Grand Canyon Education Inc.: The Story of America's Most Controversial Education Innovator

I. Introduction and Episode Roadmap

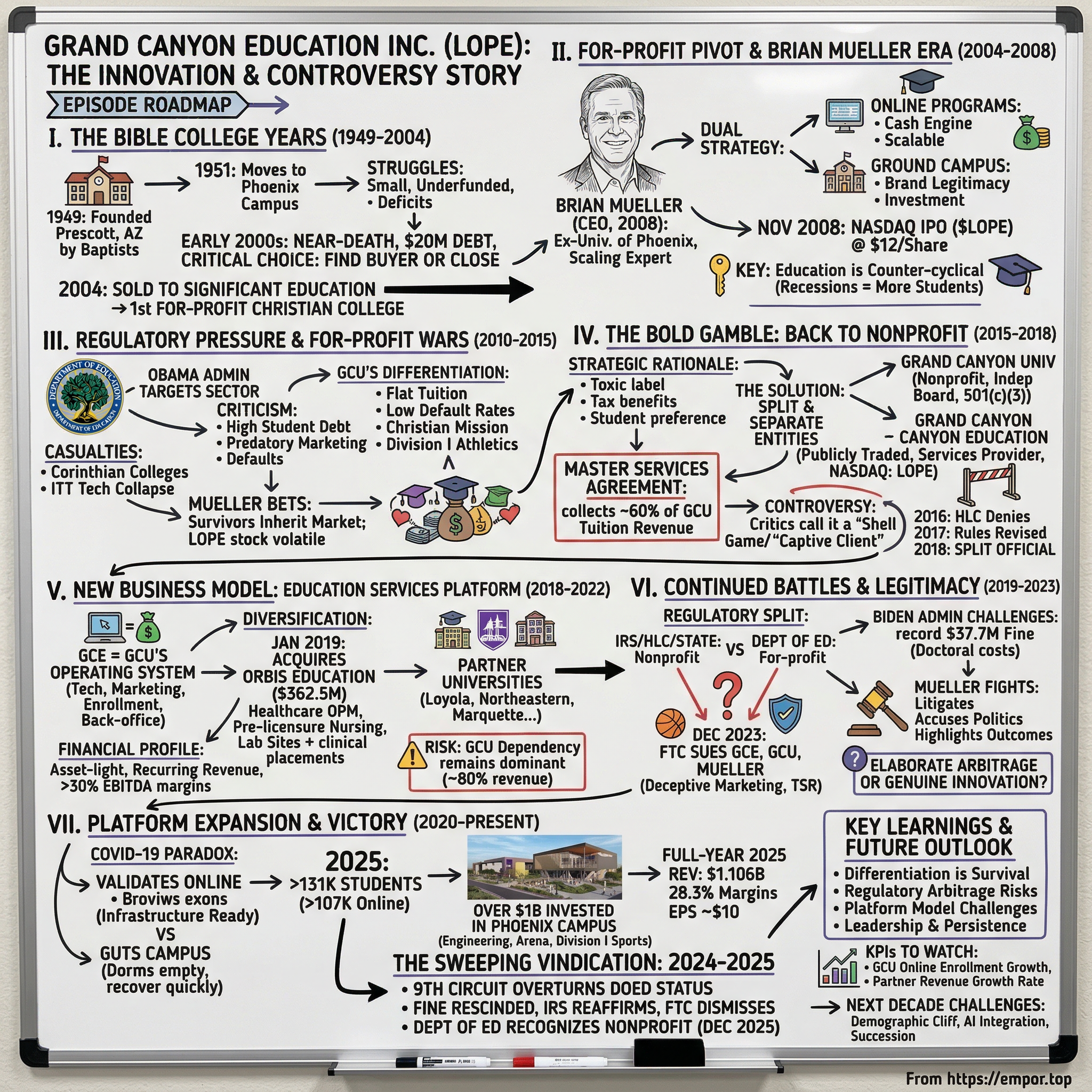

There is a building in Phoenix, Arizona, that tells one of the strangest stories in American capitalism. It sits on the campus of Grand Canyon University, a sprawling purple-and-white complex with a 7,000-seat arena, state-of-the-art engineering labs, and residence halls that would make many Ivy League schools envious. The university that owns this campus is a nonprofit. But the company that built it, runs its marketing, manages its technology, enrolls its students, and collects roughly sixty cents of every tuition dollar is a publicly traded, for-profit corporation listed on the NASDAQ under the ticker LOPE.

Grand Canyon Education Inc., with a market capitalization hovering around $4.5 billion as of early 2026, is perhaps the most paradoxical company in American higher education. It is a for-profit services company whose primary client is a nonprofit university that it itself created. The university could not function without the company. The company derives the vast majority of its revenue from the university. They share a CEO. They share a campus. And yet, legally, they are entirely separate entities.

The story of how this arrangement came to be is a seventy-seven-year saga that touches on nearly every tension in American higher education: access versus accountability, mission versus money, innovation versus regulation, and the eternal question of whether the profit motive has any place in educating the next generation. It begins with a group of Arizona Baptists who wanted a college of their own, nearly ends in bankruptcy, takes a sharp turn into the world of for-profit education, survives a decade of regulatory warfare, and arrives at a business model that has no true precedent in American history.

The major themes running through this story are regulatory arbitrage at its most creative, the brutal politics of the for-profit education wars, and the emergence of what might be called a "third way" business model that sits somewhere between the nonprofit and for-profit worlds.

Whether Grand Canyon Education represents a genuine innovation in how we deliver higher education or an elaborate end-run around the rules designed to protect students depends very much on whom you ask. What is undeniable is that few companies have navigated as treacherous a regulatory landscape with as much tenacity, or generated as much controversy in the process.

II. The Bible College Years: Founding to Near-Death (1949-2004)

In September 1949, the Arizona Baptist Convention did something that Baptist conventions across the American South and West had been doing for decades: they founded a college. Grand Canyon College, as it was christened, opened its doors in a converted National Guard armory in Prescott, Arizona, a small mountain town about a hundred miles north of Phoenix. The idea was simple and practical. Arizona's Baptists were tired of sending their children to Texas or Oklahoma for a Christian education. They wanted something closer to home.

The postwar boom in Christian higher education was real. The GI Bill was flooding campuses with returning veterans, and denominations across America were rushing to build institutions that could serve both the spiritual and educational needs of their communities. Grand Canyon College was part of this wave, though it was never among its more prominent members. It was small, regional, and perpetually underfunded, the kind of school that survived on faith and the modest generosity of its Baptist constituency.

Two years after its founding, on October 8, 1951, the college relocated to Phoenix, moving to the western part of the city and the campus it still occupies today. The move was significant. Phoenix in the early 1950s was a booming Sun Belt city, its population tripling between 1940 and 1960 as military veterans, retirees, and young families poured into the valley. Grand Canyon College, however, did not ride that wave of growth. For the next three decades, it was exactly what you would expect: a small Christian liberal arts institution offering degrees in education, nursing, and ministry, struggling to maintain enrollment, fighting for regional accreditation, and running deficits more years than not. It was the sort of school that showed up in nobody's rankings and changed the lives of many students who attended it.

The problem with small denominational colleges is that they depend on a constituency that is, by definition, limited. The Arizona Baptist Convention was not the Southern Baptist Convention. It did not have the deep pockets or vast membership of its parent denomination. Grand Canyon College's fundraising was modest, its endowment virtually nonexistent, and its operating budget perennially tight. The faculty was dedicated but poorly paid. The campus was functional but aging. The school survived on a combination of tuition revenue, convention support, and the sheer determination of administrators who believed in the mission.

The 1980s brought ambition and trouble in equal measure. In 1984, the board of trustees voted to pursue university status, a decision that reflected both genuine growth in programs and the marketing reality that "university" carried more prestige than "college" in the competition for students.

The name change became official in 1989, the school's fortieth anniversary, when it formally became Grand Canyon University. But the aspiration outpaced the economics. Enrollment was declining as competition for students intensified. Costs were rising as accreditation standards demanded investments in faculty, facilities, and student services. The university's Baptist constituency was aging and shrinking, and the convention's financial support was declining in real terms.

By the late 1990s, GCU had formally severed its ties with the Southern Baptist Convention, becoming nondenominational during the 1999-2000 academic year. The break was partly theological and partly financial. The convention could no longer sustain the school, and the school could no longer afford to limit itself to a shrinking denominational pool. It was a painful but necessary divorce, and it left GCU untethered from the institutional support network that had sustained it for half a century.

What followed was a slow-motion crisis. By the early 2000s, Grand Canyon University had accumulated roughly $20 million in debt, an enormous burden for a small school with limited revenue. Its accreditation with the Higher Learning Commission was under pressure. Enrollment had dwindled to barely a thousand students. The campus was deteriorating. The endowment was negligible. Faculty were leaving for more stable positions elsewhere.

The board of trustees faced a stark and increasingly urgent choice: find a buyer, merge with another institution, or close the doors. Closure was not hypothetical. Dozens of small denominational colleges had shut down in the preceding decades, their campuses converted to office parks or shopping centers, their histories reduced to footnotes. GCU was on the same trajectory.

What happened next was extraordinary and, at the time, unprecedented. In 2004, GCU's trustees sold the university to Significant Education, LLC, a California-based investment group founded by brothers Christopher and Brent Richardson in 2003 specifically for this purpose. The transaction converted Grand Canyon University from a nonprofit institution into a for-profit company, making it the first for-profit Christian college in the United States.

It was a legal maneuver that Arizona law permitted but that almost nobody in higher education had attempted. The conventional wisdom held that universities, particularly Christian universities, simply did not become businesses. The cultural and legal barriers were immense. But GCU's trustees were out of options, and the Richardson brothers saw an opportunity where others saw an impossibility. The Baptists' little college had just become a business, and the implications of that transformation would take another two decades to fully unfold.

III. The For-Profit Pivot and Brian Mueller Era Begins (2004-2008)

For four years after the for-profit conversion, Significant Education ran Grand Canyon University with mixed results. The school stabilized financially but did not transform. That transformation required a different kind of leader, one who understood both the mechanics of for-profit education and the soul of a campus-based institution. In the summer of 2008, they found him.

Brian Mueller grew up in a middle-class household in Wisconsin, one of eight children in a family where college was valued but not guaranteed. He studied secondary education at Concordia University, a small Lutheran school in Wisconsin, earned a master's in education, and spent his early career teaching history and coaching basketball at Christian schools and small colleges. From 1983 to 1987, he was a professor and head men's basketball coach at Concordia. He was, by training and temperament, a teacher and a competitor. But Mueller had a restless, entrepreneurial streak that coaching and classroom instruction could not contain.

In the late 1980s, Mueller moved to Arizona intending to pursue a doctorate at Arizona State University. The plan was academic. The reality was different. He walked into an enrollment counselor position at the University of Phoenix, one of the earliest and most aggressive for-profit universities in America, and never looked back. It was the kind of career-defining detour that, in retrospect, seems almost fated.

Over twenty-one years at Apollo Education Group, the parent company of the University of Phoenix, Mueller rose from that entry-level counselor role to become one of the most powerful executives in for-profit education. The ascent was steady and revealing. He moved through enrollment management, operations, and eventually into senior leadership. He served as Senior Vice President, then Chief Operating Officer, and ultimately CEO of the University of Phoenix Online, overseeing its growth from 3,500 students to an astonishing 340,000.

Think about that number for a moment. Under Mueller's operational leadership, a single division of a for-profit education company grew its enrollment by nearly a hundredfold. By 2006, he was president and a director of Apollo Education Group itself. He understood, better than almost anyone in the country, how to market higher education to working adults, how to build online enrollment operations at scale, how to convert inquiries into applications and applications into enrolled students, and how to use technology to deliver courses to people who would never set foot on a traditional campus.

But Mueller also understood something subtler. He had watched the University of Phoenix become a lightning rod for criticism. He had seen the regulatory scrutiny intensify, the media narratives harden, and the brand erode. He knew the vulnerabilities of the pure for-profit model: the dependence on federal financial aid, the political exposure, the reputational fragility. When he departed Apollo in June 2008, he carried with him not just a playbook for growth but a mental catalog of every mistake the for-profit sector had made.

Mueller arrived at Grand Canyon Education as CEO on July 1, 2008. His mandate was clear: turn GCU into a growth story. His playbook drew directly on his Phoenix experience but with a critical twist that would define his entire tenure.

Where the University of Phoenix had essentially abandoned the idea of a physical campus in favor of pure online scale, Mueller intended to do both. He would rebuild Grand Canyon University's aging Phoenix campus into a genuine collegiate experience, a real campus with dormitories, dining halls, athletics, and a sense of community, while simultaneously building a massive online enrollment machine. It was a dual strategy that skeptics said was impossible.

A ground campus is expensive, capital-intensive, and slow to scale. Online education is fast, efficient, and scalable. Doing both seemed like trying to be two different companies at once. But Mueller had a theory, and it was elegant in its simplicity. The online programs would be the cash engine. They could scale quickly with relatively low marginal costs, generating the cash flow needed to fund campus improvements. The campus improvements, in turn, would enhance the university's brand, create a physical symbol of legitimacy, and attract a different kind of student, the traditional eighteen-year-old who wanted a real college experience. The two sides of the business would feed each other in a virtuous cycle.

Mueller did not care about the skepticism. He began investing immediately in technology infrastructure, marketing systems, and enrollment operations. He also joined GCE's board as a director in March 2009 and would become Chairman in January 2017, consolidating his control over both the company's strategy and its governance.

The timing of what came next was either terrible or inspired, depending on your perspective. On November 20, 2008, in the teeth of the worst financial crisis since the Great Depression, Grand Canyon Education went public on the NASDAQ. The IPO priced at $12 per share, with Credit Suisse and Merrill Lynch as joint book-running managers, alongside co-managers BMO Capital Markets, William Blair, and Piper Jaffray. The offering sold 10.5 million shares. Lehman Brothers had collapsed two months earlier. The S&P 500 was down more than forty percent from its peak. Banks were failing. Credit markets were frozen. And here was a for-profit college in Phoenix asking investors to buy in.

But Mueller understood something about recessions that many CEOs do not. When the economy collapses, people go back to school. They lose jobs and seek new credentials. They look for affordable, flexible options that let them study while they search for work or hold down part-time employment. Grand Canyon University, with its online programs and its relatively low tuition, was positioned to be exactly that option. Education is one of the few industries that is genuinely counter-cyclical. Bad economies are good for enrollment, and the 2008-2009 recession was very, very bad.

The results were staggering. Enrollment surged from roughly 1,000 students at the time of the for-profit conversion to over 20,000 within just a few years. Online enrollment was the primary driver, powered by the digital marketing and enrollment conversion machine that Mueller had built from his University of Phoenix playbook. But the ground campus was growing too. Mueller was pouring money into dormitories, classroom buildings, and student amenities, betting that the physical campus would differentiate GCU from the pack of online-only for-profits that were sprouting up across the country. The formula was working. Cash was flowing. The stock began to climb. What had been a dying Baptist college was rapidly becoming one of the fastest-growing universities in America, and one of the most profitable companies on the NASDAQ. But the growth attracted attention, and not all of it was welcome.

IV. The For-Profit Education Wars and Regulatory Pressure (2010-2015)

The Obama administration came into office in 2009 with the for-profit education sector squarely in its crosshairs. The numbers were damning. For-profit colleges enrolled roughly ten percent of all postsecondary students but accounted for nearly half of all student loan defaults. The sector's marketing-driven enrollment model, critics charged, was designed to maximize tuition revenue from federal financial aid rather than to educate students. The phrase "predatory institution" entered the mainstream vocabulary. Documentaries, investigative reports, and congressional hearings painted a picture of an industry that was, at best, failing its students and, at worst, actively defrauding them.

To understand why this matters for the GCE story, you need to understand how federal student aid works. Title IV of the Higher Education Act authorizes the federal government to provide financial aid, including Pell Grants and subsidized student loans, to students attending accredited institutions. For-profit colleges, like all accredited schools, could access these funds. The problem was that many for-profits had built their entire business model around capturing as much Title IV money as possible, spending heavily on marketing to enroll students who would borrow federal dollars to pay tuition, regardless of whether those students were likely to graduate or find employment. The students got debt. The schools got revenue. And the federal government, meaning taxpayers, absorbed the losses when borrowers defaulted.

The regulatory assault was comprehensive. The Department of Education introduced "gainful employment" rules, which threatened to cut off federal aid to programs whose graduates carried too much debt relative to their earnings. The existing "90/10 rule" already required that for-profits derive at least ten percent of their revenue from sources other than federal Title IV financial aid, a constraint that forced schools to constantly demonstrate they were not simply federal aid harvesting operations. State attorneys general launched investigations. The Senate HELP Committee, chaired by Tom Harkin, produced a devastating report in 2012 documenting widespread abuse across the sector, including deceptive marketing, inflated job placement statistics, and student outcomes that were vastly worse than what the schools advertised.

The casualties mounted. Corinthian Colleges, which had enrolled more than 70,000 students, collapsed in 2015 after the Department of Education restricted its access to federal aid. ITT Technical Institute, one of the oldest for-profit chains, shut down in 2016. Enrollment at the University of Phoenix, Mueller's old employer, cratered from its peak of nearly half a million students to a fraction of that. Stock prices across the sector were obliterated. Investors fled.

Grand Canyon University was caught in the crossfire, but Mueller had been preparing for this fight since the day he arrived. His strategy was to differentiate GCU so aggressively from the rest of the sector that regulators and the public would see it as something fundamentally different. Where other for-profits were closing campuses, GCU was building them. Where others were raising tuition, GCU kept it flat. Where others were loading students with debt, GCU pointed to its comparatively low default rates and manageable student loan balances. And where others had abandoned any pretense of institutional identity, GCU leaned hard into its Christian mission, its Division I athletics program, and its increasingly impressive Phoenix campus.

The strategy was not just defensive. It was a calculated bet that the for-profit sector would thin out, that the weakest operators would be destroyed by regulation, and that the survivors would inherit a massive market of working adults and nontraditional students who needed affordable, accessible higher education. Mueller was not trying to save the for-profit model. He was trying to transcend it.

The Higher Learning Commission's regional accreditation was critical to this positioning. Unlike the national accreditors that blessed many for-profit schools, HLC accreditation put GCU in the same category as state universities and established private colleges. It was a mark of legitimacy that Mueller guarded fiercely and used constantly in marketing and regulatory arguments.

Through this period, LOPE stock was a roller coaster, trading between roughly $15 and $60 as investor sentiment toward the entire sector swung wildly. Every regulatory announcement, every congressional hearing, every headline about predatory lending sent shockwaves through the stock. But beneath the volatility, the business was performing. Enrollment kept growing. Revenue kept rising. Margins remained strong. Mueller's bet that GCU could survive the regulatory storm by being genuinely better than its peers was, quarter by quarter, proving correct.

The key inflection point of this era was Mueller's decision to double down on the ground campus while every other for-profit operator in America was retreating. It was expensive and counterintuitive. But it gave GCU something that no amount of marketing could manufacture: physical proof that this was a real university with a real campus and a real community. Students could visit. Parents could see the dorms. NCAA basketball games were on television. That tangibility, in an era when "for-profit college" had become synonymous with fraud, was invaluable.

V. The Bold Gamble: Converting Back to Nonprofit (2015-2018)

In 2015, Brian Mueller announced something that made Wall Street analysts do a collective double-take. Grand Canyon University, the for-profit success story he had spent seven years building, was going to convert back to nonprofit status. The university that had been saved from death by becoming a business was going to become a nonprofit again.

The strategic rationale was multilayered and characteristically Muellerian in its audacity.

First, the regulatory environment was only getting worse for for-profits. Despite GCU's differentiation strategy, it still carried the for-profit label, and that label was toxic. Every new regulation, every new investigation, every new headline about predatory colleges tainted GCU by association.

Second, nonprofit status brought tangible benefits: eligibility for tax-exempt bonds, access to philanthropic donations, exemption from property and income taxes, and the ability to market to prospective students as a nonprofit institution.

Third, and perhaps most importantly, Mueller had observed that students overwhelmingly preferred to attend nonprofit schools. The brand advantage was real and measurable in enrollment data. When a prospective student compared two online programs, one from a nonprofit and one from a for-profit, the nonprofit won almost every time, regardless of quality or price.

But there was an enormous problem. Grand Canyon Education was a publicly traded company. Its shareholders owned not just the services operation but the university itself. How do you convert a publicly traded university back to nonprofit status without either destroying shareholder value or creating a structure that regulators would view as a sham?

Mueller's solution was elegant, unprecedented, and immediately controversial. The plan was to split Grand Canyon into two entities.

Grand Canyon University would become an independent nonprofit institution, governed by its own board of trustees, with a mission-driven mandate and tax-exempt status. Grand Canyon Education Inc. would remain a publicly traded company on the NASDAQ, but it would no longer own or operate a university. Instead, it would become a third-party education services provider, offering technology, marketing, enrollment management, student support, and back-office operations to GCU under a long-term master services agreement.

Think of it like this: imagine if Apple spun off its retail stores as a separate nonprofit entity, but the stores still paid Apple sixty cents of every dollar they took in for the technology, logistics, and brand management that Apple provided. The stores would be nonprofit. Apple would remain for-profit. And the two entities would be legally separate but economically inseparable.

The financial terms of that agreement were where things got interesting and where critics sharpened their knives. Under the master services agreement, GCE would receive approximately sixty percent of GCU's tuition revenue in exchange for its comprehensive suite of services. The agreement was structured as a long-term contract, essentially making GCU a captive client of GCE. The university would get its nonprofit status and all the benefits that came with it. The public company would retain its revenue stream, its margins, and its ability to compensate employees with stock options. Both entities would share a CEO in Brian Mueller.

The first attempt at conversion hit a wall. In 2016, the Higher Learning Commission denied GCU's application, ruling that the services agreement with GCE violated the accreditor's existing guidelines on institutional independence. Mueller did not give up. He lobbied HLC to revise its guidelines, and in 2017, HLC did exactly that, creating a new framework that permitted the kind of services agreement GCU was proposing. GCU reapplied, and in July 2018, the Higher Learning Commission approved the change in ownership. The IRS simultaneously granted GCU 501(c)(3) tax-exempt status. The split was official.

The immediate reaction was polarized. Supporters hailed it as an innovative solution that preserved the benefits of public company efficiency while restoring the mission-driven governance of a nonprofit university. Critics called it a shell game, a corporate restructuring designed to look like a mission-driven conversion.

The Department of Education was not persuaded. In November 2019, despite the HLC and IRS approvals, the Department ruled that it would continue to treat GCU as a for-profit institution for Title IV federal financial aid purposes. The Department's analysis was blunt: the primary purpose of the transaction was to "drive shareholder value" for GCE, GCU was a "captive client, potentially in perpetuity," and the sixty-percent revenue share meant that GCU was functionally still a for-profit enterprise.

The phrase "captive client" would become the central term in the debate. It implied that GCU had no real independence, no real governance autonomy, and no real ability to negotiate with GCE at arm's length. If that was true, the nonprofit conversion was form without substance, a label change with no change in economic reality.

Mueller, characteristically, went to war. GCU sued the Department of Education, launching a legal battle that would consume years and millions of dollars. The market, after initial confusion, began to see the new structure more clearly. LOPE stock rose as analysts modeled the business and recognized that the separation, whatever its regulatory status, had created a genuinely attractive financial profile: an asset-light services company with high margins, recurring revenue, and a deeply embedded client relationship. The boldest gamble in Mueller's career was underway, and its outcome would not be clear for years.

VI. The New Business Model: Education Services Platform (2018-2022)

With the separation complete, Grand Canyon Education entered a new phase of its corporate existence. It was now, in essence, an OPM, an Online Program Management company. But calling GCE an OPM was like calling Amazon a bookstore. The label was technically accurate and completely inadequate to describe what the company actually did.

Traditional OPM companies partnered with universities to help them launch and manage online degree programs. They typically provided marketing, enrollment support, and technology platforms in exchange for a share of tuition revenue, usually somewhere between forty and seventy percent. The relationships were contractual and, in many cases, contentious. Universities often felt that OPMs took too large a share of revenue while exerting too much control over the student experience.

For context, think of how a hotel management company like Marriott operates hotels it does not own. The property owner gets the real estate value and the brand. The management company gets a fee for running the day-to-day operations. OPMs work similarly: the university owns the degree and the accreditation, and the OPM handles the operational machinery of delivering it online. The model was under increasing scrutiny from regulators who worried that it created incentives to enroll students regardless of their likelihood of success.

GCE's relationship with GCU was fundamentally different. This was not a vendor serving a client. This was a company that had built, over more than a decade, every system that the university used to operate.

The technology platform, the learning management system, the customer relationship management tools, the marketing automation, the enrollment call center operations, the financial aid processing, the student advising infrastructure, all of it had been developed internally at GCE over fifteen years. GCU did not choose GCE from a menu of OPM options. GCE was GCU's operating system.

The advantages of the new structure were real and significant on both sides.

For GCU, the benefits were transformative. It could now receive tax-deductible donations. It could issue tax-exempt bonds to fund campus construction at lower interest rates than a for-profit borrower would pay. It was exempt from property and income taxes. And it could market itself to prospective students as a nonprofit university, removing the single biggest stigma that had hung over its brand.

For GCE, the advantages were equally compelling. It maintained access to public capital markets and all the financial flexibility that entailed. It could compensate its employees, including Mueller, with equity-based compensation that aligned their incentives with stock performance. And it retained the high-margin, recurring-revenue financial profile that made it attractive to growth investors.

But Mueller knew that a company deriving eighty percent or more of its revenue from a single client was fundamentally vulnerable, no matter how strong that relationship was. Diversification was not just strategically desirable; it was existentially necessary. In January 2019, GCE acquired Orbis Education Services for $362.5 million, funded with cash and debt. Orbis was a niche OPM that had built a clever model around pre-licensure healthcare programs, particularly nursing. Its approach combined online coursework with physical off-campus laboratory sites where students could practice clinical skills, paired with guaranteed clinical placements at healthcare partner institutions.

The Orbis acquisition gave GCE a foothold in the broader OPM market and, crucially, a different kind of platform for growth. Orbis was not a generic OPM. It had built a highly specialized model around pre-licensure healthcare programs, the kind where students needed both classroom instruction and hands-on clinical experience. Orbis operated physical off-campus laboratory sites, essentially small training facilities located near partner healthcare systems, where nursing students could practice clinical skills before entering real hospital settings. It also managed the clinical placement process, securing guaranteed rotations at partner hospitals and health systems. This combination of online coursework, physical lab space, and clinical placement management was difficult to replicate and addressed a genuine bottleneck in American healthcare: the chronic shortage of nurses caused partly by a shortage of nursing school capacity.

The pitch to other schools was compelling: look at what we did with GCU. We took a failing institution with a thousand students and turned it into a university with over a hundred thousand. Let us do the same for your healthcare programs. Early partner wins included relationships with institutions like Loyola University Chicago, Northeastern University, Marquette University, Mercer University, and several others. The partners were primarily traditional nonprofit universities with strong reputations that wanted to expand their nursing and healthcare programs but lacked the infrastructure, marketing capability, or clinical partnerships to do so on their own.

The margin story was compelling for investors. GCE was generating EBITDA margins above thirty percent, with an asset-light model that required relatively little capital expenditure beyond technology development and the modest cost of operating Orbis lab sites. Revenue was recurring and predictable, driven by semester-based enrollment cycles. The technology platform, built over fifteen years and refined through the experience of serving more than a hundred thousand students, was proprietary and deeply integrated. It included not just a learning management system but a full customer relationship management suite, marketing automation tools, enrollment workflow systems, financial aid processing infrastructure, and student advising platforms. It was not the kind of thing a competitor could replicate in a year or two.

The diversification effort was real, but it was also slower than the most bullish projections had assumed. Signing new university partners proved harder than Mueller had hoped. Many universities were hesitant to partner with any OPM, let alone one associated with the controversial Grand Canyon brand. University provosts and faculty senates were skeptical of the revenue-sharing model, which they viewed as surrendering too much control and too much money to an outside company. The competitive OPM market was crowded, with established players like 2U, Academic Partnerships, and Coursera all vying for the same institutional clients. And an increasing number of universities were choosing to build their online capabilities in-house rather than outsource them to a third party, a trend accelerated by the forced experiment with remote learning during COVID-19.

By 2022, GCE had signed roughly twenty-five university partners through Orbis, with several thousand students enrolled at off-campus sites. It was meaningful growth, but partner revenue still represented a small fraction of the total. The GCU relationship remained dominant, accounting for approximately eighty percent of GCE's revenue. The diversification story was a work in progress, and its ultimate success remained uncertain.

VII. Continued Regulatory Battles and Legitimacy Questions (2019-2023)

The Department of Education's November 2019 denial of GCU's nonprofit status set the stage for a legal and political battle that consumed the next several years.

The denial created a bizarre regulatory split. The IRS recognized GCU as a 501(c)(3) nonprofit. The Higher Learning Commission accredited it as a nonprofit. The state of Arizona treated it as a nonprofit. But the Department of Education, the single most important federal regulator for any university because it controls access to Title IV student financial aid, classified GCU as for-profit. The practical consequence was that GCU remained subject to the more onerous regulations that applied to for-profit institutions, including the 90/10 rule and gainful employment reporting requirements. It was as if three judges ruled in your favor and the fourth, the one who controlled your bank account, ruled against you.

The situation became even more contentious under the Biden administration. The Department of Education levied a record $37.7 million fine against GCU, alleging that the university had substantially misrepresented the cost of its doctoral programs. The specific charge was that GCU advertised doctoral programs as requiring twenty courses totaling sixty credits, but that nearly all doctoral students were required to take additional "continuation courses" that added thousands of dollars in costs beyond the advertised price.

This was not a minor bookkeeping dispute. It struck at the heart of GCU's claim to be a more transparent, student-friendly alternative to predatory for-profits. If GCU was misleading students about the true cost of a doctorate, the entire differentiation narrative was in jeopardy.

Then, in December 2023, the Federal Trade Commission filed suit against both Grand Canyon Education and Grand Canyon University, with Brian Mueller personally named as a defendant. Being named personally was significant. It signaled that the FTC viewed Mueller not as a bystander but as a central architect of what it characterized as deceptive practices.

The FTC's complaint mirrored the Department of Education's doctoral program allegations and added charges of deceptive nonprofit marketing and violations of the Telemarketing Sales Rule. The agency alleged that GCE and GCU had marketed GCU as a nonprofit institution despite the fact that GCE, a for-profit company, collected sixty percent of the university's revenue, and that the two entities had made illegal telemarketing calls to individuals on the National Do Not Call Registry.

Mueller's response to all of this was characteristically combative. He fought every charge, challenged every ruling, and accused regulators of political persecution.

His argument was straightforward: look at the outcomes. GCU's graduation rates were above the national average for both online and campus-based programs. Student debt levels were manageable. Job placement rates were strong. The university had invested over a billion dollars in its Phoenix campus, creating thousands of jobs and transforming a neglected part of the city.

Whatever the regulatory classification said, GCU was doing what it was supposed to do: educating students and preparing them for careers. Mueller's posture was defiant in a way that few university presidents, and few corporate CEOs, would have dared. He did not negotiate or accommodate. He litigated.

The defense had merit, but it also had a whiff of "the ends justify the means" reasoning that made many observers uncomfortable. The structural question, whether it was appropriate for a publicly traded company to collect sixty percent of a nonprofit university's revenue in perpetuity, was not answered by pointing to graduation rates. It was a question about governance, about incentives, and about whether the nonprofit form meant anything if the economic substance was indistinguishable from a for-profit operation.

Congressional hearings added fuel to the fire. Media coverage drew frequent comparisons to the University of Phoenix and other for-profit operators whose abuses had been well documented. The irony was not lost on anyone that Mueller had come from the University of Phoenix, had helped build it into the largest for-profit university in America, and was now running a university that claimed to be fundamentally different from the institution he had left.

Throughout this period of regulatory uncertainty, the business continued to perform. Students kept enrolling. Revenue kept growing. Margins remained healthy.

Whatever Washington thought about GCU's organizational structure, the market of working adults and nontraditional students who needed affordable, accessible, online education continued to vote with their tuition dollars. It was a remarkable demonstration of the separation between regulatory headlines and operational reality.

The existential question, whether the GCE-GCU model was a legitimate innovation or an elaborate regulatory arbitrage, remained unanswered. Other universities around the country were watching closely to see whether the model would survive, because if it did, many of them were considering something similar.

VIII. The Modern Era: Platform Expansion and Market Position (2020-Present)

When COVID-19 shut down American higher education in March 2020, it created a strange paradox for Grand Canyon University.

On one hand, the virus validated everything Mueller had been saying for a decade about the importance of online education. Suddenly, every university in America was scrambling to do what GCU had been doing since 2008: deliver courses remotely to students who could not come to campus. GCU had the infrastructure, the technology, and the institutional experience. It was, in many ways, better prepared for the pandemic than almost any university in the country.

On the other hand, COVID temporarily gutted GCU's ground campus operation, the very thing that had differentiated it from every other for-profit or online-focused institution. The 25,000-plus students on the Phoenix campus went home, and the dormitories, dining halls, and classrooms that Mueller had invested so heavily in sat empty.

The recovery, when it came, was swift. GCU's online enrollment surged as displaced workers and career-changers sought new credentials. The ground campus bounced back as pandemic restrictions eased. By the end of 2025, total GCU enrollment had reached 131,826 students, with 107,148 enrolled in online programs and the remainder on the Phoenix campus.

To put those numbers in perspective: this was an institution that had enrolled roughly a thousand students two decades earlier. The growth from 1,000 to 131,000 represents a compounding rate that would be remarkable in any industry, let alone one as regulated and tradition-bound as higher education.

The campus transformation deserved its own chapter in the Mueller biography. Over fifteen years, GCE had invested more than a billion dollars in the Phoenix campus, turning what had been a collection of aging buildings into one of the most impressive university campuses in the American Southwest.

The investment included new dormitories, a 7,000-seat arena, an engineering school, science laboratories, a hotel and conference center operated by hospitality students, and an array of athletic facilities that supported GCU's NCAA Division I sports programs. The basketball team, in particular, had become a source of institutional pride and national visibility, making multiple NCAA tournament appearances and bringing television cameras to a campus that most Americans had never heard of a decade earlier.

Walk the campus today and it is hard to believe this was a school on the verge of closure two decades ago. The facilities are modern, well-maintained, and buzzing with activity. The purple-and-white color scheme is everywhere, a deliberate branding choice that gives the campus a cohesive, almost theme-park-like visual identity.

The brand that Mueller built around the campus was distinctive and deliberate. The Christian identity was front and center, not in a narrow, exclusionary way, but as a values-based proposition that resonated with a large segment of the American higher education market. Mueller positioned GCU as the "New Traditional University," a phrase that captured his ambition to combine the best of the traditional campus experience with the accessibility and efficiency of online education. It was a positioning statement that simultaneously appealed to traditional students looking for a campus experience and to working adults looking for a credible online degree.

The university partner expansion through Orbis continued, though the pace was slower than the most optimistic projections had suggested. By the end of 2025, GCE had signed relationships with roughly twenty-five to thirty university partners, primarily in healthcare fields. Enrollment at off-campus partner sites reached 5,738 students in the fourth quarter of 2025, growing at nearly seventeen percent year-over-year. It was solid growth, but still a small fraction of GCE's total business.

The challenges in diversification were real. The OPM market had become fiercely competitive and simultaneously skeptical. The spectacular collapse of 2U, which filed for Chapter 11 bankruptcy in July 2024 after years of declining enrollments and mounting losses, cast a shadow over the entire OPM model. Universities that had once been eager to outsource their online operations were increasingly bringing capabilities in-house. New entrants, including technology companies offering AI-powered tools, were fragmenting the market further. And GCE's association with the controversial GCU brand made some potential partners wary.

On the technology front, GCE was investing in artificial intelligence across its platform. Early experiments included AI-powered tutoring systems, automated grading tools, and predictive analytics for student advising. These were incremental improvements rather than revolutionary breakthroughs, but they reflected an awareness that the technology landscape was shifting rapidly and that GCE needed to evolve its platform to remain competitive.

The financial performance through this period told a story of consistent, profitable growth. Full-year 2025 revenue reached $1.106 billion, up just over seven percent from the prior year. Adjusted operating margins were 28.3 percent. Diluted earnings per share, as adjusted, were approximately $10 for the year.

The stock traded in a range between roughly $150 and $225 over the previous twelve months, reflecting both the company's strong fundamentals and the lingering uncertainty around regulatory and diversification questions. The company's 2026 guidance called for revenue between $1.17 billion and $1.19 billion, with adjusted operating margins around twenty-eight percent, implying continued steady growth.

But the most significant developments of this era were not financial. They were legal, and they came in rapid succession.

In November 2024, the U.S. Court of Appeals for the Ninth Circuit unanimously overturned the lower court's ruling and found that the Department of Education had applied the wrong legal standard in denying GCU's nonprofit status.

In March 2025, the Department of Education rescinded the $37.7 million fine with prejudice, with a joint stipulation confirming no findings, fines, liabilities, or penalties of any kind.

In May 2025, the IRS reaffirmed GCU's 501(c)(3) nonprofit status following a four-year audit, concluding that the university was "operating within the parameters of a 501(c)(3) entity."

In August 2025, the FTC voted three-to-zero to dismiss its lawsuit against GCE, GCU, and Mueller, citing the erosion of its case following the other regulatory resolutions.

And in December 2025, the Department of Education formally and officially recognized Grand Canyon University as a nonprofit institution of higher education, closing the final chapter of the six-year battle.

After six years of litigation, Mueller had won. Every regulatory challenge had been resolved in GCU's favor. The model that critics had called a "recipe for abuse" had been validated by every relevant federal authority. It was a sweeping vindication, and it removed the single largest overhang that had weighed on LOPE stock for half a decade. The sequence of victories was remarkable not just for their substance but for their comprehensiveness. Mueller had not just survived the regulatory gauntlet; he had run the table. The Ninth Circuit opinion, the IRS reaffirmation, the FTC dismissal, and the Department of Education recognition collectively established a body of legal and regulatory precedent that would make it substantially harder for any future administration to challenge the GCE-GCU structure. For investors who had held LOPE through the years of uncertainty, it was the resolution they had been waiting for. For the broader higher education industry, it was a signal that the hybrid model could work, at least legally, even if the debate about whether it should work continued.

IX. Business Model Deep Dive and Competitive Positioning

To understand how Grand Canyon Education makes money, start with the master services agreement with GCU. Under this contract, GCE provides essentially every non-academic function that a university requires: technology infrastructure, the learning management system, student enrollment and marketing, financial aid processing, student advising and support, facilities management, and back-office operations.

In exchange, GCE receives approximately sixty percent of GCU's tuition and fee revenue. With GCU generating over a billion dollars in annual tuition, this translates to roughly $600 million to $650 million flowing to GCE from the university alone. That single contract is, by itself, one of the largest and most profitable services relationships in American higher education.

The second revenue stream comes from Orbis Education and the university partner relationships. Here, GCE provides similar services, though typically with a narrower scope focused on specific programs, usually in healthcare. Revenue-sharing arrangements with partner universities vary but typically fall in the range of fifty to seventy percent of program revenue flowing to GCE. This segment generated a smaller but growing portion of total revenue, with partner enrollment growing at double-digit rates.

On the cost side, the biggest line item is marketing and student acquisition. GCE runs a sophisticated digital marketing operation, including search engine marketing, social media advertising, content marketing, and a large enrollment counselor team that manages the conversion funnel from inquiry to application to enrollment.

Think of it as a large-scale sales operation. A prospective student searches Google for "online nursing degree." GCE's marketing team has bid on that keyword, placed ads, and built landing pages designed to capture the student's contact information. An enrollment counselor calls within minutes. That counselor guides the student through the application process, helps with financial aid paperwork, and provides information about programs. This entire funnel, from keyword bid to enrolled student, is the core operational engine of GCE's business.

Technology costs, including platform development and maintenance, represent the second major expense category, followed by personnel costs for the thousands of employees who deliver the services GCE contracts to provide.

The GCU dependency is the single most important structural feature of GCE's business and simultaneously its greatest strength and greatest vulnerability.

On the strength side, the relationship is deeply embedded, contractually protected, and has no realistic alternative. GCU cannot simply switch to another services provider. GCE built and operates every system the university uses: the technology, the enrollment infrastructure, the marketing apparatus, the student support systems. The switching costs are not moderate; they are effectively infinite. Replacing GCE would be like ripping out the electrical wiring of a building while people are still living in it.

On the vulnerability side, if something were to fundamentally disrupt the GCU relationship, whether through regulatory action, contractual dispute, or GCU's decision to gradually in-source its operations, GCE would lose the vast majority of its revenue. This is the kind of concentration risk that would make any portfolio manager uncomfortable, and it is the primary reason LOPE has historically traded at a discount to what its margins and growth would otherwise justify.

The competitive landscape has shifted significantly in recent years. The traditional OPM model is under pressure from multiple directions.

The bankruptcy of 2U, once the most prominent publicly traded OPM, was a cautionary tale for the entire sector. 2U had built partnerships with elite universities including Yale, Georgetown, and the University of North Carolina, and at its peak had a market capitalization exceeding $6 billion. Its collapse in July 2024 demonstrated that the model's economics were fragile, particularly when growth slowed and universities pushed back on revenue-sharing terms. The 2U debacle also chilled the broader market for OPM partnerships, making university administrators even more skeptical of outsourcing their online operations.

Coursera has evolved from a MOOC platform into a degree marketplace but operates a fundamentally different model, one based on platform fees rather than revenue sharing. Academic Partnerships, which expanded by acquiring Wiley's university services assets, competes on price and volume in the lower end of the market.

GCE's differentiation rests on several factors.

Its integrated platform, developed over fifteen years of serving GCU, is more comprehensive than what most OPMs offer. Where a typical OPM might provide marketing and a learning management system, GCE provides the entire operational infrastructure of a university.

Its track record with GCU, turning a failing institution into a university with 130,000 students, is unmatched in the OPM industry. No other provider can point to a transformation of that magnitude.

Its focus on healthcare education through Orbis targets a market segment with strong demand fundamentals and high barriers to entry, since pre-licensure nursing programs require clinical placements and physical lab facilities that online-only competitors cannot provide.

And its association with the Christian higher education market gives it access to a niche that is large, underserved by technology-enabled providers, and culturally aligned with GCU's institutional identity.

The scalability question, however, remains open. GCE's success with GCU was built over fifteen years of investment, experimentation, and deep integration. Replicating that success with other university partners, each with their own culture, governance structure, and operational idiosyncrasies, is inherently harder. The Orbis model shows promise, but it operates in a narrow niche. Whether GCE can evolve from a company that serves primarily one client into a genuine platform company serving dozens or hundreds of institutions is the central strategic question for the next decade.

X. Playbook: Business and Strategic Lessons

The Grand Canyon Education story offers a remarkably rich set of lessons for business strategists, entrepreneurs, and investors. At its core, this is a turnaround story, and the playbook that Mueller and his team executed contains principles that apply well beyond higher education.

The first lesson is about differentiation as survival strategy. When Mueller arrived at GCU in 2008, the for-profit education sector was about to enter its darkest period. His response was not to hunker down and cut costs. It was to invest aggressively in everything that would make GCU look and feel different from every other for-profit school in America. The campus construction, the flat tuition, the Christian mission, the Division I athletics, all of it served a single strategic purpose: creating enough distance between GCU and the rest of the sector that regulators, students, and the public would see it as something categorically different. This was not cheap. It required hundreds of millions of dollars in capital expenditure at a time when the sector's access to capital was drying up. But it worked because it was grounded in a genuine commitment to building something better, not just in better marketing of the same product.

The second lesson is about regulatory arbitrage as a legitimate strategic tool, and its risks. The conversion from nonprofit to for-profit and then back to nonprofit, with the creation of a for-profit services company in between, was a masterclass in organizational design. Mueller and his team found a structural gap in the regulatory framework, the fact that a nonprofit university could outsource its operations to a for-profit services provider, and built an entire business model around it. This is not unlike what financial engineers do when they identify structural inefficiencies in tax codes or regulatory frameworks. But regulatory arbitrage carries a unique risk: the regulator can close the gap. GCE spent six years fighting to keep the gap open, and while it ultimately prevailed, the legal costs, management distraction, and stock price volatility were enormous. The lesson is that regulatory arbitrage can create value, but the entrepreneur must be prepared to defend the structure, potentially for years, against regulators who may view it as an abuse.

The third lesson is about capital allocation across organizational boundaries. GCE used public company cash flow, generated by efficiently operating a nonprofit university's services, to fund the growth of both the university and the services platform. This cross-entity capital allocation strategy was unusual and, to critics, troubling. But from a purely financial perspective, it allowed GCU to grow faster and invest more in its campus and programs than it could have as a standalone nonprofit with no access to public equity markets. The capital flowed from investors to GCE to GCU in the form of services, and the returns flowed back in the form of tuition revenue. It was a financial flywheel that created value for both entities.

The fourth lesson concerns the platform business model: the challenge and opportunity of building for one client and then scaling to many. GCE's technology platform was purpose-built for GCU. It was optimized for GCU's specific programs, student demographics, and operational workflows. Adapting that platform to serve other universities, with different needs and different cultures, proved harder than anticipated. This is a common challenge in enterprise software and services businesses. The first customer relationship is deep and productive, but the second and third customers expose all the assumptions and customizations that were built into the platform for customer number one.

The fifth and perhaps most important lesson is about leadership and persistence. Brian Mueller is a polarizing figure. To his supporters, he is a visionary who saved a dying institution, built a world-class campus, educated hundreds of thousands of students, and fought off every regulatory challenge thrown at him. To his critics, he is a for-profit education operator who found a clever way to extract value from a nonprofit institution while shielding himself from the regulatory consequences. Both characterizations contain truth. What is undeniable is that Mueller's willingness to pursue a strategy that no one else had attempted, to fight for it in courts and regulatory agencies for years, and to keep executing operationally while the legal battles raged, was extraordinary. Whether you admire the strategy or distrust it, the execution was remarkable.

XI. Bull vs. Bear Case and Strategic Analysis

The Bull Case

The resolution of every major regulatory challenge facing GCE and GCU represents a watershed moment for the company. For years, LOPE traded at a discount to its fundamental earning power because investors could not confidently model the impact of an adverse regulatory outcome. With the Department of Education, the IRS, and the FTC all having validated the GCE-GCU structure, that overhang has been removed. The base business is strong: GCU enrollment exceeded 131,000 students at the end of 2025, growing at seven percent annually, with online enrollment growing nearly nine percent. GCE's margins are healthy at roughly twenty-eight percent, and the company generates substantial free cash flow.

The diversification through Orbis is beginning to gain traction. Partner enrollment grew at nearly seventeen percent in 2025, and the healthcare education niche, particularly nursing, is supported by structural demand that will persist for decades as the American population ages and the nursing shortage intensifies. GCE's integrated platform, refined over fifteen years, represents genuine process power that competitors cannot easily replicate. The Christian higher education market is large, underserved by technology-enabled providers, and culturally aligned with GCU's institutional identity. And Mueller's track record of execution, while controversial, is objectively impressive.

The valuation argument is also compelling. At recent trading levels around $160 per share, LOPE traded at roughly sixteen to seventeen times trailing earnings, a reasonable multiple for a company generating double-digit earnings growth with strong margins and a defensible market position. If diversification accelerates and the regulatory all-clear continues to build investor confidence, there is room for both earnings growth and multiple expansion.

The Bear Case

The GCU dependency remains the elephant in the room. Despite the Orbis acquisition and the university partner expansion, GCU still accounts for approximately seventy-five to eighty percent of GCE's revenue. This is a concentration risk that would be alarming in any industry. If anything were to disrupt that relationship, whether through a change in GCU's governance, a new regulatory challenge, or GCU's decision to gradually bring services in-house, the impact on GCE would be devastating. The regulatory victories are real, but they do not guarantee permanence. A future administration with different priorities could reopen the questions that were resolved in 2024 and 2025. Regulatory risk in education is never truly extinguished; it is merely dormant between political cycles.

The OPM market itself is in a difficult transition. The bankruptcy of 2U in July 2024, after years of declining enrollment and mounting losses, demonstrated that revenue-sharing models are fragile and that even the largest OPM players can fail. Universities are increasingly skeptical of OPM partnerships and are building in-house capabilities, a trend that accelerated after COVID forced every school in America to develop some baseline competency in online education delivery. New Department of Education distance education regulations taking effect in July 2026 will increase reporting requirements and could impose additional constraints on how OPM relationships are structured and disclosed. The competitive landscape is fragmenting, with AI-powered tools potentially reducing the need for the comprehensive service bundles that GCE offers. If a university can use AI to automate student advising, personalize marketing, and optimize enrollment funnels, the value proposition of paying sixty percent of tuition to a third-party services provider becomes harder to justify.

Demographic headwinds are approaching. The "demographic cliff," a projected decline in the number of high school graduates beginning in the late 2020s, driven by lower birth rates following the 2008 financial crisis, will reduce the pool of traditional-age college students. While GCU's student body is predominantly nontraditional and online, the broader enrollment pressure will affect the entire higher education market and could intensify competition for students. When the pie shrinks, every slice gets smaller, and customer acquisition costs rise.

Mueller's age, approximately seventy-one, raises succession questions that the market has not yet priced in. He has been the architect of every major strategic decision at GCE for nearly two decades. The company's culture, strategy, regulatory posture, and institutional relationships are deeply shaped by his personality, his combative style, and the trust he has built with regulators, accreditors, and university partners over decades. No succession plan has been publicly disclosed. Whether GCE can maintain its strategic direction and execution quality under different leadership is an open question, and the transition, when it comes, will be one of the most closely watched leadership changes in the education sector.

Porter's Five Forces Assessment

The threat of new entrants is moderate to high for basic OPM services. The technology required to build a learning management system, run digital marketing campaigns, and manage enrollment funnels is increasingly commoditized. Dozens of startups and established tech companies offer components of what GCE provides. However, the barriers to replicating GCE's fully integrated platform, one that handles everything from first student inquiry to graduation and career placement, with a proven track record across 130,000 students, remain substantial. Building that integration takes years, not months.

Supplier bargaining power is low. GCE controls most of its critical inputs, having built its technology platform internally rather than depending on third-party vendors. Faculty and academic content come from the partner universities themselves, and while technology talent is competitive, it is broadly available in the Phoenix market and nationwide.

Buyer bargaining power presents a split picture. GCU, as GCE's primary client, is effectively captive. The switching costs for GCU are so high as to be functionally prohibitive; every operational system the university uses was built by GCE. But new partner universities have many OPM options and significant negotiating leverage. They can choose among GCE, Academic Partnerships, Coursera, or a growing list of specialized providers. The revenue-share model gives universities upside participation, which helps retain them, but also gives them a constant incentive to renegotiate or bring capabilities in-house if they believe they can do it more cheaply.

The threat of substitutes is the most significant competitive force facing GCE. Universities are increasingly building online capabilities internally. Alternative OPM providers offer different models, from fee-for-service arrangements to platform-based approaches. Direct-to-consumer education options, including bootcamps, micro-credentials, and corporate training platforms, are chipping away at the margins of traditional degree programs. And AI-powered teaching assistants, automated advising systems, and personalized learning tools are potentially reducing the labor intensity, and therefore the cost, of the services that GCE provides.

Competitive rivalry is moderate. The OPM market is fragmenting, with no dominant player controlling more than a small share of the total addressable market. GCE's specific niches, Christian higher education and healthcare programs, are less crowded than the broader OPM market. Price competition is limited by the focus on outcomes and program quality rather than pure cost. But the struggles and eventual bankruptcy of 2U, which was once the sector's bellwether, demonstrate that the market is unforgiving of execution failures and that even strong market positions can erode quickly.

Hamilton Helmer's Seven Powers Framework

Hamilton Helmer's framework asks a simple but powerful question: what gives a business durable pricing power and protection from competition? For GCE, the answer is nuanced and varies significantly across the seven powers.

Process power is GCE's strongest and most durable advantage. Fifteen years of refining enrollment operations, student retention systems, marketing funnels, and technology platforms through the experience of serving over 130,000 students has created organizational capabilities that are genuinely difficult to replicate. This is not about any single technology or system. It is about the accumulated learning embedded in thousands of operational decisions, workflow optimizations, and institutional adaptations. How do you convert a website visitor into an enrolled student? How do you identify students at risk of dropping out before they actually drop out? How do you optimize marketing spend across hundreds of degree programs and dozens of student demographics? GCE has been iterating on these questions for fifteen years, and the answers are encoded in its systems, its processes, and its institutional memory. A competitor could build a technology platform. Building the organizational learning that makes it effective would take years.

Counter-positioning was historically GCE's most powerful advantage. Traditional universities, governed by faculty senates, administrative bureaucracies, and boards of trustees with limited business expertise, simply could not match GCE's investment speed, marketing sophistication, or operational efficiency. Doing so would have contradicted their institutional cultures, their governance structures, and their self-image. A university provost proposing to spend fifty million dollars on digital marketing would have been laughed out of the faculty senate. Mueller spent it without asking. This advantage has eroded somewhat as the for-profit education crisis forced traditional universities to adopt more aggressive and commercially minded approaches. But the nonprofit-to-profit services model, the core structural innovation, remains difficult and politically risky to replicate.

Scale economies are moderate. GCE's platform fixed costs, particularly technology development and infrastructure, can be spread across a growing number of partners. But the customization required for each university relationship limits pure scale benefits. Every partner has different programs, different student demographics, different institutional cultures, and different compliance requirements. The scale benefits are real but not as powerful as in a pure software business.

Network effects are weak. There are no direct network effects between GCE's university partners. Each relationship is bilateral and independent. There are some modest data network effects, as GCE can apply insights learned from serving one university to improve its services for others, but these are incremental rather than transformative.

Switching costs are extremely high within the GCU relationship, where GCE is literally the operating system, but moderate for Orbis partners, where contracts are typically two to five years and the integration, while meaningful, is not as total.

Branding is moderate at the GCU level, where the university has built genuine brand recognition in the Southwest and among Christian and working-adult student populations, but weak at the GCE level, which is essentially invisible to students. Most people who attend GCU-partnered programs have no idea that GCE exists.

Cornered resources include Mueller's expertise and relationships, the proprietary technology platform, and the unique GCU relationship, though all are potentially replicable given enough time and investment.

The overall power assessment is moderate. GCE's primary moats are process power and the deeply embedded GCU relationship. The regulatory resolution has removed a significant source of uncertainty that previously undermined all other powers. But the company's long-term competitive position depends on whether it can successfully extend its process power beyond the GCU relationship and build a genuinely diversified platform business where scale economies and switching costs become more powerful.

Key Performance Indicators to Watch

For investors tracking GCE's ongoing performance, two metrics matter more than any others. First, GCU online enrollment growth, because this is the engine that drives the dominant revenue stream and reflects the health of the core business and the effectiveness of GCE's marketing and enrollment operations. Second, university partner revenue growth rate, because this measures whether the diversification thesis is actually working and whether GCE can reduce its existential dependence on a single client. These two numbers, tracked quarterly, tell you nearly everything you need to know about whether GCE's strategy is succeeding.

XII. Recent Developments and Future Outlook

The year 2025 was, by any measure, the most consequential in Grand Canyon Education's history since the 2018 separation. The systematic resolution of every major regulatory challenge, the Ninth Circuit victory, the fine rescission, the IRS reaffirmation, the FTC dismissal, and the Department of Education's formal nonprofit recognition, collectively removed the cloud that had hung over the company for six years. For the first time since the conversion, GCE and GCU could operate without the constant threat of adverse regulatory action fundamentally disrupting their business model.

The financial results for 2025 reflected a business performing well on its fundamentals. Revenue grew seven percent to $1.106 billion. Margins expanded modestly. Enrollment growth was healthy across both the GCU and partner segments. The company guided for 2026 revenue of $1.17 billion to $1.19 billion, implying continued mid-to-high single-digit growth.

The technology landscape is evolving rapidly, and GCE's investments in artificial intelligence represent both an opportunity and a potential threat. On the opportunity side, AI tools for tutoring, grading, advising, and administrative automation could improve GCE's service quality while reducing costs. On the threat side, if AI democratizes the capabilities that GCE currently provides, it could undermine the company's value proposition to partner universities who might decide that a combination of in-house staff and AI tools is sufficient.

The demographic cliff is approaching. Projections suggest that the number of high school graduates in the United States will begin declining in the late 2020s, driven by lower birth rates in the years following the 2008 financial crisis. This will create headwinds for the entire higher education sector and could intensify competition for students. GCU's predominantly online, nontraditional student base provides some insulation, as working adults returning to school are less affected by demographic trends among eighteen-year-olds. But the broader market pressure is real and will affect the competitive environment in which GCE operates.

International expansion is a possibility that GCE has discussed but not yet pursued aggressively. The services platform is theoretically portable to universities in other countries, particularly English-speaking markets with similar regulatory frameworks. However, the complexity of navigating different regulatory environments, accreditation systems, and cultural expectations makes international expansion a longer-term opportunity rather than a near-term catalyst.

The succession question grows more pressing with each passing year. Mueller has led GCE for nearly two decades and has been the strategic architect of every major decision in the company's modern history. No succession plan has been publicly disclosed, and the company's culture, strategy, and regulatory relationships are deeply intertwined with Mueller's personal involvement. How the market values GCE after Mueller steps down will depend on whether his successor can maintain the execution quality and strategic vision that have characterized his tenure.

Looking at potential scenarios, the range of outcomes remains wide despite the narrowing of regulatory risk.

The best case involves continued enrollment growth, accelerating partner diversification, successful AI integration, and the sustained benefit of the regulatory all-clear. In this scenario, GCE evolves from a single-client services company into a genuine education platform serving dozens of universities.

The base case, and arguably the most likely scenario, involves GCU remaining the dominant revenue source, modest but steady partner growth through Orbis, and the company continuing to generate strong margins and free cash flow while trading at a reasonable earnings multiple.

The worst case, now significantly less likely after the 2025 regulatory resolutions, would involve some future regulatory challenge to the GCE-GCU structure, though the legal precedents now established would make such a challenge substantially harder to mount.

The bigger question that Grand Canyon Education forces us to ask is whether its model represents the future of higher education or a one-time regulatory arbitrage that succeeded because of unique historical circumstances and an unusually tenacious leader.

The answer may be both. The model works because it combines the operational efficiency and capital access of a for-profit company with the mission-driven governance and regulatory benefits of a nonprofit university. Other institutions are watching, and some will attempt to replicate elements of the structure. But the specific combination of circumstances that made it possible, a failing university, a willing accreditor, a favorable legal environment in Arizona, and a CEO with two decades of for-profit education experience, may not be easily reproduced.

The broader context matters too. American higher education is under more pressure than at any time in its modern history. Tuition costs have risen faster than inflation for four decades straight. Student loan debt exceeds $1.7 trillion. Public confidence in the value of a college degree is declining, particularly among younger Americans. Community colleges are underfunded. State universities face budget cuts. Small private colleges are closing at an accelerating rate. In this environment, the question of whether a for-profit services company can help universities deliver education more efficiently, more affordably, and at greater scale is not just academic. It is urgent.

GCE's answer to that question has been: yes, but on our terms, with our model, and with the legal framework we have built. Whether that answer satisfies regulators, students, and the broader public over the long term remains the central open question of this story.

XIII. Epilogue and Reflections

What makes Grand Canyon Education fascinating is not just the business model or the financial performance. It is the audacity of the strategy and the sheer improbability of its success. A dying Baptist college in Arizona, sold to a group of California investors, transformed by a former University of Phoenix executive into a publicly traded education company, converted back to nonprofit status through an unprecedented corporate structure, attacked by every relevant federal regulator, and vindicated in every case. The narrative arc has the quality of fiction, but the quarterly earnings reports confirm it is real.

The story illuminates the deeper crisis in American higher education: the impossible triangle of access, quality, and affordability. Traditional nonprofit universities offer quality and, sometimes, access, but at ever-increasing cost. For-profit colleges offered access and, sometimes, affordability, but too often at the expense of quality.

Mueller's grand experiment at GCU was an attempt to break out of this triangle by combining the efficiency of for-profit management with the mission and governance of a nonprofit institution. Whether he succeeded depends on the metrics you choose and the values you bring to the evaluation.

The for-profit versus nonprofit distinction in American higher education has always been more blurry than the regulatory framework suggests. Many nonprofit universities operate with the same aggressive marketing, high administrative salaries, and growth-oriented strategies as their for-profit counterparts. The president of a prestigious nonprofit university may earn millions of dollars a year. The university's endowment may be managed with the same financial sophistication as a hedge fund. The admissions office may market with the same intensity as any consumer brand.

Many for-profit institutions, conversely, have delivered genuine educational value to students who had no other options, students who were working full-time, raising families, or stationed overseas with the military.

GCE's hybrid model simply made the blurriness explicit, and in doing so, forced regulators, accreditors, and the public to confront uncomfortable questions about what the organizational form actually means.