Keurig Dr Pepper: The Unlikely Marriage of Coffee and Soda

I. Introduction & Episode Roadmap

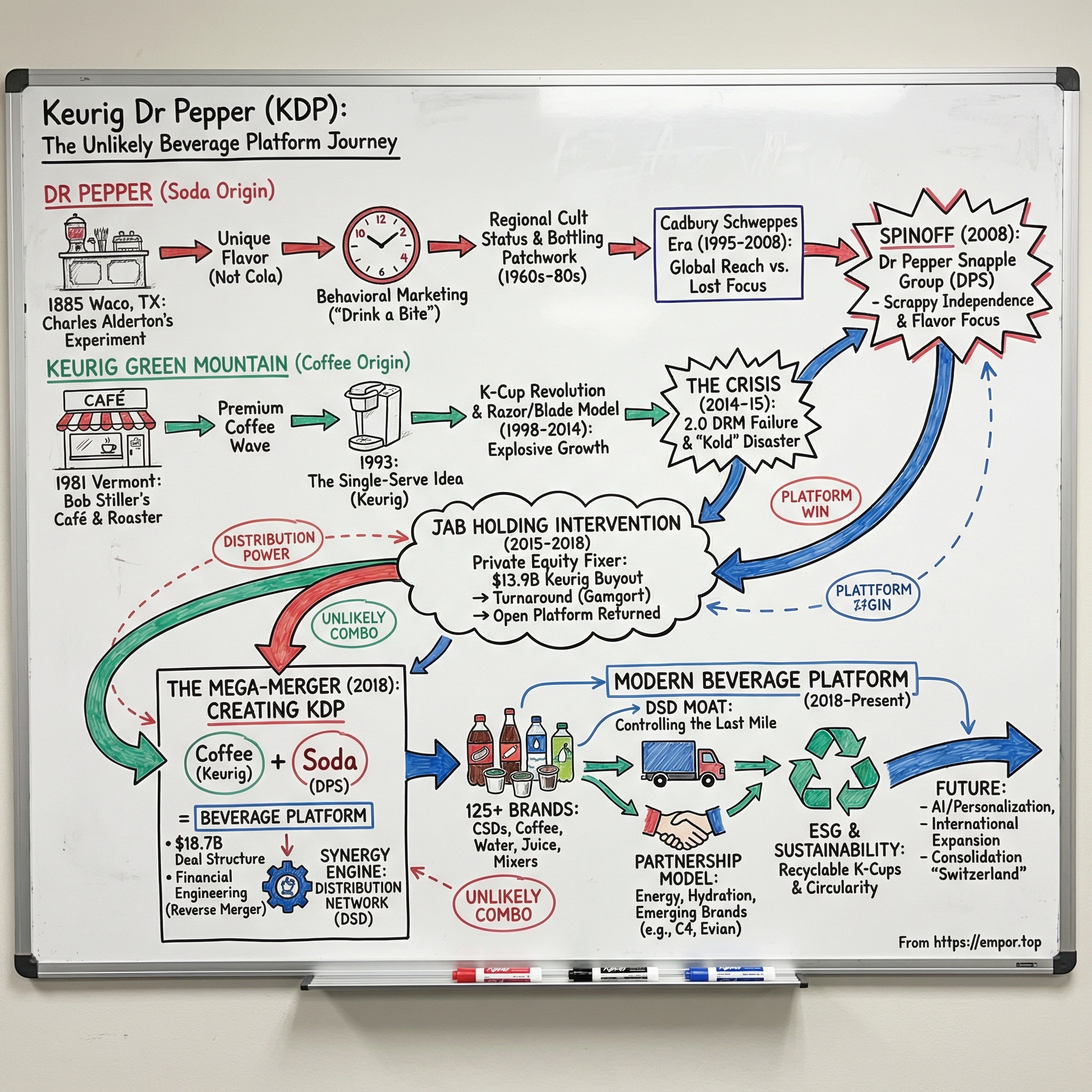

Picture this: January 2018, a Plano, Texas boardroom. Larry Young, the scrappy CEO of Dr Pepper Snapple Group, sits across from Bob Gamgort, the turnaround artist who'd just rescued Keurig from near-death. Between them lies a proposal so audacious that their investment bankers initially thought it was a joke—merge a 133-year-old soda company with a coffee pod maker owned by a secretive European investment firm. The result would create an $18.7 billion beverage giant that no one saw coming.

This is the story of how a Vermont coffee roaster that started in a converted gas station and America's oldest major soft drink—invented in a Waco drugstore before Coca-Cola even existed—came together to build the third-largest beverage company in North America. It's a tale of two companies that shouldn't work together but somehow do, united by an obsession with distribution networks, a shared belief in the power of brands, and the financial engineering wizardry of JAB Holding Company. Today, Keurig Dr Pepper is a leading beverage company in North America, with a portfolio of more than 125 owned, licensed and partner brands and annual revenue of more than $15 billion. The company holds leadership positions in beverage categories including carbonated soft drinks, coffee, tea, water, juice and mixers, and has the #1 single serve coffee brewing system in the U.S. and Canada. But how did we get here?

What we'll explore is a masterclass in platform building through unlikely combinations. We'll trace two parallel journeys: how a regional Texas soda brand survived 100+ years of industry consolidation, and how a Vermont specialty coffee roaster discovered the power of single-serve brewing. We'll see how private equity financial engineering, distribution synergies, and a shared DNA of scrappy independence created unexpected value.

The key themes that emerge: the enduring power of distribution as competitive advantage, how razor-and-blade business models create durable moats, and why sometimes the best mergers are the ones nobody expects. This isn't just a story about beverages—it's about how platforms win in mature industries.

II. The Dr Pepper Origin Story: America's Oldest Major Soft Drink (1885-1995)

The year is 1885. In Morrison's Old Corner Drug Store in Waco, Texas, a young pharmacist named Charles Alderton is experimenting behind the soda fountain. The 28-year-old, who'd studied medicine at the University of Texas and worked in a drug store in Castle Rock, Texas, notices how customers love the aroma when they walk into the store—that mix of fruit syrups and carbonated water that fills the air. He starts tinkering, mixing various fruit flavors, trying to capture that scent in a drink.

After months of experimentation with 23 different flavors (a number that would become marketing legend), Alderton creates something unique: a dark, fizzy concoction that tastes nothing like the bitter medicinal tonics of the era. The locals love it. They start coming in asking for a "Waco." The store owner, Wade Morrison, sees the potential and names it "Dr. Pepper" (the period would be dropped in the 1950s). The origin of the name remains disputed—some say it was after Dr. Charles T. Pepper, a Virginia physician Morrison knew; others claim it was purely invented for its medicinal sound. Here's what made Dr Pepper different: it wasn't a cola, and the company turned that into an advantage. By 1904, Dr Pepper was introduced to a national audience at the World's Fair in St. Louis, alongside the hamburger and the ice cream cone. But unlike Coca-Cola, which would grow through aggressive national expansion, Dr Pepper remained fiercely regional for decades, spreading slowly through Texas and the Southwest via a patchwork of independent bottlers.

The genius came in the 1920s. During the 1940s there were studies published that showed the average person experienced a slump in energy at 10:30, 2:30, and 4:30. With this information Dr. Pepper held a contest to find a new advertising slogan. The winning submission was to "Drink a bite to eat at 10, 2, and 4." The campaign launched in the 1930s and ran for roughly 20 years. This wasn't just advertising—it was behavioral engineering. Dr Pepper positioned itself not as a treat but as medicine, a three-times-daily energy boost backed by science. Clock towers with only "10," "2," and "4" on their faces appeared across Texas. The numbers became so iconic they appeared on bottles for decades.

The franchise bottling model that Dr Pepper adopted—similar to Coca-Cola's but more decentralized—created both opportunity and challenge. Each bottler was essentially an independent business owner with exclusive territorial rights. This meant Dr Pepper could expand without massive capital investment, but it also meant uneven quality, inconsistent marketing, and perpetual distribution headaches. While Coke was building a monolithic empire, Dr Pepper was herding cats.

By the 1960s, Dr Pepper faced an existential choice. The Cola Wars between Coke and Pepsi were intensifying, with both giants pressuring retailers for exclusive shelf space. Dr Pepper's response was clever: lean into being different. "Be a Pepper" campaigns celebrated the brand's outsider status. The company even promoted drinking it hot with lemon in winter—anything to avoid direct competition with the cola giants.

The 1970s and 80s saw Dr Pepper change hands repeatedly, each owner trying to solve the distribution puzzle. In 1962, a federal court ruling forced Coca-Cola to divest its Dr Pepper bottling operations, giving the brand a chance at wider distribution. By 1984, Dr Pepper was acquired by investment firm Forstmann Little for $512 million, then quickly merged with Seven Up in 1986, creating Dr Pepper/Seven Up Companies. But the combined entity still struggled against the cola duopoly. The critical turning point came in 1995. Cadbury Schweppes purchased Dr Pepper/Seven Up in 1995, paying about US$1.7 billion, plus about US$870 million of Dr Pepper/Seven-Up debt. For Dr Pepper, this meant finally having a global partner with deep pockets and international distribution expertise. For Cadbury, it meant becoming the largest soft drink company in the world not to be named after a cola beverage. The Waco wonder had found its unlikely dance partner—a British confectionery giant that saw opportunity where others saw only a third-place also-ran.

III. Green Mountain Coffee Roasters: From Vermont Café to K-Cup Revolution (1981-2006)

In 1981, Bob Stiller was visiting friends in Waitsfield, Vermont, when he wandered into a small café near Sugarbush ski resort. The aroma hit him first—rich, dark-roasted coffee unlike anything he'd tasted back in New York. The café was struggling, barely making ends meet, but Stiller saw something others didn't: Americans were ready to pay more for better coffee. This was years before Starbucks went public, before "artisanal" became a marketing buzzword. Stiller bought the café and its small roasting operation for $45,000.What Stiller lacked in coffee experience, he made up for in business acumen. He'd just sold his previous company, E-Z Wider rolling papers (yes, for exactly what you think), for $3.1 million in 1980. He spotted his next opportunity in Green Mountain's premium coffee beans and grounds, and bought and reincorporated the business in 1981. By 1982, the company had around 30 employees, and moved its production facilities to Waterbury, Vermont.

The early years were brutal. Stiller bought out his two partners for $100,000 and became sole proprietor within two years, but it took four years to turn a profit—after losing over $1 million in the first three years. Without money for advertising, Stiller gave out free samples everywhere: gas stations, high-end restaurants, anywhere people gathered. He adopted technology early, using computers to track customer orders and regulate roasting temperatures when competitors were still using paper ledgers. The pivotal moment came in 1993. Three engineering entrepreneurs from a Massachusetts start-up approached GMCR about developing a single-cup coffee brewing system. John Sylvan and Peter Dragone had founded Keurig (they thought it meant "excellence" in Dutch; it actually means "proper" or "neat"). Their vision: solve the office coffee problem where the first cup is fresh but the last cup from the pot is burnt sludge. Green Mountain immediately saw the potential and made its first investment in Keurig that year.

By 1996, GMCR had acquired a 35% stake in Keurig. The relationship deepened quickly—in 1997, GMCR became the first roaster to offer coffee in K-Cup pods, and by 1998, Keurig delivered its first brewing system designed for office use. This wasn't just an investment; it was a strategic partnership that would transform both companies.

Green Mountain went public in 1993 on NASDAQ under "GMCR," the same year it discovered Keurig. The timing was fortuitous—it gave Green Mountain the currency to continue investing in what would become its golden goose. By 2003, Green Mountain owned 43% of Keurig, and the board faced a decision: double down or stay a minority investor. In 2006, Stiller pulled the trigger. Green Mountain acquired all the outstanding shares it didn't already own for $104.3 million in cash, implying a total value of approximately $160 million for 100% of Keurig. It was a bet-the-company move—Green Mountain's revenues in 2005 were only about $161 million. But Stiller saw what others didn't: this wasn't just buying a coffee machine company; it was buying a platform that would transform coffee consumption.

The genius of the acquisition became clear immediately. It allowed GMCR to transition fully from deriving 95% of its revenue from its low-margin wholesale coffee business in the late 1990s (approximately $65 million), to deriving 95% of its revenue from high-margin sales of K-Cups as of 2014 (more than $4.3 billion). The razor-and-blade model was coffee gold—sell the brewers at breakeven, make fortunes on the pods.

But the real masterstroke was keeping Keurig open to other brands. While Green Mountain was the dominant K-Cup producer, partners like Diedrich/Gloria Jeans, Timothy's, Van Houtte, Celestial Seasonings, and Tully's could all make pods for Keurig machines. This created a virtuous cycle: more pod variety meant more brewer sales, which meant more pod sales for everyone. By 2008, K-Cups were in supermarkets nationwide. The little Vermont coffee roaster had cracked the code.

IV. The Dr Pepper Snapple Spinoff: Finding Independence (1995-2008)

While Green Mountain was discovering the power of single-serve, Dr Pepper was navigating the treacherous waters of corporate ownership. The 1995 Cadbury Schweppes acquisition had given Dr Pepper global reach and deep pockets, but it also buried the brand within a sprawling conglomerate more focused on chocolate than carbonation. By the early 2000s, something had to give. The problem was distribution warfare. In 2006 and 2007, Cadbury Schweppes purchased the Dr Pepper/Seven Up Bottling Group, along with several other regional bottlers. This was critical—Coca-Cola and Pepsi had essentially stopped bottling and distributing Cadbury-Schweppes products in favor of their own in-house alternatives. Dr Pepper was being squeezed off the shelves by its supposed distribution partners. By acquiring its own bottling operations, Dr Pepper could finally control its own destiny.

Then came the announcement that shocked no one who understood the logic: In November 2007, Cadbury Schweppes announced it would spin off its American beverages unit. The chocolate maker wanted to focus on confectionery; the beverage business needed independence to compete. On May 5, 2008, the spinoff was complete, creating Dr Pepper Snapple Group. Two days later, on May 7, 2008, shares began trading on the NYSE under "DPS."

The timing couldn't have been worse. Larry Young, who would become CEO of the newly independent company, later called it "probably the worst time to go public." The financial crisis was in full swing—Lehman Brothers would collapse just four months later. Dr Pepper Snapple's stock immediately tanked, falling from its opening price of $26 to below $15 by year-end.

But adversity bred creativity. Young and his team embraced their underdog status, positioning Dr Pepper Snapple as "the scrappy #3 player" against Coca-Cola's 34% market share and Pepsi's 25%. They couldn't win through scale, so they won through focus. While Coke and Pepsi fought over colas, Dr Pepper Snapple dominated flavored carbonated soft drinks. While the giants went global, Dr Pepper Snapple doubled down on North America.

The strategy worked. By owning their bottling operations, Dr Pepper Snapple could ensure their products stayed on shelves. By focusing on non-cola brands, they avoided direct competition. By staying regional, they could move faster and adapt quicker. The company that started 2008 as an afterthought was, by 2017, capturing 22.5% market share in North America. Independence, it turned out, was exactly what Dr Pepper needed.

V. Keurig's Rise and Fall: K-Cups, Competition, and Crisis (2006-2015)

The post-acquisition years at Keurig were nothing short of miraculous—at first. With Green Mountain's distribution muscle behind it, K-Cup sales exploded. By 2008, K-Cups were in supermarkets nationwide. Coffee pod machine sales multiplied more than six-fold between 2008 and 2014. Green Mountain's stock price reflected the euphoria, soaring from $15 in 2009 to an all-time high of $157 in November 2014.The 2014 Coca-Cola partnership looked like validation. In February 2014, The Coca-Cola Company purchased a 10% stake in the company for $1.25 billion at $74.98 per share, with an option to increase to 16% (which it quickly exercised). The partnership was meant to develop Keurig Cold, a machine that would do for sodas what K-Cups did for coffee. Wall Street loved it—the stock jumped 25% on the announcement.

But beneath the surface, cracks were forming. In 2012, Keurig's main K-Cup patents had expired, opening the floodgates to competitors. Suddenly, everyone from Dunkin' to store brands could make pods that worked in Keurig machines. Green Mountain's response would prove catastrophic. Enter the Keurig 2.0—the product that would nearly destroy the company. Launched in fall 2014, the new machines included what the tech world called "DRM for coffee." Using infrared sensors, the machines would only accept officially licensed K-Cups, locking out competitors and even Keurig's own popular My K-Cup reusable pods. CEO Brian Kelley defended it as ensuring "excellent quality beverages produced simply and consistently every brew every time."

The backlash was immediate and brutal. Consumers felt betrayed. Hackers posted YouTube videos showing how to defeat the system with Scotch tape and scissors. Competitors sued for antitrust violations—eventually winning a $31 million settlement. Amazon reviews were savage. By the first quarter of 2015, brewer sales had plummeted 23% year-over-year.

Meanwhile, the Coca-Cola partnership's crown jewel—Keurig Kold—was turning into a disaster. The machine, meant to make cold sodas at home, cost $369, required special pods that cost $1.25 each (for an 8-ounce serving!), took 90 seconds to make a drink, and sounded like a jet engine. It launched in September 2015 to universal ridicule. By June 2016, Keurig discontinued it entirely, offering full refunds to the few customers who'd bought one.

The stock price told the whole story: from $157 in November 2014 to $40 by November 2015—a 75% collapse. Coca-Cola's $2 billion investment was underwater by $1 billion. In May 2015, a chastened Kelley admitted on an earnings call: "We were wrong. We underestimated it." The company rushed to bring back the My K-Cup, but the damage was done.

Green Mountain had violated the cardinal rule of platform businesses: never abuse your market power so obviously that customers revolt. The company that had built its fortune on openness and variety had tried to become a walled garden. The walls came tumbling down, and with them, billions in market value. Something had to change—and fast.

VI. The JAB Takeover: Private Equity Meets Coffee (2015-2018)

On December 7, 2015, with Keurig's stock in freefall and its reputation in tatters, salvation arrived from an unlikely source: JAB Holding Company, the secretive investment vehicle of Germany's billionaire Reimann family. JAB announced it would acquire Keurig Green Mountain for $13.9 billion in cash—$92 per share, a stunning 78% premium over Friday's closing price. Wall Street was stunned. JAB was paying $92 a share for a stock trading at $51. Even Coca-Cola, which stood to lose $1 billion on its investment, supported the deal—anything to stop the bleeding. The acquisition closed in March 2016, taking Keurig private and giving it breathing room away from quarterly earnings pressures.

JAB wasn't new to coffee. The secretive firm, controlled by Germany's billionaire Reimann family, had been quietly assembling a coffee empire: Peet's Coffee, Caribou, Jacobs Douwe Egberts (owner of Tassimo), and now Keurig. Their playbook was consistent: buy underperforming brands, fix operations, merge strategically, create scale.

In May 2016, JAB brought in their turnaround specialist: Robert Gamgort, who'd just spent seven years as CEO of Pinnacle Foods, increasing that company's value five-fold. Gamgort was a fixer—at Mars, he'd turned around M&M; at Pinnacle, he'd revitalized tired brands like Duncan Hines and Birds Eye. Now he faced his biggest challenge yet.

Gamgort's first moves were swift and decisive. Kill Keurig Kold—done by June 2016, with full refunds offered. Fix the 2.0 debacle—bring back My K-Cup compatibility, quietly remove the DRM restrictions, rebuild trust with consumers. Cut costs ruthlessly—streamline operations, reduce SKUs, focus on what works.

But the real genius was in rebuilding partnerships. Gamgort personally visited major retailers, third-party pod makers, even competitors. The message was clear: the arrogant Keurig of 2014 was dead. The new Keurig would be a platform player again, open to all.

The numbers started turning around quickly. By 2017, K-Cup sales were growing again. Brewer sales stabilized. The bleeding stopped. But Gamgort and JAB weren't done—they had bigger plans. Coffee was just one part of the beverage market. What if you could combine Keurig's at-home platform with a portfolio of ready-to-drink beverages? What if you could merge distribution networks to create unbeatable scale?

The answer to those questions was sitting in Plano, Texas, running its own turnaround story.

VII. The Mega-Merger: Creating Keurig Dr Pepper (2018)

The meeting took place in late 2017, away from prying eyes. Bob Gamgort flew to Dallas to meet Larry Young at a neutral location—neither wanted word getting out. The proposal Gamgort brought was audacious: merge Keurig with Dr Pepper Snapple Group to create a beverage platform unlike anything in North America.

On paper, it was simple math. Dr Pepper Snapple shareholders would receive $103.75 per share in cash—about $18.7 billion total—creating a beverage giant with about $11 billion in annual sales. But the genius was in the structure. Shareholders of Dr Pepper Snapple Group would own 13% of the combined company, with Keurig shareholder Mondelez International owning 13% to 14%, and JAB Holding Company owning the remaining 73-74%.

This wasn't a takeover—it was a reverse merger disguised as an acquisition. Dr Pepper Snapple would technically acquire Keurig, inheriting its public listing and saving JAB from an expensive IPO process. Meanwhile, JAB would inject $9 billion in fresh equity, giving the combined company the firepower for future acquisitions while maintaining control.

The merger promised to create $600 million in annual cost-savings, but the real synergies went deeper. Dr Pepper Snapple's distribution network was a large part of the appeal to Keurig in their merger. With Dr Pepper's direct store delivery system reaching virtually every retail outlet in America, Keurig could finally push its ready-to-drink coffee products nationally without building infrastructure from scratch.

The cultural fit was surprisingly natural. Both companies had scrappy DNA—outsiders who'd survived through innovation rather than scale. Both understood the power of brands over commodities. Both had learned painful lessons about hubris (Keurig with 2.0, Dr Pepper with countless failed product launches).

On July 9, 2018, the merger closed successfully, and shares in Keurig Dr Pepper began trading on the New York Stock Exchange on July 10, 2018, under the ticker symbol KDP. The transaction created the seventh-largest company in the U.S. food and beverage sector and third-largest beverage company in North America, with annual revenues of approximately $11 billion.

Larry Young retired gracefully, joining the board but ceding operational control to Gamgort. The headquarters remained dual—Waterbury for coffee, Plano for beverages—preserving both cultures while building something new. Wall Street loved it: Dr Pepper stock jumped 25% on announcement day.

But the real test would come in execution. Could two companies with such different histories truly become one? Could JAB's financial engineering translate into operational excellence? The answer would reshape the North American beverage landscape.

VIII. Building the Modern Beverage Platform (2018-Present)

The first hundred days after the merger set the tone. Gamgort moved fast but carefully, keeping the best of both cultures while ruthlessly cutting redundancies. The promised $600 million in synergies? They hit it in 18 months, not the projected three years. But cost-cutting was just table stakes—the real transformation was strategic.

The combined company now controlled an astounding portfolio: over 125 owned, licensed, and partner brands spanning every beverage occasion. The organizational structure reflected this complexity, divided into three segments: U.S. Refreshment Beverages (the Dr Pepper legacy), U.S. Coffee (the Keurig business), and International (Canada, Mexico, and emerging markets). Each operated semi-autonomously but shared the crown jewel: distribution.

The Direct Store Delivery (DSD) network became KDP's ultimate moat. With a fleet of thousands of trucks and an army of route drivers who stock shelves directly, KDP could guarantee product freshness and placement in ways competitors couldn't match. This wasn't just logistics—it was a data goldmine. Every delivery driver became a market researcher, tracking what sold, what didn't, and what competitors were doing.

The partnership model, refined during Keurig's recovery, became the growth engine. Starbucks, Dunkin', and McCafé all signed licensing deals for K-Cup pods. But KDP went further—they became the distribution partner of choice for emerging brands. BodyArmor, Vita Coco, Evian in the U.S.—brands that needed national reach but couldn't afford to build it themselves.

Energy drinks emerged as the surprise winner. Through partnerships with C4 Energy and GHOST, plus the acquisition of ethical energy brand Limitless, KDP captured share in the fastest-growing beverage category without competing head-on with Monster or Red Bull. The strategy was classic KDP: find the white space, partner don't conquer, use distribution as the differentiator.

In September 2020, KDP made a strategic move, transferring its stock market listing to the Nasdaq to get access to a more diverse set of investors, with trading on the Nasdaq beginning on September 21. The company retained its "KDP" ticker, signaling continuity amid change.

The COVID-19 pandemic, rather than crushing the business, accelerated key trends. At-home coffee consumption exploded—K-Cup sales surged as offices emptied and kitchen counters became workspaces. The installed base of Keurig brewers in U.S. households reached 37 million by 2021. Meanwhile, fountain beverage sales collapsed, but retail sales more than compensated as consumers stockpiled their favorite drinks.

Premium water became the next frontier. Beyond distributing Evian and Core Hydration, KDP launched new alkaline and electrolyte-enhanced waters. The acquisition of Electrolit gave them a foothold in the growing hydration/recovery segment. Every move followed the same playbook: identify growing categories, acquire or partner strategically, leverage distribution for dominance.

But the masterstroke was maintaining independence while competitors consolidated. As PepsiCo bought Rockstar and Coca-Cola took full control of BodyArmor, KDP remained the Switzerland of beverages—happy to work with everyone, threatening to no one, essential to many. As a Keurig Dr Pepper spokeswoman stated: "We are very committed to the partnership model".

By 2023, the transformation was complete. What started as an unlikely merger of coffee and soda had become North America's most innovative beverage platform—proof that in mature industries, the best strategy isn't always direct competition. Sometimes it's being the platform that enables everyone else to compete.

IX. Playbook: Lessons in Platform Building & Financial Engineering

The Keurig Dr Pepper story isn't just about beverages—it's a masterclass in value creation through unlikely combinations. The playbook that emerged offers lessons far beyond the beverage aisle.

First, distribution as competitive advantage. In the digital age, when everyone obsesses over direct-to-consumer, KDP proved that controlling physical distribution still matters. Their DSD network isn't just trucks and drivers—it's a relationship network, data collection system, and barrier to entry rolled into one. When you control the last mile to 250,000+ retail locations, you become indispensable.

The single-serve coffee system exemplifies the enduring power of razor-and-blade business models. Keurig brewers are sold at near-breakeven, sometimes at a loss. But once that brewer sits on a counter, it generates high-margin K-Cup sales for years. The genius was keeping the system open enough to attract partners but closed enough to maintain quality control. It's a balance Nespresso never achieved and SodaStream never attempted.

Managing complexity became a core competency. With 125+ brands across multiple categories, KDP could have drowned in SKU proliferation. Instead, they built systems to manage complexity profitably. Each brand has a role: some drive volume, some command premium prices, some fill portfolio gaps, some block competitors. It's portfolio theory applied to consumer products.

The JAB financial engineering deserves its own Harvard case study. Buy distressed (Keurig at its nadir), fix operations (bring in Gamgort), merge strategically (Dr Pepper for distribution), take public efficiently (reverse merger structure), maintain control while adding liquidity (73% ownership dropping gradually). It's private equity perfection—creating value through operational improvement, not just financial leverage.

The transition from private to public was remarkably smooth. In September 2020, JAB Holding Co redistributed about 76 million shares, or 5.4%, to its minority partners. Following the redistribution, JAB owned 44% of Keurig, Mondelez International continued to own 12%, and the public float increased to 44%. This gradual democratization of ownership provided liquidity while maintaining strategic control.

Capital allocation became increasingly sophisticated. High-return investments in pod capacity and brewer innovation. Strategic tuck-in acquisitions in growing categories. Disciplined approach to M&A—buy only when distribution synergies are clear. Return cash to shareholders through dividends and buybacks when organic opportunities don't meet hurdle rates.

But perhaps the most important lesson: sometimes the best partnerships are between companies that shouldn't work together. Coffee and soda. Vermont hippies and Texas cowboys. European financial engineers and American consumer marketers. The differences weren't weaknesses to overcome but strengths to leverage.

X. Analysis & Investment Case

Today's Keurig Dr Pepper is a fundamentally different company than either of its predecessors. With over $15 billion in annual revenue and a market capitalization exceeding $40 billion, it's achieved the scale to compete while maintaining the agility to innovate.

The financial profile is compelling. Gross margins exceed 55%, driven by the high-margin K-Cup business and owned brand portfolio. Operating margins approach 23%, best-in-class for large beverage companies. Return on invested capital consistently exceeds 8%, remarkable for a mature industry. Free cash flow generation tops $2 billion annually, funding growth investments and shareholder returns.

Competitive positioning remains unique. Against Coca-Cola and PepsiCo, KDP is the scrappy alternative—large enough to matter, small enough to move fast. Against Monster and Red Bull in energy, they're the distribution partner, not the enemy. Against Nestlé in coffee, they own the at-home single-serve market in North America while Nespresso dominates elsewhere.

Growth drivers are surprisingly robust for a mature category player. Coffee pods still have runway—household penetration is only 40% in the U.S., lower in other markets. Energy drinks, enhanced waters, and functional beverages are growing double-digits annually. The e-commerce channel, while still small, is expanding rapidly with KDP well-positioned through its Keurig.com platform and Amazon partnership.

The risks are real but manageable. Consumer health trends pressure sugary drink sales, but KDP's portfolio increasingly skews toward better-for-you options. Private label competition in K-Cups intensifies, but KDP maintains 70%+ share through innovation and brand strength. Category maturity limits organic growth, but M&A opportunities abound as craft brands seek distribution.

Environmental concerns, particularly around K-Cup recyclability, posed reputational risk. KDP responded aggressively—100% recyclable K-Cups by end of 2020, investment in pod recycling programs, development of compostable options. They turned a weakness into a competitive advantage.

The valuation remains controversial. Trading at roughly 20x forward earnings, KDP commands a premium to traditional beverage companies but a discount to higher-growth consumer brands. Bulls argue the market undervalues the subscription-like nature of K-Cup sales and the platform value of distribution. Bears point to slowing category growth and increasing competition.

What's often missed: KDP is really three businesses. A traditional beverage company (Dr Pepper heritage) trading at 15x earnings. A razor-blade coffee platform (Keurig) worth 25x+. A distribution and partnership platform that's never properly valued. Sum-of-the-parts suggests meaningful upside.

XI. Epilogue & Future Outlook

In April 2024, Tim Cofer became the CEO of Keurig Dr Pepper, while Robert Gamgort remained in the position of Executive Chairman. The transition was seamless—Cofer, a KDP insider who'd run the coffee business, understood both sides of the house. Gamgort's move to Executive Chairman ensured continuity while allowing fresh operational leadership.

The sustainability challenge has evolved from threat to opportunity. K-Cup recyclability, achieved in 2020, was just the start. The company now focuses on circular packaging, water conservation, regenerative agriculture for coffee sourcing. ESG isn't just compliance—it's becoming a competitive advantage with increasingly conscious consumers.

Artificial intelligence and personalization represent the next frontier. Imagine a Keurig brewer that learns your preferences, automatically reorders your favorite K-Cups, suggests new varieties based on consumption patterns. Or a Dr Pepper fountain that customizes sweetness and carbonation to individual tastes. The beverage industry's digital transformation is just beginning.

The consolidation question looms large. Can KDP maintain independence as the beverage industry continues consolidating? JAB's gradual exit suggests eventual full public ownership. But KDP's unique position—too big to ignore, too strategic to absorb easily—might preserve independence. They've become the Switzerland of beverages, valuable to all, threatening to none.

International expansion remains the largest untapped opportunity. While dominant in North America, KDP has minimal presence elsewhere. But rather than competing globally with Coke and Pepsi, they're pursuing a partnership model—licensing Keurig technology, distributing through local partners, acquiring regional brands. It's globalization, KDP-style.

The broader lesson transcends beverages. In mature industries, value creation doesn't require disruption. Sometimes it's about combination—bringing together assets that multiply rather than add. Sometimes it's about platforms—becoming the infrastructure others need to compete. Sometimes it's about patience—playing the long game while others chase quarterly earnings.

The marriage of coffee and soda that began in that Plano boardroom has produced something neither parent could have achieved alone. It's a reminder that in business, as in life, the most successful unions are often the most unexpected. Keurig Dr Pepper isn't just a beverage company—it's proof that with the right strategy, operational excellence, and a little financial engineering, even the most unlikely combinations can create extraordinary value.

The story continues to unfold. Each morning, millions of Americans start their day with a K-Cup brew. Each afternoon, millions more reach for a Dr Pepper or Snapple. Behind these routine moments lies one of modern business's most fascinating transformation stories—a tale of two companies that found strength in their differences and built something greater than the sum of their parts.

XII. Recent News

The company continues to evolve its portfolio and strategy. Recent announcements have focused on premiumization efforts, with new specialty coffee offerings and enhanced water products gaining traction. Partnership expansions with athletic and energy brands reflect KDP's ongoing push into functional beverages.

Supply chain initiatives, including investments in U.S. manufacturing capacity and vertical integration of key inputs, demonstrate commitment to operational excellence. The company's ability to navigate inflation and supply disruptions better than peers validates its operational model.

Current market performance reflects both opportunities and challenges. While the stock has shown resilience, valuation debates continue as investors weigh growth potential against category maturity. The company's consistent execution and cash generation provide downside protection, while portfolio expansion and international opportunities offer upside potential.

XIII. Links & References

For readers seeking deeper insights into the Keurig Dr Pepper story, the following resources provide valuable perspective:

Books & Long-form Articles: - "Pour Your Heart Into It" by Howard Schultz - Context on specialty coffee's rise - JAB Holding Company analyses from Financial Times and WSJ - Harvard Business School cases on Keurig's business model evolution - Beverage Digest archives for industry context

Key SEC Filings: - 2018 Merger Proxy Statement (definitive insights on deal structure) - Annual 10-K reports showing transformation progress - Investor presentations detailing synergy achievements

Historical Documents: - Dr Pepper Museum archives in Waco, Texas - Green Mountain Coffee Roasters IPO prospectus (1993) - Keurig patent filings revealing technical evolution

Industry Resources: - Beverage Marketing Corporation market share data - Euromonitor reports on global beverage trends - Nielsen data on consumer behavior shifts

The Keurig Dr Pepper story reminds us that in business, as in chemistry, the most interesting reactions often occur when you combine elements that don't obviously belong together. The result can be transformative—creating value that neither component could achieve alone.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube