Johnson Controls: The Ultimate Corporate Transformation

I. Introduction & Episode Roadmap

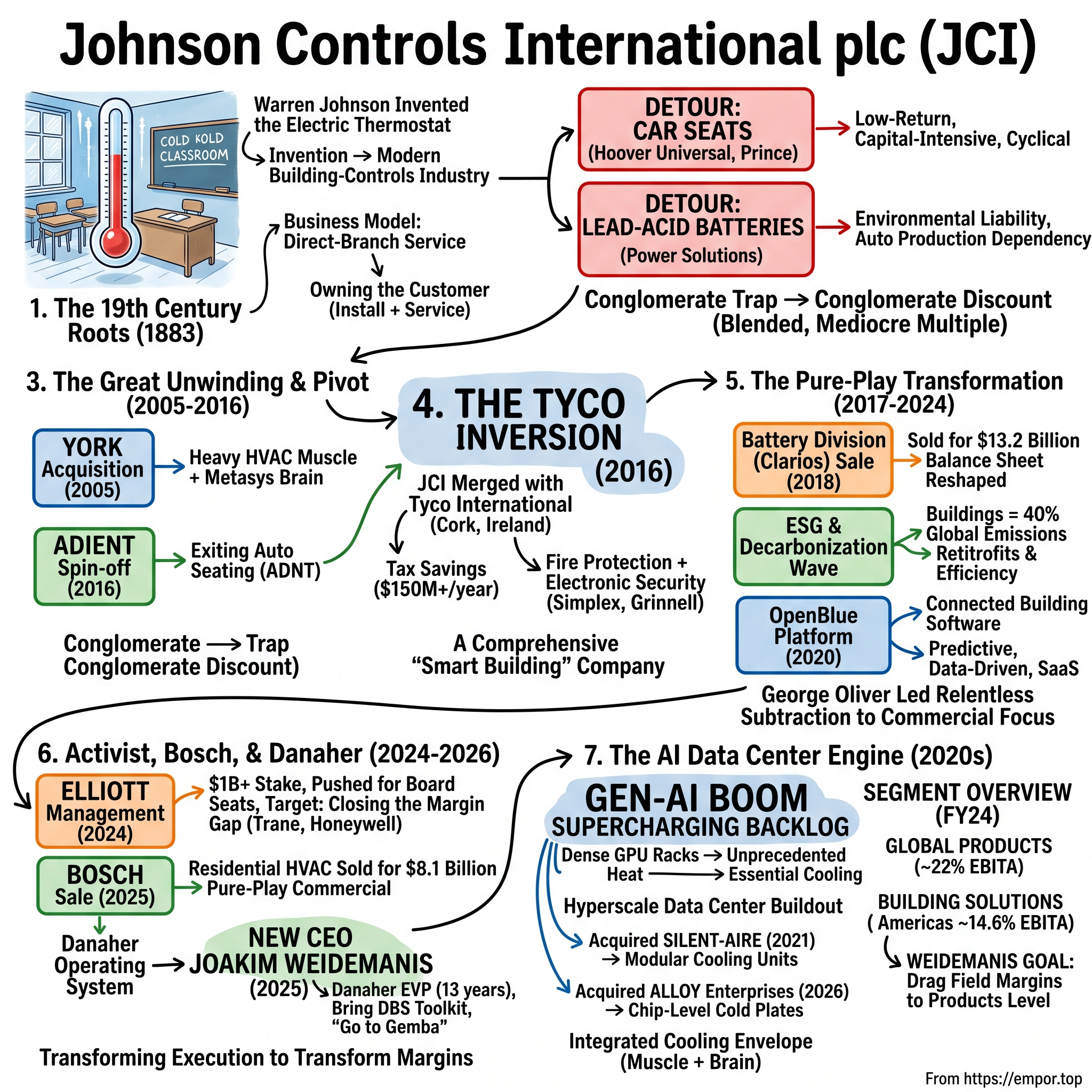

Start with a paradox that sits on a trading screen in the summer of 2026. A company founded in 1885 to sell brass thermostats to Wisconsin schoolhouses now carries a market value in the mid-$80 billions and trades at roughly 30 times forward earnings — a multiple the market normally hands to software companies, not to a firm whose products get lowered into building basements by crane. The stock is Johnson Controls International plc, ticker JCI on the New York Stock Exchange, and its share price has run from a 52-week low near $102 to above $150 inside a single year.[^15]

That re-rating is the reward for finishing one of the most radical corporate cleanups in American industrial history. Over roughly a decade, Johnson Controls did something almost no 140-year-old conglomerate manages to do: it shed its automotive skin, sold the world's largest car-battery business, spun off multiple divisions, executed a bitterly criticized multi-billion-dollar tax inversion, faced down one of the planet's most feared activist investors, and emerged as a pure-play commercial "smart building" company — hardware, software, and services aimed at a single customer: the owner of a large commercial building.

Here is the drama that makes it worth two hours of your attention, and it is a drama about a number. For years Johnson Controls trailed its focused peers on the one metric investors care most about — operating margin. Where focused rivals like Trane Technologies, Carrier, and Honeywell earned operating margins in the high teens, Johnson Controls limped along in the 11-to-13% range, despite owning some of the industry's most valuable building-management IP and a brand tradesmen have trusted for a century.8 Same industry, same tailwinds, persistently worse profitability. Why? That gap is the engine of this entire story, and closing it is now the company's central promise.

The person carrying that promise arrived in March 2025. Joakim Weidemanis, a thirteen-year veteran executive vice president of Danaher Corporation — the most admired operating machine in American industry — was hired with a single unglamorous mandate: bring the Danaher Business System to Johnson Controls, "go to Gemba" (the Japanese lean-manufacturing term for the place where work actually happens), and squeeze structural efficiency out of a sprawling global footprint.2 He inherited a company mid-transformation. Its climax came on July 31, 2025, when Johnson Controls completed the $8.1 billion sale of its Residential and Light Commercial HVAC business to Germany's Bosch Group, converting the last big consumer-facing division into cash and leaving behind a commercial-only pure-play.3[^10]

The rest of this story walks the full arc — from Warren Johnson's 1883 thermostat to the AI data-center chiller boom of the 2020s, through the conglomerate expansion, the Tyco inversion, the Elliott Management showdown, and the operational playbook now being tested in real time. The roadmap runs like this. We start with a professor's frozen classroom and the invention that created an industry, then watch a focused controls company talk itself into becoming a car-seat-and-battery conglomerate — and pay for it with two decades of investor indifference. We trace the great unwinding: the York chiller bet, the Adient spin, the Tyco inversion that made political enemies and industrial sense at once, the $13.2 billion battery sale, and the Bosch divestiture that finished the job. Then we meet the activist who forced the pace and the Danaher operator hired to finish it, before turning to the AI data-center boom now supercharging the order book, the frameworks that explain what actually protects the profits, and the bull-and-bear stress test any sober investor has to run.

A word on posture before we begin: Johnson Controls tells an excellent story about itself, and much of it is true. But "management says it will win" is a claim, not evidence. The interesting work — the work this piece is here to do — is separating the two. Let us start where the whole building-controls industry started: in a cold classroom.

II. The Thermostat & The 19th Century Roots

Picture Whitewater, Wisconsin, in the winter of 1883. Inside the State Normal School — a teacher-training college — a professor named Warren S. Johnson is losing a daily war with the weather. To adjust the heat, a janitor has to physically walk from room to room, open a furnace damper, guess, and walk away; the classrooms swing from frigid to stifling and back. Johnson, who taught natural sciences and had an inventor's low tolerance for stupid problems, decided the building itself should do the walking. He devised an electric thermostat that could sense a room's temperature and, when it drifted, ring a signal — later, actuate the damper directly — so that each room could hold its own setpoint independently. He patented the electric tele-thermoscope, the first multi-zone room thermostat, and with it effectively invented the modern building-controls industry.

The invention was clever; the business model around it was cleverer, and it still shapes the company 140 years later. In 1885 Johnson partnered with a Milwaukee businessman, William Plankinton, to commercialize the device, forming the Johnson Electric Service Company. Note the word Service in the name. From day one, Johnson grasped that a thermostat is not a product you sell and forget — it is one node in a system of sensors, valves, and controllers wired through an entire building, and that system has to be installed, calibrated, and maintained. So Johnson built his own workforce to do it. Rather than sell hardware through third-party distributors, the company created a network of company-employed "direct branch" technicians who installed and serviced complete temperature-regulation systems for the customer.

This direct-branch model became the deepest strategic feature of Johnson Controls — and, as we will see, its most persistent operational headache. On the one hand, owning the last mile to the customer builds an extraordinary moat: the people who service your equipment work for you, see the customer constantly, and can attach new contracts and upgrades. On the other hand, tens of thousands of unionized field technicians spread across thousands of branches are a labor-intensive, hard-to-standardize, margin-diluting machine. More than a century later, an ex-Danaher CEO would fly across the world specifically to fix the efficiency of that machine.

Warren Johnson himself was the restless, sprawling kind of inventor the Gilded Age produced in abundance. Temperature control was only his most durable idea; he also tinkered with pneumatic tower clocks, springless door locks, and even early automobiles, chasing patents in a dozen directions at once. That scattered energy nearly sank the company. By the time Johnson died in 1911, the firm had drifted into a grab-bag of unrelated ventures, and it took a hard corporate refocus in the following decades — a deliberate retreat back to the one thing it did better than anyone, building temperature control — to steady it. There is a lesson buried in that early near-death that the company would spend the next hundred years forgetting and relearning: Johnson Controls is at its best when it is focused, and at its most fragile when it mistakes activity for strategy. Hold that thought; it is the whole plot.

The genius of the direct-branch approach only compounds once you see what it does to the customer relationship over time. A building is not a static object. Its equipment ages, tenants change, energy codes tighten, and every few years something breaks in a way that requires someone who knows that specific building to fix it. Because Johnson Controls' own technicians were the ones who installed the system and returned to service it, they accumulated something no distributor-based rival could easily replicate: intimate, building-by-building knowledge, and a standing relationship with the facilities manager who signs the checks. That relationship is where service contracts get renewed and upgrades get sold. The hardware is the entry ticket; the decades of service that follow are the business.

The technology evolved in waves. Early room control was pneumatic — literally puffs of compressed air moving dampers and valves through networks of small copper tubes, a system so reliable that some buildings still run on it. Mid-century, the industry shifted to electronics. The defining leap came in 1990, when Johnson Controls launched Metasys, a computerized building automation system that turned a building's scattered mechanical equipment — heating, cooling, ventilation, lighting — into a single networked system managed from a central console. Metasys made the "brain of the building" a piece of Johnson Controls software.

It is worth pausing on why the building-management system is genuinely the "brain" of a building, because the metaphor does real analytical work. A large modern building is a living organism of interdependent systems: chillers and boilers regulating temperature, air handlers moving and filtering air, dampers and valves adjusting flow, lighting responding to occupancy, fire and security systems standing guard. Left uncoordinated, these systems fight each other and waste enormous energy — heating and cooling the same space, running equipment at full tilt in an empty wing. The BMS is the nervous system that senses conditions everywhere and choreographs the equipment into a single, efficient whole. Whoever supplies that brain occupies the most strategically valuable position in the building: they see all the data, they control the equipment, and they are the party the owner calls when anything goes wrong. It is a position of trust and information that is extraordinarily hard for a competitor to dislodge.

Why does that brain matter so much competitively? Because of switching costs — one of the durable sources of business power we will return to later. Once a building's controllers, sensors, and miles of wiring are embedded in its concrete floors and drywall, and once the facilities team has spent years learning one manufacturer's software, ripping it all out to switch vendors is enormously expensive and disruptive. A hospital or a university does not re-wire its climate system on a whim. The customer is, in practical terms, locked into that ecosystem for a decade or two — which means a stream of recurring service, parts, and upgrade revenue that competitors cannot easily contest. That embedded-base economics is the crown jewel of the whole enterprise. The tragedy of the next thirty years is how thoroughly management buried it.

III. The Conglomerate Trap: Auto Seating & Lead-Acid Batteries

By the 1980s, a good business inside a focused company was, by the prevailing wisdom of American management, a wasted opportunity. Scale meant safety; diversification meant stability; the conglomerate was king. Johnson Controls, sitting on a high-margin controls business with predictable cash flow, went looking for places to deploy it — and found the two lowest-return industries it could plausibly reach.

The first was car seats. In 1985 Johnson Controls acquired Hoover Universal, and in 1996 it bought Prince Corporation, a maker of automotive interior components. Bolt those together with organic growth and Johnson Controls became, improbably, the largest supplier of automotive seating and interior systems in the world. On a revenue basis it looked like a triumph — billions of dollars of new sales. On an economic basis it was a slow-motion mistake. Auto-parts supply is one of the most brutal businesses in existence: capital-intensive plants, thin margins, and a customer base — Detroit's Big Three and their global equivalents — with all the pricing power. Automakers dictate prices, demand annual cost-downs, and switch suppliers over pennies. A seat supplier has essentially zero pricing power of its own. Johnson Controls had taken the fat, defensible cash flows from building controls and used them to subsidize a gigantic, cyclical, low-return manufacturing division.

The second detour was batteries. Johnson Controls built — and eventually dominated — the global lead-acid automotive battery business, the humble 12-volt block under the hood of nearly every car with an internal-combustion engine. This was a genuinely strong franchise: at its peak the division, later branded Power Solutions, supplied more than a third of the world's car batteries, and unlike auto seating it was actually profitable. But it, too, was the wrong kind of business for a controls company to own. Batteries are heavy, capital-hungry, and wrapped in lead — meaning perpetual environmental liability, tightening regulation, and enormous ongoing capital expenditure just to stay compliant and current. It threw off cash, but it also swallowed cash, and it tied the company's fate to auto production cycles and lead prices.

It is worth dwelling on just how mismatched these businesses were, because the mismatch is the whole point. A building-controls contract is a multi-year, high-margin relationship with switching costs baked in — the customer cannot easily leave, and pays a premium for reliability. A car-seat contract is the opposite in every dimension: an automaker awards a platform, dictates the price, demands 2-to-3% annual cost reductions over the life of the program, and can re-source the work to a rival at the next model refresh. One business earns because the customer is locked in; the other bleeds because the customer holds all the cards. Running both under one roof did not create synergy — it created a permanent internal subsidy flowing from the good business to the bad one, invisible on the consolidated income statement but corrosive to returns on capital.

The battery division carried its own hidden bill. Lead-acid manufacturing is one of the most environmentally fraught industrial processes still practiced at scale: lead is a potent neurotoxin, recycling it is tightly regulated, and any plant carries perpetual exposure to remediation liability, worker-safety rules, and the slow tightening of environmental standards across every jurisdiction it operates in. Even when the batteries themselves sold well and threw off cash, the division demanded relentless reinvestment simply to stay compliant and competitive — capital that, in a focused controls company, could have gone toward software, service capacity, or shareholder returns. The market saw all of this and priced it in.

By the mid-2000s the result was a sprawling, hard-to-explain giant. The same company was simultaneously installing chiller controls in a Manhattan skyscraper, stitching seats for a Ford assembly line, and casting lead plates for car batteries in Ohio. Ask a portfolio manager to value that, and you get a shrug — and a discount. This is the conglomerate discount at work: when a business is a bundle of unrelated cash flows, investors who love one piece cannot buy it cleanly, so they either walk away or pay a blended, mediocre multiple that under-rewards the best division and over-rewards the worst. Johnson Controls' magnificent building-controls jewel spent two decades trapped inside a valuation that reflected its least attractive siblings. The market was, in effect, telling management something it did not yet want to hear: these things do not belong in the same company. The human cost of the conglomerate era is easy to overlook amid the strategy. Inside Johnson Controls, the controls business — the descendant of Warren Johnson's thermostat, staffed by engineers who understood buildings — spent decades as the quiet, profitable adult in a house dominated by the sheer revenue bulk of automotive. Capital, management attention, and boardroom oxygen flowed toward the biggest numbers, and the biggest numbers came from car seats and batteries. A generation of leaders learned to run a diversified industrial portfolio, optimizing for scale and cyclical balance, rather than to run a focused technology-and-service franchise, optimizing for margin and recurring revenue. That cultural inheritance — a company built to manage bigness rather than to compound a moat — is part of why the margin gap proved so stubborn even after the portfolio was cleaned up. Structure can be changed with a signature on a divestiture; habits take far longer.

Undoing that verdict would take the better part of fifteen years — and it began, ironically, by buying something even heavier.

IV. The York Acquisition & The Tyco Tax Inversion

In 2005, Johnson Controls made a bet that revealed both its ambition and its blind spot. It acquired York International for about $3.2 billion, buying its way into the heart of the HVAC industry. York was a legend — a maker of the massive industrial and commercial chillers that cool skyscrapers, factories, and campuses, machines the size of shipping containers that use spinning compressors to pull enormous quantities of heat out of a building's water loop. The strategic logic was elegant on paper: marry York's heavy mechanical iron with Johnson Controls' Metasys digital brain, and you could sell a building owner the complete package — the muscle and the nervous system in one purchase order.

To understand why York mattered, you have to understand what a commercial chiller actually is and why the pairing was compelling. A large building does not cool itself room by room with window units; it runs chilled water through pipes to air handlers, and a central chiller — often a magnetic-bearing centrifugal machine using a spinning impeller to compress refrigerant — is what chills that water. It is the single most expensive, most energy-hungry, most mission-critical piece of mechanical equipment in a large building. York was one of a handful of firms on earth that made the best of them. Owning both the chiller (the muscle) and Metasys (the brain) meant Johnson Controls could, in theory, sell and optimize the whole system as one — and capture the service revenue on both.

The logic was sound; the execution exposed a recurring weakness. Johnson Controls was, at its core, a service-and-controls culture — soft, relationship-driven, field-technician work. York was heavy manufacturing, with foundries, assembly lines, and a very different operating rhythm. Integrating a factory-floor business into a service organization proved slower and costlier than promised, and margins dipped in the years right after the deal. It was an early, visible instance of a pattern that would haunt the company and eventually draw activist fire: Johnson Controls could buy the right assets, but it struggled to knit them together efficiently and lift their combined profitability. Good at strategy, less good at the grinding work of integration.

Fast-forward to 2016, the year Johnson Controls did more portfolio surgery in twelve months than most companies attempt in a decade. First, the great auto escape. Bowing to years of investor pressure to stop subsidizing car seats, the company spun off its automotive seating and interiors business into a separate, publicly traded company called Adient plc, listed on the NYSE under ADNT, with the separation completing on October 31, 2016.[^8] On the way out, Adient paid a roughly $3.0 billion cash dividend back to Johnson Controls, which used the proceeds to cut debt.[^8] It was a clean amputation of the worst-economics division — though Adient's subsequent struggles through cyclical auto downturns quietly vindicated the decision to let it go.

The Adient spin is worth a second look as a case study in how hard it is to un-mix a conglomerate cleanly. The seating business was deeply entangled with the parent — shared corporate functions, shared systems, shared debt capacity — and separating it meant loading the new company with obligations and a cash dividend back to the parent that left Adient thinly capitalized just as global auto production entered a soft patch. Adient's shares struggled for years afterward. The episode cut both ways for Johnson Controls: it confirmed the wisdom of exiting an economically inferior business, but it also foreshadowed a risk that would resurface with every subsequent divestiture — that separating a business is never free, and that the costs left behind (stranded overhead, dis-synergies, transition expense) can linger long after the headline price is banked.

The bigger, louder move of 2016 was the merger with Tyco International — and the way it was structured turned it into a political lightning rod. In January 2016, Johnson Controls announced it would combine with Tyco, the fire-protection and security giant, in a deal valued at roughly $16.5 billion.7 Structurally, Johnson Controls merged into a subsidiary of the smaller, Irish-domiciled Tyco; the combined company took the Johnson Controls name and kept the JCI ticker but was legally headquartered in Cork, Ireland. This is a tax inversion — a maneuver that relocates a US company's corporate domicile abroad to escape the then-35% US corporate tax rate. Johnson Controls estimated the structure would save at least $150 million a year in taxes.7

There is a delicious irony buried in the mechanics here. Tyco itself was a company with a long and colorful history of tax-driven domicile shopping — it had bounced between Bermuda and Switzerland and finally Ireland — and it had survived one of the great corporate scandals of the early 2000s, when its former CEO Dennis Kozlowski went to prison for looting the company. That Tyco, cleaned up and rebuilt, would become the vehicle through which Johnson Controls escaped US taxes and eventually found its strategic soul is one of those plot twists that corporate history serves up more often than fiction would dare.

The backlash was immediate and fierce. This was 2016, an election year in which corporate inversions had become a symbol of companies abandoning America to dodge taxes; a sitting presidential candidate singled the deal out for attack, and the company that had started in a Wisconsin classroom was cast as a tax deserter. The optics were genuinely bad: Johnson Controls had taken US government bailout-era support and defense contracts, and now it was relocating its tax home to Cork. Management defended the move as an industrial combination first and a tax structure second — but the sequencing of benefits, with real cash savings flowing immediately and the industrial synergies promised over years, made that a hard sell in the political climate of the moment. Yet beneath the controversy lay a genuine industrial rationale that would matter far more in the long run than the tax savings. Tyco brought the missing pieces of the "complete building." Johnson Controls had HVAC and controls; Tyco brought commercial fire protection — the storied Simplex and Grinnell brands, whose sprinklers and alarm panels sit in millions of buildings — and electronic security systems. Put them together and you had, for the first time, a single company that could sell an owner the machinery to heat and cool a building, the intelligence to run it, the systems to protect it from fire, and the hardware to secure it. The tax deal made the headlines. The product logic made the modern company. And it handed the top job to a man from the Tyco side of the house.

V. The Pure-Play Pivot: Selling Batteries and the ESG Wave

George Oliver did not look like a revolutionary. A West Point graduate and former US Army officer who had spent years running industrial businesses inside General Electric before joining Tyco, he was an operator's operator — disciplined, process-minded, more comfortable talking about installed base and service attach rates than about disruption. He had run Tyco's fire and security business and then Tyco itself, and when the merger closed, the plan was for him to succeed the legacy Johnson Controls CEO Alex Molinaroli after a transition. He took the helm of the merged company and set about a task that was less about grand vision than relentless subtraction: strip the company down to one thing — commercial buildings — and do it well. The Adient spin and the Tyco combination had pointed the direction. Oliver's job, across 2017 to 2024, was to finish the demolition and start the rebuild.

The signature move came in 2018. Johnson Controls agreed to sell Power Solutions — the profitable, capital-hungry battery empire — to Brookfield Business Partners and its partners in a deal valued at $13.2 billion, announced in November 2018.6 The battery business, rebranded Clarios, went private; Johnson Controls walked away with roughly $11.6 billion in net cash. What management did with that money is the clearest evidence of intent in the whole transformation. It used the proceeds to repurchase about $3.6 billion of its own shares and to pay down roughly $4.0 billion of debt, reshaping the balance sheet in a single stroke and completing the exit from anything that wasn't a building.6 For a company that had spent three decades bolting on unrelated businesses, deliberately shrinking itself by a third of its revenue base was a genuine act of discipline — and the market began, slowly, to notice.

The Clarios sale deserves a moment's reflection on what it says about capital discipline versus timing. Selling a business that generated reliable profits — Power Solutions was, on a standalone basis, a good company — took nerve, because it shrank reported earnings in the near term. But it also crystallized value at a rich price and freed the company from a capital sink. The mirror image of that discipline showed up on the buyer's side: Brookfield and its partners took a franchise the market had valued at a conglomerate discount and, freed of Johnson Controls' complexity, positioned Clarios for its own eventual public listing years later. That is the conglomerate discount made tangible — the same assets, worth more apart than together, with the value transferring to whoever is willing to hold them cleanly. Johnson Controls, for once, was on the right side of that trade.

But subtraction alone does not make a growth story. Oliver's second act was to attach the newly focused company to a powerful secular wave: decarbonization. The pitch rested on a striking statistic that management repeated at every opportunity — buildings account for roughly 40% of global greenhouse-gas emissions, most of it from the energy they burn to heat, cool, and light themselves. As governments and corporations committed to net-zero targets, older, inefficient buildings became liabilities that owners had to upgrade. Johnson Controls positioned itself as the natural partner for that upgrade cycle: rip out the 1990s chiller, install a high-efficiency electric one, layer on smart controls, and cut both the energy bill and the carbon footprint at once.

Here a myth deserves puncturing, because it colored how investors valued the company for several years. The myth was that building decarbonization was, by itself, a near-term profit windfall — that net-zero commitments would translate directly into a wave of high-margin retrofit orders and re-rate the stock on green credentials alone. The reality was more sober. Decarbonization is a real, decades-long demand driver, but building owners upgrade on their own economic clock, not on a government's pledge date, and they weigh payback periods, financing costs, and disruption to tenants before ripping out a working chiller. The ESG wave gave Johnson Controls a genuine tailwind and a compelling story to tell, but it did not close the margin gap, and it did not spare the company from an activist's arrival. Tailwinds fill sails; they do not steer the ship. That distinction — between a real secular driver and a substitute for operational discipline — is the through-line of the whole modern chapter.

The vehicle for capturing the high-margin end of that opportunity was OpenBlue, a cloud-based, AI-branded software suite launched in 2020 that connects a building's HVAC, fire, and security systems into one data layer — monitoring air quality, predicting equipment failures before they happen, and optimizing energy use. Management claimed OpenBlue could cut a building's energy consumption dramatically and, crucially, would generate recurring, high-margin software-as-a-service revenue rather than one-time equipment sales. Here the neutral posture matters. The decarbonization tailwind is real and the software logic is sound, but for years OpenBlue was more narrative than needle-mover — Johnson Controls never broke out OpenBlue revenue as a disclosed line, and there was little hard evidence it had bent the company's margin curve. A skeptic could fairly note that the software story arrived just as the company needed a growth narrative, and that the gap between the pitch and the profit-and-loss statement was precisely the gap an activist would soon exploit. Which is exactly what happened next.

VI. Activism, The Bosch Sale, and The Danaher Coup

In May 2024, the knock came. Elliott Investment Management — the most feared activist fund in the world, a firm with a reputation for grinding boards into submission — disclosed a stake in Johnson Controls worth more than $1.0 billion.8 Elliott does not buy quietly to admire a company; it buys to force change, and its critique of Johnson Controls was surgical. The core charge was the margin gap this story opened with: Johnson Controls' operating margins languished around 11-to-13% while pure-play peers like Trane ran near 18-to-19%.8 Elliott argued the difference was not the market — it was the management. Sloppy project execution in the installation business, bloated overhead, and weak pricing discipline in the direct-branch field organization were, in Elliott's telling, leaving billions of dollars of profit on the table. To press the point, Elliott pushed for board seats and championed the appointment of Patrick Decker, the former CEO of water-technology company Xylem and a name synonymous with operational rigor.

Johnson Controls, to its credit, did not wage a scorched-earth defense; it moved. Two months later — though talks predated the Elliott disclosure — the company struck the deal that would define its endgame. In July 2024 it agreed to sell its Residential and Light Commercial HVAC business to Bosch for $8.1 billion, a package that included the York residential brand and the global Hitachi HVAC joint venture.[^10] The strategic message was unambiguous: exit the lower-margin, more cyclical world of home air conditioning and consumer-facing equipment, and become a company that sells only to commercial and industrial building owners. The transaction completed on July 31, 2025.3

The financial engineering was clean. Bosch paid $8.1 billion in enterprise value; Johnson Controls received roughly $6.9 billion in gross cash at close and, after taxes and expenses, around $5.0 billion in net proceeds.310 Capital allocation followed the now-familiar template — defend the investment-grade credit rating with debt paydown, and hand the rest back to shareholders. The company initiated $5.0 billion in accelerated share repurchases, a decisive signal that management believed its own shares were the best use of the cash.10 With the R&LC sale done, the transformation that began with the Adient spin was, in portfolio terms, complete: Johnson Controls was finally a pure-play commercial building-solutions company.

To grasp why Elliott's critique landed so hard, hold two companies side by side on a single sentence: Johnson Controls and Trane sell into overlapping markets, with overlapping products, to overlapping customers — and yet for years Trane converted its revenue into operating profit at a rate roughly five to seven percentage points higher.8 On a revenue base above $20 billion, each percentage point of margin is more than $200 million of operating profit. Elliott's arithmetic was, at its core, that simple and that damning: the gap was not destiny, it was performance, and closing even half of it would be worth billions in earnings and, through a higher multiple, tens of billions in market value. That is the prize that draws an activist. And unlike a hostile campaign at a company with no obvious fix, this one came with a ready-made remedy — better operators and tighter execution — which is exactly why the board's response was to change the operator rather than to fight.

Then came the coup. In February 2025, Johnson Controls announced that George Oliver would retire and that the board, after a comprehensive search, had appointed Joakim Weidemanis as CEO, effective March 2025.2 Weidemanis was not a building-industry lifer. He was a Danaher man — thirteen years as an executive vice president at the conglomerate whose Danaher Business System (DBS) is studied in business schools as the gold standard of continuous operational improvement, a disciplined toolkit of lean manufacturing, standardized problem-solving, and relentless measurement.

It is worth explaining what the Danaher Business System actually is, because "operational excellence" is the emptiest phrase in corporate English and DBS is the rare thing that gives it teeth. Danaher spent decades turning the Toyota production philosophy into a portable management religion: a set of standardized tools — value-stream mapping, daily visual management, structured root-cause problem solving, disciplined product development — applied relentlessly and measured obsessively, and, crucially, carried by people who are trained in it and then dispersed across the company to spread it. When Danaher buys a business, it does not just install new financial targets; it installs DBS, and the businesses tend to get measurably better at converting effort into margin. Hiring a thirteen-year Danaher EVP is therefore not a résumé line — it is a bet that the single most valuable import Johnson Controls could make is not a strategy but a system. The board also split the roles it had long combined, naming Mark Vergnano independent chairman, a governance concession of exactly the kind activists demand.2 Separating the chair and CEO roles matters beyond symbolism: it puts an independent voice at the head of the board to hold the new CEO accountable, and it signals to the market that the days of a single all-powerful executive setting his own report card are over. Combined with the earlier addition of the operations-minded Patrick Decker to the board's orbit, the governance changes amounted to Elliott getting much of what it wanted without a public proxy war — a settlement that let both sides claim victory and, more importantly, aligned the board around the single objective of margin improvement.8 The subtext was impossible to miss: the company had spent a decade fixing its portfolio; now it was rebuilding its board and management around the job of fixing its execution.

The early quarters under the new regime gave the thesis some evidentiary support, and it is worth watching how the language evolved on the earnings calls, because narrative consistency is itself a test of management credibility. In the company's fiscal second quarter of 2025 — Weidemanis's first full quarter — organic sales grew and the company raised full-year guidance, with adjusted EPS of $0.82, and management leaned hard into a story about pricing discipline and productivity rather than heroic top-line bets.12 A year later, in fiscal Q2 2026, the same themes recurred almost word for word — "converting sustained demand into consistent growth, margin expansion" — but now backed by 310 basis points of margin expansion and a doubled backlog.11 The consistency of the message across a full year, matched by numbers moving in the promised direction, is the kind of behavior that builds credibility. The skeptic's caveat is that one year is not a track record, and that the AI order surge is flattering the underlying operational story in ways that make it hard to separate self-help from tailwind.

Weidemanis wasted little time signaling how. In 2026 he staged the company's first "Going to Gemba Day," an investor-facing event whose very name — borrowed from the Toyota production lexicon for going to see the actual work being done — announced the arrival of the DBS toolkit inside Johnson Controls.4 The pitch to investors was concrete: use standardized work and lean tools to streamline branch operations, smooth the handoff from equipment installation to recurring service, and enforce pricing discipline across tens of thousands of field technicians. Whether a factory-floor operating system can actually be transplanted into a service-heavy, unionized, distributed field organization is one of the central open questions of this investment — and we will stress-test it directly. But the early financial evidence, at least, gave the skeptics something to chew on.

VII. The Data Center Cooling Engine & Segment Financials

Every few decades, a technology shift arrives that turns a sleepy industrial product into the hottest thing in the economy. For the chiller business, that shift is generative AI. Here is the physics, in plain terms. The chips that train and run large AI models — dense racks of GPUs — draw staggering amounts of power and convert nearly all of it into heat, concentrated in spaces far tighter than a traditional server room. Old-fashioned air cooling, blowing cold air across the racks, simply cannot carry that much heat away fast enough. So the industry is racing toward liquid cooling — running coolant directly to the chips through "cold plates" — and toward far more powerful, high-efficiency industrial chillers to reject the heat. Cooling has gone from a data center afterthought to mission-critical infrastructure that can gate how fast an AI buildout proceeds.

Put a number on the heat to make it visceral. A traditional server rack might have drawn five to ten kilowatts. A rack packed with the latest AI accelerators can draw well over a hundred kilowatts — as much as dozens of homes — concentrated in a cabinet the size of a refrigerator. All of that electricity becomes heat that must be removed continuously, or the chips throttle and eventually fail. This is why cooling has quietly become one of the binding constraints on how fast the AI buildout can proceed: you can order the GPUs, but if you cannot reject their heat, you cannot run them. The company that can design, build, and service the entire thermal path — from the chip's cold plate to the rooftop chiller — sits in an enviable spot, selling a mission-critical system to customers for whom downtime is measured in millions of dollars per hour.

Johnson Controls saw the edge of this wave early. In 2021 it acquired Silent-Aire, a Canadian pioneer in hyperscale data-center cooling, for up to $870 million — about $630 million upfront plus earnouts tied to performance.9 At the time, some observers thought the price rich for a niche maker of custom air handlers and modular cooling units. In hindsight it looks like one of the shrewdest deals the company ever made. Silent-Aire's custom, factory-built cooling modules — which can be trucked to a data center site and dropped into place — became one of Johnson Controls' fastest-growing, highest-margin product lines exactly as the AI capex boom detonated. It is the quiet genius of the transformation: a company busy shedding batteries and car seats happened to plant a flag in what would become the decade's premier infrastructure gold rush.

Weidemanis doubled down with his first major acquisition as CEO. In May 2026 Johnson Controls completed the purchase of Alloy Enterprises, a startup whose proprietary "Stack Forging" process 3D-prints single-piece, leak-tight metal cold plates for direct-to-chip liquid cooling, with internal microgeometries too complex to machine conventionally.5 Alloy's technology reportedly cuts thermal resistance by about 35% and pressure drop by up to four times versus standard designs — meaning chips run cooler while the cooling system itself burns less energy to do it.5 Financial terms were not disclosed. Strategically, the deal moved Johnson Controls from cooling the room to cooling the chip, staking a claim in the most technically demanding layer of the AI thermal stack. It also fit a clear acquisition pattern: where the York and Tyco eras were about buying scale and breadth, the Silent-Aire and Alloy deals were about buying specific, defensible technology in the single fastest-growing corner of the market — a smaller-bore, higher-return M&A posture that looks a great deal more like Danaher's own bolt-on discipline than like the transformational megadeals of the past.

The competitive logic that ties it all together is what management calls selling the whole "envelope." A hyperscaler building a data center campus needs chillers to reject heat, modular cooling units to condition the halls, cold plates to cool the chips directly, controls to run the whole thermal system, fire suppression designed for high-density electrical loads, and security for a facility worth billions. Johnson Controls can, uniquely, supply nearly all of it and then service it under one relationship across dozens of sites worldwide. For a customer racing to bring capacity online, that single-vendor breadth is worth real money in speed and coordination — which is precisely the differentiation management has pointed to on recent earnings calls when analysts probe why the order growth is outrunning the broader construction market. Whether that breadth commands a durable price premium or simply wins the bid on convenience is the question the margins will eventually answer.

The financial results give this data-center story real weight. Consider the segment structure as it stood at the FY2024 baseline, before the Bosch sale reshuffled the reporting. Global Products — the design-and-manufacturing core making chillers, controls, fire, and security equipment — generated about $9.5 billion in sales at roughly a 22% EBITA margin, the profit engine of the company.1 Building Solutions North America, the direct-to-customer installation and service business, produced about $11.3 billion in sales but at only a ~14.6% margin — larger, but structurally less profitable.1 The smaller EMEA/Latin America and Asia-Pacific field segments added roughly $4.3 billion and $2.2 billion respectively.1 Stare at those two big numbers and the entire Weidemanis thesis snaps into focus: the field business is nearly as big as the products business but far less profitable, so the single most valuable thing management can do is drag those direct-branch margins up toward the products level by cutting low-margin construction projects and driving high-margin recurring service and software.

There is an important subtlety in why the field business earns less, and it is not simply that Johnson Controls is worse at it. The direct-branch business bundles two very different activities under one roof: low-margin new-construction and installation work, where the company competes on price to win the initial project, and high-margin recurring service, where it earns for decades once the equipment is in. For years the installation side, chasing revenue growth, took on too many low-quality construction projects at thin or negative margins — winning the top line while starving the bottom. The Weidemanis prescription is not to abandon installation but to be ruthlessly selective about it: walk away from bad projects, price the good ones with discipline, and treat every installation primarily as a hook that lands a long-term service contract. It is a shift from a revenue mindset to a margin mindset, and it is culturally harder than it sounds inside an organization whose branch managers have been rewarded on bookings for a century.

By late 2025 and into 2026, the numbers suggested the drag was starting to lift. The company reorganized into three regional segments — Americas, EMEA, and Asia-Pacific — and reported FY2025 adjusted segment EBITA margins of 18.4% in the Americas, 13.2% in EMEA, and 17.0% in Asia-Pacific, on total continuing-operations revenue of $23.6 billion, up 6% organically, with adjusted EPS of $3.76 and a record systems-and-services backlog of about $15 billion, up 13% organically.10 The EMEA margin lagging in the low teens while the Americas ran above 18% is itself a tell: it marks exactly where the operational upside still lives, and where the next phase of the turnaround will be judged. Then came the fiscal Q2 2026 print in May 2026, and it was the strongest evidence yet: sales up 8% to $6.1 billion, orders up 30%, backlog swelling to a record $20 billion, adjusted EBIT margin expanding 310 basis points to 15.5%, and adjusted EPS up 45%.11 Management attributed the order and backlog surge directly to demand for large-scale data-center projects and said it expected about 70% of that backlog to convert to revenue within twelve months.11

Two things about that backlog deserve an analyst's scrutiny rather than a cheerleader's applause. First, the composition. A $20 billion backlog is a wonderful thing to own, but its quality depends entirely on what is inside it, and Johnson Controls has been candid that data centers are the dominant driver of the recent surge. That concentrates the company's near-term fortunes on a single end market whose spending is set by a handful of hyperscale buyers making multi-year capital bets on AI demand that even they cannot forecast with confidence. If that capex cycle cools, the order line turns first and fastest. Second, the conversion mechanics. Management's claim that roughly 70% of the backlog converts within twelve months is genuinely useful for investors, because it converts a lagging indicator into a forward one — but it also means the backlog is not a decade-long annuity so much as a rolling, refillable pipeline that has to keep being replenished by new orders. The order-growth number, not the backlog level, is the leading signal to watch.

What the evidence suggests, on balance, is real operating momentum layered on top of a genuine secular tailwind — a combination that is powerful precisely because it is hard to disentangle. The bull reads the margin expansion as proof the Danaher system is working. The bear reads it as a rising tide that would lift any competent operator, and notes that the true test comes when the AI order surge normalizes and we finally see how much of the margin gain was structural self-help and how much was cyclical volume. Both readings fit the data available in mid-2026. That ambiguity is the honest state of the investment.

VIII. The Playbook: Hamilton Helmer's 7 Powers & Porter's 5 Forces

Strip away the narrative and ask the harder question: what, precisely, protects Johnson Controls' profits from competition? Two frameworks help — Hamilton Helmer's 7 Powers, which catalogs the distinct sources of durable business advantage, and Michael Porter's Five Forces, which maps the pressures bearing on an industry.

Start with the powers Johnson Controls plausibly holds. The first and strongest is switching costs. As we saw with Metasys and now OpenBlue, once a building operating system is fused into a structure's physical wiring and the facilities team's daily routine, replacing it is prohibitively disruptive — locking customers into ten-to-twenty-year relationships of service contracts, parts, and upgrades. This is the power that makes the installed base an annuity rather than a one-time sale, and it is the reason the field business, for all its margin problems, is strategically precious.

The second is scale economies, though it is better described as a distribution advantage. Johnson Controls operates a direct branch network of thousands of offices and tens of thousands of trained technicians spanning the globe. A rival cannot simply decide to service commercial buildings at that density; recruiting, training, and positioning that many skilled people in that many local markets is the work of decades and billions of dollars. That local density is both a barrier to entry and the reason a hyperscaler building forty data centers across three continents keeps coming back — few competitors can show up everywhere the customer is building. The third, and most speculative, is an emerging cornered resource: proprietary technology like high-efficiency magnetic-bearing centrifugal chillers and the Silent-Aire and Alloy cooling IP. "Cornered" may be generous — competitors have their own advanced chillers — but in the specific niche of hyperscale and direct-to-chip cooling, Johnson Controls has assembled a genuinely differentiated toolkit.

Two further powers deserve honest weighing, one that Johnson Controls holds and one it arguably does not. The one it holds is a form of branding and process power in the professional-buyer sense: brands like YORK, Metasys, Simplex, and Grinnell carry a century of accumulated trust among the engineers, contractors, and facilities managers who actually specify equipment, and in mission-critical applications — a hospital operating theater, a hyperscale data center — that trust translates into pricing power, because the buyer will pay to not be the person who chose the cheap system that failed. The power it arguably lacks, at least so far, is process power in the Danaher sense: a proprietary way of operating that competitors cannot replicate even if they try. That is precisely the power Weidemanis is attempting to build by importing DBS. If he succeeds, Johnson Controls would add a genuinely new source of advantage to its arsenal. If he does not, the company remains a collection of good assets and strong switching costs run at merely average operational efficiency — which is the status quo the activists showed up to change.

Now Porter's forces, which temper the optimism. Rivalry is high: Johnson Controls competes head-on with Carrier, Honeywell, Trane, and Europe's Siemens and Schneider Electric, and in commodity equipment-only sales, price competition is savage — precisely why the company works so hard to sell integrated solutions where it can differentiate rather than bare metal boxes where it cannot. The bargaining power of buyers is medium and rising: hyperscale data-center operators are enormous, sophisticated, and concentrated, giving them real leverage, though in mission-critical cooling they tend to prize reliability and speed over squeezing the last dollar. The threat of new entrants, by contrast, is low — the capital to design heavy industrial chillers plus the field army to service them is a formidable double barrier that has kept the competitive set stable for decades.

It helps to game-war the competitive set concretely, because "we compete with everyone" is not analysis. Trane is the pure-play benchmark and the margin standard Johnson Controls is chasing — a focused climate company that trades at a premium precisely because it has already proven it can convert HVAC into high-teens margins and a rich service annuity. Carrier, spun out of United Technologies, is a close structural analog to Johnson Controls' own journey, having itself divested fire and security to become a focused climate player. Honeywell attacks from the software and controls direction with its own building-management franchise. Europe's Siemens and Schneider Electric come at the building from the electrical and automation side, with formidable digital platforms of their own. What is striking is that none of these rivals combines all of what Johnson Controls now offers — heavy chillers, controls, fire, security, and hyperscale cooling — under one roof selling to one building owner. That breadth is the genuine differentiator. The open question is whether breadth translates into the ability to charge more and retain customers longer, or whether it simply spreads management attention across too many legacy platforms, which is exactly the integration critique the bears press.

Which brings us to the playbook's central bet and its central risk. The Danaher Business System was forged on factory floors, where standardized work and continuous measurement have obvious purchase. Johnson Controls' hardest profit problem lives somewhere very different: in the field, where a unionized technician diagnoses a failing chiller in a hospital basement, where "standard work" collides with the messy variability of real buildings and real labor. The "Going to Gemba" approach — sending leaders to watch the actual work and drive standardization, error reduction, and service-contract attachment — is a coherent theory. Whether a system built for repeatable manufacturing can reliably lift the margins of a distributed human-service organization is genuinely unproven, and it is the pivot on which the whole investment turns.

IX. Analysis: Bull vs. Bear Case & Current Risk Radar

Lay the two cases side by side, because an honest reader has to hold both. The bull case — the "why win" — rests on three legs. First, focus: shedding residential HVAC removed a lower-margin, more cyclical, consumer-facing drag, leaving a cleaner, more defensible commercial franchise. Second, the data-center tailwind, where Johnson Controls can arguably sell the entire cooling "envelope" — YORK chillers, Silent-Aire modular units, Alloy chip-level cold plates, Metasys controls, plus Simplex fire suppression and security — to a hyperscaler in one relationship, a breadth few rivals match. Third, and most consequential, the operational lift: if Weidemanis genuinely closes the historical margin gap with Trane and Honeywell, both earnings and the valuation multiple could re-rate, because the market would stop pricing Johnson Controls as the perennial laggard of its peer group. The Q2 2026 margin expansion is the first tangible down payment on that thesis.11

The bear case — the "why lose" — is equally concrete. First, technician labor. The direct-branch model that is a moat in good times is a cost trap in a tight, unionized labor market; if wages for skilled field technicians rise faster than pricing, the very margin expansion the bulls are counting on gets eaten from below. Second, integration debt. The company's portfolio is a patchwork of legacy platforms — HVAC, fire, security, controls, all acquired at different times on different technology stacks — and making them work seamlessly under OpenBlue is an expensive, open-ended engineering commitment whose payoff has been promised for years and only partially delivered. Third, the shadow over the whole real-estate complex: even as data centers and healthcare boom, the broader commercial office market faces secular headwinds from hybrid work, and a prolonged slump in new office construction would slow the installation backlog that feeds the service annuity.

There is also a valuation dimension the bull case tends to skip past. By mid-2026 the stock had already re-rated toward a premium multiple in the low thirties on forward earnings — richer than most diversified industrials and approaching the level the market awards Trane.[^15] That matters because it means a great deal of the operational improvement is arguably already in the price. For the stock to keep working from here, management does not merely have to make progress on margins; it has to make progress faster and further than the market has already assumed. A pure-play with a premium multiple has, in effect, borrowed against its own future execution — and if the Danaher lift proves slower or shallower than the guidance implies, the same multiple that rewarded the story can compress just as quickly. The re-rating that vindicated the transformation is also what raises the stakes on delivering it.

An activist-minded skeptic would push harder still on three points. On disclosure: the company has long talked up OpenBlue and recurring software revenue without ever cleanly quantifying it, which is exactly the kind of narrative-without-numbers that invites suspicion. On concentration: the backlog and order strength are now heavily driven by data centers, so the quality of that backlog is only as durable as the AI capex cycle — a boom that could cool as fast as it heated. And on execution history: this is a company with a documented pattern of buying good assets and struggling to integrate them profitably, from York onward, which is precisely why bringing in an outside operator was necessary and why his success cannot be assumed.

The current risk radar flags two structural items beyond the cyclical ones. The first is stranded costs. Selling the R&LC business removed revenue, but the shared corporate overhead that supported it does not vanish automatically; if management cannot eliminate that overhead as fast as the revenue leaves, "stranded" costs will quietly erode the margin math of the pure-play. The second is the cost of capital. Long-cycle commercial contracting is capital-intensive, and Johnson Controls' whole capital-allocation posture — debt paydown before buybacks — is built around defending its investment-grade rating; in a higher-for-longer rate environment, protecting that rating while funding growth and returning cash is a real constraint, not a formality.

Two further risks belong on the radar precisely because the company's own strategy invites them. The first is cybersecurity, which is the shadow side of the OpenBlue story. A connected building — one where the HVAC, fire, and security systems are networked and remotely managed — is also an attack surface, and a vendor that runs the software brain for thousands of hospitals, data centers, and government buildings is an obvious target. Every dollar of recurring software revenue the company chases brings with it a corresponding obligation to secure critical infrastructure, and a serious breach would be both an operational and a reputational event. The second is geopolitical and supply-chain exposure: heavy chillers and cooling systems depend on global supply of compressors, controls chips, refrigerants, and specialty metals, and a company selling into China, the Middle East, and the West simultaneously is exposed to tariffs, export controls, and the slow bifurcation of the global economy into rival technology blocs. Neither risk is acute today, but both scale with exactly the strategy management is pursuing.

For an investor tracking whether the thesis is working, three KPIs cut through the noise. First, organic service revenue growth — because high-single-digit growth in recurring service is the direct readout on whether the installed-base annuity is compounding rather than stagnating. Service is the highest-margin, most durable, least cyclical stream in the whole company, and its growth rate is the truest measure of whether the "sell installation to land service" flywheel is actually turning. Second, adjusted segment EBITA margin, and specifically the Americas field business, which is where the Danaher-driven margin story either shows up or doesn't; watching that number climb toward the products segment's low-twenties over several years — not one flattering quarter — is how you separate a genuine structural lift from a cyclical sugar high. Third, data-center backlog and order velocity, and in particular the order-growth rate rather than the backlog level, because orders turn first when the AI capex cycle shifts. It is the cleanest available gauge of Johnson Controls' capture of the AI cooling buildout, and the number most likely to signal, early, when the boom cools. Watch those three and you are watching the actual argument, not the press release.

X. Epilogue & Outro

Step back far enough and Johnson Controls reads like a compressed history of American industry itself. It began as a focused local invention — one professor's fix for one cold classroom. It grew into a globe-spanning conglomerate on the mid-century faith that bigger and broader meant safer. It discovered, painfully and over decades, that the faith was backwards — that unrelated diversification destroyed the very value it promised to protect — and then it spent fifteen years and an activist's intervention undoing what it had built, until it arrived back at focus. From local specialist to sprawling conglomerate to activist-driven pure-play: the arc is the arc of the age.

Two ironies are worth sitting with. The first is the quiet genius of Silent-Aire — a modest 2021 acquisition, criticized as overpriced, that positioned a battery-and-seats conglomerate to become a central supplier to the AI infrastructure boom, entirely by luck as much as foresight. The second is the Tyco merger. It was sold to the world as a tax dodge and vilified as one, yet the fire, security, and Irish-domiciled structure it created quietly assembled the missing pieces of the integrated "smart building" company that Johnson Controls has finally become. The maneuver that drew the most criticism laid the foundation for the strategy that now draws the most praise.

There is a broader lesson here for anyone who studies how value gets created and destroyed in industrial companies. For most of the twentieth century, the prevailing theory held that diversification reduced risk and that scale was its own reward — that a good business was safer inside a big one. Johnson Controls lived that theory to its conclusion and paid for it with two lost decades of conglomerate discount. The correction, when it came, was not gentle: it took an activist's billion-dollar stake, an outside CEO, and the wholesale dismantling of businesses the company had spent thirty years assembling. The market's verdict, rendered in the re-rated multiple of 2025 and 2026, is that focus beats breadth — but only if the focused company can also operate well. Focus got Johnson Controls the invitation; execution is the price of staying at the table.

None of which settles the only question that matters from here: whether a 140-year-old service organization can be run with the discipline of a Danaher factory, and whether the AI cooling boom that is lifting its backlog is a decade-long structural shift or a cyclical spike that will one day break the wrong way. The transformation of the portfolio is finished. The transformation of the operations — the one the market is now paying a premium to bet on — has only just begun.

References

-

Johnson Controls Reports Fourth Quarter and Fiscal Year 2024 Results — PR Newswire, 2024-11-06 ↩↩↩

-

Johnson Controls Appoints Joakim Weidemanis as Chief Executive Officer — Johnson Controls Press Release, 2025-02-05 ↩↩↩

-

Johnson Controls Completes Sale of Residential and Light Commercial HVAC Business to Bosch — Johnson Controls Press Release, 2025-08-01 ↩↩↩

-

Johnson Controls to Host "Going to Gemba Day" to Introduce Strategy and Business System — Johnson Controls Press Release, 2026-06-01 ↩

-

Johnson Controls Completes Acquisition of Alloy Enterprises — Johnson Controls Press Release, 2026-05-13 ↩↩

-

Johnson Controls Announces Sale of Power Solutions to Brookfield for $13.2 Billion — Reuters, 2018-11-13 ↩↩

-

Johnson Controls and Tyco to Merge in Tax Inversion Deal — New York Times, 2016-01-25 ↩↩

-

Elliott Management Builds $1 Billion Stake in Johnson Controls — Bloomberg, 2024-05-20 ↩↩↩↩↩

-

Johnson Controls Acquires Silent-Aire to Expand Data Center Platform — JCI Press Release, 2021-04-12 ↩

-

Johnson Controls Reports Q4 and FY25 Results; Initiates FY26 Guidance — PR Newswire, 2025-11-14 ↩↩↩

-

Johnson Controls Reports Strong Q2 Results; Raises FY26 Guidance — PR Newswire, 2026-05-06 ↩↩↩↩

-

Johnson Controls Reports Strong Q2 Results; Raises FY25 Guidance — PR Newswire, 2025-05-07 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube