Centrus Energy Corp: The Last American in the Room

I. Introduction and Episode Roadmap

There is only one company in America that can enrich uranium using American-origin technology. One. In a world where energy security has become synonymous with national security, where artificial intelligence demands more electricity than entire nations consume, and where the specter of Russian dominance over nuclear fuel supply chains haunts Western policymakers, that single company is Centrus Energy Corp, trading on the NYSE under the ticker LEU.

Centrus reported revenue north of $440 million in 2025, holds roughly $2 billion in cash, and commands a backlog approaching $4 billion extending to 2040. Its stock swung from a 52-week low near $49 to a high above $464, a volatility band that reflects the market grappling with a deceptively simple question: Is this company building a multi-decade strategic asset that resurrects American nuclear leadership, or is it a government-funded experiment running on geopolitical hype?

The answer requires understanding how a Cold War relic, privatized in the late 1990s with aging infrastructure and a comfortable monopoly, nearly died twice before becoming indispensable. It requires following the threads of the Manhattan Project through Soviet warhead dismantlement, through billions in failed technology bets and a bankruptcy filing, all the way to an industrial facility in rural Ohio where sixteen centrifuges began spinning in late 2023, producing a material that no one else in the Western Hemisphere can make.

The themes that run through the Centrus story are the themes that define the current era: government entanglement with private enterprise, the weaponization of supply chains, technology moats in supposedly boring industries, and the collision of climate policy, artificial intelligence, and great-power competition. This is a company whose survival depended on being the last one standing when the world finally decided it needed what only they could provide.

The journey from government spin-off to bankruptcy to strategic indispensability is one of the most dramatic corporate survival stories in American industrial history. And it is far from over.

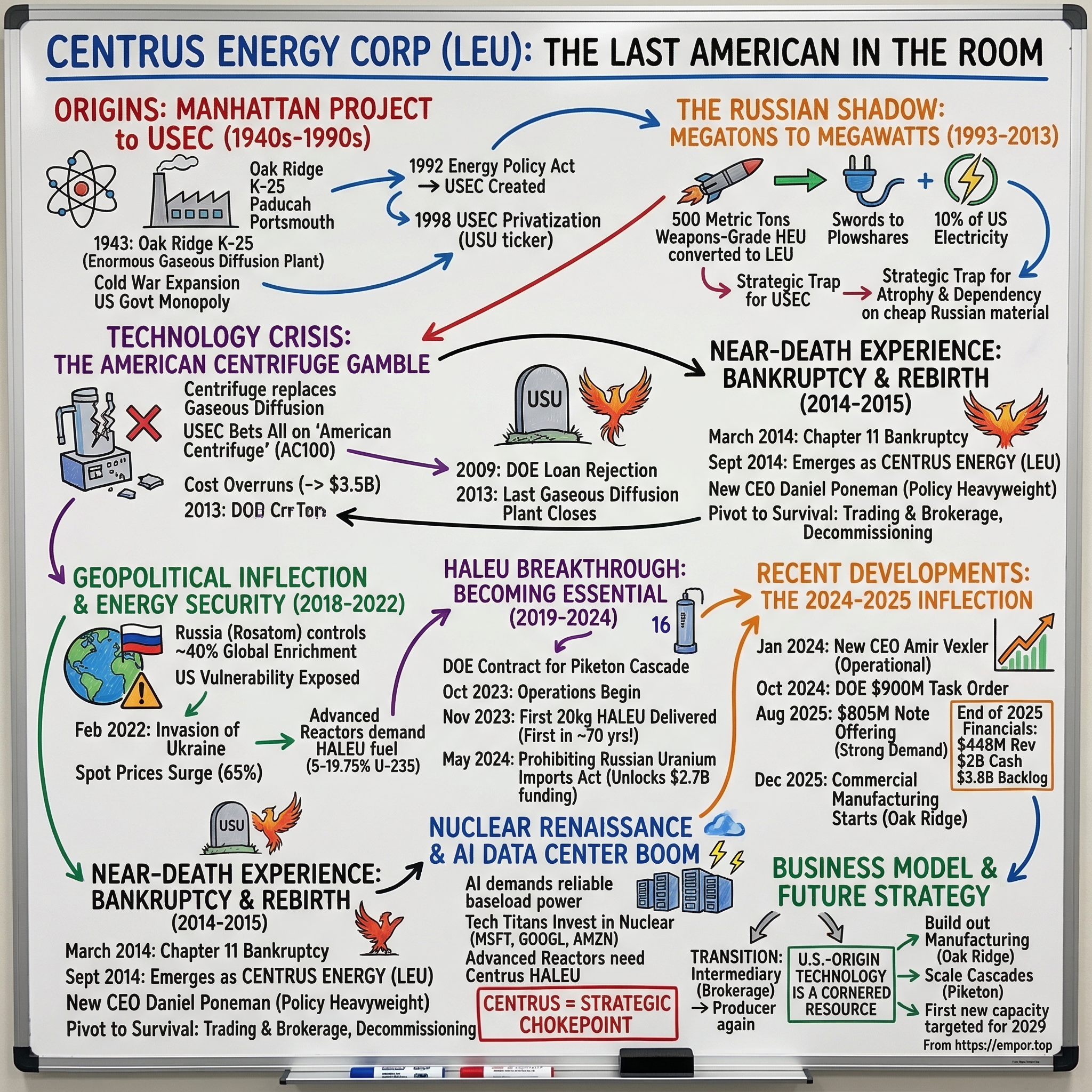

II. Origins: The Manhattan Project to USEC

Picture Oak Ridge, Tennessee in the summer of 1943. Thousands of construction workers swarm across a site that officially does not exist, building what would become the largest structure on Earth. The K-25 gaseous diffusion plant, a U-shaped behemoth measuring half a mile by a thousand feet, larger than the Pentagon, consumed over five million square feet of floor space. Its sole purpose was to separate the fissile isotope uranium-235 from the far more abundant uranium-238, a task that sounds simple in principle but required engineering on a scale the world had never attempted.

The physics are elegant but the engineering is brutal. Natural uranium contains only 0.7 percent of the fissile U-235 isotope. Nuclear reactors need fuel enriched to 3-5 percent U-235, while weapons require 90 percent or higher. The gaseous diffusion method works by converting uranium into a gas called uranium hexafluoride and forcing it through membranes containing millions of microscopic holes. The slightly lighter U-235 molecules pass through marginally faster than the heavier U-238 molecules, but the difference per pass is minuscule, roughly 0.43 percent. To achieve meaningful separation, the gas must cycle through hundreds or thousands of stages in an enormous cascade. Think of trying to sort slightly different-sized marbles by rolling them through a screen with tiny holes, over and over and over again, thousands of times, to get a useful separation.

K-25 was completed in early 1945 at a cost of $500 million, roughly $8 billion in today's dollars, employing 12,000 workers. The enriched uranium it produced fueled "Little Boy," the bomb dropped on Hiroshima. The enrichment program had proven its strategic value in the most decisive way imaginable.

During the Cold War, the government expanded the enrichment complex. The Paducah Gaseous Diffusion Plant in Kentucky began operating in 1952, and the Portsmouth plant near Piketon, Ohio followed in 1954. Together, these three facilities formed America's enrichment backbone, initially producing weapons-grade material and later shifting to commercial reactor fuel as the nuclear power industry grew in the 1960s and 1970s. For decades, the U.S. government held a virtual monopoly on Western enrichment services. The technology was too strategic, too capital-intensive, and too entwined with national security to hand over to private enterprise.

Then came the post-Cold War rethink. By the late 1980s, the U.S. enrichment enterprise's global market share had eroded from near-monopoly to less than half, as European competitors, particularly the URENCO consortium, developed more efficient centrifuge technology. Congressional leaders began pushing for privatization, arguing that a government-run operation could not compete in a globalizing market.

The Energy Policy Act of 1992 created the United States Enrichment Corporation, or USEC, as a wholly owned government corporation on July 1, 1993. Three years later, the USEC Privatization Act of 1996 set the stage for a full initial public offering. On July 28, 1998, USEC completed its IPO on the New York Stock Exchange under the ticker USU, returning approximately $1.9 billion to the U.S. Treasury.

What the new shareholders inherited looked promising on the surface: two operating enrichment plants, an established customer base of nuclear utilities worldwide, and a position as the dominant Western enrichment provider. What they actually got was a company running Cold War-era technology that consumed staggering amounts of electricity, facing increasingly efficient foreign competitors, and about to become dependent on a geopolitical arrangement that would quietly hollow out American enrichment capacity from the inside.

III. The Russian Shadow: Megatons to Megawatts

When the Soviet Union collapsed, one of the most terrifying questions facing the world was deceptively simple: What do you do with 20,000 nuclear warheads that suddenly belong to a disintegrating superpower with an imploding economy?

The answer was one of the most remarkable nonproliferation achievements in history. In February 1993, the United States and Russia signed the HEU Purchase Agreement, commonly known as "Megatons to Megawatts." The concept was elegant in its simplicity: take weapons-grade highly enriched uranium from dismantled Russian warheads, blend it down to low-enriched reactor fuel, and sell it to American nuclear power plants. Swords into plowshares, literally.

The mechanics worked through a commercial implementing contract signed in January 1994 between USEC, designated as the U.S. executive agent, and TENEX, the Russian state nuclear fuel company. Russia would downblend weapons-grade HEU, enriched to roughly 90 percent U-235, into LEU below 5 percent at its own facilities. The resulting material was shipped to the United States, where USEC marketed and sold it to utilities. Russia received payment for the separative work units embedded in the material, plus equivalent amounts of natural uranium.

Over twenty years, the program converted 500 metric tons of weapons-grade HEU, the equivalent of approximately 20,000 nuclear warheads, into commercial reactor fuel. At its peak, roughly 10 percent of all electricity generated in the United States came from fuel derived from former Soviet weapons. There is something profound and slightly surreal about the idea that the lights in American homes were powered by material originally designed to destroy American cities.

For USEC, the Megatons to Megawatts program was a commercial goldmine and a strategic trap simultaneously. The company earned substantial revenue as the middleman, purchasing Russian-origin enrichment services at competitive prices and reselling them to U.S. utilities. But the program created a devastating dependency. Why invest billions to develop new enrichment technology or maintain aging domestic plants when cheap Russian material was flowing in reliably? The economics were irresistible in the short term and catastrophic in the long term.

Throughout the 2000s, as the program pumped Russian-origin fuel into the American market, USEC's own enrichment infrastructure atrophied. The gaseous diffusion plants were energy hogs, consuming roughly 2,500 kilowatt-hours per SWU compared to approximately 50 kilowatt-hours for modern centrifuges, a 98 percent difference in energy efficiency. The Paducah plant alone consumed about 3,000 megawatts of electricity, roughly the output of three large nuclear power plants, just to enrich uranium. Competing against European centrifuge technology on cost was nearly impossible. Competing against cheap Russian supply was completely impossible.

The business model problem was more subtle than simple dependency. USEC was essentially a middleman selling someone else's product. The company did not produce the enrichment services it sold to utilities. It purchased blended-down Russian material at negotiated prices and marketed it in the American market. As long as the Russian material was available and competitively priced, USEC's margins were comfortable and its customers were happy. But the company was not building any durable competitive advantage. It was not investing in next-generation technology. It was not developing its own production capability. It was clipping a coupon on a geopolitical arrangement that had an expiration date printed clearly on it.

The agreement was scheduled to conclude in December 2013, and everyone knew it. When the final shipment arrived and the program officially ended that December, 500 tonnes of weapons material had been peacefully converted, enough for roughly 20,000 warheads, powering millions of American homes for two decades. It was a triumph of diplomacy and pragmatism. But for USEC, it was the end of the revenue stream that had masked the company's fundamental vulnerability. Without Russian material to sell, USEC would be left with obsolete technology, crumbling infrastructure, and a market that had moved on. The company needed a technological lifeline. It bet everything on one.

IV. Technology Crisis: The American Centrifuge Gamble

The centrifuge is to gaseous diffusion what the jet engine was to the propeller: a fundamentally superior technology that achieves the same result with dramatically less energy. Instead of forcing gas through membranes thousands of times, a centrifuge spins uranium hexafluoride gas at 50,000 to 70,000 revolutions per minute inside a tall, thin cylinder. The heavier U-238 molecules are flung toward the outer wall by centripetal force, while the lighter U-235 molecules concentrate near the center. A scoop system extracts the enriched stream from the center and the depleted stream from the wall. Imagine a salad spinner: put in a mixture of heavy and light items, spin it hard enough, and the heavy ones fly to the outside while the light ones stay near the center.

By the early 2000s, every major enrichment competitor had moved to centrifuge technology. URENCO, the European consortium owned jointly by the UK, Netherlands, and Germany, had been perfecting centrifuges since the 1970s and operated highly efficient plants across Europe and, beginning in 2010, in Eunice, New Mexico. Orano, the French nuclear giant, had built the massive Georges Besse II centrifuge plant to replace its own aging gaseous diffusion facility. Russia's Rosatom operated the world's largest centrifuge capacity, over 27 million SWU per year across four plants. USEC was the last major enricher still running gaseous diffusion, a technology the rest of the world had abandoned.

USEC's answer was the American Centrifuge, a program that drew on centrifuge R&D the U.S. government had pursued and then shelved in the 1980s. The backstory of that shelved program is itself revealing. During the late Cold War, the Department of Energy had invested significantly in gas centrifuge technology, building pilot facilities and developing prototype machines. But the program was canceled in 1985, partly because gaseous diffusion plants were still meeting demand and partly because the government was shifting focus to laser enrichment, another promising but ultimately unsuccessful technology bet. The centrifuge R&D was mothballed, the scientists dispersed, and the knowledge was filed away in classified archives.

Two decades later, USEC resurrected this work. The vision was ambitious: develop the AC100 centrifuge, a machine designed to leapfrog existing European and Russian designs with superior performance per machine. The company planned a massive commercial plant at Piketon, Ohio, using infrastructure from the old Portsmouth gaseous diffusion facility. If successful, it would restore American enrichment competitiveness in one bold stroke.

The initial capital cost estimate was $1.7 billion, with commercial operations expected by 2005. Within three years, costs had risen to $2.3 billion and the timeline had slipped to 2009. By February 2008, the price tag had ballooned to $3.5 billion, more than double the original estimate. USEC applied for a $2 billion DOE loan guarantee in 2008, arguing the project was critical to national energy security and could not proceed without government backing.

The Department of Energy was not convinced. In 2009, DOE officials asked USEC to withdraw its application, delivering a devastating assessment: the project "runs the risk of either major cost overruns or technological reliability problems or both." A DOE review noted that USEC had tested only 38 centrifuge machines out of the 11,000 needed for the full plant. The rejection triggered a financial meltdown. Over 1,300 project jobs were eliminated immediately, with thousands more indirect positions lost throughout the supply chain.

USEC tried to soldier on with a smaller demonstration program. In 2010, the company began operating a test cascade of AC-100 machines at a lead cascade facility in Piketon. Then, in April 2012, the Nuclear Regulatory Commission reported that six of the 38 test centrifuges had "crashed" during routine testing, setting the program back $9 million and reinforcing doubts about commercial viability.

Meanwhile, the last gaseous diffusion plant at Paducah ceased enrichment operations in May 2013 for economic reasons, making it the last gaseous diffusion plant to operate anywhere in the world. USEC now had no operating enrichment capacity, its next-generation technology remained unproven, and its primary revenue source, the Megatons to Megawatts program, concluded on schedule in December 2013.

The convergence was devastating. In the span of roughly eighteen months, USEC lost its enrichment capacity (Paducah closing), its primary revenue source (Megatons to Megawatts ending), and its technology pathway (American Centrifuge failing to achieve commercial viability). The company that had been handed a near-monopoly at privatization had managed to lose every competitive advantage it possessed. It was a case study in how government-sponsored enterprises can squander inherited advantages when competitive pressures are deferred rather than confronted.

The company that had once been America's enrichment monopoly was running out of everything: technology, revenue, and time.

V. Near-Death Experience: Bankruptcy and Rebirth

By early 2014, USEC was a company defined by what it had lost. No enrichment capacity. No proven next-generation technology. No primary revenue source. What it did have was $530 million in debt maturing in October 2014, plus $114 million in preferred stock held by Toshiba and Babcock & Wilcox, strategic investors who had bet on the American Centrifuge and lost. Global uranium and SWU prices had collapsed in the aftermath of the 2011 Fukushima disaster in Japan, which triggered reactor shutdowns worldwide and cratered demand for enrichment services. The market that USEC needed to save it had moved decisively against it.

In March 2014, USEC filed for Chapter 11 bankruptcy protection, one of the rare instances of a former government monopoly going bankrupt within two decades of privatization.

The restructuring was prearranged, meaning USEC had already negotiated a plan with major creditors before filing. The court confirmed a plan that slashed $530 million in old debt to $240 million in new obligations. Noteholders received the bulk of the new debt plus approximately 79 percent of new common stock. Toshiba and Babcock & Wilcox each received about $20 million in new debt and roughly 8 percent of equity. Previous common shareholders, whose investments were effectively wiped out, received approximately 5 percent of the restructured company. On September 30, 2014, the company emerged from bankruptcy with a new name, Centrus Energy Corp, and began trading under the ticker LEU.

What remained after the restructuring was modest: a small portfolio of LEU supply contracts, enrichment inventory purchased from foreign suppliers for resale, intellectual property related to the American Centrifuge, and critically, relationships with the Department of Energy. The company had no operating enrichment capacity and no clear path back to large-scale production.

In March 2015, the board appointed Daniel B. Poneman as President and CEO, a choice that signaled where the company's future lay. Poneman was not a corporate turnaround specialist. He was a nuclear policy heavyweight. A Harvard and Oxford-educated lawyer, he had served on the National Security Council under Presidents George H.W. Bush and Clinton, working on nonproliferation and arms control. Most significantly, he had served as the Deputy Secretary of Energy, the number-two position at DOE, under President Obama from 2009 to 2014. He had even served briefly as Acting Secretary of Energy. Poneman's Rolodex read like a who's-who of Washington energy and national security policymaking. He had co-authored a book on the North Korean nuclear crisis with former National Security Advisor Brent Scowcroft. If anyone understood the intersection of nuclear technology, government contracting, and national security policy, it was Poneman.

Under his leadership, Centrus pivoted from aspiring commercial enricher to a company that survived by doing three things: trading and brokering enrichment services by purchasing SWU from foreign enrichers like URENCO and TENEX and reselling to American utilities; performing decontamination and decommissioning work at the Paducah site, turning the cleanup of the old gaseous diffusion plant into a revenue source; and preserving the American Centrifuge technology through DOE-funded R&D contracts, keeping the intellectual capital alive until the world might need it again.

It was a lean, unglamorous existence. Revenue was a fraction of what USEC had generated in its heyday. The workforce was drastically reduced. The grand ambitions of a commercial centrifuge plant had been replaced by the modest reality of government R&D contracts and enrichment brokerage. Wall Street, to the extent it noticed Centrus at all, viewed it as a zombie company, a relic of a failed privatization with no clear path to relevance.

But Centrus held onto the one asset that would eventually prove priceless: it remained the custodian of the only U.S.-origin, deployment-ready uranium enrichment technology. The engineers who had built and tested the American Centrifuge machines were still there, or could be brought back. The manufacturing knowledge was documented. The NRC licenses were maintained. The Piketon facility, though largely dormant, was still a permitted, secured nuclear site. In an industry where creating these capabilities from scratch takes a decade or more, preserving them, even in mothballed form, was an act of strategic patience that would prove visionary.

The company had survived the valley of death. Now it needed the world to change.

VI. Geopolitical Inflection: Russia, China, and Energy Security

The world changed slowly, then all at once. Throughout the late 2010s, a growing chorus of national security analysts, congressional staffers, and DOE officials raised alarms about a vulnerability that had been building for decades. Russia's Rosatom controlled approximately 40 percent of global uranium enrichment capacity. Its four enrichment plants across Russia produced over 27 million SWU per year, dwarfing any single competitor. When you added Russia's dominance in uranium conversion services, roughly a third of global supply, the picture was stark: the Western nuclear fleet depended on a geopolitical adversary for a critical input.

The concentration was not accidental. Russia had invested heavily in centrifuge technology throughout the Cold War and maintained that investment after the Soviet collapse, while Western nations allowed their enrichment infrastructure to atrophy. The Megatons to Megawatts program, for all its nonproliferation achievements, had effectively subsidized this outcome by flooding the Western market with cheap Russian material and removing the economic incentive for domestic enrichment investment.

In 2018, the Trump administration launched a Section 232 investigation into whether uranium imports constituted a national security threat. The investigation highlighted the supply chain vulnerability, but nuclear utilities, which had been buying cheap Russian fuel for decades and had no appetite for more expensive domestic alternatives, lobbied aggressively against import restrictions. The administration ultimately established a small uranium reserve program but stopped short of the sweeping import restrictions that advocates sought. The nuclear fuel market's structure, dominated by cost-conscious utilities locked into long-term contracts, made rapid change politically difficult.

Meanwhile, China was emerging as a new variable in the equation. The China National Nuclear Corporation had been steadily expanding enrichment capacity, and Beijing was building nuclear reactors at a pace unmatched anywhere in the world. The implications for global enrichment markets were troubling. Flow data would later show a pattern described as "displacement exchanges," where China increased imports of Russian enriched uranium to fuel its domestic reactors, freeing Chinese enrichment capacity for export to Western markets unconstrained by sanctions. The Russia-China nuclear fuel axis was becoming a structural feature of global energy markets, not a temporary inconvenience.

Then came the events that transformed the conversation entirely. Russia's invasion of Ukraine in February 2022 ripped away any remaining illusions about the reliability of Russian supply chains. Spot prices for enrichment services climbed 65 percent as buyers scrambled to diversify. Paradoxically, some European utilities initially increased Russian purchases in 2022, buying 30 percent more conversion services and 22 percent more enrichment from Russia to build strategic inventories amid the uncertainty. Five EU countries operating Russian-designed reactors, Bulgaria, Czech Republic, Finland, Hungary, and Slovakia, remained particularly exposed.

Within this shifting landscape, a new fuel requirement was emerging that would prove even more consequential for Centrus than the broader Russian supply chain concerns. Advanced reactor designs, small modular reactors, microreactors, high-temperature gas reactors, required a fuel that conventional reactors did not: High-Assay Low-Enriched Uranium, or HALEU.

Traditional reactor fuel is enriched to 3-5 percent U-235. HALEU is enriched to between 5 and 19.75 percent, well below weapons-grade but far beyond what conventional enrichment services typically produce. Nine out of ten reactor designs selected by DOE's Advanced Reactor Demonstration Program required HALEU. And in 2019, there was exactly zero domestic HALEU production capacity. The only source was Russia.

Centrus, which had been quietly maintaining its American Centrifuge technology through lean years of DOE R&D contracts, won a critical contract in 2019 to license and construct a cascade of 16 advanced centrifuges at Piketon to demonstrate HALEU production. Sixteen machines. Not eleven thousand, the number the original commercial plant would have required. Sixteen. It was a demonstration-scale project, modest in scope but enormous in significance, because it represented the first step back from the brink.

The timing was not coincidental. The DOE was watching advanced reactor developers submit designs that required HALEU fuel, while simultaneously recognizing that the only existing supply came from Russia. The strategic absurdity of this situation, developing American reactors that could only be fueled by a Russian adversary, concentrated minds in Washington. Centrus, with its preserved technology and its Piketon facility already licensed for enrichment operations, was the logical, indeed the only, domestic option.

The company that nearly died in 2014 was being asked to do the one thing no one else in the Western Hemisphere could: produce enriched uranium at HALEU levels using domestic technology.

VII. The HALEU Breakthrough: Becoming Essential Again

To understand why HALEU matters, consider the difference between a Honda Civic and a Formula One car. Both burn gasoline, but they are designed for fundamentally different performance envelopes. Traditional light-water reactors, the workhorses of the current nuclear fleet, run on fuel enriched to 3-5 percent U-235. They are big, they work well, and they have been reliably generating power for decades. But the next generation of reactors, small modular reactors from companies like NuScale, high-temperature gas reactors from X-energy, molten salt reactors from Kairos Power, sodium-cooled fast reactors from TerraPower, are designed for different missions: smaller footprints, longer operating cycles, higher efficiency, and deployment in locations where a traditional gigawatt-scale plant would be impractical.

These advanced designs achieve their advantages by using fuel enriched to higher levels, between 5 and 19.75 percent U-235, which is HALEU. The higher enrichment allows reactor designers to use smaller cores, extend refueling intervals, and achieve better fuel utilization. Think of it as higher-octane fuel enabling a more powerful, more efficient engine.

The problem was that HALEU production sat in a dead zone. It was above the enrichment level that commercial enrichment plants routinely produced, so no Western facility was configured to make it. But it was well below weapons-grade, which starts at 20 percent and runs to 90-plus percent, so it was not a weapons proliferation issue in the traditional sense. Russia happened to have the capability because its military enrichment infrastructure could easily produce material at any enrichment level. For years, the small quantities of HALEU needed for research came from Russian sources. Nobody else bothered to build the capability because demand was negligible.

Then advanced reactor development accelerated, and suddenly HALEU was not a research curiosity but an industrial necessity. The entire next-generation nuclear renaissance depended on a fuel that only Russia could supply. The irony was almost too perfect: the United States was investing billions to develop advanced nuclear reactors while remaining completely dependent on a geopolitical adversary for the fuel to run them.

Centrus's 16-centrifuge cascade at Piketon became the answer to this problem. In October 2023, the company began enrichment operations, two months ahead of schedule. In November 2023, Centrus delivered its initial 20 kilograms of HALEU to the Department of Energy, completing Phase I of its production contract. This made the American Centrifuge Plant the first U.S.-owned, U.S.-technology enrichment plant to begin production in roughly 70 years.

Phase II called for production and delivery of 900 kilograms of HALEU by June 30, 2025. Centrus delivered over 920 kilograms, completing the milestone on time. It was a small quantity by commercial standards, but it proved something enormously important: the American Centrifuge technology, which had been through decades of development, billions in spending, mechanical failures, a bankruptcy, and near-cancellation, actually worked.

Meanwhile, the legislative environment was shifting dramatically in Centrus's favor. In May 2024, President Biden signed the Prohibiting Russian Uranium Imports Act into law. The ban took effect on August 11, 2024, prohibiting imports of Russian LEU with limited waivers available through January 1, 2028, subject to declining annual caps. More importantly, the law unlocked $2.72 billion in federal funding that Congress had appropriated for domestic enrichment capacity expansion but had conditioned on restricting Russian imports. Approximately $2 billion was designated for LEU enrichment capacity expansion and $700 million for HALEU specifically.

Russia responded in November 2024 with its own retaliatory ban on enriched uranium exports to the United States, though with notable loopholes allowing individual license approvals to continue some trade. The mutual bans created exactly the kind of supply disruption that Centrus was positioning itself to fill.

The Inflation Reduction Act and bipartisan infrastructure legislation had already directed billions toward nuclear energy and the domestic fuel cycle. The government was becoming both the primary customer and the primary funder of American enrichment revival. For Centrus, the convergence of HALEU production capability, Russian import restrictions, and massive federal investment had transformed its competitive position from marginal survivor to strategically indispensable.

VIII. Recent Developments: The 2024-2025 Inflection

The period from mid-2024 through early 2026 represented the most consequential transformation in Centrus's history. Every few months brought an announcement that would have been unthinkable during the company's near-death years.

On January 1, 2024, Amir Vexler succeeded Daniel Poneman as CEO. The transition was significant in its own right. Where Poneman was a policy intellectual who navigated Centrus through survival, Vexler was an operational executive shaped by twenty years at General Electric, including running Global Nuclear Fuels, the GE-Hitachi joint venture. He had also served as President and CEO of Orano USA, the U.S. arm of the French nuclear fuel giant. Vexler's appointment signaled that Centrus was transitioning from a company that needed to navigate Washington to one that needed to build industrial-scale operations. The survival phase was over. The building phase had begun.

In October 2024, the DOE announced the selection of companies for up to $2.7 billion in future HALEU and LEU enrichment task orders. Centrus's subsidiary, American Centrifuge Operating, received one of three task orders worth up to $900 million each for domestic enrichment capacity. The other recipients were General Matter for HALEU enrichment and Orano Federal Services for LEU enrichment. These were not grants but potential contract values contingent on task order awards and congressional appropriations, yet they represented the most significant government commitment to domestic enrichment in decades.

In November 2024, Centrus raised $350 million through convertible senior notes due 2030, carrying a 2.25 percent coupon and an initial conversion price around $97.50 per share. The offering was driven by the need to fund the capital-intensive expansion ahead.

Then came the August 2025 blockbuster: an $805 million offering of zero-coupon convertible senior notes due 2032, upsized from an initial $650 million due to overwhelming investor demand. The initial conversion price was approximately $229.62 per share, reflecting a 22.5 percent premium over the stock's trading price. Net proceeds of $782 million were designated for general working capital, technology development, debt repurchase, capital expenditures, and potential acquisitions.

In June 2025, Centrus completed Phase II of its HALEU contract, delivering over 920 kilograms to the DOE. The DOE exercised a one-year extension option, kicking off Phase III with continued HALEU production through June 2026, with options for up to eight additional years of production beyond that.

In August 2025, Centrus signed a memorandum of understanding with Korea Hydro & Nuclear Power, the world's third-largest nuclear plant operator with 26 reactors, and POSCO International, a major Korean trading and energy infrastructure company developing a next-generation high-temperature gas reactor powered by HALEU. The MOU explored potential Korean investment to support expansion of the Piketon enrichment plant. U.S. Secretary of Commerce and Korea's Minister of Trade attended the signing ceremony, underscoring the geopolitical significance.

The capstone came in December 2025, when Centrus announced it had begun commercial centrifuge manufacturing at its Technology and Manufacturing Center in Oak Ridge, Tennessee, the only uranium enrichment centrifuge manufacturing facility in the United States. The company disclosed plans to invest more than $560 million over several years to expand the facility, creating nearly 430 new jobs in Anderson County, Tennessee. First new production capacity was targeted for 2029.

The Tennessee investment also carried broader significance. Oak Ridge, the very city where the K-25 gaseous diffusion plant had launched the enrichment era during the Manhattan Project, was now the site where centrifuge manufacturing would sustain it. There was a certain poetry in the geography: eight decades after physicists and engineers had gathered in the Tennessee hills to crack the uranium enrichment problem for the first time, a new generation of machinists and engineers was assembling there to solve it again with fundamentally different technology.

By the end of 2025, the financial picture had transformed beyond recognition from the bankruptcy-era company. Revenue reached $448.7 million, net income was $77.8 million, and unrestricted cash stood at $2.0 billion. Total backlog was approximately $3.8 billion, including $2.3 billion in contingent LEU contracts. Long-term debt stood at $1.17 billion, almost entirely from the convertible note offerings. The stock's 52-week range of $49 to $464 captured the market's violent repricing of a company that was moving from demonstration project to industrial buildout.

IX. The Nuclear Renaissance and AI Data Center Boom

The Centrus story does not exist in isolation. It sits at the intersection of three mega-trends that are reshaping global energy markets simultaneously: the climate imperative for carbon-free baseload power, the revival of nuclear energy after decades of stagnation, and the explosive demand for electricity driven by artificial intelligence.

Start with the AI factor, because it is the most recent and perhaps the most powerful catalyst. Global electricity generation for data centers was projected to grow from 460 terawatt-hours in 2024 to over 1,000 TWh by 2030 and 1,300 TWh by 2035. U.S. data center power capacity was estimated to nearly quadruple from 33 gigawatts in 2024 to 120 GW by 2030. Major cloud companies were expected to spend over $600 billion on capital expenditures in 2026 alone, a 36 percent increase from the prior year, with roughly $450 billion directed at AI infrastructure.

This is not incremental growth. This is a step-change in electricity demand that the existing grid, dominated by intermittent renewables and retiring fossil fuel plants, cannot easily accommodate. Nuclear power offers something that wind and solar fundamentally cannot: 24/7 carbon-free baseload power at massive scale, operating at capacity factors above 90 percent regardless of weather conditions. A nuclear plant runs when the sun does not shine and the wind does not blow, which is exactly when AI data centers still need power.

The tech industry noticed, and the commitments came quickly. Microsoft signed a landmark power purchase agreement to restart the Three Mile Island Unit 1 reactor in Pennsylvania, a deal that would have been unthinkable a few years earlier, given Three Mile Island's association with America's worst nuclear accident. Google announced agreements for small modular reactor power to serve its data center operations. Amazon invested in nuclear energy projects and explored direct power procurement from nuclear facilities. These were not speculative bets by companies dabbling in clean energy marketing. These were operational commitments by the most capital-efficient companies on Earth, driven by cold-eyed calculations that their core AI businesses required reliable, carbon-free electricity in quantities that renewables and storage alone could not guarantee at acceptable cost and reliability levels.

For nuclear power, the AI data center boom created something the industry had not experienced in decades: genuine, large-scale new demand. But here is the bottleneck that connects back to Centrus. You cannot run reactors without fuel. The existing fleet needs conventional LEU, which currently depends heavily on Russian and foreign enrichment. The advanced reactors that companies like TerraPower, X-energy, and Kairos Power are developing need HALEU, which currently only Centrus can produce domestically.

The fuel supply chain has become the critical path. It does not matter how many reactors get licensed, how much capital flows into nuclear construction, or how many data center contracts get signed if there is not enough enriched uranium to fuel them. Centrus sits at this chokepoint. The company has gone from selling someone else's commodity product to occupying a position where its production capacity directly determines the pace of the American nuclear revival.

The market dynamics have shifted accordingly. Where enrichment services were once a commodity business with razor-thin margins and fierce price competition, the combination of Russian supply restrictions, surging demand, and limited Western capacity has created pricing power that the industry has not seen in years. SWU prices climbed 65 percent following the Ukraine invasion. The uranium enrichment market, valued at roughly $14 billion in 2025, was projected to grow to over $22 billion by 2030.

For investors, the framing shifted from "struggling commodity supplier" to "strategic chokepoint in the nuclear renaissance." Whether that premium is justified depends entirely on what happens next.

X. Business Model and Strategy: From Death to Dominance?

Centrus operates in two segments. The LEU segment is the larger revenue driver, focused on purchasing separative work units and uranium from foreign enrichers and reselling them to utilities that operate nuclear power plants. This is essentially a trading and brokerage business: Centrus buys enrichment services from URENCO, historically from TENEX, and from other sources, marks them up, and sells them under long-term contracts to American and international utilities. Revenue in 2025 was $448.7 million, the vast majority from this segment.

The Technical Solutions segment is smaller in revenue but disproportionately important strategically. It encompasses DOE contracts for HALEU production, American Centrifuge technology development, decontamination and decommissioning work, and other government services. This is where the company's future lies.

The business model is in the middle of a fundamental transition. For the past decade, Centrus has essentially been an intermediary, buying enrichment services produced by others and reselling them. The company's plan is to become a producer again, building out centrifuge manufacturing capacity at Oak Ridge and installing centrifuge cascades at Piketon to produce both HALEU and conventional LEU using American-origin technology. The first new production capacity is targeted for 2029.

The capital requirements are enormous. Centrus has disclosed plans to invest over $560 million to expand Oak Ridge manufacturing alone, with total capital deployment of $350-500 million planned for 2026. The two convertible note offerings raised approximately $1.15 billion. The company ended 2025 with $2 billion in cash but also $1.17 billion in long-term debt. This is a company burning through capital to build industrial infrastructure that will not generate meaningful production revenue for years.

The backlog story deserves scrutiny. Centrus reports a total backlog of approximately $3.8 billion extending to 2040, but $2.3 billion of that is classified as "contingent" LEU sales, meaning these contracts are conditional on various factors including customer elections, pricing adjustments, and other contingencies. The binding, non-contingent portion is significantly smaller. The DOE's $900 million task order selection is also subject to negotiation and congressional appropriations. The backlog is real in the sense that these are signed agreements with counterparties, but the path from contingent backlog to recognized revenue involves considerable uncertainty.

Revenue guidance for 2026 of $425-475 million suggests relatively flat near-term performance as the company transitions from trading to production. The real question is what revenue looks like in 2030 and beyond, when centrifuge capacity is supposed to come online and the Russian supply restrictions are fully binding.

The government dependency is the elephant in the room. DOE contracts underpin the Technical Solutions segment, DOE funding enabled the HALEU demonstration, DOE task orders represent the largest growth opportunity, and federal legislation created the market conditions that make domestic enrichment economically viable. Centrus needs Congress to continue appropriating funds, DOE to continue awarding contracts, and the regulatory environment to remain supportive. This is not unusual for defense and infrastructure companies, but it means political risk is a first-order concern, not an afterthought.

For investors tracking this company's execution, three metrics matter most. First, HALEU and LEU production volume in kilograms and SWU: this measures whether the company can actually produce at scale, not just demonstrate technology. Second, contract backlog conversion rate: the percentage of contingent backlog that converts to binding, revenue-generating contracts over time. Third, capital efficiency: dollars invested per SWU of production capacity added, which will determine whether the economics of American enrichment work at commercial scale.

XI. Competitive Landscape and Industry Structure

Uranium enrichment is one of the most concentrated industries on Earth. Four companies control virtually all global commercial enrichment capacity: Rosatom of Russia, URENCO of Europe, Orano of France, and CNNC of China. This is not a normal oligopoly. It exists because enrichment requires massive capital investment, decades of technology development, classified knowledge, and government licensing that no startup can replicate in any reasonable timeframe.

Rosatom dominates with roughly 40 percent of global enrichment capacity, operating over 27 million SWU per year across four plants. This is a state-owned enterprise backed by the full resources of the Russian government, with decades of centrifuge development and essentially unlimited political support. It can price aggressively, cross-subsidize from military programs, and operate on timelines that no private company can match.

URENCO is the principal Western counterweight, a consortium owned by the UK, Netherlands, and German governments with approximately 17.9 million SWU of capacity across plants in those three countries plus Eunice, New Mexico. URENCO's New Mexico facility, the National Enrichment Facility, began operations in 2010 and currently produces about 4,300 tonnes of SWU per year, with a 15 percent expansion underway expected to add 700,000 SWU by 2027. It is currently the only commercial enrichment facility operating in the United States.

This creates a nuanced competitive dynamic for Centrus. URENCO operates on American soil and serves American utilities, but it is a foreign-owned entity using foreign-origin technology. For commercial purposes, URENCO is a viable and important enrichment source. For national security applications, where U.S.-origin technology is required, URENCO cannot substitute for Centrus. The distinction matters enormously for defense applications, HALEU for government-sponsored advanced reactors, and programs where technology export controls or security clearance requirements apply.

Orano operates the Georges Besse II plant in France with approximately 7.5 million SWU of capacity. Like URENCO, it serves the global commercial market but uses French-origin technology. China's CNNC has been expanding capacity to serve its massive domestic reactor buildout, and the concerning displacement pattern, importing Russian enrichment to free domestic capacity for export, adds a further complication to Western supply security.

The HALEU competitive landscape is even more concentrated. Before Centrus began production in 2023, Russia held a complete monopoly on HALEU supply. Centrus is now the only Western producer. Potential future competitors include URENCO, which received NRC approval to enrich up to 10 percent at its New Mexico facility, and laser enrichment ventures like Global Laser Enrichment, a partnership between GE-Hitachi and Silex Systems that is developing a fundamentally different enrichment approach using lasers rather than centrifuges. Laser enrichment promises lower costs and greater flexibility but remains in development, not production.

What makes the enrichment business fundamentally different from other energy sector industries is the technology moat. Centrifuge technology is classified. You cannot license it, reverse-engineer it, or acquire it through normal commercial channels. The regulatory barriers, NRC licensing, DOE oversight, security clearances, physical security requirements, take years to navigate. A new entrant would need billions in capital, a decade of development time, government cooperation, and patience that venture capital simply does not have. These barriers explain why the global enrichment oligopoly has remained essentially unchanged for decades and why Centrus's position as the only U.S.-origin technology holder is so strategically significant.

It is also worth noting what Centrus does not control. The company is not vertically integrated across the full nuclear fuel supply chain. It does not mine uranium. It does not convert uranium ore into the uranium hexafluoride gas that enrichment requires. It does not fabricate finished fuel assemblies. Each of these steps involves its own set of concentrated suppliers and potential bottlenecks. Centrus depends on Cameco, Orano, and others for conversion services, and on companies like Westinghouse and Framatome for fuel fabrication. This means that even if Centrus perfectly executes its enrichment expansion, supply chain constraints at other steps could limit the overall pace of fuel delivery to reactors. The enrichment chokepoint is the most dramatic, but it is not the only one.

XII. Strategic Analysis: Porter's Five Forces

Threat of New Entrants: Low. Building a commercial-scale enrichment facility requires billions of dollars in capital, classified centrifuge technology that takes decades to develop, NRC licensing that involves years of review, security clearances for the entire workforce, and physical infrastructure that cannot be built quickly. The minimum time to market, even with unlimited funding, is five to ten years. Laser enrichment ventures like Global Laser Enrichment represent a potential disruptive technology, but they remain pre-commercial with uncertain timelines. The barriers protecting incumbents in this industry are among the highest of any business on Earth.

Supplier Power: Medium-High. Uranium mining is concentrated in Kazakhstan, Canada, Australia, and Namibia. Conversion services, the step that turns uranium oxide into the uranium hexafluoride gas needed for enrichment, are provided by a handful of players including Cameco, Orano, and Converdyn. Centrifuge component suppliers are highly specialized. However, the relationship is somewhat balanced because suppliers need enrichers as much as enrichers need suppliers, creating mutual dependence.

Buyer Power: Medium and Declining. Nuclear utilities are sophisticated, risk-averse buyers that plan fuel purchases years in advance and negotiate aggressively. Historically, they wielded significant buyer power because multiple enrichment sources competed for their business and Russian supply kept prices low. Post-Russia ban, buyer power has diminished. With limited alternatives to Russian enrichment and growing demand, utilities are competing for limited Western capacity. The DOE as a buyer is a different dynamic entirely: it can direct massive funding but also dictates terms and conditions. Long-term contracts, typical in the industry, reduce switching and create stickiness once relationships are established.

Threat of Substitutes: Low. There is no substitute for enriched uranium in nuclear reactors. You cannot run a light-water reactor on anything other than LEU. You cannot fuel an advanced reactor design with anything other than HALEU if that is what the design specification requires. Alternative energy sources like renewables and storage compete for new power generation capacity, but they do not substitute for uranium fuel in existing or planned nuclear plants. This is about as close to zero substitution risk as any industry gets.

Competitive Rivalry: Medium and Shifting. Historically, the enrichment oligopoly operated with rational pricing and relatively stable market shares. The geopolitical fragmentation triggered by the Ukraine war and Russian import bans is creating regional market segmentation. In the U.S. market specifically, Centrus faces limited competition: URENCO's New Mexico operation (foreign-owned, foreign technology) and diminishing Russian imports. For HALEU, Centrus currently has a quasi-monopoly in Western production. Long-term rivalry depends on whether URENCO expands into HALEU, whether laser enrichment matures, and whether new DOE-supported entrants emerge.

Overall Assessment: Across all five forces, the picture is unusually favorable for Centrus. The industry structure is highly favorable for incumbents, particularly for Centrus in the U.S.-origin HALEU segment. The combination of extreme entry barriers, low substitution threat, and declining buyer power creates conditions where a successfully executing incumbent can capture significant value. The critical variable is execution, specifically whether Centrus can scale from demonstration to commercial production, because favorable industry structure means nothing if the company cannot deliver product.

XIII. Strategic Analysis: Hamilton Helmer's Seven Powers

Scale Economies: Potential but Unproven. Enrichment is a classic scale business where fixed costs are massive and marginal costs are low. A centrifuge enrichment plant requires enormous upfront investment in manufacturing, installation, licensing, and security infrastructure, but once operating, the incremental cost of producing additional SWU is relatively modest. Centrus is currently operating at demonstration scale with 16 centrifuges. Commercial viability requires scaling to thousands of machines. The open question is whether Centrus can reach minimum efficient scale before market dynamics shift or capital runs out. If it does, scale economics become a powerful advantage. If it does not, the fixed costs become a millstone.

Network Effects: Not Applicable. Enrichment is a B2B industrial service. There are no network effects. The value of Centrus's product does not increase with the number of users.

Counter-Positioning: Moderate. Centrus is positioned as "U.S.-origin, national security aligned," a value proposition that foreign competitors fundamentally cannot replicate. Rosatom cannot credibly serve U.S. national security needs. URENCO operates in the U.S. but with foreign technology and foreign ownership. This is a form of counter-positioning because incumbents cannot respond without changing their fundamental nature. The AC100M centrifuge design may also offer technical advantages over older designs, though this is unproven at commercial scale.

Switching Costs: High. Once utilities sign long-term enrichment contracts, which typically span five to fifteen years, switching is expensive and risky. Fuel supply continuity is critical for reactor operations; utilities cannot afford disruption to their fuel cycle. Regulatory approval processes for fuel suppliers create additional lock-in. Centrus benefits enormously once customers commit, which is why the conversion of contingent backlog to binding contracts is such an important metric to track.

Branding: Moderate to Strong. This is not consumer branding, but reputation matters profoundly in the nuclear industry where safety, reliability, and security are existential concerns. "Only U.S.-origin enricher" is powerful positioning in the current geopolitical environment. The company carries historical baggage from near-bankruptcy and execution challenges, but the national security cachet is growing as geopolitical tensions intensify.

Cornered Resource: Strong. This is Centrus's most powerful strategic asset. The American Centrifuge technology is the only U.S.-origin, deployment-ready enrichment technology in existence. The Piketon facility has existing infrastructure, regulatory approvals, and a trained workforce. DOE relationships and contracts, built over decades, are nearly impossible for newcomers to replicate. HALEU production capability is currently unique in the Western Hemisphere. These resources cannot be bought, licensed, or replicated in any reasonable timeframe. A competitor starting from scratch today would need a decade and billions of dollars to reach where Centrus stands.

Process Power: Developing. Centrus has decades of enrichment expertise embedded in its workforce and institutional knowledge, but operations were mothballed for years and are only now being rebuilt. If the company successfully scales production, embedded operational advantages will compound over time as workers gain experience, processes are refined, and supply chain relationships deepen. Currently, this power is more potential than proven.

Summary of the Seven Powers:

The primary power is Cornered Resource. Centrus's entire strategic position rests on owning the only U.S.-origin enrichment technology at a moment when the country has decided it desperately needs one. No amount of capital can shortcut the decades of development, the classified knowledge base, and the regulatory approvals that Centrus already possesses.

The emerging power is Switching Costs, which will strengthen as long-term enrichment contracts lock in utility customers over five-to-fifteen-year terms. Every binding contract signed makes Centrus stickier and harder to displace.

The critical uncertainty is Scale Economies. Enrichment has attractive unit economics at scale, but Centrus must actually reach that scale. The distance between 16 demonstration centrifuges and a commercial plant with thousands of machines is where the Seven Powers framework meets cold industrial reality.

XIV. What Could Go Wrong? And What Could Go Right?

The Bear Case rests on a fundamental concern: Centrus has never successfully operated enrichment at commercial scale. The American Centrifuge program consumed billions over decades before even demonstrating viability at a small scale. Scaling from 16 centrifuges to thousands is an engineering, manufacturing, and operational challenge of an entirely different magnitude. Six of 38 test centrifuges crashed in 2012. What happens when you are running thousands of them continuously for years?

Government funding is the lifeblood of the expansion plan. Centrus needs Congress to continue appropriating billions for domestic enrichment, DOE to continue awarding and funding task orders, and the political consensus around nuclear energy and energy security to hold. Political winds shift. Administrations change. Budget priorities evolve. A single appropriations fight could delay or derail expansion plans that depend on federal dollars.

The market timing risk is acute. First new commercial production capacity is targeted for 2029, four years from now. By then, URENCO may have expanded its New Mexico facility significantly. Laser enrichment technology might have matured. Geopolitical conditions might have changed in ways that alter the calculus around Russian supply. The advanced reactor market, the primary demand driver for HALEU, has a history of overpromising and underdelivering on deployment timelines.

Dilution is a real and present risk. The two convertible note offerings total over $1.15 billion in potential dilution if converted. If additional capital raises are needed, and they likely will be given the scale of the buildout, existing shareholders face ongoing dilution. For a company with a market capitalization that fluctuates dramatically, each capital raise recalibrates the risk-reward equation.

The Bull Case is equally compelling. National security imperatives do not disappear. The bipartisan consensus on reducing dependence on Russian nuclear fuel is as strong as any energy policy agreement in recent memory. The government has already committed $2.72 billion specifically for domestic enrichment capacity. Canceling these programs would mean accepting permanent dependence on adversaries for a critical input to both civilian and military nuclear programs.

First-mover advantage in HALEU could prove decisive. If advanced reactors begin deploying in the late 2020s and early 2030s as planned, the utilities and reactor developers buying those reactors will need HALEU fuel supply locked up years in advance. Centrus, as the only Western producer, would be the default choice. Once those long-term supply contracts are signed, switching costs protect the position for decades.

The nuclear renaissance, powered by AI data center demand, climate policy, and energy security concerns, represents the first sustained positive demand catalyst for the nuclear industry in a generation. If even a fraction of the projected data center electricity demand materializes as nuclear capacity, the fuel supply chain, including enrichment, faces a structural supply shortage that would drive prices and returns for producers.

Strategic acquisition remains a wildcard. A company with Centrus's unique technology, regulatory positioning, and government relationships would be an attractive target for defense primes, major utilities, or international energy companies looking for a foothold in American nuclear fuel supply.

The Most Likely Scenario falls between these extremes. Centrus successfully scales HALEU production with sustained government support. It builds moderate commercial LEU capacity but never becomes a dominant global enricher on the scale of Rosatom or URENCO. It occupies a profitable niche as the U.S.-origin supplier for national security applications and advanced reactor fuel. Government dependency persists but generates real, growing commercial revenues as production comes online. The company trades at a premium valuation reflecting its strategic positioning, but the premium is tempered by execution risk and the long timeline to full-scale operations.

Think of it as analogous to a defense prime contractor like Huntington Ingalls, the sole builder of U.S. aircraft carriers: strategically irreplaceable, deeply government-dependent, consistently profitable, but never going to become a high-growth tech company. The question is whether Centrus can achieve that kind of stable, strategic-premium business, or whether the execution challenges and capital requirements overwhelm the opportunity before it materializes.

XV. Lessons and Reflections

Survival Through Irreplaceability. The Centrus story is ultimately about a company that survived long enough for its unique capability to become essential. When gaseous diffusion died and the American Centrifuge nearly failed, Centrus could have vanished entirely. Instead, it held onto the one asset that could not be replicated: the only U.S.-origin enrichment technology. When your core business dies, the lesson is not always to pivot to something new. Sometimes it is to identify the one thing only you can do and protect it until the world needs it. Being the "last man standing" with critical technology can be the most powerful competitive position imaginable, but only if you survive long enough to collect.

Government as Customer and Kingmaker. The double-edged sword of government dependency runs through every chapter of this story. The government created USEC through privatization. Government programs, Megatons to Megawatts, sustained it. Government loan guarantee rejection nearly killed the American Centrifuge. Government contracts kept the technology alive during bankruptcy. Government legislation, the Russian import ban, created the market opportunity. Government funding is financing the expansion. This is not a conventional competitive market narrative. It is a story about how public-private partnerships work in strategic industries, with all the attendant risks of political dependence, appropriations uncertainty, and changing administrations.

Geopolitics as Business Catalyst. Russia's invasion of Ukraine did not create the vulnerability in Western nuclear fuel supply chains. That vulnerability had been building for decades as domestic enrichment capacity atrophied while Russian supply grew. What the invasion did was make the vulnerability politically unacceptable. Overnight, a market structure that policymakers had tolerated for twenty years became a national security emergency.

The lesson for investors and strategists is that geopolitical inflection points can create sudden, massive demand for capabilities that seemed uneconomic or unnecessary just months before. The reshoring imperative in nuclear fuel mirrors what happened in semiconductors after the COVID-era chip shortage, in pharmaceuticals after the supply chain disruptions, and in rare earth minerals after China signaled its willingness to use export controls as leverage. The companies positioned to fill those needs, often the ones that stubbornly maintained capabilities through lean years, can capture extraordinary value. Being early to a geopolitical trade is lonely and unprofitable. Being positioned when the consensus arrives is transformative.

Technology Moats in Industrial Businesses. Silicon Valley has conditioned people to think of technology moats in terms of software, algorithms, and network effects. Centrus's moat is centrifuge metallurgy, cascade dynamics, and NRC licenses. It is not sexy. It took 40 years to develop. It nearly destroyed the company financially before it created value. But classified technology backed by government licensing creates an entry barrier that no amount of venture capital funding can overcome. In an era of reshoring and supply chain security, these "old economy" technology moats may prove more durable and more valuable than many software-based advantages.

Capital Intensity and Patience. Building enrichment capacity is a multi-billion-dollar, multi-decade endeavor. Centrus is asking investors to fund construction of industrial infrastructure that will not reach commercial production until 2029 at the earliest, based on technology that has been in development since the 1980s. The gap between "plans to build" and "successfully operating at scale" is where most capital-intensive industrial ventures fail. History offers plenty of cautionary tales: nuclear power construction itself has been plagued by cost overruns and delays, from Vogtle in Georgia to Flamanville in France. Building things in the physical world is harder, slower, and more expensive than projections suggest, almost without exception.

For investors, the challenge is distinguishing between a transformational story supported by genuine strategic advantage and a capital-intensive dream that consumes shareholder value before delivering returns. The convertible notes structure is worth particular attention here: $1.15 billion in convertible debt means that if the stock price rises above the conversion prices, significant dilution follows. If it does not, the company carries substantial fixed obligations against revenue that remains modest relative to its ambitions. Capital structure matters enormously in capital-intensive businesses, and Centrus's financial engineering will be tested alongside its nuclear engineering.

XVI. Where Are They Now and What Is Next

Current State. Centrus enters 2026 at an inflection point. The company launched commercial centrifuge manufacturing at Oak Ridge in December 2025, the most tangible evidence yet that the transition from demonstration to production is underway. The balance sheet is fortified with $2 billion in cash, largely from the convertible note offerings, providing runway for the capital-intensive buildout ahead. Total backlog stands at $3.8 billion extending to 2040, the DOE has selected Centrus for a $900 million HALEU task order, and Korean partners are exploring investment in the Piketon expansion. Revenue guidance for 2026 of $425-475 million reflects the transition period between trading-era revenue and production-era growth.

The stock's wild swing from under $50 to above $460 and back to roughly $200 captures the market's oscillation between enthusiasm for the strategic story and anxiety about the execution timeline. Both sentiments are justified. The volatility itself tells a story: this is a stock priced on narrative and expectation, not on current earnings. Until production revenue replaces trading revenue as the dominant contributor, the stock will remain a bet on whether the narrative becomes reality.

Kevin Harrill, who became CFO in 2023, faces the unenviable task of managing capital allocation during a period when outflows for construction will vastly exceed inflows from production for years. The financial engineering, balancing convertible debt, government contract cash flows, and potential partner investments, may prove as challenging as the nuclear engineering.

Near-Term Catalysts to Watch (2026-2028). The DOE task order negotiations represent the single largest near-term catalyst. Conversion of the $900 million selection into binding contract terms will signal whether government commitment translates into actual production orders. Construction milestones at both Oak Ridge manufacturing and Piketon enrichment facilities will provide tangible evidence of execution. The conversion of contingent backlog into binding contracts, particularly with utilities that need to secure non-Russian enrichment supply before waivers expire in January 2028, will test whether commercial demand matches the strategic narrative.

The waiver expiration date of January 1, 2028 is a structural catalyst. After that date, no Russian LEU can enter the United States under any circumstances, regardless of waivers or exemptions. The declining annual import caps under the waiver program, which decrease each year through 2027, create a tightening vice on utilities that have historically relied on Russian supply. Those utilities must secure alternative enrichment sources years in advance because reactor fuel procurement operates on multi-year planning cycles. A utility that waits until 2027 to secure post-ban supply will find itself competing with every other Russian-dependent utility for limited Western capacity. The urgency to lock in domestic enrichment contracts will increase as that deadline approaches, and Centrus's contingent backlog should begin converting to binding commitments at an accelerating pace if the strategic thesis is correct.

Long-Term Questions (2029 and Beyond). Will commercial production come online on time and on budget? The company's entire value proposition rests on this question. History, both Centrus's own and the broader history of large-scale industrial projects, suggests delays and cost overruns are more common than on-time, on-budget delivery.

Can Centrus achieve the scale needed for meaningful U.S. market share? The URENCO New Mexico facility produces 4,300 tonnes of SWU per year. Reaching comparable scale would require thousands of centrifuges operating reliably for years. The path from 16 demonstration centrifuges to thousands of commercial machines is long and uncertain.

What happens when advanced reactors actually start deploying? If SMRs and next-generation designs achieve their deployment targets, HALEU demand could exceed anything currently planned. If advanced reactor deployment is delayed, as it has been repeatedly throughout history, the HALEU demand thesis weakens.

Industry Wildcards. Laser enrichment technology, being developed by Silex Systems and GE-Hitachi's Global Laser Enrichment venture, uses a fundamentally different approach to isotope separation that could potentially offer lower costs and greater flexibility than centrifuges. If laser enrichment achieves commercial viability, it could disrupt the centrifuge-based oligopoly. The timeline remains uncertain, but the technology represents the most credible long-term disruption threat to Centrus's technology moat.

China's enrichment expansion and the displacement exchange pattern, importing Russian enrichment to free domestic capacity for Western exports, could complicate the supply picture in ways that are difficult to predict. If Chinese-origin enrichment begins displacing Western supply in third-party markets at aggressive pricing, it could undermine the economics of new Western capacity before it reaches scale.

Political changes in the U.S. could affect bipartisan support for nuclear energy and domestic enrichment funding, though the current consensus appears durable. Nuclear energy enjoys unusually strong bipartisan support in 2026, with both major parties embracing it for different reasons: Republicans for energy independence and national security, Democrats for climate and clean energy goals. But bipartisan consensus is not permanent, and appropriations are never guaranteed.

XVII. Final Reflections

The arc of the Centrus story, Cold War relic to privatization to near-death to national security savior, is the kind of narrative that usually gets told in retrospect, after the outcome is known. What makes it compelling in early 2026 is that the outcome remains genuinely uncertain. The company has survived decades of adversity, raised billions in capital, secured government support, and proved its technology works at small scale. Whether it can build and operate industrial-scale enrichment, deliver on a $3.8 billion backlog, and justify a premium valuation remains an open question that will take years to answer.

The human element of this story is easy to overlook amid the financial metrics and geopolitical analysis. In Piketon, Ohio, a workforce has maintained American nuclear enrichment expertise through decades of uncertainty, from the gaseous diffusion era through the American Centrifuge debacle through bankruptcy and mothballing and back to production. Many of these workers are the children and grandchildren of people who built the original Portsmouth plant in the 1950s. They represent an institutional knowledge base that cannot be recreated if lost.

The broader implications extend well beyond one company or one industry. Centrus is a case study in what happens when a nation allows strategic industrial capability to atrophy and then scrambles to rebuild it. The parallels to semiconductors, pharmaceuticals, rare earth minerals, and other critical supply chains are unmistakable. The reshoring and friendshoring mega-trend that gained momentum after COVID-19 and accelerated after the Ukraine invasion is playing out across dozens of industries simultaneously. Centrus may be the most dramatic example because the stakes, nuclear fuel for both civilian power and national defense, are so high and the alternatives are so limited.

The nuclear question itself remains open. The industry has experienced false dawns before, moments when a nuclear renaissance seemed imminent only to be derailed by cost overruns, regulatory delays, accidents, or shifting political winds. Fukushima in 2011 devastated the industry globally. Whether the current combination of AI-driven electricity demand, climate policy, and energy security concerns creates a genuine, sustained nuclear buildout or yet another false dawn will determine whether Centrus's strategic bet pays off.

For investors, Centrus represents a high-conviction, high-uncertainty bet on the intersection of national security, nuclear energy, and industrial policy. The strategic positioning is undeniable. The cornered resource of U.S.-origin enrichment technology is real. The government commitment is substantial. But the execution risk is significant, the timeline is long, the capital requirements are massive, and the history of large-scale industrial projects is littered with failures. The distance between a compelling strategic narrative and a successful operating business is measured in years, billions of dollars, and thousands of centrifuges that must spin reliably day after day.

What makes this story resonate beyond the nuclear industry is the universality of the underlying dynamic. Across sectors from semiconductors to pharmaceuticals to rare earth processing, the United States is discovering that capabilities lost over decades cannot be rebuilt overnight. The workers who know how to do the work retire. The supply chains that supported the facilities dissolve. The institutional knowledge that made complex processes reliable dissipates. Rebuilding is not just a matter of writing checks; it requires reconstituting an entire ecosystem of skills, suppliers, and operational expertise.

Centrus sits at the leading edge of this re-industrialization experiment. If it succeeds in scaling American Centrifuge technology to commercial production, it will stand as proof that strategic patience, government partnership, and preserved technology can bridge the gap between capability loss and capability restoration. If it fails, it will serve as a cautionary tale about the limits of policy-driven industrial revival and the gap between strategic narratives and operational reality.

For the country, the question is simpler but no less consequential: Can America rebuild strategic manufacturing capabilities after decades of outsourcing them? The Centrus story, still being written in a rural Ohio facility and a Tennessee manufacturing center, will provide part of the answer.

XVIII. Key Takeaways and Further Learning

Three Big Ideas

First, cornered resources become exponentially valuable when geopolitics shift. Centrus's U.S.-origin enrichment technology was a money-losing liability in a globalized world where cheap Russian supply dominated the market. In a fragmented world where supply chain security is a national priority, it became priceless. The lesson applies broadly: strategic assets that seem uneconomic in peacetime can become irreplaceable when the geopolitical order changes.

Second, strategic patience and government partnership can resurrect businesses that the market left for dead. Centrus survived bankruptcy, technology failures, and a decade of irrelevance because it held onto its core technology and cultivated government relationships that eventually translated into contracts, funding, and legislative support. Sometimes the right strategy is simply surviving long enough for the world to need you again.

Third, the new industrial policy era rewards domestic champions in critical industries. From semiconductors (CHIPS Act) to clean energy (Inflation Reduction Act) to nuclear fuel (Russian uranium import ban), government policy is explicitly reshoring strategic manufacturing and directing enormous capital flows to domestic producers. Companies positioned as domestic champions in critical supply chains are benefiting from a structural tailwind that transcends normal business cycles.

What to Watch

DOE contract awards and congressional appropriations remain the primary near-term drivers. Production milestones at Piketon and manufacturing progress at Oak Ridge provide the execution evidence that determines whether the strategic narrative translates into operational reality. Russian uranium market developments, including the waiver expiration timeline and any changes to the import ban, directly affect the competitive landscape. Advanced reactor deployment timelines, particularly for HALEU-dependent designs, determine the demand side of the equation.

The Myth Versus Reality Check

The consensus narrative on Centrus is straightforward: irreplaceable national security asset, massive government tailwinds, explosive growth ahead. But the reality is more nuanced. The myth says Centrus has a monopoly on American enrichment. The reality is that URENCO's New Mexico plant is the only commercial enrichment facility currently operating in the United States, producing 4,300 tonnes of SWU annually. Centrus currently produces nothing at commercial scale. The myth says HALEU demand is imminent and enormous. The reality is that advanced reactor deployment timelines have historically slipped by years or decades, and HALEU demand projections are only as good as the reactor deployment assumptions underlying them. The myth says government funding is guaranteed. The reality is that appropriations are annual, political, and subject to change with every election cycle and budget negotiation.

None of this invalidates the investment thesis. But it requires investors to distinguish between strategic positioning, which is genuinely strong, and operational execution, which remains unproven. The gap between those two things is where fortunes are made or lost.

Essential Deep Dives

The Megatons to Megawatts program stands as one of history's most successful nonproliferation initiatives and a cautionary tale about the unintended economic consequences of well-intentioned policy. Understanding how it simultaneously eliminated 20,000 nuclear warheads and gutted American enrichment capacity is essential context for the Centrus story.