J.B. Hunt: The Handshake That Rewired American Logistics

I. The Tease & The Thesis (0:00 – 0:15)

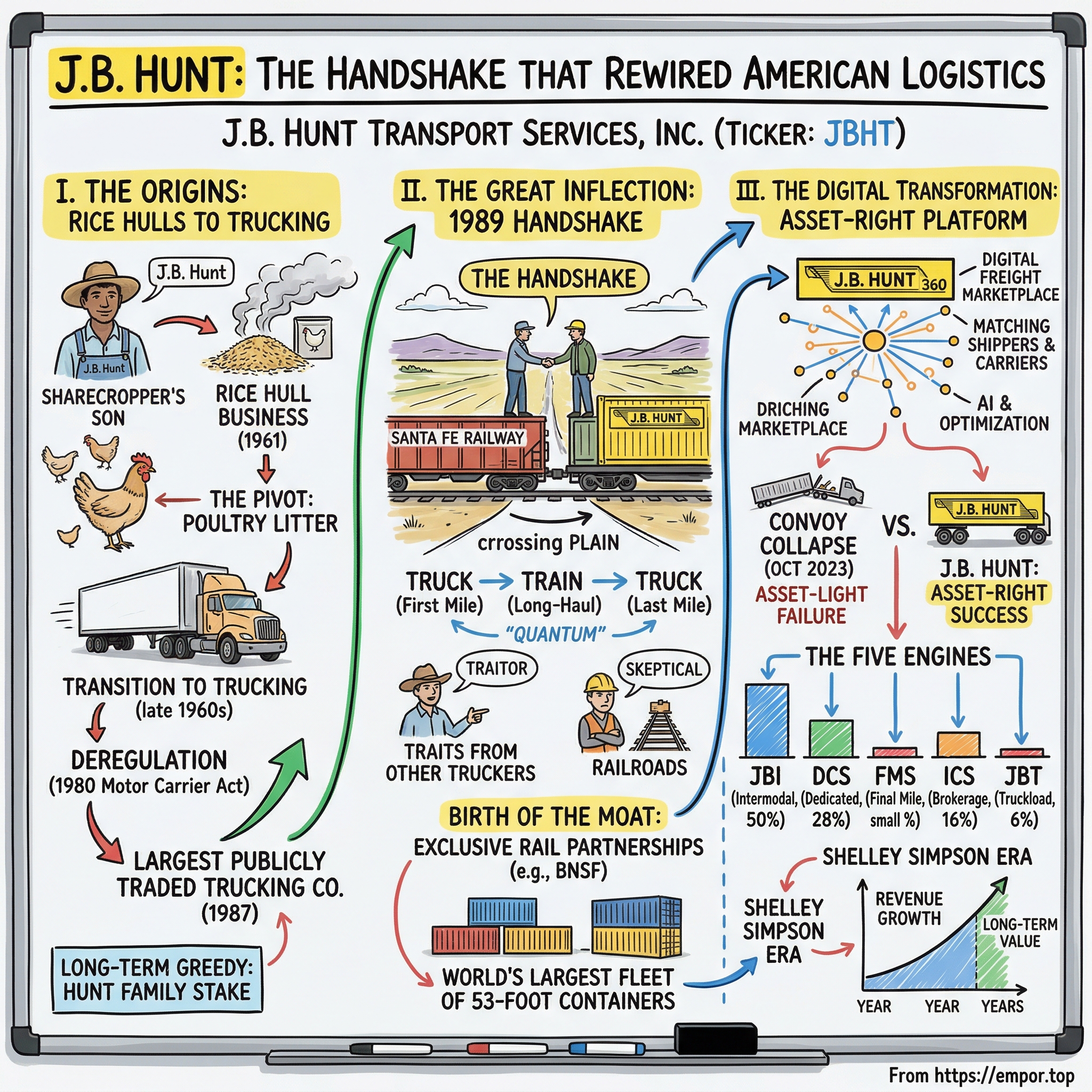

🎙 The Hook: A Handshake on a Moving Train

Picture a November afternoon in 1989. A freight train hurtles across the Kansas plains, bound from Chicago to Kansas City. Aboard that train sit two men who, by every measure of their respective industries, should be enemies.

One is Johnnie Bryan Hunt — a seventh-grade dropout turned trucking magnate who built one of the largest fleets in America. The other is Mike Haverty, the president of the Atchison, Topeka & Santa Fe Railway.

For a hundred years, trucks and trains had fought a brutal, zero-sum war for the soul of American freight. Railroads called truckers parasites. Truckers called railroads dinosaurs. Shippers played them against each other, and the American highway system groaned under the weight of eighteen-wheelers burning diesel from coast to coast.

But on that train, J.B. Hunt turned to Haverty and proposed something that the entire trucking industry would call insane: put my trailers on your trains. Let's stop fighting and start collaborating. Haverty extended his hand, and they shook on it.

That single handshake — sealed on a moving railcar somewhere between Chicago and Kansas City — would create the modern intermodal freight industry, save billions of gallons of diesel fuel, pull millions of truck loads off American highways, and turn a scrappy Arkansas trucking company into a twenty-billion-dollar logistics platform. The trucking industry was furious. Competitors called J.B. Hunt a traitor. The railroads were skeptical. Wall Street was confused. And yet, thirty-six years later, that handshake remains the most consequential strategic decision in the history of American surface transportation.

The Thesis: Not a Trucking Company

Here is the thing most people get wrong about J.B. Hunt Transport Services: they think it is a trucking company. The yellow trucks, the highway presence, the ticker symbol JBHT sitting on the NASDAQ alongside other transportation names — it all screams "trucking." But calling J.B. Hunt a trucking company is like calling Amazon a bookstore. The traditional truckload business — the segment most people associate with the J.B. Hunt name — now represents barely six percent of the company's twelve billion dollars in annual revenue. The real J.B. Hunt is something far more interesting and far harder to replicate.

It is a multi-modal logistics platform built on a cornered resource: exclusive access to the American rail network through partnerships that took decades to construct and that no competitor can simply duplicate.

It operates the largest fleet of fifty-three-foot intermodal containers in the world — over 120,000 of them — which function as portable warehouses that can move seamlessly between a truck chassis and a railcar. It runs a digital freight marketplace called J.B. Hunt 360 that matches shippers with carriers using artificial intelligence, processing millions of transactions annually.

And it embeds itself so deeply into the supply chains of Fortune 500 companies through dedicated contract services that switching away from J.B. Hunt would require a client to essentially rebuild their entire distribution operation from scratch.

The journey from rice hulls to the rails to a technology platform is one of the great multi-generational reinvention stories in American business. From a small town in Arkansas with a population of roughly ten thousand when the Hunts started, to the invisible backbone of how goods move across the continent — this is the J.B. Hunt story.

Episode Roadmap

The story unfolds in three acts.

The first act is the origin — a sharecropper's son who spotted value in discarded rice hulls, built a poultry litter empire, pivoted into trucking, and rode the deregulation wave of 1980 to become the largest publicly traded trucking company in America within seven years of going public.

The second act is the great inflection — the 1989 handshake that created the intermodal industry, the decades-long construction of an unbreakable rail partnership, and the assembly of the world's largest fleet of fifty-three-foot containers.

The third act is the digital transformation — a half-billion-dollar bet on a technology platform that turned a trucking company into a software-enabled logistics marketplace, validated by the spectacular failures of the venture-backed startups that tried to disrupt it.

Along the way, there are acquisitions, leadership transitions, a founding family that never sold, and the quiet construction of the most defensible competitive position in American freight. The narrative threads together what the company calls the "Asset-Right" model — neither fully asset-heavy like a traditional carrier nor asset-light like a pure broker, but something in between that combines the credibility of physical infrastructure with the scalability of a technology platform.

II. The Origins: Rice Hulls & The "Asset-Light" DNA (0:15 – 0:35)

🎙 The Sharecropper's Son

Johnnie Bryan Hunt was born on February 28, 1927, in Cleburne County, near Heber Springs, Arkansas. His parents were sharecroppers — tenant farmers working someone else's land for a fraction of the harvest. J.B., as everyone called him, left school after the seventh grade to work at his uncle's sawmill. He picked cotton. He sold lumber. He did whatever it took to survive in Depression-era rural Arkansas, where opportunity was measured not in degrees or connections but in sheer physical willingness to outwork everyone around you.

After a stint in the U.S. Army, Hunt spent the 1950s bouncing between jobs — lumber salesman, auctioneer, truck driver for a company called Superior Forwarding. He was, by all accounts, a born salesman with an almost preternatural ability to spot value where others saw waste. There is a particular quality shared by the great Arkansas entrepreneurs of that era — Sam Walton, Don Tyson, J.B. Hunt — a kind of hardscrabble resourcefulness born from growing up in a place where nothing was handed to you and everything had to be earned, bargained for, or improvised from whatever was lying around. Hunt had that quality in abundance.

Literally. One day in the late 1950s, while driving his truck through Stuttgart, Arkansas — the rice capital of America — Hunt noticed something that would change his life. Rice farmers were burning their post-harvest hulls in open fields. Thick plumes of smoke rose from thousands of acres of discarded organic material. The air reeked of smoldering grain waste. To the farmers, the hulls were garbage, a nuisance to be eliminated before the next planting season. To J.B. Hunt, peering through his truck windshield at those smoldering fields, they were gold.

The First Pivot: Poultry Litter

Hunt realized that rice hulls could serve as a cheap substitute for sawdust in the booming Arkansas poultry industry. Chicken farmers needed bedding material — something absorbent and disposable to line the floors of their enormous poultry houses. Sawdust worked, but it was expensive. Rice hulls were free. All you needed was a way to collect them and deliver them.

In 1961, J.B. and his wife Johnelle pooled three thousand dollars and launched a rice hull business. The first year was a disaster — they lost nineteen thousand dollars, a staggering sum for a couple scraping by in rural Arkansas. But they kept going. Within a few years, their operation had become the largest producer of poultry litter in the world.

The rice hull business was, in its own unglamorous way, the prototype for everything J.B. Hunt would become: find an inefficiency in a supply chain, build a logistics solution around it, and scale relentlessly.

Johnelle Hunt deserves far more credit than she typically receives in the telling of this story. She was not simply "the wife." She managed the books, made operational decisions, and later served on the board of directors. The company's official name — J.B. Hunt Transport Services — bears his initials, but insiders have always understood that this was a partnership in the truest sense. If J.B. was the salesman and the visionary, Johnelle was the operator and the steward — the one who made sure the money was tracked, the bills were paid, and the business did not outrun its cash flow. In the decades that followed, she would become one of the wealthiest self-made women in Arkansas and one of the state's most prominent philanthropists, but in the early 1960s, she was balancing the books of a poultry litter business that had just lost six times its initial investment in year one.

The Transition to Trucking

By the late 1960s, the Hunts had trucks running all over Arkansas delivering poultry litter. In 1969, J.B. purchased a small trucking operation — five tractors, seven trailers — initially just to support the rice hull business. But Hunt quickly recognized that the trucking operation had far more upside than the commodity it was hauling. Through the 1970s, the trucking arm grew steadily, though it remained a regional operation hemmed in by the regulatory straightjacket of the era. Before 1980, entering the interstate trucking market required navigating a Byzantine system of federal permits, rate bureaus, and geographic restrictions. Routes were assigned by regulators. Prices were fixed by committees. Innovation was, by design, nearly impossible.

Then came the Motor Carrier Act of 1980, signed by President Carter on July 1 of that year. This single piece of legislation deregulated the American trucking industry overnight. Rate controls vanished. Geographic restrictions evaporated. The number of licensed carriers more than doubled to over forty thousand by 1990.

For incumbent carriers who had grown fat under regulatory protection, deregulation was an extinction event. Hundreds of established trucking companies went bankrupt in the years that followed, unable to compete on price and service in an open market. But for hungry, aggressive operators like J.B. Hunt, deregulation was the starting gun. The act saved shippers an estimated 15.4 billion dollars annually by 1985 through lower rates and faster service — and operators who could deliver that efficiency captured enormous market share.

Hunt seized the moment with ferocious energy. By 1983, the fleet had grown to 550 tractors and over a thousand trailers, with roughly 1,050 employees. That same year, on November 22, 1983, the company went public on the NASDAQ. At the time of the IPO, J.B. Hunt ranked as the eightieth-largest trucking firm in the United States. The capital markets gave J.B. Hunt rocket fuel. With public equity to fund fleet expansion and acquisitions, the company grew at a pace that stunned the industry. By 1987 — just four years after the IPO — it was the largest publicly traded trucking company in America. The growth was staggering, fueled by deregulation, aggressive pricing, and a cultural intensity that bordered on fanatical.

It is worth pausing on that trajectory. Going from the eightieth-largest carrier to number one in four years, in an industry with over forty thousand competitors, is almost unheard of. The deregulation tailwind helped, certainly — but dozens of other carriers had the same tailwind. What set J.B. Hunt apart was an obsessive focus on operational efficiency and a willingness to invest in technology at a time when most trucking companies were still dispatching loads by telephone and tracking shipments with paper logs. Hunt was among the first carriers to equip trucks with satellite tracking systems and to use computer-aided dispatch. In a business where most operators managed their fleets by gut feel and relationships, J.B. Hunt was already building the data-driven culture that would define its future.

But even as the fleet expanded, J.B. Hunt the man was already seeing the ceiling. Pure truckload freight — loading a trailer, driving it across the country, unloading it, driving back empty — was a commodity business with razor-thin margins and brutal driver turnover. Annual driver turnover in the truckload industry regularly exceeded one hundred percent — meaning the average carrier had to replace its entire driver workforce every year. Every competitor with enough capital to buy a truck and hire a driver could undercut you. "Hauling everything yourself," as Hunt reportedly told colleagues, "is a race to the bottom."

In 1983, Hunt sold the rice hull operation entirely to focus on trucking. But even as he went all-in on trucks, he was already plotting an escape from the commodity trap. The DNA of the rice hull business — finding waste in a system and monetizing it — was about to express itself in a far more dramatic way.

The Family Stake: Long-Term Greedy

One detail that deserves attention here, because it shapes everything that follows: J.B. Hunt passed away in 2006, but the Hunt family never sold.

Johnelle Hunt, now in her nineties, personally holds approximately 17.7 million shares of JBHT stock — roughly an eighteen-and-a-half percent stake in the company, worth north of two and a half billion dollars at recent prices. When insiders and family trusts are included, the total family ownership exceeds twenty percent. The free float is approximately seventy-nine percent of outstanding shares, meaning the Hunt family remains the single largest shareholder by a wide margin.

This is not a company where the founders cashed out and moved on. This is a company where the founding family still sits at the table with a massive, concentrated, illiquid position. That creates a fundamentally different incentive structure than you see at most public companies. There is no pressure to goose quarterly earnings at the expense of long-term positioning. There is no activist investor threatening a proxy fight to force a special dividend.

The Hunt family's continued stake functions as a kind of gravitational anchor, keeping management focused on compounding value over decades rather than quarters. Warren Buffett would call it "long-term greedy." It is one of the underappreciated reasons why J.B. Hunt has been able to make bold, contrarian bets — like the one that was about to change everything.

III. The Great Inflection: The 1989 Santa Fe Handshake (0:35 – 1:10)

🎙 The Hundred-Year War

To understand why J.B. Hunt's decision to partner with a railroad was so shocking, you have to understand the depth of the animosity between the two industries.

The rivalry between trucks and trains in American freight is one of the longest-running competitive wars in business history, stretching back to the early twentieth century when the first motorized trucks began stealing short-haul freight from railroads. By mid-century, the Interstate Highway System — built with federal dollars starting in 1956 — tilted the playing field decisively toward trucking.

Railroads, burdened by legacy costs, labor agreements, and aging infrastructure, watched their market share erode decade after decade. Truckers viewed railroads as bloated, slow, and irrelevant. Railroad executives viewed truckers as subsidized interlopers riding on taxpayer-funded highways. The two industries lobbied against each other in Washington. They competed for the same freight on the same corridors. They did not collaborate. Ever.

This was not just business competition — it was cultural identity. Trucking companies hired military veterans and blue-collar workers who took pride in the independence and freedom of the open road. The trucker was an American archetype — the lone cowboy of commerce, master of his rig, beholden to no one but the open highway. Railroads, by contrast, were old-money institutions with corporate hierarchies, union contracts, and a patrician aura that truck drivers instinctively distrusted. The two industries even competed politically, with trucking lobbies fighting for highway funding while railroad interests lobbied for regulations that would limit trucking competition. The idea that a trucker would voluntarily put his trailers on a competitor's railcars was, to most of the industry, somewhere between absurd and treasonous. It would be as if Coca-Cola proposed distributing Pepsi through its bottling network.

The Crazy Idea

By the late 1980s, J.B. Hunt was generating hundreds of millions in revenue but facing the structural problem that haunted every truckload carrier: long-haul freight was punishingly inefficient. A truck driving from Los Angeles to Chicago burned enormous quantities of diesel, wore out tires and engines, and required a driver to spend days away from home — all to move a single trailer of goods that could theoretically travel the same distance on a railcar at a fraction of the fuel cost.

The math was inescapable. A train can move one ton of freight approximately four hundred miles on a single gallon of diesel. A truck can move that same ton about 130 miles. On a long-haul corridor like Los Angeles to Chicago, rail was three times more fuel-efficient.

But railroads had their own problem. They could not handle the "first mile" and "last mile" — picking up freight from a shipper's warehouse and delivering it to the receiver's door. Rail terminals were fixed in location. Trains ran on schedules, not on demand. And railroad companies had no customer service infrastructure to deal with individual shippers the way trucking companies did. Trucks excelled at those short, flexible, point-to-point movements. What if you combined the best of both?

Mike Haverty, then president of the Santa Fe Railway, was one of the few railroad executives willing to entertain the idea. Haverty was a pragmatist who understood that the railroad industry's obsession with fighting truckers was costing both sides. He would later go on to become CEO of Kansas City Southern and win Progressive Railroading's Railroad Innovator Award — a man who saw the future of freight before almost anyone else in the rail industry.

Haverty invited J.B. Hunt aboard Intermodal Train No. 198, the service running from Chicago toward Kansas City. The legendary meeting unfolded exactly as it sounds — two men from rival industries, riding together on a freight train, talking through the logistics of how a truck trailer could be lifted onto a flatcar, hauled a thousand miles by rail, and then transferred back to a truck chassis for final delivery. The rumble of the train beneath them, the Kansas prairie stretching to the horizon outside the windows — it was the kind of scene that Hollywood would struggle to make dramatic, but that changed an entire industry.

They shook hands. The formal contract was signed in June 1991, launching a service they called Quantum — the first premium domestic intermodal shipping service in American history.

The arrangement was elegantly simple. J.B. Hunt would handle the pickup and delivery on both ends using its trucks — the "first mile" from the shipper's dock to the rail terminal and the "last mile" from the destination terminal to the receiver's warehouse. Santa Fe (later BNSF after the 1995 merger with Burlington Northern) would haul the freight across the long-distance corridor by rail. Revenue would be shared between the two companies — a structure that was virtually unprecedented in transportation.

To visualize how this works in practice: imagine a manufacturer in Los Angeles needs to ship a container of goods to a retailer in Chicago. A J.B. Hunt truck picks up the loaded container from the manufacturer's warehouse, drives it to a BNSF rail terminal in Southern California, and drops it off. A crane lifts the container onto a railcar. The train carries it roughly two thousand miles to a BNSF terminal near Chicago — a journey that takes about two days by rail versus four to five days by truck. At the Chicago terminal, another crane lifts the container off the railcar and places it on a J.B. Hunt truck chassis. A local J.B. Hunt driver delivers it to the retailer's distribution center. The shipper gets one bill, one point of contact, and door-to-door service at a price point significantly below what a full truckload haul would cost.

The Industry Backlash

The reaction from the trucking industry was immediate and vicious. Competitors accused J.B. Hunt of betraying the entire industry. "J.B. is selling his soul to the railroads" became a common refrain at industry conferences and in trade publications.

Other trucking CEOs viewed the deal as an existential threat — if the largest trucker in America was admitting that rail was more efficient for long-haul, what did that say about everyone else's business model? It was an uncomfortable mirror being held up to an entire industry's economics, and the industry did not like what it saw.

Owner-operators were particularly hostile. They saw intermodal as a direct attack on their livelihoods, replacing long-haul truck routes with rail corridors that would eliminate thousands of driving jobs. At truck stops across America, the J.B. Hunt name went from respected to reviled almost overnight.

But J.B. Hunt did not care about industry popularity. He cared about margins. And the economics of intermodal were devastating to the old model. By eliminating hundreds of miles of over-the-road trucking on each load, intermodal reduced fuel costs, lowered insurance liability, decreased wear on equipment, and — critically — addressed the industry's chronic driver shortage by replacing long, lonely cross-country hauls with shorter pickup-and-delivery runs that allowed drivers to sleep in their own beds at night. For shippers, intermodal offered a price point roughly fifteen to twenty-five percent below full truckload rates, with transit times that were competitive on corridors longer than roughly five hundred miles. And for the environment, the math was equally compelling: shifting freight from truck to rail reduced carbon emissions by approximately sixty-five percent per ton-mile.

The early years were not without friction. Intermodal service quality was inconsistent. Railroads were not accustomed to the time-sensitivity that shippers expected from trucking service. Trains ran on the railroad's schedule, not the shipper's schedule, and damage rates on rail were higher than on truck. J.B. Hunt had to invest heavily in container design, tracking technology, and operational processes to bring intermodal service quality up to the standard that its shipper customers demanded. The Quantum service — the premium offering that emerged from the partnership — was specifically designed to address these issues, offering guaranteed transit times and enhanced visibility that made intermodal competitive not just on price but on reliability.

The Birth of the Moat

This is the moment when J.B. Hunt stopped being a trucking company and became something else entirely. The intermodal partnership was not just a new product line — it was the construction of a moat. Here is why: railroads do not take on intermodal partners casually. There are only seven Class I railroads in North America, and they operate on fixed infrastructure that took over a century to build. You cannot simply call up BNSF and say, "We would like to be your intermodal partner." BNSF already has one: J.B. Hunt. That relationship, now in its thirty-sixth year, functions as a de facto exclusive partnership in the western United States. On the eastern side, J.B. Hunt works with Norfolk Southern and CSX, but the BNSF relationship is the crown jewel — covering the dense freight corridors from the West Coast ports through the heartland to Chicago and beyond.

When Burlington Northern merged with Santa Fe in 1995 to form BNSF, the J.B. Hunt partnership not only survived but deepened. When Berkshire Hathaway acquired BNSF in 2010, making Warren Buffett the owner of J.B. Hunt's most critical rail partner, the relationship deepened further still. There is a delicious irony in the fact that the Oracle of Omaha — the most famous long-term investor in the world — ended up owning the railroad that is structurally intertwined with J.B. Hunt's business. Buffett bought BNSF because he believed in the long-term economics of rail freight. J.B. Hunt's intermodal business is one of the primary reasons those economics are so attractive.

In 2023, J.B. Hunt purchased the brokerage assets of BNSF Logistics, and the two companies jointly relaunched the "Quantum" service — a premium intermodal offering with dedicated oversight teams working twenty-four-seven at BNSF's Fort Worth headquarters, providing customized transit times and performance guarantees for each customer. In 2025, they expanded internationally with "Quantum de Mexico," partnering with Mexican rail company GMXT to extend the intermodal network south of the border.

The compounding nature of this relationship cannot be overstated. Every year that J.B. Hunt and BNSF work together, the switching costs for both parties increase. J.B. Hunt has invested billions in intermodal containers specifically designed for BNSF's infrastructure. BNSF has allocated rail capacity and terminal space to accommodate J.B. Hunt's volumes.

Untangling this partnership would be like trying to separate two trees whose roots have grown together over three decades. This is not a vendor relationship. It is a structural merger of capabilities that happens to be organized across two separate corporate entities.

For any competitor hoping to replicate what J.B. Hunt has built, the message is simple: you are thirty-six years too late. You would need to simultaneously build a relationship with a Class I railroad, invest billions in containers and chassis, develop the technology to manage intermodal operations at scale, and convince thousands of shippers to switch their supply chains — all while the incumbent has decades of operational data, customer relationships, and institutional trust that cannot be purchased at any price. The intermodal partnership is not just J.B. Hunt's competitive advantage. It is J.B. Hunt's reason for existence.

IV. The Modern Pivot: J.B. Hunt 360 & The Digital Moat (1:10 – 1:50)

🎙 The Hidden Software Company

Walk into J.B. Hunt's headquarters in Lowell, Arkansas — a 250,000-square-foot campus nestled in the Ozark foothills, with executive offices and a boardroom on the top floor of a four-story building — and you might expect to find the culture of a traditional trucking operation. Dispatch boards. Paper manifests. Coffee-stained route maps pinned to corkboards. Grizzled dispatchers barking into telephones.

Instead, you find something that looks more like a tech startup. Engineers cluster around screens running real-time optimization algorithms. Data scientists analyze freight flow patterns. Product managers iterate on user interfaces. The campus houses approximately three thousand employees, and a rapidly growing share of them have never driven a truck or loaded a trailer. They write code.

In April 2017, at the company's annual shareholder meeting, J.B. Hunt announced a commitment that stunned the transportation industry: five hundred million dollars in technology investment over five years. The breakdown was revealing — two hundred and twenty-three million for "creative innovation and disruptive technology," one hundred and forty-one million to modernize existing infrastructure, and one hundred and thirty-six million to enhance operating systems. For a company that most investors still classified as a trucking stock, half a billion dollars in tech spending was a bold declaration of identity. J.B. Hunt was telling the market: we are building a platform.

The product that emerged from that investment was J.B. Hunt 360 — a digital marketplace that fundamentally reimagined how freight gets matched with capacity. To understand what 360 does, it helps to understand the chaos it replaced. Before digital freight matching, the process of connecting a shipper who needed to move goods with a carrier who had an available truck worked roughly like this: the shipper's logistics manager would call a freight broker, who would call another broker, who would call a dispatcher, who would call truck drivers on their cell phones until someone said yes. The process could take hours or even days. Pricing was opaque. Visibility into the load's location was minimal. And the entire system was held together by personal relationships and phone calls — a fragmented, inefficient, deeply analog process that had not fundamentally changed since the invention of the telephone.

J.B. Hunt 360 replaced all of that with a two-sided digital marketplace, similar in concept to what Uber did for ride-hailing or Airbnb did for lodging, but applied to the vastly more complex world of freight logistics. On one side, shippers — the companies that need to move goods — post available loads with details about origin, destination, weight, timing, and special requirements. On the other side, carriers — the truck operators with available capacity — browse and bid on those loads. The platform uses artificial intelligence and machine learning to optimize matches, considering factors like carrier location, equipment type, historical performance, and real-time traffic patterns. Pricing is transparent. Booking is instant. Tracking is real-time. The entire transaction that used to require a chain of phone calls can now happen in minutes on a screen.

The "Empty Miles" Problem

To understand why 360 matters, you need to understand the single most wasteful phenomenon in American freight: empty miles. In the trucking industry, approximately thirty-five percent of all miles driven by trucks in the United States are "deadhead" miles — trucks running empty, without any freight, repositioning to their next pickup. Imagine if thirty-five percent of all airline flights took off with zero passengers. That is the scale of inefficiency that the freight industry has lived with for decades. Every empty mile burns diesel, wears out equipment, wastes a driver's time, and contributes to highway congestion and carbon emissions — all while generating zero revenue.

J.B. Hunt 360 attacks this problem directly. By creating a real-time digital marketplace where available loads and available trucks are visible to each other, the platform dramatically reduces the time and distance a truck must travel empty between loads. Since its launch, 360 has saved over 13.5 million empty miles on company equipment alone. But the real genius of the platform is that it does not just serve J.B. Hunt's own fleet. It is open to third-party carriers — independent trucking companies and owner-operators who can use the platform to find loads near their current location, reducing their own deadhead miles while simultaneously expanding the pool of capacity available to J.B. Hunt's shipper customers.

This creates a classic network effect flywheel. More shippers posting loads attract more carriers to the platform. More carriers mean better coverage, faster matching, and lower prices, which attract more shippers. The flywheel spins faster with each revolution.

And at the center of the flywheel sits J.B. Hunt, collecting transaction fees on every match while also having its own massive fleet as a backstop. If no third-party carrier is available for a particular load, J.B. Hunt can assign one of its own trucks. This is the "Asset-Right" model in action — the critical advantage that J.B. Hunt holds over the pure-play digital brokers that attempted to disrupt the industry.

Consider the difference. Uber Freight can match loads with carriers on a screen, but it does not own a single truck. When capacity gets tight — as it inevitably does during peak seasons, weather events, or supply chain disruptions — Uber Freight has nothing to fall back on. It is at the mercy of whatever carriers happen to be available and willing. J.B. Hunt, by contrast, has thousands of its own trucks, over 120,000 containers, and exclusive rail partnerships. It can always cover a load. That guarantee of capacity is worth enormous amounts to shippers who cannot afford to have their freight stranded.

The Convoy Cautionary Tale

The ultimate vindication of J.B. Hunt's "asset-right" approach came in October 2023, when Convoy — the Seattle-based digital freight broker backed by Jeff Bezos, Bill Gates, and some of the most prestigious venture capital firms in Silicon Valley — abruptly shut down. Convoy had raised over two hundred and sixty million dollars and reached a valuation of 3.8 billion at its peak. It was supposed to be the company that would disrupt old-school freight brokers like J.B. Hunt and C.H. Robinson by building a pure technology platform with no physical assets.

Instead, Convoy was burning ten million dollars per month and could not sustain operations when the freight market softened. Gross revenues had plummeted from eight hundred million dollars in 2021 to a five-hundred-million-dollar run rate by 2023. The company closed without even filing for formal bankruptcy, leaving roughly four hundred carriers owed 2.6 million dollars in unpaid loads. IKEA subsequently sued Convoy over unpaid carrier claims.

The message was unmistakable: in freight logistics, technology alone is not enough. You need trucks. You need containers. You need rail partnerships. You need the physical infrastructure that takes decades and billions of dollars to build. J.B. Hunt had all of that, plus the technology. Convoy had the technology, and nothing else.

The company doubled its engineering and technology headcount to support 360, integrated real-time visibility tools from partners like project44, and continued investing in AI-driven optimization. Today, 360 processes transactions across all five of J.B. Hunt's business segments, functioning as the connective tissue of the entire operation. What began as a digital brokerage tool has evolved into the central nervous system of a twelve-billion-dollar logistics enterprise.

The Myth vs. Reality of "Disruption"

There is a popular narrative in technology circles that incumbent industries are always vulnerable to disruption by nimble startups with superior technology. In many industries, that narrative holds true. In freight logistics, it has proven spectacularly wrong. The reason comes down to what might be called the "physical layer" problem. Freight is not like music or media or advertising — it cannot be fully digitized. At the end of every digital transaction, someone still has to load a physical object onto a physical truck and drive it to a physical destination. The companies that understood this — that technology is a necessary but not sufficient condition for success in logistics — are the ones that survived and thrived. J.B. Hunt understood it. Convoy did not.

The Uber Freight comparison is also instructive. Uber Freight launched in 2017 with the full weight of Uber's brand, engineering talent, and venture capital backing. It remains operational as of early 2026, but it has not achieved sustained profitability in freight brokerage and continues to compress industry take rates without demonstrating a path to durable competitive advantage. The fundamental problem is the same one Convoy faced: without owned assets, a digital broker is a middleman with a nice app. When the freight market tightens, carriers do not need the app to find loads — loads find them. When the market loosens, shippers do not need the app to find cheap trucks — cheap trucks are everywhere. The app adds value at the margins but does not create the kind of structural competitive advantage that sustains pricing power through cycles. J.B. Hunt's 360 platform avoids this trap because it is embedded in a company that also owns 120,000-plus containers, operates over eleven thousand dedicated trucks, and controls exclusive access to the western rail network. The technology amplifies the physical assets. The physical assets validate the technology. Neither alone would be sufficient.

V. Segment Deep Dive: The Five Engines (1:50 – 2:20)

🎙 A Company of Five Companies

Understanding J.B. Hunt requires understanding that it is not one business but five, each with distinct economics, competitive dynamics, and growth trajectories. The way these five segments interact — sharing data through 360, cross-selling services to the same customers, and leveraging shared infrastructure — is what makes the whole greater than the sum of its parts.

JBI (Intermodal): The Crown Jewel

Intermodal is the segment born from that 1989 handshake, and it remains the engine that drives the entire enterprise.

In fiscal year 2025, JBI generated roughly six billion dollars in revenue — approximately half of the company's total — making it by far the largest segment. Operating income came in at about four hundred and fifty million dollars, representing an operating margin of approximately seven and a half percent. That margin might seem modest compared to, say, a software company, but in the capital-intensive world of transportation, it represents a substantial premium over the typical truckload carrier.

The physical asset base is extraordinary. J.B. Hunt owns over 120,000 fifty-three-foot intermodal containers — the largest company-owned fleet of its kind in North America. To put that in perspective, these containers, if lined up end to end, would stretch over a thousand miles.

Each one is essentially a portable warehouse: a standardized steel box that can be loaded at a shipper's dock, placed on a truck chassis for the first-mile drive to a rail terminal, lifted onto a railcar for the long-haul segment, and then transferred back to a truck chassis for final delivery.

The company also owns over 85,000 chassis — the wheeled undercarriages that allow containers to be towed by trucks. Together, the container and chassis fleet represents the physical embodiment of the BNSF partnership and billions of dollars in invested capital that no competitor can replicate overnight.

The company has set a target of expanding to 150,000 containers by 2027, boosted in part by the 2024 acquisition of roughly 15,500 intermodal trailers from Walmart as part of a multi-year service agreement.

That Walmart deal is worth pausing on. When the world's largest retailer hands its intermodal container fleet to you and signs a long-term service agreement, it is a powerful endorsement of your operational capabilities. It also illustrates a broader trend: major shippers are increasingly concluding that managing their own intermodal operations is not a core competency and that J.B. Hunt can do it better and cheaper.

This "insourcing to J.B. Hunt" dynamic is a secular growth driver for the intermodal segment that transcends the freight cycle.

Intermodal holds roughly a twenty percent share of the approximately twenty-five-billion-dollar North American intermodal market. The company moves over two million loads per year — a milestone first reached in 2018.

But even at that scale, intermodal remains underpenetrated relative to total long-haul freight volumes. Industry estimates suggest that only about ten to fifteen percent of freight that could economically move by intermodal actually does so today, with the remainder still traveling by over-the-road truck. The opportunity for modal conversion — shifting freight from truck to rail — remains enormous, and J.B. Hunt is the primary beneficiary of every incremental load that converts.

DCS (Dedicated Contract Services): The Switching Cost Machine

If Intermodal is the crown jewel, Dedicated Contract Services is the quiet fortress. DCS generated approximately 3.4 billion dollars in revenue in fiscal 2025 with an operating margin of around eleven percent — the highest margin of any segment. The concept is deceptively simple: J.B. Hunt provides an entire private fleet to a major shipper — trucks, drivers, routing technology, maintenance, compliance — all managed by J.B. Hunt but painted in the customer's colors and dedicated exclusively to that customer's freight.

Think of it this way: if you are a company like Walmart, Home Depot, or any Fortune 500 manufacturer, you face a choice. You can build and manage your own private truck fleet — hiring drivers, maintaining vehicles, navigating federal safety regulations, managing insurance, dealing with driver turnover that regularly exceeds ninety percent annually in the trucking industry — and accept that fleet management is now one of your core competencies, even though it has nothing to do with your actual products.

Or you can hand all of that to J.B. Hunt and let them run it for you. The trucks carry your logo. The drivers wear your uniform. From the outside, it looks like your fleet. But every truck, every driver, every route optimization, every maintenance schedule, every compliance filing is managed by J.B. Hunt. You get the benefit of a private fleet without the headache of operating one.

The switching costs in DCS are enormous. Once J.B. Hunt embeds itself in a customer's supply chain — optimizing routes, training drivers on specific warehouse procedures, integrating technology systems, building customized reporting dashboards — the cost and disruption of switching to a competitor is so high that customers almost never leave.

Consider what a switch would entail. The customer would need to find a new provider, negotiate a new contract, rehire and retrain hundreds of drivers who know the specific loading procedures at each warehouse, redeploy all technology integrations, rebuild years of routing optimization data, and endure weeks or months of service degradation during the transition — all while their products need to keep moving. The pain of switching is so much greater than the pain of staying that customers effectively lock themselves in.

This is not a transactional business where a shipper shops for the lowest price each week. It is a deeply integrated operational partnership, typically governed by multi-year contracts. DCS currently operates over eleven thousand company-owned trucks and more than twenty-one thousand pieces of trailing equipment dedicated to individual customers.

FMS (Final Mile Services): The E-Commerce Bet

Final Mile is the segment that most clearly reflects J.B. Hunt's bet on the future of e-commerce. Launched as a standalone segment in 2017 through the acquisition of Special Logistics Dedicated for one hundred and thirty-six million dollars, FMS focuses on the delivery of heavy and bulky items — appliances, furniture, exercise equipment, large electronics — directly to consumers' homes. This is the "last mile" problem that every e-commerce company struggles with: getting a three-hundred-pound refrigerator from a distribution center to a customer's kitchen, assembled and installed, without damaging the product or the customer's home.

J.B. Hunt built FMS through a series of acquisitions. In 2019, the company acquired Cory 1st Choice Home Delivery, a New Jersey-based last-mile specialist, for one hundred million dollars, expanding its footprint in the Northeast. Shortly after, it acquired RDI Last Mile, a furniture and appliance delivery company, for an undisclosed sum. These acquisitions were deliberate — J.B. Hunt was buying capabilities and geographic coverage, not just revenue.

The segment grew from roughly three hundred million in revenue in 2017 to a peak of over nine hundred million by 2023 — a threefold increase in six years. The pandemic e-commerce boom supercharged this growth, as consumers stuck at home ordered furniture, appliances, and exercise equipment in record volumes, all requiring white-glove delivery to their doorsteps.

However, FMS has faced headwinds as the pandemic surge normalized. Revenue declined to eight hundred and twenty-four million in fiscal 2025, down about ten percent from the prior year. Operating margins compressed significantly, falling from about six and a half percent in 2024 to roughly three percent in 2025. The segment that once looked like a surefire growth engine now faces questions about its sustainable margin profile.

The question facing investors is whether FMS represents a long-term structural growth opportunity — heavy and bulky delivery is genuinely hard to do well, and few competitors have the national scale — or whether the segment's recent struggles signal that J.B. Hunt overpaid for these acquisitions. Compared to XPO, which operates a large last-mile delivery business with deeper experience in the category, J.B. Hunt's approach has been more disciplined on acquisition price but arguably slower to achieve the scale economics needed to generate consistent profitability. The jury remains out, but the secular trend of consumers ordering larger items online shows no sign of reversing.

ICS (Integrated Capacity Solutions) & JBT (Truckload): The Supporting Cast

The final two segments — ICS, the freight brokerage arm, and JBT, the traditional truckload business — are smaller but strategically important.

ICS generated about 1.1 billion in revenue in fiscal 2025 and is the segment most directly powered by the 360 platform. ICS is essentially a digital brokerage operation where J.B. Hunt matches shipper freight with third-party carriers, earning a margin on each transaction.

The segment has been loss-making in recent years — posting a ten-million-dollar operating loss in 2025, though that was a dramatic improvement from the fifty-six-million-dollar loss in 2024. The trajectory matters more than the current level here. ICS is a business that thrives in tight freight markets when capacity is scarce and carriers command premium rates, and struggles in loose markets when excess capacity compresses broker margins. As the freight market recovers from the 2022-2025 downturn, ICS should be one of the first segments to benefit, with high operating leverage driving margin expansion on relatively fixed technology costs.

JBT, the legacy truckload segment, generated about seven hundred and thirty-four million in revenue with a modest three percent operating margin. This is the original business — the commodity trucking operation that J.B. Hunt himself recognized as a "race to the bottom" four decades ago. The company has steadily reduced its exposure to pure truckload freight, and JBT now represents barely six percent of total revenue. It functions primarily as a capacity backstop and a feeder of loads into other segments. But it serves an important strategic purpose: JBT ensures that J.B. Hunt can always say yes to a customer, even when the customer's freight does not fit neatly into intermodal or dedicated solutions. That "never say no" capability is a powerful customer retention tool.

The Revenue Mix Tells the Story

Step back and consider how dramatically the revenue composition has changed. In 1980, J.B. Hunt was one hundred percent truckload. Today, truckload is six percent. Intermodal — a business that did not exist at J.B. Hunt before 1989 — represents half of revenue. Dedicated, which offers the highest margins and stickiest customer relationships, accounts for about twenty-eight percent. Brokerage and Final Mile — both technology-enabled, relatively asset-light businesses — make up the remaining sixteen percent.

This migration from commodity trucking to a diversified, technology-enhanced logistics platform is the central strategic narrative of J.B. Hunt's forty-plus years as a public company. It did not happen through a single dramatic pivot but through a series of deliberate, compounding decisions — the intermodal handshake, the DCS build-out, the Final Mile acquisitions, the 360 investment — each of which moved the company further from its commodity roots and closer to the integrated platform it is today. The total consolidated revenue of approximately twelve billion dollars in fiscal 2025, with consolidated operating income of roughly 865 million, reflects a business that generates nearly a billion dollars in annual operating profit across five distinct engines, each with its own growth drivers and competitive dynamics.

VI. The Changing of the Guard: The Simpson Era (2:20 – 2:45)

🎙 From an Hourly Wage to the Corner Office

In 1994, a young woman from Arkansas walked into J.B. Hunt's headquarters and took a job as an hourly customer service representative. She answered phones. She processed paperwork. She earned an hourly wage in an industry that was overwhelmingly male and overwhelmingly uninterested in the career ambitions of entry-level employees. Her name was Shelley Simpson.

Thirty years later, on July 1, 2024, Simpson became the President and Chief Executive Officer of J.B. Hunt Transport Services — the first woman to lead the company in its sixty-three-year history. She was fifty-two years old.

Her ascent from hourly worker to CEO is not just an inspiring personal narrative; it is a strategic signal about what J.B. Hunt has become and where it is headed.

Simpson's career trajectory maps almost perfectly onto the company's own evolution. After nearly two years on the phones, she moved into management. By 2007, she had been tapped to help build and lead the Integrated Capacity Solutions segment — the freight brokerage arm that would eventually become the proving ground for J.B. Hunt's technology ambitions. As president of ICS, Simpson learned the brokerage business from the inside out: how to match loads with carriers, how to price capacity dynamically, how to use data to optimize a network. In 2011, she was appointed Chief Marketing Officer. In 2017, she became Chief Commercial Officer with direct oversight of the 360 platform's development and commercialization. By 2020, she had expanded into human resources, and in August 2022, she was named President, setting the stage for the CEO transition.

The fact that J.B. Hunt chose a leader whose formative experience was in brokerage and technology — not in driving trucks or managing a fleet — tells you everything about the company's identity. Simpson's appointment was not a break from the company's direction; it was the logical culmination of a twenty-year transformation. J.B. Hunt is now led by someone whose core expertise is in the very business model — digital freight matching, capacity optimization, customer integration — that defines the company's future.

The Leadership Pipeline

Simpson did not ascend in a vacuum. She was mentored by Kirk Thompson, who joined J.B. Hunt in 1973 at age nineteen as a bookkeeper — reportedly encouraged by Johnelle Hunt herself to finish his accounting degree at the University of Arkansas. Thompson served as President and CEO from 1987 to 2011, a tenure during which revenue grew from 286 million to 3.8 billion dollars and the market capitalization expanded from roughly five hundred million to 4.4 billion. Thompson transitioned to Executive Chairman in 2011, making way for John N. Roberts III, who oversaw the digital transformation and the launch of 360 during his tenure as CEO from 2011 to 2024. Roberts now serves as Chairman of the Board. Thompson moved to an Honorary Founding Director role in 2024.

This leadership pipeline — Thompson to Roberts to Simpson — represents an unusual level of institutional continuity. Each transition was planned years in advance, with the successor deeply embedded in the company's culture and strategy. There were no outside hires parachuted in from a competitor. No boardroom coups. No activist-driven management changes.

The transitions were organic, deliberate, and aligned with the company's evolving identity. Thompson was the operations builder who scaled the fleet and navigated the intermodal revolution. Roberts was the technology visionary who bet five hundred million on digital transformation. Simpson is the platform operator who grew up inside the brokerage and technology businesses that define the company's future. Each CEO reflected the company's identity at the time of their appointment — and each helped evolve that identity for the next generation.

Incentives and Alignment

Executive compensation at J.B. Hunt is structured in a way that reinforces the long-term orientation created by the Hunt family's ownership stake. Simpson's total compensation in her first full year as CEO came to approximately 11.3 million dollars — substantial but not excessive by the standards of a twenty-billion-dollar-market-cap company. Former CEO John Roberts received 8.45 million in 2024.

More importantly, the primary short-term incentive metric is consolidated operating income, with minimum thresholds that must be met before any bonus is paid. This is not a "participation trophy" compensation system.

In both 2022 and 2023, when operating income fell below the minimum threshold of 1.24 billion dollars, no named executive received incentive bonuses. Zero. Not a reduced bonus. Not a discretionary award. Zero. In a world where many public company executives collect eight-figure payouts regardless of performance, J.B. Hunt's willingness to zero out bonuses sends a powerful signal about accountability. It also sends a signal to the rest of the organization: the people at the top eat last when times are tough.

The company's broader compensation philosophy explicitly ties a higher proportion of pay to performance as seniority increases, aligning management's interests with shareholders. Long-term incentives include stock-based awards tied to multi-year performance targets, ensuring that executives are rewarded for sustained value creation, not one-time windfalls.

And with Johnelle Hunt's eighteen-plus-percent ownership stake sitting alongside management in the shareholder register, there is a natural check against short-termism. When the company's largest shareholder is the ninety-something-year-old co-founder who built the business from scratch, the pressure to optimize for the next quarter is tempered by the pressure to preserve and grow wealth across generations. Management knows that its largest shareholder is watching not with the impatience of a hedge fund but with the patience of a family that has held the stock for over forty years.

There is an interesting cultural tension at play in Lowell, Arkansas. The company operates with what might be called "Arkansas Humility" — a no-frills, results-oriented, ego-light culture rooted in the small-town values of its founders. Executives do not give splashy keynotes at Davos. The headquarters is functional, not flashy. There is no corporate jet fleet. The town of Lowell itself is tiny — part of the broader Northwest Arkansas metro that also hosts Walmart's headquarters in Bentonville and Tyson Foods' campus in Springdale.

And yet, the ambition is unmistakably that of a Silicon Valley platform company — building network effects, investing hundreds of millions in technology, and positioning to dominate the digital infrastructure of American freight. The company employs over thirty-three thousand people. It operates in all forty-eight contiguous states, Canada, and now Mexico. It generates twelve billion dollars in revenue. All from a town that most Americans have never visited.

The combination of small-town humility with world-class ambition is one of the least appreciated aspects of J.B. Hunt's culture, and one of the hardest for competitors to replicate. It attracts people who want to build things, not people who want to be seen building things. That distinction matters more than it might seem.

VII. The Playbook: 7 Powers & Porter's 5 Forces (2:45 – 3:15)

🎙 The Strategic Architecture

Having laid out the history, the segments, and the management, the essential question for any long-term investor is this: is the competitive advantage durable?

Is this a business that can sustain above-average returns on invested capital over the next decade and beyond? Or is it a well-run company in a commodity industry that will inevitably see its margins compressed by competition and technological change?

The frameworks of Hamilton Helmer and Michael Porter provide a useful lens for answering that question.

Hamilton Helmer's 7 Powers

Helmer's framework, laid out in his book "7 Powers: The Foundations of Business Strategy," identifies seven sources of durable competitive advantage — the structural moats that allow a business to earn persistent differential returns. J.B. Hunt exhibits at least three of them in convincing form.

The first is Cornered Resource — an asset that competitors cannot access or replicate. J.B. Hunt's exclusive intermodal partnership with BNSF in the western United States is the textbook definition.

There are only seven Class I railroads in North America. BNSF operates the most extensive rail network in the western half of the continent — roughly thirty-two thousand miles of track connecting West Coast ports to the Midwest and beyond. J.B. Hunt has been BNSF's primary intermodal partner for over three decades.

The relationship is not governed by a simple contract that could be rebid to a competitor; it is a deeply integrated operational partnership with shared infrastructure, joint service teams, revenue-sharing arrangements, and billions of dollars in co-invested assets. A new entrant cannot call BNSF and propose to replace J.B. Hunt any more than a new streaming service could call Taylor Swift and propose to replace Spotify. The relationship is too deep, too old, and too mutually dependent.

This is the single most important competitive advantage J.B. Hunt possesses.

The second power is Scale Economies. In the context of the 360 marketplace, scale creates a virtuous cycle that is nearly impossible for smaller competitors to replicate.

The more freight volume flows through the platform, the denser the network becomes, which means better matching efficiency, lower empty miles, and more attractive pricing — which in turn attracts more shippers and carriers. This dynamic is particularly powerful in freight brokerage, where the quality of the matching algorithm is directly proportional to the volume of data it processes.

A startup brokerage platform with a thousand loads per day simply cannot match the optimization quality of a platform processing tens of thousands. And unlike a pure-play digital broker, J.B. Hunt's own fleet provides guaranteed base volume that keeps the platform active even during market downturns.

The third power is Switching Costs, most visibly in the Dedicated Contract Services segment. When J.B. Hunt operates a customer's entire private fleet — hiring and training drivers, maintaining vehicles, integrating technology systems, optimizing routes based on years of historical data — the cost of switching to a competitor is not just financial but operational. The customer would need to rehire and retrain hundreds of drivers, deploy new technology, rebuild routing algorithms, and endure months of service disruption during the transition. The multi-year contracts and deep operational integration make DCS one of the stickiest business models in transportation, with customer retention rates that far exceed industry norms.

Porter's 5 Forces

Turning to Michael Porter's framework, J.B. Hunt's position looks equally strong when examined through the lens of industry structure.

On bargaining power of suppliers, the most important suppliers to J.B. Hunt are the railroads — particularly BNSF. In most shipper-railroad relationships, the railroad holds enormous leverage because there are so few of them and their infrastructure is impossible to replicate. But J.B. Hunt has neutralized this dynamic by becoming BNSF's single largest intermodal customer. When you represent a massive share of a supplier's revenue, the power dynamic shifts. BNSF needs J.B. Hunt's volume as much as J.B. Hunt needs BNSF's rails. This mutual dependency creates a balanced partnership rather than a one-sided vendor relationship. There have been periodic revenue-sharing disputes — notably around 2018 and 2019 — but the relationship has always been resolved because both parties understand that the alternative to cooperation is mutual destruction of the intermodal business they built together.

On the threat of new entrants, this is where the J.B. Hunt story becomes particularly instructive. Over the past decade, the venture capital community poured billions of dollars into digital freight brokers — Convoy, Uber Freight, Transfix, and others — betting that technology could disrupt the "dinosaur" incumbents. The thesis was seductive: freight matching is an information problem, and technology companies solve information problems better than trucking companies. What these startups discovered, however, was that freight logistics is not just an information problem. It is a physical problem. When a shipper needs a truck at 6 AM tomorrow and there is no carrier available on the digital platform, someone needs to dispatch a real truck from a real terminal. The pure-play digital brokers did not have that capability. J.B. Hunt did. Convoy's collapse in October 2023 was the most dramatic illustration of this dynamic, but the broader pattern held across the category. Technology alone — without the physical layer of trucks, containers, rail partnerships, and terminal infrastructure — proved insufficient to build a durable logistics business.

On the rivalry among existing competitors, J.B. Hunt faces competition from different players in each of its segments: Hub Group and Schneider in intermodal, Werner and Ryder in dedicated, C.H. Robinson and XPO in brokerage. But no single competitor matches J.B. Hunt's breadth across all five segments.

Hub Group, the second-largest intermodal provider, operates at roughly a third of J.B. Hunt's intermodal volume. Knight-Swift, the largest truckload carrier by fleet size, has a limited intermodal presence. C.H. Robinson, the largest freight broker by revenue, owns no trucks and has no physical assets. XPO, spun off from its parent and renamed RXO for its brokerage arm, is a formidable competitor in specific niches but lacks the intermodal backbone.

No competitor possesses the combination of the BNSF partnership, the 360 platform, and the scale of owned container assets. Each competitor excels in one dimension but cannot match the integrated platform that J.B. Hunt has built across multiple modes. This breadth is itself a competitive advantage — a shipper that needs intermodal, dedicated, brokerage, and final mile services can get all of them from a single provider, with integrated technology, a single account relationship, and seamless data flow across services.

There are also material regulatory considerations worth flagging. The Surface Transportation Board oversees railroad operations and could theoretically mandate changes to intermodal access or pricing — forcing BNSF to open its network to additional intermodal partners, for instance, which would dilute J.B. Hunt's exclusivity. Environmental regulations around emissions standards continue to tighten, affecting fleet operating costs across the industry. California's Advanced Clean Trucks regulation, which requires increasing percentages of zero-emission vehicle sales, is particularly relevant.

And the classification of truck drivers as employees versus independent contractors remains an ongoing legal and regulatory issue. California's AB5 gig worker law and similar legislation in other states could affect operating costs and labor models across the industry. J.B. Hunt, which employs its drivers as W-2 employees rather than relying heavily on independent contractors, may actually benefit from tighter classification rules that increase costs for competitors who depend on contractor models.

VIII. The Bear vs. Bull Case (3:15 – 3:35)

🎙 The Tug of War

Every great business has both a compelling bull case and a credible bear case. The quality of an investment often depends less on which case is "right" and more on understanding the conditions under which each scenario unfolds.

The Bear Case

The most frequently cited bear argument against J.B. Hunt centers on autonomous trucking. If self-driving trucks become commercially viable on long-haul highway corridors — the very corridors where intermodal currently offers its greatest advantage over traditional trucking — the value proposition of intermodal could erode significantly.

The core intermodal pitch is that rail is more efficient than a human-driven truck over long distances. But if you remove the human driver — and with it the costs of wages, benefits, rest stops, hours-of-service regulations, and the chronic shortage of qualified drivers — the calculus changes. An autonomous truck that can drive twenty-four hours a day without stopping might be faster and cheaper than the intermodal combination of truck-to-rail-to-truck. The fuel cost advantage of rail would still exist, but the labor cost advantage — which represents the largest single expense in trucking — would evaporate.

This is not a theoretical threat. Aurora Innovation completed the first commercial freight route with no human in the cab, running between Dallas and Houston. Kodiak Robotics is also making progress toward commercial deployment. And J.B. Hunt itself has been proactive — partnering with Waymo in 2022 as its first self-driving freight customer (though Waymo subsequently paused its trucking program to focus on robotaxis) and launching an autonomous trucking pilot with Bot Auto on Houston-to-San Antonio routes in 2025. The company also purchased twenty hydrogen-powered trucks from Nikola Corporation in 2024, hedging across multiple next-generation technologies.

But J.B. Hunt's proactivity also reveals the discomfort: the company recognizes that autonomous trucking could cannibalize its own intermodal business. The timeline for widespread autonomous deployment remains uncertain — regulatory, liability, and technological hurdles are substantial — but the directional threat is real.

Even a partial deployment on high-volume highway corridors like Dallas-to-Houston or Los Angeles-to-Phoenix could pressure intermodal pricing and volumes on those specific lanes.

A second bear concern relates to the cyclicality of the freight market. J.B. Hunt's financial performance is heavily influenced by the freight cycle, which tends to follow broader economic activity.

Revenue peaked at nearly fifteen billion in 2022 during the freight super-cycle, then declined for three consecutive years to twelve billion by 2025. Return on invested capital followed a similar trajectory, falling from 15.4 percent in 2022 to 8.4 percent in 2024 — a level that was actually below the company's estimated weighted average cost of capital of approximately nine percent. In other words, J.B. Hunt was technically destroying value for shareholders during the trough of the cycle.

The ROIC recovered modestly to 9.3 percent in 2025, and the company posted net income of approximately 598 million dollars with diluted earnings per share of $6.12 — up ten percent year over year. But the 2024 trough illustrated a structural vulnerability: even a "best-in-class" logistics company cannot fully insulate itself from the boom-and-bust dynamics of freight demand.

To put the cyclicality in context, the typical trucking industry average ROIC runs between five and eight percent. Even at its 2024 trough, J.B. Hunt's 8.4 percent was at or above the industry average. And at the 2022 peak of 15.4 percent, it was roughly double the industry norm. The company's ROIC is structurally higher than peers, but it still swings with the cycle — a reality that investors must accept.

A third concern involves the concentration risk in intermodal. Roughly half of J.B. Hunt's revenue depends on the performance and strategic priorities of a single rail partner — BNSF. Any disruption to that relationship — whether through contract disputes, operational failures, strategic divergence, or regulatory intervention — would have immediate and severe consequences for J.B. Hunt's financial performance. The 2018-2019 revenue-sharing disputes, while ultimately resolved, hinted at the tensions inherent in a relationship where both parties have enormous leverage.

The Bull Case

The bull case begins with a simple observation: the freight market is enormous and structurally underpenetrated by the kind of integrated, technology-enabled logistics that J.B. Hunt provides. The domestic truckload market alone exceeds eight hundred billion dollars annually. Intermodal's share of long-haul freight, while growing, remains a fraction of what it could be. Every percentage point of modal conversion from truck to intermodal represents billions of dollars in potential revenue, and J.B. Hunt is the undisputed leader in facilitating that conversion.

There is also a compelling counter-argument to the autonomous trucking threat. Even if autonomous trucks become widespread on highway corridors, J.B. Hunt is better positioned to adopt and integrate autonomous technology than to be disrupted by it. The company has already partnered with autonomous truck developers. Its 360 platform is ideally suited to dispatching and routing autonomous vehicles. And its intermodal terminals — where containers are transferred between trucks and trains — could function as natural "handoff points" where autonomous trucks operating on highway corridors transfer their loads to human-driven trucks for last-mile delivery through urban areas, where full autonomy is much harder to achieve. In this scenario, autonomous trucking does not destroy J.B. Hunt's business model; it enhances it, by reducing the cost of the short-haul truck segments on either end of an intermodal move.

The e-commerce opportunity in Final Mile Services remains compelling despite the segment's recent struggles. The delivery of heavy and bulky items — appliances, furniture, mattresses, exercise equipment — to consumers' homes is one of the most operationally complex and underserved segments of the logistics industry. Amazon does not do this well. FedEx and UPS are not equipped for it. The companies that specialize in it tend to be small, fragmented, and regional. J.B. Hunt is one of the few players with the national scale, technology platform, and operational expertise to serve this market at scale. If e-commerce penetration of big-and-bulky categories continues to grow — and there is every reason to believe it will as consumers increasingly order everything online — J.B. Hunt's early investment in Final Mile could prove prescient, even if the returns have been lumpy in the short term.

The capital allocation story reinforces the bull case. J.B. Hunt has increased its dividend for twenty-two consecutive years — currently paying $1.80 per share annually — and has been an aggressive repurchaser of its own stock.

The buyback pace has accelerated dramatically: the company repurchased nearly 950 million dollars of its own shares in 2025, up from 550 million in 2024 and 197 million in 2023. Total shares outstanding have declined from over 105 million in 2021 to roughly 97.7 million by the end of 2025 — a reduction of about seven percent in four years. In October 2025, the board authorized a new one-billion-dollar share repurchase program.

The company's market capitalization sits at approximately 19.6 billion dollars, and the stock reached all-time highs as recently as February 2026, trading above two hundred and thirty dollars per share. The fifty-two-week range stretches from roughly $123 to $236, reflecting the volatility that accompanies freight cycle exposure.

The KPIs That Matter

For investors tracking J.B. Hunt's ongoing performance, three key performance indicators stand out above all others.

The first is intermodal load volume — the number of loads moving through the JBI segment. This is the single most important leading indicator of J.B. Hunt's business health. It serves as a real-time barometer of both freight demand and J.B. Hunt's competitive position within the intermodal market. When load volumes grow, it means shippers are converting freight from truck to rail, and J.B. Hunt is capturing that conversion. When volumes decline, it signals either a weak freight market or competitive pressure.

The second is return on invested capital. ROIC captures the company's ability to generate profits relative to the enormous capital base deployed in containers, trucks, technology, and rail partnerships. For a company that has invested billions in physical assets, ROIC is the single best measure of whether those investments are earning adequate returns. Tracking ROIC over time reveals whether J.B. Hunt is getting more efficient with its capital or whether the asset base is growing faster than the profits it generates.

The third is ICS operating margin. Because ICS is the segment most directly tied to the 360 platform's performance, its margin trajectory is the clearest indicator of whether J.B. Hunt's technology investments are translating into profitable brokerage operations. The swing from a fifty-six-million-dollar loss in 2024 to a ten-million-dollar loss in 2025 suggests the segment may be approaching a profitability inflection, but it needs to be sustained and ultimately turn positive to justify the hundreds of millions invested in the platform.

IX. Conclusion & Final Reflections (3:35 – 3:45)

🎙 The Invisible Infrastructure

There is a particular kind of American business story that never gets the attention it deserves — the story of the companies that built the invisible infrastructure upon which everything else depends.

People celebrate the brands they interact with directly: the iPhone they hold, the Amazon package on their doorstep, the Netflix show on their screen. But behind every one of those products is a supply chain, and behind that supply chain is a web of trucks, trains, containers, and algorithms quietly ensuring that goods move from where they are made to where they are needed. The food in your refrigerator, the couch in your living room, the parts that keep your car running — all of it moved through a logistics network at some point. And a remarkable share of that network runs through a company that most consumers have never heard of, headquartered in a small Arkansas town that most Americans could not find on a map.

J.B. Hunt sits at the center of that web.

From a rice hull operation started with three thousand dollars in rural Arkansas to a twelve-billion-dollar logistics platform — from a seventh-grade dropout's vision to the first intermodal partnership in American history — from a fleet of five tractors to over 120,000 containers and a digital marketplace processing millions of transactions — the J.B. Hunt story is one of continuous reinvention driven by a deceptively simple insight: the most valuable thing in logistics is not the truck. It is the system.

Every era of J.B. Hunt's evolution has been defined by a willingness to cannibalize the current business in pursuit of a better model. In the 1980s, J.B. Hunt cannibalized his own truckload growth by shifting freight to rail. In the 2010s, the company cannibalized its own brokerage relationships by building a digital marketplace. In the 2020s, it is actively exploring autonomous trucking partnerships that could eventually disrupt its own intermodal advantage. This is not the behavior of a company optimizing for next quarter's earnings call. It is the behavior of a company thinking in decades.

Consider the financial trajectory. Revenue has grown from 286 million dollars in 1987, when Kirk Thompson took over as CEO, to twelve billion today — a compounding that has made early shareholders extraordinarily wealthy. The company was added to the S&P 500 and the Dow Jones Transportation Average, and joined the NASDAQ-100 in February 2017. Its stock reached all-time highs as recently as February 2026, trading above two hundred and thirty dollars per share. Through it all, the Hunt family never sold. Twenty-two consecutive years of dividend increases. Nearly a billion dollars in share repurchases in 2025 alone. A company that generates roughly six hundred million dollars in net income annually, returning the majority of it to shareholders while continuing to invest in the platform.

The fact that all of this happened from Lowell, Arkansas — a town of roughly ten thousand people when the Hunts started their business, tucked into the Ozark foothills alongside Walmart's Bentonville headquarters and Tyson Foods' Springdale campus — adds a layer of improbability that borders on the mythic. Northwest Arkansas produced three of the most consequential companies in American commerce: the world's largest retailer, the world's largest protein processor, and the world's largest intermodal logistics provider. Something in the water, or perhaps something in the culture — the scrappy, no-excuses, outwork-everyone ethos of rural America — produced an extraordinary concentration of business talent.

J.B. Hunt the man is gone, but the handshake he made on that train in 1989 still reverberates through every container that moves across the American rail network, through every load matched on the 360 platform, through every appliance delivered to a consumer's doorstep by a Final Mile driver. The question for the next decade is whether the company that bears his name can continue to reinvent itself as aggressively as it has in the past — navigating the freight cycle, absorbing the autonomous trucking revolution, and deepening its technology moat — while maintaining the long-term orientation that the Hunt family's ownership stake has always provided. The infrastructure is in place. The platform is built. The cornered resources are locked in. What happens next depends on whether the next generation of leaders can match the audacity of a truck driver who decided, against all conventional wisdom, to shake hands with a railroad man.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube