Lumine Group: The Constellation Playbook on Steroids

I. Introduction & Episode Roadmap

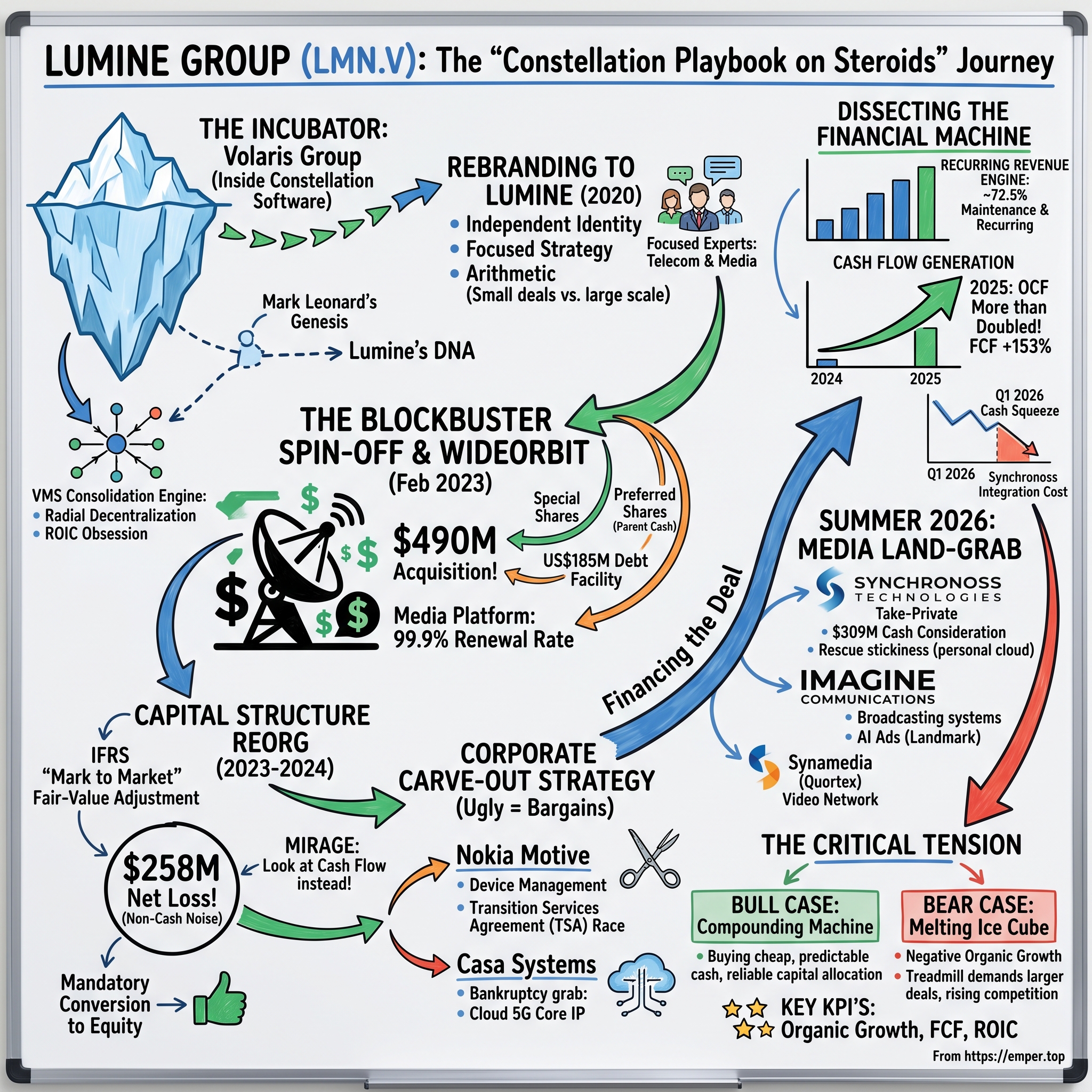

Picture the scene in late February 2023. A new ticker, LMN.V, blinks onto the Toronto Stock Exchange Venture board — the junior exchange, the place where mining exploration companies and biotech hopefuls usually live. Nothing about the venue suggests importance. And yet, on the very same day this obscure symbol begins trading, the company behind it closes a $490 million acquisition of an American media software company most investors have never heard of.1 Spin-offs are supposed to be quiet. They are supposed to shuffle onto the exchange, trade thin for a few months while index funds figure out what to do with them, and slowly find their footing. This one arrived with a platform deal already stapled to its chest.

That company was Lumine Group Inc., and it was not born in a garage or a dorm room. It was calved off a glacier — Constellation Software Inc., the Canadian serial acquirer that has become one of the most studied capital-allocation machines of the last two decades. Constellation's founder, Mark Leonard, built a $50-billion-plus empire by doing something deceptively boring: buying small, unglamorous vertical-market software (VMS) businesses, holding them forever, and reinvesting their cash into more of the same. Lumine is that machine, cloned, aimed at a single industry — the software that runs telecom networks and media companies — and set loose with its own balance sheet.

The obvious question, and the one this piece will keep returning to, is whether Lumine is simply a carbon copy of its parent, or something more aggressive and more fragile. Constellation historically hunted for tiny deals at modest prices. Lumine, from day one, has hunted elephants: a half-billion-dollar media platform, corporate carve-outs from Nokia, bankruptcy assets from Casa Systems, and — in 2026 — a public-to-private takeover of a distressed NASDAQ company and two more media acquisitions inside a single summer. The playbook is Constellation's. The scale, and the risk profile, are not.

Here is the map. We start in the incubator, inside a Constellation operating group called Volaris, where a telecom executive named David Nyland spent the better part of a decade quietly assembling the pieces. We walk through the 2020 rebrand, the 2023 spin-off, and the WideOrbit deal that gave Lumine instant heft. We untangle a capital structure so baroque it produced a reported quarter-billion-dollar net loss that had almost nothing to do with the actual business. We examine the carve-out strategy — the hardest, ugliest, most lucrative kind of deal in software — through Nokia Motive and Casa Systems. We cover the Synchronoss rescue and the summer 2026 media land-grab. Then we get cold and quantitative: the recurring-revenue engine, the cash flows, and the number that keeps skeptics up at night — organic growth that has spent more time negative than positive.

Because that is the central tension. Lumine's revenue has compounded beautifully. Its cash flow, in 2025, more than doubled.2 And yet the underlying businesses it buys are, in many cases, slowly shrinking. Bulls call it a compounding machine. Bears call it a treadmill — a company that must keep acquiring simply to stand still, buying "melting ice cubes" and hoping the acquisition math outruns the melt. Both cases are internally coherent. The job here is to test them.

There is one more piece of framing worth planting before we begin, because it recurs throughout the story. Lumine is not really a software company in the way most investors use that phrase. It does not live or die by a single product roadmap, a viral growth loop, or a land-grab for a new market. It is, more precisely, a capital-allocation engine that happens to own software. The product it manufactures is not code; it is decisions — decisions about which businesses to buy, at what price, and what to do with the cash they generate afterward. That reframing matters because it changes what you should watch. For a normal software company, you track product and market share. For Lumine, you track the price it pays, the return it earns, and the durability of the cash it is buying. Keep that lens on for the next three and a half years of history we are about to walk through, and the company's every move starts to make sense.

II. The Constellation Software Genesis & The Volaris Incubator

To understand Lumine, you first have to understand the strange genius of the thing that made it. Constellation Software was founded in 1995 by Mark Leonard, a former venture capitalist who noticed something that the rest of the technology world found boring to the point of invisibility: vertical-market software companies — the firms that write the software running a specific niche, like municipal water utilities, or bus scheduling, or funeral homes — were tiny, unloved, and astonishingly durable. Once a customer installs the software that runs their core operation, they almost never rip it out. Switching means risking a catastrophe: a billing run that fails, a scheduling system that goes dark. So these little companies could raise prices year after year and keep their customers, throwing off cash like a well with no bottom.

Leonard's insight was not that these businesses were good. Plenty of people knew that. His insight was that nobody was systematically buying them, and that if you bought enough of them, held them forever, and reinvested their cash into buying more, you could compound capital at extraordinary rates without ever needing a single blockbuster. The Constellation culture that grew around this idea became almost monastic in its discipline: radical decentralization, where each acquired business keeps its name and its managers; a tiny head office; and a near-religious obsession with return on invested capital, or ROIC — the amount of profit generated for every dollar of capital deployed. Managers who could not clear an internal hurdle rate did not get to deploy capital. Full stop.

To appreciate why this compounds so violently, it helps to sit with the arithmetic for a moment, because it is genuinely counterintuitive. Imagine a business that earns a 30% return on the capital it invests, and imagine it can find enough new acquisitions to reinvest all of that cash at the same rate. In a decade, a dollar becomes roughly thirteen. The magic is not in any single deal — each little software company is dull, throwing off a predictable trickle of maintenance revenue — but in the relentless recycling of cash into more dull, predictable trickles, each of which then throws off cash of its own. Leonard understood something that most operators never internalize: the reinvestment rate matters as much as the return itself. A great business that cannot reinvest its cash is a cash cow; a merely good business that can reinvest all of its cash at a good return is a compounding machine. Constellation's whole organizational design — the decentralization, the hurdle rates, the refusal to pay dividends for most of its history — exists to keep the reinvestment flywheel spinning.

Leonard himself became something of a cult figure among investors, in part because of his famous shareholder letters, which read less like corporate communications and more like the private notebooks of a philosopher-investor. He wrote candidly about mistakes, about the corrupting effect of cheap capital, about the danger of "empire-building," and — tellingly — he eventually stopped giving guidance, stopped doing earnings calls, and stopped holding conventional investor meetings, on the theory that catering to short-term shareholders warped long-term decision-making. This is the intellectual DNA that Lumine inherited: a deep suspicion of growth for its own sake, a preference for owner-operators with skin in the game, and a conviction that the scarcest resource in the world is not good businesses but disciplined places to put capital.

By the early 2010s, Constellation had organized itself into a handful of operating groups, each a semi-autonomous empire in its own right. One of them was Volaris Group, run by Mark Miller, a Constellation lifer who would eventually rise to become president of the entire parent company. And it was inside Volaris, in 2014, that the Lumine story actually begins — with the hiring of David Nyland, a telecom-technology executive brought in to build something Constellation did not yet have: a dedicated portfolio aimed squarely at the software that runs communications networks and media companies.10

The choice of vertical was deliberate. Telecom operational and business support systems — the unglamorous plumbing known in the industry as OSS and BSS, the software that provisions your phone line, rates your data usage, and generates your bill — sit at the deepest, stickiest layer of a carrier's operations. Ripping one out is like performing open-heart surgery on a running patient. That stickiness is precisely the quality Constellation prizes. What made the niche doubly attractive was that many of these assets were owned by large, distracted corporate parents — equipment makers, conglomerates, private-equity roll-ups — who had bought the software as an afterthought and then starved it of investment. Underloved, underfunded, and mission-critical: to a Constellation operator, that is not a problem. That is a shopping list.

So Nyland's team went to work, quietly, as a subgroup buried inside Volaris. They bought niche billing engines, number-routing databases, network-management tools — the kind of software whose names mean nothing outside a telco engineering department. There were no press conferences. For years this was an internal science experiment: could the Constellation method work in a vertical as technically specialized and cyclically exposed as telecommunications? The answer, gathered deal by deal, was yes. And that quiet accumulation of both software assets and institutional know-how is what would eventually justify cutting the whole thing loose.

III. Rebranding to Lumine & The Decoupling Rationale

Every corporate spin-off has a moment where the child gets a name of its own, and for the communications portfolio inside Volaris that moment came in 2020, when the group formally adopted the name Lumine Group.10 A rebrand is rarely just cosmetic. Names inside Constellation are signals, and giving the communications-and-media portfolio a distinct identity told the internal world that this was no longer a science experiment nested inside Volaris. It was a business unit with its own thesis, its own leadership, and — though it was not yet obvious to outsiders — its own destiny as a standalone public company.

The deeper question is why Constellation would ever want to let a piece of itself go. This is a company whose entire religion is buying and holding forever; spinning out a healthy, cash-generating division seems almost heretical. But the logic, once you see it, is pure Constellation.

The first reason was arithmetic. Constellation had grown so large that its traditional bread-and-butter — acquiring software companies for a few million dollars each — could no longer meaningfully move its results. When you are a $40-billion enterprise, a $3 million deal is a rounding error, no matter how brilliant. But those same small deals could still move the needle enormously for a smaller, dedicated vehicle. More importantly, a separately listed company could tap its own currency — its own shares and its own debt — to chase far bigger transactions than Constellation would comfortably underwrite from the center. A public Lumine could go hunting for elephants that a division of Constellation never could.

The second reason was focus. Telecom and media software marches to its own drum: brutal industry cycles, a customer base of a few hundred giant carriers and broadcasters — Verizon, AT&T, the big television networks — and a regulatory overlay that a generalist software buyer would find bewildering. Concentrating that expertise in a dedicated management team, with dedicated incentives, produces better deals and better operations than diffusing it across a sprawling parent.

And then there was the third reason, the one investors whisper about: valuation arbitrage. A focused, fast-growing VMS consolidator, trading in the open market with its own story, can command a richer multiple than the same assets buried inside a diversified conglomerate where they are invisible to all but the most obsessive analysts. Constellation had already run this experiment once, spinning out Topicus.com into a separately traded European vehicle in 2021 and watching the market assign it a healthy value. Lumine was the next iteration of a proven maneuver.

There is a subtler benefit to the spin-off structure that rewards a moment's thought, because it is central to why Constellation keeps doing this. A separately listed vehicle gives the operating team its own acquisition currency — publicly traded shares it can, when the price is right, use to buy businesses without spending cash. It gives them a cleaner scoreboard, so their performance is judged on the communications-and-media portfolio alone rather than diluted into Constellation's vast results. And it gives Constellation itself a way to keep controlling and benefiting from a growing empire while distributing shares to its own investors, effectively multiplying the number of disciplined capital-allocation vehicles it has running in parallel. Rather than one enormous ship that grows harder to steer as it gets bigger, Constellation has been deliberately spawning a fleet of smaller, faster boats — Topicus, Lumine, and others — each captained by operators with focused incentives. Lumine is one boat in that fleet, pointed at the single vertical its leadership knows best. The stage was set. What remained was to give the new company enough scale on day one that it would not be dismissed as a micro-cap curiosity — and that required a deal big enough to make the market pay attention.

IV. The Blockbuster Spin-Off & WideOrbit Acquisition (Feb 2023)

Most spin-offs are handed a portfolio and wished good luck. Lumine was handed a portfolio and, on the day it began trading, a $490 million acquisition that instantly doubled the size of the story. On February 22, 2023, Constellation and Lumine announced the completion of the purchase of WideOrbit Inc., and Lumine listed on the TSXV as an independent public company.1 It was a twin-track transaction: the spin-out and the acquisition, choreographed to close together, so that public investors met Lumine not as a collection of obscure telecom assets but as the owner of a marquee American media platform.

WideOrbit is worth dwelling on, because it explains a great deal about how Lumine thinks. If you have ever watched local television in the United States, you have interacted with WideOrbit's software without knowing it. The company builds the systems that local TV and radio stations use to manage their advertising — the software that decides which commercial airs in which slot, that traffics the ad, that reconciles what was promised against what actually ran, and that generates the invoice to the advertiser. It is deeply embedded plumbing for the local broadcast advertising business, and it enjoys the kind of customer retention that sounds like a typo: a historical renewal rate described as near-perfect, in the neighborhood of 99.9%.11 When a business keeps essentially every customer it has ever won, year after year, you are looking at a moat, not a marketing slogan. That kind of retention only happens when the cost and risk of leaving vastly outweigh whatever a competitor is offering.

Why is the retention so extreme? Because of what the software touches: money, and specifically the money a station cannot afford to get wrong. A local TV station's entire revenue depends on running the right commercial in the right slot and being able to prove it ran, so it can bill the advertiser. WideOrbit's software is the ledger, the traffic cop, and the invoice generator for that whole process, tied into the station's automation systems and its financial reporting. Swapping it out is not a software upgrade; it is a transplant of the organ that pumps the station's cash. Faced with that, stations do the rational thing and stay — even as WideOrbit raises prices. That dynamic, repeated across hundreds of broadcasters, is why a business in a mature, arguably declining medium like local television can still be a wonderful thing to own.

For Lumine, WideOrbit was the crown jewel — the high-margin, fortress-like cash engine that would fund everything to come. A consolidator lives or dies by the reliability of its internal cash generation, because that cash is the ammunition for the next deal. Anchoring the new company around an asset with near-total customer stickiness gave Lumine a dependable base from which to underwrite riskier, uglier transactions later. It also sent a signal to the market about Lumine's ambitions. Constellation had spent decades buying $2-million and $5-million companies; Lumine's opening move was a nine-figure platform. This was a declaration that the new vehicle intended to play a bigger game than its parent ever had at that stage of life — and, implicitly, that it would have to accept the higher prices and stiffer competition that bigger games entail.

The financing of the WideOrbit deal is where the Constellation family relationships get intricate, and where the seeds of a very messy capital structure were planted. Lumine did not simply write a $490 million check. It assembled the consideration from several sources. It issued 10,204,294 "Special Shares" to WideOrbit's selling shareholders, valued at roughly $222 million — meaning WideOrbit's founders rolled a large chunk of their proceeds into Lumine equity, tying their fortunes to the new company's stock rather than cashing out entirely.1 The cash portion came, in part, from Constellation itself: a Constellation entity (Trapeze) funded the cash by taking back 8,348,967 Preferred Shares in Lumine.1 And in March 2023, Lumine's WideOrbit subsidiary completed a US$185 million revolving credit facility with a syndicate of Canadian and U.S. banks, with a further US$75 million accordion available to expand it.6

Rolling the sellers into equity, leaning on the parent for the cash, and layering on bank debt — it was clever, capital-efficient, and it aligned the founders with Lumine's success. It also meant that from its very first day, Lumine carried a cap table with more moving parts than most companies accumulate in a decade, and those parts would soon produce some spectacularly confusing accounting.

V. The Complex Capital Structure & Reorganization (2023–2024)

Open Lumine's early financial statements and you meet a small zoo of securities. There were Subordinate Voting Shares, the ordinary shares that trade in the market. There was a single Super Voting Share, held by Constellation, engineered to keep the parent in control with roughly 50.1% of the vote no matter how much the public float grew. There were the convertible Preferred Shares held by the Constellation side, and the Special Shares held by WideOrbit's founders. Each of these instruments carried its own rights, its own conversion mechanics, and — crucially for what came next — its own accounting treatment.

Here is where a reader who is not an accountant needs a gentle guide, because the numbers Lumine reported in its first full year as a public company looked, on the surface, alarming. For fiscal 2024, Lumine reported a net loss of $258.9 million.7 A quarter-billion-dollar loss from a company that its own boosters describe as a cash-generating machine — how does that reconcile?

The answer is that the loss was almost entirely an accounting mirage. Under IFRS, the Preferred and Special Shares were classified not as equity but as liabilities, because of their conversion and redemption features. And liabilities like these must be "marked to market" every reporting period — that is, revalued to reflect what it would cost to settle them. As Lumine's stock price climbed, the value of the shares those instruments could convert into climbed with it, which meant the accounting value of the liability ballooned. That increase gets booked as an expense on the income statement. In other words, Lumine's stock did so well that its accounting punished it. The "loss" was the shadow cast by a rising share price on a set of convertible liabilities — a non-cash, fair-value adjustment, not a dollar of operating deterioration.7

This is the kind of thing that separates investors who read the MD&A — the management discussion and analysis buried behind the headline financials — from those who read only the top line. Anyone who saw "$258.9 million net loss" and fled missed that the underlying business was generating robust cash the entire time. It is also a useful reminder that headline net income, for a company with an exotic capital structure, can be nearly meaningless.

It is worth pausing here to puncture a myth that surrounds companies like this one. The consensus narrative on any Constellation offshoot is that reported earnings are conservative and understated, buried under acquisition amortization and non-cash noise, and that the true economics are always better than they look. Often that is right. But the Lumine capital structure cut the other way for a while: the fair-value accounting made the company look far worse than it was in 2024, then far better than the underlying business had changed when the liabilities were extinguished in 2025. The reality is neither the flattering nor the alarming headline number, but the boring middle — the cash the operating businesses actually threw off, which marched steadily upward the whole time regardless of what the net-income line said. The lesson for anyone underwriting Lumine is to anchor on cash flow and to treat reported net income, in any given year, with real suspicion until you have traced where it came from.

Recognizing that this complexity was a bug rather than a feature, Lumine moved to clean it up. Over the course of late 2024, it executed a mandatory conversion and settlement of the Preferred and Special Shares into ordinary Subordinate Voting Shares, collapsing the liability-classified instruments into plain equity.7 With the preferred and special share liabilities extinguished, the fair-value revaluations that had generated the phantom loss disappeared. The mechanical result was dramatic: net income swung from that large reported loss to a positive figure of roughly $118.8 million in fiscal 2025.2 Nothing about the actual businesses changed between those two numbers; what changed was that the accounting finally started telling a story an ordinary investor could read. The simplification also matters for a subtler reason — it made Lumine's shares a cleaner acquisition currency and its balance sheet easier to underwrite, which is exactly what a company that intends to keep buying larger and larger targets needs. And larger targets were precisely what came next.

VI. The Corporate Carve-Out Strategy: Nokia Motive & Casa Systems

There is a hierarchy of difficulty in software M&A, and at the very top — the deals that make bankers sweat and integration teams reach for the antacids — sit corporate carve-outs. Buying a whole company is comparatively simple: it arrives with its own bank accounts, its own HR systems, its own legal entity, its own coffee machines. A carve-out is the opposite. You are buying a business unit that has spent years wired into a corporate parent's shared systems — its data centers, its payroll, its customer contracts, its office leases — and you have to surgically extract it, often while its own employees are still logging into the seller's email. It is the corporate equivalent of separating conjoined twins.

This is exactly the terrain Lumine chose to specialize in, and the logic is Constellation's logic taken to its natural conclusion. Large technology conglomerates buy software assets, fail to integrate or invest in them, and eventually decide they are non-core. Starved of development capital and buried inside an indifferent parent, these assets underperform — which makes them cheap. A buyer with genuine operational expertise and a decentralized model that lets the acquired business breathe can pay a distressed price, restore focus, and unlock value the seller could never be bothered to capture. The catch is that you have to actually be good at the surgery. Most buyers are not.

Lumine's first marquee demonstration came with Nokia. In December 2023, Lumine agreed to acquire Nokia's Device Management and Service Management Platform businesses, reviving the well-known "Motive" brand under which those products had once traded.[^8] These are the systems carriers use to remotely manage the millions of devices on their networks — the software that pushes a firmware update to your home router, or diagnoses why a set-top box has gone dark. Lumine had to take over a thicket of complex, long-dated carrier contracts, transition Nokia employees onto its own payroll, and stand up independent support operations — all under a Transition Services Agreement, the temporary arrangement under which the seller keeps the lights on for a fee while the buyer builds its own infrastructure. TSAs are ticking clocks: every month you rely on the seller's systems, you are paying rent and racing to become self-sufficient. Executing one cleanly is a genuine operational skill, and it is one Lumine claims as a core competence.

It is worth dwelling on what "Motive" actually does, because it illustrates why these unglamorous assets are so defensible. When your home broadband slows to a crawl and you call your carrier, the technician on the other end does not physically inspect your router. They reach into it remotely, through exactly the kind of device-management software Motive provides, to run diagnostics, push a configuration change, or update the firmware. Multiply that across the tens of millions of devices a large carrier has deployed, and you have a system that is not optional — it is the nervous system through which the carrier manages its entire fleet of customer equipment. Nokia had let it drift as a non-core piece of a giant equipment business. In Lumine's hands, refocused and adequately funded, the same asset could serve its carrier customers better precisely because someone finally cared about it. That is the carve-out thesis in miniature: the value was always there; it was the parent's neglect that made it cheap.

Then came Casa Systems, and here Lumine showed a colder, more opportunistic side. Casa Systems was a telecom equipment and software company that spiraled into bankruptcy, and in April 2024 it moved to sell off its assets to preserve value and jobs through a court-supervised process.8 Lumine stepped into the distress and cherry-picked the pieces it wanted — Casa's cloud-native 5G core software and radio-access-network assets, strategically valuable intellectual property that, in a bankruptcy fire sale, could be had at a fraction of what it cost to build. Buying critical IP for cents on the dollar while a competitor is being carved up by creditors is not for the squeamish, and it says something about the Lumine temperament: this is a buyer that moves fastest precisely when a seller is at its most desperate.

The pattern across both deals is the same. Complexity and distress are not obstacles to be avoided; they are the source of the bargain. The harder the deal is to execute, the fewer bidders show up, and the cheaper the asset becomes. Lumine is, in effect, being paid for its willingness to do the ugly work. But there is a limit to how much value a carve-out or a bankruptcy estate can hold, and as Lumine's cash flows grew, it needed a bigger canvas. That canvas turned out to be an entire distressed public company.

VII. Public-to-Private Transition: The Synchronoss Technologies Rescue (Feb 2026)

Synchronoss Technologies was once a market darling. In its heyday it was a NASDAQ-listed telecom software company whose stock traded north of $40, riding the wave of the cloud and the smartphone boom. By the mid-2020s, it was something else entirely: a heavily indebted micro-cap, weighed down by an expensive layer of preferred stock, its equity a shadow of its former self, its story a cautionary tale about how quickly the market's affection can curdle. This is the kind of company that value investors circle and most acquirers avoid — too much debt, too much baggage, too much risk that the whole thing is a value trap.

Lumine saw something different. Underneath the balance-sheet wreckage sat a genuinely sticky asset: Synchronoss's cloud platform, the personal-cloud backup service that tier-one carriers like Verizon offer their subscribers to store photos and contacts. That is exactly the profile Lumine hunts — mission-critical, deeply embedded, high-margin recurring revenue, wrapped in a corporate structure that had destroyed shareholder value. The trick was to separate the good business from the bad capital structure.

In late 2025, Lumine agreed to take Synchronoss private in an all-cash transaction at $9.00 per share.9 The deal completed on February 13, 2026, and the numbers reveal the shape of the opportunity.4 The implied equity value was roughly $116.4 million — a modest price for the shares themselves.4 But the enterprise value, which includes the debt and the high-cost preferred stock that Lumine had to absorb or refinance, was approximately $258.4 million.4 The gap between those two figures — nearly $142 million — is the story. Lumine was not really paying for equity; it was paying to take on a distressed balance sheet and fix it. In its Q1 2026 report, Lumine disclosed the aggregate cash consideration for the acquisition at $309.3 million, reflecting the full cash cost of the transaction including debt settlement.3

The turnaround blueprint is straightforward in concept and hard in execution. Take the company private and immediately strip out the costs that only a public company bears — the listing fees, the investor-relations apparatus, the sprawling public-company G&A. Renegotiate or exit the non-core contracts that were dragging on margins. And refocus the entire organization on the one thing that actually works: the sticky, high-margin cloud-backup relationships with a handful of enormous carriers. It is the private-equity turnaround playbook, executed by a permanent owner with no five-year exit clock, which in theory allows Lumine to be more patient than the buyout firms it competes against.

There is a deeper strategic elegance to targeting a company like Synchronoss that is worth naming, because it recurs across Lumine's biggest deals. Distressed public companies are, in a sense, the ideal hunting ground for a disciplined buyer, because the market's judgment about the equity — that it is nearly worthless — is frequently correct, while its judgment about the underlying business is frequently too harsh. A company can be a terrible stock and a decent business at the same time: crushed by debt taken on years earlier, saddled with a bloated cost structure, and led by managers who lost the confidence of investors, all while its core product continues to do essential work for customers who have no intention of leaving. Lumine's edge is the ability to tell those two things apart — to see the good business trapped inside the bad security — and then to have the operational capability to free it. The private-equity firms it competes with can do the financial engineering; what Lumine claims to add is the permanent home and the operating discipline that keeps the freed business from simply being flipped and re-levered a few years later. Whether that claim survives contact with the messy reality of the Synchronoss integration is, again, a question the cash flows will answer.

Whether the theory holds is exactly the question the numbers will answer, because the Synchronoss integration did not come free — and, as we will see, it landed on Lumine's cash flow statement with a thud in the first quarter of 2026. Before we get to that reckoning, though, Lumine had a media empire to build.

VIII. The Media Empire Expands: Synamedia (Quortex) & Imagine Communications (Summer 2026)

If the first half of Lumine's story was about telecom plumbing, the summer of 2026 was about television. In the space of about a month, Lumine made two acquisitions that, taken together, amounted to a deliberate consolidation of the infrastructure that gets video from a broadcaster's control room to your screen — and the advertising that pays for it.

The first came in June 2026, when Lumine completed the acquisition of Synamedia's video network business, folding it into a business rebranded as Quortex.[^9] The technology here is the modern backbone of streaming: cloud-based systems for processing and delivering over-the-top video — the "OTT" services you know as streaming apps — at scale, spinning up capacity on demand rather than running racks of dedicated hardware. As media companies migrate from traditional broadcast to internet delivery, the software that manages that transition becomes increasingly valuable. Buying it deepened Lumine's capabilities in exactly the direction the industry is moving.

The Quortex rebrand also hints at where Lumine sees the value migrating. Traditional broadcast video ran on specialized, expensive hardware — dedicated boxes doing dedicated jobs, racked in a station's machine room. The industry's decade-long migration is toward software that does the same jobs in the cloud, elastically, paying only for the capacity used during a big live event and scaling back down afterward. A company that owns the software layer of that transition captures value regardless of which streaming service ultimately wins the battle for viewers, in much the same way a toll road profits from traffic without betting on any particular car. That is the optionality Lumine is buying into on the media side: not a wager on any one broadcaster or platform, but a position in the plumbing they all depend on.

The second, and larger in strategic significance, came on July 1, 2026, when Lumine announced the acquisition of Imagine Communications Holdings Inc.5 Imagine is a global provider of the systems that sit at the heart of a modern television operation: video connectivity, channel origination and playout — the software and hardware that assembles and transmits a television channel — and, critically, AI-enabled advertising management and monetization tools, including its Landmark sales platform.5 Lumine bought Imagine from the private-equity firm Gores Group, and the financial terms were not disclosed.5 The business would continue to operate independently under Lumine's decentralized model, as every acquisition does.

Step back and the chessboard comes into focus. On one side, WideOrbit controls how local television and radio stations traffic and bill their advertising. On the other, Imagine now gives Lumine the systems that actually originate and play out the channels themselves, plus another layer of advertising technology through Landmark. Sandwiched in the middle is the video-delivery capability from Quortex. Lumine was assembling something close to an end-to-end grip on the media supply chain — from the moment a channel is assembled, to the way its video is delivered, to how the advertising inside it is sold, trafficked, and reconciled.

The independent investor's caution here is worth stating plainly, because it cuts against the triumphant framing. "End-to-end control of the media supply chain" sounds formidable, but it is an assembled collection of separately run businesses, not an integrated product, and Lumine's own decentralized philosophy means these units are explicitly not being stitched together into a single platform. The moat, such as it is, comes from each individual business's stickiness, not from some emergent synergy across them. And the media businesses Lumine is buying face a real secular headwind: linear television, the substrate under WideOrbit and much of Imagine, is a mature-to-declining market as audiences and ad dollars migrate to digital. Lumine is buying dominant positions in a shrinking pond. That can still be a fine investment — a shrinking market with a fortress position throws off cash for a very long time — but it is a materially different proposition from buying growth. Which brings us to the numbers, where that tension becomes impossible to ignore.

IX. Dissecting the Financial Machine: Segment Dynamics & Cash Flows

For all the drama of the deals, Lumine reports itself, under IFRS, as a single operating segment. That is a common quirk of the Constellation family — the head office manages capital allocation centrally and resists the overhead of formal segment reporting — but it means investors have to reconstruct the underlying dynamics themselves. Internally, the portfolio really lives in two worlds.

The first is Media & Content — WideOrbit, Imagine Communications, the video assets in Quortex, and video-management software like Vidispine. These businesses tend to carry high margins, very high customer retention, and genuine optionality in the shift toward programmatic and connected-TV advertising. The second world is Communications & Network Applications — Synchronoss, the Motive assets from Nokia, number-management software like NetNumber, and the Casa 5G-core IP. These are the deep-value carve-outs: intensely sticky network infrastructure, bought cheaply, but structurally slower-growing and, in some cases, in gentle secular decline. One side of the house offers quality and modest growth optionality; the other offers cheap cash flows with a slow melt. Lumine's art is buying the second kind at prices low enough that the melt does not matter.

The quality of Lumine's earnings rests on a single, load-bearing fact: most of its revenue is recurring. In fiscal 2024, out of $668.4 million in total revenue, roughly $484.9 million — about 72.5% — was maintenance and other recurring revenue.7 That is the difference between a company that has to resell itself every year and one whose customers are contractually and operationally locked in. Recurring revenue of that quality is what lets a consolidator underwrite acquisitions with confidence, because the base cash flow is predictable enough to borrow against.

On top of that stable base, the acquisition machine drove impressive top-line compounding. Total revenue climbed 15% from $668.4 million in fiscal 2024 to $765.7 million in fiscal 2025.2 The momentum carried into the first quarter of 2026, when revenue reached $208.3 million, up 17% year over year.3 Growth like that, quarter after quarter, is the visible proof that the deal engine is running. But — and this is the crucial analytical point — almost all of it is bought. Strip out acquisitions and adjust for currency, and the picture is far more sober, a subject we will confront head-on in the bear case.

Where Lumine's 2025 truly shone was cash. Cash flow from operations more than doubled, from $115.0 million in fiscal 2024 to $236.5 million in fiscal 2025.2 Free cash flow available to shareholders — the company's preferred measure, roughly the cash left after the maintenance capital and taxes needed to keep the business running — jumped 153%, from $85.7 million to $217.0 million.2 A software business converting revenue to free cash at that rate is displaying the classic VMS profile: low capital intensity, high margins, and customers who pay in advance. On the surface, this is a cash machine performing exactly as advertised.

It is worth explaining why VMS businesses convert to cash so efficiently, because it is the mechanical reason the whole model works. A traditional manufacturer has to buy raw materials, build inventory, and wait to be paid, tying up cash at every step. A vertical-market software company does almost none of that. Its customers typically pay their annual maintenance and subscription fees up front, which means the business collects cash before it incurs most of its costs — negative working capital, in the jargon, where growth actually generates cash rather than consuming it. Its capital expenditure is minimal, because the "factory" is a team of engineers, not a plant. And its incremental margins are enormous, because once the software exists, selling another seat or renewing another contract costs almost nothing. Stack those traits together and you get a business that turns a strikingly high fraction of its revenue into free cash — which is precisely the fuel a serial acquirer needs. The reason Lumine can keep buying is that its existing businesses keep handing it cash faster than almost any other kind of enterprise could.

And then came the first quarter of 2026, which is where the machine sputtered and the bulls and bears got fresh ammunition at the same time. We will dissect the cash-flow squeeze in detail when we stress-test the story. For now, hold two facts in tension: full-year 2025 showed spectacular cash generation, and the very next quarter showed cash from operations falling by half. Both are true. The question is which one is the signal.

X. Competitive Edge: Porter's 5 Forces & Hamilton Helmer's 7 Powers

Why does any of this work? Why can a company buy slowly declining software assets and still compound value? The answer lives in the competitive structure of the niches Lumine operates in, and two frameworks help make it concrete. Neither should be treated as a scorecard that proves the bull case; they are lenses for locating where durable advantage actually sits — and where it does not.

Start with Hamilton Helmer's 7 Powers, a taxonomy of the specific, structural advantages that let a business earn excess returns. Lumine plausibly holds three.

The first and most important is high switching costs. This is the entire foundation. An OSS/BSS billing system or a television station's ad-trafficking engine is not a discrete product a customer can swap on a whim; it is woven into the daily operation of the enterprise. Migrating away risks operational catastrophe — a failed billing run that infuriates millions of subscribers, or an ad-scheduling meltdown that costs a station its revenue for the night. Faced with that risk, customers do something that looks irrational until you understand the stakes: they accept regular price increases rather than switch. WideOrbit's near-99.9% retention is the empirical fingerprint of this power.11 Pricing power that survives year after year is not an assumption here; it is visible in the renewal rates.

The second is closer to a cornered resource: the Constellation operating playbook itself. The decentralized management model, the internal databases of best practices, the accumulated institutional knowledge of how to price, structure, and integrate a complex carve-out — this is a genuinely proprietary corporate asset that a new entrant cannot buy or quickly replicate. It is the reason Lumine can execute a Nokia carve-out or a Casa bankruptcy grab that others would botch. The caveat, and it is a real one, is that this "power" is a claim about execution skill, and execution skill is harder to verify from the outside than a retention rate. It is credible, but it is not proven the way switching costs are.

The third is scale economies in capital and deal execution. Lumine can draw on a large corporate credit facility and shares centralized legal, tax, and M&A expertise across its whole portfolio, which lowers the marginal cost of doing each additional deal.6 A one-person shop cannot underwrite a $300 million take-private; Lumine can do it as routine. There is also a reputational flywheel embedded in scale: sellers of complex telecom and media assets — a Nokia, a Gores Group, a bankruptcy trustee — increasingly know that Lumine is a serious, fast-moving buyer that will actually close, and that reputation earns it looks at deals and a seat at negotiating tables that a first-time acquirer would never get. In a market where the hardest part of a carve-out is trusting the counterparty to complete a messy transaction, being the known quantity is itself an advantage.

Now run Porter's Five Forces over the same terrain and the picture reinforces itself. The threat of new entrants is extremely low: writing core telecom-routing or broadcast-scheduling software from scratch requires decades of accumulated domain expertise and certification, and no rational venture capitalist funds a startup to attack a market of a few hundred customers who will never switch. The bargaining power of buyers, counterintuitively for such large customers, is low — a carrier or a broadcaster is more dependent on the software than the software vendor is on any single customer, because the customer cannot easily leave. Competitive rivalry is muted because most of these niches support only one or two serious players; they are too small and too specialized to attract a crowd.

But an honest application of Porter's does not stop at the flattering forces, and here the framework earns its keep by exposing the one that genuinely threatens Lumine: the threat of substitutes. The danger to a legacy OSS/BSS or on-premise broadcast system is not a direct competitor building a better version of the same thing. It is a fundamentally different architecture — cloud-native, API-first platforms from the likes of AWS, Salesforce, Twilio, and a generation of streaming-native tools — that lets a customer bypass the old system entirely rather than replace it head-on. Switching costs protect you from a rival; they protect you far less from a customer who re-architects around you over a decade. That substitution pressure is the mechanism underneath Lumine's negative organic growth, and it is the hinge on which the entire investment debate turns. The moat is real. The pond it protects may be slowly draining.

XI. Playbook: Management, Reinvestment Incentives, & Capital Discipline

Companies like Lumine are, in the end, bets on capital allocators. The assets throw off cash; what determines whether shareholders prosper is the judgment and discipline of the people deciding where that cash goes. So the people, and more importantly their incentives, deserve scrutiny.

At the top sits David Nyland, the CEO, who has been on this journey since the 2014 hire that started it all. He is not a financier who parachuted in; he is an operator with deep telecom-technology domain knowledge, which matters enormously in a business where the difference between a good carve-out and a disaster comes down to understanding the guts of a carrier's network. The CFO, Mary Anne Lavallee, brings the corporate-finance and integration expertise that a serial acquirer lives on. And the chairman is Mark Miller, the Volaris and Constellation veteran whose presence keeps Lumine tethered, culturally and operationally, to the parent that spawned it.10

But the org chart is the least interesting thing about Lumine's management. The incentive structure is the interesting thing, because it is engineered — quite deliberately, in the Constellation tradition — to make it painful for executives to be undisciplined.

Consider Nyland's compensation. His total pay has been reported in the neighborhood of US$3.8 million, but his base salary is a relatively modest ~US$457,000.10 The overwhelming majority of his compensation is an annual incentive bonus — and here is where the Constellation machinery engages. Under the group's long-standing executive policy, key managers are required to take a significant portion of their after-tax bonus and use it to buy shares of the company in the open market. Not options granted for free. Not restricted stock that vests regardless. Actual shares, bought with their own after-tax money, at market prices.10 And those shares are then locked in escrow for a multi-year period, on the order of three to five years, during which the executive cannot sell.10 The effect is to convert managers into shareholders whose personal net worth rises and falls with the stock they are responsible for. If they destroy value, they feel it directly, in their own bank accounts, and they cannot escape it for years.

Why go to such lengths? Because the failure mode of serial acquirers is depressingly consistent across corporate history, and it almost always traces back to incentives. An executive paid to grow the enterprise — measured in revenue, or headcount, or deal count — will keep doing deals long after the good ones run out, because the compensation rewards size rather than return. The graveyard of conglomerates is full of empires built this way, bloated by acquisitions that made the boss more important and the shareholders poorer. Constellation's founder wrote about this danger explicitly and repeatedly, and the compensation architecture is his answer to it: make the people deploying capital feel the outcome in their own net worth, lock them in long enough that they cannot game a single good year, and refuse to pay them at all unless the capital actually earns its keep.

The bonus itself is gated by a return-on-invested-capital hurdle. In the Constellation model that Lumine inherited, if the business fails to generate a return above a defined hurdle rate — historically anchored to a risk-free benchmark in the range of a few percent — the incentive bonus can fall to zero.10 This is the mechanism that is supposed to prevent the single greatest danger facing any serial acquirer: growth for its own sake. A management team paid to grow revenue will happily overpay for deals, because a bad acquisition still makes the company bigger. A management team paid only when capital clears a return hurdle has to care about price. In principle, this is the discipline that stops the treadmill from becoming a trap.

The independent investor should note two things about this elegant system. First, it is genuinely rare and genuinely powerful — very few public companies force their executives to buy and hold stock with their own money, and it aligns interests far better than the usual option grants. Second, and less comfortably, ROIC is a metric management itself calculates and defines, and hurdle-based incentives create their own subtle pressures — for instance, toward using leverage or structuring deals in ways that flatter the return calculation. The alignment is real. It is not a substitute for watching what the company actually buys and what it actually earns on that capital. And whether the discipline holds under the strain of ever-larger deals is precisely what the bear case interrogates.

XII. Skeptic's Stress Test & Risk Radar (Bear vs. Bull Cases)

Now we turn the argument inside out, because a story this polished demands an adversary. What would a skeptical short-seller, or an activist with a bone to pick, actually attack? There is more here than the bulls like to admit.

The melting ice cube. Start with the single most important number in this entire company, the one that top-line growth conveniently obscures: organic revenue growth. Strip out acquisitions and currency effects, and ask whether the businesses Lumine already owns are growing on their own. The answer has mostly been no. Organic growth, adjusted for foreign exchange, was roughly -9% in fiscal 2024, recovered to a slim +1% in fiscal 2025, and slipped back to -2% in the first quarter of 2026.723 Read that sequence carefully. In two of the last three reporting periods, Lumine's existing businesses shrank in real terms. This is the empirical heart of the bear case: the legacy telecom and broadcast systems are, in aggregate, slowly dying, as customers migrate to cloud-native platforms over a period of years. The skeptic's charge is blunt — Lumine is buying melting ice cubes, and the acquisitions are not a growth strategy so much as a way of continually replacing the water that drips away. Every deal masks the underlying erosion for another quarter. On this reading, the compounding is real but precarious: it works only so long as Lumine can keep buying faster than its portfolio melts.

The capital-allocation treadmill. This connects to a structural problem of success. When Lumine was a small collection of assets, it could compound rapidly by buying tiny companies for a few million dollars at attractive prices. But at roughly $800 million of revenue and growing, small deals no longer move the needle. To keep compounding, Lumine must do bigger deals — WideOrbit at $490 million, Synchronoss at a $258 million enterprise value, Imagine at an undisclosed but presumably substantial price.145 And bigger deals are more competitive deals. At the $300-million-plus level, Lumine is no longer alone in an obscure niche; it is bidding against the aggressive private-equity giants — the Thoma Bravos and Vista Equity Partners of the world — who have raised enormous software-buyout funds and are hunting the same assets. Competition drives up prices. WideOrbit was reportedly acquired at around 13 times EBITDA — a multiple far above the mid-single-digit prices on which Constellation historically built its returns.11 Pay more for each dollar of earnings, and by definition you earn a lower return on the capital you deploy. The treadmill demands ever-larger deals, and ever-larger deals structurally erode the very ROIC the whole model is built to protect. That is the bear case's most dangerous thread, because it attacks not the assets but the math.

The cash-flow squeeze. Then there is the first quarter of 2026, which handed skeptics a vivid data point. After a 2025 in which cash generation looked unstoppable, cash flow from operations in Q1 2026 fell 51%, to $19.8 million from $40.1 million a year earlier, and free cash flow available to shareholders dropped 56%, to $15.3 million.3 The proximate cause was the Synchronoss integration: absorbing a distressed company with $309.3 million of cash consideration meant soaking up working capital, paying heavy advisory and transaction fees, and funding restructuring outflows.3 The bullish interpretation is that these are one-time costs of a value-creating deal, and that normalized cash flow will reassert itself. The bearish interpretation is that this is what integration risk looks like when it shows up in the numbers, and that a company doing multiple complex carve-outs simultaneously is one or two botched integrations away from real balance-sheet strain. Both readings are legitimate. What is not legitimate is ignoring the quarter, and the next several quarters of cash conversion will tell investors a great deal about which story is true.

The governance trap. Finally, the structural issue an activist would seize on immediately. Constellation retains control of Lumine through that single Super Voting Share, holding roughly 50.1% of the vote regardless of how much economic ownership the public holds. Public subordinate-voting shareholders are, in any meaningful sense, along for the ride. They cannot block a capital reorganization, an asset transfer to or from the Constellation family, or a related-party transaction if the controller wants it done. In practice, Constellation's stewardship has been a powerful asset — the parent's discipline and expertise are much of why anyone wants to own Lumine at all. But investors should be clear-eyed that they are trusting a controller, not governing alongside one. The dual-class structure that concentrates that trust is a genuine risk, dormant right up until the moment interests diverge.

Why win, why not. Put it together and the spine of the debate is clean. Lumine wins from here if — and only if — its switching-cost moats hold long enough for its capital allocators to keep buying sticky cash flows at prices that clear a real return hurdle, converting an ever-larger portfolio into ever-larger free cash flow faster than the legacy assets melt. It breaks if organic decline accelerates, if competition for large deals compresses returns below the hurdle, if an integration goes badly wrong, or if the controller's interests ever stop aligning with the minority's. The bull and bear cases are not really in conflict about the facts. They disagree about a rate — the pace of the melt versus the pace and quality of the buying. That is the whole game.

XIII. Epilogue & Key KPIs to Watch

Lumine Group is a fascinating experiment: an attempt to take the most admired capital-allocation model in modern software and apply it, at accelerating scale, to a vertical that is simultaneously one of the stickiest and one of the most quietly disrupted in technology. In three and a half years as a public company, its management has proven it can source, structure, and close deals that most acquirers would never attempt — a half-billion-dollar platform on day one, carve-outs from a global equipment giant, a bankruptcy estate, a distressed public company taken private, and a summer media land-grab. The revenue has compounded, the reported cash flow of 2025 was genuinely impressive, and the incentive structure is among the most shareholder-aligned in the public markets.

A word on management credibility, judged the only way it can honestly be judged — by behavior over time rather than by rhetoric. Lumine's leadership has, to date, done roughly what it said it would do: it promised to hunt larger and more complex deals than Constellation traditionally pursued, and it has demonstrably done exactly that, from WideOrbit through Synchronoss to the summer 2026 media acquisitions. Its disclosure follows the Constellation house style — spare, focused on cash and capital deployment rather than adjusted-EBITDA theater, and notably unpromotional. That restraint cuts both ways for investors: it signals a team more interested in compounding than in managing the share price, but it also means shareholders get relatively little forward guidance and must trust a controller they cannot outvote. The one live test of narrative consistency is organic growth, which management has never oversold — it reports the negative FX-adjusted figures plainly rather than burying them — but which it also has not yet proven it can arrest. Credibility here is provisional: earned on execution and honesty, still unproven on the hardest operating question the business faces.

None of that resolves the core question, and this piece has tried hard not to pretend otherwise. Lumine is a bet that disciplined, permanent-capital ownership can extract more value from slowly melting software assets than the market expects — and that the buying can outrun the melt indefinitely. The evidence so far is genuinely mixed: fortress-like retention and cash conversion on one side, persistently negative organic growth and a jarring Q1 2026 cash-flow drop on the other. A sophisticated long-term investor does not need a verdict handed to them. They need to know which few numbers actually separate the bull case from the bear case, so they can watch the story falsify or confirm itself in real time.

There are three, and only three, that matter most.

The first is organic revenue growth, adjusted for foreign exchange. This is the melting-ice-cube thesis reduced to a single figure. If Lumine can stabilize organic growth around zero to slightly positive, the bear case weakens dramatically — it would mean the portfolio is holding its own and every acquisition is pure addition. If organic growth deteriorates back toward the -9% of fiscal 2024, the skeptics are right, and the whole enterprise is running up a down escalator.7

The second is free cash flow available to shareholders. This is the ultimate output of the machine — the cash that is actually left for owners after everything needed to run the business. A consolidator can report growing revenue and growing accounting profit and still be a mirage if the deals do not convert to real, spendable cash. The 153% surge in 2025 was the bull case incarnate; the 56% Q1 2026 drop was the warning shot.23 Watching this line normalize — or fail to — over the coming quarters is how investors will learn whether the Synchronoss squeeze was a one-time integration cost or the first visible crack.

The third is the pairing of capital deployed and the return earned on it — ROIC. The entire thesis rests on management's ability to keep pushing growing cash flows into new acquisitions while still earning a high return on that capital. If Lumine can deploy hundreds of millions a year and hold its returns above the hurdle, it is the compounding machine the bulls describe. If the treadmill forces it to pay private-equity prices and returns quietly erode, it is something far more ordinary. That tension — deploy more, or earn more per dollar deployed — is the question the next decade of this company will answer, one deal at a time.

Watch those three numbers. Everything else is narrative.

References

-

Constellation Software Inc. and Lumine Group Announce the Completion of the Purchase of WideOrbit Inc. — GlobeNewswire, 2023-02-22 ↩↩↩↩↩

-

Lumine Group Inc. Announces Results for the Three Months and Year Ended December 31, 2025 — Lumine Group, 2026-03-04 ↩↩↩↩↩↩↩

-

Lumine Group Inc. Announces Results for the Three Months Ended March 31, 2026 — GlobeNewswire, 2026-05-05 ↩↩↩↩↩↩

-

Lumine Group Completes Acquisition of Synchronoss Technologies — Lumine Group, 2026-02-13 ↩↩↩↩

-

Lumine Group Acquires Imagine Communications — GlobeNewswire, 2026-07-01 ↩↩↩↩

-

Lumine Group Announces Completion of US$185M Debt Facility in Connection with Previously Announced WideOrbit Acquisition — GlobeNewswire, 2023-03-03 ↩↩

-

Lumine Group Inc. Announces Results for the Three and Twelve Months Ended December 31, 2024 — Lumine Group, 2025-03-05 ↩↩↩↩↩↩

-

Casa Systems Initiatives Financial Restructuring to Maximize Value and Preserve Jobs — GlobeNewswire, 2024-04-03 ↩

-

Lumine Group to Acquire Synchronoss Technologies — Lumine Group, 2025 ↩

-

Lumine Group Inc. (LMN.V) Regulatory Filings and Management Information Circular — SEDAR+ ↩↩↩↩↩↩↩

-

Constellation's Spin-Out of the Lumine Group — Best Anchor Stocks ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube