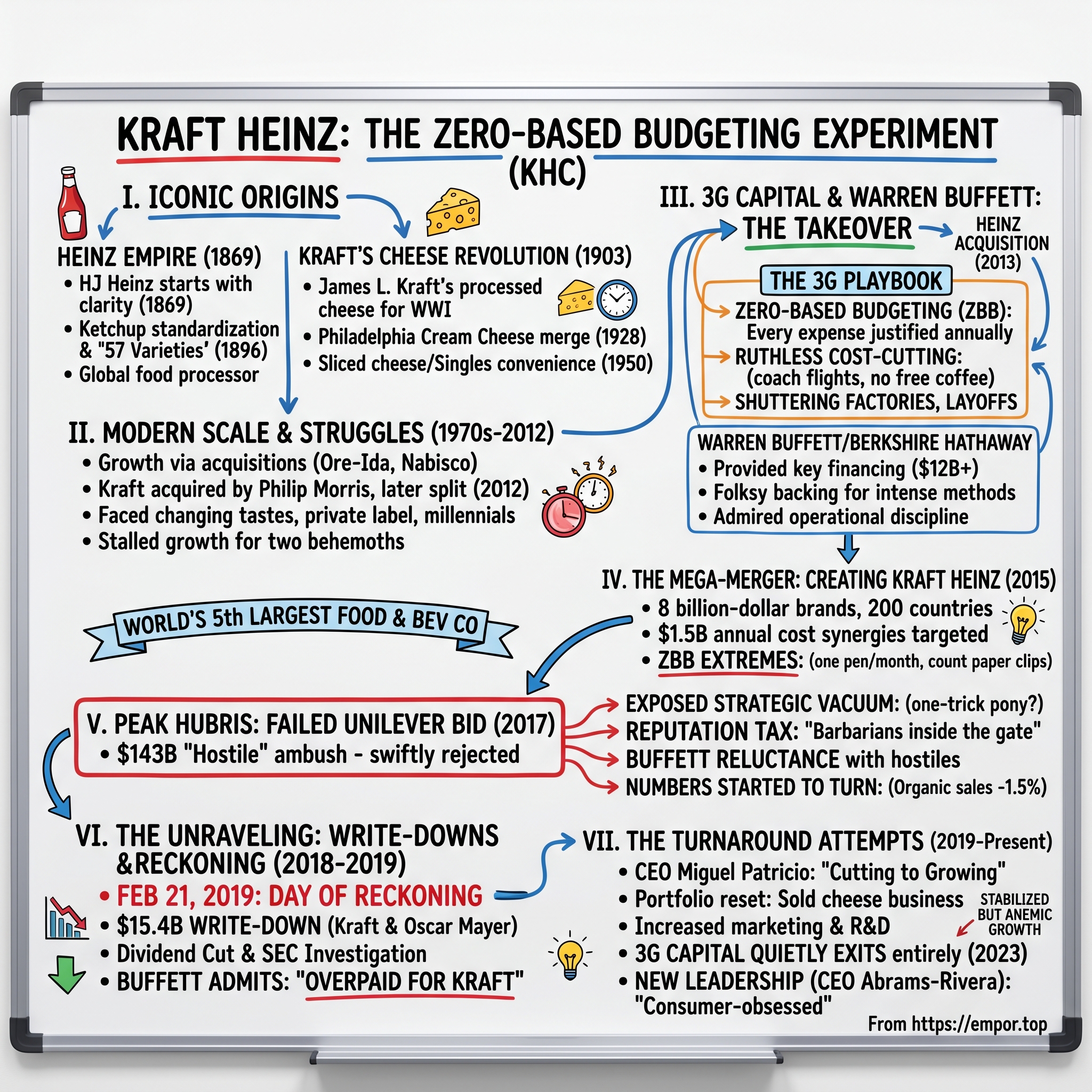

Kraft Heinz: The Zero-Based Budgeting Experiment

I. Introduction & Episode Roadmap

Picture this: February 22, 2019. Warren Buffett, the Oracle of Omaha, sits across from CNBC's Becky Quick. The man who built his reputation on buying wonderful companies at fair prices admits something almost unthinkable: "We overpaid for Kraft." In a single trading day, $16 billion in market value evaporates. The stock plunges 27%. This isn't just any company—it's Kraft Heinz, owner of brands that have sat on American kitchen tables for over a century.

How did two of America's most iconic food companies, backed by the world's most celebrated investor and Brazil's most feared private equity firm, destroy $80 billion in shareholder value in just four years?

This is the story of Kraft Heinz—currently the third-largest food and beverage company in North America and fifth-largest globally, with over $26 billion in annual sales. It's a tale that spans 150 years of American capitalism, from Henry Heinz's first horseradish bottle in 1869 to today's struggles with plant-based alternatives and private label competition. But more than that, it's a case study in the limits of financial engineering, the fragility of brand value, and what happens when you try to run a consumer goods company like a leveraged buyout.

The cast of characters reads like a who's who of global business: Jorge Paulo Lemann, the Brazilian billionaire who turned cost-cutting into an art form; Warren Buffett, whose Berkshire Hathaway would become the largest shareholder; and a parade of CEOs who tried to balance growth with austerity. Their experiment would test a fundamental question: Can you cut your way to greatness in consumer packaged goods?

The answer, as we'll see, reshaped not just Kraft Heinz but the entire food industry's approach to brand building, innovation, and the very meaning of operational excellence. This is their story—a cautionary tale of ambition, hubris, and the day ketchup met its match.

II. The Origins: Two American Icons (1869-2012)

The Heinz Empire: 57 Varieties and a Vision

In 1869, a 25-year-old Henry John Heinz stood in the ruins of his first business. His horseradish company had just collapsed in the financial panic, leaving him bankrupt. Most men would have quit. Heinz borrowed $2,400 from his family and started over—this time with a radical idea: sell food in clear glass bottles so customers could see the purity of what they were buying. In an era of adulterated foods and mystery ingredients, transparency was revolutionary.

By 1876, Heinz had introduced what would become the company's signature product: tomato ketchup. But here's what most people don't know—ketchup wasn't originally tomato-based. Early American recipes used everything from mushrooms to walnuts. Heinz's genius wasn't inventing ketchup; it was standardizing it, adding preservatives that extended shelf life, and creating the thick consistency Americans would come to expect. The iconic octagonal bottle, introduced in 1890, was designed to prevent tampering—each bottle sealed with a cork and wrapped in foil.

The "57 Varieties" slogan, coined in 1896, was pure marketing brilliance. Heinz actually produced over 60 products at the time, but he liked the sound of 57—it had, he said, a certain "psychological influence." This attention to branding was decades ahead of its time. By 1905, when Heinz incorporated, the company had become America's largest food processor, with 25 factories, including international operations in the UK.

Kraft's Cheese Revolution

Meanwhile, in Chicago, 1903, James L. Kraft was failing. The 29-year-old Canadian immigrant had invested his life savings—$65—in a cheese delivery business. His first year, he lost $3,000 and his horse, Paddy, died. But Kraft noticed something: cheese spoiled quickly, causing massive waste for grocers. His solution would transform American eating.

In 1915, Kraft developed a process for pasteurizing cheese, allowing it to be canned and shipped long distances without refrigeration. When World War I erupted, the U.S. Army became his biggest customer, ordering 6 million pounds of processed cheese. Returning soldiers had developed a taste for it, creating instant nationwide demand.

The real breakthrough came in 1928 when Kraft merged with Phenix Cheese Company, creators of Philadelphia Cream Cheese. The combined company pioneered another innovation that seems ordinary today but was revolutionary then: sliced, packaged cheese. In 1950, Kraft introduced individually wrapped cheese slices—what would become Kraft Singles. The convenience was irresistible to time-pressed American families.

The Television Age and Global Expansion

Both companies rode the post-war boom with remarkable prescience. Kraft became one of television's first major advertisers, sponsoring "Kraft Television Theatre" from 1947 to 1958—the longest-running drama series of TV's golden age. The show was so influential that "Kraft" became synonymous with quality family entertainment. Meanwhile, they introduced Cheez Whiz (1952), Kraft Macaroni & Cheese Dinner had already become a Depression-era staple (1937), and by 1960, they were selling 300 million boxes annually.

Heinz, not to be outdone, went global. By 1960, they operated in over 20 countries. Their marketing was equally innovative—the "Heinz 57" racing car competed at Le Mans, and their pickle-shaped pins became collectibles. The company's Pittsburgh headquarters, completed in 1952, featured a auditorium shaped like a can of soup.

Through the 1970s and 80s, both companies grew through acquisition. Heinz bought Ore-Ida (1965), becoming America's largest potato processor, and Weight Watchers (1978), presciently positioning for health-conscious consumers. Kraft merged with Dart Industries (1980), then was acquired by Philip Morris (1988) for $12.9 billion—at the time, the largest non-oil acquisition in U.S. history.

The Modern Era: Scale and Struggle

By 2000, both companies were behemoths struggling with a new reality. Consumer preferences were fragmenting. Organic, local, and artisanal were becoming more than buzzwords—they were existential threats. Kraft tried to adapt through sheer scale, merging with Nabisco in 2000 to create a $35 billion food giant. But size brought complexity. By 2011, Kraft operated in 170 countries with over 200 brands—an unwieldy empire.

The solution seemed logical: split the company. In 2012, Kraft divided itself into two entities. Mondelez International took the high-growth snack brands—Oreo, Cadbury, Trident. The remaining Kraft Foods Group kept the North American grocery business—the cheese, the mac and cheese, Oscar Mayer meats. It was a company rich in heritage but facing secular decline. Same-store sales were flat. Private label was gaining share. Millennials weren't buying processed cheese.

Heinz faced similar challenges. While still profitable—operating margins around 15%—growth had stalled. The company that once symbolized American innovation now looked like a mature, slow-growth enterprise. International expansion helped, but developed markets were saturated, and emerging markets required investment Heinz seemed reluctant to make.

By 2012, two icons of American capitalism stood at a crossroads. They had survived depressions, wars, and countless competitors. They had built brands worth billions and fed generations of families. But could they survive the age of quinoa, craft beer, and meal kits? As we'd soon learn, a group of Brazilian financiers thought they had the answer. They were catastrophically wrong—but their attempt would reshape the entire food industry.

III. Enter 3G Capital: The Heinz Takeover (2013)

Valentine's Day Surprise

February 14, 2013. While Americans exchanged heart-shaped boxes of chocolate, Jorge Paulo Lemann was orchestrating one of the most audacious takeovers in food industry history. At 9:00 AM, trading in Heinz stock was halted. Minutes later, the announcement: Berkshire Hathaway and 3G Capital would acquire H.J. Heinz Company for $72.50 per share—a $23.2 billion deal that represented a 19% premium to Heinz's all-time high.

The speed was breathtaking. Negotiations had lasted just seven weeks. The Heinz board met on Valentine's Day morning and unanimously approved the deal by noon. CEO William Johnson, who'd led Heinz for 15 years and had planned to retire in months, called it "bittersweet." He'd receive a $212 million golden parachute but would watch his life's work transformed by outsiders.

But who exactly was 3G Capital? To understand their playbook, you need to understand Jorge Paulo Lemann's origin story. The Swiss-Brazilian billionaire had made his fortune not in food but in investment banking and beer. Along with partners Marcel Telles and Carlos Alberto Sicupira, Lemann had perfected a management philosophy that was equal parts Swiss precision and Brazilian intensity. They'd used it to build AmBev into Latin America's largest brewer, then merged with Interbrew to create InBev, which eventually swallowed Anheuser-Busch in 2008 for $52 billion.

The Zero-Based Religion

3G's approach wasn't complicated—it was ruthless. They called it "zero-based budgeting," though that clinical term hardly captured its revolutionary nature. Every expense, every year, had to be justified from zero. No sacred cows. No inherited budgets. No "we've always done it this way."

In practice, this meant executives flew coach, shared hotel rooms, and paid for their own office coffee. It meant replacing corporate jets with commercial flights, executive assistants with shared admin pools, and company cars with personal vehicles. But these visible symbols were just the beginning. The real cuts went deeper: shuttering factories, consolidating suppliers, and most controversially, slashing the workforce. Within weeks of the deal's announcement, Heinz began transforming. Bernardo Hees, a 43-year-old 3G partner who'd previously run Burger King, replaced William Johnson as CEO. The new management team arrived with stopwatches and spreadsheets, timing how long it took to approve invoices, counting staplers in supply closets, measuring everything that could be measured.

By August 2013, Heinz laid off 600 workers, including hundreds in Pittsburgh, reducing its presence in the city by nearly a third. The symbolism was devastating—Heinz abandoning the city where Henry John had built his empire. But 3G saw sentiment as waste. They shuttered 5 of 13 factories. The corporate jet fleet was sold. The company gym was closed. Even the free cereal in break rooms disappeared.

The Warren Buffett Paradox

The involvement of Warren Buffett added credibility that 3G alone could never have achieved. Here was the world's most respected investor, famous for his folksy wisdom and long-term thinking, backing a leveraged buyout. Berkshire Hathaway provided $12.1 billion in financing—half as common equity, half as preferred stock paying 9% annually.

But Buffett's role revealed a fascinating contradiction. His investment philosophy—buying wonderful companies at fair prices and holding forever—seemed antithetical to 3G's slash-and-burn approach. In his 2013 shareholder letter, Buffett praised Heinz's "wonderful brands" and "excellent management." He didn't mention the layoffs or factory closures.

The truth was more nuanced. Buffett admired 3G's operational discipline even if he wouldn't implement it himself. He saw them as surgeons removing corporate fat that American management was too soft to cut. "They're very good at what they do," he'd later say. "I wouldn't want to work for them, and I don't think they'd want to work for me, but they're very good at what they do."

The Heinz Transformation

By the end of 2014, 3G management had improved EBITDA at Heinz by 35%. Operating margins soared from 15% to over 20%. The numbers were undeniable—3G's methods worked, at least on the income statement.

But beneath the surface, something else was happening. Marketing spend dropped by 20%. R&D budgets were slashed. The company that had once pioneered food science now spent less on innovation than almost any major food company. Talented executives fled. Those who remained described a culture of fear—daily performance metrics, constant job insecurity, an environment where missing a budget target by 1% could end your career.

The moratorium on free office snacks led to employees stealing hotel pens and being "devoid of complimentary cheese sticks"—a detail that sounds trivial but captured the penny-pinching ethos perfectly. This wasn't just cost-cutting; it was cultural revolution.

The strategy had a seductive logic. Why spend millions on Super Bowl ads when consumers already knew Heinz ketchup? Why invest in R&D when the perfect ketchup recipe was discovered decades ago? In stable, mature categories with dominant market share, 3G believed the path to value creation was efficiency, not innovation.

By early 2015, Heinz was a leaner, more profitable company. But it was also smaller—revenues had declined even as margins expanded. The question looming was whether this was sustainable. Could you really run a consumer products company like a private equity portfolio? The answer would come sooner than anyone expected, and it would involve another American icon that had seen better days.

IV. The Mega-Merger: Creating Kraft Heinz (2015)

The Deal Architecture

March 25, 2015, 7:00 AM. CNBC breaks the news: Heinz and Kraft will merge to create the world's fifth-largest food and beverage company. The structure was elegant in its simplicity yet Byzantine in its complexity. Heinz and Kraft agreed to merge with 3G, Berkshire and Heinz backers taking a 51% stake, while existing Kraft shareholders got 49% ownership plus a special $16.50 per share cash dividend—effectively a $10 billion gift funded by Berkshire and 3G.

For Kraft shareholders, it seemed like Christmas morning. Their stock jumped 35% on the announcement. They kept their shares in a larger company and received cash equal to 27% of Kraft's pre-announcement price. John Cahill, Kraft's CEO who'd been in the role just months, called it "a perfect marriage."

The industrial logic appeared compelling. Combined, the companies would have eight billion-dollar brands, 200 countries of operation, and enough scale to negotiate with anyone—from Walmart to wheat farmers. Annual cost synergies were projected at $1.5 billion by 2017. The market loved it. Within months of closing, Kraft Heinz stock hit $90, valuing the company at nearly $110 billion.

The 3G Machine Accelerates

Barely a month after the July 2015 merger close, Kraft Heinz announced plans to lay off 2,500 workers, about 5% of total employee base. But this was just the appetizer. Over the next 18 months, the company would close 7 more factories, reduce SKUs by 20%, and cut overhead costs from 18% of sales to 11%.

The Zero-Based Budgeting system reached new extremes. Employees now needed approval for color photocopies. Business travel required sign-off two levels up. Office supplies were rationed—one pen per month, paper clips counted and distributed. A former executive recalled watching colleagues bring toilet paper from home because the company had switched to single-ply to save money.

Yet the financial results were spectacular. By Q4 2015, adjusted EBITDA margins hit 30%—unheard of in food manufacturing. Free cash flow generation exceeded $4 billion annually. 3G partners took victory laps at investor conferences, preaching the gospel of efficiency.

The Hidden Decay

But visit a Kraft Heinz facility in 2016 and you'd see the real cost. Innovation labs shuttered. Marketing departments decimated. The company that invented processed cheese and shelf-stable ketchup now had one of the lowest R&D spending rates in the industry—just 1.1% of sales versus 2-3% at competitors.

The brand damage was subtler but devastating. Kraft Mac & Cheese, facing competition from Annie's organic options, saw market share erode quarter after quarter. Oscar Mayer, once America's favorite hot dog, lost ground to private label and premium competitors. The company's response? Cut prices and hope volume would compensate. It didn't.

Management focus on cost savings came at the expense of the top line. While margins expanded, organic sales growth turned negative. The company was literally shrinking itself to profitability—a strategy that worked until it didn't.

The Culture Wars

Inside Kraft Heinz, two cultures collided and never truly merged. Legacy Kraft employees, used to the methodical pace of a Midwestern food company, struggled with 3G's intensity. Legacy Heinz employees, already battle-scarred from two years of cuts, knew to keep their heads down.

The new culture prized one thing above all: hitting your number. Miss your weekly KPI and you'd get a call from Brazil. Miss your monthly target and you'd get a visit. Miss your quarterly number and you'd get a pink slip. One marketing director described it as "managing through fear rather than inspiration."

The talent exodus accelerated. Between 2015 and 2017, over 60% of senior marketing roles turned over. R&D lost its best food scientists to PepsiCo and General Mills. The institutional knowledge that had taken decades to build evaporated in quarters.

Warren's Warning Signs

By late 2016, even Warren Buffett was having doubts, though he kept them private. In Berkshire's offices, analysts noticed something unusual—Buffett had stopped talking about Kraft Heinz in his folksy, admiring way. When asked about the company at the 2017 annual meeting, his response was tellingly brief: "They're fine operators."

Behind closed doors, Buffett worried about what he called "the intangibles." Yes, the numbers looked good, but what about brand health? Customer relationships? Employee morale? These things didn't show up on financial statements until they did—usually all at once, catastrophically.

The market, however, remained believers. Kraft Heinz stock held steady around $80-85 throughout 2016. Analysts praised management's "disciplined execution" and "best-in-class margins." The company seemed to have discovered the holy grail: premium valuations for a commodity business.

Setting the Stage for Disaster

As 2016 drew to a close, Kraft Heinz faced a crossroads. The easy cuts had been made. The duplicate functions eliminated. The excess factories closed. To keep growing earnings, they needed either organic growth—which wasn't happening—or another acquisition.

In December 2016, at a board meeting in Pittsburgh, the path forward was decided. If Kraft Heinz couldn't grow organically, it would grow through acquisition. The target would need to be massive—big enough to restart the cost-cutting engine. It would need trusted brands that could benefit from 3G's efficiency. And ideally, it would bring international scale to complement Kraft Heinz's North American strength.

The perfect target seemed obvious: Unilever, the Anglo-Dutch consumer goods giant. What followed would be one of the most humiliating episodes in recent M&A history—and the beginning of the end for 3G's cost-cutting empire.

V. The Failed Unilever Bid: Peak Hubris (2017)

The $143 Billion Ambush

February 17, 2017, 4:30 AM London time. Paul Polman, Unilever's CEO, was in his Rotterdam office when the call came. Alex Behring, Kraft Heinz's chairman, was on the line with an offer: $50 per share for Unilever, an 18% premium, valuing the company at $143 billion. If successful, it would be the second-largest M&A deal in history.

Polman's response was swift and unequivocal: "No interest whatsoever." Within hours, Unilever's board unanimously rejected the approach, calling it "fundamentally undervalued" the company. But more telling was what they said next: Any deal would face "significant regulatory challenges" and wasn't in the best interests of stakeholders—not just shareholders, but stakeholders.

The philosophical clash was immediate and irreconcilable. Unilever under Polman had become the poster child for sustainable capitalism. They'd eliminated quarterly reporting, invested heavily in environmental initiatives, and pursued what Polman called "long-term value creation." The idea of being devoured by 3G's cost-cutting machine was anathema to everything Unilever represented.

The 48-Hour Fiasco

What happened next was unprecedented in modern M&A. Typically, leaked deal talks lead to weeks of negotiations, banker meetings, and competing bids. Not this time. Within 48 hours of the initial approach becoming public, Kraft Heinz withdrew its offer entirely.

The speed of the retreat revealed a crucial miscalculation. 3G and Buffett had assumed Unilever would negotiate. They hadn't anticipated the visceral reaction from multiple stakeholders. The UK government expressed "concerns." Dutch politicians called it an attack on a national champion. Unilever's employees—300,000 strong globally—mobilized against the deal.

Most damaging was the investor reaction. Unilever's stock jumped 13% on the news, but Kraft Heinz shares fell 4%. The market was sending a clear message: Kraft Heinz needed Unilever more than Unilever needed Kraft Heinz. The predator had become the desperate party.

Buffett's Reluctance

Behind the scenes, another dynamic was at play. Warren Buffett, whose blessing was essential for any major Kraft Heinz move, was uncomfortable with hostile takeovers. His entire investment philosophy was built on partnering with willing management teams. The prospect of forcing a deal on an unwilling target violated his fundamental principles.

In a later CNBC interview, Buffett would reveal his discomfort: "We wouldn't go against the wishes of the Unilever board. Not if I had anything to say about it." This constraint—Buffett's veto over hostile deals—effectively neutered Kraft Heinz's acquisition strategy. Without the ability to go hostile, they were limited to willing sellers, and after watching what happened to Kraft and Heinz, willing sellers were increasingly scarce.

The Strategic Vacuum Exposed

The failed Unilever bid exposed a fundamental flaw in the 3G model: it was a one-trick pony. The playbook—buy, cut costs, improve margins, repeat—required fresh acquisitions to sustain itself. Without Unilever or another major target, Kraft Heinz would have to grow the old-fashioned way: through innovation, marketing, and customer satisfaction.

The problem? They'd spent two years destroying those exact capabilities. Marketing spend was 40% below industry averages. R&D investment was negligible. The company's idea of innovation was Mayochup—a mixture of mayonnaise and ketchup that became a social media punchline rather than a sales driver.

Competitors smelled blood. Unilever itself went on offense, acquiring premium brands and increasing marketing spend. Nestlé accelerated its pivot to health and wellness. Even smaller players like Campbell Soup and General Mills, seeing Kraft Heinz's vulnerability, became more aggressive in defending their market positions.

The Reputation Tax

The Unilever episode inflicted lasting reputational damage. 3G was now seen as corporate raiders rather than operational experts. The financial media, once fawning, turned critical. A Forbes article called them "the barbarians inside the gate." The Economist questioned whether "financial engineering had reached its limits."

For employees and potential acquisition targets, the message was clear: 3G would gut your company, destroy your culture, and leave you with hollow brands. This reputation made future deals nearly impossible. When rumors surfaced about potential Kraft Heinz interest in Campbell Soup or Kellogg's, those stocks actually fell—investors feared becoming the next victim of 3G's cost-cutting machine.

The Numbers Start to Turn

By Q3 2017, the cracks were widening. Organic sales declined 1.5%. Market share losses accelerated across key categories. Private label penetration in cheese reached record highs. Amazon announced its Whole Foods acquisition, signaling a secular shift in food retail that Kraft Heinz was unprepared for.

The company's response was telling: more cost cuts. They announced Project Springboard, targeting another $1.7 billion in savings by 2019. But cutting costs when revenues are declining is like bailing water from a sinking ship—necessary but ultimately futile if you can't plug the holes.

Stock analysts began asking uncomfortable questions. If Kraft Heinz couldn't grow through acquisition and couldn't grow organically, what exactly was the bull case? Management's answers grew increasingly desperate. They talked about "brand renovation" and "category management" but provided few specifics. They promised innovation but had no pipeline. They committed to marketing investment but wouldn't say how much.

The narrative was shifting. Kraft Heinz was no longer the disruptor—it was the disrupted. As 2017 ended, the stock had fallen 20% from its peak. But the real disaster was still to come. The company that had prioritized financial engineering over brand building was about to learn a painful lesson: You can't cut your way to growth, and when you try, eventually the bill comes due.

VI. The Unraveling: Write-downs and Reckoning (2018-2019)

The Perfect Storm Builds

Throughout 2018, Kraft Heinz executives maintained a brave face. CEO Bernardo Hees spoke of "challenging market conditions" and "temporary headwinds." But inside the Chicago headquarters, panic was setting in. Private label penetration in key categories had reached 30%. Millennials weren't buying Velveeta. Amazon's private brands were expanding aggressively. The moat around Kraft Heinz's castle brands wasn't just narrowing—it was disappearing.

The numbers told the story. Q4 2018 organic sales fell 4.2%. Kraft Singles lost 1.5 share points to store brands. Oscar Mayer volumes declined double-digits. Even Heinz Ketchup, the crown jewel, saw flat growth in the U.S. The company's solution? More promotions, deeper discounts—a margin-destroying race to the bottom.

Meanwhile, the consumer landscape was transforming at warp speed. Beyond Meat went public. Oat milk became a billion-dollar category. Meal kits, plant-based proteins, ethnic foods—entire categories Kraft Heinz had ignored while counting paper clips were exploding. The company that once defined American eating was now desperately out of touch with American eaters.

February 21, 2019: The Day of Reckoning

The earnings call was scheduled for 4:30 PM Eastern. By 4:31, Kraft Heinz had lost $16 billion in market value. The company announced a $15.4 billion write-down of its Kraft and Oscar Mayer brands, a dividend cut, and an SEC investigation into its accounting. The stock plummeted 27%, its worst day in history.

The write-down admission was stunning in its implications. Kraft Heinz was essentially acknowledging that two of its most important assets—brands that had existed for over a century—were worth $15 billion less than they'd claimed. It was the largest write-down in consumer goods history, bigger than the entire market value of General Mills or Kellogg's.

But the SEC investigation was perhaps more damaging. The company disclosed it had received a subpoena related to its accounting practices, specifically around procurement. While details were scarce, the implication was clear: In their zealous cost-cutting, had they crossed legal lines? The investigation would drag on for years, creating a cloud of uncertainty.

Warren Buffett's Mea Culpa

Three days later, Warren Buffett appeared on CNBC with Becky Quick. The Oracle of Omaha, who rarely admits mistakes, was uncharacteristically contrite. "We overpaid for Kraft," he said simply. Then, more damningly: "The consumer packaged goods industry has been a lot tougher than I anticipated."

Buffett admitted his own rare misstep, paying too much for the deal, and acknowledging a nearly $3 billion loss. For Buffett, who built his reputation on understanding consumer behavior and brand value, it was a humbling admission. He'd been seduced by 3G's financial engineering, forgetting his own maxim: "Price is what you pay, value is what you get."

His comments sent shockwaves through the investment community. If Buffett—with his 60-year track record and unparalleled business judgment—could be this wrong, what hope did ordinary investors have? The Kraft Heinz debacle became a cautionary tale taught in business schools: Even the best investors can be blinded by financial metrics while ignoring fundamental business deterioration.

The Anatomy of Destruction

Post-mortem analyses revealed the depth of the damage. Programs focused on brand-building and innovation were ruthlessly cut, as ZBB prioritized immediate profit boosts over long-term sustainability. Marketing spending had been cut to 2.5% of sales versus 4-5% at healthy food companies. R&D spending was a paltry 1.1% of sales. The company had essentially been eating its seed corn—consuming brand equity built over decades to hit quarterly targets.

Employee morale hit rock bottom. Glassdoor reviews described a "toxic culture" where "fear dominates every decision." Turnover in critical roles exceeded 40% annually. The company that once attracted top talent now couldn't hire experienced brand managers from second-tier competitors.

The operational excellence that 3G prided itself on was also crumbling. In their cost-cutting zeal, they'd reduced quality control spending. Product recalls increased. Customer complaints soared. The Planters nuts factory shut down for weeks due to contamination. These weren't just operational hiccups—they were symptoms of a company that had cut too deep.

The $80 Billion Question

Between its 2017 peak and 2019 trough, Kraft Heinz destroyed over $80 billion in market value—more than the entire worth of Colgate-Palmolive or Mondelez. It was one of the greatest destructions of shareholder value in corporate history, made worse because it was entirely self-inflicted.

The comparison to competitors was brutal. While Kraft Heinz imploded, Unilever's stock rose 20%. Nestlé gained 30%. Even troubled General Mills outperformed. The market's verdict was unanimous: 3G's model didn't work in consumer goods. You couldn't treat beloved brands like commodity businesses.

Industry-Wide Reckoning

The Kraft Heinz collapse triggered soul-searching across the food industry. The 3G Capital cost-cutting playbook had cast a long shadow across the marketing world, with many brands and companies following suit. Companies that had embraced zero-based budgeting quickly backtracked. CEOs who had cut marketing spending reversed course. The pendulum swung from efficiency to growth, from cost-cutting to innovation.

Competitors learned valuable lessons. PepsiCo increased marketing spend and accelerated innovation, launching successful new products like Bubly sparkling water. General Mills invested in pet food and organic brands. Even Mars, traditionally conservative, bought Kind Bars for $5 billion—exactly the type of trendy, health-focused brand Kraft Heinz had ignored.

The episode also changed how investors evaluated food companies. Multiple expansion was no longer enough. Questions about brand health, innovation pipelines, and marketing investment became standard. The metric that mattered wasn't just EBITDA margin but organic growth—the one thing Kraft Heinz couldn't financially engineer.

As 2019 ended, Kraft Heinz stock languished around $30, down 65% from its peak. The company that was supposed to revolutionize the food industry had instead become a cautionary tale. But the story wasn't over. New management would attempt a turnaround, 3G would quietly exit, and the company would try to rebuild what it had destroyed. Whether it could succeed remained an open question—one that would define not just Kraft Heinz but the entire future of big food.

VII. The Turnaround Attempts (2019-Present)

The Patricio Era Begins

April 2019. Miguel Patricio arrived at Kraft Heinz's Chicago headquarters with a different resume than his predecessor. The former Anheuser-Busch InBev marketing chief had built brands, not destroyed them. His first all-hands meeting set a new tone: "We need to go from a company that was cutting to a company that is growing."

Patricio inherited a disaster. Employee morale was shattered. Retailer relationships were strained—Walmart executives openly complained about Kraft Heinz's lack of innovation. The company's Net Promoter Score among consumers had fallen to negative territory for multiple brands. It wasn't just a financial crisis; it was existential.

His first moves were symbolic but important. The office snacks returned. Business class travel for international flights was reinstated. The message was clear: The era of extreme austerity was over. But Patricio faced a delicate balance—he needed to invest in growth while still delivering profits to increasingly skeptical investors.

The Strategic Reset

Patricio's transformation plan, unveiled in September 2019, had five pillars: portfolio optimization, operational excellence, go-to-market effectiveness, innovation acceleration, and people development. Corporate speak aside, it essentially meant: sell what doesn't work, fix the supply chain, repair retailer relationships, actually innovate, and stop the talent bleeding.

In September 2020, Kraft Heinz sold its cheese business to Lactalis for $3.2 billion, including Breakstone's, Knudsen, and Cracker Barrel cheese brands. The sale was painful—cheese had been core to Kraft's identity since J.L. Kraft's horse-drawn wagon days. But these were regional brands with limited growth potential. The proceeds would fund innovation and debt reduction.

The innovation strategy marked a complete reversal from the 3G era. Marketing spending increased from 2.5% to 4% of sales. R&D investment doubled. The company launched Heinz Mayochup (properly this time), Kraft Mac & Cheese ice cream (a social media sensation), and Oscar Mayer Stuffed Dogs. Not all succeeded, but the pipeline was flowing again.

The Pandemic Windfall and Reality Check

COVID-19 initially seemed like salvation. As restaurants closed and families cooked at home, Kraft Mac & Cheese sales surged 27%. Heinz Ketchup flew off shelves. The stock recovered to $40. Bulls argued the pandemic had reminded consumers why they loved these heritage brands.

But the boost was temporary. As restaurants reopened, retail sales collapsed. Worse, inflation exposed Kraft Heinz's weakened pricing power. Input costs soared—cheese up 30%, packaging up 25%, transportation up 40%. But raising prices risked further market share losses to private label. The company was caught in a vice.

Patricio's response was "surgical pricing"—raising prices on strong brands while holding or cutting on weak ones. It worked, sort of. Revenues grew but volumes declined. The company was repeating its old pattern: shrinking to profitability. By 2022, organic volumes had declined for eight straight quarters.

The 3G Exit from Kraft Heinz

The gradual 3G retreat began in 2021. Jorge Paulo Lemann stepped down from Kraft Heinz's board, citing age and other commitments. In 2022, Alexandre Behring left the board, followed two months later by João Castro-Neves, 3G's final board member. The departures were announced in regulatory filings with no fanfare—a quiet end to a loud experiment.

The financial exit was equally stealthy. 3G had been periodically trimming its stake in Kraft Heinz since 2018, including selling 25 million shares in 2019 when the stock fell 4% on the news. In 2022, they distributed shares to fund investors. Then came the final act: In Q4 2023, 3G Capital quietly sold off its entire 16.1% stake.

No press release. No explanation. After a decade of evangelizing their management philosophy, 3G simply vanished. The message was clear: Even they had given up on making their model work in consumer packaged goods.

New Leadership, Old Problems

In 2023, Kraft Heinz tapped Carlos Abrams-Rivera as its new chief executive—the first CEO without 3G ties since the merger. Abrams-Rivera, a PepsiCo veteran, brought a different philosophy: "We need to be consumer-obsessed, not cost-obsessed."

His strategy focused on what he called "accelerate platforms"—concentrating resources on categories where Kraft Heinz could win. Away From Home (restaurants and foodservice) became a priority, growing double-digits. Emerging markets, long neglected, received investment. The company launched Kraft Heinz Kitchen, an innovation hub focused on culinary trends.

But structural challenges remained. Private label penetration in cheese exceeded 35%. Younger consumers viewed processed foods as unhealthy. The plant-based trend, which Kraft Heinz had ignored, was worth $8 billion and growing. The company's response—plant-based Oscar Mayer hot dogs—felt years late.

The Financial Reality

By 2024, Kraft Heinz had stabilized but hardly thrived. The stock traded around $35, less than half its 2017 peak. Organic growth remained anemic—low single digits in good quarters, negative in bad ones. EBITDA margins, once over 30%, settled around 20%—healthy but no longer exceptional.

Berkshire Hathaway, still the largest shareholder with a 26.8% stake, remained a committed long-term owner, but Buffett's enthusiasm had clearly waned. At the 2023 annual meeting, he spent more time discussing See's Candies than Kraft Heinz. The investment that was supposed to showcase Berkshire's partnership with 3G had become something to endure, not celebrate.

The legal overhang persisted. In 2023, Kraft Heinz agreed to a $450 million settlement related to accounting irregularities and misleading statements about cost savings—one of the largest securities settlements ever. The reputational damage was permanent.

The Portfolio Question

Kraft Heinz faced an existential question: What should it own? The portfolio included over 200 brands, but only eight generated more than $1 billion in sales. Many were regional players with limited growth potential. Others were in declining categories—who still bought Velveeta?

Management's answer was "fewer, bigger, better"—focusing on power brands while divesting subscale assets. But execution proved challenging. Potential buyers knew Kraft Heinz was a motivated seller, depressing valuations. And the power brands themselves faced headwinds—even Heinz Ketchup struggled against private label and specialty competitors.

The international opportunity remained largely untapped. Kraft Heinz generated 75% of sales in North America versus 40% for peers like Nestlé. But international expansion required investment—marketing, distribution, local product development—exactly what 3G had cut.

The Competitive Landscape

While Kraft Heinz struggled, competitors thrived. Unilever, freed from takeover threat, accelerated innovation and sustainability initiatives. Their stock outperformed Kraft Heinz by 50% from 2019-2024. PepsiCo successfully premiumized snacks and beverages, commanding higher prices for perceived quality. Even General Mills, long considered a laggard, outperformed through pet food and organic acquisitions.

The private label threat intensified. Retailers like Kroger and Walmart invested billions in store brands, offering quality comparable to national brands at 20-30% lower prices. In categories like cheese and cold cuts, private label became the market leader. Kraft Heinz's response—cutting prices to compete—only accelerated the margin compression.

New competitors emerged from unexpected places. Chobani entered mac and cheese. Impossible Foods targeted hot dogs. Every month brought another plant-based, organic, or ethnic challenger to Kraft Heinz's core categories. The moat had become a puddle.

As 2024 progressed, Kraft Heinz resembled a patient in stable but critical condition. The bleeding had stopped but recovery remained uncertain. The company that 3G and Buffett had proclaimed would revolutionize food was now just trying to survive it. The transformation attempt continued, but the question remained: Can you rebuild what's been destroyed, or had too much damage been done?

VIII. Playbook: Business & Investing Lessons

The 3G Model: Context Matters

The Kraft Heinz disaster didn't mean 3G's approach never worked—it meant context matters enormously. In beer, where 3G built InBev into AB InBev, the model succeeded brilliantly. Beer has high barriers to entry, benefits from scale in distribution, and consumers show remarkable brand loyalty even with price increases. Cost-cutting in breweries and distribution networks didn't damage the product experience.

In quick-service restaurants like Burger King, 3G's playbook also delivered. Franchisees bore most capital costs, menus could be simplified without losing customers, and operational efficiency directly improved customer experience through faster service. The asset-light model meant cost cuts flowed straight to the bottom line.

But consumer packaged goods were different. Success required constant innovation—new flavors, formats, health improvements. Brand equity needed continuous investment or it evaporated. Retailers had alternatives in private label. Consumers could easily switch brands. The cuts often came at the expense of long-term capabilities, such as creativity and innovation.

The lesson: Financial engineering works best in industries with strong competitive moats, limited need for innovation, and direct control over the customer experience. It fails where differentiation requires creativity, brand equity needs nurturing, and intermediaries control distribution.

Zero-Based Budgeting: Tool or Weapon?

ZBB itself wasn't the villain—the extreme application was. ZBB was invented in 1970 by Peter Pyrrh at Texas Instruments, who saw it as less about budgeting and more about assumption-testing and problem solving. Used thoughtfully, it eliminates lazy thinking and inherited waste.

But at Kraft Heinz, ZBB became a weapon of mass destruction. The singular focus led to the reduction of 2,600 jobs, closure of 7 plants, and even a moratorium on free office snacks that left employees stealing hotel pens. When you're counting paper clips while competitors are launching new categories, you've lost the plot.

The sustainable approach to ZBB protects growth investments. Unilever implemented ZBB but explicitly ring-fenced marketing and R&D. They used savings to fund innovation, not just boost margins. Procter & Gamble's productivity programs generated billions in savings while increasing brand investment. The difference? They viewed efficiency as funding growth, not replacing it.

The Brand Value Trap

The Kraft Heinz write-down revealed a profound truth about brand value: It's easier to destroy than create, and once destroyed, nearly impossible to recover. The $15.4 billion impairment write-down of Kraft and Oscar Mayer in February 2019 was the largest in the U.S. consumer staples industry in a decade.

Brand equity isn't just accumulated marketing spend—it's the compound interest of consistent investment over decades. When Kraft Heinz cut marketing from 4% to 2.5% of sales, they weren't just saving 1.5%—they were breaking the compound effect. Competitors who maintained spending gained share that proved nearly impossible to reclaim.

The irony was that 3G understood this in beer. They maintained marketing investment in Budweiser and Corona because beer brands are experiential—you can't cost-cut your way to "cool." But they somehow believed food brands were different, that consumers would keep buying Velveeta without being reminded why they should.

Patient Capital vs. Financial Engineering

Warren Buffett's involvement raises uncomfortable questions about patient capital. Berkshire's reputation rests on long-term ownership and operational non-interference. But with Kraft Heinz, Buffett enabled short-term value extraction that contradicted his stated philosophy.

The tension was evident in Buffett's later comments. He admitted overpaying but also said, "The management team is excellent." How could both be true? The answer: Buffett confused operational excellence with business excellence. 3G was excellent at operations—cutting costs, improving efficiency, streamlining processes. But business excellence requires growth, innovation, and brand building.

The lesson for investors: Patient capital without patient strategy is just slow-motion destruction. Long-term ownership means nothing if management is mortgaging the future for today's margins. True patient capital requires patience with investments that pay off over years, not quarters.

The Limits of Financial Metrics

Kraft Heinz's collapse highlighted the danger of managing to financial metrics alone. For years, the company reported improving EBITDA margins, rising EPS, and strong cash flow. Every metric that could be financially engineered looked great. But underneath, the business was rotting.

Market share, brand health scores, innovation vitality indices, employee engagement—these "soft" metrics were ignored or suppressed. When analysts asked about declining volumes, management pointed to margin expansion. When questions arose about innovation, they highlighted cost savings. The financial metrics became a smokescreen obscuring fundamental decay.

Smart investors learned to look beyond the numbers. Peter Lynch's "scuttlebutt" approach—talking to customers, employees, competitors—would have revealed Kraft Heinz's problems years before they showed up in financials. The lesson: If the story conflicts with the numbers, believe the story.

The Innovation Imperative

Perhaps the starkest lesson was about innovation in consumer goods. While Kraft Heinz was cutting R&D to 1% of sales, startups were reinventing every category. Oat milk went from non-existent to billions in sales. Plant-based meat created an entirely new category. Meal kits redefined cooking. Craft brands premiumized everything from pickles to peanut butter.

The mistake was viewing innovation as optional in mature categories. Yes, ketchup is ketchup—until someone creates organic, no-sugar-added, sriracha-infused ketchup that sells for 3x the price. The very stability that attracted 3G—established products, loyal customers—became vulnerability when those customers' preferences evolved.

As Prochno noted: "Well, of course, consumers are changing. They're always changing. That happens in every industry. The question is why hasn't the company responded to those customer changes? Why isn't it prepared to deal with those changes? And in this case, it's because the company has been focused on extreme cost-cutting and efficiencies, and not on creativity and innovation".

The Network Effects of Talent

The talent exodus created negative network effects that compounded over time. When top marketers left, they took relationships with agencies and retailers. When food scientists departed, they took years of formulation knowledge. When sales leaders exited, key customer relationships weakened.

Worse, Kraft Heinz became a negative signal on resumes. Recruiters reported that candidates apologized for their time there, explaining they'd joined before the 3G acquisition. The company that once attracted top CPG talent now couldn't hire mid-level brand managers from second-tier competitors.

The lesson extends beyond cost-cutting: Corporate culture is a network effect business. Good people attract good people. Innovation breeds innovation. Success compounds. But so does failure. Once the negative spiral begins, reversal requires not just new strategy but effectively building a new company.

These lessons reshaped how investors, boards, and management teams thought about value creation in consumer goods. The Kraft Heinz experiment definitively answered whether you could run a CPG company like a private equity portfolio. You could—for a while. But eventually, the bill comes due, and when it does, the cost exceeds all the savings you thought you'd captured.

IX. Analysis & Bear vs. Bull Case

Current Valuation and Financial Metrics

As of early 2025, Kraft Heinz market value is $35.15B, trading around $28-30 per share—a far cry from its $90 peak in 2017. The company trades at approximately 11x forward earnings, compared to 18-20x for peers like General Mills and Unilever. This discount reflects both skepticism about sustainable growth and the hangover from past mismanagement.

Full Year 2024 highlights show Net sales decreased 3.0%; Organic Net Sales decreased 2.1%, continuing the pattern of gradual erosion. Adjusted EPS was $3.06, up 2.7%, but this was driven more by cost management than top-line growth. Free Cash Flow was $3.2 billion, up 6.6%, providing ammunition for the dividend but limiting growth investment.

The balance sheet remains leveraged with net debt around 3.5x EBITDA—manageable but limiting flexibility. The company maintains its dividend at $1.60 annually, yielding approximately 5.5%, but this feels more like a value trap than income opportunity given the lack of growth.

The Competitive Landscape Assessment

The market structure has fundamentally shifted against Kraft Heinz. Tempered exposure to private label (11% now versus 17% in 2019) suggests some stabilization, but the threat remains existential in key categories. Amazon's private label expansion, Walmart's Great Value premiumization, and Kroger's Simple Truth success demonstrate that retailers no longer need national brands to drive categories.

Demographic headwinds compound the challenge. Millennials and Gen Z consumers view processed foods skeptically, preferring fresh, organic, or plant-based alternatives. Kraft Mac & Cheese might evoke nostalgia, but nostalgia doesn't drive purchase frequency among 25-year-olds worried about artificial ingredients.

International remains underpenetrated. Outside North America, Kraft Heinz's global reach includes a distribution network in Europe and emerging markets that drives nearly 25% of its consolidated sales base, versus 40-60% for true global players. But expanding internationally requires investment the company seems unable or unwilling to make.

Bear Case: The Structural Decline Thesis

The bear case is compelling and straightforward: Kraft Heinz is a melting ice cube in a warming world. Its core categories—processed cheese, packaged meats, shelf-stable condiments—face secular decline as consumers shift toward fresh, healthy, and sustainable options. The company's response has been too little, too late.

Market share data supports this thesis. In virtually every major category, Kraft Heinz has lost share over the past five years. The losses aren't dramatic—a point here, half a point there—but they're consistent and accelerating. When your only growth strategy is price increases and your customers are increasingly price-sensitive, the math doesn't work.

The innovation pipeline remains anemic. While competitors launch plant-based lines, functional foods, and premium offerings, Kraft Heinz introduces...pizza-flavored mac and cheese. The company seems culturally incapable of breakthrough innovation, trapped by its legacy and cost structure.

Financial engineering has reached its limits. Margins can't expand forever. The portfolio has been optimized. Further cost cuts would damage the business. Without organic growth—which management has failed to deliver for nearly a decade—the stock is dead money at best, value-destroying at worst.

The talent deficit may be insurmountable. Years of brain drain have left Kraft Heinz without the capabilities needed to compete. You can't suddenly become innovative after firing your innovators. You can't build brands after dismantling your marketing department. The company needs capabilities it systematically destroyed.

Bull Case: The Stabilization and Recovery Narrative

The bull case requires faith but isn't irrational. The argument: Kraft Heinz has stabilized, the worst is behind it, and modest improvements could drive significant multiple expansion given the stock's depressed valuation.

Portfolio optimization is working. The focus on power brands—those eight billion-dollar franchises—allows concentrated investment. Heinz remains the undisputed ketchup king globally. Philadelphia dominates cream cheese. These aren't dying brands; they're underinvested assets that could flourish with proper support.

The foodservice channel offers genuine growth. While the retail channel drives around 85% of its total sales, the firm also maintains a growing foodservice presence. As restaurants recover post-pandemic and expand globally, Kraft Heinz's scale and distribution become competitive advantages. A recovering McDonald's lifts all boats—especially ketchup boats.

Emerging markets present untapped opportunity. Rising middle classes in Asia, Africa, and Latin America are discovering packaged foods. Kraft Heinz's brands carry premium positioning in these markets. The international expansion that 3G never funded could finally happen under new management.

Inflation pass-through demonstrates pricing power. Despite volume declines, the company has successfully raised prices, suggesting stronger brand equity than bears acknowledge. If inflation moderates and volumes stabilize, margin expansion could surprise positively.

The Berkshire factor provides downside protection. Berkshire Hathaway, its largest shareholder with a 26.8% stake, is a committed long-term owner. Buffett won't sell at these levels—his average cost basis is likely $40+. This creates an implicit floor and potential catalyst if Berkshire increases its stake at depressed prices.

The Verdict: A Value Trap or Opportunity?

The truth likely lies between extremes. Kraft Heinz isn't going bankrupt—the brands have value, cash flow remains strong, and the balance sheet is manageable. But neither is it returning to growth—the structural challenges are real, competition is intensifying, and management has yet to demonstrate transformational capability.

For value investors, the stock offers optionality at a reasonable price. If management executes, international expands, and innovation improves, the stock could double. The 5.5% dividend provides some return while waiting. But this requires patience measured in years, not quarters.

For growth investors, Kraft Heinz remains uninvestable. Nothing in the company's trajectory suggests sustainable organic growth. Better opportunities exist in smaller, innovative food companies or even in Kraft Heinz's better-managed competitors.

The fundamental question isn't whether Kraft Heinz can survive—it can. It's whether survival is enough to justify investment when the opportunity cost includes companies actually growing, innovating, and building the future of food. For most investors, the answer remains no.

X. Epilogue & "What If?" Scenarios

What If Unilever Had Said Yes?

Imagine February 2017 unfolding differently. Paul Polman takes the call from Alex Behring and instead of immediate rejection, says, "Let's talk." The combined Kraft Heinz-Unilever would have created a $250 billion behemoth, the undisputed king of global consumer goods, larger than Procter & Gamble and Nestlé.

The industrial logic would have been compelling. Unilever's strength in emerging markets—60% of sales—would have complemented Kraft Heinz's North American dominance. Unilever's personal care and home care divisions, with 60% gross margins, would have offset food's structural challenges. The portfolio would have spanned from Dove soap to Heinz ketchup, Ben & Jerry's to Oscar Mayer—touching consumers at every moment of their day.

But would 3G's model have worked? The early years might have looked spectacular. Applying zero-based budgeting to Unilever's €52 billion cost base could have generated €10 billion in savings. Margins would have expanded dramatically. The stock would have soared. 3G would have been hailed as visionaries who finally brought discipline to bloated European conglomerates.

Yet the unraveling would have been even more catastrophic. Unilever's innovation machine—responsible for breakthrough products like dry shampoo and plant-based foods—would have been dismantled. The sustainability initiatives that attracted millennial consumers would have been cut as "non-essential." Talented executives would have fled to competitors or startups. Within five years, the combined entity might have faced the same fate as Kraft Heinz, but magnified—$200 billion in destroyed value instead of $80 billion.

The failed bid may have been Kraft Heinz's luckiest break. It prevented them from destroying two companies instead of one.

The Organic Growth Path Not Taken

Consider an alternative 2015 where 3G and Buffett chose a different strategy. Instead of radical cost-cutting, they invested Heinz's improved margins into growth. Marketing spend doubles. R&D triples. The company acquires not mature brands but emerging ones—Annie's, Krave Jerky, Bai Beverages—before competitors.

This Kraft Heinz would have pioneered plant-based alternatives years before Beyond Meat's IPO. They'd have launched a meal kit service competing with Blue Apron when valuations were reasonable. Their venture capital arm would have seeded dozens of food startups, creating an innovation pipeline impossible to build internally.

The financials would have looked different initially. Margins would have compressed to 15-18% versus the 30% 3G achieved. Growth would have been moderate—3-4% organic versus the negative rates realized. The stock might have traded at $60 instead of hitting $90. But it would have sustained that level.

By 2024, this alternative Kraft Heinz would be the innovation leader in food, not the laggard. Its brands would resonate with younger consumers. Private label would be less threatening because the company would be setting trends, not following them. The enterprise value might be $80-100 billion—not the $110 billion peak but far above today's $35 billion reality.

The Private Equity Precedent

The Kraft Heinz experiment's failure reshaped private equity's approach to consumer brands. Before 2019, the 3G playbook was gospel—firms like JAB Holdings and others were applying similar strategies across the industry. After Kraft Heinz's implosion, the model evolved.

Today's PE approach to consumer brands emphasizes growth over margins. Firms invest in digital capabilities, e-commerce infrastructure, and innovation labs. They hire CEOs from successful growth companies, not cost-cutting specialists. They maintain or increase marketing spend. The mantras changed from "zero-based budgeting" to "consumer-centricity" and "digital transformation."

The irony is that 3G Capital itself learned these lessons—just not at Kraft Heinz. At Restaurant Brands International, they've invested heavily in digital ordering, menu innovation, and restaurant remodels. At AB InBev, they've acquired craft breweries and invested in cannabis beverages. The firm that popularized extreme cost-cutting has quietly abandoned it everywhere except the company where it did the most damage.

The Counterfactual Buffett

Perhaps the most intriguing "what if" concerns Warren Buffett himself. What if the Oracle of Omaha had taken a more active role? Berkshire's operational non-interference principle is sacred, but Kraft Heinz tested its limits. Buffett watched 3G destroy billions in value while remaining diplomatically silent.

Imagine Buffett in 2017 calling Jorge Paulo Lemann with a different message: "This isn't working. We need to change course." His influence could have forced a strategy pivot before the worst damage was done. Marketing investment could have resumed. Innovation could have restarted. The Unilever bid could have been blocked entirely.

But this would have required Buffett to admit error earlier and more forcefully than his personality allows. It would have meant breaking with partners who'd made him billions at Burger King and AB InBev. It would have required operational involvement Berkshire studiously avoids. The structural constraints that make Berkshire successful—patience, non-interference, partnership loyalty—also prevented it from stopping the Kraft Heinz disaster.

Lessons for the Next Cycle

The Kraft Heinz story won't be the last of its kind. Somewhere, another financial engineer is eyeing another consumer brand, convinced they can cut their way to prosperity. The next version will be subtler—perhaps using AI to identify "inefficiencies" or blockchain to "optimize supply chains"—but the fundamental error will be the same: confusing operational efficiency with business excellence.

The sustainable model for consumer brands in the 2020s and beyond requires balancing multiple tensions. Efficiency and investment. Global scale and local relevance. Heritage and innovation. Digital and physical. The companies that thrive will be those that resist simple formulas and embrace complexity.

Kraft Heinz's tragedy is that it possessed all the ingredients for success—iconic brands, global distribution, manufacturing expertise, consumer trust—but combined them using the wrong recipe. The company that taught America to cook quick meals forgot that in business, as in cooking, there are no shortcuts to quality. You can't microwave your way to a gourmet meal, and you can't cost-cut your way to greatness.

As the food industry continues evolving—toward sustainability, health, convenience, and experience—Kraft Heinz serves as both cautionary tale and roadmap. Its failures illuminate what not to do. Its struggles highlight what matters. Its ongoing turnaround attempt, whether successful or not, will define how traditional food companies adapt to a radically different future.

The ultimate lesson may be the simplest: In consumer goods, the consumer comes first. The moment you prioritize financial metrics over customer satisfaction, margins over innovation, or efficiency over brand building, you begin the slow slide toward irrelevance. Kraft Heinz forgot this. The question now is whether they—and the industry watching them—can remember it in time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube