Kroger: From Corner Store to Grocery Giant

I. Introduction

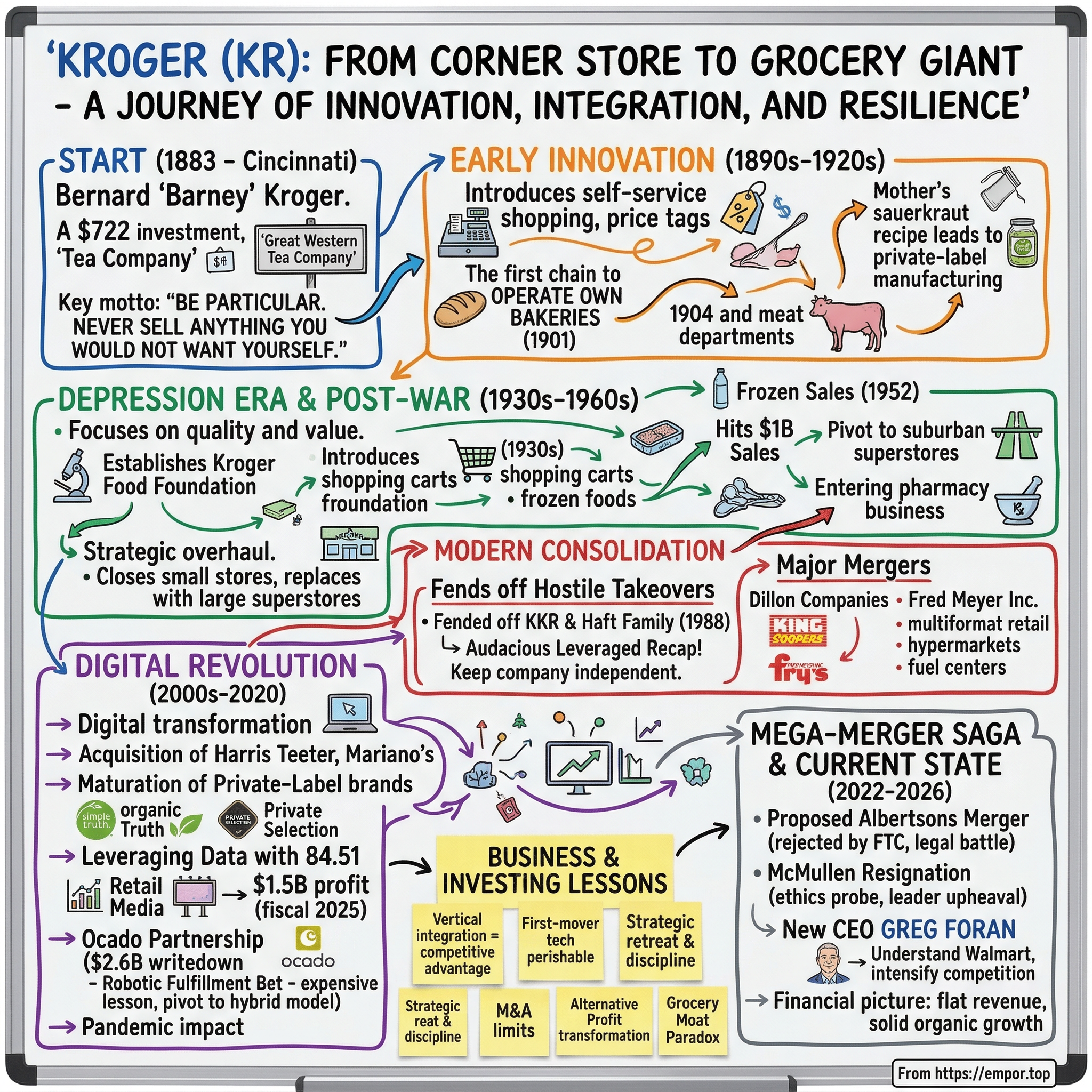

Picture this: Cincinnati, 1883. A 23-year-old son of German immigrants walks into a cramped storefront at 66 Pearl Street in downtown Cincinnati. He has exactly $372 in his pocket — every dollar he has ever saved. His business partner, an Irish immigrant named B.A. Branagan, has scraped together another $350 by borrowing from friends. Combined capital: $722. They hang a hand-painted sign that reads "Great Western Tea Company" and open the doors.

That 23-year-old was Bernard Heinrich "Barney" Kroger. The motto he lived by was deceptively simple: "Be particular. Never sell anything you would not want yourself." Over the next 143 years, that $722 corner store would grow into the largest supermarket chain in America — a $147.6 billion revenue juggernaut operating 2,731 stores across 35 states, employing over 414,000 people, and serving 11 million customers every single day.

But the story of Kroger is not a straight line from corner store to corporate colossus. It is a story of vertical integration before the term existed. Of surviving panics, depressions, and hostile takeover attempts. Of pioneering self-service shopping, electronic scanners, and digital coupons decades before competitors caught on. It is also a story of strategic retreat — of knowing when to leave markets, when to close stores, and when to walk away from a $24.6 billion merger that would have reshaped American grocery. And in early 2026, it is the story of a company navigating a leadership upheaval, a $2.6 billion technology write-down, and an intensifying competitive war with Walmart, Costco, and a rapidly expanding Aldi — all while fending off a bitter lawsuit from the partner it almost married.

This is how a German immigrant's son built America's grocery empire — and what investors need to understand about where it goes from here.

A note on terminology before diving in: Kroger's fiscal year ends in late January or early February, so "fiscal year 2025" refers to the twelve months ending in early February 2026. The company reports financial results using a 52/53-week fiscal year, which can make year-over-year comparisons tricky. Throughout this article, fiscal years are referenced as the company uses them, not by calendar year.

II. The Barney Kroger Story and Founding Context

To understand Kroger, you have to understand the man who built it, because his instincts — for thrift, for vertical control, for timing — still echo through the company's DNA today.

Bernard Heinrich Kroger was born on January 24, 1860, in Cincinnati's Over-the-Rhine neighborhood, the fifth of ten children. His parents had come to America separately from Germany — his father Johan from Westphalia, his mother Mary Gertrude Schlebbe from the tiny village of Elve. Johan Kroger had arrived in America in 1827 at age ten and eventually settled in Cincinnati, where the German immigrant community was enormous. By 1850, roughly 50,000 Germans — 27 percent of the city's entire population — called Cincinnati home. Johan opened a small dry goods store, and the family lived a modest but stable life.

Then came the Panic of 1873. America's economy collapsed. Banks failed by the hundreds. Railroads went bankrupt. And Johan Kroger lost his store. Overnight, thirteen-year-old Barney's childhood ended. He quit school and went to work.

His first job was farm labor near Pleasant Plain, Ohio — brutal physical work for a boy who was only fourteen. He earned six dollars a month, despised his employer, and found no future in it. Then something happened that the company's official histories gloss over but that shaped everything that followed: Barney contracted malaria. Weakened and broke, he walked 37 miles back to Cincinnati on foot. Thirty-seven miles. Sick with a disease that was killing people across the Ohio Valley. On foot. No money, no ride, no safety net. It was the kind of crucible that either breaks a person or forges something harder. For Barney Kroger, it was the latter.

Years later, Kroger would tell employees and business associates that the experience taught him two things: never depend on anyone else for your survival, and never stop moving forward. Those principles — self-reliance and relentless forward motion — would define not just his career but the corporate culture he created.

By sixteen, he had talked his way into a job as a door-to-door salesman for the Great Northern and Pacific Tea Company, selling coffee and tea in the same Over-the-Rhine streets where he had grown up. He was relentless. He learned which products sold, which customers were loyal, and — critically — which middlemen were taking margins that did not need to exist. He moved to the Imperial Tea Company, continued refining his instincts, and by 23 had saved $372. Every penny of it went into that first store.

The partnership with B.A. Branagan lasted exactly one year. Kroger bought out his partner in 1884 — he preferred total control — and immediately opened a second store. This preference for sole ownership was not arrogance. It was an expression of the same self-reliance principle forged during that 37-mile walk home. If you do not control the business, someone else's decisions can destroy you. Kroger would maintain this philosophy throughout his career, even as the business grew to thousands of stores.

The first year was not easy. A train struck his delivery wagon and destroyed $500 worth of product — more than his entire original investment. Then floods from the Ohio River swept through his store, costing him another $350 in inventory. In modern terms, Kroger suffered two catastrophic losses that exceeded his initial capital before his business was even a year old. Most people would have quit. Barney Kroger responded by working harder and buying smarter.

By the summer of 1885, the Great Western Tea Company had four stores in Cincinnati. When the next financial panic hit in 1893, most small grocers panicked, dumped inventory, and went under. Kroger did the opposite — he bought aggressively at distressed prices, expanding from four stores to seventeen in a single stroke. It was the first demonstration of a pattern that would repeat throughout the company's history: using economic disruption as a catalyst for growth rather than a reason to retreat.

Personal tragedy stalked him alongside professional success. In 1899, his wife Mary and his oldest son both died of diphtheria. Kroger, by all accounts a private man who poured his grief into work, pressed on. By 1902, the Great Western Tea Company had forty stores and a factory. Kroger incorporated the business and gave it a new name — the Kroger Grocery and Baking Company — putting his own name on the door for the first time.

The man who had walked 37 miles home from a failed farm job with malaria was now running the largest grocery operation in Cincinnati. But he was only getting started.

III. Early Innovation and Vertical Integration (1890s-1920s)

What made Kroger different from the dozens of other grocery chains that sprouted across America in the late 1800s was not just that he expanded — it was that he integrated. Barney Kroger had an almost instinctive understanding that the path to lower prices and higher margins ran through controlling the supply chain, not just the storefront.

The first major innovation came in 1895, when Kroger introduced what amounted to self-service shopping. Before this, grocery shopping in America looked nothing like what we know today. You walked into a store, stood at a counter, told a clerk what you wanted, and the clerk fetched it from behind the counter or from a back room. Prices were often unposted — the clerk told you what things cost, and haggling was common. Kroger turned this on its head: he put price tags on every item, displayed merchandise on open shelves, and let customers walk through the store, select what they wanted, and carry it home themselves. It sounds obvious now. In 1895, it was revolutionary — and it slashed labor costs dramatically. Where competitors needed multiple clerks to serve customers one at a time, Kroger could run a store with fewer employees while serving more people.

In 1901, Kroger made his most consequential strategic decision: he started baking bread. The Kroger Grocery and Baking Company became the first grocery chain in the country to operate its own bakeries. This was not a marketing gimmick — it was economic warfare. By baking in-house, Kroger eliminated the bread wholesaler's margin entirely. He could sell bread at lower prices than competitors who bought from outside bakeries, while simultaneously earning a higher margin on every loaf. The customers got cheaper bread. Kroger got better economics. The middleman got nothing.

Three years later, in 1904, Kroger acquired Nagel Meat Markets and Packing House, making his stores the first in the country to include full meat departments. Think about what this meant from a customer's perspective: instead of visiting a separate bakery, a separate butcher, and a separate grocer, you could get everything at Kroger. The convenience moat was being dug.

But the most charming origin story in the company's history involves sauerkraut. Kroger had been buying cabbage from local farmers — lots of it — and found himself with far more than his customers could reasonably consume fresh. Rather than waste it, he brought the surplus home to his mother, Mary Gertrude, who had grown up in Westphalia and knew exactly what to do with too much cabbage. She made sauerkraut using her family recipe, and Barney sold it in his stores. In a city where more than a quarter of the population was German, homemade sauerkraut flew off the shelves. His mother's kitchen became, in effect, Kroger's first manufacturing plant. That kitchen produced not just sauerkraut but pickles and other preserved goods, establishing the template for what would become one of the largest food manufacturing operations in the United States — a network that today includes 35 production facilities generating over $30 billion in annual private-label revenue.

The company expanded rapidly through the 1920s, mostly through the acquisition of smaller chains throughout the Midwest and South. By 1929, Kroger operated an astonishing 5,575 stores — a number the company would never reach again, because the strategy would shift from maximizing store count to maximizing store productivity.

Then Barney Kroger did something extraordinary: he sold out. In 1928, one year before the stock market crash and the onset of the Great Depression, he sold his controlling shares to Lehman Brothers for over $28 million. He stepped down as president, turning the role over to William H. Albers. The timing was either brilliant foresight or spectacular luck — probably a mix of both. Kroger was 68 years old. He had built a grocery empire from $372, survived floods, train wrecks, financial panics, and personal tragedy. He gave each of his children $1.5 million (the equivalent of roughly $16 million in today's dollars) and entered retirement.

Barney Kroger died in 1938 at age 78. His personal estate was valued at nearly $9 million — the equivalent of roughly $200 million today. He had started with less than $400 and ended as one of the wealthiest men in Ohio. But the real legacy was not the money. It was the company — and the blueprint for how a grocery business could compete by controlling everything from the wheat field to the checkout counter.

That blueprint would be tested almost immediately by the worst economic catastrophe in American history.

IV. Depression Era to Post-War Evolution (1930s-1960s)

The Great Depression arrived in 1929 like a wrecking ball through the American economy, and the grocery business was not spared. Hundreds of small chains went bankrupt. Consumer spending collapsed. Families who had been buying steak switched to beans, or went without.

Kroger survived — and in characteristic fashion, it did so by innovating rather than simply cutting. In 1930, the company established the Kroger Food Foundation, making it the first grocery chain in America to systematically monitor product quality and scientifically test foods before putting them on shelves. This might sound like a regulatory formality, but in the 1930s it was a genuine differentiator. At a time when food adulteration was common and consumers had little visibility into what they were buying, Kroger was hiring scientists to test products in a lab.

The Food Foundation produced one of the company's signature innovations: "Tenderay" beef, a proprietary process for tenderizing beef without chemicals. The name became a marketing asset. The Foundation also created a Homemakers Reference Committee — 750 real homemakers across the country who tested food samples in their own kitchens and provided feedback to the company. This was essentially crowdsourced product development, six decades before the internet made the concept fashionable.

These quality controls accomplished two things simultaneously: they built consumer trust during an era of maximum anxiety about value, and they reinforced the private-label manufacturing capability that Barney Kroger had started in his mother's kitchen. By 1933, Kroger had become the second-largest grocery chain in the United States, proving that its combination of vertical integration and quality focus could survive even the most brutal economic downturn.

The 1930s also brought the introduction of frozen foods and shopping carts to Kroger stores — both seemingly small developments that transformed the economics of grocery shopping. Frozen foods extended shelf life and reduced waste, addressing one of the oldest problems in the grocery business: perishability. Shopping carts increased average basket size by making it physically easier for customers to buy more. Before the shopping cart, customers carried their groceries in hand baskets, which meant they could only buy as much as they could physically hold. The shopping cart effectively removed the constraint on impulse buying and larger trips. Every innovation that increased the customer's convenience or the store's efficiency was adopted with the same pragmatic logic that Barney Kroger had applied to sauerkraut: if it makes economic sense and the customer benefits, do it.

The postwar period transformed American life in ways that reshaped grocery retailing permanently. Soldiers returned home, started families, and moved to suburbs. The GI Bill fueled home ownership in new developments miles from traditional downtown shopping districts. Highways and automobiles made it possible — and eventually expected — for families to drive to a large, well-stocked store rather than walk to a corner grocer. This was the birth of the modern supermarket era, and Kroger was well-positioned to capitalize on it.

By 1952, Kroger hit a major milestone: annual sales topped $1 billion for the first time. This was a company that had been founded with $722 in a single Cincinnati storefront. In less than seventy years, it had become a billion-dollar enterprise. Adjusted for inflation, that $1 billion in 1952 sales equates to roughly $12 billion in 2026 dollars — impressive, but still less than a tenth of what the company generates today. The real transformation was just beginning, because suburbanization, highway construction, and the rise of the supermarket format meant that Kroger had to evolve again — from a city-based chain of small stores to a suburban network of large supermarkets.

Beginning in 1955, Kroger shifted its growth strategy from organic expansion to acquisitions, buying supermarket chains in new markets rather than opening stores one at a time. This was a fundamental strategic pivot that would define the company for the next seven decades.

To understand why M&A became Kroger's preferred growth strategy, consider the basic economics. Building a single new supermarket from scratch — land acquisition, construction, equipment, initial inventory, hiring and training — costs tens of millions of dollars and takes 18 to 24 months before the store even opens its doors. Then it takes years to build a customer base and reach profitability. Buying an existing chain, by contrast, gives you instant market presence, established customer bases, trained employees, and supplier relationships. You pay a premium for the acquisition, but you start generating revenue on day one.

The trade-off is that you inherit someone else's problems — store layouts that do not match your standards, labor agreements you did not negotiate, real estate you might not have chosen, and a corporate culture that may clash with your own. Kroger bet that its operational playbook was strong enough to overcome these disadvantages, and for the most part, it was right. The company developed a systematic process for integrating acquisitions: rebanner the stores, retrain the employees, reset the product mix to emphasize private-label items, connect the stores to Kroger's distribution and manufacturing network, and impose Kroger's pricing and promotional strategy. This integration playbook became one of the company's core competencies.

In 1961, the company opened its first SupeRx drugstore in Milford, Ohio, located adjacent to a Kroger food store. This marked Kroger's entry into the pharmacy business — a move that would eventually grow into a network of 2,252 retail pharmacies and 226 health clinics. The logic was the same as adding bakeries and meat counters decades earlier: if customers are already coming to your store for groceries, why not capture their prescription spending too? Pharmacies added a powerful element to the grocery trip: they created a recurring, non-discretionary reason to visit the store. A customer who fills a monthly prescription at a Kroger pharmacy is a customer who visits the store at least once a month, regardless of what competitors are offering on price. Each additional category deepened the customer relationship and increased the switching cost of shopping elsewhere.

This strategy of adjacent category expansion — bakery, meat, pharmacy, fuel, financial services — is the thread that runs through Kroger's entire 143-year history. Each addition made the grocery trip more comprehensive, more convenient, and harder to replicate at a single competitor. It was Barney Kroger's original insight applied and reapplied over generations: control more of what the customer needs, and you control more of the customer's spending.

In 1963, Kroger made its boldest geographic move to date, acquiring the 56-store Market Basket chain and entering the southern California market for the first time. California was the golden prize of American retail — the most populous state, with growing suburbs and high consumer spending. But it was also fiercely competitive, and Kroger would eventually discover that being big nationally did not guarantee success regionally. The company would exit California by 1982, a strategic retreat that taught a painful but important lesson about the limits of geographic expansion.

This pattern — aggressive entry, followed by sober reassessment, followed by strategic withdrawal when the economics did not work — would become one of Kroger's defining characteristics. It is the opposite of the sunk-cost fallacy. Where many companies pour good money after bad trying to make a struggling market work, Kroger developed an institutional willingness to walk away. That discipline would prove as important as any acquisition in building long-term value.

V. The Modern Consolidation Era (1970s-1999)

In 1970, James Herring became president of The Kroger Company, and with him came the most dramatic strategic overhaul in the company's history since Barney Kroger himself.

Herring ordered an exhaustive internal review of every market Kroger operated in, every store format, and every division's economics. The findings were sobering: hundreds of Kroger's smaller supermarkets were not competitive. They were too small, too old, and too poorly located to compete with the newer, larger stores that regional competitors were building. Rather than patch and hope, Herring made a decision that shaped the modern Kroger: he closed hundreds of small stores and replaced them with "superstores" — massive retail spaces of 60,000 square feet or more, up to 50 percent larger than traditional Kroger units, with expanded specialty departments, colorful new designs, and vastly more product selection.

At the same time, Kroger pulled out of markets where its stores simply were not competitive enough to justify further investment. Chicago went first — most remaining stores were sold to Dominick's in 1971. Wisconsin followed, with 55 stores statewide sold or closed, including 19 Milwaukee locations. Minneapolis was next, with stores sold to Quality Foods. Birmingham fell in 1972. In total, the number of retail divisions was consolidated from 23 to 13. It was painful but disciplined — Kroger was choosing to be dominant in fewer markets rather than mediocre in many.

The superstore rollout moved at remarkable speed. By the end of 1974, Kroger had opened 300 new stores and converted 250 existing ones into the superstore format. This was a company that had decided exactly what it wanted to be — the largest, most comprehensive grocery store in every market it served — and was executing that vision with military precision.

Kroger's technological leadership also emerged during this era. In 1972, the company became the first grocer to test electronic checkout scanners, using an RCA system that could read product codes and automatically ring up prices. To understand why this mattered, consider what grocery checkout looked like before scanners. Every single item in a grocery store was individually price-stamped by hand — a store employee physically applied a price sticker to each can of soup, each box of cereal, each bag of flour. When a customer reached the register, a cashier read each price tag and manually keyed it into the cash register. The process was slow, error-prone, and generated zero useful data beyond the total sale amount.

Scanners changed everything. They eliminated pricing errors, dramatically sped up checkout times, and — most importantly — created a data stream. For the first time in grocery history, a retailer could automatically track exactly which products were selling, in what quantities, at what times of day, and in what combinations. This was a foundational capability. The data from those early scanners was primitive by modern standards, but the principle — that transaction data is a strategic asset, not just an accounting record — was the seed of what would eventually become 84.51, Kroger's data science subsidiary, and Kroger Precision Marketing, its billion-dollar retail media business. The connection between a 1972 RCA scanner test and a 2025 artificial intelligence-powered advertising platform is a straight line, even if the technology at each end would be unrecognizable to the other.

Kroger also formalized its consumer research department during this period, becoming the first grocer to systematically study consumer behavior and preferences. The company did not just want to know what was selling — it wanted to know why. This commitment to understanding the customer, rather than simply stocking shelves and hoping for the best, set the stage for the data-driven personalization that would become central to Kroger's competitive strategy decades later.

In 1979, Kroger officially became the second-largest supermarket chain in the United States, trailing only Safeway. The company had transformed itself from a regional Midwestern chain into a national contender in less than a decade — a testament to the power of the superstore strategy and the willingness to exit weak markets.

Four years later, in 1983, it made the move that cemented its status as a coast-to-coast operator: the merger with Dillon Companies. The deal, valued at approximately $750 million, brought King Soopers in Colorado, Fry's in Arizona, City Market in mountain communities, and Gerbes in Missouri into the Kroger fold. In a single transaction, Kroger went from being a strong Midwestern and Southern grocer to a true national player with presence from the Rockies to the Eastern Seaboard.

But the most dramatic chapter of the decade came in 1988, when Kroger found itself the target of not one but two hostile takeover bids.

The Haft family — Herbert and Robert Haft, who ran the Dart Group Corporation out of Landover, Maryland — launched the first attack, offering $4.4 billion and announcing an effort to accumulate a 15 percent stake. The Hafts were aggressive retail raiders who had already forced Safeway into a leveraged buyout earlier that year — a deal that resulted in thousands of layoffs and the closure of hundreds of stores. Kroger employees and management watched the Safeway takeover unfold and understood exactly what a Haft victory would mean for their company.

Then, in a move that escalated the situation dramatically, Kohlberg Kravis Roberts and Company — KKR, the most feared leveraged buyout firm on Wall Street — entered with a $4.6 billion bid. This was 1988, the peak of the LBO era. KKR had just completed the legendary RJR Nabisco deal — the "Barbarians at the Gate" transaction that became a symbol of 1980s corporate excess. Nobody said no to KKR.

Kroger said no — and the way it said no became legendary on Wall Street.

Rather than sell to either bidder, the company's board, under CEO Lyle Everingham, engineered a leveraged recapitalization — essentially performing its own LBO without giving up control. The logic was audacious: if raiders want to buy us because our cash flows can support massive debt, then we will take on that debt ourselves, pay shareholders a huge premium, and keep the company independent. Kroger borrowed more than $5 billion, issued stockholders a $40 per share cash dividend and a five-year note valued at $8.69 per share, and took on approximately $5.3 billion in debt. It was, by multiple accounts, the first time a U.S. company had successfully fended off a hostile takeover from KKR. The resulting debt load was crushing and required years of asset sales, cost cuts, and divisional consolidation to work through. But the company remained independent, and the stock price eventually recovered as the debt was paid down.

The experience left a lasting mark on Kroger's corporate culture: a deep respect for balance sheet strength and a wariness of financial engineering. It also demonstrated something important about the grocery business itself — that a company with thin margins, massive cash flows, and hard assets was both an attractive target for financial buyers and, if managed correctly, capable of servicing enormous debt through operational discipline.

The leveraged recapitalization reshaped Kroger's financial strategy for a generation. Having nearly lost the company to raiders, management became intensely focused on returning value to shareholders through buybacks and dividends while maintaining enough balance sheet flexibility to avoid vulnerability. The lesson was clear: in the grocery business, your stock price is your defense. If the market undervalues you, someone will try to buy you. The best defense is operational excellence that the market recognizes and rewards — a philosophy that explains Kroger's persistent focus on identical store sales growth, margin improvement, and capital returns.

The crown jewel of the consolidation era came in 1999, when Kroger completed the largest merger in its history: the $13 billion acquisition of Fred Meyer, Inc.

Fred Meyer was not just another grocery chain — it was something different entirely. Founded in Portland, Oregon, in 1922 by Fred G. Meyer, the company had pioneered the hypermarket concept in America decades before Walmart Supercenters existed. A typical Fred Meyer store combined a full supermarket with a general merchandise department, a jewelry counter, a pharmacy, a fuel station, and garden center — all under one roof. The company also operated Ralphs, one of the most recognized grocery brands in southern California; QFC (Quality Food Centers), a premium banner in the Pacific Northwest; and Smith's Food and Drug, a strong player across the Rocky Mountain states.

The deal brought Kroger something it had been building toward for decades: a truly multi-format retail operation. Before Fred Meyer, Kroger was primarily a supermarket company with some pharmacies and convenience stores. After Fred Meyer, it was a retail grocery conglomerate operating multiple formats — from neighborhood supermarkets to massive hypermarkets — with fuel centers that would eventually number over 1,700 locations. The fuel centers, in particular, proved to be a brilliant strategic addition. While fuel margins are thin, the loyalty loop they create is powerful: customers earn fuel discounts through grocery purchases, which incentivizes them to consolidate their grocery shopping at Kroger to maximize fuel savings. This flywheel — grocery spending drives fuel discounts, fuel discounts drive grocery loyalty — became a cornerstone of Kroger's customer retention strategy.

The Fred Meyer merger was the culmination of sixteen years of systematic national expansion through M&A, and it established the geographic and operational footprint that Kroger would operate from for the next two decades.

As the century closed, Kroger was the undisputed king of American grocery — a $43 billion revenue company operating more than 2,200 stores across 31 states, with manufacturing plants, fuel centers, pharmacies, and the most diversified retail grocery operation in the country. But a new century was about to bring threats that no amount of store count could address. Walmart was already becoming a grocery powerhouse. A bookseller named Amazon was beginning to reimagine retail. And in Essen, Germany, two brothers named Aldi were preparing their assault on the American grocery market.

VI. Digital Revolution and 21st Century Strategy (2000-2020)

The first two decades of the 21st century tested Kroger in ways that Barney Kroger could never have imagined. The competitive landscape shifted beneath the company's feet: Walmart became a grocery powerhouse, Amazon bought Whole Foods and launched Amazon Fresh, Aldi and Lidl began their relentless march across the American market, and a pandemic turned the entire industry upside down. Kroger's response was a combination of continued acquisition, digital transformation, and an all-in bet on its greatest inherited asset — the ability to make things.

The acquisition machine continued to run. In 2014, Kroger completed the purchase of Harris Teeter Supermarkets for approximately $2.5 billion, adding 227 upscale stores in the southeastern and mid-Atlantic markets. Harris Teeter gave Kroger something it had lacked: a premium banner with strong positions in affluent suburban communities, particularly in the Carolinas, Virginia, and the Washington, D.C. corridor.

In 2015 came the $800 million acquisition of Roundy's, an otherwise unremarkable Midwestern chain with one spectacular asset: Mariano's, a high-end grocery concept in the Chicago market. This was a strategically delicious move. Kroger had left Chicago in 1971 because it could not compete profitably with entrenched local chains at the mass-market level. Forty-four years later, it returned — but through a completely different door. Mariano's was not a mass-market grocery store. It was a premium experience: wine bars inside the store, chef-prepared meals, artisanal cheese counters, and a shopping atmosphere closer to Whole Foods than to a traditional supermarket. By entering through the premium segment, Kroger avoided the head-to-head price competition with discount chains that had driven the original exit. It was the same city, but a fundamentally different competitive strategy.

The same year, Kroger made two smaller acquisitions that signaled its digital ambitions more clearly than any press release could. The first was YOU Technology Brand Services, a Silicon Valley provider of digital coupons and personalized promotions. The second was Vitacost.com, an e-commerce health and wellness retailer purchased for approximately $280 million. YOU Technology accelerated Kroger's ability to deliver targeted offers to individual customers based on their purchase history — the beginning of a personalization capability that would become central to the company's competitive strategy. Vitacost proved less successful and was eventually sold to iHerb in January 2026.

But the most important strategic development of this era was not an acquisition. It was the maturation of Kroger's private-label manufacturing operation into something that most investors still do not fully appreciate.

When Barney Kroger started baking bread in 1901, he established a principle: own the production, and you control both quality and margin. Over the next century, Kroger built that principle into a $30 billion private-label empire. Today, the company operates 35 manufacturing plants producing everything from dairy products to snacks to pet food. Its brands — Simple Truth (the largest natural and organic brand in the country with over $3 billion in annual sales), Private Selection (premium), Kroger Brand, Heritage Farm, Smart Way, and Home Chef — collectively generate roughly 20 percent of the company's total revenue.

The economics of private label are the key to understanding Kroger's profitability. When a customer buys a can of Kroger-brand green beans instead of a national brand, Kroger captures both the retailer's margin and the manufacturer's margin. Private-label products typically carry gross margins 10 to 15 percentage points higher than national brands. Over 90 percent of Kroger's customer households purchase its store brands. More than 13,000 private-label items line the shelves of a typical store. In fiscal year 2025, Kroger launched over 900 new private-label products, including 370 fresh items. This is not a sideshow — it is the economic engine that allows a grocery company operating on overall net margins below 2 percent to generate nearly $5 billion in annual operating profit.

The other strategic pillar of this era was data. In 2003, Kroger partnered with Dunnhumby, a British data science firm best known for powering the Tesco Clubcard loyalty program. The partnership evolved into a joint venture called dunnhumbyUSA, and in 2015, Kroger acquired the U.S. operation outright, renaming it 84.51 (after the longitude coordinate of Kroger's Cincinnati headquarters). Today, 84.51 employs hundreds of data scientists who analyze purchase data from over 60 million loyalty card households, with more than 95 percent of all Kroger transactions linked to a loyalty card. The unit powers Kroger Precision Marketing, the company's retail media network, which allows consumer packaged goods companies to target advertising at specific customer segments based on actual purchase behavior, not demographic guesses.

Retail media has become one of the most important financial stories in grocery — and it is worth pausing to explain why, because most people outside the industry do not fully grasp its significance.

Think about it this way: when Procter & Gamble wants to advertise its Tide detergent, it has traditionally spent money on television commercials, digital ads, and print campaigns. But none of those channels can tell P&G whether the person who saw the ad actually bought the product. Kroger Precision Marketing can. Because Kroger knows what 60 million households actually purchase — not what they search for online, not what they click on, but what they physically put in their shopping carts — it can offer advertisers something extraordinarily valuable: closed-loop measurement. A CPG company can target an ad at Kroger shoppers who buy a competing brand, and then measure whether those shoppers actually switched. This is advertising with a direct, measurable return on investment, which is why consumer packaged goods companies are willing to pay premium rates for it.

Kroger's alternative profit businesses — including Kroger Precision Marketing, financial services, and personal finance products — generated $1.5 billion in operating profit in fiscal year 2025. To put that in perspective, that $1.5 billion represents roughly 30 percent of Kroger's total adjusted FIFO operating profit, generated from a business that essentially did not exist fifteen years ago. When the retail media division generates margins estimated at 60 to 80 percent, it contributes more absolute profit than many of Kroger's grocery divisions. This is a high-margin business built on top of a low-margin business, and it fundamentally changes the way investors should think about Kroger's earnings power. Kroger is not just a grocery company that happens to have a media business — it is increasingly a data company that happens to sell groceries.

On the technology front, Kroger made what appeared to be a transformative bet on automated fulfillment through a partnership with Ocado, a British online grocery company.

To understand the Ocado bet, you need to understand the fundamental challenge of online grocery. When a customer orders groceries for delivery, someone has to physically walk through a store (or warehouse), pick each item from the shelf, bag it, and either drive it to the customer's home or prepare it for pickup. This is labor-intensive, time-consuming, and expensive — fundamentally more costly per order than having the customer walk the aisles themselves. Ocado's solution was to remove the humans from the picking process. Its technology used massive automated warehouses — Customer Fulfillment Centers, or CFCs — where thousands of robots moved across a grid system, retrieving products and delivering them to packing stations at extraordinary speed. A single Ocado warehouse could process 300,000 orders per week with a fraction of the labor required by in-store picking.

The vision was ambitious: a national network of these robotic warehouses that would allow Kroger to serve e-commerce customers with unprecedented speed and efficiency.

As of early 2026, that vision has not played out as planned. Kroger took a $2.6 billion impairment charge on the Ocado network in the third quarter of fiscal year 2025 after a site-by-site analysis revealed that several facilities were dramatically underperforming expectations. Three Customer Fulfillment Centers — in Pleasant Prairie, Wisconsin; Frederick, Maryland; and Groveland, Florida — were closed. Planned new facilities in Charlotte, North Carolina, and Phoenix, Arizona were cancelled. Kroger paid Ocado $350 million in exit costs. It was an expensive lesson in the difference between technology that works in demonstration and technology that delivers at scale in the cutthroat economics of grocery fulfillment.

The company is now pivoting to a hybrid fulfillment model that relies more on in-store picking and third-party delivery partnerships with Instacart, DoorDash, and Uber Eats. Management projects that this shift will improve e-commerce operating profit by approximately $400 million in fiscal year 2026, and the company expects its digital business to reach overall profitability by the first half of 2026. Digital sales have grown at double-digit rates for five consecutive quarters, reaching over $16 billion for the full fiscal year 2025, with a 20 percent increase in the fourth quarter alone.

The question for investors is whether Kroger can build a profitable e-commerce channel fast enough to compete with Walmart, which has invested billions in its own online grocery capability and already dominates with over 23 percent of the U.S. grocery market. The Ocado writedown was a setback, but the pivot to lower-cost fulfillment methods may ultimately prove more sustainable than betting everything on robotic warehouses.

There is also a broader lesson here about the nature of technology adoption in grocery. The Ocado concept — centralized robotic warehouses serving a wide geographic area — worked brilliantly in the United Kingdom, where population density is high and delivery distances are short. In the sprawling geography of the American market, where a single Kroger division might cover an area larger than the entire UK, the economics were fundamentally different. The robots worked. The warehouses functioned. But the unit economics — the cost of picking, packing, and delivering an order of groceries across suburban distances — did not pencil out against the simpler model of having a store employee walk the aisles of an existing store and hand the bag to a customer waiting in the parking lot. Sometimes the low-tech solution wins because geography and economics override technological elegance.

VII. The Albertsons Mega-Merger Saga (2022-2024)

On an October morning in 2022, Kroger's management team and its advisors placed what they clearly believed was their biggest strategic bet since Fred Meyer: a $24.6 billion agreement to acquire Albertsons Companies, the second-largest traditional supermarket chain in the United States. At $34.10 per share in cash, it was the largest supermarket acquisition ever proposed in American history. The combined company would have operated roughly 5,000 stores, employed nearly 700,000 people, and challenged Walmart's grocery dominance more directly than any American supermarket company had ever attempted.

The strategic logic was straightforward — and, frankly, compelling. Grocery is a scale game. The bigger you are, the better your purchasing power, the lower your unit costs, and the more efficiently you can spread fixed investments in technology, logistics, and private-label manufacturing across stores. Consider the math: if Kroger spends $3.8 billion on capital expenditures across 2,731 stores, that is roughly $1.4 million per store. A combined Kroger-Albertsons with 5,000 stores could spread the same technology investment across a much larger base, reducing the per-store cost of innovation by nearly half. In an industry where margins are measured in pennies, that kind of scale leverage is the difference between investing in the future and slowly falling behind.

Kroger and Albertsons also had significant geographic complementarity. Kroger was strong in the Midwest, South, and Mountain West, while Albertsons — through banners like Safeway, Vons, Jewel-Osco, and Shaw's — held strong positions in the Pacific Northwest, Northern California, the Mid-Atlantic, and parts of the Northeast where Kroger had limited or no presence. On paper, the overlap was manageable. The combined company would have been a true coast-to-coast grocery giant with the scale to fight Walmart on more equal terms and the technology investment capacity to compete with Amazon. There was also a defensive dimension: both companies faced pressure from the same competitors — Walmart, Costco, Aldi — and combining would have allowed them to share the burden of investment in digital, data, and supply chain capabilities.

But antitrust regulators saw it differently. And the story of this merger — which consumed two years of management attention, over $1 billion in direct costs, and untold opportunity cost — is ultimately the story of a regulatory battle that the company lost comprehensively. It is also a case study in how the post-Lina Khan FTC approached grocery market concentration, and a precedent that may shape the industry's consolidation possibilities for a generation.

To address overlap concerns, Kroger and Albertsons negotiated a divestiture agreement with C&S Wholesale Grocers, a privately held New England-based wholesale distributor. The initial plan, announced in September 2023, called for divesting 413 stores to C&S for approximately $1.9 billion. When regulators signaled that this was insufficient, the package was expanded in April 2024 to 579 stores, with C&S paying $2.9 billion. C&S would operate the divested stores under their existing banners, essentially stepping in as a replacement competitor in markets where the merged Kroger-Albertsons would otherwise have dominated.

The Federal Trade Commission was not persuaded. In February 2024, the FTC filed suit to block the acquisition, arguing that the merger would reduce competition in hundreds of local markets, leading to higher prices for consumers and worse conditions for workers. The FTC's approach was notable for its conceptual framework: rather than evaluating the merger at the national level — where the combined company would still have been smaller than Walmart — the commission analyzed competition at the local level, market by market, neighborhood by neighborhood. In their view, what mattered was not whether America had enough grocery stores in aggregate, but whether Mrs. Johnson in suburban Denver had enough meaningful choices within a reasonable driving distance.

A bipartisan group of nine state attorneys general joined the opposition. The FTC's economic expert testified that the combined company would exceed monopoly thresholds in over 2,500 local markets where Kroger and Albertsons currently competed directly.

The divestiture plan itself came under intense scrutiny. Critics argued that C&S — primarily a wholesale distributor with limited experience operating retail grocery stores — was simply not a credible buyer. Could a company that had never run a large retail operation successfully manage 579 supermarkets across multiple states? The FTC thought not. And, in a twist that would later fuel an ugly legal battle, there were allegations that C&S itself had begun criticizing elements of the very divestiture package it had agreed to purchase.

On December 10, 2024, two courts delivered the death blow within an hour of each other — a sequence so dramatic that it felt almost choreographed.

First, U.S. District Judge Adrienne Nelson issued a preliminary injunction halting the merger while it underwent administrative review at the FTC. Judge Nelson's ruling was extensive and detailed, rejecting Kroger's arguments that Walmart's dominance justified the combination and finding that the proposed C&S divestiture was insufficient to preserve competition. Then, approximately sixty minutes later, a Washington state court judge separately ruled that the merger violated that state's consumer protection law. Two courts, two jurisdictions, two rulings — both against Kroger, both on the same day. It was a one-two punch from which the deal could not recover. Both companies announced the termination of the merger agreement.

What followed was a legal brawl that remains unresolved as of March 2026. Albertsons immediately sued Kroger in the Delaware Court of Chancery, demanding the $600 million reverse termination fee stipulated in the merger agreement, plus billions of dollars in additional damages representing the lost merger premium. Albertsons' core allegation: Kroger had willfully breached its obligations by failing to exercise "best efforts" to secure regulatory approval.

The claim was not baseless. Court filings revealed that in September 2024, Albertsons had offered Kroger approximately $800 million — about $1 per Albertsons share — to help Kroger expand the divestiture package by adding 33 stores in Washington and 2 in Colorado, potentially addressing the regulators' remaining concerns. Kroger never responded to the offer. Albertsons alleged that Kroger had developed "buyer's remorse" and was no longer motivated to close the transaction.

Kroger fired back with its own counterclaim in March 2025, painting a very different picture. According to Kroger, while it was diligently working to secure regulatory approval, Albertsons was engaged in a "secret and misguided campaign" together with C&S to pursue an unauthorized regulatory strategy that ultimately undermined the entire deal. Specifically, Kroger alleged that Albertsons executive Ms. Morris conducted secret communications with C&S's CEO using personal emails and cell phones, and that this covert collaboration resulted in C&S criticizing the divestiture package it had voluntarily agreed to — which in turn caused regulators to view C&S as an inadequate buyer.

Albertsons denied everything. "No Albertsons employee participated in any surreptitious scheme to undermine the merger," the company stated, insisting that the communications between Morris and C&S were known to Kroger.

The dispute extended further. C&S separately sued Kroger for a $125 million termination fee related to the failed divestiture plan. That dispute was settled on confidential terms in 2025. A judge also ruled that former Kroger CEO Rodney McMullen must explain the circumstances of his resignation as part of the litigation discovery process. As of February 2026, a judge ruled that both Albertsons and Kroger must pay attorneys' fees related to the failed deal proceedings.

The core lawsuit over the $600 million termination fee remains ongoing. Kroger has disclosed that the total cost of pursuing the Albertsons merger exceeded $1 billion.

What does the failed merger reveal? It suggests that traditional grocery consolidation in the United States has reached its regulatory limits. When the second and third largest supermarket chains cannot combine — even with a massive divestiture package — it means that the FTC views grocery markets as fundamentally local, not national. Kroger can be huge nationally, but what matters to regulators is whether consumers in Boise or Denver or Philadelphia have enough choices for their weekly shopping. This has profound implications for Kroger's future growth strategy: if M&A at scale is off the table, growth must come from organic investment, digital channels, and alternative profit streams rather than from buying competitors.

VIII. Current State and Competitive Position

The Kroger that exists in March 2026 is a company in transition — not decline, but genuine reinvention under new leadership following one of the most turbulent twelve-month periods in its history.

The leadership upheaval began on March 3, 2025, when CEO Rodney McMullen resigned abruptly after the board conducted an ethics investigation. McMullen had been a Kroger lifer — 46 years with the company, starting as a part-time stock clerk in Lexington, Kentucky while attending the University of Kentucky. He rose through the finance organization, became CFO in 2000, and was named CEO in January 2014. Under his leadership, Kroger had pursued an ambitious strategy of digital transformation, data analytics investment, and M&A growth. He was the architect of the Albertsons merger attempt and the champion of the Ocado partnership.

The board had been alerted to personal conduct issues on February 21, 2025, and immediately engaged independent counsel. The investigation concluded that McMullen's conduct was "inconsistent" with Kroger's business ethics policy, though "unrelated to the business" and not involving any Kroger associates or the company's financial operations. McMullen forfeited his 2024 bonus and all unvested equity awards. After 11 years at the helm, his departure was a shock — and it came at a moment when the company was navigating the aftermath of the failed Albertsons merger, the Ocado write-down, and intensifying competitive pressure. The timing could hardly have been worse.

Ronald Sargent, Kroger's Lead Director and former CEO of Staples, was appointed Chairman and Interim CEO immediately. Sargent brought stability and corporate governance experience, but he was never intended as a long-term solution. The board moved with purpose, conducting a CEO search that lasted approximately eleven months.

On February 9, 2026, Kroger named Greg Foran as its permanent CEO. Foran was a strategic choice: a New Zealand native who had served as CEO and President of Walmart U.S. from August 2014 to January 2020, overseeing Walmart's massive grocery operations during a period of intense competitive pressure. He had subsequently served as CEO of Air New Zealand through October 2025. His appointment was widely interpreted as a signal that Kroger wanted an outsider who understood exactly how Walmart thinks and operates — because understanding your most dangerous competitor from the inside is about as valuable as intelligence gets in retail warfare.

The financial picture tells a nuanced story. Kroger reported total revenue of approximately $147.6 billion for fiscal year 2025 (ended February 1, 2026), essentially flat compared to fiscal year 2024's $147.1 billion when adjusted for the sale of Kroger Specialty Pharmacy and the impact of the 53rd week. Identical store sales without fuel — the metric that matters most in grocery — grew 2.9 percent for the full year, demonstrating that the core business continues to generate solid organic growth even without acquisitions. The fourth quarter showed 2.4 percent identical sales growth, with adjusted earnings per share of $1.28, beating analyst consensus of $1.20 by over 6 percent.

The reported numbers, however, were distorted by the $2.6 billion Ocado impairment charge. On a GAAP basis, Kroger posted an operating loss of $1.54 billion in the third quarter due to this write-down. Adjusted FIFO operating profit — the metric that strips out the impairment and LIFO accounting adjustments — came in at $4.9 billion for the full year, up from $4.7 billion in fiscal year 2024. Adjusted earnings per share were $4.85, a 9 percent increase year-over-year. Gross margin improved to 22.9 percent from 22.3 percent, driven by private-label growth and lower shrink (the industry term for theft and spoilage losses).

With the Albertsons merger dead, Kroger redirected the capital it had set aside for the acquisition into a massive share repurchase program. The company authorized $7.5 billion in buybacks in December 2024 and substantially completed that program during fiscal year 2025. An additional $2 billion authorization was approved in December 2025. The buyback was aggressive — a clear message to shareholders that management believed the stock was undervalued and that returning capital was a better use of cash than pursuing another large acquisition.

The competitive landscape has intensified. Walmart dominates U.S. grocery with roughly 23 percent market share, generating approximately $276 billion in grocery revenue alone. Kroger holds roughly 8.5 to 10 percent of the market, depending on which measure is used. But the more pressing threat may come from below rather than above. Aldi announced plans to open 180 new U.S. stores in 2026 and has seen store visits increase 8 percent year-over-year, compared to Kroger's 0.8 percent growth. Costco, which has gained market share every year for the past five years, continues to attract grocery shoppers with its bulk-buy model and aggressive pricing. Amazon, while less dominant in physical grocery than initially feared, continues to invest in online grocery infrastructure.

On the labor front, Kroger faces significant pressure. Approximately 10,000 King Soopers workers in Colorado went on strike for 12 days in February 2025 before reaching a tentative agreement. In Southern California, roughly 45,000 grocery workers at Ralphs (a Kroger banner), Albertsons, Vons, and Pavilions voted to authorize an Unfair Labor Practice strike. Multiple major contract expirations are approaching in 2026: 19,500 workers at Fry's stores in Arizona in March, 14,000 Kroger workers in Michigan potentially in June, and 20,000 in Ohio in August. Labor costs are rising across the industry, and Kroger's heavily unionized workforce means these costs are not easy to manage.

Management has guided fiscal year 2026 to identical store sales growth of 1 to 2 percent, adjusted FIFO operating profit of $5.0 to $5.2 billion, adjusted earnings per share of $5.10 to $5.30, and free cash flow of $2.7 to $2.9 billion. Capital expenditures are expected to increase to $3.8 to $4.0 billion, reflecting investments in store remodels, new store openings, and technology. The company plans to increase new store builds by 30 percent over 2025 levels and is entering new markets including Jacksonville, Florida, and Kansas City through its Harris Teeter and Marketplace banners.

The company is doubling down on its Marketplace large-format banner, which carries general merchandise alongside standard grocery — a move that positions Kroger to capture more of the total shopping trip, much as Fred Meyer stores have done in the Pacific Northwest for decades. The Marketplace format, typically ranging from 80,000 to 130,000 square feet, is Kroger's answer to the Walmart Supercenter: a one-stop destination where customers can buy groceries, clothing, home goods, electronics, and pharmacy products under one roof. While Kroger will never match Walmart's general merchandise breadth, the Marketplace format allows it to compete for a larger share of the customer's total spending, rather than ceding everything outside of food to competitors.

Simultaneously, the company is closing approximately 60 underperforming locations while accelerating new openings: 30 store projects were completed in 2025, with 14 new stores breaking ground in the fourth quarter alone. This simultaneous rationalization and expansion — pruning the weakest branches while planting new ones — represents the kind of disciplined portfolio management that has characterized Kroger's approach since the Herring era of the 1970s.

For investors, the key question is whether Kroger's core strengths — scale, private-label manufacturing, data analytics, and the growing retail media business — are sufficient to maintain profitability in a market where Walmart's pricing power is unassailable, Aldi's value proposition is increasingly attractive to mainstream consumers, and digital grocery economics remain challenging. The data suggests that Kroger is not a growth story in the traditional sense — identical store sales growth of 2 to 3 percent is essentially tracking food inflation — but it is an efficiency and margin expansion story, with alternative profit streams providing a potential path to earnings growth that outpaces revenue growth.

IX. Playbook: Business and Investing Lessons

Kroger's 143-year history is an unusually rich case study in retail strategy, and several patterns emerge that are worth examining closely — not because they are unique to Kroger, but because they illustrate principles that apply across industries.

Vertical integration as competitive advantage. Barney Kroger's decision to bake bread in 1901 was not just an operational choice — it was the establishment of a strategic doctrine that his successors have followed for over a century. Today, Kroger's 35 manufacturing plants produce over $30 billion in annual private-label sales. This is the deepest vertical integration in American grocery retail. Simple Truth alone generates over $3 billion in annual revenue. The manufacturing network gives Kroger something that pure retailers do not have: control over both the production margin and the retail margin on a significant portion of its sales. In an industry where overall net margins run below 2 percent, the additional margin captured through private-label manufacturing is the difference between mediocre and acceptable profitability. This lesson extends beyond grocery: in any industry where margins are thin, owning the supply chain can be the single most important strategic advantage.

First-mover advantage in retail technology. Kroger has a pattern of being the first grocer to adopt technologies that later become industry standard: self-service shopping in 1895, in-store bakeries in 1901, meat departments in 1904, electronic scanners in 1972, digital coupons and AI personalization in 2014. Each innovation gave Kroger a temporary advantage in either cost efficiency or customer experience. But first-mover advantage in technology is perishable — once competitors adopt the same technology, the advantage disappears unless you are already investing in the next wave. Kroger's $2.6 billion Ocado write-down is a cautionary note on this front: being first does not mean being right, and the cost of betting on the wrong technology at scale can wipe out years of operational gains.

Strategic retreat as discipline. Kroger has exited more markets than most companies have entered: Chicago in 1971, Wisconsin, Minneapolis, and Birmingham in the early 1970s, California in 1982, and numerous other markets over the decades. In each case, the company made a cold-eyed assessment that the cost of remaining competitive in those markets exceeded the potential returns. This is the opposite of the "fight for every inch" mentality that many retailers adopt, and it has served Kroger well. The resources freed up by exiting underperforming markets were redeployed into markets where Kroger could win. It is worth noting, however, that Kroger's recent return to Chicago (through Mariano's) and planned expansion into Jacksonville and Kansas City suggest that market exits are not necessarily permanent — they are tactical decisions that can be reversed when conditions change. The underlying principle is capital allocation discipline: deploy resources where returns are highest, not where tradition or ego demand.

M&A as primary growth strategy. From the Dillon Companies in 1983 to Fred Meyer in 1999 to Harris Teeter in 2014 to the attempted Albertsons merger, Kroger has been an acquisition-driven company for most of its modern history. This approach has clear advantages: it is faster than organic growth, it provides instant market presence, and it allows the acquirer to impose its operational playbook on the target's stores. But the Albertsons failure exposed the limits of this strategy. When the second and third largest players in an industry cannot combine, the largest cannot grow through M&A. This is a structural shift that forces Kroger to find other paths to growth — and the company's increased investment in new store builds, digital channels, and alternative profit businesses suggests that management has internalized this lesson.

Alternative profit as margin transformer. The emergence of Kroger's retail media and data analytics business — $1.5 billion in operating profit from alternative sources in fiscal year 2025 — may be the most underappreciated element of the company's financial story. Grocery is a low-margin business by definition. But advertising and data monetization are high-margin businesses. When Kroger Precision Marketing sells a consumer packaged goods company the ability to target ads at specific customer segments based on actual purchase data from 60 million households, the margins on that transaction are estimated at 60 to 80 percent. This is a fundamentally different business than selling groceries, and it is growing fast. For investors, the question is whether Kroger can scale this business to the point where it meaningfully transforms the company's overall margin profile — and the $1.5 billion number suggests it already has.

The grocery moat paradox. Perhaps the most important lesson from Kroger's history is that the grocery business is simultaneously one of the hardest industries to build a moat in and one of the hardest to disrupt from the outside. The reason is the same in both cases: groceries are a daily necessity, purchased locally, with extreme price sensitivity. This means that no single retailer can ever fully dominate — because consumers will always comparison-shop and switch. But it also means that outsiders cannot easily displace incumbents — because the logistics of moving fresh, perishable food from farm to shelf to consumer are enormously complex, capital-intensive, and deeply local. Amazon discovered this when it bought Whole Foods in 2017 and found that grocery was not simply another category to add to its e-commerce platform. The produce had to be fresh. The stores had to be clean. The labor had to be trained. The supply chains had to work in real time, not just in warehouses. This is why grocery retailing rewards patience, operational discipline, and incremental improvement over revolutionary disruption — and it is why a 143-year-old company still holds the largest market share among traditional supermarkets.

X. Bear vs. Bull Case

Bull Case

Start with scale. Kroger's $147.6 billion in revenue makes it the largest traditional supermarket company in the United States. That scale translates directly into purchasing power: when you are buying for 2,731 stores, you negotiate prices with suppliers that smaller competitors simply cannot match. The 35 manufacturing plants producing $30 billion in private-label products take this further — Kroger is not just buying at scale, it is producing at scale, capturing margins that even other large retailers forfeit to third-party manufacturers.

The omnichannel position is strengthening. Digital sales exceeded $16 billion in fiscal year 2025, growing 20 percent in the fourth quarter. The pivot away from expensive automated fulfillment centers toward lower-cost hybrid fulfillment models should improve e-commerce profitability by an estimated $400 million in fiscal year 2026. Five consecutive quarters of double-digit digital sales growth suggest that Kroger's online channel is gaining traction with customers, not just spending money.

The alternative profit engine — retail media, data analytics, financial services — generated $1.5 billion in operating profit and is growing faster than the core grocery business. This is a high-margin overlay on a low-margin base, and it leverages Kroger's most defensible asset: first-party purchase data from 60 million loyalty households linked to 95 percent of transactions. No other grocer except Walmart has this combination of scale and data depth.

The private-label portfolio, led by Simple Truth's $3 billion in annual sales, provides both margin uplift and customer differentiation. Over 90 percent of Kroger households buy the company's brands. And new CEO Greg Foran brings direct experience from the most successful grocery operator in the world — Walmart — which could inject fresh operational discipline and strategic clarity at exactly the right moment.

Finally, the aggressive buyback program — $7.5 billion substantially completed in fiscal year 2025, plus an additional $2 billion authorization — is returning substantial capital to shareholders while the stock trades at a modest multiple relative to earnings growth. The buyback has the effect of concentrating future earnings among fewer shares, meaning that even modest absolute profit growth translates into meaningful per-share earnings growth. At fiscal year 2026's guided midpoint of $5.20 per share, earnings have grown roughly 16 percent from the $4.47 reported in fiscal year 2024 — a growth rate driven in significant part by share count reduction rather than revenue expansion. This is financial engineering in the best sense: returning excess capital to shareholders through tax-efficient buybacks rather than letting it accumulate on the balance sheet or chase value-destroying acquisitions.

Bear Case

Walmart's dominance is the elephant in every room where Kroger's future is discussed. With approximately 23 percent of the U.S. grocery market versus Kroger's roughly 9 percent, Walmart has more than double the purchasing power and a demonstrated willingness to use price as a competitive weapon. Walmart can lose money on groceries and make it up in general merchandise. Kroger cannot. This asymmetry is structural and permanent.

Amazon remains a threat, though a less immediate one than initially feared. Amazon's grocery ambitions have been somewhat tempered — the scaling back of Amazon Fresh stores and the operational challenges at Whole Foods suggest that online grocery profitability is difficult for everyone. But Amazon's willingness to invest at a loss for years, combined with its logistics infrastructure and Prime membership ecosystem, means the threat never fully goes away.

Aldi's expansion is arguably the most underestimated competitive threat. The German discounter is opening 180 stores in the United States in 2026 and has seen 8 percent growth in store visits — ten times Kroger's rate. Aldi's value proposition — dramatically lower prices on a curated selection of mostly private-label products — is increasingly appealing to mainstream consumers across income levels. Costco continues to gain market share every year, drawing grocery spending into a club format that Kroger does not compete in.

The failed Albertsons merger is not just a financial setback (the $1 billion cost) — it represents a strategic dead end. If Kroger cannot grow through large-scale M&A, its primary growth engine for the past four decades is effectively shut down. Organic growth in grocery — driven mostly by food inflation — runs at 2 to 3 percent annually. That is not enough to excite investors.

Labor cost pressures are intensifying. With major contract negotiations across Arizona, Michigan, and Ohio in 2026, following the Colorado King Soopers strike in early 2025 and union authorization votes in Southern California and Las Vegas, Kroger faces the prospect of higher wages, richer benefits, and potential work stoppages that could disrupt operations and compress margins.

The $2.6 billion Ocado write-down raises questions about management's capital allocation judgment. Kroger bet billions on a technology that did not deliver at scale, and the pivot to lower-cost fulfillment methods, while pragmatic, effectively concedes that the original strategy was wrong. Technology investment requirements continue to grow — AI, supply chain automation, cybersecurity — and each investment carries execution risk that a company operating on sub-2-percent net margins cannot easily absorb.

Porter's Five Forces Analysis

Applying Michael Porter's framework to Kroger's competitive environment:

Threat of new entrants: Moderate. While starting a traditional supermarket chain from scratch is capital-intensive and difficult, non-traditional entrants like Aldi, Lidl, and Amazon have demonstrated that entry is possible through different formats. The barriers are high but not insurmountable.

Bargaining power of suppliers: Low for Kroger. With $147.6 billion in purchasing power and 35 manufacturing plants, Kroger has significant leverage over food suppliers. Large consumer packaged goods companies have some countervailing power through brand strength, but Kroger's private-label capability gives it the ultimate negotiating tool: the ability to replace a supplier's product entirely.

Bargaining power of buyers: High. Grocery shoppers are notoriously price-sensitive and face essentially zero switching costs. There is no contract, no lock-in, and the competitor's store is usually within a few miles. Loyalty programs and fuel points create modest behavioral stickiness, but they do not fundamentally alter the power dynamic.

Threat of substitutes: Growing. Meal kit delivery, restaurant delivery apps, convenience store expansion, and even the rise of prepared foods in non-grocery retailers (think Costco's food court, Trader Joe's prepared meals) all substitute for traditional grocery shopping occasions.

Rivalry among existing competitors: Intense. Walmart, Costco, Aldi, Publix, Albertsons, and numerous regional chains compete aggressively on price, selection, convenience, and increasingly on digital capabilities. The industry is mature, growth rates are low, and market share gains come at someone else's expense.

Hamilton Helmer's 7 Powers Assessment

Applying the 7 Powers framework from Hamilton Helmer provides a more granular view of Kroger's competitive position:

Scale Economies: Moderate. Kroger's $147.6 billion in revenue provides real procurement leverage and fixed-cost absorption across manufacturing, distribution, and technology. But Walmart has 2.5 times the grocery scale, meaning Kroger's scale advantage only operates against smaller competitors, not the market leader.

Network Effects: Weak in traditional grocery. Some emerging network effects exist in retail media — more customer data enables better ad targeting, which attracts more advertisers, which funds more data collection — but these are early-stage and not yet a significant competitive moat.

Counter-Positioning: Moderate. Kroger's deep vertical integration into private-label manufacturing represents a model that national brand companies and pure retailers cannot easily replicate without building their own manufacturing infrastructure. This creates a structural advantage in margin capture.

Switching Costs: Weak. Grocery shoppers can switch stores freely. Loyalty programs and fuel points provide modest behavioral friction, but nothing approaching genuine lock-in.

Branding: Moderate. Simple Truth and Private Selection have meaningful brand equity in their respective categories. But Kroger's store brand is not generally considered premium by consumers in the way that Trader Joe's or Whole Foods brands are.

Cornered Resource: Moderate to Strong. The 84.51 data analytics platform, built on first-party purchase data from 60 million households with 95 percent transaction linkage, is a genuinely unique asset. No competitor except Walmart has comparable data depth, and it would take years and billions of dollars for a new entrant to build something similar.

Process Power: Moderate. Kroger's decades of accumulated expertise in private-label product development, supply chain optimization, and data-driven personalization represent embedded process advantages that are difficult to replicate quickly. The question is whether these processes are durable advantages or simply competencies that competitors will eventually match.

Morningstar rates Kroger as having "No Moat," reflecting the reality that grocery retail is a structurally low-margin, high-competition, low-switching-cost industry where even significant scale does not guarantee durable excess returns. This is a harsh but fair assessment — but it may also be somewhat incomplete. The traditional moat analysis focuses on the grocery business itself, where the absence of switching costs and the intensity of price competition make excess returns difficult to sustain. But Kroger's alternative profit businesses — retail media, data analytics, financial services — operate in fundamentally different economic structures, with higher margins and stronger competitive advantages rooted in proprietary data. The question is whether these businesses will grow large enough relative to the grocery base to change the overall moat assessment. At $1.5 billion in operating profit and growing, they are starting to matter.

Myth vs. Reality

There are several common narratives about Kroger that deserve scrutiny:

Myth: Kroger is just a grocery store competing on price. Reality: Kroger is increasingly a data and media company that uses grocery stores as its customer acquisition and data collection channel. The retail media business generates higher margins than most software companies, and the data analytics capability is a genuine strategic asset.

Myth: The failed Albertsons merger was a catastrophic loss. Reality: The merger would have come with enormous integration risk, significant debt, regulatory conditions, and the challenge of managing 5,000 stores across every U.S. market. The $1 billion cost is painful but not existential for a company generating nearly $5 billion in annual operating profit. The redirected capital into buybacks may ultimately create more shareholder value than the merger would have.

Myth: Amazon will destroy traditional grocery. Reality: Amazon has struggled with grocery more than perhaps any other retail category. The Amazon Fresh expansion has stalled, Whole Foods has not been transformed as dramatically as many predicted, and the core challenge of online grocery — that fresh food is expensive to pick, pack, and deliver, and customers are extremely particular about produce quality — has proven resistant to Amazon's usual technological advantages. This does not mean Amazon is not a threat, but the existential danger to Kroger comes more from Walmart and Aldi than from Amazon.

Key KPIs for Investors

For investors tracking Kroger's ongoing performance, two metrics matter most:

Identical store sales without fuel: This is the single best indicator of Kroger's organic competitive health. It strips out the noise of fuel price volatility, new store openings, and store closures to show whether existing stores are attracting more spending from customers. Growth of 2 to 3 percent is healthy; below 1 percent would signal competitive trouble. Why "without fuel"? Because fuel prices are driven by global commodity markets that have nothing to do with how well Kroger is running its grocery business. A spike in oil prices could inflate total revenue numbers while masking weakness in the core grocery operation — or a collapse in oil prices could make a perfectly healthy grocery business look like it is shrinking. Stripping out fuel gives the clearest view of what is actually happening inside the stores.

FIFO gross margin rate (excluding fuel, rent, and depreciation): This metric reveals the true profitability of Kroger's grocery operations by adjusting for LIFO inventory accounting. A brief explanation is warranted here, because LIFO accounting is one of the most misunderstood elements of grocery company financials. LIFO — Last In, First Out — assumes that the most recently purchased inventory is sold first. During periods of food price inflation, this means that the cost of goods sold on the income statement reflects the highest, most recent prices, which depresses reported profit margins. The actual groceries sitting on Kroger's shelves were likely purchased at lower prices months ago. FIFO — First In, First Out — reverses this, reflecting the actual economic profit more accurately. When Kroger reports "FIFO operating profit," it is showing what the business actually earned from selling groceries at today's prices, regardless of when the inventory was purchased. Improvement in this metric signals that private-label growth, shrink reduction, and operational efficiency are delivering real margin gains.

XI. Power and Strategy Analysis

Kroger's strategic position in 2026 can be understood through the lens of three core capabilities that differentiate it from most competitors, even if none of them individually constitute an impenetrable moat.