Linde plc: The Reunion of the Century and the King of Industrial Gases

I. Episode Introduction & The 101-Year Corporate Separation

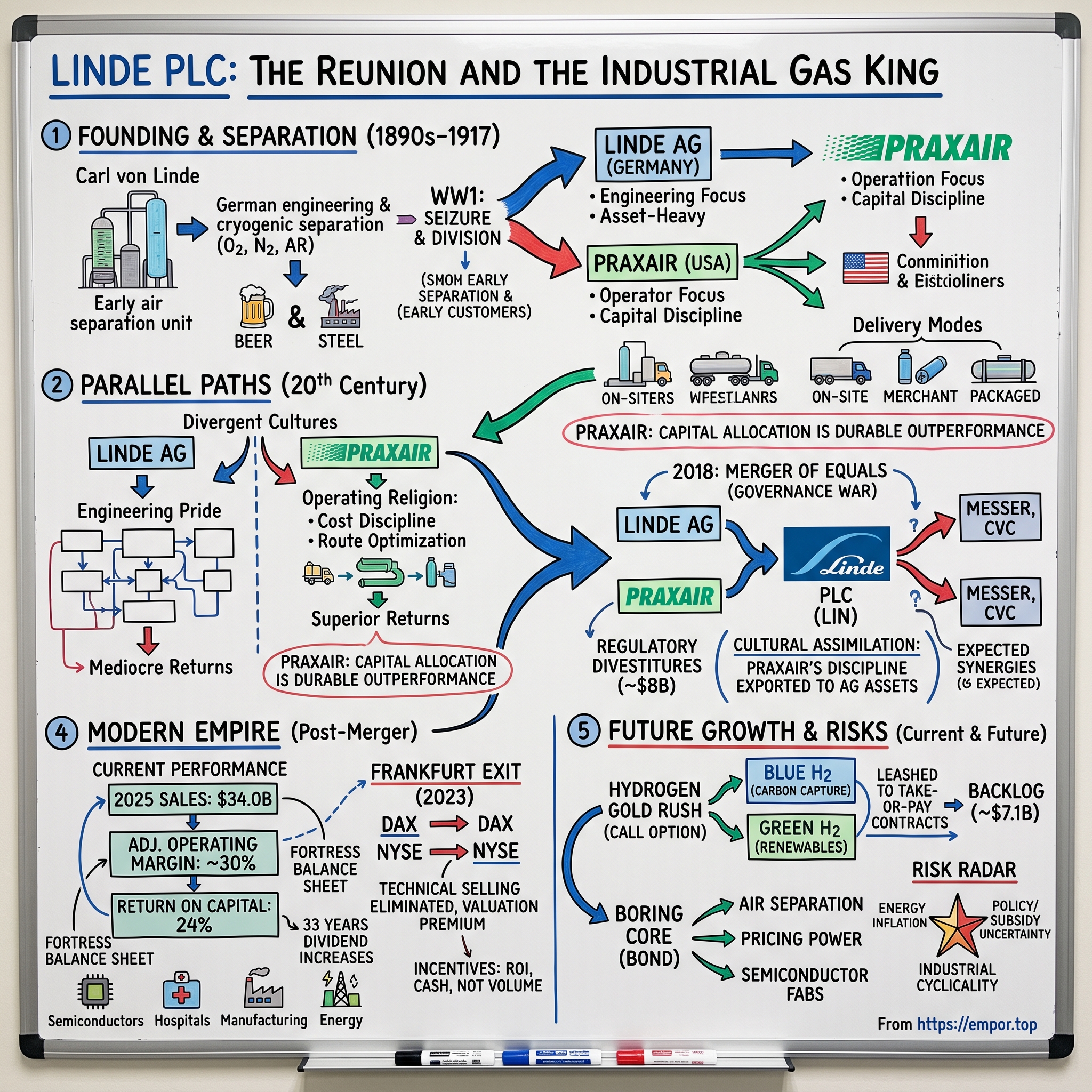

Picture a boardroom in 2017, split across two continents and two languages. On one side sits a German engineering institution more than a century old, an icon of the DAX, proud of building the most technically sophisticated chemical plants on the planet. On the other sits its estranged American offspring — a leaner, harder-nosed operator that a US government had literally confiscated from its German parent during the First World War and set loose to grow up alone. For 101 years, the two halves of Carl von Linde's house had lived apart, one in Munich and one in Danbury, Connecticut, competing against each other across the globe. In 2018, against the objections of German unions, politicians, and no small number of antitrust regulators, they merged back together into a single entity — and the reunited family promptly became the undisputed monarch of the industrial gases world.

The scale of what they built is difficult to overstate. Linde plc, trading under the ticker LIN, reported full-year 2025 sales of $34.0 billion, up 3% on the prior year, with an adjusted operating margin of 29.8% — a level of profitability that would make many software companies blush.[^1] By the first quarter of 2026, that margin had touched 30.0% and the company was generating a return on capital of 24%, a number that sits in a rarefied tier for any capital-intensive industrial business.[^2] For a company whose core product is quite literally free — it comes out of the sky — Linde has engineered one of the most durable profit machines in global industry.

The core thesis of this story is that industrial gases are the ultimate hidden utility. The physics are more than a century old and hardly a secret; a competent chemical engineer can describe how to separate air over lunch. And yet the economics are close to impregnable, because industrial gas is a business where the molecule is cheap but the logistics are brutal. Gas is heavy, cold, and expensive to move. Ship it more than a hundred miles or so and the economics collapse. The result is not one global market but thousands of tiny local monopolies, each defended by geography, contracts, and a customer's terror of ever losing supply. Linde does not so much dominate a market as own a constellation of them.

Consider what "hidden utility" actually means through a single day. The oxygen in a hospital's wall outlet, the nitrogen blanketing a bag of potato chips to keep them fresh, the argon shielding a welder's arc on a construction site, the ultra-pure gases flowing through the machine that etched the chip in the phone in your pocket, the carbon dioxide dissolved in a soft drink — a startling share of these passed through the pipes, trucks, and cylinders of one of three companies, and more likely than not through Linde. It is infrastructure in the truest sense: invisible when it works, catastrophic when it fails, and taken utterly for granted by the customers whose businesses would collapse without it. That combination — indispensable yet unnoticed — is the ideal habitat for durable pricing power, because nobody negotiates hard over a small line item that could shut their whole operation down.

This is also a story about culture and capital discipline. The narrative arc runs from Carl von Linde's cryogenic breakthroughs in the 1890s, through the ruthless operating religion that a company called Praxair built in the American Rust Belt, to the two executives — Steve Angel and, since 2022, Sanjiv Lamba — who took that religion and imposed it on a reunited global empire. The question that hangs over the whole enterprise, and the one a sophisticated investor must keep asking, is whether the towering returns are the product of a genuinely unassailable business model or of a valuation that has come to price Linde like something it is not. We will get there. First, we have to go back to a German engineer and a very cold idea.

II. Carl von Linde and the Birth of Cryogenic Separation

In 1879, a Bavarian engineering professor named Carl von Linde did something faintly heretical for an academic: he quit his university post to build machines. Linde had become obsessed with cold. Not cold as weather, but cold as a controllable industrial force. His first commercial triumph was the ammonia refrigeration machine, a device that let breweries and meatpackers make ice reliably for the first time, freeing them from the seasonal tyranny of harvested lake ice. Refrigeration made him wealthy and, more importantly, taught him the thermodynamics that would define the rest of his life.5

It is worth pausing on who this man was, because the culture of a company is often set by the temperament of its founder, and Linde's temperament was that of the meticulous problem-solver rather than the flamboyant promoter. He was a professor at the Technical University of Munich, a man more comfortable with a thermodynamic equation than a sales pitch, and he approached the cold as an engineering discipline to be mastered rather than a spectacle to be sold. That instinct — solve the physics precisely, then build the machine that monetizes it — is a thread that runs unbroken from the 1870s to the modern engineering division that still bears his name. It is not a coincidence that a company founded by a professor became, more than a century later, the operator whose proprietary plant designs give it an edge rivals must purchase from outside.

Then Linde asked the harder question. If you could cool a gas enough, could you turn air itself into a liquid — and if you could liquefy air, could you pull it apart into its ingredients? In 1895 he succeeded, achieving the industrial-scale liquefaction of air and filing for patent protection on the process.5 To understand why this mattered, it helps to strip the physics down to a kitchen-table analogy. Squeeze a gas hard (compression) and it heats up, the way a bicycle pump gets warm. Cool that compressed gas back down, then suddenly let it expand through a valve, and it cools dramatically — this is the Joule-Thomson effect, the same reason an aerosol can turns frosty as you spray it. Cycle air through that squeeze-cool-expand loop enough times and it gets so cold — roughly minus 195 degrees Celsius — that it becomes a pale blue liquid.

The trick, and the genius, was what came next. Liquid air is not one substance; it is a cocktail. Each component boils off at a slightly different temperature: nitrogen at about minus 196°C, argon around minus 186°C, oxygen at minus 183°C. So if you warm the liquid back up very, very carefully inside a tall distillation column, the gases evaporate off in sequence, and you can capture each one at high purity. This is fractional distillation of air, and it is essentially the same principle as distilling whiskey, only run at temperatures cold enough to freeze the planet. The device that does it is called an air separation unit, or ASU, and the modern versions Linde builds today are direct descendants of the columns Carl von Linde first drew.

The elegance of the model is that a single machine, fed by nothing but the atmosphere, produces three or four saleable products at once, each with its own market. Oxygen goes to steelmakers, who blow it into furnaces to burn off impurities, and to hospitals, where it keeps patients alive. Nitrogen, being inert, goes to food packagers who use it to displace oxygen and stop food from spoiling, and to electronics makers who need an atmosphere that will not react with delicate components. Argon, rarer and pricier, goes to welders and to the semiconductor industry. The economics of running one plant to yield several revenue streams is part of why the business throws off so much cash: the fixed cost of the ASU and its enormous electricity draw is spread across multiple products, so each incremental molecule sold at the margin is close to pure profit. Purity is the quiet lever here — the difference between industrial-grade nitrogen and the ultra-high-purity nitrogen a chip fab demands is a difference of several decimal places and a large difference in price, and the ability to hit those specs reliably is itself a barrier that keeps casual competitors out.

Here is where the physics collided with economics, and the collision defined the industry forever. The raw material — air — is free and infinite. But the finished product, whether a chilled liquid or a compressed gas, is heavy and awkward. A truck full of liquid oxygen weighs a great deal and delivers relatively little value per mile. This single fact — that the product is cheap to make but ruinous to transport far — meant industrial gas could never be a national business shipped from a few giant factories. It had to be made locally, near where it was consumed. From the very beginning, the winners would be whoever built the densest local networks, and the birth of the "merchant" model — small regional plants serving customers within a tight radius — was baked into the chemistry.

This physical reality — cheap molecule, expensive mile — is the single most important fact in the entire industry, and it is worth dwelling on because everything strategic about Linde flows from it. A steel mill in Ohio cannot economically buy its oxygen from a plant in Texas; the transport cost would dwarf the value of the gas. So the industry never consolidated into a handful of mega-factories the way, say, semiconductor manufacturing did. It fragmented into a patchwork of local supply zones, each with a natural radius of perhaps a hundred miles for liquid product, inside which whoever got there first and built density enjoyed something close to a natural monopoly. A century before economists coined the term "network effects," Carl von Linde's cold machines had created a business whose defensibility was written into the laws of thermodynamics and the price of diesel.

Linde expanded aggressively, and in 1907 he formed the Linde Air Products Company in the United States, opening his first American plant in Buffalo, New York.6 It should have been the start of a seamless transatlantic empire. Instead, it became the setup for one of the strangest corporate amputations in industrial history. When the United States entered the First World War, the Trading with the Enemy Act gave the government sweeping power over German-owned assets on American soil. In 1917, Linde Air Products — a German-owned company — was effectively seized and, together with four other producers of acetylene and related chemicals, folded into a new American conglomerate: the Union Carbide and Carbon Corporation.6 Carl von Linde's house was now formally divided, one half in Germany and one half absorbed into a sprawling American chemicals giant. Neither half would rejoin the other for over a century, and in the meantime they would grow into two utterly different animals.

III. The Parallel Paths: Linde AG and Praxair

For most of the twentieth century, the two Lindes could not have been more different, and their divergence is really a case study in how national culture and corporate structure shape returns on capital.

Linde AG: the engineer's engineer. Back in Germany, the surviving parent — Linde AG — rebuilt itself twice from rubble, through the wreckage of two world wars, and emerged as the platonic ideal of German industrial engineering. Its people were brilliant at building things. If you wanted the most thermodynamically efficient air separation unit on earth, or a fiendishly complex plant to liquefy natural gas at scale, Linde AG's engineering arm was the address. But that engineering pride carried a cost. The company grew asset-heavy and, over the decades, accumulated the sort of sprawling divisional structure and management layers that afflicted many European industrial champions. It built magnificent machines and generated persistently mediocre returns on the capital sunk into them. For a business, engineering elegance is a means, not an end, and Linde AG at times seemed to confuse the two.

Praxair: the operator's operator. The American half took the opposite path, though it took a while. For seventy-odd years it sat inside Union Carbide, a company whose name would become synonymous with industrial disaster after the 1984 Bhopal gas tragedy in India, in which a leak at a Union Carbide pesticide plant killed thousands. Whatever the merits of the parent, the gas division was a fundamentally sound business trapped inside a conglomerate that neither understood nor prioritized it — a classic setup for the value that a spinoff can unlock when a good business is finally allowed to run itself. In June 1992, Union Carbide spun off its industrial gases division as an independent, publicly traded company, and three years later it took a new name: Praxair, from the Greek praxis, meaning practical application, welded to "air."6 The name was a manifesto. Freed from a troubled parent and forced to stand on its own, Praxair developed what can only be described as an operating religion — a near-fanatical culture of cost discipline, route optimization, and rigorous project selection. Under CEOs William Lichtenberger and, from 2007, Steve Angel, Praxair became the most profitable operator in the entire global industry, out-earning larger rivals not by owning better molecules but by squeezing more cash out of every plant, truck, and cylinder.

The divergence between the two Lindes is one of the more instructive natural experiments in industrial history, because it isolates the variable that matters. Same founder, same technology, same product, same physics of local monopoly — and yet for decades the German parent earned mediocre returns while the American offshoot earned superb ones. The difference was not engineering talent; if anything Linde AG had more of it. The difference was that Praxair treated capital as scarce and precious, to be deployed only where it earned its keep, while Linde AG treated engineering achievement as an end in itself and let the returns take care of themselves. For a long-term investor, this is the whole ballgame in miniature: in a mature, capital-intensive industry, superior technology is table stakes, but superior capital allocation is the actual source of durable outperformance. Hold that thought, because it is exactly what the 2018 merger was designed to exploit.

To understand why one company could earn so much more than another selling identical gases, you have to understand the three ways industrial gas actually reaches a customer — the three delivery modes that, together, form the industry's moat.

The first is on-site, or tonnage, supply. Here Linde builds an entire air separation unit right next to a giant customer — an oil refinery, a steel mill, a semiconductor fab — and pipes gas directly over the fence. These plants cost enormous sums, often well north of $100 million, so no one builds them on spec. They are underwritten by take-or-pay contracts running fifteen to twenty years, in which the customer commits to pay whether or not it takes the gas, and energy and feedstock costs are contractually passed straight through. The economics resemble a regulated utility: predictable, inflation-protected, and boring in the best possible way.

The second is merchant, or bulk liquid, supply. Here gas is liquefied, loaded onto cryogenic tanker trucks, and delivered to storage tanks at mid-sized customers. This is the mode where route density becomes everything. A plant serving fifty customers packed within a fifty-mile radius earns far more than one serving a dozen scattered across a state, because the cost is in the driving, not the gas. And crucially, density is self-defending: a competitor cannot economically justify sending trucks into your delivery radius to poach one account, because it would be running long, half-empty routes against your dense, efficient ones. Win a region early and you own it.

The third is packaged, or cylinder, gases. These are the familiar steel bottles delivered to welding shops, hospitals, and laboratories. It is a retail-like, high-touch, high-margin business — recurring revenue from thousands of small customers who value reliability far more than price, and switching for a few percent savings is rarely worth the risk of running dry mid-job. The operational complexity is real — tracking hundreds of thousands of cylinders, refilling them, managing rental fees on the bottles themselves — but that very complexity is a barrier, because it is a logistics business masquerading as a gas business, and logistics at scale is hard to replicate.

The three modes together form a ladder of capital intensity and contract length. On-site is the most capital-hungry and the most locked-in, with the longest contracts and the most utility-like cash flows. Merchant sits in the middle, defended by density rather than pipelines. Packaged is the least capital-intensive and the stickiest at the individual-customer level. A well-run operator uses one ASU to feed all three: the same plant that pipes tonnage gas over the fence to an anchor customer also fills the tankers that serve merchant accounts and the cylinders that serve the corner welding shop, wringing the maximum revenue out of a single fixed asset. The art of the business is loading that plant as fully as possible, because a half-empty ASU is a balance sheet disaster and a full one is a money fountain.

Praxair's playbook was to attack all three with relentless discipline: build only projects that cleared a strict return hurdle, optimize route density obsessively, and refuse the volume-for-volume's-sake growth that flattered revenue but starved returns. The man who came to personify that discipline was Steve Angel, an engineer by training who had done time at General Electric — the corporate finishing school that produced a generation of process-obsessed American operating executives — before joining Praxair and rising to chief executive in 2007. Angel's reputation was not for vision or charisma but for an almost merciless focus on operating metrics: pricing that stayed ahead of cost inflation, productivity programs that ran every year without exception, and a refusal to sign a growth project that could not defend its returns in a spreadsheet. Under him Praxair became, by margin, the most profitable operator in the industry despite being smaller than both Air Liquide and the old Linde AG — proof that in this business, how you run the assets matters more than how many you own. That discipline is the reason the story's next act happened the way it did. When the two Lindes finally reunited, the interesting question was not which company was bigger. It was whose culture would win.

IV. The Reunion of the Century: The 2018 Merger of Equals

On paper, the logic was almost too neat. Linde AG had world-class engineering and a commanding footprint across Europe and Asia. Praxair had world-class capital discipline and the dominant position in the Americas. Stitch them together and you would create a single company that leapfrogged the French giant Air Liquide to become the largest industrial gas company on earth, combining the best engineering brains with the hardest-nosed operators. The strategic dream was to marry the machine-builders to the money-counters.

The deal was also, in truth, a second attempt. An earlier round of merger talks between the two companies had collapsed, foundering on precisely the questions of national identity, headquarters, and control that would haunt the successful attempt. That history mattered, because it meant both sides went into the 2017 negotiations knowing exactly how fragile the arrangement was and how easily German stakeholder politics could blow it up. The structure they eventually agreed was less a clean corporate design than a peace treaty.

The reality was a governance war. When Linde and Praxair confirmed their intention to merge, the reaction in Germany was visceral. Unions on Linde AG's supervisory board feared the loss of German jobs and the gutting of a national engineering champion by American cost-cutters. Politicians fretted about the disappearance of corporate identity. The compromise that emerged was a masterpiece of diplomatic engineering in its own right: the new parent, Linde plc, would be incorporated in Ireland, tax-resident in the United Kingdom, and listed on both the New York and Frankfurt exchanges, with a genuine "merger of equals" governance structure. Steve Angel, Praxair's chairman and CEO, would run the combined company as chief executive, while Linde AG's Wolfgang Reitzle would chair the board — a balance of power carefully calibrated to reassure both sides.[^6] The combination legally closed on October 31, 2018.7

Then came the regulatory obstacle course, which was formidable precisely because the merger was so logical. When you combine the two dominant players in dozens of local oligopolies, antitrust regulators on multiple continents object — and they did. The US Federal Trade Commission required the merged company to divest assets across nine distinct industrial gas markets in the United States as a condition of approval.[^7] Regulators from the European Commission to China's 国家市场监督管理总局 State Administration for Market Regulation (SAMR) demanded their own pounds of flesh. All told, the two companies were forced to shed roughly $8 billion of assets worldwide to clear the deal. The largest US carve-out went to the Messer Group GmbH, partnered with the private equity firm CVC, which acquired a package of divested Linde businesses across the Americas; other assets went to Matheson Tri-Gas.[^8]

Here a skeptic should pause and ask the uncomfortable question: did Linde destroy value by being forced to sell high-quality assets, at regulator-dictated speed, to companies that would become competitors? The honest answer is that the divestitures were real friction — you never want to sell good businesses under duress. But the offsetting math worked out in Linde's favor. Management targeted $1.1 billion to $1.2 billion in annual cost synergies to be captured over roughly three years, and it hit those targets ahead of schedule.[^6] The recurring cash from synergies swamped the one-time cost of the forced sales. It is a useful reminder that in a business defined by local density, selling a cleanly separable regional package to a rival does not necessarily wound you, so long as your remaining network stays dense where it matters.

There is a second-order lesson in the divestiture episode that investors in any consolidating industry should file away. Regulators do not measure market power at the national level; they measure it market by market, product by product, region by region — which is exactly how this business actually works. The FTC's demand for divestitures across nine specific US markets was, in a sense, an official confirmation of the density thesis: the regulator understood that combining the two leaders in a given metropolitan area created genuine local monopoly power even if the national market remained competitive. Linde surrendered the overlaps and kept the network, and the fact that regulators focused so precisely on local concentration is itself evidence of how local this business really is.

The subtler and more consequential story is cultural. Officially this was a merger of equals. In practice, Praxair acquired Linde AG's soul. Steve Angel took the CEO chair and methodically exported Praxair's ROI-obsessed capital allocation framework onto the legacy German assets — killing underperforming projects, restructuring bloated divisions, and refusing to fund growth that did not clear the return hurdle. The engineers kept building beautiful machines, but now every machine had to earn its keep. For investors, this is the crux of the entire Linde thesis: the merger's value did not come from combining two balance sheets. It came from imposing one company's discipline on the other's assets. Which raises the next question — if the operating culture was American, why was the stock still tethered to a German exchange at all?

V. The Frankfurt Exit and NYSE Consolidation

It is not often that a company's biggest problem is that its stock goes up too much. But by the early 2020s, Linde had exactly that problem, and it was costing shareholders real money in a way almost invisible from the outside.

Following the merger, Linde plc had become the single largest constituent of Germany's DAX index. That sounds like an honor, and in a sense it was. But the DAX carried a rule with an ugly side effect: no single stock was permitted to exceed a 10% weighting in the index. Every time Linde's shares performed well — which was often — its index weight bumped against that ceiling, and the passive funds that mechanically track the DAX were forced to sell Linde shares to stay in compliance. The company was being punished for success. Its own strong performance generated a steady stream of technical, non-fundamental selling pressure, an artificial headwind blowing against the stock for reasons that had nothing to do with the business.

In early 2023, management proposed a radical fix: leave Germany entirely. Linde would delist from the Frankfurt Stock Exchange and consolidate into a sole listing on the New York Stock Exchange. Shareholders approved the reorganization in January 2023, and the delisting from Frankfurt was completed on March 1, 2023.[^4][^5] In Germany, the decision landed as something close to a national insult — the country's most valuable listed company was walking out the door. But the corporate logic was hard to argue with. A single US listing eliminated the cost and complexity of maintaining parallel accounting and reporting regimes, removed the DAX weighting-cap selling pressure at a stroke, and repositioned Linde to be valued alongside premium American industrial compounders rather than as a European chemicals name.

The German reaction is worth sitting with, because it captures a genuine tension in how different capital markets value the same asset. To German commentators, Linde's departure was a symbol of something larger — a fear that the country's premier companies were being pulled toward American markets that would pay more for them, hollowing out the domestic exchange. And they were not wrong about the economics: part of Linde's own rationale was that a US listing would attract a valuation premium relative to what European investors would pay for identical cash flows. That premium is real, and it is a recurring feature of global markets, where American investors have historically been willing to pay more for high-quality compounders than their European counterparts. Whether that premium reflects deeper, more liquid capital markets and a more equity-friendly investor base, or simply a mood that could one day reverse, is a question the bear case will return to. Linde's management, characteristically, did not wait to resolve the philosophical debate; it acted on the arithmetic in front of it.

The bears predicted chaos — a wave of forced "flow-back" selling as European index funds, no longer able to hold a non-DAX stock, dumped their shares. That selling did materialize, but it was absorbed with striking ease by global capital, and the feared dislocation proved brief. In the years since, Linde's valuation multiple expanded as it took its place among the highest-quality industrials on the US market. For a management team, it was a clarifying demonstration of priorities: they were willing to absorb a political firestorm and sever a century-old tie to their founding country because the math for shareholders was unambiguous. That same clarity — a willingness to do the unsentimental thing when the returns demand it — is the throughline that connects this decision to the people now running the company.

VI. Current Management, Incentives, and Capital Allocation

If you wanted to design a CEO to run a business built on discipline, you might build someone like Sanjiv Lamba. Born and educated in India, Lamba joined the Linde organization in 1989 and spent more than three decades climbing through its operations across Asia and beyond — a genuine company lifer who absorbed the culture rather than importing it.1 He took over as chief executive in March 2022, and on January 31, 2026, he assumed the additional role of chairman of the board following the retirement of Steve Angel after twenty-five years with the company and its predecessor.1 Combining the chairman and CEO roles is a governance choice that some investors instinctively dislike, because it concentrates power and weakens board oversight; Linde's board framed it as the most effective structure for the company at this time.1 A skeptic is entitled to keep an eye on it.

Lamba's ascent also says something about how deep the operating culture now runs. He is not an American Praxair transplant imposing discipline on a foreign body; he is an India-raised, Asia-forged executive who rose inside the combined organization and internalized the Praxair religion as his own. When Steve Angel handed over the CEO role in 2022 and then the chairmanship in 2026, the continuity was seamless precisely because the framework had become bigger than any individual. Alongside the leadership transition, Linde appointed Sean Durbin, a thirty-year company veteran, as chief operating officer effective October 2025 — a move that placed a deep operational hand beneath the newly combined chairman-CEO and signaled that the day-to-day discipline would not slacken as roles consolidated at the top.1 For a business whose entire edge is execution rather than invention, the depth of the operating bench is a genuine competitive asset, and the fact that the succession involved no external star hire is a quiet vote of confidence in the system the company has built.

What Lamba has not done is deviate from the playbook, and the results so far support the case that the discipline is institutional rather than personal. Under his leadership the operating margin has pushed to 30% and return on capital has reached a best-in-class 24%.[^2] On the first-quarter 2026 earnings call, Lamba framed the quarter around exactly those three numbers — 10% EPS growth, a 30% operating margin, and 24% return on capital — and pointedly noted they were delivered "under increasingly challenging global conditions," a tell that management sees the growth as self-generated through pricing and productivity rather than handed to it by a booming economy.4

The incentive structure explains a great deal about the behavior. Linde's annual bonus plan is weighted heavily toward core profitability and execution rather than empire-building: net income carries the largest weight at 55%, operating cash flow 25%, and sales just 20%. The message embedded in that design is that growing revenue for its own sake earns you almost nothing; converting it to profit and cash earns you everything. The long-term incentive program reinforces the point, with roughly half of the awards taking the form of performance share units measured over a three-year period and split between two metrics that a capital-discipline zealot would choose: return on capital, which rewards squeezing more profit from every dollar of assets, and relative total shareholder return against a global peer group, which rewards actually beating the alternatives rather than merely rising with the market. You tend to get the behavior you pay for, and Linde pays for efficiency and outperformance, not for size.

That philosophy shows up most clearly in capital allocation, where Linde runs what it likes to call a "fortress balance sheet." The company generates far more cash than it can reinvest at its required returns, and it disposes of the surplus with metronomic consistency. In the first quarter of 2026 alone, Linde repurchased $800 million of stock and lifted its quarterly dividend by 7%, to $1.60 per share, extending its streak to 33 consecutive years of dividend increases — a record that spans multiple recessions, the merger, and the Frankfurt exit.[^2]3 Including dividends, the company returned roughly $1.5 billion to shareholders in that single quarter.[^2] The disciplining mechanism behind all of it is a strict double-digit return hurdle on growth capital expenditure: management's stated position is that it will simply not fund a project that fails to clear the bar, and it would rather hand the cash back than chase low-return volume.

This is where an analyst should apply pressure rather than take management at its word, because "we maintain capital discipline" is the most common and least verifiable claim in all of corporate finance. The way to test it is not to listen to the rhetoric but to watch the behavior across cycles. On the discipline side of the ledger: Linde has raised its dividend for 33 straight years, expanded margins essentially every year, and kept its return on capital roughly double its nearest peer's — outcomes that are extraordinarily hard to fake over three decades and multiple management teams.[^2]3 On the skeptic's side of the ledger: the ultimate stress test of capital discipline is not what a company does when returns are easy, but what it does when a shiny new growth narrative tempts the whole industry to overspend. Linde is living through exactly such a moment now, in clean energy, and the honest verdict is that the discipline has so far held — but the test is ongoing, not passed. The credibility of the claim is the thing to watch, and the cleanest place to see it play out is in the arena where a rival made the opposite bet and paid dearly.

VII. The Battle of the Giants: Linde plc vs. Air Products vs. Air Liquide

To see how Linde's discipline translates into an empire, it helps to walk the map segment by segment, because the company reports its world in four pieces and each tells a different story.

The Americas are the crown jewel, generating full-year 2025 sales of roughly $15.2 billion and operating profit of about $4.7 billion — an operating margin near 31%.[^1] This is Praxair's home turf, and it shows: dense route networks, extensive pipeline systems threaded through the US Gulf Coast chemical corridor, and the highest structural profitability in the company. EMEA — Europe, the Middle East, and Africa — produced about $8.5 billion in sales and roughly $3.1 billion in operating profit, an eye-catching margin near 36%.[^1] That EMEA is Linde's most profitable region on a margin basis, despite Europe's sluggish industrial growth, is the single clearest piece of evidence that the post-merger surgery on legacy Linde AG assets worked: those were precisely the underperforming, over-invested businesses that Praxair's framework was imposed upon.

APAC — Asia Pacific — delivered around $6.7 billion in sales and $1.9 billion in operating profit.[^1] This is the growth engine, anchored in India and China and wired directly into the region's most demanding customers: the semiconductor fabs of 台湾積體電路製造 TSMC, which need ultra-high-purity gases delivered with zero interruption, and heavy industrial giants like 中国石化 Sinopec. The semiconductor relationship deserves a moment, because it is where the switching-cost moat is at its most extreme. A modern chip fab consumes vast quantities of ultra-high-purity nitrogen, oxygen, argon, and specialty gases, and a supply interruption of even minutes can ruin batches of wafers worth enormous sums. So the gas supplier is typically embedded on-site under a long-term contract, its equipment woven into the fab's own infrastructure, its reliability record a precondition of even being considered. As the world races to build new fabs — in Taiwan, in the United States under subsidy programs, across Asia — each new plant is a decades-long annuity for whichever gas company wins it, and the incumbents' reliability records make them very hard to dislodge. The semiconductor build-out is one of the genuine secular tailwinds beneath Linde's APAC and Americas growth, and unlike hydrogen it is already large, already contracted, and already paying. Finally, Engineering — the descendant of Carl von Linde's original machine shop — generated about $2.25 billion in sales at a lower margin near 18%.[^1] Judged as a standalone business, Engineering looks unremarkable. Judged strategically, it is quietly essential: it designs and builds the proprietary, highly efficient ASUs that Linde then owns and operates, giving the company a vertical-integration advantage rivals must buy from third parties.

Now the war game. The global industry has consolidated into a three-player oligopoly, and each player embodies a different philosophy. Air Liquide, the French national champion, is a formidable and resilient business, but it has historically earned lower returns on capital — a return on capital employed around 11% in 2025 — reflecting a heavier tilt toward large industrial engineering and European infrastructure projects, and arguably a less unsentimental approach to capital than Linde's.[^9] The gap between Air Liquide's ~11% and Linde's ~24% return on capital is the whole thesis rendered as a single comparison: same molecules, same physics, roughly double the capital efficiency.

The most instructive rivalry, though, is with Air Products & Chemicals, because it functions as a live experiment in what happens when an industrial gas company abandons the discipline. Where Linde insisted on contract-backing every dollar of growth capital, Air Products made an aggressive, first-mover bet on clean hydrogen, committing well over $15 billion to enormous, largely uncontracted green hydrogen "megaprojects," most famously the NEOM development in Saudi Arabia. The strategy was to build first and sign customers later, in the conviction that the hydrogen economy would arrive to fill the plants. It was a genuine philosophical fork in the road: build-it-and-they-will-come versus never-build-without-a-signed-buyer.

The market rendered its verdict. Through 2024 and into 2025, Air Products drew intense activist pressure. Elliott Investment Management disclosed a large stake and publicly criticized the company's megaproject spending, and D.E. Shaw pressed a similar case, targeting compressed margins, project delays, and the sheer scale of capital committed to projects without buyers.2 The activist critique was, at its core, an accusation that Air Products had forgotten the industry's oldest rule — that in a capital-intensive business, you contract the demand before you pour the concrete. Building a multibillion-dollar green hydrogen plant in the Saudi desert with no signed offtake was a bet not on the physics of hydrogen, which work fine, but on the arrival of a market and a subsidy regime that had not yet materialized on schedule. When the timeline slipped, the uncontracted capital sat idle, dragging down returns and inviting exactly the kind of shareholder revolt that discipline is meant to prevent. It was a cautionary tale delivered in real time, and it played directly to Linde's positioning.

Linde, by contrast, kept its clean-hydrogen ambitions strictly leashed to take-or-pay offtake — its roughly $400 million low-carbon ammonia and clean hydrogen investment in Louisiana, for instance, was anchored to contracted demand before the capital went out the door. The contrast is the cleanest possible evidence for the durability of Linde's culture: given the identical temptation of a hydrogen gold rush, one major peer chased it and got hammered by its own owners, while Linde declined and kept compounding. Discipline, it turns out, is most valuable precisely when everyone else is abandoning it.

There is a common myth worth puncturing here — the notion that because the three giants sell identical molecules through identical delivery modes, they are essentially interchangeable, and the industry is a commodity oligopoly where returns should converge. The numbers say otherwise. If the business were truly commoditized, Linde and Air Liquide would not earn returns on capital that differ by roughly a factor of two, and Air Products would not have been able to imperil its own returns through a single strategic choice. The reality is that the physics and the delivery modes are indeed identical, but the outcomes are dominated by decisions — which projects to fund, at what return hurdle, in which regions, under what contracts — and those decisions compound. In a business where the moat is local and the differentiation is managerial, the spread between the best and worst operator is not a rounding error; it is the whole story. That is precisely why the analytical work here is less about the industry and more about the discipline of the people running each company within it.

VIII. Hamilton Helmer's 7 Powers & Porter's 5 Forces Analysis

Strip away the corporate history and the segment tables, and the question an investor really wants answered is simple: what, precisely, stops someone from competing this away? Two analytical frameworks help name the moat with more rigor than "it's a good business."

Start with Hamilton Helmer's 7 Powers, of which Linde plausibly holds three. The first is scale economies expressed as route density — the merchant moat described earlier. Because gas is heavy and expensive to transport, the operator with the densest local network delivers at a structurally lower unit cost than any newcomer, and a new entrant cannot match that cost without first winning enough customers to build density, which it cannot do without already having the low cost. It is a chicken-and-egg trap that protects incumbents region by region. The second is high switching costs, which govern the on-site business. Once Linde's pipeline is physically welded into a customer's chemical plant or semiconductor fab, switching supplier means re-engineering critical infrastructure and risking an interruption to a gas supply whose failure can cost the customer millions of dollars an hour in ruined production. No purchasing manager volunteers for that risk to save a few percent. The third is a cornered resource in the form of pipeline rights-of-way: the dense pipeline grids Linde operates in corridors like the US Gulf Coast were assembled over decades and cannot be readily replicated, because acquiring new right-of-way through populated, regulated, environmentally sensitive land is now extraordinarily difficult. You cannot simply build a competing pipeline network next to Linde's; the permits alone would take a generation.

Porter's 5 Forces paints the same picture from the industry's angle. The threat of new entrants is extremely low: a modern ASU is a nine-figure capital commitment tied to specialized technology and long-dated contracts, and the density economics mean a subscale entrant loses money by construction. The bargaining power of buyers is limited for on-site and merchant customers, because gas is typically a small fraction of their total costs but an absolutely critical input — the classic "cheap but essential" position that gives the supplier pricing power, since no customer will fight over a line item that could shut their whole plant if it fails. The bargaining power of suppliers is close to nonexistent, for the delightful reason that the primary raw material is the atmosphere, which sends no invoice. The threat of substitutes is effectively nil — there is no substitute for oxygen in a steel furnace or nitrogen in a fab; the periodic table does not offer alternatives. And the intensity of rivalry is unusually rational: three global players competing chiefly on localized logistics rather than on price, because in a business of local monopolies, starting a price war in a region you already dominate is simply lighting your own margins on fire.

The honest caveat is that these powers are strong but not infinite. Route density protects the merchant and packaged business but does nothing to guarantee that management allocates the resulting cash well — the moat protects the castle, not the treasury. And switching costs lock in existing on-site customers but do not compel new capital projects to earn adequate returns. It is also worth naming the powers Linde does not rely on, because it clarifies what kind of business this is. There is essentially no brand power here in the consumer sense — no one pays a premium because the cylinder says Linde rather than a rival. Nor is there much in the way of counter-positioning, the power that lets a startup do something incumbents cannot copy without damaging their existing business; the three giants are structurally similar and compete on the same terms. What Linde has instead is the unglamorous trio of scale, switching costs, and cornered resources, reinforced by a process advantage in how efficiently it designs and runs its plants. This is not a business that wins through a single brilliant product or a viral network; it wins through the patient accumulation of thousands of local advantages and the discipline to price and operate them well. That is a less exciting story than a disruptive-technology narrative, but for a long-term holder it is a more reassuring one, because advantages built brick by brick over a century are correspondingly hard to tear down quickly.

The moat, in other words, explains why Linde's revenue is durable; it does not by itself explain the 24% return on capital. That number is a product of the moat plus the discipline — and discipline, unlike geography, is a choice that can be un-made. Which is exactly why the next chapter, on where Linde chooses to point its capital, matters as much as the moat itself.

IX. The Future Strategy & Risk Radar

The great temptation of the coming decade is hydrogen, and the great discipline is to size it honestly rather than romantically. Linde carries a sale-of-gas project backlog of roughly $7.1 billion — the pipeline of contracted plants that will convert into revenue over the next several years — and clean energy, meaning blue and green hydrogen plus carbon capture, represents the largest single growth theme within it. Management talks about clean hydrogen constantly, and for good reason: it is genuinely strategic to the core business and offers real long-term optionality if the energy transition accelerates.

It helps to demystify the jargon, because "clean hydrogen" covers two quite different things. Today almost all industrial hydrogen is "grey" — made by stripping it from natural gas in a process that emits large volumes of carbon dioxide. "Blue" hydrogen is the same process with the carbon dioxide captured and stored underground rather than released, which requires carbon-capture equipment bolted onto the plant. "Green" hydrogen skips fossil fuels entirely, using renewable electricity to split water into hydrogen and oxygen — cleaner, but far more expensive at current power prices and dependent on cheap renewable electricity that is not yet available everywhere. Carbon capture, the enabling technology for blue hydrogen and for cleaning up other industrial emissions, is itself a growth line for Linde, since separating and handling gases like carbon dioxide is precisely the company's core competence pointed at a new application. The strategic logic is sound: Linde already knows how to build and operate the gas infrastructure the energy transition will require, whichever color of hydrogen wins.

But strategic importance and current economic weight are two very different things, and conflating them is how investors get hurt. The materiality check is sobering in a useful way: clean hydrogen today represents less than 5% of Linde's total operating revenue. The overwhelming majority of the company's cash still comes from the century-old business of separating air and selling oxygen, nitrogen, and argon to steelmakers, chemical plants, hospitals, and fabs. Hydrogen is the call option; industrial gas is the bond. A reader who takes away only one thing from this section should take away this: Linde's near-term earnings will be determined by the boring core, not the exciting frontier, and any thesis that leans primarily on hydrogen is buying a story the numbers do not yet support.

That framing sets up the material risk radar. The first risk is energy and feedstock inflation. Air separation is enormously electricity-intensive — the whole business is essentially selling repackaged electricity in molecular form — so power prices are Linde's dominant variable cost. The contractual defense is the pass-through clauses embedded in on-site take-or-pay contracts, which shift energy costs to the customer. Those clauses are powerful, but they are not frictionless: when energy prices spike suddenly, particularly in Europe, there can be timing lags and volume effects as customers cut production, and the pass-through protects margin dollars better than it protects volumes.

The second risk is policy and subsidy exposure. Much of the clean-hydrogen opportunity depends on government incentives, and those incentives can move. Changes or rollbacks to US Inflation Reduction Act provisions supporting clean hydrogen would alter the returns on precisely the projects management is being careful to contract. Here Linde's discipline is itself the hedge — by refusing to build uncontracted capacity, it has far less stranded-asset risk than a peer that bet ahead of the subsidies — but a less generous policy backdrop still shrinks the size of the future prize. The third risk is the oldest one: industrial cyclicality. Merchant and packaged volumes track steel, chemicals, and general manufacturing output, so a sustained global industrial slowdown, especially a simultaneous one across Europe and Asia, would pressure the parts of the business least protected by long-term contracts. The take-or-pay on-site book is the ballast that keeps the whole thing steady through a downturn — but ballast dampens a storm, it does not repeal the weather.

What is striking, and worth crediting, is that Linde has been growing profits through a period of essentially flat underlying volumes. On the first-quarter 2026 call, management was explicit that the quarter's growth came from price attainment and productivity rather than from a robust industrial economy — volumes were roughly stable while margins and earnings rose.4 That is a double-edged fact for investors. On the bullish read, it demonstrates real pricing power and cost control: the company can compound earnings even when the macro environment offers no help, which is the hallmark of a business with genuine control over its own destiny. On the bearish read, it raises the question of what happens to the growth algorithm when the easy price and productivity gains eventually thin out, since a company cannot raise price faster than inflation forever, and volumes will need to do more of the work in the long run. The honest synthesis is that Linde's recent performance is a testament to operational skill operating against a weak demand backdrop — impressive, but not the same as riding a strong one, and investors should be clear-eyed about which they are paying for.

X. Playbook & Core Business Lessons

Step back from Linde the stock and consider Linde the case study, because a handful of transferable lessons fall out of this century-long story that apply well beyond industrial gas.

The first is that density is destiny. In any business where the product is heavy, perishable, or expensive to move relative to its value, national market share is close to a vanity metric. What actually determines profitability is local density — how many customers you serve within a tight delivery radius from a single facility. Linde does not win because it is the biggest gas company in America; it wins because it is the densest operator in hundreds of specific regions, each of which is effectively a separate contest. The strategic implication is that the right unit of analysis for a logistics-bound business is the region, not the nation, and the right growth strategy is to deepen your best regions before broadening into weak ones.

The second lesson is the power of the utility-contract model. Linde pairs enormous upfront capital expenditure — the nine-figure ASU — with fifteen-to-twenty-year take-or-pay contracts that pass through input costs. That combination transforms a scary, capital-intensive, cyclical-looking business into something closer to a regulated utility: predictable cash flows, structural inflation protection, and returns visible years in advance. The general principle is that heavy capital intensity is not inherently bad for shareholders; it is bad only when it is un-contracted. Marry the same capital to a long-dated, cost-protected contract, and the intensity becomes a moat rather than a liability, because it deters the very entrants who cannot secure equivalent contracts.

The third lesson is the most subtle and the most contested: cultural assimilation in M&A. The conventional wisdom is that "merger of equals" is a polite fiction and that most large mergers destroy value. Linde is the exception that proves the rule about why they fail. The 2018 combination created value not because two companies blended into a harmonious average, but because one operating culture — Praxair's margin obsession — was allowed to conquer the other and impose its standards on the whole. The lesson for acquirers is uncomfortable but clear: a successful merger of equals usually requires that one culture, quietly and decisively, stop being equal. Blending cultures produces mush; imposing the better one produces returns. Whether that is a repeatable formula or a one-time stroke of good fortune is exactly the debate that defines the bull and bear cases.

XI. The Bull vs. Bear Case & Key KPIs to Track

Lay the two cases side by side and the disagreement is not really about the business — both sides largely agree Linde is a superb operator. The disagreement is about price and about what could crack a machine that currently looks flawless.

The bull case rests on three pillars. First, Linde holds undisputed global leadership in a rational oligopoly, with a defensive, utility-like model insulated by route density, switching costs, and long-dated contracts — the powers detailed earlier. Second, it earns demonstrably superior returns: a 24% return on capital against roughly 11% for its nearest global peer is not a rounding error, it is evidence of a structurally better business, and it is backed by the pricing power to push margins to 30% even as global conditions toughen.[^2][^9] Third, the company offers contract-backed exposure to genuine secular tailwinds — the insatiable gas appetite of semiconductor fabs and the long, uncertain, but potentially enormous clean-energy transition — without the reckless capital commitments that sank a rival. The bull's Linde compounds cash at high returns, hands the surplus back through a 33-year dividend streak and steady buybacks, and lets time do the work.3

The bear case does not dispute the quality; it disputes what you pay for it. The central worry is valuation: after the Frankfurt exit and years of multiple expansion, Linde trades at premium multiples more reminiscent of a high-growth software company than an industrial that grows sales in the low-to-mid single digits. At that price, the stock has priced in near-flawless execution, leaving little cushion for a stumble — a missed margin target, a hydrogen project that disappoints, a policy reversal. The second bear pillar is cyclicality colliding with that rich multiple: a sustained industrial slowdown across Europe and Asia would hit merchant and packaged volumes and could compress both earnings and the premium multiple at the same time, a double hit.

Run the full activist stress test and a few more pressure points emerge, even against a company this well-run. On governance, the combination of the chairman and CEO roles in a single person removes the independent-chair check just as the last of the founder-era Praxair and Linde AG leadership departs — a reasonable board can defend the choice on grounds of execution continuity, but a skeptical investor is right to want a strong lead independent director and to watch that concentration of power. On the growth algorithm, a short-seller would zero in on exactly the point raised above: that recent earnings growth has leaned heavily on price and productivity against flat volumes, and would argue that the market is extrapolating a compounding rate that depends on conditions — pricing power ahead of a soft cost base — that may not persist indefinitely. On capital allocation, the bear would ask whether the clean-energy build-out, however carefully contracted today, will over a decade require the company to accept structurally lower-return projects to stay strategically relevant, quietly eroding the 24% return on capital that is the linchpin of the entire premium. None of these are accusations of mismanagement; Linde's execution record is, if anything, the strongest in its industry. They are the honest questions a disciplined skeptic would attach to a superb business trading at a price that leaves little margin for disappointment.

The reconciliation between the two cases is that both are, in a sense, correct: Linde is very likely to remain an excellent business and may still be a mediocre investment from an expensive entry point, or a fine one from a cheaper one. The framework here refuses to resolve that with a verdict, because the resolution depends on price, time horizon, and assumptions no one can prove in advance. What it can offer is a short, honest watch list — the metrics that will reveal, in real time, whether the machine is still running as advertised.

Three KPIs matter most. The first is operating margin expansion: the clearest single gauge of whether Linde is still extracting efficiencies, especially from the legacy Linde AG assets that were the whole point of the merger. Stalling or reversing margins would signal the discipline is fading. The second is return on capital: the number that separates Linde from its peers and the one most at risk from a hydrogen buildout, so the question to ask every year is whether new investment is holding the 24% line or quietly eroding it. The third is the sale-of-gas project backlog: at roughly $7.1 billion today, it is the leading indicator of top- and bottom-line growth over the next three-to-five years, and its mix — how much is high-return core gas versus lower-certainty clean energy — tells you where the company is really pointing its capital. Watch those three, and you are watching the actual thesis rather than the quarterly noise.

XII. Epilogue & Outro

There is a tidy symmetry to end on. Carl von Linde spent his life proving that you could reach into the air and pull out something valuable, and that the hard part was never the science but the logistics and the discipline to make the economics work. More than a century later, the company that bears his name has become one of the most efficient cash-compounding machines in global industry by holding to exactly that insight: the molecules are free, the moat is in the network, and the returns are in the refusal to waste capital.

The reunion of his divided house — German engineering and American operating rigor, torn apart by a world war and rejoined a century later — did not produce a gentle blending of the two. It produced a company where one culture's ruthless capital discipline was stamped onto the other's magnificent assets, and the result was a business that out-earns every peer selling the same invisible product. Whether that discipline survives the temptations of the next decade — the hydrogen gold rush, the pressure of a premium valuation, the concentration of power in a single chairman-CEO — is the open question that will define the next chapter of Carl von Linde's reunited family. The physics are settled. The compounding, as always, remains a matter of choices.

References

-

Linde Appoints Sanjiv Lamba as Chairman & CEO — Linde plc / Business Wire, 2025-10-23 ↩↩↩↩

-

Elliott Targets Air Products, Criticizing Megaproject Spending — Bloomberg, 2024-10-30 ↩

-

Linde Extends 33-Year Streak of Dividend Raises with 7% Hike — StockTitan, 2026 ↩↩↩

-

Linde (LIN) Q1 2026 Earnings Call Transcript — The Globe and Mail / The Motley Fool, 2026-05-01 ↩↩

-

About Linde — A Leading Global Industrial Gases and Engineering Company — Linde plc ↩↩↩

-

Linde plc Announces Satisfaction of Final Conditions to Close Business Combination between Linde AG and Praxair — Linde plc, 2018-10-31 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube