Kirby Corporation: America's Inland Marine Powerhouse

I. Introduction and Episode Roadmap

Somewhere between Houston and New Orleans, on a muddy stretch of the Gulf Intracoastal Waterway, a Kirby Corporation towboat is pushing three tank barges loaded with styrene toward a petrochemical plant. There is no fanfare. No headline. No app notification.

Just 90,000 barrels of chemical feedstock gliding silently through bayou country at six miles per hour, keeping the plastics supply chain alive for another day. The towboat captain has been running this route for twenty years. The styrene will become the polystyrene in coffee cups, food packaging, and insulation. And almost nobody in America knows this is happening.

Multiply that scene a thousand times across America's 25,000 miles of navigable inland waterways, and you begin to understand Kirby Corporation — the company that quietly moves America.

Kirby is the kind of business that Wall Street struggles to get excited about. There are no viral products, no charismatic founder pitching a vision of the future, no TAM slides with hockey-stick projections. Instead, there are barges. Lots of barges. Over 1,100 inland tank barges and nearly 300 towboats, carrying petrochemicals, refined petroleum products, and black oil along the Mississippi River, the Gulf Intracoastal Waterway, and America's coastal routes. With more than $3.3 billion in annual revenue and a market capitalization approaching $7 billion, Kirby is the largest domestic tank barge operator in the United States — and it is not particularly close.

Why does Kirby matter? Because virtually every gallon of gasoline refined on the Gulf Coast, every ton of ethylene produced in Louisiana's Chemical Corridor, every barrel of asphalt that paves American highways — much of it moves by barge at some point in its journey. Inland waterway transportation is the most cost-effective way to move bulk liquids in America. A single barge tow replaces more than 2,200 trucks on the highway. The cost per ton-mile is roughly one-twelfth that of trucking and one-quarter that of rail. And yet almost no one outside the energy industry has heard of Kirby Corporation.

That invisibility is, in a way, the point. The best infrastructure businesses are the ones nobody thinks about — until they stop working. Water utilities, electric grids, waste haulers, and yes, barge operators — these are the invisible sinews that hold the modern economy together. Kirby is critical infrastructure hiding in plain sight.

The central question of Kirby's story is deceptively simple: how did a small Houston marine operator become an unstoppable consolidator in one of the most fragmented, cyclical, and capital-intensive industries in America? The answer involves a century of Houston ambition, a Depression-era federal law that created an impenetrable regulatory moat, two transformative CEOs, billions of dollars in disciplined acquisitions, and the good fortune of sitting at the epicenter of America's petrochemical renaissance. Along the way, Kirby survived oil price collapses, a global pandemic, and the existential question of what happens to a fossil-fuel-adjacent business in a world pivoting toward decarbonization.

What makes Kirby's story particularly fascinating for investors is that it challenges several conventional narratives. It proves that roll-up strategies can work — in the right industry, with the right discipline. It shows that regulatory moats, often dismissed as fragile, can persist for over a century. It demonstrates that "boring" infrastructure businesses can compound wealth with extraordinary patience. And it raises uncomfortable questions about what "essential" really means in a world that increasingly wants to move beyond fossil fuels. This is the story of boring brilliance — the unsexy infrastructure play that has quietly compounded wealth for decades.

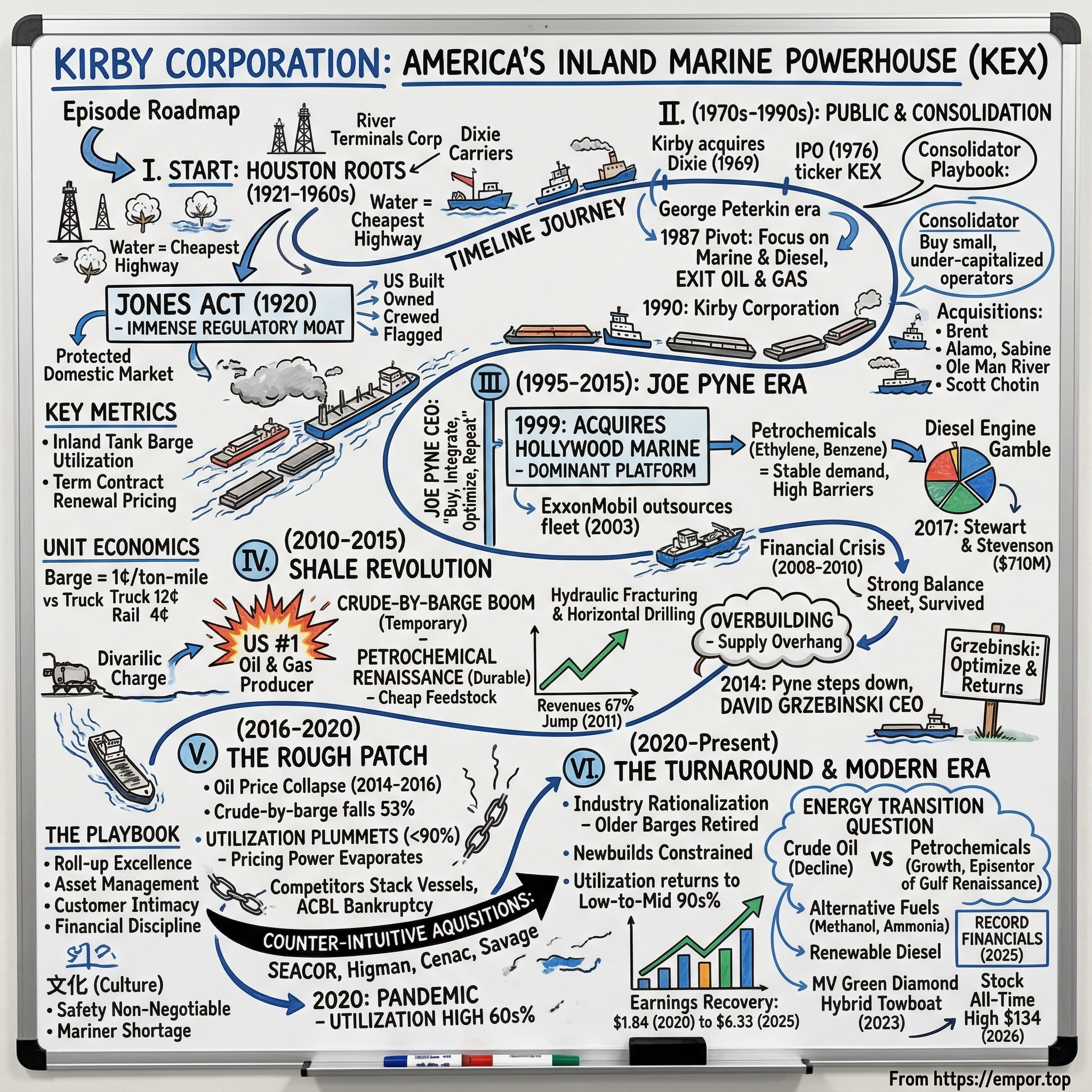

II. The Founding and Early Years: Houston Roots (1921–1960s)

The Kirby name in Texas is older than the oil industry itself. John Henry Kirby was born in 1860 in the piney woods of East Texas, the son of a modest farmer. By sheer force of ambition, he worked his way from sawmill hand to lumber magnate, founding the Kirby Lumber Company in 1901 and becoming the largest lumber manufacturer in the American South. He built railroads to haul timber, developed Houston real estate, and helped shape the city's identity as a center of commerce. Kirby Drive, the Kirby Building, and the Kirby Mansion in downtown Houston all bear his name — monuments to a man who understood that real wealth came from controlling the movement of raw materials.

In 1921, John Henry Kirby formed the Kirby Petroleum Company, an independent oil and gas exploration outfit. Texas was awash in crude — Spindletop had blown in two decades earlier, and Houston was rapidly transforming from a cotton-and-lumber town into the energy capital of the world. Kirby Petroleum rode this wave, drilling wells and building a modest exploration business. But the corporate ancestor of today's Kirby Corporation was not yet a marine company. That pivot would take another half-century.

The marine story actually begins in 1948, not with the Kirby family at all, but with a group of Houston investors led by George Peterkin Sr. They purchased River Terminals Corporation, a small operator that moved petroleum between Houston and New Orleans and cotton down the Mississippi River. This became Dixie Carriers — an unglamorous but profitable business that understood a fundamental truth about Gulf Coast commerce: water is the cheapest highway. The Peterkin family would remain a guiding force in the business for nearly half a century, embedding a culture of patient capital allocation and operational pragmatism that persists to this day.

Post-World War II America was building furiously. The interstate highway system was under construction, refineries were expanding along the Gulf Coast, and the petrochemical industry was taking shape in the corridor between Houston and Baton Rouge that would become known as "Cancer Alley" — a 150-mile stretch along the Mississippi River between Baton Rouge and New Orleans that is home to more than 150 petrochemical plants and refineries. The inland waterway system — the Mississippi River, the Ohio, the Illinois, and the Gulf Intracoastal Waterway connecting Gulf ports from Mobile to Brownsville — was the arterial network that made it all possible. Stretching 25,000 miles across 38 states, it is one of the largest navigable waterway systems in the world. The U.S. Army Corps of Engineers maintained the channels. The federal government subsidized the locks and dams. And a small fraternity of barge operators hauled the cargo.

The legal foundation for this protected domestic market was the Jones Act — Section 27 of the Merchant Marine Act of 1920. Passed in the aftermath of World War I, when America's dependence on foreign-flagged vessels during the war effort exposed a critical vulnerability, the Jones Act required that all goods transported by water between U.S. ports be carried on vessels that were built in American shipyards, owned by American citizens, crewed by American mariners, and flying the American flag. For the inland marine industry, this was a transformative piece of regulation. It meant that foreign operators — who could build vessels at a quarter of the cost — could never compete in domestic waterway transportation. The Jones Act created a closed market, and everyone inside that market was protected from the most dangerous form of competition: low-cost foreign entrants. Today, the Jones Act fleet of approximately 40,000 vessels supports 650,000 American jobs and generates over $150 billion in annual economic output.

For the early barge operators like Dixie Carriers, this regulatory protection combined with growing industrial demand created a foundation for steady, asset-heavy businesses. The work was dangerous — moving flammable and toxic liquids on open waterways required rigorous safety protocols — and capital-intensive. But operators who built reliable fleets, maintained strong customer relationships, and cultivated a safety culture could count on long-term contracts with the refiners and chemical companies that lined the Gulf Coast.

To understand why this mattered, consider the economics. Inland waterways move approximately 630 million tons of cargo annually in the United States, valued at over $73 billion. The Mississippi River alone carries 257 million tons per year. On the lower Mississippi, a single 10,000-horsepower towboat pushing 40 barges can carry the equivalent of 600 railcars or 2,200 trucks — at roughly one cent per ton-mile compared to four cents for rail and twelve cents for trucking. The physics of moving heavy cargo on water are simply unbeatable. The friction is lower, the energy efficiency is higher, and the carrying capacity per unit of motive power dwarfs any land-based alternative. This structural advantage was as true in 1950 as it is today.

But the early inland marine industry was a Wild West of small, under-capitalized operators competing on price in a market where safety standards varied wildly and equipment quality ranged from modern double-hull vessels to aging single-hull relics. There was no dominant player, no industry consolidator, and no standardized approach to operations. That fragmentation was both the industry's weakness and, for a future consolidator, its great opportunity. This was the business model that would eventually define Kirby Corporation: boring, essential, protected, and quietly profitable.

III. Going Public and the Consolidation Vision (1970s–1990s)

In 1969, the Kirby Petroleum Company made the move that would define the next half-century of its corporate life: it acquired Dixie Carriers. The combination of Kirby's oil and gas assets with Dixie's marine transportation fleet created a diversified energy company — but it was the marine division that would prove to be the durable engine of value creation. The combined entity, known as Kirby Exploration Company, began trading publicly on the New York Stock Exchange in 1976 under the ticker KEX.

The IPO was not a glamorous event. Kirby Exploration was a mid-cap Houston company in the oil and gas and marine transportation businesses — the kind of company that institutional investors might hold in a diversified industrials portfolio but rarely got excited about. The stock debuted at the equivalent of roughly 44 cents per share on a split-adjusted basis. Nobody watching that first trade could have imagined that the stock would eventually reach $134 by 2026 — a return of over 300 times the initial offering price, excluding dividends. That kind of compounding, sustained over five decades, is the hallmark of a business that found a structural advantage and exploited it relentlessly.

George Peterkin, whose family had been involved in the barge business since the 1948 purchase of River Terminals Corporation, served as president from 1973 to 1995. Under his leadership, Kirby began to recognize the strategic opportunity in the inland tank barge market's defining characteristic: extreme fragmentation. Hundreds of small, family-owned operators ran fleets of a dozen or fewer barges along regional routes. Many lacked the capital to modernize their equipment, the scale to negotiate favorable insurance rates, or the operational sophistication to meet tightening environmental and safety regulations. They were, in the language of private equity, ripe for consolidation.

The inland marine industry is different from most transportation markets in ways that matter enormously for competitive dynamics. First, the capital intensity is staggering — a new inland tank barge costs upward of $5 million, and a towboat can run $10 million or more, all of which must be built at expensive American shipyards under the Jones Act. Second, the regulatory complexity is substantial — the Coast Guard, the Environmental Protection Agency, and various state agencies all have jurisdiction over vessel operations, crew licensing, and cargo handling. Third, operational expertise is genuinely scarce — navigating a 25-barge tow through a river lock, or maneuvering loaded chemical barges through the Houston Ship Channel, requires years of training and experience that cannot be easily replicated.

These characteristics created an industry where small operators faced persistent disadvantages but where the barriers to building a large, scaled platform were immense. Kirby's strategic insight was that a disciplined consolidator could buy these struggling operators at reasonable prices, integrate their fleets and customer relationships into a larger network, extract cost synergies through shared infrastructure and purchasing power, and build a competitive moat that would widen with every acquisition.

In 1987, the board made a pivotal decision: Kirby would focus exclusively on marine transportation and diesel engine services, exiting the oil and gas business entirely. The following year, Kirby sold its exploration and production assets. In 1990, the company was renamed from Kirby Exploration Company to Kirby Corporation — a symbolic break with the petroleum past and a commitment to the marine future.

This strategic focus was counterintuitive for a Houston company in the 1980s. Texas was oil country, and most Houston-based companies were doubling down on exploration and production. Kirby went the other direction — choosing the stable, essential, and deeply unglamorous business of pushing barges over the speculative thrill of drilling for oil. It was a decision that reflected the Peterkin family's long-term orientation and their intimate understanding that transportation assets — the picks and shovels of the energy economy — could generate steady returns without the wildcat risk of exploration.

The early acquisitions were modest in scale but important in establishing the playbook. In 1989, Kirby acquired Brent Towing Company for $25 million in cash and Alamo Inland Marine Company for $27 million — two deals completed within weeks of each other that doubled the fleet to 164 barges and 64 towboats. In 1992, three more acquisitions followed in rapid succession: Sabine Towing and Transportation for $36.9 million, Ole Man River Towing for $25.6 million, and Scott Chotin for $34.9 million. Each deal added barges, towboats, customer relationships, and geographic coverage.

What emerged from this period was the "boring but beautiful" business model that would define Kirby for the next three decades. Buy undervalued or struggling operators. Integrate their fleets and customer contracts into a larger, more efficient network. Impose Kirby's safety standards and operational systems. Extract cost synergies from shared maintenance, insurance, and administrative functions. And repeat. It was the roll-up playbook applied to one of America's most essential but overlooked industries.

The myth versus reality here is worth examining. The consensus narrative is that Kirby simply bought everything that moved on the waterways. The reality is more disciplined than that. Kirby was selective — targeting operators with strong customer relationships, modern equipment, or strategic geographic positioning. The company walked away from deals that did not meet its return thresholds, even during periods of easy credit. The integration process was systematic, not cavalier: acquired crews were retrained to Kirby safety standards, equipment was inspected and upgraded to Kirby specifications, and customer contracts were migrated to Kirby's operating platform. This discipline is what separates a successful roll-up from a leveraged house of cards — and it is the reason Kirby's acquisitions have generally created lasting value rather than temporary revenue bumps.

IV. The Joe Pyne Era and Transformation (1995–2015)

A. The Consolidation Machine (1995–2008)

When Joe Pyne became CEO in 1995, Kirby was already the largest inland tank barge operator in the United States. But Pyne — who had joined the company in 1984 and served as president of Kirby Inland Marine for fifteen years — had a grander vision. He saw an industry where the top player controlled perhaps 15 percent of the market and where dozens of subscale competitors were limping along with aging equipment, thin margins, and limited access to capital. Pyne's strategy crystallized into four words: buy, integrate, optimize, repeat.

The defining deal of the Pyne era came in 1999, when Kirby acquired Hollywood Marine for $322 million. Hollywood Marine was the third-largest inland tank barge operator in the country, running 256 tank barges and 104 towboats under the leadership of C. Berdon Lawrence — a well-respected figure in the Houston marine community.

The deal combined the number-one and number-three operators in the industry, creating a dominant platform with unmatched scale on the Gulf Coast and the Mississippi River system. Lawrence became Kirby's chairman as part of the transaction, serving until 2010 — a signal that this was a merger of strong operators, not a hostile takeover. In one stroke, Kirby had gone from the largest player in a fragmented market to the clearly dominant one. The competitive gap between Kirby and its closest rivals widened permanently.

The Hollywood Marine acquisition was a template for what followed — and its success emboldened Pyne to pursue an aggressive acquisition cadence that would define the next decade. In 2002, Kirby acquired inland tank barge assets from Cargill's Cargo Carriers, added ten double-hull black oil barges and thirteen towboats from Coastal Towing, and purchased 94 double-hull tank barges from Union Carbide Finance Corporation. In 2003, Kirby bought ExxonMobil's domestic barge fleet through its SeaRiver Maritime subsidiary for $35.4 million, adding 48 double-hull inland tank barges and seven towboats.

The ExxonMobil deal was particularly significant — not for its size, but for what it signaled. ExxonMobil, the world's largest publicly traded oil company, had decided that operating its own domestic barge fleet was not a core competency. It chose to outsource that function to Kirby. When the largest and most operationally sophisticated oil company in the world decides that you are better at running barges than they are, it is a powerful endorsement of your competitive position. Other major oil companies and chemical producers followed ExxonMobil's lead, outsourcing their barge operations to Kirby and signing long-term contracts that deepened the customer relationship.

Beyond petroleum products, Pyne expanded Kirby's cargo mix to include a broader range of petrochemicals — ethylene, propylene, benzene, styrene — as well as refined products and black oil. This diversification proved prescient. Petrochemical transportation was more stable than crude oil movement, driven by steady demand for plastics, packaging, and industrial chemicals rather than the volatile price of oil.

The expansion into petrochemicals was not just a cargo diversification strategy — it was a customer diversification strategy. Petrochemical companies like Dow, Shell Chemical, and LyondellBasell are among the most demanding customers in the transportation industry. They require specialized equipment — tank barges with specific coatings, vapor-recovery systems, and temperature management capabilities for chemicals that can be corrosive, flammable, or toxic. They vet their carriers exhaustively, requiring years of safety track records before qualifying a new operator. And once qualified, they tend to stay. This is precisely the kind of customer relationship that creates a durable competitive advantage — high barriers to entry, high switching costs, and a premium placed on reliability over price.

By the mid-2000s, Kirby's competitive moat had deepened substantially: its scale advantages in purchasing, maintenance, and fleet utilization were meaningful; its customer relationships created genuine switching costs; and the Jones Act ensured that no foreign competitor could undercut on price.

B. Diversification: The Diesel Engine Gamble (1990s–2000s)

While marine transportation was the core business, Kirby pursued a second strategic track beginning in 1982 with the acquisition of Marine Systems, a small Gulf Coast facility that serviced medium-speed and high-speed diesel engines for marine applications. The logic was straightforward: Kirby's marine customers also needed engine maintenance, and the adjacent market of oil and gas equipment services shared many of the same customers and geographies.

Over the following two decades, Kirby built the diesel engine services business through organic growth and acquisitions, adding parts distribution, overhaul services, and engine manufacturing capabilities. The segment provided some diversification against the cyclicality of the marine transportation business, though it introduced its own form of cyclicality — oil and gas drilling activity.

The transformative move came in 2017, when Kirby acquired Stewart and Stevenson for approximately $710 million. This was a bold departure from Kirby's traditional playbook of buying barge fleets. Stewart and Stevenson, founded in 1902, was a storied Houston industrial company that distributed diesel engines and power systems, manufactured oilfield equipment including frac pumps and coiled tubing units, and provided aftermarket support across 43 locations in the United States and internationally. The deal closed in September 2017 — just weeks before Hurricane Harvey devastated Houston. It was Kirby's largest acquisition ever and fundamentally reshaped the Distribution and Services segment from a niche marine repair business into a significant industrial platform.

The strategic logic was that Stewart and Stevenson's aftermarket service business — parts, maintenance, overhauls — would provide recurring revenue that was less cyclical than new equipment sales. In practice, the oil and gas segment has proven more volatile than hoped, but the power generation division has emerged as an unexpected growth driver.

The results of the diesel diversification strategy have been mixed. During periods of strong oil and gas activity, the Distribution and Services segment has generated solid returns. During downturns — particularly the 2014–2016 oil price collapse and the 2020 pandemic — the segment has been a drag on earnings. In the first quarter of 2020, Kirby took $433 million in non-cash impairments, primarily in the Distribution and Services segment, reflecting the severity of the oilfield downturn. More recently, however, the segment has found new growth in power generation equipment, with revenue jumping 47 percent year-over-year in the fourth quarter of 2025 — driven by data center construction and other power-intensive applications.

C. Surviving the Financial Crisis (2008–2010)

The 2008 financial crisis tested every capital-intensive business in America, and inland marine transportation was no exception. Lehman Brothers collapsed in September 2008, and within months the credit markets that financed barge purchases and fleet expansions had frozen solid. Industrial demand collapsed across the Gulf Coast as refineries cut runs and petrochemical plants reduced output. Barge utilization rates fell sharply. Competitors with weak balance sheets and heavy debt loads were forced to stack vessels — literally tying barges and towboats to the riverbank and idling their crews. Some operators deferred maintenance, creating safety risks that would compound over time. Others were forced to sell assets at distressed prices just to meet debt obligations.

Kirby's advantage during this period was straightforward: it had the strongest balance sheet in the industry. Years of disciplined financial management — maintaining moderate leverage, generating consistent free cash flow, and avoiding the temptation to over-expand during boom times — gave Kirby the ability to continue operating at near-normal levels while competitors retrenched. Long-term contracts with major petrochemical companies provided a floor under revenues. And the essential nature of the cargo — refineries and chemical plants cannot simply stop shipping their products — meant that even in a severe recession, demand did not go to zero.

When the crisis passed, Kirby emerged stronger. Distressed competitors became acquisition targets, and the company's market share expanded. This pattern — using financial discipline to survive downturns and then capitalizing on the wreckage — would become a defining feature of Kirby's playbook. It is the classic Buffett axiom in action: be fearful when others are greedy, and greedy when others are fearful. Except Kirby applied it not to stocks, but to physical barges and towboats — assets that cannot be created quickly in a recovery because of the Jones Act shipyard bottleneck. The company that bought barges at the bottom of the cycle owned the only equipment available when demand snapped back. It was financial engineering through operational assets, and it worked spectacularly.

V. The Shale Revolution and Inflection Point (2010–2015)

In the early 2010s, a technology that had been gestating for decades suddenly changed the American energy landscape forever. Hydraulic fracturing, combined with horizontal drilling, unlocked vast reserves of oil and natural gas trapped in shale rock formations across Texas, North Dakota, Pennsylvania, and other states. The United States went from being a declining oil producer to the largest oil and gas producer in the world. It was the most significant shift in global energy markets since the Arab oil embargo.

For Kirby, the shale revolution was a dual tailwind of extraordinary force. On the marine transportation side, the surge in domestic oil production created massive demand for crude-by-barge transportation, as pipeline infrastructure could not keep pace with production growth. Inland barges suddenly became critical infrastructure for moving crude from production areas to Gulf Coast refineries. More importantly, cheap natural gas from shale production is a primary feedstock for petrochemical manufacturing. American petrochemical producers found themselves with a massive cost advantage over international competitors, triggering a wave of capacity expansion along the Gulf Coast. New ethylene crackers, polyethylene plants, and chemical complexes required more raw materials and produced more finished products — all of which needed to move by barge.

On the Distribution and Services side, the shale revolution drove enormous demand for diesel engines, transmissions, and oilfield equipment used in hydraulic fracturing operations. Kirby's engine distribution and repair network was perfectly positioned to serve the frac fleet buildout.

To understand the magnitude of the shale opportunity, consider the crude-by-barge phenomenon. Before 2010, moving crude oil by barge was a niche business — most crude traveled by pipeline from wellhead to refinery. But the shale revolution produced oil faster than pipelines could be built, particularly from the Bakken formation in North Dakota and the Eagle Ford in South Texas. Suddenly, barges on the Mississippi River system became a critical bridge between production and refining. At peak, crude-by-barge movements surged to volumes that would have been unimaginable a few years earlier. Kirby, with the largest fleet on the river, captured a disproportionate share of this business. But crude-by-barge was always going to be transitory — pipelines would eventually catch up. The more durable opportunity was in petrochemicals, where cheap natural gas feedstocks were driving a structural shift in the global competitive landscape that would benefit Gulf Coast chemical producers — and their barge transportation providers — for decades.

The financial results were dramatic. Consolidated revenues jumped from $1.1 billion in 2010 to $1.85 billion in 2011 — a 67 percent increase in a single year. Marine transportation revenues in the fourth quarter of 2011 rose 44 percent year-over-year. Barge utilization tightened into the low-to-mid 90 percent range, and pricing power improved significantly. For several years, Kirby appeared to be riding a super-cycle — a once-in-a-generation alignment of supply constraints and demand growth that drove margins and returns to exceptional levels.

But even during the euphoria, there were warning signs. Record deliveries of new tank barges in 2013 and 2014 — with Kirby itself being the largest buyer — were building a supply overhang that would eventually crush pricing. New entrants, attracted by the industry's apparent profitability, ordered barges at a pace that outstripped demand growth. From 2006 to 2019, the U.S. inland tank barge fleet expanded from approximately 2,750 to 4,000 barges — a growth rate that was fundamentally unsustainable.

In 2014, Joe Pyne stepped down as CEO after nearly two decades at the helm, handing the reins to David Grzebinski. Pyne had joined Kirby in 1984, spent fifteen years running Kirby Inland Marine, and served as CEO from 1995 to 2014. He was the architect of Kirby's transformation from a mid-size regional operator into the dominant national platform. His legacy was the consolidation playbook, the scale advantages, and the culture of operational discipline that would carry the company through the turbulent years ahead.

Grzebinski was a different kind of leader. A chemical engineer by training with an MBA from Tulane and a CFA designation, he had spent twenty-two years at FMC Technologies — the subsea equipment manufacturer — before joining Kirby as CFO in 2010. Where Pyne was the acquisitive operator who grew up in the marine business, Grzebinski was the financial engineer who came from the outside with fresh perspective. He understood the chemical industry from his engineering background and the capital markets from his finance career. He served as CFO and then president and COO before taking the CEO role in April 2014. Named the 2023 Maritime Leader of the Year by the Greater Houston Port Bureau, Grzebinski has proven to be a worthy successor — but his style is distinctly different. Where Pyne built the empire, Grzebinski optimized it. Where Pyne focused on scale, Grzebinski focused on returns. He would need every bit of that discipline for what was coming.

VI. The Rough Patch: Overcapacity and Market Correction (2016–2020)

The hangover arrived with brutal speed. Starting in mid-2014, oil prices collapsed from over $100 per barrel to below $30 by early 2016 — a 70 percent decline that rippled through every corner of the energy economy. Crude-by-barge volumes, which had surged during the shale boom, fell off a cliff as pipeline infrastructure caught up with production. Crude oil barge movements dropped 53 percent year-over-year by the third quarter of 2016. Refined product and petrochemical demand held up better, but the industry's real problem was on the supply side: all those barges ordered during the boom years were now flooding the market.

Tank barge utilization, the single most important metric in the inland marine business, plummeted to the low-to-mid 80 percent range by mid-2016. For context, utilization below 90 percent in this industry means there are too many barges chasing too little cargo, and pricing power evaporates. Spot rates fell sharply, and even long-term contract renewals came under pressure as customers leveraged the oversupply to negotiate lower rates.

Kirby's fourth-quarter 2015 revenue of $484 million was down 28 percent from $668 million in the fourth quarter of 2014. Profits declined in tandem. The Distribution and Services segment, heavily exposed to the oil and gas drilling market, was hit even harder as frac fleet activity collapsed.

Grzebinski faced a defining leadership test. In hindsight, it was the kind of crucible that separates good managers from great ones. The instinct in a downturn is to cut costs, stack vessels, and wait for the cycle to turn. Kirby did all of those things — reducing the workforce, selling aging and inefficient towboats, and maintaining cost discipline. Management kept the company out of financial distress even as peers wobbled. But Grzebinski also made a counter-intuitive bet that would define his tenure: he used the downturn to acquire, deploying capital aggressively when every instinct in the market was screaming to preserve cash. In 2016, Kirby purchased SEACOR Holdings' inland tank barge fleet for $88 million — picking up 27 modern inland tank barges and 13 towboats at a price that reflected the industry's distress. In 2018, Kirby acquired Higman Marine for $419 million, adding 159 inland tank barges with an average age of only about seven years and 75 towboats. In 2019, Cenac Marine Services followed for $244 million — 63 barges with an average age of roughly four years and 34 towboats.

The logic was pure Kirby playbook: buy high-quality assets from distressed or motivated sellers, integrate them into the existing network, and emerge from the downturn with greater scale and younger equipment. Between the SEACOR, Higman, Cenac, and subsequent Savage Inland Marine acquisitions, Kirby spent nearly a billion dollars on vessel acquisitions during one of the worst periods in the industry's history. It was a bet that the cycle would eventually turn — and that Kirby would be positioned to benefit disproportionately when it did.

Then came 2020. The COVID-19 pandemic delivered a second body blow before the industry had fully recovered from the first. Refinery and petrochemical plant utilization rates dropped sharply as demand for transportation fuels evaporated. Inland barge utilization plummeted to the high 60 percent range by the fourth quarter of 2020 — levels that were worse than anything seen during the oil price collapse. Spot market pricing dropped 25 percent year-over-year. In the first quarter of 2020, Kirby reported a net loss of $248 million, including $433 million in non-cash impairments concentrated in the Distribution and Services segment.

It was the darkest period in Kirby's modern history. But even in 2020, excluding the one-time impairment charges, the company generated $110 million in net earnings and solid operating cash flow. The essential nature of the cargo — petrochemicals and refined products must move regardless of economic conditions — provided a floor that many other transportation businesses did not have.

Meanwhile, Kirby's competitors were crumbling. American Commercial Barge Line filed for Chapter 11 bankruptcy for the second time in February 2020, restructuring more than $1 billion in debt and requiring a $200 million cash infusion to emerge. The contrast was telling: ACBL, which had loaded up on debt during better times, was forced into bankruptcy protection while Kirby — with its conservative balance sheet — was writing acquisition checks. In April 2020, while other companies were canceling capital projects and furloughing employees, Kirby closed the Savage Inland Marine acquisition for $278 million, adding 90 barges and 46 towboats along with ship bunkering and fleeting services on the Gulf Coast. The deal had been signed in January, before COVID hit, and Grzebinski chose to close it despite the uncertainty. It was the kind of move that only a company with financial discipline and strategic conviction could make — and it would prove enormously valuable as the recovery unfolded.

VII. The Turnaround and Modern Era (2020–Present)

A. Industry Rationalization (2020–2022)

The darkest hour proved to be just before dawn. Beginning in 2021, the inland tank barge industry underwent a structural rationalization that fundamentally changed the supply-demand balance. Aging barges — many built during the pre-2008 boom — were reaching the end of their useful lives and being retired or scrapped. Regulatory inspections, which had been deferred during the pandemic, created a "maintenance bubble" that forced operators to make expensive repair-or-retire decisions on older equipment. Newbuild orders, which had slowed dramatically during the downturn, were constrained by elevated steel prices and limited U.S. shipyard capacity. The industry shrank from approximately 4,000 inland tank barges to roughly flat, as retirements matched or exceeded new deliveries.

For the survivors — and Kirby was the strongest survivor of all — this capacity rationalization was transformative. Utilization rates climbed from the high 60s in late 2020 back into the low-to-mid 90 percent range by 2022. Pricing power returned, with spot rates and term contract renewals both trending higher. The 2021–2022 supply chain disruptions, which snarled trucking and rail networks across the country, further highlighted the value of inland waterway transportation as a reliable, high-capacity alternative.

Kirby's disciplined approach during the downturn — buying young, high-quality fleets at distressed prices while competitors were retrenching or going bankrupt — paid enormous dividends. The company emerged from the cycle with a younger fleet, greater scale, and a stronger competitive position than it had entered it. Customer stickiness, which had been a theoretical advantage, proved very real: Kirby's 92 percent customer retention rate and 17.6-year average customer relationship reflected the deep operational integration between Kirby and its petrochemical and refining customers.

The 2021-2022 supply chain crisis provided an unexpected showcase for inland marine's value proposition. When trucking networks were overwhelmed by driver shortages and port congestion, and rail networks were snarled by equipment imbalances and labor disputes, the inland waterway system continued to function with relative normalcy. Shippers who had taken barge transportation for granted suddenly recognized its reliability and capacity advantages. Several major petrochemical companies signed longer-term contracts with Kirby during this period, locking in capacity at rates that reflected the new appreciation for supply chain resilience. The crisis did not create Kirby's competitive advantages, but it made them visible to customers and investors in a way that years of steady performance had not.

B. The Energy Transition Question (2021–Present)

The most important strategic question facing Kirby today is what happens to a business built on transporting fossil fuel derivatives in a world that is slowly — or perhaps not so slowly — pivoting toward renewable energy. It is a question that hangs over every investor conversation, every analyst report, and every management presentation. And it is a question that Kirby's management has been thoughtful — perhaps surprisingly so for a Houston marine company — about addressing.

The answer, for Kirby, is more nuanced than the headline suggests. The company's cargo mix has shifted meaningfully away from crude oil — which was always the most vulnerable to the energy transition — toward petrochemicals, which face a very different demand trajectory. Petrochemicals are the building blocks of plastics, packaging, synthetic fibers, construction materials, medical equipment, and thousands of other products that are growing, not shrinking, as the global middle class expands. The International Energy Agency has identified petrochemicals as the single largest driver of oil demand growth through 2030, even in aggressive decarbonization scenarios.

Moreover, Kirby is positioned at the epicenter of America's petrochemical renaissance. More than a dozen multibillion-dollar integrated ethylene complexes have been built or expanded on the Gulf Coast, adding approximately 11 million metric tons per year of new ethylene capacity — a nearly 50 percent increase in U.S. capacity. Every one of these plants requires feedstock to be delivered and finished products to be shipped, much of it by barge. Chevron Phillips Chemical and QatarEnergy have a major expansion underway in Texas targeting 2026 completion. The Gulf Coast petrochemical boom is not theoretical — it is happening, and Kirby is its primary beneficiary.

Kirby is also adapting to new cargoes. The company transports increasing volumes of alternative fuels like methanol and ammonia, renewable diesel, and sustainable aviation fuel — products that are themselves part of the energy transition. The infrastructure advantage is real: existing tank barges and towboats can be adapted for new liquid cargoes without building entirely new fleets. A tank barge does not care whether it is carrying conventional diesel or renewable diesel — the asset is agnostic to the molecule. This adaptability is an underappreciated strategic advantage. As the mix of liquid products evolves over the coming decades, Kirby's fleet can evolve with it without requiring massive capital reinvestment.

On the environmental front, Kirby christened the M/V Green Diamond in 2023 — one of the first plug-in diesel-electric hybrid towboats in the United States, delivering an 88 to 95 percent reduction in emissions compared to conventional towboats. A second hybrid vessel is under construction. The company has reduced emissions per barrel of capacity by 24 percent and has set a long-term target of 40 percent reduction by 2040. And barge transportation itself is already the most carbon-efficient mode of freight transportation: barges emit roughly one-ninth the carbon dioxide per ton-mile of trucks and half that of rail.

C. Recent Strategic Moves and Financial Performance

The financial results of Kirby's turnaround have been exceptional. Revenue grew from $2.15 billion in the pandemic trough of 2020 to $3.36 billion in 2025 — a record year. Net income reached $354.6 million, or $6.33 per share, also a record. EBITDA hit $785 million with a margin of 23.3 percent. Marine transportation operating margins expanded to over 20 percent, reflecting the tight utilization environment and Kirby's pricing power.

Free cash flow generation accelerated to $406 million in 2025, funding a balanced capital allocation strategy. Kirby reduced debt by approximately $130 million during the year, bringing the debt-to-capitalization ratio down to 21.4 percent. The company repurchased over $100 million in stock in the fourth quarter alone, having repurchased roughly $175 million over the full year. Kirby has not paid a dividend since 1989 — capital returns come exclusively through buybacks, a tax-efficient approach that rewards long-term holders.

The stock reached an all-time high of $134.69 on March 3, 2026, reflecting the market's recognition that Kirby's competitive position and earnings power have reached a new plateau. For 2026, management has guided to flat to 12 percent earnings growth, operating cash flow of $575 to $675 million, and inland utilization in the low 90 percent range — a continuation of the favorable environment.

The trajectory of Kirby's earnings recovery tells its own story. From $1.84 per share in 2020 (excluding impairments), earnings climbed to $2.03 in 2022, $3.72 in 2023, $4.91 in 2024, and $6.33 in 2025. That is more than a tripling of per-share earnings in five years, driven by the combination of improving utilization, stronger pricing, fleet optimization, and share repurchases reducing the share count. The company that many investors wrote off during the pandemic has delivered one of the most impressive earnings recoveries in the industrial transportation sector.

Looking at the fleet dynamics, the supply picture continues to favor incumbents. In 2025, Kirby estimates that only 66 new inland tank barges were placed in service industry-wide, while 65 were retired — essentially flat fleet growth. Nearly 40 percent of the total U.S. inland barge fleet is now 20 years old or older, creating a structural tailwind for replacement demand. Newbuild costs remain elevated due to steel prices and constrained shipyard capacity. A new inland tank barge now costs upward of $6 million, and construction lead times stretch to 18 months or more.

This is the supply discipline that the industry lacked during the shale boom, and it suggests that the current favorable pricing environment may prove more durable than previous cycles. The industry has, in effect, learned from the overbuilding mistakes of 2012-2014. Whether that discipline holds if utilization remains tight and pricing continues to improve — or whether the temptation to overbuild will once again prove irresistible — is one of the key uncertainties in the Kirby thesis.

VIII. The Kirby Playbook: What Makes This Work

Strategic Principles

Kirby's success is built on a set of strategic principles that are easy to articulate but extraordinarily difficult to execute, particularly over decades and through multiple industry cycles.

The first principle is roll-up excellence. Kirby has completed dozens of acquisitions over thirty-plus years, ranging from $25 million bolt-ons to the $710 million Stewart and Stevenson deal. What sets Kirby apart from the many failed roll-up stories in American business is integration discipline. Each acquired fleet is absorbed into Kirby's existing operational network, with standardized safety protocols, maintenance schedules, insurance coverage, and customer management systems. The company does not simply buy barges — it buys customer relationships, geographic coverage, and operational capabilities, and then optimizes them within a larger platform.

The second principle is asset management through the cycle. Kirby's management has demonstrated a willingness to stack vessels during downturns, retire aging equipment when repair costs exceed replacement value, and — critically — buy distressed assets when competitors are forced to sell. The billion dollars spent on fleet acquisitions between 2016 and 2020 was the most important capital allocation decision of the Grzebinski era. Knowing when to build, when to buy, when to stack, and when to scrap is a form of institutional wisdom that takes decades to develop.

The third principle is customer intimacy. Kirby's 92 percent customer retention rate and 17.6-year average relationship are not accidents. They reflect a deliberate strategy of becoming operationally embedded in customers' supply chains — handling their most sensitive and hazardous cargoes, maintaining specialized equipment configurations for specific products, and providing the reliability that allows petrochemical plants to run continuously. Switching barge operators is not like switching trucking companies; it requires re-qualifying equipment, re-vetting safety records, and rebuilding the operational integration that keeps cargo flowing smoothly.

The fourth principle is financial discipline. Kirby has maintained a conservative balance sheet through every cycle, avoiding the debt-fueled expansion that destroyed competitors like American Commercial Barge Line, which filed for Chapter 11 bankruptcy twice — in 2003 and again in 2020. Kirby's debt-to-capitalization ratio of 21.4 percent provides ample financial flexibility for acquisitions, buybacks, and weathering downturns.

Cultural Elements

Safety is the non-negotiable cultural foundation. Inland marine transportation involves moving flammable, toxic, and corrosive liquids through congested waterways, often in poor visibility conditions. Kirby records and reports every cargo spill, "even if only one drop," and has reduced cargo spills to water by 76 percent since 2002. This is not a marketing slogan — it is an operational reality that directly impacts customer retention and regulatory standing.

The company's safety record has not been spotless. In March 2014, a Kirby towboat pushing two oil barges in the Houston Ship Channel collided with a bulk cargo ship in foggy conditions, spilling approximately 168,000 gallons of heavy marine fuel oil that spread across 160 miles of Texas coastline, fouling sensitive marsh habitat, wildlife refuges, and state parks. The incident resulted in $4.9 million in Clean Water Act penalties and $15.3 million in natural resource damages — over $20 million in total costs. In 2016, the Nathan E. Stewart, a Kirby offshore vessel, spilled over 107,000 liters of diesel fuel in British Columbia, resulting in a $2.7 million fine — the largest in Canadian history under the Fisheries Act. These incidents were serious and costly. But rather than treating them as crises to be managed and forgotten, Kirby used them as catalysts for fleet-wide operational improvements — enhanced navigational equipment, additional crew training, and tighter operating protocols. The 76 percent reduction in cargo spills since 2002 suggests that this institutional commitment to learning from failures is genuine.

The talent dimension is often overlooked. Inland marine is a specialized workforce — towboat captains, tankermen, and engineers require Coast Guard licensing, extensive training, and years of experience navigating rivers, canals, and ship channels. A mariner shortage has emerged as a meaningful industry challenge, driving labor cost inflation. Kirby's scale and reputation give it an advantage in recruiting and retaining experienced crews, but this remains a constraint on the entire industry's ability to grow capacity.

Why It Is Hard to Replicate

The most important question for investors evaluating Kirby's moat is whether a well-capitalized competitor could simply replicate Kirby's position. The answer is: not easily, and not quickly. Building a fleet of 1,100 inland tank barges and 270 towboats — all Jones Act-compliant, all U.S.-built — would require billions of dollars in capital and years of shipyard time, at construction costs that are roughly four times world prices. Even if a competitor had the capital, U.S. shipyard capacity is limited, and newbuild slots are constrained. The specialized crews required to operate tank barges carrying hazardous chemicals take years to train and qualify. The customer relationships that Kirby has built over decades cannot be replicated with a checkbook.

American Commercial Barge Line, which was once Kirby's closest competitor in scale, went through two bankruptcies and closed its JeffBoat shipyard — once the largest inland shipyard in America — in 2018. The closure of JeffBoat itself was a telling signal about the industry's capital dynamics: even building the barges had become uneconomical for all but the most specialized yards. Ingram Barge, the largest dry cargo operator with nearly 3,900 barges, is primarily focused on grain, coal, and aggregates — not the liquid chemical cargoes that are Kirby's specialty. Genesis Energy operates just 82 inland barges. Martin Midstream has 29. In the inland tank barge market, Kirby does not just have a leading position — it has a dominant one, with roughly 28 percent market share and no competitor even close to half that size. If Kirby were a tech company with this kind of market dominance, Wall Street would be talking about it as a platform monopoly. In the unglamorous world of inland marine, it barely registers on most investors' radar.

IX. Business Model Deep Dive and Unit Economics

Understanding how Kirby makes money requires understanding how inland marine transportation actually works. Think of it as a bus system for liquids. A typical tow on the Gulf Intracoastal Waterway consists of three to five tank barges lashed together and pushed by a towboat with 1,400 to 2,200 horsepower. On the Mississippi River, where channels are deeper and wider, a tow might include ten to twenty-five barges pushed by a 3,000 to 5,600 horsepower towboat. Each standard inland tank barge holds either 10,000 barrels (for shallower upper-river routes) or 30,000 barrels (for the deeper lower Mississippi and Gulf Intracoastal Waterway).

The barges operate like a linehaul bus route — the towboat picks up and drops off barges at various points along its route, delivering petrochemicals to one plant while picking up refined products from another. This flexibility is a key advantage over pipelines, which are fixed point-to-point connections that cannot be rerouted.

Contract structures fall into two categories. Term contracts, also known as contracts of affreightment, typically run one to five years and provide guaranteed capacity for the shipper and revenue visibility for Kirby. Approximately 70 percent of Kirby's inland revenues and 100 percent of its coastal revenues are under term contracts. Spot market transactions cover the remaining 30 percent of inland revenues — these are short-term, per-voyage charters that adjust rapidly to supply and demand conditions. Spot rates serve as a leading indicator of market tightness and are closely watched by investors.

The cost structure is dominated by vessel depreciation and maintenance, crew wages and benefits, fuel (which is typically passed through to customers in contract terms), insurance, and regulatory compliance costs. A new 30,000-barrel inland tank barge costs upward of $5 million. A new towboat runs $6 million to $10 million or more. These assets have useful lives of 25 to 40 years, with periodic dry-docking and hull inspections required by the Coast Guard.

The economics of barge transportation versus alternatives are stark. Barges move cargo at roughly one cent per ton-mile, compared to four cents for rail and twelve cents for trucking. A single barge carries the equivalent of 60 semi-trailers or 15 rail cars. One large tow on the Mississippi can replace 2,200 trucks on the highway. This cost advantage is structural — driven by the physics of moving heavy cargo on water versus over land — and is unlikely to change.

The Distribution and Services segment, which accounts for roughly 43 percent of total revenue, operates through three subsidiaries: Stewart and Stevenson (oilfield manufacturing, power generation, and aftermarket support), Marine Systems (marine engine repair and parts), and Engine Systems (diesel generators for commercial and nuclear power plants). This segment operates at lower margins than marine transportation — high-single-digit operating margins versus 20 percent for the marine segment — but provides diversification and is seeing growth in power generation applications driven by data center construction.

Capital allocation priorities under Grzebinski have emphasized a balanced approach: fleet maintenance and modernization (roughly $170 to $210 million annually in maintenance capital expenditure), accretive acquisitions when available, share repurchases (approximately $175 million in 2025), and debt reduction ($130 million in 2025). The company guided to operating cash flow of $575 to $675 million for 2026, providing substantial financial flexibility.

One nuance worth exploring is the seasonality and weather sensitivity of the business. Low water on the Mississippi River — as occurred dramatically in late 2022 — can restrict barge drafts, reduce tow sizes, and disrupt traffic patterns. Conversely, flooding can close stretches of the river entirely. Hurricane season on the Gulf Coast creates periodic disruptions to coastal operations. These weather events create short-term earnings volatility but can also benefit Kirby through surge pricing when capacity is constrained. The company's geographic diversification across the Gulf Intracoastal Waterway, the Mississippi system, and coastal routes provides some natural hedging against region-specific weather events.

The return on invested capital question is central to the investment thesis. In peak years like 2025, Kirby generates impressive returns. But through a full cycle — including the trough years of 2016 through 2020 — the returns are more modest. The capital-intensive nature of the business, with vessels depreciating over 25 to 40 years and requiring periodic dry-docking, means that maintenance capital expenditure alone consumes a significant portion of operating cash flow. Understanding the difference between peak-year returns and through-cycle returns is essential for properly valuing Kirby.

X. Competitive Landscape and Industry Dynamics

The inland tank barge industry is a study in consolidation dynamics. Kirby's approximately 28 percent market share makes it the undisputed leader, but the remaining 72 percent is spread across hundreds of operators, from regional family businesses to private-equity-backed platforms.

The most significant competitors operate primarily in dry cargo — grain, coal, aggregates — rather than the liquid chemicals and petroleum products that are Kirby's specialty. Ingram Barge Company, a privately held subsidiary of Ingram Industries, runs nearly 3,900 barges and is the largest dry cargo operator in the country, having recently acquired over 1,000 barges from SEACOR to further scale its network. American Commercial Barge Line, which emerged from its second Chapter 11 bankruptcy in April 2020 after restructuring over $1 billion in debt and injecting $200 million in new capital, is another major dry barge operator that is rebuilding from a position of weakness. Neither Ingram nor ACBL competes meaningfully with Kirby in the inland tank barge segment.

In the liquid cargo space, Kirby's competitors are dramatically smaller. Genesis Energy operates 82 inland barges with 2.3 million barrels of total capacity, primarily transporting crude oil and intermediate refined products — a fleet roughly one-thirteenth the size of Kirby's. Martin Midstream Partners runs 29 inland tank barges and 14 pushboats, focused on niche specialty products like sulfur and petroleum by-products. Canal Barge Company and Marquette Transportation, both acquired by Redwood Holdings in 2024, were meaningful regional operators but remained far smaller than Kirby in the tank barge segment. The Redwood consolidation is worth watching — it signals that private equity sees value in the industry and could create a more formidable number-two competitor over time. But even the combined Redwood platform is substantially smaller than Kirby.

The Jones Act is the foundation of Kirby's competitive moat. Foreign operators cannot enter the U.S. domestic waterway market, period. A Chinese or European barge operator could build equivalent vessels at a quarter of the cost, but they would be barred from operating between American ports. This regulatory barrier is the single most important structural advantage in the industry, and it has survived every attempt at reform over its 106-year history. More than 100 countries have cabotage laws, but the Jones Act is among the most restrictive in the world, requiring not just domestic ownership and crewing but domestic construction — a provision that adds enormous cost but also creates enormous barriers.

Alternative transportation modes provide limited substitution risk. Pipelines are the cheapest option for high-volume, point-to-point movements of a single commodity, but they are inflexible — you cannot reroute a pipeline — and politically difficult to build in the current regulatory environment. Rail transport costs roughly four times as much per ton-mile as barge. Trucking costs twelve times as much. For bulk liquid cargoes moving along waterway corridors, there is simply no cost-effective alternative to barges.

Several secular trends support Kirby's long-term positioning. The reshoring of American manufacturing, driven by geopolitical considerations and supply chain security concerns, is increasing demand for domestic transportation infrastructure. Energy independence, which has been a bipartisan policy goal for decades, requires continued development of Gulf Coast refining and petrochemical capacity. And the petrochemical industry itself is in a structural growth phase, driven by cheap natural gas feedstocks and expanding global demand for plastics and chemicals. U.S. ethylene demand is forecast to grow 45 percent between 2020 and 2028.

One often-overlooked dynamic is the aging infrastructure of the inland waterway system itself. The U.S. Army Corps of Engineers maintains the locks, dams, and channels that make inland navigation possible. Many of these structures were built in the 1930s through 1950s and are approaching the end of their design lives. The American Society of Civil Engineers has repeatedly flagged inland waterways as a critical infrastructure concern. Lock closures and maintenance delays can disrupt traffic patterns, creating both risks and opportunities for operators with the fleet flexibility to reroute tows. Kirby's scale provides a meaningful advantage here — a larger fleet can absorb disruptions more easily than a small operator with limited geographic coverage.

The industry also faces a structural tension between consolidation and competition. As Kirby grows larger, regulators and customers may push back against further concentration. If Kirby were to acquire another large tank barge operator, antitrust scrutiny could become a meaningful hurdle — particularly for routes where Kirby already dominates. This natural ceiling on market share through acquisition means that future growth may need to come increasingly from organic expansion and pricing power rather than the roll-up playbook that built the business.

XI. Porter's Five Forces and Hamilton's Seven Powers Analysis

Porter's Five Forces

Threat of New Entrants: LOW. The barriers to entry in the inland tank barge industry are among the highest in any transportation market. A single new tank barge costs $5 million or more, and it must be built at an American shipyard under the Jones Act — at roughly four times world prices. Building a competitive fleet of even 100 barges would require $500 million to $1 billion in capital and several years of shipyard time. Beyond the financial barriers, new entrants must establish safety track records, obtain Coast Guard certifications, qualify with major petrochemical customers, and recruit experienced crews in a tight labor market. The existing overcapacity in the fleet further deters greenfield entry — why build new when used barges are available from distressed operators? The combination of capital intensity, regulatory barriers, and customer qualification requirements makes new entry extremely difficult.

Bargaining Power of Suppliers: LOW TO MODERATE. Kirby's primary suppliers are U.S. shipyards (for new construction and maintenance), crew labor, fuel providers, and engine manufacturers. Shipyard capacity is limited but not monopolistic — several Gulf Coast and Midwest yards compete for barge construction and repair work. Crew labor is specialized but trainable, though a mariner shortage has driven labor cost inflation in recent years. Fuel costs are largely passed through to customers in contract terms, neutralizing their impact on margins. Engine suppliers (primarily Caterpillar/MaK and EMD) have limited alternatives, but this affects the industry broadly rather than disadvantaging Kirby specifically.

Bargaining Power of Buyers: MODERATE. Kirby's customers include some of the largest companies in the world — ExxonMobil, Shell, Dow, LyondellBasell, and other refining and petrochemical giants. These customers have significant leverage in contract negotiations, particularly during periods of barge oversupply. However, several factors limit buyer power: switching costs are meaningful due to safety qualification requirements and operational integration; long-term contracts (70 percent of inland revenues) provide stability; the service is essential — products must move regardless of economic conditions; and during tight capacity periods, buyers have limited alternatives. Smaller customers have significantly less bargaining power.

Threat of Substitutes: LOW TO MODERATE. The primary substitutes for inland barge transportation are pipelines, rail, and trucking. Pipelines are cheaper for high-volume, fixed-route commodity movements but are inflexible, capital-intensive, and politically difficult to build. Rail costs roughly four times more per ton-mile. Trucking costs twelve times more. For bulk liquid cargoes moving along waterway corridors, barges are the most cost-effective option by a wide margin. The energy transition represents a long-term substitution threat — if petrochemical production eventually declines, barge demand would fall — but this is a multi-decade horizon.

Industry Rivalry: MODERATE TO HIGH. The inland tank barge industry is consolidating but remains fragmented outside of Kirby's dominant position. During periods of tight capacity, competition is rational and pricing is favorable. During periods of oversupply — as in 2016–2020 — rivalry becomes destructive, with operators cutting prices to maintain utilization. Differentiation is limited primarily to safety records, reliability, and fleet quality. Kirby's scale provides advantages in cost, coverage, and customer service, but it does not eliminate rivalry. The cyclical nature of the industry means that the competitive environment oscillates between favorable and brutal, driven primarily by the utilization rate.

The net assessment from Porter's framework is that Kirby operates in an industry with favorable structural characteristics — low threat of entry, low substitution risk, moderate buyer power — but with the critical vulnerability of cyclical industry rivalry. The moat is real but conditional: it functions best when the industry operates near capacity. When excess capacity floods the market, even a dominant player like Kirby cannot fully escape the gravitational pull of price competition. This is why utilization is the master variable for Kirby investors — it determines whether the structural advantages translate into economic returns.

Hamilton's Seven Powers

Scale Economies: STRONG. This is Kirby's primary competitive power. With 28 percent of the inland tank barge market, Kirby achieves lower unit costs through route density (less empty repositioning), purchasing power (fuel, insurance, equipment), overhead absorption (fixed costs spread across a large revenue base), and shipyard relationships (priority access and better pricing). The Jones Act amplifies scale economies by making fleet expansion extraordinarily expensive — a new entrant cannot quickly or cheaply build a comparable fleet. Scale economies are strongest during tight capacity periods when Kirby's fleet size translates directly into superior service and coverage.

Switching Costs: MODERATE TO STRONG. Kirby's 92 percent customer retention rate is empirical evidence of meaningful switching costs. These arise from safety and regulatory qualification (petrochemical companies extensively vet carriers and switching requires re-qualification), operational integration (scheduling, loading procedures, and communication systems built over years), specialized equipment (tank barges configured for specific chemical cargoes), and long-term contracts that create lock-in. These switching costs are real but not absolute — a sufficiently motivated customer can switch, but the friction is substantial.

Process Power: STRONG. Kirby has built institutional knowledge over decades that is difficult to replicate. This includes fleet management and optimization across 1,100-plus barges, maintenance and dry-docking scheduling, crew training and safety protocols (76 percent reduction in cargo spills since 2002), acquisition integration playbooks refined over thirty-plus deals, and regulatory compliance expertise across multiple federal and state agencies. These capabilities are embedded in the organization — in its systems, its people, and its culture — and would take any competitor years to develop.

Cornered Resource: MODERATE. Kirby's Jones Act-compliant fleet of 1,105 inland tank barges is a resource that took decades and billions of dollars to assemble. New construction is constrained by limited U.S. shipyard capacity and elevated costs. Experienced mariners are a scarce resource in a tight labor market. Customer relationships built over an average of 17.6 years cannot be quickly replicated. However, these resources are not truly "cornered" in Helmer's strict sense — a sufficiently capitalized competitor could theoretically build a fleet over time, though it would take many years and billions of dollars.

Branding: MODERATE. Kirby's reputation for safety and reliability matters in an industry where customers are entrusting the operator with hazardous chemicals that, if spilled, could cause catastrophic environmental damage. This brand value is real but operates in a business-to-business context rather than a consumer-facing one. It supplements other powers rather than standing alone.

Network Effects: WEAK. There are limited true network effects in barge transportation. More barges on the water do not exponentially increase the value of the service. The benefits of fleet size are better characterized as scale economies and density advantages than network effects.

Counter-Positioning: NOT PRESENT. Kirby is the incumbent, not the challenger. No disruptive business model has emerged that Kirby cannot or would not adopt. The Jones Act prevents foreign low-cost disruptors from entering the market.

Summary. Kirby's moat is real, durable, and multi-layered, built on the combination of scale economies, switching costs, and process power, all reinforced by the Jones Act's regulatory protection. The moat is strongest during periods of tight capacity, when Kirby's advantages translate directly into pricing power and market share gains. It is most vulnerable during periods of sustained overcapacity, when the structural advantages are overwhelmed by the cyclical dynamics of a capital-intensive industry.

This is a critical nuance that separates Kirby from true wide-moat businesses like Visa or Google. Kirby has a real moat — but it is a cyclical moat. During tight markets, the moat functions beautifully: scale advantages translate to pricing power, customers are locked in, and competitors cannot easily add capacity. During loose markets, the moat still exists but is less valuable: the fundamental advantages in cost, safety, and customer relationships do not disappear, but they cannot prevent margin compression when there are simply too many barges chasing too little cargo. The investor's challenge is determining where in the cycle Kirby sits at any given moment — and whether the current environment reflects structural improvement or merely a cyclical peak.

The comparison to other cyclical moat businesses is useful. Think of Nucor in steel, or Deere in agricultural equipment. Both have genuine competitive advantages — Nucor's mini-mill cost structure, Deere's dealer network and precision agriculture technology — but both are subject to end-market cyclicality that can temporarily overwhelm those advantages. Kirby fits this pattern. The question is whether the petrochemical growth story provides a secular tailwind strong enough to moderate the cyclicality, or whether the industry's history of boom-bust will inevitably repeat.

XII. Bull vs. Bear Case

Bull Case

The bull case for Kirby rests on the American petrochemical renaissance. Cheap natural gas feedstocks have made U.S. petrochemical producers the most competitive in the world, driving a generational wave of capacity expansion along the Gulf Coast. Ethylene demand is forecast to grow 45 percent between 2020 and 2028, and 51 percent by 2035. Every new cracker and chemical plant generates incremental barge demand for feedstocks and finished products. Kirby, as the dominant operator on the Gulf Coast waterway network, is the primary beneficiary.

Consolidation continues to work in Kirby's favor. The company has demonstrated that it can buy, integrate, and optimize acquired fleets with disciplined execution. With 28 percent market share and no competitor even close to half that size, Kirby has the financial and operational capacity to continue consolidating the industry. Every acquisition extends the scale advantages, deepens customer relationships, and widens the moat.

The supply-demand balance favors incumbents. Nearly 40 percent of the U.S. inland barge fleet is 20 years old or older. Retirements are accelerating as operators face expensive maintenance decisions on aging equipment. Newbuild activity is constrained by limited shipyard capacity and elevated steel prices. This structural tightness supports sustained pricing power and high utilization rates.

Barge transportation is also the most environmentally efficient form of freight transportation — emitting one-ninth the carbon of trucking per ton-mile. In a world increasingly focused on carbon footprint, this structural advantage could become a positive ESG narrative rather than a headwind.

There is also a less-discussed bull argument around Kirby's infrastructure irreplaceability. The inland waterway system is a natural monopoly — there is only one Mississippi River, one Gulf Intracoastal Waterway, one Houston Ship Channel. You cannot build a parallel river. And the petrochemical plants, refineries, and terminals that line these waterways are fixed assets with multi-decade lifespans. As long as these plants operate, their products must move by barge. This geographic lock-in creates a demand floor that is more durable than many investors appreciate.

Bear Case

The bear case centers on the long-term demand trajectory for fossil fuel-derived products. If the energy transition accelerates beyond current projections, demand for refined petroleum products — gasoline, diesel, jet fuel — could peak and decline, reducing barge volumes on key Gulf Coast routes. While petrochemicals are more durable than transportation fuels, they are not immune to a world that aggressively limits plastic production or develops bio-based alternatives.

Cyclicality remains Kirby's fundamental vulnerability. The inland tank barge industry has a long history of boom-bust cycles driven by the interplay of demand fluctuations and capacity additions. The 2016–2020 downturn demonstrated how quickly pricing power can evaporate when utilization drops below 90 percent. The current tight market could attract new vessel orders that eventually re-create overcapacity.

Capital intensity limits returns. Barges and towboats are expensive to build, maintain, and replace — all at U.S. shipyard prices that are four times world levels. Returns on invested capital through the full cycle may be less impressive than peak-year margins suggest. The Distribution and Services segment, while providing diversification, has demonstrated marginal economics at best during oil and gas downturns, raising the question of whether the Stewart and Stevenson acquisition created lasting value or simply added another source of cyclicality.

Regulatory risk cuts both ways. The Jones Act protects Kirby from foreign competition but also constrains the industry's ability to reduce costs. Any political erosion of the Jones Act — however unlikely — would fundamentally change the competitive dynamics. Environmental regulations are increasing the cost of fleet operations, from Tier 3 engine requirements to potential carbon pricing.

There is also the question of management succession. Grzebinski has been CEO since 2014 and is now in his sixties. Kirby's track record through only two CEO transitions — Peterkin to Pyne, Pyne to Grzebinski — makes succession an infrequent but high-stakes event. The next CEO will need to navigate the energy transition, manage a more consolidated competitive landscape, and potentially transform the Distribution and Services segment. The quality of that transition will matter enormously.

Finally, the accounting reality of a capital-intensive roll-up deserves scrutiny. Kirby carries approximately $2.3 billion in net property and equipment on its balance sheet. Depreciation policies, impairment testing, and the treatment of acquisition goodwill all involve significant management judgment. The $433 million impairment charge in 2020 was a reminder that asset values in this industry can change dramatically when cycle conditions deteriorate.

Key Metrics to Watch

For investors tracking Kirby's ongoing performance, two KPIs stand above all others:

Inland tank barge utilization rate. This is the single most important leading indicator of Kirby's earnings power. When utilization is in the low-to-mid 90 percent range, pricing power is strong and margins expand. When utilization drops below 90 percent, pricing deteriorates rapidly. Management reports this metric quarterly, and it should be the first number investors look for in every earnings release.

Term contract renewal pricing. Because 70 percent of inland revenues are under multi-year term contracts, the rate at which these contracts renew relative to expiring rates is a critical indicator of forward earnings trajectory. Mid-single-digit or higher renewal increases signal a healthy market. Flat or declining renewals indicate softening conditions. This metric provides visibility into future revenue quality and should be tracked alongside utilization.

Together, these two metrics — utilization and contract renewal pricing — tell investors nearly everything they need to know about Kirby's near-term earnings trajectory. When both are trending favorably, as they have been since 2022, Kirby is in the sweet spot. When either begins to deteriorate, it is time to reassess.

XIII. Epilogue: What Is Next for Kirby?

David Grzebinski, now in his twelfth year as CEO, has guided Kirby through the worst downturn in the company's history and delivered record financial results on the other side. The stock's all-time high in early March 2026 is a market endorsement of his leadership. But the next chapter raises questions that neither financial discipline nor operational excellence can fully answer.

The next wave of consolidation is coming. The Redwood Holdings acquisitions of Canal Barge Company and Marquette Transportation in 2024 signal that private equity capital sees opportunity in the inland marine space. Smaller operators with aging fleets and retirement-age owners will continue to look for exits. Kirby, with its integration track record and financial capacity, remains the natural acquirer — but it will face more competition for deals as the industry attracts outside capital.

Technology and automation are slowly transforming marine operations. Digital fleet optimization, predictive maintenance using sensor data, and eventually autonomous navigation could change the economics of inland transportation. Kirby has invested in technology for fleet management and safety, but the pace of technological change in maritime is slower than in other transportation sectors — partly due to regulatory conservatism, Coast Guard oversight, and the complexity of river navigation where conditions change with every season and every storm.