Kinder Morgan: Pipeline Empire Built from Enron's Ashes

I. Introduction & The Enron Connection

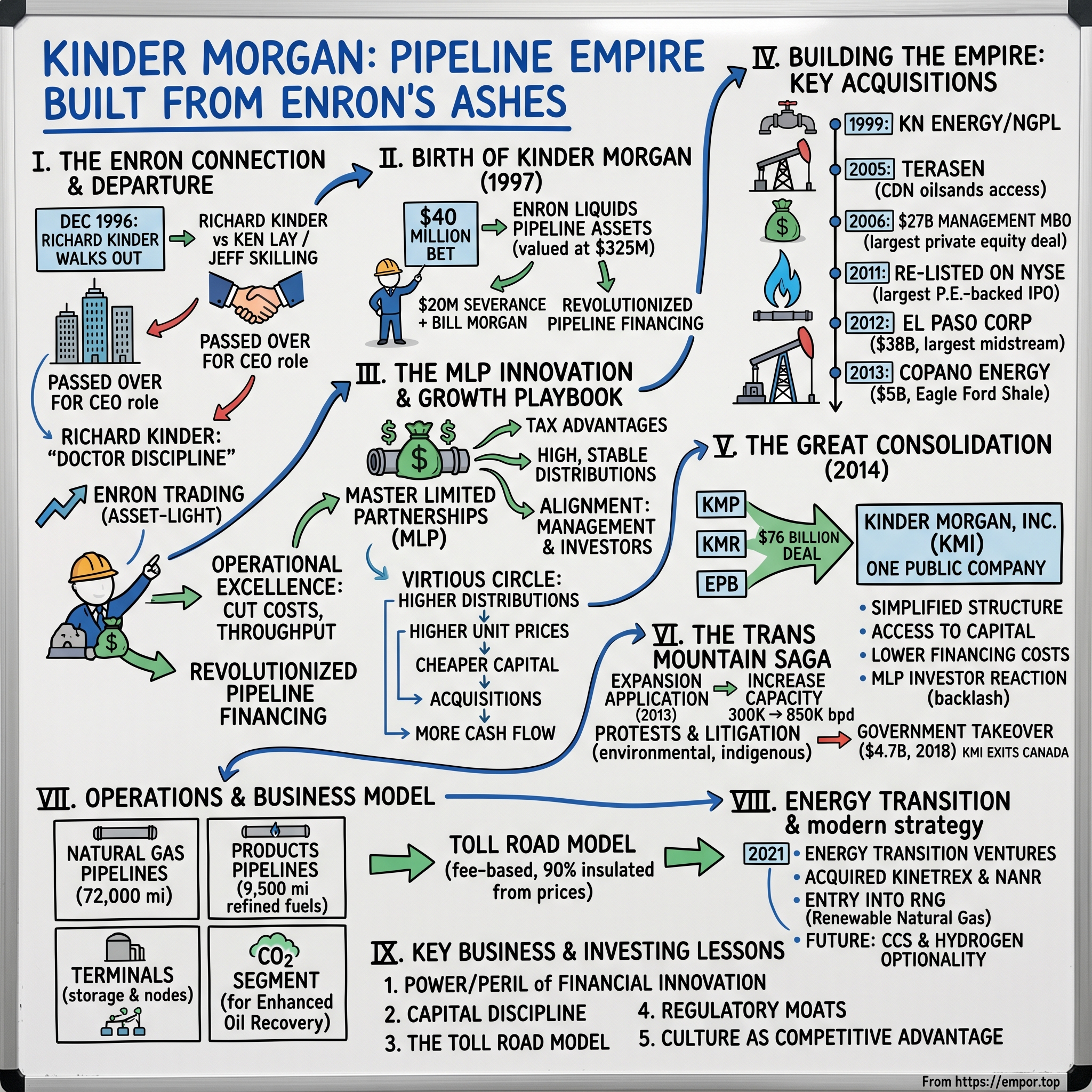

Picture this: December 1996, Houston. Richard Kinder, the second most powerful executive at Enron, walks out of the gleaming fifty-story tower for the last time. No fanfare, no press conference—just a man with a $20 million severance package and a radical idea. Within months, he would turn a $40 million bet on discarded pipeline assets into what would become North America's energy infrastructure colossus.

The story of Kinder Morgan is fundamentally a story about seeing value where others see scrap metal. When Kinder and his college friend William Morgan purchased Enron Liquids Pipeline for $40 million in 1997, the assets on paper were worth $325 million. But here's what makes this tale extraordinary: they didn't just buy pipelines—they revolutionized how pipeline companies could be financed and operated, pioneering the use of Master Limited Partnerships (MLPs) as a growth vehicle in ways the energy sector had never imagined.

Today, Kinder Morgan operates approximately 79,000 miles of pipelines—enough to circle the Earth three times—and 139 terminals across North America. The company moves about 40% of the natural gas consumed in the United States. Its market capitalization hovers around $50 billion, and it has delivered billions in distributions to shareholders since its founding. Yet this empire emerged from the ashes of America's most spectacular corporate fraud.

The central paradox demands examination: How did two executives from Enron—a company whose name became synonymous with corporate malfeasance—build one of the most trusted and essential energy infrastructure networks in North America? The answer lies in a philosophy diametrically opposed to everything Enron came to represent. Where Enron chased phantom profits through mark-to-market accounting and special purpose entities, Kinder Morgan focused on tangible steel in the ground generating predictable toll revenue. Where Enron's executives flew in corporate jets and built crystal palaces, Kinder instituted a company-wide policy of flying coach and took a $1 annual salary. The numbers tell the same story at different scales: approximately 79,000 miles of pipelines and 139 terminals, though Wikipedia cites 83,000 miles (134,000 km) of pipelines and 143 terminals. What matters is the transformation from that modest $40 million beginning to an infrastructure network that literally powers American industry.

As we embark on this journey through Kinder Morgan's evolution, we'll discover how a company born from corporate catastrophe became the antithesis of its predecessor—a story that reveals fundamental truths about infrastructure investing, capital discipline, and the enduring value of owning the toll roads of American energy.

II. The Enron Years & The Departure

The conference room at Enron's Houston headquarters crackled with tension in late 1996. Richard Kinder, the company's president and chief operating officer, had just been passed over for the CEO position he'd been promised. Kenneth Lay, Enron's founder and Kinder's college friend from the University of Missouri, had decided to remain at the helm. The heir apparent would not inherit the throne. Within weeks, Kinder would walk away from the second-highest position at one of America's fastest-growing companies, taking with him hard-earned lessons that would reshape an entire industry. To understand Kinder's journey, we must first grasp his origins. The Missouri native's path to Enron began modestly, as an attorney with Florida Gas Transmission. His college friendship with Kenneth Lay would prove fateful—Lay was working for Florida Gas and hired William Morgan, who in turn brought Kinder aboard. The company went through a series of mergers, with Florida Gas being sold to Houston Natural Gas in 1984, and the following year Houston Natural Gas merged with InterNorth to create Enron.

By 1990, Kinder had risen to become Enron's president and chief operating officer. During his tenure, he transformed the company's operations with remarkable efficiency. From 1990 to December 1996, he served as president and COO, and under his watch, Enron's revenues grew from $5.7 billion in 1991 to $13.3 billion in 1996—a compound annual growth rate exceeding 18%. Yet while the numbers climbed, Kinder maintained a reputation that would later prove prophetic: he was known as "Doctor Discipline" for the steel grip he maintained over cash flow and expenses. The discipline that earned him this nickname was legendary even within Enron. Richard Kinder, known throughout Enron as "Doctor Discipline", was both people and numbers oriented. He held a meeting in the boardroom every Monday morning where he interrogated every business unit leader, frequently challenging their strategic plans and numbers. He focused hawk-like on expenses, cash flows, and employee levels. Cash management was so important for Kinder that he gave all business group managers a budget target for cash flow and profits, with bonuses tied to meeting both targets.

Yet this management philosophy clashed fundamentally with the vision Ken Lay and his eventual successor Jeff Skilling had for Enron's future. "Plodding" Kinder, with his to-do lists and penchant for flying coach class, distrusted Lay's "shiny new world" of leveraged energy trading. "Let's make sure we're not smoking our own dope," was his favourite saying. The contrast couldn't have been starker: while Kinder obsessed over cash flow from real assets, Lay and Skilling dreamed of transforming Enron into an asset-light trading powerhouse.

The succession drama that unfolded in 1996 reads like a Shakespearean tragedy of corporate ambition. Kinder, who was Enron's president then, and his college buddy at the University of Missouri, Ken Lay, had a succession plan. At the end of 1996, Lay would remain at Enron as chairman but would hand over his CEO title and the job of running the company's day-to-day operations to Kinder. The plan seemed set in stone—until it wasn't.

Some say Lay changed his mind about giving up the CEO seat and badmouthed Kinder to the board of directors in order to win a new five-year contract. Others whispered about personal tensions, including gossip about Kinder's relationship with Nancy McNeil, Ken Lay's assistant, whom Kinder would marry in 1997. But the fundamental issue was strategic: Lay had chosen a different path for Enron, one that favored Jeff Skilling's vision of energy trading over Kinder's focus on physical infrastructure.

The aftermath of Kinder's departure proved the wisdom of his approach. Upon his departure, Ken Lay later replaced him with Jeff Skilling, and the Enron implosion began. Almost faster than you can say mark-to-market accounting, management controls disappeared once Jeff Skilling became CEO of Enron. The rest is sad history and a shareholder's worst nightmare come true.

What Kinder took from Enron wasn't just a $20 million severance package—it was a playbook of what worked and, perhaps more importantly, what didn't. He had witnessed firsthand how financial engineering and accounting gymnastics could create the illusion of success while destroying real value. He had seen how a culture of excess—private jets, lavish bonuses, corporate hubris—could corrupt even the most successful enterprises. And he had learned that in the energy business, cash flow from real assets beats paper profits every time.

As 1996 drew to a close, Kinder faced a choice that would define not just his career but an entire industry. He could have taken his millions and retired, or joined another energy giant. Instead, he chose to build something new—something that would be the antithesis of everything Enron was becoming. His parting from Enron wasn't just a resignation; it was a philosophical declaration about what an energy company should be.

III. Birth of Kinder Morgan: The $40 Million Bet

On a humid Houston morning in early 1997, Richard Kinder and Bill Morgan sat across from Enron's negotiating team, finalizing paperwork for what industry observers considered a puzzling transaction. They were purchasing Enron Liquids Pipeline—a collection of aging pipelines and a rail-to-barge coal terminal in Illinois—for $40 million. The assets, buried deep in Enron's financial statements as a tax shelter, carried a book value of $325 million. To Wall Street's high-flying traders, these were yesterday's infrastructure, the detritus of the old energy economy. To Kinder and Morgan, they were gold.

Armed with a $20 million severance package, he joined with another Enron alumnus and university classmate, Bill Morgan, to buy up some pipelines and an Illinois rail-to-barge transfer terminal that Enron was unloading for a price tag of $40 million (the assets were worth $325 million). In 1997, they closed a deal for the Enron Liquids Pipeline Company—an Enron tax shelter — and the entity which would later become Kinder Morgan was formed.

The first order of business wasn't expansion—it was surgery. Before even thinking about growth, Kinder wielded his scalpel with the precision of a cardiac surgeon, cutting $5 million in annual expenses. Staff positions disappeared. First-class travel became coach—no exceptions. The executive dining room? Gone. Corporate memberships? Cancelled. But the most radical move was yet to come.

Kinder and Morgan made a decision that would have been unthinkable at Enron: they would each take salaries of exactly $1 per year. Not $1 million. Not $100,000. One dollar. The only reason for even that token amount was to qualify for healthcare benefits. This wasn't a publicity stunt or temporary gesture—it was a fundamental restructuring of executive incentives. Dependent entirely on dividends under this arrangement, Kinder and Morgan would only prosper to the extent that their unit holders were rewarded.

At Enron, Kinder had been nicknamed "Doctor Discipline" for the steel grip he maintained over cash flow and expenses, and at Kinder Morgan he immediately began slashing costs, laying off employees, and clamping down on corporate luxuries like private jets. "We wanted to drive home one culture here: Cheap. Cheap. Cheap," he told Fortune magazine

The results were immediate and dramatic. Within six months, Kinder increased the distribution paid to unit holders by 50 percent. This wasn't financial engineering or accounting tricks—it was operational excellence applied to undervalued assets. By October 1997, barely nine months after the company's formation, KMP made its first major acquisition, buying Santa Fe Pacific Pipeline Partners, L.P. The pattern was set: find undervalued or undermanaged pipeline assets, apply rigorous operational discipline, and deliver consistent cash distributions to investors.

What made this approach revolutionary wasn't just the operational efficiency—it was the financial structure Kinder chose to employ. While Enron was pioneering exotic derivatives and special purpose entities, Kinder was resurrecting and reimagining an old structure: the Master Limited Partnership (MLP). MLPs had existed since the 1980s, primarily in real estate, but had never been successfully deployed as a growth vehicle for energy infrastructure. Kinder saw what others missed: the MLP structure's tax advantages and yield requirements would create perfect alignment between management and investors while providing access to capital at attractive rates.

The mechanics were elegant in their simplicity. Unlike a corporation, an MLP doesn't pay corporate taxes. Instead, it distributes most of its "available cash" to its partners each quarter, who then pay taxes at their individual rates—typically much lower than the 35% corporate rate of the era. This tax efficiency meant that every dollar of operating cash flow was worth more to investors in an MLP than in a traditional corporation. For yield-hungry investors in a low-interest-rate environment, Kinder Morgan units offered something irresistible: high, stable, tax-advantaged distributions backed by real assets with predictable cash flows.

But the MLP structure came with a discipline that Kinder embraced: the requirement to distribute most cash meant that growth had to be funded externally, subjecting every acquisition and expansion project to market scrutiny. There was no room for empire building or pet projects. Every dollar spent had to generate returns that justified accessing external capital. It was financial democracy in action—a stark contrast to Enron's increasingly opaque financial machinations.

The cultural transformation was equally dramatic. Where Enron's trading floors buzzed with testosterone-fueled energy and million-dollar bonuses, Kinder Morgan's offices hummed with the quiet efficiency of engineers and accountants. Where Enron executives flew private jets to weekend getaways, Kinder Morgan employees flew coach to inspect pipelines. The message was clear: this was a company built on substance, not style.

By the end of 1997, Kinder Morgan had established the three pillars that would define its success for the next two decades: operational excellence that squeezed maximum value from every asset; a financial structure that aligned management and investor interests while providing tax-efficient returns; and a culture of frugality and discipline that permeated every level of the organization.

The $40 million bet had paid off spectacularly. In less than a year, Kinder and Morgan had not only proved that their model worked—they had begun to transform how the entire energy infrastructure sector thought about value creation. While Enron was building castles in the sky, Kinder Morgan was laying pipelines in the ground. The contrast would only become more stark as the calendar turned toward the new millennium.

IV. The MLP Innovation & Growth Playbook

Standing before a packed conference room at the Waldorf Astoria in New York in early 1998, Richard Kinder faced skeptical institutional investors who had gathered to hear about this unusual creature called Kinder Morgan Energy Partners. "We're not trying to be the smartest guys in the room," Kinder said, a not-so-subtle jab at Enron's infamous tagline. "We're trying to be the most predictable." The investors leaned in. In an era of dot-com mania and Enron's mark-to-market mysteries, predictability was becoming the new sexy.

Since creating Kinder Morgan in 1997, the company has increased distributions to shareholders at a 40 percent compounded annual growth rate. But what Kinder was proposing wasn't just another high-yield investment—it was a fundamental reimagining of how energy infrastructure could be financed and operated.

The Master Limited Partnership structure that Kinder championed operated on a deceptively simple principle. Most of Kinder Morgan's $18 billion in assets would eventually be held by Kinder Morgan Energy Partners, L.P. (KMP), with units that traded like shares of stock. But unlike a corporation, the MLP paid no corporate taxes. This wasn't a loophole—it was an intentional policy designed to encourage infrastructure investment. The catch? The MLP had to distribute essentially all its available cash to unit holders each quarter.

This requirement created what Kinder called "the discipline of the distribution." Every quarter, management had to generate enough cash to meet or exceed the distribution. No hiding behind "adjusted EBITDA" or "pro forma earnings." Cash was king, and cash was what unit holders received. The beauty of the model was its self-reinforcing nature: higher distributions meant higher unit prices, which meant cheaper access to capital for acquisitions, which meant more cash flow, which meant higher distributions. It was a virtuous circle, but only if executed flawlessly.

The tax advantages were compelling. MLPs don't pay corporate taxes, instead distributing most of their profits to investors, who then pay income taxes at their individual rates which is usually much lower than the corporate tax rate. For a high-income investor in 1998, the difference between receiving a dividend taxed at both the corporate level (35%) and personal level (39.6%) versus receiving an MLP distribution taxed only at the personal level was enormous. A dollar of pre-tax earnings at a corporation might deliver only 40 cents to the investor; the same dollar at an MLP delivered 60 cents.

But Kinder's true innovation wasn't just adopting the MLP structure—it was weaponizing it for growth. Previous MLPs had been largely static, holding mature assets and slowly returning capital to investors. Kinder saw the MLP as a growth vehicle, using its tax advantages and yield-hungry investor base to fund an acquisition spree that would consolidate the fragmented pipeline sector.

The playbook was methodical:

First, identify undervalued or undermanaged pipeline assets. In the late 1990s, these were everywhere. Major oil companies were divesting "non-core" pipeline assets to focus on exploration and production. Utilities were selling pipelines to deregulate. Enron was jettisoning physical assets to become an trading company.

Second, acquire these assets using a combination of debt and equity issued by the MLP. Because MLP units yielded 7-8% in an era of 5% Treasury bonds, there was insatiable investor demand. Kinder could issue units at attractive valuations, using the proceeds to buy assets at distressed prices.

Third, apply operational discipline to increase cash flow. This meant cutting costs, optimizing throughput, renegotiating contracts, and eliminating redundancies. Kinder's team typically found 10-20% expense savings within the first year of ownership.

Fourth, use the increased cash flow to raise distributions, which increased unit prices, which lowered the cost of capital, which made the next acquisition even more accretive. Rinse and repeat.

The first major test of this playbook came in 1999 with the reverse merger with KN Energy, a Denver-based utility and pipeline company. The deal brought Natural Gas Pipeline Company of America (NGPL), a critical asset serving the Chicago market. The integration was flawless—costs were cut, synergies realized, and distributions increased ahead of schedule.

This allowed Kinder Morgan to generate enormous returns, a total of 350 per cent in its first decade, compared with the 83 per cent returns generated by the S&P 500

By 2000, as Enron's stock soared on promises of revolutionary new markets in weather derivatives and broadband, Kinder Morgan quietly went about buying real pipelines moving real molecules for real customers. The contrast in approaches was philosophical. Enron saw pipelines as antiquated infrastructure in a world moving toward virtual markets. Kinder saw them as irreplaceable monopolies with decades of predictable cash flow.

The MLP structure also enforced a discipline that would prove crucial when the energy bubble burst. Because MLPs must distribute their cash, they can't accumulate war chests for speculative investments. Every major capital allocation decision requires returning to the capital markets, subjecting it to investor scrutiny. This "short leash" prevented the kind of unchecked expansion that destroyed Enron.

Yet the model wasn't without its critics. Some argued that MLPs' high distributions left little margin for error—one bad acquisition or operational stumble could spiral into a distribution cut and unit price collapse. Others worried about the complexity of MLP tax reporting, which required investors to deal with K-1 forms rather than simple 1099s. And institutional investors, particularly tax-exempt entities like pension funds, faced restrictions on MLP ownership.

Kinder addressed these concerns with characteristic bluntness: "We're not for everyone. We're for investors who want predictable, tax-advantaged cash flow from essential infrastructure. If you want to bet on the next big thing, buy Enron."

By the dawn of the new millennium, the MLP innovation had transformed Kinder Morgan from a $40 million collection of cast-off assets into a multi-billion-dollar enterprise. More importantly, it had created a template that would reshape the entire midstream sector. Companies like Enterprise Products Partners, Plains All American, and Energy Transfer would adopt similar structures, creating an entire ecosystem of MLPs that would eventually control most of America's energy infrastructure.

V. Building the Empire: Key Acquisitions

The boardroom at Terasen Inc.'s Vancouver headquarters fell silent in July 2005 when the final offer was presented: $5.6 billion in cash, a 25% premium to the market price. The Canadian company's directors looked at each other, knowing they were witnessing not just a takeover but a transformation. Richard Kinder was bringing his pipeline empire north, and with it, access to one of the world's most controversial and lucrative energy plays: the Alberta oil sands.

In August 2005, KMI purchases Canadian company Terasen, Inc. for approximately $5.6 billion to broaden its footprint in Canada and gain access to the oilsands via the Trans Mountain Pipeline The acquisition of Terasen represented a strategic masterstroke. The crown jewel was the Trans Mountain Pipeline, the only pipeline carrying crude oil from Alberta to the Pacific Coast. Built in 1953, it was a 1,150-kilometer lifeline that transported 300,000 barrels per day to refineries in Washington State and British Columbia. In an era of rising Asian energy demand and landlocked Canadian crude selling at steep discounts, Trans Mountain was essentially a toll road to the Pacific.

But 2005 was just the appetizer. The real feast came in 2006 when Kinder orchestrated one of the most audacious moves in private equity history: a management-led buyout to take Kinder Morgan private. The $27 billion transaction, including assumed debt, was the largest private equity deal ever at the time. Kinder himself rolled his entire stake, while partners including Goldman Sachs, Carlyle Group, and Riverstone Holdings provided the equity. The rationale was simple but powerful: the public markets weren't properly valuing the long-term cash flow potential of pipeline assets. Going private would allow for more aggressive expansion without quarterly earnings pressure.

For five years, Kinder Morgan operated in the shadows, methodically acquiring and integrating assets away from public scrutiny. The company expanded its footprint, optimized operations, and prepared for what would become one of the most successful IPOs in history. On February 11, 2011, Kinder Morgan returned to the public markets with a bang. On February 11, 2011, KMI again begins trading on the New York Stock Exchange following the largest private equity-backed initial public offering in U.S. history. The IPO issues nearly 110 million shares and raises approximately $3.3 billion

The timing was perfect. The shale revolution was transforming America's energy landscape, and pipelines were the arteries through which this new abundance would flow. Natural gas, once scarce and expensive, was now abundant and cheap. Crude oil production, which had declined for decades, was surging. Every new well needed gathering pipelines. Every processing plant needed transmission lines. Every refinery and export terminal needed connectivity. Kinder Morgan was positioned at the center of it all.

Then came the deal that would define Kinder's legacy: El Paso Corporation. In May 2012, KMI completes an approximately $38 billion acquisition of El Paso Corporation making KMI the largest midstream and one of the largest energy companies and natural gas network operators in North America The acquisition was breathtaking in its scope. El Paso brought 42,000 miles of interstate natural gas pipelines, complementing Kinder Morgan's existing network to create an infrastructure colossus spanning from coast to coast.

The integration of El Paso showcased Kinder's operational philosophy at scale. Within months, duplicate headquarters were consolidated, overlapping functions eliminated, and systems integrated. The promised $350 million in annual cost synergies were achieved ahead of schedule. But more importantly, the combined network created commercial synergies—gas that previously required multiple pipelines to reach markets could now flow seamlessly across an integrated system.

The acquisition spree continued with surgical precision. In May 2013, KMP completes an approximately $5 billion acquisition of Copano Energy, which enables the company to significantly expand its midstream services footprint Copano brought critical Eagle Ford Shale gathering and processing assets, positioning Kinder Morgan at the wellhead of one of America's most prolific oil and gas plays.

Each acquisition followed the same pattern: identify strategic assets trading below replacement cost, use the MLP structure's access to capital to fund the purchase, apply operational discipline to extract synergies, and increase distributions to unit holders. It was a formula as reliable as the pipelines themselves.

But the empire building wasn't without controversy. Environmental groups increasingly targeted Kinder Morgan as the enabler of fossil fuel expansion. First Nations groups in Canada opposed pipeline expansions through their territories. Competitors complained about market concentration. Regulators scrutinized the interlocking ownership structures between Kinder Morgan Inc. (the general partner) and the various publicly traded MLPs.

The complexity had indeed become dizzying. By 2014, the Kinder Morgan family included four separate publicly traded entities: Kinder Morgan Inc. (KMI), the general partner and parent company; Kinder Morgan Energy Partners (KMP), the main MLP holding most pipeline assets; Kinder Morgan Management (KMR), a corporation that held KMP units for investors who couldn't own MLPs directly; and El Paso Pipeline Partners (EPB), an MLP that came with the El Paso acquisition.

This structure, while tax-efficient, created confusion among investors and inefficiencies in capital allocation. Different investor bases meant different costs of capital. Complex transfer pricing agreements between entities raised governance concerns. The very innovation that had enabled Kinder Morgan's growth was now constraining it.

Kinder, never one to let structure impede strategy, prepared his next move. If the multiple-entity structure no longer served its purpose, it was time for another transformation. The empire had been built through two decades of acquisitions. Now it was time to simplify, consolidate, and prepare for the next phase of growth.

Standing at the podium at the annual investor day in January 2014, Kinder looked out at the assembled analysts and portfolio managers. Kinder Morgan controlled more pipeline miles than any company in America. It moved 40% of the country's natural gas. It operated 180 terminals. The empire was complete. The question now was how to rule it.

VI. The Great Consolidation (2014)

Richard Kinder stood before a hastily assembled press conference on August 10, 2014, preparing to announce what would be the fourth-largest acquisition in the energy sector's history. But this time, the target wasn't a competitor—it was Kinder Morgan itself. "We're simplifying our structure," Kinder said with characteristic understatement. In reality, he was about to execute a $76 billion transaction that would collapse four public companies into one, ending the MLP era he had pioneered and shocking investors who had come to rely on those generous distributions.

On August 10, 2014, Kinder announced it was moving to full ownership of its partially owned subsidiaries Kinder Morgan Energy Partners, Kinder Morgan Management, and El Paso Pipeline Partners in a deal worth $71 billion. The transaction closed on November 26, 2014.

The announcement sent shockwaves through the MLP sector. For seventeen years, the multiple-entity structure had been gospel at Kinder Morgan. The tax advantages were undeniable. The access to yield-seeking capital had funded unprecedented growth. Why destroy what had worked so well?

The answer lay in a confluence of factors that Kinder, with his deep understanding of capital markets, had seen coming. First, the shale revolution had created massive infrastructure needs that required equally massive capital investments. The MLP structure, with its requirement to distribute most cash flow, limited the ability to fund these projects internally. Every major project meant returning to the capital markets, and the MLP investor base was showing signs of fatigue after years of equity issuances.

Second, the cost of capital divergence between the entities had become problematic. KMI stock traded at a lower yield than KMP units, meaning KMI could raise capital more cheaply. But regulatory restrictions limited how much capital KMI could downstream to KMP without triggering complex tax issues. The structure that had once enabled growth was now constraining it.

Third, the governance complexity had become untenable. Prior to November 26, 2014, the Kinder Morgan group publicly traded companies included Kinder Morgan, Inc. (NYSE: KMI), Kinder Morgan Energy Partners, L.P. (NYSE: KMP), Kinder Morgan Management, LLC (NYSE: KMR) and El Paso Pipeline Partners, L.P. Each entity had different investor bases with different expectations. Institutional investors who couldn't own MLPs were shut out from most of Kinder Morgan's assets. The K-1 tax forms required for MLP investors were cumbersome. International investors faced withholding tax issues.

The mechanics of the consolidation were complex but the logic was simple. KMI would acquire all outstanding units of KMP, KMR, and EPB, offering a mix of cash and KMI shares. KMP unit holders could choose between $10.77 in cash plus 2.1931 KMI shares, or 2.4849 KMI shares. The deal valued KMP at a 14% premium to its closing price, with similar premiums for KMR and EPB.

The immediate backlash was fierce. MLP investors, particularly retail investors who had come to depend on the quarterly distributions for income, felt betrayed. They were being forced to exchange tax-advantaged MLP units yielding 6-7% for corporate shares yielding less than 3%. The tax consequences were significant—many long-term MLP holders faced substantial capital gains taxes on the forced sale.

But Kinder had done the math. The simplified structure would save $350 million annually in administrative costs. The single entity could access deeper pools of capital, including international investors and index funds that couldn't own MLPs. The corporate structure provided more flexibility for capital allocation, allowing Kinder Morgan to retain more cash for growth projects while still providing attractive dividends.

The market's initial reaction was harsh. KMI shares fell 10% in the days following the announcement as investors digested the implications. The broader MLP sector was devastated, with the Alerian MLP Index falling 15% in sympathy. The structure that Kinder had pioneered and that dozens of companies had copied was suddenly being abandoned by its creator.

Yet Kinder's timing, as usual, proved prescient. Within months of the consolidation closing in November 2014, oil prices began their precipitous decline from over $100 per barrel to under $30. The MLP sector, dependent on capital markets access for growth, was devastated. Many MLPs were forced to cut distributions, enter into dilutive equity issuances, or restructure. The companies that had followed Kinder into the MLP structure now struggled as capital markets closed.

Kinder Morgan, now a simplified C-corporation, weathered the storm better than most. The retained cash flow that would have been distributed under the MLP structure instead funded capital projects internally. The broader investor base provided stability. The simplified structure made it easier to cut costs and optimize operations during the downturn.

The consolidation also positioned Kinder Morgan for a new era of energy infrastructure. The company could now compete for international projects where MLP structures were disadvantaged. It could participate in joint ventures with major oil companies that preferred corporate partners. It could retain capital for large-scale projects without the quarterly distribution pressure.

By year-end 2015, as the energy sector reeled from collapsed commodity prices, Kinder stood before investors again. "The consolidation wasn't about abandoning what made us successful," he explained. "It was about evolving to remain successful. The MLP structure served us brilliantly for seventeen years. But structures are tools, not religions. When the tool no longer serves its purpose, you get a new tool."

The Great Consolidation marked the end of an era—not just for Kinder Morgan but for the entire MLP sector. The structure that had enabled the financialization of America's energy infrastructure was giving way to a more traditional but perhaps more sustainable model. Kinder Morgan had once again transformed itself, proving that in business, as in evolution, it's not the strongest that survive but the most adaptable.

VII. Operations & Business Model

At 5:47 AM on a Tuesday morning, deep in the computer systems at Kinder Morgan's Houston headquarters, an algorithm detects a 0.3% pressure drop in a pipeline segment near Tulsa. Within seconds, control room operators are notified. Within minutes, field technicians are dispatched. Within hours, the issue—a minor valve malfunction—is resolved. No customer notices. No delivery is delayed. No headline is written. This is the hidden choreography of American energy infrastructure, a ballet of steel and software that Kinder Morgan performs 24 hours a day, 365 days a year across approximately 83,000 miles (134,000 km) of pipelines and 143 terminals. The company has approximately 72,000 miles (116,000 km) of natural gas pipelines and is the largest natural gas pipeline operator in the United States, moving about 40 percent of the natural gas consumed in the country.

Understanding Kinder Morgan's business model requires appreciating a fundamental truth that Richard Kinder grasped early: pipelines aren't in the energy business—they're in the toll road business. The company doesn't care if natural gas costs $2 or $10 per thousand cubic feet. It doesn't matter if oil trades at $30 or $130 per barrel. What matters is that molecules move from Point A to Point B, and Kinder Morgan collects a fee for that movement.

The company operates through four distinct segments, each with its own economics but united by the same toll road philosophy:

Natural Gas Pipelines represent the historical heart of the empire. This segment owns and operates interstate and intrastate natural gas pipelines and storage systems spanning from the Pacific Northwest to the Florida coast. The crown jewel remains Natural Gas Pipeline Company of America (NGPL), with approximately 9,100 miles of pipeline, more than 1 million compression horsepower and 288 billion cubic feet (Bcf) of working natural gas storage. Tennessee Gas Pipeline (TGP) stretches approximately 11,760 miles that transports natural gas supplied from the Northeast section of the United States, to diverse end-use demand markets including New York City and Boston in the Northeast, the Louisiana and Texas Gulf Coast, and Mexico.

These aren't just pipes in the ground—they're complex engineering systems. Every pipeline operates under carefully calibrated pressure, with compressor stations every 50-100 miles boosting the gas to maintain flow rates. Storage facilities, often depleted oil and gas reservoirs or salt caverns, act as giant batteries, storing gas when demand is low and releasing it during peak periods.

Products Pipelines move refined petroleum products—gasoline, diesel, jet fuel—from refineries to markets. This network includes about 9,500 miles of pipelines that function as America's energy circulatory system. The economics here are even more stable than natural gas. Regardless of crude oil prices or refinery margins, Americans need gasoline for their cars and jet fuel for their planes. Kinder Morgan simply collects its toll for moving these products efficiently and safely.

Terminals represent the nodes in the energy network—the places where products change hands, change modes of transport, or get stored. The company maintains roughly 65 liquid terminals that not only store these fuels but also blend in ethanol and biofuels. These facilities are like parking garages for molecules—customers pay for storage capacity whether they use it or not, providing remarkably stable cash flows.

The CO2 segment might be the most fascinating and underappreciated part of the portfolio. Kinder Morgan produces, transports, and markets CO2 for enhanced oil recovery, where the gas is injected into mature oil fields to boost production. The company owns the two largest natural CO2 sources in the United States—McElmo Dome in Colorado and Doe Canyon in Colorado—and operates over 1,300 miles of CO2 pipelines. It's a circular business model: produce CO2, transport it to oil fields, use it to extract more oil, which creates demand for more pipelines.

The beauty of this diversified toll road model reveals itself in the contract structures. Approximately 90% of Kinder Morgan's cash flow comes from fee-based contracts that aren't sensitive to commodity prices. These take several forms:

Take-or-pay contracts require customers to pay for capacity whether they use it or not. A utility might contract for 500 million cubic feet per day of pipeline capacity to ensure it can meet peak winter demand, paying for that capacity year-round even if it only uses it a few dozen days per year.

Cost-of-service contracts allow Kinder Morgan to recover its invested capital plus a regulated return, similar to how electric utilities operate. These contracts, common on interstate pipelines, provide極其 stable returns regardless of throughput volumes.

Fee-based contracts charge fixed fees per unit transported. Whether natural gas costs $2 or $20, Kinder Morgan receives the same 50 cents per thousand cubic feet for transportation.

This contract structure insulates Kinder Morgan from the commodity price volatility that devastates exploration and production companies. During the 2014-2016 oil price collapse, when crude fell from $107 to $26 per barrel, dozens of E&P companies went bankrupt. Kinder Morgan's revenues barely budged.

The operational philosophy that governs this vast network remains remarkably consistent with what Kinder instituted in 1997: maximize efficiency, minimize risk, and prioritize reliability over growth. This manifests in countless ways:

Maintenance spending is non-negotiable. While competitors might defer maintenance to boost short-term earnings, Kinder Morgan religiously maintains its assets. This isn't altruism—it's economics. A pipeline failure can cost hundreds of millions in cleanup, lawsuits, and lost revenue. Preventive maintenance costs a fraction of that.

Technology deployment is selective but effective. The company uses sophisticated pipeline inspection tools called "smart pigs" that travel through pipelines detecting corrosion, cracks, and other defects before they become problems. Drone inspections reduce the need for helicopter flyovers. Automated control systems allow a handful of operators to manage thousands of miles of pipeline.

Capital allocation remains disciplined. Every growth project must clear specific return hurdles—typically 3-5 times EBITDA for acquisitions and 6-8 times EBITDA for new construction. Projects that don't meet these thresholds don't get built, regardless of strategic considerations or competitive pressures.

The result is a business model that Warren Buffett would appreciate: simple, predictable, and durable. It's telling that when Buffett's Berkshire Hathaway bought Northern Natural Gas from Enron's bankruptcy, it operated the pipeline using essentially the same model Kinder Morgan employs. Great business models, like great pipelines, don't need frequent replacement—they just need proper maintenance.

VIII. The Trans Mountain Saga & Canadian Exit

The protest camp outside Kinder Morgan's Burnaby Terminal looked like a small city by March 2018. Hundreds of tents, a makeshift kitchen, and a stage for daily rallies had transformed the industrial site into ground zero of Canada's climate wars. Indigenous leaders, environmental activists, and local politicians had maintained a blockade for months, preventing construction crews from beginning work on the Trans Mountain Pipeline expansion. Richard Kinder, watching from Houston, faced a decision that would have been unthinkable when he bought Terasen thirteen years earlier: should he abandon a $7.4 billion project that had already consumed $1 billion and years of planning?

The Trans Mountain expansion had seemed like a classic Kinder Morgan play when formally proposed in 2013. In 2013, Kinder Morgan filed its application to the Canadian National Energy Board (NEB) for building a second pipeline roughly parallel to the existing Trans Mountain, for transporting diluted bitumen between Edmonton, Alberta, and Burnaby, British Columbia. The new pipeline would nearly triple the transportation capacity from 300,000 to 850,000 barrels per day, for an estimated investment of $6.8 billion.

The economics were compelling. Western Canadian oil was selling at massive discounts to global prices—sometimes $30-40 per barrel—because of insufficient pipeline capacity to reach export markets. The expansion would essentially twin the existing Trans Mountain route, following the same right-of-way for most of its length. Asian refiners were eager for Canadian heavy oil. The project had support from the federal government and Alberta. What could go wrong?

Everything, as it turned out.

The first signs of trouble came from British Columbia's newly elected NDP government in 2017, which had campaigned on opposing the pipeline. Premier John Horgan announced his government would use "every tool in the toolbox" to stop the expansion, including regulatory challenges, permit delays, and legal battles. Municipalities along the route passed bylaws making construction difficult or impossible. First Nations groups split, with some supporting the economic benefits and others opposing on environmental and sovereignty grounds.

But the real shock came from the streets. What had been sporadic protests escalated into sustained civil disobedience. Thousands of arrests were made. Construction sites were occupied. Kinder Morgan's employees faced harassment. The situation was unlike anything the company had encountered in the United States, where pipeline opposition, while present, rarely reached this intensity.

The financial implications were staggering. Every month of delay added tens of millions in costs. The original $5.4 billion budget ballooned to $7.4 billion, then higher. International investors began questioning whether Canada was a reliable place to build energy infrastructure. Kinder Morgan's share price, which had weathered the oil price collapse, began to suffer from Trans Mountain uncertainty. On April 8, 2018, Kinder delivered an ultimatum that stunned both Ottawa and the energy sector. Kinder Morgan suspended "non-essential" activities relating to the pipeline, as the company did not want to "put [its] shareholders at risk on the remaining project spend". The company stated that it would attempt to reach agreements on a funding plan with stakeholders by May 31. The message was clear: without government intervention, Trans Mountain was dead.

What followed was one of the most extraordinary transactions in Canadian business history. The Liberal government agreed to buy the Trans Mountain pipeline and related infrastructure for $4.5 billion. Finance Minister Bill Morneau announced details of the agreement reached with Kinder Morgan, framing the short-term purchase agreement as financially sound and necessary to ensure a vital piece of energy infrastructure gets built.

On August 31, 2018, the Government of Canada purchased the pipeline for $4.7 billion from Kinder Morgan through the creation of the Trans Mountain Corporation (TMC), in order to "keep the project alive". For Kinder Morgan, it was a masterful exit—recovering their investment plus a profit while avoiding years of additional political risk and capital expenditure.

The irony was thick: a company built on acquiring government-divested assets was now selling assets back to government. But for Kinder, it was a rational decision. The Canadian regulatory and political environment had become incompatible with private infrastructure investment. The skills that had built Kinder Morgan—operational excellence, financial discipline, stakeholder management—couldn't overcome fundamental political opposition.

The Trans Mountain sale wasn't the end of Kinder Morgan's Canadian retreat. In May 2017, KMI completes an initial public offering of Kinder Morgan Canada Limited (TSX: KML). The proceeds are used by KML to indirectly acquire an approximate 30% interest in a limited partnership from KMI that holds the Canadian business of Kinder Morgan But even this entity wouldn't survive long. In December 2019, the Pembina Pipeline Corporation acquires the U.S. portion of the Cochin Pipeline and the outstanding common equity of KML, including the 70% majority voting interest held by KMI

The Canadian exit represented more than just a strategic retreat—it was a philosophical statement about the limits of private infrastructure investment in politically charged environments. Kinder Morgan had always succeeded by focusing on the economics of moving molecules, not the politics. When politics overwhelmed economics, it was time to leave.

The Trans Mountain saga also highlighted the growing challenges facing fossil fuel infrastructure globally. What had once been seen as essential national infrastructure was increasingly viewed through the lens of climate change and Indigenous rights. The toll road model that had worked so well for decades was colliding with a changing world.

Yet the financial outcome vindicated Kinder's discipline. While other companies might have stubbornly persisted, pouring good money after bad, Kinder Morgan cut its losses and redeployed capital to more favorable opportunities in the United States. The company that had started with a $40 million bet on unwanted assets had shown it knew when to fold a losing hand.

As Kinder Morgan's Canadian chapter closed, the Trans Mountain expansion project continued under government ownership, eventually costing over $30 billion—more than four times the original estimate. The pipeline that Kinder Morgan sold for $4.5 billion had become a $30 billion government project, a sobering reminder of the value of knowing when to walk away.

IX. Energy Transition & Modern Strategy

The conference room at Kinder Morgan's Houston headquarters hummed with tension in early 2021. Outside, Texas was recovering from Winter Storm Uri, which had devastated the state's power grid just weeks earlier. Inside, executives were reviewing numbers that seemed almost surreal: Kinder Morgan had just posted a nearly $1 billion one-time profit from a natural disaster that had left millions without power and caused hundreds of deaths. The company had voluntarily curtailed its own power consumption, saving $116 million, while selling natural gas at spot prices that had spiked from $3 to over $400 per million British thermal units, generating $880 million in windfall profits.

An analyst at Mizuho Securities said Kinder Morgan "was not really on anyone's list of potential winners from Winter Storm Uri. Shame on us [for not seeing it]"

The Uri windfall crystallized a fundamental reality about Kinder Morgan's position in the energy transition: the company owned irreplaceable infrastructure that became even more valuable during system stress. While politicians debated renewable mandates and environmentalists protested pipelines, the physics of energy delivery remained unchanged. Natural gas was still needed to heat homes, power factories, and increasingly, to backup intermittent renewable generation.

But Kinder, now 77 and still at the helm, understood that ignoring the energy transition would be as foolish as embracing it wholesale. The solution was characteristically pragmatic: adapt existing infrastructure for new energy sources while continuing to profit from traditional hydrocarbons. In 2021, KMI forms the Energy Transition Ventures group. Shortly thereafter, Kinetrex Energy was acquired, marking Kinder Morgan's entry into the landfill-based Renewable Natural Gas (RNG) businessThe Kinetrex acquisition represented a calculated bet on the energy transition. In August 2021, Kinder Morgan made a significant move into the RNG market by acquiring Kinetrex Energy for $310 million. The acquisition includes two small scale, domestic LNG production and fuelling facilities, a 50% interest in a landfill-based renewable natural gas (RNG) facility in Indiana, and signed commercial agreements for three additional RNG facilities

The logic was quintessentially Kinder: use existing infrastructure and expertise to capture new revenue streams without abandoning core businesses. RNG—essentially methane captured from landfills, wastewater treatment plants, and agricultural operations—could flow through the same pipelines as conventional natural gas. The molecules were identical; only the source differed. By capturing methane produced from the decomposition of organic waste, the RNG production process reduces or eliminates greenhouse gas emissions. In August 2022, Kinder Morgan further expanded its RNG footprint by acquiring North American Natural Resources Inc. (NANR) for $135 million. The $135 million acquisition in combined purchase price and related transaction costs includes seven landfill gas-to-power facilities in Michigan and Kentucky. Shortly following close, KMI will make a final investment decision (FID) on the conversion of up to four of the seven gas-to-power facilities to renewable natural gas (RNG) facilities with a capital spend of approximately $175 million.

These acquisitions were projected to add approximately 2 Bcf of RNG to KMI's annual production. The combined RNG operations will provide KMI with annual RNG generation capacity of approximately 7.7 Bcf per year once all of the RNG facilities are in service.

The RNG strategy wasn't about abandoning fossil fuels—it was about owning the infrastructure that would be needed regardless of which molecules flowed through it. As ETV President Jesse Arenivas explained, "We have been focused on RNG due to its potential to grow rapidly in the near term and deliver attractive returns, with landfills providing a low cost, predictable and long-term feedstock."

Meanwhile, the core business continued to benefit from the energy transition in unexpected ways. Natural gas demand was surging, driven not by traditional uses but by new sources: data centers powering artificial intelligence, cryptocurrency mining operations, and most importantly, gas-fired power plants backing up intermittent renewable generation. Every solar farm and wind project increased the need for quick-start gas generation to maintain grid stability.

The company's current growth projects reflect this dual strategy. Major pipeline expansions continue, with billions allocated to traditional infrastructure. The Mississippi Crossing Project, approved in 2024, will deliver up to 1.5 Bcf/d to Southeast U.S. markets by 2028. The Trident Intrastate Pipeline, a $1.7 billion project spanning 216 miles, will enhance natural gas transportation between Katy, Texas, and the Gulf Coast's LNG and industrial hub near Port Arthur.

But alongside these traditional projects, Kinder Morgan is positioning for multiple energy futures. The company's CO2 business, long focused on enhanced oil recovery, is being reimagined for carbon capture and sequestration. The same pipelines that transport CO2 to oil fields could transport captured carbon to permanent storage sites. The terminals that store petroleum products could be converted to handle hydrogen or ammonia.

The strategic brilliance lies in the optionality. Kinder Morgan isn't betting on a specific energy future—it's positioning to profit from any energy future. If renewables dominate, the company provides backup gas generation and RNG. If hydrogen emerges, the pipelines can be retrofitted. If fossil fuels persist longer than expected, the core infrastructure remains essential.

This pragmatic approach to the energy transition reflects the same discipline that built the company. No grand proclamations about saving the planet. No virtue signaling about abandoning fossil fuels. Just a clear-eyed assessment of where energy markets are heading and how to profit from the transition.

As 2024 unfolds, Kinder Morgan finds itself in an enviable position. The company that started by buying unwanted pipelines for $40 million now operates critical infrastructure worth tens of billions. The energy transition, rather than threatening this empire, has created new opportunities for growth. Natural gas, once thought to be a bridge fuel, increasingly looks like a destination fuel—essential for balancing renewable grids, powering data centers, and providing industrial heat.

The Winter Storm Uri windfall, while controversial, demonstrated a fundamental truth: when energy systems are stressed, infrastructure owners win. As the energy transition creates more volatility—from renewable intermittency, extreme weather, and changing demand patterns—the value of reliable infrastructure only increases. Kinder Morgan, with its vast network and operational excellence, stands ready to capture that value.

X. Playbook: Business & Investing Lessons

The PowerPoint slide that Richard Kinder displays at every investor presentation contains a single chart that tells the entire story. Since creating Kinder Morgan in 1997, the company has increased distributions to shareholders at a 40 percent compounded annual growth rate. No energy company in America can match that record. The secret isn't complicated—it's disciplined execution of simple principles that most companies find impossible to maintain.

Lesson 1: The Power and Peril of Financial Innovation

The Master Limited Partnership structure that Kinder pioneered was a stroke of genius—until it wasn't. For seventeen years, the MLP model provided Kinder Morgan with a sustainable competitive advantage. The tax efficiency meant every dollar of operating cash flow was worth more to KMP unitholders than to shareholders of taxable corporations. The yield-seeking investor base provided patient capital at attractive rates. The requirement to distribute cash enforced discipline on capital allocation.

But Kinder understood something crucial: financial structures are tools, not strategies. When the MLP structure began constraining growth and limiting investor access, he didn't hesitate to abandon it. The 2014 consolidation, while painful for some investors, demonstrated that operational excellence matters more than financial engineering. The companies that slavishly copied Kinder's MLP structure but lacked his operational discipline learned this lesson the hard way during the 2014-2016 oil price collapse.

Lesson 2: Capital Discipline in a Capital-Intensive Business

Every pipeline company talks about capital discipline. Kinder Morgan lives it. The company's hurdle rates—3-5 times EBITDA for acquisitions, 6-8 times for new construction—haven't changed in twenty years. Projects that don't meet these thresholds don't get built, regardless of strategic importance or competitive dynamics.

This discipline extends to the balance sheet. Kinder maintains leverage around 4.0-4.5 times debt-to-EBITDA, providing financial flexibility without excessive risk. During the 2020 pandemic, when energy demand collapsed, Kinder Morgan cut its dividend—a decision that shocked investors accustomed to decades of increases. But the cut preserved capital, protected the balance sheet, and positioned the company to emerge stronger. By 2024, the dividend had been restored and was growing again.

The lesson: in commodity-exposed businesses, balance sheet strength matters more than earnings growth. Companies that stretch for growth eventually break.

Lesson 3: The Toll Road Model

Kinder's greatest insight was recognizing that pipelines aren't in the energy business—they're in the transportation business. This distinction is crucial. Energy producers face commodity price risk, demand uncertainty, and technological disruption. Transportation providers face none of these risks if structured properly.

Approximately 90% of Kinder Morgan's cash flow comes from fee-based contracts insensitive to commodity prices. Whether natural gas costs $2 or $20, oil trades at $30 or $130, Kinder Morgan collects its transportation fee. This toll road model provides remarkable stability through commodity cycles.

But the model requires discipline. The temptation to take commodity exposure—through storage plays, trading operations, or unhedged processing—is constant. Kinder Morgan occasionally succumbs, as with the Winter Storm Uri windfall, but these remain exceptions. The core business remains boringly predictable, exactly as investors want it.

Lesson 4: Regulatory Moats and Natural Monopolies

Warren Buffett loves businesses with moats. Kinder Morgan's moats are literal—regulatory barriers that make pipeline competition nearly impossible. Building a new interstate pipeline requires years of permitting, environmental reviews, and legal challenges. Even with permits, construction faces opposition from landowners, environmentalists, and competing interests.

These regulatory moats create natural monopolies. Once a pipeline is built, it's virtually impossible to compete against it. The economics of building a parallel pipeline rarely make sense. This dynamic gives incumbent pipeline owners tremendous pricing power, limited only by regulation.

Kinder understood this dynamic from day one. Every acquisition targeted strategic assets that couldn't be replicated. The Natural Gas Pipeline of America serving Chicago. The Trans Mountain pipeline to the Pacific. The Products Pipelines serving California. These aren't just pipelines—they're irreplaceable infrastructure with decades of protected cash flow.

Lesson 5: Culture as Competitive Advantage

"We wanted to drive home one culture here: Cheap. Cheap. Cheap," Kinder told Fortune magazine. This wasn't just cost-cutting—it was cultural transformation. At Enron, executives flew private jets and built monuments to their egos. At Kinder Morgan, the CEO flies coach and takes a $1 salary.

This culture permeates every level. Field operators are empowered to make decisions but held accountable for results. Engineers are rewarded for finding efficiencies, not building empires. Executives eat in the company cafeteria, not private dining rooms.

The result is an operating efficiency that competitors can't match. Kinder Morgan operates with fewer employees per mile of pipeline than any major competitor. Maintenance costs are lower. Administrative expenses are minimal. These advantages compound over time, creating a widening gap between Kinder Morgan and less disciplined operators.

Lesson 6: The Enron Shadow—What Not to Do

Perhaps Kinder Morgan's greatest advantage is what it learned from Enron's collapse. Having witnessed the destruction of mark-to-market accounting, special purpose entities, and off-balance-sheet financing, Kinder built a company on opposite principles:

- Real assets generating real cash flow, not paper profits from derivative trades

- Simple, transparent accounting that a retail investor can understand

- Conservative leverage that can withstand commodity price collapse

- Management incentives aligned with long-term value, not quarterly earnings

The lessons from Enron extend beyond financial engineering. Kinder saw how a culture of arrogance and entitlement destroyed one of America's most admired companies. He built Kinder Morgan on humility and discipline, values that seem quaint but prove durable.

Lesson 7: Timing and Optionality

Kinder's career demonstrates impeccable timing. He left Enron just before its trading culture destroyed the company. He pioneered MLPs just as yield-seeking investors needed alternatives to low bond yields. He consolidated the MLP structure just before the oil price collapse made the model unsustainable. He entered renewable natural gas just as ESG pressures intensified.

But this isn't luck—it's optionality. Kinder Morgan maintains strategic flexibility to adapt to changing conditions. The company doesn't bet everything on a single strategy or commodity. When conditions change, Kinder Morgan changes with them.

This optionality extends to the asset base. Pipelines can carry different products. Terminals can store different commodities. Rights-of-way can accommodate new infrastructure. This flexibility provides resilience through energy transitions.

Lesson 8: The Power of Compounding

Since its founding, Kinder Morgan has generated total returns exceeding 1,000% for long-term shareholders. This isn't from discovering oil or inventing new technology—it's from the relentless compounding of predictable cash flows reinvested at attractive returns.

Every acquisition adds incremental cash flow. Every efficiency improvement drops to the bottom line. Every contract renewal provides pricing power. These small improvements compound over decades into extraordinary wealth creation.

The key is patience. Pipeline investing isn't exciting. There are no "ten-baggers" or moonshots. Just steady, predictable, boring returns that compound into fortune over time. In a world obsessed with disruption and innovation, Kinder Morgan proves that executing the basics brilliantly beats chasing the next big thing.

XI. Analysis & Future Outlook

The investment thesis for Kinder Morgan in 2025 reads like a Rorschach test for energy investors. Bulls see irreplaceable infrastructure benefiting from AI-driven power demand and LNG exports. Bears see stranded assets in a decarbonizing world. Both might be right—just on different timelines.

The Bull Case: Infrastructure for Multiple Energy Futures

The optimistic view starts with a simple observation: America needs more energy, not less. Data centers powering artificial intelligence are projected to consume 35 gigawatts of additional power by 2030—equivalent to the entire electricity consumption of New York State. These facilities require 24/7 reliability that renewables alone cannot provide. Natural gas, transported through Kinder Morgan's pipelines, provides the instant dispatchable power these facilities demand.

LNG exports represent another demand driver. The United States has become the world's largest LNG exporter, shipping over 14 billion cubic feet per day to global markets. Every molecule of that gas travels through pipelines to reach export terminals. Kinder Morgan's Gulf Coast pipeline network is ideally positioned to capture this growth, with multiple expansion projects targeting LNG feed gas delivery.

The financials support the bullish narrative. At current valuations around 11-12 times EV/EBITDA, Kinder Morgan trades at a discount to historical averages and pipeline peers. The dividend yield of approximately 5.5% is well-covered by cash flow, with a coverage ratio exceeding 2.0x. The balance sheet has been deleveraged to 4.0x net debt/EBITDA, providing flexibility for growth investments or shareholder returns.

Perhaps most compelling is the replacement cost argument. Kinder Morgan's 79,000 miles of pipelines would cost over $200 billion to replicate at today's construction costs—assuming you could even get permits, which is increasingly doubtful. The company trades at a fraction of replacement value, suggesting significant upside if energy infrastructure scarcity increases.

The Bear Case: Stranded Assets and Transition Risk

The pessimistic view focuses on long-term demand destruction. Electric vehicles are reducing gasoline demand, with U.S. gasoline consumption potentially peaking in 2025. Heat pumps are displacing natural gas furnaces. Renewable electricity is becoming cheaper than gas-fired generation in many markets. The energy transition isn't coming—it's here.

Regulatory risks are mounting. The Federal Energy Regulatory Commission (FERC) faces pressure to deny pipeline certificates. States like New York and California actively obstruct new pipeline construction. Environmental litigation has become more sophisticated and successful, as demonstrated by the Trans Mountain saga.

The capital intensity of the business model presents challenges. Kinder Morgan must continuously invest billions to maintain and expand its network. As cash flows from legacy assets decline, finding attractive reinvestment opportunities becomes harder. The company's 2025 capital budget of $2.4 billion represents about 30% of EBITDA—a significant reinvestment requirement that pressures shareholder returns.

ESG pressures are intensifying. Major institutional investors are reducing or eliminating fossil fuel infrastructure investments. Banks face pressure to stop financing pipeline projects. Insurance companies are withdrawing coverage. These pressures increase Kinder Morgan's cost of capital and limit strategic flexibility.

Competition and Market Dynamics

Kinder Morgan faces formidable competitors. Enterprise Products Partners (EPD) boasts a superior balance sheet and more integrated operations. TC Energy (TRP) dominates Canadian gas exports. Williams Companies (WMB) controls critical Transco pipeline serving the Atlantic coast.

The competitive landscape is evolving beyond traditional players. Electric transmission companies are competing for the same capital and serving similar reliability needs. Renewable developers with battery storage are displacing gas peaker plants. Even technology companies like Google and Microsoft are investing directly in energy infrastructure.

Market dynamics are shifting unfavorably. Pipeline capacity additions have outpaced demand growth in key regions, pressuring utilization and rates. The Permian Basin, once constrained, now has excess takeaway capacity. The Marcellus/Utica region similarly shifted from shortage to surplus. This overcapacity limits pricing power and return potential.

Natural Gas: Bridge or Destination?

The future of Kinder Morgan ultimately depends on natural gas's role in the energy transition. The "bridge fuel" narrative suggests gas is a temporary solution while renewables scale. The "destination fuel" narrative argues gas remains essential for grid reliability, industrial processes, and chemical feedstock indefinitely.

Current evidence supports the destination fuel thesis, at least for the next decade. Natural gas power generation is growing, not shrinking. U.S. gas demand reached record highs in 2024. LNG exports are projected to double by 2030. Industrial reshoring requires reliable gas supply. Even aggressive renewable scenarios require gas backup through 2040.

But technology wildcards could disrupt this outlook. Breakthrough battery storage could eliminate the need for gas peakers. Small modular nuclear reactors could provide reliable baseload without emissions. Green hydrogen could replace industrial gas consumption. These technologies remain expensive and unproven, but so were shale drilling and solar panels twenty years ago.

Capital Allocation and Shareholder Returns

Management's capital allocation priorities provide insight into their outlook. The 2025 plan allocates growth capital primarily to natural gas infrastructure (60%), with smaller allocations to products pipelines (20%), terminals (15%), and energy transition ventures (5%). This suggests management sees gas infrastructure as the highest return opportunity despite transition risks.

Shareholder returns remain robust. The dividend of $1.17 per share annually represents a 5.5% yield. Share buybacks have been modest but consistent, retiring 2-3% of shares annually. Total shareholder returns have averaged 12-15% annually over the past five years, outperforming utilities but lagging technology stocks.

The key question is sustainability. Can Kinder Morgan maintain these returns as energy systems transform? The company's track record suggests yes—it has navigated the shale revolution, oil price collapses, and a pandemic while maintaining distributions. But past performance doesn't guarantee future results, especially amid fundamental energy transition.

The Verdict: Tactical Long, Strategic Uncertain

For investors with a 3-5 year horizon, Kinder Morgan appears attractive. Natural gas demand will grow through 2030. The existing infrastructure is irreplaceable and essential. The valuation is reasonable, the yield is attractive, and the balance sheet is strong. This is a classic value investment in an unfashionable sector.

For investors with a 10-20 year horizon, the outlook is murkier. Will natural gas pipelines be the coal mines of 2040—stranded assets in a decarbonized economy? Or will they carry hydrogen, renewable natural gas, and captured carbon in a net-zero world? The answer depends on technology development, policy decisions, and consumer behavior—all highly uncertain.

Kinder Morgan is essentially a bet on American energy pragmatism triumphing over energy idealism. It's a wager that physics and economics matter more than politics and promises. History suggests this is a reasonable bet. But then again, history also suggested that coal would remain king.

XII. Epilogue: The Kinder Legacy

On a crisp October morning in 2022, Richard and Nancy Kinder stood before Rice University's president as a crowd of students and faculty applauded. The couple had just announced their latest gift: $50 million to expand the Kinder Institute for Urban Research. Combined with previous donations, the Kinders had now given over $70 million to Rice alone. It was a fortune built on pipelines, distributed through philanthropy—a uniquely American story of capitalism and conscience.

The Kinders founded the Kinder Foundation in an effort to support Greater Houston. As of December 2022, the Kinder Foundation has given more than $506.9 million in gifts. The foundation's focus—urban parks, education, quality of life—reflects a pragmatic approach to philanthropy that mirrors Kinder's approach to business. No moonshots or grand visions, just practical investments in community infrastructure.

The majority of Kinder's fortune comes from a 12% stake in Kinder Morgan. He owns about 12% of the company in his own name, his wife's name and through a limited partnership he controls. The billionaire has collected more than $2 billion worth of dividends from Kinder Morgan. Forbes estimates his net worth at approximately $7.8 billion, making him one of America's wealthiest energy executives.

Yet wealth was never the primary motivation. In interviews, Kinder speaks less about money and more about building something enduring. The company that started with $40 million in cast-off assets now operates infrastructure that literally powers American life. Every time someone in Chicago turns on their heat, drives on California highways, or powers up a data center in Texas, they're likely using energy that flowed through Kinder Morgan's network.

The story of building from Enron's ruins carries profound lessons about American capitalism. Enron represented capitalism's worst excesses—financial engineering divorced from real value creation, a culture of arrogance and entitlement, and executives who enriched themselves while destroying shareholder value. Its collapse shattered trust in corporate America and led to Sarbanes-Oxley and enhanced regulation.

Kinder Morgan represents capitalism's redemption. It proved that creating real value for customers, employees, and shareholders remained possible. That operational excellence beats financial engineering. That discipline and frugality create more wealth than excess and speculation. That boring businesses solving real problems generate better returns than exciting companies chasing phantoms.

The contrast between Kinder's path and that of his Enron contemporaries is stark. Ken Lay died in disgrace, convicted of fraud. Jeff Skilling served twelve years in federal prison. Andy Fastow became a cautionary tale taught in business schools. Meanwhile, Kinder built one of America's great fortunes through entirely legal and ethical means. The plodding tortoise beat the clever hares.

As Kinder, now 80, gradually steps back from day-to-day operations, questions about succession and strategy loom. Can Kinder Morgan maintain its culture without its founder's presence? Will new leadership pursue growth over discipline? Can the company navigate the energy transition while remaining true to its infrastructure roots?

The early signs are encouraging. CEO Steven Kean, who joined from Enron but absorbed Kinder's lessons, maintains the conservative approach. The company has avoided the mega-deals and transformative acquisitions that often destroy value. The focus remains on operational excellence and shareholder returns rather than empire building.

The energy transition presents both the greatest risk and opportunity in Kinder Morgan's history. The company that thrived through multiple energy cycles must now navigate the potential transformation of energy itself. But if history is any guide, Kinder Morgan will adapt through pragmatism rather than ideology, focusing on what works rather than what's popular.

Reflecting on the journey from Enron's ashes to infrastructure empire, several themes emerge:

Resilience Through Simplicity: While competitors pursued complex financial structures and exotic strategies, Kinder Morgan stuck to simple principles: own good assets, operate them efficiently, and share the proceeds with investors. This simplicity proved remarkably resilient through multiple crises.

Value in the Unfashionable: Kinder's greatest returns came from buying what others didn't want—Enron's cast-off pipelines, El Paso during bankruptcy fears, Canadian assets amid political opposition. The ability to see value where others see problems created extraordinary wealth.

The Compound Effect: Small improvements, consistently applied over decades, created enormous value. A 1% efficiency gain here, a 2% cost reduction there, a 3% volume increase elsewhere—these marginal gains compounded into billions of shareholder value.

Culture as Strategy: The cheap, disciplined, accountable culture wasn't just about saving money—it was a competitive advantage that competitors couldn't replicate. Every employee flying coach while competitors flew first class saved money, but more importantly, it reinforced values.

What the Kinder Morgan story ultimately teaches is that American capitalism, despite its flaws, rewards those who create genuine value. In an era of SPACs, meme stocks, and cryptocurrency speculation, Kinder Morgan stands as a reminder that building real businesses solving real problems remains the surest path to enduring wealth.

The pipelines that Kinder assembled will likely outlive him, carrying energy—in whatever form it takes—for decades to come. The fortune he created will continue flowing through philanthropic channels, improving Houston and beyond. The company he built from Enron's ashes will continue generating cash for shareholders, pensioners, and endowments.

This is Richard Kinder's legacy: proof that in American capitalism, discipline beats genius, operations beat financial engineering, and tortoises beat hares—given enough time and the right track. It's a legacy built not on revolutionary innovation or charismatic leadership, but on the decidedly unsexy business of moving molecules through pipes. And perhaps that's the greatest lesson of all: in business, as in life, the boring fundamentals matter more than the exciting possibilities.

As America grapples with its energy future—balancing climate concerns with economic needs, idealism with pragmatism—Kinder Morgan stands ready to provide the infrastructure for whatever path the nation chooses. The company that rose from Enron's ashes has become too essential to fail, too valuable to abandon, and too pragmatic to ignore.

The empire of pipes endures.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube