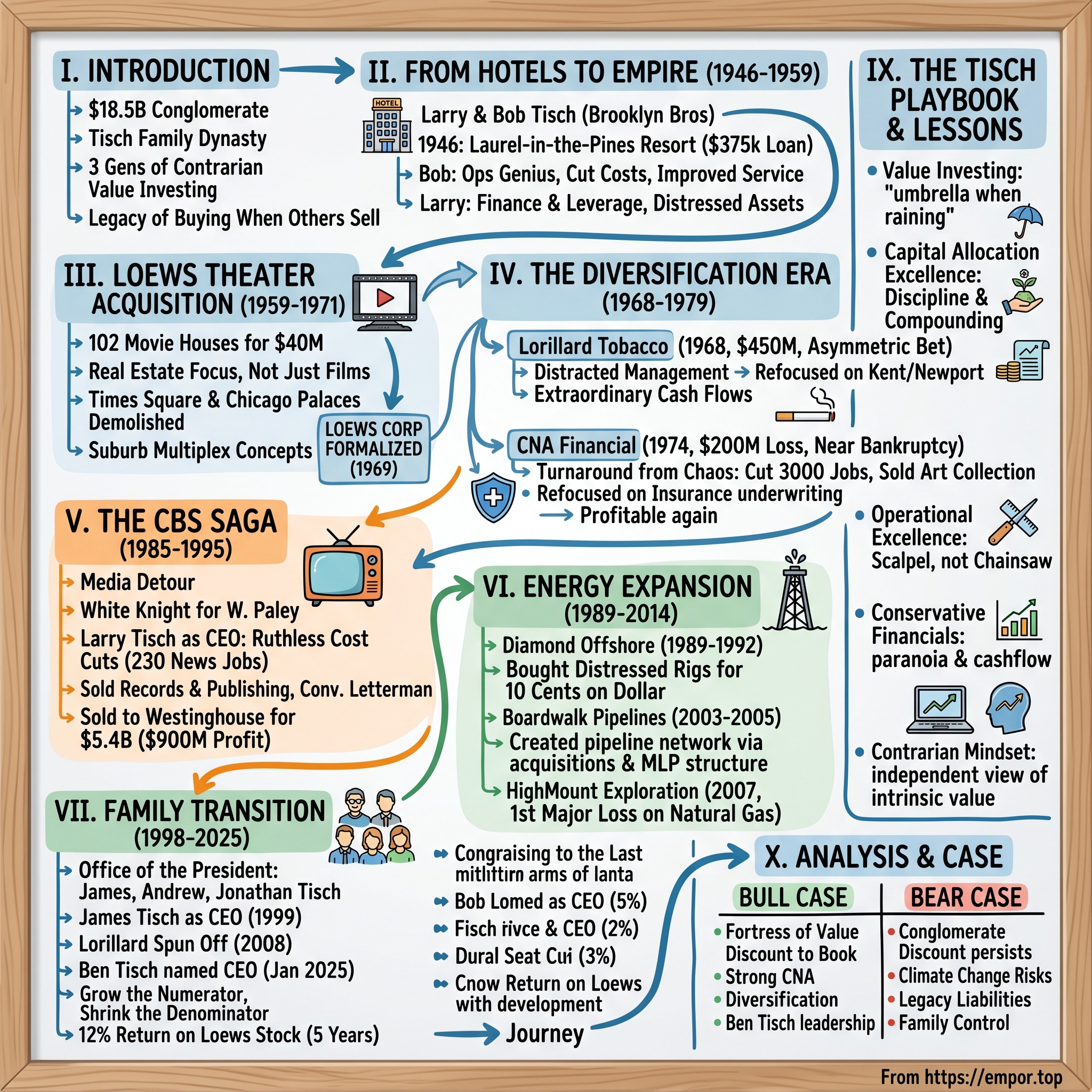

Loews Corporation: The Tisch Empire of Value Investing

I. Introduction & Episode Roadmap

Picture this: A $18.5 billion conglomerate that owns everything from catastrophe insurance to natural gas pipelines, from luxury hotels to plastic packaging plants. At first glance, it seems like a random collection of businesses thrown together by chance. But zoom out, and you'll see the fingerprints of one of America's most successful—yet underappreciated—business dynasties: the Tisch family.

In January 2025, Ben Tisch became the third generation to take the helm at Loews Corporation (NYSE: L), inheriting not just a collection of assets but a 79-year legacy of contrarian value investing. His grandfather Larry and great-uncle Bob started with a single resort hotel in New Jersey, borrowed money from their parents. Today, their creation generates over $16 billion in annual revenues and employs thousands across wildly different industries.

The paradox at the heart of this story? How does a family that started by running Catskills resorts end up controlling one of America's largest property and casualty insurers? Why would hotel operators become pipeline magnates? And perhaps most intriguingly—in an era when conglomerates are out of fashion and activists demand focused pure-plays—how has the Tisch family maintained iron-clad control while still creating enormous shareholder value?

This is a story about seeing value where others see junk. About the discipline to buy when everyone's selling and the wisdom to sell when everyone's buying. It's about operational excellence applied across seemingly unrelated industries. And ultimately, it's about how three generations of one family built, maintained, and evolved an empire by following a deceptively simple philosophy: buy distressed assets, fix the operations, and either hold for cash flow or sell for multiples.

The Tisch playbook isn't just about financial engineering—though they've certainly mastered that art. It's about understanding that beneath every struggling business lies either valuable assets being mismanaged or good businesses being poorly capitalized. They've applied this lens to movie theaters sitting on prime real estate, to tobacco companies distracted by pet food, to insurance giants drowning in their own complexity.

What makes Loews particularly fascinating for students of business history is how it serves as a bridge between the conglomerate era of the 1960s-70s and today's focused, activist-driven markets. While ITT and Gulf + Western imploded, while General Electric dismantled itself, Loews quietly persisted—neither growing for growth's sake nor shrinking under pressure, but methodically allocating capital where they saw the best risk-adjusted returns.

As we dive into this story, we'll explore several key themes that run through eight decades of Tisch family stewardship: the power of patient capital in impatient markets, the advantage of permanent capital in cyclical industries, the importance of operational excellence over financial engineering, and perhaps most critically, how to successfully hand power from one generation to the next without destroying what made the enterprise special in the first place.

We'll see how two brothers from Brooklyn built a hotel empire by understanding post-war leisure trends, how they recognized that movie theaters were actually real estate plays in disguise, how they saved a major insurer from bankruptcy by simply focusing on insurance, and how they've navigated everything from tobacco litigation to natural gas booms to pandemic-era hotel closures.

This isn't just a story about money—though there's plenty of that, with the Tisch family worth over $10 billion today. It's about a particular approach to business that feels almost anachronistic in our age of growth-at-all-costs unicorns and meme-stock volatility. In a world obsessed with disruption, the Tisches have built their fortune on the decidedly undisruptive principle that good businesses bought cheap and run well tend to compound wealth over time.

So buckle up for a journey through American business history, seen through the lens of one remarkable family's ability to find value in the unloved, fix what's broken, and know when to hold versus when to fold. Because while the assets have changed over the decades—from theaters to cigarettes to pipelines—the underlying philosophy has remained remarkably consistent. And in that consistency lies a masterclass in long-term value creation.

II. The Tisch Brothers: From Hotels to Empire (1946-1959)

The year was 1946. America had just won the war, GIs were streaming home, and the nation was ready to celebrate, travel, and spend after years of rationing and sacrifice. In this moment of national optimism, two brothers from Brooklyn saw an opportunity that would launch one of America's great business dynasties.

Larry Tisch was 23, fresh out of the Navy, with a finance degree from NYU and a mind that could calculate compound interest faster than most people could tie their shoes. His younger brother Bob, just 20, had dropped out of college but possessed an almost supernatural ability to understand what made hotels tick—from the thread count of the sheets to the optimal staffing ratios for the night shift. Together, they approached their parents, Al and Sadye Tisch, with a proposition that must have seemed both ambitious and terrifying: loan us the money to buy a resort.

The target was Laurel-in-the-Pines, a 300-room resort in Lakewood, New Jersey, that had seen better days. The price tag: $375,000—a fortune for a family that had built a modest garment business in Manhattan. But Al Tisch had taught his sons to see beyond appearances. "Look for the value others miss," he would say, wisdom earned from years of buying distressed textile inventory and turning it into profitable clothing lines.

What the brothers saw in Laurel-in-the-Pines wasn't just a tired resort—it was a perfectly positioned property for the coming leisure boom. The Catskills and Jersey Shore were about to experience an unprecedented surge as newly prosperous Americans sought affordable vacations within driving distance of New York and Philadelphia. The infrastructure was there; it just needed someone who understood both the numbers and the operations.

The transformation of Laurel-in-the-Pines became the template for everything that followed. Bob attacked the operational inefficiencies with obsessive zeal. He discovered that the previous owners were buying supplies from a dozen different vendors, missing volume discounts. The kitchen was throwing away enough food to feed another hundred guests. The housekeeping staff was scheduled without regard to actual occupancy patterns. Within six months, Bob had cut operating costs by 30% while actually improving service quality—a magic trick he would repeat dozens of times over the coming decades.

Meanwhile, Larry worked the financial side with equal brilliance. He negotiated payment terms with suppliers, established credit lines with local banks who initially wouldn't even return his calls, and most importantly, structured the financing so that the hotel's improved cash flow could fund their next acquisition. He understood intuitively what modern private equity firms would later codify: the power of leverage when applied to stable, cash-flowing assets.

By 1948, the brothers had paid back their parents and were hunting for their second property. They found it in Atlantic City—the Traymore Hotel, a grand but fading monument to the resort's pre-war glory days. The sellers saw a white elephant in a declining resort town. The Tisch brothers saw beachfront real estate that would only become more valuable and a hotel that could be restored to profitability with their proven playbook.

The pattern repeated throughout the early 1950s: find a distressed or underperforming hotel in a good location, acquire it with creative financing, send Bob in to fix operations while Larry optimized the capital structure, then use the cash flow to fund the next deal. They bought properties in Spring Valley, New York; Asbury Park, New Jersey; and throughout the Catskill Mountains—that legendary "Borscht Belt" where Jewish families from New York spent their summers and where young comedians like Sid Caesar and Mel Brooks honed their acts.

But the brothers weren't content to simply accumulate properties. They understood that the hotel business was changing. The rise of automobile culture meant guests expected different amenities. Air conditioning was becoming essential, not optional. Families wanted pools for the kids and golf courses for dad. The old model of a grand dining room and nightly entertainment was giving way to more flexible, casual operations.

This insight led to their most ambitious project yet: building the Americana Hotel in Bal Harbour, Florida, in 1956. Rather than buying and renovating, they decided to create something from scratch—a modern resort that embodied everything they'd learned about what post-war travelers actually wanted. The Americana wasn't just a hotel; it was a statement of intent. The Tisch brothers weren't merely operators of aging resorts anymore. They were players in the big leagues.

The Americana's success—it was profitable from month one, almost unheard of for a new hotel—attracted attention from beyond the hospitality industry. Investment bankers started calling. Other hotel chains inquired about partnerships. And most intriguingly, distressed asset owners in completely different industries began approaching them with opportunities. The brothers had developed a reputation: if you had an underperforming asset with hidden value, the Tisches could find it and unlock it.

By 1959, their hotel empire was generating millions in annual cash flow. They controlled properties from New York to Miami, employed thousands, and had built one of the most efficient hospitality operations in America. But Larry, ever the strategist, saw both opportunity and risk in their concentration. The hotel business was cyclical, seasonal, and increasingly competitive as chains like Holiday Inn began their national expansion. They needed diversification—but not the scattershot kind that would doom so many conglomerates. They needed to find other industries where their playbook—buy distressed, fix operations, optimize capital structure—could work just as well.

What happened next would transform them from successful hotel operators into architects of one of America's most enduring conglomerates. The opportunity came from an unexpected source: Hollywood. Or more precisely, from the fading movie palaces that Hollywood had built in its golden age and then abandoned as television began its conquest of American living rooms. Once again, where others saw obsolescence, the Tisch brothers saw opportunity. But this time, the opportunity wasn't in the business itself—it was in what lay beneath.

III. The Loews Theater Acquisition & Real Estate Genius (1959-1971)

MGM's chief executive was desperate when he picked up the phone to call Larry Tisch in the summer of 1959. The studio's theater chain, Loew's Theatres, was hemorrhaging money—102 movie houses across America that had once showcased Gable and Garbo to packed audiences now sat half-empty most nights, their velvet seats gathering dust as Americans stayed home to watch TV. The executive had heard about the Tisch brothers' magic touch with distressed properties. Could they possibly be interested in a dying theater chain?

Larry's response was vintage Tisch: "We'll take a look." But he wasn't looking at what MGM wanted him to see. While the sellers focused on declining ticket sales and the rise of television, Larry and Bob saw something entirely different during their due diligence tours. In Manhattan, the Loew's State sat on prime Times Square real estate. In downtown Chicago, the Loew's Palace occupied an entire city block. These weren't just theaters—they were incredibly valuable parcels of urban real estate trapped inside an obsolete business model.

The negotiation was a masterclass in information asymmetry. MGM, fixated on stemming their entertainment division losses, valued the chain based on its declining cash flows—essentially pricing it as a melting ice cube. The Tisches valued it based on the underlying real estate, which they estimated was worth three times what MGM was asking. They acquired control for $40 million, using mostly borrowed money and the cash flow from their hotel empire.

What happened next scandalized film preservationists but delighted shareholders. Almost immediately after taking control, the brothers began what critics called "the great demolition." The ornate Loew's State in Times Square, with its gilt moldings and crystal chandeliers? Torn down to build an office tower. The palatial Loew's Palace in Chicago, where thousands had once gasped at King Kong? Demolished for a parking garage and commercial development.

Bob Tisch later recalled the hate mail they received from film buffs and architecture lovers. "They acted like we were burning the Library of Alexandria," he said. "But we weren't in the preservation business. We were in the value creation business." And create value they did. A theater purchased for $400,000 would yield land that sold for $2 million. The proceeds funded more acquisitions, both of additional distressed properties and of the remaining Loew's shares they didn't own.

But the brothers weren't simply real estate liquidators. In markets where the theater business still made sense—typically suburban locations with parking and multiple screens—they invested in modernization. They pioneered the multiplex concept, dividing grand old single-screen theaters into two or three smaller venues that could show different films simultaneously. They understood that the future of movie exhibition wasn't in downtown palaces but in suburban shopping centers where families could park easily and choose from multiple options.

This dual strategy—liquidate the valuable urban real estate, modernize the viable suburban locations—generated enormous cash flows. By 1968, what had started as a $40 million acquisition of a dying business was throwing off tens of millions in annual profits. But more importantly, it gave the Tisches something invaluable: a publicly traded platform for further acquisitions.

In 1969, they formalized this structure by incorporating Loews Corporation as a holding company for their diverse interests. The name was deliberately chosen—dropping the apostrophe from Loew's Theatres to create a distinct corporate identity. This wasn't just a semantic change; it was a declaration of intent. Loews Corporation would be the vehicle through which the Tisch brothers would build something much larger than either hotels or theaters.

The structure they created was elegant in its simplicity. Loews Corporation would be the parent company, publicly traded to provide liquidity and currency for acquisitions. Below it would sit various operating subsidiaries—some wholly owned, others partially owned but controlled. This structure provided maximum flexibility: they could buy entire companies or just controlling stakes, could use cash or stock for acquisitions, could tap public markets for capital while maintaining family control through supervoting shares.

Wall Street initially didn't know what to make of Loews Corporation. It wasn't quite a real estate company, wasn't purely a hotel operator, wasn't really an entertainment company despite owning theaters. Analysts struggled to categorize it, often settling on the catch-all term "conglomerate"—though the Tisches bristled at being lumped in with the sprawling, unfocused giants like ITT or Litton Industries that were gobbling up everything from bakeries to defense contractors.

The difference, Larry would explain to anyone who'd listen, was discipline. "We don't buy companies to build an empire," he said in a rare 1970 interview. "We buy them because we see value that others miss, and because we believe we can operate them better than the current management." This wasn't about ego or empire-building—it was about applying a consistent methodology across different industries.

The theater transformation also taught the brothers a crucial lesson about timing. They had perfectly caught the urban renewal wave of the 1960s, when cities were demolishing old structures to build modern office towers and shopping complexes. But they also recognized that this window wouldn't stay open forever. By 1971, they had liquidated most of the valuable urban real estate and were looking for the next opportunity.

They found it in an industry that seemed about as far from show business as possible: tobacco. But once again, what looked like a radical departure was actually a logical extension of their core strategy. Lorillard wasn't just a tobacco company—it was an undervalued asset with strong cash flows, distracted management, and fixable operational problems. The fact that it made cigarettes instead of running hotels was almost incidental.

The Loews Theatres acquisition had transformed the Tisch brothers from successful regional hotel operators into major players in American business. They had demonstrated that their approach—buying distressed assets, improving operations, and either harvesting cash flows or selling at a premium—could work across different industries. They had created a corporate structure that could accommodate further diversification. And perhaps most importantly, they had shown Wall Street that not all conglomerates were created equal.

As the 1970s dawned, Loews Corporation was perfectly positioned for what would become its golden age of acquisitions. The lessons learned from the theater deal—the importance of underlying asset value, the power of patient capital, the wisdom of selling into strength—would guide them through the next phase of empire building. But first, they had to navigate one of the most controversial acquisitions in their history: a tobacco company that everyone else was running from.

IV. The Diversification Era: Tobacco, Insurance & Beyond (1968-1979)

When Larry Tisch walked into Lorillard's headquarters in 1968, he found executives in the midst of a passionate debate—about cat food. The fifth-largest tobacco company in America, maker of Kent and Newport cigarettes, was dedicating three-quarters of its management meetings to its pet food division, which generated exactly 5% of revenues. This single observation told Larry everything he needed to know: Lorillard wasn't a failing business; it was a distracted one.

The acquisition structure was quintessentially Tisch—bold yet conservative, leveraged yet protected. Loews put up virtually no cash for the $450 million purchase, instead using a complex mix of debt and warrants on Loews stock. If Lorillard performed well, the warrants would be exercised and dilution would be minimal. If it failed, the debt was non-recourse to the parent company. Heads they won big, tails they didn't lose much—the kind of asymmetric bet that Larry had been structuring since his hotel days.

Wall Street was horrified. The Surgeon General's report linking smoking to cancer had come out just four years earlier. Television advertising for cigarettes would be banned within two years. Lawsuits were beginning to percolate through the courts. Why would anyone buy a tobacco company in 1968?

Larry's answer was characteristically unsentimental: "We don't make moral judgments about legal businesses. We make economic judgments about undervalued assets." Lorillard was generating $100 million in annual cash flow, had powerful brands, and was trading at less than five times earnings because everyone was running scared. Moreover, he saw something others missed: while overall cigarette consumption might decline, pricing power would likely increase as the industry consolidated and competition shifted from advertising to brand loyalty.

The operational transformation was swift and ruthless. Within six months, Bob Tisch had sold off the pet food division, the candy subsidiary, and various other "diversification" experiments that previous management had pursued. The executives who spent their time on these distractions? Gone. The corporate jet? Sold. The executive dining room with its French chef? Converted to a cafeteria serving sandwiches.

But the cuts were just the beginning. The real transformation came in refocusing the company on what it did best: selling cigarettes. Bob discovered that Lorillard had been neglecting its core Newport brand, a mentholated cigarette that was quietly gaining share in urban markets. While Kent was the prestige brand that management loved to talk about, Newport was where the growth was. He shifted marketing dollars, repositioned sales forces, and within three years, Newport had doubled its market share.

The tobacco cash flows were extraordinary—Lorillard went from contributing nothing to Loews' bottom line to generating over $200 million annually by 1973. But Larry wasn't content to just harvest cash. He was already hunting for the next big opportunity, and he found it in the wreckage of one of America's most spectacular corporate failures.

CNA Financial Corporation in 1974 was a case study in how not to run a conglomerate. The Chicago-based insurance giant had spent the previous decade on an acquisition spree that would make even the most aggressive 1960s conglomerateurs blush. They owned nursing homes, a mortgage company, a consumer finance operation, even a company that made mobile homes. The only thing they seemed to have forgotten about was insurance.

When the 1973-74 bear market hit, CNA's investment portfolio cratered. When inflation spiked, their long-tail insurance liabilities exploded. The company reported a staggering $208 million loss in 1974—at the time, one of the largest corporate losses in American history. The stock had fallen from $60 to $5. Bankruptcy seemed inevitable.

Larry saw what he had seen at Lorillard: a good business buried under bad management and worse strategy. The core insurance operations, particularly the commercial property and casualty business, were fundamentally sound. The investment portfolio, while battered, contained valuable long-term assets. The company had strong market positions and established distribution relationships. It just needed someone to strip away the distractions and focus on insurance.

The negotiation to acquire control was complex—CNA had multiple classes of stock, contentious bondholders, and regulators breathing down their necks. But Loews gradually accumulated shares throughout 1974, eventually securing control with an investment of roughly $200 million—money that came largely from Lorillard's cash flows. The tobacco company was essentially buying the insurance company.

The turnaround at CNA made the Lorillard transformation look gentle. Three thousand employees were terminated in the first year. Entire floors of CNA's Chicago tower were emptied and leased out. The corporate art collection—including several Picassos—was sold at auction. The company plane wasn't just sold; it was sold to a competitor as a very public signal that the days of executive excess were over.

But again, the cuts were just table stakes. The real work was in the insurance operations. Bob brought in new underwriting leadership who instituted something radical for CNA: actually analyzing risks before insuring them. They pulled out of unprofitable lines, raised prices where they had market power, and perhaps most importantly, completely restructured the investment portfolio to match assets with liabilities—basic insurance management that had been ignored during the go-go years.

The results were stunning. CNA went from a $208 million loss in 1974 to a $110 million profit in 1975. By 1976, it was generating over $150 million annually. The company that had been days from bankruptcy was now one of the most profitable insurers in America.

The Bulova Watch acquisition in 1979 seemed minor compared to Lorillard and CNA—just $65 million for a fading luxury brand that had been losing market share to Seiko and Citizen. But it demonstrated that the Tisch playbook could work even in smaller deals. Within two years, they had streamlined operations, refocused on core watch-making rather than jewelry, and returned the company to profitability.

By the end of the 1970s, Loews Corporation had been transformed from a hotel and theater company into a true conglomerate—but one unlike any other. While ITT was struggling with its hundred-plus subsidiaries and Gulf + Western was earning its "Engulf & Devour" nickname, Loews maintained strict discipline. They owned a small number of large positions in industries they understood, each generating substantial cash flows.

The numbers told the story: revenues had grown from $100 million in 1970 to over $3 billion by 1980. But more importantly, the company was generating over $400 million in annual free cash flow—money that could be reinvested, returned to shareholders, or used for the next big acquisition. The Tisch brothers had built a money machine, powered by cigarettes, insurance, and their uncanny ability to fix broken companies.

Yet as the 1980s began, Larry was growing restless. He had conquered hospitality, real estate, tobacco, and insurance. What mountain was left to climb? The answer would come from an unexpected source: a phone call from the legendary William S. Paley, founder of CBS, who had a problem only someone like Larry Tisch could solve. It would lead to the most controversial chapter in the Tisch story—and the one that would test whether their magic touch could work in the glamorous but treacherous world of network television.

V. The CBS Saga: Larry Tisch's Media Detour (1985-1995)

The call came on a humid September morning in 1985. William S. Paley, the 84-year-old founder and patriarch of CBS, had a problem. His creation—the "Tiffany Network" that had brought Edward R. Murrow and Walter Cronkite into American homes—was under siege. Ted Turner was circling with a hostile takeover bid. Ivan Boesky was accumulating shares. Even Senator Jesse Helms was trying to organize a conservative buyout to combat what he called CBS's "liberal bias." Paley needed what he called "a white knight with sharp teeth."

Larry Tisch seemed an unlikely savior for America's most prestigious television network. He had never worked in media, rarely watched television except for the news, and was famous for staying at budget motels when traveling on business. CBS executives, accustomed to limousines and four-star restaurants, would soon discover that their new major shareholder thought room service was a frivolous expense.

But Paley saw something in Tisch that others missed: here was someone with the financial firepower to repel the raiders but potentially the discipline to fix CBS's bloated cost structure. The network was still enormously profitable, but margins were shrinking as cable television eroded viewership and programming costs soared. Maybe, Paley thought, CBS needed less William Paley and more Larry Tisch.

The initial investment was presented as a defensive move. Loews purchased $750 million worth of CBS stock—about 12% of the company—explicitly to help management fend off the hostile takeover attempts. Larry joined the board as a director, promising to be a "passive investor" who would support current management. That promise lasted exactly 11 months.

By September 1986, Larry had seen enough. CBS was spending $30,000 to send a news crew to cover a routine story that local affiliates could handle for $3,000. The network maintained bureaus in cities where they hadn't originated a story in years. Executive producers had executive producers. The news division alone employed 1,400 people—more than many entire networks.

When CEO Thomas Wyman attempted his own management buyout—essentially trying to take the company private without Paley or Tisch—it provided the opening Larry needed. Wyman was forced out, and in a boardroom coup that shocked the media world, Laurence Tisch became CEO of CBS. The boy from Brooklyn who had started with a single resort hotel now controlled America's most prestigious broadcasting company.

What followed was perhaps the most controversial period in CBS history. Larry approached the network like he had approached every other acquisition: identify waste, cut costs, focus on core operations. But CBS wasn't a tobacco company or an insurance firm—it was a cultural institution whose product was creativity and whose assets walked out the door every night.

The cuts came fast and deep. Within his first year, Larry eliminated 230 jobs from CBS News—about 15% of the division. He sold the CBS Records division to Sony for $2 billion, arguing that music had nothing to do with broadcasting. He divested the publishing operations, shut down marginal programming, and even sold the CBS building in New York, leasing back only the space the network actually needed.

The news division cuts were particularly controversial. When Larry reduced the budget for CBS News by $30 million, Dan Rather publicly complained that quality journalism was being sacrificed for profits. The Washington bureau was downsized. Foreign bureaus were closed. The documentary unit was gutted. Critics said Larry was destroying Edward R. Murrow's legacy; Larry responded that Murrow never had to compete with CNN.

But the Tisch era at CBS wasn't purely about cuts. He made one crucial hire that would define the network for the next decade: convincing David Letterman to leave NBC for CBS in 1993. The deal—$14 million per year, astronomical at the time—showed that Larry would spend when he saw value. Letterman would become CBS's most profitable program and its calling card for younger viewers.

Larry also understood earlier than most that the network television model was fundamentally broken. Cable was fragmenting audiences. Fox had emerged as a fourth network. The internet, while still nascent, was beginning to change how people consumed media. The old model of three networks commanding 90% of American viewership was never coming back.

His response was typically unsentimental: if the business model was broken, it was time to sell. Throughout 1994 and early 1995, Larry quietly shopped CBS to potential buyers. When Westinghouse Electric Corporation offered $5.4 billion—a massive premium to what Loews had paid—Larry didn't hesitate. The same company that he had acquired for $750 million in stock was sold for nearly six times that amount.

The CBS saga revealed both the strengths and limitations of the Tisch approach. The financial results were undeniable: Loews made nearly $900 million on its CBS investment, a spectacular return. The network was more profitable when Larry left than when he arrived, with operating margins nearly double their 1986 levels.

But the cultural cost was significant. CBS never fully recovered its news preeminence. The network that had defined television journalism became just another content provider. Many of the people Larry fired went on to build CNN and Fox News into the powers they became. The Tiffany Network's luster was permanently dimmed.

Larry himself seemed to recognize that CBS had been different from his other acquisitions. In a rare reflective moment years later, he admitted that he had underestimated the role of morale and creativity in a media company. "You can't run a television network like an insurance company," he said. "I learned that maybe too late."

Yet from a pure business perspective, the CBS experience was another Tisch triumph. They had identified an undervalued asset, protected it from hostile takeover, improved its profitability, and sold it at the perfect moment—just before the internet would begin its assault on traditional media. The $900 million profit would fund Loews' next phase of growth, particularly its expansion into energy.

The CBS episode also marked a transition in the Tisch story. Larry was approaching 70, and while still sharp as ever, was beginning to think about succession. The late 1990s would see the gradual transfer of power to the next generation, particularly his son James, who had been watching and learning for decades. But first, there was one more industry to conquer—one that would prove even more lucrative than tobacco or insurance: energy.

VI. Energy Expansion: Diamond Offshore & Boardwalk Pipelines (1989-2014)

The helicopter banked sharply over the Gulf of Mexico, and James Tisch pressed his face against the window to get a better look at the massive oil rig below. It was 1989, oil prices had crashed, and Diamond M Drilling was hemorrhaging money. The sellers, desperate to unload the company, couldn't understand why anyone would want to buy offshore drilling assets when crude was at $15 a barrel. James smiled. He had learned from his father that the best time to buy cyclical assets was when everyone else was selling.

Diamond M owned and operated thirteen offshore drilling rigs—massive, complex machines that could drill in water depths up to 1,000 feet. The replacement cost for this fleet was over $2 billion. Loews bought the entire company for $175 million, essentially paying ten cents on the dollar for hard assets that weren't going anywhere. Oil prices might fluctuate, but the world's thirst for energy would only grow.

The acquisition timing was vintage Tisch. The late 1980s had seen a perfect storm of negative factors for offshore drilling: oil prices had collapsed from over $30 to under $15, the Tax Reform Act of 1986 had eliminated many energy investment incentives, and memories of the Exxon Valdez spill had turned public sentiment against offshore drilling. Day rates for rigs—what oil companies paid to lease them—had fallen by 70%.

But James, who was increasingly taking the lead on new acquisitions as his father focused on CBS, saw what others missed. The easy onshore oil was running out. Future production would have to come from increasingly challenging environments—deeper water, harsher conditions—where only sophisticated offshore rigs could operate. And the industry's depression meant that no one was building new rigs, setting up a supply squeeze when demand inevitably returned.

The operational improvements at Diamond M followed the familiar Tisch playbook, but with a twist. Bob Tisch, now in his sixties but still the operational genius, discovered that rig downtime was killing profitability. When a rig needed maintenance, it could be out of service for weeks. He instituted predictive maintenance schedules, cross-trained crews, and pre-positioned spare parts. Downtime fell from 15% to 5%, effectively adding two rigs' worth of capacity without buying anything.

In 1992, with oil prices still depressed, Loews doubled down, acquiring ODECO (Ocean Drilling & Exploration Company) for $200 million. ODECO brought 39 additional rigs, making the combined company—renamed Diamond Offshore—one of the world's largest offshore drilling contractors. The total investment was now $375 million for assets that would have cost $5 billion to build from scratch.

The payoff came faster than even the optimistic Tisches expected. By 1995, oil prices had recovered to $25, and day rates for offshore rigs had tripled. Diamond Offshore was generating over $300 million in annual cash flow. James convinced his father it was time for a partial monetization—not a full sale, but an IPO that would crystallize some value while maintaining control.

The Diamond Offshore IPO in October 1995 was a sensation. Loews sold 30% of the company for $300 million—nearly recovering their entire investment while still owning 70% of a business now valued at $1 billion. Within two years, Diamond's market cap had reached $3 billion. The offshore drilling investment that everyone thought was crazy had generated a twenty-fold return.

But James wasn't done with energy. He had been studying another beaten-down sector: natural gas pipelines. The deregulation of natural gas markets in the 1990s had created chaos. Pipeline companies that had enjoyed regulated monopolies suddenly faced competition. Many were poorly managed, overleveraged, or both. It was exactly the kind of distressed situation where Loews thrived.

In 2003, Loews paid $1.2 billion for Texas Gas Transmission, a pipeline system moving natural gas from the Gulf Coast to the Midwest and Northeast. The seller, Williams Companies, was in financial distress and needed cash immediately. The price was roughly 60% of replacement cost for pipelines that served critical markets with limited competition.

A year later, they added Gulf South Pipeline Company for $1.1 billion, creating a 20,000-mile network of interstate pipelines. James then executed a brilliant financial engineering move: he combined the two systems into a master limited partnership (MLP) called Boardwalk Pipeline Partners. MLPs were tax-advantaged structures that paid no corporate taxes if they distributed most of their cash flow to investors.

The Boardwalk IPO in 2005 raised $400 million while leaving Loews with 85% ownership. The structure was elegant: Boardwalk's stable, fee-based cash flows supported large distributions to unitholders, Loews received hundreds of millions in annual cash distributions, and the public market provided both a valuation benchmark and potential liquidity.

The timing, once again, proved impeccable. The shale revolution was just beginning, and America was about to transform from a natural gas importer to an exporter. Boardwalk's pipelines were perfectly positioned to transport gas from new shale fields to demand centers. The company that Loews had assembled for $2.3 billion was soon generating $500 million in annual EBITDA.

The HighMount Exploration acquisition in 2007 represented James's attempt to move upstream into actual energy production. Loews paid $4 billion for natural gas fields that Dominion Resources was divesting. The thesis was compelling: own the gas, own the pipelines, capture the entire value chain. But this time, the Tisch timing magic failed.

Natural gas prices, which had been above $8 per thousand cubic feet when the deal was struck, collapsed to under $3 as the shale revolution created a supply glut. HighMount went from generating hundreds of millions in cash flow to barely breaking even. In 2014, after seven years of trying to make it work, Loews sold HighMount for just $1 billion—their first major loss on an acquisition.

The HighMount failure was instructive. It showed that even the Tisches could misread a market, particularly one undergoing revolutionary change. But it also demonstrated their discipline: when an investment wasn't working, they didn't throw good money after bad. They took their loss and moved on.

Despite the HighMount setback, the energy investments were enormously successful overall. Diamond Offshore and Boardwalk Pipelines generated billions in cash flow over two decades. They provided Loews with exposure to the American energy boom while maintaining the capital discipline that had always defined the company. And perhaps most importantly, they proved that the next generation—particularly James—could execute the Tisch playbook as well as the founders.

By 2014, energy had become a core pillar of Loews alongside insurance and hotels. The company that had started with New Jersey resorts now owned drilling rigs in the Gulf of Mexico and pipelines across Middle America. It was a transformation that would have seemed impossible to predict, yet made perfect sense in retrospect. The Tisches had simply followed their north star: buy good assets cheap, improve operations, and let cash flow compound over time. The industry didn't matter; the methodology did.

VII. Family Transition & Modern Governance (1998-2025)

The boardroom at 667 Madison Avenue fell silent as Larry Tisch stood up at the December 1998 board meeting. At 75, the man who had built an empire from a single hotel was ready to step back. But this wasn't a retirement speech—it was an orchestration. Larry and his brother Bob had spent years planning this moment, engineering perhaps their most delicate transaction: transferring power without destroying what made Loews special.

"Bob and I aren't going anywhere," Larry said, surprising no one who knew the brothers' inability to fully let go. "We're simply making room for fresh energy while remaining as co-chairmen." The real news was the creation of the Office of the President—a triumvirate consisting of Larry's son James, Bob's sons Andrew and Jonathan. Three cousins, each raised in the business, would share authority while the patriarchs watched from above.

The arrangement seemed destined for conflict. Business historians could cite dozens of family companies destroyed by cousin rivalries and unclear succession plans. But the Tisches had thought this through with characteristic precision. Each cousin had a clearly defined domain: James focused on capital allocation and new investments, Andrew on Lorillard and the core Loews operations, and Jonathan on the hotel business. They met weekly, decided jointly, but executed separately.

On January 1, 1999, the structure evolved again. James was elevated to sole CEO while Andrew and Jonathan remained as co-chairmen of the executive committee. The message was clear: James would run Loews, but this remained a family enterprise where multiple voices mattered. It was a delicate balance between clear leadership and family cohesion.

James's first major test came almost immediately. CNA Financial, which had been a cash cow for decades, was struggling. The insurer had made an ill-advised acquisition of Continental Insurance in 1995, taking on billions in asbestos and environmental liabilities. By 1999, CNA was bleeding cash, its stock had crashed, and rating agencies were threatening downgrades that would cripple its ability to write new business.

The easy solution would have been to sell or abandon CNA—cut losses and move on. Several board members quietly suggested this path. But James saw an opportunity to prove he wasn't just Larry's son but a worthy successor. He engineered a complex recapitalization: Loews injected $1 billion in fresh capital, but negotiated terms that gave them additional board seats and effective control over major decisions.

Then came the painful part. James ordered CNA to exit entire business lines, terminate 2,400 employees, and take massive reserve charges to finally clean up the Continental mess. Wall Street howled—Loews stock fell 30% as investors worried about good money after bad. But James held firm, channeling his father's patience. By 2003, CNA was profitable again. By 2005, it was generating $500 million annually for Loews.

But the second generation faced challenges the founders never encountered. The tobacco business, once Loews' crown jewel, was under existential threat. The 1998 Master Settlement Agreement between tobacco companies and 46 states had cost Lorillard billions. Individual lawsuits were proliferating—520 in 2001 alone. Public opinion had turned decisively against smoking. ESG investing, still nascent, was beginning to exclude tobacco companies.

James's solution was pragmatic rather than sentimental. He couldn't sell Lorillard—the liability tail was too long and uncertain. But he could optimize it for cash generation while it lasted. Lorillard focused exclusively on Newport, its menthol cigarette that commanded premium prices. Marketing spend was slashed—why advertise a product everyone knew? The workforce was reduced to skeleton crews. Lorillard became a cash machine, generating $400-500 million annually with minimal investment.

The real masterstroke came in 2008 when Lorillard was spun off as a separate public company through a tax-free distribution to Loews shareholders. This accomplished multiple objectives: it removed tobacco from Loews' portfolio (addressing ESG concerns), crystallized value (Lorillard's market cap reached $15 billion), and gave shareholders the choice to own tobacco exposure or not. When Lorillard was sold to Reynolds American in 2014 for $27 billion, early shareholders had made a fortune.

Meanwhile, the family dynamics were evolving. Larry Tisch died in 2003 at age 80, having built a fortune estimated at $4 billion. Bob continued as co-chairman until his death in 2005. The founders were gone, but their influence permeated everything. James kept Larry's sparse office exactly as it was—metal desk, basic chairs, no art—as a reminder that frugality and focus mattered more than appearances.

The third generation was already being groomed. Ben Tisch, James's son, joined Loews in 2006 after stints at Goldman Sachs and private equity firm Oak Hill Capital. Like his father and grandfather, he started at the bottom—working in CNA's surety division, analyzing pipeline contracts at Boardwalk, learning hotel operations from the ground up. The Tisch tradition held: you earned authority, you weren't born into it.

Andrew and Jonathan, meanwhile, had carved out their own domains. Andrew focused on Loews' investment portfolio and capital allocation, becoming James's key strategic partner. Jonathan transformed Loews Hotels from a small collection of properties into a significant player, developing partnerships with Universal Orlando and other theme park operators that generated steady cash flows with minimal capital investment.

The 2008 financial crisis tested the second generation's crisis management skills. Diamond Offshore's revenues collapsed as oil companies canceled drilling projects. CNA's investment portfolio was hammered. Boardwalk's customers were going bankrupt. Loews stock fell from $50 to $20. Some analysts questioned whether the conglomerate model could survive modern markets.

James's response was vintage Tisch: use the crisis to get stronger. While competitors were selling assets at distressed prices, Loews was buying. They increased their CNA stake when the stock hit $15. They ordered new drilling rigs for Diamond at 40% discounts from Korean shipyards desperate for orders. They bought pipeline capacity that distressed sellers were dumping. By 2010, when markets recovered, Loews had significantly strengthened its competitive position.

The governance structure also evolved with the times. Independent directors were added—no longer just family friends but serious business leaders who would challenge management. Compensation was tied to long-term value creation rather than annual earnings. Risk committees were established to monitor everything from cyber threats to climate change impacts on coastal hotels.

In January 2025, the transition reached its next milestone: Ben Tisch was named CEO, with James becoming Executive Chairman. The announcement was deliberately low-key—a press release on a quiet Monday, no fanfare or celebration. The message was clear: this was a continuation, not a revolution. The third generation would lead, but the Tisch principles would endure.

The challenges facing Ben are different from those his grandfather or father confronted. Activist investors question the conglomerate structure. ESG pressures complicate capital allocation. Technology threatens traditional business models. But the family's 79-year history suggests they'll adapt while maintaining their core discipline: buying undervalued assets, improving operations, and compounding wealth over generations.

VIII. Current Portfolio & Financial Performance (2020-2025)

The waiting room at 667 Madison Avenue hummed with nervous energy as major media conglomerates gathered to make their pitches. In the spring of 2025, James Tisch looked across the polished conference table at his son Ben and smiled slightly—a gesture his father Larry would have recognized. After a quarter-century at the helm, James was passing control of Loews Corporation to the third generation. The portfolio that greeted Ben Tisch was radically different from the one his grandfather had assembled, yet the underlying philosophy remained unchanged: own good businesses, run them well, and compound wealth over time.

CNA Financial: The Insurance Colossus

CNA Financial (NYSE: CNA) represents the largest piece of the Loews empire, with the parent company holding an 86.5% stake in one of America's ten largest property and casualty insurers. The insurance subsidiary that Larry and Bob Tisch rescued from near-bankruptcy in 1974 has become the primary engine of Loews' cash generation, contributing approximately 75% of the parent company's revenues.

The transformation has been remarkable. CNA's net income attributable to Loews improved year-over-year in 2024 due to higher net investment income and favorable net prior year loss reserve development, partially offset by higher net catastrophe losses. The insurer has masterfully navigated the hard market conditions of recent years, with net written premiums growing by 6% and net earned premiums growing by 7% in the second quarter of 2024.

What makes CNA particularly valuable in the current environment is its disciplined underwriting combined with sophisticated investment management. Net investment income increased due to higher income from fixed income securities as a result of favorable reinvestment rates and a larger invested asset base, along with favorable returns from limited partnerships. The company has been reinvesting maturing bonds at rates not seen since before the financial crisis, creating a powerful tailwind for future earnings.

The property and casualty operations remain the core focus, with management maintaining strict underwriting discipline even as competitors chase growth. Property and Casualty combined ratio increased by one point to 93.1% compared to 92.1% as a result of higher catastrophe losses, while the underlying combined ratio remained steady at 91.4% for both periods. This consistency in the underlying ratio—which strips out catastrophe losses and reserve development—demonstrates the fundamental health of the insurance operations.

Yet challenges loom. The fourth quarter of 2024 included a pension settlement charge of $265 million (after-tax and noncontrolling interests), a reminder that legacy liabilities still require attention. Hurricane season has become increasingly costly, with Property and Casualty underwriting income decreasing due to higher catastrophe losses, including Hurricane Milton. Climate change isn't just an ESG talking point for CNA—it's a fundamental risk that must be priced into every coastal property policy.

Boardwalk Pipelines: Energy Infrastructure Cash Machine

Boardwalk Pipelines represents Loews' bet on America's energy infrastructure, operating 14,000 miles of natural gas and natural gas liquids pipelines across the central United States. The business James Tisch assembled through acquisitions in 2003-2004 has evolved into a steady cash generator, benefiting from the structural shift in American energy production.

Boardwalk's results improved year-over-year mainly due to increased revenues from re-contracting at higher rates and recently completed growth projects. The business model is elegantly simple: long-term contracts with creditworthy counterparties, minimal commodity exposure, and strategic positioning in high-demand corridors. It's the kind of boring, predictable business that the Tisches have always loved.

The shale revolution that destroyed HighMount has been a boon for Boardwalk. As natural gas production shifted from traditional fields to shale plays, Boardwalk's pipelines became essential infrastructure for moving gas from new production areas to demand centers. The company has capitalized on this by re-contracting at higher rates and completing growth projects that expand capacity in key markets.

But the energy transition poses long-term questions. Will natural gas remain the "bridge fuel" as America decarbonizes? Can pipelines be repurposed for hydrogen or other alternative fuels? Boardwalk's management is exploring these options, but the uncertainty adds complexity to capital allocation decisions. For now, the cash flows remain robust, but Ben Tisch will need to navigate an energy landscape his grandfather could never have imagined.

Loews Hotels: The Family Legacy Business

Loews Hotels holds special significance as the original family business, though it now represents the smallest piece of the portfolio. The company operates 25 properties across the United States and Canada, focusing on convention hotels and resort destinations that can command premium rates.

The hotel division faced unique challenges in recent years. Higher interest expense, driven by the Loews Arlington which opened in the first quarter of 2024, along with lower capitalized interest on projects under development and higher interest rates on debt refinanced in 2024, negatively impacted earnings. Results also decreased due to lower equity income from joint ventures.

Yet the long-term strategy remains sound. By partnering with theme park operators like Universal Orlando, Loews Hotels has created a differentiated model that's less dependent on business travel than traditional city-center hotels. Adjusted EBITDA increased to $81 million compared to $80 million as higher earnings from a full quarter of the Loews Arlington offset lower earnings from Universal Orlando Resort properties.

The hotel business also serves as a training ground for the next generation. Alex Tisch, Ben's cousin, now leads the division, continuing the family tradition of hands-on operational management. It's a reminder that despite the billions in market cap and sophisticated financial engineering, the Tisches still understand the basics of hospitality: clean rooms, good service, and operational efficiency.

Altium Packaging: The Newest Addition

Altium Packaging represents Loews' most recent major platform investment, manufacturing rigid plastic packaging for consumer and industrial markets. The company develops, manufactures, and markets a range of extrusion blow-molded and injection molded plastic containers, as well as manufactures commodity and differentiated plastic resins.

The packaging business might seem like an odd addition to a portfolio of insurance, pipelines, and hotels, but it fits the Tisch criteria: stable cash flows, essential products, and opportunities for operational improvement. The plastic packaging industry is fragmented, creating consolidation opportunities. Environmental concerns about single-use plastics create both risks and opportunities for companies that can innovate in recycling and sustainable materials.

Financial Performance: The Numbers Tell the Story

The 2024 financial results validated the Tisch approach to conglomerate management. Loews Corporation reported net income of $457 million, or $2.05 per share, in the first quarter of 2024, which represents a 22% increase over $375 million, or $1.61 per share, in the first quarter of 2023. For the full year, net income reached $1,414 million, demonstrating the earning power of the diversified portfolio.

The capital allocation machine continues to hum. Book value per share, excluding AOCI, increased to $85.42 as of June 30, 2024, from $81.92 as of December 31, 2023 due to strong operating results and repurchases of common shares. This steady book value growth, combined with aggressive share repurchases, creates a powerful compounding effect for remaining shareholders.

Speaking of buybacks, the company has been voracious in repurchasing its own stock. During the three months ended March 31, 2025, Loews Corporation repurchased 4.5 million shares of its common stock for a total cost of $376 million. With 210.3 million shares outstanding as of March 31, 2025, the company has dramatically reduced its share count from the 600 million shares outstanding when James took over in 1999.

Loews Corporation shares are currently $83, up 12% over the past year and up 55% over the past five years. While not spectacular compared to high-flying tech stocks, this steady appreciation combined with the company's conservative balance sheet—$3.2 billion in cash and investments against $1.8 billion in debt as of March 31, 2024—represents exactly the kind of risk-adjusted returns the Tisches have always pursued.

Parent Company Operations: The Capital Allocation Engine

Beyond the operating subsidiaries, the parent company itself functions as a capital allocation machine. The corporate segment manages the investment portfolio, oversees capital allocation decisions, and occasionally makes new platform investments. This structure provides maximum flexibility—Loews can buy entire companies, take minority stakes, or simply return capital to shareholders depending on available opportunities.

The parent company investment portfolio has been a significant contributor to results, though returns can be volatile. The corporate segment reported a net loss of $34 million in Q1 2025 compared to net income of $10 million in Q1 2024, with results decreasing primarily due to investment losses compared to investment gains from parent company equity securities. This volatility is the price of maintaining a flexible, opportunistic investment approach.

James Tisch's greatest innovation was perhaps the aggressive share repurchase program. By reducing the share count by two-thirds during his tenure, he effectively tripled the ownership stake of remaining shareholders without requiring any operational improvements. It's financial engineering at its finest—simple, powerful, and perfectly aligned with long-term shareholders.

Looking Forward: The Ben Tisch Era

As Ben Tisch takes the helm, he inherits a company generating over $16 billion in annual revenues with dominant positions in insurance and energy infrastructure. The challenges are different from those his grandfather faced—ESG pressures, climate change, technological disruption—but the toolkit remains the same: patient capital, operational excellence, and contrarian thinking.

The "personal tutoring" Ben received can be distilled into "six simple words: Grow the numerator, shrink the denominator." He explained: "The numerator is the intrinsic value of the enterprise, or more colloquially the sum of our parts. Therefore, we focus on actions we can take, mainly from a capital allocation perspective, to increase the intrinsic value of our underlying businesses".

This philosophy—grow value per share rather than absolute size—distinguishes Loews from empire-building conglomerates. It's why the company has survived and thrived while contemporaries have broken apart or disappeared. In an era of activist investors and demands for "pure plays," Loews continues to prove that disciplined conglomerate management can create value.

The portfolio today generates enormous cash flows, maintains conservative leverage, and operates in industries with high barriers to entry. It's a collection of businesses that would be difficult to replicate and expensive to acquire separately. For long-term investors seeking exposure to multiple sectors through a single, well-managed vehicle, Loews offers a compelling proposition—even if Wall Street continues to apply its habitual conglomerate discount.

IX. The Tisch Playbook: Business & Investing Lessons

In the fall of 1968, a reporter asked Larry Tisch why he was buying a tobacco company when everyone else was selling. His response became legendary among value investors: "We buy umbrellas when it's raining. Everyone else waits for sunshine, then wonders why umbrellas are so expensive." This simple metaphor encapsulates the Tisch playbook—a methodology that has created billions in value across eight decades and three generations.

The Value Investing Philosophy: Seeing What Others Miss

The Tisches didn't invent value investing—Benjamin Graham did that. But they perfected its application to entire businesses rather than just stocks. When Larry and Bob bought Lorillard, they didn't see a tobacco company facing regulatory doom; they saw a cash-generating machine trading at five times earnings. When they acquired CNA, they didn't see a bankrupt insurer; they saw a fundamentally sound business buried under terrible management.

This ability to separate temporary problems from permanent impairments is perhaps the most important lesson from the Tisch story. Lorillard faced regulatory headwinds, but people weren't going to stop smoking overnight. CNA had massive losses, but insurance would always be necessary. Offshore drilling was out of favor when they bought Diamond M, but oil wasn't going away. The pattern repeats: identify essential businesses facing temporary distress, buy them cheap, then wait.

But here's the crucial insight that separates the Tisches from mere bottom-feeders: they never bought bad businesses just because they were cheap. Every acquisition had to pass what Larry called the "sleep test"—could you own this business for ten years and sleep soundly? No technology bets, no fashion companies, no businesses dependent on brilliant management or favorable regulation. Just steady, cash-generating enterprises that would survive regardless of the economic weather.

Capital Allocation Excellence: The Art of Doing Nothing

Warren Buffett once said that investing should be like watching paint dry. If you want excitement, take $800 and go to Las Vegas. The Tisches would agree, but they'd probably suggest keeping the $800 and buying more shares. Their capital allocation philosophy can be summed up in four rules:

First, never overpay, no matter how attractive the business. Larry famously walked away from deals over a few percentage points of valuation. This discipline meant missing some opportunities, but it also meant never suffering catastrophic losses. As James likes to say, "The first rule of compounding is don't lose money. The second rule is see rule one."

Second, always maintain financial flexibility. Loews has never been highly leveraged, never dependent on capital markets, never forced to sell assets at distressed prices. This conservative balance sheet management might reduce returns in good times, but it ensures survival in bad times—and bad times are when the best opportunities appear.

Third, be willing to hold forever but ready to sell tomorrow. The Tisches aren't sentimental about their investments. They held Lorillard for 40 years, then spun it off when the liability risks became too uncertain. They bought CBS to protect it from raiders, then sold it when the media landscape shifted. This emotional detachment from assets is rare in family businesses, where ego often overrides economics.

Fourth, and perhaps most importantly: when you don't see good opportunities, return capital to shareholders. The massive share repurchase program under James wasn't just financial engineering—it was an admission that buying back stock at a discount to intrinsic value was the best available use of capital. Too many conglomerates destroy value by forcing investment; the Tisches create value by exercising restraint.

Operational Excellence: The Unglamorous Path to Wealth

Every Tisch acquisition follows a predictable pattern that would bore most MBA students to tears. First, cut unnecessary costs—not with a chainsaw, but with a scalpel. Bob Tisch's approach to cost-cutting was almost surgical in its precision. He didn't just slash budgets; he understood where every dollar went and why.

At CNA, they discovered executives had company cars but rarely drove them. The cars were sold, but executives who actually needed transportation got allowances. At Lorillard, they found the company was sponsoring yacht races. The sponsorships ended, but legitimate marketing programs continued. This wasn't about being cheap—it was about being intelligent with capital.

The second step: focus relentlessly on core operations. Every Tisch acquisition involved divesting distractions. Lorillard's pet food division, CNA's nursing homes, CBS's record label—all sold to companies that actually wanted to be in those businesses. This focus sounds obvious, but it's surprisingly rare. Most managers empire-build; the Tisches empire-optimize.

Third: invest in the business, but only where returns justify it. Diamond Offshore ordered new rigs during the downturn when construction costs were low. Boardwalk built pipeline expansions where long-term contracts guaranteed returns. Loews Hotels developed properties adjacent to theme parks where premium pricing was sustainable. Growth for growth's sake was never the goal—profitable growth was.

Family Business Dynamics: Building a Dynasty Without Drama

The Tisch family has avoided the succession disasters that destroy most business dynasties. No Shakespearean battles between brothers, no incompetent nephews given senior roles, no family feuds played out in the Wall Street Journal. How did they manage this?

The answer starts with meritocracy. Yes, family members got opportunities, but they had to earn their positions. Ben Tisch didn't become CEO just because his last name was Tisch—he spent 14 years learning the business, managing subsidiaries, proving his competence. When family members weren't suited for operational roles, they found other ways to contribute or pursued different careers entirely.

The structure helps too. By maintaining a holding company with separate operating subsidiaries, different family members could run different businesses without stepping on each other's toes. Jonathan ran hotels, Andrew focused on investments, James oversaw everything. Clear lines of authority prevented the confusion that often paralyzes family businesses.

Most importantly, the family maintained unity around core principles. Every Tisch understood that the goal was building long-term value, not extracting short-term benefits. No one used company jets for vacations, no one hired unqualified friends, no one confused the company's money with their own. This discipline, instilled by Larry and Bob and maintained by subsequent generations, created a culture where the business came first.

Conservative Financial Management: The Power of Paranoia

Andy Grove said only the paranoid survive. The Tisches would modify that: only the paranoid thrive. Their financial conservatism seems almost quaint in an era of leveraged buyouts and SPAC mania, but it's this conservatism that has allowed them to survive and capitalize on multiple crises.

Loews never stretches for returns. When interest rates were near zero and everyone was reaching for yield, Loews kept its powder dry. When private equity firms were paying 15x EBITDA for acquisitions, Loews sat on its hands. This patience is painful—shareholders complain, analysts downgrade, competitors seem to race ahead. But when markets crack, Loews has capital while others are scrambling for liquidity.

The company also maintains multiple sources of financial flexibility. The parent company has its own cash and investments. Each subsidiary maintains appropriate capital for its needs. Credit facilities remain undrawn until needed. This belt-and-suspenders approach means paying for unused capacity, but it also means never being forced into unfavorable terms.

As Ben Tisch noted, "My grandfather Larry Tisch was a cashflow-based investor, my father Jim is a cashflow-based investor, and—you may have figured this out by now—I too am a cashflow-based investor". This focus on cash rather than accounting earnings means the Tisches avoid the financial engineering that makes numbers look good but doesn't create real value.

The Contrarian Mindset: Comfort with Discomfort

Perhaps the hardest lesson to internalize from the Tisch playbook is the willingness to be contrarian. It's psychologically painful to buy when everyone's selling, to hold when everyone's panicking, to sell when everyone's euphoric. The Tisches have developed an almost Buddhist detachment from market sentiment.

This contrarianism isn't reflexive—they don't buy things just because they're unpopular. But they've trained themselves to see panic as opportunity and euphoria as danger. When offshore drilling was "uninvestable" in 1989, they saw a chance to buy irreplaceable assets at scrap value. When everyone wanted to own CBS in the 1980s, they saw an overvalued property ready for sale.

The key is having an independent view of intrinsic value. The Tisches don't care what the market thinks something is worth today—they care what it will generate in cash over the next decade. This long-term orientation provides the confidence to act against the crowd. When you know what something is worth, market prices become opportunities rather than judgments.

Lessons for Investors

For those seeking to apply the Tisch playbook, several principles emerge:

First, develop deep expertise in valuing businesses, not just stocks. Understanding industrial economics, competitive dynamics, and operational realities matters more than financial modeling. The Tisches could value a hotel, an insurance company, or a pipeline because they understood the businesses, not just the numbers.

Second, maintain permanent capital. The Tisch magic works because they're never forced sellers. Individual investors can replicate this by avoiding leverage, maintaining emergency funds, and investing only money they won't need for a decade.

Third, embrace boredom. The best investments are often the most boring—steady businesses in unglamorous industries generating predictable cash flows. The excitement should come from compounding returns, not from daily price movements.

Finally, remember that not investing is also a decision. The Tisches have probably walked away from a thousand deals for every one they've made. This discipline—the willingness to do nothing when nothing is the right thing to do—might be their greatest edge.

The Tisch playbook isn't revolutionary. It's not sophisticated. It doesn't require complex mathematics or inside information. It simply requires discipline, patience, and the courage to act when opportunities arise. In a world obsessed with disruption and innovation, the Tisches have built a fortune on the radical idea that buying good businesses cheaply and running them well creates lasting wealth. Eight decades and three generations later, it's still working.

X. Analysis & Bear vs. Bull Case

Wall Street has never quite known what to make of Loews Corporation. The analyst reports read like Rorschach tests—value investors see a disciplined allocator trading at a discount, growth investors see a sleepy conglomerate in mature industries, and quants see a complex entity that doesn't fit neatly into their models. This confusion creates opportunity, but it also raises legitimate questions about Loews' future in modern capital markets.

The Bull Case: A Fortress of Value

The optimists start with the numbers. Trading at roughly 0.7 times book value, Loews offers investors the rare opportunity to buy a dollar of assets for seventy cents. This isn't some cigar-butt portfolio of declining businesses—these are high-quality franchises generating substantial cash flows. CNA alone, if valued at the same multiple as peer insurers, would be worth close to Loews' entire market cap.

The diversification that confuses Wall Street actually reduces risk for long-term investors. When hurricanes hammer CNA's underwriting results, Boardwalk's steady pipeline fees provide ballast. When energy prices crater, insurance investment income keeps flowing. This isn't the random diversification of 1960s conglomerates—it's a carefully curated portfolio of uncorrelated cash streams.

Book value per share growth tells the real story—increasing to $85.42 from $81.92 in just six months of 2024, and that's excluding accumulated other comprehensive income. Add in the aggressive share repurchases, and the math becomes compelling. Fewer shares dividing growing book value equals accelerating per-share value creation, regardless of what the stock market recognizes today.

The capital allocation flexibility provides another advantage. Unlike pure-play companies locked into their industries, Loews can deploy capital wherever returns are highest. When insurance pricing hardens, they can retain more risk at CNA. When energy infrastructure looks attractive, they can fund Boardwalk expansions. When everything looks expensive, they buy back stock. This optionality has value that traditional valuation models struggle to capture.

The third generation leadership under Ben Tisch brings fresh energy while maintaining proven disciplines. He inherits a company with minimal debt, substantial cash, and subsidiaries that largely run themselves. This is not a turnaround situation requiring heroic intervention—it's a wealth compounding machine that needs only competent steering.

Insurance and energy infrastructure—Loews' core holdings—are essential services with pricing power. Property insurance isn't optional for businesses; natural gas pipelines can't be easily replaced. These aren't businesses facing disruption from Silicon Valley startups. They're complex, regulated, capital-intensive operations with massive barriers to entry.

The hidden assets provide additional upside. Boardwalk's pipelines would cost tens of billions to replicate today. CNA's insurance licenses and distribution relationships took decades to build. Loews Hotels sits on irreplaceable real estate in key markets. The replacement value far exceeds the carrying value, creating a margin of safety for investors.

The Bear Case: A Melting Ice Cube

The skeptics have their own compelling arguments. Start with the conglomerate discount, which has persisted for decades despite the Tisches' best efforts. Markets hate complexity, and Loews is complex. The company requires investors to understand insurance, energy infrastructure, hospitality, and packaging—most won't bother. This structural discount shows no signs of disappearing.

Climate change poses existential risks to multiple subsidiaries. CNA faces escalating catastrophe losses from hurricanes, wildfires, and floods. Boardwalk's pipelines transport fossil fuels that many believe must be phased out. Loews Hotels has significant coastal exposure. The company is essentially long climate stability—a increasingly questionable bet.

The insurance industry faces structural headwinds beyond climate. Social inflation—juries awarding ever-larger verdicts—pressures liability lines. Cyber risks are exploding but remain difficult to price. Low interest rates for most of the last decade compressed investment returns. CNA has navigated these challenges so far, but the degree of difficulty keeps rising.

Energy transition threatens Boardwalk's long-term value. Yes, natural gas is cleaner than coal, but renewable energy costs continue falling. Electrification of heating and transportation reduces gas demand. The Infrastructure Investment and Jobs Act funds alternatives to fossil fuel infrastructure. Boardwalk's pipelines might become stranded assets—valuable today, worthless tomorrow.

The family control structure, while providing stability, limits shareholder influence. The Tisch family votes control key decisions, and they've shown little interest in breaking up the company or selling assets just to close the conglomerate discount. Activist investors who might unlock value at other companies have no leverage here.

The capital allocation record, while strong, isn't perfect. HighMount was a multi-billion dollar mistake. The CBS experience, while profitable, distracted management and damaged institutional knowledge. For every Lorillard or Diamond Offshore success, there's a reminder that even the Tisches can misread markets.

Competition for acquisitions has intensified dramatically. Private equity firms with trillions in dry powder bid aggressively for the same distressed assets Loews traditionally bought. Sovereign wealth funds accept lower returns. Strategic buyers pay synergy premiums. The Tisch playbook of buying cheap and fixing operations works only if you can find things to buy cheaply.

Competitive Positioning: David Among Goliaths

Comparing Loews to other conglomerates reveals both strengths and weaknesses. Berkshire Hathaway, the obvious comparison, trades at a premium to book value while Loews trades at a discount. Why? Berkshire is simpler to understand, has Warren Buffett's halo effect, and owns higher-quality businesses like Apple and Coca-Cola. But Berkshire is also too large to generate exceptional returns—Loews' smaller size provides more flexibility.

Markel Corporation, another insurance-focused conglomerate, trades at 1.3 times book despite a less impressive long-term record. The difference? Markel is purely focused on insurance and venture investments—easier for analysts to model and value. Complexity has a cost, and Loews pays it.

Against pure-play competitors, each Loews subsidiary holds its own. CNA ranks among the top commercial insurers despite lacking the scale of Chubb or Travelers. Boardwalk competes effectively with larger pipeline companies like Kinder Morgan. Loews Hotels punches above its weight in the convention and resort segments. The businesses are solid, even if the conglomerate structure obscures their value.

The Future of Conglomerates

The broader question is whether conglomerates make sense in modern markets. The academic consensus says no—investors can diversify themselves more efficiently than companies can. The market agrees, consistently applying discounts to complex entities. Yet a handful of conglomerates continue creating value, suggesting the model isn't dead, just difficult.

Loews' answer is that permanent capital and patient management create advantages that overcome the conglomerate discount. When markets panic, Loews has capital. When industries consolidate, Loews can participate. When technological change creates disruption, Loews can adapt without stock market pressure. These advantages are real but hard to quantify.

The ESG movement poses particular challenges for conglomerates. How do you rate a company that owns both renewable energy infrastructure (good for ESG) and natural gas pipelines (bad for ESG)? How do you evaluate governance when family control limits shareholder rights but also enables long-term thinking? Loews doesn't fit neatly into ESG frameworks, potentially limiting institutional ownership.

The Verdict: Compelling but Complicated