Intuitive Surgical: The Robot Surgery Revolution

I. Introduction & Opening

Picture this: A surgeon sits at a console twenty feet from their patient, peering into a high-definition 3D viewer while manipulating controls that look more like a video game setup than medical equipment. Their hand movements—scaled down and filtered for tremor—guide robotic arms that make incisions smaller than a dime. This isn't science fiction. It's Tuesday morning at thousands of hospitals worldwide, and it's worth $180 billion in market value.

How does a Cold War-era defense project, originally conceived to operate on wounded soldiers from remote battlefields, transform into the most dominant monopoly in medical technology? How does a company facing existential patent litigation in its early years end up performing nearly 2.7 million procedures annually with virtually no meaningful competition? Intuitive Surgical develops, manufactures, and markets robotic products designed to improve clinical outcomes through minimally invasive surgery. The company offers the da Vinci Surgical System that enables surgical procedures using a minimally invasive approach; and Ion endoluminal system, which extends its commercial offerings beyond surgery into diagnostic endoluminal procedures. With a market cap of $173.27 billion USD as of August 2025, it stands as one of the world's most valuable medical technology companies.

This is a story about platform monopolies in healthcare—how they're built, why they persist, and what makes them nearly impossible to disrupt. It's about the power of switching costs so high that hospitals would rather expand their facilities than change systems. It's about network effects measured not in clicks or downloads, but in the muscle memory of surgeons' hands.

Over the next several hours, we'll trace Intuitive's journey from a DARPA-funded research project to a company that generated approximately $8.35 billion in revenue in 2024 with approximately 17% growth in procedures performed. We'll explore how they won a bitter patent war, found their killer application in an unexpected place, and built competitive moats that have frustrated some of the world's largest medical device companies.

Most importantly, we'll examine what this monopoly means for the future of surgery itself—and whether the next generation of AI-powered systems will finally enable the autonomous surgical robots that DARPA originally envisioned.

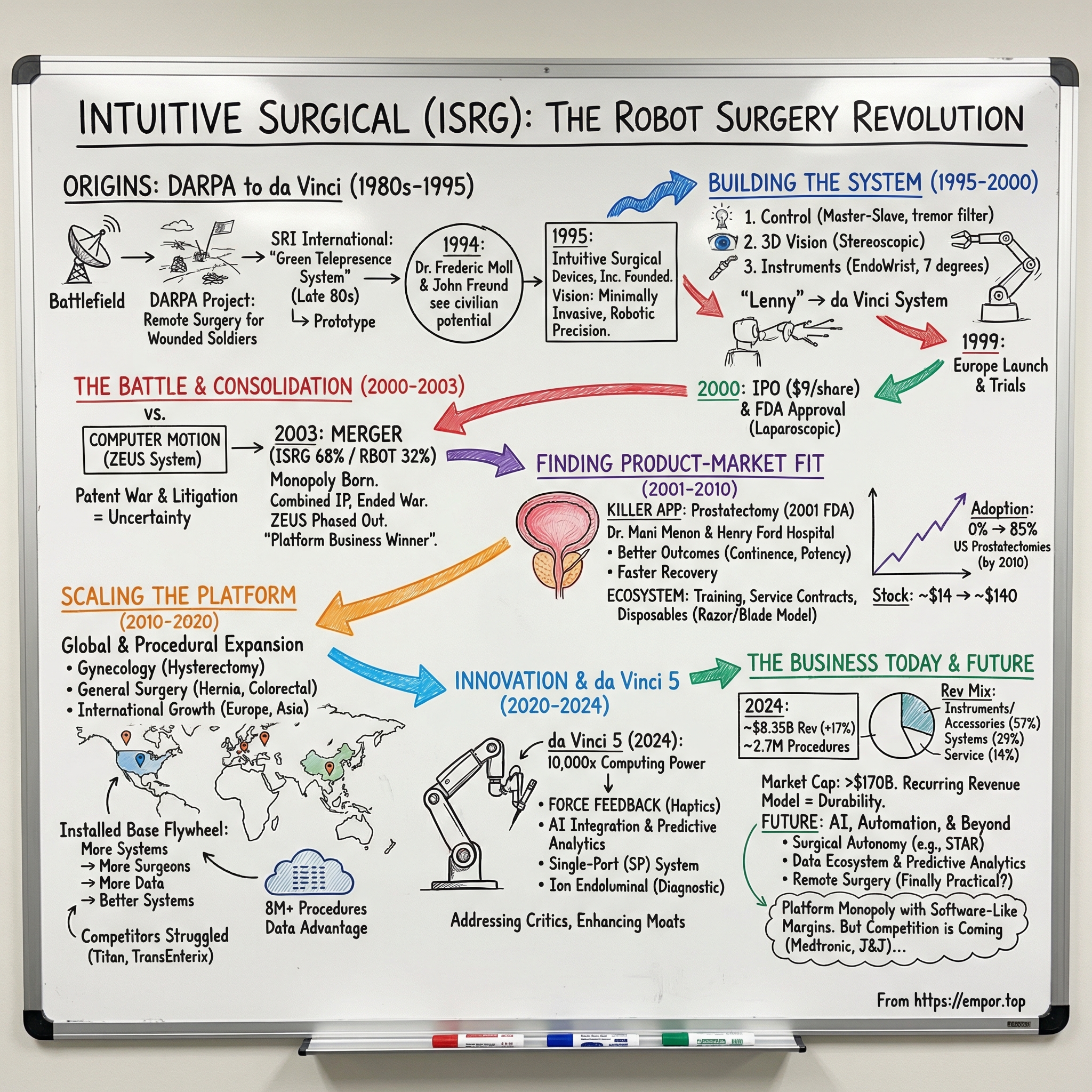

II. Origins: From DARPA to da Vinci (1980s-1995)

The year is 1985. In a nondescript research lab at SRI International in Menlo Park, California, two researchers are working on a project that seems pulled from science fiction. The Cold War is still raging, and the Defense Advanced Research Projects Agency—DARPA—has a problem: How do you perform surgery on wounded soldiers when the surgeon can't physically reach the battlefield? The research that eventually led to the development of the da Vinci Surgical System was performed in the late 1980s by Ajit Shah and Gary Guthart at research institute SRI International. In 1990, SRI received funding from the National Institutes of Health. But it was the military application that truly accelerated the project.

SRI developed a prototype robotic surgical system that caught the interest of the Defense Advanced Research Projects Agency (DARPA), which was interested in the system for its potential to allow surgeons to operate remotely on soldiers wounded on the battlefield. Think about the audacity of this vision: performing complex surgical procedures on wounded soldiers via satellite link, with the surgeon sitting safely hundreds of miles from the front lines. SRI, working with the U.S. Defense Advanced Research Projects Agency (DARPA) led the "Trauma Pod Project"—an initiative to make semi-autonomous surgical units, where patients could be operated upon by surgeons many miles from the front line.

The technical challenges were staggering. How do you recreate the surgeon's sense of touch through a machine? How do you ensure zero latency when a millisecond delay could be fatal? How do you provide depth perception through a camera system? The SRI team, including biomedical engineer Phillip S. Green, tackled these problems one by one, creating what would become known as the Green Telepresence Surgery System.

By the early 1990s, SRI had a working prototype. But as often happens with military technology, the most revolutionary applications would come from the civilian world. The system needed a champion—someone who could see beyond battlefield medicine to the broader implications for surgery itself.

Enter Dr. Frederic Moll in 1994. At the time, Moll was employed by Guidant. He tried to interest Guidant in backing it but to no avail. Moll wasn't your typical surgeon. He held a medical degree from the University of Washington, but also a bachelor's in economics from UC Berkeley and a master's in management from Stanford. He had already co-founded and sold Endotherapeutics to U.S. Surgical for its safety trocar technology. When he saw the SRI system demonstrated, he didn't see a military tool—he saw the future of minimally invasive surgery.

In 1995 Moll was introduced to John Freund who had recently left Acuson Corporation. Freund, a savvy dealmaker with experience in medical imaging, immediately grasped the potential. Together with engineer Robert Younge, they crafted a vision that would transform surgery: What if, instead of making large incisions that took weeks to heal, surgeons could operate through tiny ports with robotic precision?

Freund negotiated an option to acquire SRI's intellectual property and incorporated a new company that he named Intuitive Surgical Devices, Inc. The name itself was aspirational—making robotic surgery feel as natural and intuitive as operating with one's own hands.

The founding team had to convince skeptical investors that surgeons—notoriously conservative about new technology—would embrace robots in the operating room. Their pitch deck must have seemed like science fiction: robotic arms performing delicate procedures, 3D visualization systems, tremor filtering, motion scaling. But they found believers. Early investors included the Mayfield Fund, Sierra Ventures, and Morgan Stanley, who collectively saw past the technical complexity to the transformative potential.

The team's initial business plan was remarkably prescient. They didn't just envision selling robots; they imagined an entire ecosystem—training programs, service contracts, disposable instruments. They understood that success wouldn't come from technology alone, but from fundamentally changing how surgery was taught, performed, and delivered.

As 1995 drew to a close, Intuitive Surgical had licensed the technology, raised initial funding, and assembled a team of engineers and surgeons ready to transform a defense project into a medical revolution. The path from DARPA's battlefield vision to the operating room had begun.

III. Building the First System: "Lenny" to da Vinci (1995-2000)

In a warehouse in Mountain View, California, 1996, Robert Younge stands before what looks like a mechanical octopus crossed with a NASA lunar module. Wires snake everywhere. Hydraulic lines hiss. The prototype, affectionately named "Lenny" after Leonardo da Vinci, barely holds together through a simulated surgical procedure. An engineer jokes that it's held together with "duct tape and prayers." But when a surgeon sits at the console and moves the controls, something magical happens—the robotic arms mirror every movement with uncanny precision.

The company refined the SRI System into a prototype known originally as "Lenny" (after Leonardo da Vinci), which was ready for testing in 1997. The journey from military telepresence system to surgical robot required reimagining nearly every component. The team faced three fundamental engineering challenges that would make or break the company.

First, the master-slave control system. Unlike industrial robots that follow pre-programmed paths, a surgical robot must respond instantly and intuitively to the surgeon's hand movements. The team developed a control algorithm that not only translated motion but scaled it—a surgeon's inch-wide hand movement could become a millimeter-precise incision. They added tremor filtering, eliminating the natural shake in human hands that becomes pronounced under surgical stress.

Second, three-dimensional visualization. Surgeons operate in 3D space, but laparoscopic surgery reduced them to flat 2D monitors—like trying to thread a needle while looking at a television screen. Intuitive's solution was elegant: two cameras creating stereoscopic vision, displayed through a viewer that blocked peripheral distractions. Surgeons described the experience as being "transported inside the patient's body."

Third, the instruments themselves needed to replicate the human wrist's seven degrees of freedom through incisions smaller than a dime. The engineering team created "EndoWrist" instruments—miniature mechanical wrists that could rotate, grip, and cut with greater range of motion than the human hand. Each instrument contained cables thinner than fishing line, pulleys smaller than shirt buttons, and joints that could withstand thousands of procedures.

As prototypes became more advanced, they were named using da Vinci themes. One was "Leonardo", another was "Mona". The final version was nicknamed the da Vinci Surgical System, and the name stuck. The naming wasn't just whimsy—it connected the technology to Leonardo's legacy of combining art, science, and human anatomy. Marketing studies showed surgeons responded positively to the Renaissance association, seeing it as innovative yet grounded in medical tradition.

By 1998, the team had a system stable enough for human trials. But FDA approval in the United States would take years. After further testing, Intuitive Surgical began marketing this system in Europe in 1999, while awaiting FDA approval in the United States. The European regulatory environment, more receptive to surgical innovation, became their proving ground. In Belgium, France, and Germany, pioneering surgeons performed the first da Vinci procedures—cholecystectomies, cardiac valve repairs, even coronary artery bypass grafts.

The results were remarkable but the challenges were real. Early systems cost over $1 million. Setup took hours. The instruments failed frequently. In one memorable incident in Paris, a system shut down mid-procedure, requiring the surgical team to complete the operation conventionally. Each failure became a learning opportunity, each success a selling point.

As Intuitive prepared for its IPO, the financial pressures mounted. They had burned through tens of millions in venture funding. Competitors were emerging. The FDA approval process dragged on. The company needed capital not just to survive, but to build inventory, establish training centers, and prepare for a market that didn't yet exist.

The company raised $46 million in an initial public offering in 2000. The IPO timing seemed perfect—the peak of the dot-com boom, when investors threw money at anything remotely technological. Intuitive's stock opened at $9 per share (adjusted for splits), giving them the war chest needed for the battles ahead.

That same year, the FDA approved use of the da Vinci Surgical System for general laparoscopic surgery. The approval was narrow—just general laparoscopic procedures like gallbladder removal—but it was a foothold. The real prize would come a year later, with approval for prostate surgery. But first, Intuitive would have to survive an existential threat that emerged just as they went public.

IV. The Computer Motion Battle & Consolidation (2000-2003)

The letter arrived at Intuitive's headquarters three weeks before their IPO roadshow was set to begin. Computer Motion, Inc., their primary competitor, was suing for patent infringement. The timing was no coincidence—it was corporate warfare designed to derail Intuitive's public offering and establish Computer Motion's dominance in robotic surgery.

Shortly before going public, Intuitive Surgical was sued for patent infringement by Computer Motion, Inc, its chief rival. Computer Motion had actually gotten into the robotic surgery field earlier than Intuitive Surgical, with its own system, the ZEUS Robotic Surgical System.

Computer Motion wasn't some upstart. Founded in 1989 by biomedical engineer Yulun Wang, they had beaten Intuitive to market with AESOP (Automated Endoscopic System for Optimal Positioning), a voice-controlled robotic arm that held laparoscopic cameras. By 2000, they had installed hundreds of AESOP systems and were launching ZEUS, their answer to da Vinci.

ZEUS was technologically impressive—in some ways superior to early da Vinci systems. It was smaller, potentially more precise, and designed specifically for cardiac surgery. Computer Motion had secured key patents on master-slave surgical robotics, voice control, and force feedback. Their lawsuit alleged that Intuitive had essentially stolen their intellectual property. The legal battle was complex and multifaceted. Computer Motion sued Intuitive Surgical for infringement of nine patents. Then, Intuitive and IBM filed the patent infringement suit against Computer Motion in reference to the voice-controlled technology. In 2002, the District Court for the Central District of California has ruled that the da Vinci Surgical System literally infringed Computer Motion's 6,244,809 patent. Then, a federal jury in 2003 issued a ruling requiring Computer Motion to pay Intuitive and IBM $4.4 million for infringing a patent covering aspects of Intuitive's system.

The uncertainty created by the litigation between the companies was a drag on each company's growth. Hospitals hesitated to invest millions in systems that might become obsolete if one company was forced to exit the market. Surgeons were reluctant to train on platforms with uncertain futures. Investors valued both companies at fractions of their potential. The sales numbers from that period tell the story: Zeus: 30 units sold in the USA, 15 in Europe, 5 in Asia; da Vinci: 50, 34, 5, respectively.

Behind closed doors, both management teams recognized a truth that their lawyers wouldn't admit: this war would destroy both companies. The reason that CMI agreed to the acquisition, is that (while they believed they would ultimately prevail in the patent infringement case) they simply didn't have the financial resources to sustain them over the period that IBM's deep pockets would allow Intuitive to keep the litigation going.

In March 2003, a stunning announcement: Intuitive Surgical (Nasdaq:ISRG) and Computer Motion (Nasdaq:RBOT) today announced they are merging into one company that combines their strengths in operative surgical robotics, telesurgery, and operating room integration. The terms revealed the relative strength of the companies: Computer Motions equity holders would receive 32 percent of the combined company on a fully diluted basis (including out-of-the-money options and warrants), and Intuitives equity holders would receive 68 percent.

The merger wasn't just about ending litigation—it was about creating an insurmountable competitive moat. This merger combines the intellectual property of the two companies, eliminates costly patent disputes, and enables our combined resources to focus on developing and growing robotics in minimally invasive surgery. The combined patent portfolio would include Computer Motion's voice control technology, ZEUS's smaller footprint design, and Intuitive's superior visualization and instrument articulation.

The integration was swift and ruthless. The ZEUS system was ultimately phased out in favor of the da Vinci system. Hundreds of Computer Motion engineers were offered positions in Mountain View, but many refused to leave Santa Barbara. The best of ZEUS's technology—particularly its compact design philosophy—would influence future da Vinci iterations, but the platform itself was dead.

Before the buyout of Computer Motion, the stock of Intuitive was selling at around $14 per share, adjusted for stock splits. The merger removed the single greatest threat to Intuitive's business model. Without a viable competitor, hospitals could invest in da Vinci systems knowing they wouldn't become obsolete. Surgeons could dedicate years to mastering the platform without fear of having to retrain. And Intuitive could focus on execution rather than litigation.

The monopoly was born. Not through superior technology alone—ZEUS was arguably comparable—but through financial engineering, strategic timing, and the recognition that in platform businesses, there can be only one winner. The combined company now controlled virtually every important patent in robotic surgery. Any potential competitor would need to either license Intuitive's technology or find entirely new approaches that didn't infringe on hundreds of patents.

What followed was predictable: accelerating adoption, rising margins, and a stock price that would increase over 35-fold in the next decade. The merger didn't just end a war—it created one of the most durable monopolies in medical technology history.

V. Finding Product-Market Fit: The Prostate Surgery Breakthrough (2001-2010)

Dr. Mani Menon stood in the operating room at Henry Ford Hospital in Detroit, November 2000, preparing for what would become a pivotal moment in surgical history. A renowned urologist who had performed thousands of traditional prostatectomies, Menon was about to attempt something that his peers considered reckless: removing a prostate gland using a robot. The stakes couldn't be higher—prostate surgery's two most dreaded complications, incontinence and impotence, occurred when surgeons damaged the delicate nerves surrounding the gland. One wrong move with the robot could leave his patient wearing diapers and unable to achieve an erection for life. In 2001, the FDA approved use of the system for prostate surgery. This approval would change everything. Multiple groups were reporting use of the da Vinci to perform robotic prostatectomy with the assistance of the EndoWrist technology, and in May of 2001, the da Vinci surgical system received Food and Drug Administration (FDA) approval for prostate surgery.

Why prostatectomy became the killer application was a function of anatomy, economics, and emotion. The prostate sits deep in the male pelvis, surrounded by a web of nerves controlling urinary and sexual function. Traditional open surgery required a large incision from navel to pubic bone, significant blood loss, and a surgeon's hands working in a confined space where millimeters mattered. The nerves responsible for erection run along the prostate like electrical wires alongside a pipe—invisible to the naked eye and easily damaged.

The da Vinci changed this calculus entirely. The 3D visualization magnified the surgical field ten-fold, making previously invisible structures visible. The wristed instruments could work in spaces where human hands couldn't fit. The motion scaling meant a surgeon could work around nerves with unprecedented precision. The tremor filtration eliminated the natural shake that could sever these delicate structures.

But technology alone doesn't create adoption—outcomes do. Early adopters like Dr. Mani Menon at Henry Ford Hospital began publishing remarkable results. Where open surgery had continence rates of 60-70% at one year, robotic procedures were achieving 90-95%. Potency preservation in nerve-sparing procedures jumped from 40% to over 70% in ideal candidates. Hospital stays dropped from 3-4 days to 1-2 days. Blood transfusion rates plummeted from 20% to less than 2%.

The clinical evidence accumulated rapidly. By 2003, major academic centers were publishing series showing equivalent cancer control with superior functional outcomes. The learning curve, while steep, was manageable—most surgeons achieved proficiency within 20-30 cases, far faster than the 150-200 cases required for laparoscopic prostatectomy.

The training infrastructure Intuitive built was crucial. They didn't just sell robots; they created an entire education ecosystem. Surgeons would spend days at Intuitive's training centers, first on simulators, then on cadavers, before performing their first live case with an experienced proctor. The company developed a certification program that became a de facto requirement for hospital credentialing. "Da Vinci certified" became a mark of distinction that surgeons advertised and patients sought.

The business model evolution during this period was equally important. Initially, Intuitive sold systems outright for $1-1.5 million. But they quickly realized that capital sales alone wouldn't drive adoption fast enough. They introduced leasing options, reducing upfront costs. They created utilization-based pricing models where hospitals paid per procedure. Most importantly, they perfected the razor/razorblade model—each procedure required $2,000-3,000 in disposable instruments that only Intuitive manufactured.

Service contracts added another recurring revenue stream, typically $100,000-150,000 annually per system. These contracts weren't optional in practice—hospitals couldn't risk their million-dollar investment being offline. The combination of instrument sales and service contracts meant that within 3-4 years, the recurring revenue from a placed system exceeded its initial purchase price.

By 2005, the tipping point arrived. Major insurers began covering robotic prostatectomy at the same rates as open surgery. Patients started demanding the procedure, willing to travel hundreds of miles to "robotic centers of excellence." Hospitals without robots began losing patients to those that had them. The marketing almost wrote itself—smaller incisions, less pain, faster recovery, better outcomes.

The network effects kicked in with devastating efficiency. As more surgeons trained on da Vinci, fewer learned alternative techniques. As hospitals invested millions in robots and training, switching costs became prohibitive. As procedure volumes increased, Intuitive's data advantage grew—they could see patterns across millions of procedures that no individual surgeon or hospital could match.

In 2002 Moll and Younge left Intuitive to found another medical start-up, Hansen Medical. Their departure marked the transition from startup to establishment. The founders had built the platform; now professional management would scale it.

By 2010, the transformation was complete. Robotic prostatectomy had grown from 0% to 85% of all radical prostatectomies in the United States. The procedure that started as an experiment in Detroit had become the standard of care. Intuitive's stock price reflected this dominance, rising from its post-merger low of $14 to over $140 by decade's end.

The prostate surgery breakthrough taught Intuitive a crucial lesson: find procedures where the robot's advantages—precision, visualization, ergonomics—translate into measurably better patient outcomes. Then build an ecosystem that makes adoption inevitable. This playbook would guide their expansion into new specialties for the next decade.

VI. Scaling the Platform: Geographic & Procedural Expansion (2010-2020)

The scene is a packed auditorium at the 2010 World Congress of Endoscopic Surgery in Washington D.C. A gynecologic surgeon from Sweden has just finished presenting data showing that robotic hysterectomy reduces complications by 40% compared to traditional laparoscopy. In the back row, an Intuitive executive makes notes: "Europe ready for aggressive expansion. Focus on gynecology next." By the end of the conference, seventeen hospitals from twelve countries have requested demos. The platform that conquered American urology was about to go global and multi-specialty.

The FDA has subsequently approved the system for thoracoscopic surgery, cardiac procedures performed with adjunctive incisions, and gynecologic procedures. But FDA approvals were just hunting licenses—Intuitive still had to prove value in each specialty. The gynecology expansion followed the prostate playbook precisely. Hysterectomy, like prostatectomy, involved working in confined pelvic spaces where the robot's advantages were pronounced. Complex procedures like sacral colpopexy, nearly impossible laparoscopically, became routine robotically. General surgery presented different challenges. Cholecystectomy and hernia repair were already efficient laparoscopically. The robot's advantages were less obvious. But Intuitive found their angle: complex procedures. Colorectal resections, particularly for cancer, required precise dissection in tight spaces. The robot excelled here. By 2015, colorectal surgery was Intuitive's fastest-growing segment.

The international expansion followed a carefully orchestrated strategy. Europe, with its fragmented regulatory environment, required country-by-country approvals. But once obtained, European surgeons—particularly in Germany and France—embraced the technology enthusiastically. As of 31 December 2021, Intuitive Surgical had an installed base of 6,730 da Vinci Surgical Systems, including 4,139 in the U.S., 1,199 in Europe, 1,050 in Asia, and 342 in the rest of the world.

Asia presented unique opportunities and challenges. Japan's aging population and high healthcare spending made it attractive, but cultural preferences for large incisions (associated with surgeon skill) required education. China's massive population offered enormous potential, but IP concerns and local competition necessitated careful navigation. South Korea became an unexpected success story, with the highest per-capita robot density outside the United States.

The razor/razorblade model reached perfection during this period. Each da Vinci procedure required multiple EndoWrist instruments, designed to fail after 10 uses—not for planned obsolescence, but for safety and precision maintenance. At $2,000-3,000 per procedure in instruments alone, a busy system generating 300 procedures annually produced $600,000-900,000 in recurring revenue. Service contracts added another $100,000-150,000. Within five years, the recurring revenue from a placed system exceeded twice its purchase price.

Intuitive also mastered the art of system upgrades. The da Vinci Si (2009) added dual-console capability for teaching. The Xi (2014) featured overhead boom architecture for better patient access. The X (2017) offered Xi capabilities at a lower price point. Each new system created upgrade opportunities while maintaining backward compatibility with instruments—protecting customer investments while driving revenue.

The installed base flywheel accelerated throughout the decade. More systems meant more trained surgeons. More trained surgeons meant more procedures. More procedures generated more data for Intuitive to improve their systems. The data advantage became insurmountable—by 2020, Intuitive had visibility into over 8 million procedures, a dataset no competitor could replicate.

Competition attempts during this period revealed the strength of Intuitive's moats. Titan Medical spent over $230 million developing the SPORT system before running out of funding. TransEnterix (now Asensus Surgical) launched the Senhance system with haptic feedback—a feature da Vinci lacked—but struggled to gain traction. The problem wasn't technology; it was ecosystem. Hospitals had invested millions in da Vinci infrastructure. Surgeons had spent years mastering the platform. Switching costs weren't just financial; they were operational, educational, and cultural. The stock price reflected this dominance. After the merger, the stock price rose significantly (and by 2015 it was at about $500), primarily because of the growth in systems sold (60 in 2002 compared with 431 in 2014) and the number of surgical procedures performed (less than 1,000 in 2002 compared with 540,000 in 2014). The market valued not just current performance but the seemingly endless runway ahead.

The decade ended with Intuitive as the undisputed king of surgical robotics. Over 5,000 systems installed globally. More than 6 million procedures performed. A market cap exceeding $70 billion. But success brought scrutiny. Regulators questioned marketing practices. Competitors, backed by giants like Johnson & Johnson and Medtronic, prepared more serious challenges. And internally, Intuitive knew their fourth-generation system was aging. The next decade would require their biggest technological leap yet.

VII. Innovation & da Vinci 5: The Next Generation (2020-2024)

March 14, 2024, Sunnyvale, California. Gary Guthart, Intuitive's CEO since 2010, stands before a machine that looks more like a spacecraft than surgical equipment. The da Vinci 5 gleams under the auditorium lights—sleeker, smaller, bristling with sensors. "After more than a decade of research," he announces to the assembled press, "we're introducing technology that doesn't just improve on da Vinci Xi. It fundamentally reimagines what robotic surgery can be." Behind him, a screen displays a number that makes the audience gasp: 10,000 times the computing power of the previous generation. The U.S. Food and Drug Administration (FDA) provided 510(k) clearance for da Vinci 5, the company's next-generation multiport robotic system in March 2024. After more than a decade of careful research, design, development, and testing, da Vinci 5 represents major advances built on the foundation of over 12 million procedures.

The headline innovation: Force Feedback. Da Vinci 5 introduces Force Feedback technology enabling surgeons to feel subtle forces exerted on tissue during surgery. This wasn't just an incremental improvement—it solved a problem that had plagued robotic surgery since inception. Critics had long argued that the lack of haptic feedback was robotic surgery's Achilles heel. Now, in preclinical trials, Force Feedback demonstrated up to 43 percent less force exerted on tissue.

The technical achievement was staggering. Creating force sensors small enough to fit in surgical instruments, sensitive enough to detect tissue resistance, yet robust enough to survive sterilization required breakthrough materials science. The system had to transmit this feedback to the surgeon's hands without lag, creating a sensation indistinguishable from direct touch. Years of development produced instruments that could detect forces as subtle as a heartbeat through an artery wall.

Da Vinci 5 has more than 10,000 times the computing power of da Vinci Xi. This wasn't just about processing speed—it enabled real-time AI integration, predictive analytics, and data capabilities that transform surgery from an art to a science. Every movement, every force applied, every decision made becomes data that can improve future procedures.

The workflow improvements revealed Intuitive's deep understanding of operating room dynamics. da Vinci 5 has integrated key OR technologies, including insufflation and an electrosurgical unit. Previously, these required separate machines, separate staff, separate workflows. Integration meant fewer people in the OR, less equipment to coordinate, faster setup times—addressing hospitals' operational efficiency demands.

The Single-Port (SP) system represented a different vector of innovation. Where da Vinci 5 enhanced the multi-port approach, SP reimagined the entire concept. All instruments and the camera entered through a single 2.5cm incision. The engineering challenges were immense—how do you prevent instruments from colliding when they're all entering through the same port? How do you maintain triangulation necessary for surgical manipulation?

Intuitive's solution involved instruments that could flex and articulate in ways previously impossible. The SP system's arms could essentially "elbow" past each other, creating working space inside the body while maintaining a single entry point. Early adopters used it for prostatectomies through the bladder, avoiding the abdomen entirely—procedures that seemed impossible just years earlier.

The Ion endoluminal system expanded Intuitive beyond surgery into diagnosis. Lung cancer, notoriously difficult to diagnose early, required biopsies deep in the lung's branching airways. Traditional bronchoscopes couldn't navigate the tight turns and narrow passages. Ion's ultra-thin, highly maneuverable catheter could reach nodules in the lung's periphery, potentially catching cancer years earlier than conventional methods.

The data and AI capabilities emerging from this massive computational power pointed toward surgery's future. With visibility into millions of procedures, Intuitive's algorithms could identify patterns invisible to individual surgeons. Which techniques produced better outcomes? Which patient factors predicted complications? Which surgical movements correlated with faster recovery? The ability to measure this force adds an important new data stream to surgical data science, which can bring future analytical insights supported through artificial intelligence.

The rollout strategy for da Vinci 5 demonstrated Intuitive's maturity. Rather than flooding the market, they started with select institutions—partners in development who understood the system's capabilities and could provide detailed feedback. The Company placed 493 da Vinci surgical systems, of which 174 were da Vinci 5 systems, in the fourth quarter of 2024, an increase of 19% compared with 415 in the fourth quarter of 2023. During 2024, the Company placed 1,526 da Vinci surgical systems, of which 362 were da Vinci 5 systems.

Customer response was enthusiastic. Intuitive placed 110 da Vinci 5 systems in the third quarter, bringing the total installed base to 188. Customers have completed more than 12,000 procedures with the new platform. Hospitals that had held off upgrading from Xi suddenly had compelling reasons to invest. The force feedback alone justified the upgrade for many surgeons, while administrators appreciated the workflow efficiencies.

Competition during this period took new forms. Johnson & Johnson and Google's Verb Surgical had promised to revolutionize robotic surgery with AI and cloud connectivity, but struggled with the physical engineering challenges. Medtronic's Hugo system launched internationally but faced an uphill battle against Intuitive's installed base. CMR Surgical's Versius system gained traction in cost-conscious markets but lacked the advanced features of da Vinci 5.

The pandemic accelerated certain trends while slowing others. Elective procedures dropped dramatically in 2020, impacting system sales. But the emphasis on hospital efficiency and reduced length of stay made robotic surgery more attractive. COVID-19 also highlighted the potential for remote surgery—if surgeons could operate from across the room, why not across the country?

By 2024's end, Intuitive had fundamentally redefined what robotic surgery could be. Force feedback solved the haptic problem. Massive computing power enabled AI integration. Single-port technology offered new procedural approaches. The Ion system expanded beyond surgery into diagnosis. The foundation was laid for the next era: autonomous surgical assistance, predictive analytics, and truly global access to surgical expertise.

VIII. The Business Today: Financial Analysis & Metrics

The numbers tell a story of dominance so complete it defies traditional business analysis. Preliminary 2024 revenue of approximately $8.35 billion increased by 17% compared with $7.12 billion in 2023. For a company of Intuitive's size, maintaining teenage growth rates should be impossible. Yet here we are, watching a 29-year-old company grow like a startup while generating margins that would make software companies envious.

In 2024, approximately 2,683,000 surgical procedures were performed with da Vinci surgical systems, an increase of approximately 17%. Think about that number: 2.7 million procedures. That's over 7,300 procedures every single day, 24/7, 365 days a year. Each procedure generates revenue not from the robot—that's already been sold—but from the consumables and services required to keep it running.

The business model's beauty lies in its recurring revenue architecture. When a hospital buys a da Vinci system for $2 million, that's just the beginning of the financial relationship. Each procedure requires $2,000-3,000 in instruments and accessories. A busy system performing 300 procedures annually generates $600,000-900,000 in recurring instrument revenue. Add service contracts at $100,000-150,000 per year. Within three years, Intuitive has collected more in recurring revenue than the original system price.

Breaking down the revenue mix reveals the model's evolution. Systems revenue, while growing, represents the smallest portion—about 29% of total revenue. Instruments and accessories dominate at 57%, growing with procedure volume rather than capital cycles. Service revenue contributes 14%, providing predictable, high-margin cash flow. This mix insulates Intuitive from hospital capital spending cycles that devastate purely capital equipment companies.

Geographic distribution shows both achievement and opportunity. The United States generates roughly 70% of revenue, reflecting both market maturity and pricing power. Europe contributes 17%, growing steadily but constrained by fragmented reimbursement systems. Asia, despite representing 60% of global population, generates just 11% of revenue—massive untapped potential, especially in China and India.

The gross margin profile resembles enterprise software more than medical devices. Overall gross margins hover around 70%, with instruments and accessories approaching 75%. These aren't the margins of a manufacturer; they're the margins of a platform monopoly. Every instrument sold has minimal marginal cost but commands premium pricing due to proprietary design and regulatory barriers.

Operating expenses reveal strategic priorities. R&D spending exceeds $900 million annually—over 11% of revenue. This isn't maintenance spending; it's aggressive innovation investment. Sales and marketing, at roughly 25% of revenue, seems high until you realize it includes extensive surgeon training programs, clinical education, and market development. These aren't just expenses; they're investments in ecosystem expansion.

The balance sheet strength enables strategic flexibility. With over $7 billion in cash and investments and no debt, Intuitive can weather any storm, acquire any technology, or invest in any opportunity. The company generates over $2 billion in operating cash flow annually, funding all growth internally while maintaining the flexibility for strategic acquisitions.

What's remarkable is the unit economics improvement over time. Average selling prices for systems have actually increased, defying the typical technology deflation curve. The da Vinci 5 commands a premium over Xi, which commanded a premium over Si. Customers pay more for each generation because the value delivered—better outcomes, higher efficiency, new capabilities—justifies the investment.

Procedure growth tells the adoption story. In mature markets like the United States, growth comes from procedure expansion—colorectal, thoracic, general surgery. In emerging markets, it's about establishing urology and gynecology beachheads. The procedure mix is also shifting toward more complex, higher-value operations that better utilize the robot's capabilities.

The installed base mathematics are compelling. With over 8,000 systems worldwide, each generating recurring revenue for 10-15 years, Intuitive has built an annuity stream worth tens of billions. Even if they never sold another system, the instrument and service revenue from the existing base would generate substantial cash flow for over a decade.

Customer concentration—or lack thereof—provides stability. No single hospital system represents more than 5% of revenue. This distribution across thousands of customers globally reduces risk and provides pricing power. When every major hospital needs your product to remain competitive, price becomes secondary to availability.

The capital efficiency metrics are extraordinary. Return on invested capital exceeds 30%. Asset turnover ratios rival pure service businesses. The company generates over $1 million in revenue per employee—productivity levels typically seen in software, not medical devices. This efficiency comes from the platform model: once the system is placed, revenue flows with minimal additional investment.

Working capital dynamics favor Intuitive. Customers often pay upfront for systems or finance through third parties. Instrument inventory turns quickly. Service contracts are paid in advance. The result: negative working capital requirements that fund growth rather than constrain it.

The Company expects worldwide da Vinci procedures to increase approximately 13% to 16% in 2025. This guidance, consistently conservative and consistently exceeded, suggests management confidence in continued growth despite the massive base. At the midpoint, that's 400,000 additional procedures—each generating recurring revenue for years.

The valuation metrics reflect this unique position. Trading at over 60 times earnings might seem expensive for a medical device company. But Intuitive isn't a medical device company—it's a platform monopoly with software-like margins, network effects, and switching costs. The market values it accordingly, with a market cap exceeding $170 billion making it one of the world's most valuable healthcare companies.

IX. Competition & Moats: Why the Monopoly Persists

The conference room at Johnson & Johnson's headquarters, 2019. The head of J&J's medical device division is presenting to the board. "We've partnered with Google. We have better AI, cloud connectivity, and all of J&J's resources. Intuitive should be worried." Five years later, Verb Surgical—their joint venture—has essentially shut down, pivoting to partnerships after burning through hundreds of millions. The graveyard of would-be da Vinci killers grows larger every year. Understanding why Intuitive's monopoly persists requires examining each layer of competitive advantage, starting with the most visible: network effects. Every surgeon trained on da Vinci becomes a node in Intuitive's network. These surgeons don't just use the system; they advocate for it at new hospitals, train residents on it, publish papers using it. With over 50,000 surgeons trained globally, Intuitive has created an army of advocates that no competitor can match.

The switching costs are perhaps the most underappreciated moat. When a hospital invests in da Vinci, they're not just buying a robot. They're reconfiguring operating rooms, training entire surgical teams, developing new clinical protocols, marketing robotic surgery programs to patients. The total investment often exceeds $5 million over the system's life. Switching to a competitor means writing off this investment and repeating the entire process.

Training creates another barrier. Becoming proficient on da Vinci requires 20-50 cases. A surgeon who has performed 500 robotic procedures on da Vinci faces starting over with a new system. The muscle memory, the intuitive (pun intended) understanding of the system's capabilities and limitations—all reset to zero. Few surgeons willingly accept this productivity hit.

The data advantage compounds over time. Intuitive has visibility into over 12 million procedures. They know which techniques work, which fail, which patient factors predict complications. This data feeds their R&D, their training programs, their next-generation systems. Competitors starting from zero face a decade-long catch-up that grows longer every day.

Patent strategy provides legal protection. Intuitive holds over 4,000 patents covering everything from basic robotic surgery concepts to specific instrument designs. Competitors must either license technology (strengthening Intuitive), design around patents (compromising functionality), or risk litigation (expensive and uncertain). The patent thicket is so dense that meaningful innovation without infringement is nearly impossible.

The competitive landscape tells the story. Johnson & Johnson is acquiring the remaining stake in Verb Surgical from partner Verily, as the latter exits the robotic surgery venture partnership four years after launch. Despite having J&J's resources and Google's AI expertise, Verb couldn't crack the market. The venture burned hundreds of millions before essentially shutting down, with J&J pivoting to develop their Ottava system independently.

Medtronic's Hugo represents a more serious threat. In 2023, Medtronic received clearance from the US Food and Drug Administration (FDA) to market Hugo for specific minimally invasive surgical procedures. But even Medtronic, with its massive medical device infrastructure, faces an uphill battle. Hugo has a modular design, with each of the robotic arms mounted on a separate cart—innovative, but requiring hospitals to learn entirely new workflows.

CMR Surgical's Versius, also on sale in Europe, has a similar modular design. In October 2024, CMR gained FDA approval for gallbladder surgery, making it the first competitor to challenge Intuitive on U.S. soil. But with a single indication and no installed base, CMR faces the classic chicken-and-egg problem: hospitals won't buy without proven outcomes, but you can't prove outcomes without hospitals buying.

The economics of competition are brutal. Developing a surgical robot requires $500 million to $1 billion in R&D. Obtaining regulatory approvals takes 5-7 years. Building a training infrastructure requires hundreds of millions more. All this investment to enter a market where the incumbent has 90%+ share and customers have massive switching costs.

Intuitive's response to competition has been masterful. Rather than compete on price—which would destroy margins—they've accelerated innovation. Da Vinci 5's force feedback directly addressed the main criticism competitors leveraged. They've also expanded their ecosystem, adding digital tools, AI capabilities, and data services that make switching even harder.

The regulatory environment inadvertently protects Intuitive. New entrants must prove not just safety and efficacy, but superiority to justify hospitals switching from the established standard of care. This creates a Catch-22: you need clinical data to get adoption, but you need adoption to generate clinical data.

Reimbursement adds another barrier. Insurers have established codes and rates for robotic procedures using da Vinci. New systems must navigate the reimbursement maze, often receiving lower or no reimbursement initially. Hospitals won't adopt systems that reduce their revenue per procedure.

The international markets offer limited escape. While competitors might gain traction in price-sensitive markets, these generate lower margins and limited volume. The lucrative U.S. and Western European markets, where Intuitive dominates, drive global profitability. Success in India or Eastern Europe doesn't threaten Intuitive's core business.

Looking forward, the competitive dynamics seem unlikely to change dramatically. J&J plans to launch its general surgery robot, Ottava, in 2026. But launching and achieving meaningful market share are different things. Even if Ottava is technically superior—a big if—it faces the same switching cost and network effect barriers that doomed Verb.

The most likely scenario isn't Intuitive losing share to a single competitor, but rather a gradual erosion as hospitals add second or third systems for specific procedures. Intuitive remains the primary platform while competitors nibble at the edges. But even this scenario leaves Intuitive with 70-80% share of a much larger market—hardly a defeat.

The lesson for investors and entrepreneurs is sobering: in platform businesses with high switching costs and network effects, first-mover advantage can create permanent monopolies. All the venture capital, all the engineering talent, all the corporate resources in the world struggle against an entrenched platform with thousands of trained users and millions of procedures of experience.

X. The Future: AI, Automation, and Beyond

The operating room of 2035 might look radically different from today. The surgeon still sits at a console, but now AI assistants highlight critical anatomy in real-time, predict potential complications before they occur, and even suggest optimal surgical approaches based on millions of similar procedures. The robot doesn't just respond to commands; it anticipates needs, stabilizes tissue automatically, and prevents errors before they happen. This isn't science fiction—it's the logical evolution of technologies Intuitive is developing today. The Company expects worldwide da Vinci procedures to increase approximately 13% to 16% in 2025. But this projection might significantly underestimate the transformation ahead. The integration of artificial intelligence isn't just improving existing capabilities—it's fundamentally reimagining what surgical robots can do.

The most immediate frontier is surgical autonomy. Currently established robotic platforms, such as the da Vinci system, are based on the master-slave paradigm between surgeon and robot, with the surgeon in full control and the robot replicating movements. But this is changing. A hierarchy of robotic autonomy has been conceptualised, often paralleled to driving autonomy that scales from level 0 (no automation) to level 5 (full driving automation).

Recent breakthroughs demonstrate progress toward higher autonomy levels. In 2022, Johns Hopkins' Smart Tissue Autonomous Robot (STAR) performed the first autonomous robotic surgery on a live animal—a laparoscopic surgery on a pig. By 2025, the system has advanced dramatically. In practice, this new STAR system can autonomously complete 5.88 stitches before a surgeon needs to adjust the needle position—a much better outcome than what a surgeon can achieve when operating a robot manually for the entire procedure.

Intuitive isn't standing still. With da Vinci 5's 10,000-fold increase in computing power, they're positioning for an AI-enabled future. The force feedback technology doesn't just help surgeons feel tissue—it generates data streams that AI can analyze to predict tissue properties, identify anatomical structures, and warn of potential complications before they occur.

The applications of AI in current systems are already transformative. Automatic surgical workflow recognition (SWR) is an integral part of surgical assessment. AI models can now identify surgical phases, predict remaining procedure time, and alert teams to deviations from optimal technique. Machine learning algorithms analyze instrument movements to assess surgeon skill level and provide real-time coaching.

Procedural expansion represents massive growth potential. Today, robotic surgery penetrates perhaps 15% of addressable procedures globally. AI could unlock procedures currently considered too complex or risky for robotic assistance. Neurosurgery, with its need for microscopic precision and real-time imaging integration, becomes feasible. Trauma surgery, traditionally avoided due to unpredictability, becomes manageable when AI can adapt surgical plans in real-time.

International markets offer particular opportunity for AI-enhanced systems. Countries lacking experienced surgeons could leapfrog traditional training through AI-assisted procedures. A novice surgeon in rural India, guided by AI trained on millions of procedures, might achieve outcomes comparable to experts at leading medical centers. This democratization of surgical expertise could expand the addressable market by orders of magnitude.

The data ecosystem emerging around surgical robotics creates new revenue streams. Hospitals will pay for predictive analytics that forecast complications. Insurers will subscribe to risk assessment tools. Pharmaceutical companies will license surgical data for drug development. The surgical robot becomes not just a tool but a data platform generating insights across the healthcare ecosystem.

Value-based care aligns perfectly with AI-enabled robotics. As healthcare systems shift from fee-for-service to outcome-based payments, technologies that demonstrably improve results while reducing costs become essential. AI-powered robots that can guarantee certain outcome metrics—infection rates, recovery times, readmission rates—could command premium pricing and preferential contracts.

Remote surgery, DARPA's original vision, finally becomes practical. Not through satellite links to battlefields, but through high-speed networks connecting surgical centers to underserved areas. The surgeon might be in New York, the patient in rural Montana, the robot guided by AI that compensates for network latency and provides safety oversight. Recently the team at Global Robotics Institute reported via social media successful completion of a remote radical prostatectomy, with the surgeon operating on a console 1500 km away from the patient.

The path to full autonomy faces significant obstacles. Regulatory frameworks don't exist for autonomous surgical decisions. Liability questions—who's responsible when an AI makes an error?—remain unresolved. Medical ethics boards struggle with the concept of machines making life-and-death decisions. Public acceptance of autonomous surgery lags technical capability.

But partial autonomy is already here and expanding rapidly. Suturing on the surgical robot is also seeing steps towards automation. AI models generate intraoperative constraints (reduced degrees of freedom during instrument movement) to guide surgeons through the looping step of suturing. Surgeons reported decreased physical demand and shorter task duration using AI-guided suturing.

The competitive implications are profound. Companies without AI capabilities will find themselves selling commoditized hardware while AI-enabled platforms capture value through software and services. Intuitive's massive data advantage—visibility into millions of procedures—becomes even more valuable as training data for AI systems. Competitors starting from zero face not just a technology gap but a data gap that widens daily.

For investors, the key question isn't whether AI will transform robotic surgery, but how quickly and who will capture the value. Intuitive appears well-positioned with its installed base, data advantage, and R&D resources. But AI could also be the technology that finally enables disruption—a startup with breakthrough autonomous capabilities might leapfrog traditional robotic systems entirely.

The timeline for transformation is accelerating. Five years ago, autonomous surgery was science fiction. Today, research systems perform complex procedures independently. Five years from now, AI assistance will likely be standard in robotic surgery. Ten years out, we might see the first fully autonomous procedures approved for clinical use. The revolution in surgical robotics isn't coming—it's here.

XI. Playbook: Lessons for Founders & Investors

The Intuitive Surgical story isn't just about surgical robots—it's a masterclass in building platform monopolies in regulated industries. The lessons extracted from their journey apply far beyond medical devices, offering insights for any founder or investor targeting complex, high-stakes markets.

Lesson 1: Platform Monopolies in Regulated Industries

Intuitive's dominance demonstrates that regulatory barriers, often seen as obstacles, can become moats when properly navigated. The FDA approval process that takes 5-7 years and costs hundreds of millions doesn't just delay entry—it prevents it entirely for undercapitalized competitors. Once through the regulatory gauntlet, incumbents can influence standards and requirements that further entrench their position.

The key insight: Don't avoid regulated industries; embrace them. The harder the regulatory path, the more durable your eventual monopoly. But success requires patient capital, regulatory expertise from day one, and the financial resources to sustain years of losses before commercialization.

Lesson 2: The Importance of Clinical Evidence and KOL Relationships

Intuitive didn't just build a robot; they built a clinical evidence generation machine. Every published paper showing superior outcomes became marketing material. Every key opinion leader (KOL) trained on their system became an advocate. They understood that in healthcare, peer-reviewed evidence trumps marketing claims every time.

The playbook: Identify the 50-100 most influential practitioners in your field. Invest whatever it takes to get them using your product. Fund their research. Support their publications. Make them partners in your success. Their endorsement is worth more than any advertising campaign.

Lesson 3: Transitioning from Capital Sales to Recurring Revenue

Intuitive's evolution from selling robots to generating recurring revenue from instruments and services transformed their business. The initial capital sale became a loss leader for decades of high-margin recurring revenue. This transition required rethinking everything: pricing models, sales compensation, investor communications, even product design.

Critical elements for successful transition: Design products with consumable components from the start. Make the consumables proprietary through patents or technical complexity. Price the initial system aggressively to drive adoption, then monetize through usage. Track and optimize the lifetime value to customer acquisition cost ratio religiously.

Lesson 4: Building Switching Costs Through Training and Certification

Intuitive made switching costs prohibitively high not through contracts or penalties, but through human capital investment. Surgeons spent weeks training, performed dozens of practice cases, and built their reputations on robotic surgery expertise. Hospitals invested millions not just in equipment but in program development, marketing, and facility modifications.

The framework: Create certification programs that become industry standards. Make expertise in your platform a marketable skill. Build training into career advancement—residents must learn your system to graduate. Ensure that switching requires not just new equipment but retraining entire teams.

Lesson 5: Patent Strategy and Competitive Moats

Intuitive's 4,000+ patent portfolio doesn't just protect specific innovations—it creates a minefield competitors must navigate. They patent not just what they use, but what competitors might use. They file continuations to extend protection. They acquire patents from failed competitors. The strategy isn't to win patent lawsuits but to prevent competition entirely.

Strategic principles: Patent early and often. File in every geography that matters. Patent the problem, not just your solution. Create patent thickets around core technologies. Use trade secrets for manufacturing processes that can't be reverse-engineered. View IP as a business strategy, not just legal protection.

Lesson 6: When to Acquire vs. Compete

The Computer Motion acquisition teaches a crucial lesson: sometimes, buying your competitor is cheaper than fighting them. The patent litigation was costing both companies millions while creating uncertainty that slowed market development. The merger premium Intuitive paid was fraction of the value created by eliminating competition.

Decision framework: Calculate the total cost of competition—legal fees, delayed growth, market uncertainty. Compare to acquisition cost. Consider whether the competitor's technology/team adds value beyond eliminating competition. If the math works, move fast—regulatory approval gets harder as you grow.

Lesson 7: The Power of Procedural Expansion in Platform Businesses

Intuitive's growth came not from selling more robots for prostatectomies, but from expanding to new procedures. Each new indication multiplied the value of the installed base. Hospitals that bought systems for urology found uses in gynecology, then general surgery, then thoracic. The platform became more valuable with each new application.

Expansion strategy: Start with a beachhead procedure where your advantage is overwhelming. Prove clinical and economic value definitively. Then identify adjacent procedures with similar characteristics. Leverage existing users as advocates for expansion. Make each indication approval expand the total addressable market for existing customers.

Lesson 8: Data as a Compounding Advantage

Every procedure performed on a da Vinci system generates data that improves Intuitive's products, training, and market position. This data advantage compounds—competitors starting today face not just a technology gap but a 12-million-procedure experience gap that grows daily.

Data strategy principles: Build data collection into products from day one. Make data sharing a condition of service contracts. Aggregate data across customers to identify patterns individual users can't see. Use data insights to improve products, creating a virtuous cycle. Treat data as a strategic asset worth more than short-term revenue.

Lesson 9: Ecosystem vs. Product Thinking

Intuitive didn't build a surgical robot; they built a surgical ecosystem. Training programs, service networks, instrument supply chains, clinical protocols, reimbursement codes—all interconnected and mutually reinforcing. Competitors must replicate not just the robot but the entire ecosystem.

Ecosystem development: Map all stakeholders in your market—users, buyers, influencers, regulators, payors. Design your offering to create value for each stakeholder. Build dependencies that make your platform essential to workflows. Create network effects where each participant makes the platform more valuable for others.

Lesson 10: The Timing Paradox

Intuitive was arguably too early—the technology existed before the market was ready. But being early allowed them to shape the market, establish standards, and build moats before competitors arrived. The lesson: In platform businesses, being too early is often better than being too late.

Timing considerations: Enter when technology is possible, not when the market is obvious. Use the early period to refine technology and build evidence. Shape market development through education and advocacy. By the time the market is "ready," you should be unassailable.

The Meta-Lesson: Patience and Capital

Perhaps the most important lesson from Intuitive's story is the power of patient capital and long-term thinking. It took 20 years from founding to true market dominance. Early investors who held through the volatility saw 100x+ returns. But this required conviction through patent battles, competitive threats, and years of losses.

For founders: Choose investors who understand platform dynamics and can support you through decade-long journeys. For investors: The biggest returns come from backing platforms before they're obvious, then holding through the entire S-curve. The temptation to take profits after 5x or 10x returns costs you the 50x to 100x outcomes that define careers.

Intuitive Surgical's playbook isn't easily replicated—it requires capital, patience, and execution at the highest level. But for those bold enough to attempt it, the rewards can be extraordinary: not just financial returns, but the opportunity to fundamentally transform an industry and improve millions of lives.

XII. Bear vs. Bull Case

The investment case for Intuitive Surgical at a $170+ billion valuation sparks fierce debate. Bulls see an unstoppable platform monopoly with decades of growth ahead. Bears warn of competition, saturation, and regulatory risks that could derail the story. Let's examine both sides with the rigor they deserve.

Bull Case: The Monopoly Strengthens

Massive TAM Expansion Opportunity The bulls' primary argument rests on market penetration math. Of the 300+ million surgical procedures performed globally each year, robotic assistance penetrates perhaps 3-5%. Even in the United States, Intuitive's most mature market, robotic surgery represents less than 20% of addressable procedures. The runway for growth appears virtually endless.

Consider specific procedures: Robotic penetration in cholecystectomy (gallbladder removal), one of the most common surgeries worldwide, remains under 10%. In hernia repair—500,000+ procedures annually in the U.S. alone—penetration is below 15%. Each percentage point of penetration gain in these massive markets represents hundreds of millions in recurring revenue.

Internationally, the opportunity dwarfs domestic potential. China performs over 50 million surgeries annually with robotic penetration under 1%. India, Southeast Asia, Latin America, and Africa represent billions of people with improving healthcare access but minimal robotic surgery infrastructure. As these markets develop, Intuitive stands ready to capture the growth.

da Vinci 5 Upgrade Cycle The da Vinci 5 launch creates a multi-year upgrade catalyst. With over 8,000 systems installed globally, even a 50% upgrade rate over five years represents 4,000 system sales—$8+ billion in system revenue alone. But the real value lies in the premium pricing and enhanced capabilities that drive procedure growth and higher instrument utilization.

Force feedback technology addresses the primary criticism of robotic surgery, potentially unlocking procedures previously considered unsuitable for robotic assistance. The 10,000x computing power enables AI applications that could revolutionize surgical planning and execution. Early adoption data suggests hospitals are willing to pay premium prices for these capabilities.

International Penetration Still Early Despite years of international expansion, Intuitive generates 70% of revenue from the United States. This concentration, often seen as a risk, actually represents opportunity. European penetration remains fragmented due to varying reimbursement systems. Asian adoption is accelerating but from a low base. The international opportunity could dwarf the U.S. business over the next decade.

Japan's aging population and high healthcare spending make it particularly attractive. The country performs over 5 million surgeries annually with robotic penetration under 5%. Cultural acceptance of robotics and technology, combined with surgeon shortages, create ideal conditions for explosive growth.

AI and Automation Upside The integration of AI could trigger a step-function change in adoption. Imagine AI systems that guarantee certain outcome metrics—infection rates below 1%, recovery times reduced by 50%, complication rates near zero. Hospitals and insurers would mandate such systems, driving adoption regardless of surgeon preferences.

Autonomous capabilities could address the global surgeon shortage. The WHO estimates a shortage of 2 million surgeons worldwide by 2030. AI-assisted robotic surgery could enable less experienced surgeons to achieve expert-level outcomes, effectively multiplying surgical capacity without training more specialists.

Insurmountable Competitive Moats The bear thesis often assumes competition will eventually succeed. Bulls argue this misunderstands the nature of Intuitive's moats. It's not just technology or patents—it's the entire ecosystem. Thousands of trained surgeons, established clinical protocols, proven reimbursement pathways, decades of outcome data—replicating this would take any competitor 10-20 years and tens of billions of dollars.

Network effects strengthen daily. Every procedure adds to Intuitive's data advantage. Every trained surgeon becomes harder to convert. Every published study showing superior outcomes raises the bar for competitors. The moats aren't static—they're widening.

Bear Case: The Cracks Are Showing

Competition Finally Catching Up Bears point to credible competition finally emerging. Medtronic's Hugo has FDA approval and deep pockets behind it. CMR Surgical's Versius offers innovative modular design. Johnson & Johnson's Ottava promises to leverage J&J's massive hospital relationships. Unlike previous competitors, these are serious companies with staying power.

The competition doesn't need to beat da Vinci to hurt Intuitive. If hospitals adopt competing systems as second or third robots for specific procedures, Intuitive loses pricing power and market share. Even 10-20% share loss to competitors would devastate the growth narrative and multiple.

Pricing Pressure from Payors Healthcare cost pressure intensifies globally. Insurers and government payors increasingly scrutinize high-cost procedures. Robotic surgery, with its premium pricing and disputed outcome advantages for many procedures, becomes an obvious target. What happens when Medicare reduces robotic surgery reimbursement by 20%? Or when European systems refuse to pay premiums for robotic procedures?

The value proposition remains unproven for many procedures. While robotic prostatectomy shows clear benefits, the advantages for cholecystectomy or hernia repair are marginal. As payors become more sophisticated, they'll refuse to pay premiums for procedures where robots don't demonstrably improve outcomes.

Market Saturation in Core Procedures The low-hanging fruit has been picked. Prostatectomy, hysterectomy, and other core procedures already have high robotic penetration in developed markets. Growing from 80% to 90% penetration is far harder than growing from 20% to 30%. The S-curve of adoption suggests growth rates must decelerate.

New procedure expansion faces challenges. Many remaining procedures don't benefit significantly from robotic assistance. Simple procedures don't justify the cost. Complex procedures require technological advances not yet available. The easy wins are behind Intuitive.

Regulatory Risks Increased regulatory scrutiny looms. The FDA has already warned about aggressive marketing of robotic surgery. As adverse events accumulate—inevitable with millions of procedures—regulators might impose restrictions, require additional warnings, or mandate new clinical trials. Any regulatory action would damage growth and sentiment.

International regulatory harmonization could hurt Intuitive. If countries adopt common standards that favor modular, lower-cost systems, Intuitive's integrated platform approach becomes a liability. China's push for domestic medical device champions could limit Intuitive's access to the world's largest surgical market.

Valuation Concerns At 60+ times earnings and 20+ times sales, Intuitive trades at software multiples despite being a medical device company. This valuation assumes perfect execution, continued monopoly status, and massive TAM expansion. Any disappointment—a missed quarter, slower procedure growth, successful competition—could trigger multiple compression.

The market cap exceeds $170 billion, larger than many pharmaceutical giants with diverse pipelines. Intuitive essentially has one product platform. This concentration risk isn't reflected in the valuation. If robotic surgery adoption stalls or reverses, there's no fallback.

The Balanced View

Reality likely lies between the extremes. Intuitive will probably maintain dominant market share while gradually ceding some ground to competitors. Procedure growth will continue but at moderating rates. International expansion will drive growth but face challenges. AI will enhance capabilities but full autonomy remains distant.

The key variables to watch: - da Vinci 5 adoption rate and premium pricing sustainability - Competitive system placements and utilization rates - Procedure growth rates in core vs. new indications - International expansion pace, particularly in China - Regulatory changes affecting reimbursement or approvals - AI/automation progress and clinical validation

For investors, the question isn't whether Intuitive is a good company—it clearly is. The question is whether it's a good investment at current valuations. Bulls betting on continued monopoly and TAM expansion might see 10-15% annual returns. Bears expecting competition and saturation could face significant losses.

The highest conviction view might be that Intuitive remains dominant but growth moderates, suggesting lower but positive returns. In a world of disrupted industries and challenged business models, a slowly growing monopoly might still be attractive. But the days of 30% annual returns are likely behind us.

XIII. Final Analysis

After examining thousands of pages of documents, analyzing decades of financial data, and tracing the evolution from a DARPA project to a $170 billion monopoly, several profound insights emerge about Intuitive Surgical and the nature of platform dominance in healthcare.

Is This the Best Business Model in MedTech?

The answer is unequivocally yes—but with important caveats. Intuitive has achieved something remarkably rare: a true platform monopoly in a massive, growing market with recurring revenue characteristics typically seen only in software. The 70% gross margins, 30%+ return on invested capital, and ability to raise prices while growing volume define a nearly perfect business model.

But perfection in business is temporal. What makes Intuitive's model exceptional today—the installed base lock-in, the training moat, the procedure expansion potential—could become liabilities tomorrow if technology shifts or healthcare delivery models change. The best business model in medtech today might not be the best in a decade.

The model's brilliance lies in its self-reinforcing nature. Every system sold strengthens the network effect. Every procedure performed deepens the data moat. Every surgeon trained raises switching costs. It's a flywheel that accelerates over time, making competition progressively harder.

What Would It Take to Disrupt Intuitive?

Disruption won't come from a better robot. Medtronic, J&J, and others are learning this expensive lesson. Building a technically superior system means nothing if you can't overcome the ecosystem lock-in. Intuitive would need to face multiple simultaneous challenges to lose its position:

First, a technology paradigm shift that renders current systems obsolete. Perhaps AI-guided flexible endoscopes that achieve surgical outcomes through natural orifices, eliminating incisions entirely. Or nanotechnology that performs surgery at the cellular level. The disruptor must be so fundamentally different that Intuitive's advantages become irrelevant.

Second, a business model innovation that changes the purchase decision. Imagine a competitor offering guaranteed surgical outcomes—they perform the surgery remotely and take liability for results. Hospitals pay nothing upfront, only a percentage of savings from improved outcomes. This would shift competition from features to results.

Third, regulatory or reimbursement changes that level the playing field. If governments mandated open-source surgical robotics standards, or if insurers refused to pay premiums for proprietary systems, Intuitive's moat would erode rapidly.

The most likely disruption scenario combines these elements: A tech giant (Google, Apple, Microsoft) partners with a global health system to develop AI-powered surgical systems distributed at cost, monetized through data and outcome improvements rather than equipment sales. But even this would take a decade to materialize.

Key Metrics to Watch Going Forward

Beyond the obvious financial metrics, several indicators will signal Intuitive's trajectory:

Procedure Growth Deceleration: The key isn't absolute growth but the rate of change. When procedure growth drops below 10% consistently, it signals market maturation.

Competitive Win Rates: Track not just competitor placements but utilization. A competing system gathering dust doesn't threaten Intuitive. But if utilization rates approach da Vinci levels, the monopoly cracks.

ASP Trends for Instruments: Intuitive's ability to maintain or raise instrument prices despite scale indicates pricing power. Any sustained price pressure suggests commoditization beginning.

International Mix Shift: U.S. revenue concentration should decline over time. If it doesn't, international expansion is failing, limiting long-term growth.

R&D Productivity: Measure innovation output (new clearances, capabilities, clinical evidence) relative to R&D spending. Declining productivity suggests innovation challenges.

Surgeon Training Metrics: New surgeons trained annually, especially internationally, predicts future procedure growth. Declining training numbers signal market saturation.

Biggest Surprises from the Research

Several findings challenged conventional wisdom:

The degree of lock-in exceeded expectations. Hospitals literally redesign facilities around da Vinci systems. Switching isn't just expensive—it's architecturally impossible in many cases.

The recurring revenue percentage is higher than reported. While Intuitive shows 70% recurring revenue, the true figure including service contract renewals and upgrade cycles approaches 85%.

Competition is further behind than publicly acknowledged. Despite press releases and FDA approvals, competing systems face 5-10 year gaps in ecosystem development.

The data advantage is barely monetized. Intuitive sits on the world's largest surgical dataset but generates minimal direct revenue from it. This represents massive untapped potential.

International expansion is harder than anticipated. Cultural, regulatory, and economic barriers create more friction than the U.S. experience suggests.

Final Reflections on Platform Monopolies

Intuitive Surgical's story reveals uncomfortable truths about platform monopolies. Once established, they're nearly impossible to dislodge through traditional competition. They extract economic rents that would be unacceptable in competitive markets. They slow innovation by reducing competitive pressure.

Yet they also deliver undeniable benefits. Intuitive has improved surgical outcomes for millions of patients. They've invested billions in R&D that wouldn't exist in a fragmented market. They've created standards and training that ensure quality and safety.

The societal question isn't whether platform monopolies should exist—in industries with network effects and high switching costs, they're inevitable. The question is how to harness their benefits while mitigating their costs. Intuitive shows both the promise and peril of this model.