Invesco: The Transatlantic Consolidation & The Power of QQQ

I. Introduction & Episode Roadmap

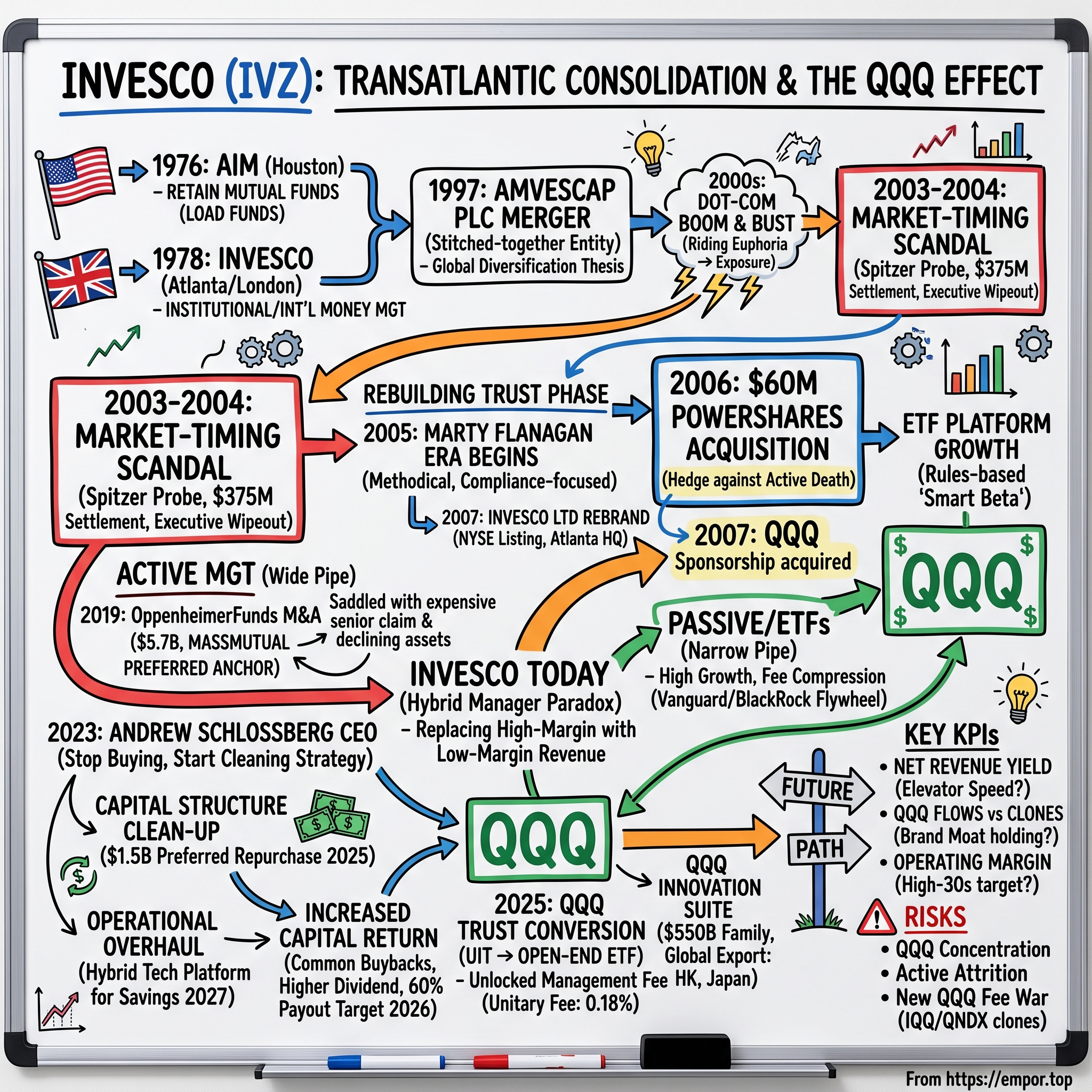

Picture a single ticker symbol, four letters long, that has become shorthand for an entire era of American capitalism. When a retail investor in Ohio, a hedge-fund trader in Connecticut, and a wealth manager in Hong Kong all want to buy "the Nasdaq," they reach for the same instrument: QQQ. It is one of the most heavily traded securities on Earth, a proxy for the twenty-first century's most valuable companies — NVIDIA, Apple, Microsoft, Amazon — bundled into a single share. And for most of its life, almost nobody who owned it could have told you which company actually ran it.

The answer is Invesco Ltd., an asset manager headquartered in Atlanta, Georgia, trading on the New York Stock Exchange under the ticker IVZ. As of the first quarter of 2026, Invesco oversaw roughly $2.2 trillion in assets under management, with the figure climbing back toward the $2.3 trillion range as markets recovered through April.13 That is a staggering sum — larger than the GDP of all but a handful of nations. Yet Invesco is not a household name the way BlackRock or Vanguard are. It occupies a stranger, more precarious position in the financial ecosystem: a "hybrid" manager, straddling two worlds that are actively at war with each other.

Here is the paradox at the heart of this story. On one side, Invesco runs a large, old-fashioned active management business — human stock-pickers and bond managers charging fifty to seventy basis points to try to beat the market. That business is a melting ice cube, bleeding assets year after year as investors abandon expensive active funds. On the other side, Invesco operates one of the largest exchange-traded fund franchises in the United States, roughly the fourth-largest ETF issuer behind BlackRock's iShares, Vanguard, and State Street. Its ETF and index platform ended the first quarter of 2026 at a record $638 billion — or over $1 trillion once you fold in the crown jewel.3 The problem is that these low-cost index products charge a fraction of what the active funds do. Invesco is, in effect, replacing high-margin revenue with low-margin revenue and calling it growth.

The star of this show is the Invesco QQQ Trust. At roughly $400 billion in assets at the end of 2025 — nearly a fifth of the entire company — QQQ is the single most important product Invesco owns.1 And in late 2025, after twenty-six years frozen inside a rigid, antiquated legal structure, QQQ underwent a quiet but historic transformation, converting from a Unit Investment Trust into an open-end ETF. For the first time in its history, Invesco began collecting a genuine management fee on it.3

But this is not a triumphant story, and it would be a disservice to tell it as one. Because at the very moment Invesco finally unlocked QQQ's economics, the ground shifted beneath it. In April 2026, Nasdaq ended the exclusive license that had made QQQ the only game in town — and within weeks, BlackRock and State Street launched cheaper clones aimed directly at it.1819 The moat that the bull case rests upon was breached in the same year it was monetized.

To understand how Invesco arrived at this knife's-edge moment, we have to travel back through a corporate saga stranger than most fiction: a transatlantic merger of a Houston mutual-fund shop and a London institutional manager; a near-death regulatory scandal that wiped out the executive suite; a $60 million bet on an obscure Chicago startup that became one of the great bargains in financial history; a debt-fueled consolidation spree that saddled the company with a $4 billion preferred-stock anchor; an activist siege led by Nelson Peltz; and a modern-day CEO whose entire strategy amounts to cleaning up the mess his predecessors left behind. Let's begin where the money did.

II. Transatlantic Roots: AIM, Invesco, and the AMVESCAP Merger

In 1976, three men pooled roughly $120,000 in a Houston office and started a mutual fund company.8 Charles "Ted" Bauer, Robert Graham, and Gary Crum called it AIM Management Group, and their timing was, in retrospect, close to perfect. America was on the cusp of a thirty-year revolution in how ordinary people saved for retirement. The 401(k) had not yet been invented, but the appetite for professionally managed pools of stocks was about to explode, and AIM positioned itself squarely in the fattest part of that wave: retail equity mutual funds sold through brokers and financial advisers.

Bauer, a courtly former investment banker, understood something that many of his contemporaries did not. In the mutual-fund business, the product itself — the fund's performance — matters less than the distribution machine that sells it. Money does not walk into a fund on its own; it is carried there by an army of brokers and advisers who earn commissions for the carrying. AIM built a formidable network of exactly those relationships, and it fed them a diet of aggressive, tech-heavy growth strategies designed to sell. Funds like AIM Constellation and AIM Weingarten became names to conjure with in the 1990s. This was the age of the "load fund," where an investor might pay a sales charge of several percent off the top just to get in the door, and where the adviser who sold it took a cut — an economic model that aligned the fund company and the salesman perfectly, and left the customer to hope the performance justified the toll.

As the dot-com bull market inflated, AIM's growth funds soared, and tens of billions of dollars poured in. The firm was minting money on high-margin active equity flows at the exact moment American households were pivoting en masse into the stock market through their new 401(k) plans. It was, for a stretch in the late 1990s, one of the great growth stories in American money management — and like so many stories built on a single roaring bull market, its greatest strength was quietly becoming its greatest vulnerability.

Meanwhile, an ocean away, a very different company was assembling itself. The Invesco name has a convoluted lineage. Its American root traces to 1978, when Atlanta's Citizens & Southern National Bank spun off its money-management operation as an independent firm. A decade later, in 1988, the London-listed Britannia Arrow acquired the business and eventually adopted the Invesco name for the whole enterprise.8 Where AIM was a retail machine built on American broker relationships, Invesco was an institutional and international animal — managing money for pension funds and sovereign entities, with real strength in London, continental Europe, and Asia. It spoke the language of consultants and trustees, not commission-driven brokers.

You can already see the logic that would eventually bring these two together. AIM had a peerless retail distribution network in the United States but limited global reach. Invesco had institutional heft and a genuinely international footprint — a book of pension-fund and sovereign mandates built on the sober, consultant-driven relationships that dominate institutional money — but lacked AIM's grip on the lucrative American retail channel. The two halves were complementary in almost textbook fashion: one owned the customer, the other owned the geography. In 1997, they merged to form a company with a name only a committee could love: AMVESCAP PLC, a portmanteau of AIM and Invesco, listed in London and overseeing roughly $200 billion at the time.8

There is a lesson buried in that clumsy name that echoes through the rest of this story. AMVESCAP was, from birth, a stitched-together entity — a collection of brands, cultures, and legal vehicles bolted onto a single holding company. The strategy of growth-by-combination was baked into the company's DNA from the very first day, and over the following three decades Invesco would return to that same playbook again and again, each time acquiring its way toward scale. Sometimes it worked brilliantly. Sometimes it nearly destroyed the firm.

The strategic thesis was sound on paper — combine American retail muscle with European and Asian institutional reach to build a truly global, diversified manager. And for a few glorious years, it worked spectacularly, largely because the timing again favored the bulls. AMVESCAP rode the final, euphoric stretch of the dot-com boom, drawing in enormous quantities of high-margin active equity money. When technology stocks are doubling every eighteen months and your funds are packed with them, gathering assets is easy and the fees roll in.

But a business model that depends on a rising market carries a hidden liability: it is exposed not just to the market's declines, but to the temptations that arise when performance is everything and oversight is an afterthought. AMVESCAP had built a machine optimized for gathering hot money quickly. The question that would soon define the company's survival was whether, in its haste to feed that machine, it had cut corners that a regulator might one day notice. It had. And the regulator noticed.

III. The Market-Timing Scandal and the Marty Flanagan Era

In September 2003, New York Attorney General Eliot Spitzer detonated a bomb under the entire American mutual-fund industry. His office, alongside the Securities and Exchange Commission, launched a sweeping investigation into two related abuses: "late trading" and "market timing." To understand why this nearly killed AMVESCAP, you need to understand what these practices actually were — and why they were a betrayal of the ordinary investor.

Think of a mutual fund as a shared swimming pool. Every long-term investor owns a piece of the water, and the fund is priced once a day, after the market closes. "Market timing" was the practice of certain favored clients — typically hedge funds — rapidly diving in and out of the pool to exploit stale prices, particularly in funds holding international stocks whose home markets had already closed. Each quick in-and-out trade skimmed a little value from the long-term holders still in the water, like a swimmer who keeps cannonballing in and splashing everyone else's drinks off the pool deck. Fund companies were supposed to police this. Instead, regulators found that some of them had quietly cut deals to allow it, because the timers parked other assets with the firm and generated fees.

This was not a scandal confined to one bad actor. Spitzer's probe swept across the industry, ensnaring dozens of the biggest names in American fund management and forcing a wave of settlements, executive resignations, and new "fair fund" restitution mechanisms designed to return money to harmed investors. It was, in its way, the mutual-fund industry's Enron moment — a collective revelation that the people paid to be fiduciaries had, in more than a few cases, been quietly serving the clients who mattered most to their own revenue rather than the millions of small savers who trusted them.

AMVESCAP's American subsidiaries were caught in the dragnet. Regulators concluded that Invesco Funds Group and AIM Advisors had facilitated exactly this kind of short-term timing arrangement for select institutional clients, at the direct expense of the ordinary retail investors whose money sat in the funds. The irony was brutal: the very retail-distribution excellence that AIM had spent decades building was now revealed to have been quietly diluting the returns of those same retail customers. A firm that had won its customers' trust one broker relationship at a time had, in a stroke, forfeited it on the front page of every financial newspaper in the country.

The reckoning came in October 2004. AMVESCAP agreed to settle with the SEC and state regulators for a combined $375 million — $325 million tied to Invesco Funds Group and $50 million to AIM Advisors — including substantial civil penalties and fee reductions for investors.5 But the financial penalty was almost beside the point. In the trust business, reputation is the product. A fund company that has been publicly branded as one that cheats its own customers has nothing left to sell. The executive suite was effectively wiped clean, and the company faced an existential question: who could possibly restore its credibility?

The answer arrived in 2005 in the person of Martin L. "Marty" Flanagan. Flanagan came from Franklin Resources, the storied mutual-fund house behind the Franklin and Templeton brands, where he had spent more than two decades and risen to co-president. He had trained as an accountant — a certified public accountant by background — and that showed in how he ran things: he was a numbers-and-controls man, fluent in the unglamorous machinery of fund administration, compliance, and cost. He built a reputation as a disciplined, low-ego operator who understood the plumbing of the asset-management business intimately. He was, in temperament, almost the opposite of the swashbuckling growth culture that had gotten AMVESCAP into trouble: methodical, process-driven, and obsessed with rebuilding institutional trust.

Flanagan understood that trust, once broken in this business, is rebuilt not through a single grand gesture but through a thousand boring acts of governance. He consolidated the sprawling patchwork of fund boards and operations that AMVESCAP had accumulated, tightened compliance, and set about proving to regulators, distributors, and investors that the firm's fiduciary house was back in order. This was unglamorous, multi-year work, and it is precisely the kind of work that a firm coming off a reputational catastrophe must do before it can dream of growth again.

Flanagan's first act was symbolic and clarifying. In 2007, he swept away the awkward AMVESCAP name and rebranded the entire enterprise as Invesco Ltd. He moved the company's primary stock listing from London to the New York Stock Exchange, re-domiciled the holding company in Bermuda, and established Atlanta as the unified global headquarters.8 (It is worth correcting a common misconception here: Invesco's holding company is incorporated in Bermuda, not Delaware.) The message to the market was that this was a new, consolidated, American-facing company with a clean name and clean governance.

But rebranding is cosmetic. Flanagan's real challenge was strategic. He had inherited a firm whose core business — active equity mutual funds — was about to face an extinction-level competitive threat from a new kind of product. And in a decision that would define Invesco for the next two decades, he chose not to defend the old castle but to buy a foothold in the new one. For sixty million dollars.

IV. The $60 Million PowerShares Acquisition: A Strategic Masterstroke

In January 2006 — before the rebrand, in the final AMVESCAP days and just as Flanagan was taking the reins — the company announced the acquisition of a tiny, obscure firm from suburban Chicago called PowerShares Capital Management. The headline number was almost comically small for a company managing hundreds of billions: $60 million in cash at closing, with a series of performance-based earn-outs that could eventually push the total toward roughly $730 million if the business hit aggressive growth targets.6 At the time, it barely registered as news.

PowerShares was the creation of H. Bruce Bond, an evangelist for a then-heretical idea. Exchange-traded funds in the mid-2000s were overwhelmingly plain-vanilla index trackers — buy the S&P 500, hold it, charge almost nothing. Bond's insight was that the ETF wrapper — the tax-efficient, exchange-listed, intraday-tradable structure — could hold far more than a market-cap index. It could hold rules-based strategies that tilted toward value, or quality, or equal weighting: what the industry would later christen "smart beta." He was building an arsenal of these products, and he needed a bigger balance sheet and distribution muscle to scale them.

It is worth pausing on why the ETF wrapper itself is such an elegant piece of financial engineering, because it explains almost everything about where the industry went. A traditional mutual fund is bought and sold once a day, directly from the fund company, and every time the manager sells a winning stock to meet redemptions, the remaining shareholders can get stuck with a taxable capital-gains distribution they never asked for. An ETF, by contrast, trades on an exchange like a stock, and through a clever "in-kind" creation-and-redemption mechanism it can usually shuffle securities in and out without triggering those taxable events. The result is a vehicle that is cheaper to run, more tax-efficient, and tradable at any moment of the day. Bond grasped that this wrapper would eventually swallow the fund industry — and that the firm controlling the best wrappers would inherit the flows. "Smart beta," in plain English, simply means following a transparent rulebook other than "own the biggest companies by size." Equal weighting, for instance, holds a little of everything rather than letting a handful of mega-caps dominate — a rule that sounds trivial but produces meaningfully different returns over time.

Why does this rank among the great bargains in financial history? Because tucked inside PowerShares was something whose value nobody fully appreciated in 2006: the marketing and administrative relationship with the QQQ. QQQ had been launched in March 1999 by a Nasdaq subsidiary as a Unit Investment Trust tracking the Nasdaq-100 index.16 It was a curiosity of the dot-com era. But its sponsorship was in transition, and in 2007 the sponsor role passed formally to PowerShares — by then owned by Invesco.16 Invesco had, almost as an afterthought, acquired stewardship of what would become a multi-hundred-billion-dollar asset. It is difficult to overstate the asymmetry: a $60 million initial outlay that would, two decades later, sit alongside an ETF platform approaching $640 billion and a QQQ franchise worth hundreds of billions.3

But here we should resist the temptation — one the outline's "masterstroke" framing invites — to narrate this purely as visionary genius. The honest reading is more nuanced. Flanagan and AMVESCAP did not pay $60 million because they foresaw NVIDIA-driven trillions; they bought a struggling boutique for cheap because it was cheap, and the QQQ jackpot was substantially a matter of being in the right seat when a secular tsunami — the passive revolution and the concentration of the Nasdaq-100 into a handful of world-conquering technology giants — rolled in over the following twenty years. The strategic credit Invesco genuinely deserves is subtler: having stumbled into the ETF business, it committed to it, building out infrastructure, licensing, and distribution rather than treating it as a sideshow to the "real" active business. That commitment is what turned a lucky purchase into a durable platform.

The deeper strategic logic, though, is the one that matters most for investors trying to understand Invesco today. The PowerShares deal was a hedge against Invesco's own core business. Flanagan was buying insurance against the slow death of active stock-picking, planting a flag in the low-cost passive world that would eventually cannibalize his high-margin funds. That hedge would prove prescient. The trouble is that a hedge, by design, tends to pay off precisely when your main position is losing money — and as the 2010s unfolded, Invesco's main position began losing money in earnest. The company's response would be far more expensive, and far more debatable, than a $60 million flyer.

V. Active Consolidation & The MassMutual Preferred Stock Overhang

By the middle of the 2010s, the asset-management industry had bifurcated into winners and the walking wounded, and the dividing line was fees. At one end stood the passive colossi — BlackRock's iShares and Vanguard — hoovering up trillions at expense ratios approaching zero, their scale so vast that they could profitably run an index fund for three or four basis points. At the other end stood a large middle tier of active managers, Invesco among them, watching investors pull money out of their expensive funds quarter after quarter and redeploy it into those near-free index products. This is the "great migration" from active to passive, and it was — and remains — the defining structural fact of the industry.

Why can Vanguard and BlackRock push fees toward zero when Invesco cannot? The answer is a brutal flywheel. Vanguard is owned by its own funds, so it runs essentially at cost and passes savings to investors, dragging the whole industry's pricing down with it. BlackRock, through iShares, reached such enormous scale that even three or four basis points on trillions of dollars generates billions in revenue, and that scale funds the technology, index-licensing, and distribution muscle that makes it still harder for a challenger to compete. Each dollar of new assets makes these giants cheaper and stronger, which attracts the next dollar. For a mid-tier manager charging higher fees on a shrinking active book, that flywheel is a nightmare: it cannot match the price without destroying its own economics, and it cannot keep the price without losing the assets.

Flanagan's strategic answer was scale. If fee compression was relentless and unavoidable, then survival depended on spreading fixed costs — compliance, technology, back-office operations, distribution — across an ever-larger asset base. Bigger was cheaper, and cheaper was survival. It was a defensible instinct. But there is a crucial difference between buying scale in the growing part of the business and buying it in the shrinking part, and Invesco was about to do both — one wisely, one not. So Invesco went shopping.

The first significant move was disciplined and logical. In April 2018, Invesco completed the acquisition of Guggenheim Investments' ETF business for $1.2 billion in cash.9 This was a bolt-on that strengthened exactly the right part of the company. It brought over the popular BulletShares suite of defined-maturity bond ETFs and, crucially, the S&P 500 Equal Weight ETF — ticker RSP — a smart-beta product that let investors own the index without being dominated by its largest handful of stocks. Consolidating these under the Invesco banner deepened the ETF franchise that PowerShares had seeded. It was consolidation in service of the future.

The second move was neither disciplined nor obviously logical, and it would haunt the company for years. In 2018 Invesco agreed, and in May 2019 completed, the acquisition of OppenheimerFunds from Massachusetts Mutual Life Insurance Company — MassMutual — in a transaction valued at roughly $5.7 billion.7 OppenheimerFunds brought with it about $224 billion in assets, heavily concentrated in international and emerging-market equity strategies, and the deal vaulted Invesco's total AUM past $1.2 trillion. On the surface, it delivered exactly the scale Flanagan wanted.

But look at how Invesco paid, because the structure of this deal is the single most important thing to understand about the company's capital structure for the following six years. Invesco did not pay cash. Instead, it handed MassMutual roughly 81.9 million newly issued common shares — making the insurer Invesco's largest single shareholder, with a stake of around 15.7% at closing — plus $4.0 billion of a peculiar instrument: perpetual, non-cumulative Series A preferred stock carrying a 5.9% dividend rate.7

Here is why that preferred stock became known, in effect, as an anchor chained to the common shareholder's ankle. Perpetual preferred stock sits ahead of common stock in the capital structure. Its dividends must be paid before common shareholders see a dime of buybacks or dividend growth. And at 5.9% on $4.0 billion, the obligation was roughly $236 million per year in pre-tax dividends flowing to MassMutual — a fixed, senior claim on Invesco's cash, year after year, that did not shrink when markets fell or flows turned negative.1 Invesco had bought scale by mortgaging its own equity. Every dollar of that preferred dividend was a dollar not returned to common holders, and the instrument was structured to be non-callable for its first twenty-one years, meaning Invesco could not simply pay it off early on its own terms until 2040.

And what did the $5.7 billion actually buy? This is where the analytical verdict turns harsh. OppenheimerFunds' crown assets were active equity funds — precisely the category the entire industry was fleeing. In the years after the acquisition, several of those flagship strategies, including Oppenheimer's developing-markets equity fund, suffered persistent, heavy outflows; as late as the first quarter of 2026 Invesco was still absorbing expected net outflows from that developing-markets fund, though management noted the bleeding had moderated sharply to its smallest fundamental-equity outflow in nearly nine years.3 The uncomfortable conclusion is that Invesco paid a rich price, in a senior and expensive currency, to acquire a large pile of assets in secular decline. The back-office synergies were real and the company hit its cost-cutting targets; but you cannot cut your way out of owning the wrong products, and the preferred-dividend drag meant common shareholders bore the cost of the mistake twice over — once in the outflows, and again in the cash siphoned off to service the instrument that financed them.

By 2020, Invesco was a scaled but financially encumbered company: bigger than ever, but carrying a $4 billion senior obligation and a shrinking base of high-fee assets. To a certain kind of investor, that combination — a cheap stock, a bloated cost structure, and an obvious strategic logic for further consolidation — looked less like a problem and more like an opportunity. One of the most feared activists in America was about to come knocking.

VI. The Activist Siege: Nelson Peltz and Trian's Consolidation Push

Nelson Peltz does not buy stocks quietly. In October 2020, his firm Trian Fund Management disclosed that it had built a 9.9% stake in Invesco — and, simultaneously, an identical 9.9% stake in rival Janus Henderson.10 The dual position was the tell. Peltz and his Trian co-founder Ed Garden were not making a bet on Invesco's stand-alone recovery. They were making a bet on a wedding.

To understand why this rattled Invesco's board, you have to understand Peltz. By 2020 he was among the most successful and most feared activist investors in the world, with a decades-long track record of buying stakes in large, underperforming consumer and financial companies and agitating — sometimes politely, sometimes ferociously — for change. His Trian had left its fingerprints on H.J. Heinz, Mondelez, Procter & Gamble, and others; a Peltz stake was a signal to the market that management was about to be put on the clock. When a man with that résumé buys a tenth of your company and a tenth of your closest rival simultaneously, he is not asking a question. He is proposing a merger and daring you to say no.

Trian's thesis was elegant and, frankly, hard to argue with in the abstract. The middle tier of the asset-management industry, they argued, was structurally stranded. Firms like Invesco and Janus Henderson were too big to be nimble boutiques and too small to compete with the passive giants on cost. The only escape was consolidation: combine two mid-sized managers, strip out the duplicated overhead — two sets of compliance staff, two technology stacks, two distribution networks — and emerge with the scale to survive. Peltz wanted Invesco to be a consolidator or be consolidated, and he was positioned to profit whichever mid-tier managers ended up dancing together. It was a coldly rational reading of the industry's math, and its logic still hangs over Invesco today.

By November 2020, Peltz and Garden had joined Invesco's board, giving Trian a direct hand in steering the company.10 What followed was one of the more tantalizing near-misses in recent financial history. Through 2021, with Trian's encouragement, Invesco entered serious exploratory talks with State Street to combine with State Street Global Advisors, the arm behind the SPDR ETF franchise and the original S&P 500 fund. State Street Global Advisors alone managed close to $4 trillion at the time; a combination would have created one of the largest asset managers on the planet, a genuine rival in scale to iShares and Vanguard.11

The talks collapsed. The sticking points were the ones that so often kill "mergers of equals" — governance, leadership control, and the fundamental question of who would actually run the combined entity. When two large organizations each believe they are the acquirer, no deal gets done. The State Street tie-up evaporated, and with it the grandest version of the consolidation dream.

By February 2022, Peltz and Garden had had enough of Invesco. They resigned from its board, pivoting their attention and capital toward Janus Henderson, where Trian increased its stake and pressed a similar consolidation agenda.10 Their parting assessment of Invesco was telling: they praised management's operational cost discipline but left with the central strategic problem — the relentless fee compression and the melting active book — fundamentally unresolved. The activist had come, agitated for a transformational merger, failed to force one, and departed. Invesco was left to solve its own problems, from the inside, with a new CEO who would take a conspicuously different approach: not empire-building, but house-cleaning.

VII. Andrew Schlossberg and the Capital Structure Clean-Up

When a company has spent fifteen years buying growth — PowerShares, Guggenheim, OppenheimerFunds — the most radical thing a new leader can do is stop. In June 2023, after eighteen years at the helm, Marty Flanagan retired, and Andrew Schlossberg became president and CEO.12 Schlossberg was not an outside change agent parachuted in to blow things up. He was an Invesco lifer, having joined the firm in 2001 and worked his way up through senior roles including head of the Americas and head of the EMEA region — a man who knew where every body was buried because he had helped bury some of them.12

Schlossberg's strategy can be summarized in a phrase the previous era would have found almost heretical: stop buying, start cleaning. Rather than chase another transformational merger, he set out to simplify the sprawling company, rationalize its product lineup, and — above all — dismantle the financial encumbrances that the OppenheimerFunds deal had bolted onto the balance sheet. The centerpiece of that effort was the assault on the MassMutual preferred stock.

Recall that the $4 billion preferred was structured to be non-callable until 2040. Schlossberg could not simply redeem it. So instead, Invesco negotiated. In April 2025, the company announced an agreement to repurchase $1.0 billion of the preferred stock directly from MassMutual — funded largely with lower-cost debt — a transaction that closed the following month and came bundled with a new strategic product and distribution partnership with the alternatives manager Barings, a MassMutual affiliate.13 Then, in December 2025, Invesco went back for more, repurchasing a further $500 million of the preferred, this time paying a premium of roughly 18% over the instrument's $1,000 liquidation value to persuade MassMutual to part with it.14

The economic logic here is clean and, unlike the OppenheimerFunds deal itself, genuinely accretive to common holders. Retiring $1.5 billion of preferred stock in 2025 eliminated roughly $88.5 million per year in preferred dividends — cash that had been flowing straight to MassMutual and now belongs, in effect, to Invesco's common shareholders.1 After the two repurchases, approximately $2.5 billion of the preferred remained outstanding at the end of 2025.1 The willingness to pay an 18% premium to accelerate the December tranche is itself an analytical signal: management judged that freeing up the cash flow and simplifying the capital structure was worth more than the premium cost — a bet on the value of a clean balance sheet.

There is a subtle craft to how these buybacks were engineered that rewards a second look. Because the preferred was non-callable, Invesco could not force MassMutual to sell; it had to make the insurer want to. The April 2025 transaction did this partly by bundling the repurchase with a new commercial relationship — a product and distribution partnership with Barings, MassMutual's own alternatives affiliate — turning a pure balance-sheet cleanup into a mutually beneficial commercial deal.13 It is a reminder that sophisticated capital-structure work is often as much about negotiation and relationship as it is about arithmetic. The December premium, meanwhile, was simply the price of speed: Invesco decided that owning its cash flows a decade and a half early was worth paying up for. Whether that judgment proves wise depends on what the company does with the freed-up capital — the eternal test of any capital-allocation decision.

The deleveraging campaign extended to conventional debt as well. During 2025 Invesco repaid in full a $500 million term loan it had taken out earlier in the year, and in January 2026 it redeemed a further $500 million of senior notes that had reached maturity, funding that redemption through its revolving credit facility to capture a lower floating rate and retain the flexibility to pay it down as cash allowed.13

With the balance sheet visibly lighter, Schlossberg pivoted to returning capital. In February 2026, Invesco's board authorized a fresh $1.0 billion common share repurchase program with no stated expiration, and the company raised its quarterly common dividend to $0.215 per share.3 On the first-quarter 2026 earnings call, CFO Allison Dukes framed the ambition concretely: a total payout ratio — combining common dividends and buybacks — targeted near 60% for 2026.3 This is the clearest evidence that the clean-up is real rather than rhetorical. For years, the preferred drag and the leverage had choked common capital returns; now the cash is beginning to flow toward common holders in a disciplined, quantified way.

Behind the balance-sheet work sits a quieter operational overhaul that matters just as much to the long-term cost structure: the migration of Invesco's investment operations onto a single "hybrid" technology platform, run in partnership with an outsourced provider. In plain terms, Invesco is replacing a patchwork of legacy systems — many of them inherited, predictably, from all those acquisitions — with one modern, largely outsourced backbone for trading, data, and portfolio operations. On the first-quarter 2026 call, Dukes guided that the implementation would be complete by the end of 2026 and would deliver at least $60 million of annual cost savings beginning in 2027, once the one-time implementation costs of roughly $10 to $15 million per quarter roll off.3 This is the unglamorous engine of the margin story: scale in asset management only becomes profit if the cost base is genuinely fixed and increasingly automated, and platform consolidation is how that happens.

Schlossberg has also been reshaping what Invesco does, not just how it is financed. Rather than acquire, he has been forging partnerships to push into faster-growing corners of the market — notably alliances with Barings and with the Liechtenstein-based alternatives specialist LGT Capital Partners to build out private-markets products for wealth-management and defined-contribution clients.3 Private markets — real estate, private credit, infrastructure — carry higher fees and stickier assets than public index funds, and they are exactly where the industry's fee-compression pressure is weakest. It is a logical place for a fee-squeezed manager to hunt, though Invesco enters it as a relatively small player against entrenched giants like Blackstone and Apollo.

The credibility question every investor should ask is whether Schlossberg's discipline will survive the next temptation. Asset-management CEOs have a long history of promising restraint and then reaching for the next empire-building deal when a rival puts an asset in play. So far, the behavioral evidence supports him: he has pruned rather than acquired, divesting the Intelliflo technology unit, entering a joint venture in India through a partial sale, and striking a sub-advisory partnership with CI in Canada that will move roughly $19 billion of AUM off Invesco's books.3 The narrative has been consistent across calls — a rare virtue in a company whose past was defined by strategic lurches. But the true test will come the moment a large, distressed competitor becomes available at a "strategic" price — and Invesco's own history warns exactly how that story can end.

VIII. Segment Economics: The "Mix Shift" and QQQ's Structural Re-engineering

Invesco reports as a single operating segment — Investment Management — which sounds simple until you realize it obscures a civil war being waged inside the income statement. The war is between fee-rich assets that are shrinking and fee-poor assets that are growing, and the industry's term of art for it is the "mix shift." It is the most important dynamic in the business, so it is worth slowing down to explain in plain terms.

Imagine Invesco's revenue as water flowing through pipes of different widths. The active equity and fixed-income funds are wide pipes: they carry a high fee yield, on the order of fifty to seventy basis points, meaning every dollar of assets generates a lot of revenue. But those pipes are draining — chronic industry outflows mean less water flows through them each year. The passive ETFs and index products are narrow pipes: they charge only a handful of basis points, so each dollar generates little revenue. But they are filling fast, capturing the overwhelming share of net new money. Invesco gathered $81.2 billion of long-term net inflows in 2025, and the bulk of it went into those narrow, low-fee pipes.2

The consequence shows up in a single, telling metric: net revenue yield, which measures how many basis points of revenue Invesco earns across its whole asset base. On the company's older, cleaner measure — excluding performance fees and QQQ — that yield fell from 32.4 basis points in 2023 to 30.2 basis points in 2024.4 Read that decline carefully, because it captures the entire strategic dilemma: Invesco must gather assets faster every year just to stand still on revenue. Growing AUM while your yield compresses is like running up a down escalator. Encouragingly, on the first-quarter 2026 call, CFO Dukes argued the compression was moderating and might be approaching "a degree of stabilization or an inflection point," with the blended net revenue yield around 22.9 basis points on the newer, post-QQQ basis.3 Whether that inflection holds is one of the two or three things worth watching most closely; it depends entirely on the future direction of the mix shift, which no management team controls.

The QQQ machine, finally switched on

Now to the crown jewel — and its strange, decades-long structural handicap. For its first twenty-six years, the Invesco QQQ Trust was organized as a Unit Investment Trust, or UIT. A UIT is a fossil of an earlier era of fund regulation: a rigid, largely un-managed vehicle that essentially holds a fixed basket and runs on autopilot. QQQ's UIT structure carried a literal termination date of March 4, 2124, and, more importantly, it prohibited the fund from doing things modern ETFs take for granted.16 It could not lend out its securities. It could not immediately reinvest the dividends its holdings paid, instead letting cash pile up until quarter-end — a subtle drag on returns. And here is the part that matters most for Invesco's shareholders: under the old structure, Invesco did not collect a conventional management fee on QQQ at all. It was compensated through a sponsor arrangement, while the trust's expenses were paid out directly to third parties.15

In 2025, Invesco set out to fix this. It proposed converting QQQ from a UIT into an open-end management investment company — a normal, modern ETF. The proposal went to the fund's shareholders, who approved it, and QQQ began trading in its new open-end form on December 22, 2025.17 The mechanics were carefully engineered to be tax-free to existing holders, with BNY shifting from trustee to custodian and administrator and a new board of trustees installed.15

Two things changed that investors should understand. First, the fee. The total expense ratio was lowered from 0.20% to 0.18%, structured as a "unitary" fee — a single all-in charge out of which Invesco now pays substantially all of the fund's operating costs, including the index-licensing fee owed to Nasdaq, and keeps the remainder as revenue.15 The reduction saved shareholders an estimated $70-plus million a year in aggregate, but the strategically decisive point is that, for the first time, Invesco began earning a management fee on QQQ.15 Under its license agreement, Invesco pays Nasdaq an index royalty of roughly 0.08%, leaving it something on the order of a dime per hundred dollars, net of the royalty, to cover costs and generate profit.153 On a base of roughly $400 billion, even a net retention of a few basis points translates into a large, high-margin, and remarkably stable revenue stream — arguably the highest-quality earnings Invesco owns.

But the outline's most seductive claim about the conversion deserves a skeptic's scrutiny. The bull narrative held that the new structure would unlock "a massive, high-margin future profit pool" from securities lending on QQQ's ultra-liquid holdings. Invesco's own CEO threw cold water on that on the Q1 2026 call. Asked directly what securities-lending revenue the Qs might generate, Schlossberg was candid: the opportunity is "there, but they're not super large," and "we don't see that as a huge opportunity."3 That is a striking gap between the promotional framing and management's own guidance, and it is exactly the kind of claim a neutral analyst should flag. The real prize of the conversion is not securities lending; it is the management fee itself.

The QQQ ecosystem, not just the ticker

One of the smartest things Invesco has done with QQQ is refuse to treat it as a single product. Over the years it has built an entire "innovation suite" of related vehicles around the Nasdaq-100 brand — a family of products that, by management's account on the Q1 2026 call, totals roughly $550 billion in assets worldwide.3 The most important sibling is QQQM, a lower-cost, lower-share-price twin launched to capture cost-conscious, long-term, buy-and-hold investors — precisely the sort who might otherwise be tempted away by a cheaper competitor. Here is the counterintuitive lesson management repeatedly emphasizes: rather than cannibalizing the flagship, QQQM expanded the overall pool of Nasdaq-100 assets Invesco controls, letting the firm serve traders (who prize QQQ's unrivaled liquidity) and savers (who prize QQQM's lower fee) without forcing either group to defect. It is a segmentation strategy — the same product, priced and packaged two ways for two audiences.

Invesco has also begun exporting the brand. It extended the QQQ lineup into Hong Kong in 2024 and was rolling it into Japan in 2026, with a UCITS version already available for European and international institutions.3 The strategic bet is that the Nasdaq-100 — a basket of American technology champions — is a globally desired export, and that Invesco's decades of brand-building and marketing spend give it a head start in each new market. Whether that head start survives the arrival of cheaper clones is now, as we will see, the central question hanging over the whole franchise.

The quieter growth engines

QQQ dominates the headlines, but the more revealing story about where Invesco is actually growing lies in a few less-glamorous capabilities that scale beautifully. The first is separately managed accounts, or SMAs — customized portfolios held directly in an investor's own account rather than pooled in a fund, which allows for personalized tax management. Invesco's SMA platform reached roughly $37 billion in assets by early 2026 and was growing at a blistering annualized organic rate of around 19%, among the fastest in the U.S. wealth market.3 The second is active ETFs — funds that put human stock- and bond-picking inside the cheap, tax-efficient ETF wrapper — where Invesco managed over $20 billion, rising to more than $35 billion including index strategies run by its active teams.3

Notice the common thread: personalization and tax efficiency. On the Q1 2026 call, Schlossberg framed the entire forward strategy around a shift toward after-tax returns and customization in the wealth channel, arguing that ETFs, SMAs, and model portfolios are the three vehicles best positioned to capture it.3 This is a coherent and evidence-backed thesis — the growth rates are real and the demand is visibly there. The catch, familiar by now, is that these vehicles are structurally lower-fee than the active mutual funds they are replacing. Invesco is winning the products of the future; it is simply winning them at a fraction of the margin of the products of the past.

One further capability deserves mention because it quietly generates high-quality revenue: Invesco's international fundamental equity franchise, anchored by its Global Equity Income Fund, which on the Q1 2026 call management flagged as the top-selling retail active fund in the Japanese market, having grown to roughly $23 billion in assets at an attractive fee yield.3 It is a useful reminder that active management is not uniformly dying — in the right product, in the right geography, human-managed equity funds can still gather assets at healthy margins. Invesco's problem has never been that active management is worthless; it is that the firm owns too much of the wrong active product and not enough of the right kind.

The China wedge

One more piece of Invesco's economics deserves attention because it is both unusually profitable and unusually fragile: the company's Chinese joint venture. 景顺长城 Invesco Great Wall is a fund-management JV in which Invesco holds a 49% economic interest, and it has been one of the firm's genuine growth engines. In 2024 the venture contributed $318.1 million in net revenues on roughly $93.2 billion of assets; by the first quarter of 2026 its AUM had climbed to a record of about $142 billion, growing at a 31% annualized organic rate even amid volatile global markets.43 Its margins, management noted, have run in the high-50s to low-60s percent range — extraordinary for this business.3

The fragility is regulatory. Chinese authorities have mandated retail fee cuts across the domestic fund industry, and the venture's growth is skewed toward lower-fee "Fixed Income Plus" products — balanced funds that sit between pure bonds and equities. On the Q1 2026 call, Dukes acknowledged that JV fee rates would likely "compress a bit over time," even as she argued the scaled, hard-to-replicate platform would preserve strong margins.3 It is a microcosm of the whole company: a highly profitable business growing fast in low-fee products, running to stand still against fee compression. Which brings us to the question every long-term investor must answer for themselves — can this company actually win from here, and what would break the case?

IX. Strategic Playbook, Risks, and the Bull vs. Bear Case

To war-game Invesco's future, it helps to run its business through two analytical lenses that sophisticated investors use to test whether a competitive advantage is real or illusory: Hamilton Helmer's 7 Powers and Michael Porter's Five Forces. Both frameworks converge on the same uncomfortable conclusion — Invesco has genuine advantages, but the most cited one is eroding in real time.

The 7 Powers view: which moats are real?

Of Helmer's seven sources of durable advantage, two are plausibly present at Invesco. The first is scale economies. Running a near-$640-billion ETF platform lets Invesco spread the fixed costs of compliance, technology, and distribution across an enormous asset base, absorbing regulatory and operational burdens that would crush a smaller issuer.3 This is real, and it is the foundation of the bull case: Invesco has arguably reached "escape velocity" scale, placing it among the consolidated survivors of the industry's shakeout rather than among the stranded mid-tier casualties Trian warned about.

The second alleged power is a cornered resource — the exclusive Nasdaq license behind QQQ. For decades this was Invesco's most-cited moat: only Invesco could sell the definitive Nasdaq-100 ETF, and that exclusivity was said to be un-replicable. Here is where the story turns, and where any analysis written in mid-2026 must part company with the optimistic framing. In April 2026, Nasdaq announced it would extend Nasdaq-100 licensing to a select set of new partners, ending Invesco's exclusivity.18 Within weeks the giants pounced: State Street launched a competing Nasdaq-100 fund (QNDX) at a 0.10% expense ratio, and on July 9, 2026, BlackRock's iShares launched its own — ticker IQQ — at 0.12% gross, waived to 0.10% through July 2027, and priced at a low $24 per share to court dollar-based retail buyers.19 Both undercut QQQ's headline 0.18%. The "cornered resource" is no longer cornered. It has become, at best, a brand advantage rather than a legal monopoly — a very different and more contestable thing.

Management's rebuttal, delivered forcefully on the Q1 2026 call, is worth taking seriously even as we scrutinize it. Schlossberg argued that ETF investors judge "total cost of ownership," not headline fees — that QQQ's unmatched liquidity, razor-thin bid-ask spreads, deep options and derivatives ecosystem, twenty-five-plus years of brand recognition, and enormous entrenched institutional and retail base create switching costs far higher than a two-basis-point fee gap suggests. For a large trader, the cost of crossing a wide bid-ask spread can dwarf a rounding-error difference in the annual expense ratio, which is why the most liquid ETF in a category tends to keep the trading crowd even when cheaper clones exist. Tellingly, Schlossberg also cited harder evidence: taxes. A long-term QQQ holder sitting on large embedded capital gains cannot switch to a cheaper clone without selling and triggering a tax bill, which effectively locks in the installed base. He pointed, too, to QQQM as proof that adding products expands rather than erodes the franchise.3 These are legitimate points, and the tax-lock argument in particular is a genuine switching-cost moat.

But the honest verdict is that the moat has narrowed from "legal exclusivity" to "brand plus liquidity plus tax friction" — durable for the existing $400 billion, but a real threat to Invesco's share of future Nasdaq-100 flows, which will now be split with the two most powerful distributors in the industry. And here the historical precedents cut against complacency. The plain-vanilla S&P 500 ETF market and, more recently, the spot-Bitcoin ETF market both showed that when powerful issuers compete on price, fees grind toward zero and assets migrate faster than incumbents expect — a dynamic the Benzinga coverage of BlackRock's launch explicitly invoked.19 New money, in particular, has no tax lock-in and no loyalty; a first-time buyer opening a brokerage app has every reason to pick the cheapest Nasdaq-100 ETF on the screen, and starting in July 2026 that was no longer necessarily QQQ. The installed base may be defensible; the marginal buyer is now genuinely up for grabs.

This is the crux of the myth-versus-reality question at the heart of Invesco's story. The consensus narrative — the one the outline itself leans into — treats QQQ as an unassailable, un-replicable monopoly asset. The reality as of mid-2026 is more sober: QQQ is a powerful brand with a deep liquidity and tax moat around its existing assets, now competing for new flows against cheaper products from the two largest ETF machines on Earth. That is still an enviable position. It is not the impregnable fortress the bull case imagines.

Porter's Five Forces: a tough neighborhood

Porter's framework paints asset management as a structurally difficult business, and Invesco sits in the harder end of it. The bargaining power of buyers is extreme: the mega-distribution wealth platforms — Morgan Stanley, Merrill, Schwab and their peers — control access to the end investor and use that leverage to demand fee rebates and cheaper share classes. On the Q1 2026 call, an analyst pressed Schlossberg directly on rising shelf-space fees at platforms like Schwab; his answer, that Invesco would evaluate any new platform fees case by case and did not expect a "material impact," was measured but conceded the underlying pressure.3 The threat of substitutes is equally high: direct indexing, model portfolios, and near-zero-cost core beta all offer investors ways to get exposure without paying a traditional manager. And competitive rivalry is ferocious, dominated by two firms — BlackRock and Vanguard — whose scale lets them win pure price wars, as the QQQ clones now demonstrate.

The risk radar

Three risks stand out as material, and they compound one another. The first is concentration risk: QQQ alone represents close to a fifth of Invesco's assets and a still larger share of its highest-quality revenue, which leaves the company acutely exposed to a severe technology-led drawdown in the Nasdaq-100. The vulnerability is not hypothetical — in the first quarter of 2026, QQQ swung to net outflows amid volatility and profit-taking, a reminder that its assets are not sticky retirement money but partly hot, tactical, trader-driven capital that can leave as fast as it arrives.3 The second is active attrition: if the high-yielding Oppenheimer-legacy active funds melt faster than the low-fee passive products can scale in revenue terms, overall profitability compresses even when headline flows look positive. The third is the new fee war on QQQ described above, which could, over years, chip away at both the growth and the pricing of the single most valuable franchise Invesco owns.

The bull and bear cases, honestly stated

The bull case rests on three legs. The balance-sheet clean-up is real and mechanically accretive: retiring the preferred and paying down debt transfers hundreds of millions of dollars of annual cash flow toward common shareholders, and the newly authorized buyback and 60%-payout target put numbers on it.13 The QQQ conversion switched on a genuine management fee for the first time, structurally improving the quality of Invesco's earnings.15 And the operating leverage is showing up: adjusted operating margin climbed from 28.2% in 2023 to 33.4% in 2025 and 34.5% in the first quarter of 2026, with management targeting the high-30s as its cost-simplification and hybrid-platform programs mature.13 The company has posted eleven consecutive quarters of positive organic growth, with real strength in Asia-Pacific, EMEA, fixed income, and a fast-growing separately managed account platform.3

The bear case is equally coherent, and it is fundamentally about arithmetic that management cannot repeal. Active outflows are a melting ice cube, and low-fee passive inflows cannot replace lost active revenue dollar-for-dollar — the mix shift is a one-way ratchet on yield. The competitive rivalry from Vanguard and BlackRock is not a threat Invesco can out-spend or out-scale; those firms are larger and structurally lower-cost, and they have now planted their flags directly on Invesco's most prized turf. And the whole enterprise remains a price-taker in an industry where the buyers — the distribution platforms — hold the whip hand on fees. Strip away the one-time benefits of the capital-structure clean-up, and the underlying organic business is still running up a down escalator.

The activist's stress test

If a skeptical activist or short-seller sat across the table from Schlossberg today, what would they press on? Four things. First, portfolio complexity: even after the divestitures, Invesco remains a sprawling, multi-brand, multi-geography organization assembled from a dozen acquisitions, and complexity is where costs and mediocrity hide. Second, the remaining preferred: roughly $2.5 billion of MassMutual's stake still sits ahead of common holders, and until it is gone the capital structure is not truly clean — the pace of its retirement is a direct test of management's promises. Third, the QQQ concentration: a single product driving so much of the firm's highest-quality revenue is a governance and risk-disclosure question as much as a market-risk one, and the arrival of cheaper competitors sharpens it. Fourth, capital-allocation discipline: the whole bull case rests on management continuing to return cash and resist empire-building M&A, and the market has been fooled by asset-management CEOs' discipline promises before. The reassuring counterpoint is that Invesco's recent behavior — buybacks, debt paydown, divestitures, a quantified payout target — matches its words. The activist's job is to keep watching for the moment the words and the behavior diverge.

A brief note on the softer overlays that a thorough diligence process would touch. On technology, management spent much of the Q1 2026 call describing how it is embedding artificial intelligence across research, client servicing, and operations, estimating that close to 80% of its roughly 7,500 employees use such tools in some form — a plausible efficiency tailwind, though one every competitor is chasing simultaneously, which means it is more likely to be table stakes than a durable edge.3 On related-party dynamics, the MassMutual relationship — simultaneously a large shareholder, the preferred holder, and now a commercial partner through Barings — is worth monitoring for governance cleanliness, though nothing in the disclosures suggests it is anything other than arm's-length. These are watch-items, not alarms.

The KPIs that actually matter

An investor does not need to track dozens of metrics to follow this story. Three will tell most of the tale. First, net revenue yield in basis points — the single cleanest measure of whether the mix shift is stabilizing (as management now claims) or still grinding lower; it is the escalator's speed. Second, QQQ's assets and net flows relative to its new competitors — the real-time scoreboard on whether the brand-and-liquidity moat is holding the installed base and defending its share of Nasdaq-100 inflows against IQQ and QNDX. Third, the adjusted operating margin against management's high-30s ambition — the proof of whether cost discipline and scale are genuinely translating into profit as the preferred and leverage roll off. Watch those three, and the rest of Invesco's complexity resolves into a legible picture.

X. Epilogue & Outro

Invesco in mid-2026 is a company caught between two identities it never fully chose. It is, on one hand, the accidental custodian of one of the most valuable brands in modern finance — a four-letter ticker that a generation of investors treats as synonymous with American technology itself. It is, on the other hand, a traditional active manager still digesting an expensive acquisition of assets the market no longer wants, running hard just to keep its revenue from sliding.

The Flanagan era bought scale and, in the end, mortgaged the balance sheet to do it. The Schlossberg era has been an act of financial restoration — retiring the preferred, paying down debt, switching on QQQ's fee, and finally routing cash back to common shareholders. That work is genuine, quantifiable, and to management's credit, executed with a consistency of narrative across filings and calls that the company's scandal-scarred past did not always display. Whether it amounts to a durable turnaround or merely a well-managed holding action depends on forces largely outside Atlanta's control: the pace of the active-to-passive migration, the ferocity of a fee war that BlackRock and State Street have only just opened on QQQ, and the direction of a revenue yield that has spent a decade compressing.

The company has stopped digging and started building. The open question — the one the next several years of net flows, yields, and margins will answer — is whether it is building on rock or on the shrinking island of high-fee active management. For now, Invesco has bought itself the one thing its 2004 self could only have dreamed of: time, a clean balance sheet, and a fighting chance.

References

-

Invesco Ltd. Form 10-K for fiscal year ended December 31, 2025 — U.S. Securities and Exchange Commission ↩↩↩↩↩↩↩↩

-

Invesco Reports Results for the Three Months and Year Ended December 31, 2025 — PRNewswire, 2026-01-27 ↩

-

Invesco Reports Results for the Three Months Ended March 31, 2026, and Q1 2026 earnings call (April 28, 2026) — PRNewswire ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Invesco Ltd. Form 10-K for fiscal year ended December 31, 2024 — U.S. Securities and Exchange Commission ↩↩

-

Enforcement claims administration: Invesco Funds Group / AIM market-timing settlements — U.S. Securities and Exchange Commission ↩

-

AMVESCAP to Acquire PowerShares Capital Management — FTV Capital, 2006-01-23 ↩

-

Invesco to Acquire MassMutual's OppenheimerFunds — Financial Times, 2018-10-18 ↩↩

-

Invesco Completes Acquisition of Guggenheim's ETF Business — ETF Strategy, 2018-04-06 ↩

-

Invesco Ltd. Announces Changes to Its Board of Directors (Trian's Peltz and Garden to step down) — PRNewswire, 2022-02-14 ↩↩↩

-

Invesco in Merger Talks with State Street Global Advisors (WSJ report) — Citywire, 2021-09-16 ↩

-

Invesco President and CEO Marty Flanagan to Retire; Andrew Schlossberg to Become President and CEO on June 30, 2023 — PRNewswire ↩↩

-

Invesco and MassMutual Announce Repurchase of $1 Billion of Invesco Preferred Stock and New Partnership with Barings — PRNewswire, 2025-04-22 ↩↩

-

Invesco Ltd. Form 8-K — repurchase of $500 million Series A preferred stock (December 2025) — StockTitan ↩

-

Invesco QQQ Trust Definitive Proxy Statement (reclassification to open-end fund) — U.S. Securities and Exchange Commission ↩↩↩↩↩↩

-

Invesco QQQ Trust, Series 1 Form 485BPOS (UIT structure, 1999 inception, sponsorship history, 2124 termination) — U.S. Securities and Exchange Commission ↩↩↩

-

Invesco QQQ Shareholders Vote to Approve Modernization — PRNewswire, 2025-12-19 ↩

-

Investors Will Soon Have Two New Alternatives to Invesco QQQ — The Motley Fool, 2026-04-24 ↩↩

-

Nasdaq-100 ETF: BlackRock Launches IQQ to Challenge QQQ — Benzinga, 2026-07 ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube