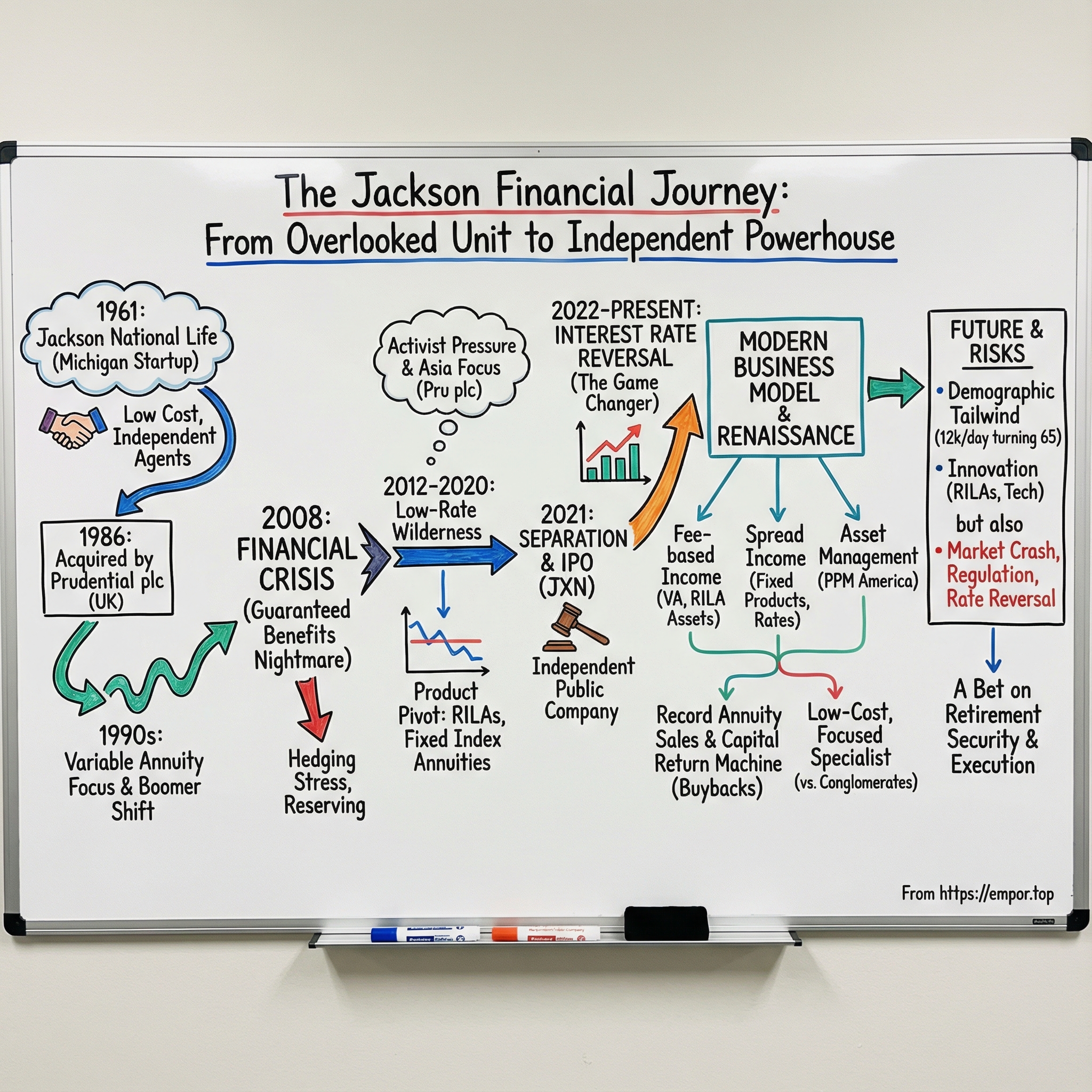

Jackson Financial Inc.: From Prudential Spin to Independent Annuity Powerhouse

I. Introduction & Episode Roadmap

Picture a quiet office in Lansing, Michigan, where actuaries stare at spreadsheets that try to answer an impossibly human question: will millions of Americans outlive their savings? Outside, snow settles over the city. Inside, the leadership team is preparing for something the company has never done: operate on its own.

It’s September 2021. Jackson Financial is about to become one of the most intriguing corporate separations of the decade—a 60-year-old insurer spun out from its British parent at a moment when American retirement anxiety is peaking, and interest rates are on the verge of snapping upward.

Today, Jackson is anything but small. As of December 2024, it managed $252 billion in assets, up from the prior year. In the third quarter of 2025 alone, it sold more than $5.4 billion of retail annuities, including a record $2.1 billion of RILA sales. And yet, until recently, most investors wouldn’t have recognized the name.

So here’s the question that drives this story: how did a business Prudential plc bought for $608 million in 1986 become an independent public company that now generates more than a billion dollars a year in operating earnings—and why did its parent choose the middle of a pandemic to finally let it go?

The answer runs straight through the biggest forces in modern financial services: the collapse of pensions, the aging of the baby boomers, the brutal math of hedging promises in volatile markets, and the strategic logic of corporate separations. Above all, it’s about interest rates—how they can quietly suffocate an insurer for a decade, then suddenly turn the entire industry into a cash machine.

This is a story that starts in Victorian England, swings to a Michigan insurance upstart, survives the existential terror of 2008, and lands on an IPO that, in hindsight, was timed just ahead of a once-in-a-generation rate reversal. Along the way: activist pressure, actuarial nightmares, product innovation, and a quiet revolution in how Americans are funding retirement.

Through 2029, more than 4 million Americans will turn 65 each year, and more of them than ever will do it without a pension to catch them. Jackson sits right at the center of that demographic quake—and if you understand how its business actually works, you start to see why this “boring” insurer might be a key character in one of the biggest financial shifts of the next two decades.

II. The Prudential Backstory: Where Jackson Came From

To understand Jackson, you have to start with its parent—and with a point of confusion that trips up almost everyone: this Prudential is not the American Prudential Financial. Jackson began life in Michigan, but for most of its modern history it sat inside Prudential plc, the British insurer.

Prudential plc was founded in London in May 1848, originally to provide loans to working people and professionals. Those Victorian roots weren’t window dressing; they shaped how the company grew. Prudential built its brand around the “Man from the Pru,” a vast network of agents who went door to door collecting tiny premiums and selling “industrial” insurance—penny-a-week policies to households for whom even basic coverage was a leap of faith in the future.

In 1854, Prudential formally pushed into this new category of Industrial Branch insurance, selling to working-class customers through door-to-door agents, with premiums as low as a penny a week. From that model—high volume, small ticket, relentless distribution—came scale. And from scale came an empire.

Fast-forward to the 1980s. Prudential plc was one of Britain’s biggest financial institutions, but it faced the classic problem of mature European incumbents: growth at home was harder to find, and America looked like the most attractive market in the world. The U.S. wasn’t just bigger; it offered a different set of rules and opportunities, where insurance products could increasingly double as investment vehicles.

Then came the move that would define Jackson’s future. In 1986, Prudential acquired Jackson National Life for $608 million. At the time, Jackson was a regional Michigan insurer—not an obvious crown jewel. But Prudential wasn’t simply buying a book of policies. It was buying a foothold in the American retirement market just as that market was about to surge.

The mid-1980s were also an era of financial deregulation and corporate experimentation. Prudential chased diversification in the UK too, including buying estate agencies after deregulation made that possible. That particular adventure went badly—Prudential lost roughly 90% on those acquisitions when the housing market fell apart in 1989. But while the UK strategy imploded, the U.S. purchase quietly compounded.

What Prudential saw in Jackson was distribution. Jackson had built relationships with independent agents and brokers, a model that could scale without the heavy cost of a captive sales force. And those independent channels were increasingly selling one product in particular—annuities—right as more Americans began confronting retirement without the backstop of traditional pensions.

That’s the pattern worth remembering as we move forward: European financial giants came to the U.S. hunting for growth and often paid for their mistakes. But every so often, they found an asset that fit the moment perfectly. Jackson would become Prudential’s best American bet—which is exactly why the eventual decision to let it go is so interesting.

III. The Birth of Jackson National Life: A Michigan Story (1961–2000s)

Jackson National started small. In 1961, A. J. “Tony” Pasant—a Lansing insurance salesman and field manager with 16 years in the business—founded a regional life insurer with a simple creed: keep overhead low and keep customers happy.

That founding philosophy wasn’t a slogan. It became the operating system. Pasant named the company after President Andrew Jackson and launched with just 12 employees and about $650,000 in assets. Early on, Jackson mostly sold ordinary life insurance to individuals, and it didn’t look particularly exotic. But even then, its instincts were different.

Instead of leaning into the whole life policies that dominated the era, Jackson emphasized term insurance—cheaper, cleaner, and more practical. It was the Midwest version of insurance: buy protection, skip the frills.

Then, in 1971, Pasant made the move that would shape Jackson’s trajectory for decades. He largely dismantled the traditional sales force and embraced what became known as “piggybacking.” Rather than paying to recruit, train, and manage a captive army of agents, Jackson recruited independent agents to sell its products while those agents continued working with other insurers. Pasant found them through direct mail and ads in trade journals. As Forbes later noted, a relatively inexpensive ad could bring in sales capacity—without the fixed cost of building it.

This wasn’t just clever marketing. It was distribution arbitrage. Jackson cut the cost structure, then used that advantage to do three things at once: price competitively for customers, pay attractive commissions to agents, and offer annuity rates that made advisors pay attention. The model fed itself. More agents brought more sales, which supported better economics, which attracted more agents.

By the time Prudential came knocking in 1986, Jackson was no longer a sleepy regional carrier. It had grown into one of the fastest-growing insurers in the country, with $2.2 billion in assets and 550 employees. Among roughly 2,000 U.S. insurance companies, it ranked 18th in new policies sold, 91st in assets, and 60th in premium income. That growth—and, crucially, that distribution engine—made it a compelling target. In 1986, Prudential Corporation plc of London acquired Jackson National.

The acquisition changed the scale of what was possible, but it didn’t change the basic playbook. Prudential largely let Jackson keep doing what worked—and poured fuel on it. In 1991, Prudential made a $300 million surplus contribution. By 1993, Jackson’s capital and surplus exceeded $1 billion, doubling from 1990 levels. Jackson became a major piece of Prudential’s international footprint—described as representing about half of Prudential’s foreign investments—and helped the parent build assets in excess of $90 billion.

And then came the product pivot that mattered most. In 1995, Jackson launched its first variable annuity and began selling guaranteed investment contracts and funding agreements through its Institutional Products Department. This was the hinge moment. Variable annuities wouldn’t just become another line of business—they would become the center of gravity.

The timing was almost unfair. In the 1990s, baby boomers hit their peak earning years. The 401(k) increasingly replaced pensions as the primary retirement vehicle. And as markets got bigger—and more volatile—the promise of guarantees wrapped around market participation became easier to sell. Jackson had already built the independent distribution relationships to ride that wave.

The corporate structure evolved alongside the strategy. In 1992, the company formed Jackson National Life of Michigan as a wholly owned subsidiary, transferring its Michigan business into the new entity. That same year, it incorporated Jackson National Financial Services, Inc., a broker-dealer built to distribute mutual funds and variable products.

The growth showed up in the rankings. In 1992, Fortune listed the company as the 23rd largest life insurer. That year, it reported $16.6 billion in assets and $212 million in earnings, and its individual life insurance and annuity results placed it among the top writers in the country.

By the early 2000s, Jackson had a sharper identity than most insurers: not a generalist trying to compete across every product category, but an annuity specialist with a distribution machine and an obsession with cost efficiency. That focus would become a superpower in normal times—and, later, a point of real danger when the annuity business itself turned volatile.

IV. The Golden Age: Riding the Annuity Wave (2000–2008)

The years before the financial crisis were the peak era for variable annuities—and Jackson didn’t just participate. It led. Its Perspective lineup became the bestselling variable annuity franchise in the country, and Perspective II Flexible Premium Variable & Fixed Deferred Annuity sat at No. 1 for 26 straight quarters across all channels.

That kind of dominance only makes sense once you understand what a pre-crisis variable annuity really was. At its core, it was a tax-deferred investment account where the customer picked “subaccounts” that looked a lot like mutual funds. Then, for an extra fee, you could bolt on insurance features—guarantees that softened the blow of market losses or promised a stream of income that couldn’t be outlived.

In the mid-2000s, that design was a profit engine—as long as three conditions stayed true. Markets needed to rise, because higher account values meant higher fee income. Interest rates needed to be healthy enough that promised crediting rates didn’t become a losing proposition. And customers needed to leave the guarantees mostly untouched, because in good markets, people don’t pull the ripcord. From 2003 through 2007, those conditions lined up about as cleanly as they ever would.

Jackson’s distribution strategy poured gasoline on the fire. Instead of building an expensive captive sales force, it leaned into independent broker-dealers—advisors who could choose from anyone’s products, but kept coming back to Jackson because the offerings were competitive, the commissions were workable, and the service was fast and consistent. Over time, the network widened beyond independents into wirehouses, regional broker-dealers, banks, independent registered investment advisors, third-party platforms, and insurance agents.

That breadth mattered, but the real advantage was the relationship loop. Advisors who got quick answers and clean execution sold more Jackson. More sales funded better technology and service. Better service kept advisors loyal. The company’s call center performance became part of the pitch, with the SQM Call Center Awards Program recognizing Jackson’s customer service repeatedly—starting in 2004 and 2006, and then year after year from 2006 through 2023.

Meanwhile, product development was running at full speed. Jackson leaned hard into guaranteed living benefits—riders that promised a minimum income stream for life, even if markets crashed. That shifted variable annuities from “investment wrapper” to “retirement solution,” tapping into the single fear that sits underneath almost every retirement conversation: What if I run out of money?

And on paper, the economics looked bulletproof. Fees rose with assets under management. Spread income added margin as the company earned on its general account and credited less to fixed obligations. The guarantee riders added still more fee revenue. And the hedging program was supposed to keep the whole machine stable when markets turned.

By 2007, Jackson was firmly one of the top three retail annuity sellers in the U.S., managing vast pools of customer assets. For Prudential plc, it was starting to look like one of the best deals the company had ever made.

Then came September 2008.

V. The Financial Crisis & Guaranteed Benefits Nightmare (2008–2012)

The crisis hit the variable annuity industry like a meteor. As the S&P 500 plunged 57% from peak to trough, the very feature that made variable annuities so easy to sell in the boom years—guaranteed living benefits—turned into a slow-motion balance-sheet explosion.

Here’s the ugly arithmetic. Imagine a policyholder who put in $100,000 and bought a guaranteed minimum withdrawal benefit. After the crash, their account might be worth $43,000. But the guarantee could still let them withdraw 5% of the original $100,000 each year for life. That’s $5,000 annually, backed by an account that—at this point—might only be throwing off a fraction of that in fee income. Now scale that across huge blocks of policies, all at once, while markets are crashing and volatility is spiking. You don’t just have losses. You have a system-wide solvency question.

And the problem was worst in the “vintage” products—annuities sold before 2008, when competition pushed insurers to offer richer, more generous income terms. Those pre-crisis promises looked like customer-friendly features in 2006. After 2008, they became poison.

Some insurers tried to claw back risk any way they could. The Hartford, for example, pushed policyholders to change their allocations or risk losing benefits—because the original rider terms had become so uneconomic. The goal was simple: force money into more conservative portfolios so the protected income balance didn’t grow as fast, and so the liabilities didn’t balloon further.

Across the industry, the damage was severe. Multiple competitors either restructured aggressively or effectively fled the market. Names like Hartford, ING, and MetLife took enormous hits and pulled back from the most guarantee-heavy designs. Advisors and customers watched in real time as companies rewrote product terms, narrowed investment menus, and admitted—sometimes indirectly—that the old economics no longer worked.

Jackson survived, but that survival wasn’t automatic. It was the product of how its book had been built going into the storm.

Only 1% of Jackson’s in-force variable annuity policies (measured by account value as of December 31, 2020) had been sold prior to the 2008 financial crisis—exactly the era when many competitors were writing variable annuities that were, in hindsight, mispriced and loaded with hard-to-hedge features.

That statistic matters because it tells you Jackson’s risk posture was different. It didn’t win by being the most generous issuer at the peak of the cycle. It won by staying competitive while keeping guarantees within a range the company believed it could actually manage. When the crash arrived, Jackson’s book was, on average, newer and better priced than many of the blocks that broke other insurers.

Jackson also leaned into designs that reduced the most dangerous exposures. It emphasized products that either didn’t offer guaranteed living benefits at all—like an investment-only variable annuity—or offered optional guarantees with risk characteristics it believed were easier to manage, such as GMWB and GMWB for Life. As of December 31, 2020, 23% of Jackson’s total variable annuity account value had no guaranteed living benefits, and 76% included a GMWB or GMWB for Life optional guarantee benefit.

Even with better positioning, the crisis demanded support and rapid change. Prudential plc injected capital into Jackson to help it meet regulatory requirements and protect its credit standing. Hedging programs—imperfect, but essential—helped prevent truly catastrophic outcomes. And product redesign moved from “continuous improvement” to emergency response: newer variable annuities came with more conservative guarantees, higher fees, and tighter allocation restrictions.

The regulators responded too. Reserving standards tightened through updated actuarial guidelines, forcing insurers to hold more capital against guaranteed products. That raised the cost of doing business and, for survivors, created a kind of moat: if you hadn’t lived through the crisis and built the modeling, hedging, and capital-management muscle, it got much harder to compete.

But the most important consequence was competitive. As rivals retreated, advisors still needed solutions for clients who wanted market participation with a safety net. Jackson had demonstrated—under the worst conditions in generations—that it could keep its promises. A conservative hedging posture protected Jackson in 2008 and helped it take meaningful market share in the years that followed.

The crisis rewired the company. Risk management stopped being a back-office function and became a core competency. Jackson came out of 2008 with hard-earned institutional knowledge—how to hedge guarantees, how to structure riders, how to manage capital under stress—that would define its strategy for the next decade.

And unfortunately for insurers, the next decade had its own kind of brutality. The crash ended. But the interest-rate world that followed would test Jackson all over again.

VI. The Low-Rate Wilderness Years (2012–2020)

The decade after the crisis brought a different kind of pain. Markets recovered, but interest rates collapsed toward zero—and for annuity companies, low rates are like gravity. They pull down everything.

When yields are tiny, the math stops working as cleanly. Fixed products still need to credit customers a competitive rate, even when the insurer can’t earn much on its own portfolio. Variable annuity guarantees become pricier to hedge because volatility is higher relative to the return you can safely generate. Across the industry, returns on equity got squeezed. The trauma of 2008 had faded, but the economics stayed brutal.

Jackson’s response was to change what it sold—without abandoning the annuity focus that made it successful in the first place.

It began broadening beyond traditional variable annuities into fixed indexed annuities and, increasingly, registered index-linked annuities, or RILAs. By 2020, fixed indexed annuities were still a smaller slice of the mix—$997 million of sales, about 5% of the company’s retail annuities segment—but the direction mattered: Jackson was building a portfolio that could live in a low-rate world.

The bigger strategic swing was RILAs. Jackson entered the structured variable annuity market with two versions of its first registered index-linked annuity: Jackson Market Link Pro for securities-licensed advisers who earn commissions, and Jackson Market Link Pro Advisory for advisers who charge asset-based fees. This was Jackson meeting the market where it was headed—supporting both the traditional commission model and the fast-growing fee-based advisory world.

RILAs were attractive because they threaded the needle. To a consumer, the pitch was intuitive: you get participation in an equity index, but with some defined protection on the downside. You might give up a chunk of upside in exchange for limiting losses to a set level. To an insurer, the risk profile was often more manageable than the open-ended promises embedded in the richest variable annuity riders. And unlike many variable annuities, RILAs could be designed with few, if any, explicit fees—which helped them stand out in a world increasingly allergic to layered costs.

Distribution got deeper, too. Jackson didn’t just rely on relationships; it tried to embed itself into how advisors actually work. The company invested in technology to make quoting, selling, and servicing smoother, and pushed integrations with the planning and wealth platforms advisors already used. Jackson’s own view was blunt: annuities had been underused partly because they didn’t fit cleanly into modern advice workflows, and that friction was fixable. So it worked with distribution partners and financial technology firms to bring annuities into the same tools advisors used to build plans.

Regulation added another layer of uncertainty. The Department of Labor’s fiduciary rule fight from 2016 through 2018 cast a shadow over commission-based retirement products before the rule was ultimately vacated. Then came newer frameworks—Regulation Best Interest and the Fiduciary Advice Rule—which Jackson believed would, over time, push more professionals to consider annuities as legitimate tools for managing market and longevity risk, not just as sales products.

While Jackson was retooling in the U.S., the bigger strategic decision was forming an ocean away. Back in London, Prudential plc was looking at its own portfolio and seeing an uncomfortable contrast: Asia was throwing off spectacular growth and returns, while Jackson—though profitable—was operating in a low-rate American environment that made it hard to look exciting on paper. CEO Mike Wells told journalists that in Asia in 2019, every $1 invested in new business generated $6 of new business profit, with internal rates of return in the 20s. Jackson simply couldn’t compete with that narrative.

Investor pressure sharpened the question. Third Point LLC pushed Prudential plc to divest Jackson, arguing the parent lacked a clear strategic path for the business and that capital should be directed toward higher-return opportunities.

Then, in March 2020, as COVID-19 shut down global economies and markets reeled, Prudential plc made its call anyway: it would separate Jackson. The board said the full separation and divestment would allow Prudential to focus on its higher-growth Asia and Africa businesses, creating two separately listed companies with distinct investment propositions—and better alignment for management, employees, and shareholders on both sides.

A few months later, Jackson took another step that revealed just how much the annuity world had changed since 2008. In June 2020, it executed a major transaction with Athene, the Apollo-backed insurer that had become a powerhouse in annuity reinsurance. On June 18, 2020, Jackson agreed to fully reinsure $27.6 billion of its in-force fixed and fixed indexed annuity liabilities, receiving $1.2 billion in ceding commission from Athene. The deal strengthened Jackson’s capital position.

Strategically, it did three things at once: it moved lower-return fixed exposure off Jackson’s balance sheet, generated immediate capital, and freed the company to focus more on the products it believed could win—variable annuities and the emerging RILA category. And it carried a broader signal: sophisticated, well-capitalized players were eager to own annuity blocks. The business wasn’t broken; it was being reorganized.

By late 2020, the separation machinery was humming. Jackson was preparing to stand on its own—just as interest rates were about to flip from a decade-long headwind into the tailwind that would reshape everything.

VII. The Separation & IPO: Creating Jackson Financial (2021)

In early 2021, Jackson started acting like a company that was about to live or die on its own decisions.

In February, Prudential plc announced a leadership reset ahead of the separation. Laura Prieskorn was named CEO of Jackson, and Marcia Wadsten became CFO. At the same time, Michael Falcon and Axel Andre stepped down from the CEO and CFO roles they held at Jackson. The message was clear: Prudential wanted a team built for a standalone, well-capitalized public company with one job—create shareholder value.

Prieskorn was the definition of an internal operator. She had spent more than three decades at Jackson, most recently as Executive Vice President and Chief Operating Officer, and she’d been deeply involved in the company’s operating, investment, and product decisions. She wasn’t being brought in to “transform” Jackson. She was being promoted because she already knew how the machine worked—how to keep costs down, how to serve advisors fast, and how to run the platform that made the distribution engine hum.

When she took the role, Prieskorn framed it as a continuation of the same Michigan-built story: “It is a huge privilege to become CEO of an enterprise which I have helped to grow from a modest regional firm to what it is today, an admired leader in the American annuities market.” Her background reinforced the point. She held a business degree from Central Michigan University—not a coastal pedigree, but a reflection of Jackson’s culture: practical, operationally focused, and allergic to unnecessary overhead.

Then came the actual separation mechanics—and they were not a typical IPO roadshow.

Prudential didn’t sell Jackson to new investors. It executed a demerger, distributing Jackson shares directly to Prudential shareholders. Prudential shareholders approved the deal on August 27, 2021. Jackson stock began trading “when-issued” on the NYSE on September 1, 2021. Shareholders of record as of September 2 received one share of Jackson Class A common stock for every 40 Prudential ordinary shares they held. And on September 20, 2021, Jackson began “regular way” trading on the NYSE under the ticker JXN.

Alongside the mechanics, Prudential staffed up governance for the new reality. Former MetLife CEO Steven Kandarian was appointed nonexecutive chair of Jackson’s board—an experienced insurance hand meant to signal the company was ready to stand alone.

Jackson also laid out a capital profile designed to look sturdy from day one. In connection with the separation, it expected a risk-based capital ratio in the range of 425% to 450% and total financial leverage between 25% and 30%, depending on market conditions. The point wasn’t to wow anyone with growth projections. It was to reassure investors that this would be a conservative balance sheet built to withstand market swings.

But even with the new leadership team, the board, and the capital cushion, the market’s first reaction was chilly.

Jackson began trading around $25 a share. Within days, it fell as low as $22.29 on September 15, 2021. The skepticism was easy to understand: to many investors, this looked like a legacy insurer being cut loose—interest-rate sensitive, financially complex, and unlikely to be a high-growth story.

Behind the scenes, Jackson was also paying the unavoidable “independence tax.” Functions that had been shared inside Prudential—treasury, IT, and corporate infrastructure—now had to be fully built or replicated. The upside was clarity. For the first time, Jackson didn’t have to compete for attention or capital inside a global conglomerate. It was now a pure-play annuity company with a single focus.

And while the timing looked questionable in the shadow of COVID-era uncertainty, it turned out to be almost perfect. Jackson became independent just months before the Federal Reserve kicked off the most aggressive rate-hiking cycle in decades.

VIII. The Interest Rate Reversal & Renaissance (2021–Present)

The game changer arrived in early 2022. After more than a decade of near-zero rates, the Federal Reserve started hiking aggressively to fight inflation, eventually pushing short-term rates into the mid–5% range by late 2023. For Jackson, that wasn’t a macro headline—it was a full reset of the math behind its products.

And consumers felt it too. “Since the pandemic, we have seen a significant rise in consumer interest in investment protection and guaranteed retirement income solutions,” said Bryan Hodgens, senior vice president and head of LIMRA research. “Fixed-rate deferred annuities drove the record demand for annuities in 2023. As interest rates began to fall in 2024, we saw a shift to products—such as registered indexed-linked and fixed indexed annuities—with greater investment growth potential. We expect this shift to continue in 2025.”

The category took off. Total annuity sales hit $432.4 billion in 2024, up 12% year over year, according to preliminary results from LIMRA’s U.S. Individual Annuity Sales Survey (covering 83% of the market). It was the third straight year of record-high annuity sales—an “annuity boom” that looked a lot like a long-suppressed market finally snapping back.

Jackson didn’t just ride the wave; it stood out in it. Retail annuity sales were $4.7 billion in the fourth quarter of 2024, up 42% from the prior-year quarter. The business benefited from higher markets too: total annuity assets under management rose 7% year over year, from $235 billion at the end of 2023 to $252 billion at the end of 2024, helped largely by stronger equity markets.

“Our full year retail annuity sales were up 39% with growth across all product lines, demonstrating our distribution strength and our continued focus and commitment to offering differentiated and innovative solutions while generating value for our shareholders.”

Nowhere was the shift more obvious than in RILAs. This part of the market had gone from niche to mainstream: RILA sales grew from $3.7 billion in 2015 to $65.4 billion in 2024, as the number of carriers offering them jumped from 4 to 21. Jackson’s timing proved fortunate. In the fourth quarter of 2024, its registered index-linked annuity sales were $1.5 billion, up 47% from the year-ago quarter.

Those sales translated into real scale. RILA balances rose 74% year over year, helped by new advisor relationships and partnerships, including J.P. Morgan Chase. That relationship was a meaningful distribution expansion, putting Jackson products in front of customers across one of the largest retail banking networks in the country.

Then came the second-order effect of higher rates: capital. Jackson’s capital generation accelerated. Net income attributable to Jackson Financial Inc. common shareholders was $902 million in 2024 (or $11.74 per diluted share), compared to $899 million in 2023 (or $10.76 per diluted share). Adjusted operating earnings were $1.4 billion in 2024 (or $18.79 per diluted share), up from $1.1 billion in 2023 (or $12.84 per diluted share), driven largely by growth in variable annuity AUM, higher spread income, and fewer shares outstanding from repurchases.

That last point became the story. Jackson turned into a capital return machine. “We have once again achieved our financial targets by returning $631 million to common shareholders in 2024, ending the year with an estimated RBC ratio well above our target of 425%, and holding robust levels of excess cash at the holding company.”

The share count tells you just how aggressive this was. Shares outstanding fell from 0.089 billion in 2022 to 0.084 billion in 2023, and to 0.077 billion in 2024. In roughly three years, buybacks reduced the share count by about 20%—a powerful lever for per-share earnings.

The market noticed. JXN’s all-time low came on September 15, 2021, at $22.29—right in the immediate post-spin skepticism. Its all-time high arrived on November 11, 2024, at $115.22. In a little over three years, the stock climbed more than 400% from trough to peak.

And the momentum carried into 2025. Adjusted operating EPS was $6.16 in Q3 2025, up from $4.60 in Q3 2024. Adjusted book value per share was $158.44. Free cash flow was $719 million for the nine months ended September 30, 2025, and nearly $1 billion over the trailing 12 months.

Management expected full-year 2025 capital return to exceed its $700–$800 million target, with momentum carrying into 2026. The board approved a $1 billion increase to share repurchase authorization and a Q4 dividend of $0.80 per share.

Underneath all of it was the demographic reality finally showing up in the data. 2024 was also the year more Americans turned 65 than at any other point in history—roughly 12,000 people a day reaching the age most people associate with retirement. LIMRA research shows annuity buyers tend to be around 65, and with the U.S. population ages 65 and over expected to grow by more than 7.5 million from 2023 to 2027, the demand backdrop looked less like a one-time spike and more like the front edge of a long trend.

IX. The Modern Business Model & Competitive Position

By the time Jackson became independent, it had already evolved into something pretty unusual in insurance: a focused annuity company with a business model that’s complex under the hood, but straightforward in how it makes money. It’s built on three main pillars.

Fee-based income starts with variable annuities. When a customer buys a variable annuity, their money typically sits in “separate accounts,” invested in subaccounts that look and behave a lot like mutual funds. Jackson then collects a base contract fee, plus additional fees if the customer adds optional living or death benefit riders. This is the cleaner, more “asset manager–like” part of the model: the bigger the asset base, the more fee revenue flows through. In Jackson’s Retail Annuities segment, this spans variable annuities, fixed and fixed indexed annuities, payout annuities, RILAs, and lifetime income solutions.

Spread income comes from the more classic insurer playbook. For fixed products, Jackson invests the premiums in its general account, earns a return, and credits a lower rate back to policyholders. The gap between what it earns and what it credits is the spread. This is why interest rates matter so much: when market yields rise, spread income can expand quickly. In the most recent period, adjusted operating earnings per share benefited from higher spread income tied to growth in average RILA assets under management.

Asset management is the third pillar, and it runs through PPM America, Jackson’s wholly owned investment management subsidiary. PPM manages Jackson’s general account and also takes on third-party mandates. Craig Smith leads PPM America and is responsible for investment performance and service for both Jackson and PPM’s institutional clients.

The product portfolio reflects the lessons of the last two decades. Variable annuities are still the franchise. Jackson National was the only annuity carrier to exceed $7 billion in variable annuity sales through the third quarter of 2024, and its lineup includes long-running products like Perspective II, which advertises a core contract fee of 1.3%.

But the growth engine has shifted toward RILAs, with fixed indexed annuities adding diversification. Put together, the mix lets Jackson compete across the spectrum—from investment-only variable annuities, to defined-downside growth products like RILAs, to principal-protection-oriented fixed products—without concentrating all its risk in one design.

Distribution remains the advantage that keeps showing up, decade after decade. Jackson leans on deep relationships with independent financial advisors, backed by steady product development and a risk-management culture that was hardened by 2008. It also emphasizes capital-efficient product design and disciplined pricing—two phrases that sound boring, but in annuities they’re the difference between gaining share profitably and buying sales that later explode on you.

Then there’s cost. Jackson positions itself as a low-cost operator. It reports a combined statutory operating expense-to-asset ratio of 26 basis points, which it says is among the lowest in the life insurance industry. It also notes that variable annuity peers like Brighthouse, Equitable, Lincoln, and Prudential average 57 basis points. If you can run the platform at roughly half the expense load of competitors, you get two choices—and Jackson benefits from both: you can price more aggressively when you need to, and you can keep more margin when you don’t.

Competitive Positioning:

Against Athene/Apollo, Jackson is playing a different game. Athene is built around spread-based annuities and an investment strategy deeply tied to Apollo’s private credit machine. Jackson, by contrast, has a broader product mix and leans harder on traditional advisor distribution. The bigger backdrop here is structural: the annuity market has seen increased consolidation as private equity and asset managers have bought in. Deals like KKR acquiring Global Atlantic, Blackstone’s investment in FG Life, and Apollo’s acquisition of Athene have reshaped the competitive field and changed what “well-capitalized” looks like in insurance.

Against Equitable, it’s closer to a head-to-head category fight—especially in structured products. In third-quarter structured annuity rankings, Equitable Financial ranked No. 1 with a 19.4% market share, with Allianz Life second and Jackson National Life, Brighthouse Financial, and Prudential rounding out the top five. Equitable got into RILAs earlier and has led the category, but Jackson has been taking share quickly.

Against Nationwide and Lincoln, Jackson competes on execution: service, technology integration, and product flexibility for independent advisors who don’t want to be locked into one carrier’s ecosystem.

And zooming out to the biggest legacy category—variable annuities—Jackson is still a heavyweight. In 2024 rankings, Equitable Financial led with $22.4 billion in variable annuity sales, with Jackson National Life second at $15.3 billion. Even as RILAs take a larger piece of the industry’s growth, Jackson’s variable annuity franchise remains a central part of its competitive identity.

X. Strategy & Future Moves

Management has been clear about the playbook: controlled growth, steady capital returns, and product innovation.

Controlled growth, in Jackson’s language, means it would rather walk away from “bad” sales than win share at any price. The company has stayed disciplined on pricing even when competitors got aggressive, because it has lived the movie where underpriced guarantees turn into balance-sheet emergencies. The lesson from 2008 wasn’t “don’t grow.” It was “don’t grow faster than your risk management.”

Capital returns have become the centerpiece of the post-spin story. With a profitable book and capital generation running strong, management said it had confidence in its $700–$800 million capital return target for 2025. The deeper point isn’t just the number—it’s the pattern. Jackson has repeatedly met or exceeded its return targets, and that consistency is a big reason investors have started to treat the stock less like a neglected insurer and more like a cash-generating franchise.

Product innovation is where Jackson is trying to win the next decade, and it’s increasingly about meeting advisors where the industry is moving: toward fee-based advice. The company has focused on RILAs and advisory-friendly products that can sit alongside traditional commission-based offerings. As Jackson has put it, there’s “greater interest in balancing commission-based products and fee-based products,” and only about half of RIAs report selling annuities today. The bet is that expanding fee-based annuity options—and making them easier to use with modern advisor tech—pulls annuities further into the RIA channel. Industry research Jackson cites underscores the shift: fee-based variable annuities and fixed indexed annuities have grown quickly since 2020, reaching $7.7 billion in 2024.

The M&A question is still hanging out there. Jackson could be a buyer, picking up annuity blocks from companies that want out. Or it could be a target itself. Private equity’s appetite for insurance hasn’t gone away, and Jackson’s combination of scale, distribution relationships, and operating infrastructure would be meaningful to almost any would-be acquirer.

Distribution is another frontier. Direct-to-consumer annuities are still underdeveloped, mostly because the products are complicated and the stakes are high. But as products get simplified and digital onboarding improves, that channel becomes more plausible. Robo-advisor partnerships are another angle—less about selling complex guarantees to 30-year-olds, and more about building a pathway to younger savers before they ever sit down with a human advisor.

Key risks:

Another market crash would test the machine again. Jackson has proven it can operate through stress events like 2008–2009 and 2020, but the core truth hasn’t changed: guarantees are still obligations, and equity sell-offs still shrink separate-account fee income.

Regulatory changes could reshape what’s sellable and how it’s sold. Stronger fiduciary standards could limit certain features or tighten distribution practices. State regulators remain the primary oversight, but federal involvement is always a looming possibility in retirement products.

An interest-rate reversal would take away one of the biggest tailwinds of the past few years. If rates fell back toward the near-zero world of the 2010s, spread income would compress and the business would feel familiar pressure again.

And there’s a newer competitive threat forming at the edges: asset managers. If firms like BlackRock and Vanguard keep moving toward products with guarantees, they could eventually push into territory that has historically belonged to insurers—and potentially disintermediate parts of the traditional annuity value chain.

XI. Porter's 5 Forces Analysis

Competitive Rivalry (Medium-High): This is a consolidated market, but it doesn’t feel calm. The fight is for distribution—who gets shelf space with advisors, broker-dealers, and platforms. In 2024, multiple carriers were each doing tens of billions in annuity sales, which tells you two things at once: the prize is huge, and there are plenty of heavyweight incumbents still swinging. There’s real commoditization risk in the simpler corners of the business, especially fixed products. But the industry has also learned the hard way that “growth at any price” can be fatal. Most major players try to keep pricing rational, because unprofitable annuities don’t just hurt margins—they can come back years later as capital problems.

Threat of New Entrants (Low-Medium): The barriers are real: you need a lot of capital, a web of state regulatory approvals, and deep actuarial and hedging capabilities. Then you still have to do the slow, unglamorous work of earning distribution relationships, which can take years. The reason this isn’t simply “low” is that private equity has shown a credible playbook for entering at scale, with the Athene model as the reference point. Asset managers are also sniffing around the edges, looking for ways to pair investment management with some form of guarantee.

Supplier Power (Low-Medium): Reinsurers can exert leverage at the margins, but they also need volume, and Jackson is a meaningful counterparty. On the investment side, asset management is competitive, with plenty of firms able to manage large fixed-income portfolios. Technology vendors are becoming more important as annuities get pushed into modern planning and wealth platforms—but for a company of Jackson’s scale, those relationships are rarely truly irreplaceable.

Buyer Power (Medium): The end customer base is fragmented, but the real buyers in practice are concentrated: advisors, broker-dealers, and large platforms deciding what gets recommended and sold. Wirehouses and big broker-dealers can shift flows quickly if pricing, service, or product design slips. At the same time, the products are complex enough that most consumers don’t shop annuities like they shop index funds, which tempers pure price pressure. Still, sophistication is rising, and with it, scrutiny on fees. The Alliance for Lifetime Income has reported that 28% of retail investors ages 61 to 65 are likely to consider the benefits of protected, guaranteed income in their portfolio—big enough interest to matter, but not so universal that any carrier can take demand for granted.

Threat of Substitutes (Medium-High): Annuities compete against the default options: target-date funds, systematic withdrawal plans, and the “I’ll just manage it myself” approach to retirement. When rates are high, the substitute gets even simpler—bonds and CDs start looking like clean, no-explanation-needed alternatives. Underneath it all is the existential substitution question for the category: do people actually value paying an insurer to take longevity and market-risk off the table, or will more Americans choose to self-insure and accept the chance they’ll run out of money later?

XII. Hamilton's 7 Powers Analysis

Scale Economies: STRONG. Jackson runs a lean platform. Its combined statutory operating expense-to-asset ratio is 26 basis points—far below the variable annuity peer average of 57 basis points. In a business where you’re carrying big fixed costs in technology, compliance, hedging infrastructure, and the day-to-day work of maintaining distribution relationships, that kind of scale isn’t just nice to have. It’s a structural advantage. Being a top-three player matters because it spreads those costs over a massive base—and lets you reinvest in service and systems without blowing up the expense line.

Network Effects: WEAK. This isn’t a network business in the classic sense. Jackson doesn’t get stronger just because more people buy the same annuity. There are some light, indirect effects—more advisor relationships can mean more feedback loops for product design and operational improvements—but nothing like the flywheel you’d see in software or marketplaces.

Counter-Positioning: MEDIUM. Jackson’s independent distribution model—selling through advisors and broker-dealers instead of a captive agent army—gives it a different posture than carriers built around proprietary channels. Its pure-play focus on annuities also creates clarity compared to conglomerates balancing competing priorities. And its push into RILAs has helped it keep pace with where advisor demand has been moving. The limitation is obvious, though: competitors can copy what works, and many do.

Switching Costs: STRONG (for existing book). Once a customer owns an annuity, it’s often “sticky” for practical reasons: tax consequences, surrender charges, and the sheer hassle of comparing complex alternatives. That’s a real source of durability for the in-force block. The Alliance for Lifetime Income has reported that 28% of retail investors ages 61 to 65 are likely to consider protected, guaranteed income in their portfolio—evidence that the underlying need isn’t going away. Advisor relationships can be sticky too once established. But for new sales, switching costs are low. No one is locked into choosing Jackson.

Branding: MEDIUM. Jackson’s brand is powerful where it matters most: with advisors. Products like its Perspective II Flexible Premium Variable & Fixed Deferred Annuity have led category rankings, reinforcing credibility at the point of sale. But to most consumers, Jackson is largely invisible, because the advisor relationship is the front door. Trust matters in annuities, yet commoditization pressure is always present—especially when competitors can match features and price.

Cornered Resource: MEDIUM. The scarce asset here is expertise. Actuarial talent, risk management judgment, and the modeling muscle built across decades of real market stress aren’t easy to replicate quickly. Jackson also benefits from historical data and an operating playbook refined over time. Distribution relationships are valuable, but they’re not exclusive. Licenses and compliance infrastructure raise the bar for would-be entrants, but they don’t lock the market.

Process Power: STRONG. Jackson’s edge is operational, and it’s been forged the hard way. Its hedging and derivatives capability has been shaped by multiple volatile market regimes. Its underwriting and risk selection processes have been refined across a huge policy base. And its focus on technology integration with advisor platforms creates day-to-day execution advantages that are difficult to reverse-engineer from the outside.

Overall Assessment: Jackson’s strongest powers are Scale Economies, Switching Costs in the existing book, and Process Power. That combination makes the business durable—but not invincible. Competitive pressure and substitutes are real, and the last few years have also proven a humbling truth: in annuities, macro conditions—especially interest rates—can swamp almost everything else.

XIII. Bull vs. Bear Case

Bull Case:

-

Structural Retirement Crisis: The need is real and getting louder. In 2024, only about half of pre-retirees said they had enough guaranteed lifetime income to cover basic living expenses, down from 58% in 2017. With pensions disappearing and lifespans stretching, more households are looking for products that can turn savings into predictable income.

-

Interest Rate Normalization: Even with some rate cuts, the world still looks nothing like 2012–2021. If rates remain meaningfully above the near-zero era, Jackson’s spread income stays structurally healthier than it was during the “low-rate wilderness.”

-

RILA Market Leadership: RILAs have been one of the clearest growth stories in annuities, coming off an eleven-year run of record sales. LIMRA expects RILA sales to be roughly in line with, or slightly above, the 2024 record—projecting a range of $62 billion to $66 billion—supporting the case that the category isn’t a one-season fad.

-

Capital Return Engine: Jackson doesn’t need explosive sales growth to compound per-share value. Buybacks shrink the share count, which can lift EPS even in a flatter revenue environment. Over the last 12 months, capital returned to shareholders reached $805 million, alongside a $1 billion increase to share repurchase authorization.

-

Valuation Discount: Even after the post-spin rerating, the stock still trades at a meaningful discount to book value. If investors gain more confidence in the durability of earnings and capital generation, there’s room for that gap to narrow.

-

Management Execution: Laura Prieskorn, Jackson’s president and CEO, is a long-tenured operator with more than 30 years at the company. The bull case here isn’t a heroic turnaround—it’s that the same institutionally learned discipline in pricing, risk management, and operations continues to show up in results.

-

Demographic Tailwind: With more than 10,000 Americans turning 65 every day, the demand backdrop doesn’t need to be “created.” It’s arriving on schedule.

Bear Case:

-

Cyclical Masquerading as Secular: The recent annuity surge may prove more cyclical than structural—driven by the rate environment and market uncertainty, not a durable shift in consumer preference.

-

Rate Cut Risk: A meaningful decline in interest rates would pressure spread income and profitability. Rates might not return to zero, but they don’t have to for the economics to tighten.

-

Regulatory Risk: Stronger fiduciary standards, product restrictions, or changes in capital rules could limit what can be sold, how it’s sold, or how much capital must be held against it.

-

Market Crash Scenario: Another major equity drawdown would hit both sides of the model: separate-account fees fall with markets, and hedging costs can rise just as guarantees become more valuable to policyholders.

-

Distribution Power Shifts: If large platforms or new technology-led advice models gain more control of product selection, Jackson’s relationship-driven distribution advantage could erode.

-

Consumer Preference Question: There’s a persistent skepticism hanging over the category: do consumers truly want annuities, or are they often sold because advisors and distributors are incentivized to sell them—an issue that could worsen as fee transparency rises?

-

Complex Financials: Insurance accounting is complicated, and complexity can hide problems until stress hits. Investors may be underestimating risks embedded in hedging, reserves, or guarantee exposure simply because the model is hard to “see” from the outside.

XIV. Epilogue & Recent Developments

By late 2025, Jackson’s post-spin story still had momentum. In Q3 2025, retail annuity sales topped $5.4 billion, powered by record RILA sales of $2.1 billion. Institutional sales grew 34% to $1 billion. That volume flowed through to earnings: adjusted operating earnings were $433 million in the quarter, up from $350 million a year earlier, helped by higher spread and fee income, lower expenses, and the compounding effect of a shrinking share count.

You could see that compounding show up in per-share value. Total common shareholders’ equity was $9.8 billion, or $135.43 per diluted share, as of March 31, 2025, up from $9.2 billion, or $124.21 per diluted share, at December 31, 2024. Adjusted book value attributed to common shareholders was $11.0 billion, or $152.84 per diluted share, as of March 31, 2025. The increase was driven primarily by adjusted operating earnings and a lower diluted share count from continued repurchases.

Jackson also began preparing for a key leadership handoff in its investment arm. Craig Smith, President and CEO of PPM, said he intends to retire on December 31, 2025, and will transition day-to-day leadership responsibilities to Chris Raub, President of Jackson National Life.

Key Metrics to Watch:

For investors tracking Jackson from here, three measures tend to tell the cleanest story:

-

Retail annuity sales growth: This is the real-time read on competitiveness and distribution strength. Sustained year-over-year growth signals share gains and staying power in the current demand cycle.

-

Risk-based capital ratio: Statutory total adjusted capital at Jackson National Life was $5.6 billion, with an estimated RBC ratio of 579%. That matters because capital is both a safety buffer and the fuel for dividends and buybacks. Management’s 425% target leaves meaningful room above regulatory minimums.

-

Adjusted operating earnings per share: With buybacks steadily reducing the share count, per-share performance matters more than the headline earnings number. Adjusted operating EPS was $6.16 in Q3 2025, up from $4.60 in Q3 2024—exactly the kind of trajectory that makes the capital-return strategy feel real.

And that brings us to the unresolved question hanging over the entire annuity boom: is this the start of a longer supercycle, or a powerful—but temporary—bounce driven by rates and demographics? LIMRA put it plainly: “For the third consecutive year, quarterly and year-to-date annuity sales have set records. If you look underneath the top-level results, however, we see a slight softening in the market, which could result in a contraction in the second half of the year.”

XV. Closing Reflections

The Jackson Financial story is a reminder that the “boring” businesses are often the ones where the real lessons live.

On timing, a 60-year-old insurer became independent at exactly the right macro moment. Prudential’s decision to demerge Jackson—shaped by activist pressure and the parent’s pivot toward Asia—looked, at the time, like an awkward move to make in the middle of the COVID-era chaos of 2020. Then the rate world flipped. The hiking cycle that followed didn’t just help around the edges; it rewrote the economics of annuities and made Jackson’s standalone story suddenly make sense to the market. But it wasn’t just luck. Jackson had spent the post-2008 era building the hedging, capital, and operating discipline required to actually benefit when the wind changed.

On focus, Jackson’s decision to be an annuities company—full stop—created clarity and edge. It isn’t trying to win every insurance category. It’s trying to be the best partner to advisors who need retirement income solutions, and to run that platform at a cost and service level that’s hard for diversified rivals to match. That kind of focus shows up in product cadence, in distribution loyalty, and in operational efficiency.

On risk management, 2008 was the tuition bill that bought Jackson a real capability. Surviving the guaranteed-benefits nightmare didn’t just keep the company alive; it built institutional muscle. The disciplines that matter most in this category—hedging under stress, designing products you can actually support, and managing capital through volatility—were forged when the industry was closest to breaking.

On distribution, annuities are rarely won by a single feature. They’re won by trust, shelf space, and execution. Jackson has spent decades building relationships with independent advisors and the platforms they live on. Technology may change how those relationships are formed and maintained, and it may even disintermediate parts of the process over time. But today, in a product category this complex, distribution relationships are still the difference between being “available” and being sold.

And on macro, the story is brutally simple: interest rates can overpower almost everything else. From 2012 to 2020, Jackson operated in a world where rates compressed spreads and made guarantees expensive, even with strong execution. From 2022 through 2024, higher yields turned the same business into a stronger earnings and capital-generation engine without any dramatic change in the company’s identity. You can’t analyze Jackson—or any annuity carrier—without holding both truths at once: execution matters, and macro can still dominate.

The bigger narrative underneath all of this is retirement insecurity—how modern Americans are being asked to do something historically difficult: fund decades of life after work, often without a pension, and with markets that don’t move in straight lines. Annuities exist because that problem exists. They take the fear of outliving your money and, for a price, transfer that risk to an insurer built to pool it.

Jackson’s future, in a way, is a bet on what America decides to do with that fear. If guaranteed income becomes a standard part of retirement planning—embedded in 401(k)s, normalized by advisors, and actively demanded by consumers—Jackson is positioned as a scaled specialist with real know-how. If the culture continues to prefer self-insurance, target-date funds, and DIY drawdown strategies, the market is smaller than the “boom” headlines suggest.

For now, the signal from consumers is encouraging. LIMRA research shows interest in converting a portion of assets into an annuity remains historically high, with more than half of pre-retirees and retirees saying they would be interested.

So the ingredients are on the table: real demand, powerful demographics, and products that are steadily getting easier to use and explain. The open question is capture. Whether Jackson turns this moment into a durable next chapter depends on executing the same playbook it’s been refining for decades—from Tony Pasant’s lean Michigan startup to Laura Prieskorn’s public-company machine operating in the middle of the largest retirement wave in American history.

XVI. Further Reading & Resources

Essential Primary Sources:

-

Jackson Financial SEC Filings — The 10-Ks, 10-Qs, and the IPO prospectus are the closest thing to a “source code” for the business: how the products work, where the earnings come from, and what can go wrong.

-

Prudential plc Annual Reports 2010–2021 — The best window into why the parent ultimately chose to separate Jackson, and how it fit (and later didn’t fit) inside Prudential’s global strategy.

-

LIMRA Secure Retirement Institute Reports — The definitive industry tracker for annuity sales, product mix shifts, and the demographic forces driving demand.

For Industry Context:

-

The Annuity Advisor by Moshe Milevsky — A clear, rigorous look at annuity economics and the math behind longevity risk.

-

Falling Short: The Coming Retirement Crisis by Ellis, Munnell, and Eschtruth — The broader demographic and policy backdrop: why retirement insecurity keeps growing, and why guaranteed income keeps resurfacing.

-

Society of Actuaries research on variable annuities — For the deep technical view of guarantees, reserving, and the risk engineering that shaped the category after 2008.

For Financial Crisis Understanding:

-

Federal Reserve papers on interest rates and insurance — Useful framing for the central macro point in this story: rate regimes don’t just affect insurers—they can redefine them.

-

GAO report on the insurance industry and the financial crisis (2013) — A government-level postmortem on how guarantee-heavy products pressured solvency across the industry.

For Ongoing Analysis:

-

Insurance trade publications — InsuranceNewsNet, ThinkAdvisor, and Retirement Income Journal are good for keeping up with product launches, distribution shifts, and competitive moves.

-

Academic papers on hedging strategies in variable annuities — The unglamorous but decisive topic: whether an insurer can actually hedge what it promises, especially when markets break.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube