Keros Therapeutics: The Biology-First Bet on TGF-Beta Superfamily

I. Introduction and Episode Roadmap

Somewhere in a Lexington, Massachusetts office park, a modest biotech headquarters sits nestled among the sprawl of Route 128, Boston's technology corridor. There is no gleaming campus, no grand lobby with scale models of drug molecules. Just a small team of scientists and executives working on molecules that could transform the lives of patients with some of medicine's cruelest diseases, or could amount to nothing at all. This is Keros Therapeutics, and like so many clinical-stage biotechs, its future hinges on a handful of data readouts that have not yet arrived.

But the story behind Keros is anything but ordinary. Picture a scientist who spent six years building the engine inside one of biotech's most spectacular success stories, then walked away, studied the blueprints, and said: "I can build a better one." That is the founding story of Keros Therapeutics, and it tells you almost everything you need to know about this company, its promise, and its peril.

Keros Therapeutics trades on the Nasdaq under the ticker KROS. As of early 2026, it carries a market capitalization of roughly $350 million, a figure that has swung wildly over the company's short public life, from a peak above $2 billion to its current contracted state. The company is clinical-stage, meaning it has no approved drugs generating recurring revenue. What it does have is a platform built on one of the most fundamental signaling pathways in human biology: the TGF-beta superfamily.

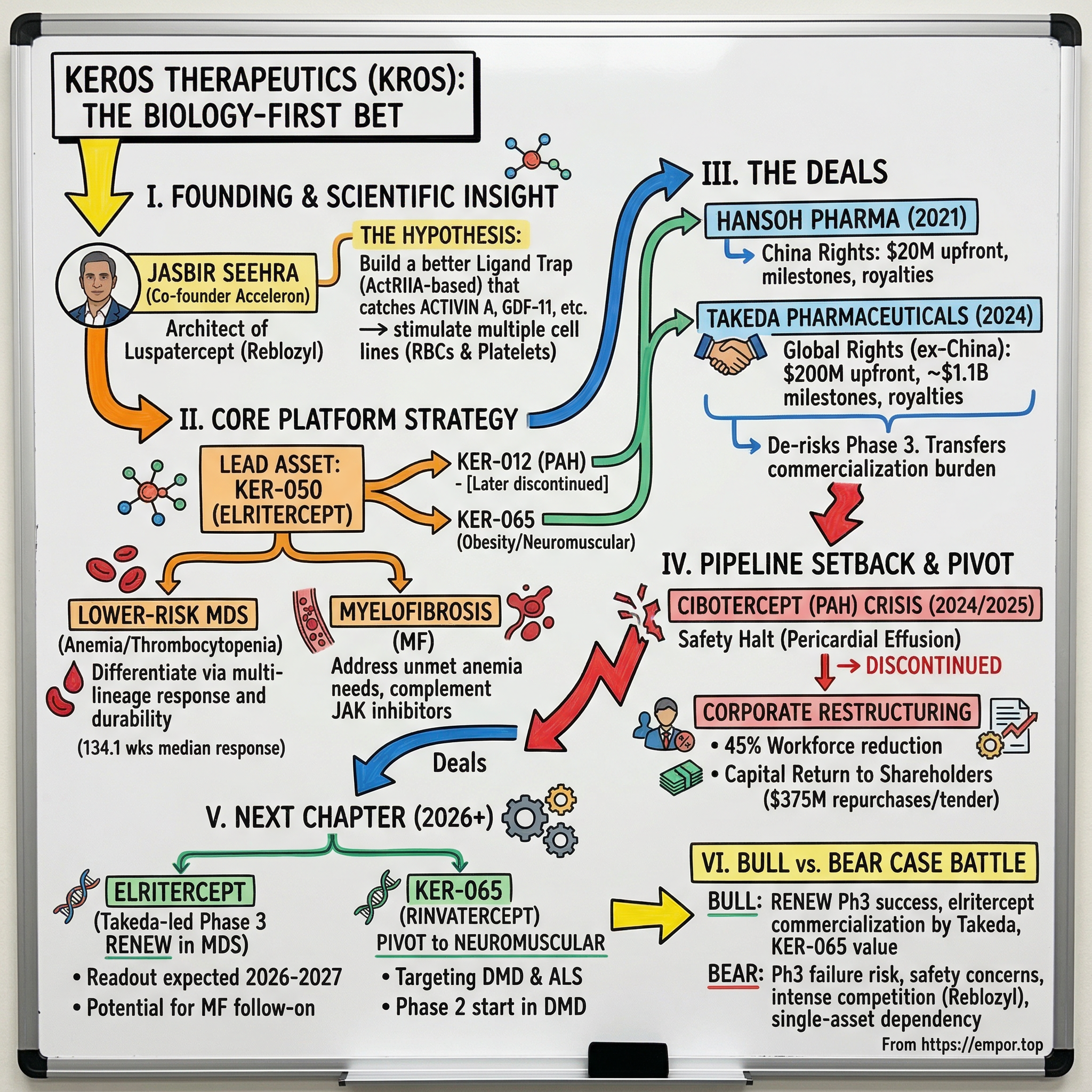

The central question of this story is deceptively simple: can one scientist's deep familiarity with a proven drug class unlock the next generation of therapies for devastating blood disorders and beyond? Jasbir Seehra co-founded Acceleron Pharma and helped architect luspatercept, a drug that became Reblozyl, now generating nearly $1.8 billion in annual sales for Bristol Myers Squibb. Then he left, started Keros, and set out to do it better. That tension between proven pedigree and unfinished ambition runs through every chapter of this story.

What makes Keros particularly interesting for investors and biotech observers is how it illustrates the full lifecycle of a clinical-stage company in compressed form. In just over a decade, Keros has experienced a founding rooted in deep science, a pandemic-era IPO, promising clinical data, a transformative licensing deal, a devastating pipeline setback, activist investor pressure, a strategic review, and a massive capital return to shareholders. It is a company that has lived several lifetimes already, and the next chapter, whether it ends in vindication or cautionary tale, hinges on data that has yet to be generated.

This story moves from the underlying science to the founding insight, through the clinical milestones that built investor excitement, into the deals and setbacks that reshaped the company, and finally to the strategic and competitive questions that will determine whether Keros Therapeutics becomes a category-defining franchise or a footnote in the long, humbling history of TGF-beta drug development.

II. The Scientific Foundation: Why TGF-Beta Matters

To understand why Keros exists, why investors have poured hundreds of millions of dollars into it, and why its future matters to patients with some of the cruelest diseases in medicine, you first need to understand the TGF-beta superfamily. It is both one of biology's greatest opportunities and one of drug development's most punishing arenas.

The transforming growth factor-beta superfamily is a sprawling network of signaling proteins that governs some of the most basic functions in human biology: how cells grow, how they differentiate into specialized types, how tissues repair themselves, and how the body maintains balance between building new structures and tearing old ones down. Think of it as the body's master regulatory switchboard. The superfamily includes not just the TGF-betas themselves, but also activins, bone morphogenetic proteins (BMPs), and growth differentiation factors (GDFs) like myostatin and GDF-11. Dozens of ligands, multiple receptors, two major intracellular signaling branches. It is, to put it mildly, complicated.

These proteins signal through cell-surface receptors called type I and type II activin receptors. When a ligand like activin A binds to these receptors, it triggers a cascade inside the cell involving proteins called SMADs, which act as transcription factors, essentially flipping genetic switches on or off. There are two main SMAD branches. The SMAD2/3 pathway generally acts as a brake on red blood cell and platelet production, while promoting cell proliferation in blood vessels. The SMAD1/5/9 pathway does roughly the opposite: it promotes bone formation and has anti-proliferative effects in blood vessels. The interplay between these two branches determines outcomes across hematology, musculoskeletal biology, cardiovascular function, and metabolism.

Scientists began uncovering this pathway in the 1980s and 1990s, and by the 2000s, academic research had mapped it in extraordinary detail. But here is the paradox that defined the opportunity: despite decades of study and thousands of published papers, very few drugs targeting this pathway had ever reached patients. The reason is the pathway's complexity. Blocking TGF-beta broadly is like cutting the power to an entire building when you only want to turn off one light. Indiscriminate inhibition causes systemic side effects because TGF-beta plays essential roles in immune regulation, wound healing, and tumor suppression. Multiple pharmaceutical companies tried and failed. Merck KGaA's bintrafusp alfa, a bifunctional molecule targeting both PD-L1 and TGF-beta, failed head-to-head against pembrolizumab in lung cancer. Eli Lilly's galunisertib, a TGF-beta receptor inhibitor, was quietly abandoned. Novartis, Sanofi, Pfizer, even Bristol Myers Squibb itself: all took runs at direct TGF-beta inhibition and came away empty-handed.

The founding insight that would eventually become Keros was born from this wreckage. What if the problem was not the pathway itself, but the approach? What if, instead of trying to inhibit TGF-beta receptors directly, you could selectively intercept specific ligands before they ever reached the cell surface? Instead of cutting the power line, you would intercept specific messages before they arrived at the switchboard. This is the concept of a ligand trap: a bioengineered protein that circulates in the bloodstream, grabs onto specific signaling molecules, and prevents them from reaching their natural receptors. The elegance of the approach lies in its selectivity. By engineering the binding domain of the trap, you can choose which ligands to capture and which to leave alone.

To make this concrete, consider how a ligand trap actually works at the molecular level. The architecture is elegant: you take the extracellular portion of a cell-surface receptor, the part that normally sticks out of the cell and binds to passing signaling molecules, and fuse it to the Fc region of a human antibody. The Fc region serves two purposes. First, it extends the molecule's half-life in the bloodstream by exploiting the body's natural antibody recycling machinery. Second, it creates a bivalent structure, meaning each molecule has two binding arms instead of one, increasing its ability to capture target ligands. When injected into a patient, this engineered protein circulates through the blood, acting like a molecular sponge that soaks up specific signaling molecules before they can reach the receptors on cell surfaces. The cells never receive the inhibitory signal, so they proceed with normal development. In the case of red blood cell production, this means erythroid precursors that would normally be suppressed by excess activin or GDF-11 signaling can instead mature into functional red blood cells.

The convergence of structural biology, antibody engineering, and a growing clinical understanding of rare disease biology in the 2010s made this approach increasingly feasible. Researchers could now model receptor-ligand interactions at atomic resolution and engineer modified receptor domains with precise binding profiles. By changing even a handful of amino acids in the receptor domain, scientists could alter which ligands the trap would capture and which it would ignore, a level of molecular precision that was simply not possible a decade earlier.

The question was not whether ligand traps could work, since Acceleron had already proven they could with luspatercept, but whether a next-generation design could work better, in more patients, across more diseases, with fewer limitations. That question is what Keros was built to answer.

III. Founding Story and the Pontifax Connection (2015-2017)

In December 2015, Jasbir Seehra filed incorporation papers in Delaware for a company called Keros Therapeutics. The name, derived from the Greek word keras, meaning horn, was chosen to evoke strength and power. But the real power behind Keros was not in the name. It was in the mind of its founder and in the relationships he had spent decades building.

To understand Seehra, you need to trace a career arc that reads like a masterclass in biotech drug discovery. Born and educated in England, Seehra earned both his bachelor's and doctorate in biochemistry from the University of Southampton. He then crossed the Atlantic for a postdoctoral fellowship at MIT, where he worked under Nobel Laureate H. Gobind Khorana, the scientist who helped crack the genetic code in the 1960s. Working under Khorana was not just a credential; it instilled in Seehra a first-principles approach to biology that would define his entire career.

From MIT, Seehra joined Genetics Institute in 1983 as a bench scientist and spent nearly twenty years there, building the company's small molecule drug discovery capabilities from the ground up. He created programs in medicinal chemistry, high-throughput screening, and structural biology, rising through the ranks as the company was acquired by Wyeth Pharmaceuticals and ultimately absorbed into Pfizer. By the early 2000s, Seehra was Vice President of Biological Chemistry at Wyeth, leading a team responsible for small molecule lead discovery. He had become one of those rare figures who understood both the academic science and the industrial machinery needed to turn discoveries into drugs.

Then came the move that would define everything. In 2003, Seehra co-founded Acceleron Pharma alongside a constellation of scientific luminaries: Harvard geneticist Tom Maniatis, molecular biologist Mark Ptashne, Salk Institute neuroendocrinologist Wylie Vale, and Memorial Sloan Kettering's Joan Massague, one of the world's foremost authorities on TGF-beta signaling.

Consider the caliber of that founding team for a moment. Maniatis had pioneered molecular cloning techniques that became standard tools in every genetics laboratory in the world. Ptashne had done foundational work on gene regulation that opened entire fields of research. Vale had discovered corticotropin-releasing factor and helped characterize multiple TGF-beta superfamily members. And Massague had literally written the textbook on TGF-beta signaling, with decades of research elucidating how the pathway works at a mechanistic level. Polaris Venture Partners led the $25 million Series A, and the company began operations in Cambridge, Massachusetts in early 2004.

The scientific firepower assembled at Acceleron was staggering, and Seehra served as its Chief Scientific Officer from the company's operational launch in 2004 through 2010.

During those six years, Seehra was the scientific architect of Acceleron's ligand trap platform. He oversaw the development of two foundational molecules: luspatercept, based on a modified activin receptor type IIB domain, and sotatercept, based on the activin receptor type IIA domain. These molecules would eventually become blockbuster drugs. Luspatercept became Reblozyl, approved for anemia in MDS and beta-thalassemia, now generating nearly $1.8 billion in annual revenue. Sotatercept became Winrevair, approved for pulmonary arterial hypertension. And Merck ultimately acquired Acceleron for $11.5 billion in November 2021, vindicating the science Seehra had helped build.

But Seehra left Acceleron in 2010, five years before that validation. The reasons for his departure are not publicly detailed, but the timing suggests a familiar biotech pattern: a scientific founder who has done the foundational work and is ready for the next challenge, combined with the natural evolution of a growing company toward commercial execution and away from early-stage research.

After a stint as Chief Scientific Officer at Ember Therapeutics, a metabolic disease-focused biotech that explored brown fat biology for obesity treatment, he began formulating what would become Keros. His founding hypothesis was precise and informed by intimate knowledge of Acceleron's platform: the ligand trap architecture he had built could be engineered further. Luspatercept was designed to avoid binding activin A while capturing other TGF-beta superfamily ligands. This was a deliberate design choice at Acceleron, based on the concern that trapping activin A might cause unwanted effects on other tissues. Seehra believed that a modified receptor domain that did bind activin A, combined with optimized selectivity for other key ligands, could produce a therapeutic with broader and more durable effects, particularly in diseases where patients suffered from multiple blood cell deficiencies simultaneously.

The technical bet was specific: activin A is one of the most potent suppressors of red blood cell and platelet maturation in the TGF-beta superfamily. By deliberately including it in the trap's binding profile rather than excluding it, Seehra hypothesized that elritercept would stimulate both erythropoiesis (red blood cell production) and thrombopoiesis (platelet production) simultaneously. Luspatercept only does the former. If Seehra was right, this would matter enormously in diseases like myelofibrosis and MDS where patients suffer from deficiencies in both cell types.

He worked with Pontifax, an Israeli biotech-focused venture capital firm, and academic collaborators to in-license the founding technology and structure the company. Pontifax is not a Silicon Valley generalist fund; it is a specialist life sciences investor based in Israel with a track record of backing early-stage pharmaceutical companies. The firm's partners understood the TGF-beta superfamily, understood the competitive landscape versus Acceleron, and crucially, understood that Seehra's intimate knowledge of what Acceleron had built and what it had left on the table was itself a competitive advantage that no amount of money could replicate.

Pontifax led the Series A funding in April 2016, investing approximately $11 million alongside Arkin Bio Ventures, Partners Innovation Fund, and Medison Pharma. The company established its headquarters in Lexington, Massachusetts, a short drive from the Boston biotech corridor where Acceleron was based. These were not household-name investors, but they were experienced healthcare specialists who understood the science and the competitive landscape. The founding team was deliberately lean: Seehra brought in scientists and drug development professionals he had worked with before, people who did not need to be trained on the biology or the regulatory pathway because they had already done it once.

From the beginning, Keros was designed as a platform company, not a single-drug bet. Seehra knew from his Acceleron experience that the TGF-beta superfamily contained multiple therapeutic opportunities across hematology, musculoskeletal disorders, cardiovascular disease, and metabolism. The goal was to build a pipeline of rationally engineered molecules, each targeting specific ligand subsets for specific diseases, all built on a common scientific foundation. It was an ambitious plan for a startup with a handful of employees and $11 million in the bank, but Seehra had something no competitor possessed: the lived experience of having built and walked away from the most successful TGF-beta drug program in history.

IV. Building the Pipeline: The Platform Strategy (2017-2019)

By 2017, Keros had moved beyond conceptual work into the concrete business of designing drug candidates. The platform strategy was deliberately multi-asset from the start. Seehra had watched Acceleron evolve from a platform company into a two-drug story (luspatercept and sotatercept), and he wanted Keros to maintain breadth while pushing each program toward clinical proof of concept as quickly as possible.

The lead program was KER-050, which would later receive the generic name elritercept. To understand what makes elritercept different from luspatercept, imagine two fishing nets cast into the same ocean of signaling molecules. Luspatercept, based on the activin receptor type IIB, was engineered to catch certain fish (GDF-8, GDF-11, activin B) while letting activin A swim free. Elritercept, based on a modified activin receptor type IIA domain, was designed to catch activin A along with the others. This seemingly small difference in binding profile has potentially large clinical implications.

In diseases like myelodysplastic syndromes (MDS) and myelofibrosis, patients often suffer from both anemia and thrombocytopenia, meaning their bodies cannot produce enough red blood cells or platelets. Luspatercept addresses anemia effectively but does nothing for platelet counts. Elritercept, by trapping a broader set of inhibitory ligands including activin A, showed the ability to stimulate both red blood cell and platelet production in preclinical models. If this translated to humans, it would represent a meaningful advance for patients who need help with multiple blood cell lineages simultaneously.

The target indication for KER-050 was anemia in lower-risk MDS. To understand why this particular disease matters, it helps to start with what MDS actually does to a patient. Myelodysplastic syndromes are a group of cancers in which the bone marrow, the body's blood cell factory, begins producing defective blood cells. The marrow is not empty; it is working overtime. But the cells it produces are malformed, dysfunctional, and often die before reaching the bloodstream. The result is chronic, debilitating anemia: fatigue so severe it limits daily activity, shortness of breath climbing stairs, and for many patients, a dependence on regular blood transfusions that can stretch for years.

There are roughly 21,000 new cases of MDS diagnosed in the United States each year, predominantly in patients over 65. The disease exists on a spectrum from lower-risk (where patients can live for years with supportive care) to higher-risk (which can transform into acute myeloid leukemia). Lower-risk MDS patients are not dying immediately, but their quality of life erodes steadily as anemia worsens and transfusion dependence increases. Each transfusion carries risks of iron overload, infection, and immune reactions. Patients spend hours at infusion centers every two to four weeks. It is a slow, grinding disease that takes away independence one blood draw at a time.

The MDS treatment market was valued at nearly $3 billion in 2024 and is projected to grow to over $5 billion by 2032. Luspatercept had already proven the market existed and the regulatory pathway was viable, which actually made the competitive case clearer: Keros did not need to educate physicians or regulators about the concept of ligand traps. It needed to demonstrate that its version worked better.

The second program was KER-047, and it represented a departure from the ligand trap architecture. KER-047 was a small molecule inhibitor targeting ALK2, a type I receptor in the TGF-beta superfamily. When ALK2 is overactive, it drives elevated production of hepcidin, the master regulator of iron metabolism. High hepcidin levels cause the body to lock iron away in storage cells, making it unavailable for red blood cell production, a condition known as functional iron deficiency. KER-047 aimed to lower hepcidin and liberate stored iron, potentially addressing anemia from a completely different angle than the ligand traps. It was also being explored in fibrodysplasia ossificans progressiva (FOP), an extraordinarily rare genetic disease caused by gain-of-function mutations in ALK2, where soft tissue progressively and irreversibly turns to bone.

The third program, KER-012, later named cibotercept, was another ligand trap, this time based on a modified activin receptor type IIB domain engineered specifically for pulmonary arterial hypertension (PAH). PAH is a deadly condition in which the small arteries of the lungs thicken and narrow, forcing the right side of the heart to work harder until it eventually fails. Cibotercept was designed to block the SMAD2/3 signaling that drives this vascular proliferation while preserving the protective SMAD1/5/9 BMP signaling that keeps blood vessels healthy. The opportunity was enormous: sotatercept, from Seehra's former company Acceleron, was pursuing the same indication and would eventually be approved as Winrevair by Merck.

The intellectual property strategy was aggressive and deliberate. In biotech, the moat is the patent portfolio. Unlike software, where competitive advantages often derive from network effects or switching costs, pharmaceutical companies live and die by composition of matter patents: legal protections on the specific molecular structures of their drugs. Seehra, already an inventor on more than 70 patents from his time at Genetics Institute, Wyeth, and Acceleron, understood this deeply. He ensured that Keros secured composition of matter patents on its engineered receptor domains, covering not just the specific molecules being developed clinically but also the broader design space around them.

The modified amino acid sequences that determined each molecule's binding profile were the core of the moat. A ligand trap based on a wild-type receptor domain would not be patentable in the same way, but an engineered variant with specific mutations that alter binding selectivity is genuinely novel and protectable. Even if a competitor understood the general concept of ligand trapping, replicating Keros' specific engineering without infringing its patents would be difficult. This is the biotech equivalent of building a castle on a hill: the science is the hill, and the patents are the walls.

What made the early pipeline strategy compelling was its coherence. Every program emerged from the same scientific understanding of the TGF-beta superfamily, shared manufacturing and regulatory learnings, and could be advanced by the same core team. In January 2019, Keros closed a $23 million Series B round, again led by Pontifax with participation from the original investor syndicate and new investor Global Health Sciences Fund. The money would fund Phase 1 trials for KER-050 and KER-047 and advance KER-012 through preclinical development. It was a lean operation with a clear plan, built by a team that knew exactly which mistakes to avoid because they had watched those mistakes being made, or not made, at Acceleron.

V. The IPO and Going Public (April 2020)

The timing of Keros' IPO was either brilliantly opportunistic or astonishingly lucky, depending on your level of cynicism about biotech capital markets.

On March 4, 2020, Keros closed a $56 million Series C round led by Foresite Capital and OrbiMed, two of the most respected names in healthcare investing. Venrock and Cowen Healthcare Investments also came in, alongside the existing investor base. Carl Gordon, the Managing Partner of OrbiMed and a fixture of biotech venture investing, joined the board. The total pre-IPO capital raised across three rounds was approximately $90 million.

Then the world fell apart. COVID-19 sent global markets into freefall through mid-March 2020. The S&P 500 dropped 34% in five weeks. Biotech IPO windows slammed shut. Companies that had been preparing to go public scrambled to postpone.

Keros did not postpone. The S-1 registration statement had been filed in mid-March, during the depths of the crash. And on April 7, 2020, as markets were tentatively recovering and investor appetite for biotech was beginning to surge on the back of vaccine development excitement, Keros priced its IPO at $16 per share, the top of the $14 to $16 range, in an upsized offering of six million shares. Jefferies, SVB Leerink, and Piper Sandler served as joint book-runners.

The market's verdict was emphatic. Shares climbed more than 70% on the first day of trading, closing near $27.50. It was one of the first significant biotech IPOs to price after the pandemic crash began, and the response signaled that investors were hungry for clinical-stage stories with strong scientific pedigree. The underwriters exercised their full overallotment option of 900,000 additional shares, bringing total gross proceeds to approximately $110 million. Including pre-IPO funding, Keros now had nearly $200 million in total capital raised.

The investor thesis at IPO was straightforward: you were buying a platform built by the co-founder and former CSO of Acceleron Pharma, targeting the same biology that had produced a blockbuster drug, with multiple clinical catalysts ahead and enough cash to fund several Phase 2 trials simultaneously. The experienced team, the clear scientific rationale, and the de-risked biology (luspatercept had already proven ligand traps worked in humans) made this a compelling story at a moment when biotech capital was flowing freely.

Context matters here. The year 2020 would see roughly 120 life sciences IPOs, the busiest year the industry had ever experienced. Two-thirds of those companies had only preclinical or Phase 1 assets. Low interest rates were pushing capital into risk assets, COVID-19 was generating unprecedented enthusiasm for biotech innovation, and the XBI biotech index was on its way to a February 2021 peak. Keros rode this wave. By December 17, 2020, barely eight months after the IPO, KROS reached an all-time closing high of $82.74, giving the company a market capitalization approaching $1.7 billion.

For the founding investors at Pontifax who had written an $11 million check in 2016, the paper gains were extraordinary. But paper gains in clinical-stage biotech are just that: paper. The real test, whether the drugs worked, was still ahead.

