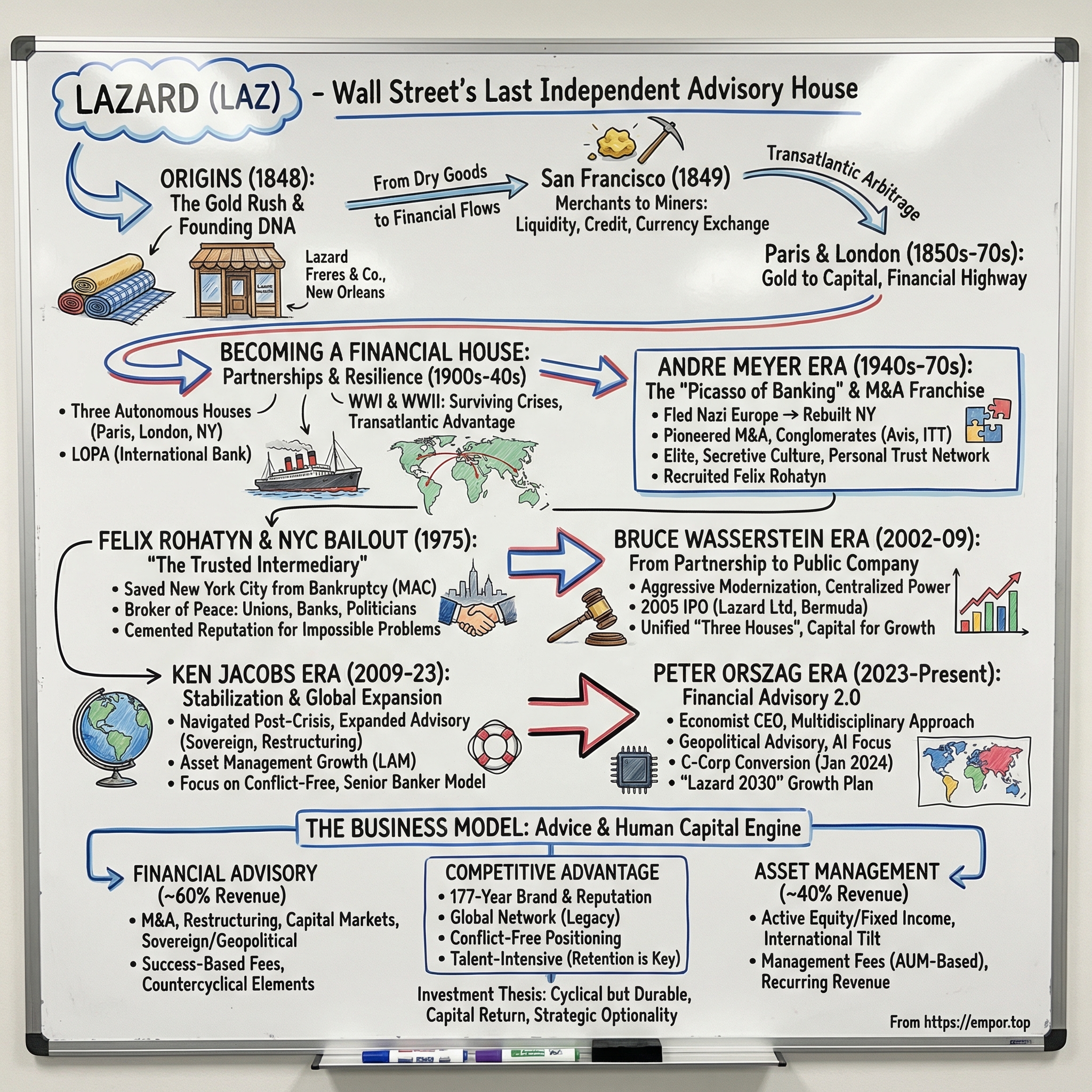

Lazard: Wall Street's Last Independent Advisory House

The Gold Rush Origins and the Founding DNA

The Lazard story begins not with banking but with bolts of cloth.

Alexandre and Lazare Lazard arrived in New Orleans around 1841, two Jewish Frenchmen fleeing the limited economic horizons of post-Napoleonic France. They bought goods wholesale from the docks of the Mississippi River and trudged through rural Louisiana, selling piecemeal to farmers and settlers. It was itinerant, unglamorous work. But they were good at it. Within a few years, they had earned enough to write home and summon a third brother, Simon.

In 1848, the three brothers formalized their partnership and founded Lazard Freres & Co. on Frenchmen Street, a short walk from the city docks where they could attend the daily unloading of cargo from clippers and steamships. Their timing could not have been better.

News of gold strikes in California had begun filtering east, and by 1849, half of America seemed to be heading for the Sierra Nevada foothills. Simon, along with two younger brothers who had since emigrated, Elie and Maurice, decamped for San Francisco to open a new store serving the booming Gold Rush economy.

Here is the detail that separates the Lazard brothers from thousands of other merchants who chased the Gold Rush: they never mined for gold. They were merchants to miners, selling supplies, fabric, and provisions to men who had gold dust in their pockets but no way to spend it.

The Gold Rush economy was chronically short of liquidity. Miners had flakes and nuggets but needed hard currency and credit to buy food, clothing, and equipment. Lazard stepped into that gap, offering foreign currency exchange and letters of credit as early as 1849. Think of it as the 1849 equivalent of a fintech company: the Lazard brothers saw a market with a massive supply-demand mismatch and built a business in the gap. This was the firm's founding insight, the DNA that would persist for nearly two centuries: Lazard as intermediary, never as principal. They did not dig for gold. They moved it.

Alexandre Lazard, the eldest brother, grasped something even more profound. Gold was pouring out of California, but it needed to reach the financial capitals of Europe to be converted into capital. The three brothers created what was essentially a transatlantic arbitrage operation: buy gold cheaply in San Francisco, ship it across the ocean, and sell it at a premium in Paris, where European banks and governments were hungry for the metal.

Alexandre returned to Paris in 1854 to open an office that could receive San Francisco gold and channel it into European markets. A London office followed around 1870, positioned at 60 Old Broad Street in the City of London's financial district. By 1876, the brothers had liquidated their last bolt of fabric and become a chartered bank. They had built what amounted to a transatlantic financial highway: San Francisco to New York to Paris to London, with Lazard tollbooths at every node.

Alexandre himself moved to New York in 1880 to open the Manhattan office, arriving with almost no local relationships. He was sixty years old, leaving San Francisco after three decades, to start again in the most competitive financial city on earth. But he leveraged the family's retail contacts to build a banking business, discounting bills and financing the growth of small but quality clients. Working in coordination with the Paris and London offices and assisted by George Blumenthal, who would later become senior partner, Alexandre shaped Lazard Freres New York into a major speculator in railroad and utilities securities and mastered the precious metals markets, orchestrating sensational gold shipments to France that made headlines in the financial press.

Within a few years, Lazard Freres New York had become one of the nation's leading exporters of gold and a major player in currency exchange, earning the firm entry to the inner circles of New York's banking syndicates. By 1884, a dry goods store on Frenchmen Street had transformed into a transatlantic banking house. The founding DNA was set: Lazard would always be the intermediary, the firm that moved value between parties rather than accumulating it for itself. That instinct, born in the Gold Rush, would define the next century and a half.

Becoming a Financial House: Partnerships and European Expansion

The transition from merchant house to financial house did not happen overnight. It unfolded over decades, shaped by the peculiar organizational structure the Lazard brothers had created.

Each of the three offices, Paris, London, and New York, was managed by family members and operated with significant autonomy. Steamships took weeks to cross the Atlantic, and the lack of rapid communication cemented each office's independence. The Paris partners did not know what the New York partners were doing on any given day, and vice versa. This semi-autonomous "three houses" structure would persist for over a century, creating both a competitive advantage, the ability to operate nimbly in three financial capitals simultaneously, and a persistent governance headache that would eventually require Bruce Wasserstein's iron hand to resolve.

To fund the expansion of their banking operations, the Lazard partners created an innovative vehicle: the London, Paris and American Bank Ltd., known as LOPA. Capital was raised primarily in San Francisco, but the bank operated with a London charter to take advantage of lower costs of capital in Britain and Britain's commercial ties to Asia. It was a preview of the kind of cross-border financial engineering that would later define Lazard's advisory business.

In New York, George Blumenthal became senior partner in 1904. A formidable financier who would later serve as president of the Metropolitan Museum of Art, Blumenthal shaped Lazard New York as a major speculator in railroad and utilities stocks and bonds. Frank Altschul, whose father had been an early employee of the San Francisco office since 1877, became the leading partner of the New York house in 1916 and held that role until 1943.

In Paris, the David-Weill family, who had married into the Lazard dynasty, became the dominant force. David David-Weill turned Lazard Paris into the most powerful of the three houses, establishing a family grip on the firm's governance that would endure for generations. The David-Weill influence would shape Lazard for nearly a century, through two world wars, a public offering, and a succession of legendary leaders.

The world wars tested Lazard's resilience in ways that few institutions have experienced.

During World War I, the Paris office operated short-staffed as partners joined the French military, but continued assisting the French government with war financing. The London office did the same for Britain. Lazard's transatlantic position, straddling the Allied powers, was both a risk and an advantage: the firm could facilitate financial flows between the allied capitals in ways that domestic banks could not.

After the armistice, the partners strengthened local ownership of Lazard Brothers London by selling a minority stake to Weetman Pearson, Lord Cowdray, a wealthy industrialist and prominent client. The London office was formalized as a separate company, Lazard Brothers and Co., in 1908, further entrenching the independence of the three houses.

World War II was existential. Pierre David-Weill, the grandson of David David-Weill, and Andre Meyer, a minority partner at Lazard Paris, fled the German occupation of France to the United States. The circumstances of their departure were harrowing. Meyer, a Jewish Frenchman who had built his career in the Paris financial world, watched as the Vichy regime collaborated with Nazi Germany to systematically strip Jewish citizens of their livelihoods and freedoms. By February 1941, the Nazis had seized the David-Weill family's bank and shuttered its properties. The Vichy regime stripped Meyer of his French citizenship and froze or seized his assets. Everything he had built in France was gone.

Pierre David-Weill took charge of the New York office and installed Meyer alongside him. The two men, thrown together by catastrophe, ran the American operations through the war years. After the liberation of France by Allied forces in 1944, Pierre returned to Paris to rebuild the European business from the rubble. The decision he made before departing would transform the entire trajectory of the firm: he left Andre Meyer in charge of American operations. It was, in retrospect, one of the most consequential personnel decisions in the history of Wall Street.

The Andre Meyer Era: Building the M&A Franchise

Andre Meyer was born on September 3, 1898, in Paris. He never attended university. A self-taught financier of prodigious intellect and volcanic temperament, Meyer had risen through the Paris financial world by sheer force of personality, joining Lazard Paris as a partner in his twenties. When he fled Nazi-occupied France in 1940, he was forty-two years old and arrived in New York with limited personal capital and a profound sense of displacement that never fully left him.

What Meyer built over the next thirty-five years is one of the most remarkable chapters in the history of American finance. He did not simply run Lazard New York. He remade it from a second-tier branch into the most powerful and profitable advisory house on Wall Street. David Rockefeller called him "the most creative financial genius of our time in the investment banking world." The nickname that stuck, however, captured something more essential: "The Picasso of Banking."

Meyer's genius lay in seeing deals where no one else did. He pioneered techniques that are now commonplace, early forms of leveraged buyouts, conglomerate strategies, and creative financing structures, but which in the 1950s and 1960s were genuinely revolutionary. He understood before almost anyone else that the real money in finance was not in lending or trading but in orchestrating the combination and recombination of corporate assets, in being the architect of transactions rather than the supplier of capital.

His most legendary transaction involved Avis Rent a Car. Meyer engineered Lazard's purchase of Avis for approximately seven million dollars. A few years later, he sold it to ITT for fifty-two million dollars in ITT stock. That is a return of roughly seven times the investment, orchestrated by an advisory firm that was not supposed to be doing principal investing at all. The Avis deal encapsulated Meyer's approach: find an undervalued asset, use Lazard's relationships and financial creativity to unlock its value, and exit at an enormous profit. It was private equity avant la lettre, decades before the term existed.

The ITT relationship was Meyer's masterpiece. Under Harold Geneen, ITT's CEO and a Lazard client, the company acquired forty-eight companies over a three-year period in the 1960s, growing to become the ninth-largest industrial corporation in the United States. The acquisitions spanned everything from Continental Baking to Sheraton Hotels to Hartford Fire Insurance. Lazard advised on deal after deal, earning fees that were staggering for the era.

The McDonnell-Douglas merger in 1966 alone generated a one-million-dollar advisory fee, a figure that made headlines when most banks were lucky to earn a fraction of that on any single transaction. To put that in perspective, a million-dollar fee in 1966 would be equivalent to roughly nine million dollars in 2026 terms. It was a signal that M&A advisory, a business that barely existed in its modern form, could generate enormous revenue from pure intellectual capital.

But Meyer was more than a dealmaker. He was a connector of extraordinary range, a spider sitting at the center of a web that stretched from corporate boardrooms to the Kennedy White House. He served as a director of RCA and Allied Chemical in the United States and Fiat and Montecatini Edison in Europe, straddling the Atlantic in a way that no other banker of his era could match. He built or revitalized corporate giants including Holiday Inns, Warner-Lambert, and Engelhard Minerals and Chemicals. He was a trusted financial adviser and close personal friend to Jacqueline Kennedy Onassis, managing her financial affairs from the assassination of President Kennedy until his own death. His client list read like a power directory: Robert Kennedy, David Rockefeller, Lyndon Johnson, Katharine Graham of the Washington Post.

What made Meyer's network different from the Rolodex-driven relationships that every banker cultivated was the depth of the trust he inspired. These were not transactional relationships. Jackie Kennedy relied on him not merely for investment advice but for counsel on the most personal financial decisions of her life. David Rockefeller, who could have had any banker in the world, chose Meyer. The trust economy that Meyer built was Lazard's true competitive advantage, far more durable than any balance sheet, and it was entirely personal. It lived in Meyer's head, in his relationships, and in the culture of discretion and secrecy he cultivated with almost obsessive intensity.

The culture Meyer created at Lazard was deliberately opaque and intensely elitist. Cary Reich's biography, "Financier," described Meyer's financial wizardry as "tempered only by the volatile tantrums, ruthlessness, and insatiable greed that went hand in hand with his genius." He was secretive about his personal affairs, left behind almost no letters or papers, and had no confidants. Despite his success, Meyer was never psychologically secure after fleeing Europe.

He operated through tight syndicates, personal relationships, and an insular approach inherited from European merchant banking traditions. Partners at Lazard did not collaborate openly. They competed with each other for Meyer's favor, for the best deals, and for the largest share of the profits. The atmosphere was electric but brutal, a hothouse of ambition and paranoia. Lazard under Meyer was famously lean: a small number of partners generating enormous profits per capita, disdaining the bureaucratic structures of the bulge-bracket banks that were growing larger around them.

Meyer's most consequential act of talent identification was recruiting Felix Rohatyn. Born on May 29, 1928, in Vienna, Rohatyn was himself a child refugee from Nazi Europe. He had fled with his family through France, Spain, Portugal, and Morocco before reaching the United States. The experience of displacement, of being an outsider who had to earn every foothold, gave Rohatyn an emotional intelligence and political instinct that would later prove invaluable. He joined Lazard in 1948 at age twenty as a clerk and built his entire career under Meyer's direct tutelage. Meyer preferred to operate behind the scenes, leaving the spotlight to younger partners like Rohatyn. Industry insiders understood that Meyer was the true power at Lazard, but it was Rohatyn who became the public face of the firm's deal-making prowess. Rohatyn was ITT's primary banker and held a seat on ITT's board of directors. He engineered the Avis purchase and many others during the Geneen conglomerate era.

Andre Meyer died on September 9, 1979, at age eighty-one, in Lausanne, Switzerland. His personal fortune exceeded two hundred million dollars, an enormous sum for a man who had arrived in America as a wartime refugee with limited capital. He was interred in the Jewish section of the Cemetery of Montparnasse in Paris, returning in death to the city he had been forced to flee four decades earlier. The firm he had rebuilt was, by that point, arguably the most prestigious advisory house on Wall Street. But what happened next, what Rohatyn would do with the reputation Meyer had built, would cement Lazard's place in American history in a way that even Meyer could not have anticipated.

Felix Rohatyn and the New York City Bailout: Lazard's Finest Hour

By 1975, New York City was dying.

Years of overspending, generous pension commitments, a shrinking tax base as middle-class residents fled to the suburbs, and the brutal 1973-1974 recession had pushed the city to the brink of insolvency. The city could no longer sell its bonds. Investors had lost confidence. Municipal workers faced layoffs. Essential services were being cut. Crime was surging. The fiscal death spiral seemed irreversible.

And on October 29, 1975, President Gerald Ford refused to provide a federal bailout, a decision immortalized by the New York Daily News in one of the most famous newspaper headlines in American history: "FORD TO CITY: DROP DEAD."

Into this maelstrom stepped Felix Rohatyn. Governor Hugh Carey turned to the Lazard partner who had established his reputation as Wall Street's preeminent dealmaker and asked him to do something that no financial adviser had ever attempted: save a city. Think about what that meant for a moment. Rohatyn was not a politician. He was not an elected official. He had no formal authority, no regulatory power, and no legal mandate. He was a private-sector banker being asked to broker a peace among constituencies that had been at war for years. The unions hated the banks. The banks blamed the politicians. The politicians blamed Albany. And Albany blamed Washington. Rohatyn's only tool was his reputation, and the reputation of the firm that employed him.

The solution Rohatyn engineered was the Municipal Assistance Corporation, known universally as MAC. Established on June 10, 1975, MAC was an independent corporation authorized to sell bonds to meet the city's borrowing needs. The concept was elegant in its simplicity: create a new credit entity, separate from the city government, that could borrow in capital markets where the city itself could not. MAC would issue its own bonds, backed by a dedicated stream of city sales tax revenue, and use the proceeds to refinance the city's crushing short-term debt into longer-term obligations.

Rohatyn served as MAC's chairman and insisted on reforms that were painful to every constituency. City employees faced a wage freeze. Thousands of municipal workers were laid off. The subway fare went up. The City University of New York, which had offered free tuition since 1847, began charging students for the first time. The unions screamed. The banks demanded more. The politicians blamed everyone except themselves.

What made Rohatyn's achievement remarkable was not just the financial engineering but the political brokering. He spent months in excruciating all-night negotiating sessions, extracting compromises from labor unions, banks, state government, and city officials. These were groups that had no reason to trust each other and every incentive to defect. The union leaders viewed the banks as predators. The banks viewed the politicians as irresponsible. The politicians viewed Albany and Washington as indifferent. And everyone viewed everyone else as negotiating in bad faith.

Rohatyn sat in the middle of this chaos, cajoling, threatening, and persuading. It took months and one cliff-hanger after another. This was classic Lazard: the trusted intermediary, sitting between warring parties, with no balance sheet exposure and therefore no conflict of interest. No one could accuse Rohatyn of having a hidden agenda, because Lazard had no loans to the city, no bonds to protect, and no trading positions to defend. His only interest was in solving the problem. New York City averted the bankruptcy that had seemed inevitable.

Under Rohatyn's chairmanship, MAC successfully sold ten billion dollars in bonds, restoring the city's access to capital markets. Rohatyn remained MAC chairman for twenty years, overseeing the city's financial recovery through the 1980s and into the mid-1990s. He became a local and national hero, the man who saved New York. He later served as U.S. Ambassador to France from 1997 to 2000 under President Clinton, a fitting appointment given Lazard's deep Franco-American roots. He was awarded the Commander of the French Legion of Honour. Rohatyn died on December 14, 2019, at age ninety-one. Lazard commemorated his legacy with the Felix G. Rohatyn Rooms at its New York headquarters.

The NYC bailout did something for Lazard that no amount of advertising could have achieved. It cemented the firm's reputation as the place you called when the problem was truly impossible, when the stakes were existential, and when you needed someone who could sit in a room with every hostile party and walk out with a deal. That reputation proved to be worth far more than any balance sheet.

Meanwhile, the 1980s brought the leveraged buyout boom, and Lazard rode the wave. The firm advised on some of the era's largest transactions, working both sides of the takeover wars that defined the decade. Goldman Sachs and Morgan Stanley were building massive M&A machines with hundreds of bankers, armies of analysts, and dedicated capital. Lazard competed with a fraction of the headcount, relying on the sheer quality of its senior partners and the gravitational pull of its brand. It was artisanal banking in an increasingly industrial age, and the question of whether that model could survive was already being whispered in boardrooms and trading floors across Manhattan.

The Bruce Wasserstein Era: From Partnership to Public Company

By the late 1990s, the investment banking industry was consolidating at a furious pace. Citigroup merged with Travelers. Deutsche Bank acquired Bankers Trust. UBS swallowed SBC Warburg. Everywhere you looked, balance sheets were getting bigger, product offerings broader, and the competitive pressure on independent firms more intense.

Lazard, still organized as a loose confederation of three semi-autonomous partnerships, faced a genuine existential question: could a pure advisory firm survive in a world of financial supermarkets?

The answer, or at least the man brought in to provide one, was Bruce Wasserstein. Born on Christmas Day, 1947, Wasserstein was one of the most famous M&A bankers of his generation. At First Boston in the 1980s, he and Joseph Perella had built the most formidable hostile takeover advisory practice on Wall Street. The nickname "Bid 'em up Bruce" captured his aggressive philosophy: in takeover battles, he consistently counseled clients to raise their offers, arguing that the winner of an acquisition contest was the one willing to pay the most. Key deals included Revlon's takeover fight, Texaco's ten-billion-dollar acquisition of Getty Oil, and the advisory role on the twenty-six-billion-dollar KKR-Nabisco leveraged buyout, at the time the largest deal in history.

In 1988, Wasserstein and Perella left First Boston to found Wasserstein Perella & Co. In September 2000, they sold it to Dresdner Bank for approximately 1.4 billion dollars, of which 650 million went to Wasserstein personally. With that fortune in hand, Wasserstein was recruited by Michel David-Weill, the grandson of David David-Weill and the dominant partner of Lazard for decades. David-Weill had been trying to lure Wasserstein for eighteen months. In early 2002, Wasserstein joined Lazard as CEO, reportedly using a portion of his 650 million to purchase a substantial ownership stake from David-Weill, fundamentally shifting the firm's power dynamics.

Wasserstein's arrival was a cultural earthquake. For over 150 years, Lazard had operated as three separate partnerships, each with its own culture, management, and economics. The houses had been formally unified in 2000 as Lazard LLC under Michel David-Weill's leadership, but true integration required Wasserstein's iron hand.

He centralized decision-making, imposed a more unified corporate identity, and hired aggressively. Approximately fifty high-profile bankers were brought on board with guaranteed bonuses totaling an estimated fifty million dollars. He clashed openly with legacy partners who resented the loss of the firm's genteel, secretive culture. Senior partners who had spent decades operating with near-total autonomy suddenly found themselves reporting to a CEO who demanded accountability, results, and, above all, revenue growth. Several prominent partners departed in frustration.

The internal dynamics during this period were intense. Wasserstein and David-Weill, who had recruited him, quickly found themselves in a power struggle. David-Weill represented the old-world partnership ethos: discretion, family control, consensus. Wasserstein represented the new Wall Street: aggressive, deal-driven, and impatient with tradition. The tension between them played out in boardrooms and hallways, and it was Wasserstein who prevailed. William Cohan's book "The Last Tycoons" documented the drama in exhaustive detail, portraying a firm riven by generational and cultural conflict even as it was being dragged into the modern era.

The crowning achievement of Wasserstein's tenure was the 2005 IPO. Lazard Ltd was incorporated in Bermuda on October 25, 2004, as the holding company for the firm's operations. The Bermuda structure was chosen for tax efficiency, with Lazard electing to be treated as a partnership for U.S. federal income tax purposes, meaning shareholders received K-1 tax forms rather than simpler 1099s. On May 5, 2005, Lazard completed its initial public offering on the New York Stock Exchange, pricing shares at twenty-five dollars and selling approximately thirty-four million shares. The equity offering raised roughly 850 million dollars, with concurrent offerings of 287.5 million in equity security units and 550 million in senior unsecured notes placed privately.

The IPO was controversial within the partnership. Many partners resented the loss of privacy and the dilution of the exclusive partnership culture. For decades, Lazard had been a place where compensation was secret, governance was opaque, and the partners answered to no one but each other. Going public meant quarterly earnings calls, mandatory disclosure of executive compensation, Sarbanes-Oxley compliance, and the relentless scrutiny of public market analysts. For a firm that had cultivated mystique as a competitive weapon, transparency felt like surrender.

But the IPO was necessary. The firm needed permanent capital to compete in a consolidating industry, and the fractious three-house partnership needed a single corporate governance structure to function in the modern world. Wasserstein also committed to reducing the compensation ratio from 74 percent of revenue in 2004 to 57.5 percent, a promise that signaled to public market investors that Lazard could be run as a disciplined corporation, not merely a collection of highly paid individuals dividing the spoils. The broader Wall Street community remained skeptical. "Can you really value an advice business?" was the question on everyone's lips. Advisory firms had no hard assets, no recurring revenue in the traditional sense, and their most valuable "assets" could resign at any time. The IPO priced at the low end of expectations, but it got done. That was what mattered.

The financial crisis of 2008-2009 was, paradoxically, Lazard's vindication. While bulge-bracket banks were drowning in toxic assets, facing existential balance sheet crises, and watching their stock prices crater, Lazard had no toxic assets. No balance sheet risk. No proprietary trading losses. It was pure advisory, and in a crisis, companies and governments needed advice more than ever.

Lehman Brothers collapsed. Bear Stearns was sold in a fire sale. AIG required the largest government bailout in American history. The firms that had built their empires on leverage, on the very balance-sheet-intensive businesses that Lazard had always eschewed, were fighting for survival. Lazard, meanwhile, found itself advising on some of the most consequential transactions of the era: restructurings, distressed sales, and government interventions. The advisory model that skeptics had dismissed as too small, too niche, and too antiquated looked, in the harsh light of the crisis, like the smartest business model on Wall Street.

Lazard also spun off its broker-dealer business, Lazard Capital Markets, in connection with the IPO, further clarifying the firm's identity as a pure advisory and asset management platform. The message to investors was unmistakable: Lazard was not trying to be a mini-Goldman. It was betting its future on the proposition that advice, delivered by the best people in the world, was a business worth owning.

Then, on October 11, 2009, Bruce Wasserstein suffered sudden cardiac arrhythmia while riding in a chauffeur-driven car en route to lunch with his daughter Pamela. He was rushed to the hospital and placed on life support. Three days later, on October 14, 2009, he died at age sixty-one. His net worth at death was estimated at 2.3 billion dollars, making him the 190th wealthiest American according to Forbes. The Wasserstein family's stake in Lazard, which had originated from an investment of roughly thirty million dollars, was worth approximately six hundred million. But the man who had taken Lazard public, unified its three houses, and bet his reputation on transforming a nineteenth-century partnership into a modern corporation was gone.

The Ken Jacobs Stabilization and Modern Lazard

Kenneth M. Jacobs was appointed Chairman and CEO of Lazard on November 17, 2009, just one month after Wasserstein's death. Jacobs was the continuity candidate, a longtime insider who had been with the firm since the 1980s, serving as Deputy Chairman and head of the North American advisory business. His mandate was clear: stabilize the firm after the shock of losing its CEO, restore morale among partners who had been buffeted by years of cultural upheaval, and navigate the aftermath of the worst financial crisis since the Great Depression.

Jacobs was, in many ways, the antithesis of Wasserstein. Where Wasserstein had been flamboyant, aggressive, and transformative, Jacobs was measured, institutional, and focused on steady execution. He was the builder, not the visionary, the operator who took the platform Wasserstein had created and made it work.

Over his nearly fourteen-year tenure, he expanded Lazard's advisory business into power and energy, technology, and healthcare, adding sector expertise that deepened the firm's relevance to a broader set of corporate clients. He built the restructuring practice into a top-tier franchise, recognizing that a firm without a balance sheet could thrive in precisely the environments where balance-sheet-dependent banks struggled. When the economy weakened and companies defaulted, Lazard was there to advise, free from the conflicts that plagued lender-advisors.

He pushed into sovereign advisory, advising governments around the world on debt restructurings, privatizations, and economic policy, leveraging Lazard's unique combination of financial expertise and geopolitical sophistication. The sovereign franchise was a competitive moat that no other boutique possessed in comparable depth. When countries like Greece, Argentina, or Ecuador needed to restructure billions of dollars of sovereign debt, the list of credible advisors was vanishingly short, and Lazard was on it.

On the asset management side, Jacobs maintained what had grown into a roughly two-hundred-to-two-hundred-fifty-billion-dollar platform in Lazard Asset Management. This was always the more complicated part of the story.

LAM managed money primarily in active equity and fixed income strategies with a pronounced international and emerging markets tilt. As the relentless shift from active to passive investing compressed fees across the industry, LAM faced persistent outflow challenges. The business generated stable, recurring management fee revenue, which provided ballast against the cyclicality of advisory fees, but it also required constant defense against the gravitational pull of index funds and ETFs. Whether asset management was a core strategic asset or a distraction from the purity of the advisory model was a debate that would persist throughout Jacobs' tenure and into the Orszag era.

Jacobs also refined the advisory model in important ways. He emphasized the senior banker model, where Vice Chairmen and Managing Directors personally did deals rather than delegating to junior associates. This was a meaningful differentiation point against bulge-bracket banks, where a CEO might meet the senior banker during the pitch but then find the actual work being done by a team of twenty-five-year-old analysts. At Lazard, the senior partner who pitched the deal was the senior partner who executed it.

He reinforced Lazard's positioning as a conflict-free adviser: no lending, no underwriting, no proprietary trading meant no conflicts. In an era when regulators and boards were increasingly scrutinizing adviser conflicts, particularly after the financial crisis had revealed just how conflicted some of the bulge-bracket advice had been, this was a genuine competitive advantage.

The competitive landscape shifted significantly during Jacobs' tenure. Evercore, founded by Roger Altman in 1995, grew into a formidable rival, eventually surpassing Lazard in pure advisory revenue. Centerview Partners, PJT Partners, and Moelis emerged as credible boutique competitors, each founded by teams that had defected from larger institutions. Meanwhile, Goldman Sachs, JPMorgan, and Morgan Stanley continued to dominate league tables by pairing advisory with balance-sheet firepower.

Lazard's response was to lean into what made it different: cross-border expertise born from the three-house legacy, sovereign advisory depth that no competitor could match, and the Lazard brand itself, 175 years of accumulated trust and prestige. The strategy was essentially to compete on quality and reputation rather than on scale or bundled offerings. Whether that strategy was sufficient to maintain market share over the long term was an open question that Jacobs' successor would need to answer.

The financial performance under Jacobs reflected both the strengths and limitations of the advisory model. In good M&A years, revenue surged and margins expanded. In downturns, revenue dropped sharply but the lack of balance sheet exposure meant there were no catastrophic losses. The cyclicality was the price of asset-light purity. Jacobs managed this tension by building countercyclical businesses, particularly restructuring, that generated fees when the M&A market dried up. The restructuring franchise became one of the strongest on Wall Street, advising distressed companies, sovereign debtors, and creditor committees through some of the most complex workouts of the post-crisis era.

Jacobs also recognized that the world of private equity had fundamentally changed the M&A landscape. PE firms were no longer niche operators doing occasional leveraged buyouts. They had become the dominant acquirers in many sectors, deploying trillions of dollars of capital and generating massive advisory fee pools. Lazard positioned itself as the preferred conflict-free adviser to PE firms on sell-side M&A, portfolio company advisory, and capital structure optimization. This private capital advisory business grew steadily under Jacobs and would later become one of Orszag's key growth levers.

Jacobs served as CEO from November 2009 through September 2023, when he transitioned to Executive Chairman. Effective December 31, 2024, he became Senior Chairman, relinquishing his board seat. His tenure was not flashy, but it was effective. He kept Lazard independent, relevant, and profitable through one of the most turbulent periods in financial industry history. The firm he handed to his successor was fundamentally stronger than the one Wasserstein had left behind: more global, more diversified by practice area, and better positioned for the multidisciplinary advisory world that was emerging.

The Peter Orszag Pivot: Financial Advisory 2.0

On May 26, 2023, Lazard announced that Peter R. Orszag would succeed Ken Jacobs as CEO, effective October 1, 2023. The choice surprised Wall Street.

Orszag was not a career banker. He was an economist with a PhD from the London School of Economics, a Marshall Scholar who had spent his early career in the corridors of academic economics and government policy. He had served as a Special Assistant to the President for Economic Policy under Clinton, as Director of the Congressional Budget Office under Bush, and as Director of the Office of Management and Budget under President Obama, where he served as a key architect of the Affordable Care Act.

His path to Lazard's corner office ran through Citigroup, where he had served as Vice Chairman of Corporate and Investment Banking, and then Lazard itself, which he had joined in May 2016 as Vice Chairman of Investment Banking. His resume was unlike that of any other Wall Street CEO: it read more like a cabinet secretary's biography than a deal sheet.

The question everyone asked was obvious: why would Wall Street's most prestigious advisory firm hand the keys to an economist rather than a deal jockey?

The answer revealed something important about where Lazard believed the advisory business was heading. Orszag had risen rapidly through Lazard's ranks after joining in May 2016 as Vice Chairman of Investment Banking. He was named Global Co-Head of Healthcare in 2018, then Head of North American M&A, then CEO of the Financial Advisory business in April 2019. His trajectory was unusual but not accidental: at each step, he demonstrated that deep policy expertise could be translated into advisory mandates.

Orszag's thesis was that advisory work was becoming fundamentally more complex and multidisciplinary. The days when M&A advice meant running a DCF model and calling five potential buyers were over. Modern advisory required understanding geopolitics, regulatory complexity, antitrust resurgence, energy transition, healthcare policy, and sovereign risk. It required, in short, exactly the kind of cross-disciplinary thinking that Orszag embodied. His background, bridging government, academia, and finance, was not a liability. It was the product differentiation.

One of Orszag's first major strategic moves was creating Lazard Geopolitical Advisory in 2022, hiring former UK national security adviser Stephen Lovegrove in September 2023 and building a dedicated team to help clients navigate the intersection of geopolitics and capital markets. In an era of U.S.-China decoupling, Russia sanctions, Middle East instability, and the reshoring of supply chains, this was not a boutique add-on. It was a recognition that every major deal now had a geopolitical dimension.

Orszag articulated an ambitious long-term plan called "Lazard 2030." The targets were bold: double revenue by 2030 from the approximately 2.4 billion dollar baseline in 2023, deliver 10 to 15 percent annual shareholder returns, and add 10 to 15 net Managing Directors per year.

The execution so far has been impressive. In 2025, the firm hired twenty-one new MDs, more than double the eleven hired in 2024, putting it well ahead of the plan. Revenue per Managing Director reached 8.9 million dollars in 2025, surpassing the 8.5 million target that had been set for that year. Orszag noted in early 2026 that the firm was "ahead of schedule" on its 2030 targets.

Geographic expansion accelerated, with new offices in the Middle East and Denmark and reinforced presence in North America and Europe. The Middle East push was particularly noteworthy: as sovereign wealth funds in the Gulf states deployed hundreds of billions of dollars into global assets, having local presence in Riyadh and Abu Dhabi was becoming essential for any serious advisory firm.

Orszag also flagged AI as "a massive focus for Lazard moving forward," signaling investment in technology platforms and data analytics that could enhance the productivity of the firm's advisory teams.

The financial results under Orszag have been striking. 2023 was a trough year, reflecting the global M&A drought and transition costs, with Financial Advisory revenue dropping 18 percent to 1.36 billion dollars. The GAAP net income for 2023 was actually negative, at minus seventy-five million dollars, a reminder of just how punishing the cyclical downturns can be for an advisory-dependent firm.

But 2024 delivered a powerful recovery: adjusted advisory revenue surged 28 percent to 1.73 billion dollars. The M&A market thawed, and Lazard captured what Orszag described as market share gains.

And 2025 was a record: adjusted Financial Advisory revenue reached 1.825 billion dollars, the highest in the firm's history. Asset management also inflected positively, with AUM reaching 254 billion dollars, up 12 percent year over year, driven by record gross inflows and market appreciation. Full-year adjusted net revenue hit 3.03 billion dollars. Adjusted net income was 266 million dollars, or 2.44 per diluted share.

Perhaps the most consequential structural change under Orszag's watch was the January 2024 conversion from Lazard Ltd, a Bermuda exempted company treated as a partnership, to Lazard Inc., a Delaware C-corporation. This deserves explanation because it mattered enormously for investors.

The original Bermuda structure, created for the 2005 IPO, had Lazard issue K-1 tax forms to its shareholders rather than the standard 1099 forms that most public companies issue. K-1s are more complex to process, require additional accounting work at tax time, and, critically, many large institutional investors, including pension funds, endowments, and certain mutual funds, are prohibited by their charters from holding securities that issue K-1s. This meant that a large universe of potential investors simply could not own Lazard stock.

The "domestication" to a Delaware C-corporation eliminated the K-1 issue, broadened the eligible investor base, and enhanced trading liquidity. Each share converted one-for-one. Effective January 1, 2025, Orszag added the Chairman title, consolidating leadership as Jacobs stepped into the Senior Chairman role.

The board also brought in fresh perspectives. Dan Schulman, the former CEO of PayPal, was appointed Lead Independent Director, and Stephen R. Howe Jr., the former chairman of Ernst and Young, joined as well. The new asset management CEO, Chris Hogan, was named in December 2025 with a mandate to reverse the long-running outflow narrative and position LAM for the next phase of growth.

Private capital advisory emerged as a particular growth engine. Revenue from advising private equity firms, infrastructure funds, and other alternative capital providers grew to represent over 40 percent of total advisory revenue in 2025, up from roughly 25 percent historically and 33 percent in 2023. This was a deliberate strategic pivot: as PE firms became the dominant acquirers in many sectors, Lazard positioned itself as their preferred conflict-free adviser. The logic was compelling: PE firms needed external advisory precisely because they operated on the buy side. They could not credibly advise themselves on the sale of portfolio companies, and they increasingly needed independent counsel on valuations, structuring, and regulatory strategy.

Lazard also largely sat out the SPAC boom of 2020-2021, a decision that looked like discipline or a missed opportunity depending on your vantage point. While competitors reaped massive fees from the SPAC frenzy, Lazard stayed on the sidelines. In retrospect, given the wreckage that many SPAC deals subsequently inflicted on investors, the decision looks wise. It was consistent with the firm's longstanding instinct to prioritize reputation over short-term revenue, the same instinct that had kept Lazard out of proprietary trading, leveraged lending, and every other balance-sheet-intensive activity that periodically blew up its competitors.

The Business Model: How Lazard Actually Makes Money

To understand Lazard, you have to understand the economics of selling advice. It is a business model of elegant simplicity and maddening cyclicality.

At its core, Lazard is a people factory that converts relationships and intellectual capital into fees. There are no raw materials, no supply chains, no manufacturing processes. The only inputs are talented human beings and the brand that attracts clients to them. The firm has two business segments, and the interplay between them defines everything about the investment case.

Financial Advisory generates roughly 60 percent of revenue. This is M&A advice, restructuring, capital markets advisory, shareholder advisory (defending against activist campaigns), sovereign advisory, and the newer geopolitical advisory. Fees are primarily success-based, typically 0.5 to 2 percent of deal value for M&A, with higher percentages on smaller deals and lower on mega-transactions. On a one-billion-dollar deal, a two-percent fee means twenty million dollars. On a ten-billion-dollar deal, the percentage drops but the absolute fee is still enormous.

Restructuring fees tend to be structured as retainers plus success fees, providing some revenue stability even when M&A markets are frozen. This is the countercyclical insurance policy that makes Lazard's model more resilient than it might otherwise appear: when the economy weakens and companies get into trouble, restructuring revenue rises.

The economics are straightforward: senior bankers develop relationships with CEOs and boards, those relationships generate mandates, mandates generate fees. There is no inventory, no balance sheet, no cost of goods sold in any traditional sense. The primary cost is compensation. This is a business of pure human capital.

Asset Management generates approximately 40 percent of revenue and manages 254 billion dollars in assets as of year-end 2025, up 12 percent from the prior year. Lazard Asset Management has a pronounced tilt toward international and emerging market equities, with 67 percent of AUM denominated in non-U.S.-dollar securities. This international orientation is a legacy of the firm's European roots and differentiates it from most American asset managers, which tend to be heavily weighted toward domestic equities.

Management fees, the annuity-like revenue stream generated by basis point charges on AUM, totaled 1.1 billion dollars in 2025. Think of management fees as the subscription revenue of the asset management world: as long as assets stay in the fund, fees accrue automatically. The asset management business provides critical diversification against the cyclicality of advisory fees. When M&A markets freeze, as they did in 2023, management fees provide steady income. But the business faces structural headwinds from the active-to-passive investing shift, which has compressed fees across the industry.

The talent model is where Lazard's economics get interesting and where the firm's competitive position becomes most fragile. Top bankers are the product. They are the ones with the CEO relationships, the industry expertise, and the deal judgment. This gives them immense leverage. A single senior partner at Lazard might personally generate twenty to fifty million dollars in annual advisory fees. If that partner leaves, those fees often leave with them.

The firm's adjusted compensation ratio runs around 60 percent of revenue, meaning roughly sixty cents of every dollar Lazard earns goes to pay its people. The firm employed approximately 3,309 people at the end of 2025, and average compensation per employee reached 630,000 dollars. But that average masks enormous variation: a junior analyst might earn 200,000 dollars while a senior Managing Director could take home several million.

This is the fundamental tension of the advisory business: the primary "asset" walks out the door every night. Retention is not a human resources concern at Lazard. It is an existential one. The firm's ability to recruit and retain top talent while managing compensation costs is the single most important operational challenge it faces, and it is a challenge that never ends.

Lazard's competitive differentiation among independent advisory firms rests on several pillars.

First, it is the only elite independent with both a major advisory franchise and a major asset management platform, a dual structure that Evercore, PJT Partners, and Centerview lack. This dual platform provides revenue diversification that pure-play advisory firms do not enjoy.

Second, it is genuinely global, with deep presence across the U.S., Europe, the Middle East, and Asia, while most boutiques remain North America-centric. For a multinational corporation contemplating a cross-border acquisition involving regulatory approvals in five countries, Lazard's global footprint is a genuine advantage.

Third, its sovereign advisory franchise, built over decades of advising governments on debt restructurings and privatizations, has no peer among the independents. When a country needs to restructure its debt, the list of credible advisors is short. Lazard has been on that list for decades.

Fourth, its 177-year brand, a cumulative asset that cannot be replicated, carries signaling value: when a board hires Lazard, it signals to shareholders, regulators, and counterparties that it is serious about the transaction and the quality of advice it is receiving.

The geographic footprint deserves attention because it is genuinely different from what most boutiques offer. Lazard operates in over forty cities across more than twenty-five countries. This is a legacy of the three-house structure: when you have had offices in Paris, London, and New York for over a century, you develop relationships and cultural fluency that cannot be built overnight. For cross-border M&A, where understanding regulatory environments, cultural norms, and political dynamics in multiple jurisdictions simultaneously is essential, Lazard's global network is a genuine competitive advantage. Most boutiques, even successful ones like Evercore and PJT Partners, remain heavily North America-centric.

The choice to remain asset-light, to never build a balance sheet, was not passive. It was deliberate and it was costly. Lazard cannot offer financing packages to win mandates. It cannot provide the "one-stop-shop" that Goldman Sachs or JPMorgan can. In competitive pitches for large M&A mandates, the bulge brackets can and do offer below-market financing to sweeten advisory engagements, a subsidy that no independent can match. Lazard's counter-argument is straightforward: "Advisory firms providing acquisition financing and engaging in significant proprietary trading can develop conflicts with advisory clients." In an era of heightened regulatory scrutiny and corporate governance sensitivity, this is not merely a marketing slogan. It is a genuine competitive advantage.

Competitive Landscape and Strategic Positioning

The independent advisory landscape has never been more competitive. To understand Lazard's position, you need to understand its peers.

Evercore, founded by Roger Altman in 1995, has grown into the largest independent advisory firm by revenue, generating approximately 2.9 billion dollars in total investment banking and equities revenue in 2024 and ranking number one among independents for advisory revenues. Evercore is North America-focused, considered the strongest domestic advisory franchise, and has surpassed Lazard in pure advisory revenue. Evercore was named "Best Bank for Independent Advisory in North America" by Euromoney in 2025. But Evercore lacks Lazard's asset management platform, sovereign advisory depth, and European presence.

Centerview Partners, a private partnership, does not disclose revenue but is considered the most elite advisory boutique by deal size and selectivity. Centerview focuses on the very largest, most complex M&A transactions, maintaining an extremely lean partner count with extraordinarily high revenue per partner. Where Lazard and Evercore are broad platforms covering many industries and geographies, Centerview is a rifle shot: fewer deals, bigger fees, and an obsessive focus on the transactions that move markets.

PJT Partners, founded in 2015 by Paul Taubman after spinning out of Blackstone, has grown rapidly, moving from seventh to fifth in independent advisory rankings, with particular strength in restructuring. PJT's average compensation per head was approximately 903,000 dollars in 2024, the highest among the publicly traded independents and a marker of the intense competition for talent.

Moelis and Company, founded by Ken Moelis in 2007, is strong in mid-cap M&A advisory and has built a global platform, though smaller than Lazard and Evercore. And Rothschild, which completed 351 M&A transactions in 2024, 43 percent more than its closest independent rival, dominates European and cross-border advisory but went private under family control in 2023, removing itself from the publicly traded competitive set.

The bulge-bracket banks remain the eight-hundred-pound gorillas. Goldman Sachs generated roughly 3.7 billion dollars in advisory and investment banking revenue in 2024. Goldman, JPMorgan, and Morgan Stanley can offer what no independent can: balance-sheet firepower. They provide acquisition financing, bridge loans, and capital markets execution alongside advisory mandates, creating a bundled offering that is difficult to unbundle.

Consider a typical mega-deal scenario. A Fortune 500 company wants to acquire a competitor for fifteen billion dollars. Goldman Sachs can offer advisory, provide the bridge financing, arrange the bond issuance, and execute the stock offering, all under one roof. Lazard can offer only the advisory. In theory, the Goldman offering is more compelling. In practice, many boards worry that Goldman's lending relationship creates conflicts: if Goldman has fifteen billion dollars of credit exposure, can it truly give objective advice about whether the acquisition makes sense? This conflict concern is the crack in the bulge-bracket armor through which every independent boutique has built its business.

The independent boutiques exist in these cracks, thriving when clients prioritize conflict-free advice over one-stop convenience.

Private equity represents a fascinating dual dynamic for Lazard. PE firms are massive clients, generating sell-side M&A mandates, portfolio advisory fees, and capital structure work. But they are also, increasingly, competitors. The largest PE firms have built internal M&A teams that handle smaller transactions in-house, and some have launched advisory businesses that compete directly with independent firms. Lazard's positioning, conflict-free, independent, with no competing fund management business, gives it an edge in this relationship. But the dynamic is evolving, and the line between client and competitor grows blurrier with each passing year.

The "barbell" trend in advisory is real: the market is consolidating around bulge brackets at one end and elite boutiques at the other, with mid-tier firms getting squeezed. For Lazard, the strategic question is whether its dual-platform model (advisory plus asset management) is a strength or a distraction. The asset management business provides revenue diversification and recurring fee income but has faced persistent outflow pressure. Orszag has signaled interest in acquisitions in private credit, infrastructure, and real estate to refresh the asset management offering, a pivot that could either strengthen the dual platform or dilute the advisory brand.

Porter's Five Forces: The Advisory Industry

Understanding Lazard's competitive position requires examining the structural forces shaping the advisory industry. Porter's Five Forces framework, which assesses the competitive dynamics of any industry by looking at five key pressures, provides a useful lens.

The threat of new entrants is moderate. On one hand, advisory requires no balance sheet, no regulatory capital, and minimal physical infrastructure. Any group of senior bankers can hang out a shingle, and they frequently do. Every year, new boutiques are launched by defecting teams. The history of the advisory industry is, in some ways, a history of spin-offs: Wasserstein left First Boston to start Wasserstein Perella. Taubman left Morgan Stanley to start PJT Partners. Ken Moelis left UBS to start Moelis and Company.

On the other hand, the barriers that matter, brand, relationships, and talent, take decades to build. You can start an advisory firm in a week. You cannot build a Lazard in a lifetime.

The bargaining power of suppliers, meaning talent, is high. Top bankers are the product, and they know it. Public company disclosure of compensation creates a transparent market for talent, making poaching easier. The limited pool of senior bankers who can credibly advise on multi-billion-dollar transactions gives those individuals immense leverage. Retention is the existential challenge of every advisory firm, and the firms that fail at it disappear.

The bargaining power of buyers, meaning corporate and institutional clients, is moderate to high. Corporates shop advisors aggressively, and fee pressure on smaller deals is intense. A company doing a five-hundred-million-dollar acquisition might interview five advisory firms and negotiate fees down to thirty or forty basis points. PE firms, which do deals repeatedly and can offer a stream of future mandates, are particularly aggressive negotiators.

But for mission-critical mega-deals, transformative mergers, hostile defense, or sovereign debt restructurings, clients are willing to pay premium fees for the best advice. When the deal determines the fate of the company, fee sensitivity drops dramatically. Relationship stickiness matters: boards that have worked with a Lazard senior partner through one crisis tend to call the same person for the next one.

The threat of substitutes is moderate to low. Internal M&A teams at corporations have grown more sophisticated, reducing reliance on external advisors for smaller transactions. Management consultancies like McKinsey and BCG have encroached on strategic advisory, offering "strategic due diligence" and "merger integration planning" that overlaps with traditional investment banking advice. Law firms are doing more deal work, with M&A practices at top firms like Wachtell, Lipton, Rosen and Katz providing strategic counsel that sometimes rivals what advisory firms offer.

But for high-stakes decisions, where the outcome determines the fate of the company, external validation from a credible advisor remains essential. No board of directors wants to tell shareholders that it handled a ten-billion-dollar merger without hiring an independent financial advisor. The liability exposure alone, the risk of being sued by shareholders who allege the board did not fulfill its fiduciary duty, virtually guarantees continued demand for external advisory.

Competitive rivalry is high. The advisory market is fragmented, with many credible competitors. League tables, those obsessively tracked rankings of advisory firms by deal count and dollar volume, are a zero-sum game. Every mandate Lazard wins is one that Evercore, Goldman, or Centerview did not. Poaching wars are constant: a single senior banker with strong client relationships can shift millions of dollars in annual fee revenue by changing firms. Differentiation is genuinely difficult because everyone is selling the same thing: advice. The firms that win do so on the basis of relationships, brand, sector expertise, and the quality of their senior bankers, all of which are hard to sustain and easy to lose. The net takeaway from the Five Forces analysis is sobering: the advisory industry is structurally competitive, and Lazard's position, while strong, requires constant reinvestment in talent and brand to maintain.

Hamilton's Seven Powers: Lazard's Competitive Advantages

Hamilton Helmer's Seven Powers framework asks a more fundamental question than Porter: not just "is the industry attractive?" but "does the company have a durable competitive advantage?" The framework identifies seven potential sources of strategic power, and Lazard's position against each reveals a nuanced picture. The firm possesses some genuine powers but faces significant vulnerabilities.

Scale economies are weak. Advisory does not benefit from traditional scale the way that software or manufacturing businesses do. Adding more bankers does not reduce the cost of providing advice on any individual deal. Each deal requires the same amount of senior attention, the same due diligence, the same all-night negotiating sessions regardless of whether the firm has fifty Managing Directors or five hundred. There is some overhead leverage in technology, back-office functions, and research platforms, but talent costs, which are the dominant cost, scale linearly with headcount. This means Lazard cannot build the kind of cost advantages that manufacturing or technology companies enjoy.

Network economies are moderate. Relationship networks matter enormously in advisory. A banker who has advised the CEO of a major corporation will often receive the next mandate from that CEO, and introductions across the network generate deal flow. When a Lazard partner in Paris identifies an acquisition opportunity for a client that involves targets in New York, London, and Dubai, the firm's multi-office network can mobilize faster and more credibly than a boutique with a single office.

Lazard's geographic network, the legacy of the three-house structure, provides genuine cross-border network effects that most boutiques cannot replicate. But these networks are personal, not institutional. They live in individual bankers' heads and Rolodexes, not in Lazard's systems. When a senior banker retires or defects, the network goes with them.

Counter-positioning is moderate but fading. Historically, Lazard's absence of a balance sheet was a genuine counter-position against bulge-bracket banks. Goldman Sachs could not copy the pure-advisory model without abandoning its lending, trading, and principal investing businesses, which generated far more revenue than advisory. This gave Lazard a structural advantage in winning mandates from clients who valued conflict-free advice.

But the market has evolved. Boutiques have proliferated, and the counter-position is no longer unique to Lazard. Evercore, Centerview, PJT Partners, and Moelis all make the same conflict-free argument. What was once a distinctive stance has become an industry category. In Helmer's framework, counter-positioning is most powerful when the incumbent cannot respond without destroying its own business. That was true when Lazard was the only major conflict-free advisor. It is less true now that an entire ecosystem of boutiques has adopted the same positioning.

Switching costs are low to moderate. There is some relationship stickiness: boards that trust a Lazard senior partner will often return for the next deal. The best advisory relationships function almost like a retained law firm: the client calls the same banker year after year, building a deep understanding of the company's strategy, culture, and decision-making processes. Retainer-based relationships in restructuring and activist defense create recurring revenue that provides some predictability.

But fundamentally, it is easy to hire a different advisor for the next transaction. There is no lock-in, no proprietary technology, no integration cost that prevents a client from walking across the street to Evercore or picking up the phone to call Centerview. Each deal is a new competitive pitch, and the mandate goes to whoever makes the most compelling case.

Branding is strong, and this is Lazard's primary power. The name "Lazard" carries 177 years of accumulated prestige, discretion, and deal heritage. It signals seriousness: when a board hires Lazard, it tells the world that the situation is consequential and the advice will be world-class.

This brand creates a virtuous cycle. The prestige attracts top talent. Top talent generates great deals. Great deals burnish the reputation. The burnished reputation attracts more top talent. And so on. It is a flywheel that has been spinning since Andre Meyer first picked up the telephone in his Rockefeller Center office in the 1940s. The only competitors with comparable brand equity in advisory are Goldman Sachs and Rothschild, both of which are also centuries-old institutions with deep heritage and global reach.

Cornered resource is moderate. Top banking talent is the critical resource, but it is not exclusive. Talent is mobile, and individual bankers can and do move between firms. The industry operates on a free-agent model that looks more like professional sports than traditional corporate employment. Some proprietary relationships and institutional knowledge provide advantages, but information asymmetries are declining as data becomes more widely available. Bloomberg terminals, public filings, and AI-powered analytics have democratized much of the information that used to be exclusive to the top advisory firms.

Process power is moderate. Lazard has accumulated decades of deal experience and pattern recognition. A partner who has advised on fifty restructurings has seen almost every conceivable scenario and can pattern-match more quickly than a less experienced competitor. The junior-to-senior apprenticeship model transmits institutional knowledge across generations, as younger bankers learn by watching their seniors negotiate, structure, and close deals. But this knowledge lives in people's heads, not in codified processes. It is not as defensible as a manufacturing process or a software algorithm. You cannot patent the ability to read a boardroom.

The overall assessment is clear: Lazard's primary power is its brand, a reputational asset that compounds over decades but is ultimately fragile. It takes a century to build a Lazard, but it could take only a few years of poor deal execution or talent departures to undermine it.

Its secondary power is counter-positioning, though this is eroding as boutiques proliferate and the conflict-free argument becomes table stakes rather than differentiation.

Its primary weakness is the portability of its assets: the powers walk out the door with the bankers who embody them. Unlike a factory or a software platform, Lazard's competitive advantages are stored in human beings who can and do change employers. This fundamental fragility is the central risk of investing in any advisory firm, and it is a risk that can never be fully mitigated.

Bear versus Bull: The Investment Thesis

The bear case for Lazard begins with cyclicality. Advisory revenue can drop 30 to 40 percent in a downturn, as it did in 2023, and the firm's cost structure, dominated by highly compensated senior bankers, is difficult to cut. You cannot lay off the senior partners who generate the deals. This creates operating deleverage in bad years that is painful for shareholders.

The asset management business faces structural headwinds from the passive investing revolution, and while 2025 showed improvement, with record gross inflows and AUM rising to 254 billion dollars, the long-term trend toward fee compression and outflows from active strategies is unlikely to reverse. Lazard Asset Management's pronounced tilt toward international and emerging market equities means it is also exposed to currency movements and geopolitical risk in ways that a domestic index fund is not.

Talent risk is ever-present: the public company structure, with its mandatory compensation disclosure, makes it easier for competitors to identify and recruit Lazard's best bankers. Average compensation per employee reached 630,000 dollars in 2025, which sounds generous until you compare it to the 830,000 per head at Evercore or the 903,000 at PJT Partners. Boutique proliferation means that every year brings new competitors, often founded by teams that defected from existing firms. And the philosophical question lingers: can you build a durable moat around a business where the primary asset is human judgment? The answer is, at best, uncertain.

The technology question deserves special attention. Will AI commoditize advisory work? The bear argument is that large language models and data analytics platforms could eventually replicate much of what junior and mid-level bankers do: building financial models, conducting comparable company analyses, drafting pitch books, and screening potential targets. If that happens, the pyramid model of advisory, in which a few senior bankers are supported by large teams of junior analysts, could collapse, putting pressure on fees across the industry. The counter-argument is that high-stakes M&A advisory is fundamentally about human judgment, relationship trust, and the ability to read a room during a contentious board meeting. No AI can tell a CEO whether to accept a hostile bid. That judgment call, and the reputation that backs it, is what clients pay for. Both sides of the technology argument have merit, and the resolution will likely play out over the next decade.

The bull case is equally compelling. Advisory sits at the center of an oligopoly: the top ten global advisors dominate deal flow, and breaking into that elite circle requires decades of brand-building that no startup can shortcut. Restructuring revenue is countercyclical, providing natural hedging against M&A downturns. When interest rates rose sharply in 2022 and 2023, many overleveraged companies found themselves unable to service their debt. This generated a wave of restructuring mandates that partially offset the decline in M&A advisory revenue. Lazard's restructuring franchise, which ranks among the strongest on Wall Street alongside PJT Partners and Houlihan Lokey, was well positioned to capture this demand.

Geopolitical complexity is increasing, not decreasing. U.S.-China decoupling, energy transition, supply chain reshoring, antitrust resurgence, and sovereign debt stress all drive demand for the kind of sophisticated, multidisciplinary advice that Lazard under Orszag is explicitly positioning to provide. In a simpler world, M&A advice was primarily a financial exercise. In the current world, every major transaction has regulatory, geopolitical, and policy dimensions that require expertise beyond traditional investment banking.

The asset-light model means no balance sheet risk, high return on invested capital, and the ability to return substantial capital to shareholders. Lazard returned 393 million dollars to shareholders in 2025 through dividends and buybacks, a capital return that most asset-heavy businesses could only dream of. Because the firm needs almost no capital to operate, nearly all of its free cash flow after compensation can be distributed to shareholders. This makes Lazard one of the few financial services firms that functions more like a professional services partnership than a bank, even as it trades on a public exchange.

The brand, at 177 years old, has survived two world wars, the deaths of three transformative leaders, the complete restructuring of the financial industry, and the Great Financial Crisis. If it has not been destroyed by now, the odds are good that it endures. And secular drivers of M&A activity, technological disruption, industry consolidation, energy transition, and demographic shifts, suggest that the total addressable market for advisory will grow over the coming decades. The Lazard 2030 plan targets doubling revenue, and the firm is ahead of schedule on key metrics.

The two KPIs that matter most for tracking Lazard's performance going forward are straightforward to understand and easy to monitor.

The first is Financial Advisory revenue per Managing Director, which measures the productivity and quality of the firm's senior talent. This metric currently stands at 8.9 million dollars and has been trending upward under Orszag's leadership. If it continues to rise, it means Lazard is winning higher-quality mandates with better bankers. If it stagnates or declines, it means either the firm is hiring lower-productivity MDs or losing market share on the deals that matter most.

The second is the adjusted compensation ratio, which measures how much of the revenue pie goes to employees versus shareholders. It currently runs around 60 percent. This is the metric that tells you whether Lazard is being run as a business for shareholders or as an employment scheme for bankers. If the ratio rises above 65 percent, shareholders are subsidizing banker compensation. If it falls below 55 percent, the firm risks losing talent to competitors who pay more.

The Road Ahead

Lazard's stock price tells an interesting story in its own right. The shares were priced at twenty-five dollars at the 2005 IPO. They hit an all-time high closing price of fifty-eight dollars and one cent on November 6, 2024, during the M&A recovery, and traded around fifty-six dollars and eighty cents in early February 2026. The market capitalization stood at approximately 5.8 billion dollars. Over its two decades as a public company, Lazard had returned substantial capital to shareholders through dividends and buybacks, reflecting the cash-generative nature of the asset-light model. But the stock has also experienced the kind of cyclical drawdowns that make it a difficult hold during M&A downturns. The 52-week range as of early 2026 stretched from roughly thirty-two dollars to fifty-eight dollars, a nearly two-to-one range that underscores the cyclicality embedded in the business.

The near-term outlook for Lazard is shaped by the M&A recovery that began in 2024 and gained momentum in 2025. After two years of depressed deal activity, driven by rising interest rates, regulatory uncertainty, and geopolitical volatility, the M&A market showed clear signs of recovery.

If deal activity continues to accelerate, as most industry observers expect given the pent-up demand for transactions and the need for corporate portfolio rationalization, Lazard's advisory revenue should benefit. The Lazard 2030 plan targets a doubling of revenue, and the firm is ahead of schedule on key metrics like MD hiring and revenue per MD. The hiring of twenty-one net new Managing Directors in 2025 alone, well above the target of ten to fifteen per year, suggests Orszag is investing aggressively for growth.

The asset management business is showing early signs of inflection, with record gross inflows in 2025, though the active-versus-passive dynamic remains a structural headwind. The appointment of Chris Hogan as Asset Management CEO in December 2025 signaled a renewed commitment to the business.

The medium-term strategic questions are more interesting. Will Lazard remain a pure advisory and asset management firm, or will Orszag's interest in acquiring private credit, infrastructure, and real estate capabilities transform the platform into something broader? Bloomberg reported in mid-2024 that Orszag was eyeing acquisitions in these areas, a signal that the traditional advisory-plus-asset-management model may not be sufficient for the next decade of growth.

How large can the private capital advisory practice, already over 40 percent of advisory revenue, become? The global private equity industry manages trillions of dollars, and every deployment and exit requires advisory services. If Lazard can establish itself as the go-to conflict-free adviser for PE firms, this practice alone could be a multi-billion-dollar revenue stream.

And can the geopolitical advisory offering, still nascent, become a meaningful revenue contributor as the world grows more fragmented? The hiring of Stephen Lovegrove, the former UK national security adviser, in September 2023 signaled real commitment. But it remains to be seen whether geopolitical advisory can generate the kind of fee revenue that justifies the investment.

The long-term existential questions are the ones that have been asked about Lazard for decades: Can independence survive? Will a bulge bracket or private equity firm eventually acquire Lazard? Can human advisory survive AI disruption? Is the partnership ethos sustainable inside a public company shell?

Consider the acquisition question. At a market capitalization of roughly six billion dollars, Lazard is theoretically acquirable by any of the major bulge-bracket banks or the largest private equity firms. Goldman Sachs or JPMorgan could buy Lazard with a quarter's worth of profits. But what would they be buying? An advisory franchise whose value depends on the continued employment of a few hundred senior bankers, any of whom could walk out the door if the culture changed. A brand that derives its power precisely from independence, and which would lose that power the moment it was absorbed into a conflicted conglomerate. The most valuable thing about Lazard, its independence, would be destroyed by the act of acquiring it. This is, paradoxically, the firm's best defense against takeover.

These questions have no definitive answers. But they have been asked, in various forms, since 1848. And so far, through wars, financial crises, the death of leaders, and the complete transformation of the industry around it, the answer has always been the same: Lazard endures.

Lessons from Lazard

For builders of businesses, Lazard demonstrates that asset-light models can create enormous and enduring value. The Lazard brothers started with nothing more than a storefront and an instinct for intermediation. They never mined for gold, never built a factory, never manufactured a product. They moved value between parties and took a fee for the privilege. Nearly two centuries later, the firm they founded does exactly the same thing, albeit with bigger numbers and fancier offices. The lesson is that you do not need to own assets to build a durable enterprise. You need to own a reputation.

Brand, the most intangible of assets, is also the most durable competitive advantage in a people business. It takes decades to build and can be destroyed in months. Meyer understood this. Rohatyn understood this. Wasserstein understood this, even as he pushed the firm in directions that made the old guard uncomfortable. Independence is expensive to maintain but creates strategic optionality that diversified conglomerates cannot replicate. And culture, for better or worse, eats strategy, especially in businesses where the product is the judgment of the people who walk through the door each morning.