Kimco Realty Corporation: The Architects of the Modern REIT and the Battle for the Open-Air Shopping Center

I. Episode Introduction & The Grand Thesis

Picture the American suburb on a Saturday morning. A minivan pulls into a parking lot the size of a small farm. Inside the low-slung building at the far end, a Kroger or a Publix hums with shoppers filling carts. Flanking it, a TJ Maxx, a nail salon, an urgent-care clinic, a taco spot with a line out the door. Nobody photographs this place. Nobody writes love letters to the strip mall. And yet this unglamorous rectangle of concrete and asphalt is one of the most quietly resilient assets in American finance—and for more than six decades, one company has been assembling these rectangles at industrial scale.

That company is Kimco Realty Corporation, listed on the New York Stock Exchange under the ticker KIM. As of the end of 2024 it held interests in 568 shopping-center properties totaling roughly 101 million square feet of gross leasable area across 30 states, making it the largest publicly traded owner and operator of open-air, grocery-anchored shopping centers in the United States.1 By mid-2026 its equity was worth roughly $17 billion. It is not a household name. Its tenants are.

Here is the paradox that makes Kimco worth two hours of your attention. For most of the 2010s, the dominant narrative in retail was death. E-commerce was going to eat the store. The "Retail Apocalypse" filled headlines—Toys "R" Us, Sears, Payless, a graveyard of banners. Physical retail real estate was supposed to be a melting ice cube. Instead, the open-air, grocery-anchored format did something the enclosed regional mall did not: it survived, and then it thrived. By early 2026 Kimco reported leased occupancy of 96.3%, new-lease rent spreads of nearly 24%, and a signed-but-not-yet-open lease pipeline at an all-time company record—hardly the vital signs of a dying asset class.2 The question this episode keeps returning to is why the consensus was so wrong, and whether the current optimism is itself the next thing to be wrong about.

The distinction that the apocalypse narrative missed is the difference between a shopping destination and a shopping convenience. The enclosed regional mall was a destination—you drove to it, spent an afternoon, and its economic logic depended on that afternoon being pleasant enough to compete with the couch and the smartphone. The open-air grocery center never asked for the afternoon. It asked for six minutes: park, grab the prescription, grab the rotisserie chicken, leave. When Amazon offered a better version of the afternoon, the destination lost. But Amazon never offered a better version of the six-minute errand, because the physics of fresh food, immediate need, and human services do not compress into a cardboard box on a doorstep. Kimco's entire history is a wager that the six-minute errand is one of the most defensible pieces of economic real estate in America. The wager looks smart today. Whether it is smart because of enduring structure or merely because of a favorable moment in the cycle is the tension a serious investor has to sit with for the length of this story.

To understand Kimco is to understand four intertwined stories, and this episode is organized around them. The first is a piece of financial engineering: Kimco's 1991 initial public offering, which historians of the sector credit with igniting the modern equity REIT era and unlocking the flood of institutional capital that reshaped how Americans finance the buildings they shop in.3 The second is a thesis about human behavior—that people will always need to buy groceries, fill prescriptions, and get a haircut, and that a shopping center anchored by necessity is structurally sturdier than one anchored by discretionary desire. The third is a piece of opportunistic merchant banking: how a roughly $180 million bet on a distressed grocery chain called Albertsons was harvested for more than $1.7 billion in cash. And the fourth is consolidation—the multibillion-dollar absorptions of Weingarten Realty in 2021 and RPT Realty in 2024 that turned Kimco into the scale leader of its niche.

It is worth naming the analytical posture this episode takes, because Kimco is a company that inspires cheerleading. Its own investor materials are polished, its management is articulate and consistent, and its recent results are genuinely strong. None of that is the same as an investment case. Management is paid to be confident; the reader is not. So throughout, the discipline is to separate what Kimco has proven from what it merely asserts—to treat "our pipeline will convert to cash flow" and "our redevelopment will earn high yields" and "the market undervalues us" as claims to be tested against evidence, not as facts because a CEO said them on a call.

None of these stories is a straight line, and none proves that Kimco will keep winning. A neutral observer has to hold two ideas at once: the format is genuinely advantaged right now, and much of that advantage is cyclical, capital-intensive, and sensitive to interest rates in ways that management's confident tone tends to underplay. So let us start where the company started—not in a boardroom, but with two men, a lawyer and a builder, who decided that the boring business of the strip center was the business worth being in.

II. Milton Cooper, Martin Kimmel, and the Birth of Kimco

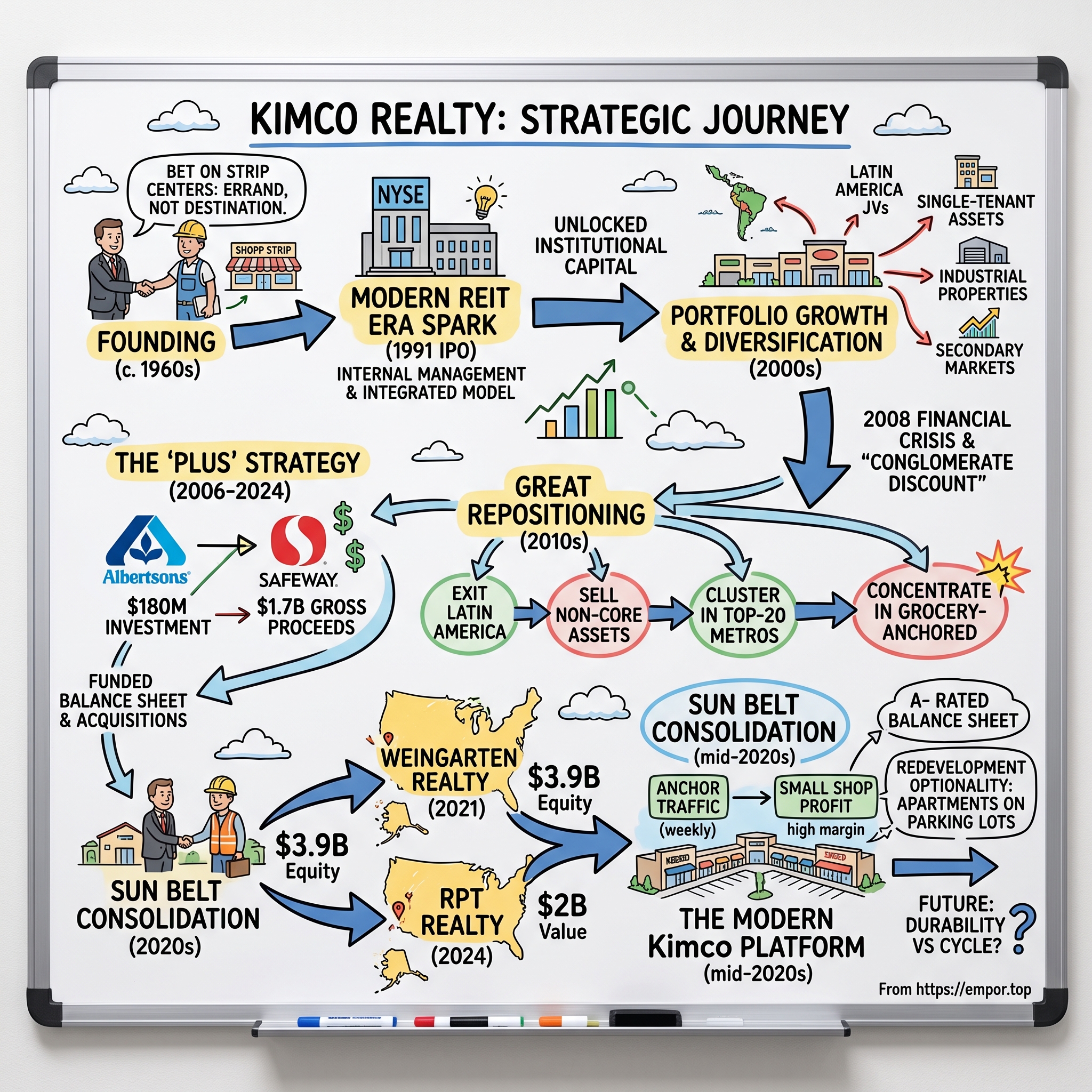

The origin story of Kimco does not feature a garage or a dorm room. It features a title search. Milton Cooper was a real estate attorney in New York—a lawyer's lawyer, precise, patient, and temperamentally allergic to hype. Martin Kimmel was a developer, a man who liked to build things and put tenants in them. Around 1960 the two began working together, pooling retail properties, and over the following years their partnership coalesced into a company whose name was a simple contraction of Kimmel and Cooper: Kim-co. The corporate lineage that became today's Kimco traces to the mid-1960s, with the entity later formally incorporated as the enterprise grew.3 The name is almost aggressively unromantic, which turns out to be a tell about the whole philosophy.

While a generation of American developers in the 1960s and 1970s chased the glamour of the enclosed regional shopping mall—climate-controlled cathedrals of consumption, all fountains and skylights and department-store anchors—Cooper and Kimmel went the other way. They bet on the open-air "strip" center: a row of stores facing a parking lot, no roof over the walkway, no soaring atrium. It was the architectural equivalent of a pickup truck. And that was exactly the point. The enclosed mall was a bet on shopping as entertainment and destination. The strip center was a bet on shopping as errand.

The underlying thesis was almost embarrassingly simple, and Cooper repeated versions of it for the rest of his career: anchor the center with a supermarket, a pharmacy, or a discount department store, because those are the things people have to buy. A family in a recession still needs milk, bread, and antibiotics. It may skip the trip to the mall for a new blazer; it does not skip the trip for dinner. Necessity-based retail, the logic went, would be less volatile across the economic cycle than the fashion-and-leisure retail that filled the enclosed malls. This is not a sophisticated insight. Its power came from being applied with discipline over sixty years, in an industry that repeatedly found more exciting things to do.

There is a temperamental dimension to this worth dwelling on, because it explains the whole company. Cooper was, by every account, a patient man in an impatient business. Real estate development has always attracted a certain kind of operator—the promoter who falls in love with the building, the visionary who wants his name on a skyline. Cooper was the opposite. He treated real estate as arithmetic wrapped in law: what does the land cost, what will the tenant pay, how durable is that payment, and what is the margin of safety if the tenant leaves? A lawyer by training, he was preoccupied with downside—with the lease clause, the co-tenancy provision, the recapture right—in a way that developers chasing the upside routinely were not. That defensive instinct is the through-line from the first strip center to the "fortress balance sheet" language management still uses today.

To appreciate why what came later was revolutionary, you have to understand the sorry state of the REIT before Kimco reshaped it. Congress created the real estate investment trust in 1960, the same era Cooper and Kimmel were getting started, with a clean idea: let ordinary investors own income-producing real estate the way they own stocks, and exempt the vehicle from corporate tax so long as it pays out the vast majority of its income as dividends. It was a democratizing concept. In practice, for three decades, it was a mess. Many early REITs were finite-life vehicles designed to be liquidated on a schedule. Many were externally managed—run by an outside advisor paid a fee on assets rather than on performance. Many were heavily leveraged mortgage pools that blew up spectacularly in the mid-1970s. The word "REIT," to a sophisticated 1980s investor, connoted something between a tax dodge and a landmine.

The tax bargain at the heart of the REIT structure is worth understanding in plain terms, because it dictates almost everything about how a company like Kimco behaves. A normal corporation pays tax on its profits and then, if it chooses, pays a dividend out of what remains—the money is taxed twice, once at the company and once at the shareholder. A REIT escapes the corporate layer entirely, but only by agreeing to distribute at least 90% of its taxable income to shareholders every year. That single rule is the REIT's blessing and its cage. The blessing is that far more cash reaches the owner. The cage is that the company can retain almost nothing to fund its own growth; to expand, it must go back to the capital markets, hat in hand, and issue new stock or new debt. This is why a REIT's cost of capital is not an accounting footnote but the whole ballgame—and why the vehicle that could raise permanent public equity most cheaply and credibly would win. In 1991, that vehicle did not yet exist in respectable form.

So on the eve of the 1990s, here was Kimco: a disciplined operator of a boring, resilient asset class, with a coherent thesis and a clean reputation—sitting inside an industry structure that institutional capital fundamentally did not trust. What it lacked was a way to turn that operating quality into permanent, liquid, credible capital. The vehicle to do that did not yet exist. Kimco was about to invent it, and it took a crisis to force the issue.

III. The 1991 IPO: The Spark that Ignited the Modern REIT Era

By the late 1980s, the American commercial real estate market was walking toward a cliff. The savings and loan crisis had gutted the banking system's appetite—and capacity—for real estate lending. Hundreds of S&Ls failed; the federal government stood up the Resolution Trust Corporation to dispose of the wreckage; and the spigot of bank debt that had financed a generation of shopping centers slammed shut. For an operator like Kimco, which had grown on the assumption that property debt would always be available to refinance and expand, this was existential. The old playbook—borrow from a bank, buy a center, repeat—no longer worked because the banks were gone.

Milton Cooper's response was to reach for a source of capital that did not depend on the banks at all: the public equity markets. In November 1991, Kimco went public on the New York Stock Exchange. On paper it was one more small-cap listing in a quiet market. In hindsight it was the starting gun for the modern REIT industry, because of what kind of REIT it was. Kimco came to market as the first significant public equity REIT of its era that was internally managed and fully integrated—it employed its own people to acquire, lease, and manage its own properties, rather than farming those functions out to an external advisor collecting fees.3

Why did that structural detail matter so much? Consider the incentives. An externally managed REIT pays its advisor based on assets under management. The advisor therefore makes more money the more it buys, whether or not the buying is wise—a machine engineered to grow for growth's sake. Internal management inverts the incentive: the people running the company are compensated on how the company actually performs, and their careers and, increasingly, their net worth ride on the stock. It is the difference between a fund manager clipping a fee and an owner-operator eating their own cooking. For institutions burned by the fee-extraction abuses of the 1970s REITs, this alignment was the unlock.

The second unlock was permanence. Kimco was replacing the finite-life partnership and private syndicate—structures designed to be wound down—with a permanent corporate capital base that could compound indefinitely. A pension fund could buy Kimco stock knowing the vehicle would not be liquidated out from under it on some predetermined date. The third unlock followed from the first two: liquidity and transparency. A public REIT filed audited financials, traded every day, and could be bought and sold in size. For the enormous pools of pension and mutual-fund money looking for a way to own institutional-grade real estate without buying buildings directly, Kimco offered a door that had not previously existed in credible form.

There is a human detail in the timing that is easy to miss. Kimco went public not because Cooper woke up one morning wanting to ring a bell at the NYSE, but because the private financing model he had relied on for thirty years had simply stopped functioning. The best financial innovations are frequently born of necessity rather than genius, and this one was no exception—the S&L collapse took away the old road, and Cooper's contribution was to be disciplined and credible enough that when he tried a new one, institutions believed him. A less reputable operator attempting the same maneuver in the same window would likely have failed to clear the skepticism. Reputation, accumulated over decades of boring competence, was the collateral that made the 1991 offering possible.

The market noticed, and then it copied. Within roughly three years of Kimco's listing, a wave of real estate operators brought internally managed equity REITs public, and the sector that had been a distrusted backwater began its transformation into a mainstream asset class that would eventually exceed a trillion dollars in equity market value. It is worth being precise about the claim here, because it is easy to over-credit a single company. Kimco did not invent the REIT, and it was not the only firm moving in this direction. What it did was provide the proof of concept at the right moment—demonstrating that a well-run, internally managed equity REIT could raise permanent public capital and earn institutional trust—and that proof arrived precisely when the S&L collapse had made public equity the only game in town.3

That is the analytical takeaway an investor should carry forward: Kimco's founding advantage was never a building or a location. It was a capital-markets innovation that lowered its cost of equity and gave it a structural edge in an industry starved for trustworthy vehicles. The rest of the Kimco story is, in large part, the story of what a company does—well and badly—once it has cheap, permanent capital and the temptation to deploy it. And in the 2000s, Kimco deployed it in a lot of places it would later regret.

IV. The Great Repositioning (2010–2018): Exiting Latin America and Narrowing Focus

Give a company a low cost of capital and a mandate to grow, and it will find things to buy. Through the 2000s, Kimco did exactly that, and the portfolio it assembled would today be described, charitably, as eclectic. The company pushed into joint ventures across Latin America—Mexico, Chile, Peru—chasing the demographics of a rising middle class. It accumulated interests well beyond core neighborhood strip centers: master-leased industrial properties, standalone single-tenant retail, preferred-equity positions, secondary-market centers in slower-growth towns. Management called it diversification. The market, eventually, called it something less flattering.

The reckoning came after the 2008 financial crisis. When capital is free and confidence is high, investors tolerate complexity; when both evaporate, they punish it. In the post-crisis decade, public markets developed a strong preference for the "pure play"—the focused operator whose business you could describe in one sentence and whose assets you could underwrite without a decoder ring. Kimco, a sprawling collection of geographies and property types, traded at a persistent discount to cleaner-focused shopping-center peers. This is the "conglomerate discount" in its real estate form: the market assigns a lower multiple to a dollar of earnings when that dollar arrives wrapped in complexity, foreign-currency risk, and non-core distractions.

It is worth being fair about why Kimco sprawled in the first place, because the 2000s expansion was not stupidity—it was the logic of the era taken too far. In a world of cheap capital and a rising global middle class, diversification into Mexico or Chile looked like prudent risk-spreading, and buying single-tenant and industrial assets looked like sensible yield-harvesting. The mistake was not any single acquisition; it was the aggregate loss of focus, the accumulation of a portfolio that no analyst could hold in their head and no acquirer would pay full price for. Complexity rarely arrives as one bad decision. It accretes as a series of individually defensible ones, and by the time the market punishes it, the company has forgotten how it got there.

The person who inherited the job of fixing this was Conor Flynn. Flynn had joined Kimco in 2003 and climbed the operating ranks, running the West Coast region and then the national portfolio before being named Chief Investment Officer in 2014 and Chief Executive Officer in 2016. He represented a generational and temperamental shift—an operator's operator focused on portfolio quality and simplicity rather than empire. The strategy he executed, alongside a management team that had watched the complexity discount compound for years, amounted to a deliberate act of corporate subtraction.

The most visible move was the exit from Latin America. Kimco methodically unwound its international joint ventures and sold down its foreign holdings, retreating to a purely domestic footprint. It pruned the tail of the portfolio—selling secondary and tertiary-market centers, single-tenant assets, and other non-core positions, often at low capitalization rates that reflected buyers' willingness to pay up for stable, if unexciting, cash flow. A low cap rate on a sale is good news for the seller: it means a high price relative to the income being sold. Kimco was, in effect, selling its lower-quality assets dear and redeploying the proceeds into fewer, better ones.

Where did the money go? Into concentration. Management set a target of clustering the portfolio in the top 20 major U.S. metropolitan markets—dense, higher-income coastal and Sun Belt metros where land is constrained, incomes are high, and new competing supply is hard to build—with a growing tilt toward grocery-anchored and mixed-use assets. The logic is that the same tenant, paying the same rent, is worth more in a supply-constrained affluent submarket than in a town where a competitor can build a rival center across the street next year. This "capital recycling"—sell the marginal, buy the prime—became the discipline of the era, executed in billions of dollars of transactions over roughly a decade.

Concentration also meant deepening the grocery tilt specifically. A center anchored by a strong supermarket is a fundamentally different risk than one anchored by a discretionary big-box; the grocer's traffic is weekly and weather-proof, and lenders and buyers pay up for that reliability. By early 2026 Kimco reported that more than 86% of its annual base rent came from grocery-anchored centers, up sharply from the more mixed profile of a decade earlier, with roughly 15 active projects under construction adding grocery anchors to centers that previously lacked one.2 The strategic message is consistent: when in doubt, become more of a grocery landlord and less of a general retail landlord. It is a coherent story, and it is one management has told the same way across years of filings and calls—consistency that, at minimum, argues the strategy is a genuine conviction rather than a rotating slogan.

There is also a subtle trap in the "top-20 markets" framing that deserves scrutiny. Concentrating in supply-constrained affluent metros genuinely improves asset quality, but it also means buying where every other institution wants to buy, which compresses the yield you earn on invested capital. A landlord can end up owning better real estate that generates lower going-in returns, betting that superior rent growth over time makes up the difference. That bet has largely paid off in the current supply-starved cycle. It is not guaranteed to pay off in a cycle where affluent-suburb rents stop outrunning the premium prices paid to acquire them. The quality-versus-yield tension is permanent; the current environment merely resolves it in quality's favor.

Here is where a neutral observer should pump the brakes on the tidy narrative. Simplification undeniably improved the story management could tell, and probably improved the durability of the cash flows. But "sell low-growth assets, buy high-quality assets" is easy to say and expensive to do: every sale crystallizes transaction costs and taxes, and every purchase in a prime market is made at a prime price. The strategy's payoff shows up not in a single dazzling number but in the slow re-rating of how the market perceives the portfolio—and, as later sections show, Kimco's own management was still complaining in 2026 that the market was not giving it full credit. Simplification was necessary. Whether it was sufficient is a live question. And it was made a great deal easier by a windfall arriving from an entirely different corner of the company—a grocery bet that had been quietly ripening for years.

V. The Albertsons "Plus" Strategy: How a Gamble Returned $1.7B

Milton Cooper had a habit that made his own board occasionally nervous. Every so often, he wanted Kimco—a landlord—to buy a piece of a retailer. Not a store to lease back, but actual equity in the operating company. His reasoning was that Kimco spent its whole life underwriting retailers as tenants, so it understood their real estate and their economics better than most financial investors. When a "real estate-rich" retailer fell into distress, Cooper argued, the landlord who knew the value of the underlying dirt could sometimes buy the whole business for less than the property was worth. He called this the "Plus" strategy: the shopping-center company, plus opportunistic merchant-banking bets on the retailers inside them.

The defining example arrived in 2006. A consortium including Cerberus Capital Management, SuperValu, and CVS moved to break up and acquire the struggling Albertsons supermarket empire, one of the largest grocery operators in America. Kimco joined as an equity investor, drawn by exactly the thing Cooper always looked for: enormous quantities of owned and well-located real estate sitting inside a troubled operating company. Kimco's participation was not a single check but a series of investments layered in over years—roughly $51 million in the initial 2006 transaction, a further roughly $37 million in 2013 when the group bought additional banners from SuperValu, and roughly $85 million in 2015 around the Safeway combination—cumulatively on the order of $180 million of invested equity.45

What made the bet work was that it had two engines, not one. The first engine was the real estate: Kimco and its partners could stabilize, lease, and monetize the underlying store locations regardless of how the grocery business fared. The second engine was the operating turnaround itself—Albertsons, restructured and eventually merged with Safeway under Cerberus's ownership, went from distressed also-ran to a scaled national grocer. For years this position sat on Kimco's balance sheet as a private, illiquid, hard-to-value curiosity that analysts mostly ignored. Then it became one of the best-performing investments in the company's history.

Pause on why a shopping-center landlord had any business making this trade, because the answer is the only thing that makes the "Plus" strategy intellectually respectable rather than reckless. Kimco spent every day of its existence answering one question: how much is a grocery store's real estate worth, and how reliably will a grocer pay rent on it? That is precisely the question that determined whether the Albertsons buyout was cheap or expensive. A generic private-equity firm had to hire consultants to answer it. Kimco answered it as a matter of core competence. When a landlord underwrites a retailer's real estate for a living, buying equity in a real-estate-rich retailer at a distressed price is arguably closer to its circle of competence than most people assume. The danger, which Kimco's own board reportedly felt, is that this reasoning is seductive and elastic—it can justify almost any retailer bet if you squint, and the line between "we uniquely understand this real estate" and "we are stock-picking with shareholder money" is thinner than management likes to admit.

The monetization came in stages, and the mechanism matters. When Albertsons finally completed its initial public offering in 2020, it created something the private stake had always lacked: a liquid public market in which Kimco could sell. Kimco began trimming, announcing a partial monetization in May 2020 that reduced its stake and pulled cash off the table.4 Over the following years it sold down the position in tranches into public-market strength, and it also collected the fruits of ownership along the way—including a large special dividend Albertsons paid its shareholders in early 2023, which delivered roughly $194 million of cash to Kimco and, in turn, prompted Kimco to pass a special $0.09-per-share dividend on to its own shareholders in late 2023.6 The final cleanup came in January 2024, when Kimco disposed of its remaining Albertsons shares. All told, Kimco has described gross proceeds from the Albertsons investment in excess of $1.7 billion against that roughly $180 million of cumulative cost—a multiple that would flatter any private-equity fund, let alone a shopping-center landlord.

What did Kimco do with the money, and what does the episode actually prove? The proceeds were not returned in a lump; they were woven into the balance sheet—funding development and redevelopment, paying down debt to support an investment-grade credit profile, and providing non-dilutive firepower for acquisitions that Kimco would otherwise have had to fund by selling stock. That last point is the crux: a REIT's core constraint is that it pays out most of its income and must therefore raise external capital to grow, usually by issuing shares. A $1.7 billion windfall let Kimco grow without printing as many new shares, which protects per-share value. The honest caveat is that this was a one-time, non-repeatable event resting substantially on a single position, and it is not a business model. Cooper's "Plus" instinct produced a spectacular result here; the same instinct in other hands, or against a retailer whose real estate proved less valuable, could have produced a write-off. It funded the next chapter, but it does not, by itself, make Kimco a great capital allocator forever. The next chapter would test that skill directly, because Kimco used its strengthened position to go shopping for other landlords.

VI. The Sun Belt Consolidation Wave: Weingarten (2021) & RPT Realty (2024)

In a fragmented business, scale is a slow-acting drug. It does not transform a company overnight, but administered patiently it lowers the cost of nearly everything: a national landlord negotiates one master relationship with TJX or Kroger instead of dozens of local ones, spreads its corporate overhead across more square feet, and—crucially—earns a lower cost of capital because size and liquidity attract the big institutional buyers of both its stock and its bonds. Kimco spent the first half of the 2020s pressing this advantage through two large acquisitions, each aimed squarely at the fast-growing Sun Belt.

The Sun Belt itself deserves a word, because "grow where the people are going" sounds obvious and is not. The demographic migration of Americans and their employers toward the lower-tax, lower-cost, warmer states—Texas, Florida, Arizona, Georgia, the Carolinas—has been one of the defining internal shifts of the past two decades, and it changes the arithmetic of retail real estate. A shopping center's rent growth ultimately tracks the spending power of the households within a few miles of it; when those households are multiplying and their incomes rising, the anchor sells more, the small shops thrive, and the landlord's pricing power compounds. Kimco's legacy portfolio was tilted toward the dense, mature, slower-growing coasts. Both of its major acquisitions were, at their core, purchases of Sun Belt demographic tailwind—buying not just square footage but the population arrow pointing up.

The first was Weingarten Realty Investors, announced in April 2021. Weingarten was a Houston institution, a shopping-center REIT with a portfolio concentrated in exactly the high-growth Southern and Western markets—Houston, Miami, Phoenix, Atlanta, Orlando—where population and income were migrating. The deal was structured as a mix of stock and cash: each Weingarten share converted into 1.408 newly issued Kimco shares plus $2.89 in cash, valuing Weingarten at roughly $30.32 per share based on Kimco's price the day before the announcement, about $3.9 billion in equity value and roughly $5.9 billion including assumed debt.7 Weingarten shareholders received a premium of around 19% and ended up owning roughly 29% of the combined company; Kimco holders kept about 71%.7 The combination created a national platform of roughly 559 open-air centers and about 100 million square feet.7

Did Kimco overpay? The timing invites the question. April 2021 was a moment of surging optimism about exactly this asset class—vaccines were rolling out, consumers were flush with stimulus, and grocery-anchored retail was suddenly the belle of the ball. Buying at the top of a sentiment wave is how acquirers destroy value. In Kimco's defense, the deal was structured to be immediately accretive to funds from operations—the REIT industry's cash-earnings measure—and it delivered a strategic result that would have taken years to build organically: it pushed the Sun Belt from roughly 42% of the portfolio's base rent to more than half. The neutral read is that Kimco paid a full but not reckless price for a genuine acceleration of a strategy it had already committed to, and it used its own richly valued stock as the currency, which softens the risk of overpaying in cash. The proof would be in the integration—and, more importantly, in whether the Sun Belt's fundamentals held up. So far they largely have.

There is a broader point about paying with stock rather than cash that runs through both Kimco deals and deserves stating once, clearly. When an acquirer pays in its own shares, it is effectively asking the target's shareholders to become its shareholders—and if the acquirer's stock is itself richly valued, it is buying with an expensive currency, which is favorable. The risk is the mirror image: if the acquirer's stock is cheap, paying in stock dilutes existing holders at a bad price. The RPT deal, struck when Kimco's own shares were arguably undervalued, is the case where this logic cuts less favorably—Kimco issued stock it may have considered cheap to buy assets it considered valuable, a trade that only works if the acquired assets outperform enough to overcome the dilution. This is exactly the kind of judgment on which acquisitive management teams are ultimately graded, and it cannot be judged from the press release alone.

The second acquisition, RPT Realty, closed on January 2, 2024, and was a smaller, cleaner, all-stock affair valued at roughly $2 billion including assumed debt and preferred stock. RPT holders received 0.6049 of a new Kimco share for each RPT share.8 The strategic logic was threefold. First, quality: RPT brought 56 open-air centers, 13.3 million square feet of GLA, in markets that fit Kimco's map, with a substantial mark-to-market opportunity—meaning RPT's in-place rents sat well below current market rents, so as leases rolled Kimco could re-lease at meaningfully higher rates.8 Second, cost: Kimco identified roughly $34 million of annual run-rate corporate synergies, most of it realizable in the first year, the classic scale benefit of folding a standalone REIT's overhead into an existing platform.8 Third, visibility: RPT carried a backlog of signed-but-not-yet-opened leases—tenants who had committed and would begin paying rent as their spaces were built out—providing a slug of near-term, contractually visible income growth.

The single most telling data point about whether these deals were operationally sound came not at closing but two years later. On Kimco's first-quarter 2026 earnings call, management noted that when RPT was acquired its portfolio ran about 130 basis points below Kimco's legacy occupancy; by early 2026 Kimco had not only closed that gap but pushed the former RPT centers to slightly higher occupancy than its own legacy assets.2 That is what successful integration looks like in this business—taking someone else's under-leased real estate and filling it using a bigger platform's tenant relationships and leasing muscle. It is also, notably, the kind of value creation that is only visible with hindsight, which is why the scale-consolidation thesis has to be judged on execution rather than announcement. To judge that execution, you have to understand the actual economics of the box Kimco is filling.

VII. Inside the Core: The Economics of Open-Air, Grocery-Anchored Real Estate

Strip away the ticker and the M&A and you are left with a deceptively simple machine, and it is worth walking slowly through how it actually makes money, because the economics are counterintuitive. A grocery-anchored center has two very different kinds of tenants, and the landlord makes its money in a way that runs opposite to intuition.

At one end sits the anchor: a supermarket like Kroger, Publix, Whole Foods, or Albertsons, or a necessity-driven big-box discounter like a TJ Maxx, Ross, Target, or Home Depot. Anchors are enormous, occupying 40,000 square feet or more, and they pay strikingly little per square foot—often in the range of $8 to $15. On the face of it, this is the landlord's worst tenant: huge footprint, tiny rent. But the anchor is not really paying in rent. It is paying in traffic. The supermarket is the reason the minivan pulls into the lot two or three times a week, every week, in good times and bad. The anchor's job is to manufacture reliable, recurring footfall.

At the other end sit the small-shop tenants—the nail salon, the local restaurant, the dental office, the boutique, the phone-repair kiosk. They occupy under 10,000 square feet, often far less, and they pay dramatically more per square foot, frequently $25 to $50 and up. This is where the landlord's real profit lives. The small-shop tenant is buying access to the foot traffic the anchor generates, and it pays a premium for it. The grocery anchor is the loss-leader that fills the parking lot; the small shops are the high-margin business that the full lot makes possible. Understand that inversion and you understand why the health of the small-shop segment, not the anchor, is the number that matters most.

There is a further wrinkle in how these tenants pay that shapes the landlord's risk. Most retail leases in this format are "triple-net" or close to it, meaning the tenant reimburses the landlord for its share of property taxes, insurance, and common-area maintenance on top of base rent. That structure pushes the volatile costs of owning real estate onto the tenant and leaves the landlord with a cleaner, more predictable stream—one reason grocery-anchored REITs can carry the debt they do. Leases also typically embed contractual rent escalators, often in the low single digits annually, which provide a baked-in growth floor independent of re-leasing. When management points to "higher minimum rents" as the driver of earnings growth—as CFO Glenn Cohen did in explaining the roughly $8 million increase behind first-quarter 2026 results—this is the machinery underneath: escalators plus mark-to-market re-leasing, compounding quietly.2

Which brings us to the metrics that actually tell you how Kimco is doing. Occupancy splits along the same anchor/small-shop line: anchor space runs very tight, near 98%, because there are only so many operators who can fill a 40,000-square-foot box and they tend to stay for decades. Small-shop occupancy is the sensitive instrument—it moves with the health of local entrepreneurs and the confidence of regional and national service retailers. In the first quarter of 2026, Kimco reported small-shop occupancy of 92.5%, up 80 basis points year over year and near historic highs, while overall leased occupancy hit 96.3%.2 When small-shop occupancy is climbing, it means the landlord has pricing power and the local economy is healthy; when it falls, it is the canary in the coal mine.

One more distinction is essential to reading this company honestly: the gap between leased occupancy and economic occupancy. A space can be leased—a tenant has signed—without yet being economic, meaning the tenant is not yet open and paying cash rent, because the space is still being built out. Kimco ended the first quarter of 2026 with a record 410-basis-point spread between the two, which the company frames as the single clearest indicator of where earnings are headed: contracted, visible cash flow sitting in the pipeline, waiting to switch on.2 The bull reads this as guaranteed future growth. The neutral reads it as guaranteed only insofar as the tenants actually open, actually pay, and do not go bankrupt between signing and commencing—a gap that, in a downturn, can widen rather than close.

The second metric is the leasing spread—the percentage change in rent when an old lease expires and the space is re-leased. This is the purest measure of pricing power a landlord has. In Q1 2026, Kimco reported new-lease spreads of 23.8% and blended spreads (new leases plus renewals and options) of 11.3%, extending a streak the company described as 15 consecutive years of positive leasing spreads.2 A new lease signed at nearly a quarter more rent than the prior tenant paid is a landlord capturing years of below-market rent in one stroke—and it is why management argues the portfolio is an inflation hedge. The third metric, same-property net operating income (SPNOI) growth, measures the organic growth of the existing portfolio; Kimco guided full-year 2026 SPNOI growth to a range of 2.8% to 3.5%, having raised it during the year.2 These three numbers—small-shop occupancy, leasing spreads, and SPNOI—are the dashboard for this company.

How does Kimco stack against its direct rivals? Four names define the peer set, and each embodies a different philosophy. Regency Centers (REG), at a market capitalization around $15 billion, concentrates on affluent, high-density suburban grocery-anchored centers—arguably the highest-quality core portfolio in the group. Federal Realty (FRT), around $11 billion, plays at the ultra-premium end, building mixed-use "urban village" destinations like Santana Row and Assembly Row that command very high rents but demand enormous, ongoing capital expenditure. Brixmor Property Group (BRX), around $10 billion, runs a more value-oriented portfolio with significant redevelopment upside. Kimco is the volume leader—the largest platform, the most square feet, the broadest national footprint. That scale is its distinguishing asset, but scale in real estate is a double-edged sword: it buys efficiency and cost of capital, and it dilutes the per-asset quality that a focused operator like Regency can maintain. Which of those trade-offs matters more depends heavily on who is steering the ship.

VIII. Leadership & Dynasty: The Flynn Era, Ross Cooper, and Capital Allocation

Most public companies are run by professional managers who arrive, serve, and depart. Kimco is unusual in that it still carries the fingerprints—and, in one case, the bloodline—of its founder. Understanding who holds the levers, and how they are paid, tells you a great deal about how this company will behave when the next hard decision arrives.

Conor Flynn, chief executive since 2016, is the operator. His rise from a regional role in 2003 to CIO in 2014 to the corner office reflects a company that promotes from within its leasing and asset-management ranks rather than importing financiers—a cultural choice that shows up in how management talks about the business, in the language of boxes, spreads, and traffic rather than balance-sheet abstraction. Flynn's personal ownership—on the order of 1.4 million shares—ties a meaningful portion of his net worth to the same stock his shareholders hold, which is the alignment that the 1991 internalization was supposed to create in the first place.

The dynastic thread runs through Ross Cooper, grandson of co-founder Milton Cooper, who has served as President and Chief Investment Officer since 2017 and was appointed to Kimco's board of directors effective January 21, 2025.9 Ross Cooper is the deal-maker—the executive most associated with the Weingarten and RPT acquisitions and the structured-investment pipeline that Kimco increasingly uses to source future acquisitions off-market. His presence raises the question every family-influenced public company invites: is dynastic continuity a source of long-term stewardship, or a governance risk that entrenches insiders? The honest answer is that it can be either, and the safeguards are what matter—an independent board, performance-linked pay, and a track record of decisions that serve all shareholders rather than the family.

The structured-investment strategy Ross Cooper has built is worth understanding because it is where the next chapter of capital allocation is being written, and it carries its own risk profile. Rather than only buying finished centers in open competition—where Kimco is one bidder among many private funds paying low-to-mid 5% cap rates—Kimco increasingly provides financing to owners of centers it would like to own, structured so that it earns an attractive current yield and secures a right of first offer or first refusal to buy the property later. On the first-quarter 2026 call, Cooper described committing capital to several such deals at yields above where finished assets trade, each carrying a future acquisition right, and noted the company was running slightly ahead of plan on this front.2 The appeal is real: it is a proprietary pipeline "largely insulated from open-market competition," in his words. The caution is equally real: structured lending against retail real estate is a credit business, and a landlord that lends to weaker owners is taking on default risk that a pure equity owner does not. It is a sensible way to source deals in a hot market; it is not free money, and it will be tested by the first borrower that cannot pay.

The generational transition became formal in early 2026. In January 2025 Kimco announced that Milton Cooper, after more than sixty years at the helm, would retire as Executive Chairman at the 2025 annual meeting and assume the ceremonial title of Chairman Emeritus, with independent director Richard Saltzman becoming Chairman of the board.9 Handing the chairmanship to an independent director rather than to a family member or the CEO is, on paper, a governance upgrade—it separates the roles of running the company and overseeing management. Whether that independence has teeth is something investors will only learn when the board has to say no to management, which has not visibly been tested.

A word on how these three—Flynn, Ross Cooper, and CFO Glenn Cohen—divide the labor, because it reveals the company's operating philosophy. On earnings calls the roles are consistent quarter after quarter: Flynn frames strategy and the macro backdrop, Chief Operating Officer David Jamieson walks through leasing and the operational engine, Ross Cooper covers the transaction market, and Cohen handles the balance sheet and guidance. It is a tidy division that mirrors the business itself—operate the existing centers, transact to improve the portfolio, and finance it conservatively. The consistency of this cast and its messaging across years of calls is itself a governance data point: management turnover is low, the story does not lurch, and the same people are held accountable for the same numbers over time. That stability cuts both ways—it can signal a healthy, aligned culture, or it can signal an insular one that struggles to hear dissent. On the current evidence, with an outside chairman now in place and a relative-performance pay design, the former reading is better supported.

The compensation architecture is where intentions become incentives. Kimco's short-term incentive plan weights heavily toward normalized FFO per share and balance-sheet leverage targets—specifically net debt to adjusted EBITDA—which pushes management to grow per-share cash earnings without over-borrowing. The long-term incentive plan ties a large share of executive pay to three-year relative total shareholder return measured against the FTSE Nareit Equity Retail index, meaning management is rewarded or punished based on how Kimco's stock performs against its direct competitors, not the market as a whole.[^12] That relative-TSR design is genuinely disciplining: it strips out the sector-wide tide and grades management on whether it out-executes Regency, Federal, and Brixmor. It is a well-constructed plan on paper. The skeptic's note is that relative benchmarks can reward a management team for losing less badly than peers in a sector that is falling together, and that FFO-based metrics can be flattered by acquisitions that add earnings while diluting per-share quality.

The credibility case for this management team rests on behavioral consistency, and here the record is reasonably strong. For years Kimco told investors it would prioritize deleveraging to reach a stronger credit rating, and by 2026 it reported an A-/A3 rating from the major agencies and net debt to EBITDA around 5.2x consolidated—among the lowest leverage in the retail-REIT sector, and consistent with what it had promised.2 Management set conservative guidance and then raised it through 2025 and into 2026 rather than the reverse. That pattern—promise discipline, deliver discipline, guide conservatively, beat modestly—is the profile of a credible team. It is exactly the profile that should invite the most scrutiny when the story is this good, because credibility is the thing companies spend right before they disappoint. The best test of that credibility is to run the whole business through an adversarial framework and see what survives.

IX. Playbook: Key Strategic & Capital Allocation Lessons

Step back from the quarter-to-quarter and Kimco's six decades resolve into a handful of transferable lessons—the kind an investor can carry to any real-asset business. They are not laws. They are patterns that worked in a particular context, and part of the exercise is noticing where the context is doing the heavy lifting.

The first lesson is the anti-fragility of necessity-based anchors. The reason grocery-anchored centers survived the e-commerce onslaught that gutted enclosed malls is not luck; it is that their traffic driver is structurally hard to digitize. You can buy a sweater online more easily than you can buy a week's fresh groceries, and even as grocery e-commerce grew, the physical store turned out to be the cheapest fulfillment node for it—the place where curbside pickup happens, where last-mile delivery originates, where the freezer and the produce section still live. Service retail—the haircut, the dental cleaning, the workout, the restaurant meal—cannot be shipped in a box at all. Amazon disrupted the department store; it has struggled to disrupt the errand. That structural insulation is real, but it is worth stating the limit plainly: it protects the format, not any particular tenant, and a landlord still lives or dies on filling the boxes.

The second lesson is the "Plus" business as a capital source—the idea that a company embedded in an ecosystem can sometimes make outsized returns by taking calculated equity bets inside that ecosystem, as Kimco did with Albertsons. The lesson is genuine but dangerous to over-learn: it worked because Kimco had a real informational edge in underwriting retail real estate and because the specific asset was real-estate-rich. Treated as a repeatable strategy rather than an opportunistic one, the same instinct is how disciplined landlords turn into undisciplined stock-pickers.

The third lesson is the premium the market pays for simplicity—the mirror image of the complexity discount that dogged Kimco in the 2010s. The company's own experience is the case study: the conglomerate sprawl of the 2000s depressed its multiple, and years of subtraction were required to earn a cleaner valuation. Focus lowers the cost of equity capital because investors will pay more for a business they can fully understand. The fourth lesson is the most operationally distinctive: organic redevelopment over greenfield development. Kimco does not generally go buy raw land to build on. It looks at the vast surface parking lots it already owns—land carried at essentially zero incremental cost—and builds apartments, and occasionally hotels or other uses, on top of successful centers. On the Q1 2026 call, Flynn framed the shopping center as one of the most underutilized forms of commercial real estate: a single-story building using perhaps 20% of a site's buildable area, surrounded by 80% parking that generates no revenue.2 Entitling that "free" land for residential density, often through capital-light joint-venture and preferred-equity structures, is how Kimco tries to manufacture high-return growth without the cost and risk of buying land in the open market—Kimco cited roughly 3,700 multifamily units already entitled across its portfolio.2

A fifth lesson lurks beneath the redevelopment story and is worth surfacing, because it is where management's rhetoric outruns its proof. Flynn talks about driverless cars reducing the need for parking, freeing even more of that 80% of "underutilized" land for higher-and-better use.2 It is a genuinely interesting long-term option, and options have value. But it is also the kind of far-horizon narrative that costs nothing to assert and may take a decade or never to materialize. A disciplined investor should file the parking-lot-to-apartments thesis under "real but unproven optionality"—valuable if it works, immaterial to the next few years of cash flow, and precisely the sort of visionary flourish that a company otherwise known for arithmetic should be made to demonstrate rather than merely describe. Kimco's own numbers help here: it points to completed projects like Coulter at Suburban Square where a mid-single-digit gross development yield translated into a return on Kimco's actual invested capital in the 8% range, precisely because the land came in at near-zero cost and the structure was capital-light.2 That is a real proof point. Whether it scales across thousands of entitled units is the open question.

The connective tissue across all four lessons is capital discipline under a REIT's structural constraint. Because a REIT must distribute most of its taxable income, it cannot self-fund growth from retained earnings the way a normal company can; every dollar of external growth must be justified against the cost of the equity or debt raised to fund it. Kimco's playbook—recycle rather than simply buy, redevelop free land rather than buy new land, harvest opportunistic windfalls to avoid dilution—is fundamentally a set of techniques for growing per-share value inside that constraint. Whether the techniques keep working depends on conditions that are not permanent, which is exactly what a proper stress test has to probe.

X. The Analyst Stress Test: Powers, Risks, and Bear vs. Bull

Now the war game. Strip away management's confidence and run Kimco through the frameworks a skeptical investor would actually use, and a more textured picture emerges—one in which the company holds several genuine advantages that are, uncomfortably, entangled with the interest-rate cycle.

Start with Hamilton Helmer's 7 Powers and Porter's Five Forces, applied honestly. The most defensible Power is the cornered resource: irreplaceable, high-traffic real estate on hard corners in land-constrained, affluent suburban submarkets. You cannot manufacture a well-located grocery-anchored corner in an established coastal or Sun Belt suburb; the zoning, the entitlement, and the physical land are effectively fixed. This shades into the single strongest structural argument in the entire bull case, which management returns to constantly: almost no new open-air retail supply has been built since the 2008 crisis, because construction costs and rents did not justify it, and by early 2026 Kimco pegged new supply under construction at roughly 0.2% of stock—the lowest of any commercial real estate sector.2 When demand rises against fixed supply, the owner of the existing supply gets pricing power. That is not a management slogan; it is visible in 15 straight years of positive leasing spreads.2

The second Power is scale economies—the ability to negotiate national master relationships with TJX, Ross, Kroger, and the rest across 100-plus locations, cutting transaction costs and vacancy downtime while spreading corporate overhead across a huge base. The evidence that scale is real appears in Kimco's low G&A load and its A-/A3 balance sheet, which lowers borrowing costs relative to smaller peers.2 There is also a "package leasing" dynamic that scale unlocks: because Kimco can offer a national retailer multiple sites at once, it can move faster and win share of a tenant's store-opening program. On the first-quarter 2026 call, management pointed to signing several Dollar Tree deals within weeks and negotiating multi-site packages with grocers like Sprouts, framing speed and breadth—not just price—as the competitive edge a large platform provides.2 A small landlord cannot make a chain that kind of offer.

Now run the rest of Porter's forces. The threat of new entrants is unusually low, which is the whole supply story—entering means building, and building does not pencil at current rents and construction costs, so the incumbents are structurally protected. The threat of substitutes is the e-commerce question, largely answered in the format's favor for necessity retail but never fully closed. And then the sharpest counterweight: tenant bargaining power. The grocery anchors that generate the traffic hold real leverage and keep anchor rents low—the landlord does not win on the anchor. Kimco's model only works because it recaptures margin on the high-rent small-shop space, which means the entire economic edifice depends on the anchor continuing to generate the traffic that gives small shops a reason to pay up. Pull the anchor's traffic and the small-shop premium collapses.

That dependency is the doorway to the risk radar. The first and most important material risk is cost of capital. A REIT is a spread business—it borrows and issues equity to buy assets yielding more than its funding costs—and sustained high interest rates raise refinancing costs, compress that spread, and, by pushing up the cap rates at which real estate trades, mechanically lower the net asset value of the portfolio. Kimco has managed this risk about as well as the sector allows—the bulk of its 2026 debt maturities were term-able and pre-planned, it launched a commercial paper program for cheap short-term funding, and it carries roughly $2.2 billion of liquidity2—but management cannot repeal the rate cycle. A prolonged high-rate environment squeezes the FFO-to-dividend cushion and shrinks the accretive-acquisition opportunity set, and that risk sits largely outside management's control.

The second material risk is retailer bankruptcy. Kimco's cash flow is a portfolio of tenant promises, and mid-tier and discount retailers fail in waves. The company's recent history reads like a roll call of the fallen—it has absorbed rent losses from the bankruptcies of Bed Bath & Beyond, Rite Aid, Big Lots, JOANN, and Party City, among others, and management explicitly cited lapping those lost rents as the reason first-quarter 2026 SPNOI growth would be the low point of the year.2 The reassuring counter-fact is that in an under-supplied market, a vacated box is a re-leasing opportunity at a higher rent rather than a permanent hole—Kimco reported backfilling recent anchor vacancies at double-digit mark-to-market gains.2 But that reassurance holds only so long as demand stays strong; in a genuine consumer recession, vacancies would cluster precisely in the small-shop segment where Kimco earns its highest margins, and re-leasing spreads would invert.

The third, subtler risk is capital-expenditure leakage. Reported FFO does not fully capture the tenant improvements and leasing commissions a landlord must pay to attract and retain tenants—real cash that quietly erodes the free cash flow available for dividends and growth. In a heavy leasing period like the current one, those costs run high, which is why sophisticated investors watch AFFO (adjusted funds from operations, which subtracts recurring capex) rather than headline FFO. Management's argument, made on the Q1 2026 call, is that as the signed-but-not-open pipeline converts to paying rent and the capex load tapers, free cash flow inflects upward.2 That is a plausible thesis, not a proven fact, and it is precisely the kind of forward promise that should be checked against results over the next several years.

An activist or short-seller stress-testing Kimco would press on three softer spots that the bull case tends to glide past. First, the reliance on non-cash and one-time items in reported revenue: management flagged that first-quarter 2026 GAAP revenue included roughly $7 million of accelerated below-market rent from early lease recaptures—non-cash, non-recurring, and helpful to the optics of the quarter—alongside seasonally front-loaded percentage rent.2 None of this is improper, and management disclosed it plainly, but a skeptic notes that headline FFO is a noisier number than it looks and that the quality of earnings deserves the same scrutiny as the quantity. Second, the acquisitive growth model itself: a company that has bought close to $10 billion of assets in five years is a company whose per-share results depend on integration and on not overpaying, and serial acquirers are exactly the cohort where discipline eventually slips. Third, the persistent valuation discount management complains about is itself a piece of evidence—if the market has priced Kimco below both its peers and private-market values for years, either the market is wrong or it is seeing risks (rate sensitivity, tenant credit, capex intensity, size-as-liability) that management is discounting. A neutral observer cannot simply assume the former.

So, bull versus bear, stated plainly. The bull case: a structurally supply-starved asset class, an A-rated balance sheet with manageable near-term maturities, record leasing demand, a contractually visible growth pipeline (the record signed-but-not-open backlog worth $77 million of future annual base rent),2 and demonstrated success integrating Weingarten and RPT. Management argues, with some justification, that the stock trades at a discount—an implied cap rate around 6.8% and roughly a 15% multiple discount to peers, per the Q1 2026 call—even as private capital pays low-to-mid 5% cap rates for the same kind of assets.2 The bear case: this is a rate-sensitive, capital-intensive business whose current results reflect an unusually benign combination of high demand and no supply, and whose most-cited advantages—pricing power, a full acquisition pipeline, rising NAV—all weaken together if rates stay high or the consumer cracks. A recession that hits small-shop tenants would strike the exact segment where Kimco makes its money, and cap-rate expansion would erode the NAV that underwrites its growth ambitions. Both cases are legitimate. The tension between them is the investment.

XI. Episode Epilogue & Wrap-Up

Sixty-six years is a long time to be right about parking lots. From a title-searching attorney and a builder pooling strip centers around 1960, to the 1991 IPO that helped drag the entire REIT industry from disrepute into institutional respectability, to a 2026 portfolio of roughly 568 centers and 100-plus million square feet, Kimco has mostly succeeded by refusing to be interesting.31 It bet on the errand over the experience, on necessity over desire, on the boring box that fills the parking lot rather than the cathedral of consumption. For most of the last two decades that looked like a company being left behind by history. In the post-pandemic reality it looks, at least for now, like a company that understood something durable about how people actually live.

But an episode that ends in triumph would be doing the reader a disservice, because the most important facts about Kimco in mid-2026 are unresolved tensions rather than settled victories. The company is executing well—converting a record lease pipeline, integrating acquisitions above plan, deleveraging to the strongest balance sheet in its history—and it is doing so inside a macro environment it does not control, on the strength of a supply-demand imbalance that will not last forever. Management's own repeated complaint that the market undervalues the stock is, read neutrally, a reminder that plenty of sophisticated investors are pricing in exactly the cyclical risks the bull case waves away.

For an investor tracking this company from here, the signal-to-noise ratio is highest in a very small number of places. Watch small-shop occupancy: it is the truest barometer of both the local economy and Kimco's pricing power, and the first place a consumer slowdown will show up. Watch the leasing spreads and the conversion of the signed-but-not-open pipeline into actual, cash-paying economic occupancy, because that conversion is the difference between a promising story and realized earnings. And watch the "Kimco Signature" redevelopment engine—the apartments rising on those free parking lots—as the test of whether the company can manufacture growth when the acquisition market is too expensive. Everything else, in a sense, is commentary on these three.

It is fitting that a company built by a lawyer who obsessed over downside now presents investors with a case that is fundamentally about the durability of an advantage rather than the existence of one. Nobody disputes that Kimco owns good real estate, runs it well, and finances it conservatively. The dispute is about time: how much of today's exceptional leasing, spreads, and occupancy is a permanent feature of a supply-starved format, and how much is the peak of a cycle that a recession or a prolonged era of high rates would reveal. Management, understandably, emphasizes the structural. The market, by holding the stock at a discount, is pricing in more of the cyclical. Both are looking at the same parking lots and reaching different conclusions. That gap—not any single quarter's beat or miss—is where the real work of judging Kimco lives. The architects of the modern REIT built something that lasted six decades; whether it keeps compounding is a question the next few years, not the last sixty, will answer.

References

-

Kimco Realty Corporation Form 10-K, Fiscal Year 2024 — U.S. Securities and Exchange Commission, 2025-02-26 ↩↩

-

Kimco Realty Announces First Quarter 2026 Results — GlobeNewswire, 2026-04-30 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Kimco Realty Announces Partial Monetization of its Investment in Albertsons Companies, Inc. — Business Wire, 2020-05-20 ↩↩

-

Kimco Realty Announces Second Quarter 2023 Results — U.S. Securities and Exchange Commission (Form 8-K), 2023-07-27 ↩

-

Kimco Realty Declares Special Cash Dividend of $0.09 Per Share of Common Stock — Business Wire, 2023-11-13 ↩

-

Kimco Realty and Weingarten Realty Announce Strategic Merger — Business Wire, 2021-04-15 ↩↩↩

-

Kimco Realty Closes Acquisition of RPT Realty — Kimco Realty, 2024-01-02 ↩↩↩

-

Kimco Realty Announces Board Leadership Transition — GlobeNewswire, 2025-01-21 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube