Klaviyo, Inc.: The Database That Captured E-Commerce

I. Introduction & Episode Roadmap

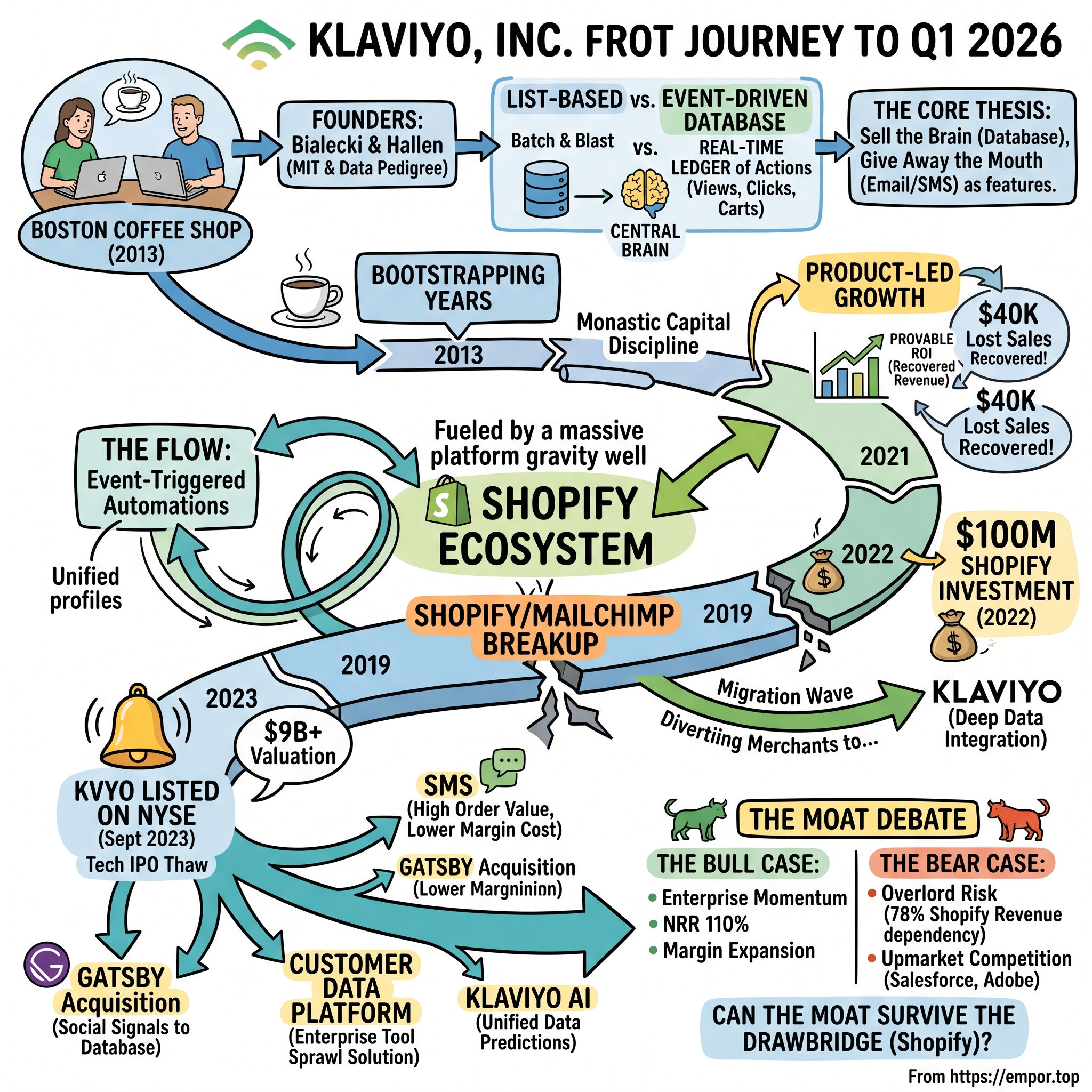

Picture a Boston coffee shop sometime in 2013. Two software engineers are hunched over laptops, nursing cold drinks well past the point where the barista starts giving them looks. They have no venture capital, no sales team, and no marketing budget. What they do have is a conviction that borders on stubbornness: that the entire multi-billion-dollar industry of email marketing software has been built on the wrong foundation. Everyone else is building a nicer envelope. Andrew Bialecki and Ed Hallen want to build the filing cabinet underneath it.

That distinction sounds academic. It is not. It is the whole story of how Klaviyo, a company that took almost no institutional money for its first five years, grew into a business that as of its first quarter of fiscal 2026 was generating $358.0 million in quarterly revenue, growing 28% year over year, and serving roughly 196,000 customers around the world.7 By mid-2026 the company carried an equity value comfortably in the multiple-billions and traded on the New York Stock Exchange under the ticker KVYO.

Here is the thesis worth holding in your head for the next two hours. Klaviyo did not win by building a better email app. Plenty of companies built perfectly good email apps and most of them are footnotes now. Klaviyo won by building a hyper-optimized, real-time customer database first, and then treating email, SMS, and push notifications as applications that sit on top of that database. The founders' phrase for it internally was the "central brain." Everyone else sold the mouth. Klaviyo sold the brain and gave away the mouth as a feature.

That architectural bet had a commercial consequence that shaped everything: it made Klaviyo almost impossible to rip out once installed. When a merchant's entire history of purchases, clicks, page views, and abandoned carts lives inside your database, and every automated message the brand sends is wired to that data, switching to a competitor is not a software migration. It is an organ transplant.

But the story has a second protagonist, and it is not entirely under Klaviyo's control. That protagonist is Shopify. If Klaviyo is the brain of the direct-to-consumer economy, Shopify is the nervous system it plugs into. As of Q1 2026, roughly 78% of Klaviyo's annual recurring revenue was tied to brands running on the Shopify platform.10 That relationship has made Klaviyo enormously rich. It has also made Klaviyo structurally dependent on a partner that is, in some plausible futures, also a competitor. Understanding Klaviyo means understanding this gravity well — how a company can be both a beneficiary and a hostage of the same ecosystem.

Our roadmap runs from those Boston coffee shops through the watershed 2019 divorce between Shopify and Mailchimp that handed Klaviyo a market on a silver platter; through the $100 million strategic investment Shopify made in 2022 that turned an alliance into something closer to a marriage with a prenup; through the September 2023 IPO that reopened the American tech listing market after a long freeze; and into today's high-stakes campaign to move upmarket into the enterprise with a native Customer Data Platform and an AI engine. Along the way we will keep testing one question that matters to any long-term owner of this business: is the moat as deep as it looks, or is it a moat with one very large drawbridge controlled by someone else?

Let's start where every good origin story starts — with two people and a problem nobody else thought was interesting.

II. The Boston Bootstrap: Relational Databases vs. Standard CRM

Andrew Bialecki is not the archetype of the swashbuckling startup founder. He is an MIT-trained engineer — physics and math — who reads like the smartest person in the room precisely because he never seems to be trying to prove it. Ed Hallen is the product mind, an operator who thinks in terms of what a customer actually does on a Tuesday afternoon rather than what a slide deck says they want. The two met at Applied Predictive Technologies, a Washington-area analytics firm that built software to help large enterprises run controlled business experiments — the kind of place where you learn, in your bones, that the answer to almost every commercial question lives in data most companies are too disorganized to use. APT was later acquired by Mastercard, which tells you the pedigree of the shop.1

The insight that became Klaviyo came from noticing an asymmetry. In the world of business-to-business selling, sales teams had Salesforce — a system of record that captured every account, contact, deal, and interaction, and let a rep segment and act on it. In the world of business-to-consumer e-commerce, there was nothing comparable. A merchant might have thousands or millions of customers, each with a messy trail of transactions in one system, browsing behavior in another, and email history in a third. The data existed. It just lived in silos that never talked to each other, which meant a merchant could not easily answer a question as basic as "show me everyone who bought running shoes twice, browsed socks last week, and hasn't opened an email in a month."

Here is the technical heart of the thing, explained without the jargon. The dominant email tools of the era — think early Mailchimp, Constant Contact — were built on what engineers call a list-based architecture. You imagine your customers as rows on a spreadsheet. You upload a list. You blast an email to the list. It is "batch and blast," and it treats every customer as a static entry that occasionally gets refreshed. It is a mailing list with a nicer font.

Bialecki and Hallen built something categorically different: an event-driven database. Instead of a spreadsheet of people, imagine a continuously running ledger that records actions as they happen — this person viewed this product at 2:14 p.m., added it to cart at 2:16, abandoned it at 2:19, came back and purchased a different item three days later. Every click, checkout, page view, and historical order flows into a single unified profile in real time. The customer is not a static row; the customer is a living stream of behavior. And because the data model is built around events rather than lists, you can ask it almost any question and get an answer in seconds, across billions of records.

Think of it this way. The old tools were a bulletin board where you pinned up one notice for everyone to read. Klaviyo was a librarian who knew every book each patron had ever checked out, when, and what they browsed on the way to the counter — and could pull up any subset of patrons on command. That is a different kind of product living in a different part of the merchant's operation. The bulletin board is a marketing expense. The librarian is a system of record.

Now here is the part that separates Klaviyo from a hundred other clever architecture stories: they had almost no money, and they turned that constraint into a discipline. From its 2012 founding, the company operated with what can only be described as monastic capital efficiency, funding itself largely out of revenue rather than venture rounds for its early years — the coffee-shop years were literal.2 Bialecki has told the story that they didn't raise a meaningful institutional round until the business was already working, which for a Silicon Valley–era software company was practically heresy.

Why does that matter beyond founder folklore? Because self-funding forces a brutal clarity about value. When you cannot paper over a weak product with a fat sales budget, the product has to sell itself. And Klaviyo's did, through a mechanism that later got a fashionable name — product-led growth — but which the founders arrived at out of necessity. A merchant could install Klaviyo, watch their entire historical order data sync into the platform automatically, and within minutes see a number that changed the conversation: the exact dollars generated by an automated abandoned-cart sequence. Not an estimate. Not a vanity open-rate. Attributed revenue.

That single design choice — leading with provable ROI — is the commercial genius hiding inside the technical one. It converted the software from a cost center into a revenue line the merchant could point to. When your marketing tool tells the founder of a fast-growing brand that it just recovered $40,000 in otherwise-lost sales this month, you do not get churned. You get evangelized. Capital discipline, in other words, was not just a financial virtue; it was the forcing function that produced a product people would refuse to give up.

The bootstrapped years also seeded the governance structure that would later define the company. Because they raised so little and so late, the founders never diluted themselves into irrelevance — a fact that would matter enormously when Klaviyo went public a decade later with the founders still firmly in control. Capital efficiency compounded not just into cash flow but into power.

By the mid-2010s, Klaviyo had a differentiated product, a growing base of loyal merchants, and near-zero brand recognition outside the small world of e-commerce operators. What it needed was a wave to ride. And out in the wider retail economy, a wave was building that would carry Klaviyo further than any marketing budget could — the explosion of a platform called Shopify.

III. The Shopify Kingmaker and the Mailchimp Breakup

Every gold rush needs its Levi Strauss — the person who gets rich selling picks and shovels rather than digging for gold. In the direct-to-consumer boom of the mid-2010s, the gold was the sudden ability for anyone with a good product and an Instagram account to build a real brand without a retailer's permission. The shovel was Shopify, which let those brands stand up a professional online store in an afternoon. And the single most valuable pick sold to those brand-builders turned out to be the tool that told them who their customers were and how to bring them back.

That tool, increasingly, was Klaviyo. As Shopify onboarded hundreds of thousands of merchants, a self-reinforcing dynamic took hold in the DTC community. Agencies, consultants, and the founders themselves talked to each other constantly on forums, in Slack groups, at trade shows. When the ambitious operator of a $5-million skincare brand asked "what email platform should I use," the answer came back, over and over, from people they trusted: Klaviyo. It became the default recommendation for the high-growth merchant — not through advertising, but through word of mouth inside a tight community that Klaviyo had earned by being demonstrably better at the one thing that mattered, which was turning data into recovered revenue.

The product innovation that cemented this was the flow. If the database was Klaviyo's foundation, flows were the cathedral built on top of it — and the feature customers actually fell in love with. A flow is a visual, event-triggered automation: a canvas where a merchant, without writing code, could design a sequence like if a customer has spent more than $100 historically, abandoned a cart containing item X, and opened a specific email in the last seven days, then wait two hours and send a 10%-off SMS. Read that sentence again and notice how many different data types it braids together — lifetime spend, real-time cart behavior, recent engagement, and a channel decision — all firing automatically. That is only possible because the underlying event database can evaluate all of those conditions against a live profile in real time. The flow was the visible payoff of the invisible architecture. Competitors could copy the flow-builder interface; they could not easily copy the database that made complex flows fast and reliable.

And then, in 2019, Klaviyo got the kind of gift that a company cannot manufacture and can only be ready to receive.

For years, the dominant email tool in the Shopify App Store had been Mailchimp — a beloved, mass-market brand with far more name recognition than Klaviyo. But underneath the partnership, tension was building over exactly the thing Klaviyo cared most about: customer data. The dispute centered on how customer information flowed between the two platforms, on API access and integration terms, and on the commercial relationship between them. In March 2019, it ruptured publicly and messily. Shopify removed Mailchimp from its App Store, and the two companies traded pointed public statements, each blaming the other over data-sharing and terms.[^3]

Overnight, hundreds of thousands of Shopify merchants who ran Mailchimp faced a problem: their email tool no longer integrated cleanly with their store. And into that vacuum stepped a company that had spent seven years building precisely the deep, data-native Shopify integration that the moment demanded. Klaviyo was primed and waiting. The migration that followed was not just large; it was high quality. The merchants most motivated to switch to a better-integrated, more powerful platform were the growing, sophisticated, mid-market brands — exactly the cohort with expanding budgets and long lifetimes. Klaviyo did not just absorb refugees; it absorbed the most valuable refugees.

It is worth pausing on what this episode reveals, because it is easy to tell it as pure luck. It was not pure luck. Luck is the timing of the Mailchimp breakup. Everything else was preparation. Klaviyo had made a philosophical bet — that owning the customer's data relationship was the whole game — and Mailchimp's willingness to fight Shopify over data terms suggests the incumbent had, at some level, made the opposite bet and was unwilling to concede control. When the music stopped, Klaviyo was standing next to the only chair that mattered. (The two combatants eventually reconciled: Mailchimp and Shopify patched things up and relaunched a direct integration in October 2021, but by then the strategic damage was done and the high-value cohort had moved on.[^15])

The migration wave finally justified taking real institutional money to pour fuel on the fire. Klaviyo brought in capital from firms including Accomplice, Summit Partners, and Accel to scale its go-to-market engine as it transitioned from a scrappy SMB tool into a genuine mid-market leader.2 But note the sequencing, because it is the whole ethos of the company: the money came after the product-market fit was undeniable, not before. Klaviyo raised to accelerate a machine that already worked, not to go looking for one that might.

By the end of the decade, Klaviyo had become something close to essential infrastructure for the Shopify economy. Which raised an obvious and uncomfortable question — one that Shopify itself was clearly asking. If a third-party app has become this central to your merchants' success, do you compete with it, acquire it, or bind it to you? In 2022, Shopify chose door number three, and the answer would reshape Klaviyo's cap table and its risk profile at the same time.

IV. The $100M Shopify Alliance & Dual-Class Power Structure

In the summer of 2022, the tech world was in a very different mood than it had been a year earlier. The zero-interest-rate party was over, software multiples were collapsing, and the great DTC boom was cooling as customer-acquisition costs rose and pandemic demand normalized. It was against that darkening backdrop that Klaviyo and Shopify announced something that surprised the market: not just a deeper partnership, but Shopify putting real money on the table.

On July 28, 2022, Shopify invested $100 million in Klaviyo, purchasing roughly 2.9 million shares. Alongside the cash, Shopify received warrants to buy an additional 15.7 million shares at the nominal price of a penny each, vesting over time — a structure that gave Shopify the right to accumulate a substantial equity position as the partnership matured.1[^5] The companies signed a seven-year collaboration agreement, and Klaviyo was named the recommended email marketing platform for Shopify Plus, the merchant tier that serves Shopify's largest and most valuable brands.[^4] By the time Klaviyo filed to go public the following year, Shopify's stake worked out to roughly 11.3% of the company.1

Consider what each side actually got, because a smart deal always tells you something about how both parties see the future. Shopify got financial exposure to the growth of one of its most important ecosystem partners, a formal say in the relationship, and a hedge — if Klaviyo was going to capture enormous value on top of Shopify's platform, Shopify would at least own a slice of that value. Klaviyo got the ultimate distribution endorsement, a preferred position at the top of the market it most wanted to reach, and $100 million of validation at a moment when capital was suddenly scarce. On paper, it was elegant. Underneath, it was an admission that neither company could easily live without the other — and that is a more comfortable position for the one that controls the platform than for the one that lives on it.

Which brings us to the uncomfortable arithmetic at the center of the Klaviyo investment case. As of Q1 2026, roughly 78% of Klaviyo's annual recurring revenue was derived from customers on the Shopify platform.10 Read that number slowly. Nearly four out of every five dollars Klaviyo earns are, in some sense, downstream of decisions made in Ottawa at Shopify's headquarters. And the dependency runs both financial and structural: under the collaboration terms, Klaviyo shares a portion of the revenue it generates from Shopify merchants back to Shopify.1 The relationship is not free rent; it is a revenue-sharing arrangement in which the landlord takes a cut.

Management is not blind to this, and the mitigation strategy is exactly what you would expect: build the same deep, native integrations everywhere else that Klaviyo built with Shopify. The company has invested in connectors for WooCommerce (the open-source commerce engine that runs on WordPress), Adobe Commerce (the platform formerly known as Magento), Salesforce Commerce Cloud, and Wix, so that a brand running on any of those systems can get a Klaviyo experience close to what a Shopify merchant gets.[^16] The strategic logic is diversification: every dollar of ARR that comes from a non-Shopify platform is a dollar that is insulated from any future change in Shopify's terms.

But the honest reading of the disclosure is that diversification is proceeding slowly. The overwhelming majority of the base remains Shopify-centric, and here a subtle point in the outline deserves scrutiny rather than applause. It is true that only a small single-digit share of new ARR comes directly through the Shopify App Store itself — a fact management uses to argue that the company's growth is increasingly driven by its own direct sales force and its agency network rather than by Shopify's storefront. That is a fair point about distribution. But it should not be confused with reduced dependency. A merchant Klaviyo signs through its own sales team is still, most of the time, a merchant whose store runs on Shopify. Changing how you acquire a customer does not change whose platform that customer sits on. The distribution is diversifying faster than the underlying platform exposure, and an investor should keep those two things separate in their head.

If the revenue base concentrates power in Shopify's hands, the voting base concentrates power just as tightly in the founders' hands. When Klaviyo went public, it did so with a dual-class share structure — the now-familiar Silicon Valley mechanism in which insiders hold a class of stock carrying ten votes per share while public investors buy a class carrying one. Bialecki and Hallen came into the IPO owning large economic stakes — Bialecki around 38% and Hallen around 14% on a pre-offering basis — and the ten-to-one voting structure translated those stakes into commanding control of the company's total voting power, well beyond a simple majority.1[^5]

For a long-term investor this is a double-edged sword worth naming plainly rather than celebrating. On the favorable side, the founders' track record is one of genuine capital discipline: a company built with minimal dilution, that reached cash generation early, and that consistently chose partnership structures over serial dilutive equity raises. Founders who bootstrapped for years tend to spend other people's money as if it were their own, because for a long time it was their own. On the unfavorable side, dual-class control means public shareholders own the economics but not the steering wheel. If the founders make a value-destroying decision — an overpriced acquisition, a strategic detour, a governance lapse — ordinary holders have little formal recourse. The structure asks investors to underwrite the founders' judgment for the very long run. So far that judgment has been good. The point of independent analysis is to keep watching whether it stays good, rather than to assume it will.

With the cap table set and the Shopify alliance sealed, Klaviyo had the pieces in place for the event that would test all of it in public view. In September 2023, it walked onto the floor of the New York Stock Exchange — and in doing so, became the company that a frozen tech-IPO market had been waiting on.

V. M&A Strategy, Multi-Product Expansion & AI

Before we get to the trading floor, we have to talk about how Klaviyo spends money — because a company's acquisition strategy is one of the purest windows into how management actually thinks, as opposed to how it talks. And Klaviyo's M&A record is conspicuous for what it does not contain: there is no debt-fueled mega-merger, no attempt to buy growth by bolting on a large competitor, no "diworsification" into adjacent businesses that dilute focus. What you find instead is a pattern of small, surgical, technology-and-talent tuck-ins, each aimed at extending the core rather than changing what the company is.

The first tell came in November 2022 with the acquisition of Napkin.io, a developer platform.[^9] Napkin's technology let developers write and run custom serverless functions — small snippets of code that execute on demand without the developer having to manage servers — and Klaviyo folded that capability inside its platform. In plain terms, it meant that a sophisticated merchant or their agency could write bespoke code to pull in unusual data sources or build custom syncs directly within Klaviyo, rather than duct-taping external tools onto it. Why does a marketing company buy a developer tool? Because if your entire strategy rests on being the definitive customer database, you want to make it as easy as possible for anyone to get any data into that database. Napkin was not about email; it was about deepening the moat around the data layer.

The second tell came in August 2025 with the acquisition of Gatsby, announced on August 19.6 Gatsby is a social-automation product that captures email and SMS subscribers directly from high-intent interactions on social media — the DMs, mentions, tags, and follows that happen on Instagram and TikTok — and maps user-generated content back to individual customer profiles. The strategic gap it fills is real and increasingly urgent. A brand's most valuable early relationship with a customer often now begins on social media, in a channel the brand does not own and cannot easily convert into a durable relationship. Gatsby is a bridge from the rented land of social platforms to the owned land of a brand's email and SMS list — and, crucially, it feeds those social signals back into Klaviyo's central profile, enriching the very database that is the company's reason for being. Once again, the acquisition logic bends back to the same north star: more signals, better profiles, deeper lock-in.

Both deals share a discipline worth naming. They are cheap relative to the company's size, they are additive to the core data platform rather than tangential to it, and they buy capability and talent rather than revenue. This is the M&A behavior of operators who believe their own product is the compounding asset and who treat acquisitions as ways to make that asset better, not as ways to paper over a growth problem. It is the opposite of the empire-building that destroys value at so many software companies. Whether that discipline survives the pressure of the enterprise pivot — where the temptation to buy a big-name capability is real — is a genuine open question, but the record to date is clean.

The most important product expansion, though, is not something Klaviyo bought. It is two things it built: SMS and the Customer Data Platform.

SMS has become a material revenue driver, and it changes the shape of the business in an instructive way. The pitch to merchants is straightforward and backed by Klaviyo's own attribution data: brands that run both email and SMS through Klaviyo tend to see meaningfully higher sales than those running email alone, and text-message-driven order value has in recent periods grown faster than every other channel Klaviyo measures.8 The strategic beauty is that email and SMS run off the same profiles, the same flows, the same database — so adding SMS is not adding a second tool, it is turning on a second faucet connected to the same reservoir. That raises the average revenue Klaviyo earns per customer without asking the merchant to learn a new system.

But SMS carries a cost that email does not, and it is important to be clear-eyed about it. Sending an email costs Klaviyo essentially nothing at the margin — the incremental cost of one more email is a rounding error. Sending a text message, by contrast, means paying carrier fees to the mobile networks that actually deliver the message. Those fees are a real cost of goods sold. So as SMS grows as a share of the mix, it exerts a structural drag on gross margin — a lower-margin dollar riding alongside higher-margin software. Management's answer is that the higher overall revenue per customer more than compensates, and that the software layer around SMS (the segmentation, the flows, the analytics) keeps the blended economics attractive. That is a reasonable argument, but it is one an investor should track empirically rather than accept on faith: watch whether gross margin holds as the channel mix shifts, because the two forces genuinely pull in opposite directions.

The Customer Data Platform is the more consequential strategic move, and it goes directly at the enterprise. Here is the problem it solves, in the language of the merchants who feel it. A large brand — say, one with physical stores, multiple websites, a mobile app, and a wholesale channel — accumulates customer data in a dozen disconnected systems. To make sense of it, big companies have historically bought a specialized, expensive piece of software called a Customer Data Platform (the category leaders being tools like Segment, now owned by Twilio, and Tealium) whose only job is to ingest all those data sources, resolve them into single customer identities, and pipe the result to downstream tools. The catch is that the CDP and the marketing tool were two different products from two different vendors, and stitching them together was a costly, brittle integration project.

Klaviyo's bet is that a brand should not have to buy and integrate a separate CDP at all, because the whole point of Klaviyo is that it is already a customer data platform with marketing built on top. So the company packaged and sold its native CDP capabilities as a distinct enterprise offering — identity resolution across stores and channels, unified profiles, the ingestion layer — positioned explicitly as a way to eliminate "tool sprawl."10 The pitch to a large enterprise is: collapse two vendors into one, and get your data layer and your action layer from the same system so they never fall out of sync. If it works, it is a wedge into exactly the large-account market where Klaviyo has historically been weakest, and it makes the platform even stickier, because now the brand's identity graph — the map of who its customers actually are — lives inside Klaviyo too.

And the CDP is not an end in itself; it is the fuel tank for the engine that management increasingly wants to talk about, which is Klaviyo AI. The logic is clean: artificial intelligence is only as good as the data it learns from, and a unified, real-time, event-level database of customer behavior is close to an ideal training substrate for commerce-specific machine learning. Klaviyo AI applies that data to concrete, sellable predictions — the likelihood that a given customer is about to churn, a forecast of a customer's lifetime value, the optimal time to send a message, and generative help with writing the copy itself. Each of these is a high-margin software feature that a merchant can be upsold, and each becomes more useful the more of the merchant's data lives in Klaviyo. The AI is where the database bet is supposed to finally compound into pricing power. Whether it does — whether these predictions are meaningfully better than what competitors can offer and whether merchants will pay a premium for them — is one of the central unproven questions in the bull case, and we will return to it when we war-game the competition.

