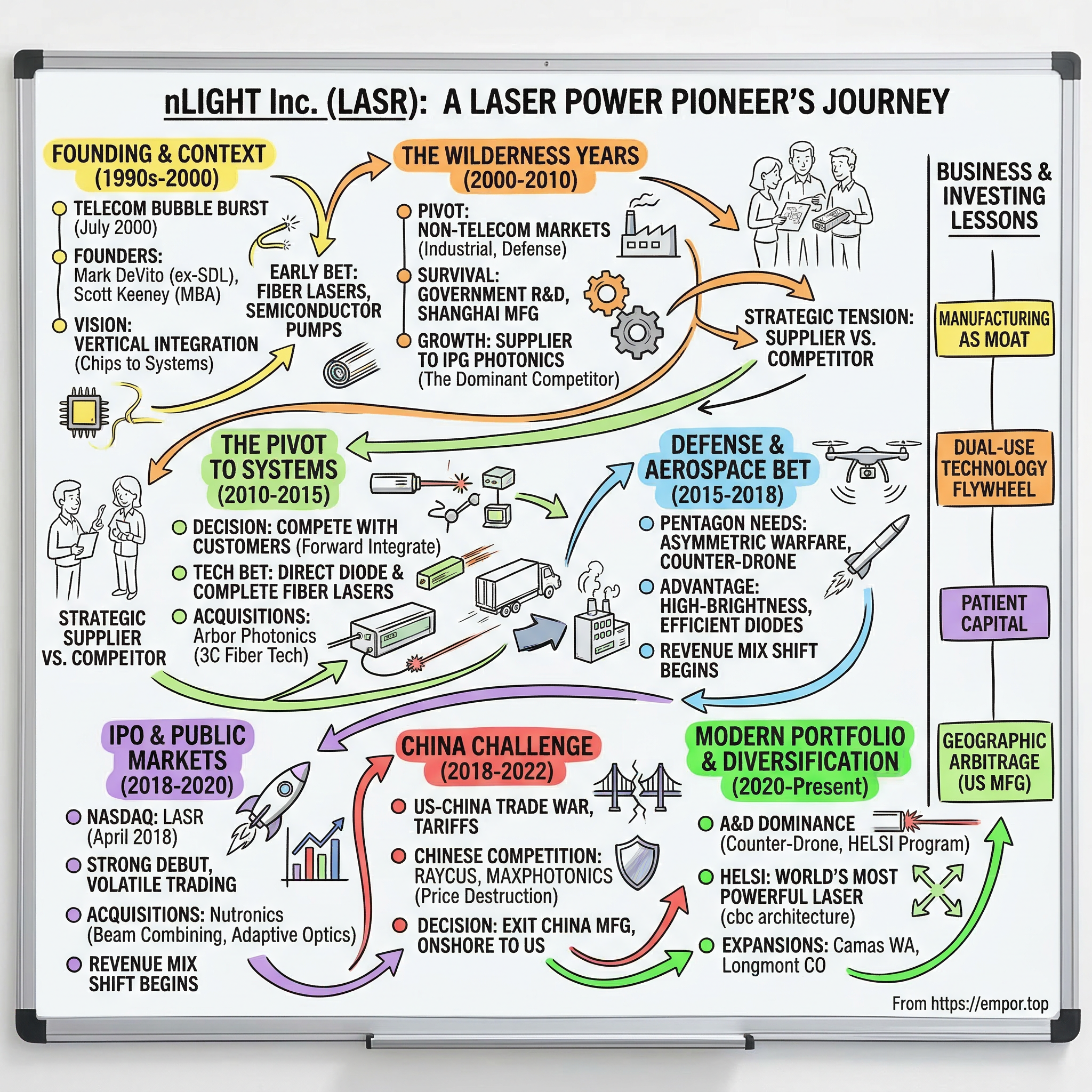

nLIGHT Inc.: The Story of America's Laser Power Pioneer

I. Introduction and Episode Roadmap

Somewhere in Camas, Washington — a small city of twenty-seven thousand people nestled along the Columbia River, better known for its paper mill than for cutting-edge photonics — sits a manufacturing facility that may be the most strategically important laser factory in the Western world. Inside, in cleanrooms maintained at Class 1000 purity, engineers grow semiconductor crystals atom by atom on gallium arsenide wafers, fabricate laser chips capable of producing hundreds of watts from a device smaller than a grain of rice, and assemble those chips into modules that power everything from the robots welding Tesla battery packs to prototype weapon systems designed to shoot drones out of the sky at the speed of light.

The company is nLIGHT. The ticker is LASR. And most people have never heard of it.

That anonymity is partly by design. For most of its twenty-five-year history, nLIGHT has operated as a component supplier — the company behind the company, the chipmaker inside the laser, the invisible layer in someone else's product. But a series of strategic pivots have transformed nLIGHT from a quiet photonics parts shop into something far more ambitious: a vertically integrated laser powerhouse that controls the technology stack from semiconductor wafer to megawatt weapon system.

The question at the heart of this story is one that would fascinate any student of competitive strategy: how did a scrappy photonics spin-out, founded in the summer of 2000 at the precise moment the telecom bubble was bursting, survive eighteen years as a private company, navigate the rise and dominance of a single competitor that controlled eighty percent of its market, endure the onslaught of Chinese manufacturers who cratered laser prices by fifty percent or more, and emerge in 2025 and 2026 as one of the most important companies in the directed energy weapons revolution?

The answer involves patience measured in decades. It involves a decision, taken around 2010, that violated the cardinal rule of component suppliers: never compete with your customers. It involves a founder who spent his career at the intersection of Harvard Business School strategy and frontier photonics, and who had the conviction to build manufacturing capability in the United States when every economic signal said to build it in Asia. And it involves a geopolitical transformation — the return of great power competition, the proliferation of cheap drones, and the Pentagon's sudden, urgent need for laser weapons — that turned nLIGHT's perceived weaknesses into its greatest strengths.

Three secular forces explain why this company matters right now. First, the manufacturing renaissance: industrial laser demand in the West is being driven by EV production, reshoring, and advanced manufacturing. Second, defense spending on directed energy weapons has shifted from science-fiction line items to multi-billion-dollar Pentagon priorities, with nLIGHT positioned as the only publicly traded, vertically integrated, pure-play directed energy laser source. Third, the U.S.-China technology competition has transformed nLIGHT's American manufacturing base from a cost disadvantage into a strategic moat that no Chinese competitor can cross and that even well-funded domestic entrants would need years to replicate.

The stock tells the convergence story in its own way: from an all-time low near six dollars in April 2025 to an all-time high above sixty-seven dollars in early March 2026. That tenfold move signals the market is beginning to understand what nLIGHT has been quietly building for a quarter century. This is a story about patience, about the rare courage to compete with your own customers, about the geopolitical forces that turned a cost disadvantage into a strategic moat, and about what happens when a technology that was always theoretically possible finally becomes militarily necessary.

II. The Photonics Revolution and Founding Context (1990s–2000)

To understand nLIGHT, you first need to understand what a semiconductor laser actually is — and why making one well is so extraordinarily difficult.

Think of it this way. A traditional laser, the kind you might picture from a James Bond movie, uses a tube of gas or a crystal rod to generate a beam of light. These work, but they are bulky, inefficient, and expensive to maintain. A semiconductor laser does the same job on a chip the size of a grain of rice. It takes electricity in and sends coherent light out. The physics are similar to an LED — the little light on your phone charger — except a semiconductor laser concentrates the light into a beam millions of times brighter and perfectly coherent, meaning every photon marches in lockstep.

The critical breakthrough that made modern industrial lasers possible was the fiber laser. Imagine a garden hose. A fiber laser takes a special glass fiber, thinner than a human hair, and dopes it with rare earth elements like ytterbium. Then it pumps light from semiconductor laser diodes into the cladding of that fiber, like pouring water into the outer jacket of a garden hose. The rare earth atoms absorb that pump light and re-emit it as a single, perfectly focused beam that emerges from the fiber's core. The magic trick is brightness conversion: you take cheap, somewhat messy light from many semiconductor pump diodes and the fiber converts it into a single, diffraction-limited beam that can cut through an inch of steel. The efficiency is remarkable — a fiber laser converts more than half of its electrical input into useful laser output, compared to roughly ten percent for a traditional CO2 gas laser. That is not an incremental improvement. That is a paradigm shift.

The person who commercialized this breakthrough was Valentin Gapontsev, a Russian physicist who founded IPG Photonics in 1990 near Moscow before relocating to Oxford, Massachusetts. Gapontsev was a force of nature — a perfectionist who insisted on controlling every element of the fiber laser supply chain, from the semiconductor pump diodes to the specialty fibers to the final system. His genius was recognizing that when the telecom bubble burst, the real opportunity for fiber lasers was not in telecommunications but in replacing the CO2 gas lasers that dominated industrial cutting and welding.

The disruption was swift and total. By 2006, IPG launched commercially available multi-kilowatt fiber lasers that could cut inch-thick steel plate faster, cheaper, and more reliably than any CO2 laser on the market. No consumable flashlamps. No gas tubes. No mirror alignment. Within five years, IPG controlled approximately eighty percent of the high-power fiber laser market. Revenue reached $1.4 billion by 2017. It was a classic disruptive technology story: fiber lasers were smaller, cheaper to operate, more efficient, and fundamentally better than the incumbent technology. The fiber laser was to industrial lasers what the transistor had been to vacuum tubes — not an incremental improvement, but a generational leap.

But here is the part that matters for nLIGHT: every fiber laser needs semiconductor pump diodes. These are the engines, the fuel injectors, the critical component without which the whole system does not work. And making high-power semiconductor laser diodes is extraordinarily difficult.

The manufacturing process starts with epitaxial growth — building crystal structures atom by atom on gallium arsenide wafers inside specialized reactors. The slightest impurity, a single misaligned atomic layer, and the chip fails. Then those wafers must be processed through photolithography, etched, metallized, cleaved into individual chips, and packaged onto heat sinks capable of dissipating enormous thermal loads. A high-power diode bar generates heat densities comparable to the surface of the sun. Getting the heat out fast enough to keep the chip alive requires microchannel cooling systems machined to tolerances of a few microns. It is semiconductor manufacturing, but for power rather than logic, and the yield and reliability requirements are punishing. This is not the kind of manufacturing you can learn from a textbook or buy off the shelf. It takes years of process iteration and thousands of failed experiments to master.

This is where nLIGHT's founding story begins. In the late 1990s, the epicenter of semiconductor laser expertise in America was a company called Spectra Diode Labs — SDL — based in San Jose. SDL was founded in 1983 as a joint venture between Xerox and Spectra-Physics, and it became the premier supplier of high-power semiconductor laser diodes, including the pump lasers that powered the erbium-doped fiber amplifiers enabling long-haul fiber optic telecommunications. When the telecom boom inflated into a bubble, SDL's value soared. In July 2000, JDS Uniphase announced it would acquire SDL for forty-one billion dollars in stock — the largest technology acquisition ever announced at that point.

Among SDL's engineers was Mark DeVito, who held a master's degree in electronic science and had spent years at the company learning the deep craft of semiconductor laser fabrication. DeVito had started his career at Varian Associates, one of Silicon Valley's original high-tech firms, before joining SDL. He did not become fabulously wealthy from SDL's IPO in 1995, but he accumulated something more valuable: deep expertise in the one thing that mattered most for the future of fiber lasers — making the pump diodes work reliably at high power.

Meanwhile, in Bothell, Washington, a company called Aculight Corporation was developing solid-state lasers for defense applications — countermeasures, laser radar, directed energy research. Aculight had about ninety employees and was doing interesting work at the intersection of optics and national security. Leading it as CEO and president was Scott Keeney, a man with an unusual profile for the laser industry.

Keeney held a BA in economics from the University of Washington and an MBA from Harvard Business School. Before entering the laser world, he had spent time at McKinsey and Company as a management consultant in San Francisco and Seattle, and earlier had worked in manufacturing and quality management at Pacific Coast Feather Company. He was not a physicist by training. He was a strategist who understood technology markets and had the unusual ability to translate deep technical concepts into business strategy.

At Aculight, Keeney gained firsthand exposure to the Pentagon's laser ambitions and frustrations — the long-running quest for directed energy weapons that always seemed to be a decade away from reality. He met Mark DeVito in July 1998, and the two quickly recognized a shared vision. Keeney had the strategic framework and defense relationships; DeVito had the semiconductor laser manufacturing expertise. Together, they saw what others missed: that whoever controlled the pump diode supply chain would own a chokepoint in the entire photonics industry.

In the summer of 2000, Keeney, DeVito, and a third co-founder, optical engineer Scott Karlsen, incorporated nLIGHT Photonics Corporation. The founding team drew from a network of engineers scattered by the telecom implosion — talent from Corning, Lucent, Nortel, and Agilent who brought deep expertise in optical components and semiconductor manufacturing.

Their bet was straightforward but contrarian: semiconductor lasers would improve at a rapid rate, and whoever controlled the manufacturing process — from epitaxial wafer growth through chip fabrication and packaging — would own the most defensible position in the photonics value chain. They were not building lasers for telecom, where the bubble was already showing cracks. They were building the engines that every fiber laser would need. The initial pitch to venture investors centered on Raman amplification for next-generation telecom networks, but the team's deeper conviction was that high-power semiconductor lasers would find applications far beyond fiber optics.

They raised sixty million dollars from investors including Menlo Ventures, Oak Investment Partners, and Mohr Davidow Ventures. The decision to locate in Vancouver, Washington — rather than Silicon Valley or Boston — was driven by affordable real estate, proximity to Portland's semiconductor manufacturing infrastructure, and available skilled labor. They broke ground on a fifty-seven-thousand-square-foot manufacturing plant complete with twenty-two thousand square feet of cleanroom, and began production in October 2001.

The timing was brutal: founded at the precise apex of the telecom bubble. But that timing, paradoxically, would prove to be their salvation, because it scattered the talent they needed and forced them to look beyond telecom from the very beginning.

III. The Wilderness Years: Building in the Shadow of IPG (2000–2010)

The first years were a survival story. nLIGHT secured seven million dollars from Oak Investment Partners in March 2001, just as the NASDAQ was in freefall and the telecom industry was imploding. The JDSU acquisition of SDL had closed in February 2001, but euphoria gave way to catastrophe within months. By mid-2001, JDSU announced a write-down exceeding forty-five billion dollars, the largest in business history at that time. The company that had paid forty-one billion for SDL would eventually see its stock fall from one hundred fifty-three dollars to under two dollars. Thousands of photonics engineers were laid off across the industry. Entire semiconductor laser fabrication lines went dark.

Against this backdrop, nLIGHT's twenty-odd employees in their new Vancouver facility were trying to build a company. The initial strategy of selling pump lasers for telecom Raman amplification was instantly obsolete. As CEO Keeney later recalled, "We didn't expect the industrial market to be interesting for some time, but we were forced to pivot very quickly." By the summer of 2002, the pivot was formal: nLIGHT would redirect its semiconductor laser technology toward industrial, defense, and medical applications. The company hunkered down and began the painstaking work of building manufacturing capability for non-telecom markets.

What kept nLIGHT alive during this decade was a combination of government contracts and the fundamental difficulty of what they did. The Department of Defense awarded a five-million-dollar R&D contract in 2003, and nLIGHT participated in DARPA's Super High Efficiency Diode Sources program, pushing the boundaries of semiconductor laser efficiency. These were small contracts, but they kept the lights on and — critically — they built the security clearances and government relationships that would prove invaluable fifteen years later. Also in 2003, the company made a prescient move: establishing a six-thousand-square-foot manufacturing and sales operation in Shanghai, China, recognizing early that the fastest-growing market for industrial lasers would be in Asia.

The central challenge of this era was the relationship with IPG Photonics. As IPG's fiber lasers conquered the industrial market, demand for nLIGHT's semiconductor pump diodes grew. But IPG, under Gapontsev's relentless vertical integration strategy, was simultaneously building its own internal pump diode manufacturing capacity.

nLIGHT was the proverbial supplier to a customer that wanted to become its own supplier. This is one of the most treacherous positions in business: providing a critical component to a dominant customer who views your product as a cost center to be internalized. Every pump diode nLIGHT sold to IPG simultaneously funded its customer's growth and incentivized that customer to eliminate the dependency. It is the classic innovator's dilemma applied to the supply chain — your best customer is also your greatest strategic threat.

The manufacturing moat was nLIGHT's primary defense. Making high-power semiconductor lasers requires mastering a chain of processes that each take years to optimize: epitaxial crystal growth with atomic-level precision, wafer fabrication, facet passivation to prevent catastrophic optical damage, and advanced packaging with thermal management. Each step involves proprietary know-how accumulated over thousands of process iterations. This is process power in its purest form — the kind of competitive advantage that cannot be bought, only built through years of disciplined manufacturing refinement.

Two acquisitions during this period fundamentally shaped nLIGHT's future. In August 2006, the company acquired the photonics division of Flextronics International in Hillsboro, Oregon, adding forty employees and high-volume packaging design capabilities. The deal expanded nLIGHT's total workforce to roughly one hundred seventy and broadened its ability to serve emerging high-volume applications. Then in November 2007 came the move that would prove genuinely transformative: nLIGHT acquired LIEKKI Corporation, a specialty optical fiber manufacturer based in Lohja, Finland.

LIEKKI had developed something special: a proprietary process called Direct Nanoparticle Deposition — DND — that deposits rare-earth nanoparticles directly into fiber preforms during fabrication. Think of conventional fiber doping as painting a wall with a roller — you get coverage, but the uniformity is limited. DND is more like inkjet printing at the atomic scale, enabling precise control of doping profiles that produce gain fibers with exceptional performance. These were the exact type of fibers used as the amplifying medium in high-power fiber lasers.

The strategic brilliance of the LIEKKI deal becomes clear in hindsight. nLIGHT now controlled the two most technically challenging components in a fiber laser: the semiconductor pump diodes and the specialty gain fiber. No other company in the world had this combination under one roof. The pieces for vertical integration were falling into place, even if the company was not yet ready to build complete laser systems. The Finland facility — operating as nLIGHT Oy — would remain the sole location for all of the company's optical fiber development and manufacturing through the present day.

The numbers tell the survival story. nLIGHT turned profitable for the first time in 2007 and averaged seventy percent annual revenue growth from 2004 to 2008, landing on Deloitte's Technology Fast 500 four consecutive years. By 2009, the company ranked seventy-sixth on that list. Keeney was recognized as Ernst and Young's Entrepreneur of the Year for the Pacific Northwest in 2006, and the company won the Governor's Emerging Trader of the Year Award in 2008.

By 2011, nLIGHT expected roughly seventy million dollars in revenue with over four hundred employees globally. It was not a unicorn. It was not a household name. It was a deep-tech manufacturing company funded by patient venture capital, waiting for the market to catch up with the technology.

Over the full private period, nLIGHT would raise approximately two hundred million dollars across eleven funding rounds — a substantial sum, but one that reflected the capital intensity and long time horizons of photonics manufacturing. In an era when software companies were raising similar amounts and reaching billion-dollar valuations in five years, nLIGHT's investors were signing up for a fundamentally different risk-reward profile: slower growth, harder technology, more capital intensity, but the potential for a durable competitive position rooted in manufacturing expertise that software companies could never replicate.

IV. The Pivot to Direct Diode and Fiber Lasers (2010–2015)

Around 2010, a strategic tension inside nLIGHT reached its breaking point.

The company was a world-class component supplier, but components are a commodity trap. IPG was capturing the lion's share of value in the fiber laser market, and every pump diode nLIGHT sold represented only a fraction of a much larger system price. The math was sobering: a high-power fiber laser system might sell for hundreds of thousands of dollars, but the semiconductor pump modules inside it represented perhaps fifteen to twenty percent of that. The customer captured most of the margin.

Worse, IPG's internal pump diode capability was growing, shrinking nLIGHT's addressable market within its largest customer even as the overall fiber laser market expanded. It was the strategic equivalent of watching the tide go out: the ocean was getting bigger, but nLIGHT's beach was getting smaller.

The decision to compete with your own customers is one of the most consequential and dangerous moves a component supplier can make. It is the business equivalent of a supporting actor deciding to audition for the lead role while still performing in the same play. Get it wrong, and you lose both the component revenue and the systems business. Get it right, and you transform from a price-taking supplier into a value-capturing competitor.

There is a reason most companies in this position choose not to make the leap. The immediate revenue risk is obvious and quantifiable. The potential upside is speculative and distant. Board members and investors tend to prefer the certainty of existing revenue streams over the uncertainty of new ones, even when the existing streams are slowly eroding.

Keeney's strategic instincts, honed at McKinsey and refined through a decade of navigating the photonics industry, told him that the risk of remaining a pure component supplier was greater than the risk of forward integration. The key question was not whether to move, but how to manage the transition without collapsing the existing business before the new one could scale.

The technology bet had two prongs. First, direct diode lasers: systems that use semiconductor laser diodes directly for materials processing, cutting out the intermediate fiber amplification step. Think of it as eliminating the middleman. Direct diode lasers are simpler, potentially cheaper, and inherently more efficient because they eliminate the energy losses in the pumping and conversion process. The tradeoff is beam quality — semiconductor diodes produce light with inferior spatial characteristics compared to fiber lasers. But for applications where raw power matters more than a perfectly focused beam, such as heat treating, cladding, and some welding processes, direct diode lasers are compelling.

Second, complete fiber lasers. nLIGHT would leverage its proprietary pump diodes and LIEKKI's specialty fibers to build fiber laser systems from the chip up. The company called this its "chip-to-system" strategy — controlling every layer of the technology stack.

The Pearl product family, introduced around 2009-2010, was a key commercial platform in this transition. These high-brightness, fiber-coupled diode laser modules — based on nLIGHT's proprietary nXLT single-emitter architecture — served as both standalone products and as the pump engines for the company's emerging fiber laser systems. By combining single-emitter diodes with optimized optical designs, nLIGHT achieved fiber-coupling efficiencies exceeding fifty percent. By the first half of 2011, the company had registered more than sixty million dollars in order bookings, reflecting rapid growth as the global fiber laser market expanded.

In January 2013, nLIGHT made another strategically important acquisition: Arbor Photonics, a University of Michigan spinout based in Ann Arbor. Arbor's prize asset was its Chirally-Coupled Core — or 3C — fiber technology, a patented fiber architecture that enables near-diffraction-limited beam quality at very high power levels. The physics are elegant: a helical coupling structure around the fiber core suppresses unwanted higher-order light modes while guiding the fundamental mode, solving the beam quality degradation that limits conventional fibers at high power. For defense applications, where beam quality at extreme power levels is paramount, this technology would prove essential.

The "coopetition" strategy required extraordinary diplomatic skill. nLIGHT continued selling semiconductor pump modules to IPG and other fiber laser manufacturers while simultaneously offering competing fiber laser systems to end users. This is a dance that few companies execute successfully. Intel tried it with its own PC brand in the 1990s and retreated. Samsung sells display panels to Apple while competing fiercely in smartphones. nLIGHT navigated the tightrope by targeting different market segments with its systems business than those dominated by IPG, focusing on applications where its vertical integration and programmable laser architecture offered differentiated value.

By March 2015, the company launched its first fiber laser product line with power levels up to three kilowatts, and by 2016 it had shipped its thousandth fiber laser, with six-kilowatt and eight-kilowatt models available. These were programmable, serviceable systems designed to compete not on price against IPG's scale advantage, but on flexibility and ease of integration for OEM customers. In January 2016, the transformation warranted a new identity: nLIGHT Photonics Corporation formally changed its name to nLIGHT, Inc., dropping "Photonics" to reflect a portfolio that had grown well beyond components.

During this period, nLIGHT also continued deepening its process capabilities. The company developed its Element and Pearl product families — fiber-coupled diode modules optimized for pumping ytterbium fiber lasers at the critical 976-nanometer wavelength. These products competed on "price per bright watt," the metric that matters most to fiber laser manufacturers, against IPG's internal pump capabilities. The fact that nLIGHT's external components remained competitive against a customer manufacturing at massive scale spoke to the depth of the company's process expertise.

The financial logic of the pivot was compelling. At the component level, nLIGHT was selling pump modules at typical semiconductor margins. At the systems level, a complete fiber laser captures multiples of that revenue per unit. Even if moving into systems cost some component sales, the net effect on revenue and margin could be transformative. And the strategic imperative was undeniable: reducing dependency on any single customer, particularly one as dominant and vertically integrated as IPG, was essential for long-term survival. But the most important pivot was still ahead — one that would ultimately define the company's identity and drive its greatest value creation.

V. Defense and Aerospace: The Game-Changing Bet (2015–2018)

In a classified briefing room at the Pentagon, sometime around 2014-2015, the conversation about directed energy weapons shifted from "someday" to "soon." The catalyst was asymmetric warfare. American forces in the Middle East and the Pacific were confronting a new reality: adversaries could deploy cheap drones, rockets, and mortar rounds by the dozen, while each American interceptor missile cost between one and three million dollars. The math simply did not work. A Patriot missile costing three million dollars to shoot down a thirty-thousand-dollar drone was economic suicide. The military needed a fundamentally different approach.

High-energy lasers offered a tantalizing solution: a deep magazine with near-zero cost per shot, the speed of light for targeting, and the ability to engage threats in rapid succession without reloading. Where a conventional interceptor system might carry eight to sixteen missiles and then need to return to base for reloading, a laser weapon can fire thousands of times limited only by its power supply. The economics are staggering: roughly three to ten dollars per shot for a laser versus hundreds of thousands to millions for a kinetic interceptor.

But turning laboratory demonstrations into battlefield-ready weapon systems required solving a cascade of engineering problems. Military lasers needed to be ruggedized for vibration, dust, humidity, and temperature extremes that would destroy a laboratory prototype in hours. They needed to scale to power levels of tens or hundreds of kilowatts while maintaining beam quality good enough to focus energy on a target at kilometers of range. They needed to be efficient enough that mobile platforms could power them without dedicated generator trucks. And they needed to be manufactured by companies with security clearances, ITAR-compliant facilities, and the ability to deliver on Department of Defense timelines.

nLIGHT was positioned for this moment in ways that were not obvious to outside observers. Scott Keeney's pre-nLIGHT role as CEO of Aculight Corporation — which would be acquired by Lockheed Martin in September 2008 for its directed energy and countermeasure laser expertise — had given him firsthand exposure to the military's laser ambitions. He knew the Pentagon had been funding directed energy research since Reagan's Strategic Defense Initiative in the 1980s, and he knew why the technology had never quite arrived: the lasers were too big, too power-hungry, too fragile, and not bright enough. Every few years, a new program would promise battlefield-ready laser weapons, and every few years, the physics would win.

What changed in the 2010s was fiber laser technology. Specifically, the ability to combine many individual fiber laser beams into a single, devastatingly powerful output while maintaining the beam quality needed to project that power over kilometers. The fiber laser architecture that IPG had commercialized for cutting sheet metal turned out to be the same architecture — scaled up, ruggedized, and beam-combined — that could power a weapon system capable of destroying a drone at several kilometers of range.

The technology fit was natural. nLIGHT's core competency — building the highest-brightness, most efficient semiconductor laser diodes in the world — was exactly what directed energy weapons needed. The company's process expertise in thermal management, efficiency optimization, and reliability testing translated directly from industrial requirements to military specifications. A semiconductor laser diode that must run continuously for tens of thousands of hours in a factory has already solved most of the reliability problems that a military system encounters. Those early DARPA contracts had built institutional relationships with the defense acquisition community and given nLIGHT's facilities and personnel the security clearances required to work on classified programs.

The margin implications were transformative. Industrial laser components are commodity products sold on price per watt — a metric that invites constant price comparison and drives margins toward the cost of production. Defense laser systems are sold on performance, reliability, and the unique ability to meet classified specifications that no one else can match. The pricing power difference is enormous: defense contracts typically carry gross margins meaningfully higher than industrial component sales, and programs with sole-source positions carry even more.

For nLIGHT, shifting revenue mix toward defense was not just a growth strategy — it was a margin transformation story. The same manufacturing platform that produced pump diodes at commodity margins could produce defense-qualified laser modules at premium margins, simply by directing output toward different end markets with different competitive dynamics.

The cultural shift was equally significant. An industrial component company optimizes for cost, throughput, and standard specifications. A defense contractor optimizes for performance, documentation, testing, and compliance with a Byzantine procurement system. nLIGHT had to build a defense-contracting apparatus: program management offices, DCAA-compliant accounting, classified computing networks, and the institutional patience to manage multi-year development programs. Many commercial technology companies have tried to enter the defense market and failed because they underestimated the cultural and operational requirements.

There was also an important government-funding dynamic at work. Defense R&D contracts served as de facto external funding for nLIGHT's technology development. The Pentagon paid nLIGHT to push the boundaries of laser power and beam quality — research that simultaneously advanced the company's commercial capabilities. This is the dual-use technology advantage at its finest: taxpayer-funded defense R&D creates intellectual property and manufacturing know-how that flows into commercial products, reducing the company's effective R&D burden and accelerating the entire technology roadmap.

By 2017, the defense push was paying off. The company reported $138.6 million in revenue and $1.8 million in profit — a dramatic turnaround from the $14.2 million loss on $101.3 million of revenue the previous year. Raytheon and BAE Systems were named as defense customers. The company served over three hundred customers overall and employed approximately one thousand people, about half at its Washington facilities. Roughly sixty-six percent of business was generated internationally. The defense programs were real but still relatively small as a share of total revenue. The true inflection was coming — but first, the company needed to go public.

VI. The IPO and Public Markets Journey (2018–2020)

On April 26, 2018, nLIGHT began trading on the Nasdaq Global Select Market under the ticker LASR — as subtle as a laser beam itself.

The S-1 had been filed with the SEC on March 30, 2018, initially targeting a price range of thirteen to fifteen dollars per share. Strong investor demand pushed the final pricing above range, to sixteen dollars, on an upsized offering. The stock surged sixty-eight percent on its first day of trading, closing at twenty-six dollars and ninety-five cents, valuing the eighteen-year-old company at approximately nine hundred million dollars. The offering, led by Stifel and Raymond James with Needham & Company, Canaccord Genuity, and D.A. Davidson as co-managers, raised roughly ninety-six million dollars in gross proceeds.

For a company that had spent nearly two decades in the private markets, the first-day pop was a powerful market signal. Investors were hungry for a pure-play laser company at the intersection of industrial technology and defense — a relatively rare animal in public markets.

For the venture investors who had funded nLIGHT's patient journey — Oak Investment Partners, Menlo Ventures, and Mohr Davidow Ventures — it was a long-awaited liquidity event after more than two hundred million dollars in private funding across eleven rounds over eighteen years. In an industry obsessed with rapid exits, nLIGHT stood as a testament to the deep-tech venture model: invest in hard science, wait for the market to mature, trust that process expertise creates durable advantage.

The S-1 filing told a story of three end markets. Microfabrication, accounting for forty-four percent of 2017 revenue, served semiconductor equipment makers and electronics manufacturers with precision laser sources. Industrial, at forty-one percent, supplied the fiber laser market through pump modules and complete systems for cutting, welding, and materials processing. Aerospace and defense, at fifteen percent, was the smallest segment but the one with the most compelling growth trajectory.

The board of directors assembled for the public debut reflected the company's strategic ambitions. Alongside the venture partners sat Gary Locke, the former two-term Governor of Washington State who had also served as U.S. Secretary of Commerce under President Obama and as U.S. Ambassador to China. Locke's diplomatic credentials were not decorative: with more than forty percent of nLIGHT's revenue coming from Chinese customers at that time, his expertise in U.S.-China relations was operationally significant.

The public company faced a perennial challenge of investor education. Laser photonics is not a market that most generalist fund managers understand intuitively. The distinction between a semiconductor pump diode, a fiber laser system, and a directed energy weapon module requires technical context that quarterly earnings calls struggled to convey. The stock's performance in those early public years reflected this complexity — volatile swings driven as much by macro sentiment and trade headlines as by the company's underlying execution.

The first full year as a public company was strong: 2018 revenue reached one hundred ninety-one million dollars, up thirty-eight percent from the pre-IPO year, with defense-related sales growing approximately sixty percent. But the honeymoon was brief.

The stock peaked around forty dollars in the summer of 2018 before the U.S.-China trade war sent it tumbling. The irony was painful: the same Chinese market that had driven nLIGHT's growth — with over forty percent of revenue coming from Chinese customers — was now a source of risk rather than opportunity. By year-end, LASR had fallen to roughly eighteen dollars as investors repriced the China exposure that had been a selling point just months earlier. Revenue in 2019 declined to one hundred seventy-seven million dollars as the microfabrication segment contracted and trade tensions disrupted industrial supply chains. The stock would eventually reach a nadir around forty-five dollars during the pandemic rally of early 2021 before sliding again.

Management responded by accelerating the defense pivot. In November 2019, nLIGHT made what would prove to be its most strategically important acquisition since LIEKKI: purchasing Nutronics, a thirty-two-person company in Longmont, Colorado, for approximately thirty-three million dollars — $17.5 million in cash plus $15.8 million in restricted stock units. Nutronics, founded in 1995, specialized in two technologies nLIGHT desperately needed for directed energy: coherent beam combining and adaptive optics.

Here is why that mattered. Coherent beam combining is the technique of taking multiple individual laser beams and phase-locking them so they constructively interfere into a single combined beam with the brightness and power of all the individual beams together. Think of it as the laser equivalent of a symphony orchestra: individual fiber lasers each produce their own beam, like instruments playing their own notes, and coherent combining synchronizes them precisely so they produce a single, vastly more powerful output. It is the difference between noise and music. And it is the enabling architecture for scaling laser weapons from tens of kilowatts to hundreds of kilowatts and beyond, because it allows you to add power simply by adding more fiber laser modules rather than trying to push a single laser beyond its physical limits.

Adaptive optics, meanwhile, corrects for atmospheric distortion that would scatter the beam before it reaches the target. The atmosphere is not a clean optical path — turbulence, humidity, and thermal gradients all bend and disperse a laser beam as it travels. Adaptive optics measures those distortions hundreds of times per second and adjusts the outgoing beam in real time to compensate. It is the same technology ground-based telescopes use to produce sharp images of distant galaxies through turbulent air, applied in reverse to project power rather than collect light.

With Nutronics integrated, nLIGHT now controlled an unbroken technology chain from semiconductor chip fabrication through fiber amplifier manufacturing through coherent beam combining through atmospheric beam control. No other company in the world offered this complete stack in a single entity. The directed energy weapon market had found its pure-play champion. But China would test the commercial side of the business severely before the defense story could fully mature.

VII. The China Challenge and Supply Chain Reckoning (2018–2022)

While nLIGHT was building its defense franchise, its commercial business was being squeezed from two directions simultaneously. The first was geopolitical: the U.S.-China trade war launched in 2018, with escalating tariffs directly impacting nLIGHT's industrial laser sales to Chinese customers. The second was competitive: Chinese domestic laser companies were rapidly closing the technology gap and undercutting Western suppliers on price in ways that permanently repriced the market.

The rise of Raycus Fiber Laser Technology and Maxphotonics, both based in Shenzhen, represented Chinese industrial policy in action. Backed by government subsidies, preferential financing under Made in China 2025, and a massive domestic market, these companies built fiber laser manufacturing capacity at scale and offered products at prices thirty-five to fifty percent below Western competitors.

The price destruction was not gradual. Industry observers documented periods where the price per watt of fiber laser output fell fifty percent in a single year. A ten-kilowatt fiber laser system in China that once sold for roughly five million renminbi — about $760,000 — saw prices plummet over ninety-five percent as domestic competition arrived. In the one-kilowatt-and-below segment, Raycus and Maxphotonics captured roughly ninety percent of the Chinese market. For the majority of industrial cutting and welding applications, the Chinese quality was good enough. And "good enough" at a fraction of the price is a death sentence for premium-priced incumbents.

The effect on Western incumbents was devastating. IPG Photonics, which had built its empire on fiber laser dominance with significant Chinese industrial demand, saw its revenue peak at approximately $1.46 billion in 2021 and then decline steadily — to $1.43 billion in 2022, $1.29 billion in 2023, and below one billion dollars to $977 million in 2024. That last number was the first time in a decade IPG had fallen below the billion-dollar threshold, a stark illustration of how quickly Chinese competition could erode a seemingly impregnable market position.

The lesson for the entire Western laser industry was brutal in its clarity: in commodity industrial applications where performance differences are marginal, there is no sustainable advantage against a competitor with lower costs, government backing, and a protected home market of enormous scale. The only defensible positions are in segments where performance is genuinely differentiated, where supply chain trust matters, or where regulatory barriers exclude foreign competition.

For nLIGHT, the impact cascaded through both its component and systems businesses. The company's Shanghai operation, which at its peak employed hundreds of people assembling semiconductor lasers and fiber laser products, was increasingly exposed to tariff risks, IP concerns, and the strategic awkwardness of manufacturing in a country that was simultaneously a customer, a competitor, and a geopolitical adversary. Chinese laser companies were also beginning to develop their own semiconductor pump diode capabilities, threatening the component market that had been nLIGHT's foundation.

COVID-19 added another layer of disruption that reverberated through the business for years. Initial demand volatility in 2020 gave way to a brief recovery, but the Shanghai lockdowns of 2022 proved more damaging. Chinese authorities physically shut down nLIGHT's manufacturing operations for weeks, creating delivery delays and customer frustration that accelerated the case for supply chain diversification.

The pandemic also disrupted global semiconductor equipment supply chains, extending lead times for the specialized tools needed for epitaxial growth and chip fabrication. This made it harder to expand domestic capacity precisely when it was most needed — a cruel irony that affected the entire semiconductor industry during this period.

The decision to exit China manufacturing was painful but strategically clear. It was one of those decisions where the long-term answer is obvious but the short-term cost is real and immediate.

Beginning around 2022, nLIGHT undertook a major supply chain transformation: establishing highly automated semiconductor laser production at its Camas, Washington headquarters, contracting with a third-party manufacturer in Thailand for commercial assembly, and progressively winding down the Shanghai facility. The automation investment in Camas was particularly significant — the new production lines could produce semiconductor laser packages with far fewer manual steps than the Shanghai facility, partially offsetting the labor cost differential.

By late 2024, the company had substantially completed the China exit, with no remaining manufacturing operations in China. The financial cost was significant: revenue declined from a peak of $270 million in 2021 to $199 million in 2024, a cumulative drop of more than twenty-five percent, driven by the China exit, Chinese competitive pressure, and soft global industrial demand.

But the China challenge contained its own silver lining. As U.S. policymakers intensified their focus on supply chain security and technology competition, nLIGHT's domestic manufacturing base transformed from a cost burden into a strategic asset. The company's "trusted supplier" status for defense applications, its ITAR-compliant facilities, and its American and Finnish manufacturing footprint became more valuable with each new export control regulation. The Finland-based fiber operation in Lohja, located in a NATO ally country, added another dimension of supply chain credibility in the emerging "friend-shoring" paradigm.

There is an important legal and regulatory dimension worth flagging. Export controls on semiconductor technology tightened throughout this period, with the Commerce Department closing loopholes for foreign companies supplying semiconductor manufacturing equipment to China. For nLIGHT, this was a double-edged sword: it threatened remaining commercial revenue in Asia, but it reinforced the barriers protecting nLIGHT's defense business from foreign competition. Potential Chinese rare earth export controls represented a supply chain risk worth monitoring, though management had not flagged it as a major exposure. The broader ITAR regulatory framework — the International Traffic in Arms Regulations that govern defense-related exports — simultaneously constrained nLIGHT's ability to sell certain products internationally while creating an impenetrable moat around its defense customer base.

The revenue mix shifted dramatically: by 2024, aerospace and defense represented fifty-five percent of total revenue, up from fifteen percent at the time of the IPO just six years earlier. The China crisis, painful as it was, forced the strategic transformation that would define nLIGHT's future. The commercial market had been permanently repriced by Chinese competition — this was structural, not cyclical. The question was whether the defense opportunity was large enough and durable enough to replace what had been lost.

VIII. The Modern Portfolio: Diversification Payoff (2020–Present)

In July 2020, nLIGHT made a small acquisition that signaled broadening ambition: OPI Photonics of Turin, Italy, founded by Andrea Braglia and Guido Perrone of Politecnico di Torino, for approximately $1.6 million. OPI added novel multi-emitter diode laser module technology and kW-range free-space optics capabilities. In February 2022, the company added Plasmo Industrietechnik of Austria, a specialist in automated quality assurance for welding and additive manufacturing — a smart acquisition for industrial laser monitoring, though its strategic value diminished as nLIGHT subsequently pivoted away from commodity welding markets.

But the real story of this era was defense revenue scaling at a pace that even the most optimistic investors had not anticipated.

The HELSI program — the High Energy Laser Scaling Initiative — became nLIGHT's flagship defense effort and the centerpiece of its directed energy strategy. In Phase 1, the company was selected to develop a three-hundred-kilowatt coherent beam combined laser using the architecture acquired through Nutronics. By 2022, the HELSI Phase 1 laser had exceeded all program power and brightness objectives at the three-hundred-kilowatt class. Think about what that means in practical terms: three hundred kilowatts is enough power to heat a small neighborhood, concentrated into a beam that can track and destroy targets at the speed of light. No one had ever demonstrated that kind of power through coherent beam combining before. nLIGHT did it, and they did it on schedule. The company described this achievement as "the highest power laser in the world" through CBC architecture.

The success triggered Phase 2. In May 2023, the company was awarded eighty-six million dollars to scale from three hundred kilowatts to one megawatt — a power level that opens entirely new military applications including ballistic missile defense and potentially space-based systems. By November 2023, additional contract options expanded the Phase 2 award to one hundred seventy-one million dollars. In the same month, nLIGHT won a $34.5 million subcontract for the Army's DE M-SHORAD program — Directed Energy Maneuver-Short Range Air Defense — supplying a fifty-kilowatt laser weapon module for integration onto Stryker combat vehicles. These were not study contracts or paper exercises. These were hardware programs requiring the delivery of functioning directed energy systems to the United States military.

Then in the third quarter of 2025, the company signed a fifty-million-dollar contract for a missile sensing program, incorporating one of its laser sensing products for guidance, proximity detection, and countermeasures. By the fourth quarter, nLIGHT had begun low-rate initial production on a new classified sensing program. The defense pipeline was deepening across multiple applications.

The modern nLIGHT operates across two reporting segments — Laser Products and Advanced Development — with revenue tracked across three end markets.

Aerospace and defense, now dominant at sixty-seven percent of 2025 revenue, encompasses everything from semiconductor laser components for infrared countermeasures to complete directed energy weapon systems. This segment generated approximately one hundred seventy-five million dollars in 2025, growing sixty percent year-over-year. The growth is not coming from a single program — it spans counter-drone systems, missile sensing, high-energy scaling initiatives, and classified programs that management cannot discuss on earnings calls. The breadth matters because it reduces single-program risk and builds institutional knowledge across multiple defense application domains.

Microfabrication, at roughly eighteen percent of revenue, serves semiconductor equipment and electronics manufacturers with precision laser sources. This is a steady, cyclical business tied to semiconductor capital expenditure cycles — not a growth engine, but a profitable base that leverages the same manufacturing platform.

Industrial, at fifteen percent, is transitioning away from cutting and welding to focus on additive manufacturing — metal three-dimensional printing for aerospace and defense applications. This is a deliberate strategic choice: retain the industrial applications where nLIGHT's technology is genuinely differentiated and the customer base overlaps with the defense franchise, while exiting the commodity segments where Chinese price competition has made the economics untenable.

The manufacturing footprint tells the vertical integration story in geographic terms. Vancouver, Washington houses the semiconductor wafer fab where epitaxial crystal growth and chip fabrication happen — the foundational technology from which everything else flows. Camas, Washington — adjacent to Vancouver — is headquarters, with over five hundred employees handling assembly and testing for semiconductor modules and fiber laser systems. Management has noted the Camas facility has capacity to support roughly one billion dollars of annual production, a figure that underscores how much runway exists for growth without major new facility investment in the US.

Hillsboro, Oregon provides additional fiber laser packaging capacity, a legacy of the Flextronics Photonics acquisition. Lohja, Finland — the former LIEKKI facility, now operating as nLIGHT Oy — manufactures all specialty optical fiber using Direct Nanoparticle Deposition. And Longmont, Colorado — the former Nutronics site — has become the directed energy integration center where complete beam-combined laser weapon modules are assembled and tested in classified environments.

In January 2026, nLIGHT announced a fifty-thousand-square-foot expansion of the Longmont facility, more than doubling its directed energy manufacturing capacity. This was not speculative — it was driven by contracted demand. By the fourth quarter of 2025, the company had achieved substantial completion of the DE M-SHORAD deliverable, shipping a functioning fifty-kilowatt laser weapon module and beam director for integration into the Stryker vehicle.

The financial trajectory captured the transformation. Full-year 2025 revenue reached a record $261.3 million, surpassing the previous 2021 peak, but with a fundamentally different composition: defense revenue had roughly tripled since 2021. Gross margin recovered to nearly thirty percent, up from a painful nadir of less than seventeen percent in 2024 — a year when the company took roughly six million dollars in inventory reserve charges on industrial products that could no longer be sold at profitable prices. The fourth quarter of 2024 had been particularly ugly: gross margins collapsed to 2.4 percent, a number that seemed to confirm the bears' thesis that nLIGHT's business model was structurally impaired.

The 2025 recovery disproved that thesis emphatically. For the first time, the company achieved non-GAAP profitability for the full year, with non-GAAP net income of thirteen million dollars versus a thirty-one million dollar loss the prior year. Adjusted EBITDA swung from negative nineteen million to positive twenty-four million. The record fourth quarter, at $81.2 million in revenue with thirty-one percent gross margin, demonstrated the operating leverage inherent in the defense-heavy business model. The company that had been left for dead at six dollars was now generating genuine earnings power.

IX. The Directed Energy Future and Strategic Position (2023–2025)

The global security environment has transformed the directed energy market from a niche procurement curiosity into a strategic imperative. The Houthi campaign against commercial shipping in the Red Sea, beginning in late 2023, provided the most vivid demonstration of the problem laser weapons solve: naval vessels expending interceptor missiles costing millions per shot against drones and cruise missiles that cost a fraction of that amount. Ukraine's experience defending against Russian drone warfare underscored the same lesson for ground forces. The Pentagon is now spending roughly a billion dollars annually on directed energy programs, with the Army alone allocating approximately $447 million for counter-drone R&D in fiscal year 2025, including $140 million specifically for directed energy.

In April 2024, the Army deployed its first operational laser weapon overseas — the P-HEL, a twenty-kilowatt palletized system — to shoot down enemy drones in an undisclosed location. In December 2025, AeroVironment delivered JLTV-mounted laser weapon systems under a separate program. The Army issued a Request for Information in October 2025 for its Enduring-HEL production program, with plans to produce up to twenty platforms and competitive source selection anticipated as early as the second quarter of fiscal 2026. Directed energy is transitioning from laboratory demonstrations to fielded capability, and each transition from development to production represents a revenue multiplier for companies positioned in the supply chain.

In early March 2026, nLIGHT showcased a seventy-kilowatt laser weapon system at the Pacific Operational Science and Technology conference, alongside thirty-kilowatt and ten-kilowatt systems targeting counter-drone, counter-rocket, and counter-missile missions across ground, naval, air, and space domains. The company has ascended from component supplier to complete directed energy solutions provider — a transformation that would have seemed improbable a decade ago when the business was primarily selling pump diode modules to fiber laser OEMs.

The technology roadmap points toward continued power scaling, improved wall-plug efficiency, new wavelengths for specialized applications, and miniaturization of beam control systems. Each advancement in the commercial fiber laser domain feeds back into defense capabilities, and vice versa — the dual-use flywheel continues to turn.

The competitive landscape is formidable but fragmented. Lockheed Martin, the Army's HELSI prime and winner of the IFPC-HEL contract in October 2023 for three-hundred-kilowatt systems, is the most prominent competitor. Northrop Grumman participates in HELSI and has delivered its miniaturized Phantom laser system. General Atomics, the Air Force's HELSI partner, uses a different approach called spectral beam combining. RTX, formerly Raytheon, has fielded counter-drone laser systems in military exercises. These are all significantly larger companies with deeper pockets and broader defense portfolios.

But nLIGHT possesses a differentiation that none of them can easily replicate: complete vertical integration from semiconductor chip through specialty fiber through beam-combined directed energy system, all manufactured on American and allied soil. The primes can build laser weapon platforms, but they typically source their core laser subsystems from companies like nLIGHT. This creates an interesting dynamic: nLIGHT is simultaneously a supplier to and a competitor of the defense giants — a position of unusual strategic leverage. As one industry observer noted, the primes need nLIGHT's technology even as they compete against nLIGHT's systems.

The Department of Defense's power roadmap calls for scaling from 150-kilowatt systems to 500 kilowatts with reduced size, weight, and power by 2025 to 2030, and toward megawatt-class systems thereafter. nLIGHT's HELSI program sits squarely on this roadmap. The company is not just participating in the directed energy buildout — it is defining the technology frontier.

On the commercial side, the exit from cutting and welding, formalized during the fourth-quarter 2025 earnings call, was the culmination of years of Chinese-driven margin erosion. Management estimated a twenty-five to thirty million dollar revenue headwind in 2026, with cutting and welding revenue expected to reach zero by the second half. The retained industrial business focuses on additive manufacturing — metal three-dimensional printing where nLIGHT's technology is more differentiated and the customer base overlaps with defense — and the microfabrication segment remains a steady contributor serving semiconductor equipment manufacturers.

The February 2026 equity offering — roughly four million shares at forty-four dollars, raising approximately $201 million in gross proceeds including the full overallotment exercise — was designed to fund the next phase. Proceeds are earmarked for Longmont facility expansion, supply chain readiness, staffing, and potential acquisitions. Following the raise, the balance sheet holds more than $250 million in cash, providing substantial runway for the defense production ramp that management sees ahead.

X. Playbook: Business and Investing Lessons

nLIGHT's quarter-century journey offers a masterclass in several strategic frameworks that transcend the laser industry.

When to compete with your customers. The conventional wisdom says never bite the hand that feeds you. But nLIGHT's story demonstrates that remaining a pure component supplier to a vertically integrating customer is a slow death sentence. The key insight is timing: nLIGHT waited until it had an alternative growth vector — defense — before aggressively pushing into systems that competed with its industrial customers. The transition was not a reckless gamble; it was a calculated repositioning executed over years, with defense revenue providing the safety net that made the industrial disruption survivable.

Dual-use technology as a flywheel. nLIGHT spent two decades perfecting semiconductor laser diodes for commercial applications, and those same capabilities — thermal management, efficiency optimization, reliability testing — translated directly to military specifications. The commercial market funded the R&D that defense applications monetized at premium margins. This is the ideal dual-use flywheel: commercial volume drives down manufacturing costs and improves processes, while defense provides high margins and long-term contract visibility. Companies that ride this flywheel have a structural advantage over pure defense contractors who must amortize R&D across smaller runs.

Manufacturing as moat. In a world of asset-light business models and software margins, nLIGHT's insistence on owning its own semiconductor fabrication, fiber manufacturing, and system assembly is contrarian. But in photonics, manufacturing IS the product. The twenty-plus years of accumulated process knowledge embedded in nLIGHT's production lines — the thousands of epitaxial growth recipes, the packaging techniques, the institutional expertise — cannot be replicated by writing a check. Over 450 patents formalize some of this knowledge, but the tacit expertise of the manufacturing team is equally important and far harder to copy. When the government requires a domestically manufactured, ITAR-compliant, vertically integrated laser source for a classified weapon program, the list of qualified suppliers is very short.

Patient capital in deep tech. nLIGHT was private for eighteen years and then spent another seven years as a public company before the defense inflection produced truly compelling growth. That is a quarter-century from founding to strategic validation. The investors who funded this journey exemplify the patient capital model that deep-tech companies require. The lesson is not simply "be patient" — it is that some companies with genuine process expertise have exponential value creation events that are impossible to predict but, in hindsight, feel inevitable. The directed energy market did not exist as a meaningful procurement category when nLIGHT was founded. The company built the capabilities, and then the world created the demand.

Geographic arbitrage. Manufacturing in the United States and Finland was a competitive disadvantage for two decades when China offered lower costs and faster construction timelines. But in a world of great power competition, export controls, friend-shoring, and defense industrial base concerns, domestic manufacturing became the competitive advantage. nLIGHT's exit from China manufacturing, painful as it was, positioned the company on the right side of every major geopolitical trend shaping technology supply chains. The CHIPS and Science Act, signed in August 2022 with $52.7 billion for semiconductor research and manufacturing, explicitly covers compound semiconductor manufacturers — the exact supply chain nLIGHT operates in. And Finland's NATO membership, formalized in 2023, means nLIGHT's Lohja fiber facility operates in allied territory with full supply chain credibility for Western defense applications.

The defense contractor transformation. Going from an industrial component company to a defense systems provider requires building an entirely new organizational muscle: program management, DCAA-compliant accounting, classified computing networks, export compliance, and the institutional patience to manage development programs that may not reach production for a decade. nLIGHT appears to have navigated this transition successfully, as evidenced by on-time HELSI and DE M-SHORAD deliveries. But the operational demands will only intensify as programs scale from development to production. Many commercial technology companies have attempted the defense pivot and failed because they underestimated the cultural requirements. nLIGHT's advantage was that Keeney came from the defense world originally — his Aculight experience gave him the playbook, and his McKinsey training gave him the organizational discipline to execute it.

The "picks and shovels" lesson. There is a popular investing metaphor about selling picks and shovels during a gold rush rather than panning for gold yourself. nLIGHT tried this approach for its first decade — selling the semiconductor components that every fiber laser needed — and discovered its limitations. When your largest customer wants to make its own shovels, and when Chinese manufacturers can produce shovels at a fraction of the price, being the pick-and-shovel supplier is not the safe haven that the metaphor suggests. Sometimes you need to go prospect for gold yourself.

XI. Porter's Five Forces and Hamilton's 7 Powers Analysis

Understanding nLIGHT's competitive position requires recognizing that the company effectively operates in two distinct industries with radically different dynamics. This duality is both its greatest analytical challenge and its most important strategic insight.

The following analysis applies both Porter's and Helmer's frameworks to each side of the business separately, because the conclusions differ dramatically depending on which market you are evaluating.

Threat of New Entrants. Bifurcated. In commercial lasers, Chinese companies have demonstrated that barriers, while high, can be overcome with sufficient state support and domestic market access. Raycus and Maxphotonics built competitive fiber laser businesses in roughly a decade, proving technology leadership alone does not prevent entry. In defense directed energy, the barriers are formidable and compounding: capital intensity of semiconductor fabrication, decades of process knowledge, security clearances for classified programs, ITAR manufacturing compliance, and multi-year supplier qualification timelines create a moat that no Chinese company can cross and that even well-funded Western entrants would need years to navigate.

Bargaining Power of Suppliers. Moderate. nLIGHT purchases semiconductor equipment from specialized vendors and raw materials — gallium arsenide wafers, rare earth dopants, specialty glass — from multiple sources. Equipment markets are concentrated but alternatives exist, and nLIGHT's vertical integration means most critical components are manufactured internally. The potential risk from Chinese rare earth export controls is worth monitoring but has not been flagged as a major exposure by management.

Bargaining Power of Buyers. The defining split in nLIGHT's business. In commercial and industrial markets, buyer power is high: Chinese alternatives provide credible substitutes at dramatically lower prices, and switching between fiber laser suppliers involves moderate effort. In defense, the dynamic inverts completely. When the Army needs a fifty-kilowatt laser weapon module qualified for a Stryker vehicle, the number of suppliers who can deliver is measured on one hand. Specifications are exacting, switching costs are enormous — requalification can take years — and sole-source positions are common.

Threat of Substitutes. Moderate to high in commercial markets, where alternative laser technologies and Chinese-manufactured fiber lasers are real threats. Low in defense, where no viable substitute for high-power directed energy exists for the specific mission sets these weapons address. A laser provides near-zero cost per shot, speed-of-light engagement, and deep magazine — no kinetic interceptor can match that combination.

Competitive Rivalry. Intense in commercial lasers: IPG Photonics (now under new leadership following founder Gapontsev's passing in 2021), Coherent (which absorbed II-VI in 2022 to become a photonics giant with over five billion in revenue but has pivoted heavily toward AI datacenter optical transceivers under CEO Jim Anderson), Trumpf (the privately held German powerhouse that remains dominant in European industrial laser markets), and Chinese challengers all compete aggressively on price and performance. Moderate in defense: competition is structured around government programs with fewer qualified participants — Lockheed Martin, Northrop Grumman, General Atomics, RTX, and nLIGHT are the primary HELSI ecosystem players, competing for program awards rather than fighting over shelf-space pricing.

Turning to Hamilton Helmer's Seven Powers:

Process Power: HIGH. This is nLIGHT's strongest source of competitive advantage. The ability to grow epitaxial semiconductor structures, fabricate high-power chips, draw specialty fiber using DND technology, and combine multiple laser beams coherently represents accumulated process knowledge developed over more than twenty years. A competitor cannot license this knowledge or hire it away in bulk. It is embedded in institutional routines, equipment configurations, and iterative refinements. Process power is the most durable of Helmer's seven powers because it resists both imitation and substitution.

Switching Costs: HIGH in defense, MODERATE in industrial. Once nLIGHT's laser modules are qualified into a weapon system program, replacing them requires years of requalification testing, interface redesign, and re-certification through defense acquisition processes. Even in industrial applications, customers who have optimized processes around nLIGHT's specific beam characteristics face meaningful switching costs.

Counter-Positioning: MODERATE. The defense primes are primarily systems integrators that buy laser sources rather than manufacturing them. For a prime to vertically integrate into semiconductor laser fabrication would require billions in investment and decades of development — for a market that represents a small fraction of their revenue. The commercial laser giants have manufacturing expertise but lack defense relationships and security clearances. nLIGHT sits at the intersection that neither group can easily reach.

Cornered Resource: MODERATE. The combination of a domestic semiconductor wafer fab, security-cleared personnel, classified program history, proprietary laser designs, and over 450 patents represents a resource bundle competitors cannot easily assemble. No single element is an absolute lock, but collectively they create a barrier that would take years and hundreds of millions of dollars to replicate.

Scale Economies: MODERATE. Manufacturing scale matters in semiconductor production but the market is not winner-take-all. Defense programs inherently limit scale advantages with their small production volumes and unique specifications.

Network Effects: LOW. Hardware manufacturing without meaningful network dynamics.

Branding: WEAK commercially, MODERATE in defense. nLIGHT has earned credibility in defense for on-time delivery and technical performance, but this is closer to reputation than brand power in the traditional sense.

Overall Assessment. nLIGHT's competitive power is concentrated in process power and switching costs, with emerging counter-positioning as the company transitions from component supplier to directed energy systems provider.

The key strategic question is whether these powers are sufficient to sustain premium pricing as the market scales and attracts increased competition from larger, better-capitalized players. History offers mixed guidance: in defense markets, the combination of process expertise and program incumbency has historically been highly durable — once you are qualified on a platform, you tend to stay. But the directed energy market is young enough that the competitive landscape has not fully crystallized. The primes are watching, and if the market grows large enough, vertical integration by Lockheed or Northrop into laser source manufacturing becomes more likely.

The company's durable advantage lies not in any single barrier but in the combination of physical assets, institutional knowledge, and security clearances that no competitor can quickly replicate. In Helmer's language, nLIGHT's moat is a bundle — process power provides the foundation, switching costs lock in defense relationships, and counter-positioning keeps both the primes and the commercial laser giants from easily entering nLIGHT's strategic territory.

XII. Bear vs. Bull Case

The Bull Case.

The bullish thesis rests on a multi-decade defense spending tailwind that is only beginning to accelerate. Directed energy weapons are transitioning from demonstration to deployment, driven by drone proliferation and the economics of cost-per-shot. nLIGHT is arguably the best-positioned company in the world to supply the laser engines for this transition, given its unique vertical integration from semiconductor chip to megawatt beam-combined system.

The HELSI achievement — the most powerful coherently combined laser ever demonstrated — creates first-mover advantage in a market where qualification and track record are decisive. As programs transition from development to production, revenue should scale nonlinearly while margins expand: defense product margins meaningfully exceed those in commercial markets, and growing production contract share should drive that expansion. Management has guided for product gross margins in the upper twenties to low thirties for early 2026, with the trajectory pointing higher as mix continues to shift.

The trusted supplier moat is durable and expanding. In a deglobalized world, US-based manufacturing of critical defense technology is a regulatory requirement, not just a preference. The CHIPS Act and related industrial policy create additional tailwinds. The funded backlog of approximately $162 million at year-end 2025, combined with the pipeline of anticipated awards including the Army's Enduring-HEL production competition, provides multi-year revenue visibility.

The adjacency opportunities are significant. Space-based laser systems for communications and sensing. Medical lasers for surgical applications. Semiconductor equipment requiring increasingly precise laser sources. Each represents a market where nLIGHT's core technology — high-brightness semiconductor lasers and specialty fibers — has potential application, though the company has wisely avoided diluting focus across too many fronts simultaneously.

Perhaps most compellingly, nLIGHT remains underappreciated because its most valuable programs are classified. The true scope of the defense pipeline — program count, future production contract sizes, adjacencies in space and missile defense — is largely invisible to equity analysts. As classified becomes unclassified and development converts to production, the market may discover the addressable opportunity is far larger than current estimates suggest. This information asymmetry is both a risk, since investors cannot fully diligence what they cannot see, and an opportunity, since the hidden value may be substantial.

The Bear Case.

The bearish thesis begins with the structural impairment of the commercial laser market. Chinese competition has permanently repriced commodity fiber lasers, destroying what was once nLIGHT's core revenue stream. The exit from cutting and welding removes twenty-five to thirty million in annual revenue. The microfabrication segment faces its own headwinds. These losses narrow the company's addressable market and increase concentration on defense.

Customer concentration is a persistent risk even as it shifts from commercial to government. The top ten customers represent roughly seventy-five percent of revenue. Large government programs carry their own concentration risk: budget sequestration, program cancellations, or political reprioritization could impact multiple contracts simultaneously. Defense spending, while currently elevated, is subject to Congressional appropriation and geopolitical sentiment.

Program timing is notoriously unpredictable. The Army's production competition has been anticipated for years and continues to shift. HELSI Phase 2 is development, not production. Cost-plus development contracts carry lower margins than production contracts, and the timeline from development to full-rate production in defense is measured in years, sometimes a decade. Bears would argue the stock's tenfold appreciation from its April 2025 low already prices in successful execution that has not yet occurred.

Competition from larger players intensifies as the market matures. Lockheed Martin, with hundreds of times nLIGHT's revenue and deep political relationships, competes directly in HELSI and won the IFPC-HEL program. If the market consolidates around a small number of production programs, the primes' scale and program management depth could prove decisive. The acquisition question cuts both ways: nLIGHT's capabilities make it an attractive target, but a takeout could cap public shareholder upside at a modest premium.

Capital intensity limits free cash flow generation. Semiconductor fabrication, specialty fiber manufacturing, and directed energy system assembly all require continuous investment. The new Longmont facility represents a bet that production volumes will materialize to fill that capacity; if they do not, underutilization will pressure margins. The February 2026 equity offering diluted existing shareholders by roughly eight percent. If defense revenue growth slows or margins disappoint, additional raises may be needed. At roughly $261 million in revenue, nLIGHT remains small relative to competitors like Coherent, which operates at multi-billion-dollar scale following the II-VI merger.

There is also a technology disruption risk. Laser architectures evolve, and new approaches — different wavelengths, novel beam-combining methods, alternative gain media — could theoretically leapfrog nLIGHT's current capabilities. The company's heavy investment in fiber laser and coherent beam combining technology is the right bet today, but the directed energy field is advancing rapidly, and maintaining technology leadership requires sustained R&D spending that compresses near-term margins.

Key Metrics to Watch.

For investors tracking nLIGHT's ongoing performance, two KPIs capture the essence of the investment thesis more clearly than any others.