LPL Financial: The Independent Broker-Dealer Revolution

I. Introduction & Episode Setup

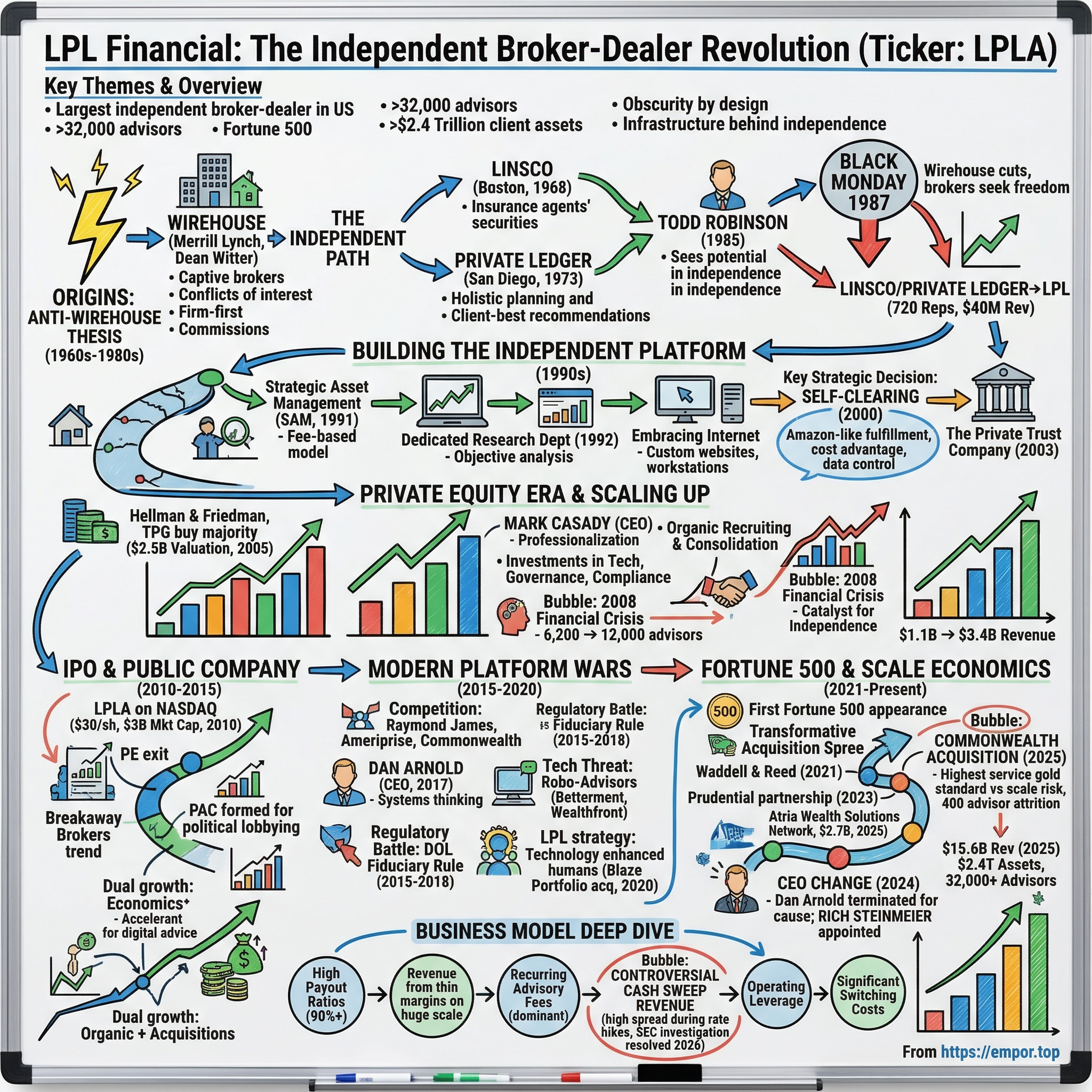

Picture this: somewhere in America right now, a financial advisor is sitting across the table from a family, helping them plan for retirement, their children's college fund, or the sale of a small business. That advisor does not work for Morgan Stanley. They do not work for Merrill Lynch. They do not work for any wirehouse at all. They work for themselves — but they are supported by a company most people outside finance have never heard of: LPL Financial.

LPL is the largest independent broker-dealer in the United States — and it is not particularly close. More than 32,000 financial advisors operate on its platform, serving roughly 11 million client accounts. It custodies and administers over $2.4 trillion in client assets — a number that has roughly doubled in the last three years alone. For the 2025 fiscal year, LPL generated approximately $15.6 billion in revenue and produced record adjusted earnings per share north of twenty dollars. It sits on the Fortune 500 list and commands a market capitalization exceeding $25 billion.

And yet, if you stopped ten people on the street and asked them what LPL Financial does, nine would have no idea. That obscurity is by design. LPL is the infrastructure behind independence — the picks-and-shovels provider in the financial advice gold rush. The advisors are the faces. LPL is the engine room.

The central question of this story is deceptively simple: How did two small firms, founded in the shadows of Wall Street's great wirehouses, build the infrastructure to revolutionize an entire industry?

The answer spans nearly six decades and touches on some of the most consequential transformations in American finance: the shift from commissions to fees, the rise of fiduciary advice, the explosive growth of private equity-fueled consolidation, and the ongoing battle between independence and institutional control. It is a story about disruption — but not the Silicon Valley variety. This is disruption in a heavily regulated, relationship-driven industry where trust is the ultimate currency and change happens in decades, not quarters.

Here is a company that has grown revenue nearly 400-fold in thirty-six years — from $40 million at its founding to over $15 billion today. A company that has survived Black Monday, the dot-com bust, the 2008 financial crisis, the pandemic, and a CEO termination for cause. A company that has consolidated an industry, redefined a business model, and quietly become one of the most important financial institutions in America while remaining almost completely unknown to the general public.

The themes that emerge are remarkably consistent across every chapter of LPL's history: independence as ideology, technology as competitive moat, scale economics as destiny, and regulatory navigation as survival skill. This is the story of how a company that most Americans have never heard of became the single most important platform in the business of financial advice — and what that means for the future of the industry.

II. Origins & The Anti-Wirehouse Thesis (1968-1989)

To understand LPL Financial, you first have to understand the world it was born to disrupt.

In the 1960s and 1970s, the American financial advice industry operated under a model that would strike modern observers as almost feudal. If you were a financial advisor — they were called stockbrokers back then — you worked for a wirehouse. Merrill Lynch, Dean Witter, Shearson Lehman, Kidder Peabody. These were the temples of Wall Street, and the brokers who worked inside them were, in every meaningful sense, captive. The firm told you what products to sell. The firm set your compensation grid. The firm owned your client relationships. And the firm's interests — generating trading commissions, pushing proprietary products, maximizing transaction volume — came first. Always.

The name "wirehouse" itself tells the story. It referred to the private telegraph wires that connected branch offices to the firm's trading floor. Information flowed one way: from headquarters to the field. The broker's job was to execute, not to think independently. If Merrill Lynch decided that a particular mutual fund family deserved shelf space, every broker in every branch office across America would be pushing that fund by Monday morning. Whether it was the best choice for Mrs. Johnson's retirement portfolio was, at best, a secondary consideration.

The conflicts of interest were not subtle. A wirehouse might earn millions in investment banking fees from a corporation and then instruct its brokers to recommend that corporation's stock to retail clients. The broker who refused — who said, "Actually, I think this is a terrible investment for my client" — risked his career. The one who complied earned a commission and a pat on the back. The client, more often than not, never knew the difference. This was not a system designed for the client's benefit. It was a system designed for the firm's benefit, with the client's interests addressed only when they happened to align.

Into this world stepped two men with remarkably similar instincts and almost no connection to each other.

In 1968, in Boston, a group of insurance companies created an entity called Life Insurance Securities Corporation — LINSCO, for short. The idea was practical rather than visionary: insurance agents needed the ability to offer mutual funds and securities alongside their insurance products. LINSCO would provide the regulatory framework and back-office support that made this possible. It was a modest beginning — a cooperative venture designed to broaden what insurance agents could sell, not a grand challenge to the established order. Nobody involved imagined they were planting a seed that would grow into a Fortune 500 company.

Five years later and three thousand miles away, in San Diego, a former naval aviator named Bob Ritzman saw something different. Ritzman, along with fellow Navy veteran Al Monahan, founded Private Ledger in 1973. Ritzman had recognized an insight that was genuinely ahead of its time: very few advisors in America actually offered comprehensive financial planning. Most brokers sold products — a stock here, a bond there, an annuity when the commission was right. Ritzman believed there was an enormous untapped market for advisors who could sit down with clients and build holistic financial plans, selecting from a broad universe of investment options based on what was actually best for the client rather than what generated the fattest commission check.

This was radical. In 1973, the very concept of an independent financial advisor — one who was not beholden to a wirehouse's product shelf — was almost unheard of. The military background mattered. Both Ritzman and Monahan brought a sense of duty and service orientation that was fundamentally at odds with the commission-driven culture of Wall Street. Naval aviators are trained to trust their judgment, follow their training, and put the mission first. Ritzman applied the same mindset to financial advice: the mission was serving the client, and every other consideration was secondary.

Ritzman equipped his advisors with access to a wide array of mutual funds and investment options and explicitly told them: base your recommendations on what is best for the client, not what is best for the firm's bottom line. It was the founding philosophy that would eventually define LPL, articulated more than a decade before the company itself existed.

Then came Todd Robinson. In 1985, Robinson purchased Linsco, the Boston-based entity that had been operating for nearly two decades as a relatively sleepy broker-dealer for insurance agents. Robinson was not a sleepy operator. He was an entrepreneur with a keen eye for structural shifts in the financial services industry — the kind of person who read demographic trends and regulatory changes with the same intensity that a trader reads price charts. He saw something that Ritzman had seen on the West Coast: a growing desire among financial advisors to run their own practices, free from wirehouse control. Robinson bet that this desire would only intensify, and he positioned Linsco as the vehicle to capture it.

His timing proved prescient in a way that even he probably did not anticipate. On October 19, 1987 — Black Monday — the stock market crashed. The Dow Jones Industrial Average fell 22.6% in a single day, the largest one-day percentage decline in the index's history. The carnage on Wall Street was immediate and devastating. Wirehouses slashed headcount. Thousands of brokers were laid off. And in the wreckage, something interesting happened: many of those displaced brokers discovered that they did not want to go back to another wirehouse. They wanted independence.

Black Monday did not create the independent advisor movement, but it poured gasoline on a smoldering fire. Suddenly, the risks of being a captive wirehouse employee — where your career depended on the whims of a distant home office that might eliminate your position in a single afternoon — were viscerally real. The appeal of running your own practice, owning your own client relationships, and controlling your own destiny had never been stronger.

Robinson and Ritzman recognized the moment. Though they came from different coasts, different backgrounds, and different corners of the financial services industry, they shared a conviction: the future of financial advice would be built on independence, not captivity. In 1989, they merged Linsco and Private Ledger to form Linsco/Private Ledger — LPL. The combined firm launched with 720 registered representatives and approximately $40 million in annual revenue, with dual headquarters in Boston and San Diego that reflected its bicoastal DNA. Those numbers were modest by any measure. The wirehouses of the era each employed tens of thousands of brokers and generated billions in revenue. Merrill Lynch alone had over 10,000 brokers. LPL's 720 representatives barely registered as a rounding error.

But LPL had something the wirehouses did not: a founding vision built on a simple, powerful idea.

As the company would later articulate it, "the client's best interests are not just a priority but the cornerstone of every decision." That sounds like boilerplate corporate language today — the kind of phrase that gets etched on a lobby wall and promptly ignored. In 1989, in an industry built on commissions and proprietary product pushing, it was revolutionary. It meant that the advisor, not the firm, would decide what was best for the client. And that the firm's role was to support the advisor, not to control them.

The merger also created something strategically important: geographic and cultural breadth. Linsco brought East Coast relationships and insurance industry connections. Private Ledger brought West Coast innovation and a financial planning philosophy. Together, they created a platform with national reach and a coherent ideology that could attract advisors from every corner of the industry.

What made the timing especially powerful was the broader deregulatory trend in American finance. The Glass-Steagall Act, which had separated commercial banking from investment banking since the Depression, was being steadily eroded through regulatory interpretations and would ultimately be repealed in 1999. Financial products were proliferating. Mutual funds, variable annuities, wrap accounts, and fee-based planning services were all gaining traction. The advisor who wanted to offer comprehensive financial planning needed a platform that could handle this complexity without the conflicts of a wirehouse. LPL was built to be exactly that platform. The anti-wirehouse thesis had found its institutional home.

III. Building the Independent Platform (1990s)

Having a philosophy is one thing.

Building the infrastructure to operationalize that philosophy across thousands of independent advisors scattered across the country — that is something else entirely.

Think about the problem LPL faced in the early 1990s. The company had committed to supporting independent financial advisors — people who, by definition, wanted to run their own businesses. But those advisors still needed everything a wirehouse provided: trade execution, compliance oversight, research, client reporting, custody of assets, regulatory filings, and technology. They just wanted it without the wirehouse's strings attached.

This was the fundamental challenge — and the fundamental opportunity. LPL had to build, essentially, all the back-office capabilities of a major Wall Street firm, but deliver them as a service to entrepreneurs rather than as corporate mandates to employees. It was the difference between building an army and building an arsenal: LPL was not assembling troops under a single command, but arming independent operators with the weapons they needed to compete.

The first breakthrough came in 1991, with the creation of Strategic Asset Management — SAM. This was one of the first fully fee-based advisory platforms in the American financial services industry, and it elegantly solved a problem that had nagged independent advisors for years. Before SAM, if an advisor wanted to build a diversified portfolio using multiple mutual funds, each fund sat in a separate account with separate paperwork, separate reporting, and separate commission structures. It was administratively chaotic and economically misaligned — the advisor got paid per transaction, which created an inherent incentive to trade more, not to manage better.

SAM changed the equation. It grouped multiple mutual funds into a single consolidated account and shifted the advisor's compensation from per-transaction commissions to an annual percentage fee based on total assets under management. This was more than a product innovation; it was a philosophical statement embedded in a technology platform. When your income rises and falls with the total value of your client's portfolio, your incentives are naturally aligned with making that portfolio grow. When your income depends on transactions, your incentives are aligned with making the phone ring.

The market validated SAM immediately. Within a few years, the platform had accumulated $5 billion in assets. By the time LPL celebrated SAM's thirtieth anniversary in 2021, the platform had become the foundational architecture upon which the entire modern fee-based advisory industry was built.

To support SAM, LPL created a dedicated research department in 1992. This was not a cosmetic move. Independent advisors needed objective investment analysis — research that was not tainted by wirehouse conflicts of interest, where the firm's investment banking relationships might influence which stocks received favorable coverage. At the wirehouses, a common criticism was that "buy" ratings seemed to flow disproportionately to companies that happened to be investment banking clients. The research might be technically competent, but its independence was perpetually in question.

LPL Research provided a genuinely independent voice, covering asset classes, market conditions, and investment themes without the baggage of investment banking relationships. Over the decades, it grew into one of the largest and most tenured research groups among independent brokerage firms. The research department became a powerful recruiting tool — an advisor considering the leap from a wirehouse to independence could look at LPL and see not just a trading platform, but an intellectual infrastructure that would help them serve clients at a professional level.

Through the mid and late 1990s, LPL embraced the emerging internet with a speed that belied its relatively modest size. While many established financial firms were still debating whether the internet was a fad or a transformative force — some wirehouses famously resisted online trading because it threatened their commission revenue — LPL was building customized advisor websites, fee-based investment platforms, and online workstation functionality.

The company understood intuitively that technology would be the great equalizer — that a well-built digital platform could give a solo independent advisor in Topeka access to the same tools and information that a wirehouse broker in Manhattan enjoyed. This was a democratizing force, and LPL leaned into it aggressively. Every dollar spent on technology was a dollar that made independence more viable and the wirehouse model less essential.

But the single most consequential infrastructure decision of the decade came in 2000, when LPL transitioned to self-clearing. This was, at the time, one of the largest conversions to self-clearing in U.S. securities industry history, affecting approximately 440,000 client accounts. To understand why this matters, think of clearing as the plumbing of the brokerage industry. When an advisor executes a trade on behalf of a client, someone has to process that trade, settle the securities, maintain custody of the assets, and handle all the regulatory reporting. Most independent broker-dealers outsourced this function to third-party clearing firms — paying a per-transaction fee and, critically, ceding control over client data and the client experience.

By bringing clearing in-house, LPL accomplished three things simultaneously. First, it eliminated the per-trade fees it had been paying to third-party clearers, dramatically improving unit economics. Second, it gained complete control over client data, enabling better analytics and more sophisticated advisor tools. Third, it took ownership of the entire client experience from trade execution to statement delivery, ensuring that every touchpoint met LPL's standards rather than a third party's.

This decision was the equivalent of Amazon building its own fulfillment network. It was expensive, risky, and operationally complex. But once completed, it created a structural cost advantage and capability moat that competitors who relied on third-party clearing simply could not match. Self-clearing became LPL's hidden superpower — invisible to end clients but foundational to everything the company built afterward.

In 2003, LPL acquired The Private Trust Company, adding specialized custody, trust administration, and tax services for high-net-worth clients. This was a significant strategic move because it signaled LPL's ambition to serve not just the mass affluent market — the bread and butter of independent advisors — but also the wealthier clients who had traditionally been the exclusive province of wirehouses and private banks. An independent advisor affiliated with LPL could now offer trust services alongside investment management and financial planning, a comprehensive capability set that rivaled anything a wirehouse could provide.

By 2006, the numbers told a compelling story. LPL supported more than 6,500 advisors, generated $1.7 billion in annual revenue, and managed $115 billion in client assets. The company had evolved from a scrappy startup with 720 representatives and $40 million in revenue into a sophisticated financial services platform. The infrastructure was in place. The philosophy was proven. The question was no longer whether independent advice could work at scale — it was how big the opportunity actually was.

IV. Private Equity Era & Scaling Up (2005-2010)

If the 1990s had proven that the independent model could work, the next decade would prove that it could scale — dramatically. The answer to the question of how big the opportunity really was arrived in October 2005, when two of the most prominent private equity firms in the world placed one of the largest bets the independent broker-dealer industry had ever seen.

Hellman & Friedman and Texas Pacific Group — now known as TPG Capital — agreed to acquire a majority stake in LPL Financial in a transaction that valued the company at $2.5 billion, or roughly 2.5 times gross revenue. Industry analysts at the time noted that this was the highest valuation multiple ever paid for an independent broker-dealer — a signal that sophisticated financial buyers saw something in the independent model that the broader market had not yet fully appreciated. The deal closed on December 28, 2005, with the PE firms taking approximately 60% of the company's equity while LPL's founders and employees retained about 40%. The retention of 40% by insiders was deliberate: it ensured that the founders and management team had meaningful skin in the game and would remain aligned with the PE sponsors through the next phase of growth.

At the time of the acquisition, LPL served just under 6,200 financial advisors and generated approximately $1.1 billion in annual revenue from more than $100 billion in client assets. These were respectable numbers, but they represented only a fraction of the total addressable market. Hellman & Friedman and TPG saw what LPL's founders had always believed: that the secular shift toward independent financial advice was still in its early innings, and that the company with the best platform would capture a disproportionate share of that shift.

To understand why PE firms were willing to pay such a premium, consider the economics. LPL's revenue was highly recurring — advisory fees and commissions generated by a stable base of affiliated advisors. The revenue was also highly scalable — each new advisor who joined the platform generated incremental revenue with minimal incremental infrastructure cost. And the market opportunity was enormous: at the time, the wirehouse model still dominated American financial advice, but every industry survey showed growing advisor dissatisfaction with captive employment and growing client demand for unconflicted advice. For a private equity investor, LPL looked like a tollbooth on a highway that was about to get much busier.

The private equity playbook that followed was textbook — but executed with unusual discipline. PE firms are often criticized for loading portfolio companies with debt and slashing costs. At LPL, the approach was different. The PE sponsors invested heavily in three areas that would prove decisive: professionalization of management, technology infrastructure, and acquisitive growth.

Mark Casady, who had served as CEO since the mid-2000s, became the face of LPL's PE-era transformation. Casady was an energetic, high-profile industry figure — a frequent presence at industry conferences, a quotable source for financial media, and a charismatic leader who could articulate the independent advisor vision with genuine passion. He understood that the independent broker-dealer needed to evolve from a collection of entrepreneurial advisors into a sophisticated, institutional-grade platform. The company needed board governance, internal audit functions, risk management frameworks, financial reporting systems, and all the other apparatus of a professionally managed corporation — not because anyone was demanding it yet, but because the IPO window would not wait for a company that was not ready.

Under Casady's leadership, LPL invested in the systems, governance structures, and operational processes that would be required for a public company — building the airplane while flying it, as the management cliche goes.

The growth numbers during this period tell a remarkable story. Between 2005 and 2010, LPL more than doubled its advisor force, growing from roughly 6,200 representatives to over 12,000. Revenue scaled proportionately, climbing from $1.1 billion to approximately $3.4 billion. This growth came from two sources: organic recruiting of advisors leaving wirehouses and regional firms, and strategic acquisitions that consolidated smaller independent broker-dealers onto LPL's platform.

The organic recruiting engine was powered by a simple but compelling value proposition. At a wirehouse, an advisor typically received a payout of 40-50% of the revenue they generated. At LPL, that payout was 90% or higher. For a producing advisor generating $500,000 in annual revenue, the difference between keeping $200,000 and keeping $450,000 was life-changing — the difference between an upper-middle-class income and genuine wealth creation. And the economic argument was just the beginning.

Unlike starting a fully independent registered investment advisory (RIA) firm — which required building compliance infrastructure, technology platforms, back-office operations, and custodial relationships from scratch — joining LPL meant plugging into a ready-made platform. The advisor got to keep the vast majority of their revenue while LPL handled everything behind the curtain: trade execution, compliance monitoring, statement generation, regulatory filings, technology support, and continuing education. For an advisor who wanted to own their practice but did not want to become a technology company, a compliance shop, and an operations center all at once, LPL offered the best of both worlds.

This period also saw LPL make critical investments in its technology infrastructure. The ClientWorks platform — LPL's core advisor-facing workstation — evolved from a basic trading and reporting tool into an integrated practice management system. Mobile access, dashboard customization, CRM integration, and streamlined account opening workflows transformed the advisor experience and became key differentiators in recruiting conversations.

Perhaps most importantly, the PE era forced LPL to build the governance and compliance infrastructure required for institutional scale. The financial services industry is among the most heavily regulated in America. Every trade, every client interaction, every marketing piece, every fee disclosure must comply with a thicket of rules from FINRA, the SEC, and state regulators. For a company supporting thousands of independent advisors — each running their own business with their own clients — compliance was an enormous operational challenge. LPL built centralized compliance systems that could monitor advisor activity at scale, a capability that became both a competitive advantage and a regulatory necessity.

The period also coincided with the 2008 financial crisis, which — like Black Monday two decades earlier — served as a powerful catalyst for the independence movement. The collapse of Bear Stearns and Lehman Brothers, the forced mergers of Merrill Lynch into Bank of America and Wachovia Securities into Wells Fargo, sent shockwaves through the wirehouse advisor population. Advisors who had spent entire careers at these firms suddenly found themselves working for institutions they had never chosen, under management teams they did not know, with compensation structures being rewritten overnight. The appeal of owning your own practice — of being insulated from the institutional upheavals of Wall Street — had never been more visceral.

LPL was positioned perfectly to capture this wave of disaffected wirehouse advisors. Its platform was mature, its technology was competitive, and its economics were compelling. Between 2008 and 2010, the pace of advisor recruitment accelerated markedly.

By 2010, the PE sponsors had accomplished what they set out to do: they had transformed LPL from a successful but subscale independent broker-dealer into an institutional-grade platform ready for the public markets. The stage was set for the next chapter.

V. The IPO & Public Company Transformation (2010-2015)

On November 18, 2010, LPL Financial Holdings Inc. began trading on the NASDAQ Global Select Market under the ticker symbol LPLA, after pricing its initial public offering at $30 per share. The IPO raised approximately $470 million, with Goldman Sachs, Morgan Stanley, Bank of America Merrill Lynch, and J.P. Morgan serving as joint book-running managers.

The pricing was a statement. At $30 per share, LPL's market capitalization at the open was approximately $3 billion — a meaningful premium to the $2.5 billion valuation from the PE acquisition five years earlier, reflecting the growth and professionalization that had occurred in the interim. The stock opened at $32.15, above the IPO price, signaling healthy institutional demand. By 2025, that $30 IPO share price would be worth more than ten times its original value — one of the best-performing IPOs of the 2010 vintage in the financial services sector.

The choice of NASDAQ over the New York Stock Exchange was itself a subtle signal. NASDAQ was the exchange of technology companies, of innovators, of firms that saw themselves as disruptors rather than establishment players. For a company that had spent its entire existence challenging the Wall Street establishment, listing on NASDAQ rather than the NYSE felt fitting.

For Hellman & Friedman and TPG, the IPO was the beginning of their exit — and a highly successful one. H&F would fully exit its position by 2013, having generated substantial returns on its 2005 investment. For LPL's advisors, many of whom had been granted equity participation during the PE era, the IPO was a tangible validation of the independent model. Their platform company was now a publicly traded entity, subject to the scrutiny of Wall Street analysts and public market investors — the very establishment that the wirehouse model represented.

The same year, LPL formed a political action committee — the LPL Financial LLC PAC — to lobby Washington on behalf of independent advisors and their clients. This was a quietly significant move that reflected a maturing political awareness within the company. The financial services regulatory landscape was shifting dramatically in the aftermath of the 2008 financial crisis. The Dodd-Frank Act, signed into law in July 2010, imposed sweeping new regulations on financial institutions. While the law's primary targets were large banks and systemically important financial institutions, the ripple effects reached every corner of the industry.

LPL recognized that independent broker-dealers needed a political voice to ensure that regulations designed to rein in Wall Street banks did not inadvertently crush independent advice. A compliance requirement that cost Morgan Stanley $10 million to implement might cost LPL $5 million — a much larger percentage of its operating budget. And a requirement that was burdensome for LPL might be fatal for smaller independent broker-dealers, which would accelerate consolidation and reduce advisor choice. The PAC was LPL's way of ensuring that the independent channel had a seat at the table when these regulations were being written.

The early years as a public company brought both opportunities and tensions. On the opportunity side, LPL had access to public market capital to fund acquisitions and technology investments — resources that private competitors like Commonwealth Financial Network could not match. Analyst coverage from major investment banks raised the company's profile, making it easier to recruit advisors who might not have heard of the firm. And the discipline of quarterly earnings reports, investor presentations, and annual meetings forced a level of operational rigor and strategic clarity across the organization that benefited the business even when it felt burdensome.

But public company life also introduced pressures that sometimes chafed against LPL's advisor-first culture. Wall Street analysts wanted predictable, growing earnings every quarter. Advisors wanted a platform that invested in their experience regardless of short-term earnings impact. Managing this tension — between the demands of public investors and the expectations of independent advisors — became one of the central challenges of LPL's public company era.

Mark Casady continued to lead the company through this transition, and his leadership style was critical. Casady was a charismatic, high-energy executive who could speak the language of Wall Street analysts in quarterly earnings calls and then turn around and address a room full of independent advisors with genuine enthusiasm for their entrepreneurial journeys. He understood intuitively that LPL's dual constituency — investors who wanted growing earnings and advisors who wanted a better platform — required constant balancing. His tenure, which ran for approximately a decade through the end of 2016, defined LPL's identity as a public company.

The company pursued a dual growth strategy during this period: organic recruiting of advisors and strategic acquisitions. On the organic side, LPL continued to capture a significant share of the "breakaway broker" movement — advisors leaving wirehouses for independence. The economics remained compelling: advisors could dramatically increase their take-home compensation while gaining control over their practice, their client relationships, and their professional identity.

On the acquisition side, LPL made selective purchases to fill capability gaps and add scale. In February 2003, the company had already acquired The Private Trust Company, adding specialized custody and trust services for high-net-worth clients. In the post-IPO years, the company continued to evaluate opportunities to consolidate smaller independent broker-dealers, a strategy that would accelerate dramatically in later years.

The institutional business also began to emerge as a meaningful growth vector during this period. Banks and credit unions across America had historically offered investment services through their own captive broker-dealers or through relationships with mid-tier firms. LPL recognized that these institutions represented a massive, underserved market. By offering a turnkey platform — technology, compliance, clearing, and research — LPL could enable banks and credit unions to offer sophisticated investment advice to their customers without building the infrastructure themselves. Think of it as software-as-a-service for wealth management: the bank provides the client relationships and the physical branches, LPL provides everything else. This B2B channel would eventually become one of the fastest-growing segments of LPL's business, culminating in partnerships with Prudential, Wintrust, and hundreds of other financial institutions.

The significance of LPL's post-IPO trajectory for investors cannot be overstated. Between 2010 and 2015, the company demonstrated that the independent broker-dealer model could operate successfully under public market scrutiny — that advisor-first culture and shareholder value creation were not mutually exclusive. The stock performed well, analyst coverage expanded, and the company's visibility in the broader financial services industry rose dramatically. But Casady and his team also recognized that organic growth alone would not be sufficient to build the kind of platform dominance they envisioned. The independent broker-dealer industry remained highly fragmented, with more than 120 firms competing for advisor affiliations. Consolidation was not just an opportunity — it was an imperative. And the tools to execute that consolidation — public market capital, institutional credibility, and a proven integration playbook — were now firmly in hand.

By the middle of the decade, LPL had firmly established itself as the undisputed leader of the independent broker-dealer channel. But the competitive landscape was evolving. New challengers were emerging, technology was reshaping client expectations, and regulators were preparing a battle that would test the entire industry's business model.

VI. The Modern Platform Wars (2015-2020)

The period from 2015 to 2020 was defined by three simultaneous conflicts: a competitive arms race among independent broker-dealers, a regulatory battle over the very definition of fiduciary duty, and a technological disruption that threatened to make human financial advisors obsolete.

Dan Arnold succeeded Casady as CEO in 2017, bringing a more operationally focused, less outwardly charismatic leadership style. Arnold was a systems thinker — quieter than Casady but deeply committed to building the operational excellence that would support LPL's growing scale. Under his leadership, total shareholder return would eventually exceed 537%, a remarkable run of value creation.

Start with competition. By 2015, the independent broker-dealer landscape was no longer a wide-open frontier. Raymond James Financial had built a formidable independent channel alongside its traditional employee model, competing directly with LPL for breakaway wirehouse brokers. Ameriprise Financial operated a franchise-like independent channel that attracted advisors who wanted independence with a household brand name behind them. Commonwealth Financial Network, a privately held firm founded in 1979 by Joe Deitch, had carved out a premium niche, consistently earning the highest advisor satisfaction scores in the industry — J.D. Power ranked it number one twelve consecutive times. And aggregators like Advisor Group and Cetera Financial Group were assembling multi-brand IBD networks that competed for the same advisor population.

The competition for advisors was intense because the independent channel was growing faster than any other segment of the wealth management industry. Every wirehouse in America was losing advisors to independence — a trickle that had become a steady stream. Industry data showed that independent broker-dealers and registered investment advisors were gaining market share from wirehouses year after year, a structural shift that showed no sign of reversing. The question was not whether those advisors would leave — it was which independent platform they would choose.

LPL's scale gave it inherent advantages in technology, compliance infrastructure, and cost efficiency. But smaller competitors often won on culture, personal service, and the promise of a more intimate relationship. The tension between scale and intimacy would become one of the defining strategic challenges of LPL's next decade — and the Commonwealth acquisition would bring it into sharp relief.

LPL's most significant acquisition of this era came on August 15, 2017, when it signed and closed the purchase of the independent broker-dealer network of National Planning Holdings, Inc. This was no ordinary deal. NPH was the holding company for four separate independent broker-dealer firms, and the transaction brought approximately 3,200 advisors onto LPL's platform in a single stroke. The initial purchase price was $325 million, with up to $123 million in additional contingent payments tied to advisor retention — an important structural feature that aligned the incentives of both parties around successful integration.

The NPH acquisition was LPL's first true test of large-scale broker-dealer integration, and the experience would shape the company's acquisition playbook for years to come. Integrating thousands of advisors, each with their own clients, systems, and workflows, onto a single platform was an enormous operational challenge. Every advisor had to be re-registered with FINRA under LPL's broker-dealer license. Every client account had to be transferred, re-papered, and re-coded. Every compliance record had to be migrated and reconciled. And through all of this, the advisors had to continue serving their clients without interruption — because a missed phone call or a delayed trade during a market correction could mean losing a client permanently.

The contingent payment structure of the NPH deal — with up to $123 million in additional consideration tied to production retention thresholds — was an innovation that LPL would replicate in future acquisitions. It aligned the incentives of both parties: LPL wanted to retain advisors, and NPH's former owners wanted to maximize their payout. The lessons learned about communication cadence, technology migration sequencing, cultural sensitivity, and retention incentives would prove invaluable when even larger deals came along later.

Meanwhile, the Department of Labor was waging a regulatory war that consumed the attention of every broker-dealer in America. The DOL Fiduciary Rule, proposed in 2015 and finalized in April 2016, would have required all financial advisors — including broker-dealer representatives — to act as fiduciaries when providing advice on retirement accounts. Under existing rules, brokers were held to a lower "suitability" standard, which required only that recommendations be appropriate, not that they be in the client's best interest.

For LPL and the broader independent broker-dealer industry, the implications were enormous. To understand the stakes, consider the difference between the two standards. Under a "suitability" standard, a broker can recommend a product that is appropriate for a client, even if a cheaper or better alternative exists — as long as the recommended product is not unsuitable. Under a "fiduciary" standard, the advisor must recommend the best available option for the client, period. The practical difference is the difference between "this product won't hurt you" and "this product is the best thing for you." The fiduciary standard threatened to eliminate or severely constrain commission-based compensation models — the traditional revenue engine for broker-dealers. If an advisor could not demonstrate that a commission-based product was in the client's best interest compared to a lower-cost alternative, the sale could be considered a fiduciary breach. LPL had been moving toward fee-based advisory services for years, but commissions still represented a significant portion of revenue. More fundamentally, the rule raised compliance costs and legal liability for every advisor interaction.

LPL engaged aggressively in the political and regulatory debate, through its PAC, through industry associations, and through direct advocacy. The company also accelerated its internal shift toward fee-based advisory models, recognizing that the direction of regulatory travel was clear regardless of the specific rule's fate. When a federal appeals court vacated the DOL Fiduciary Rule in March 2018, before full implementation, it was a significant short-term victory for the broker-dealer model — but the trend toward fiduciary standards and fee-based advice was irreversible.

The technology front presented a different kind of challenge entirely — not regulatory, but existential. Between 2015 and 2020, robo-advisors — automated digital platforms like Betterment and Wealthfront that offered algorithmically generated portfolio management at a fraction of the cost of human advice — captured the public imagination and billions of dollars in assets. The value proposition was alluring in its simplicity: answer a few questions about your risk tolerance and time horizon, and an algorithm will build and manage a diversified portfolio for you, charging 25 basis points or less. No human advisor, no office visit, no relationship to manage. For a generation of younger investors raised on apps and algorithms, the appeal was obvious. The fear was that technology would disintermediate human advisors entirely, rendering the broker-dealer platform model obsolete.

What actually happened was more nuanced than the doomsday predictions suggested. Robo-advisors captured assets, but primarily among younger, lower-balance clients who were not the core market for human financial advisors. When clients had complex financial situations — estate planning, tax optimization, business succession, charitable giving, emotional reactions to market volatility — they still wanted a human being on the other end of the phone. The robo-advisor threat turned out to be real but bounded: technology was excellent at portfolio construction but poor at the emotional and relational dimensions of financial advice.

LPL's response was characteristically pragmatic. Rather than building a competing consumer-facing robo-advisor, the company invested in technology that made its human advisors more efficient and effective. The acquisition of Blaze Portfolio on October 26, 2020 — a Chicago-based fintech firm that specialized in portfolio management and trading technology — was emblematic of this approach. For approximately $12 million, with up to $5 million in additional milestone-based payments, LPL acquired sophisticated automated trading and rebalancing capabilities that it could integrate into its advisor platform. The bet was that the future of financial advice was not human versus machine, but human enhanced by machine.

This period also brought regulatory settlements that tested LPL's reputation. FINRA fines for supervisory failures — including a $10 million penalty in 2015 for failures to supervise brokers' use of consolidated reports — highlighted the challenges of maintaining compliance oversight across thousands of independent advisors. The company's cumulative regulatory sanctions numbered in the hundreds, a reflection both of the inherent difficulty of supervising a distributed advisor network and of the intensity of regulatory scrutiny that came with being the industry's largest player.

The COVID-19 pandemic in 2020 added an unexpected accelerant. Lockdowns forced the entire financial advice industry to go virtual overnight. Advisors who had robust digital tools — video conferencing integration, electronic account opening, digital document signing, online client portals — thrived. Those who depended on in-person meetings at their local branch office struggled. LPL's years of technology investment suddenly paid dividends in a way that nobody had anticipated. Advisors on the LPL platform could serve clients remotely without missing a beat, and the company's recruiting engine actually accelerated during the pandemic as wirehouse advisors experienced firsthand the limitations of their firms' technology.

By the end of 2020, LPL had navigated the platform wars, the fiduciary battle, and the robo-advisor threat with its market position not just intact but strengthened. Revenue had grown to nearly $6 billion. The advisor count exceeded 17,000. The foundation was laid for an even more ambitious phase of growth.

VII. Fortune 500 & Scale Economics (2021-Present)

In 2021, LPL Financial appeared on the Fortune 500 list for the first time, debuting at number 466. To put this in perspective: a company that had started with 720 representatives and $40 million in revenue just three decades earlier was now ranked alongside names like General Electric, FedEx, and Goldman Sachs in America's most prestigious corporate ranking. By 2024, LPL had climbed to number 392. These rankings, based on annual revenue, reflected a company that had quietly ascended from the niche world of independent broker-dealers into the upper echelon of American corporations.

But the Fortune 500 milestone was not just a vanity metric. It mattered for recruiting. When a wirehouse advisor was considering whether to leave the safety of Morgan Stanley or Merrill Lynch for the uncertainty of independence, knowing that the platform they were joining was a Fortune 500 company with $15 billion in revenue provided a level of institutional comfort that a smaller broker-dealer simply could not match. The Fortune 500 ranking was, in effect, a recruiting credential — proof that LPL was not a fringe player but a mainstream financial institution.

The period from 2021 onward also represented a fundamental shift in LPL's strategic ambition — from organic growth supplemented by occasional acquisitions to an aggressive, acquisition-driven consolidation strategy aimed at achieving a scale that would make the company's platform advantages virtually unassailable.

The acquisition spree began in April 2021, when LPL closed the purchase of the wealth management business of Waddell & Reed for approximately $300 million, adding roughly 900 advisors and $71 billion in client assets. Waddell & Reed was a storied Kansas City-based firm with roots dating back to 1937 — its acquisition by LPL was a poignant symbol of how the independent model was absorbing even historically significant financial services brands.

This was followed by a stream of increasingly large and complex deals. In August 2023, LPL announced a strategic partnership with Prudential Financial, investing over $300 million to build the technology platform needed to onboard approximately 2,800 Prudential Advisors serving 3.5 million families with roughly $60 billion in assets. That integration was completed in November 2024.

The Atria Wealth Solutions acquisition, which closed on October 1, 2024, brought approximately 2,400 advisors and $100 billion in assets from roughly 150 banks and credit unions onto LPL's platform. Atria was particularly significant because it strengthened LPL's position in the institutional channel — the bank and credit union partnerships that were rapidly becoming a core growth driver.

Each successive deal reinforced the same thesis: in a world where compliance costs, technology investment, and regulatory complexity were all rising, scale was not just an advantage but a survival requirement. The independent broker-dealer industry had consolidated from 124 firms at the end of 2014 to just 79 by the end of 2024. Smaller broker-dealers simply could not afford the infrastructure investment needed to compete. They faced a stark choice: invest hundreds of millions in technology and compliance systems they could not afford, merge with a larger platform, or slowly fade into irrelevance. LPL was the natural acquirer for firms choosing the middle path.

Then came the deal that redefined LPL's ambitions entirely. On March 31, 2025, LPL announced the acquisition of Commonwealth Financial Network for $2.7 billion in cash — the largest acquisition in the company's history and one of the largest in the independent broker-dealer industry's history. Commonwealth represented something unique: approximately 3,000 advisors managing roughly $285 billion in assets, backed by a culture that was widely regarded as the gold standard in advisor satisfaction. Joe Deitch had founded Commonwealth 46 years earlier with a vision remarkably similar to LPL's — advisor independence supported by premium service — and had built a firm that advisors loved with an intensity that bordered on devotion.

The Commonwealth acquisition was both strategically compelling and culturally fraught. The expected run-rate EBITDA contribution of approximately $425 million — representing more than a 20% boost to LPL's pre-deal earnings power — made the financial logic clear. But Commonwealth advisors had chosen the firm precisely because it was not LPL. They valued the boutique service model, the personal relationships with home office staff, and the cultural identity of being part of something smaller and more intimate. The deal closed on August 1, 2025, and the platform conversion is expected to complete by the fourth quarter of 2026. As of early 2026, approximately 80% of Commonwealth's assets are under contract to migrate to LPL, though roughly 400 advisors have departed since the acquisition announcement — a retention challenge that underscores the difficulty of integrating a firm whose primary asset is cultural rather than technological.

Amid this acquisition spree — and in the middle of integrating multiple transformative deals simultaneously — LPL experienced its most dramatic leadership transition. The timing could hardly have been worse. On October 1, 2024, the board terminated President and CEO Dan Arnold for cause, following an investigation by an outside law firm that found Arnold had made statements to employees violating LPL's Code of Conduct and respectful workplace policies. Arnold, who had led LPL since 2017 and presided over a period in which total shareholder return exceeded 500%, forfeited his severance and outstanding equity awards — compensation that had totaled $16.9 million in 2023 alone. The board immediately named Rich Steinmeier, LPL's Managing Director and Chief Growth Officer, as CEO.

Steinmeier brought a markedly different profile to the role. A former Managing Director and Chief Digital Officer at UBS Wealth Management USA, he came from the very wirehouse world that LPL had spent decades disrupting. That background gave him an intimate understanding of what wirehouses offered — and what they did not — that informed his approach to making LPL's platform more competitive. He had joined LPL in 2018 and was credited with more than doubling the company's organic growth rate during his tenure as Chief Growth Officer. Board Chairman Jim Putnam specifically cited this growth acceleration in announcing the appointment.

Where Arnold was operationally focused and somewhat reserved, Steinmeier was growth-oriented and forward-looking, emphasizing technology investment, advisor experience, and the institutional partnership channel that had become one of LPL's fastest-growing segments. His appointment signaled that the board's priority was growth — continuing the momentum of what had been LPL's most aggressive expansion period — rather than a period of consolidation or reflection.

Despite the leadership disruption, the business continued to perform. In fact, the seamlessness of the transition said something important about the strength of LPL's platform and organizational depth — the company was no longer dependent on any single individual, not even its CEO.

The financial results during this period have been staggering. Full-year 2025 revenue reached approximately $15.6 billion — nearly triple the 2020 figure. Adjusted EBITDA hit $2.91 billion, up 31% year-over-year. Total advisory and brokerage assets reached a record $2.4 trillion. And the advisor count exceeded 32,000, a number that will climb further as the Commonwealth conversion completes. Advisory fee revenue alone grew 49% in 2025 to $8.16 billion, reflecting both market appreciation and the successful migration of acquired advisor practices onto LPL's fee-based platforms.

The company's business model evolution is evident in its revenue mix, which has shifted dramatically over the past decade. Advisory fees now represent the dominant and fastest-growing revenue stream, reflecting the industry-wide shift from commissions to asset-based fees that LPL helped pioneer with the SAM platform back in 1991. Commission revenue, while still significant at $2.65 billion in 2025, is declining as a percentage of the total. Asset-based revenue from client cash sweep programs contributed approximately $1.66 billion — a stream that is highly sensitive to interest rates and that has generated both enormous profits and significant controversy, as we will examine shortly.

The revenue trajectory tells the story of a company that has fundamentally changed its scale. From $40 million at the 1989 merger, to $1.1 billion when private equity arrived in 2005, to $3.4 billion at the 2010 IPO, to $10 billion by 2023, to approximately $15.6 billion in 2025 — LPL's revenue has grown nearly 400-fold in thirty-six years. No other company in the independent broker-dealer space comes close to this trajectory. The gap between LPL and its nearest competitor has widened with every passing year, and the Commonwealth acquisition will push the company further ahead still.

For investors, the question is no longer whether LPL can grow, but whether the pace of acquisition-driven growth can be sustained without compromising platform quality, advisor satisfaction, or regulatory standing. The company is simultaneously integrating multiple large acquisitions, navigating a shifting interest rate environment, and competing with wirehouses that are fighting harder than ever to retain their best advisors. The scale economics are real, but so are the execution risks.

VIII. Business Model Deep Dive

So how does this machine actually work?

At its core, LPL Financial operates what might be called a "franchise without the franchise" model. Independent financial advisors affiliate with LPL not as employees but as independent contractors running their own businesses. LPL provides the infrastructure — technology, clearing, compliance, research, and practice management support — and takes a portion of the revenue those advisors generate. The advisor keeps the rest.

The payout economics are the engine of LPL's recruiting machine. At a wirehouse like Morgan Stanley or Merrill Lynch, a financial advisor typically receives 40-50% of the revenue they generate. The rest goes to the firm to cover overhead, technology, compliance, real estate, and profit. At LPL, the advisor payout ranges from 90% to nearly 100% of production. For a top-producing advisor generating $1 million in annual revenue, the difference between keeping $450,000 at a wirehouse and keeping $900,000 at LPL is transformative. It is the single most powerful recruiting argument in the industry.

But if LPL is paying advisors 90% of revenue, where does the company's profit come from? This is the question that confuses most observers when they first encounter the LPL business model. If you are giving away ninety cents of every dollar, how can you possibly be profitable — let alone generate $2.9 billion in adjusted EBITDA, as LPL did in 2025?

The answer lies in the layered economics of the platform model and the multiple revenue streams that flow from scale. LPL does not depend on a single margin on advisory revenue. Instead, it generates income from multiple touchpoints across the advisor and client relationship — some obvious, some hidden, and some controversial.

Advisory fees are the largest and fastest-growing revenue category. When an advisor manages a client's portfolio on a fee-based basis — typically charging 75 to 100 basis points of assets under management annually — LPL retains a small portion of that fee as a platform charge. To illustrate: if an advisor manages $100 million and charges clients an average of 1% annually, that generates $1 million in advisory fees. The advisor might keep $900,000 under their payout arrangement, while LPL retains $100,000. Now multiply that by the more than 32,000 advisors on the platform, many managing far more than $100 million, and the revenue scales enormously even on thin individual margins.

On $2.4 trillion in total assets, even a thin margin generates substantial revenue. The shift from commissions to advisory fees has been structurally positive for LPL because fee-based revenue is recurring and predictable — it accrues daily based on asset values, like a subscription — unlike commission-based revenue which fluctuates with transaction activity and market sentiment.

Client cash sweep revenue represents one of the most lucrative and controversial elements of LPL's business model. When clients hold uninvested cash in their accounts, LPL automatically sweeps that cash into FDIC-insured bank deposit accounts at partner banks. LPL negotiates the interest rate it pays to clients and the rate it earns from the banks, pocketing the spread. During the Federal Reserve's aggressive rate-hiking cycle of 2022-2023, this spread became extraordinarily profitable. LPL was earning upward of 3.2% from partner banks while paying clients as little as 0.35% in some cases — a spread of nearly 300 basis points on over $40 billion in cash balances.

To put this in perspective: a client with $500,000 sitting in a cash sweep account might earn $1,750 per year at 0.35%, while a money market fund might have paid 4% or more during the same period — a difference of nearly $18,000. Critics argued that clients were losing thousands of dollars annually without fully understanding the economics of the sweep arrangement.

This dynamic drew scrutiny. Multiple class-action lawsuits were filed in 2024, alleging that LPL's cash sweep rates were unconscionably low relative to prevailing market rates. The SEC opened an investigation. But in January 2026, the SEC informed LPL that it had concluded its investigation and did not intend to recommend an enforcement action — a significant resolution of what had been a meaningful regulatory overhang. The civil litigation remains ongoing but the regulatory risk has diminished substantially.

The self-clearing infrastructure that LPL built in 2000 continues to deliver structural advantages. By processing trades, settling securities, and maintaining custody of client assets internally, LPL avoids the per-transaction fees that competitors using third-party clearing firms must pay. More importantly, self-clearing gives LPL complete control over the client experience and comprehensive access to client data, enabling sophisticated analytics and personalized advisor tools. It is the invisible foundation upon which every other competitive advantage rests.

Transaction fees, margin lending interest, and institutional service charges provide additional revenue streams. LPL also generates significant revenue from advisor transition loans — forgivable loans extended to advisors who move their practices to LPL, which amortize over multi-year periods and are effectively a customer acquisition cost. In 2024, LPL had $2.14 billion in outstanding advisor loans, up 57% from $1.36 billion the prior year, reflecting the scale and intensity of its recruitment spending.

The institutional business — providing turnkey technology, clearing, and compliance platforms to banks, credit unions, and insurance companies — has emerged as a particularly high-margin growth vector. When Prudential Financial, Wintrust Financial, or other institutions partner with LPL, they bring thousands of advisors and billions in assets that generate revenue at minimal incremental cost, because the platform infrastructure is already built and paid for. The marginal cost of adding another advisor to a self-clearing, integrated technology platform is trivially small compared to the marginal revenue that advisor generates. This operating leverage is the fundamental economic engine of LPL's business model at scale.

The switching costs embedded in LPL's model are substantial and underappreciated. When a financial advisor affiliates with LPL, they invest significant time learning the technology platform, migrating client accounts, establishing new compliance workflows, and building relationships with LPL's support staff. Their clients receive statements, online portals, and account numbers that are specific to LPL's infrastructure. Moving to a different platform means repeating that entire process — re-papering accounts, learning new systems, disrupting client relationships, and absorbing the lost productivity of a transition that can take months. For most advisors, once they are on LPL's platform and established, the cost of switching exceeds any marginal benefit a competitor might offer.

There is a myth in the advisory industry that LPL is simply a "body shop" — a low-cost, low-service platform that attracts advisors purely on economics. The reality is more nuanced. While payout ratios are the primary recruiting tool, LPL has invested billions over the years in building a technology and service infrastructure that rivals what the wirehouses offer. The ClientWorks platform, the research department, the compliance infrastructure, the clearing capabilities, the institutional partnerships — these are not the hallmarks of a cut-rate operation. The company reported that advisors using its enhanced financial planning tools see approximately 53% higher revenue, a statistic that underscores the platform's role as a productivity multiplier, not just a low-cost provider.

This combination of high payout ratios for advisors, diversified revenue streams for the company, scale-driven cost advantages, and significant switching costs creates a business model that is both powerful and defensible. It is not without vulnerabilities — interest rate sensitivity, regulatory risk, and the ever-present challenge of maintaining service quality at scale are real concerns. But the structural economics of the platform model, at LPL's scale, are remarkably attractive.

IX. Playbook: Lessons for Builders

LPL Financial's fifty-seven-year journey from a small insurance securities cooperative to the largest independent broker-dealer in America — from $40 million in revenue to $15.6 billion, from 720 representatives to over 32,000 — offers lessons that extend well beyond financial services. These are patterns that recur across industries, and they are worth examining not just for what they tell us about LPL, but for what they reveal about how disruption and consolidation work in highly regulated markets.

The first and most fundamental lesson is the power of disrupting from below. This is perhaps the most instructive aspect of LPL's entire history, and it applies far beyond financial services. LPL did not try to outcompete the wirehouses by building a better wirehouse. It did not recruit the most prestigious advisors, open the most glamorous offices, or create the most exclusive client experiences. Instead, it recognized that thousands of financial advisors wanted something the wirehouses would never willingly provide: independence. LPL built infrastructure for that unmet need. The wirehouses dismissed the independent model for years as a refuge for second-tier advisors who could not make it on Wall Street. By the time they recognized the threat, LPL had captured an enormous share of the market for financial advice.

This pattern — the incumbent dismissing the disruptor because the disruptor's initial customers are not the incumbent's most valued customers — is one of the most reliable dynamics in business strategy. Clayton Christensen described it as disruptive innovation. Hamilton Helmer might call it counter-positioning: LPL built a business model that the wirehouses could not copy without cannibalizing their own economics. A wirehouse cannot offer 90% payouts to advisors without destroying its own profitability. It cannot embrace genuine advisor independence without undermining its ability to push proprietary products and maintain brand consistency across thousands of offices.

The second lesson is the strategic value of owning the infrastructure layer — of being the platform rather than the participant. LPL's decision to build self-clearing capabilities, to invest in its own technology platform, and to create proprietary compliance systems gave it control over the entire value chain of independent financial advice. This is the Amazon Web Services analogy: by building the platform that others run their businesses on, LPL created a position that is both highly profitable and extremely difficult to displace. Every advisor who joins LPL strengthens the platform by adding to the data, the scale economics, and the switching costs. Every advisor who leaves bears enormous transition costs.

The third lesson involves the PE-to-public-markets transition. Hellman & Friedman and TPG's investment in LPL in 2005 was a masterclass in private equity value creation. They did not simply lever up the company and extract dividends. They invested in professionalizing the management team, building systems and governance, and scaling the business to a size that could sustain public market scrutiny. The result was an IPO that created value for all stakeholders — PE sponsors, company management, and the advisors who had equity participation. The lesson for builders is clear: the best PE partnerships are not purely financial — they are operational. The PE sponsors brought not just capital but management expertise, governance frameworks, and a roadmap to public markets that LPL's entrepreneurial founders could not have built alone.

The fourth lesson is about roll-up strategy in fragmented industries. LPL has been the primary consolidator in the independent broker-dealer space, acquiring NPH, Waddell & Reed, Atria, and Commonwealth in a series of increasingly large deals. The playbook is consistent: acquire the firm, migrate advisors to LPL's platform, realize cost synergies from eliminating redundant technology and compliance infrastructure, and retain advisors through a combination of superior economics and technology. Each acquisition makes the next one easier because the platform has more scale to absorb the new advisors and more synergies to extract. The playbook also becomes more credible with each successful execution — advisors at the next acquisition target can look at previous integrations and see that the transition, while disruptive, ultimately delivered a better platform and more resources.

But the Commonwealth acquisition also illustrates the limits of roll-up strategy. When the asset you are acquiring is primarily cultural — advisor loyalty, service reputation, community identity — the standard integration playbook may not apply. The attrition of approximately 400 Commonwealth advisors since the acquisition announcement is a reminder that not all value can be captured by migrating accounts to a new technology platform.

The fifth lesson is about the paradox of culture in acquisitions. LPL's acquisition of Commonwealth Financial Network illustrates a challenge that every roll-up acquirer eventually confronts: when the primary value of the target is cultural rather than financial, the act of acquiring it may destroy the very thing you paid for. Commonwealth's advisors chose the firm because it was not LPL — because it was smaller, more personal, more attentive. LPL paid $2.7 billion for that culture, and now faces the difficult task of preserving it within a much larger organization. The early attrition numbers suggest this is harder than the deal models assumed. For any builder contemplating a roll-up strategy in a relationship-driven industry, the Commonwealth experience is a cautionary case study worth watching closely.

The sixth lesson is about balancing growth with regulatory compliance. LPL's long list of regulatory sanctions — 190 and counting from state and federal regulators — might seem alarming. But it reflects an inherent tension in the independent broker-dealer model: LPL is responsible for supervising the activities of thousands of independent advisors whom it does not directly employ or control. Every advisor interaction with every client is a potential compliance event. The company must monitor trades, review communications, audit fee disclosures, and ensure suitability or best-interest standards are met — across tens of thousands of advisor-client relationships, in real time. LPL's investment in centralized compliance technology, its engagement with regulators, and its willingness to pay fines and remediate failures are all part of the cost of operating at scale in a heavily regulated industry. The $50 million SEC fine for off-channel communications in 2024 — part of an industry-wide sweep that hit Ameriprise, Raymond James, and Edward Jones for identical amounts — illustrates that these costs are not unique to LPL but are endemic to the industry.

X. Bear & Bull Case Analysis

Bull Case

The structural tailwinds behind LPL Financial are among the most durable in financial services. The secular trend toward independent financial advice shows no signs of slowing. Every major wirehouse in America continues to lose advisors to independence, and LPL captures roughly 10% of all brokers leaving wirehouses and regionals, along with approximately 25% of all moves by independent brokers. With an estimated 27,000 advisors expected to retire by 2033, representing $2.7 trillion in client assets that will need succession solutions, LPL's platform is positioned as the natural landing place for practices in transition.

Scale advantages compound over time, and in a way that is difficult for competitors to overcome. Consider the math: LPL spends roughly $1.8 billion annually on core general and administrative expenses, which covers technology development, compliance infrastructure, clearing operations, and corporate overhead. Spread across more than 32,000 advisors and $2.4 trillion in assets, that cost per advisor is roughly $56,000 per year — a figure that would be ruinous for a smaller firm with 2,000 advisors but is easily absorbed by the revenue each LPL advisor generates. Every new advisor who joins the platform generates incremental revenue at minimal incremental cost. Competitors operating at one-tenth LPL's scale simply cannot match its per-advisor investment in technology and compliance without charging significantly higher platform fees — which makes them less competitive in recruiting, which keeps them smaller, which keeps their per-advisor costs higher. It is a classic scale economy flywheel.

The institutional partnership channel — providing turnkey wealth management infrastructure to banks, credit unions, and insurance companies — represents a growth vector that most investors underappreciate. The Prudential, Wintrust, and Atria relationships demonstrate that large financial institutions increasingly prefer to outsource the complexity of wealth management to a specialized platform provider rather than build the capability internally. This is analogous to the shift from on-premise software to cloud computing: institutions are choosing to rent LPL's infrastructure rather than own their own.

Technology investment creates a widening moat. LPL's ClientWorks platform, enhanced by the Blaze Portfolio acquisition and ongoing investments in artificial intelligence and advisor workflow automation, is creating an experience gap that smaller competitors cannot close. The company reported that advisors using enhanced planning tools see approximately 53% higher revenue — a powerful demonstration of how technology investment translates directly into advisor productivity and, therefore, into LPL's revenue.

Bear Case

Regulatory risk remains LPL's most persistent vulnerability. The company has paid an estimated $183 million or more in cumulative regulatory penalties since 2000, and the frequency of enforcement actions shows no sign of declining. Major fines in 2024 alone included a $50 million SEC penalty for off-channel communications violations and $6 million in FINRA fines for supervisory lapses. Each new enforcement action creates reputational risk that competitors exploit in recruiting conversations. More fundamentally, the evolving regulatory landscape — including potential future iterations of fiduciary rules — could increase compliance costs and constrain business practices in ways that are difficult to predict.

Fee compression is a structural headwind that even LPL's scale cannot fully offset. The average advisory fee charged to clients has been declining across the industry for years, squeezed by competition from low-cost digital platforms, increased price transparency, and client awareness. Vanguard's Personal Advisor service charges just 30 basis points. Schwab's Intelligent Portfolios charges nothing for basic portfolio management. These services are not perfect substitutes for a human advisor managing complex financial situations, but they set client expectations about what financial advice should cost.

While LPL's unit economics are strong at current fee levels, a sustained decline in the average fee charged per dollar of assets under management would pressure revenue growth even if total assets continue to rise. If the average advisory fee drops from 100 basis points to 80 basis points over the next decade — a plausible scenario given competitive dynamics — LPL would need 25% more assets just to maintain the same revenue level. Scale helps absorb fee compression, but it does not eliminate it.

Interest rate sensitivity is a real and meaningful risk. Client cash sweep revenue contributed approximately $1.66 billion in 2025, making it a material portion of total revenue. To understand the mechanics: when the Federal Reserve raises interest rates, the rates that LPL's partner banks pay on deposited cash rise, but the rates LPL passes through to clients rise more slowly, widening the spread. Conversely, when the Fed cuts rates, the spread compresses because bank rates fall while client expectations for yield remain sticky. This creates a powerful earnings tailwind in rising rate environments and an equally powerful headwind when rates decline. The stock's decline of roughly 25% from its mid-2025 all-time high reflects, in part, market anxiety about this sensitivity as the Federal Reserve has cut rates. For investors, the cash sweep business effectively makes LPL a leveraged bet on interest rates in addition to being a bet on the independent advisor movement — a duality that complicates the investment thesis.

Integration execution risk is elevated — perhaps the highest it has ever been in LPL's history. The company is simultaneously digesting multiple large acquisitions — Atria, Prudential, and Commonwealth — each with its own technology migration timeline, advisor retention challenges, and cultural integration requirements. The Commonwealth acquisition alone involves converting approximately $285 billion in assets and 3,000 advisors onto LPL's platform by the end of 2026. History suggests that large-scale advisor migrations are inherently messy, and the attrition of roughly 400 Commonwealth advisors since the deal's announcement is an early warning sign.

Through the lens of Porter's Five Forces, the independent broker-dealer industry presents a nuanced picture. Barriers to entry are high — self-clearing capabilities, compliance infrastructure, and technology platforms require enormous capital investment — but the threat of substitutes is real and growing. Direct-to-consumer platforms, low-cost index funds, and AI-powered financial planning tools all nibble at the edges of the human advisor value proposition. Buyer power is moderate: individual advisors have meaningful choice among platforms, but the switching costs once affiliated are substantial. Supplier power — from technology vendors, clearing banks, and regulators — is manageable but rising. And competitive rivalry, while intense, is increasingly concentrated among fewer and larger players, which tends to favor the incumbent scale leader.

Under Hamilton Helmer's 7 Powers framework, LPL's most defensible powers are scale economies (spreading fixed technology and compliance costs across the largest advisor base), switching costs (the friction of migrating advisor practices between platforms), and counter-positioning (a business model that wirehouses cannot replicate without destroying their own economics). The company also benefits from a form of network effects: as LPL's platform grows, it attracts more technology vendors, more product sponsors, and more institutional partners, creating an ecosystem that becomes more valuable with each participant.