For now, hold onto the shape of the strategy: buy small to strengthen the core, grow SMS for revenue per customer while watching the margin cost, and use the CDP to pull the whole apparatus upmarket where the AI can turn data into durable advantage. That is the plan Klaviyo carried onto the public stage. Which is exactly where we go next.

VI. Playbook: Operating Strategy & Competitive Moat

Every business eventually has to answer a simple, brutal question: why can't someone else just do this? For Klaviyo the question is sharper than usual, because on the surface "email and SMS marketing software" sounds like the most commoditized corner of the software universe. There are hundreds of tools that will send an email. So let's run the company through the two frameworks serious investors use to interrogate durability — Hamilton Helmer's 7 Powers and, in the next section, Porter's Five Forces — and see what actually holds up under pressure.

Start with the power that matters most here: switching costs, and understand why they are unusually high in this specific case rather than just asserting that they exist. When a brand has been running Klaviyo for two years, four things have accumulated inside the platform that are painful to move. First, the historical data — every order, every event, the full behavioral ledger — which is the raw material for all the brand's segmentation. Second, the tracking scripts embedded across the brand's website that feed real-time behavior into the database. Third, the flows — often dozens of intricate, revenue-generating automations that took months to build and tune. Fourth, and most legally sensitive, the subscriber opt-in and consent history, which under modern privacy and anti-spam rules is not trivially portable. To switch vendors, a brand must migrate all four, re-establish attribution from scratch, and accept a period of degraded performance during the transition — all to move to a competitor that, at best, does the same job. This is why Klaviyo functions less like a marketing app and more like a system of record, the operational spine a brand runs on. Systems of record do not churn easily. That is the deepest source of the moat, and it is real.

The second power is what Helmer calls a cornered resource, and here Klaviyo's claim rests on the database architecture itself. Because the platform was built from day one as an event store optimized for this workload, it can segment across billions of profiles in seconds — a computational feat that legacy list-based tools struggle to match without bolting on expensive third-party database infrastructure. The counterargument, which honesty requires, is that a proprietary architecture is a durable head start rather than a truly cornered resource in the strict Helmer sense; a well-funded competitor can, in principle, build a fast event database too. The advantage is that doing so while also matching Klaviyo's decade of accumulated product depth, integrations, and data is expensive and slow — the resource is cornered not by patent but by the compounding of time and focus. That is a weaker form of the power than, say, an exclusive mineral deposit, and an investor should size it accordingly.

The third power is scale economies with a data flywheel. As Klaviyo processes transaction and behavioral data across roughly 196,000 brands, its machine-learning models have more examples to learn from — more sends, more opens, more purchases — which in principle makes its predictions about send times, open rates, and purchase propensity structurally better than a smaller rival could achieve.7 This is the most fashionable part of the story and also the one to hold most skeptically. Data network effects are real but they saturate: the difference between a model trained on ten billion events and one trained on twenty billion is often marginal, and a competitor with "enough" data may close most of the gap. The flywheel is a genuine advantage; it is probably not an infinite one. The right posture is to treat it as a supporting power, not the load-bearing one. The load-bearing power remains switching costs.

Beyond the 7 Powers, two operating strategies deserve their own spotlight because they explain how Klaviyo grew without the enormous enterprise sales force its larger competitors carry. The first is the agency ecosystem. Rather than hiring an army of expensive direct salespeople to knock on every merchant's door, Klaviyo deputized the thousands of digital-marketing agencies and systems integrators who already do the day-to-day marketing work for e-commerce brands. Klaviyo made these agencies expert in its platform, gave them tools, and paid them recurring commissions to bring their clients onto Klaviyo and keep them there. It is a brilliant piece of go-to-market judo: the agencies become an outsourced, variable-cost sales and success force that only gets paid when it delivers, and — just as importantly — an agency that has trained its whole team on Klaviyo becomes a second layer of switching cost, because moving a client off Klaviyo means retraining the agency too. The people who implement the software have their own economic reasons to keep it installed.

The second is the ROI attribution engine, and while we met it in the origin story, its role as an ongoing competitive weapon is worth stating precisely. Klaviyo's native dashboards show a merchant the specific revenue attributed to each automated email and SMS. This does something subtle and powerful to the sales conversation: it moves the product out of the "marketing expense" budget line, where spending is scrutinized and cut in downturns, and into the "revenue generator" line, where spending is defended. When a CFO can see that a tool generated ten times its cost in attributed sales, that tool survives budget cuts that kill its rivals. In a cooling consumer economy — precisely the environment of the mid-2020s — being the software a merchant can prove pays for itself is a formidable defensive position.

So the honest verdict on the moat is layered. The switching costs are deep and real. The database architecture is a durable head start. The data flywheel is a genuine but bounded tailwind. The agency network and attribution engine are underappreciated structural advantages that reinforce the whole. What none of these powers defends against is the one threat that sits above the entire structure — the platform Klaviyo depends on. A moat is only as good as the terrain around it, and Klaviyo's terrain is largely owned by Shopify. That tension is the heart of the bull-versus-bear debate, and it is where we turn now.

But first, the moment the whole company had been building toward. On September 20, 2023, after a nearly two-year drought in which almost no venture-backed U.S. software company had dared to go public, Klaviyo priced its IPO at $30 per share, selling 19.2 million shares and valuing the company at just over $9 billion on a fully diluted basis.3 The stock opened at $36.75, rose as much as the mid-$30s intraday, and closed its first session up about 9% — a solid if unspectacular debut that put roughly $345 million of fresh cash on the company's balance sheet from the shares it sold directly.4 The significance was as much symbolic as financial: Klaviyo was the first notable U.S. venture-backed software IPO since late 2021, and the market watched it as a bellwether for whether the tech-listing window had reopened. A profitable, cash-generative, capital-efficient company was a fitting one to reopen it — the anti-thesis of the growth-at-all-costs unicorns that had defined the prior cycle.5 The bootstrappers from the Boston coffee shops now had to answer to the public market every ninety days. How they have answered is the next chapter.

VII. The Bull vs. Bear Case & Investor Stress Test

Let's do what a good investment committee does: put the optimist and the skeptic in the same room and make them fight it out with evidence rather than adjectives.

The Bull Case: Enterprise Momentum & Margin Expansion

The bull's central claim is that Klaviyo is no longer just a tool for scrappy DTC brands — it is successfully climbing into the enterprise, and that climb changes the entire trajectory of the business. The single most persuasive piece of evidence sits in the customer-cohort data. As of Q1 2026, the number of customers generating more than $50,000 of annual recurring revenue grew 38% year over year to 4,175.7 That growth rate matters more than the absolute number, because it is a direct, hard measure of the upmarket motion working. These are not skincare startups; they are substantial brands making a considered, committed spend. When your most valuable cohort is also your fastest-growing, the mix is shifting in your favor — toward larger, stickier, more defensible relationships.

The financial performance underneath the cohort data supports the story. Q1 2026 revenue of $358.0 million grew 28% year over year, and the company reported net revenue retention of 110%, up two points from a year earlier.7 Pause on that retention figure, because it is arguably the most important single number in the whole business (we will return to it as a KPI). A net revenue retention of 110% means that, ignoring any new customers entirely, the existing customer base spent 10% more this year than last — expansion from more contacts, more channels like SMS, and more products like the CDP and AI, net of any customers who left. It means the base grows even if Klaviyo never signs another logo, and it is the mathematical engine of durable software compounding.

The margin story is the bull's clincher. Klaviyo reported non-GAAP operating income of $58.6 million in Q1 2026, a 16.4% non-GAAP operating margin — nearly five percentage points higher than a year earlier — and, notably, its first positive GAAP operating margin as a public company.7 For a company still growing revenue at 28%, generating expanding profitability at the same time is the combination investors prize most, because it signals that growth is not being purchased with unsustainable spending. Management backed the confidence with guidance, raising the full-year 2026 revenue outlook to a range of $1.514 billion to $1.522 billion.7 And the mechanism the bull points to for continued margin expansion is exactly the product strategy we walked through: the high-margin, software-only ARR from the CDP and AI products is supposed to grow faster than the lower-margin, carrier-fee-burdened SMS dollars, lifting the blended margin over time even as SMS scales.

The Bear Case / Skeptical Investor Stress Test

Now hand the floor to the short-seller, who has been waiting patiently and has one word written at the top of the page: Shopify.

The overlord risk is not a footnote; it is the whole bear case, and it is structural rather than speculative. With roughly 78% of ARR tied to Shopify-based brands, Klaviyo's fate is welded to the strategic decisions of a company it does not control.10 Play out the scenarios a skeptic must underwrite. Shopify could alter its API terms, change the economics of the revenue-share, downgrade Klaviyo's preferred status, or — the nightmare — decide that the customer-data-and-marketing layer is too valuable to leave to a partner and build or buy a competing native product. Shopify already owns adjacent pieces of the merchant stack, and it has both the distribution and the data to make a credible run at Klaviyo's territory. The $100 million investment and the warrant structure bind the two companies for now, and the collaboration agreement runs for years, but agreements expire and incentives change. An investor in Klaviyo is, whether they like it or not, making a bet on the durability of Shopify's goodwill. That is a genuinely uncomfortable place to sit, and no amount of switching-cost moat protects against the platform itself deciding to compete, because the platform sits upstream of the moat.

The second bear argument is upmarket competition, and here the war-game gets interesting. As Klaviyo climbs into the enterprise, it leaves the pond where it is the biggest fish and swims into an ocean of sharks. At the very top sit the incumbent suites — Salesforce Marketing Cloud and Adobe Experience Cloud — which large enterprises already own as part of sprawling relationships, and which can bundle marketing into deals a specialist cannot match on procurement terms. On the more nimble flank sit cross-channel challengers like Braze, built natively for multi-channel engagement, and HubSpot, which has been pushing down from B2B into commerce. Run Porter's Five Forces on this and the picture sharpens: the threat of substitutes and rivalry among competitors both intensify as Klaviyo moves upmarket, precisely because the enterprise is where the entrenched giants are strongest and where Klaviyo's DTC-community word-of-mouth advantage counts for least. The bargaining power of buyers also rises — large enterprises negotiate hard, demand customization, and lengthen sales cycles, which is a different and more expensive game than the self-serve, product-led motion that made Klaviyo efficient. The company's edge in the enterprise — the native CDP eliminating tool sprawl — is a real differentiator, but it is a claim that must be proven deal by deal against buyers with real alternatives, not a settled advantage.

The third bear point is nearer-term and specific: management transition. In May 2026, Klaviyo announced that CFO Amanda Whalen would step down, remaining in the role through August 21, 2026 and then serving as an advisor through mid-November, with a formal search underway for a successor.9 The company was explicit that the departure was not tied to any disagreement or financial concern, and there is no reason on the public record to doubt that.7 But the timing is awkward regardless of the reason. A CFO transition during a delicate enterprise-expansion cycle removes a steady hand precisely when guidance discipline, margin management, and investor communication matter most — and the market noticed, sending the shares sharply lower on the news despite an otherwise strong quarter.9 It is not an existential risk. It is an execution risk, and execution risk during a transition is exactly the kind of thing that turns a good quarter into a disappointing year if the handoff is bumpy.

Weighing the two cases, the intellectually honest position is that the bull and bear are arguing about different time horizons. The bull is right about the near-to-medium term: the operating metrics are genuinely strong, the upmarket motion is genuinely working, and the margin trajectory is genuinely improving. The bear is right about the tail risk: the Shopify concentration is a real, structural vulnerability that no operating excellence can fully neutralize, and the enterprise fight is against opponents who do not lose gracefully. A long-term owner of this business has to be comfortable holding both truths at once — a well-run, compounding company sitting on top of a dependency it cannot control.

VIII. Epilogue

Step back from the numbers and the frameworks, and Klaviyo's story resolves into a small set of durable lessons that outlast whatever the stock does next.

The first is the one the founders bet the company on: build the database first, the application second. It is tempting to build the shiny, visible thing — the app people see and click. Klaviyo's founders built the invisible thing underneath it, the system of record, and let the visible applications be consequences of it. That ordering is what turned a marketing tool into operational infrastructure, and infrastructure is what generates the switching costs that let a company keep its customers through downturns, competition, and its own mistakes. Founders and investors alike should notice how often durable moats live in the unglamorous layer.

The second lesson is more double-edged, and Klaviyo embodies both edges: platform ecosystems are the fastest way to grow and the most dangerous way to depend. Riding the Shopify wave gave Klaviyo distribution that no marketing budget could have bought. It also created a concentration risk that will shadow the equity for as long as it persists. The strategic resolution — keep harnessing the partner's ecosystem while relentlessly building native capabilities and diversifying the platform base — is correct in theory and slow in practice. The tension between growth-through-dependence and safety-through-independence is not a problem Klaviyo will ever fully solve; it is a balance it will have to keep managing forever.

The third lesson is about capital discipline as a source of strategic freedom. Because Klaviyo bootstrapped, it never had to grow at any cost, never diluted its founders into irrelevance, and never confused fundraising with progress. That discipline bought the founders control and bought the company the ability to reach profitability on its own terms. The open question — the one that dual-class control makes especially pointed — is whether that discipline survives success. Disciplined bootstrappers sometimes become undisciplined empire-builders once they have a public currency and a war chest. The record through mid-2026 is clean. The record is not the same as a guarantee.

So what should a serious observer actually watch from here? Amid all the metrics a company reports, focus on a small number that carry disproportionate signal. Net revenue retention is the first — the single cleanest read on whether the existing base is expanding, which is the true engine of a subscription business and the number that will reveal weakness earliest if the enterprise push stalls or competition bites. The second is the growth of the large-customer cohort — the count of customers above the $50,000 ARR threshold — because it is the direct scoreboard for whether the upmarket strategy that underpins the entire bull case is actually working. And the third, quieter than the others but arguably the most important, is the trajectory of Shopify concentration — whether that ~78% figure meaningfully declines over time, because that number is the measure of how much of Klaviyo's destiny remains in someone else's hands.

The narrower things to track are already visible on the horizon: the search for a new CFO and how cleanly that handoff goes; the pace of enterprise wins specifically outside the Shopify base; and the real-world adoption of the CDP and AI products that are supposed to justify the enterprise valuation and defend the margins. Each is a test of a specific claim management has made about the future, and each will either add evidence to the bull case or hand ammunition to the bear.

Klaviyo began as two engineers who believed the entire industry had built its house on the wrong foundation. A decade later they had built a $9-billion-plus public company on the foundation they preferred — a database pretending to be a marketing tool. The database captured e-commerce. The remaining question, the one that will define the next decade as surely as the last one defined this one, is whether the company that owns the database can also, finally, own its own front door.

References

-

Klaviyo, Inc. — Form S-1 (IPO Prospectus), SEC EDGAR, 2023-08-25 ↩↩↩↩↩

-

Klaviyo: From Bootstrapped Beginnings to IPO — Summit Partners ↩↩

-

Klaviyo Announces Pricing of Initial Public Offering — Klaviyo Investor Relations, 2023-09-19 ↩

-

Klaviyo rises 9% in muted NYSE debut after software vendor priced IPO at $30 a share — CNBC, 2023-09-20 ↩

-

Klaviyo's strong IPO pricing should give unicorns an idea of what they are worth — TechCrunch, 2023-09-20 ↩

-

Klaviyo Slides into DMs with Acquisition of Gatsby — Klaviyo Newsroom, 2025-08-19 ↩

-

Klaviyo Delivers Strong Q1 2026 Results: 28% Revenue Growth, Record Operating Margin, and Raises Full Year Outlook — Business Wire, 2026-05-05 ↩↩↩↩↩↩↩

-

Klaviyo (KVYO) Q1 2026 Earnings Call Transcript — The Motley Fool, 2026-05-05 ↩

-

Klaviyo shares tumble despite Q1 beat as CFO steps down — Investing.com, 2026-05-05 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube