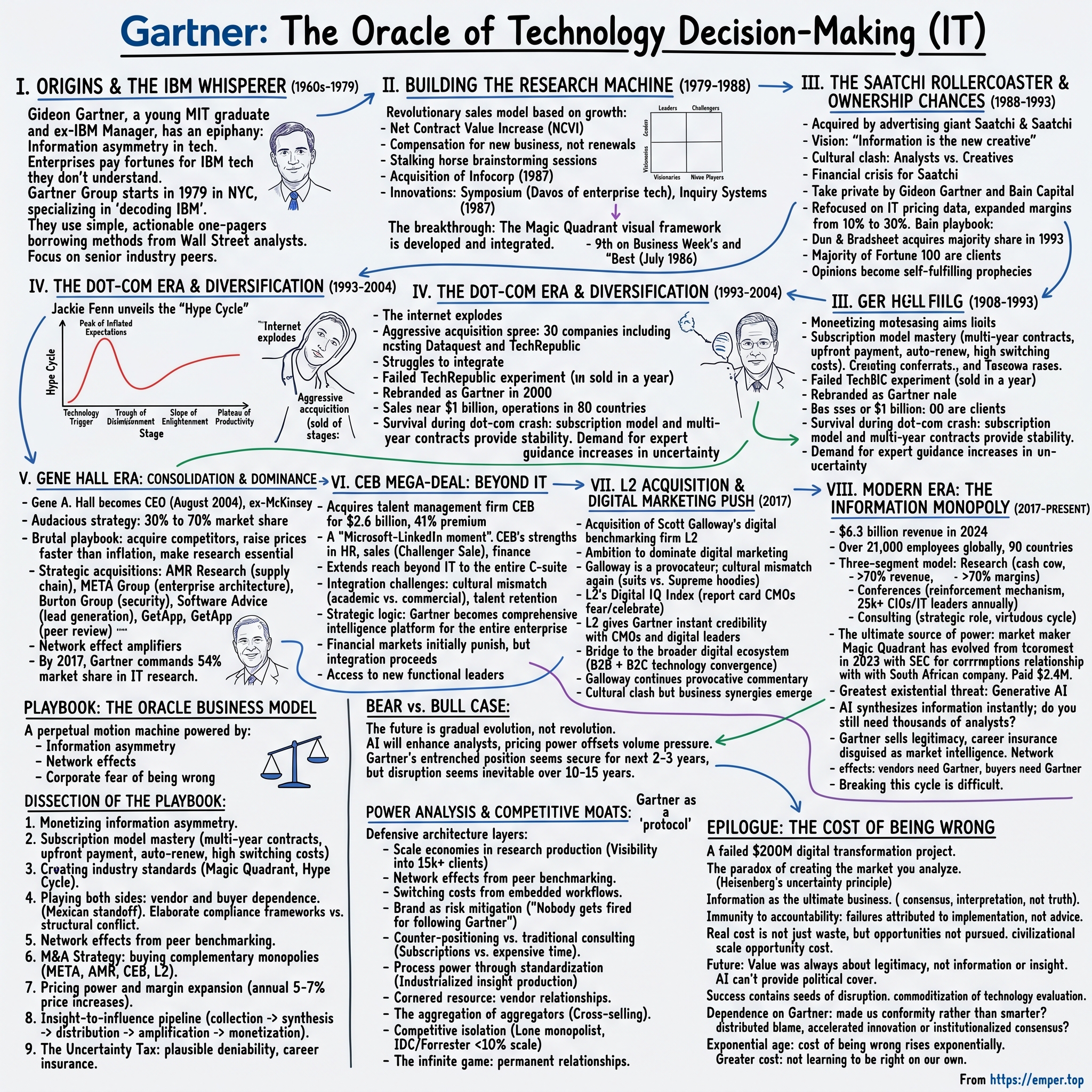

Gartner: The Oracle of Technology Decision-Making

I. Introduction & Episode Roadmap

Picture this: It's 2024, and a Fortune 500 CIO is about to sign a $50 million cloud infrastructure deal. Before putting pen to paper, she checks one thing—what does Gartner say? In boardrooms from Silicon Valley to Singapore, this scene plays out thousands of times daily. The company that started as a two-person consultancy helping clients navigate IBM's labyrinthine product catalog has become the ultimate kingmaker in enterprise technology, a $6.3 billion S&P 500 component whose opinions can make or break billion-dollar markets.

The story of Gartner is fundamentally a story about information asymmetry—and one man's realization that in the technology industry, knowing what to buy was becoming as valuable as the technology itself. When Gideon Gartner left his comfortable perch as a top-rated Wall Street analyst in 1979, he wasn't just starting another research firm. He was creating an entirely new business model: the commercialization of technology intelligence.

Think about the audacity of the value proposition. Gartner doesn't build software, manufacture hardware, or implement systems. It sells opinions—expensive opinions, packaged as research, delivered through subscriptions that can cost enterprises millions annually. Yet today, 73% of the Fortune 1000 wouldn't dream of making a major technology decision without consulting Gartner's research. The company commands a 54% market share in IT research, dwarfing competitors IDC and Forrester, which hover around $300 million in revenue—less than 5% of Gartner's scale.

How did a startup focused on decoding IBM's product strategy evolve into the supreme court of technology decisions? How did it survive the dot-com bust, navigate multiple ownership changes, and emerge stronger from each crisis? And perhaps most intriguingly, how did it build a business model so powerful that clients pay premium prices for research that often critiques the very vendors who also pay Gartner millions for access and influence?

This is a story of monopolistic market dynamics, information economics, and the peculiar psychology of enterprise decision-making. It's about creating standards—like the Magic Quadrant—that become so embedded in corporate culture that not appearing on them becomes an existential threat for vendors. It's about building switching costs so high that even when clients grumble about seven-figure renewal invoices, they sign anyway because the alternative—making technology decisions without Gartner—feels like flying blind.

From Gideon Gartner's first insight about IBM's market dominance to today's AI-threatened future, we'll trace how this company built an information empire that touches nearly every technology decision made by the world's largest organizations. Along the way, we'll unpack the playbook of turning expertise into monopoly, the art of playing both sides of a market, and the ultimate business model: selling certainty in an uncertain world.

II. Origins: The IBM Whisperer (1960s–1979)

The conference room at System Development Corporation in Santa Monica was thick with cigarette smoke and tension. It was 1963, and Gideon Gartner, a young MIT graduate with an unusual background—he'd helped program Israel's first transistor computer, the WEIZAC—was watching his colleagues struggle with a problem that would define his career: IBM was everywhere, IBM was everything, and nobody really understood what IBM was selling.

Gartner had taken an unconventional path to this moment. After his stint in Israel, where he'd worked on one of the world's earliest computers, he'd been recruited by Philco, then poached by IBM itself. At Big Blue, he rose quickly to Manager of Market Information, a position that gave him an insider's view of how the computing giant operated. But it was what happened after he left IBM that would prove revolutionary. By 1970, Gartner had made the leap to Wall Street, joining E.F. Hutton as a securities analyst. It was here that his unique IBM expertise became gold. While other analysts struggled to decode IBM's Byzantine product strategies and pricing models, Gartner could predict the company's moves with uncanny accuracy. He was voted the top individual technology analyst on Wall Street every year from 1972 through 1977 in Institutional Investor Magazine's annual poll—an unprecedented streak that made him the most sought-after voice in technology investing.

At Oppenheimer & Co., where he rose to VP and head of the Technology Group, eventually becoming a partner, Gartner had an epiphany that would reshape an entire industry. While working at Oppenheimer in the late 1970s, Gartner realized that his investor insights would be valuable to computer manufacturers and end users too. The same intelligence that helped investors make millions could help enterprises avoid millions in mistakes.

The timing was perfect. By 1979, IBM controlled nearly 70% of the global computer market. Every major corporation was essentially an IBM customer, but few understood what they were buying. IBM's product line had become so complex—with overlapping systems, incompatible architectures, and constantly shifting roadmaps—that even IBM's own salespeople struggled to explain it coherently. Companies were spending fortunes on technology they didn't understand, making decisions that would lock them into architectures for decades.

Gartner joined with David L. Stein, an industry veteran, to form Gartner Group in 1979. Gideon Gartner's new firm specialized in information about IBM and its products. The initial business model was elegantly simple: they would decode IBM for the rest of the world. But Gartner brought something revolutionary to this mission—a methodology borrowed from Wall Street but foreign to technology consulting.

Gartner initially operated in an office rented from its first client, the New York brokerage house Dillon, Read & Co. This wasn't just convenient—it was strategic. Being embedded with a major financial firm gave Gartner instant credibility and access to the money managers who controlled technology budgets. By 1983, the firm employed 80 research analysts and generated $8 million in revenue.

What made Gartner different wasn't just what they knew—it was how they delivered it. Gartner's reports were often delivered as a one-pager containing only high-level insights, a radical departure from the dense, technical tomes that consulting firms typically produced. Having come from Wall Street, Gartner adopted the idea of employing senior industry people, who were in fact "peers" of their prospective clients. This was a departure from the current industry practice at the time, where analysts were relatively young and relatively inexperienced albeit bright.

The genius of Gartner's approach was treating technology intelligence like financial intelligence. Just as Wall Street analysts helped investors navigate complex markets, Gartner analysts would help enterprises navigate the increasingly complex technology landscape. And just as financial research commanded premium prices from those who needed it most, so too would technology research. The IBM whisperer had found his calling—and an industry was about to be born.

III. Building the Research Machine (1979–1988)

The conference room at Gartner Group's modest Manhattan office was buzzing with an energy that would have seemed bizarre to any traditional consultant. It was 1982, and Gideon Gartner was running what he called a "stalking horse" session—a collaborative brainstorming technique he'd invented where analysts would present deliberately controversial positions to spark debate. "IBM will abandon the mainframe within five years," one analyst declared, knowing it was absurd but using it to surface insights about IBM's real strategy. This wasn't how McKinsey or Booz Allen worked. This was something entirely new.

Gartner instituted a sales measurement and compensation scheme, based upon how IBM had measured its rental sales, but novel when applied to consulting/advisory firms: since Gartner Group sold annual renewable contracts and recorded "Contract Value", it based progress reporting and compensation on the growth of appropriate Contract Value during a period of time; this was called Net Contract Value Increase (NCVI). Uniquely, compared with all prior consulting and advisory models, all variable compensation was based upon growth and not on revenue from renewals, an important factor in developing a strong growth culture.

This compensation model was revolutionary. Traditional consulting firms paid bonuses based on total billings, which meant senior partners could coast on existing relationships. At Gartner, you only ate what you killed—new business, not renewals. It created a hunger that permeated the entire organization. Analysts weren't just researchers; they were entrepreneurs within the firm, constantly seeking new ways to add value.

The Gartner methodology evolved rapidly during these early years. While competitors produced 50-page reports that took months to complete, Gartner's one-page research notes could be turned around in days. Each note followed a rigid structure: situation, implications, recommendations. No fluff, no academic theory—just actionable intelligence. Clients loved it. By 1985, Gartner had grown so rapidly that it needed to restructure. In 1985, Gartner's brokerage and investment division separated from the firm to become a wholly owned subsidiary called Gartner Securities, later renamed SoundView Financial Group.

The real breakthrough came with the development of what would become Gartner's most famous framework. Gartner analysts developed the Magic Quadrant visual framework of placing companies within defined market quadrants during the early 1980s and began to integrate the methodology into their presentations and later reports. The elegance of the Magic Quadrant was its simplicity: a two-by-two matrix plotting vendors on axes of "completeness of vision" and "ability to execute." Leaders, Challengers, Visionaries, Niche Players—every technology vendor suddenly had a label, a position, a destiny. In July 1986, Gartner rebranded as Gartner Group and became a publicly traded company. The IPO was a watershed moment—Wall Street was now financing the very firm that decoded technology for Wall Street. In January 1987, Gartner Group acquired another technology research firm, the Cupertino-based Infocorp. This acquisition brought critical West Coast presence and deep expertise in the emerging personal computer market.

That same year Gartner reported $25 million in sales and $1.9 million in earnings. The numbers were impressive, but what really caught attention was Gartner's client list. By 1987, the majority of the Fortune 100 were Gartner clients. The company was ranked 9th on Business Week's "Best Small Companies" list, #1 in profitability.

The secret to Gartner's explosive growth wasn't just good research—it was the creation of an entirely new business model. Other innovations were introduced, in areas such as research-hiring interview methods, conferences including the breakthrough Symposium, inquiry systems to connect clients with internal analysts. The Symposium, launched in the mid-1980s, would become the Davos of enterprise technology—the one conference where CIOs had to be seen.

But perhaps the most ingenious aspect of Gartner's model was how it created dependency. Once a company subscribed to Gartner's research, stopping the subscription felt like flying blind. The cost of being wrong on a major technology decision far exceeded Gartner's subscription fees. It was insurance disguised as intelligence.

The Magic Quadrant, meanwhile, had evolved from an internal analytical tool into something far more powerful—a kingmaking mechanism. Vendors began structuring entire product strategies around moving from "Niche Players" to "Leaders." Being absent from a Magic Quadrant could kill a startup's enterprise sales efforts. Being poorly positioned could cost millions in lost deals.

By 1988, Gartner had built something unprecedented: a research machine that didn't just analyze the technology industry—it shaped it. The company's opinions had become self-fulfilling prophecies. When Gartner declared a technology trend, vendors pivoted, buyers budgeted, and markets moved. The research firm had become more powerful than many of the companies it researched. But this success had attracted attention from an unexpected quarter—the acquisition-hungry advertising giant Saatchi & Saatchi was about to make Gartner an offer it couldn't refuse.

IV. The Saatchi Rollercoaster (1988–1993)

Maurice Saatchi leaned back in his London office chair, surveying a wall covered with acquisition targets. It was early 1988, and the advertising mogul's empire was expanding far beyond Madison Avenue. "Information," he told his brother Charles, "is the new creative." On that wall, circled in red marker, was Gartner Group—a company that seemed to have nothing to do with advertising but everything to do with the future Saatchi envisioned.

The U.K.-based Saatchi & Saatchi acquired Gartner Group in 1988. The deal, valued at $90.3 million, represented a massive premium for a company that had gone public less than two years earlier. For Gideon Gartner, who signed a contract to remain as CEO until April 1991, it seemed like the perfect marriage—access to global resources while maintaining operational independence.

The 1988 fiscal year validated the acquisition price: Gartner posted $40 million in revenue with $2.3 million in profit. The Saatchi brothers were ecstatic. They imagined Gartner's analytical capabilities enhancing their advertising services, creating a new kind of integrated business intelligence offering. But almost immediately, cracks began to show in this vision.

The cultural clash was immediate and profound. Gartner's analysts, accustomed to rigorous, data-driven methodology, found themselves in meetings with creative directors discussing "brand essence" and "emotional resonance." Saatchi executives, meanwhile, couldn't understand why Gartner needed so many expensive senior analysts when junior staff could surely write reports just as well. One Gartner veteran recalled a Saatchi executive asking, "Can't we just hire recent graduates and train them? How hard can it be to have opinions about computers?"

But the real crisis came from Saatchi's own precarious financial position. The advertising giant had gorged itself on acquisitions throughout the 1980s, borrowing heavily to finance its shopping spree. By late 1989, with a recession looming and clients cutting advertising budgets, Saatchi & Saatchi found itself desperately over-leveraged. The company that had swallowed Gartner was now choking on its own debt.

The fire sale began in late 1989. Saatchi needed cash, and every non-core asset was on the block. For Gideon Gartner, watching his company being shopped around like a distressed property was agonizing. But it also presented an opportunity. If Saatchi was desperate enough, perhaps he could buy his company back.

In 1990, Gartner Group was taken private by Gideon Gartner and other executives in an acquisition deal backed by funding from Bain Capital and Dun & Bradstreet, then a Bain client. The negotiation was brutal. Gideon Gartner delivered an ultimatum that would become legend in private equity circles: if he lost the bidding, he would quit immediately, taking key executives with him. Without Gartner and his team, the company would be worth a fraction of any bid price. It was corporate brinksmanship at its finest.

Bain Capital, still a relatively young private equity firm, saw in Gartner exactly the kind of business they loved: subscription-based, high-margin, with massive pricing power. Dun & Bradstreet, which provided business information services, understood the value of Gartner's intelligence network. Together, they backed Gideon's buyout.

Under Bain ownership, Gartner underwent a dramatic transformation. Under Bain ownership, Gartner refocused on IT industry pricing data and expanded its profit margins from 10 percent to 30 percent. The Bain playbook was surgical: cut non-essential costs, raise prices on captive customers, focus relentlessly on the most profitable services. Research that didn't directly drive subscription renewals was eliminated. The one-page research notes became even more focused, even more essential.

The transformation was remarkable. In less than two years, Gartner had tripled its profitability while barely growing revenues. The Saatchi era's expansionist dreams were replaced by Bain's operational excellence. Every analyst's productivity was measured, every client interaction tracked, every research note evaluated for its impact on contract renewals.

Dun & Bradstreet acquired a majority share in Gartner in 1993. Gartner went public again in October 1993, with Dun & Bradstreet maintaining a 50 percent stake. The second IPO was even more successful than the first. The market now understood what Gartner was: not a consulting firm, not a research company, but something unique—a subscription-based intelligence service with monopolistic characteristics.

For Gideon Gartner, however, the second IPO marked the end of an era. He sold his equity position and completely severed ties with the company in 1993. His departure was abrupt and final. The man who had created the IT analyst industry was walking away from his creation at the moment of its greatest triumph.

The Saatchi rollercoaster had taken Gartner from independence to conglomerate subsidiary to private equity portfolio company to public markets—all in just five years. Each transition had stripped away something non-essential while strengthening the core business model. What emerged was leaner, more profitable, and more powerful than ever. The company that had started as the IBM whisperer was now ready to become the oracle for the entire technology industry.

V. The Dot-Com Era & Diversification (1993–2004)

The Gartner conference hall in Orlando was electric with possibility. It was 1995, and analyst Jackie Fenn was about to unveil a framework that would define how the technology industry understood itself for decades to come. On the screen behind her appeared a simple curve—rising sharply, crashing dramatically, then climbing again more gradually. "We call it the Hype Cycle," she announced to the packed room of CIOs. "Every transformative technology follows this pattern: Technology Trigger, Peak of Inflated Expectations, Trough of Disillusionment, Slope of Enlightenment, and Plateau of Productivity."

The timing couldn't have been more perfect. The internet was exploding, and everyone—vendors, investors, enterprises—desperately needed a framework to understand which technologies were real and which were merely hype. Gartner had created not just a research tool but a language for discussing technological change.

With Gideon Gartner's departure, the company entered a new phase. No longer guided by its founder's vision, Gartner became more corporate, more systematic, and paradoxically, more aggressive. Over the next eight years, the company would embark on an acquisition spree that would have seemed unthinkable under its founder's cautious leadership.

Over the next eight years, Gartner acquired or made substantial investments in 30 companies, including the market research firm Dataquest and the online news outlet TechRepublic. The Dataquest acquisition in 1995 was particularly significant—it brought deep semiconductor and hardware market data that complemented Gartner's enterprise IT focus. TechRepublic, acquired during the height of the dot-com boom, was meant to give Gartner a foothold in online communities and user-generated content. The deals were part of a diversification strategy that coincided with the dot-com bubble, and Gartner acknowledged that it struggled to integrate these new companies into its operations. The TechRepublic experiment was particularly embarrassing—Gartner sold TechRepublic to CNET only a year after acquiring the company. The vision of becoming a multi-media technology intelligence empire had collided with the reality that Gartner's core competency was premium research, not mass-market content.

In 2000, Gartner changed its name from Gartner Group to simply Gartner—a subtle but significant shift that signaled its evolution from a research group to something broader. Sales neared the $1 billion mark, and the company operated in 80 countries. The global expansion had been methodical, following enterprises as they globalized their own IT operations.

But the real test came with the dot-com crash. Between March 2000 and October 2002, the NASDAQ fell 75%, wiping out trillions in market value. Technology spending froze. Startups that had been Gartner's fastest-growing customer segment vanished overnight. Yet remarkably, Gartner not only survived but thrived during the downturn.

The secret was the subscription model. While consulting firms saw projects cancelled and advisory firms watched deal flow evaporate, Gartner's multi-year contracts kept revenue flowing. More importantly, the crash actually increased demand for Gartner's services. In times of uncertainty, the need for expert guidance becomes more acute, not less. CIOs facing budget cuts needed Gartner's help to identify which technologies to keep and which to abandon. The Hype Cycle, introduced just five years earlier, became essential reading as executives tried to separate lasting innovation from temporary fads.

The dot-com era had taught Gartner a crucial lesson: stick to your core competency. The failed acquisitions and integration struggles of the boom years gave way to a more focused strategy. Gartner would be the premium research provider, period. Let others chase page views and advertising dollars. Gartner would focus on what it did best—charging premium prices for premium insights to enterprises that couldn't afford to be wrong.

By 2004, as the technology industry emerged from its deepest recession, Gartner had consolidated its position as the undisputed leader in IT research. The company that had introduced the Hype Cycle at the beginning of the bubble had successfully navigated its own journey through inflated expectations and disillusionment to reach a plateau of productivity. The stage was set for its next phase: building a true monopoly under new leadership that would transform Gartner from market leader to market dominator.

VI. The Gene Hall Era: Consolidation & Dominance (2004–2017)

Gene Hall stood before Gartner's board in Stamford, Connecticut, with a simple PowerPoint slide showing two numbers: 30% and 70%. It was August 2004, his first week as CEO, and the former McKinsey consultant was about to propose something audacious. "We have 30% market share," he said, pointing to the first number. "There's no reason we can't have 70%. The only question is whether we buy it or build it."

In August 2004, Gene A. Hall became Gartner's new CEO, replacing Michael D. Fleisher. Hall previously worked with the consulting firm McKinsey & Company before managing a division at Automatic Data Processing. His background was telling—McKinsey DNA combined with operational experience at ADP, a company that had built monopolistic positions in payroll processing. Hall understood scale economics and network effects. He saw in Gartner the potential for something unprecedented in professional services: a true monopoly.

Hall's strategy was elegantly brutal: acquire every meaningful competitor, raise prices faster than inflation, and make Gartner research so essential that not having it became a career risk for technology executives. The execution would span thirteen years and transform Gartner from a large research firm into an inescapable force in enterprise technology.

In 2008, Gartner reached $1.3 billion in revenues and achieved 40 percent of the IT research market. But Hall wasn't satisfied with 40%. He wanted dominance so complete that the question wouldn't be whether to subscribe to Gartner, but how much to subscribe.

The acquisition strategy began with surgical precision. In 2009, Gartner acquired AMR Research, a Boston-based research and advisory firm focused on supply chain management. AMR wasn't just another IT research firm—it was the leader in supply chain intelligence, with deep relationships in manufacturing and logistics. The acquisition brought Gartner into conversations it had never been part of before: operations, not just IT.

The META Group acquisition was even more strategic. META had been Gartner's most credible competitor in enterprise architecture and IT strategy. By absorbing META, Gartner didn't just eliminate competition—it acquired a different analytical perspective that could be integrated into its research. The Burton Group acquisition followed similar logic, bringing deep technical expertise in infrastructure and security.

But Hall's masterstroke was recognizing that the nature of technology decision-making was changing. The consumerization of IT meant that technology choices were no longer made exclusively by IT departments. Marketing was choosing marketing automation platforms. Sales was selecting CRM systems. HR was buying talent management software.

In March 2014, Gartner announced that it had acquired the privately held company Software Advice for an undisclosed amount. Software Advice wasn't a research firm—it was a lead generation platform that connected software buyers with vendors. The acquisition signaled Gartner's evolution from passive observer to active market maker.

Also in 2014, Gartner coined the term "Digital BizOps" and further developed the early philosophy for digital business operations. This wasn't just new terminology—it was Gartner's recognition that digital transformation was erasing the boundaries between IT and business operations. Every company was becoming a technology company, which meant every executive needed Gartner.

In July 2015, Gartner acquired Nubera, the business app discovery network that owns properties like GetApp (a peer review site), AppStorm, AppAppeal, further expanding its reach into the software selection process. These weren't traditional research acquisitions—they were digital properties that captured buyer intent data. Gartner was building a funnel that started with free software comparisons and ended with million-dollar research contracts.

The financial results were staggering. Revenue grew from under $1 billion when Hall took over to approaching $2 billion by 2016. More importantly, margins expanded dramatically. Gartner had pricing power that would make a luxury brand jealous. Annual price increases of 5-7% were standard, regardless of inflation. Clients grumbled but renewed—what choice did they have?

The Magic Quadrant had evolved from analytical framework to kingmaking mechanism. Vendors would spend millions on products and marketing specifically to improve their quadrant position. Some hired former Gartner analysts as consultants, paying six figures for insights on how to move from "Niche Player" to "Leader." A poor Magic Quadrant position could kill a startup's enterprise sales; a good position could generate billions in pipeline.

Hall also understood the power of events. Gartner Symposium had become the Davos of enterprise technology—the one conference where CIOs had to be seen. Ticket prices reached $5,000, not including travel, yet attendance grew every year. Vendors paid hundreds of thousands for speaking slots and booth space. The conferences weren't just revenue generators—they were network effect amplifiers. The more attendees Gartner attracted, the more valuable attendance became.

By 2017, Gartner's dominance was absolute. The company commanded 54% market share in IT research. The next largest competitor, IDC, had less than 10%. In Magic Quadrant terms, Gartner wasn't just a Leader—it was in a quadrant by itself.

But Hall had one more move to make. The IT research market was conquered, but technology was eating every business function. Marketing, sales, HR, finance—all were being transformed by technology. To truly dominate, Gartner needed to be present in every boardroom, every strategic discussion, every technology decision. The opportunity was massive, but it would require Gartner's biggest acquisition ever—a $2.6 billion bet that would either cement Gartner's monopoly or destroy it.

VII. The CEB Mega-Deal: Beyond IT (2017)

The investment bankers from Goldman Sachs had seen many hostile situations, but the Gartner-CEB negotiation was uniquely tense. It was December 2016, and in a conference room overlooking the Potomac, CEB's board was in revolt. "They want to buy us to bury us," one director said. Another countered: "They're offering a 40% premium. Our fiduciary duty is clear." Meanwhile, at Gartner's Stamford headquarters, Gene Hall was making his final push: "This is our Microsoft-LinkedIn moment. We either do this, or we remain an IT company forever."

In 2017, Gartner acquired CEB, an Arlington-based talent management and operations consulting firm, for $2.6 billion. The deal included $700 million in CEB debt. The acquisition announcement in January 2017 sent shockwaves through the industry. CEB (originally the Corporate Executive Board) was not an IT research firm—it provided best practice insights across HR, sales, finance, and legal functions.

The premium Gartner paid was extraordinary—31% over CEB's 30-day average stock price, 41% over the 60-day average. Wall Street was skeptical. CEB's growth had stalled, its subscription renewal rates were declining, and its culture was notoriously insular. One analyst called it "the most expensive acquisition in research industry history."

But Hall saw something others missed. CEB had achieved in HR, sales, and finance what Gartner had achieved in IT: near-monopolistic positions in their respective research markets. CEB's sales research, particularly around the Challenger Sale methodology, had become gospel in B2B sales organizations. Their HR research on talent management was considered definitive. The combined entity would serve every major function in the enterprise.

The integration challenges were immediate and profound. CEB's culture was academic, even more so than Gartner's. Their research methodology emphasized longitudinal studies and peer benchmarking, while Gartner favored rapid-cycle analysis and vendor evaluation. CEB analysts viewed themselves as management scientists; Gartner analysts saw themselves as technology strategists.

The client overlap was substantial but problematic. Many enterprises subscribed to both Gartner and CEB, but through different departments with different buyers. The CFO's office bought CEB's finance research. The CHRO bought their HR insights. The CIO bought Gartner. Suddenly, Gartner sales representatives were calling on executives they'd never engaged before, selling research they didn't fully understand. On a pro forma basis, the combined company's reported results for the last 12 months ended September 30, 2016 include approximately $3.3 billion in revenue, making Gartner one of the largest professional services firms in the world. The combined entity would have more than 13,000 associates serving clients in more than 100 countries worldwide. The numbers were staggering, but the execution would prove even more challenging.

The most controversial aspect of the deal was Gartner's intention to maintain its aggressive pricing strategy across CEB's products. CEB had traditionally priced below Gartner, positioning itself as the value alternative. Hall's plan was to harmonize pricing upward—essentially betting that CEB's research was underpriced relative to its value. Some CEB clients saw renewal increases of 20-30% in the first year post-acquisition.

The talent retention challenges were severe. Many CEB analysts, who had joined the firm for its academic culture and peer-benchmarking methodology, found Gartner's more commercial approach jarring. Within 18 months, an estimated 30% of CEB's senior analysts had departed. Gartner had to scramble to backfill positions while maintaining research quality.

But the strategic logic proved sound. With the CEB acquisition, Gartner gets access to new C-suite roles. CEB also serves HR, Sales, Finance and Legal functions. For the first time, Gartner could walk into a boardroom and credibly claim to serve every major business function. The cross-selling opportunities were enormous—a Gartner IT client could be introduced to CEB's sales research; a CEB HR client could be sold Gartner's digital workplace insights.

The financial markets initially punished the deal. Gartner's stock fell 15% on the announcement as investors worried about integration risk and the dilution from issuing 8 million shares. The skeptics pointed to CEB's declining growth rates and questioned whether Gartner was buying a dying business at a premium price.

Yet Hall remained confident. In investor calls, he emphasized that CEB's slower growth was a fixable execution problem, not a structural issue. Hall acknowledged CEB's slower growth and expressed a need to improve the company's "wallet retention." He said he hopes to improve the firm's retention rates by applying new management principles from Gartner's "playbook." "They have great margins, they're just not growing that great," he said. "We have playbooks on how to improve retention".

By late 2017, early signs suggested the integration was working. Combined company revenues were growing, margins were expanding, and client retention—while still below Gartner's traditional levels—was improving. The CEB deal had transformed Gartner from an IT research firm into something unprecedented: a comprehensive intelligence platform for the entire enterprise.

The acquisition marked the culmination of Hall's vision. Gartner now touched every major decision in the enterprise—from technology selection to talent management, from sales strategy to supply chain optimization. The company that had started by decoding IBM now decoded everything. But even as Gartner celebrated its expanded empire, a new acquisition was about to test whether the company could extend its influence beyond the enterprise and into the consumer-facing digital world.

VIII. The L2 Acquisition & Digital Marketing Push (2017)

Scott Galloway was holding court at L2's SoHo headquarters, his signature blend of data and profanity flowing freely. "Amazon isn't a retailer," he declared to his team of millennial analysts, "it's a fucking IQ test for every other business." It was March 2017, and Galloway had just agreed to sell his digital intelligence firm L2 to Gartner. The irony wasn't lost on him—the professor who railed against monopolies was selling to the ultimate monopolist.

Two months later, Gartner further expanded its marketing offerings with the acquisition of Scott Galloway's digital benchmarking firm L2. The L2 acquisition, coming just months after the massive CEB deal, signaled Gartner's ambition to dominate not just enterprise IT and business functions, but also the rapidly evolving digital marketing landscape.

L2 was unlike anything Gartner had acquired before. Founded by Galloway, a clinical professor of marketing at NYU Stern School of Business, L2 evaluated 2,200+ brands annually across digital marketing, social media, and e-commerce. Their Digital IQ Index had become the report card that CMOs feared and celebrated in equal measure. A poor L2 score could trigger boardroom discussions; a good one could justify millions in digital spending.

Galloway himself was a force of nature—part academic, part entertainer, part provocateur. His YouTube videos dissecting Amazon's dominance or predicting the breakup of big tech regularly went viral. He had built L2 into something unique: a research firm with personality, attitude, and a rabid following among marketers and venture capitalists.

The cultural fit with Gartner seemed impossible. Where Gartner was corporate and measured, L2 was irreverent and bold. Gartner's Magic Quadrant was a 2x2 matrix; L2's reports featured rankings like "Genius" and "Challenged" with colorful commentary that named and shamed underperformers. Gartner analysts wore suits; L2 analysts wore Supreme hoodies.

But Gene Hall saw something others missed. Digital transformation meant that every company was becoming a digital marketing company. The CMO was becoming as important as the CIO in technology decisions. Marketing technology—martech—was the fastest-growing category of enterprise software. Gartner needed credibility in this space, and L2 had it in spades.

The integration challenges were immediate. L2's Manhattan office, with its exposed brick and craft beer on tap, was a world away from Gartner's Stamford corporate campus. L2's research methodology—which combined social media scraping, website analysis, and mystery shopping—was antithetical to Gartner's interview-based approach. L2's clients were brands and agencies; Gartner's were enterprises and vendors.

Galloway's presence created its own complications. His continued role at NYU, his popular podcast, and his increasingly political commentary on tech monopolies created awkward moments for Gartner. When Galloway called for breaking up Amazon on cable news, Gartner's AWS relationship team cringed. When he predicted the death of traditional advertising agencies, Gartner's agency clients complained.

The business model clash was equally challenging. L2's revenue came primarily from annual subscriptions to their Digital IQ reports, priced at $15,000-$50,000—a fraction of Gartner's typical enterprise deals. L2 also generated significant revenue from speaking engagements, with Galloway commanding $100,000+ per keynote. This personality-driven business model was alien to Gartner's systematic approach.

Yet the strategic value was undeniable. L2 gave Gartner instant credibility with CMOs and digital leaders. Their brand rankings influenced billions in marketing spend. Their data on digital performance complemented Gartner's vendor assessments. Most importantly, L2 brought Gartner into conversations about consumer behavior, not just enterprise technology.

The L2 acquisition also highlighted a broader challenge: Gartner's traditional B2B focus was increasingly artificial in a world where B2B and B2C technologies were converging. The same cloud platforms, AI tools, and digital channels served both enterprise and consumer applications. L2 was Gartner's bridge to this broader digital ecosystem.

By late 2017, the integration was proceeding, albeit uncomfortably. L2 maintained its brand and methodology while gaining access to Gartner's resources and global reach. Galloway continued his provocative commentary, though now with subtle disclaimers about his Gartner affiliation. The cultures remained distinct, but the business synergies were emerging.

The L2 deal, though small compared to CEB, represented something significant: Gartner's recognition that its future lay beyond traditional enterprise IT. In acquiring L2, Gartner wasn't just buying research capabilities—it was buying relevance in an increasingly digital, consumer-centric, personality-driven business world. The question was whether Gartner's corporate DNA could accommodate such a different species, or whether, like organ rejection, the body would ultimately expel the foreign element.

IX. Modern Era: The Information Monopoly (2017–Present)

The Gartner Symposium in Orlando, October 2023, felt different. The usual parade of vendor booths and CIO networking had a nervous edge. In the keynote hall, Gene Hall's successor was explaining how generative AI would transform enterprise decision-making, carefully avoiding the obvious question: if AI could synthesize information instantly, why did anyone need Gartner's 3,000 analysts?

In 2024, Gartner's revenue was $6.27 billion, an increase of 6.10% compared to the previous year's $5.91 billion. Earnings were $1.25 billion, an increase of 42.07%. The numbers were impressive, but they masked underlying tensions. The company that had built a monopoly on human-curated technology intelligence was facing an existential question: what happens when machines can do the curation?

The modern Gartner is a testament to the power of network effects and switching costs. As of December 2024, Gartner has over 21,000 employees globally and operates in 90 countries and territories. The company serves virtually every Fortune 1000 company, most government agencies, and thousands of mid-market enterprises. The three-segment model—Research, Conferences, Consulting—has proven remarkably resilient.

The Research segment remains the cash cow, generating over 70% of revenue with margins exceeding 70%. The subscription model is a thing of beauty: multi-year contracts, paid upfront, with autorenewal clauses and built-in price escalations. Client retention rates hover around 85%, and wallet retention (including upsells and cross-sells) exceeds 100%. Every year, clients pay more for essentially the same service.

The Conferences segment has evolved into a powerful reinforcement mechanism. Gartner Symposium/Xpo, held in multiple locations globally, attracts over 25,000 CIOs and IT leaders annually. The conferences aren't just revenue generators—they're network effect amplifiers. The more executives attend, the more valuable attendance becomes. Missing Symposium means missing the conversations that shape next year's IT strategy.

The Consulting segment, while smaller, plays a crucial strategic role. Gartner consultants help enterprises implement the strategies that Gartner research recommends, creating a virtuous cycle. Research identifies the need, consulting implements the solution, and conferences share the best practices. It's a fully integrated influence machine.

But the true source of Gartner's power lies in its role as market maker. The Magic Quadrant has evolved from analytical tool to market-defining mechanism. Inclusion or exclusion can determine a vendor's enterprise viability. Position changes can shift billions in market value. Gartner doesn't just observe markets; it creates them.

Consider the "hyperconverged infrastructure" market. The category didn't exist until Gartner created a Magic Quadrant for it. Suddenly, vendors were repositioning products, investors were funding startups, and enterprises were allocating budgets—all for a category that Gartner had essentially invented. The power to define markets is the ultimate monopolistic advantage.

The vendor relationship is particularly complex. Vendors pay Gartner millions for "vendor briefings," "inquiry access," and "reprint rights." While Gartner maintains that commercial relationships don't influence research, the appearance of conflict is unavoidable. Vendors that don't participate in Gartner's programs often find themselves disadvantaged in evaluations—not through bias, but through lack of access to explain their strategies. The company's regulatory challenges came to light in 2023. On May 26, 2023 the Securities and Exchange Commission (SEC) settled charges against Gartner for violating the Foreign Corrupt Practices Act (FCPA). The SEC asserted that from approximately December 2014 through August 2015 Gartner had a corrupt relationship with a South African company with close ties to the South African government which Gartner knew would result in official bribery. In the settlement the SEC ordered Gartner to stop violating the FCPA and Gartner agreed to pay $2,456,764.

The FCPA violation, while relatively minor in financial terms, highlighted a deeper challenge: as Gartner expanded globally, maintaining ethical standards across diverse markets became increasingly complex. The company's response—enhanced compliance procedures, training, and self-disclosure—demonstrated both the challenges and responsibilities of operating at monopolistic scale.

The modern Gartner faces its greatest existential threat not from competitors but from technology itself. Generative AI promises to democratize the very intelligence that Gartner monopolizes. Why pay millions for analyst reports when AI can synthesize information from thousands of sources instantly? Why attend conferences when virtual collaboration tools enable continuous knowledge sharing? Why trust human analysts when machines can process more data more objectively?

Yet Gartner's moat may be deeper than it appears. The company doesn't just provide information—it provides legitimacy. When a CIO selects a vendor in Gartner's "Leaders" quadrant, they're not just making a technology choice; they're making a defensible decision. If the implementation fails, they followed best practice. If it succeeds, they made a smart choice. Gartner sells career insurance disguised as market intelligence.

The network effects remain powerful. Vendors need Gartner because buyers use Gartner. Buyers need Gartner because vendors optimize for Gartner's evaluations. The conferences create communities that transcend individual transactions. The research becomes embedded in procurement processes, governance frameworks, and board presentations. Breaking this cycle would require coordinated action that seems unlikely in a fragmented market.

As Gartner approaches 2025, the company stands at an inflection point. Revenue continues to grow, margins remain robust, and market dominance seems secure. But beneath the surface, fundamental questions emerge: Can human curation maintain its premium in an age of artificial intelligence? Will enterprises continue to pay for certainty when uncertainty might drive innovation? Has Gartner become so powerful that it stifles the very disruption it claims to identify?

The modern Gartner is both oracle and kingmaker, researcher and market maker, observer and participant. It has achieved something remarkable: a monopoly on opinion in an industry built on disruption. Whether this position proves sustainable in the age of AI remains the ultimate question—one that even Gartner's thousands of analysts may struggle to answer.

X. Playbook: The Oracle Business Model

In a nondescript conference room at a Fortune 500 company, a vendor sales team waits nervously. They're not preparing for a customer presentation—they're about to brief Gartner analysts. The stakes couldn't be higher. A positive mention in Gartner research could unlock millions in pipeline; a negative assessment could end their enterprise ambitions. The vendor has paid Gartner $150,000 for this "advisory" session, but everyone knows what they're really buying: a chance to influence the influencer.

This scene captures the genius of Gartner's business model—a perpetual motion machine powered by information asymmetry, network effects, and the corporate world's deepest fear: being wrong. Let's dissect the playbook that transformed a two-person consultancy into a $6 billion monopoly.

Information Asymmetry as a Business

Gartner's fundamental insight was that in technology markets, information is more valuable than the technology itself. The company doesn't reduce information asymmetry—it monetizes it. By positioning itself as the authoritative source of technology intelligence, Gartner becomes indispensable to both sides of every transaction.

Consider the dynamics: vendors know their own products but don't understand the competitive landscape or buyer priorities. Buyers know their needs but don't understand the vendor landscape or technology trajectories. Gartner sits in the middle, selling clarity to confusion—at premium prices to both sides.

Subscription Model Mastery

The subscription model is Gartner's masterpiece of financial engineering. Clients pay upfront for annual or multi-year contracts, providing predictable cash flow. Contracts auto-renew with built-in price escalations. Canceling requires formal notification months in advance. Most critically, the switching costs are enormous—not just financially but psychologically.

Once Gartner research becomes embedded in an organization's decision-making process, removing it feels like organizational lobotomy. Budget presentations reference Gartner forecasts. Vendor selections cite Magic Quadrants. Strategic plans quote Gartner predictions. The research becomes organizational scripture, making cancellation heretical.

Creating Industry Standards

The Magic Quadrant wasn't just an analytical framework—it was a colonization of mental models. By creating a simple, memorable way to evaluate vendors, Gartner didn't just describe markets; it defined them. Categories exist because Gartner creates Magic Quadrants for them. Vendors position themselves using Gartner's terminology. Investors evaluate companies through Gartner's lens.

The Hype Cycle performs similar colonization for technology adoption. Every emerging technology is now discussed in terms of triggers, peaks, troughs, and plateaus. Gartner didn't discover these patterns—it created a language that became self-fulfilling prophecy.

Playing Both Sides: The Vendor-Buyer Dynamic

Gartner's most controversial—and profitable—innovation is serving both vendors and buyers simultaneously. Vendors pay for advisory services, conference sponsorships, and reprint rights. Buyers pay for research subscriptions, inquiry calls, and consulting. Both sides know the other is paying, creating a Mexican standoff of mutual dependence.

The company maintains elaborate compliance frameworks to claim independence—separate research and sales teams, disclosure policies, ethical guidelines. But the structural conflict is unavoidable. Vendors that don't participate in Gartner's programs often find themselves disadvantaged, not through explicit bias but through lack of visibility. It's not corruption; it's architecture.

Network Effects and Peer Benchmarking

Gartner has achieved something rare in professional services: true network effects. The more organizations use Gartner, the more valuable it becomes for others to use it. If your competitors are making decisions based on Gartner research, you need it too—if only to understand their thinking.

The peer benchmarking capabilities acquired through CEB amplified these effects. Now organizations don't just want to know what Gartner thinks—they want to know what their peers are doing. Gartner becomes the platform for industry-wide coordination, a role that grows more valuable with scale.

M&A Strategy: Buying Complementary Monopolies

Gartner's acquisition strategy follows a clear pattern: buy leaders in adjacent monopolies. META Group dominated enterprise architecture. AMR Research owned supply chain intelligence. CEB controlled HR and sales best practices. L2 ruled digital marketing benchmarks.

Each acquisition brought not just content but captive markets. The integration playbook was consistent: maintain the research quality, harmonize the pricing upward, cross-sell to existing clients, and eliminate duplicate costs. The result: immediate margin expansion and gradual revenue synergies.

Pricing Power and Margin Expansion

Gartner's pricing power defies conventional economics. Annual price increases of 5-7% are standard, regardless of inflation or competitive pressure. Clients grumble but pay because the alternative—making critical decisions without Gartner—seems riskier than overpaying for certainty.

The margin expansion over time has been remarkable. Research margins exceed 70%. Conference margins approach 60%. Even consulting, traditionally a lower-margin business, generates 30%+ margins at Gartner's scale. The company has achieved the holy grail of professional services: scaling revenue faster than costs.

The Insight-to-Influence Pipeline

Gartner has built a sophisticated pipeline that transforms raw information into market influence:

- Collection: Thousands of client interactions generate data about technology adoption, challenges, and priorities

- Synthesis: Analysts transform this data into frameworks, forecasts, and recommendations

- Distribution: Research reports, conferences, and media appearances disseminate insights

- Amplification: Vendors reference Gartner positioning, media quotes Gartner predictions, boards cite Gartner analysis

- Monetization: The influence creates demand for more research, more conferences, more consulting

This pipeline creates a virtuous cycle where influence generates information, which generates more influence.

The Uncertainty Tax

Perhaps Gartner's greatest innovation is what might be called the "uncertainty tax"—the price enterprises pay to reduce decision-making risk. In a world where wrong technology decisions can end careers, Gartner offers something invaluable: plausible deniability.

When projects fail, executives can point to Gartner's recommendation. When budgets are questioned, Gartner's forecasts provide cover. When vendors are selected, Gartner's evaluation justifies the choice. The company doesn't sell answers—it sells defensibility.

This playbook has created one of the most powerful business models in professional services: high margins, predictable revenue, strong competitive moats, and pricing power that seems immune to economic cycles. It's a monopoly hiding in plain sight, charging admission to the future while shaping the very future it predicts.

XI. Bear vs. Bull Case

The Gartner board meeting in February 2024 had an unusual tension. For the first time in years, a director asked the uncomfortable question: "What happens when ChatGPT can do what our analysts do, but for free?" The room fell silent. After building an impregnable monopoly over four decades, Gartner faced a threat that couldn't be acquired, out-priced, or ignored: artificial intelligence that could synthesize information instantly, globally, and at zero marginal cost.

Bear Case: The Empire's Vulnerabilities

The bear case against Gartner starts with a simple observation: monopolies invite disruption, and Gartner's monopoly has never been more complete—or more vulnerable.

AI and Automated Insights: The existential threat is obvious. Large language models can already synthesize technology information, compare vendors, and provide recommendations. Today's ChatGPT might not match a senior Gartner analyst, but tomorrow's AI might exceed them. When every company can have an AI analyst working 24/7 at marginal cost approaching zero, why pay millions for human opinions? The deflation of information value could be swift and brutal.

Vendor Conflict of Interest: The dual-revenue model that has been Gartner's strength could become its achilles heel. As scrutiny of corporate influence increases, the appearance of pay-to-play becomes harder to defend. One high-profile case of demonstrated bias—a leaked email, a whistleblower revelation—could trigger a crisis of confidence. If buyers stop trusting Gartner's independence, the entire model collapses.

High Valuation Multiples: Trading at premium multiples to the S&P 500, Gartner's valuation assumes continued growth and margin expansion. But professional services businesses rarely sustain such multiples indefinitely. Any growth deceleration or margin compression could trigger multiple compression, creating a double hit to valuation.

Enterprise IT Spending Cyclicality: Despite its subscription model, Gartner isn't immune to IT spending cycles. When enterprises cut technology budgets, they scrutinize all spending—including research. The next serious recession could reveal that Gartner's "essential" services are more discretionary than assumed.

Innovation Bottleneck: Gartner's very success might be stifling innovation. Startups optimize for Magic Quadrant positioning rather than customer value. Enterprises make safe choices rather than innovative ones. The industry's deference to Gartner might be creating the stagnation that eventually makes Gartner itself irrelevant.

Generational Change: Younger technology leaders, raised on Google and Stack Overflow, might not share their predecessors' reverence for analyst firms. They trust peer networks, open-source communities, and real-time data over formal research. As digital natives ascend to decision-making roles, Gartner's authority could erode.

Bull Case: The Entrenched Oracle

The bull case for Gartner rests on a different observation: in enterprise technology, being right matters less than being defensible, and nobody provides defensibility like Gartner.

Mission-Critical Decision Support: Technology decisions have never been more critical or complex. Cloud migrations, digital transformations, AI implementations—these are bet-the-company moves. The cost of wrong decisions dwarfs Gartner's fees. As technology complexity increases, the need for expert guidance grows, not shrinks.

Expanding Addressable Market: The CEB acquisition proved Gartner can expand beyond IT. Every business function is being digitized. Marketing needs martech guidance. HR needs HR tech evaluation. Finance needs fintech intelligence. Gartner's addressable market isn't shrinking—it's exploding.

Pricing Power: Gartner has proven it can raise prices faster than inflation for decades. The subscription model, combined with high switching costs, creates pricing power that few businesses enjoy. Even if growth slows, margin expansion through pricing could drive earnings growth.

High Switching Costs and Renewal Rates: With 85%+ retention rates and 100%+ wallet retention, Gartner's installed base is incredibly sticky. Organizations have built Gartner into their processes, governance, and culture. Switching isn't just expensive—it's organizational surgery.

Network Effects at Scale: Gartner's network effects only strengthen with scale. The more organizations use Gartner, the more essential it becomes. Vendors must participate because buyers use it. Buyers must subscribe because vendors optimize for it. This circular dynamic is nearly impossible to break.

AI as Complement, Not Replacement: Rather than replacing Gartner, AI might enhance its value. Gartner has the proprietary data, client relationships, and analytical frameworks that AI needs. The company could become the premium layer on top of commoditized AI—providing the judgment, context, and accountability that machines can't.

Brand as Risk Mitigation: In enterprise technology, nobody gets fired for following Gartner's advice. This risk mitigation value transcends analytical accuracy. Even if AI provides better analysis, it can't provide political cover. Gartner sells career insurance, and that market never shrinks.

Operating Leverage: With massive fixed costs already absorbed, incremental revenue drops straight to the bottom line. Every new subscription, conference attendee, or consulting engagement has minimal marginal cost. This operating leverage means that even modest growth generates substantial earnings expansion.

The Synthesis: Gradual Evolution, Not Revolution

The reality likely lies between the extremes. Gartner faces real threats—AI, generational change, potential disruption. But it also has real strengths—network effects, switching costs, brand power. The most probable scenario isn't dramatic disruption but gradual evolution.

Gartner will likely adopt AI to enhance analyst productivity, allowing fewer analysts to cover more ground. Pricing power will offset volume pressure. The company will expand into new functions and geographies. Growth will slow from exceptional to merely good. Margins might compress but remain industry-leading.

The key question isn't whether Gartner's monopoly will end—all monopolies eventually do. It's whether the company can evolve fast enough to remain relevant as the nature of information and decision-making fundamentally changes. The bear case assumes Gartner is a dinosaur awaiting the asteroid. The bull case assumes it's an apex predator that will adapt and survive.

For investors, the calculation comes down to timeframe. Over the next 2-3 years, Gartner's entrenched position seems secure. Over 10-15 years, disruption seems inevitable. The art lies in identifying the inflection point—the moment when gradual change becomes sudden obsolescence. Until then, betting against Gartner means betting against enterprise inertia, human psychology, and the profound corporate need for someone else to blame when things go wrong.

XII. Power Analysis & Competitive Moats

The venture capitalist leaned forward, genuinely puzzled. "I don't understand," he said to his partner. "We've funded three different startups trying to disrupt Gartner. They all had better technology, lower prices, and innovative models. They all failed. What are we missing?" His partner, a former Gartner analyst, smiled. "You're trying to compete with a product. Gartner isn't a product—it's a protocol. You might as well try to replace TCP/IP."

This exchange captures something essential about Gartner's competitive position. The company has achieved something rare in business: multiple, reinforcing power dynamics that create an effectively impregnable market position. Let's examine each layer of this defensive architecture.

Scale Economies in Research Production

Gartner employs over 2,000 analysts covering every conceivable technology domain. The cost of replicating this coverage would be astronomical—hundreds of millions annually before generating a dollar of revenue. But the real scale economy isn't in analyst headcount; it's in information gathering.

Every client interaction generates data. With 15,000+ client organizations, Gartner has visibility into technology decisions, challenges, and outcomes that no competitor can match. This data exhaust becomes the raw material for research, creating a virtuous cycle: more clients generate more data, enabling better research, attracting more clients.

The mathematics are compelling. If research costs $500 million annually and you have 1,000 clients, each pays $500,000. If you have 10,000 clients, each pays $50,000. Gartner's scale allows it to spread fixed research costs across a massive base, delivering comprehensive coverage at prices no subscale competitor can match.

Network Effects from Peer Benchmarking

The CEB acquisition supercharged Gartner's network effects by adding peer benchmarking to vendor evaluation. Now clients don't just want to know Gartner's opinion—they want to know what their peers are doing. This creates a different kind of network effect: the value increases with the square of the number of participants.

When 73% of the Fortune 1000 uses Gartner, not using it means operating blind to industry consensus. You don't know what your competitors know. You can't benchmark against industry standards. You're excluded from the conversation that shapes market direction. The fear of missing out becomes self-fulfilling—organizations subscribe because other organizations subscribe.

Switching Costs from Embedded Workflows

Gartner has achieved the ultimate lock-in: procedural embedding. Enterprise workflows reference Gartner research. Procurement processes require Magic Quadrant positioning. Board presentations cite Gartner forecasts. Job descriptions specify Gartner framework knowledge.

Switching from Gartner isn't just changing vendors—it's rewiring organizational DNA. Every process document needs updating. Every historical comparison breaks. Every employee needs retraining. The switching cost isn't the fee; it's the organizational disruption. Most CIOs calculate that it's cheaper to overpay for Gartner than to undergo this transformation.

Brand as Risk Mitigation

"Nobody gets fired for buying IBM" has been replaced by "Nobody gets fired for following Gartner." This isn't about analytical quality—it's about political cover. When a technology decision goes wrong, pointing to Gartner's recommendation provides defensibility. The brand has become synonymous with prudent decision-making.

This creates a perverse dynamic: Gartner's recommendations become self-fulfilling because organizations follow them to avoid criticism for not following them. The brand power transcends accuracy—it's about conformity to accepted practice. Fighting this dynamic is like fighting culture itself.

Counter-Positioning vs. Traditional Consulting

Gartner has positioned itself brilliantly against traditional consulting firms. McKinsey, Accenture, and others sell time—expensive time. Projects take months, cost millions, and deliver one-time insights. Gartner sells subscriptions—continuous access to evolving intelligence at a fraction of consulting costs.

This counter-positioning is structural. Consulting firms can't match Gartner's model without cannibalizing their core business. Why pay $2 million for a McKinsey digital strategy when Gartner provides continuous strategic intelligence for $200,000 annually? The subscription model isn't just cheaper—it's philosophically different, providing ongoing guidance rather than point-in-time answers.

Process Power Through Standardization

Gartner has standardized the unstandardizable: technology evaluation. The Magic Quadrant, Hype Cycle, and other frameworks transform subjective assessments into seemingly objective analyses. This standardization creates process power—the ability to produce consistent outputs at scale.

A new analyst can be trained to produce Magic Quadrants. The methodology is documented, repeatable, scalable. This isn't true for traditional consulting, where each engagement is bespoke. Gartner has industrialized insight production, creating a factory for intelligence that competitors struggle to replicate.

Cornered Resource: Vendor Relationships

Every major technology vendor has a Gartner relationship. They brief analysts, sponsor conferences, purchase reprints. These relationships, built over decades, represent a cornered resource. New entrants can't instantly access vendor product roadmaps, strategic plans, or executive thinking.

These vendor relationships create an information advantage that compounds over time. Vendors share more with Gartner because Gartner influences buyers. This inside information improves research quality, which increases influence, which encourages more vendor sharing. It's a resource that can't be bought—only earned over decades.

The Aggregation of Aggregators

Through acquisitions, Gartner has become the aggregator of aggregators. It owns the leading research positions in IT (organic), supply chain (AMR), HR (CEB), digital marketing (L2), and numerous sub-specialties. Each acquisition brought its own network effects, switching costs, and brand power.

This aggregation creates cross-selling opportunities that multiply value. An IT client becomes an HR client. A supply chain client adds digital marketing research. The corporate subscription expands from one department to enterprise-wide. The lifetime value of each client multiplies while acquisition costs remain flat.

The Anti-Network: Competitive Isolation

Perhaps Gartner's most subtle moat is competitive isolation. Unlike industries with clear #2 and #3 players that create competitive dynamics, Gartner stands alone. IDC and Forrester operate at less than 10% of Gartner's scale. They're not competitors; they're alternatives for budget-constrained buyers.

This isolation means Gartner doesn't face normal competitive pressures. It doesn't need to match competitor innovations, respond to pricing pressure, or worry about talent poaching. The company operates in a competitive vacuum, setting its own pace, prices, and priorities.

The Infinite Game

Gartner's ultimate power might be that it's playing an infinite game while competitors play finite ones. Consulting firms chase projects. Research firms chase reports. Gartner chases permanent relationships. The company isn't trying to win—it's trying to continue playing indefinitely.

This infinite game mentality creates a different kind of moat: strategic patience. Gartner can invest in relationships that take years to monetize. It can maintain research coverage in emerging areas that won't generate revenue for decades. It can absorb short-term losses to preserve long-term position.

The combination of these power dynamics creates something approaching corporate invulnerability. Each moat reinforces the others. Scale enables network effects. Network effects increase switching costs. Switching costs strengthen brand. Brand supports pricing power. Pricing power funds scale. It's not a business model—it's a fortress, built over decades, defended by economics, psychology, and organizational inertia.

XIII. Epilogue: The Cost of Being Wrong

The CIO of a Fortune 500 retailer sat alone in her office, staring at the post-mortem report. The digital transformation project—$200 million, three years, guided entirely by Gartner's research and recommendations—had failed catastrophically. The vendors were all from Gartner's Leaders quadrant. The approach followed Gartner's digital maturity model. The timeline matched Gartner's predictions. Everything was done "right," yet everything went wrong.

This scene plays out more often than the industry admits, raising profound questions about Gartner's role in enterprise technology. When an oracle becomes so powerful that its predictions shape reality, what happens when the oracle is wrong? And perhaps more troublingly, can we even tell the difference between Gartner being right and everyone simply acting as if it were?

The Paradox of Creating the Market You Analyze

Gartner occupies a unique position in capitalism: it simultaneously observes and creates markets. When Gartner declares a technology trend, vendors pivot, investors fund, and enterprises budget. The prediction becomes self-fulfilling not because Gartner saw the future, but because it shaped it.

Consider the "digital transformation" narrative. Gartner didn't discover this trend—it manufactured it, packaged it, and sold it to millions. Every enterprise now has a digital transformation initiative, not necessarily because they need one, but because Gartner says they do. The oracle doesn't predict rain; it seeds clouds.

This creates an epistemological puzzle: How do we evaluate Gartner's accuracy when its predictions alter the very reality they purport to describe? It's Heisenberg's uncertainty principle applied to markets—the act of observation changes the observed.

Information as the Ultimate Business

Gartner has achieved something remarkable: selling the same information to everyone while maintaining its value to each buyer. Traditional information businesses face a paradox—information wants to be free, and once shared, loses exclusivity. Gartner solved this by selling not information but interpretation, not data but judgment, not answers but authority.

The business model is almost philosophical in its elegance. Gartner doesn't sell truth; it sells consensus. In a world where everyone has access to the same information, competitive advantage comes from everyone agreeing to use the same framework for interpreting it. Gartner provides that framework, charging admission to a shared reality.

What Happens When the Oracle Is Wrong?

The dirty secret of enterprise technology is that most projects fail—70% by some estimates. Many of these failures followed Gartner's guidance precisely. But here's the remarkable thing: these failures rarely damage Gartner's reputation. The failure is attributed to implementation, not strategy; execution, not advice; the organization, not the oracle.

This immunity to accountability is Gartner's greatest achievement. When recommendations succeed, Gartner's wisdom is validated. When they fail, implementation was flawed. It's a heads-I-win, tails-you-lose dynamic that would make a casino owner envious.

But the real cost isn't the failed projects—it's the innovations that never happen. How many breakthrough technologies were stillborn because they didn't fit Gartner's frameworks? How many radical approaches were rejected because they weren't in the Magic Quadrant? The cost of being wrong isn't just waste—it's opportunity cost on a civilizational scale.

The Future of Institutional Knowledge

As we stand on the cusp of the AI revolution, Gartner faces an existential question: What is the value of human judgment in an age of machine intelligence? If AI can process more information, identify more patterns, and generate more insights than any human analyst, what role remains for Gartner's 2,000 researchers?

The answer might be that Gartner's value was never really about information or even insight—it was about institutional legitimacy. Enterprises don't just need answers; they need answers they can defend to boards, shareholders, and regulators. AI might provide better analysis, but it can't provide political cover. It can't testify to Congress. It can't be blamed when things go wrong.

The Paradox of Success

Gartner's monopolistic success contains the seeds of its own disruption. By becoming the single source of truth, it has created a single point of failure. By standardizing technology evaluation, it has commoditized it. By making everyone dependent on its frameworks, it has created massive incentive for alternatives.

The question isn't whether Gartner will be disrupted—all monopolies eventually are. The question is what comes next. Will it be a new monopolist with a different model? A decentralized ecosystem of specialized intelligence providers? An AI-powered platform that democratizes technology intelligence? Or something we can't yet imagine?

The Ultimate Question

Perhaps the most profound question Gartner raises isn't about technology or business models but about knowledge itself. In an industry built on innovation and disruption, we've allowed a single entity to become the arbiter of truth. We've outsourced our judgment to an oracle, our thinking to a framework, our decisions to a quadrant.

The cost of being wrong isn't just Gartner's to bear—it's ours. Every time we defer to the Magic Quadrant instead of our own judgment, every time we cite Gartner instead of thinking deeply, every time we choose safety over innovation because Gartner says so, we pay a price. That price isn't denominated in dollars but in possibilities—the futures we don't explore, the innovations we don't pursue, the risks we don't take.

Gartner has built an extraordinary business by monetizing uncertainty in an uncertain industry. It has created value for shareholders, careers for analysts, and cover for executives. But as we enter an age where artificial intelligence promises to reshape how we make decisions, we must ask: Has our dependence on Gartner made us smarter or just more conformist? Has it reduced risk or just redistributed blame? Has it accelerated innovation or institutionalized consensus?

The oracle of technology decision-making has served us for four decades. As we face the next four, the question isn't whether we still need Gartner, but whether we can afford to need it. In an exponential age, the cost of being wrong is rising exponentially. But perhaps the greater cost is not learning to be right on our own.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube