Knight-Swift: The Consolidation of the American Highway

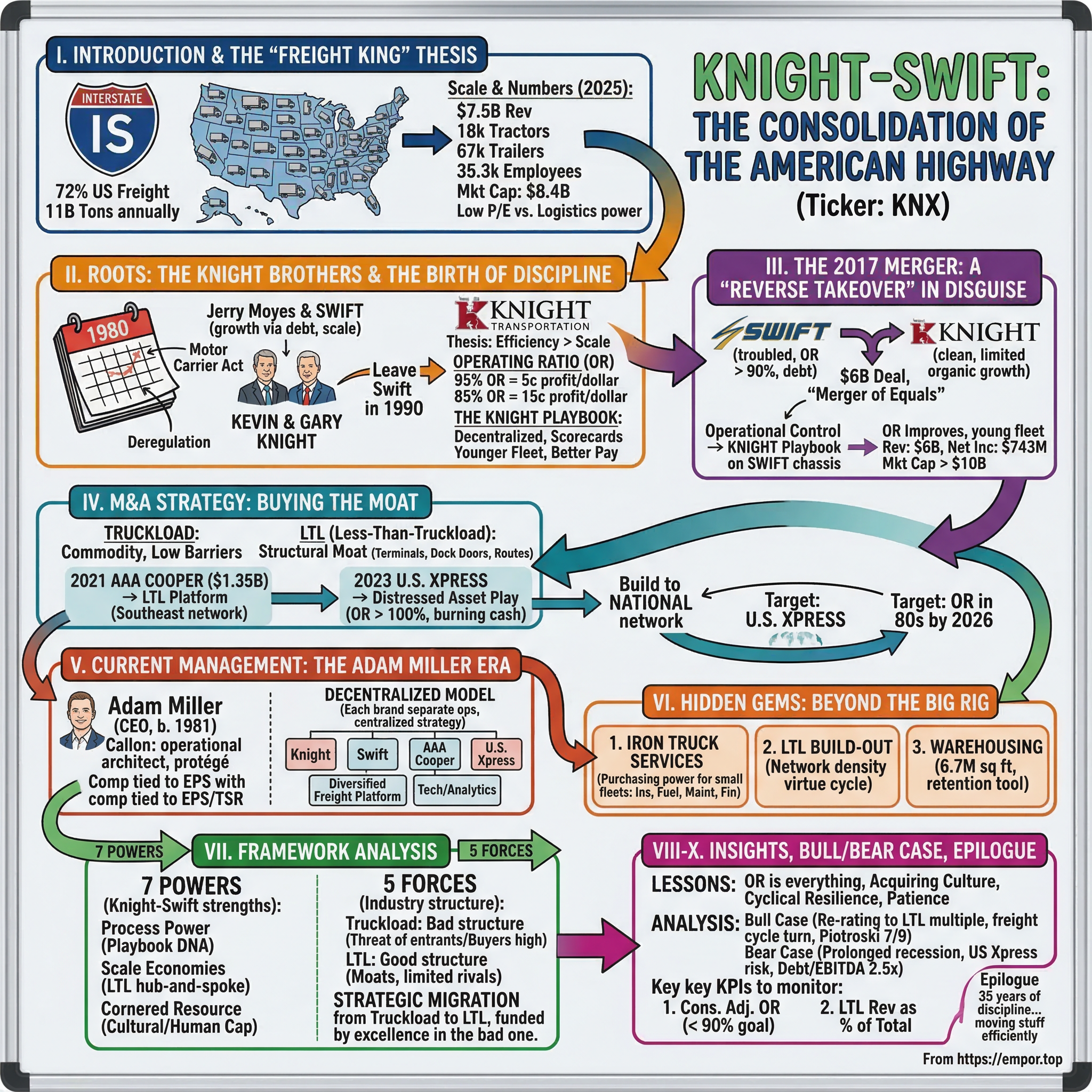

I. Introduction and The "Freight King" Thesis

Picture Interstate 10 stretching from Phoenix toward the California border. It is six lanes of blacktop shimmering in the desert heat, and every third vehicle is a tractor-trailer. Some carry Amazon boxes, others haul lettuce from Yuma, a few flatbeds are loaded with steel beams for a housing development in Tempe. Now zoom out. Across the entire continental United States, roughly 72 percent of all freight by weight moves on a truck. That is eleven billion tons every year. And sitting atop this colossal industry, directing more trucks than any other company in North America, is Knight-Swift Transportation Holdings.

The numbers alone tell a striking story. Knight-Swift generated nearly $7.5 billion in revenue in 2025, operates more than 18,000 tractors and 67,000 trailers, and employs 35,300 people across the United States, Mexico, and Canada. Its market capitalization hovers around $8.4 billion. Yet for all that scale, the company's stock trades at a valuation that would make many growth investors yawn. Its price-to-earnings multiple looks more like a regional bank than a logistics powerhouse. The question that makes Knight-Swift one of the most interesting stories in American industry is whether this is a company perpetually trapped in the commodity grind of trucking or whether it is quietly assembling something far more durable, something with real competitive moats, hiding in plain sight beneath the rumble of diesel engines.

The answer requires understanding a family saga, a once-in-a-generation merger, and a playbook for acquiring and fixing broken trucking companies that has no parallel in the industry. Knight-Swift did not become the dominant force on the American highway through luck or timing. It got there through an almost pathological obsession with a single metric, the operating ratio, and by applying that obsession with surgical discipline across every acquisition it touched.

This is the story of how two brothers from Arizona left their cousin's trucking empire to build something better, how they engineered a merger that doubled their scale overnight, how they bought their way into entirely new markets, and how a new generation of leadership is now trying to transform a trucking company into something the industry has never quite seen before. It is a story about the unsexy economics of moving stuff from point A to point B, and why, if you look closely enough, those economics might be more powerful than anyone gives them credit for.

II. Roots: The Knight Brothers and the Birth of Discipline

The modern trucking industry was born on July 1, 1980, the day President Jimmy Carter signed the Motor Carrier Act into law. Before that date, trucking in America operated like a regulated utility. The Interstate Commerce Commission controlled which companies could haul freight, on which routes, and at what prices. Carriers held "operating authorities" like medieval land grants, and new entrants were effectively locked out. The result was an industry of comfortable incumbents charging high prices with little incentive to innovate.

Deregulation changed everything overnight. Thousands of new carriers flooded the market. Rates collapsed. Many of the old-guard companies, bloated from decades of regulatory protection, went bankrupt. But for entrepreneurs willing to start lean and compete on cost, it was a gold rush. One of the companies that had already established itself in this new world was Swift Transportation, founded in Phoenix by Jerry Moyes in the early 1960s and turbo-charged by deregulation into one of America's largest truckload carriers. Moyes built Swift through aggressive growth, leveraging debt to buy trucks and terminals, always chasing the next increment of scale. By the late 1980s, Swift was hauling freight from coast to coast.

Working inside that Swift machine were two young men who happened to be Jerry Moyes's cousins: Kevin Knight, born in 1957, and Gary Knight, born in 1952. They learned the trucking business from the inside, watching Moyes build his empire through sheer velocity of expansion. But the Knight brothers saw something that troubled them. Swift was getting bigger, but was it getting better? Operating margins were thin. The fleet was aging. Driver turnover, the trucking industry's chronic disease, was astronomical. The culture was "move more freight," and the financial discipline required to actually make money doing it was a secondary concern.

In 1990, Kevin and Gary Knight made the decision that would define their careers. They left Swift to start their own company, Knight Transportation, with just a handful of trucks in Phoenix. The founding thesis was deceptively simple: instead of chasing scale at all costs, they would chase efficiency. In an industry where the Operating Ratio, the percentage of revenue consumed by operating expenses, was the only number that truly mattered, the Knights would obsess over pennies.

Think of the Operating Ratio as trucking's version of a batting average. A 95 percent OR means that for every dollar of revenue, ninety-five cents goes to costs, and only five cents drops to the operating line. An 85 percent OR means fifteen cents of operating profit per dollar. In an industry moving billions of dollars, that ten-point difference is the gap between a dominant company and one fighting for survival. The Knight brothers understood this intuitively. They ran their terminals like independent profit centers, each one with its own scorecard, its own targets, its own accountability. They invested in newer trucks, knowing that a two-year-old tractor burns less fuel and needs fewer repairs than a seven-year-old one. They paid drivers slightly better, understanding that the real cost of turnover, recruiting, training, lost productivity, dwarfed the cost of a modest raise.

Knight Transportation went public in 1994, and over the next two decades, it developed a reputation as perhaps the best-run truckload carrier in America. While peers swung wildly with the freight cycle, Knight delivered consistent, industry-leading operating ratios in the low-to-mid 80s. It was not the biggest. Swift, Werner, J.B. Hunt, and Schneider all ran larger fleets. But Knight was arguably the most profitable per truck, per mile, per dollar of capital deployed. The "Knight Playbook," as it came to be known on Wall Street, was a proprietary management system built on decentralized decision-making, relentless cost tracking, and a culture that treated every terminal manager like a small-business owner.

The irony was not lost on anyone. The Knight brothers had left Swift because they believed bigger was not necessarily better. They built a company that proved the point. But as the 2010s unfolded, a new question emerged. Knight had perfection, but it was running out of room to grow organically in a truckload market that was consolidating rapidly. And Swift, the company they had left behind, was in trouble. The stage was being set for one of the most unlikely reunions in American business.

III. The 2017 Merger: A "Reverse Takeover" in Disguise

By 2016, Swift Transportation was a company at war with itself. It was still the largest truckload carrier in North America, generating roughly $3.7 billion in revenue, with dedicated trucking, refrigerated, and intermodal segments sprawling across the continent. But beneath the scale was a mess. Years of debt-fueled expansion had left the balance sheet strained. The operating ratio had crept above 90 percent, dangerously close to the breakeven line in a cyclical downturn. Driver retention was poor. Technology investments had been sporadic. And the Moyes family, which still controlled the company, was dealing with its own complicated dynamics, including Jerry Moyes's involvement with the Arizona Coyotes NHL team and various legal and financial entanglements.

Knight Transportation, by contrast, was a jewel, but a small one. It generated about $1.1 billion in revenue from Knight Trucking and another $234 million from its logistics brokerage arm. Its operating ratio was consistently among the best in the industry. Its balance sheet was clean. Its management bench was deep. But at roughly one-third the size of Swift, Knight's organic growth options were limited. The truckload market was fiercely competitive, with low barriers to entry and razor-thin margins for the average carrier. To build real scale, Knight needed a transformative deal.

The announcement came on April 9, 2017. Knight Transportation and Swift Transportation would merge in a deal valued at approximately $6 billion, creating the largest truckload carrier in North America. On paper, it was structured as a "merger of equals." In practice, it was something closer to a reverse takeover. The Knight family and Knight management would take operational control of the combined entity. Kevin Knight became Executive Chairman. Adam Miller, Knight's longtime CFO who had been with the company for over a decade, was positioned as the operational architect of the integration. The new company would be headquartered in Phoenix, Knight's home turf. The message was clear: this was the Knight Playbook being installed on the Swift chassis.

What happened next was a case study in operational transformation. The Knight management team fanned out across Swift's sprawling network of terminals and began applying their decentralized, scorecard-driven approach. Each terminal was given clear targets for revenue per truck, cost per mile, and driver utilization. Underperforming assets were parked or sold. The fleet was gradually refreshed. The combined company's average tractor age dropped to roughly 2.6 years, one of the youngest in the industry, because newer trucks mean better fuel efficiency, lower maintenance costs, and happier drivers.

The financial results were dramatic. In the first full year after the merger closed in September 2017, the combined company reported roughly $5.1 billion in revenue with improving margins. By 2021, revenue had climbed to $6.0 billion, and the company earned $743 million in net income, an extraordinary figure for a truckload carrier. The market cap, which had been roughly $5 billion combined at the time of the merger announcement, surged past $10 billion by late 2021. The Knight brothers had essentially doubled their shareholders' money not by discovering a new market or inventing a new technology, but by "fixing the plumbing," by taking a bloated, undermanaged operation and imposing the discipline they had spent three decades perfecting.

The merger also revealed something important about the Knight Playbook that would become central to the company's future strategy. It was not just a set of management practices. It was a transferable operating system. The Knight brothers had demonstrated that their approach to running a trucking company could be lifted out of their original small operation and installed in a much larger, more complex organization. This insight, that operational excellence was not size-dependent but culture-dependent, would become the intellectual foundation for everything Knight-Swift did next.

The stock market took notice. Investors who had valued Knight and Swift separately as two mid-cap trucking companies began to see the combined entity differently. This was not just a bigger trucking company. It was a platform, a machine for acquiring underperforming assets and extracting value through operational discipline. The question was no longer whether the Knight Playbook worked. The question was: where would they deploy it next?

IV. M&A Strategy: Buying the Moat

To understand Knight-Swift's acquisition strategy, you first need to understand a fundamental truth about the American freight market. Truckload, the business of filling an entire 53-foot trailer and driving it from origin to destination, is a commodity. There are hundreds of thousands of truckload carriers in the United States, from one-truck owner-operators to mega-fleets like Knight-Swift. Barriers to entry are essentially a CDL license, a truck, and a willingness to drive. This means pricing power is limited, margins are thin, and cycles are brutal. When the economy booms, trucks are scarce and rates spike. When it slows, capacity floods the market and rates crater.

Less-Than-Truckload, or LTL, is an entirely different animal. LTL carriers handle smaller shipments, typically between 150 and 10,000 pounds, consolidating freight from multiple shippers onto shared trailers. To do this efficiently, you need something truckload carriers do not: a network of physical terminals. Think of an LTL network like a hub-and-spoke airline system. Freight arrives at a local terminal, gets sorted and consolidated, moves on linehaul trucks to regional or national hubs, gets broken down and re-sorted, and goes out for local delivery. Building this network requires massive upfront capital investment in real estate, equipment, and technology. You cannot start an LTL company with one truck and a dream. You need hundreds of terminals, thousands of dock doors, and decades of network optimization.

This structural difference creates a profound competitive moat. The top LTL carriers, companies like Old Dominion Freight Line, which commands a nearly $38 billion market capitalization, and Saia, valued at roughly $8.6 billion, trade at dramatically higher multiples than truckload carriers. Old Dominion trades at a premium that reflects its pristine operating ratio in the low 70s and its essentially unassailable network position. The market is telling you something: LTL is a better business than truckload, full stop.

Knight-Swift's leadership understood this, and in July 2021, they made the move. The company announced the acquisition of AAA Cooper Transportation for approximately $1.35 billion. AAA Cooper was a regional LTL carrier based in Dothan, Alabama, with a network concentrated in the southeastern United States. It was a well-run company with a solid reputation, roughly $1.3 billion in annual revenue, and a clean operational profile. At approximately 9.6 times EBITDA, the purchase price was fair by LTL standards but not cheap. The critical point was what Knight-Swift was buying: not just a trucking company, but a terminal network. Real estate. Dock doors. Established pickup-and-delivery routes. Customer relationships built over decades. These were assets that could not be replicated without years and billions of dollars of investment.

The strategic vision was ambitious. Knight-Swift would use AAA Cooper as a platform, the LTL equivalent of what Swift had been in the truckload world, and build it into a national network. The 2021 acquisition gave them the Southeast. The plan was to expand organically and through tuck-in acquisitions to achieve coast-to-coast coverage, directly challenging incumbents like Old Dominion and Saia. By 2026, management's stated goal was to have a unified national LTL network operating under the AAA Cooper brand.

Then came the second major deal. In 2023, Knight-Swift acquired U.S. Xpress Enterprises, a struggling truckload carrier that was the quintessential distressed asset play. U.S. Xpress had been losing money, with an operating ratio above 100 percent, meaning it was spending more than a dollar for every dollar of revenue it brought in. The company was essentially burning cash. Knight-Swift paid a 310 percent premium on U.S. Xpress's beaten-down stock price, which sounds alarming until you look at the math differently. On a forward EBITDA basis, the price worked out to roughly 5 to 6 times, a bargain if the Knight Playbook could bring U.S. Xpress's operating ratio down to something sustainable. Management's target was to get U.S. Xpress into the 80s by 2026, a transformation that would require the same kind of terminal-by-terminal, driver-by-driver overhaul that had worked at Swift.

What emerges from these deals is a coherent capital deployment philosophy that some analysts have compared to Berkshire Hathaway's approach. Knight-Swift generates steady, if cyclically variable, cash flow from its core truckload business, roughly $1.3 billion in operating cash flow in 2025. It then deploys that cash into acquisitions that either buy it into structurally better businesses (LTL) or buy it distressed assets in its existing business that can be fixed through operational discipline (U.S. Xpress). The truckload business is the cash cow. The LTL network is the growth engine. And the Knight Playbook is the value-creation tool that ties it all together.

The risk, of course, is execution. Integrating trucking companies is notoriously difficult because the most important assets, the drivers, can literally walk away. The U.S. Xpress turnaround was still in its early innings through 2025, and the freight market's cyclical downturn made the timeline more challenging. But the bet is that Knight-Swift has proven it can do this repeatedly, and that each successful integration reinforces the next.

V. Current Management: The Adam Miller Era

On a conference call in early 2025, Knight-Swift's CEO Adam Miller was asked about the company's decision to keep investing in LTL terminal expansion even as the freight market remained soft. His answer was characteristically analytical and devoid of bravado: "We are building for the next decade, not the next quarter. The terminal network is the asset that appreciates, and we will not stop building it because of a cyclical trough." It was the kind of response that reveals everything about the man running Knight-Swift and the transition the company has undergone from a founder-led enterprise to a professionally managed one.

Adam Miller was born in 1981, making him just 44 years old in 2026, young for the CEO of a Fortune 500-caliber company. He joined Knight Transportation in the early 2000s, shortly after college, and spent his entire career inside the organization. He rose through the finance function, eventually becoming CFO, a role in which he was the financial architect behind the 2017 Swift merger and every major acquisition since. When he was elevated to CEO, it was not a surprise to anyone who had watched the company closely. Miller was Kevin Knight's protege, steeped in the Knight Playbook but with a fluency in capital markets, technology investment, and institutional investor relations that the founders, for all their operational genius, had never prioritized in quite the same way.

Kevin Knight remains Executive Chairman, and Gary Knight serves as Executive Vice Chairman. Their continued presence provides institutional continuity and cultural guardrails. But make no mistake: the day-to-day strategic and operational leadership of the company rests with Miller. His compensation structure tells the story. His base pay is approximately $1.7 million, but the majority of his compensation comes from performance-based restricted stock units tied to earnings-per-share growth and total shareholder return relative to transportation industry peers. Roughly 60 percent of his total incentive package is structured around these performance metrics, with the remainder in time-vested equity. The company requires its CEO to hold at least six times base salary in company stock, and Miller's holdings exceed $10 million.

The leadership bench beneath Miller reflects the company's hybrid heritage. Andrew Hess serves as CFO, bringing financial rigor to the capital allocation process. James Fitzsimmons, a Swift veteran, runs Swift's operations as Chief Operating Officer. Timothy Harrington leads the U.S. Xpress integration as President of that division. Todd Carlson serves as General Counsel. The structure is deliberately decentralized. Each operating brand, Knight, Swift, AAA Cooper, U.S. Xpress, maintains its own operational identity and management team, while strategy, capital allocation, and technology investments are coordinated centrally.

This federated model is unusual in trucking, where most large carriers centralize everything. But it reflects the Knight philosophy that trucking is fundamentally a local business. A terminal manager in Memphis knows his drivers, his customers, and his lanes better than anyone at headquarters in Phoenix. The role of corporate is to set targets, provide resources, and hold people accountable, not to micromanage load planning or driver scheduling. It is the same philosophy that made Knight Transportation the best-run small carrier in America, now scaled across a $7.5 billion enterprise.

Miller's strategic priorities represent an evolution of the Knight legacy. While the founders built their reputation on operational discipline in truckload, Miller is pushing the company toward becoming what he calls a "diversified freight platform." This means continued investment in the LTL network, expansion of the logistics and brokerage segment, and increasing investment in technology, particularly in fleet management software, route optimization, and data analytics tools that can improve utilization across all segments. The vision is a company that can offer shippers a one-stop solution: truckload, LTL, intermodal, brokerage, and warehousing, all coordinated through a single technology platform.

Whether Miller can achieve this vision while maintaining the operational discipline that defines the Knight culture is the central question facing the company. The history of transportation conglomerates attempting to become "platforms" is littered with failures, companies that chased breadth at the expense of depth and lost the operational focus that made them successful in the first place. Miller's advantage is that he was raised inside the Knight system. He does not need to learn the playbook. He helped write it.

VI. Hidden Gems: Beyond the Big Rig

There is a part of Knight-Swift's business that almost never gets mentioned on earnings calls or in sell-side research reports, but it may be the most strategically interesting asset the company owns. It is called Iron Truck Services, and it represents a quiet but potentially transformative bet on the fragmented underbelly of American trucking.

Here is the context. There are roughly 900,000 trucking companies in the United States, and the vast majority of them are tiny. About 97 percent operate fewer than twenty trucks. These small fleets and owner-operators are Knight-Swift's competitors on the road, but they are also potential customers. Running a small trucking company is punishingly expensive. You need insurance, and as a small fleet with limited bargaining power, you pay through the nose for it. You need fuel, and you do not get volume discounts. You need maintenance, and you cannot afford your own shop. You need financing for equipment, and your rates are higher because you are a credit risk. Every one of these pain points represents an opportunity.

Iron Truck Services is Knight-Swift's answer. By leveraging the purchasing power of the largest truckload fleet in North America, Knight-Swift can offer insurance, fuel cards, maintenance programs, and equipment financing to small carriers at rates those carriers could never negotiate on their own. Think of it as a kind of services platform that transforms competitors into customers. The small carrier gets better economics, and Knight-Swift gets recurring, high-margin revenue that is largely insulated from the freight cycle. Whether freight rates are booming or busting, small carriers still need insurance and fuel.

This model has analogs in other industries. Amazon Web Services started as internal infrastructure that Amazon then offered to external developers. Shopify built tools for its own e-commerce platform and then opened them to every small merchant on the internet. Iron Truck Services is not at that scale, and it would be premature to call it a technology platform in the same breath. But the strategic logic is identical: use your scale advantages to serve the long tail of your industry, and in doing so, create a relationship that makes those small players more dependent on you, not less.

The second hidden gem is the LTL build-out, which deserves separate attention beyond the acquisition story. Knight-Swift is not simply running AAA Cooper as a standalone regional LTL carrier. It is actively expanding the terminal network, opening new facilities, extending routes, and investing in the technology infrastructure needed to compete at the national level. The ambition is to create a third major national LTL player alongside Old Dominion and FedEx Freight. The advantage of building this from the AAA Cooper base is that the existing southeastern network provides a strong foundation of density, the single most important driver of LTL profitability. Density, in LTL terms, means more freight moving through each terminal, which means better trailer utilization, shorter dock-to-dock times, and lower cost per hundredweight. Every new terminal added to the network improves the density of the existing terminals, creating a virtuous cycle.

The third asset worth understanding is Knight-Swift's warehousing operation, which encompasses approximately 6.7 million square feet of warehouse space across the country. In isolation, warehousing is a low-margin business. But within the context of a transportation network, it serves as a critical customer retention tool. When a shipper stores inventory in Knight-Swift's warehouse and uses Knight-Swift trucks to move that inventory, the relationship becomes deeply integrated. Switching costs rise. The shipper would need to find not just a new trucking provider, but a new warehouse, new inventory management systems, and new coordination workflows. This kind of operational stickiness is exactly the type of competitive advantage that is invisible in financial statements but enormously valuable over time.

