The St. Joe Company: Florida's Great Land Bank

I. Introduction & The "Florida Thesis"

Picture this: a single entity owns a contiguous stretch of Northwest Florida land twice the size of Manhattan. The cost basis on the books dates back to the 1930s — pennies per acre, acquired during the Great Depression when no one wanted Florida swampland and cut-over pine forest. Today, that same corridor sits in one of the fastest-growing regions in the United States, flanked by sugar-white Gulf beaches, a brand-new international airport, and a wave of migration that shows no signs of cresting.

That entity is The St. Joe Company, ticker JOE on the New York Stock Exchange, and its story is one of the most unusual transformations in American corporate history. For seven decades, this was a paper mill. A timber operation. A sleepy, vertically integrated business that grew pine trees, harvested them, turned them into containerboard, and repeated the cycle. The land was an afterthought — a production input, not a strategic asset.

Then something shifted. The world discovered the Florida Panhandle. And JOE's management, after a bruising proxy war and a near-death experience during the Great Recession, realized they were sitting on something far more valuable than pulpwood. They were sitting on a generational real estate platform.

The arc of JOE is really a story about patience and transformation. It moved from "selling dirt" — the cyclical, commodity-like business of raw land sales — to "building yield," a model centered on recurring revenue from hospitality, leasing, and membership clubs. That shift did not happen overnight. It required a billionaire activist investor who was willing to bet his entire fund on the thesis, a CEO who grew up in the Panhandle and understood its potential at a granular level, and a willingness to endure years of skepticism from Wall Street.

The roadmap of this episode traces the full journey: from the DuPont family trust that assembled the land bank in the first place, through the Berkowitz revolution that remade the company from the board level down, and into the modern era where JOE has quietly become a hospitality and real estate powerhouse generating over half a billion dollars in annual revenue. Along the way, there are legendary short-sellers, Category 5 hurricanes, and a Jimmy Buffett-branded retirement community. It is, in every sense, a Florida story.

But it is also a masterclass in capital allocation. How do you take a hundred-year-old land bank and turn it into a cash-flowing business without selling the farm? That question — and the answer JOE's leadership arrived at — carries lessons for anyone thinking about long-duration assets, patient capital, and the power of waiting for the world to come to you.

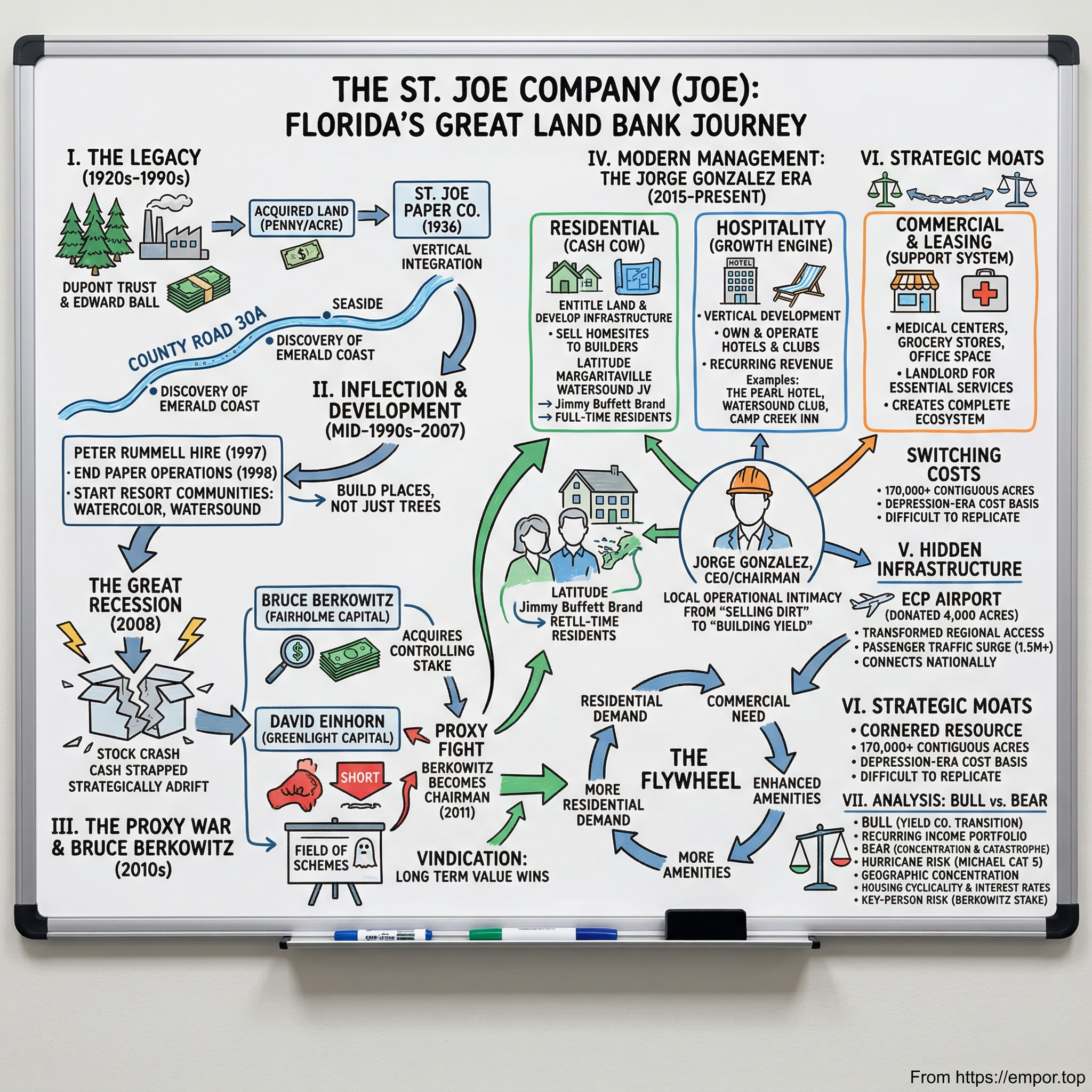

II. The Legacy: Paper, Pines, and the DuPont Trust

In the mid-1920s, a bitter family feud among the du Ponts of Delaware sent one of America's wealthiest men south. Alfred Irene du Pont, tired of warring with his cousin Pierre over control of the family chemical empire, relocated to Jacksonville, Florida in 1926. He brought with him a fortune, a grudge, and a keen eye for distressed assets.

Florida in the late 1920s was the aftermath of a speculative mania. The great Florida land boom of 1925 had collapsed spectacularly, leaving behind busted developments, abandoned subdivisions, and vast tracts of land that nobody wanted. Alfred du Pont saw opportunity. He dispatched his brother-in-law, Edward Ball — a sharp-elbowed dealmaker who would become one of the most powerful men in Florida history — to start buying.

Ball moved methodically. By the early 1930s, the du Pont interests had accumulated nearly 100,000 acres of cut-over timberland in Northwest Florida at fire-sale prices. But the transformational deal came in 1933, during the depths of the Great Depression. In a single transaction, Ball secured roughly 240,000 acres in the Panhandle, along with two railroads, telephone companies, a port terminal, a sawmill, and virtually the entire Gulf coast town of Port St. Joe. The price per acre was negligible — these were lands that commercial loggers had already stripped of their old-growth timber, leaving behind scraggly second-growth pine that nobody valued.

Alfred du Pont had a vision for all this land: a paper mill. The slowly regrowing pine forests could be harvested for pulpwood, and a vertically integrated operation could turn that wood into containerboard and kraft linerboard. It was a classic Depression-era industrial play — buy the raw materials, own the means of production, control the supply chain. He never saw it realized. Alfred du Pont died in 1935, leaving behind a testamentary trust with a single charitable beneficiary: the Nemours Foundation, which would go on to establish one of the nation's premier pediatric healthcare systems.

Edward Ball carried the dream forward. The St. Joe Paper Company was incorporated in 1936, and the paper mill in Port St. Joe began operations in 1938. For the next four decades, Ball ran the company with an iron fist. He was a legendary figure in Florida politics and business — crusty, autocratic, and deeply skeptical of anyone who suggested the land might be worth more as real estate than as a timber plantation.

Under Ball's stewardship, St. Joe became the largest private landowner in Florida. At its peak, the company controlled nearly one million acres. The paper mill churned out containerboard. The pine forests grew and were harvested in rotation. And the land — those hundreds of thousands of acres stretching from the Gulf Coast inland through the Panhandle — simply sat there. No homes. No hotels. No development of any kind. Ball died in 1981, and the Nemours Foundation trust continued to hold a controlling stake, perpetuating the same conservative, timber-focused strategy.

For two decades after Ball's death, St. Joe Paper was the corporate equivalent of a sleeping giant. The Panhandle was still remote, still undeveloped, still considered a backwater compared to the glamour of Miami or the theme-park economy of Orlando. But something was quietly changing. The stretch of coastline along County Road 30A — a two-lane road winding through dune lakes and coastal forests between Destin and Panama City Beach — was being discovered. Developers began building boutique communities like Seaside, the pastel-colored New Urbanist village that would later serve as the filming location for The Truman Show. Vacationers from Atlanta, Birmingham, and Nashville started calling it the "Emerald Coast" for its startlingly clear, green-blue water.

By the mid-1990s, the board recognized the inflection. The Panhandle was no longer a backwater — it was becoming a world-class coastal destination. And St. Joe was sitting on the largest contiguous land position in the region. In 1997, they made a hire that would change the company's trajectory: Peter Rummell, the former president of Disney Development Company and chairman of Walt Disney Imagineering.

Rummell was not a timber man. He was the architect behind Celebration, Florida — Disney's ambitious 5,000-acre planned community. He had overseen the construction of over 20,000 hotel rooms and hundreds of thousands of square feet of themed retail. His mandate at St. Joe was clear: stop growing trees and start building places. Under Rummell, the paper mill was shut down in 1998, ending six decades of operations and definitively killing the paper company identity. He launched roughly twenty major resort and residential communities along the 30A corridor, including WaterColor and WaterSound — names that would become synonymous with upscale Panhandle living.

But Rummell's tenure also planted the seeds of the company's near-destruction. The development strategy required massive upfront capital, and the revenue model depended on selling homesites in a rising market. When that market turned, the consequences would be severe.

III. The Great Inflection: The Proxy War & Bruce Berkowitz

The 2008 financial crisis hit Florida real estate like a wrecking ball, and no company felt the impact more acutely than St. Joe. The stock, which had traded above $80 during the mid-2000s housing boom, cratered to under $15 by 2009. Homesite sales — the lifeblood of Rummell's development strategy — dried up almost overnight. The planned communities along 30A, which had been selling lots to eager buyers from across the Southeast, suddenly looked like ghost towns. Peter Rummell departed in May 2008, just as the crisis was accelerating, leaving behind a company that was cash-strapped, strategically adrift, and sitting on an enormous land bank that the market was now valuing at close to zero.

Enter Bruce Berkowitz.

Berkowitz is one of the more colorful figures in the value investing world. A Miami-based fund manager who founded Fairholme Capital Management in 1999, he had built a reputation for concentrated bets on deeply out-of-favor assets. His flagship Fairholme Fund was named Morningstar's Domestic Stock Fund Manager of the Decade for the 2000s — a remarkable achievement built on contrarian wagers in financials, energy, and real estate. Berkowitz's investment philosophy was simple and extreme: find assets trading below intrinsic value, buy as much as possible, and wait. He was not afraid to own half of something.

When JOE's stock collapsed, Berkowitz saw what the market was missing. The land bank — those 170,000 contiguous acres in the Panhandle — had a cost basis on the balance sheet of essentially nothing, reflecting Depression-era purchase prices. The market was pricing JOE as if the land were worthless, but Berkowitz believed the opposite. He saw a generational asset in one of the most desirable coastal regions in the country, temporarily obscured by a cyclical downturn. Fairholme began accumulating shares aggressively, eventually building a position that would grow to roughly 40% of the company.

But Berkowitz was not a passive investor. He wanted control.

The drama escalated in October 2010 when David Einhorn, the cerebral hedge fund manager who ran Greenlight Capital, took the stage at the Value Investing Congress in New York and delivered a now-legendary 139-slide presentation titled "Field of Schemes: If You Build It, They Won't Come." Einhorn's thesis was devastating. He argued that JOE's land portfolio was massively overvalued on the balance sheet, that the company needed significant impairments it was refusing to take, and that intrinsic value was somewhere between $7 and $10 per share — against a stock trading around $24.50.

Einhorn showed photographs of empty developments, vacant lots, and barren commercial spaces. He called the WaterSound communities "ghost towns." He methodically dissected the company's financial statements, arguing that virtually all of JOE's profits over the prior decade had come from one-time land sales that masked the unprofitability of everything else. The presentation was classic Einhorn: rigorous, detailed, and delivered with quiet confidence. The stock plunged roughly 20% on the day.

What followed was one of the great long-versus-short battles in modern investing history. On one side, Einhorn and the shorts, arguing that JOE was fundamentally broken and the land was worth a fraction of what the company claimed. On the other, Berkowitz and Fairholme, buying more shares into the selloff, convinced that the market was gifting them an irreplaceable asset at a generational discount.

Berkowitz did not simply sit and wait. He went to war. In late 2010, he joined JOE's board of directors — then resigned just six weeks later in early 2011, citing irreconcilable differences with management over compensation and governance. The resignation was a tactical move. Within weeks, he orchestrated the removal of CEO Britt Greene and three other board members. On March 4, 2011, Berkowitz was named Chairman of the Board. Hugh Durden served as acting CEO for a brief transition period, and Park Brady was quietly installed as CEO by October 2011.

The Berkowitz takeover was swift and decisive. He moved the company's operational center of gravity to the Panhandle itself — a symbolic and practical statement that JOE would no longer be run from a distant corporate office but from the land it owned. He brought in a lean, operationally focused management team and began the slow, methodical process of repositioning the company from a land-sales machine into something more durable.

The SEC launched an informal inquiry into JOE's accounting practices in the wake of the Einhorn presentation, but no enforcement action ever materialized. Einhorn eventually covered his short. Berkowitz held on. And over the next decade, the stock would rise from the teens to over $70 — a vindication so complete that the "Field of Schemes" presentation became a cautionary tale about shorting irreplaceable assets during a cyclical trough.

For investors, the Berkowitz-Einhorn showdown offers a lasting lesson. Einhorn's analysis was not wrong on the facts — the developments were underperforming, and the company did need to take impairments. But he was catastrophically wrong on the thesis, because he underestimated two things: the intrinsic scarcity of JOE's land position, and the willingness of a concentrated, patient owner-operator to wait for the cycle to turn. Berkowitz understood that you could not replicate 170,000 contiguous acres on the Gulf Coast of Florida. That asset was permanent. Everything else was temporary.

IV. Modern Management: The Jorge Gonzalez Era

By the mid-2010s, the proxy war was history and the question facing JOE had evolved. Berkowitz had won control and installed a new board. The company was no longer hemorrhaging value. But the fundamental strategic question remained: what do you actually do with 170,000 acres of Florida Panhandle?

The answer came in the person of Jorge Luis Gonzalez, who became President and CEO in November 2015. Gonzalez was not a flashy outside hire. He had joined St. Joe back in 2002 — during the Rummell era — and had spent over a decade working his way through the organization in roles of increasing responsibility. He held undergraduate and graduate degrees from Florida State University. He had three decades of experience in planning and real estate development. Most importantly, he was a local. He understood the Panhandle not as an abstraction on a map but as a place where he lived, worked, and raised a family. He served as chairman of the Bay County Economic Development Alliance, sat on the FSU Board of Trustees, and was deeply embedded in the civic fabric of the region.

This mattered more than it might seem. The Rummell era had been defined by a Disney executive's vision — grand, ambitious, but ultimately disconnected from the rhythms of Northwest Florida. The Berkowitz era was defined by a Miami billionaire's financial thesis — correct on value, but inherently an outsider's perspective. Gonzalez represented something different: operational intimacy. He knew which parcels flooded during heavy rains. He knew which county commissioners controlled zoning approvals. He knew the school board members, the hospital administrators, the local contractors. In a business built on developing a specific geography, that granular local knowledge was a genuine competitive advantage.

The strategic shift Gonzalez engineered was subtle but profound. Under previous leadership, JOE's business model was essentially land entitlement: acquire raw land, navigate the labyrinthine permitting process to secure development approvals, then sell entitled parcels to third-party builders and developers. It was asset-light but cyclical — when the housing market was hot, entitlement was a cash machine; when it turned cold, there was nothing to sell. Gonzalez moved the company toward vertical development: instead of just selling the land, JOE would build on it and own what it built. Hotels, membership clubs, commercial buildings, rental properties — assets that generated recurring revenue regardless of the homesite sales cycle.

This was not an obvious move. Vertical development requires far more capital, far more operational complexity, and far more risk than simply selling land. But Gonzalez understood that the flywheel only worked if JOE controlled the entire ecosystem. If you sell someone a homesite in WaterSound, they need a hotel for visiting family, a club for recreation, a grocery store, a medical center, restaurants. Every piece of that ecosystem that JOE builds and owns creates value for the homesites, which in turn creates demand for more ecosystem amenities. It is a self-reinforcing loop, and you can only capture it fully if you own both the land and the infrastructure on top of it.

The incentive structure at JOE reinforced this long-term orientation. Berkowitz, who served as Chairman from 2011 through October 2024, owned roughly 40% of the company through Fairholme and did not take a salary. His compensation was entirely aligned with share price appreciation — the purest form of skin in the game. Management's long-term incentive plan was tied to cash flow from operations rather than stock price, a critical distinction that discouraged the kind of land-sale manipulation that had plagued previous regimes. When your bonus depends on recurring cash flow, you build assets that generate recurring cash flow. When it depends on stock price, you are tempted to boost short-term earnings through one-time land sales.

The corporate structure remained remarkably lean. Despite managing a multi-billion dollar asset base that includes thousands of homesites, a dozen hotels, membership clubs, commercial properties, and an active timber operation, JOE operated with minimal overhead. Gonzalez ran the company from the Panhandle, not from a glass tower in Jacksonville or Miami. The organizational culture was pragmatic and execution-focused — a reflection of both Gonzalez's planning background and Berkowitz's insistence on capital discipline.

In October 2024, Gonzalez added the Chairman title to his role, succeeding Berkowitz. It was a quiet but significant milestone. For the first time in over a decade, the CEO and Chairman were the same person — and that person was a lifelong Panhandle operator, not a financial engineer. Berkowitz remained the dominant shareholder through Fairholme, but the day-to-day stewardship of the company now rested entirely with the man who had been building it from the inside for over two decades. This consolidation of leadership signaled that JOE's transformation from financial restructuring project to operating company was complete.

V. The Three Pillars & "Hidden" Businesses

Walk along County Road 30A today and you will see a stretch of coastline that looks nothing like it did twenty years ago. Boutique hotels tucked behind dune ridges. Gated communities with Mediterranean-style clubhouses. A private membership club where the waitlist stretches for months. All of it sits on land that St. Joe has owned since the 1930s. The company's modern business operates on three distinct pillars, each playing a specific role in what management calls the "flywheel."

Residential: The Cash Cow

The residential segment is where the story begins for most investors, because it is the most visible and the most immediately profitable. But this is not a traditional homebuilder business. JOE does not swing hammers. It entitles land, develops infrastructure — roads, utilities, drainage, common areas — and sells finished homesites to national and regional builders who construct the actual homes. The capital intensity is far lower than homebuilding, and the margins are far higher, because the cost basis on the underlying land dates back decades.

The transformational residential deal was the Latitude Margaritaville Watersound joint venture, announced around 2019 and breaking ground in 2020. This was a three-way partnership between St. Joe (the landowner), Minto Communities USA (the master developer and homebuilder), and Margaritaville Holdings — the lifestyle brand built by the late Jimmy Buffett. Latitude Margaritaville is a 55-plus active adult community, and the Watersound location was planned as the largest in the entire Latitude system, with an initial phase of approximately 3,500 homes.

The impact was immediate and dramatic. When sales opened in June 2021 — right as the pandemic-era migration wave was cresting — demand was overwhelming. Over 1,000 prospective buyers attended a virtual lot-drawing event. The community celebrated its 1,000th home sale in 2022. The Margaritaville brand fundamentally changed the demographics of the Panhandle. Previously, the 30A corridor attracted primarily affluent second-home buyers from the Southeast. Latitude brought a wave of full-time retirees — people selling homes in the Northeast and Midwest, moving their primary residence to Northwest Florida, and spending twelve months a year in the local economy. They needed doctors, grocery stores, restaurants, and entertainment. They became the customer base for everything else JOE was building.

At year-end 2025, the company reported approximately 23,900 homesites in various stages of planning, engineering, permitting, or development — up roughly 2,200 from the prior year. This pipeline represents decades of future revenue, released in carefully controlled phases to match demand. JOE is not trying to maximize short-term sales volume. It is managing the land bank like a multi-generational endowment, releasing inventory at a pace that supports pricing power.

Hospitality: The Growth Engine

If residential is the cash cow, hospitality is the story that gets investors excited about what JOE might become. In 2010, the company owned essentially zero hotel rooms. By early 2026, it owns — individually or through joint ventures — twelve hotels with 1,298 rooms. This is the "hidden" gem in the JOE story, and the segment that most clearly illustrates the transformation from land seller to operating company.

The flagship property is The Pearl Hotel, a luxury 55-room boutique hotel in Rosemary Beach with private Gulf beach access. St. Joe managed the property starting in 2014 and acquired full ownership in December 2022. But The Pearl is the tip of the iceberg. The company has opened six hotels since the start of 2023 alone, ranging from upscale branded properties like the Hotel Indigo Panama City Marina (which received IHG's prestigious Torchbearer Award in March 2026) to select-service hotels like the Home2 Suites and Hilton Garden Inn near the airport.

The Watersound Club is perhaps the most strategically important hospitality asset. This private membership club has seen explosive growth, with membership rising from 2,853 members in mid-2023 to 3,571 members by mid-2024. The Camp Creek Inn, a 75-room property adjacent to the club's golf course, opened as part of a broader amenity expansion. Membership clubs generate recurring revenue with high margins — annual dues, food and beverage, events — and they create a stickiness that raw land sales cannot. Once a family joins the Watersound Club, builds a house on a JOE homesite, and enrolls their kids in local schools, they are deeply embedded in the JOE ecosystem.

The hospitality segment's revenue contribution has grown from roughly $47 million in 2019 to a material portion of the company's $513 million in total 2025 revenue. And the pipeline continues to expand. Management has signaled plans for additional hotel development, marina expansion, and enhanced food and beverage offerings across the portfolio.

Commercial and Leasing: The Support System

The third pillar is the quietest but may be the most important for the long-term "yield company" thesis. JOE is not just building homes and hotels — it is building the connective tissue that makes a community function. Medical centers, grocery-anchored retail centers, office space, self-storage facilities. These are the mundane, essential services that residents and visitors require, and JOE is positioning itself as the landlord for all of them.

The logic is straightforward. When you develop a community of 3,500 homes, the residents need healthcare. Rather than waiting for a third-party developer to build a medical office, JOE builds it on its own land and leases it to a healthcare provider. The same logic applies to retail, dining, and professional services. Each commercial tenant reinforces the attractiveness of the residential communities, which drives more homesite demand, which creates more commercial tenants. The flywheel spins.

The Hidden Infrastructure

Beyond the three operating pillars, JOE possesses infrastructure assets that do not appear in any segment reporting but are critical to the thesis. The most important is the company's relationship with the Northwest Florida Beaches International Airport, known by its code ECP. St. Joe donated 4,000 acres of land for the airport, which opened in May 2010 as the first new commercial airport built in the United States since September 11th. The old Panama City airport had short runways and no room for expansion. ECP changed everything.

Passenger traffic has grown from roughly 300,000 annual passengers at the old airport to approximately 1.5 million by 2022, with records continuing through 2025. In March 2025, the first-ever nonstop flight from New York's LaGuardia Airport to ECP was announced — a milestone that signals the Panhandle's arrival as a nationally recognized destination rather than a regional drive-to market. St. Joe's major land holdings are strategically located near the airport, meaning every incremental flight and every new passenger is a potential homebuyer, hotel guest, or club member.

JOE also has port access and controls key infrastructure corridors across the region. The company is not merely a developer. It functions as something closer to the utility of Northwest Florida — the entity whose land, infrastructure, and planning decisions shape the region's growth trajectory for decades to come. That role is virtually impossible to replicate, and it provides a moat that goes far beyond the acreage itself.

VI. Capital Deployment & M&A Benchmarking

In the decade following the Berkowitz takeover, JOE became one of the more disciplined capital allocators in the small-cap real estate universe. The strategy was not flashy, but it was relentless and internally consistent.

The Buyback Machine

During the early-to-mid 2010s, when the market still doubted the value of JOE's land bank and the stock languished in the teens and twenties, the company aggressively repurchased its own shares. This was textbook value investing from the operator's seat: management and the board believed the market was dramatically undervaluing the land, so they used free cash flow to cannibalize outstanding shares at what they considered a fraction of intrinsic value. Every share retired at $20 that the land bank supported at $50 or more was an enormous transfer of value from selling shareholders to remaining ones.

The buyback program has continued in recent years, though with different intensity depending on valuation. In 2024, repurchases were modest — only about 71,000 shares. But in 2025, as the stock pulled back from its highs, the company ramped up significantly, repurchasing nearly 800,000 shares at an average price of roughly $50 per share, totaling $40 million. In February 2025, the board authorized a $100 million repurchase program, signaling continued willingness to buy back stock when the price is right.

Capital allocation in 2025 was balanced across three channels: $33.6 million in dividends (at $0.16 per share quarterly), $40 million in buybacks, and $46.6 million in net debt reduction. The quarterly dividend is modest by REIT standards but reflects the company's preference for reinvesting in development rather than distributing cash. The share count has declined gradually over the years, with weighted average diluted shares outstanding at roughly 57.6 million in 2025. It is not a dramatic cannibalizer like a Dillard's or AutoZone, but the direction is consistently downward, and it matters over a multi-decade holding period.

Joint Ventures Over Acquisitions

JOE's most distinctive capital deployment strategy is its use of joint ventures rather than traditional acquisitions. The Latitude Margaritaville Watersound deal is the paradigmatic example. A conventional developer wanting to build a 3,500-home retirement community on the Gulf Coast would need to first acquire the land — at current market prices, potentially hundreds of millions of dollars — and then spend additional hundreds of millions on infrastructure and construction. JOE simply contributed land it already owned into the joint venture. Its cost basis on that land was essentially zero. In return, it gained a share of the development profits, ongoing revenue from the surrounding ecosystem, and access to Margaritaville's brand and Minto's homebuilding expertise.

This pattern repeats across the business. When JOE partners with Hilton or IHG to develop branded hotels, it contributes land while the brand partner contributes management expertise, reservation systems, and brand recognition. When it develops commercial properties, it often structures deals where the land contribution gives JOE an ownership stake that would be prohibitively expensive for a competitor starting from scratch.

The math is simple but powerful. A competitor looking to replicate JOE's position would need to acquire 170,000 contiguous acres in coastal Northwest Florida — land that does not exist on the open market at any price. They would then need to spend decades navigating environmental permitting, securing water and sewer approvals, building roads and utilities, and establishing relationships with local governments. JOE has already done all of this. Its land bank is not just an asset; it is a barrier to entry that gets higher with every dollar of infrastructure invested on top of it.

Did They Overpay?

Benchmarking JOE against real estate peers on M&A discipline reveals a company that has been remarkably conservative with external capital deployment. The Pearl Hotel acquisition in December 2022 — a property JOE had already been managing for nearly a decade — was the kind of deal that made obvious strategic sense and carried minimal integration risk. The broader hotel expansion has been executed primarily through new construction on existing land rather than acquisition of operating properties at market multiples.

The company's largest "acquisition" cost was actually donated: the 4,000 acres given to establish ECP airport. That donation, viewed purely as a capital outlay, created more value per dollar than perhaps any transaction in JOE's history. The airport transformed the region's accessibility, drove population growth, and increased the value of every surrounding acre JOE retained. It was, in hindsight, one of the great infrastructure investments by a private company — a sacrifice of a small portion of the land bank that multiplied the value of the rest.

The key metric for tracking JOE's ongoing capital efficiency is revenue per entitled acre — how much economic output the company generates for each acre it has moved through the permitting and development process. The second critical KPI is hospitality revenue as a percentage of total revenue, which tracks the progress of the transformation from cyclical land sales to recurring operating income. As that percentage rises, earnings quality improves and the company's valuation multiple should expand to reflect the shift from a developer to an owner-operator.

VII. The Playbook: Strategic Moats and Competitive Position

Analyzing JOE through the lens of Hamilton Helmer's Seven Powers framework reveals a company with an unusually durable competitive position built on two dominant powers.

Cornered Resource

The most obvious and most powerful moat is the land itself. JOE's approximately 170,000 contiguous acres in Northwest Florida constitute a cornered resource in the purest sense. This is not simply about owning a lot of land — plenty of landowners in Florida have significant acreage. The critical distinction is contiguity, location, and entitlement.

Contiguity matters because master-planned community development requires large, unbroken parcels. You cannot build a Latitude Margaritaville by assembling hundreds of individual lots from different sellers — the coordination costs, holdout problems, and regulatory fragmentation make it practically impossible. JOE's Bay-Walton Sector Plan encompasses approximately 110,500 acres with fifteen miles of Intracoastal Waterway frontage, all under single ownership. This is the kind of land position that existed in the American West in the nineteenth century. It does not exist in twenty-first century coastal Florida — with one exception.

Location matters because the Florida Panhandle has emerged as the "last frontier" of Gulf Coast development. Central Florida is saturated with theme parks and suburban sprawl. South Florida is built out, expensive, and increasingly threatened by sea-level rise and insurance costs. The Panhandle offers white-sand beaches, lower cost of living, a pro-development regulatory environment, and a new international airport with growing connectivity. The geographic alternatives for a developer seeking to build at scale on the Gulf Coast have effectively narrowed to one place.

Entitlement matters because the environmental permitting process for large-scale development in Florida is measured in decades, not years. Wetland delineation, endangered species habitat assessment, stormwater management plans, water and sewer capacity studies — JOE has already navigated this labyrinth for enormous swaths of its land bank. A hypothetical competitor who somehow acquired comparable acreage would still face ten to twenty years of permitting before turning a single shovel of dirt. JOE has already completed that work.

Switching Costs

The second major power is the switching costs embedded in JOE's ecosystem. Once a hospital system builds a $500 million medical complex on JOE land, it is not relocating. Once Latitude Margaritaville constructs a 3,500-home community with pools, fitness centers, and a commercial village, it is permanently tied to the JOE infrastructure. Once airlines add routes to ECP, the surrounding economy orients around that connectivity. Each major investment by a third party on JOE's land deepens the moat and raises the cost of defection.

The Watersound Club membership model exemplifies this dynamic. Members pay initiation fees and annual dues for access to golf, beach, dining, and social amenities. Many of them own homes in adjacent JOE communities. Their social networks, recreational habits, and daily routines are woven into the JOE ecosystem. The switching cost is not just financial — it is lifestyle.

Porter's Five Forces

Examining JOE through Porter's framework reinforces the strength of the position:

Barriers to Entry are extreme. The combination of land scarcity, permitting timelines, infrastructure requirements, and capital needs makes it effectively impossible for a new entrant to challenge JOE's position in Northwest Florida. A well-capitalized developer could enter the region on a small scale — individual subdivisions or standalone hotels — but cannot replicate the integrated, multi-decade development platform.

Threat of Substitutes is limited and narrowing. The relevant substitute for a JOE homesite or hotel room is a comparable offering in another Florida coastal region. But South Florida faces escalating insurance costs, congestion, and affordability challenges. Central Florida lacks the beach lifestyle. The Panhandle's competitive position relative to substitute markets has improved consistently over the past decade and shows no signs of reversing.

Supplier Power is moderate. JOE depends on national homebuilders (like its new partnership with PulteGroup, announced in March 2026), hotel brand operators (Hilton, IHG), and construction contractors. These are competitive markets with multiple potential partners, giving JOE reasonable leverage. The land itself is the scarcest input, and JOE owns it.

Buyer Power is fragmented. Homesite purchasers are individual builders and consumers. Hotel guests are individual travelers. No single buyer has meaningful negotiating leverage over JOE. The Latitude Margaritaville waitlist dynamic — where demand consistently exceeds supply — illustrates the favorable supply-demand balance.

Competitive Rivalry is low in JOE's core market. There is no comparable large-scale, integrated developer-operator in the Panhandle. Smaller developers build individual communities or commercial projects, but none has the land bank, infrastructure, or institutional relationships to compete at JOE's scale. The company competes more broadly with other Florida real estate markets for migration flows, but within its geography, it operates with near-monopoly characteristics.

The third important KPI to track, alongside revenue per entitled acre and hospitality revenue mix, is homesite absorption rate — the pace at which finished homesites are sold to builders and end buyers. This metric captures the demand side of the flywheel. Consistent absorption in the range of historical averages signals that migration trends and pricing power remain intact. A sharp decline would be an early warning that the demand thesis is weakening.

VIII. Analysis: The Bull vs. Bear Case

The Bull Case: The Yield Company Transition

The optimistic vision for JOE is elegant and, if it plays out, enormously valuable. The thesis goes like this: the company is currently in a transitional phase, spending heavily on vertical development — hotels, clubs, commercial buildings, infrastructure — that depresses near-term margins but creates a portfolio of recurring-income assets. When the development phase matures, JOE will effectively become a "yield company": a diversified owner-operator of hospitality, commercial, and residential assets generating substantial recurring cash flow, sitting on a balance sheet with land carried at nearly zero cost.

The financial trajectory supports this narrative. Revenue grew from $116 million in 2019 to $513 million in 2025 — a compound annual growth rate of roughly 28%. Net income reached $115.6 million in 2025, with earnings per share hitting $2.00 for the first time in twenty-three years. The hospitality segment, which barely existed a decade ago, now contributes meaningfully to total revenue and is growing faster than any other segment. Each new hotel, each new club member, each new commercial lease adds a layer of recurring income that is less sensitive to the homesite sales cycle.

The land bank provides what is effectively an infinite development pipeline. With 23,900 homesites in various stages of development and 170,000 total acres, JOE has decades of inventory at current absorption rates. This is not a developer that will run out of land and need to acquire more at market prices. Every future project draws from the same Depression-era cost basis, meaning development margins should remain structurally higher than peers who must purchase land at current values.

The remote work revolution and Florida's continued population growth provide secular tailwinds. Florida gained an estimated 330,000 new residents between April 2020 and April 2021 alone, and the trend has continued as hybrid work normalizes and high-tax states push residents toward Florida's zero-income-tax environment. The Panhandle, once a seasonal vacation market, is increasingly a year-round destination for permanent residents — exactly the demographic that drives the flywheel.

If one projecting forward another decade, the bull case envisions JOE as something like a vertically integrated REIT with a hospitality franchise — a company generating hundreds of millions in recurring revenue from hotels, clubs, commercial leases, and residential fees, with an optionality kicker from continued homesite development on a massive, nearly free land bank.

The Bear Case: Concentration and Catastrophe

The bear case for JOE is not complicated, and it deserves serious consideration precisely because it is so straightforward.

First, hurricane risk. The Florida Panhandle sits squarely in the path of Gulf Coast hurricanes. Hurricane Michael, which made landfall on October 10, 2018 as a Category 5 storm with 161 mph winds, demonstrated the severity of this risk with devastating clarity. Michael was the strongest storm to hit the Panhandle in recorded history, causing roughly $25 billion in damage and virtually destroying the town of Mexico Beach. Port St. Joe — the company's historic home — suffered significant damage.

JOE was fortunate that the majority of its developed properties in Walton County and along the 30A corridor sustained minimal damage, as the storm's worst impact was concentrated further east. But fortune is not a strategy. A major hurricane tracking through JOE's core development corridor could cause billions in property damage, destroy years of development work, and shatter the demand narrative. Insurance costs in coastal Florida are already elevated and rising, with several major insurers exiting the state entirely. This is not a theoretical risk — it is a when-not-if scenario in a region that has experienced multiple major hurricanes in the past two decades.

Second, geographic concentration. JOE's entire business is in Northwest Florida. There is no geographic diversification. A regional economic downturn, a shift in migration patterns, a major environmental event (oil spills, red tide), or a sustained increase in insurance costs could all impair the fundamental demand thesis. When a single company's fortunes are tied entirely to a single geography, any negative development in that geography has outsized impact.

Third, the interest rate environment and housing cyclicality. While JOE is not a traditional homebuilder, its residential segment is inherently tied to the housing market. Rising interest rates reduce affordability and dampen demand for second homes and retirement relocations. The 2008 crisis demonstrated how quickly Florida real estate demand can evaporate. JOE's development pipeline is measured in decades, but demand can shift in quarters.

Fourth, key-person risk. Berkowitz's roughly 39% stake through Fairholme represents extraordinary ownership concentration. While his long-term commitment to the thesis has been a source of stability, any forced selling — due to fund redemptions, personal circumstances, or a change in investment thesis — could flood the market with shares and depress the stock price. Berkowitz stepped down as Chairman in 2024 but remains the dominant shareholder. The overhang of a single holder with nearly 40% of shares outstanding is a structural risk that should not be dismissed.

Finally, the accounting reality. JOE's land is carried at historical cost, which creates an enormous gap between book value and estimated market value. This is the foundation of the bull thesis — but it also means the balance sheet provides limited insight into true asset values. Land valuation is inherently subjective, and the "intrinsic value per acre" that bulls cite is ultimately a function of future development success, which depends on continued demand, favorable permitting, and the absence of catastrophic events. The Einhorn episode demonstrated that reasonable people can look at the same land bank and reach radically different conclusions about its value.

Myth vs. Reality

One common narrative holds that JOE is simply a "land play" — a bet on Florida real estate appreciation. The reality is more nuanced. The company's transformation under Gonzalez has created genuine operating businesses with growing recurring revenue. The hospitality segment alone would be a meaningful business if separated from the land bank. The Watersound Club's membership growth suggests real brand equity and pricing power. This is no longer just selling dirt.

Another narrative claims that JOE is "recession-proof" because its land cost is zero. This overstates the case. While the low cost basis provides a margin cushion, JOE still spends significant capital on infrastructure development, and homesite demand is unquestionably cyclical. The 2008 experience — when the stock fell over 80% — is a reminder that low land cost does not insulate against a demand collapse.

The most interesting question for long-term investors is not whether JOE's land is valuable — it clearly is — but whether the current management can successfully complete the transition from a primarily cyclical land business to a primarily recurring-revenue operating company. The hospitality revenue mix is the single most important indicator of that transition's progress. As that number rises, the investment thesis shifts from "discounted land bank" to "growing operating franchise," and the appropriate valuation framework shifts with it.

IX. Epilogue & Closing

Nearly a century ago, a feuding du Pont heir sent his brother-in-law to buy worthless Florida scrubland during the worst economic crisis in American history. The cost was trivial. The bet was that the land would eventually be worth something.

For seventy years, "something" meant pine trees and paper mills. Then it meant beachfront lots and planned communities. Then it meant a proxy war, a famous short-seller, and a stock that nearly went to zero. And now, in 2026, it means a half-billion-dollar diversified real estate and hospitality company with twelve hotels, a growing membership club empire, and a development pipeline that stretches to the horizon.

The St. Joe Company's story is, at its core, about the power of an infinite time horizon. Alfred du Pont could not have imagined Latitude Margaritaville or the Watersound Club. Edward Ball would have scoffed at the idea of closing the paper mill. Peter Rummell built the vision but could not survive the cycle. Bruce Berkowitz had the conviction to hold through the trough. And Jorge Gonzalez had the operational skill to build the flywheel.

Each era's steward added a layer to the asset. The du Pont trust assembled the land. Ball grew the timber and preserved the acreage. Rummell entitled it for development. Berkowitz recapitalized the company and installed disciplined governance. Gonzalez is building the recurring-revenue machine on top of it all. No single generation created the value — it accumulated across nearly a hundred years of patient ownership.

For investors watching this story unfold, the lesson is both simple and deeply counterintuitive in an era of quarterly earnings calls and algorithmic trading. Sometimes the best business strategy is to wait for the world to come to you. The Florida Panhandle was worthless in the 1930s, marginal in the 1970s, promising in the 1990s, and booming in the 2020s. JOE did not need to move its land to a better location or manufacture demand. It needed to own the land long enough for demographics, infrastructure, and migration patterns to make the value obvious.

That patience is JOE's ultimate competitive advantage — and its ultimate test. The next hurricane season, the next economic cycle, the next shift in migration patterns will all test the thesis. But the land will still be there. It has been there since the Cretaceous Period. The question is whether the people running the company can continue to convert geological patience into financial returns. So far, the answer has been yes.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube