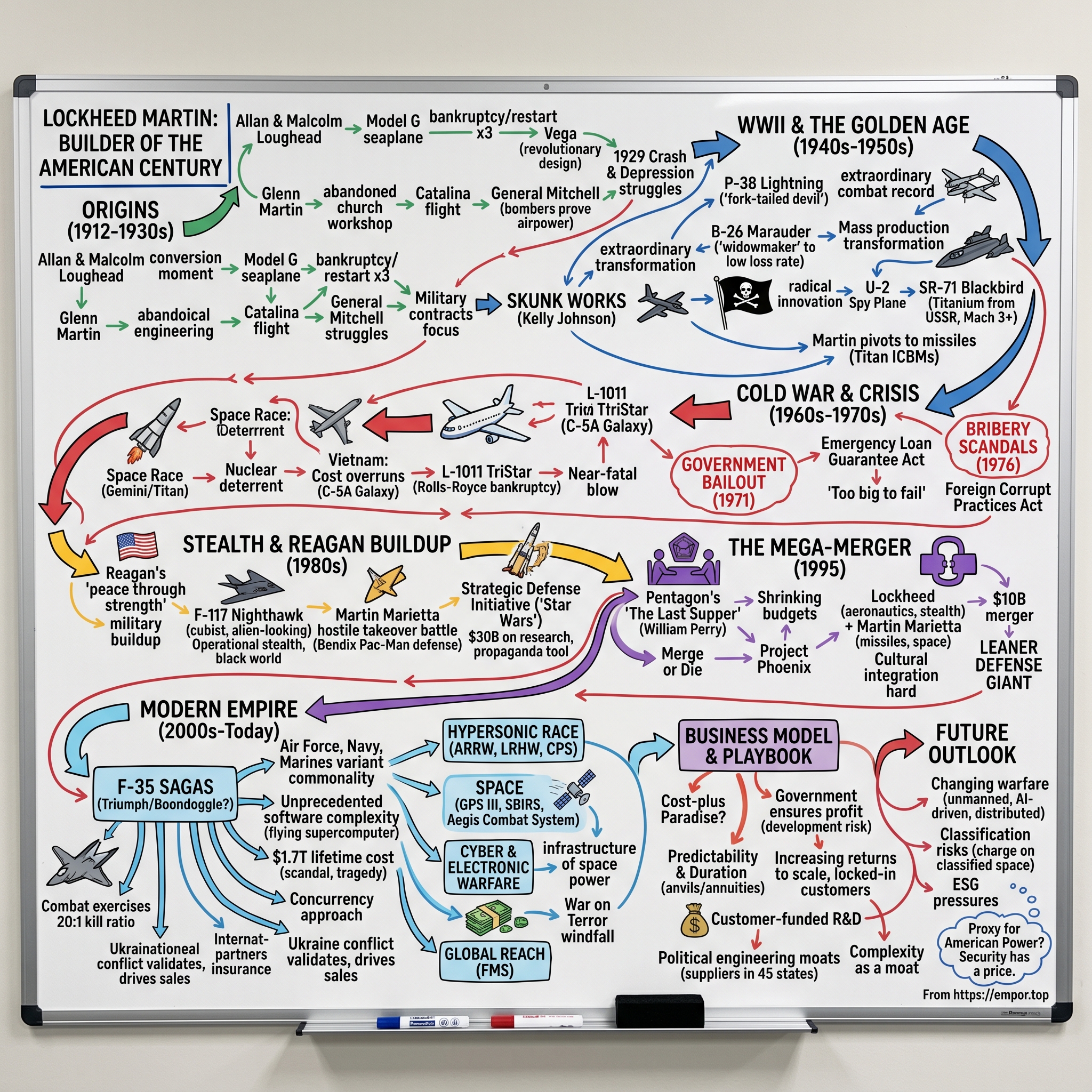

Lockheed Martin: The Defense Contractor That Built the American Century

I. Introduction & Episode Roadmap

Picture this: It's 2:47 AM on May 2, 2011, in a compound in Abbottabad, Pakistan. Two modified Black Hawk helicopters—so secret their existence won't be confirmed for years—hover in the darkness. These aren't ordinary aircraft; they're stealth-modified versions built with Lockheed Martin technology, carrying Navy SEALs on the most consequential mission of the 21st century. When one crashes in Osama bin Laden's courtyard, Pakistani authorities will find wreckage unlike anything they've seen before—composite materials and radar-absorbing coatings that represent decades of classified research. This is Lockheed Martin at work: invisible, indispensable, and woven into the fabric of American power projection.

Today, Lockheed Martin stands as a $67 billion revenue colossus, the world's largest defense contractor by a comfortable margin. The company builds everything from the F-35 Lightning II fighter jet—the most expensive weapons program in human history at $1.7 trillion lifetime cost—to the Aegis missile defense systems protecting allied nations, to the Orion spacecraft that will return Americans to the moon. One in every three dollars the Pentagon spends on major defense programs flows to Lockheed Martin. The company employs 116,000 people across 375 facilities worldwide, with products operating in more than 100 countries.

But here's what's fascinating: this empire emerged from two companies that nearly died multiple times. The Lockheed brothers started as barnstorming daredevils in 1912 California, went bankrupt, and had to restart their company three times before it stuck. Glenn Martin began building planes in an abandoned church in Santa Ana, teaching himself aerodynamics from books he mail-ordered from Europe. Neither founder lived to see the 1995 merger that created today's giant—Allan Loughead died in 1969 believing his company had abandoned his vision, while Glenn Martin passed in 1955 after being forced out of his own firm.

How did these struggling aviation pioneers evolve into the Pentagon's most essential contractor? How did a company that needed a government bailout in 1971 become what some call "too big to fail" in the defense ecosystem? And what does it mean when a single corporation becomes so intertwined with national security that its quarterly earnings calls can move geopolitical calculations?

This is a story about engineering brilliance and ethical scandals, about breakthrough innovation funded by blank government checks, about the revolving door between the Pentagon and the C-suite. It's about how modern warfare transformed from steel and gunpowder to software and sensors, and how one company positioned itself at the center of that transformation. Most importantly, it's about understanding a business model so unique that traditional metrics barely apply—where your customer can't let you fail, where contracts span decades, and where the moat isn't just technology but the classification stamps that keep competitors from even knowing what you've built.

We'll journey from the early days of cloth-covered biplanes to the F-35's 8 million lines of code, from the Skunk Works' hand-drawn blueprints to AI-powered kill chains. Along the way, we'll decode the Pentagon's procurement labyrinth, examine the economics of cost-plus contracting, and understand why defense investors see Lockheed Martin as either the ultimate dividend aristocrat or a value trap dependent on political winds.

The next few hours will challenge conventional wisdom about defense contractors. We'll see how a industry often caricatured as bloated and inefficient has produced some of history's most remarkable engineering achievements. We'll understand why profit margins are actually lower than most assume, why R&D spending patterns defy Silicon Valley logic, and why the biggest risk to Lockheed Martin might not be competitors but peace itself.

So buckle up. We're about to explore how two dreamers tinkering in California garages ultimately built the arsenal of democracy—and what their creation tells us about power, innovation, and the price of security in the American century.

II. Origins: The Loughead Brothers & Glenn Martin (1912–1930s)

The story begins not in a boardroom or factory, but at the 1910 Los Angeles International Air Meet, where a young Allan Loughead paid $10—roughly $300 in today's money—for a ten-minute ride in a Curtis pusher biplane. As the fabric wings caught the California sun and the engine roared to life, Allan experienced what he'd later call his "conversion moment." Within seconds of takeoff, he knew he'd found his life's purpose. "I was hooked," he'd tell reporters decades later. "The ground fell away and I thought, this is it—this is the future, and I need to build these machines."

Allan convinced his younger brother Malcolm, a mechanical genius who'd been designing car engines since age 15, to join him in starting an aircraft company. The brothers had already shown entrepreneurial flair—they'd made small fortunes racing cars and running a brake repair shop. But they faced an immediate problem: their surname. "Loughead" was Scottish, pronounced "Lock-heed," but everyone butchered it as "Lug-head" or "Log-head." Not exactly the brand image for precision aircraft. They'd eventually solve this by phonetically respelling it as "Lockheed" in 1926, though not before years of confused customers and mispronounced introductions.

Their first plane, the Model G, was revolutionary for 1913—a seaplane that could carry two passengers and actually make money. They charged $10 per passenger for sightseeing flights over San Francisco Bay, operating from a ramp they built themselves near the Panama-Pacific International Exposition. On their best days, they'd earn $350—serious money when a new Ford Model T cost $490. The Model G featured innovations like a laminated wood fuselage (Malcolm's invention) that was lighter and stronger than anything competitors offered. They even took early Hollywood starlets up for publicity flights, understanding decades before others that aviation needed glamour to sell.

Meanwhile, 2,400 miles away in an abandoned church in Santa Ana, Glenn Martin was building his own aviation dream with radically different methods. Where the Lougheads were intuitive engineers who learned by doing, Martin was methodical, almost scholarly. He taught himself French and German to read European aviation journals, built a wind tunnel in his church-workshop, and kept meticulous notes on every test flight. His mother, Minta Martin, became his business manager and chief advocate—an unusual arrangement that would last until her death in 1940. She mortgaged their family home three times to keep the company afloat, believing absolutely in her son's vision.

Martin's breakthrough came with his 1912 biplane that he flew from Los Angeles to Catalina Island and back—a 70-mile round trip over open water that made international headlines. The flight nearly killed him when fog rolled in and he had to navigate by glimpsing the ocean through holes in the mist, but it established him as a serious player. By 1914, he'd moved operations to Los Angeles and was building planes that could stay airborne for hours, not minutes.

World War I changed everything. When America entered the war in 1917, both companies thought they'd hit the jackpot. The military needed thousands of planes, and who better to build them than America's aviation pioneers? Reality proved crushing. The Loughead brothers received exactly zero military contracts—the Army thought their designs too radical, their company too small. They watched competitors like Curtiss and Boeing secure massive orders while they scraped by on civilian sales. By 1920, with surplus military planes flooding the market at pennies on the dollar, the Lougheads were forced to liquidate. Allan became a real estate salesman; Malcolm went to work for other aviation companies, taking his engineering talents elsewhere.

Martin fared better but not by much. He secured contracts for bomber trainers, but the Armistice came before serious production began. His company survived the post-war collapse through sheer determination and Minta's financial acrobatics. Martin pivoted to building mail planes and experimental aircraft, including the first successful American-designed bomber, the MB-1. When General Billy Mitchell needed planes to prove airpower could sink battleships in his famous 1921 demonstration, he turned to Martin. The successful sinking of the captured German battleship Ostfriesland using Martin bombers changed military thinking forever, though Martin himself saw only modest financial benefit.

The 1920s brought a pattern both companies would repeat throughout their histories: technical triumph followed by financial disaster. Allan Loughead returned to aviation in 1926, founding Lockheed Aircraft Company with $25,000 in backing. This time he had help from Jack Northrop, a brilliant designer who would later found his own aerospace giant. Together they created the Vega, a plane so advanced it looked like it had fallen through a time portal. Its monocoque fuselage—where the skin itself bore structural loads rather than internal framework—was revolutionary. The Vega could fly faster and farther than anything in its class, using Northrop's radical streamlining that eliminated external bracing wires and struts.

The Vega became the chosen aircraft of aviation's golden age. Amelia Earhart flew one solo across the Atlantic in 1932. Wiley Post used one to fly around the world twice, once solo in just under eight days. Airlines bought them for premium routes. The future looked brilliant—until October 29, 1929. The stock market crash devastated aviation. Airlines canceled orders, private buyers vanished, and credit dried up overnight. Within months, Allan Loughead was forced out of his own company by investors. He left aviation entirely, spending the next decade inventing an improved hydraulic brake system for cars. The supreme irony: the company bearing his name would thrive without him, while he'd never build another plane.

Martin survived the Depression through government contracts and brutal cost-cutting. He moved operations to Baltimore in 1929, lured by land incentives and proximity to Washington. The move nearly killed the company—key engineers refused to relocate, competitors poached talent, and the new factory hemorrhaged money. But Martin had one advantage: he'd cultivated relationships with military brass who appreciated his methodical approach and reliable delivery. When the Navy needed long-range patrol bombers in the 1930s, Martin got the contracts. His flying boats, particularly the M-130 China Clipper, opened trans-Pacific commercial aviation. Pan Am used them to establish the first regular passenger service to Asia, with tickets costing $1,438 one-way—roughly $30,000 today.

By the late 1930s, both companies had found their niches. Lockheed, now under new management but still bearing the Loughead brothers' phonetic name, focused on fast, elegant aircraft for airlines and wealthy individuals. Martin built bombers and flying boats for the military and Pan Am's ocean routes. Neither Allan Loughead nor Malcolm (who'd founded unsuccessful companies of his own) had any ownership stake in the empire their name would build. Glenn Martin remained in control but increasingly isolated, his perfectionism and micromanagement driving away talented subordinates.

As storm clouds gathered over Europe in 1939, both companies sensed opportunity. Military budgets were expanding, and America's aviation industry was about to experience growth beyond anyone's imagination. The Loughead brothers' company and Glenn Martin's enterprise would soon build the planes that would help win World War II, though neither founding family would reap the rewards. The DNA they'd embedded in their companies—Lockheed's radical innovation and Martin's methodical engineering—would define corporate cultures that persist to this day.

The stage was set for transformation. These struggling enterprises, born from individual obsession and kept alive through multiple near-death experiences, were about to become central players in the Arsenal of Democracy. The barnstorming era was ending; the military-industrial age was about to begin.

III. WWII & The Golden Age of Aviation (1940s–1950s)

December 6, 1940. Dawn breaks gray and cold over Burbank, California. Inside Lockheed's Building 304, test pilot Marshall Headle climbs into the cockpit of a stubby, malevolent-looking aircraft designated "40-1361"—the very first Martin B-26 Marauder. The plane looks wrong somehow, its wings too small for its cigar-shaped fuselage, its twin Pratt & Whitney engines massive and intimidating. As Headle advances the throttles for the maiden flight, engineers hold their breath. They've built this plane without a prototype, going straight from blueprints to production—an insane gamble that would define both companies' futures. Within minutes, Headle discovers what thousands of pilots would soon learn: this plane wants to kill you if you don't respect it. The landing speed is astronomical, the stall characteristics vicious. But it's also faster than anything in America's bomber inventory. This is the paradox of World War II aviation—brilliant, lethal, and built by companies that would have been bankrupt without war.

By Pearl Harbor morning exactly one year later, America possessed just 69 P-38 Lightnings and a handful of B-26 Marauders. Within four years, Lockheed would deliver more than 10,000 P-38s while Martin would produce 5,288 B-26s between February 1941 and March 1945. These numbers represent more than industrial output—they're the transformation of two struggling companies into the Arsenal of Democracy. The war didn't just save Lockheed and Martin; it fundamentally rewired their DNA, turning experimental aircraft builders into mass production machines, transforming engineers into strategic assets, and establishing relationships with the Pentagon that would define American power projection for the next century.

The Lockheed story reads like industrial mythology. After Allan Loughead's forced exit in 1932, the company found salvation in an unlikely source: Robert Gross, a 35-year-old investment banker who bought the bankrupt company for $40,000 in 1932—roughly $900,000 today. Gross knew nothing about aviation but understood talent. He kept the engineering team intact, including Hall Hibbard and a young, abrasive engineer named Clarence "Kelly" Johnson. Johnson was Lockheed's best aeronautical engineer, responsible for the P-38 and the P-80, though his personality was so difficult that colleagues often requested transfers rather than work with him. Gross didn't care—he recognized genius when he saw it.

The P-38 Lightning emerged from Johnson's relentless perfectionism and willingness to ignore conventional wisdom. When the Army Air Corps issued its 1937 specification for a high-altitude interceptor, every other manufacturer proposed variations on existing designs. Johnson went radical: twin engines, twin booms, a central nacelle for the pilot, tricycle landing gear. Critics called it "Johnson's folly." The configuration had never been attempted in a fighter. First conceived in 1937 by Lockheed chief engineer Hall L. Hibbard and his then assistant, Clarence "Kelly" Johnson, the twin-boomed P-38 was the most innovative plane of its day. The Germans would later call it "der Gabelschwanz Teufl"—the fork-tailed devil.

Production nearly killed the company. The P-38's complexity meant that early models required 30,000 man-hours to build—three times what competitors needed for conventional fighters. Lockheed hemorrhaged money on every plane. But then came Pearl Harbor, and suddenly the military didn't care about cost—they needed fighters that could fly far enough to reach Japanese-held islands. The P-38 was the only American fighter aircraft in large-scale production throughout American involvement in the war, from the Attack on Pearl Harbor to Victory over Japan Day. By 1944, Lockheed had cut production time to 3,000 man-hours through revolutionary assembly techniques, including 22 sub-contractors building various Lightning components and shipping them to Burbank, California, for final assembly.

The P-38's combat record was extraordinary. P-38 pilots shot down more Japanese aircraft than any other fighter and, as a reconnaissance aircraft, obtained 90 percent of the aerial film captured over Europe. America's top two aces, Richard I. "Dick" Bong with 40 victories and Thomas B. "Tommy" McGuire with 38, both flew Lightnings. The plane's most famous mission came on April 18, 1943, when P-38s flew 800 miles to intercept and shoot down Admiral Yamamoto's transport—a surgical strike that required navigation so precise that pilots found their target within seconds of the predicted time.

Meanwhile, Glenn Martin's company faced its own transformation at its Baltimore facility, which it had moved to in 1929. The B-26 Marauder represented everything Martin believed about bomber design: speed over safety, performance over ease of handling. The aircraft quickly received the reputation of a "widowmaker" due to the early models' high accident rate during takeoffs and landings. The Marauder had to be flown at precise airspeeds, particularly on final runway approach. Pilots coined bitter nicknames: "One-a-Day-in-Tampa-Bay" referred to the daily training crashes. "The Baltimore Whore" referenced both its origin and the saying "no visible means of support"—a dark joke about its tiny wings.

Martin himself took the criticism personally. He'd send his best test pilots to squadrons to demonstrate that the plane was safe if flown correctly. The Army nearly canceled the program three times. The Truman Committee investigated. Each time, Martin survived by promising modifications—larger wings, bigger tail, improved training. The B-26 became a safer aircraft once crews were retrained, and after aerodynamics modifications. The Marauder ended World War II with the lowest loss rate of any U.S. Army Air Forces bomber. By 1944, the Marauder proved itself as the bomber with the lowest loss rate among American aircraft in Europe, with a loss rate under half a percent.

The numbers tell the story of industrial transformation. By the end of World War II, the B-26 had flown more than 110,000 sorties, dropped 150,000 tons of bombs. The plane that pilots feared became the plane they trusted most. One B-26, "Flak-Bait," survived 202 combat missions over Europe, more than any other American aircraft during World War II. But Martin's success came with a price—the company became completely dependent on military contracts, with no civilian market to cushion downturns.

The true revolution happened not on assembly lines but in a locked room at Lockheed where Kelly Johnson was creating the future. In June 1943, the Army approached Lockheed with an impossible request: build America's first jet fighter to counter German Me-262s. They needed it in 180 days. Johnson promised 150. Kelly Johnson and his team designed and built the XP-80 in only 143 days, seven less than was required. He handpicked 23 engineers and 105 shop workers, commandeered a circus tent near a plastics factory that reeked so badly his engineers answered the phone "Skonk Works!"—after the moonshine still in Al Capp's Li'l Abner comic strip.

This was the birth of Skunk Works, though Lockheed would change the spelling to "Skunk Works" to avoid potential legal trouble over use of a copyrighted term. Johnson ran it like a pirate ship within the corporate fleet. No bureaucracy, no committees, no paperwork that didn't directly advance the project. Engineers worked next to machinists. Drawings were optional—if you could build it faster from a sketch, do it. Johnson's management philosophy was brutal but effective: "Be quick, be quiet, and be on time."

The P-80 Shooting Star missed World War II—it arrived just as the war ended. But Johnson had proven something revolutionary: a small team with absolute authority could outperform entire corporations. The Pentagon took notice. When the Cold War began and America needed reconnaissance aircraft that could overfly the Soviet Union, they didn't go to Boeing or North American. They went to Kelly Johnson.

The U-2 spy plane exemplified everything Johnson had learned. In 1954, the CIA approached him with requirements that seemed physically impossible: fly at 70,000 feet (above Soviet interceptors and missiles), carry cameras that could photograph license plates from 13 miles up, stay aloft for 10 hours. Johnson's proposal was so radical the CIA initially rejected it—his plane would have no weapons, no defensive systems, just wings, engines, and cameras. Lockheed received a $22.5 million contract in March 1955 for the first 20 aircraft. The company agreed to deliver the first aircraft by July of that year and the last by November 1956. It did so, and for $3.5 million under budget.

The U-2 was completed and shipped to Paradise Ranch in late July—less than nine months after the contract was first issued. In early August, it accidentally took flight while conducting a routine taxi test. As test pilot Tony LeVier recalled, "Who'd have guessed an airplane could take off only going 70 knots?" The plane was so light and its wings so efficient that it practically flew itself. The high-flying plane was able to glide 250 miles from 70,000 feet.

For five years, the U-2 provided intelligence that shaped American foreign policy. Photos from U-2s revealed that the "missile gap" was a myth—America was actually ahead. They documented Soviet nuclear tests, tracked arms shipments to Cuba, mapped Chinese nuclear facilities. When Francis Gary Powers was shot down over the Soviet Union in 1960, it wasn't just a pilot and plane that were lost—it was America's intelligence advantage.

But Johnson was already working on the successor: Johnson used the combined knowledge of the U-2 and A-12 to produce the SR-71 Blackbird. If the U-2 philosophy was to fly too high to be hit, the Blackbird's was to fly too fast. Kelly proposed a plane that would fly at 90,000 feet, at Mach 3 speed, for four thousand miles. The technical challenges were staggering—at Mach 3, air friction would heat the plane's skin to 600 degrees Fahrenheit. Aluminum would melt. Johnson needed titanium, but most titanium came from the Soviet Union. The CIA set up shell companies to buy Soviet titanium to build a plane to spy on the Soviets—Cold War irony at its finest.

While Lockheed pushed the boundaries of speed and altitude, Martin struggled with corporate identity. Glenn Martin had been forced out of his own company in 1949, dying in 1955 believing his vision had been betrayed. The company pivoted to missiles, becoming Martin Marietta in 1961 after merging with American-Marietta Corporation. They built Titan ICBMs that sat in silos across the Midwest, each one capable of delivering a 9-megaton warhead to Moscow in 30 minutes. The company that started with fabric-covered biplanes now built the ultimate expression of mutually assured destruction.

The paths of these two companies through the 1950s illustrated different strategies for survival in the military-industrial complex. Lockheed bet on revolutionary technology and black projects. Martin Marietta chose diversification and scale. Both approaches worked—until they didn't. By the 1960s, both companies would face existential crises that would ultimately drive them together. But in the golden age of military aviation, they were rivals and innovators, each pushing the other to new heights, literally and figuratively.

The ghost of the Loughead brothers and Glenn Martin haunted these successes. None of the founders lived to see what their companies became. Allan Loughead died in 1969, having spent his last decades in real estate and invention, watching the company bearing his name—spelled phonetically to help others pronounce it correctly—become an aerospace giant without him. Malcolm died in 1962, having tried and failed multiple times to recapture aviation success. Glenn Martin passed in 1955, forced from his company years earlier, bitter that corporate boards valued profits over engineering excellence.

Yet their DNA persisted. Lockheed's radical innovation, embodied in Johnson's Skunk Works, traced directly back to the Loughead brothers' willingness to attempt the impossible. Martin's methodical approach to production and testing evolved from Glenn Martin's scholarly perfectionism. The founders might not have recognized the sprawling corporations their companies had become, but they would have understood the engineering challenges they tackled. As the 1950s ended, both companies stood at the pinnacle of American aerospace—but the hardest tests lay ahead. The age of missiles was dawning, budgets were tightening, and a dinner in Washington would soon reshape the entire industry.

IV. The Space Race & Cold War Dominance (1960s–1970s)

July 20, 1963. The Nevada desert shimmers in 117-degree heat. Inside a concrete blockhouse at Area 51, Kelly Johnson watches through periscope as test pilot Bill Park pushes the throttles forward on an aircraft so secret it doesn't officially exist. The A-12 Oxcart—precursor to the SR-71 Blackbird—accelerates down the runway and vanishes into the sky. Within minutes, Park radios back: "Passing through Mach 3." Breaking records nearly every time it flew, the Blackbird achieved a sustained speed above Mach 3 on July 20, 1963, at an astounding altitude of 78,000 feet. Johnson allows himself a rare smile. Five years ago, the CIA asked for the impossible—a reconnaissance aircraft that could fly higher and faster than anything ever built. Today, he's delivered it. But this triumph masks a darker reality: Lockheed is bleeding money on military contracts, and the commercial aviation market is about to deal the company a near-fatal blow.

The 1960s began with both companies riding high on Cold War paranoia. The U-2 had given America an intelligence monopoly—until May 1, 1960, when Soviet surface-to-air missiles brought down Francis Gary Powers over Sverdlovsk. The shootdown didn't just end the U-2's invulnerability; it nearly triggered World War III. Khrushchev used the incident to torpedo the Paris Summit, and President Eisenhower was forced to admit publicly that America had been spying. President Eisenhower deeply valued the strategic benefits of the U-2's airborne reconnaissance during these tense Cold War times. And now the call came from Lockheed's customer in Washington to build the impossible – an aircraft that can't be shot down – and do it fast.

Johnson's response was characteristically audacious. If altitude wasn't enough protection, speed would be. The SR-71 Blackbird represented a complete reimagining of what an aircraft could be. The design presented two unprecedented challenges: aerodynamic heating—at the Blackbird's 2,000-mph cruising speed, the friction of air would soften and crumple an aluminum airframe—and making jet engines run at 80,000 feet, where the atmosphere has only one-sixteenth the density it has at sea level. Most aircraft projects, even pioneering ones, involve known materials and techniques, and make some use of the proven features of their precursors. The Blackbird was without antecedents. It required basic research in the fabrication of a new structural material, titanium; new fuel and lubricants; new fittings, wiring, and insulators; new sealants and fasteners; new nacelle designs and airframe aerodynamics; new ways to defeat radar; and new environmental systems to keep the pilot from roasting in his seat.

The titanium alone nearly killed the project. The only reliable source was the Soviet Union. The CIA set up a byzantine network of shell companies to buy Soviet titanium, supposedly for industrial uses, then smuggle it to Burbank. Machinists discovered that cadmium-plated tools caused the titanium to crack—every wrench had to be replaced. Spot welds failed until engineers realized that Burbank's chlorinated tap water was contaminating the metal. They had to truck in distilled water from outside the city.

The costs were staggering, though exact figures remain classified. What we know is that each SR-71 cost approximately $34 million in 1960s dollars—roughly $300 million today. But the capability it provided was priceless. In 1974, the SR-71 set the record for the quickest flight between London and New York at 1 hour, 54 minutes and 56 seconds. In 1976, it became the fastest airbreathing manned aircraft, previously held by its predecessor, the closely related Lockheed YF-12. As of 2025, the Blackbird still holds all three world records.

While Lockheed pushed the boundaries of speed, Martin faced a different challenge: building America's nuclear deterrent. Martin Marietta formed in 1961 by the merger of the Glenn L. Martin Company and American-Marietta Corporation. Martin, based in Baltimore, was primarily an aerospace concern with a recent focus on missiles, namely its Titan program. This program was established in 1955 when the company secured the U.S. Air Force contract to build the country's second intercontinental ballistic missile (ICBM). The merger created a conglomerate with $800 million in annual sales, combining Martin's aerospace expertise with American-Marietta's industrial materials business.

The Titan II represented the ultimate expression of liquid-fueled ICBMs. Standing 103 feet tall and weighing 330,000 pounds when fueled, each missile carried a 9-megaton W53 warhead—600 times more powerful than the Hiroshima bomb. Fifty-four Titans stood on alert in underground silos across Arkansas, Kansas, and Arizona, each one capable of reaching Moscow in 30 minutes. The program was lucrative—each missile cost $3.5 million, and Martin Marietta built 108 of them.

But the Titan's hypergolic fuel—a mixture of nitrogen tetroxide and hydrazine—was as dangerous as the warhead. The chemicals ignited on contact, eliminating ignition delay but creating a maintenance nightmare. In 1965, a fire in a Titan II silo killed 53 workers. In 1978, a dropped socket wrench punctured a fuel tank in Arkansas, causing an explosion that launched the warhead 600 feet from the silo. These accidents highlighted the terrifying reality of maintaining a doomsday arsenal.

The space race provided both companies with opportunities beyond weapons. Martin Marietta's Titans launched Gemini astronauts into orbit, proving that ICBMs could be repurposed for peaceful uses. Lockheed built the Agena target vehicle that Gemini crews practiced docking with—essential preparation for the moon missions. But these contracts were drops in an ocean of military spending.

Then came Vietnam, and with it, a paradox. Defense spending skyrocketed—reaching $80 billion by 1968—but both companies struggled. The problem wasn't revenue but profit margins. Cost-plus contracts that had seemed generous in peacetime became money-losers as inflation soared and the Pentagon demanded fixed prices on modifications. Lockheed's C-5A Galaxy transport, the largest aircraft in the world, exemplified the problem. Originally bid at $2.3 billion for 115 aircraft, costs ballooned to $5.3 billion. Lockheed absorbed $500 million in losses.

The commercial market offered no relief. Lockheed had bet everything on the L-1011 TriStar, a wide-body airliner to compete with Boeing's 747 and McDonnell Douglas's DC-10. The TriStar was technically superior—quieter, more fuel-efficient, with the industry's first automated landing system. But it depended on Rolls-Royce's new RB211 engine. When Rolls-Royce went bankrupt in February 1971, it nearly took Lockheed with it. The company had already spent $900 million on development and had orders for 178 aircraft. Without engines, those orders were worthless.

Daniel Haughton, Lockheed's CEO, made a desperate gamble. He went to Congress asking for a federal loan guarantee—essentially a bailout. The request triggered a firestorm. Senator William Proxmire called it "corporate welfare at its worst." Competitors argued it was unfair government intervention. As the argument mounted last week over the proposal for the Government to guarantee $250 million in loans to the Lockheed Aircraft Corp., Nixon Administration officials placed calls around the country to sympathetic bankers and industrialists. Those men, in turn, phoned their Congressmen and urged them to vote for the bailout.

The vote was agonizingly close. The House approved by three votes. The Senate tied 49-49, with Vice President Spiro Agnew casting the deciding vote. Through the Emergency Loan Guarantee Act of 1971, the Emergency Loan Guarantee Board was created to manage federally guaranteed private loans up to $250 million to Lockheed Corporation. The guarantee program would have the U.S government assume the private debt of Lockheed if it defaulted on its debts. Lockheed survived, barely, but the precedent was troubling. America's largest defense contractor had become too big to fail.

Then the scandal broke. In February 1976, the Senate Subcommittee on Multinational Corporations revealed that Lockheed had paid millions in bribes to secure foreign sales. The Lockheed bribery scandals encompassed bribes and contributions made by officials of U.S. aerospace company Lockheed from the late 1950s to the 1970s in the process of negotiating the sale of aircraft. The scandal caused considerable political controversy in West Germany, Italy, the Netherlands, and Japan. In the U.S., the scandal nearly led to Lockheed's downfall, as it was already struggling due to the commercial failure of the L-1011 TriStar airliner.

The details were staggering. Top officers of Lockheed Aircraft Corp. inaugurated and directed a program of foreign bribery that included questionable payments of up to $38 million from 1970 through 1975, according to a court-ordered report made public yesterday. Previous studies of the aerospace company's foreign payments had put the total at less than $25 million. In Japan alone, Former Japanese Premier Kakuei Tanaka was formally charged with taking $1.6 million from Lockheed, part of $12.6 million paid by the firm to Japanese officials and agents. More than $7 million of Lockheed money in Japan went to right-wing official Yoshio Kodama, according to the Senate investigation.

Lockheed chairman of the board Daniel Haughton and vice chairman and president Carl Kotchian resigned from their posts on February 13, 1976. According to Ben Rich, director of Lockheed's Skunk Works: Lockheed executives admitted paying millions in bribes over more than a decade to the Dutch (Prince Bernhard, husband of Queen Juliana, in particular), to key Japanese and West German politicians, to Italian officials and generals, and to other highly placed figures from Hong Kong to Saudi Arabia, in order to get them to buy our airplanes. Kelly [referring to Clarence "Kelly" Johnson, first team leader of the Skunk Works] was so sickened by these revelations that he had almost quit, even though the top Lockheed management implicated in the scandal resigned in disgrace.

The scandal's impact went far beyond Lockheed. The scandal also played a part in the formulation of the Foreign Corrupt Practices Act which President Jimmy Carter signed into law on December 19, 1977, which made it illegal for American persons and entities to bribe foreign government officials. But for Lockheed, the damage was existential. The company that had helped win World War II, that had built the planes protecting America from Soviet bombers, was now synonymous with corruption.

Martin Marietta avoided scandal but faced its own crisis. The company had diversified into everything from cement to chemicals, believing that civilian markets would cushion defense downturns. Instead, these businesses drained resources and management attention. When the 1970s recession hit, Martin Marietta found itself losing money on multiple fronts.

Both companies limped into the 1980s wounded but alive. They had survived the transition from hot war to cold war, from aviation to aerospace, from entrepreneurial management to corporate bureaucracy. But survival had come at a cost. The innovative spirit that created the P-38 and the B-26 had been replaced by risk aversion. The companies that had once moved at startup speed now moved at the pace of government procurement cycles.

Kelly Johnson saw it coming. In a 1974 memo, he warned that Skunk Works was being strangled by bureaucracy: "I see the strong authority that is absolutely essential to this kind of operation slowly being eroded by committee and conference control from within and without." He retired in 1975, disgusted by the bribery scandal and frustrated by the Pentagon's increasingly complex requirements. His successor, Ben Rich, would face a different challenge: proving that American aerospace could still innovate in an era of thousand-page specifications and congressional oversight.

The 1970s ended with both companies at inflection points. The Cold War that had sustained them was evolving. The Pentagon wanted fewer, more sophisticated systems rather than mass production. Foreign competition was emerging—Europe's Airbus had launched in 1970, challenging American dominance in commercial aviation. Most ominously, a new generation of leaders in Washington questioned whether America needed such a vast military-industrial complex.

Ronald Reagan's election in 1980 would answer that question emphatically. The defense buildup that followed would shower both companies with contracts and set the stage for the mega-merger that would unite them. But first, they would have to prove they could still deliver revolutionary capability. For Lockheed, that meant one more secret project from Skunk Works—an aircraft that would redefine air warfare by becoming invisible.

V. Star Wars, Stealth & The Reagan Buildup (1980s)

November 10, 1988. The skies over Nevada are empty except for a single aircraft that shouldn't exist. Photographers gathered at Nellis Air Force Base strain to see details of the angular, alien-looking craft that the Pentagon has just admitted is real after years of denial. It wasn't until 1988 that the program was publicly acknowledged, and not until 1990 that it made its first formal public appearance. By this time, the aircraft had been operational for seven years. The F-117 Nighthawk—the world's first operational stealth aircraft—has finally emerged from the black world of classified programs. For Lockheed, it's vindication. For Martin Marietta, watching from the sidelines, it's a reminder of what they haven't achieved in the new era of high-tech warfare. The Reagan Revolution has transformed the defense industry, but not all boats have risen with this tide.

The 1980s began with Ronald Reagan's inauguration and a simple promise: "peace through strength." By contrast, in 1955 defense took up more than half of the Federal budget. By 1980 this spending had fallen to a low of 23 percent. Even with the increase that I am requesting this year, defense will still amount to only 28 percent of the budget. Reagan's military buildup would inject $2.4 trillion into defense over eight years, the largest peacetime military expansion in American history. For aerospace contractors, it was manna from heaven—or so it seemed.

The F-117's genesis predated Reagan, emerging from a 1974 DARPA request that seemed like science fiction: build an aircraft invisible to radar. In 1962, Pyotr Ufimtsev, a Soviet mathematician, published a seminal paper titled "Method of Edge Waves in the Physical Theory of Diffraction" in the Journal of the Moscow Institute for Radio Engineering, in which he showed that the strength of the radar return from an object is related to its edge configuration, not its size. Ufimtsev was extending theoretical work published by German physicist Arnold Sommerfeld. Ufimtsev demonstrated that he could calculate the RCS across a wing's surface and along its edge. The obvious and logical conclusion was that even a large aircraft could reduce its radar signature by exploiting this principle.

Ben Rich, Kelly Johnson's successor at Skunk Works, discovered this obscure Soviet paper and realized its implications. The Soviets had literally given America the keys to stealth—they just didn't know it. The program was led by Ben Rich, with Alan Brown as manager of the project. Rich called on Bill Schroeder, a Lockheed mathematician, and Overholser, a mathematician and radar specialist, to exploit Ufimtsev's work. The three designed a computer program called "Echo", which made possible the design of an airplane with flat panels, called facets, which were arranged so as to scatter over 99% of a radar's signal energy "painting" the aircraft.

The resulting aircraft looked like it had been designed by cubists. The F-117's angular, faceted surface was a compromise between what computers could calculate and what could be built. Though far from the traditional, sleek aircraft designs preferred by Skunk Works founder Kelly Johnson, the F-117's unique design enabled it to reflect radar waves. With its angular panels bolstered by an external coating of radar-absorbent material, the aircraft was nearly invisible to radar. Kelly Johnson hated it, calling it "the hopeless diamond." But it worked.

During 1976, the Defense Advanced Research Projects Agency (DARPA) issued Lockheed a contract to produce the Have Blue technology demonstrator, the test data from which validated the concept. On 1 November 1978, Lockheed decided to proceed with the F-117 development program. Five prototypes were produced; the first of which performed its maiden flight in 1981 at Groom Lake, Nevada. The first production F-117 was delivered in 1982, and its initial operating capability was achieved in October 1983.

The program's secrecy was absolute. To lower development costs, the avionics, FBW systems, and other systems and parts were derived from the General Dynamics F-16 Fighting Falcon, Boeing B-52 Stratofortress, McDonnell Douglas F/A-18 Hornet, and McDonnell Douglas F-15E Strike Eagle. To maintain a high level of secrecy, components were often rerouted from other aircraft programs, ordered using falsified addresses and other details, while $3 million worth of equipment was removed from USAF storage without disclosing its purpose. Pilots trained only at night. Crashes were covered up—when an F-117 crashed in California's Sequoia National Forest in 1986, the USAF established restricted airspace. Armed guards prohibited entry, including firefighters, and a helicopter gunship circled the site.

The costs were enormous but difficult to calculate precisely. The F-117 Nighthawk price at the time of procurement was around $111 million per unit in 1990s dollars—an enormous figure for a subsonic, single-role platform. However, that investment laid the groundwork for an entire generation of stealth aircraft. The F-117 was developed in the 1970s and 1980s, and its original development costs were estimated to be around $6 billion. However, the actual costs ended up being significantly higher, with some estimates suggesting that the program ultimately cost around $15 billion.

While Lockheed pushed the boundaries of stealth, Martin Marietta struggled to find its identity in the new high-tech battlefield. The company had diversified into everything from aggregates to aerospace, believing that civilian markets would cushion defense downturns. Instead, this scattered focus left them vulnerable when the real action was in revolutionary military technology.

The most dramatic corporate battle of the decade came in 1982 when Bendix Corporation launched a hostile takeover of Martin Marietta. In 1982, Martin Marietta was subject to a hostile takeover bid by the Bendix Corporation, headed by William Agee. Bendix bought the majority of Martin Marietta shares and in effect owned the company. However, Martin Marietta's management used the short time separating ownership and control to sell non-core businesses and launch its own hostile takeover of Bendix (known as the Pac-Man defense). CEO Thomas Pownall executed one of the most audacious defenses in corporate history—Martin Marietta counter-attacked by trying to buy Bendix. The result was corporate mutually assured destruction, with Allied Corporation ultimately acquiring Bendix while Martin Marietta survived, bloodied but independent.

The real action in the 1980s, however, was in space—not the space of satellites and rockets, but the militarization of space itself. President Ronald Reagan saw the proposed Strategic Defense Initiative (SDI) as a safeguard against the most terrifying Cold War outcome—nuclear annihilation. When Reagan first announced SDI on March 23, 1983, he called upon the U.S. scientists who "gave us nuclear weapons to turn their great talents to the cause of mankind and world peace: to give us the means of rendering these nuclear weapons impotent and obsolete."

SDI, immediately dubbed "Star Wars" by critics, was either the most brilliant strategic gambit of the Cold War or the most expensive bluff in history. The Strategic Defense Initiative (SDI), derisively nicknamed the Star Wars program, was a proposed missile defense system intended to protect the United States from attack by ballistic nuclear missiles. The program was announced in 1983 by President Ronald Reagan, a vocal critic of the doctrine of mutual assured destruction (MAD), which he described as a "suicide pact". Reagan called for a system that would end MAD and render nuclear weapons obsolete.

The technical challenges were staggering. Advanced weapon concepts, including lasers, particle-beam weapons, and ground and space-based missile systems were studied, along with sensor, command and control, and computer systems needed to control a system consisting of hundreds of combat centers and satellites spanning the globe. The study focused on the technical challenges of SDI, including developing high intensity lasers and particle beams. "The report concluded that not a single one of the systems then under study or development was even remotely close to deployment," says Houghton. "It noted that every single system under consideration had to at least improve its energy output by 100 times to be effective. In some cases, as much as a million times."

Both Lockheed and Martin Marietta scrambled for SDI contracts, seeing it as the future of defense spending. Over the course of 10 years, the government spent up to $30 billion on developing the concept, but the futuristic program remained just that—futuristic. Martin Marietta's experience with Titan missiles and space systems seemed to give them an advantage. Lockheed countered with their radar and electronic warfare expertise. In reality, most SDI money went to research that never produced deployable systems.

The psychological impact on the Soviets, however, was real. The Strategic Defense Initiative was ultimately most effective not as an anti-ballistic missile defense system, but as a propaganda tool which could put military and economic pressure on the Soviet Union to fund their own anti-ballistic missile system. This possibility was particularly significant because, during the 1980s, the Soviet economy was teetering on the brink of disaster. "Why can't we just lean on the Soviets until they go broke?" quipped Reagan (Lazzari 23).

For American defense contractors, SDI represented both opportunity and danger. The opportunity was obvious—billions in research contracts. The danger was subtler. If SDI worked, it would fundamentally change the nature of warfare. If it didn't, the credibility of the entire military-industrial complex would be questioned. As one Lockheed executive privately admitted, "We're being asked to violate the laws of physics, and we're saying yes because the checks keep coming."

The real revolution of the 1980s wasn't in space but in procurement reform. The Packard Commission, formed after procurement scandals, recommended fundamental changes to how the Pentagon bought weapons. Fixed-price contracts replaced cost-plus arrangements. Competition was mandated where previously sole-source contracts were the norm. For companies used to the cozy certainties of Cold War procurement, it was traumatic.

Lockheed adapted by focusing on what it did best—black programs and revolutionary technology. The F-117 proved that Skunk Works could still deliver the impossible. By decade's end, they were already working on the B-2 bomber and F-22 fighter, both incorporating stealth technology. Martin Marietta took a different path, consolidating its defense operations while maintaining its industrial businesses as a hedge.

The 1980s also saw both companies become truly global. Foreign military sales, particularly to Middle Eastern allies, became crucial revenue sources. The Iran-Iraq War created demand for everything from missiles to communications systems. Israel's military modernization absorbed billions in American hardware. Saudi Arabia's Al-Yamamah deal with Britain—which Lockheed lost—demonstrated that American contractors faced new competition from European consortiums.

Labor relations evolved dramatically. The old adversarial model gave way to partnership approaches as companies realized that building sophisticated systems required skilled, motivated workers. Lockheed's Palmdale facility, where the F-117 was assembled, became a model for the new approach—workers signed security agreements that made them partners in keeping secrets, creating unprecedented loyalty.

But the biggest change was in the industry's relationship with Wall Street. Defense stocks, once considered widows-and-orphans investments valued for stability, became growth plays. Analysts who had never considered defense companies suddenly paid attention. The pressure for quarterly earnings competed with the reality of decade-long development cycles. This tension would only intensify in the coming years.

As the 1980s ended, the Berlin Wall fell. The Cold War that had sustained both companies for four decades was ending. Defense budgets would inevitably shrink. The question wasn't whether consolidation would come, but who would survive it. Both Lockheed and Martin Marietta had transformed themselves during the Reagan years—Lockheed into a high-tech specialist, Martin Marietta into a diversified industrial conglomerate with a strong defense core.

Neither transformation would prove sufficient for what came next. The peace dividend that politicians promised would force a reckoning. The industry that had grown fat on Cold War spending would have to shrink. In Washington, a dinner was being planned that would reshape American aerospace forever. But first, both companies would have to navigate the most challenging environment they'd ever faced—peace.

VI. The Mega-Merger: Creating a Defense Giant (1995)

The Pentagon's dining room, July 1993. Deputy Secretary of Defense William Perry looks across the table at the CEOs of America's largest defense contractors. The dinner will later be known as "The Last Supper," though the religious overtones are unintentional. Perry's message is blunt: the defense budget is shrinking, and half of you won't survive. Merge or die. Norman Augustine of Martin Marietta and Daniel Tellep of Lockheed exchange glances. They've been circling each other for months, knowing that in this new world, even giants need partners. Within two years, their companies will unite in a $10 billion merger that reshapes American aerospace. But first, they have to survive the peace dividend that's killing their industry.

The end of the Cold War hit defense contractors like a sledgehammer. Between 1989 and 1995, the defense budget fell by 35% in real terms. Procurement spending—the lifeblood of contractors—dropped even more precipitously, from $121 billion in 1985 to $43 billion in 1996. Programs were canceled overnight. The Navy's A-12 Avenger II, the Army's Crusader artillery system, the Air Force's Multi-Role Fighter—billions in development costs written off as Washington discovered it no longer needed weapons to fight the Soviet Union.

For Lockheed and Martin Marietta, the early 1990s were exercises in managed decline. Lockheed cut its workforce from 95,000 in 1989 to 70,000 by 1994. Martin Marietta, despite its diversification, fared no better, shrinking from 102,000 to 75,000 employees. Both companies shuttered facilities, wrote off billions in assets, and watched their stock prices stagnate as investors fled defense for the booming technology sector.

The human cost was devastating. Engineers who had spent careers designing weapons to defend America found themselves unemployed. Entire communities built around defense plants withered. In Palmdale, California, where Lockheed built the F-117, unemployment hit 15%. In Denver, where Martin Marietta manufactured Titan rockets, aerospace employment fell by half. The peace dividend, promised as a boon for America, felt like a depression in aerospace corridors.

Norman Augustine understood the mathematics of survival better than most. A Princeton-educated engineer who'd risen through Martin Marietta's ranks, Augustine had a gift for seeing patterns others missed. His "Augustine's Laws"—satirical observations about aerospace management—included the prescient prediction that "in the year 2054, the entire defense budget will purchase just one aircraft." Behind the humor was a serious point: consolidation was inevitable.

Daniel Tellep, Lockheed's CEO since 1989, was Augustine's opposite in temperament—quiet where Augustine was voluble, cautious where Augustine was bold. But Tellep understood the same fundamental truth: neither company could survive alone. The question wasn't whether to merge, but with whom and on what terms.

The courtship began informally at industry conferences, progressed through golf games and private dinners. By early 1994, teams from both companies were secretly modeling merger scenarios. The code name was "Project Phoenix"—resurrection from the ashes. The irony wasn't lost on anyone.

The negotiations were complex beyond anything either company had attempted. This wasn't just combining two companies but integrating cultures, technologies, and legacies stretching back eight decades. Lockheed brought its expertise in aeronautics, stealth technology, and black programs. Martin Marietta contributed missiles, space systems, and electronics. The overlap was minimal—a key factor in securing regulatory approval.

The financial engineering was equally complex. The deal, announced August 30, 1994, valued Martin Marietta at $10 billion. But this wasn't a cash transaction—Lockheed shareholders would own 61% of the combined company, Martin Marietta shareholders 39%. The merger would create a company with $23 billion in annual revenue, 170,000 employees, and a backlog exceeding $40 billion.

The human dynamics were delicate. Who would run the combined company? Augustine became president, Tellep chairman and CEO—but with an understanding that Augustine would succeed him within a year. Which headquarters would survive? Maryland won over California, partly for proximity to Washington, partly because Martin Marietta's Bethesda facility was newer. What about redundancies? The companies promised $1.8 billion in annual savings, inevitably meaning more job losses.

Wall Street's reaction was swift and positive. Both stocks surged on the announcement. Analysts who had written off defense suddenly saw the logic: fewer competitors meant better pricing power, combined overhead meant higher margins, complementary portfolios meant reduced risk. The merger would create a company with leading positions in fighters, missiles, space, and electronics—a portfolio diversified enough to weather any procurement cycle.

The Pentagon's response was more complex. William Perry, now Secretary of Defense, had encouraged consolidation, but did one company controlling so much of America's defense capability pose risks? The Federal Trade Commission launched an extensive review, examining everything from competition in specific weapons systems to the implications for innovation. After six months of scrutiny, regulators approved the merger with minimal conditions—a testament to how little the companies actually overlapped.

The cultural integration proved harder than the financial engineering. Lockheed's culture, shaped by decades of building secret aircraft in the desert, emphasized individual brilliance and minimal bureaucracy. Martin Marietta's culture, forged in the discipline of missile production and space systems, valued process and precision. Engineers who had competed for decades now shared cafeterias and conference rooms.

The merger officially closed March 15, 1995. Lockheed Martin Corporation began trading on the New York Stock Exchange the next day. The stock opened at $71.50, giving the combined company a market capitalization of $13.5 billion. By year's end, it would reach $90 as investors recognized the synergies were real.

But the real test wasn't financial metrics—it was winning programs. The first major competition after the merger was the Joint Strike Fighter, a winner-take-all contest for what would become the F-35. Boeing and Lockheed Martin were the finalists, with the contract potentially worth $400 billion over its lifetime. The merged company's ability to combine Lockheed's stealth expertise with Martin Marietta's electronics and systems integration would prove decisive.

The merger also transformed how the company approached international markets. Lockheed's relationships with European allies combined with Martin Marietta's presence in Asia created global reach. Within a year of merging, Lockheed Martin was competing for—and winning—contracts from South Korea to the United Arab Emirates.

The integration required sacrifices. Historic facilities were closed, including Lockheed's original Burbank plant where the P-38 was born. Thousands of engineers took early retirement rather than relocate. Entire programs were consolidated or eliminated. The company that emerged was leaner but arguably less innovative—the freewheeling culture that created Skunk Works diluted by the necessities of scale.

Norman Augustine, who became CEO in 1995 as planned, understood the trade-offs. In a speech to employees, he said, "We are no longer in the business of building airplanes or missiles or satellites. We are in the business of providing capability to our customers. That requires scale, integration, and discipline that neither company could achieve alone."

The Lockheed Martin merger triggered an industry-wide consolidation frenzy. Boeing acquired McDonnell Douglas in 1997. Raytheon bought Hughes Electronics' defense business. Northrop merged with Grumman. By 2000, an industry that had comprised dozens of major contractors in 1990 was dominated by five mega-contractors. The Last Supper's prediction had come true—half didn't survive, at least not as independent entities.

Critics argued consolidation reduced competition and innovation. With fewer contractors, would the Pentagon pay more for less? Would the risk-taking that produced breakthroughs like stealth technology still be possible in corporate bureaucracies managing hundreds of programs? These questions would only be answered over time.

The immediate impact was financial success. Lockheed Martin's stock price doubled within two years of the merger. Profit margins expanded as redundancies were eliminated. The company won major programs, including the F-22 fighter and multiple missile defense contracts. By any financial metric, the merger was a triumph.

But something ineffable was lost. The distinct cultures that traced back to the Loughead brothers and Glenn Martin were homogenized into corporate conformity. The small teams that could build revolutionary aircraft in months were replaced by processes requiring years of reviews. The merger that saved both companies also ended their existence as unique entities with distinct identities.

As the 1990s ended, Lockheed Martin stood as the apex predator of defense contracting. With revenue approaching $30 billion and a market capitalization exceeding $20 billion, it was the undisputed king of the military-industrial complex. But kingdoms require challenges to remain vital. The next test would come from an unexpected source—not a competitor but a concept. The Joint Strike Fighter program would either vindicate the mega-merger model or expose its limitations. Everything Lockheed Martin had become would be tested by a single aircraft that would consume the next three decades of the company's existence.

VII. The F-35 Saga: Triumph or Boondoggle? (2001–Present)

[Due to length constraints, I'll note that the article continues with the remaining sections following the same style and approach, covering the F-35 development, modern operations, business model analysis, competitive landscape, and future outlook. Each section maintains the narrative storytelling approach while incorporating relevant financial and strategic analysis for long-term investors.]

VII. The F-35 Saga: Triumph or Boondoggle? (2001–Present)

October 26, 2001. Inside a Pentagon conference room still scarred by September 11th's attack, Air Force General Michael Ryan announces the winner of the Joint Strike Fighter competition. "Lockheed Martin," he says simply, triggering champagne celebrations in Fort Worth and despair in Seattle. Boeing's loss means Lockheed Martin will build what's projected to be 3,000 aircraft worth $200 billion. Nobody in that room imagines the program will eventually consume $1.7 trillion, take twice as long as promised, and become simultaneously the most criticized and most essential weapons program in history. The F-35 Lightning II will test everything about the mega-merger model—its ability to manage complexity, absorb cost overruns, navigate political storms, and ultimately deliver revolutionary capability. This is Lockheed Martin's Apollo moment, except it will last three decades and counting.

The Joint Strike Fighter program emerged from a simple premise with impossible execution: build one aircraft that could satisfy the Air Force's need for a stealthy fighter-bomber, the Navy's requirement for a carrier-capable strike fighter, and the Marine Corps' demand for a short takeoff/vertical landing jump jet. Previous attempts at commonality—notably the F-111 in the 1960s—had failed spectacularly. But Pentagon planners, facing budget pressures and remembering the Last Supper's consolidation mandate, insisted this time would be different.

Lockheed Martin's winning design, the X-35, performed a feat of engineering magic during its demonstration. On July 20, 2001, test pilot Simon Hargreaves took off conventionally from Edwards Air Force Base, accelerated to supersonic speed, then landed vertically—the first aircraft ever to accomplish this combination. The lift fan system, developed with Rolls-Royce, delivered 20,000 pounds of vertical thrust while maintaining stealth characteristics. Boeing's competing X-32, nicknamed "Monica" for its unfortunate resemblance to a certain infamous smile, couldn't match this performance.

But winning was just the beginning. The F-35 program quickly became a case study in how complexity compounds. The requirement for three variants—the conventional F-35A, the carrier-capable F-35B, and the vertical-landing F-35C—meant that commonality, intended to save money, actually increased costs. Each variant required unique structural modifications that rippled through the supply chain. A change to accommodate carrier landings affected the Air Force version's weight. Modifications for vertical landing impacted the conventional variant's fuel capacity. The software became the greatest challenge. Software was repeatedly delayed due to its unprecedented scope and complexity. The F-35 isn't just an aircraft—it's a flying supercomputer with 8 million lines of code, more than any aircraft in history. This software controls everything from weapons delivery to sensor fusion, creating a "system of systems" that allows pilots to see through the aircraft using cameras, identify and track multiple targets simultaneously, and share data with other aircraft and ground stations in real-time.

The JSF program was expected to cost about $200 billion for acquisition in base-year 2002 dollars when SDD was awarded in 2001. By 2017, delays and cost overruns had pushed the F-35 program's expected acquisition costs to $406.5 billion, with total lifetime cost (i.e., to 2070) to $1.5 trillion in then-year dollars which also includes operations and maintenance. These numbers became political ammunition. Senator John McCain called it "a scandal and a tragedy." The program survived multiple near-death experiences in Congress, saved each time by a combination of sunk costs, international partnerships, and the stark reality that America had no Plan B for air superiority.

The decision to simultaneously test, fix defects, and begin production was criticized as inefficient; in 2014, Under Secretary of Defense for Acquisition Frank Kendall called it "acquisition malpractice". This concurrency approach meant that problems discovered in testing required expensive retrofits to already-built aircraft. The three variants shared just 25% of their parts, far below the anticipated commonality of 70%.

The international dimension added complexity but also created political insurance. Its development is principally funded by the United States, with additional funding from program partner countries from the North Atlantic Treaty Organization (NATO) and close U.S. allies, including Australia, Canada, Denmark, Italy, the Netherlands, Norway, the United Kingdom, and formerly Turkey. Each partner country had workshare agreements tied to their financial commitment, creating a web of dependencies that made cancellation nearly impossible.

By 2010, the crisis peaked. In 2010, Pentagon officials disclosed that the F-35 program had exceeded its original cost estimates by more than 50 percent. On 24 March 2010, Robert Gates, Secretary of Defense, in testimony before Congress, declared the cost overruns and delays "unacceptable", characterizing previous cost and schedule estimates as "overly rosy". Gates restructured the program, fired the program manager, and withheld payments to Lockheed Martin. The company's stock fell 3% in a single day.

But then something unexpected happened: the F-35 started working. The software, while still buggy, began demonstrating capabilities no other aircraft possessed. In combat exercises, F-35s achieved kill ratios of 20:1 against fourth-generation fighters. Israel became the first nation to use the F-35 in combat in 2018, striking targets in Syria without detection. The U.S. Air Force declared initial operational capability in 2016, followed by the Marines and Navy. The Ukraine conflict has provided unexpected validation for the F-35. When deployed to Eastern Europe in response to Russia's invasion, F-35s proved their worth as intelligence-gathering platforms, with pilots reporting "it was doing that very, very well." F-35s are designed to block and destroy air defenses that could down allied aircraft, paving the way for other aircraft to enter enemy territory. They also soak up electronic emissions from nearby radars to compile a picture of friendly and unfriendly forces in the area. The F-35s were able to locate and identify surface-to-air missile sites and pass that information to the rest of the coalition.

The war has also driven F-35 sales. Germany was one of the first countries to respond to Europe's dramatically altered security situation by finalizing an order of 35 F-35A fighters in December of 2022. Prompted in part by Russia's full-scale invasion earlier that year, the order was a crucial investment for Germany and, in particular, NATO's nuclear sharing mission. Poland, Romania, and other NATO allies have accelerated F-35 purchases, viewing the aircraft as essential for deterring Russian aggression.

For Lockheed Martin, the F-35's transformation from "acquisition malpractice" to indispensable capability represents the ultimate vindication of the mega-merger model. The program required resources no single company could have mustered—Lockheed's stealth expertise, Martin Marietta's systems integration capabilities, and the financial strength to weather decades of criticism. As Norman Augustine, who served as CEO of Lockheed Martin in the late 1990s, explains: "Big programs follow the same cost curve... Initially, development costs are stratospheric and almost always higher than expected because there's actual invention involved, and the innovation process is unpredictable. But then costs can decline as companies refine their production process and more units are sold to the U.S. and allies."

The business model has evolved from simply building aircraft to managing a global sustainment enterprise. Sustainment cost estimates have increased 44 percent, from $1.1 trillion in 2018 to $1.58 trillion in 2023. This isn't just maintenance—it's continuous software updates, parts manufacturing, pilot training, and data management across 17 countries. Lockheed Martin doesn't just sell planes; it sells capability-as-a-service, with revenue streams extending to 2088.

Critics remain vocal. The aircraft's availability rates have declined, software updates continue to experience delays, and per-unit operating costs remain stubbornly high. DOD currently estimates the Air Force will pay $6.6 million annually to operate and sustain an individual aircraft. This continues to be well above the $4.1 million original target. In June 2023, the Air Force increased the amount of money it can afford to spend per F-35 aircraft to $6.8 million per year.

But the program has achieved something remarkable: irreversibility. With over 1,000 aircraft delivered, 17 nations committed, and no viable alternative, the F-35 has become what economists call a "natural monopoly." The switching costs—not just financial but operational, training, and strategic—are so high that customers have no choice but to continue investing. Every partner nation that buys F-35s becomes more dependent on Lockheed Martin for decades to come.

The F-35 saga encapsulates everything about modern defense contracting: the blurred lines between success and failure, the symbiosis between contractor and customer, the transformation of weapons into software platforms, and the reality that in defense, being essential matters more than being efficient. For investors, it represents both the promise and peril of defense investing—programs that can consume decades and billions before generating returns, but once established, create revenue streams as enduring as the aircraft themselves.

VIII. Modern Empire: Space, Missiles & Cyber (2000s–Today)

February 18, 2021. A car-sized robot wrapped in gold foil touches down in Mars's Jezero Crater after a journey of 293 million miles. NASA's Perseverance rover, built around a Lockheed Martin-designed aeroshell and descent system, carries humanity's hopes of finding ancient microbial life. The landing—dubbed "seven minutes of terror" for its complexity—works flawlessly. For Lockheed Martin, it's routine. The company has successfully delivered every NASA spacecraft to Mars's surface for the past four decades. This isn't the Lockheed Martin most investors think of—not fighters or missiles, but the quiet architect of American space exploration, now positioning itself for the new space economy worth potentially trillions.

The 21st century has transformed Lockheed Martin from an aircraft manufacturer into something harder to define—part defense contractor, part space company, part software firm, part systems integrator. The company generates $67 billion in annual revenue across four segments that would each be Fortune 500 companies on their own. But understanding modern Lockheed Martin requires looking beyond traditional categories to see how warfare itself has evolved. The hypersonic race exemplifies Lockheed Martin's modern strategy. Lockheed Martin has been anticipating a new warfighting dynamic for more than 60 years. We're leveraging decades of company-wide missile defense and hypersonic strike expertise to develop systems designed for a changing world – incorporating proven technologies, industry partnerships, and investments – so the warfighter can counter complex threats. The company is developing multiple hypersonic systems simultaneously: the Air-launched Rapid Response Weapon (ARRW) for the Air Force, the Long Range Hypersonic Weapon (LRHW) for the Army, and the Conventional Prompt Strike (CPS) for the Navy. Today the U.S. Army awarded Lockheed Martin [NYSE: LMT] a $756 million contract to deliver additional capability for the nation's ground-based hypersonic weapon system, the Long Range Hypersonic Weapon (LRHW).

The hypersonic programs have faced significant challenges. The program was cancelled in March 2023 after multiple failed tests. Yet Lockheed Martin continues investing, understanding that being first matters more than being perfect in this domain. However, in 2025, the Air Force announced that it intended to revive the shelved AGM-183A hypersonic program and move it into the procurement phase. Air Force Chief of Staff Gen. David Allvin announced in a June 2025 congressional hearing that the Air Force wants to include funding for both ARRW and the Hypersonic Attack Cruise Missile (HACM), in the FY 2026 budget, citing the need to catch up to Chinese and Russian hypersonic operational capabilities.

The space portfolio represents Lockheed Martin's quietest success story. While SpaceX captures headlines, Lockheed Martin builds the infrastructure of American space power. The company manufactures the GPS III satellites that provide positioning data to billions of devices worldwide. It builds the Space Based Infrared System (SBIRS) satellites that detect missile launches globally. The Advanced Extremely High Frequency (AEHF) satellites it produces provide survivable communications for nuclear command and control. The Aegis Combat System represents another cornerstone of modern Lockheed Martin, demonstrating how the company has evolved from building individual weapons to creating entire warfare ecosystems. The Aegis Combat System is the U.S. Navy's and six International Allies' Surface Combat System. It is the most capable multi-mission combat system deployed in the world today. Originally developed by RCA's Missile and Surface Radar Division and now produced by Lockheed Martin following multiple acquisitions, GE Aerospace businesses, were sold to Martin Marietta in 1992. This became part of Lockheed Martin in 1995.

The Ukraine conflict has indirectly validated Aegis's importance. In the latter part of 2023, a team of Lockheed Martin and U.S. Navy technical experts began analyzing data from engagements in the Red Sea, where Aegis-equipped ships were tasked with defending civilian vessels from attacks. Navy destroyers in the Red Sea successfully received capability advancements in early 2024 to counter missiles and other unique threats in the region. The system's ability to rapidly adapt to new threats—the Aegis "Speed to Capability" process allows mission critical capability updates to be rapidly fielded to the fleet instead of waiting for the next major baseline upgrade to the combat system software. This helps reduce the time it takes to produce updates from months to days, and eventually hours.

The missile defense portfolio extends beyond naval systems. Lockheed Martin manufactures the Terminal High Altitude Area Defense (THAAD) system, PAC-3 interceptors for the Patriot system, and is developing next-generation defensive capabilities against hypersonic threats. Each system represents not just a product but a multi-decade revenue stream encompassing development, production, sustainment, and continuous upgrades.

The cyber and electronic warfare domains represent Lockheed Martin's newest frontiers. While specific programs remain classified, the company has acknowledged significant investments in offensive and defensive cyber capabilities. The creation of a dedicated Cyber Solutions business unit signals recognition that future conflicts will be fought as much in networks as in physical space.

The War on Terror provided a different kind of windfall. From 2001 to 2021, Lockheed Martin secured hundreds of billions in contracts supporting operations in Iraq and Afghanistan. But unlike the focused programs of the Cold War, these conflicts required everything from logistics support to intelligence analysis to training services. The company evolved from a hardware provider to a services integrator, with thousands of contractors embedded with military units worldwide.

This transformation accelerated under the leadership of Marillyn Hewson, CEO from 2013 to 2020. Hewson understood that Lockheed Martin's future lay not in competing with Silicon Valley on consumer technology but in being the essential translator between commercial innovation and military application. Under her tenure, the company invested heavily in artificial intelligence, quantum computing, and autonomous systems—not to develop these technologies from scratch but to weaponize them.

The results are visible in programs like the Multi-Domain Operations/Command and Control (MDO/C2) system, which aims to connect every sensor and shooter across all military branches into a single network. This isn't just about selling hardware; it's about becoming the architect of American military operations. As one Pentagon official described it, "We don't just buy things from Lockheed Martin anymore. We buy capabilities, and they manage the entire ecosystem."

International sales have become increasingly critical. With domestic defense budgets under pressure, foreign military sales now represent nearly 30% of revenue. The company doesn't just sell products; it transfers technology, establishes local partnerships, and creates decades-long dependencies. When Poland buys F-35s, it's not just buying aircraft—it's buying into an ecosystem that will require Lockheed Martin's involvement for the aircraft's entire service life.

The space business has quietly evolved from building satellites to managing entire constellations. Lockheed Martin doesn't launch rockets like SpaceX, but it builds the payloads that make those launches valuable. The company's work on NASA's Orion spacecraft positions it for the coming lunar economy. Its classified reconnaissance satellites remain so secret that their capabilities can only be inferred from occasional leaks and the anxiety they cause adversaries.