What is worth pausing to appreciate is how the 2020 biotech IPO window operated. In a normal environment, a company like Keros, with Phase 1 data and a promising but unproven platform, might have struggled to generate this level of investor enthusiasm. But 2020 was not a normal environment. The combination of near-zero interest rates, pandemic-driven interest in life sciences innovation, and a flood of retail and institutional capital looking for the next big thing in biotech created a window that was historically unprecedented. Of the roughly 120 life sciences IPOs in 2020, many were for companies at even earlier stages than Keros, some with nothing more than preclinical programs and a PowerPoint deck. Keros, with its Acceleron pedigree, experienced management team, and multiple clinical-stage assets, was a relative standout in this cohort.

The exuberance would not last. The XBI biotech index peaked in February 2021 and subsequently fell approximately 65% through its 2022 lows, wiping out hundreds of billions in market value across the sector. Many of the companies that IPO'd alongside Keros in 2020 and 2021 would see their stock prices fall 80% or more, and some would fail to reach clinical milestones and wind down entirely. The biotech bust of 2022-2023 would test every clinical-stage company's thesis, and Keros would be no exception. The question was whether the science could withstand the scrutiny that a rising-rate, risk-off market would impose.

VI. Clinical Inflection Point No. 1: KER-050 Phase 2 Data (2021-2022)

Every December, thousands of hematologists descend on a major American city for the Annual Meeting of the American Society of Hematology, the single most important conference in blood cancer research. For clinical-stage hematology companies, ASH is judgment day. Investors, physicians, and competitors scrutinize every poster, every oral presentation, every data table for signs of progress or failure. Career-defining moments happen in ballroom presentations that last fifteen minutes.

The first meaningful clinical data for Keros came at the 64th ASH meeting in December 2022, and it arrived at a moment when the company badly needed good news. The pandemic biotech boom had given way to a brutal correction. The XBI had fallen roughly 65% from its February 2021 peak. KROS shares had retreated from their $82 high to the $20s and $30s. The market was no longer willing to pay for platform stories on faith alone. It wanted data.

The Phase 2 trial, designated KER050-MD-201, was a dose-finding study in patients with lower-risk MDS who had anemia. Of 36 patients treated at the recommended Phase 2 dose, 29 were evaluable for efficacy after completing at least eight weeks of treatment. The patient population was mixed: roughly 64% had ring sideroblasts, a subtype where luspatercept performs well, and 36% did not, a subtype where treatment options are far more limited.

The headline number was an overall erythroid response rate of 51.7%, meaning 15 of 29 evaluable patients showed meaningful increases in hemoglobin. Among transfused patients, 50% achieved transfusion independence for at least eight weeks, and among those with high transfusion burden, the sickest group that needed the most blood, the transfusion independence rate was also 50%. There were no dose-limiting toxicities, no cases of progression to acute myeloid leukemia, and the safety profile was manageable: diarrhea, fatigue, and dyspnea were the most common side effects.

These numbers might not look spectacular to a lay observer, but in the context of lower-risk MDS, they were genuinely encouraging. To understand why, consider the bar that clinical trials must clear in this disease. MDS is a condition where spontaneous improvement is rare. Most untreated patients see their anemia worsen over time. A drug that achieves transfusion independence in half of heavily transfused patients is not just matching expectations; it is fundamentally changing the disease trajectory for those patients.

Half of the sickest patients were freed from regular blood transfusions, a result that translates directly into quality of life. No more biweekly trips to the infusion center. No more iron chelation therapy to manage transfusion-related iron overload. No more the grinding logistics of coordinating blood product availability.

An important additional signal emerged from iron metabolism: nearly half of patients with elevated ferritin levels, a marker of iron overload from chronic transfusions, saw their ferritin decrease meaningfully. This suggested that elritercept was not just masking the problem but actually improving the underlying biology.

The data also offered the first clinical evidence for elritercept's platelet-boosting effects. Unlike luspatercept, which has no meaningful impact on platelet counts, elritercept showed signs of stimulating thrombopoiesis. For MDS patients who struggle with both anemia and low platelets, this dual-lineage effect could represent a genuine differentiation from the existing standard of care.

How did elritercept compare to luspatercept? This was the question every analyst and investor was asking, and the honest answer was: it was too early for direct comparison. The Phase 2 trial was single-arm (no control group), the patient populations were not identical, and cross-trial comparisons in oncology are notoriously unreliable. But the signal was strong enough to justify moving forward, and critically, the responses appeared durable. By the time Keros presented updated data at ASH 2023, with a larger cohort of 60 evaluable patients over 24 weeks, the overall erythroid response rate held steady at 50%, and the median duration of response had extended to an impressive 134.1 weeks, over two and a half years. Among patients who achieved transfusion independence, 72% maintained it for at least 24 additional weeks.

To put the quality of life data in perspective, the ASH 2023 presentation showed that patients who achieved transfusion independence had a mean improvement of 5.8 points on the FACIT-Fatigue scale at week 24, compared to a decline of 3.2 points for non-responders. That nine-point gap is clinically meaningful. For an older patient who has been getting blood transfusions every few weeks, the difference between responding and not responding to elritercept is the difference between independence and dependence, between living at home and spending days at an infusion center.

The ASH 2024 presentation, with a data cutoff of April 2024, added another compelling piece of the puzzle. Among the 15 non-transfusion-dependent patients in the trial, 93.3% achieved a hemoglobin increase greater than 1.0 grams per deciliter, and 86.7% met the formal criteria for erythroid response. Among responders, every single one maintained their response for more than 24 weeks, and 77% maintained it for more than 52 weeks. No patients progressed to acute myeloid leukemia. For a disease where the natural trajectory is progressive decline, these are remarkable numbers.

The market reacted favorably. KROS shares bounced on the ASH 2022 data and held up through the 2023 update. More importantly, the data gave Keros the confidence to pursue a pivotal Phase 3 trial, and it attracted something far more valuable than a stock price bump: the attention of large pharmaceutical companies looking for late-stage assets in hematology.

VII. Clinical Inflection Point No. 2: Expanding to Myelofibrosis (2022-2024)

While the MDS program was generating headlines, Keros was quietly pursuing a second front that could prove equally important.

To understand why myelofibrosis matters, imagine the bone marrow as a factory floor. In a healthy person, the factory runs smoothly, producing billions of red blood cells, white blood cells, and platelets every day. In myelofibrosis, the factory is slowly being bricked over. Fibrous scar tissue infiltrates the marrow, progressively destroying the production capacity for all blood cell types. The spleen, which normally filters old blood cells, tries to compensate by taking on blood cell production itself, swelling to enormous size, sometimes filling the entire left side of the abdomen. Patients develop severe anemia, dangerous platelet deficiencies, constitutional symptoms like night sweats and bone pain, and a profound fatigue that makes normal daily functioning impossible.

There are roughly 56,000 prevalent cases across the seven major pharmaceutical markets. Median survival from diagnosis is five to seven years, making it one of the more lethal blood cancers. And the condition is as cruel as it is complex.

The standard of care in myelofibrosis is JAK inhibitors, a class of drugs that work by blocking the Janus kinase enzymes involved in inflammatory signaling. Ruxolitinib, marketed as Jakafi by Incyte and Novartis, was approved in 2011 and remains the most widely prescribed treatment. It does a reasonable job of reducing spleen size and alleviating symptoms like night sweats, bone pain, and fatigue. But here is the problem: JAK inhibitors do remarkably little for the underlying blood count problems. In fact, they often make anemia worse.

This creates a cruel treatment paradox. The drug that most effectively treats the symptoms of myelofibrosis simultaneously worsens one of its most debilitating complications. At least 40% of patients become refractory to ruxolitinib within a few years, and 70 to 80% of myelofibrosis patients develop significant anemia by the time they exhaust frontline therapy. Half of those anemic patients become transfusion-dependent. There is simply no good approved treatment for myelofibrosis-associated anemia, a gap that represents both a profound patient need and a substantial commercial opportunity.

Keros launched the RESTORE trial, an open-label, two-part Phase 2 study evaluating elritercept in myelofibrosis patients with anemia, both as monotherapy and in combination with ruxolitinib. The rationale was scientifically elegant: if elritercept could boost both red blood cell and platelet production through its ligand-trapping mechanism, it could address the exact deficiencies that JAK inhibitors leave untouched, potentially transforming it into a perfect complement to existing therapy.

Early data presented at ASH 2022 and 2023, from a small initial cohort of patients, showed encouraging safety and preliminary signs of hemoglobin increases and spleen volume reduction. By ASH 2024, with 73 patients enrolled and a data cutoff of August 30, 2024, the picture had sharpened considerably. In non-transfusion-dependent patients, 82.8% showed hemoglobin increases over a 12-week period in both the monotherapy and combination arms. Spleen volume reductions were observed, and total symptom scores improved. There were no treatment-related serious adverse events at the recommended dose.

The myelofibrosis opportunity represented a potentially faster and more differentiated path than MDS. The patient population was smaller, meaning clinical trials could be conducted with fewer patients. The unmet need was more acute, creating regulatory tailwinds for expedited review pathways. And critically, there was no direct competitor with a ligand trap mechanism in the myelofibrosis anemia space. Luspatercept, while being explored in MF, had not demonstrated the same platelet-stimulating effects that made elritercept particularly suited to a disease where multiple blood cell lineages are compromised.

In March 2024, the FDA granted Fast Track designation for KER-050 in lower-risk MDS. Fast Track is not a guarantee of approval, but it provides meaningful procedural advantages: more frequent meetings with FDA reviewers, the ability to submit sections of the biologics license application on a rolling basis rather than all at once, and eligibility for priority review. The designation was supported by the Phase 2 data from 79 patients and signaled the FDA's recognition that elritercept addressed an unmet need in the MDS population.

The regulatory strategy reflected a clear prioritization. MDS, with its larger patient population and established regulatory precedent from luspatercept's approval pathway, became the lead indication for Phase 3 development. Myelofibrosis, while offering potentially greater differentiation and higher unmet need, remained at Phase 2 and would likely follow a separate regulatory track. This sequencing made sense both scientifically (the MDS data was more mature) and financially (pursuing one Phase 3 trial at a time is far less expensive than pursuing two simultaneously). It also set the stage for what would become Keros' most important strategic decision: the Takeda partnership that would fund the Phase 3 program and fundamentally alter the company's trajectory.

VIII. The Licensing Deals: From Hansoh to Takeda (2021-2025)

Every clinical-stage biotech eventually faces a fundamental strategic question: do you build it yourself, or do you partner?

This is not just a financial question. It is a question about identity, ambition, and risk tolerance. Building a commercial-stage pharmaceutical company from scratch requires hundreds of millions of dollars, years of infrastructure development, and a completely different set of organizational capabilities than running clinical trials. Most clinical-stage biotechs never make it there. They either partner, get acquired, or run out of money trying to do it alone.

For Keros, this question arrived with increasing urgency as elritercept advanced through clinical development and the capital requirements for Phase 3 trials and eventual commercialization came into sharper focus. The company's deal-making history reveals how management navigated this tension.

The first major deal came in December 2021, when Keros licensed the rights to KER-050 in mainland China, Hong Kong, and Macau to Hansoh Pharma, a leading Chinese biopharmaceutical company. The terms were significant: $20 million upfront, up to $170.5 million in development and commercial milestones, and tiered royalties ranging from low double-digit to high-teen percentages on net sales. For a company with no approved products, the Hansoh deal provided validation and non-dilutive capital at a crucial moment.

But the truly transformative deal came three years later. On December 3, 2024, Keros announced a global license agreement with Takeda Pharmaceuticals for the exclusive rights to develop, manufacture, and commercialize elritercept worldwide outside of China. The terms were remarkable: $200 million upfront, development, approval, and commercial milestones potentially exceeding $1.1 billion, and tiered royalties on net sales. The deal became effective on January 16, 2025, after HSR antitrust clearance.

The Takeda deal fundamentally reshaped Keros. In one stroke, it provided immediate financial security, as the $200 million upfront payment arrived in February 2025, boosting Keros' cash position to over $720 million. It transferred the burden of Phase 3 development and eventual commercialization to a global pharmaceutical company with deep hematology expertise and the infrastructure to launch drugs in dozens of countries simultaneously. And it preserved Keros' economic interest through milestones and royalties, meaning the company would participate in elritercept's commercial success without bearing the cost of achieving it.

Takeda would fund and run the Phase 3 RENEW trial in MDS. The first patient was dosed in July 2025, triggering a $10 million milestone payment to Keros. Additional milestones are tied to regulatory submissions, approvals in the United States and Europe, and commercial sales thresholds, creating a multi-year stream of potential payments that could substantially exceed the upfront amount.

The strategic logic was sound but not without trade-offs. By licensing elritercept, Keros gave up the enormous potential upside of owning a blockbuster drug's commercial rights. If elritercept becomes a standard of care in MDS and myelofibrosis, the royalty stream will be valuable but will represent a fraction of what full ownership would have delivered. On the other hand, Keros was a company with fewer than 200 employees, no commercial infrastructure, and a cash burn rate that would have made self-funded Phase 3 trials and commercial launch extremely challenging. The Takeda deal was a pragmatic acknowledgment of these realities.

For investors watching the deal, the question became: what is Keros now? Post-Takeda, the company's relationship to elritercept shifted from drug developer to royalty recipient and milestone collector. The upside was capped but the risk was dramatically reduced. And the massive cash infusion created a new set of questions about capital allocation that would dominate the next chapter of the story.

It is instructive to compare the Keros-Takeda deal to how other clinical-stage biotechs have handled similar crossroads. Some, like Vertex Pharmaceuticals in its early days, chose to go it alone, building commercial infrastructure from scratch, a strategy that eventually produced extraordinary returns but required years of losses and dilutive financing. Others, like Acceleron itself, partnered their lead asset (luspatercept with Celgene/BMS) early and retained only economic interest, not commercial control. Keros chose the Acceleron model, which is perhaps fitting given Seehra's familiarity with how that partnership played out. The Acceleron-Celgene partnership ultimately worked spectacularly for Acceleron's shareholders: Merck acquired the company for $11.5 billion in 2021. Whether the Keros-Takeda partnership follows a similar trajectory depends entirely on the Phase 3 data.

The Hansoh deal for China rights added a geographic dimension to the partnership strategy. With Takeda covering the rest of the world and Hansoh covering Greater China, Keros had effectively outsourced global commercial development of its lead asset while retaining meaningful economic participation. The total potential deal value across both partnerships, including upfront payments, milestones, and royalties, could substantially exceed $1.5 billion if elritercept achieves multiple approvals and commercial success. For a company with a current market capitalization of roughly $350 million, that represents significant embedded optionality.

IX. The Cibotercept Crisis and Corporate Restructuring (2024-2025)

In the space of just six weeks, Keros Therapeutics experienced the highest high and the lowest low that a clinical-stage biotech can face. If the Takeda deal was the best thing that happened to Keros in late 2024, what happened next was the worst.

KER-012, cibotercept, had been developing as Keros' second major ligand trap program, targeting pulmonary arterial hypertension. The science was compelling: sotatercept, from Seehra's former company Acceleron, had been approved as Winrevair for PAH, validating the entire concept of using TGF-beta superfamily ligand traps in pulmonary vascular disease. Cibotercept used a modified ActRIIB domain engineered for the same pathway. If it worked, Keros would have two major clinical programs across two large markets.

The Phase 2 TROPOS trial began enrolling PAH patients across multiple dose levels. The goal was to find the sweet spot: a dose that was high enough to produce meaningful reductions in pulmonary artery pressure but low enough to avoid the safety issues that had plagued earlier TGF-beta pathway interventions.

In December 2024, barely days after the Takeda deal announcement, Keros voluntarily halted the two highest dose arms, 3.0 mg/kg and 4.5 mg/kg, after observing cases of pericardial effusion, the accumulation of fluid around the heart. Pericardial effusion is a known class effect of TGF-beta superfamily modulation; even Merck's Winrevair carries warnings about this risk. But the frequency and severity at these dose levels raised safety concerns that could not be ignored.

Then, in January 2025, new safety data emerged at the lower 1.5 mg/kg dose. Keros halted all dosing across the entire trial, including placebo arms. By May 2025, topline data confirmed that the safety profile was unacceptable, and Keros made the difficult decision to discontinue all development of cibotercept in PAH.

The fallout was immediate and severe. The company announced a 45% reduction in its workforce, cutting to approximately 85 full-time employees, with expected annualized cost savings of roughly $17 million. The stock, which had been trading in the $50-70 range on the back of the Takeda deal excitement, cratered. By April 2025, KROS hit a 52-week low of $9.12 per share.

The cibotercept failure also exposed Keros to a challenge that many clinical-stage biotechs face after a major pipeline loss: activist investor pressure. In April 2025, an investor disclosed an 11.2% stake in the company, and the board initiated a formal review of strategic alternatives, including a potential sale of the entire company. Keros adopted a shareholder rights plan, commonly known as a poison pill, expiring April 2026, to ensure an orderly process.

For two months, the future of Keros hung in the balance. The strategic review involved outreach to multiple third parties, engagement with potential acquirers, and extensive dialogue with stockholders. This is the kind of existential moment that clinical-stage biotech companies dread: the pipeline has contracted, the stock is depressed, and outside investors are circling with ideas about how to unlock value, ideas that may or may not align with management's vision.

When the review concluded on June 9, 2025, the board decided against a sale. The reasoning, though not fully disclosed, likely reflected a view that selling the company at a depressed valuation would not fairly compensate shareholders for the option value of elritercept under Takeda's stewardship and the potential of KER-065 in neuromuscular disease. Instead, Keros announced it would return $375 million in excess capital to shareholders, a dramatic move for a company that had only been public for five years. The capital return was effectively a concession to the activist thesis: if the company cannot deploy the excess cash productively, it should give it back to shareholders rather than sitting on it.

The mechanics of the capital return were executed in the fall of 2025. Keros negotiated direct share repurchases with two of its largest holders, ADAR1 Capital Management and Pontifax Venture Capital, at $17.75 per share. Together, these negotiated transactions totaled approximately $181 million. A separate tender offer for up to $194.4 million at the same $17.75 price was launched in October and completed in November. The tender was oversubscribed, with 17.7 million shares tendered against 10.95 million sought, resulting in a pro-rata acceptance of roughly 62%. In total, the capital return program repurchased approximately 36% of outstanding shares.

The Pontifax repurchase carried an additional consequence: Tomer Kariv and Ran Nussbaum, the Pontifax co-founders who had been on Keros' board since the earliest days, resigned their directorships as part of the transaction. The departure of the company's original venture backers from the boardroom marked the end of an era.

The cibotercept episode deserves closer examination because it illustrates a fundamental tension in biotech platform companies. The same scientific foundation that makes a platform strategy attractive, a shared understanding of a biological pathway that enables multiple drug candidates, also creates correlated risk. When Keros' PAH program failed on safety due to a class effect of TGF-beta superfamily modulation, it raised questions about whether similar safety issues could emerge in other programs built on the same biology. The elritercept program operates in a different receptor class (ActRIIA versus ActRIIB) and targets a different disease with different tissues and endpoints, so the mechanistic read-across is limited. But the psychological impact on investors was real: if one ligand trap can cause pericardial effusion, might another? This is the kind of question that clinical data, not scientific argument, must ultimately answer.

The broader lesson for biotech investors is that clinical-stage companies with multiple programs built on a single platform are not truly diversified in the way that a portfolio of independent assets would be. The programs share scientific, regulatory, and reputational risk in ways that are not always obvious until something goes wrong. Keros' cibotercept experience is now a case study in this dynamic.

X. KER-065, the Pivot to Neuromuscular Disease, and the Phase 3 in MDS (2024-2026)

After the cibotercept failure and corporate restructuring, Keros emerged as a fundamentally different company. The metamorphosis was dramatic. In the span of six months, Keros went from a multi-program platform company with 155 employees and three active clinical programs to a focused operation with roughly 85 people and two remaining stories: the elritercept royalty stream from Takeda, and KER-065, a new pipeline asset that would need to carry the weight of the company's independent future.

KER-065, which received the generic name rinvatercept, is an activin receptor-based ligand trap initially positioned for obesity and metabolic disease. The original thesis was that by inhibiting myostatin and activin A, two TGF-beta superfamily ligands that regulate muscle and fat metabolism, KER-065 could shift body composition toward more muscle and less fat. It was a compelling concept in a market that had been electrified by the success of GLP-1 agonists like semaglutide.

But clinical data from the Phase 1 trial in healthy volunteers, reported in March 2025, told a more nuanced story. KER-065 was well-tolerated across all dose levels from 1 to 5 mg/kg, with no dose-limiting toxicities or serious adverse events. The key findings showed increases in bone mineral density and muscle mass, along with decreases in fat mass, consistent with activin pathway inhibition. However, the effects on body composition, while real, suggested that the neuromuscular applications were more compelling than the obesity angle.

Keros pivoted KER-065 away from obesity, a commercially enormous but intensely competitive market dominated by GLP-1 agonists, and refocused it on Duchenne muscular dystrophy (DMD) and amyotrophic lateral sclerosis (ALS). These are devastating neuromuscular diseases with enormous unmet need and, critically, orphan drug economics that favor small companies. The pivot reflected a pragmatic assessment: competing with Eli Lilly and Novo Nordisk in obesity was a losing proposition for a company of Keros' size, but being a leader in DMD muscle preservation was achievable and potentially transformative.

The FDA granted Orphan Drug Designation for KER-065 in DMD, providing seven years of market exclusivity upon potential approval. In March 2026, just days before this article, Keros presented additional Phase 1 data at the MDA Clinical and Scientific Conference. A Phase 2 trial in DMD is targeted for initiation in the first quarter of 2026, with ALS Phase 2 discussions ongoing with the FDA.

Meanwhile, the elritercept story continued to advance under Takeda's stewardship. The Phase 3 RENEW trial, a global, randomized, double-blind, placebo-controlled study in transfusion-dependent MDS patients, dosed its first patient in July 2025. The trial targets red blood cell transfusion reduction as its primary endpoint, aligning with the regulatory precedent established by luspatercept's COMMANDS trial. A readout is expected in the 2026-2027 timeframe. If RENEW meets its primary endpoint, Keros stands to receive substantial milestone payments from Takeda, and the royalty stream on eventual commercial sales could be significant given that luspatercept already generates nearly $1.8 billion annually.

The company stated that its remaining cash, estimated at $693 million as of September 30, 2025, and reduced after the $375 million capital return, should fund operations into the first half of 2028. Additionally, Keros committed to distributing 25% of any net milestone payments received from Takeda on or before December 31, 2028 to stockholders, a mechanism designed to align the interests of remaining shareholders with the elritercept program's success even though Keros no longer controls it operationally.

XI. The Competitive Landscape and Strategic Positioning

The competitive map around Keros has shifted dramatically since the company's founding, and understanding it requires examining several distinct theaters of competition.

In MDS, the dominant force is Bristol Myers Squibb's Reblozyl. Luspatercept received its original FDA approval in November 2019 for MDS patients with ring sideroblasts and was expanded to first-line treatment of transfusion-dependent anemia in all lower-risk MDS patients in August 2023, based on the landmark COMMANDS trial. That trial showed 58.5% of luspatercept patients achieving red blood cell transfusion independence for at least 12 weeks combined with a hemoglobin increase of at least 1.5 grams per deciliter, versus 31.2% for epoetin alfa. Reblozyl's U.S. sales grew 80% in 2024, driven by the first-line label expansion, and global revenues approached $1.8 billion.

For elritercept to succeed commercially, it does not necessarily need to beat luspatercept head-to-head in ring sideroblast-positive patients, where Reblozyl is well-established. The differentiation strategy rests on three pillars. First, elritercept's broader ligand-binding profile, including activin A capture, may provide activity in non-ring-sideroblast patients where luspatercept is less effective. Second, the dual-lineage effect on both red blood cells and platelets could matter enormously in patients with concurrent thrombocytopenia. Third, the median duration of response of 134.1 weeks observed in Phase 2, if confirmed in Phase 3, would position elritercept as potentially the most durable option in its class.

In myelofibrosis, the competitive landscape is dominated by JAK inhibitors: ruxolitinib (Jakafi by Incyte and Novartis), fedratinib (Inrebic by BMS), pacritinib (Vonjo), and momelotinib (Ojjaara by GSK). These drugs address spleen size and symptoms but leave the anemia problem largely unsolved. The myelofibrosis treatment market is projected to reach $5.6 billion by 2034, and the anemia niche within it is essentially unaddressed by approved therapies. Elritercept's Phase 2 RESTORE data showing simultaneous hemoglobin improvement, spleen reduction, and symptom benefit in MF positions it uniquely in this space, though the program remains at an earlier stage than the MDS track.

The broader TGF-beta superfamily drug development landscape remains challenging. The long list of failed programs from major pharmaceutical companies, from Merck KGaA's bintrafusp alfa to Eli Lilly's galunisertib, serves as a reminder that this pathway punishes imprecision. Keros' ligand trap approach, which targets specific secreted ligands rather than inhibiting receptors directly, has proven more tractable than pan-TGF-beta inhibition. But even within the ligand trap class, the cibotercept failure in PAH demonstrated that the therapeutic window can be narrow and safety issues can emerge unexpectedly.

There is a poetic dimension to the competitive story that bears acknowledging. Jasbir Seehra built the scientific foundation at Acceleron that became luspatercept. He then left and created Keros to build what he believed would be the next generation. Acceleron was subsequently acquired by Merck for $11.5 billion. The ligand trap technology Seehra originally helped develop now generates billions in revenue for two of the world's largest pharmaceutical companies. Keros represents Seehra's bet that the best is yet to come, a bet that has not yet been fully resolved.

In the neuromuscular disease space, where KER-065 is now being developed, the competitive dynamics are different. Duchenne muscular dystrophy affects roughly 1 in 3,500 male births, with approximately 10,000 to 15,000 patients in the United States. The current treatment landscape is dominated by corticosteroids, which slow disease progression but carry severe side effects, and gene therapies from Sarepta Therapeutics and others, which aim to replace the defective dystrophin gene. KER-065's approach is complementary rather than competitive: by blocking myostatin and activin signaling to promote muscle growth and reduce muscle wasting, it could theoretically work alongside gene therapy rather than replacing it. This positions Keros in a potentially collaborative rather than purely competitive dynamic, which is relatively unusual in pharmaceutical markets.

For ALS, the competitive landscape is even more sparse. The disease, which progressively destroys motor neurons and leads to paralysis and death typically within three to five years of diagnosis, has only a handful of approved therapies, none of which significantly extend survival. If KER-065 can demonstrate even modest preservation of muscle function in ALS patients, the regulatory and commercial pathway could be compelling. The FDA has shown willingness to approve ALS therapies on the basis of functional endpoints and surrogate biomarkers, reflecting the desperate unmet need.

XII. Company Culture and Execution Playbook

Running a clinical-stage biotech company is an exercise in managing contradictions. You need to be bold enough to pursue ambitious science but disciplined enough to kill programs that are not working. You need to spend heavily on clinical trials while maintaining enough cash to survive if things go wrong. And you need to attract world-class talent while operating with a fraction of the resources that large pharmaceutical companies can deploy. It is a business model that resembles venture capital more than traditional pharmaceutical manufacturing: you are placing a series of bets, each with a relatively low probability of success, hoping that the ones that work will generate returns large enough to justify the entire portfolio.

The base rates in drug development are sobering. Industry-wide, only about 10% of drugs that enter Phase 1 clinical trials eventually receive FDA approval. For hematology biologics, the success rate is somewhat higher, closer to 15-20%, but the bar is still extraordinarily steep. A clinical-stage biotech like Keros is essentially asking investors to bet on beating those odds across multiple programs simultaneously. The math only works if the potential payoff for success is enormous, which in orphan disease, it often is.

Jasbir Seehra's leadership style has been shaped by decades of these contradictions. His career spans the transition from large pharmaceutical companies like Wyeth and Pfizer to the scrappier world of biotech startups. His scientific orientation is evident in how Keros has operated: the company makes decisions based on biology first, then works backward to the commercial and financial implications. This is the opposite of many biotech companies that start with a market opportunity and go shopping for science to fill it.

The capital allocation record at Keros has been a study in both ambition and adaptation. At its peak, the company was running multiple clinical programs simultaneously: Phase 2 trials for KER-050 in MDS and myelofibrosis, the TROPOS trial for cibotercept in PAH, early-stage development of KER-047 for iron deficiency and FOP, and preclinical work on KER-065. For a company with roughly 175 employees at its largest, this was an aggressive portfolio. The annual R&D spend reached $173.6 million in 2024, a significant number for a company with essentially no recurring revenue.

When the cibotercept safety signal forced a reckoning, Seehra and the board made tough decisions quickly. There is a phrase in biotech circles: "fail fast, fail cheap." In practice, most companies struggle to do either. They hold onto failing programs too long, burning cash and distracting management attention. Keros, to its credit, moved decisively. Within months of the first safety signal, the program was terminated, the workforce was reduced by 45%, and the company's strategic direction was reset.

The financial impact was immediate and measurable. R&D expenses dropped from $49.2 million in the third quarter of 2024 to $19.5 million in the third quarter of 2025. The net loss compressed from $53 million to $7.3 million in the same period. The company that emerged was leaner and more focused, but also more dependent on fewer bets.

The board composition has evolved with the company's trajectory, reflecting its shifting strategic priorities. Carl Gordon of OrbiMed, who joined during the Series C and served as Chairman until July 2024, brought deep biotech investing expertise and the pattern recognition that comes from evaluating hundreds of clinical-stage companies over a career spanning decades.

Jean-Jacques Bienaimé, the former CEO of BioMarin Pharmaceutical, joined as an independent director in June 2024 and became Lead Independent Director that same month. Bienaimé spent over 15 years leading BioMarin, one of the most successful rare disease companies in history, from a small clinical-stage biotech into a multi-billion-dollar commercial enterprise. His experience navigating FDA regulatory pathways, building commercial organizations for orphan drugs, and managing the expectations of a rare disease patient community brought governance perspective that Keros would need as it navigated the post-cibotercept transition.

The departure of Pontifax's representatives from the board in October 2025, as part of the share repurchase agreement, marked a significant governance transition. The founding venture capital investors, who had backed Seehra since the $11 million Series A in 2016, were cashing out and moving on. Whether this represents healthy maturation or the loss of founding DNA is a matter of perspective.

One lesson that the Keros story offers to biotech founders is the importance of sequencing risk. Seehra built on proven biology rather than pursuing entirely novel targets. He staffed the company with people who had done this before, who had already navigated clinical development, regulatory interactions, and deal-making. And when the Takeda deal offered a way to de-risk the elritercept program financially, he took it, even though it meant giving up the dream of building a fully integrated pharmaceutical company. These are the pragmatic decisions that separate companies that survive the clinical-stage gauntlet from those that do not.

XIII. Porter's Five Forces and Hamilton's 7 Powers Analysis

Every investment thesis in biotech eventually comes down to two questions: does the science work, and if it does, can the company capture the value? The first question is answered in clinical trials. The second requires a structural analysis of the markets, the competition, and the sources of durable competitive advantage. Understanding Keros' strategic position requires looking beyond the clinical data to the structural economics of the markets it operates in and the sources of competitive advantage it can or cannot claim.

Starting with the threat of new entrants: the barriers to entering the TGF-beta superfamily therapeutic space are genuinely high. Developing a biologic ligand trap requires deep expertise in protein engineering, structural biology, and the regulatory complexities of biologics manufacturing. Clinical trials in rare hematologic diseases are expensive and take years. Intellectual property, including composition of matter patents on specific engineered receptor domains, creates meaningful legal barriers. However, the success of luspatercept and sotatercept has validated the approach and attracted more attention to the field, increasing the likelihood that well-funded competitors will pursue similar mechanisms. On balance, barriers are high but not insurmountable, particularly for established pharmaceutical companies looking to build or acquire TGF-beta programs.

The bargaining power of suppliers in clinical-stage biotech is relatively low. Contract research organizations (CROs) that run clinical trials and contract development and manufacturing organizations (CDMOs) that produce biologic drugs operate in competitive markets. There is no single supplier with monopolistic pricing power over companies like Keros. This is a structural advantage for the industry that keeps input costs predictable.

The bargaining power of buyers, however, is a different story entirely. In the United States, drug pricing for orphan and rare disease therapies is governed by a complex web of payers, pharmacy benefit managers, hospital formulary committees, and increasingly, government negotiation. The Inflation Reduction Act of 2022 introduced Medicare price negotiation for certain drugs, including orphan drugs indicated for more than one disease. For a drug like elritercept that could potentially be approved in both MDS and myelofibrosis, this has implications for long-term pricing power. On the other hand, rare disease patients are often desperate, physician advocacy is strong, and manufacturers have historically been able to command premium pricing, often exceeding $150,000 per patient per year, for drugs that address genuine unmet needs. The dynamic is one of tension: enormous list prices tempered by an increasingly assertive payer environment.

The threat of substitutes is moderate to high and growing. In MDS, luspatercept is already an established standard of care, and any new entrant must demonstrate clear superiority or differentiation to gain market share. In myelofibrosis, JAK inhibitors address different aspects of the disease but may evolve to better manage anemia. Looking further ahead, gene therapies and cell-based approaches could potentially address the root causes of these diseases in ways that chronic biologic therapies cannot. The competitive moat around any single drug in hematology is therefore time-limited.

Competitive rivalry is currently moderate but asymmetric. In the specific niche of ligand traps for MDS anemia, the primary rivalry is between elritercept and luspatercept. BMS has the enormous advantage of an established commercial presence, physician familiarity, a first-line label, and the institutional knowledge that comes from having marketed Reblozyl for years. Physicians know the dosing, the side effects, the patient profiles that respond best. Elritercept, now under Takeda's commercial direction, will need to differentiate on efficacy, durability, or safety to carve out meaningful market share. The advantage Takeda brings is its own deep hematology expertise, having marketed drugs like Adcetris and Ninlaro in blood cancers for years.

In myelofibrosis anemia, there is essentially no approved competitor with a comparable mechanism, which represents a genuine first-mover opportunity. This is the market where elritercept could achieve its most distinctive positioning: not competing against an established drug, but creating an entirely new treatment category.

Turning to Hamilton Helmer's 7 Powers framework, which asks where enduring competitive advantages come from, Keros' position is nuanced. Scale economies are not yet relevant because the company has no commercial operations. Network effects do not apply in traditional pharmaceutical markets. Branding power is minimal since drug adoption is driven by clinical data and physician relationships rather than consumer brand loyalty.

Where Keros does have power is in cornered resources. The company's specific intellectual property on engineered ligand trap domains, Seehra's deep expertise and the clinical data generated from the elritercept trials, represent resources that competitors cannot easily replicate. An inventor on over 70 patents, Seehra's personal knowledge of TGF-beta superfamily biology and ligand trap engineering is itself a cornered resource. The clinical data, particularly the 134-week median duration of response in MDS Phase 2, is a proprietary asset that de-risks future development.

Counter-positioning is the second power that applies. Seehra's team saw what Acceleron had done with luspatercept, identified its limitations, particularly the lack of platelet stimulation and the restriction to ring sideroblast patients, and engineered a next-generation molecule to address those gaps. This is classic counter-positioning: the incumbent's existing product architecture makes it difficult for BMS to pivot luspatercept to match elritercept's binding profile without developing an entirely new molecule, which would take years and face its own regulatory and commercial hurdles.

Switching costs represent a potential future power. Once patients are stabilized on a biologic therapy and achieving transfusion independence, physicians and patients are generally reluctant to switch to a different agent. If elritercept can establish itself as a first-line or second-line treatment, the biological and psychological switching costs could create significant retention.

The verdict is that Keros' power resides primarily in cornered resources and counter-positioning, with the potential for switching costs to develop post-approval. The critical question is whether the company, through Takeda, can convert clinical success into these durable competitive advantages before competitors close the gap.

Process power, the ability to execute complex operational tasks better than competitors through accumulated institutional knowledge, is still developing. Keros has demonstrated competence in clinical trial design and execution through Phase 2, and the Takeda partnership transfers much of the Phase 3 and commercial execution burden to a partner with proven capabilities in hematology. But Keros has not yet demonstrated the end-to-end process power, from clinical development through regulatory approval to commercial launch, that defines a mature pharmaceutical company. That capacity, if it develops at all, will likely come through the KER-065 program, which Keros intends to advance independently.

One framework worth applying here is the concept of "platform decay." In technology companies, platform advantages tend to compound over time as network effects and switching costs accumulate. In biotech, platform advantages can decay because the underlying science becomes better understood by competitors, patents eventually expire, and new therapeutic modalities (gene therapy, cell therapy, gene editing) can leap-frog existing approaches entirely. Keros' platform advantage in TGF-beta superfamily ligand traps is real but time-limited. The window during which Keros' specific engineering innovations provide competitive differentiation will narrow as other companies, including large pharmaceutical companies with vastly greater resources, invest in similar approaches. The urgency of clinical progress is therefore not just about patient need; it is about staying ahead of the competitive clock.

XIV. Bull vs. Bear Case

With the strategic framework established, it is time to lay out the competing visions for Keros' future. In clinical-stage biotech, the bull and bear cases are not gentle gradations; they are starkly different worlds.

The bullish case for Keros rests on a chain of events that begins with clinical data and cascades into commercial value.

Start with elritercept in MDS. If the Phase 3 RENEW trial meets its primary endpoint, demonstrating meaningful transfusion independence in lower-risk MDS patients, the drug is on track for regulatory approval. The precedent is clear: luspatercept was approved on a similar endpoint. Takeda has the global commercial infrastructure, the hematology sales force, and the regulatory expertise to launch elritercept efficiently. Analyst projections suggest the addressable MDS market could exceed $5 billion by 2032. Even a modest share of that market would generate significant royalty revenue for Keros, and the milestone payments from Takeda, potentially exceeding $1.1 billion in aggregate, would transform the company's financial profile.

The bull case extends to myelofibrosis, where elritercept's dual-lineage effect on red blood cells and platelets could make it the first therapy specifically addressing the devastating anemia that JAK inhibitors leave untouched. The myelofibrosis treatment market is projected at $5.6 billion by 2034. If elritercept proves effective in this indication, the additional milestones and royalties from Takeda would compound the financial upside substantially.

Then there is KER-065, rinvatercept, the neuromuscular disease program. DMD and ALS are diseases with enormous unmet need and strong orphan drug economics. The Orphan Drug Designation from the FDA provides seven years of market exclusivity. If Phase 2 data in DMD demonstrates meaningful preservation or improvement of muscle function, KER-065 could become a significant asset in its own right. Some analysts have noted that the actomyosin mechanism of action, promoting muscle mass through activin pathway inhibition, addresses the underlying pathology of DMD in a way that complements existing gene therapy approaches.

Orphan drug economics provide a structural tailwind. The global orphan drug market was valued at approximately $189 billion in 2024 and is projected to grow to $688 billion by 2035, a compound annual growth rate of roughly 12.5%, twice the rate of non-rare-disease drugs. Hematology accounts for roughly 17% of the orphan drug market, or approximately $38 billion. Orphan drug designation provides seven years of market exclusivity, tax credits for clinical development costs, and waiver of FDA application fees. These economic incentives were designed precisely to encourage companies like Keros to pursue therapies for small patient populations where the unit economics would otherwise be challenging.

The terminal bull case is acquisition. A pharmaceutical company looking to acquire a diversified TGF-beta superfamily platform, with a validated licensing deal already in place and a second pipeline asset in rare neuromuscular disease, might find Keros attractive at current valuations, which reflect significant discount to the potential value of the elritercept royalty stream alone.

The bearish case is equally well-founded and starts with the most fundamental risk in clinical-stage biotech: Phase 3 trials can fail.

This is not a theoretical concern. The history of drug development is littered with promising Phase 2 programs that fell apart in Phase 3. The reasons are varied and often unpredictable. A drug that shows impressive results in a carefully selected 60-patient Phase 2 trial may show diminished effects when tested in a broader, more heterogeneous Phase 3 population. Safety signals that were absent in small trials can emerge when thousands of patients are treated. The placebo effect, which is particularly strong in diseases with subjective symptoms, can erode the apparent benefit of an active drug in a controlled trial.

The RENEW trial in MDS is randomized and placebo-controlled, and while the Phase 2 data was encouraging, single-arm Phase 2 results do not always translate to Phase 3 success. The placebo response rate in MDS trials can be meaningful, and the bar for statistical significance in a registrational study is higher than in dose-finding work. If RENEW misses its endpoint, the milestone payments from Takeda evaporate, the royalty stream never materializes, and Keros' financial thesis collapses.

Safety remains a persistent concern. The cibotercept failure in PAH was driven by pericardial effusion, a class effect of TGF-beta superfamily modulation. While elritercept uses a different receptor domain and has shown a clean safety profile through Phase 2, the possibility that safety issues emerge at larger scale or with longer follow-up cannot be dismissed. The TGF-beta pathway is involved in so many biological processes that unexpected toxicities can surface in ways that are difficult to predict from smaller trials.