Coca-Cola: The Real Thing Behind $300 Billion

I. Introduction & Episode Setup

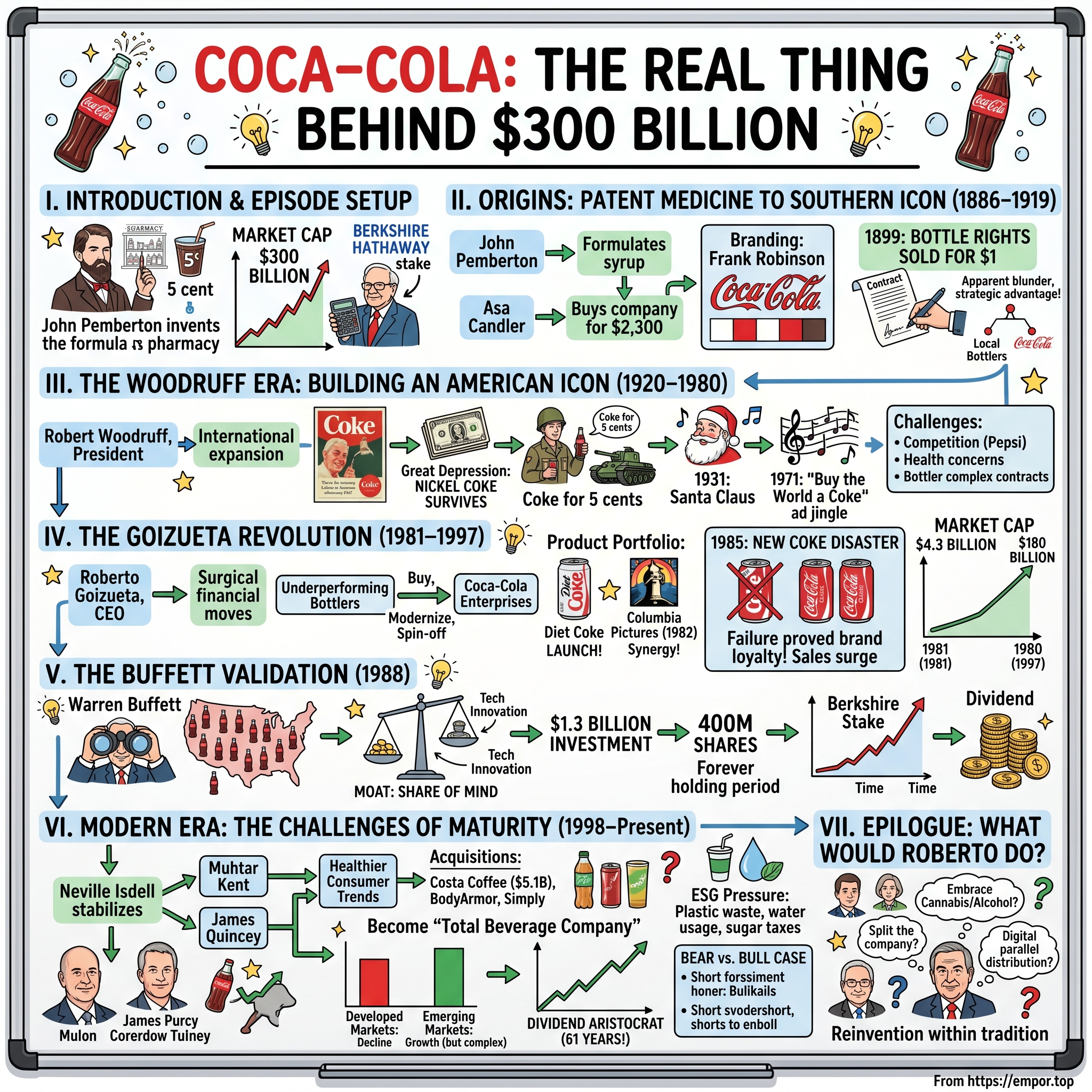

Picture this: It's May 8, 1886, and Jacob's Pharmacy on Peachtree Street in Atlanta is buzzing with its usual afternoon crowd. A Confederate veteran turned pharmacist named John Pemberton shuffles behind the counter, his movements betraying the chronic pain that has haunted him since a saber slashed across his chest at the Battle of Columbus twenty-one years earlier. He reaches for a new syrup he's been perfecting—a caramel-colored concoction he hopes will cure headaches and calm nerves. Little does he know, he's about to pour the first glass of what will become the world's most valuable beverage brand.

Today, that five-cent drink commands a market capitalization hovering around $300 billion, making Coca-Cola one of the most valuable companies on Earth. The beverage that started as a morphine addiction cure in post-Civil War Atlanta now sells 2.2 billion servings daily across more than 200 countries. Warren Buffett's Berkshire Hathaway has held its stake for thirty-five years, collecting nearly $750 million in annual dividends on a $1.3 billion investment. The brand itself is valued at over $100 billion—more than the entire market cap of most Fortune 500 companies.

But here's the question that matters: How did a patent medicine concocted by a wounded veteran transform into the ultimate toll bridge of capitalism? How did sugar water become more valuable than oil wells, tech platforms, or pharmaceutical patents? And perhaps most intriguingly—in an era of health consciousness, regulatory scrutiny, and changing consumer preferences—why does this 138-year-old formula still mint money like it's 1950?

This is the story of three transformations that built modern Coca-Cola. First, how Asa Candler turned a local tonic into a national obsession through the franchise bottling system—a stroke of genius that created aligned incentives across thousands of independent operators. Second, how Roberto Goizueta engineered one of history's greatest corporate turnarounds, growing market cap from $4.3 billion to $180 billion in just sixteen years through financial discipline and portfolio expansion. And third, how Warren Buffett saw value hiding in plain sight after the 1987 crash, making perhaps his greatest investment by recognizing that the market was pricing in 3% growth for a company delivering 7%.

We'll explore the power moves and the mistakes—from the contour bottle that became a design icon to the New Coke disaster that somehow strengthened the brand. We'll dissect the economics of selling syrup at 90% gross margins while others handle the capital-intensive bottling. And we'll examine whether the moat that protected Coca-Cola for over a century can withstand the forces reshaping consumer behavior today.

The roadmap ahead takes us from Reconstruction-era Atlanta to boardrooms in Omaha, from World War II beachheads to TikTok algorithms. It's a story about American capitalism at its most ingenious and most controversial. Because understanding Coca-Cola isn't just about understanding a beverage company—it's about understanding how brands become religions, how distribution creates value, and how the simplest products often build the strongest moats.

II. Origins: Patent Medicine to Southern Icon (1886–1919)

The morphine was supposed to help with the pain, but by 1885, John Stith Pemberton knew he'd traded one demon for another. The Columbus physician had survived that Confederate cavalry saber to the chest at the Battle of Columbus in April 1865—one of the war's final skirmishes—but the laudanum prescribed for his wounds had left him with an addiction that threatened to destroy everything he'd built. His solution? Create a "nerve tonic" that could wean him off opiates while potentially making him rich. He called his first attempt "Pemberton's French Wine Coca," modeled after Vin Mariani, a cocaine-laced wine popular in Europe. But when Atlanta voted for prohibition in November 1885, Pemberton had to pivot fast.

Working in a backyard laboratory at 107 Marietta Street, Pemberton spent months experimenting with a non-alcoholic version. His breakthrough formula combined extracts from coca leaves (yes, the ones that produce cocaine) and kola nuts (providing caffeine), mixed with sugar, caramel for coloring, and a secret blend of oils and spices. On May 8, 1886, he carried a jug of this syrup to Jacob's Pharmacy, where it was mixed with carbonated water and sold for five cents a glass. First-year sales: a underwhelming $50 against $70 in expenses. The genius of the brand, however, came from Pemberton's bookkeeper, Frank Mason Robinson. A methodical man with impeccable penmanship, Robinson understood something fundamental about the emerging consumer economy: presentation mattered as much as product. Robinson suggested the name "Coca-Cola," thinking that "the two Cs would look well in advertising." He experimented in writing out an adaptation of the elaborate Spencerian script, a form of penmanship characteristic of that day. The logo he created—flowing, elegant, instantly memorable—would become arguably the most valuable piece of intellectual property ever designed by a bookkeeper. Consider this: Robinson gave Coca-Cola its red and white colors in 1886. That simple color choice would embed itself so deeply in global culture that seeing red and white together instantly triggers brand recognition across continents.

But Pemberton, increasingly desperate to fund his morphine habit and failing in health, began selling off pieces of his company. By 1888, he'd sold most of his interest to various Atlanta businessmen for roughly $2,300 total—about $75,000 in today's money. The buyer who would matter was Asa Griggs Candler, a fellow pharmacist and shrewd businessman who saw potential where others saw merely another patent medicine. Candler was the anti-Pemberton—a teetotaling Methodist workaholic who viewed business as a moral crusade. He acquired sole ownership of Coca-Cola by 1891 for a total of $2,300—roughly $75,000 in today's dollars. What he bought wasn't just a formula but a barely breathing business. By 1892, Candler's flair for merchandising had boosted sales of Coca-Cola syrup nearly tenfold.

His genius lay in understanding that he wasn't selling a beverage; he was selling an experience. In 1891, when most business owners viewed advertising as wasteful spending, Candler invested $11,000 of his early Coca-Cola profits into marketing—over $300,000 in today's dollars. The typical Atlanta merchant spent less than $100 annually on advertising. Candler distributed free drink coupons—revolutionary in the 1890s—essentially paying people to try his product. He plastered the Coca-Cola logo on calendars, clocks, serving trays, and the sides of buildings. By 1895, he could boast that "Coca-Cola is now drunk in every state and territory in the United States".

But the masterstroke came in 1899, and it happened almost by accident. Two lawyers from Chattanooga, Benjamin Thomas and Joseph Whitehead, approached Candler about bottling Coca-Cola. Candler, who believed the future lay in soda fountains, thought bottling was a dead end. He sold the exclusive bottling rights for one dollar—a decision that cost the company billions in future revenue. Candler believed bottled Coca-Cola would fail. He worried that glass bottles would alter the drink's taste, and that inconsistent carbonation would damage the brand's reputation.

This apparent blunder became Coca-Cola's greatest strategic advantage. Thomas and Whitehead couldn't finance a national bottling operation themselves, so they created a franchise system, contracting with local entrepreneurs to bottle and distribute Coca-Cola in specific territories. They contracted with competent individuals to establish Coca-Cola bottling operations within certain defined geographic areas. Over the next 20 years, the number of plants grew from two to more than 1,000—95 percent of them locally owned and operated

. The fact that these local entrepreneurs had skin in the game aligned incentives perfectly—their success depended entirely on Coca-Cola's success.

In early 1916, a committee composed of bottlers and Company officials met to choose the bottle design. The Root version was the clear winner, marking one of the most important branding decisions in corporate history. The Root Glass Company's patent registration was granted on November 16th, 1915, and the contract called for the bottles to be colored with "German Green" which was later called "Georgia Green" in a patriotic nod during World War I tensions. The weight of glass was to be no less than 14.5 ounces, which when filled with the 6.5 ounces of Coca-Cola meant each bottle weighed more than a pound—a hefty investment for bottlers.

Even though the bottle had gone into production in early 1916, not all bottlers immediately jumped to change out their glass stock. For many bottlers, the glass bottles were the most expensive portion of their business and they needed to be convinced to make the change. The company began to do that with national advertising featuring the exclusive bottle. The first national calendar featuring the bottle appeared in 1918 and by 1920, most of the bottlers were using the distinctive bottle.

The design genius wasn't accidental. Coke wanted a "bottle so distinct that you would recognize it by feel in the dark or lying broken on the ground." Renowned as a design classic and described by noted industrial designer, Raymond Loewy as the "perfect liquid wrapper," the bottle has been celebrated in art, music and advertising. When Andy Warhol wanted a shape to represent mass culture, he drew the bottle—understanding instinctively what Coca-Cola had achieved: democratic luxury.

Then came the watershed moment. Ernest Woodruff leads a syndicate of businessmen to buy The Coca-Cola Company for $25 million. Stock is sold for $40 a share. Son Robert is among the investors. The 1919 transaction wasn't just a sale—it was a transformation from family business to public corporation. In 1919 a consortium of businessmen, headed by Woodruff's father and including Woodruff's friend W. C. Bradley, purchased Coca-Cola for $25 million. By 1913, before the sale, one out of every nine Americans had tried Coca-Cola. The stage was set for something bigger.

III. The Woodruff Era: Building an American Icon (1920–1980)

Soon thereafter, the company's stock value and sales of syrup plunged, in part due to market fluctuations in sugar's price after World War I. A "frail bark struggling upon a tempestuous sea" was how the company's attorney described the business. Vigorous leadership was urgently needed, and with the evidence of Woodruff's meteoric rise before the board, chairman Bradley offered him the job of president in 1923. Woodruff accepted it, though his starting salary of $36,000 represented a $50,000 pay cut. He was thirty-three years old.

Robert Woodruff didn't just run Coca-Cola; he architected a cultural empire. Where his father Ernest saw a financial opportunity, Robert saw something more profound: the chance to sell not just a beverage, but belonging itself. His philosophy was deceptively simple—keep Coca-Cola within "an arm's reach of desire"—but the execution required rethinking everything from distribution to diplomacy.

Woodruff believed Coca-Cola could become an international drink, too. When he became president in 1923, Coca-Cola was only bottled in five countries outside the United States. By 1930, that number had climbed to almost 30. But raw expansion wasn't the goal; cultural infiltration was. Woodruff understood that Coca-Cola couldn't just enter markets—it had to become part of their fabric.

The masterstroke came with his approach to advertising. Rather than selling refreshment, Woodruff sold moments. The company's ads didn't feature product benefits but emotional connections—families gathering, friends celebrating, lovers sharing. By 1929, the company had sold nearly 27 million gallons of syrup, up 150% from 1920, but more importantly, it had sold an idea: that Coca-Cola was essential to the American experience.

Then came the Great Depression, and with it, Woodruff's defining test. While competitors slashed advertising budgets, Woodruff doubled down. He reasoned that when people had little money, small luxuries became more important, not less. A nickel Coke was affordable escapism. The gamble paid off spectacularly—The company weathers the Great Depression with rising profits every year, since "everyone has a nickel" to spend on a Coke.

But World War II transformed Coca-Cola from an American product into American soft power itself. Woodruff's promise was audacious: every American soldier would be able to buy a Coke for five cents, wherever they were stationed, regardless of the cost to the company. Eisenhower himself requested ten bottling plants for troops in North Africa. By war's end, sixty-four bottling plants had been established on every continent except Antarctica, all following American forces.

The tactical genius wasn't just patriotic; it was strategic. These wartime bottling plants became beachheads for peacetime expansion. Local populations who had discovered Coca-Cola through GIs became customers. The infrastructure built for military supply became commercial distribution networks. By the late 1930s, Coca-Cola is a household name and bottling plants are operating in 44 countries.

The cultural campaigns of this era weren't just advertising; they were mythology creation. The 1931 campaign featuring Haddon Sundblom's Santa Claus didn't just promote Coca-Cola—it literally shaped how the world visualizes Christmas. The jolly, red-suited Santa we know today? That's Coca-Cola's Santa, so embedded in culture that few remember its commercial origins. Similarly, the 1971 "I'd Like to Buy the World a Coke" wasn't selling soda; it was positioning Coca-Cola as a force for global harmony during the Vietnam War's darkest days.

Yet the 1970s brought challenges that advertising couldn't solve. The Federal Trade Commission investigated the bottler franchise system as potentially anti-competitive. Environmental groups attacked the company over bottle waste. Sugar prices spiked during the commodity crisis. Health consciousness began its slow emergence. The fortress Woodruff had built was under siege from all sides.

The bottler relationships, once Coca-Cola's greatest strength, became its greatest complexity. The perpetual contracts signed in 1899 and reinforced over decades meant that Coca-Cola couldn't unilaterally change terms, prices, or territories. Bottlers had grown into powerful, often publicly traded companies with their own agendas. What had been a brilliant solution for capital-light expansion had become a structural handicap in a rapidly changing market.

By 1980, as Robert Woodruff's direct influence waned (though he remained on the board), Coca-Cola faced an existential question: Could a company built on nostalgia and tradition adapt to a world that increasingly valued innovation and health? Sales growth was slowing. Pepsi was gaining market share with the "Pepsi Generation" campaign that made Coke seem old. The stage was set for either transformation or decline.

IV. The Goizueta Revolution: Financial Engineering Meets Brand Power (1981–1997)

Roberto Goizueta's appointment as CEO in 1981 was controversial from the start. Mr. Woodruff later handpicks The Coca-Cola Company's next generation of leaders: Roberto C. Goizueta, Chairman, but the board needed convincing. Here was a Cuban immigrant, a chemical engineer who'd spent most of his career in technical roles, chosen to lead America's most iconic brand. The skeptics saw an insider without marketing experience taking over during the company's most challenging period. They couldn't have been more wrong.

Goizueta had fled Cuba in 1960 with his family and $40 in his pocket, leaving behind wealth and status for uncertainty in Miami. That experience—losing everything and rebuilding from nothing—shaped his approach to business. He understood reinvention viscerally. His famous quote, "The world belongs to the discontented," wasn't corporate speak; it was personal philosophy born from revolution and exile.

His first move was radical: he declared that Coca-Cola's mission was to maximize shareholder value, period. This might seem obvious now, but in 1981, it was revolutionary for a company that had long prioritized tradition over returns. Goizueta introduced economic value added (EVA) metrics, demanding that every division earn returns above its cost of capital. Sacred cows were suddenly on the chopping block.

The financial engineering was surgical. Goizueta identified that many bottlers were underperforming assets—family-run operations that had grown complacent under perpetual contracts. His solution was elegant: purchase struggling bottlers, modernize operations, improve performance, then spin them off to Coca-Cola Enterprises, a newly created public company where Coca-Cola retained a 49% stake. This allowed Coca-Cola to influence operations while keeping debt off its balance sheet—having your cake and eating it too.

But Goizueta understood that financial engineering alone wouldn't restore growth. The product portfolio needed revolution. For seventy-eight years, "Coca-Cola" meant one thing. Goizueta changed that. Diet Coke launched in 1982—not as a diet version of Coca-Cola, but as an entirely new formula. The gamble was enormous: cannibalization was certain, but Goizueta bet that market expansion would more than compensate. Within two years, Diet Coke was the third-best-selling soft drink in America.

The Columbia Pictures acquisition in 1982 for $750 million seemed bizarre—what did movies have to do with soda? But Goizueta saw synergies others missed: content for new entertainment-based marketing, product placement opportunities, and most importantly, a hedge against the beverage business's maturation. Critics called it empire building. Goizueta called it portfolio theory.

Then came April 23, 1985—"Black Tuesday" in Coca-Cola lore. The company announced New Coke, reformulated to beat Pepsi in blind taste tests. The backlash was instant and visceral. Psychiatrists likened it to grieving. Protesters staged demonstrations. The company received 400,000 angry calls and letters. Stock dropped 3%. Within seventy-seven days, Goizueta announced the return of "Coca-Cola Classic."

What seemed like disaster became triumph. New Coke's failure paradoxically proved Coca-Cola's cultural power—consumers didn't want a better-tasting cola; they wanted their Coca-Cola. Sales of Coca-Cola Classic surged beyond pre-New Coke levels. Goizueta, whether by design or accident, had orchestrated the greatest brand loyalty demonstration in corporate history. Cynics suggested it was planned; Goizueta famously responded, "We're not that dumb, and we're not that smart."

The numbers under Goizueta's stewardship defy comprehension. Market capitalization grew from $4.3 billion in 1981 to $180 billion by 1997—a 4,086% increase. Stock price increased 3,500%. Return on equity averaged 35%. International operations, which contributed 50% of profits in 1981, reached 80% by 1997. He transformed a mature American beverage company into a global growth machine.

His approach to emerging markets was particularly prescient. While competitors focused on developed economies, Goizueta poured resources into Latin America, Eastern Europe after the Berlin Wall fell, and especially Asia. He understood that selling Coca-Cola in Indonesia or India wasn't about current purchasing power but about establishing presence before prosperity arrived. Plant the flag now, harvest returns later.

The cultural transformation was equally dramatic. Goizueta broke the Southern gentleman's club atmosphere that had defined Coca-Cola since Woodruff. He promoted based on merit, not pedigree. He demanded data-driven decisions in a company that had operated on tradition and intuition. He turned Coca-Cola from a paternalistic employer into a performance-driven meritocracy.

When lung cancer claimed Goizueta on October 18, 1997, just days after he'd attended a board meeting, he left behind more than wealth creation. He'd proven that even the most tradition-bound companies could reinvent themselves. That financial discipline and brand romance weren't mutually exclusive. That an immigrant could run America's most American company and make it more valuable than ever.

V. The Buffett Validation: Value Hiding in Plain Sight (1988)

Warren Buffett's 1988 Coca-Cola investment represents perhaps the purest expression of value investing ever executed—not because it was complex, but because it was so simple that everyone else missed it. After the October 1987 crash dragged Coca-Cola's stock 30% off its highs, the Oracle of Omaha saw what the market couldn't: basic arithmetic.

The setup was perfect Buffett territory. Here was a company he understood completely—he'd been drinking five Cokes a day since childhood. The product hadn't fundamentally changed since 1886. The business model was transparent: sell syrup at 90% gross margins while others handle the capital-intensive bottling. And after the crash, it was statistically cheap.

Buffett's analysis was devastatingly simple. At the prevailing price, applying a 10% discount rate to Coca-Cola's free cash flow implied the market was pricing in just 3% perpetual growth. But worldwide volume was already growing at 7% in 1988. Either Coca-Cola would suddenly stop growing after a century of expansion, or the market was wrong. Buffett bet $1 billion on the latter.

The investment thesis went deeper than numbers. Buffett saw that Coca-Cola possessed what he called "share of mind"—the ultimate moat. In blind taste tests, people might prefer Pepsi, but they bought Coca-Cola. Why? Because Coca-Cola wasn't selling flavored sugar water; it was selling identity, nostalgia, belonging. You can't replicate a century of emotional associations with a Super Bowl ad.

Mr. Woodruff presides over the growth of The Coca-Cola Company, which flourishes under his visionary leadership and high standards for quality and service. The company weathers the Great Depression with rising profits every year, since "everyone has a nickel" to spend on a Coke. By the late 1930s, Coca-Cola is a household name and bottling plants are operating in 44 countries. This foundation, built over decades, was what Buffett was really buying.

The geographic arbitrage opportunity was obvious to anyone who looked. Coca-Cola's per capita consumption in the United States was already 296 eight-ounce servings annually. In Indonesia, it was 4. In China, 1. These weren't mature markets facing decline; they were virgin territories with decades of growth ahead. As Goizueta famously noted, the per capita consumption of water worldwide was 64 ounces daily—Coca-Cola's market share of throat was still minuscule.

Buffett's famous 1988 letter to shareholders explained his thinking with characteristic clarity: "We expect to hold these securities for a long time. In fact, when we own portions of outstanding businesses with outstanding managements, our favorite holding period is forever." This wasn't just quotable wisdom; it was tax strategy. By never selling, Buffett deferred capital gains taxes indefinitely, letting compound interest work its magic undisturbed.

The structure of the investment was crucial. Berkshire invested approximately $1.3 billion between 1988 and 1994, acquiring 400 million shares (split-adjusted). But this wasn't a takeover play or an activist position. Buffett wanted to be a passive investor in a business that didn't need his help. Coca-Cola's management was already excellent under Goizueta. The business model was proven. The brand was unassailable. All Buffett had to do was sit and wait.

What Buffett understood that Wall Street didn't was the power of predictability. Tech stocks might offer higher growth, but they required constant innovation and faced disruption risk. Pharmaceutical companies had patent cliffs. Banks faced credit cycles. But Coca-Cola? People would drink Coca-Cola tomorrow for the same reasons they drank it yesterday. That predictability was worth paying for.

The returns validated everything. By 2020, Berkshire's stake was worth $21.5 billion—a 1,550% return, not including dividends. Speaking of dividends, Berkshire collected $736 million annually by 2020—almost the entire initial investment returned every year. Total return including dividends: 3,534% since 1988. Adjusted for inflation, still over 1,500%. In a world obsessed with disruption, the non-disruptable business won.

But perhaps the most remarkable aspect wasn't the return but the effort required: zero. Buffett didn't need to evaluate new technologies, assess competitive threats, or worry about obsolescence. He didn't attend strategy meetings or suggest operational improvements. He simply collected ever-growing dividend checks while the stake appreciated. It was the platonic ideal of passive investing.

The investment also demonstrated Buffett's evolution as an investor. The younger Buffett, influenced by Benjamin Graham, bought "cigar butts"—cheap companies with one last puff of profit. The mature Buffett, influenced by Charlie Munger, bought wonderful companies at fair prices. Coca-Cola was the full expression of this philosophy: paying up for quality and holding forever.

Critics argued Buffett was late—Coca-Cola had already 100x'd since going public. But Buffett understood that great companies can compound for centuries. The question wasn't whether you'd missed gains but whether gains remained. At 16-18x earnings for a company growing high single digits with infinite duration, Coca-Cola remained mathematically attractive.

The Coca-Cola investment became Buffett's teaching tool, the example he'd return to repeatedly in shareholder letters and speeches. It demonstrated every Buffett principle: circle of competence (consumer products), moat (brand power), management quality (Goizueta), price discipline (post-crash purchase), and patience (holding for 35+ years and counting).

VI. Modern Era: The Challenges of Maturity (1998–Present)

The post-Goizueta era began with a harsh reality check. Roberto's handpicked successor, Doug Ivester, lasted just two years as CEO—a brilliant CFO who couldn't navigate the political and cultural demands of leadership. His replacement, Douglas Daft, an Australian who'd run the Asian business, survived four years but struggled with execution. The message was clear: replacing a legend is nearly impossible.

Then came Neville Isdell in 2004, called out of retirement to stabilize a company that had lost its way. Coca-Cola's stock had gone nowhere for five years. Volume growth was anemic. Pepsi had briefly surpassed Coca-Cola in market cap—unthinkable under Goizueta. The brand that had seemed invincible suddenly looked vulnerable.

The fundamental challenge was structural: how do you grow when you're already everywhere? Coca-Cola products were available in over 200 countries—more than the United Nations has members. The company was selling 1.9 billion servings daily. In developed markets, consumption was plateauing or declining. The easy growth was gone.

Muhtar Kent, who took over in 2008, faced the Great Recession immediately but navigated it well through emerging market strength. His "2020 Vision" aimed to double revenues by 2020. The strategy was portfolio expansion—moving beyond carbonated soft drinks into juices, waters, teas, energy drinks, and even coffee. If throat share was the game, Coca-Cola would compete for every sip.

But by 2017, the chickens came home to roost. Sales fell 11% as consumers, especially millennials, fled sugar. The word "soda" became almost pejorative, associated with obesity, diabetes, and environmental waste. Coca-Cola—once the symbol of American vitality—was increasingly seen as part of the problem, not the solution.

James Quincey, appointed CEO in 2017, represented a new generation of leadership—British, internationally minded, willing to sacred-cow slaughter. His first major move was radical: selling off the bottling operations that Coca-Cola had been reacquiring. The company would return to its asset-light model, focusing on brand and innovation while others handled distribution.

The portfolio transformation accelerated. Major acquisitions included Costa Coffee ($5.1 billion in 2018), giving Coca-Cola a platform in the growing coffee shop market. The company bought or invested in kombucha makers, premium water brands, plant-based beverages, and even alcoholic drinks in select markets. The goal: become a "total beverage company."

But transformation is expensive and dilutive to margins. Healthier beverages typically have lower margins than classic Coca-Cola. Water, even premium water, can't command cola's pricing power. Energy drinks face regulatory scrutiny. Coffee shops require capital investment. The more Coca-Cola diversified, the more it looked like an ordinary consumer goods company rather than the magical syrup seller of old.

Digital transformation presented another challenge. Direct-to-consumer experiments like Coca-Cola's freestyle machines (offering 100+ flavor combinations) generated buzz but limited revenue impact. E-commerce initiatives struggled against the reality that most beverages are impulse purchases at physical retail. Social media engagement was high, but translating likes into sales proved difficult.

ESG (Environmental, Social, Governance) pressures intensified. Coca-Cola produces over 100 billion plastic bottles annually—a environmental nightmare in an increasingly eco-conscious world. The company pledged to collect and recycle a bottle for every one sold by 2030, but critics called it greenwashing. Water usage in water-stressed regions drew protests. Sugar taxes spread from Mexico to Philadelphia, explicitly targeting Coca-Cola's core products.

Competition evolved beyond traditional rivals. Energy drink companies like Red Bull and Monster created entirely new categories. Craft sodas appealed to premium consumers. Private label gained share during recessions. Tech companies entered beverages—Amazon bought Whole Foods; Google invested in vending technology. The competitive moat that seemed impregnable was under assault from all angles.

International expansion, long Coca-Cola's growth engine, faced headwinds. China, the great hope, proved complex—local competitors understood consumer preferences better. India remained price-sensitive. Russia and Eastern Europe faced geopolitical tensions. Latin America, historically strong, struggled with economic instability. The easy emerging market gains were harvested.

Yet the company showed resilience. Despite all challenges, Coca-Cola maintained its dividend aristocrat status, raising dividends for 61 consecutive years. The brand value, estimated at over $100 billion, remained in the global top five. Market cap stayed above $250 billion. The business still generated enormous cash flow—over $10 billion annually.

The current strategy under Quincey focuses on premiumization and "occasion-based" marketing. Instead of pushing volume, Coca-Cola wants to capture higher-value moments—the craft cocktail mixer, the premium coffee break, the post-workout recovery drink. It's a tacit admission that the days of democratic, universal consumption are over. The future is fragmented, premium, and purposeful.

Recent initiatives show both promise and peril. Coca-Cola Zero Sugar is growing double digits, suggesting successful reformulation. The Simply and Innocent juice brands command premium prices. BodyArmor sports drinks compete with Gatorade. But for every success, there's a failure—Odwalla shut down, Zico coconut water divested, Tab discontinued. The hit rate on innovation remains frustratingly low.

VII. The Playbook: Timeless Lessons

The Power of the Toll Bridge

Coca-Cola's greatest insight wasn't about beverages—it was about distribution. By controlling the syrup formula while franchising bottling and distribution, the company created the ultimate toll bridge. Every Coca-Cola sold anywhere generates a royalty-like return to Atlanta. No capital investment, no operational risk, just a percentage of every transaction. It's the business equivalent of owning the only bridge across a river—you don't need to maintain the vehicles or employ the drivers; you just collect tolls.

The genius deepens when you consider the incentive alignment. Bottlers invest their own capital in trucks, warehouses, and sales forces. They fight for shelf space, manage retail relationships, and handle returns. Their success depends entirely on selling more Coca-Cola. Meanwhile, the company focuses on what it does best: brand building and product innovation. It's division of labor at its most elegant.

Brand as Religion

Coca-Cola understood before anyone that brands aren't about products—they're about identity. The company doesn't sell beverages; it sells belonging. Every marketing campaign, from Santa Claus to "Share a Coke," reinforces the same message: Coca-Cola is how humans connect. This emotional architecture, built over 138 years, creates switching costs that have nothing to do with taste or price.

Consider the New Coke debacle through this lens. Consumers didn't reject a formula change; they rejected identity change. Coca-Cola had become so embedded in personal history—first dates, family gatherings, childhood memories—that altering it felt like betrayal. The company had achieved the ultimate marketing goal: making its product inseparable from customers' life stories.

Scale Economics Shared

The bottler franchise system represents one of history's great business model innovations. By sharing economics with bottlers—giving them exclusive territories and perpetual contracts—Coca-Cola created thousands of zealous partners. Each bottler became a local advocate, investing their own money to build the brand in their market. The company achieved global scale without global capital.

This model also created competitive advantages beyond capital efficiency. Local bottlers understood their markets intimately—which stores mattered, which events to sponsor, which flavors would resonate. They could respond to competitive threats immediately without waiting for corporate approval. Pepsi, trying to compete with centralized operations, couldn't match this local responsiveness.

Capital Light, Cash Heavy

The concentrate model is financially beautiful. Gross margins exceed 60%. Return on invested capital approaches infinity—you can't calculate ROIC when you have no IC. The company needs minimal working capital, no heavy machinery, and few employees relative to revenue. It's the anti-industrial business: no factories, no inventory, no depreciation.

This capital efficiency enables extraordinary shareholder returns. Without reinvestment needs, virtually all profit can be returned via dividends and buybacks. The company has raised its dividend for 61 consecutive years not through heroic effort but through business model design. When your product is flavored syrup selling at 100x production cost, generating cash is inevitable.

Geographic Arbitrage

Coca-Cola mastered the art of exporting culture profitably. The product sold in Tokyo is identical to what's sold in Toledo, yet it commands premium pricing abroad as an "American" experience. This geographic arbitrage—selling American-ness to non-Americans—generates higher margins internationally than domestically.

The company understood that globalization wasn't just about market access but about cultural transmission. Every Coca-Cola sold in China or India carries with it associations of modernity, prosperity, and Western lifestyle. The company wasn't just entering markets; it was selling admission to a global consumer culture. The fact that this culture was largely Coca-Cola's creation only deepens the competitive advantage.

Management Matters

The contrast between the Woodruff era and the Goizueta era proves that even the best businesses need great management. Woodruff built the emotional and physical infrastructure—the brand love and bottler network. Goizueta added financial discipline and portfolio expansion. Each era's success required different skills, proving that leadership isn't one-size-fits-all.

The failures matter too. Post-Goizueta CEOs struggled not because they were incompetent but because they couldn't match his unique combination of vision and execution. Great businesses can survive mediocre management temporarily, but they can't thrive without great leadership. The CEO matters, even in businesses with massive moats.

Patient Capital

Buffett's Coca-Cola investment demonstrates the power of patience in a world obsessed with quarterly earnings. By holding for 35+ years, Buffett let compound interest work its magic. The dividend income alone now exceeds his initial investment. This isn't just buy-and-hold; it's buy-and-hold-forever—a strategy only possible with truly great businesses.

The patience extends beyond holding periods to business evaluation. Buffett didn't need Coca-Cola to innovate or disrupt or transform. He needed it to keep doing what it had done for a century: sell more sugar water at high margins. Sometimes the best investment thesis is the absence of a thesis—betting that tomorrow will look like today.

Reinvention Within Tradition

Diet Coke's success versus New Coke's failure teaches a crucial lesson about innovation in traditional companies. Diet Coke worked because it extended the brand without replacing it. New Coke failed because it tried to replace the irreplaceable. The lesson: innovate around the core, not through it.

This principle guides Coca-Cola today. Zero Sugar extends the original formula for health-conscious consumers. Mini cans offer portion control without abandoning the product. Premium mixers target cocktail culture. Each innovation respects the core while expanding the franchise. It's evolution, not revolution—exactly what century-old brands require.

VIII. Bear vs. Bull: The $300B Question

Bull Case: The Eternal Spring

The bulls start with a simple observation: people have predicted Coca-Cola's demise for fifty years, yet the company keeps growing. Every generation discovers health consciousness anew, yet Coca-Cola adapts and survives. The brand that survived two world wars, the Great Depression, and countless health scares won't be killed by kombucha and kale.

The math remains compelling. Current per capita consumption outside the United States is still a fraction of American levels. If China reaches just 25% of U.S. consumption, that's billions in incremental revenue. India, Indonesia, and Africa represent decades of growth. The company doesn't need new products—it needs existing products to reach new people.

Portfolio diversification is working, albeit slowly. Costa Coffee provides a platform for competing with Starbucks. Energy drinks through Monster partnership capture younger consumers. Premium waters and enhanced hydration target wellness trends. The company is transforming from a soda company to a beverage portfolio, just as it transformed from a fountain drink to a global brand.

Pricing power remains intact, perhaps the most crucial bull argument. Despite all challenges, Coca-Cola can still raise prices faster than inflation. The brand commands premium pricing globally. Even as volumes face pressure, revenue grows through mix and pricing. This pricing power—the ability to charge more for essentially the same product—is the hallmark of a great business.

The distribution network represents an unreplicable asset. Coca-Cola products reach places that roads don't. The company's route to market, refined over a century, can't be replicated by startups or even large competitors. This distribution moat matters more as e-commerce proves inadequate for impulse beverage purchases.

Finally, bulls point to management's newfound realism. The company is rationalizing its portfolio, shedding underperforming brands, and focusing resources on winners. The refranchising of bottlers improves returns on capital. Cost discipline is increasing. This isn't the growth-at-any-cost mentality that characterized the early 2000s—it's mature management for a mature business.

Bear Case: The Slow Decline

Bears see structural, not cyclical, challenges. Sugar consumption is declining in developed markets and will eventually decline everywhere. Health consciousness isn't a fad—it's a generational shift. Parents who won't let their children drink Coca-Cola raise adults who won't drink it either. The product that defined the 20th century may be incompatible with the 21st.

The numbers support bear concerns. Volume growth is essentially flat in developed markets. Pricing power masks unit decline. The company talks about "occasions" and "transactions" to avoid discussing servings. Financial engineering—buybacks, refranchising, cost cuts—maintains EPS growth while the business stagnates.

Private label is gaining share, especially during economic downturns. Store brands now match Coca-Cola's quality at half the price. Young consumers, lacking brand loyalty, buy on price. The emotional moat that protected Coca-Cola for a century means nothing to algorithmic shopping and price-comparison apps.

Regulatory risks are multiplying. Sugar taxes spread globally, explicitly targeting Coca-Cola's core products. Plastic bans threaten the package format. Water usage regulations impact production. ESG investing excludes sugar and plastic producers. The regulatory environment that enabled Coca-Cola's rise now threatens its future.

Competition is more intense than ever. Energy drinks cannibalize soda consumption. Coffee culture reduces afternoon Coke occasions. Craft beverages appeal to premium consumers. Cannabis beverages loom as potential disruptors. The competitive landscape is fragmenting, and Coca-Cola can't win every battle.

Most fundamentally, bears question the growth algorithm. Emerging markets aren't developing as expected. China prefers tea. India remains price-sensitive. Africa lacks infrastructure. The billions of new consumers that bulls expect may never materialize, or may materialize too slowly to offset developed market declines.

The Verdict

The truth, as always, lies between extremes. Coca-Cola isn't disappearing, but it's not dominating either. The company will likely muddle through—growing slowly, returning cash to shareholders, gradually transforming its portfolio. It's not a disaster, but it's not a triumph. It's maturity.

The valuation reflects this reality. At roughly 25x earnings, Coca-Cola trades at a premium to the market despite growing slower. The market is paying for safety and dividends, not growth. It's a bond substitute in equity form—appropriate for a business that's more about preservation than expansion.

IX. Power & Counter-Positioning Analysis

Applying Hamilton Helmer's Seven Powers framework to Coca-Cola reveals both enduring strengths and emerging vulnerabilities.

Scale Economies—Coca-Cola's global scale enables advertising spending that no competitor can match. A Super Bowl ad's cost spreads across billions of servings. This scale advantage is real but diminishing as advertising fragments across digital channels where scale matters less.

Network Effects—Surprisingly weak. Drinking Coca-Cola doesn't become more valuable as others drink it. Unlike platform businesses, consumption is independent. The social aspects—sharing Coke moments—are marketing constructs, not network effects.

Switching Costs—Emotional, not economic. The cost of switching from Coca-Cola to Pepsi is zero dollars but considerable psychic pain for loyal consumers. These emotional switching costs are Coca-Cola's true moat, though they're weakening generationally.

Branding—The ultimate power. Coca-Cola can charge more for sugar water than anyone else because of accumulated brand equity. This power persists but faces pressure as consumers increasingly buy on health attributes rather than brand affinity.

Cornered Resource—The secret formula is theater. The real cornered resource is the distribution network—the trucks, relationships, and shelf space accumulated over a century. This physical network is Coca-Cola's least appreciated but most durable advantage.

Process Power—Limited. Coca-Cola's processes aren't significantly better than competitors'. The company doesn't manufacture more efficiently or innovate faster. What operational advantages exist come from scale, not superior processes.

Counter-Positioning—Coca-Cola is the positioned-against, not the positioner. Craft sodas counter-position against Coca-Cola's mass market approach. Health beverages counter-position against sugar content. The company that once defined the category now defends against insurgents.

The framework reveals an important truth: Coca-Cola's powers are defensive, not offensive. The company protects existing advantages rather than creating new ones. In a static world, these defensive powers would suffice. In a dynamic world, they may not.

X. Epilogue: What Would Roberto Do?

If Roberto Goizueta were resurrected to run Coca-Cola today, what would he do? The question isn't academic—it illuminates what radical leadership might accomplish even in mature businesses.

Goizueta would likely start with portfolio surgery far more dramatic than current management contemplates. He'd recognize that trying to compete in every beverage category dilutes focus and returns. Better to dominate three categories than participate in thirty. He'd probably divest everything except carbonated soft drinks, coffee, and perhaps energy drinks—the categories with true pricing power.

He'd restructure the bottler system again, but more radically. The current franchise model, designed for physical retail, doesn't work for digital commerce. Goizueta might create a parallel distribution system for direct-to-consumer, subscription, and personalization—areas where traditional bottlers can't compete.

On products, Goizueta would embrace cannabis and alcohol, regulations permitting. These are the new "nerve tonics," the socially acceptable drugs that Coca-Cola originally was. The company that started with cocaine and pivoted to caffeine would pivot again to whatever mild intoxicants society permits.

Most radically, Goizueta might split the company. One entity would milk the traditional business—maximizing cash flow from carbonated soft drinks in developed markets. Another would pursue growth—investing aggressively in emerging markets and new categories. This would resolve the current strategic schizophrenia where one company tries to simultaneously harvest and invest.

But even Goizueta might struggle with the fundamental question: Can a company built on sugar thrive in a world rejecting sugar? Can a brand synonymous with indulgence succeed when indulgence is sin? Can American cultural exports maintain premium pricing as American culture loses global cachet?

The platform versus product debate is particularly relevant. Modern tech giants are platforms—they enable others to create value. Coca-Cola is pure product—it creates and captures value directly. In a world where platforms dominate, product companies look antiquated. Should Coca-Cola become the iOS of beverages, enabling others to build on its distribution?

The answer may be that Coca-Cola represents a business model perfected for the 20th century but increasingly obsolete in the 21st. The company succeeded by mass manufacturing identity—making everyone feel special by consuming the same thing. But modern consumers want genuine uniqueness, not manufactured community. They want their beverages, like their media, personalized and on-demand.

Yet perhaps this obsolescence is overstated. Humans haven't fundamentally changed. We still crave sweetness, still seek community, still respond to symbols. Coca-Cola provides all three in a shelf-stable, globally available format. The delivery mechanism may be dated, but the human needs are eternal.

Can mature companies grow forever? Coca-Cola suggests yes, but with caveats. Growth slows from exponential to linear to marginal. The business becomes a utility—essential but unexciting, profitable but not transformational. Investors seeking 10x returns should look elsewhere. Those seeking 10% returns for decades might find exactly what they're looking for.

The final lesson may be the most important: Great businesses aren't great forever, but they can be good for longer than anyone expects. Coca-Cola will likely never again be the growth machine it was under Goizueta or the cultural force it was under Woodruff. But it will probably still be selling sugar water profitably long after its critics have moved on to predicting other companies' demises.

In the end, Coca-Cola's story is capitalism's story—the triumph of mass production, the power of marketing, the challenges of maturity, and the eternal tension between tradition and innovation. It's a story without a clear ending because the company, like capitalism itself, keeps adapting just enough to survive. Whether that's triumph or tragedy depends on your perspective. What's certain is that it's profitable, and in business, that's often enough.

XI. Recent News

The company's most recent developments reflect both the challenges and opportunities facing this 138-year-old giant. In 2024, Coca-Cola announced a partnership with Bacardi to launch ready-to-drink cocktails, marking its most serious entry into alcohol since Prohibition forced Pemberton to reformulate. The move signals recognition that growth requires entering categories previously considered off-limits.

The company's venture into AI-generated flavors with "Y3000" showed both innovation and desperation—using algorithms to create a "futuristic" taste that reviewers described as "confusing" and "unnecessarily complex." The experiment highlighted a crucial tension: Coca-Cola's strength is timeless simplicity, not technological complexity.

Environmental initiatives accelerated with the announcement of paper bottles in limited European trials. Whether consumers will accept Coca-Cola in anything but its iconic packaging remains uncertain. The company seems caught between environmental necessity and brand identity—a microcosm of its larger challenges.

Most tellingly, recent earnings calls focus increasingly on "revenue growth management"—corporate speak for price increases. With volumes flat, pricing is the only growth lever. But how long can you raise prices on sugar water before consumers revolt? The answer may determine Coca-Cola's next century.

XII. Links & Further Reading

For those seeking deeper understanding, several resources prove invaluable:

"For God, Country, and Coca-Cola" by Mark Pendergrast remains the definitive history, combining exhaustive research with readable narrative. Pendergrast had unprecedented access to company archives and interviews with key figures, creating a comprehensive chronicle of Coca-Cola's first century.

Roberto Goizueta's speeches and shareholder letters from 1981-1997 offer masterclasses in strategic thinking. His 1996 speech "The World Belongs to the Discontented" should be required reading for any executive facing transformation challenges.

Warren Buffett's annual letters discussing Coca-Cola, particularly from 1988-1992, demonstrate how great investors think about great businesses. His explanation of "share of mind" and economic moats uses Coca-Cola as the prime example.

The Coca-Cola Company's own archives, partially digitized, provide primary sources including early advertising, bottler contracts, and internal memos that shaped strategy. The 1899 bottling contract, available online, shows how simple agreements can have century-long implications.

For contemporary analysis, industry publications like Beverage Digest provide real-time coverage of market share shifts, product launches, and strategic pivots. Their annual fact books contain data on consumption patterns, pricing trends, and competitive dynamics.

Academic studies on brand equity frequently use Coca-Cola as their subject, offering rigorous analysis of how emotional connections translate to pricing power. The Harvard Business School case studies on New Coke and Diet Coke remain exemplary examinations of innovation in mature companies.

Finally, visiting the World of Coca-Cola museum in Atlanta, while obviously corporate propaganda, provides visceral understanding of the brand's cultural impact. Seeing visitors from every continent taking photos with Coca-Cola artifacts demonstrates a moat that no financial analysis fully captures.

The story of Coca-Cola is far from over. Whether the next chapter is renaissance or decline remains unwritten. What's certain is that few companies have provided richer lessons in strategy, marketing, and the nature of competitive advantage. For students of business, Coca-Cola remains essential curriculum—a case study in how simple products can build complex moats, how tradition and innovation must balance, and how even the greatest franchises face mortality.

The real thing, it turns out, isn't the formula locked in an Atlanta vault. It's the ongoing experiment in corporate longevity, the daily test of whether a 19th-century product can thrive in the 21st century. That experiment continues, one serving at a time, 2.2 billion times per day, in every country on Earth except North Korea and Cuba—a testament to capitalism's reach and a reminder that no moat, however wide, is forever.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube