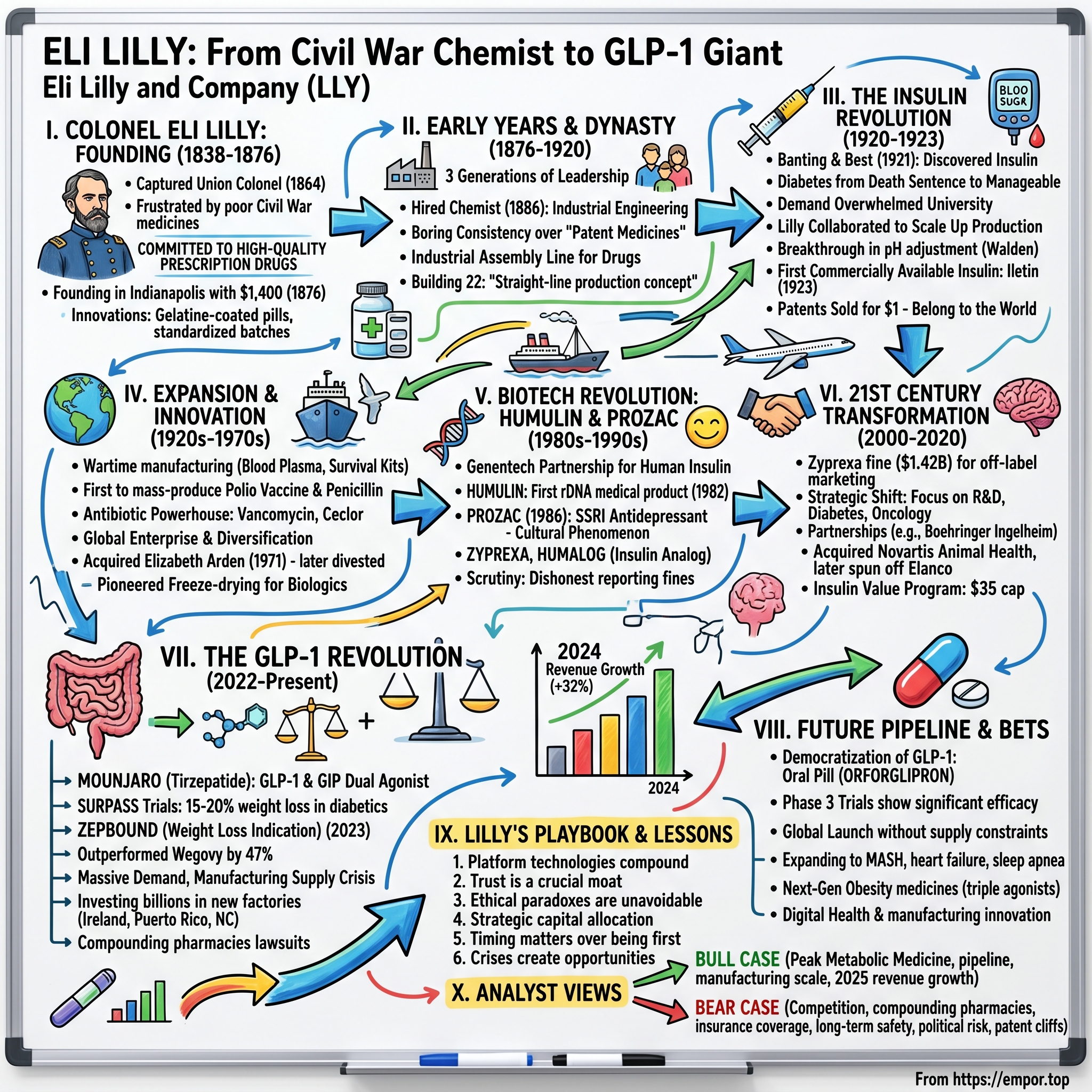

Eli Lilly: From Civil War Chemist to GLP-1 Giant

I. Introduction & Episode Roadmap

Picture this moment: It's early 2025, and Eli Lilly has a market cap of $628.62 Billion USD, making it one of the world's most valuable pharmaceutical companies. The company expects 2024 full-year worldwide revenue to be approximately $45.0 billion, which represents growth of 32% compared to the previous year. How did a Civil War veteran's two-story Indianapolis pharmacy, opened with just $1,400 in working capital, transform into the titan that today produces the world's hottest obesity drugs?

This is a story that spans nearly 150 years—from a Union Army colonel frustrated by poorly prepared battlefield medicines to a company racing to produce enough GLP-1 drugs to meet unprecedented global demand. It's a tale of scientific breakthroughs that turned death sentences into manageable conditions, of family dynasties that built empires, and of calculated risks that reshaped entire industries.

We'll journey from that original Pearl Street laboratory in 1876, through the insulin revolution that saved millions of lives, to today's GLP-1 gold rush where sales of Mounjaro and Zepbound posted robust sales growth in Q4 2024. Along the way, we'll uncover the strategic decisions, scientific innovations, and sometimes controversial choices that built one of pharma's most enduring franchises.

Three themes will guide our exploration: the power of long-term thinking across generations, the delicate balance between scientific innovation and commercial imperatives, and the eternal tension in pharmaceutical development—how do you create life-saving medicines while navigating the ethical complexities of drug pricing and access?

II. Colonel Eli Lilly: War, Loss, and Founding (1838–1876)

The rain was falling on Enterprise, Mississippi, in January 1865 when Confederate guards finally released their Union prisoners. Among them walked a gaunt figure who'd spent the last four months in captivity—Colonel Eli Lilly, captured at the Battle of Sulphur Creek Trestle while commanding cavalry under the infamous Nathan Bedford Forrest's pursuit. Lilly was captured in September 1864 and held as a prisoner of war until January 1865.

But let's rewind. Before he was Colonel Lilly, before the war that would define his generation, young Eli was just a teenager visiting Henry Lawrence's Good Samaritan Drug Store in 1854. He completed a four-year apprenticeship to become a chemist and pharmacist, with Lawrence teaching him to mix chemicals, manage funds, and operate a business. This wasn't just vocational training—it was the foundation of a philosophy that would later revolutionize American pharmaceuticals.

When Fort Sumter fell in April 1861, Lilly had just opened his own drugstore in Greencastle, Indiana, and married his childhood sweetheart, Emily Lemon. In the spring of the same year, April 1861, President Lincoln issued a call to arms in the Civil War. This would influence Lilly to lock the doors of his new drugstore, say goodbye to his new wife, and join the infantry of the Union Army.

What followed was a Civil War career that reads like a military thriller. Lilly enlisted in the Union Army during the American Civil War and recruited a company of men to serve with him in the 18th Independent Battery Indiana Light Artillery. His recruitment poster promised to form "the crack battery of Indiana," and he delivered—his unit's six ten-pound Parrott guns would see action at Hoover's Gap and Chickamauga as part of Colonel John T. Wilder's legendary Lightning Brigade.

He was later promoted to major and then colonel, and was given command of the 9th Indiana Infantry Regiment. The title "Colonel" would stick with him for life, becoming so integral to his identity that even corporate documents referred to him this way decades later.

But here's what makes Lilly's story different from countless other war veterans who returned to civilian life: Following his experience with low-quality medicines used in the Civil War, Lilly committed himself to producing only high-quality prescription drugs, in contrast to the common and often ineffective patent medicines of the day. Those months watching soldiers suffer from inconsistent, adulterated, or simply fake medicines had planted a seed.

The post-war years brought personal tragedy. After the war, he attempted to run a plantation in Mississippi, but it failed and he returned to his pharmacy profession after the death of his first wife, Emily, in 1866. He remarried Maria Cynthia Sloan and tried various pharmaceutical partnerships in Illinois and Indiana, but none satisfied his vision.

By 1876, at age 38, Lilly was ready for his defining move. He approached Augustus Keifer, a family friend and Indianapolis drug wholesaler, with a proposition: Keifer and two associated drugstores would purchase all their drugs from Lilly at lower costs than they were currently paying. With this guaranteed customer base, on May 10, 1876, Lilly opened his own laboratory in a rented two-story building at 15 West Pearl Street in Indianapolis.

The sign for the business said "Eli Lilly, Chemist". Lilly's manufacturing venture began with $1,400 ($34,024 in 2020 chained dollars) in working capital and three employees: Albert Hall (chief compounder), Caroline Kruger (bottler and product finisher), and Lilly's fourteen-year-old son, Josiah, who had quit school to work as his father's apprentice.

The innovations started immediately. Lilly's first innovation was gelatine-coated pills and capsules. Other early innovations included fruit flavorings and sugarcoated pills, which made medicines easier to swallow. These might seem trivial today, but in an era when medicines were often bitter concoctions that patients struggled to keep down, Lilly's improvements directly impacted treatment compliance.

More fundamentally, Lilly brought a chemist's precision to an industry dominated by hucksters and patent medicine salesmen. Every batch was standardized. Every ingredient was tested. Every claim was backed by evidence. In the Wild West of 1870s American pharmaceuticals, this was revolutionary.

By the end of 1876, sales had reached $4,470. Within three years, they'd grown to $48,000. At the time of Lilly's death in 1898, Eli Lilly and Company had a product line of 2,005 items and annual sales of more than $300,000—roughly $9.3 million in today's dollars.

The frustrated Civil War colonel who'd seen too many soldiers die from bad medicine had built something extraordinary: not just a company, but a new standard for pharmaceutical manufacturing. His greatest contribution wasn't any single drug—it was the idea that medicines should be pure, consistent, and effective every single time.

III. Building the Foundation: Early Years & Family Dynasty (1876–1920)

The late 19th century pharmaceutical industry was a curious beast—part chemistry lab, part botanical garden, part traveling medicine show. Into this chaos, the Lilly company brought something radical: boring consistency. While competitors hawked miracle elixirs with outlandish claims, by the company's 50th anniversary in 1926, its sales had reached $9 million and it was producing over 2,800 products.

But the real story here isn't the products—it's the systematic transformation of a craft business into an industrial enterprise. In 1878, Lilly hired his brother, James, as his first full-time salesman, and the subsequent sales team marketed the company's drugs nationally. By 1879, the company had grown to $48,000 in sales. The company moved its Indianapolis headquarters from Pearl Street to larger quarters at 36 South Meridian Street.

The pivotal moment came in 1881. In 1881, the company moved to its current headquarters in Indianapolis's south-side industrial area, and the company later purchased additional facilities for research and production. The same year, Lilly incorporated the business as Eli Lilly and Company, elected a board of directors, and issued stock to family members and close associates. This wasn't just a legal formality—it was Colonel Lilly preparing for succession.

And what a succession it would be. By 1890, Col. Lilly was a wealthy man. Less interested in the pharmaceutical business than civic affairs, he turned over much of the running of the company to his son, Josiah. Josiah K. Lilly Sr.—J.K. to everyone—represented a new generation of pharmaceutical leadership. Where his father was a craftsman-soldier, J.K. was a businessman-scientist.

J.K.'s masterstroke came in 1886 with a decision that would define Lilly's next century: establishing one of the industry's first dedicated research programs. The company hired Ernest Eberhardt as its first pharmaceutical chemist—not to make existing products better, but to discover entirely new ones. This was heretical thinking in an industry that mostly reformulated traditional remedies.

After Colonel Lilly's death from cancer in 1898, J.K. took full control and accelerated the transformation. By 1905, under his leadership, annual sales crossed $1 million for the first time. But J.K. wasn't just scaling up—he was reimagining what a pharmaceutical company could be.

Enter the third generation: Eli Lilly, the Colonel's grandson and J.K.'s son. If the Colonel brought military discipline and J.K. brought business acumen, young Eli brought something else entirely: industrial engineering. He also introduced scientific management principles, implemented cost-savings measures that modernized the company, and expanded the company's research efforts and collaborations with university researchers.

Around 1909, young Eli introduced a concept that seems obvious now but was revolutionary then: the pharmaceutical assembly line. He developed a "blueprinting" method for drug formulas—detailed, step-by-step instructions that any trained technician could follow to produce identical results. Think Henry Ford, but for pills instead of Model Ts.

The crown jewel of this industrial philosophy was Building 22, completed in 1926. This five-floor plant implemented what Lilly called the "straight-line production concept"—raw materials entered on one floor and moved systematically through processing, with finished products emerging at the other end. Gravity did much of the work, with materials flowing downward through the building. It was elegant, efficient, and unlike anything the pharmaceutical industry had seen.

But the most important hire of this era wasn't an engineer or a chemist—it was George Henry Alexander Clowes, a biochemist hired in 1919 as director of biochemical research. Clowes came from the cutting edge of cancer research at Buffalo's Gratwick Laboratory. His arrival signaled Lilly's ambition to move beyond manufacturing into genuine pharmaceutical discovery.

Clowes would prove instrumental in what came next, but his immediate contribution was cultural. He brought academic rigor to industrial research, establishing collaborations with universities and insisting on publishing results in peer-reviewed journals. This transparency was unusual for a commercial enterprise, but it built credibility with the medical establishment—credibility that would prove invaluable when Lilly needed physicians to trust a revolutionary new treatment.

The company culture that emerged during these years was distinctive: methodical but innovative, profitable but principled. Employees called it the "Lilly way"—a commitment to quality that bordered on obsession. Products were tested and retested. Manufacturing processes were documented in exhaustive detail. Sales representatives were trained as educators, not mere order-takers.

This foundation—three generations of leadership, industrial-scale manufacturing, serious research capabilities, and unimpeachable credibility—positioned Lilly perfectly for what was about to unfold in Toronto. The company had spent 45 years preparing for a moment it couldn't have predicted: the discovery that would transform diabetes from a death sentence into a manageable disease.

IV. The Insulin Revolution: Changing Diabetes Forever (1920–1923)

The bedroom reeked of acetone—the sickly sweet smell of a body eating itself to survive. Fourteen-year-old Leonard Thompson lay dying in Toronto General Hospital on January 11, 1922, weighing just 65 pounds. Type 1 diabetes in 1922 meant one thing: a slow, inevitable death, typically within months of diagnosis. The only treatment was a starvation diet that might buy a few extra weeks of agony.

But on this January day, something unprecedented was about to happen.

Let's rewind to October 1920, when Frederick Banting, after reading a paper on the relationship of the islets of Langerhans to diabetes, realized that the key to treating diabetes may be to extract insulin from pancreatic islet cells. Banting, a struggling surgeon with a failing practice in London, Ontario, had no research experience. But he had an idea that wouldn't let go.

On 7 November 1920 he paid a visit to a top professor at the University of Toronto, John Macleod. They put their minds together and began to work on a plan. Macleod was skeptical—dozens of researchers had tried to extract insulin from the pancreas, all failing because digestive enzymes destroyed the insulin during extraction. But Banting proposed something different: tie off the pancreatic duct, let the enzyme-producing cells die, then extract insulin from the remaining islet cells.

Macleod provided Banting with the labs needed to conduct their experiments and brought in a research student, called Charles Best, to help out. Best specialised in testing blood to check glucose levels. On May 17, 1921, they began their experiments on dogs. The work was grueling, often grotesque—removing pancreases from dogs to induce diabetes, then trying to keep them alive with extracts from other dogs' pancreases.

Progress came in fits and starts. Many dogs died. Extracts failed. But by July, they achieved something remarkable: With this murky concoction, Banting and Best kept another dog with severe diabetes alive for 70 days—the dog died only when there was no more extract.

By December 1921, biochemist James Collip joined the team, bringing expertise in purification that would prove crucial. On January 11, 14-year-old Leonard Thompson became the first patient to receive Banting and Best's pancreatic extract — which lowered his blood glucose and urine glucose, but not ketones. Though Thompson's condition was much improved, he had an allergic reaction to impurities in the extract. In the following weeks, James Bertram Collip developed an improved process that removed contaminants.

Twelve days later, Thompson received Collip's purified extract. This time, the results were spectacular—blood sugar normalized, ketones disappeared, and the boy who'd been days from death began to recover.

Word spread through Toronto General like wildfire. Parents of dying children began arriving at the hospital, desperate for the miracle extract. The Toronto team had proven insulin could save lives, but they faced a crushing problem: Physicians who heard about the new wonder drug were clamoring for insulin to save their dying patients, but the university was unable to produce significant quantities.

Enter George Clowes of Eli Lilly. In attendance was George Clowes of Eli Lilly and Company, who proposed a collaboration to produce insulin for the commercial market for the first time. His offer was declined, as the treatment was not yet ready when Banting first presented at the American Physiology Society in December 1921.

But by May 1922, with demand overwhelming and children dying while waiting for insulin, pragmatism won. In late May, the University of Toronto and Lilly signed a licensing agreement for the production of insulin in the U.S., Mexico, Cuba, and Central and South America.

What happened next was a masterclass in industrial pharmaceutical development. In May 1922, pharmaceutical company Eli Lilly & Company began collaborating with the university to scale up and commercialize production of insulin in the Americas. The effort was led by Lilly chemist George Walden. By July, the firm shipped its first batches of Iletin® insulin for clinical testing.

The engineering challenges were staggering. Insulin production required processing thousands of pounds of animal pancreases—initially from cattle at local slaughterhouses. The pancreases had to be frozen immediately after slaughter, ground up, extracted with alcohol, then purified through multiple steps. One batch might require 7,000 pounds of pancreas to produce just one pound of insulin.

George Walden, Lilly's lead chemist on the project, made a crucial breakthrough. He discovered that by adjusting the pH during extraction, he could dramatically improve yields and purity. This "isoelectric precipitation" method became the standard for insulin production for decades.

But the real drama was the race against time. Children were dying daily. Parents camped outside Lilly's Indianapolis facility, begging for any available insulin. The company ran production lines 24 hours a day. Scientists slept in the labs. In 1923, the company began selling Iletin, the company's tradename for the first commercially available insulin product in the U.S for the treatment of diabetes.

In 1923, Banting and Macleod received the Nobel Prize in Medicine, which they shared with Best and Collip. But here's the remarkable part: On 23 January 1923, Banting, Collip and Best were awarded U.S. patents on insulin and the method used to make it. They all sold these patents to the University of Toronto for $1 each. Banting famously said, "Insulin does not belong to me, it belongs to the world".

This decision—to essentially give away one of the most valuable medical discoveries in history—set a precedent that reverberates today. It also created an interesting dynamic: Lilly had exclusive commercial rights in much of the Americas but couldn't price insulin as a monopoly product because the inventors had explicitly wanted it accessible to all.

The impact was immediate and profound. Elizabeth Hughes, daughter of U.S. Secretary of State Charles Evans Hughes, arrived in Toronto weighing 45 pounds and near death. After insulin treatment, she lived to age 73. Elizabeth Hughes, one of the first people Banting treated with insulin, died at the age of 73, having received approximately 42,000 insulin injections over 58 years.

Insulin, "the most important drug" in the company's history, did "more than any other" to make Lilly "one of the major pharmaceutical manufacturers in the world". By 1923, Lilly was producing enough insulin to supply all of North America. The company that Colonel Eli Lilly founded to make pure, reliable medicines had delivered on that promise in the most spectacular way possible: turning a death sentence into a life sentence.

V. Expansion & Innovation: Building a Pharmaceutical Empire (1920s–1970s)

The Great Depression should have destroyed Eli Lilly. Banks failed. Competitors collapsed. Unemployment hit 25%. Yet somehow, in 1932, sales rose to $13 million, and Eli Lilly (grandson) was named president to succeed his father Josiah K. Lilly Sr. How does a luxury goods company—and make no mistake, pharmaceuticals were luxuries when people couldn't afford food—thrive during economic catastrophe?

The answer lay in insulin's halo effect. Lilly wasn't just another drug company anymore; it was the company that had helped save diabetic children. That reputation, combined with relentless innovation, created a flywheel that would spin for decades.

World War II transformed Lilly from a successful pharmaceutical company into an industrial powerhouse. Throughout World War II, Lilly manufactured more than two hundred products for military use, including aviator survival kits and seasickness medications for the D-Day invasion. In addition Lilly dried more than two million pints of blood plasma by the war's end.

But the real wartime story was penicillin. When the U.S. government launched a crash program to mass-produce this new wonder drug, they turned to companies with proven fermentation expertise. Lilly's insulin experience made them an obvious choice. By 1943, the company was one of the first to mass-produce penicillin, ramping up from laboratory curiosity to industrial-scale production in months.

The post-war era brought a parade of innovations that reads like a greatest hits of 20th-century medicine. In the 1950s, Lilly introduced vancomycin, still used today as an antibiotic of last resort. They developed erythromycin, which became a mainstay for patients allergic to penicillin. In the 1960s came the cephalosporin antibiotics, and by the 1970s, Ceclor had become the world's top-selling oral antibiotic.

Lilly was the first company to mass-produce both the polio vaccine, developed in 1955 by Jonas Salk, and insulin. This wasn't their vaccine—Jonas Salk developed it at the University of Pittsburgh—but when it came time to scale production to vaccinate millions of children, the National Foundation for Infantile Paralysis turned to Lilly. Why? Because of that Toronto insulin experience. Lilly had proven they could take a university laboratory discovery and manufacture it at previously unimaginable scales while maintaining quality.

By 1955, Lilly was manufacturing 60% of all Salk polio vaccine in the United States. The logistics were mind-boggling: growing poliovirus in monkey kidney cells, inactivating it with formaldehyde, testing every batch for safety. One contaminated batch could paralyze children instead of protecting them. The pressure was immense, the margins were thin, but Lilly delivered.

The 1950s also saw Lilly's transformation into a truly global enterprise. In 1954, the company formed Elanco Products Company for veterinary pharmaceuticals—a seemingly odd diversification that made perfect sense. Who better to make animal medicines than a company already processing thousands of animal pancreases for insulin?

International expansion accelerated through the 1960s. The company operated 13 affiliate companies outside the U.S. In 1962, they acquired the pharmaceutical division of Distillers Company and established a major factory in Liverpool, England. This wasn't just about sales—it was about establishing local manufacturing to navigate trade barriers and currency restrictions.

Then came 1971 and one of the most bizarre acquisitions in pharmaceutical history: In 1971, Lilly bought Elizabeth Arden cosmetics for $38 million. On paper, it made no sense. What did a pharmaceutical company know about makeup? But dig deeper and the logic emerges: both businesses sold through similar channels, both relied on quality and brand reputation, and both targeted affluent consumers. The acquisition would prove remarkably profitable, though Lilly would eventually divest it to refocus on pharmaceuticals.

The 1970s brought a different kind of innovation—process innovation. Lilly pioneered new manufacturing techniques like lyophilization (freeze-drying) for biologics, automated quality control systems, and some of the industry's first computer-controlled production lines. Boring? Perhaps. But these innovations dramatically reduced costs and improved consistency.

Throughout this expansion, Lilly maintained its peculiar corporate culture. In 1937, Josiah K. Lilly Sr. and his two sons, Eli and Joe, founded the Lilly Endowment, a private charitable foundation, with gifts of Lilly stock. The endowment still owns 11.3% of the company. This created an unusual ownership structure—a major pharmaceutical company partially owned by a charitable foundation focused primarily on education and community development in Indiana.

By 1980, Lilly had grown from that two-story Pearl Street laboratory into a global enterprise with over $2 billion in annual sales. They'd built or acquired facilities on every inhabited continent. They'd created entire new categories of medicines. They'd survived wars, depressions, and countless competitive threats.

But the company stood at an inflection point. The age of discovering drugs by grinding up plants or extracting hormones from animal organs was ending. The age of biotechnology was beginning. And once again, Lilly's insulin experience would prove invaluable—though in ways no one could have predicted.

VI. The Biotech Revolution: Humulin & Prozac (1980s–1990s)

The petri dish in Genentech's South San Francisco lab contained something that shouldn't exist: bacteria making human insulin. It was 1978, and scientists had just accomplished what seemed like science fiction—they'd inserted human genes into E. coli bacteria and convinced these microscopic factories to produce a human protein.

In 1978 scientists at City of Hope and Genentech developed a method for producing biosynthetic human insulin (BHI) using recombinant DNA technology in a unique multi-step process. After extracting and manipulating the two polypeptide chains, A and B, that make up the human insulin gene, they inserted these into a common bacteria, which they programmed genetically to produce large amounts of insulin.

For Eli Lilly, this breakthrough represented both enormous opportunity and existential threat. Animal insulin had made the company, but it had limitations—some patients developed allergic reactions, and there were growing concerns about long-term supply as diabetes rates soared globally. Whoever controlled human insulin would own the future of diabetes treatment.

Eli Lilly & Co. signed an agreement with Genentech to use the rDNA method to make human insulin commercially available. This partnership married Genentech's cutting-edge science with Lilly's decades of insulin manufacturing expertise. It was like combining Tesla's innovation with Ford's production capabilities.

The development timeline was breathtaking. On October 28, 1982, after only 5 months of review, the FDA approved Humulin, the first biosynthetic human insulin product and the first approved medical product of any kind that derived from this technology. Five months! Today, drug approvals typically take years. But the FDA recognized they were looking at something revolutionary—not just a new drug, but an entirely new way of making drugs.

It was one of the first pharmaceutical companies to produce human insulin using recombinant DNA, including Humulin (insulin medication), Humalog (insulin lispro), and the first approved biosimilar insulin product in the U.S., Basaglar (insulin glargine). Humulin wasn't just a product; it was proof that the future of medicine lay in biotechnology.

But the 1980s brought another kind of revolution, this one targeting the human mind rather than the pancreas.

By the mid-1980s, depression treatment hadn't fundamentally changed since the 1950s. The existing drugs—tricyclics and MAO inhibitors—worked but came with brutal side effects. Patients often chose to live with depression rather than endure the treatment. Enter Prozac.

Lilly is known for its clinical depression drugs Prozac (fluoxetine) (1986), Cymbalta (duloxetine) (2004), and its antipsychotic medication Zyprexa (olanzapine) (1996). Prozac, launched in 1986, was different. It was a selective serotonin reuptake inhibitor (SSRI)—a precise molecular key designed to fit one specific lock in the brain's chemistry.

The drug's development actually began in the early 1970s when Lilly scientist Ray Fuller was investigating compounds that might affect neurotransmitter levels. The compound that would become fluoxetine was initially shelved as uninteresting. It took years of additional research to recognize its potential for treating depression with fewer side effects than existing drugs.

Prozac's cultural impact exceeded its clinical significance. Peter Kramer's 1993 book "Listening to Prozac" sparked debates about cosmetic psychopharmacology—were we treating disease or engineering personality? The drug appeared on magazine covers, in pop songs, in everyday conversation. "Prozac Nation" became shorthand for a generation's relationship with mental health.

By 1999, Prozac had been prescribed to more than 40 million people worldwide, generating over $2.8 billion in annual sales at its peak. It wasn't just a blockbuster drug; it was a cultural phenomenon that destigmatized antidepressant use and opened conversations about mental health that continue today.

The 1990s brought more innovations leveraging Lilly's biotech capabilities. Humalog, approved in 1996, was the first insulin analog—a modified version of human insulin engineered to act faster after injection. This was intelligent design at the molecular level, tweaking insulin's structure to improve its pharmacological properties.

Then came Zyprexa for schizophrenia in 1996, Evista for osteoporosis in 1997, and Gemzar for cancer in 1998. Each represented not just a new drug but a new approach to drug development—using genomics, proteomics, and high-throughput screening to identify and optimize compounds.

But success bred scrutiny. The same Oraflex arthritis medication that showed promise in clinical trials was linked to deaths in Europe. In 1982, courts found Lilly not guilty of willfully withholding information but fined them $25,000. The late 1980s brought FDA charges of dishonest reporting and manufacturing irregularities—Lilly was found innocent but still fined $75,000.

These controversies foreshadowed bigger challenges ahead. As drugs became more powerful and profitable, questions about marketing practices, pricing, and corporate responsibility would intensify. The company that had given insulin to the world for $1 now faced accusations of putting profits before patients.

Yet the innovation continued. By 2000, Lilly had established itself as a leader in both traditional pharmaceuticals and biotechnology. The company that started by coating pills in gelatin was now engineering proteins, designing molecules, and manipulating genes. The transformation from 19th-century pharmacy to 21st-century biotech was complete.

VII. The 21st Century Transformation (2000–2020)

The year 2009 should have been a disaster for Eli Lilly. The company paid the largest criminal fine in pharmaceutical history - $1.42 billion for unlawfully marketing Zyprexa for off-label uses, including dementia in elderly patients. The headlines were brutal. Trust was shattered. Yet somehow, this crisis catalyzed one of the most successful transformations in pharmaceutical history.

The Zyprexa debacle forced a reckoning. The blockbuster model—betting everything on a few billion-dollar drugs and marketing them aggressively—was broken. Patents were expiring. Pipelines were drying up. The company needed a new playbook.

Enter John Lechleiter, who became CEO in 2008 amid the crisis. A Lilly lifer with a PhD in organic chemistry, Lechleiter understood both the science and the business. His strategy was counterintuitive: while competitors were merging to achieve scale, Lilly would stay independent and double down on R&D, particularly in diabetes.

The diabetes focus wasn't random. Lilly had watched the global obesity epidemic unfold and recognized that Type 2 diabetes would follow like a shadow. By 2010, 285 million people worldwide had diabetes. By 2030, that number was projected to reach 438 million. This wasn't just a medical crisis—it was a massive market opportunity.

The first piece of the puzzle came in 2002 with Cialis for erectile dysfunction approved in EU, US launch 2004. While not a diabetes drug, Cialis proved Lilly could still develop blockbusters. More importantly, its success in a crowded market (competing against Viagra) showed the company could win through superior execution and patient focus.

But the real transformation came through strategic partnerships. In January 2011, Boehringer Ingelheim and Lilly announced a global agreement to jointly develop and market new APIs for diabetes therapy. Lilly could receive more than $1 billion for their work on the project, while Boehringer Ingelheim could receive more than $800 million from development of the new drugs.

This alliance was brilliant for both parties. Boehringer brought compounds; Lilly brought diabetes expertise and commercial infrastructure. Together, they could share costs and risks while accelerating development. The partnership would eventually produce multiple successful drugs, including Jardiance, which became a multi-billion dollar franchise.

The 2010s also saw Lilly making bold moves in animal health. In April 2014, Lilly announced plans to acquire Switzerland-based Novartis AG's animal health business for $5.4 billion in cash to strengthen and diversify its Elanco unit. Lilly said it planned to fund the deal with about $3.4 billion of cash on hand and $2 billion of loans.

This was Lilly's largest acquisition ever, and it raised eyebrows. Why was a company refocusing on human pharmaceuticals doubling down on animal health? The answer lay in portfolio theory—animal health provided steady cash flows with different risk profiles than human drugs. It was a hedge against the volatility of pharmaceutical development.

But by 2018, the strategy shifted again. Lilly spun off Elanco Animal Health in a $1.7 billion IPO. The timing was perfect—animal health valuations were high, and Lilly needed capital for what was coming next.

Throughout this period, Lilly never forgot the insulin legacy. In early 2020, Lilly introduced the Lilly Insulin Value Program, where people who have commercial insurance or no insurance can receive a savings card to fill their entire monthly prescription of any Lilly insulin for $35. In 2023, the Inflation Reduction Act extended a similar concept across all insulin suppliers by capping out-of-pocket costs for insulin at $35 per monthly prescription among Medicare Parts B and D enrollees.

This wasn't just corporate social responsibility—it was strategic positioning. As drug pricing became a political flashpoint, Lilly's voluntary price caps on insulin bought goodwill and potentially headed off more aggressive regulation.

The company also began investing heavily in next-generation manufacturing. New facilities in Ireland, Puerto Rico, and North Carolina weren't just bigger—they were smarter, using continuous manufacturing, real-time quality control, and modular design that could be rapidly reconfigured for different products.

By 2020, the transformation was complete. Lilly had evolved from a diversified pharmaceutical conglomerate into a focused biopharma company with deep expertise in diabetes, oncology, immunology, and neuroscience. Revenue had grown from $10 billion in 2000 to over $24 billion in 2020.

But the biggest transformation was yet to come. Hidden in Lilly's pipeline was a class of drugs that would revolutionize not just diabetes treatment but potentially all of medicine. The company that had brought insulin to the masses was about to do something similar with a new class of molecules that mimicked gut hormones.

The stage was set for the GLP-1 revolution.

VIII. The GLP-1 Revolution: Mounjaro & Zepbound (2022–Present)

The Zoom call in May 2022 was supposed to be routine—another FDA approval announcement for Eli Lilly's investor relations team. But when the news broke that Mounjaro (tirzepatide) had been approved for Type 2 diabetes, something unexpected happened. The phones didn't stop ringing. Not from diabetics, but from people wanting to lose weight.

Lilly brought exenatide to market—the first of the GLP-1 receptor agonists—followed by blockbuster drugs in the same class such as Mounjaro and Zepbound (tirzepatide). But tirzepatide was different from earlier GLP-1 drugs. It was a dual agonist, activating both GLP-1 and GIP receptors—like playing a piano with both hands instead of one.

The science behind tirzepatide represents decades of research finally clicking into place. GLP-1 (glucagon-like peptide-1) and GIP (glucose-dependent insulinotropic polypeptide) are natural hormones released by your intestines after eating. They tell your pancreas to produce insulin, your liver to stop making glucose, your stomach to slow down, and—crucially—your brain that you're full. Tirzepatide hijacks this entire system with synthetic precision.

The company offers Basaglar, Humalog, Humalog Mix 75/25, Humalog U-100, Humalog U-200, Humalog Mix 50/50, insulin lispro, insulin lispro protamine, insulin lispro mix 75/25, Humulin, Humulin 70/30, Humulin N, Humulin R, and Humulin U-500 for diabetes; Jardiance, Mounjaro, and Trulicity for type 2 diabetes; and Zepbound for obesity.

The Phase 3 SURPASS trials for Mounjaro in diabetes were impressive enough—showing A1C reductions that outperformed everything on the market. But the weight loss data made jaws drop. Diabetic patients were losing 15-20% of their body weight. This wasn't a side effect; it was a revolution.

November 2023 brought the inevitable: FDA approves Zepbound for obesity - first and only treatment activating both GIP and GLP-1. Same molecule as Mounjaro, different indication, new brand name. The obesity market had been waiting for something like this since... well, forever.

The clinical data was staggering. The SURMOUNT-1 trial showed that nearly 99% of participants with pre-diabetes remained diabetes-free after three years. Participants maintained an average weight loss of 22.9% through 176 weeks. These weren't marginal improvements—they were transformational outcomes that challenged our understanding of obesity as a chronic, progressive disease.

Then came the head-to-head data everyone was waiting for. In the SURMOUNT-5 trial, Zepbound demonstrated 47% greater relative weight loss versus Novo Nordisk's Wegovy—20.2% average weight loss compared to 13.7% with Wegovy at 72 weeks. In pharma, beating the market leader by 47% is like Usain Bolt winning the 100m by 20 meters.

But success created its own crisis: supply. Eli Lilly's blockbuster weight loss drug Zepbound and diabetes treatment Mounjaro posted weaker-than-expected sales for the third quarter, even as supply of both medicines has largely recovered from widespread shortages in the U.S. The company blamed inventory dynamics, but the real story was more complex.

Demand was literally unprecedented. Lilly had built massive manufacturing capacity, investing over $18 billion since 2020 in new facilities. The company continues to invest heavily in increasing manufacturing capacity and estimates producing at least 1.6 times the amount of salable incretin doses in the first half of 2025, compared to the first half of 2024. Yet it still wasn't enough.

The numbers tell the story of a market exploding in real-time. Mounjaro brought in $3.84 billion for the quarter, a 113% increase over $1.81 billion in the same period during 2024. Zepbound sold $2.31 billion compared to $517 million for the first quarter of 2024, when it was fresh on the market.

For 2024, Mounjaro and Zepbound brought in $3.5 billion and $1.9 billion, respectively in Q4 alone. The full-year 2024 numbers were even more impressive, with the company making a revenue of $45.04 Billion USD, an increase over the revenue in the year 2023 that were of $34.12 Billion USD.

The competitive dynamics with Novo Nordisk turned the obesity market into a two-horse race worth potentially $100+ billion by 2030. Novo had first-mover advantage with Ozempic and Wegovy, but Lilly had the dual agonist advantage. It was Coke versus Pepsi, but with life-changing medicines instead of sugar water.

Pricing strategy became crucial. Zepbound launched at $1,060 per month before insurance—deliberately priced 20% below Wegovy. This wasn't charity; it was market capture. Lilly understood that in a market this large, market share mattered more than margins.

The shortage situation created unexpected complications. Compounding pharmacies began making knockoff versions, arguing that FDA shortage designations allowed them to produce alternatives. Earlier this month, a trade group representing compounding pharmacies, which make customized and often cheaper alternatives to branded drugs in shortage, sued the FDA when the agency removed tirzepatide from its shortage list.

Manufacturing became the bottleneck for growth. We'll also bring additional manufacturing capacity online and expect to produce at least 60% more salable doses of incretins in the first half of the year compared to the first half of 2024, CEO David Ricks promised investors. The company was essentially building pharmaceutical factories as fast as construction crews could pour concrete.

The medical implications kept expanding. Beyond diabetes and obesity, tirzepatide showed promise for sleep apnea (approved December 2024), heart failure, MASH (metabolic dysfunction-associated steatohepatitis), and potentially even addiction and neurodegenerative diseases. Each new indication represented billions in potential revenue.

By mid-2025, the GLP-1 revolution had fundamentally changed Eli Lilly. The company that invented commercial insulin was now leading another transformation in metabolic medicine. Stock price reflected this: shares had risen over 100% since Mounjaro's approval, making Lilly one of the world's most valuable pharmaceutical companies.

IX. Innovation Pipeline & Future Bets

The small white pill sitting in the Phase 3 trial looked unremarkable—just another oral medication among thousands. But orforglipron represented something profound: the democratization of the GLP-1 revolution. No more weekly injections. No more refrigeration. Just a daily pill you could take with your morning coffee.

Orforglipron is the first oral small molecule glucagon-like peptide-1 (GLP-1) receptor agonist, taken without food and water restrictions, to successfully complete a Phase 3 trial. The ACHIEVE-1 results in April 2025 sent shockwaves through the industry: lowering A1C by an average of 1.3% to 1.6% across doses with an average 16.0 lbs (7.9%) weight loss at the highest dose.

But the real story was what came next. The ATTAIN-1 obesity trial results in August 2025 showed weight loss of up to an average of 27.3 lbs at 72 weeks. This wasn't just matching injectable GLP-1s—it was proving that oral delivery could achieve similar efficacy to injections.

Think about the implications. Currently, GLP-1 drugs require weekly injections, cold storage, and significant patient education. They're expensive to manufacture, ship, and store. Orforglipron changes all of that. If approved, the company is confident in its ability to launch orforglipron worldwide without supply constraints.

The development of orforglipron showcases Lilly's strategic thinking. Orforglipron was discovered by Chugai Pharmaceutical Co., Ltd. and licensed by Lilly in 2018. Rather than developing everything in-house, Lilly increasingly scouts global innovation, bringing in promising molecules and applying its development and commercialization expertise.

Lilly plans to submit orforglipron for regulatory review for the treatment of overweight or obesity in 2025, and for type 2 diabetes in 2026. The staggered submission is strategic—obesity represents the larger market opportunity, while diabetes provides a fallback indication.

Beyond orforglipron, Lilly's pipeline reveals ambitious bets across multiple frontiers:

Expanding GLP-1 Indications: The company is systematically testing tirzepatide for conditions beyond diabetes and obesity. Sleep apnea approval came in December 2024. Studies in chronic kidney disease, heart failure with preserved ejection fraction, and MASH are ongoing. Each successful indication adds billions in potential revenue while reinforcing tirzepatide's position as a platform drug.

Next-Generation Obesity Medicines: The company isn't resting on tirzepatide's success. Multiple candidates targeting different mechanisms are in development—triple agonists adding glucagon receptor activation, small molecules targeting different pathways, and combination therapies that could push weight loss beyond 25%.

Manufacturing Innovation: Perhaps the most underappreciated aspect of Lilly's strategy is manufacturing. The company is pioneering continuous manufacturing for biologics, using AI to optimize production schedules, and building modular facilities that can be rapidly reconfigured. This isn't sexy, but it's essential—whoever can make these drugs fastest and cheapest wins.

Digital Therapeutics: Lilly is quietly building capabilities in digital health, recognizing that GLP-1 drugs work best with lifestyle modification. The company is exploring digital coaching platforms, continuous glucose monitoring integration, and AI-powered personalization of treatment regimens.

The competition isn't standing still. Pfizer discontinued its oral GLP-1 due to liver toxicity concerns, but others are advancing. Viking Therapeutics showed promising Phase 2 data. Novo Nordisk is developing its own oral semaglutide. The race for the next generation of metabolic medicines is intensifying.

But Lilly has structural advantages that are hard to replicate:

-

Manufacturing Scale: Those $18+ billion in manufacturing investments create a moat. Building GLP-1 production capacity takes 3-5 years. Lilly has a multi-year head start.

-

Regulatory Expertise: The company's experience navigating FDA approvals for dozens of indications creates institutional knowledge that accelerates development timelines.

-

Real-World Data: With millions of patients on Mounjaro and Zepbound, Lilly has unprecedented real-world data on GLP-1 responses, side effects, and optimal dosing. This data advantage compounds over time.

-

Platform Approach: Rather than viewing each drug as isolated, Lilly treats GLP-1s as a platform—each new indication, formulation, or combination builds on previous learning.

The biggest risk isn't competition—it's success. If GLP-1 drugs work as well as early data suggests for conditions ranging from addiction to Alzheimer's, the ethical questions become profound. Who gets access? How does society pay for drugs that could benefit 40% of the population? What happens when a drug that treats individual illness also addresses societal problems?

The company anticipates 2025 revenue to be between $58 billion and $61.0 billion, representing 32% growth. But these numbers might actually be conservative if GLP-1 adoption accelerates and new indications prove successful.

X. Playbook: Business & Investing Lessons

After 148 years, what can we learn from Eli Lilly's journey from Civil War pharmacy to GLP-1 giant? The lessons transcend pharmaceuticals, offering insights for any business navigating technological disruption, regulatory complexity, and societal expectations.

Lesson 1: Platform Technologies Compound Over Generations

Lilly's insulin expertise didn't just create one product—it created a capability that compounded for a century. From animal insulin to recombinant DNA to insulin analogs to GLP-1 agonists, each innovation built on previous knowledge. The company that learned to extract insulin from pig pancreases in 1922 used that expertise to scale penicillin in 1943, produce polio vaccine in 1955, pioneer recombinant DNA in 1982, and develop dual agonists in 2022.

The lesson: Transformative businesses don't just create products; they create capabilities that compound across technological generations.

Lesson 2: Trust Is the Ultimate Moat

When insulin was discovered, Lilly could have been just another manufacturer. Instead, George Clowes' insistence on publishing research, maintaining quality standards, and collaborating with academics built trust that became Lilly's greatest asset. That trust allowed them to charge premium prices, attract top talent, and weather controversies that would have destroyed companies with weaker reputations.

Even after the $1.42 billion Zyprexa fine, physicians still prescribed Lilly drugs because 100+ years of reliability mattered more than one scandal.

Lesson 3: Family Control + Professional Management = Longevity

The Lilly Endowment still owns 11.3% of the company, creating unusual stability. This structure allows long-term thinking while maintaining professional management. The Endowment doesn't meddle in operations but provides patient capital and prevents hostile takeovers.

This hybrid model—family values with professional execution—enabled Lilly to resist short-term pressures that forced competitors into ill-advised mergers or premature cost-cutting.

Lesson 4: Ethical Paradoxes Are Unavoidable

Lilly faces an impossible tension: developing life-saving drugs requires billions in investment, which requires high prices, which limits access to those life-saving drugs. The company that distributed insulin for the price of patents now sells Zepbound for $1,060 per month.

The Lilly Insulin Value Program offering $35 insulin represents one attempt to square this circle, but it's a band-aid on a systemic problem. The lesson isn't that this paradox can be solved—it's that managing it requires constant recalibration between profit and purpose.

Lesson 5: Geographic Concentration Can Be Strategic

While competitors globalized operations, Lilly remained stubbornly Midwestern. Headquarters stayed in Indianapolis. Manufacturing concentrated in the U.S. and select countries. This focus created advantages: simpler logistics, deeper local relationships, better quality control, and a distinctive corporate culture.

In an era of globalization, Lilly proved that geographic concentration—if executed well—can be a strategic advantage rather than provincial limitation.

Lesson 6: R&D Productivity Requires Portfolio Thinking

Lilly's R&D strategy resembles venture capital more than traditional corporate research. They make many bets across different mechanisms, diseases, and risk levels. Most fail. A few succeed spectacularly. The winners (insulin, Prozac, tirzepatide) more than pay for the losers.

This portfolio approach requires accepting failure as normal, maintaining multiple shots on goal, and having the financial strength to sustain long droughts between breakthroughs.

Lesson 7: Timing Matters More Than Being First

Lilly wasn't first in insulin (Toronto discovered it), wasn't first in GLP-1s (Novo's Ozempic preceded Mounjaro), wasn't first in SSRIs (several companies developed them simultaneously). But Lilly excelled at being ready when markets inflected.

They had manufacturing ready when insulin was discovered, had Prozac ready when mental health destigmatized, had tirzepatide ready when obesity became recognized as a disease. The lesson: Position for inevitable trends, then execute flawlessly when the moment arrives.

Lesson 8: Capital Allocation Follows Strategy

Lilly's capital allocation over the decades reveals strategic clarity: - 1920s-1950s: Build manufacturing scale - 1960s-1980s: Geographic expansion - 1990s-2000s: Diversification (animal health, cosmetics) - 2010s: Refocus and partnerships - 2020s: All-in on manufacturing capacity for GLP-1s

Each era's capital allocation aligned with strategic priorities. When strategy shifted, capital allocation shifted immediately and decisively.

Lesson 9: Crises Create Opportunities

Lilly's greatest leaps followed crises: - Post-Civil War: Colonel Lilly founded company after war trauma - 1920s insulin shortage: Forced industrial-scale production - WWII: Accelerated penicillin manufacturing - Zyprexa scandal: Catalyzed strategic refocus - COVID-19: Accelerated GLP-1 manufacturing investment

Companies that survive crises by adapting rather than retreating often emerge stronger.

Lesson 10: The Next Platform Is Always Emerging

Just as insulin expertise enabled GLP-1 development, today's GLP-1 platform will enable tomorrow's breakthroughs. The capabilities being built—precision manufacturing, real-world data analytics, combination therapies, oral delivery—will compound into advantages we can't yet imagine.

XI. Analysis & Bear vs. Bull Case

Bull Case: The Decade of Metabolic Medicine

The bulls see Eli Lilly at the beginning, not the end, of a generational opportunity. Start with the addressable market: 40% of American adults are obese, 10% have diabetes, millions more have metabolic dysfunction. Globally, these numbers are growing, not shrinking. The GLP-1 total addressable market could exceed $200 billion by 2035—larger than the entire current oncology market.

Lilly's dual agonist approach with tirzepatide provides a sustainable competitive advantage. The SURMOUNT-5 data showing 47% better efficacy than Wegovy isn't a marginal improvement—it's a different class of efficacy. As real-world evidence accumulates showing GLP-1s reducing heart disease, kidney disease, sleep apnea, and potentially even addiction and neurodegenerative diseases, these become not just diabetes or obesity drugs but foundational medicines for modern chronic disease.

The oral GLP-1 pipeline changes everything. Orforglipron's ability to launch globally without supply constraints means Lilly can finally match demand. No more shortages, no more allocation decisions, no more leaving money on the table. The convenience of a daily pill versus weekly injection expands the addressable market to patients who would never consider injections.

Manufacturing scale becomes Lilly's moat. Those $18+ billion in capacity investments aren't easily replicated. Building a GLP-1 manufacturing facility takes 3-5 years minimum. By the time competitors catch up, Lilly will have moved to next-generation products. Lilly expects it will be able to crank out 1.6 times the amount of marketable incretin doses in the first half of the year versus the first half of 2024.

The 2025 guidance of revenue between $58 billion and $61.0 billion implies continued 32% growth. But this might be sandbagging. If orforglipron launches successfully, if new indications get approved, if international markets open up faster than expected, revenue could surprise significantly to the upside.

Valuation concerns are overblown. Yes, Lilly trades at historic multiples, but this isn't a typical pharma company anymore. It's a metabolic medicine platform company with decades of growth ahead. The terminal value of a company that helps billions of people avoid diabetes, heart disease, and premature death is enormous.

Bear Case: Peak GLP-1 and the Coming Compression

The bears see multiple storms gathering that could devastate Lilly's seemingly impregnable position.

Start with competition. Novo Nordisk isn't sitting still—their next-generation obesity drugs target 25% weight loss. Viking Therapeutics, Structure Therapeutics, and dozens of other biotechs are developing oral GLP-1s. Chinese companies are developing biosimilars. The moat around GLP-1s is narrowing rapidly. Within 5 years, these could be commodity drugs with multiple suppliers and compressed margins.

Compounding pharmacies represent an existential threat no one's pricing in. These pharmacies are already producing tirzepatide copies, arguing shortage exceptions allow production. Even after shortages end, the infrastructure and demand are established. If courts rule that compounding pharmacies can continue producing GLP-1s, Lilly's pricing power evaporates overnight.

Insurance coverage remains the elephant in the room. Most insurers don't cover GLP-1s for obesity, considering them "lifestyle" drugs. Medicare explicitly excludes weight-loss drugs. Without insurance coverage, the addressable market shrinks dramatically—how many people can afford $12,000+ annually out of pocket? Political pressure to expand coverage could paradoxically hurt Lilly by forcing price negotiations.

Safety concerns lurk beneath the enthusiasm. GLP-1 drugs have been used at scale for less than five years. Long-term effects remain unknown. Reports of muscle loss, gastroparesis, and potential thyroid cancer risk (black box warning on some GLP-1s) could explode into the next Vioxx or Fen-Phen scandal. One high-profile adverse event could crater the entire class.

The oral GLP-1 data disappointments are concerning. The new phase 3 findings are down from Lilly's earlier orforglipron study that demonstrated a 14.7% weight loss at 36 weeks. The 12.4% weight loss is also significantly lower than Lilly's Zepbound (tirzepatide), an injectable GLP-1. If patients need to choose between convenience and efficacy, many will choose efficacy—limiting orforglipron's market potential.

Manufacturing capacity could become a liability. Lilly is building massive factories based on projected demand that might not materialize. If GLP-1 adoption slows, if competitors capture share, if new technologies obsolete current drugs, Lilly will have billions in stranded assets.

The valuation is genuinely stretched. At a market cap of $628.62 Billion, Lilly trades at over 30x forward earnings—pricing in perfect execution for years. Any disappointment (missed quarter, delayed approval, competitive loss) could trigger a 30-40% correction.

Patent cliffs are approaching. Key tirzepatide patents expire in the 2030s. Unlike small molecules, biologics face biosimilar rather than generic competition, but the threat remains real. Lilly needs to develop next-generation drugs before current patents expire—a race against time they might not win.

The political risk is extreme and growing. Drug pricing is one of the few bipartisan issues in American politics. Lilly's success makes it a target. Future legislation could include price controls, mandatory rebates, or international reference pricing that destroys the U.S. pricing umbrella supporting global R&D.

Finally, the bear case questions the entire GLP-1 narrative. Are these drugs treating disease or symptoms? When patients stop taking GLP-1s, weight returns. This creates lifetime dependency at enormous cost. Society might decide this isn't sustainable, leading to usage restrictions or payment reforms that crush the market.

XII. Epilogue & "If We Were CEOs"

Standing in Lilly's Indianapolis headquarters, you can trace a direct line from Colonel Eli Lilly's two-story Pearl Street laboratory to today's gleaming research centers. The portraits on the walls—three generations of Lillys, the scientists who developed insulin, Prozac, and now tirzepatide—tell a story of continuous innovation across 148 years. But what would we do if handed the keys to this pharmaceutical kingdom today?

The Obesity Epidemic as Defining Healthcare Challenge

First, we'd recognize that Lilly sits at the intersection of the 21st century's defining health crisis and its most promising solution. The obesity epidemic isn't just about weight—it's about diabetes, heart disease, cancer, dementia, and healthcare systems collapsing under chronic disease burden. GLP-1 drugs aren't just pharmaceuticals; they're potentially civilization-saving interventions.

But with great power comes great complexity. If we were CEO, we'd frame Lilly's mission not as "selling GLP-1 drugs" but as "ending the metabolic disease epidemic." This reframing changes everything—from R&D priorities to pricing strategies to partnership approaches.

Balancing Innovation with Affordability

The affordability crisis demands radical thinking. We'd propose a global tiered pricing system based on country GDP per capita and individual income. Rich countries and wealthy individuals subsidize access for poor countries and low-income patients. This isn't charity—it's market expansion. A billion people paying $50 per month generates more revenue than 10 million paying $1,000.

We'd accelerate the development of ultra-low-cost formulations for emerging markets. If Indian generic manufacturers can produce drugs at 95% lower cost, why can't Lilly create a subsidiary focused exclusively on radical cost reduction? License older-generation GLP-1s to generics manufacturers while maintaining premium pricing for cutting-edge formulations.

What Would We Prioritize?

Oral drugs would be priority one. Injectable medications will never reach full market potential. Despite orforglipron's mixed results, we'd double down on oral formulation development. The company that cracks truly effective oral GLP-1s owns the future of metabolic medicine.

New mechanisms would be priority two. Dual agonists were revolutionary; triple agonists adding glucagon could be even better. But we'd also explore completely novel approaches—gene therapy for obesity, engineered bacteria producing GLP-1 in the gut, implantable devices providing continuous hormone delivery. Most will fail, but one breakthrough could define the next decade.

Access programs would be priority three. Create a Lilly Global Health subsidiary operating as a public benefit corporation. This entity would provide GLP-1s at cost to low-income countries, displaced populations, and humanitarian crises. Fund it with 5% of profits from commercial sales. This isn't just corporate social responsibility—it's building markets, gathering real-world data, and creating political capital for when drug pricing battles intensify.

Manufacturing innovation would be priority four. Current GLP-1 production is too complex, too expensive, too slow. We'd launch a "Manhattan Project" for manufacturing—targeting 90% cost reduction within 10 years. Continuous manufacturing, cell-free synthesis, plant-based production, even synthetic biology approaches. Make GLP-1s as cheap to produce as aspirin.

The Next 150 Years: What Diseases Define Lilly's Future?

Looking beyond GLP-1s, three areas would define Lilly's next century:

Neurodegeneration: Alzheimer's, Parkinson's, ALS remain largely untreatable. Lilly's experience with complex biologics and chronic disease management positions it well for neurology. We'd acquire or partner with companies developing novel approaches—tau antibodies, gene therapies, even brain-computer interfaces for symptom management.

Aging itself: Rather than treating diseases of aging individually, target aging biology directly. Senolytics, epigenetic reprogramming, mitochondrial therapeutics—these sound like science fiction but represent the logical evolution of medicine. The company that helps humans live healthily to 120 captures immense value.

Pandemic preparedness: COVID-19 won't be the last pandemic. We'd build surge capacity for rapid vaccine and therapeutic development. Partner with governments to maintain warm manufacturing bases. When the next pandemic hits, Lilly would be ready to scale production of countermeasures within weeks, not months.

Final Reflections on Building Century-Spanning Companies

Eli Lilly's story reveals uncomfortable truths about building enduring companies. Success requires patient capital (the Endowment's steady ownership), geographic stability (staying in Indianapolis), and family continuity (three generations of Lillys) that modern capitalism rarely allows.

It requires balancing stakeholders in ways that satisfy none completely—charging enough to fund R&D while ensuring access, pursuing profits while maintaining purpose, competing fiercely while collaborating on pre-competitive research.

Most importantly, it requires thinking in decades, not quarters. Colonel Lilly couldn't have imagined GLP-1 agonists, but he built a foundation strong enough to support innovations he couldn't conceive. Today's leaders must similarly build for futures they can't fully envision.

If we were CEOs, our north star would be simple: In 2176, when Lilly celebrates its 300th anniversary, what will they say we built? The answer should be: a platform for human flourishing that turned the 21st century's greatest health challenges into solved problems, while creating sustainable value for all stakeholders.

The next chapter of Lilly's story is being written now, in research labs where scientists investigate triple agonists, in factories racing to meet GLP-1 demand, in boardrooms debating access versus profits. The company that brought insulin to the masses and Prozac to the millions now stands ready to tackle obesity, aging, and whatever comes next.

The journey from Civil War pharmacy to GLP-1 giant isn't complete—it's just beginning.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube