had won the Defense Logistics Agency's scrap property contract, adding another major revenue stream. The business was growing rapidly, and in February 2006, Liquidity Services went public on the NASDAQ. The IPO priced at $10 per share, with the company selling five million new shares and existing stockholders selling an additional 2.7 million shares. The stock opened for trading at $11.85, a modest first-day pop that reflected solid but not frothy institutional demand. At the offering price, the company's market capitalization was approximately $77 million.

The business model at this stage was primarily a purchase model for government contracts: Liquidity Services would buy surplus inventory outright from the DoD, take physical possession, and then resell it through its online auctions. Revenue was recognized as the full sale price to buyers, which made the top line look large but meant margins reflected the spread between purchase cost and resale value. This model was capital-intensive but highly profitable when commodity prices cooperated.

Traditional liquidators and regional auctioneers, the incumbents in this space, were beginning to feel the pressure. A local auctioneer might have deep relationships in one geographic area, but could not match the reach of an online marketplace that attracted bidders from across the country and around the world. The technology moat was not about sophisticated algorithms at this point; it was about having the platform, the buyer base, and the government relationships. Network effects were beginning to compound: more buyers meant better prices for sellers, which attracted more sellers, which attracted more buyers. This virtuous cycle, once established, would prove very difficult for traditional competitors to break.

For investors watching in 2006 and 2007, LQDT looked like a steady, growing business with a strong government anchor, improving margins, and a clear technology advantage over offline incumbents. What they could not yet see was how dramatically the next chapter would change the company's trajectory.

IV. The Retail Apocalypse 1.0 & Expansion (2008-2012)

When Lehman Brothers collapsed in September 2008, the shockwaves rippled through every corner of the American economy. Retail was hit especially hard. Circuit City filed for bankruptcy in November 2008. Linens 'n Things, Mervyns, Sharper Image, and dozens of other retailers followed. The wave of retail failures produced an unprecedented flood of surplus inventory: millions of consumer electronics, home goods, apparel, and other merchandise that needed to go somewhere fast.

For Liquidity Services, this was a defining moment. The company had built its business on government surplus, but the retail apocalypse opened an entirely new market. Bankrupt retailers needed to convert inventory to cash quickly. Surviving retailers needed to clear excess stock to make room for new merchandise. Manufacturers were stuck with returned goods, overstock, and cancelled orders. All of them needed a marketplace, and the existing infrastructure of regional liquidators and closeout dealers could not handle the volume.

For Liquidity Services, crisis meant opportunity. The company moved aggressively to expand beyond its government base. It acquired GovDeals in 2008, a self-directed auction platform used by state, county, and city government agencies across the United States and Canada. GovDeals operated on a fundamentally different model from Government Liquidation: instead of Liquidity Services buying and reselling goods, GovDeals let individual agencies list and sell their own surplus, with the platform taking a commission. This acquisition would prove to be one of the most consequential in the company's history, though its full value would not become apparent for another decade.

Alongside GovDeals, the company expanded through additional acquisitions: Network International for oil and gas equipment, TruckCenter.com for vehicle remarketing, and Jacobs Trading's remarketing business for retail surplus. It was building a portfolio of specialized vertical marketplaces, each serving a distinct customer base with different needs. Liquidation.com handled consumer goods, GovDeals handled government assets, NetworkINTL covered industrial equipment, and Government Liquidation maintained the DoD relationship.

The strategic shift during this period was significant and ultimately dangerous. As the company chased the retail opportunity, it moved deeper into the purchase model, where it bought inventory outright from sellers and then resold it. This approach made sense from a client acquisition perspective: large retailers wanted a guaranteed price for their surplus, not the uncertainty of auction outcomes. Guaranteed purchase contracts simplified the seller's decision, but they transferred commodity risk and working capital burden to Liquidity Services.

The economics worked brilliantly in 2011 and 2012, when scrap metal prices were high and demand for discounted consumer goods was strong. Revenue surged from roughly $240 million in fiscal 2009 to $490 million by fiscal 2012. The stock price followed, climbing from the low teens to its all-time high of $65.26 in May 2012. Wall Street loved the growth story, and the company's market capitalization exceeded $2 billion at its peak. For a company that had IPO'd at $77 million in market cap just six years earlier, this was a remarkable ascent that made early investors very wealthy.

But the purchase model's hidden risk was that it turned Liquidity Services into a commodity trader as much as a technology company. When the company bought a container of scrap metal from the DoD, it was betting that the price of scrap would hold or rise between purchase and resale. When it bought pallets of returned consumer electronics, it was betting that the merchandise would be in saleable condition and that buyers would pay enough to cover the purchase price plus a margin. These bets mostly worked during the commodity super-cycle of 2010-2012, but they were not the foundation of a durable technology business.

In 2012, the company made its largest acquisition: GoIndustry DoveBid, a global online auction company with operations in more than twenty countries, for approximately $31 million. The deal was intended to give Liquidity Services an international platform and access to industrial surplus markets in Europe, Asia, and the Middle East.

Meanwhile, an important competitor was quietly forming. B-Stock Solutions launched in 2008, founded by Howard Rosenberg, who had spent six years at eBay building private marketplace solutions for brands like HP, Motorola, and Dell. Rosenberg's insight was different from Angrick's: rather than building a centralized marketplace where all sellers aggregated their goods, B-Stock created white-label, private-branded auction marketplaces for individual retailers. This gave brands more control over their liquidation channel and avoided the "brand tarnishment" concern that made some retailers uncomfortable with Liquidation.com. B-Stock would eventually raise over $73 million in venture funding and build relationships with Amazon, Walmart, Target, Home Depot, and Costco. But in 2008, it was a startup, and Liquidity Services barely noticed.

The Amazon relationship also began during this era, with early deals to handle customer returns. Amazon, already the largest online retailer, was generating enormous volumes of returned merchandise, items that customers sent back for every reason from "didn't fit" to "changed my mind" to "arrived damaged." The logistics of processing these returns, inspecting them, categorizing their condition, and finding new buyers, was a massive headache that Amazon preferred to outsource. Liquidity Services was a natural partner: it had the marketplace infrastructure, the buyer network, and the operational capability to handle volume. At the time, it seemed like just another client win in the company's retail expansion. Nobody could have predicted how important, and how complicated, that relationship would become.

The period from 2008 to 2012 was Liquidity Services at its most expansive and most confident. Revenue was growing, margins were healthy, the stock was soaring, and the company was diversifying into new verticals and new geographies. But beneath the surface, the seeds of a crisis were germinating. The purchase model that was driving revenue growth was also creating a fragility that would soon become painfully apparent.

V. The Great Pivot: From Merchant to Marketplace (2013-2016)

Revenue peaked at approximately $506 million in fiscal year 2013. On the surface, Liquidity Services looked stronger than ever. But Bill Angrick was staring at a set of numbers that told a different story. Gross merchandise value was growing, but margins were compressing. The purchase model meant the company was effectively acting as a merchant, buying low and selling higher, but "higher" was becoming less and less impressive as commodity prices fluctuated and competition intensified.

The problem with the merchant model in a low-margin, high-volume business is structural. Every dollar of inventory on your balance sheet is a dollar of risk. If commodity prices drop between the time you buy surplus and the time you sell it, you eat the loss. If a large lot of returned merchandise turns out to be more damaged than expected, you take the write-down. Working capital gets trapped in inventory rather than compounding in the platform. And perhaps most importantly, the merchant model does not scale the way a marketplace does. A marketplace earns a commission on transactions facilitated; a merchant earns a spread on transactions executed. The marketplace model's marginal cost approaches zero as volume grows. The merchant model's marginal cost is always the next truckload of inventory.

Then came the body blows. In December 2014, Walmart, which had accounted for roughly eleven percent of the company's GMV, terminated its supply deal with Liquidity Services. The loss was devastating, both financially and symbolically. Walmart was exactly the type of marquee retail client the company had been courting, and losing it signaled that the competitive landscape was shifting. B-Stock's white-label model, which gave retailers their own branded liquidation marketplace, was proving more attractive to major brands than listing goods on Liquidation.com alongside goods from dozens of other sellers.

In 2015, the company declined to rebid the DoD rolling stock contract for surplus vehicles, as competing bidders had driven pricing to levels that made the economics unworkable. This was a smaller blow, but it underscored the vulnerability of the purchase model: when competitors bid aggressively for contracts, the winner often got stuck with unfavorable economics.

Angrick made the call that would define his legacy as CEO. He decided to fundamentally transform Liquidity Services from a merchant, a company that buys and resells surplus goods, into a pure marketplace and technology platform, a company that facilitates transactions and earns commissions. Think of it as the difference between a used car dealer and an auto auction house. The dealer takes risk on every car it buys and parks on its lot. The auction house simply brings buyers and sellers together and takes a percentage of every sale.

The implications of this pivot were severe in the short term. Revenue plummeted because the company was no longer recognizing the full sale price of goods it purchased; it was only recognizing commissions on goods sold through its marketplace. Revenue dropped from roughly $490 million in fiscal 2014 to $330 million in fiscal 2015, then continued declining to around $210 million by fiscal 2018. The stock collapsed in tandem. From its 2012 peak of $65, LQDT shares fell through the twenties, the teens, and into single digits. Investors who had bought the growth story felt betrayed.

Wall Street's reaction was predictable: sell first, ask questions later. Revenue was declining. Margins were volatile. The company was telling a complex story about business model transformation that required patience and faith in management's strategic vision. Most institutional investors do not have the mandate or the temperament for that kind of patience.

But here is where Angrick's twenty-one percent ownership stake becomes relevant. When a CEO owns more than a fifth of the company, the decision to sacrifice short-term stock price for long-term value is not theoretical. It is personal. Angrick was destroying hundreds of millions of dollars in his own paper wealth. He did it anyway, because he believed the merchant model was a dead end and the marketplace model was the only path to durable competitive advantage.

The company also launched IronDirect in September 2016, an ambitious attempt to build an Amazon-style marketplace for new and used construction equipment. The concept was compelling in theory: create a one-stop shop where contractors could browse, compare, and purchase heavy equipment with the same ease they bought consumer goods on Amazon. But the heavy equipment market operates on relationships, financing arrangements, and physical inspections that do not translate easily to an e-commerce model. The venture underperformed significantly and was realigned and essentially shut down during fiscal 2018, adding to the losses during an already painful transition period. Not every bet paid off, and IronDirect served as an expensive reminder that marketplace dynamics vary dramatically by category. What works for consumer electronics does not necessarily work for excavators.

Meanwhile, the company invested heavily in technology: building the AllSurplus.com platform as a unified marketplace, improving self-service tools for sellers, and developing pricing algorithms that could help both buyers and sellers understand what surplus goods were actually worth. These investments consumed cash and depressed earnings in the near term, but they were building the foundation for the capital-light, scalable business that Angrick envisioned.

The internal cultural transformation was arguably even harder than the financial one. Employees who had spent years operating warehouses, inspecting merchandise, and managing inventory had to adapt to a world where the company's value was in its technology platform and buyer network, not in its physical operations. Some adapted. Others left.

This was the corporate equivalent of ripping out your own foundation while trying to build a new house on top of it. And while the company was going through this wrenching transformation, B-Stock was raising capital, signing deals with the biggest retailers in America, and eating Liquidity Services' lunch in the retail returns category.

VI. The Competitive Crucible: B-Stock and the Recommerce Wars (2016-2020)

The retail returns market was exploding, and everyone could see the prize. E-commerce was growing at double-digit rates, and with it, return rates were climbing. Online purchases were returned at roughly eighteen to twenty percent, nearly double the rate of in-store purchases. By the late 2010s, the National Retail Federation estimated that American retailers were dealing with over $400 billion in annual returns, a figure that would continue growing toward $760 billion. Within that enormous number, at least $100 billion was flowing through secondary liquidation markets. This was a massive and rapidly expanding total addressable market.

B-Stock's model was brilliantly designed for this moment. Howard Rosenberg understood something fundamental about retail brands: they did not want their excess merchandise showing up on a generic liquidation marketplace next to everyone else's castoffs. They wanted control. B-Stock built private-label, white-labeled auction sites for individual retailers. Amazon Liquidation Auctions ran on B-Stock's platform. So did Walmart Liquidation Auctions, Target Auctions, Home Depot, and Costco. Each retailer got its own branded experience, its own buyer pool, and the ability to set its own terms. For retailers worried about brand dilution, this was vastly more attractive than listing on Liquidation.com.

With over $73 million in venture funding from firms like Spectrum Equity and Susquehanna Growth Equity, B-Stock had the capital to invest aggressively in technology and client acquisition. By revenue, B-Stock was much smaller than Liquidity Services, generating roughly $26 million as of late 2025. But in the specific category of retail returns from major brands, B-Stock was winning the war for exclusive relationships.

The loss of the Walmart relationship was the most visible defeat, but the pattern was broader. Major retailers were gravitating toward B-Stock's brand-controlled model, and Liquidity Services was being pushed toward the segments where its advantages were strongest: government surplus, industrial equipment, and the long tail of mid-market retail sellers who did not need or want their own private marketplace.

Angrick's response was to double down on the marketplace transformation and invest in technology. If the company could not compete for exclusive retail relationships through a branded model, it would compete by building the best horizontal marketplace with the deepest buyer liquidity. The thesis was that while B-Stock might win individual retailer accounts, Liquidity Services could offer something B-Stock could not: a massive, diverse buyer network that had been cultivated over two decades, with over five million registered buyers who purchased across categories.

The financial performance during this period was grim. Revenue continued to decline from $320 million in fiscal 2016 to $210 million in fiscal 2020. The stock languished in single digits, testing the patience of even the most committed long-term shareholders. The company was investing in technology at a time when it could barely show consistent profitability. Adjusted EBITDA was thin. The IronDirect failure added insult to injury.

But something important was happening beneath the headline numbers. The company's consignment and marketplace revenue, while smaller than what the old purchase model generated, was inherently higher margin. The shift in business mix meant that while the top line was shrinking, the quality of revenue was improving. Take rates, the percentage of GMV that the company kept as revenue, were more stable and predictable. Working capital requirements were declining. The company was de-risking its balance sheet transaction by transaction.

New competitive threats continued to emerge from unexpected directions. Direct-to-consumer liquidation models, where individual buyers could purchase returned merchandise in small quantities through apps and online platforms, started gaining traction. YouTube and social media created an entire content genre around "liquidation pallet unboxing," where influencers would film themselves opening pallets of returned Amazon merchandise and revealing what was inside. This generated enormous consumer awareness of the liquidation market and attracted a new class of small-scale, individual buyers who had previously never considered purchasing returned goods. Shopify-integrated solutions allowed small retailers to sell their own surplus directly. The liquidation space, once dominated by a handful of large players and a long tail of regional auctioneers, was fragmenting in ways that were simultaneously creating opportunity and competition.

There was also the Optoro threat to consider. Optoro, a venture-backed software company that had raised over $80 million in equity and $40 million in venture debt, took a technology-first approach to the returns problem. Rather than building a marketplace, Optoro built software that helped retailers decide what to do with each returned item: resell it as new, refurbish it, liquidate it through a secondary marketplace, recycle it, or donate it. Optoro integrated with platforms like eBay for direct-to-consumer resale and offered its own consumer brand, Blinq. While not a direct marketplace competitor, Optoro represented a different vision of the returns ecosystem, one where intelligent routing software, rather than marketplace liquidity, was the key value driver.

Through all of this, Liquidity Services had two advantages that competitors could not easily replicate. First, its government relationships, particularly GovDeals' network of over seven thousand municipal agencies at the time, provided a stable and growing base of business that was largely insulated from the retail recommerce wars. Second, its global buyer network represented decades of accumulated trust and engagement. A buyer who had been purchasing surplus goods through Liquidity Services for fifteen years was not going to switch to a new platform just because it had a shinier user interface. The buyer came for the deals, and the deals existed because the seller came for the buyers.

By 2019, Liquidity Services looked like a company at its lowest point. The stock traded around $5 to $8. Revenue had been cut in half from its peak. The marketplace transformation that Angrick had bet the company on had not yet produced the financial results that would vindicate the strategy. And then the world changed.

VII. COVID, E-commerce Explosion, and Reinvention (2020-2022)

On March 27, 2020, as markets cratered in the early days of the pandemic, Liquidity Services stock hit $3.06 per share. That was a ninety-five percent decline from the 2012 highs and represented a market capitalization of roughly $100 million for a company that had been doing over $200 million in annual revenue. The moment of maximum pessimism, as it often does, coincided with the beginning of a fundamental shift in the company's fortunes.

The pandemic initially disrupted operations as government agencies and businesses shut down. Warehouses went idle. Auctions were paused. For a company that had spent years investing in its marketplace transformation, COVID looked like it might be the final blow. Jorge Celaya, the CFO who had joined in 2015 during the company's darkest period, implemented aggressive cost controls that kept the company cash-flow positive even during the disruption. It was a testament to the financial discipline that the team had developed during years of operating under duress.

But as the economy reopened, the structural tailwinds that the company had been positioning for over the previous half-decade arrived with force.

E-commerce surged to levels that forecasters had not expected to see for years. In 2021, the return rate on all merchandise sold in the United States hit a record 16.6 percent, up from 10.6 percent the prior year. For online purchases, the return rate was even higher at 20.8 percent. To put these numbers in tangible terms: for every hundred dollars of merchandise sold online, roughly twenty-one dollars' worth was coming back. That is not a rounding error; it is a fundamental characteristic of the e-commerce business model that creates a permanent, structural demand for secondary markets.

The math was relentless: more e-commerce meant more returns, and more returns meant more surplus merchandise that needed a secondary market. The global reverse logistics market was projected to reach nearly $960 billion by 2028, growing at a compound annual rate of roughly 5.6 percent. The reverse logistics industry was suddenly getting attention from investors and executives who had previously considered it a back-office afterthought.

GovDeals, the self-service platform for state and local governments acquired back in 2008, emerged as the company's crown jewel. When COVID forced municipalities to limit in-person interactions, GovDeals offered a contactless way to auction surplus assets. Government agencies that had been reluctant to move online suddenly had no choice. The platform added hundreds of new agency clients, accelerating a trend that had been building for years. A government fleet manager in rural Texas could now list a surplus fire truck, have it photographed and described, and attract bidders from across the country without anyone setting foot on the premises.

Retail clients were flooding in as well. COVID-era bankruptcies created inventory gluts. Retailers that survived were dealing with massive excess stock from disrupted supply chains, orders placed for a pre-pandemic world that no longer existed. The holiday seasons of 2020 and 2021 produced record return volumes. All of this surplus needed to flow through secondary markets, and Liquidity Services' marketplace platform was finally positioned to capture it efficiently.

The technology investments that had seemed premature during the lean years were now paying dividends. Self-service listing tools meant sellers could onboard without hand-holding from LQDT staff. Improved search and discovery features helped buyers find relevant items across categories. The AllSurplus.com platform unified the company's various marketplaces under one roof, making it easier for both buyers and sellers to transact across categories.

The scrap metal and commodity super-cycle of 2021 and 2022 provided an additional tailwind. Global commodity prices surged as supply chains were disrupted and demand recovered unevenly. Industrial surplus and scrap, a significant category for Liquidity Services, saw dramatically higher values. A lot of surplus aluminum or steel that might have fetched modest prices in 2019 was suddenly worth multiples of that in 2021.

The financial inflection was unmistakable. GMV accelerated, and because the company was now primarily operating as a marketplace rather than a merchant, the improving volume flowed through to higher-margin commission revenue. By the third quarter of fiscal 2022, GMV hit a then-record $325 million, a thirty-three percent increase from the same period the prior year.

In November 2021, the company made a strategic acquisition: Bid4Assets, a pioneering online marketplace for government real estate, including tax foreclosure sales and sheriff's sales. Since its inception, Bid4Assets had completed over $1 billion in asset sales to more than 800,000 registered buyers. The acquisition expanded the company's capabilities within the government sector, adding real property to the categories it could offer alongside vehicles, equipment, and general surplus. Bid4Assets was integrated into the GovDeals segment.

In July 2018, the company had also acquired Machinio, a global online equipment listing platform with 1.2 million assets for sale valued at $25 billion, with ten million annual website visits across 190 countries. The acquisition price was approximately $20 million in cash plus restricted stock and an earnout. Machinio provided analytics tools and software solutions for equipment sellers, adding a SaaS-like revenue stream and expanding the company's international reach.

The stock market finally started to recognize what was happening. From its $3.06 low, LQDT shares recovered dramatically through 2021 and 2022, as improving financial results validated the marketplace transformation thesis. The multiple expanded as investors began to value the company's recurring, high-margin marketplace revenue rather than punishing it for declining merchant revenue.

For the management team that had endured years of skepticism, the recovery was vindication. The marketplace model that Wall Street had punished Angrick for pursuing was now demonstrably working. The company that had nearly been written off as a declining government contractor was emerging as a scalable technology platform with improving economics and expanding addressable markets. Revenue began growing again. Margins expanded. Free cash flow turned meaningfully positive.

But the vindication was incomplete. The company had survived the transformation, proved the model, and positioned itself for sustained growth. The competitive landscape had not gotten any easier, and the question of how large and how profitable Liquidity Services could ultimately become remained very much open. What was clear, however, was that the patient, capital-light marketplace approach had survived its most severe test and emerged stronger.

VIII. The Modern Business and The Path Forward (2023-Present)

Fiscal year 2025, which ended September 30, 2025, was a record year for Liquidity Services by virtually every meaningful measure. GMV surpassed $1.57 billion for the first time, up fifteen percent year-over-year. Revenue reached $477 million, up thirty-one percent. Net income hit $28 million, a forty-one percent increase. Adjusted EBITDA was nearly $61 million, and the company generated $59 million in free cash flow. All of this with zero financial debt and over $185 million in cash.

The first quarter of fiscal year 2026, reported in February 2026, continued the trajectory: $398 million in GMV, $121 million in revenue, and $18 million in adjusted EBITDA, representing a thirty-eight percent year-over-year increase in the latter metric. Notably, consignment sales now represent eighty-one percent of consolidated GMV, confirming that the marketplace transformation Angrick began a decade ago is essentially complete.

The business operates through three main reporting segments plus a smaller software segment. GovDeals, the government surplus marketplace, is the largest and most consistently growing segment, with record GMV of $903 million in fiscal 2025. The platform now serves over ten thousand government agencies and added a record five hundred new agency clients in a single quarter. RSCG, the Retail Supply Chain Group centered on Liquidation.com, handles consumer goods liquidation for retailers and manufacturers. CAG, the Capital Assets Group, covers industrial and commercial equipment through AllSurplus.com, NetworkINTL, and the GoIndustry DoveBid international operations. Machinio, the global equipment listing platform acquired in 2018 for roughly $20 million, provides software and analytics tools for equipment sellers and sits within a smaller reporting segment alongside the company's auction software solutions.

The recommerce infrastructure thesis that Angrick has articulated for years is increasingly resonating. The reverse supply chain, the process of getting returned, surplus, and end-of-life goods from consumers and businesses back into productive use, is becoming recognized as critical infrastructure. It is the mirror image of the forward supply chain that companies have spent decades optimizing. While forward logistics moves goods from factories to consumers, reverse logistics moves goods from consumers back to wherever they can capture the most value: resale, refurbishment, recycling, or responsible disposal.

On the competitive landscape, Liquidity Services and B-Stock have essentially settled into differentiated positions. B-Stock dominates the private-label, brand-controlled liquidation space for major retailers. Liquidity Services dominates government surplus and operates the largest open marketplace for a wide range of surplus categories. There is overlap in the middle market, where mid-size retailers and manufacturers might choose either platform, but the two companies are competing less directly than they were five years ago.

The technology stack has matured significantly. With over six million registered buyers and twenty-five-plus years of transaction data, the company is deploying artificial intelligence for asset categorization, buyer navigation and conversion optimization, and predictive lead scoring. Management has emphasized that automation is driving record direct profit per labor hour, a key efficiency metric that indicates the platform is scaling without proportional headcount growth.

The sustainability narrative provides additional tailwinds. Every item resold through Liquidity Services' marketplaces is an item that did not end up in a landfill. The environmental cost of retail returns is staggering: according to various industry estimates, returned merchandise generates billions of pounds of waste annually, and the carbon emissions from return shipping alone are significant. As corporations face increasing pressure from ESG mandates and consumers demand more sustainable practices, the circular economy positioning of a recommerce platform becomes a genuine competitive advantage rather than just marketing. Several major retailers have begun including recommerce and waste reduction metrics in their sustainability reports, and the ability to demonstrate that returned merchandise was resold rather than destroyed is becoming a reporting requirement for some companies.

Recent strategic moves signal continued evolution. The company launched Retail Rush, a new business-to-consumer auction channel, with its first prototype in Columbus, Ohio. This represents a meaningful expansion from the company's traditional B2B model into the consumer market, and management reports higher recovery rates in the Retail Rush channel compared to wholesale. The company has also highlighted its heavy equipment vertical as a significant growth opportunity, with GMV growing at roughly thirty percent on a compound quarterly basis and management targeting $1 billion in heavy equipment GMV, up from approximately $100 to $110 million annually today.

On earnings calls, Angrick has characterized the current tariff environment as neutral-to-positive for the business, arguing that tariffs create scarcity value for products already in the United States and make used equipment more attractive when new imports become more expensive. The company acknowledged in SEC filings that the tariff situation remains fluid and could impact buyers, sellers, and asset availability in various ways.

Management has also hinted at "ten-digit asset sales," meaning billion-dollar programs, being announced with Fortune 1000 clients as the company moves through fiscal 2026. If these materialize, they would represent a step-change in the scale of the company's commercial relationships.

The share repurchase program signals capital allocation discipline. The board authorized $10 million in buybacks in December 2024, which was fully utilized, followed by a new $15 million authorization in November 2025. In the first quarter of fiscal 2026 alone, the company repurchased over 55,000 shares for $1.5 million. With $181 million in cash and zero debt, the company has significant financial flexibility for acquisitions, organic investment, and continued returns to shareholders.

One area worth watching closely is the growing fraud problem in the returns and reverse logistics space. As the volume of returned merchandise flowing through secondary markets increases, so does the incentive for bad actors to exploit the system. Fraudulent returns, misrepresented merchandise, and buyer-side scams are all increasing. Management has positioned Liquidity Services' decades of experience in vetting and qualifying its buyer base as a competitive differentiator, arguing that the company's fraud prevention capabilities remove risk for sellers in a way that newer platforms cannot match. This is a subtle but potentially significant advantage: a seller choosing between two platforms with similar recovery rates will choose the one that minimizes fraud risk and operational headaches.

Another noteworthy development is the company's approach to auction participation. Fiscal 2025 saw a record 4.1 million auction participants across the platform. This metric matters because auction participation is the lifeblood of a marketplace: more bidders mean more competitive auctions, higher recovery rates for sellers, and a stronger value proposition for attracting additional sellers. The fact that participation is growing at the same time as GMV suggests the flywheel is functioning as intended.

Bill Angrick, now in his twenty-sixth year as CEO with a twenty-one percent ownership stake worth roughly $163 million at current prices, remains firmly in control. His total annual compensation of approximately $4.3 million is modest relative to peer CEOs, and the overwhelming majority comes from equity-based compensation, keeping his incentives aligned with shareholders. Angrick was named Ernst and Young Entrepreneur of the Year for the D.C. region in 2005, early in the company's history, and has since maintained a relatively low public profile, preferring to let the business results speak. He is a trustee of Georgetown Preparatory School and maintains advisory ties to his alma mater Notre Dame. His leadership style is characterized by long-term strategic thinking, willingness to endure short-term pain, and a deep understanding of marketplace dynamics that comes from having built one from scratch.

IX. Porter's Five Forces and Hamilton's Seven Powers Analysis

To understand whether Liquidity Services' current position is durable, it helps to apply two rigorous analytical frameworks: Michael Porter's Five Forces, which assesses industry attractiveness, and Hamilton Helmer's Seven Powers, which identifies the sources of sustainable competitive advantage.

Threat of New Entrants: Medium-High. Starting an online auction marketplace is not technically difficult. The barriers to entry in terms of technology and capital are relatively low, especially for a marketplace model that does not require inventory ownership. Any well-funded startup could build an auction platform, integrate payment processing, and start soliciting sellers. But here is the critical distinction: building the technology is easy; building the liquidity is brutally hard. A new entrant needs buyers who show up reliably and bid competitively. That buyer network takes years to cultivate. Liquidity Services has spent twenty-five years building a base of over six million registered buyers who trust the platform and know how to navigate its categories. A new entrant would face the classic cold-start problem: no buyers means no sellers, and no sellers means no buyers. This is the moat, not the technology itself. However, a well-capitalized competitor with an existing buyer base in an adjacent market, think eBay, Amazon, or a large logistics company, could potentially overcome the cold-start problem more quickly. The threat is real but not immediate.

Bargaining Power of Suppliers (Sellers): Medium-High. The seller side of the marketplace is concentrated in a way that creates meaningful bargaining power. A handful of very large clients, government agencies, major retailers, and large manufacturers, generate a disproportionate share of GMV. When one of these large sellers decides to leave, as Walmart did in 2014, the impact is severe. Switching costs for sellers are relatively low; they can list goods on multiple platforms simultaneously or switch to a competitor without significant operational disruption. However, Liquidity Services' buyer liquidity creates meaningful stickiness: a seller who moves to a platform with fewer buyers will likely receive lower prices, which creates a natural incentive to stay. The company's strategy of deepening operational integration with sellers, embedding its technology into clients' reverse logistics processes, is an attempt to increase switching costs over time.

Bargaining Power of Buyers: Medium. The buyer base is fragmented, consisting of thousands of resellers, exporters, scrap dealers, and bargain hunters, which limits any individual buyer's bargaining power. Professional buyers do comparison shop across platforms, and there is nothing preventing a buyer from bidding on both Liquidation.com and a B-Stock marketplace. But network effects create value that keeps buyers returning: the platform with the most diverse selection of goods at the best prices will naturally attract the most active buyers. The key risk here is multi-homing. If buyers can easily browse and bid across multiple platforms with minimal friction, the competitive dynamics favor sellers (who can play platforms against each other) and reduce the marketplace's pricing power.

Threat of Substitutes: High. This is arguably the most challenging force for Liquidity Services. The alternatives to using a dedicated liquidation marketplace are numerous: selling directly on eBay or Amazon Marketplace, donating goods for a tax write-off, using Craigslist or Facebook Marketplace for local sales, hiring a traditional auctioneer, or building an in-house liquidation operation. Amazon itself has been building internal capabilities through Amazon Warehouse and Amazon Renewed, handling some of its own returns rather than routing them through third parties. For large enterprises, the build-versus-buy decision is always present: at sufficient scale, it may make economic sense to invest in proprietary liquidation capabilities rather than paying a marketplace commission.

Competitive Rivalry: High. The competitive environment is intense and fragmented. B-Stock is well-funded and focused specifically on the retail returns category. Regional liquidation companies compete in local markets. Vertical specialists focus on specific categories like heavy equipment, electronics, or vehicles. New entrants continue to emerge, and the race to sign exclusive seller relationships creates ongoing pressure. Genco, now part of FedEx Supply Chain, represents yet another competitive vector: a full-service third-party logistics provider with over $1.6 billion in sales and eleven thousand employees that handles refurbishment, repair, and product liquidation as part of a broader logistics offering. The presence of major logistics companies in adjacent spaces means that competitive threats could come from unexpected directions. This is not a winner-take-all market; it is more likely to evolve into an oligopoly with a few major platforms coexisting alongside a long tail of specialized players.

Turning to Hamilton Helmer's Seven Powers framework, the picture becomes more nuanced.

Turning to Hamilton Helmer's Seven Powers framework, the picture becomes more nuanced.

Network Effects are the company's primary source of durable competitive advantage. Two-sided marketplace network effects are powerful when they work: more sellers bring more selection, which attracts more buyers, which drives higher prices and attracts more sellers. Liquidity Services has category-specific network effects that are particularly strong in government surplus, where GovDeals' ten-thousand-plus agency relationships create a flywheel that would be very expensive for a competitor to replicate. The data flywheel compounds over time: more transactions generate better pricing data, which enables better price guidance for sellers and better deal discovery for buyers, which drives more transactions. After twenty-five years and over eight billion dollars in cumulative transactions, this data advantage is substantial.

Scale Economies are moderate and growing. The technology platform's fixed costs are amortized over larger GMV, and buyer acquisition costs are spread across more transactions. The company's recent record of improving direct profit per labor hour suggests that scale economies are beginning to materialize in operational efficiency. But reverse logistics has strong local and regional dynamics that limit pure scale advantages. A heavy equipment auction in Texas has different logistics than a consumer electronics liquidation in New Jersey. Unlike a pure software marketplace where marginal costs approach zero, surplus goods still require physical inspection, storage, and shipment, all of which have local cost structures.

Process Power is emerging as a meaningful advantage. Twenty-five years of operational learning in inspecting, categorizing, pricing, and selling surplus goods across dozens of categories has created institutional knowledge that is difficult to replicate quickly. The pricing algorithms, logistics optimization, and fraud prevention capabilities represent accumulated intellectual capital. However, with sufficient capital and time, a determined competitor could build comparable capabilities.

Counter-Positioning was historically powerful but is eroding. When Liquidity Services first digitized government surplus auctions, traditional brick-and-mortar liquidators could not match the online model without cannibalizing their existing business. That advantage has largely disappeared as the industry has moved online.

Switching Costs are low to moderate. Sellers can multi-home with minimal effort. Buyers' loyalty is driven by finding good deals rather than any lock-in mechanism. The operational integration that Liquidity Services builds with large clients creates some friction, but it is not insurmountable.

Branding provides moderate advantage in specific niches. GovDeals is the trusted name in government surplus. Government Liquidation carries weight with DoD-related buyers. But in retail liquidation, the perception is more commoditized. Cornered Resources include the long-standing government relationships and regulatory compliance expertise, though these are not permanent exclusive advantages.

It is worth comparing Liquidity Services to other marketplace businesses to calibrate expectations. Copart, the auto salvage auction marketplace, has demonstrated that a well-run two-sided marketplace in a specialized category can compound returns for decades. Copart's network effects in damaged vehicle auctions are so strong that its take rates have actually expanded over time, a rare and powerful dynamic. Liquidity Services aspires to a similar position in surplus and returned goods, but it operates across many more categories with more heterogeneous dynamics, making it harder to achieve the same degree of dominance in any single vertical. The exception may be GovDeals, which has Copart-like characteristics within government surplus: strong network effects, high trust, growing agency adoption, and limited viable competitors.

The overall verdict: Liquidity Services' competitive position rests primarily on network effects in specific verticals and emerging process power. The moat is real and defensible, particularly in government surplus, but it is not insurmountable. The company's value accrues from the breadth and depth of its buyer network, its operational expertise, and the data advantages that compound with scale and time.

X. Playbook: Business and Investing Lessons

The Liquidity Services story offers an unusually rich set of lessons for both operators building businesses and investors evaluating them. Few public companies have navigated as dramatic a strategic transformation while maintaining the same founding CEO, and fewer still have done so in a category as overlooked as reverse logistics.

For Founders: The Merchant vs. Marketplace Decision

The single most important strategic question Liquidity Services confronted was whether to be a merchant or a marketplace, and the answer changed over time. In the early years, acting as a merchant, buying surplus goods outright and reselling them, was necessary to prove the business model, attract sellers, and build credibility with the Department of Defense. Sellers, particularly government agencies, wanted simplicity: here is our surplus, give us a check, you deal with finding buyers. The merchant model provided that simplicity and was highly profitable when commodity prices cooperated.

But the merchant model had a ceiling. Capital trapped in inventory could not be reinvested in the platform. Commodity price fluctuations created earnings volatility that made long-term planning difficult. And most importantly, the merchant model did not generate the network effects that would make the business defensible over time. Every year, the company had to rebid for government contracts and compete for retail relationships. There was no flywheel, just a treadmill.

The transition to a marketplace model was existentially necessary, but it required a CEO willing to accept years of declining revenue, a collapsing stock price, and intense skepticism from investors and employees alike. Angrick's willingness to make this call, and to stick with it through the darkest years, is a case study in the kind of long-term thinking that is almost impossible in public markets. His twenty-one percent ownership stake gave him both the conviction and the economic alignment to weather the storm.

The lesson for founders is counterintuitive: sometimes you need to be a merchant first to bootstrap liquidity, but you need the strategic clarity to recognize when the merchant model has served its purpose and the courage to let revenue decline while you build a more defensible business. This is the equivalent of a restaurant owner who starts by cooking every dish herself, builds a loyal customer base, and then transitions to a franchise model where she licenses her recipes and brand. The restaurant's revenue from direct sales drops, but the franchise fees create a more scalable, capital-light income stream. Most founders understand this intellectually. Very few have the stomach to execute it when it means watching their stock price fall ninety-five percent.

For Founders: Building Boring Infrastructure

There is nothing glamorous about inspecting surplus office furniture, photographing lots of returned consumer electronics, or managing the logistics of shipping decommissioned military equipment. Reverse logistics is thankless, operationally complex, and decidedly unsexy. It will never make the cover of a technology magazine or attract the breathless attention of Silicon Valley venture capitalists.

But it is essential. The forward supply chain, the process of getting goods from factories to consumers, attracts trillions of dollars in investment and has been optimized by some of the most sophisticated companies in the world. The reverse supply chain, the process of getting goods back from consumers to wherever they can create the most value, has been comparatively neglected. That neglect creates opportunity for companies willing to do the unglamorous work.

The technology moat in a business like Liquidity Services does not come from a single brilliant algorithm or a revolutionary user interface. It comes from data accumulated over decades, from operational processes refined through millions of transactions, from buyer relationships cultivated across thousands of categories, and from the institutional knowledge of what a lot of surplus medical equipment is actually worth versus what a lot of returned consumer electronics is actually worth. This is process power in the Hamilton Helmer sense: a competitive advantage that emerges from doing something complex, repeatedly, and getting better at it each time.

For Founders: Vertical Specialization

The decision to build multiple specialized marketplaces rather than a single general-purpose platform was strategically sound. GovDeals serves government agencies with a self-service model that emphasizes compliance and simplicity. Liquidation.com serves retail liquidators who care about lot sizes and merchandise categories. NetworkINTL serves oil and gas companies that need specialized knowledge about industrial equipment. AllSurplus.com covers heavy equipment and capital assets for buyers who think in terms of machinery specifications rather than consumer product descriptions.

These are fundamentally different customer types with different needs, different buying behaviors, and different definitions of value. A government fleet manager disposing of surplus police cruisers has nothing in common with a retail entrepreneur looking to buy pallets of returned Amazon merchandise. Trying to serve both through a single undifferentiated platform would have diluted the experience for everyone.

The success of this approach is visible in the numbers. GovDeals alone generated $903 million in GMV in fiscal 2025, more than half the company's total, while maintaining strong margins and adding clients at an accelerating rate. It turns out that building deep expertise in specific verticals, understanding the regulations, the buyer types, the pricing dynamics, and the operational quirks, creates a kind of stickiness that a horizontal platform simply cannot replicate. For founders contemplating their own marketplace strategies, the lesson is clear: go deep before you go wide.

For Investors: Recognizing Platform Transition Value

The period from 2013 to 2019 was a test of investor patience and analytical rigor. Revenue was declining. The stock was collapsing. On a superficial level, Liquidity Services looked like a deteriorating business. But investors who understood the distinction between revenue quality and revenue quantity could see that the underlying economics were improving. Commission-based marketplace revenue is structurally higher margin, lower risk, and more scalable than merchant revenue. The decline in top-line revenue masked an improvement in the fundamental health of the business.

The lesson is that platform transitions often look like value destruction before they look like value creation. Revenue declines because the company is no longer recognizing the full sale price of goods it purchases. Margins may be volatile during the transition period. Management's narrative shifts from simple growth metrics to more complex explanations about GMV, take rates, and capital efficiency. Most investors cannot or will not make the effort to understand the distinction, which creates opportunity for those who do.

For Investors: Following Management Incentives

Bill Angrick's twenty-one percent ownership stake, worth approximately $163 million at current prices, is an unusually strong alignment mechanism. When a CEO owns that much of the company, the incentive to maximize long-term value per share rather than short-term stock price is powerful and authentic. Angrick could have sold the company during the growth years, could have continued the merchant model to maintain the stock price, could have walked away during the trough years. He did none of those things. His patience has been rewarded with a stock price that has recovered more than tenfold from its lows, though it remains well below its all-time high.

The broader lesson: in small-cap companies, management quality and alignment are disproportionately important. A well-aligned management team with a sound long-term strategy can create enormous value, but it requires investors who are willing to underwrite multi-year transformation timelines. The window during which LQDT traded at single-digit prices, from roughly 2017 to 2020, represented an opportunity that was visible primarily to investors who understood the difference between revenue contraction from business deterioration and revenue contraction from business model transformation. That distinction, obvious in hindsight, required genuine analytical work in real time.

XI. Bull vs. Bear Case

The Bull Case

The structural case for Liquidity Services rests on a simple chain of logic: e-commerce continues to grow, e-commerce generates returns at roughly double the rate of in-store purchases, returns generate surplus merchandise that needs secondary market channels, and Liquidity Services operates one of the largest and most established secondary market platforms in the world. The total addressable market is enormous and expanding.

The marketplace model is now hitting the inflection point that Angrick bet the company on a decade ago. Operating leverage is becoming visible: fiscal 2025 revenue grew thirty-one percent while adjusted EBITDA grew twenty-five percent, and the first quarter of fiscal 2026 showed adjusted EBITDA growth of thirty-eight percent. As the consignment mix continues to increase, each incremental dollar of GMV flows through at higher margins.

Circular economy and sustainability mandates are providing regulatory tailwinds. As corporations face increasing pressure to minimize waste and maximize the productive reuse of goods, professional recommerce platforms become compliance necessities rather than optional cost recovery tools. The European Union has already implemented extended producer responsibility regulations that make brands financially responsible for the end-of-life management of their products. Similar regulatory trends are emerging in the United States and could significantly increase demand for professional recommerce infrastructure.

GovDeals provides a stable, growing base that is largely insulated from competitive dynamics in the retail space. With ten thousand agency clients and five hundred new agencies added in a single quarter, the government segment has strong network effects and high barriers to competitive displacement. The Bid4Assets acquisition added real property to this ecosystem, expanding the total addressable market within government. Municipal governments across the country are still in the early innings of digitizing their surplus disposition processes, with thousands of agencies still relying on local auctions or informal sales. The greenfield opportunity within GovDeals alone is meaningful.

The twenty-five years of transaction data, combined with AI and machine learning capabilities, creates a data advantage that compounds over time. Better pricing data leads to better outcomes for sellers, which attracts more volume, which generates more data. This flywheel is difficult for competitors to replicate.

The Retail Rush initiative, if successful, opens an entirely new distribution channel by bringing B2C consumers into an ecosystem that has historically been B2B only. Management reports higher recovery rates in this channel, which would translate to higher take rates and better economics. The logic is straightforward: a consumer willing to buy a single returned blender at sixty percent off retail will pay more per unit than a wholesale liquidator buying a pallet of five hundred blenders at ninety percent off. Disaggregating the merchandise and selling to end consumers rather than middlemen captures more of the residual value, and the technology platform makes this economically feasible at scale.

The heavy equipment vertical growth target of $1 billion in GMV represents a potential five-to-ten-fold increase from current levels. If the approximately thirty percent compound quarterly growth rate continues, this vertical alone could become a significant driver of overall company performance. Heavy equipment is a particularly attractive category because the average transaction value is high, the buyer base is global, and the assets are durable enough to ship internationally, creating cross-border liquidity that amplifies the network effects.

The twenty-five years of transaction data, combined with AI and machine learning capabilities, creates a data advantage that compounds over time. Better pricing data leads to better outcomes for sellers, which attracts more volume, which generates more data. This flywheel is difficult for competitors to replicate.

Finally, the balance sheet is fortress-like: $181 million in cash, zero debt, and strong free cash flow generation. This provides optionality for acquisitions, share repurchases, and organic investment without dilution or leverage.

The Bear Case

Amazon remains the elephant in the room. As the single largest generator of returned merchandise in the world, Amazon has both the incentive and the capability to build internal liquidation infrastructure. Amazon Warehouse and Amazon Renewed already handle significant volumes of returned and refurbished goods. To the extent that Amazon internalizes more of its own reverse logistics, the total addressable market for third-party platforms like Liquidity Services shrinks.

B-Stock continues to hold strong positions with major retailers through its white-label model. For a Fortune 500 retailer evaluating liquidation options, B-Stock's brand-controlled approach may be more attractive than listing goods on a shared marketplace. This limits Liquidity Services' ability to win exclusive relationships with the largest commercial sellers.

Switching costs are genuinely low for sellers. A retailer can test multiple liquidation channels simultaneously and shift volume to whichever platform delivers the best recovery rates. This makes client relationships inherently fragile and creates ongoing pressure to deliver competitive results.

Technology commoditization is a real risk. The auction platform technology that was differentiating twenty years ago is now widely available. Several companies offer white-label auction solutions, and building a basic liquidation marketplace is within reach of any well-funded startup. The competitive advantage increasingly depends on buyer network depth and operational expertise rather than technology per se.

Margin pressure from competition limits pricing power. In a market with multiple viable platforms and low switching costs, take rates face downward pressure. The company's current take rates are healthy, but sustainable pricing power in a competitive marketplace is never guaranteed.

The company remains a small cap, with a market capitalization around $950 million. Small-cap stocks face structural headwinds including limited institutional coverage, lower liquidity, and wider bid-ask spreads. Many institutional investors simply cannot or will not own positions of this size, which limits the potential shareholder base. The irony is that a company called Liquidity Services has, in public equity markets, a liquidity problem of its own.

Management concentration risk is real. Angrick has been CEO for twenty-six years and is the visionary behind every major strategic decision. Co-founder Mateus-Tique stepped down from operational roles back in 2009 and has served only as a board member since. The bench of proven executive talent below Angrick, while capable, has not been publicly groomed for succession. Succession planning is a critical question for a company this dependent on a single leader, and to date, management has not provided detailed public commentary on this topic. For a company with a twenty-year time horizon, this is a gap that investors should monitor.

The KPIs That Matter

For investors tracking Liquidity Services' ongoing performance, three metrics stand out as the most important indicators of business health and strategic progress.

First, GMV growth rate, which measures the total value of goods transacted through the company's marketplaces. Because the business has largely transitioned to a consignment model, revenue growth can be misleading. Revenue depends on the mix between purchase and consignment transactions, and a shift toward consignment can cause revenue to decline even as the underlying business grows. GMV growth captures the true trajectory of marketplace volume regardless of business model mix.

Second, consignment mix as a percentage of GMV, which measures how far the marketplace transition has progressed and the quality of the revenue base. At eighty-one percent consignment in the most recent quarter, the transition is largely complete, but any reversal toward purchase-model transactions would signal potential strategic backsliding. Higher consignment mix means lower revenue recognition per dollar of GMV but higher margins, lower risk, and better capital efficiency.

Third, GovDeals new agency additions, which serves as a leading indicator of network effect strength in the company's most defensible segment. The rate at which new government agencies join the platform reflects both competitive positioning and the secular shift from offline to online surplus disposition. The record five hundred additions in the most recent quarter suggest the flywheel is accelerating. Any deceleration would warrant investigation into competitive dynamics or market saturation. Together, these three metrics, GMV growth, consignment mix, and GovDeals agency additions, provide a comprehensive dashboard for tracking whether the marketplace flywheel is strengthening or weakening over time.

XII. Epilogue and Reflections

There is a kind of business story that rarely gets told on the main stage. It is not the story of the brilliant founder who raises hundreds of millions in venture capital, disrupts an industry in five years, and goes public in a blaze of media attention. It is the story of the founder who starts with $100,000 of his own money, builds a business around a genuine and persistent market need, survives multiple near-death experiences, makes the gut-wrenching decision to sacrifice short-term performance for long-term positioning, endures years of stock price pain, and emerges two decades later with a business that is quietly essential to the functioning of modern commerce.

Bill Angrick is not a household name. Liquidity Services does not appear in discussions of the most innovative technology companies. Reverse logistics does not inspire TED talks or magazine covers. But consider what the company actually does: it ensures that surplus government helicopters, returned consumer electronics, excess retail inventory, foreclosed real estate, decommissioned industrial equipment, and millions of other items find new owners who value them rather than ending up in landfills. In a world that produces more goods than it can consume and returns a growing percentage of what it buys, that function is becoming more important with each passing year.

The marketplace dynamics that Liquidity Services navigated over the past quarter century offer lessons that extend far beyond this specific company. Liquidity, in the marketplace sense of having enough active buyers and sellers to generate fair prices consistently, is the single most important attribute of any two-sided platform. It is harder to build than technology, harder to maintain than brand, and more valuable than either. It is what makes the difference between a marketplace that works and an auction site that sits empty.