Together, these businesses, Iron Truck Services, the expanding LTL network, and the warehousing operations, tell a story about Knight-Swift that is very different from the simple "big trucking company" narrative. They suggest a company that is deliberately building multiple layers of competitive advantage, some visible and some not, that collectively make it harder and harder for customers to leave and for competitors to replicate.

VII. Framework Analysis: 7 Powers and 5 Forces

To truly understand whether Knight-Swift's advantages are durable, it helps to apply two of the most rigorous frameworks in business strategy. Hamilton Helmer's 7 Powers framework identifies the specific sources of persistent differential returns, the "powers" that allow a business to earn more than its cost of capital over long periods. Michael Porter's 5 Forces framework examines the structural attractiveness of the industry itself. Together, they paint a nuanced picture of where Knight-Swift is strong and where it remains vulnerable.

Starting with Helmer's framework, the most compelling power Knight-Swift possesses is Process Power. This is the Knight Playbook itself, the decentralized terminal management system, the scorecard-driven accountability, the discipline around fleet age and driver retention. Process Power is defined as embedded company organization and activity sets that enable lower costs or superior product. The critical feature of Process Power is that it cannot be acquired through a licensing deal or copied from a playbook manual. It is built over decades through thousands of small decisions, institutional learning, and cultural reinforcement. Competitors can see that Knight-Swift runs a younger fleet and has better driver retention. But replicating the management systems, incentive structures, and cultural norms that produce those outcomes is extraordinarily difficult. It is the difference between knowing that a Michelin-starred restaurant uses fresh ingredients and actually running one yourself.

The second relevant power is Scale Economies. Knight-Swift's sheer size gives it purchasing advantages that smaller carriers cannot match. It buys trucks in volumes that command significant manufacturer discounts. Its fuel consumption gives it negotiating leverage with fuel suppliers. Its insurance operation, partly internalized through its captive insurance arrangements, benefits from a larger risk pool. And the LTL terminal network, once it reaches national scale, will exhibit the classic scale economics of a hub-and-spoke system, where the cost per shipment declines as volume through each node increases. This last point is crucial because it represents a power that is still being built. Knight-Swift does not yet have the LTL scale economies of Old Dominion, but it is investing aggressively to get there.

The third applicable power is what Helmer calls Cornered Resource, a privileged access to a value-creating asset. In Knight-Swift's case, the cornered resource is cultural. It is the "Knight DNA," the institutional knowledge embedded in hundreds of terminal managers, operations leaders, and senior executives who have been trained in the Knight system over decades. This human capital is not transferable. You cannot hire away one Knight executive and install the whole system at a competitor. The system is greater than any individual, and it is continuously reinforced through the company's promotion-from-within philosophy.

Now turn to Porter's 5 Forces. The picture here is mixed, which is precisely what makes Knight-Swift's strategic evolution so important. In the truckload segment, the Threat of New Entrants is high. Anyone with a truck and a license can compete for loads. Bargaining Power of Buyers, meaning shippers, is also high because they can easily switch between truckload carriers. Rivalry Among Existing Competitors is intense, with thousands of firms competing on price. The Threat of Substitutes is moderate, with rail intermodal providing an alternative for some long-haul lanes. And Bargaining Power of Suppliers, primarily truck manufacturers and fuel companies, is moderate.

This five-forces analysis explains why truckload carriers trade at low valuations. The industry structure is terrible. But it also explains why Knight-Swift's pivot toward LTL is so strategically important. In LTL, the forces are dramatically more favorable. The Threat of New Entrants is effectively zero because building a terminal network from scratch requires billions of dollars and decades of investment. Bargaining Power of Buyers is lower because shippers have fewer LTL options and switching costs are higher. Rivalry is intense but limited to a handful of national and regional players rather than hundreds of thousands of competitors. The industry structure is fundamentally better, and that is reflected in the valuations. Old Dominion's market cap of nearly $38 billion on revenues of roughly $6 billion dwarfs Knight-Swift's $8.4 billion market cap on revenues of $7.5 billion. The difference is almost entirely explained by industry structure.

This framework analysis reveals the essence of Knight-Swift's strategy. The company is using the cash generated by its structurally challenged truckload business to buy and build its way into the structurally advantaged LTL business, while using Process Power to extract more margin from the truckload segment than any competitor. It is a strategy of strategic migration, moving the center of gravity of the enterprise from a bad industry to a good one, funded by excellence in the bad one. Whether it will work depends on execution, timing, and the freight cycle. But the logic is sound, and the track record of execution provides reason for cautious optimism.

VIII. Playbook: Business and Investing Lessons

Every great company teaches lessons that extend beyond its industry, and Knight-Swift offers several that are worth dwelling on for anyone who studies businesses or allocates capital.

The first and most important lesson is what might be called the "Operating Ratio is Everything" principle. In trucking, and frankly in many capital-intensive industries, the difference between a good business and a bad one is not revenue growth or market share. It is operating efficiency. Knight-Swift's history demonstrates this with almost mathematical precision. When the company took over Swift in 2017, Swift was generating billions in revenue but converting very little of it to profit. Knight's smaller operation was generating less revenue but dramatically more profit per dollar. The lesson for investors is that in commodity businesses, the quality of the operator matters far more than the size of the operation. A one-percentage-point improvement in operating ratio across Knight-Swift's $7.5 billion revenue base translates to roughly $75 million of additional operating income. That is the power of operational discipline at scale.

The second lesson is about acquiring culture versus acquiring assets. Most acquisitions in the trucking industry fail because the acquirer buys trucks and terminals but cannot change the management culture of the target. Knight-Swift has developed an approach that is almost the opposite of what most acquirers do. It does not try to preserve the target's culture or even to blend cultures. It installs its own operating system. When it acquired Swift, it did not negotiate a compromise between the Knight way and the Swift way. It imposed the Knight way, terminal by terminal, scorecard by scorecard. When it acquired U.S. Xpress, the same approach applied. This works because the Knight Playbook is not a set of abstract principles. It is a concrete, measurable system with specific KPIs, processes, and accountability mechanisms. It is more like installing an enterprise software system than negotiating a cultural merger.

The third lesson concerns building resilience in a cyclical business. Trucking is one of the most cyclical industries in the American economy. When GDP grows, freight volumes surge and rates spike. When the economy softens, capacity floods the market and rates collapse. Knight-Swift has experienced this firsthand. Its net income swung from $771 million in 2022, at the peak of the post-pandemic freight boom, to $66 million in 2025, at the trough of the freight recession. Earnings per share went from $4.73 to $0.41 over that same period. Many trucking companies have gone bankrupt in downturns like this, including some of Knight-Swift's acquisition targets.

Knight-Swift has survived, and even thrived, during these cycles because of its diversification strategy. The LTL segment provides revenue that is less cyclically volatile than truckload. The logistics brokerage business is asset-light and can scale down costs quickly when volumes decline. The warehousing operations generate steady rental income. And the Iron Truck Services business provides recurring, cycle-resistant revenue from small carriers who need insurance and fuel regardless of freight rates. No single buffer eliminates cyclicality, but together they create a portfolio effect that smooths the extremes.

There is also a subtler lesson about patience and compounding. Kevin and Gary Knight started with a few trucks in 1990. It took them 27 years to reach the point where they could merge with Swift. It took another four years to complete the AAA Cooper acquisition. And the LTL build-out is a project that management has said will take the better part of a decade. This is not a story of overnight disruption or hockey-stick growth charts. It is a story of incremental improvement, compounded over decades, by people who understood that the most powerful competitive advantages in business are the ones that take the longest to build.

IX. Analysis: Bear vs. Bull Case

The bull case for Knight-Swift rests on a straightforward but powerful thesis: re-rating. Today, the market values Knight-Swift primarily as a truckload carrier. Its enterprise value of roughly $11 billion represents about 10.6 times trailing EBITDA, a reasonable multiple for a cyclically depressed trucking company but a fraction of what pure-play LTL carriers command. Old Dominion, the gold standard of LTL, trades at well over 20 times earnings. Saia, a smaller but fast-growing LTL operator, commands a similar premium.

The bull argument is that as Knight-Swift's LTL segment grows to represent a larger share of total revenue and profit, the market will gradually re-rate the stock from a "trucking multiple" to something closer to an "LTL multiple." This does not require the LTL business to become as good as Old Dominion's, which has spent decades optimizing its network to achieve an operating ratio in the low 70s. It simply requires the LTL segment to become large enough and profitable enough that the overall business mix tilts meaningfully toward the higher-valued segment. If Knight-Swift can achieve a national LTL network with operating ratios in the mid-80s, and if that segment grows to represent 30 percent or more of total operating income, the math suggests significant upside to the current valuation.

Additionally, the freight cycle itself is a tailwind waiting to arrive. The trucking industry has been in a prolonged downturn, with capacity exceeding demand and rates under pressure. But freight cycles are, by definition, cyclical. When the cycle turns, and it always does, Knight-Swift's massive fleet will benefit from rising rates while its operational discipline ensures that more of that revenue flows to the bottom line. The 2021-2022 period, when the company earned over $4.00 per share, provides a blueprint for what a strong freight market can mean for the income statement. A Piotroski Score of 7 out of 9 suggests reasonable financial health despite the cyclical trough.

The bear case is equally straightforward. The freight recession has been longer and deeper than most industry participants expected. Knight-Swift's net income collapsed from $771 million in 2022 to $66 million in 2025. Free cash flow turned negative in 2024 before recovering to $763 million in 2025, partly aided by asset disposition timing. The company carries roughly $2.9 billion in total debt against an EBITDA of about $1.05 billion, producing a net debt-to-EBITDA ratio of approximately 2.5 times. This is manageable but not conservative, especially if the freight downturn extends further.

The U.S. Xpress turnaround represents a specific risk. Fixing a trucking company with a 101 percent operating ratio is not a guaranteed outcome, no matter how good the playbook. Driver attrition, customer defection, and equipment condition issues can all derail the plan. If U.S. Xpress continues to bleed cash rather than improving toward the targeted operating ratio in the 80s, it becomes a drag on the overall enterprise rather than a value-creation engine.

There are also macro risks that deserve attention. The rise of autonomous trucking technology, still in its early commercial stages, could eventually disrupt the competitive dynamics of the truckload market in ways that are hard to predict. Regulatory changes around emissions, driver hours-of-service rules, and cross-border freight could impose costs that disproportionately affect large carriers. And tariff uncertainty, particularly related to Mexico-U.S. freight flows, creates an overhang for a company that operates significant cross-border routes.

Analyst consensus reflects this tension. The consensus price target sits around $61 per share against a recent price near $52, suggesting roughly 17 percent upside. Individual targets range from $53 to $70, with Barclays among the most bullish at $75. Citigroup recently upgraded the stock to Buy with a $64 target, citing improving freight fundamentals and the LTL build-out as catalysts.

For investors tracking this story, two KPIs matter most. First is the Consolidated Adjusted Operating Ratio. Management's goal is to drive this below 90 percent on a sustained basis, and its trajectory tells you whether the operational playbook is working across all segments. When this number improves, it means the company is converting more of every revenue dollar into profit, regardless of where the freight cycle sits. Second is LTL revenue as a percentage of total revenue. This metric tracks the strategic migration from truckload to LTL. As this number grows, it signals that the company's business mix is shifting toward the higher-quality, higher-multiple segment. Together, these two numbers capture both the operational execution story and the strategic transformation story in a way that no single financial metric can.

X. Epilogue and Final Reflections

In the spring of 2026, Kevin Knight is 68 years old. His brother Gary is 73. Between them, they have spent more than seven decades in the trucking business, starting from the seat of a cab and ending in the boardroom of the largest fleet in North America. The company they built carries their name, literally, and its culture carries their fingerprints on every terminal scorecard and every fleet refresh cycle.

The journey from a handful of trucks in Phoenix in 1990 to a $7.5 billion revenue enterprise with 35,000 employees is remarkable by any measure. But what makes the Knight-Swift story more than just a tale of growth is the philosophy embedded in its DNA. In an industry known for boom-and-bust cycles, reckless expansion, and chronic value destruction, the Knight brothers proved that discipline, patience, and an obsessive focus on operating efficiency could create extraordinary value over time.

Now that philosophy is being tested in new ways. Adam Miller and his team are attempting something the Knight brothers never attempted: transforming a trucking company into a diversified freight platform. The LTL build-out, the logistics expansion, the Iron Truck Services concept, the warehousing integration, these are all bets that the Knight Playbook can be applied not just to fixing underperforming trucking companies but to building entirely new businesses. The stakes are high. The freight recession has compressed valuations and strained cash flows. The U.S. Xpress turnaround is unfinished. The LTL network is still years from national scale. And the freight cycle, that great equalizer of the trucking industry, remains stubbornly weak.

But if there is one lesson from the Knight-Swift story, it is that the most powerful competitive advantages are the ones built slowly, through thousands of small decisions compounded over decades. The Knights did not disrupt the trucking industry. They disciplined it. And in an age of rapid disruption and overnight fortunes, there is something deeply compelling about a company that got to the top of its industry by doing the same unglamorous thing, slightly better, every single day, for thirty-five years.

The American highway stretches on, and the trucks keep rolling. The question is not whether freight will move. It always will. The question is who will move it most efficiently, most reliably, and most profitably over the next decade. Knight-Swift has spent its entire existence preparing to answer that question.

XI. Further Reading

For readers interested in going deeper, Marc Levinson's "The Box: How the Shipping Container Made the World Smaller and the World Economy Bigger" provides essential context on the logistics revolution that shaped modern freight networks. Knight-Swift's 2024 Investor Day presentation, titled "Diversified Freight Power," offers the company's own articulation of its platform strategy and LTL ambitions. The company's annual 10-K filings provide detailed segment-level data on Trucking, LTL, Logistics, and Intermodal operations that reward careful reading.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube