Ingersoll Rand: The Heavy Metal Compounding Machine

I. Introduction & Episode Roadmap

Walk onto the floor of a semiconductor fab in Arizona, a pharmaceutical fill-finish line in Ireland, or an automotive body shop in Kentucky, and somewhere in the background — usually in a mechanical room nobody photographs for the annual report — a machine is humming that the entire operation quietly depends on. It compresses ordinary air to eight or ten times atmospheric pressure and pushes it through the plant to drive tools, actuate valves, move powders, and keep the line breathing. It is loud, heavy, painted an industrial shade of gray or blue, and about as far from a glamorous technology story as a piece of capital equipment can get. And yet the company that makes a great many of these machines has, over the last decade, compounded shareholder capital at a rate that would make a software founder blush.

That is the paradox worth sitting with for the next couple of hours. Ingersoll Rand Inc. (NYSE: IR) manufactures air compressors, blowers, vacuum pumps, and dosing systems — the least sexy corner of the industrial economy. By mid-2026 it carried a market capitalization of roughly $31 billion, generated about $7.65 billion in annual revenue, and was routinely mentioned in the same breath as Danaher and Roper as one of the most disciplined serial acquirers in the public markets.[^12]5 How does a business built on heavy metal end up behaving, financially, like a capital-light compounding machine? That is the question this episode exists to answer, and the answer is not "because compressors are a great business." It is because a specific group of people bolted a specific operating system and a specific ownership philosophy onto a mediocre commodity, and the machine they built turned out to be the interesting part.

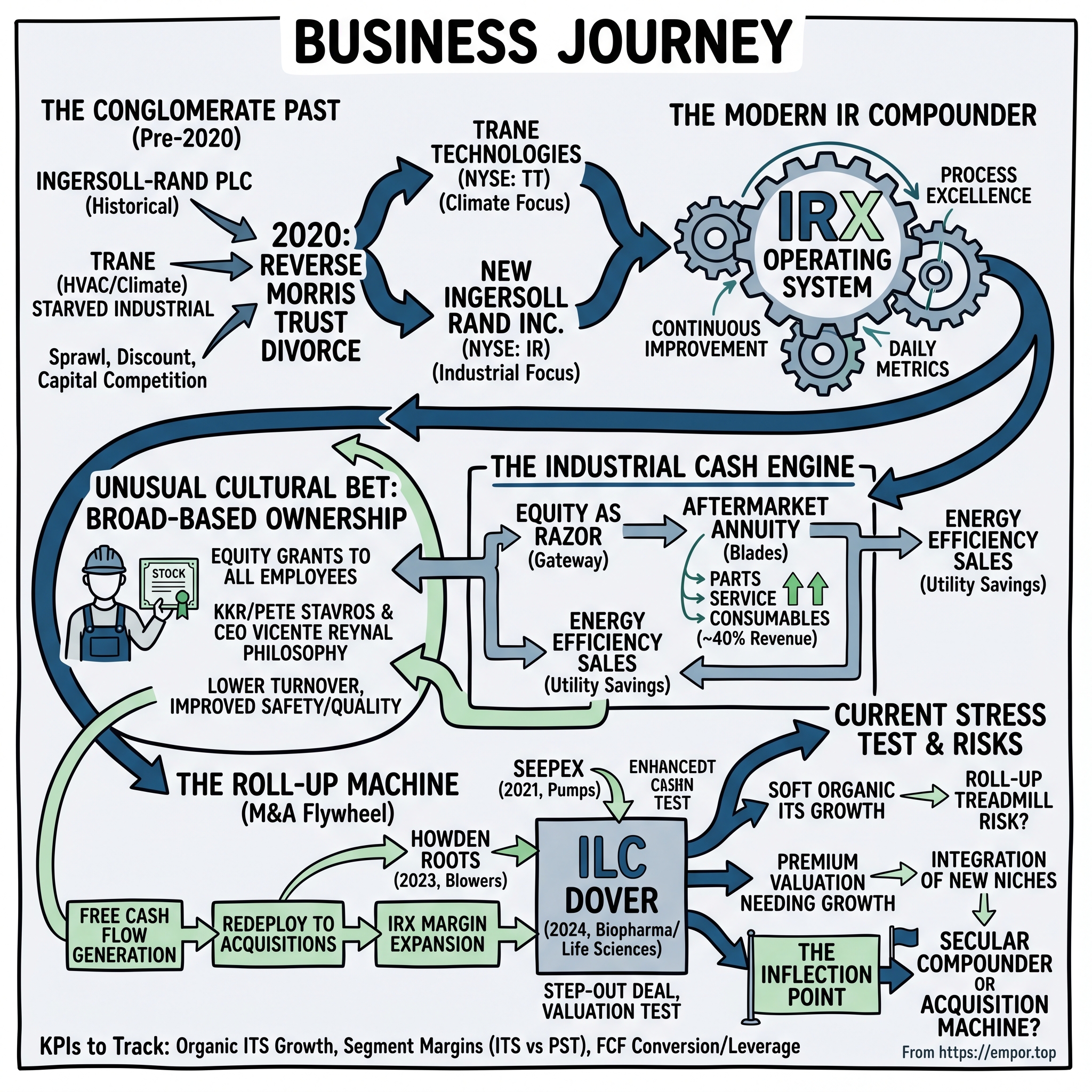

To understand the modern company, you have to start with a divorce. For most of the twentieth century "Ingersoll-Rand" was a sprawling industrial conglomerate — rock drills, golf carts, pneumatic tools, and eventually a giant heating-and-cooling business acquired at the top of a cycle. Then, in early 2020, the whole thing was cleaved in two. The climate business, home to the Trane and Thermo King brands, kept the crown jewels and rebranded itself Trane Technologies plc (NYSE: TT).[^8] The unglamorous industrial segment — the compressors and blowers — was spun off and immediately merged with a private-equity-owned competitor called Gardner Denver in a tax-free maneuver called a Reverse Morris Trust.4 The combined company took the old, storied name, Ingersoll Rand Inc., and the legacy ticker, IR. In other words, the company trading today is barely six years old in its current form, even though the name on the building is more than a century old. Getting that gap right — between the heritage brand and the young, reconstructed business underneath it — is the first act of analysis on this stock.

Three threads run through everything that follows, and it is worth naming them up front so you can watch them develop. The first is the operating system its leaders call IRX — a home-grown descendant of the famous Danaher Business System, imported by a CEO who spent eleven years inside Danaher before he ever ran a company of his own. The second is a genuinely unusual cultural bet: broad-based employee ownership, the idea, championed by KKR's Pete Stavros and executed by CEO Vicente Reynal, that handing equity to the person torquing bolts on the factory floor is not charity but a cold-blooded operating lever. The third is the aftermarket annuity — the parts, service, and consumables that flow, year after year, from every machine already installed in a customer's plant, and that quietly account for something like 40% of revenue at margins the equipment itself could never earn.1

This is the place to puncture the central myth, because it colors how many investors approach the stock. The myth is that Ingersoll Rand is a stodgy, low-tech maker of noisy iron — a cyclical industrial whose fortunes rise and fall purely with the manufacturing economy, worth a modest multiple and little more. The reality is more interesting and more demanding: today's Ingersoll Rand is a young, financially engineered compounder that happens to manufacture unglamorous hardware, whose economics are driven far less by the sale of the iron than by the recurring aftermarket attached to it, the operating system layered on top, and the acquisition machine bolted to the side. The heritage name and the heavy-metal aesthetic are, in a sense, camouflage. The failure mode for an investor is to price the camouflage rather than the machine — either dismissing it as a cyclical or, at the other extreme, paying a compounder's premium for what might, on a bad day, revert to being a cyclical. Holding both possibilities in view at once is the discipline this story requires.

Our job here is not to sell any of that. Management tells a clean, confident story, and its investor relations machine is polished. The independent question is always the same: which parts are proven, and which are asserted? So the roadmap runs like this. First, the conglomerate era and why it ended. Then the KKR chapter and the ownership gospel. Then the financial engineering of the 2020 split. Then the economics of the compressor itself — why a factory treats it as a fourth utility. Then IRX and the roll-up machine that runs on it. And finally the stress test: the organic slowdown surfacing in the most recent numbers, the skeptic's case that this is a roll-up dressed as a compounder, and the bull-and-bear spine that will decide whether the last decade repeats. Let's begin where the name begins — with a rock drill.

II. Legacy of the 20th Century: Conglomerate Bloat

The origin story is almost comically literal. In 1871, a New York inventor named Simon Ingersoll patented a steam-powered rock drill — a machine for boring holes into stone faster than a man with a hammer could. It was the kind of invention the age demanded: America was tunneling through mountains for railroads, blasting canals, and digging mines faster than muscle could keep up. A few decades later, in 1905, Ingersoll's drill company merged with the Rand Drill Company to form Ingersoll-Rand, and for the better part of the next century the hyphenated name became a kind of shorthand for the physical infrastructure of industrial civilization. If something on Earth needed to be drilled, compressed, pumped, or tightened, there was a decent chance an Ingersoll-Rand machine was doing it.

That heritage matters less for the specific products than for the identity it created. Ingersoll-Rand grew up as a heavy-metal company — proud of its cyclicality, comfortable selling big iron to miners and builders, organized around the boom-and-bust rhythm of construction and commodity capital spending. Through the postwar decades it did what nearly every large American industrial did: it diversified. It bought its way into pneumatic tools, into golf and utility vehicles through the Club Car brand, into door hardware and security, into refrigerated transport. The logic of the era was that a well-run management team could allocate capital across unrelated businesses and smooth out the cycles — a little conglomerate discount was the price of stability.

The apex of that instinct came in the late 2000s, and it is the single most important event in the pre-history of today's company. In December 2007, Ingersoll-Rand agreed to acquire Trane Inc. — the air-conditioning giant formerly known as American Standard — for roughly $10 billion, closing the deal in June 2008.[^8] Overnight, a heavy-metal industrial became, more than anything else, a climate-control company. Trane and the Thermo King refrigerated-transport brand were high-quality, brand-rich, aftermarket-heavy businesses with the kind of steady demand — buildings always need cooling — that the cyclical compressor and tools operations could only envy. The timing, arriving on the doorstep of the global financial crisis, looked reckless for a year or two. But strategically it reoriented the entire company around HVAC.

And here is where the conglomerate curse set in. Once climate became the crown jewel, everything else in the portfolio became, in effect, a supporting act competing for capital and attention it increasingly did not get. The industrial compressor business — a perfectly good franchise with strong brands and a global installed base — was buried inside a company whose investors, analysts, and management bandwidth were all pointed at Trane. Capital that might have gone into new compressor products or bolt-on acquisitions instead flowed toward the higher-multiple climate story. The industrial segment was, in the language management would later use, starved. Its returns were dragged down by the structural overhead of a diversified giant, and its cyclicality — very real — was used as a reason to under-invest rather than a problem to be managed.

It is worth being precise about why this hurt, because "conglomerate discount" gets thrown around loosely. The mechanism is return on invested capital. A diversified industrial spreads a large corporate overhead — headquarters, shared services, a management team whose attention is finite — across businesses with very different economics, and it allocates capital by internal politics as much as by returns. The unit with the best growth story and the friendliest analysts tends to win the next dollar of investment, regardless of where that dollar would actually earn the most. Inside the old Ingersoll-Rand, the climate business had the better story, so it got the capital, the talent, and the airtime. The compressor franchise, meanwhile, generated respectable returns on the capital it had but was denied the capital it could have deployed — the textbook definition of a good business held back by a bad owner. Investors, unable to buy the compressor business on its own, applied a blended, discounted multiple to the whole, and everyone lost a little.

By the mid-2010s the market's verdict on conglomerates had hardened. Investors had stopped paying for diversification and started paying for focus; the era's winning template was the "pure-play" operator that did one thing and compounded it, ideally with a rules-based acquisition engine bolted on. Activist and shareholder pressure pushed sprawling industrials to break themselves apart and let each piece be valued on its own merits. Ingersoll-Rand had already been shedding parts — spinning security into Allegion in 2013, for instance — and the strategic logic pointed in one direction: separate the high-multiple climate business from the lower-multiple industrial one, and stop letting the two drag on each other. The realization that the compressor franchise was worth more free than trapped set the stage for everything that followed. But the compressor business could not simply be set loose on its own — it needed a partner, an operator, and a new culture. That partner was already being assembled, in private, by one of the most influential private-equity investors of his generation.

III. KKR, Peter Stavros, and the Gospel of Employee Ownership

To find the other half of the modern company, rewind to 2013 and cross town — figuratively — to Milwaukee, where a 155-year-old maker of industrial compressors, pumps, and blowers called Gardner Denver was about to change hands. The private-equity firm KKR agreed to take Gardner Denver private for roughly $3.9 billion, one of those unglamorous industrial buyouts that rarely make headlines.3 What made it consequential was not the price. It was the man who led the deal for KKR: Pete Stavros, head of the firm's industrials team, who had spent years nursing an idea that most of Wall Street regarded as sentimental at best.

Stavros's thesis was simple to state and radical to implement: give equity to everyone. Not just the executives, not just the salaried managers, but the hourly workers on the assembly line, the technicians in the field, the people in customer service. His conviction, formed partly by watching his own father work as a union construction worker, was that ownership changes behavior in ways no bonus scheme can. A worker who owns a slice of the company treats the machine, the scrap bin, and the safety protocol differently — not because a supervisor is watching, but because the outcome is partly theirs. In private-equity terms, Stavros was arguing that broad-based ownership was an untapped source of alpha: lower turnover, fewer accidents, less waste, faster throughput, all of it flowing to the bottom line and, eventually, to the exit multiple.[^11] The industry's reflex was skepticism. Equity is dilutive; why hand it to people who, the conventional wisdom held, don't move the needle?

KKR needed an operator who could turn the philosophy into performance, and in 2016 it hired one: Vicente Reynal, who took over as CEO of Gardner Denver. Reynal's pedigree is the key to the whole story. Before Gardner Denver he had spent roughly eleven years at Danaher, the conglomerate whose Danaher Business System (DBS) is the most-copied management operating system in modern industry — a relentless, almost religious discipline of continuous improvement, standardized processes, and daily metrics. Reynal had not just worked at Danaher; he had absorbed its operating religion. Pairing a Danaher-trained operator with a KKR ownership philosophy created the combination that would define Ingersoll Rand: DBS-style execution on top, worker equity underneath.

The philosophy became public — and unmistakable — in May 2017, when KKR returned Gardner Denver to the stock market. The IPO priced at $20 a share and raised about $826 million, a routine private-equity exit on its face.3 What was not routine was the announcement that accompanied it. Stavros and Reynal granted more than $100 million in stock to all of the company's roughly 6,100 employees worldwide, with each worker receiving grants equal to about 40% of their annual base salary.3 Hourly workers, customer-service reps, salespeople — people who had never owned a share of anything — suddenly held equity in the company they built. The video message announcing it reduced some employees to tears. For KKR it was, in part, a public-relations answer to private equity's reputation as an extractor of value; but Stavros insisted, and the operating data KKR would later publish was marshaled to argue, that it was also a business decision — the firm has pointed to reduced turnover, improved safety, and stronger engagement across its employee-owned industrial companies as evidence that the model pays for itself.[^10]

Stavros believed in the idea enough that he would eventually build an institution around it. A few years after the Gardner Denver grant he co-founded a nonprofit, Ownership Works, to push broad-based employee ownership across the private-equity industry and beyond — recruiting other buyout firms, pension funds, and corporations to adopt the model. That later crusade matters to the Ingersoll Rand story for a simple reason: it demonstrates that the ownership philosophy was not a one-off marketing gesture attached to a single IPO but a genuine conviction its architect was willing to stake his reputation on. Skeptics can fairly note that a nonprofit and a movement are also very good branding for a private-equity firm eager to soften its image. Both things can be true at once, and the investor's job is to separate the sincerity of the belief from the size of its financial payoff — which remain distinct questions.

Reynal himself is worth lingering on, because operating systems are ultimately carried by people. He is an engineer by training and temperament, and his years at Danaher were formative in a specific way: Danaher does not merely tolerate its business system, it indoctrinates managers into it, rotating them through problem-solving "kaizen" events until continuous improvement becomes reflexive rather than optional. Managers who emerge from that machine tend to share a vocabulary and a habit of mind — measure everything, standardize what works, attack waste relentlessly, and distrust any explanation that cannot be shown on a metrics board. What made Reynal unusual was pairing that clinical, process-obsessed formation with a genuine embrace of the softer ownership thesis, which many Danaher-bred operators would have dismissed as un-rigorous. The synthesis — cold process discipline plus warm ownership alignment — is the distinctive DNA he would carry from Gardner Denver into the far larger company that was about to bear his stamp.

The framework worth applying here is Hamilton Helmer's idea of a Cornered Resource — an asset a company controls that produces outsized value and that rivals cannot easily replicate. Culture is usually too soft to qualify. But the argument Reynal and Stavros make is concrete: when the person assembling a compressor owns stock, warranty claims fall because defects get caught, factory waste drops because scrap is money out of the worker's own pocket, and turnover declines because leaving means walking away from an appreciating asset. Whether those effects are as large and as durable as management claims is a genuinely open question — the data is largely company-supplied, and low turnover in a given period can have many causes. But the mechanism is real and, importantly, hard to copy, because a competitor can announce an equity grant in an afternoon and still spend a decade failing to build the culture that makes it mean something. That combination — a proven operator, a differentiated ownership model, and a public company to run it in — was about to be pointed at a much bigger target. The compressor business trapped inside the old Ingersoll-Rand conglomerate was coming free, and it needed exactly what Gardner Denver had.

IV. The Reverse Morris Trust Masterstroke

Some corporate transactions are merely large. A few are elegant, and the deal that created the modern Ingersoll Rand belongs in the second category. To appreciate it, you first have to understand the problem it solved. Ingersoll-Rand plc wanted to get rid of its industrial segment. Gardner Denver's owners wanted scale and a public platform. A conventional sale would have triggered an enormous tax bill — separating a business and selling it for cash is a taxable event, and the government's share of a multi-billion-dollar gain can wreck the economics of an otherwise sensible deal. The maneuver that avoids this is called a Reverse Morris Trust, and it is one of the more beautiful pieces of legal machinery in corporate finance.

Here is the trick, in plain terms. A parent company can spin off a division to its own shareholders tax-free, and it can merge that division with another company tax-free — provided the original parent's shareholders end up owning more than half of the combined entity. Cross that 50% threshold and the whole transaction escapes taxation as a reorganization rather than a sale. So instead of selling the industrial segment to Gardner Denver for cash, Ingersoll-Rand spun the segment off to its own shareholders and simultaneously merged it into Gardner Denver, structured so that legacy Ingersoll-Rand holders wound up with the majority of the combined company. No cash changed hands at the corporate level; no capital-gains tax was triggered. Value was moved, not sold.

The execution completed in the last days of February 2020 — with, in retrospect, exquisitely bad timing, closing just weeks before COVID-19 shut down the global economy.4 When the dust settled, the corporate map had been redrawn. The remaining climate-focused parent renamed itself Trane Technologies plc and repositioned as a pure-play in building efficiency and sustainable cooling.[^8] The industrial segment — compressors, blowers, vacuum, power tools — merged into Gardner Denver, and the combined company adopted the more storied name, becoming Ingersoll Rand Inc. and trading under the legacy ticker IR. One heritage name split into two focused public companies, each free to be valued on its own economics, and the industrial half was now run by the Gardner Denver team rather than buried beneath an HVAC giant.

Vicente Reynal took the helm of the newly merged Ingersoll Rand, and his very first move told you exactly which playbook he intended to run. Roughly 16,000 employees who had come over from the legacy Ingersoll-Rand industrial business had never participated in an equity plan. Reynal announced a one-time grant of about $150 million in restricted stock units to those employees — importing the Gardner Denver ownership gospel wholesale into the newly enlarged company.[^9] It was a deliberate act of cultural engineering. Post-merger integrations usually curdle into "us versus them" — the acquirer's people and the acquired people, each protecting turf. By making every one of the new employees an owner on day one, Reynal attempted to dissolve that line before it could harden, giving two legacy organizations a single, literal stake in the same outcome.

The timing turned the merger into an unintentional stress test. Closing a multi-billion-dollar combination in the final days of February 2020 meant that management spent its first weeks as a unified company not celebrating synergies but scrambling to protect employees and cash as factories idled and demand fell off a cliff. In hindsight, that baptism may have accelerated the integration rather than derailing it: a common crisis forces two workforces to pull together faster than any team-building exercise, and the cost discipline the downturn demanded was exactly the muscle IRX was built to flex. The company emerged from 2020 with its costs cut, its balance sheet intact, and a leaner structure that positioned it to ride the powerful industrial recovery of 2021 and 2022. It is a genuine data point in favor of the operating model — though a fair skeptic would note that surviving a demand shock and thriving because of a culture are different claims, and only the first is cleanly demonstrated by the record.

Whether that cultural glue actually held is a fair thing to interrogate, and the honest answer is that it is difficult to isolate from everything else that happened. The company integrated the two workforces during a pandemic, cut costs aggressively, and rode a strong post-COVID industrial recovery, so attributing the smooth combination specifically to broad-based ownership requires taking management partly at its word. What can be said is that the RMT gave Ingersoll Rand something rare: a clean balance sheet, a focused portfolio, a Danaher-trained operator, and a distinctive culture, all assembled in a single stroke of financial engineering. The structure was elegant; the real test was whether the underlying business could earn its keep. To judge that, you have to understand how a compressor actually makes money — and why customers, once locked in, almost never leave.

V. The Industrial Cash Engine: How Compressors Make Money

Ask a plant manager what happens if the electricity goes out, and they will tell you they call the utility. Ask what happens if the compressed air goes out, and their face changes. Compressed air is the invisible fourth utility of modern manufacturing, sitting alongside electricity, water, and gas — and unlike the others, the factory generates it itself, on-site, with a compressor. When that machine stops, the plant stops. Pneumatic tools go dead, robotic actuators freeze, packaging lines halt, and in a semiconductor fab or a sterile pharmaceutical suite the losses can run to thousands of dollars a minute. This is the single most important fact about the business: the compressor is not a convenience, it is a dependency. And dependencies are where durable economics come from.

Understanding that reframes the whole competitive picture. The industry's undisputed heavyweight is the Swedish giant Atlas Copco — larger, highly sophisticated, with vast global scale and a reputation for engineering excellence. Ingersoll Rand plays the aggressive American challenger, but its weapon is not a single dominant brand; it is a portfolio of strong regional and application-specific names — Gardner Denver, CompAir, Nash, Thomas, Roots, and others — that let it show up in dozens of niches under a label the local customer already trusts. Around the two leaders sit specialists like Germany's family-owned Kaeser, Japan-owned Sullair under Hitachi, and India's ELGi. It is a fragmented, application-specific market, and fragmentation, as we will see, is the raw material for a roll-up strategy.

The brand-portfolio approach deserves a moment of war-gaming, because it is a genuine strategic choice rather than an accident of history. Atlas Copco largely competes as Atlas Copco — one powerful global brand, one channel, one reputation. Ingersoll Rand runs the opposite play: it keeps the acquired names alive. A pulp mill that has trusted Nash liquid-ring vacuum pumps for forty years keeps buying Nash; a European manufacturer loyal to CompAir keeps buying CompAir; a wastewater plant standardized on Roots blowers keeps specifying Roots. Each brand carries its own installed base, its own switching costs, and its own aftermarket annuity, and by preserving rather than absorbing them, Ingersoll Rand collects dozens of small, defensible franchises under one corporate roof. The cost of that strategy is complexity — more product lines, more channels, more SKUs to manage — which is precisely the kind of complexity IRX is designed to tame. The benefit is that it turns the roll-up from a financial exercise into a genuine competitive structure: buy a trusted niche brand, keep the customers who trust it, and run the operation better than the family that sold it ever could. Whether that beats Atlas Copco's cleaner single-brand scale is the central duel of the industry, and it is not obvious either model dominates — they are two coherent answers to the same fragmented market.

But the equipment sale is not where the real money lives. Selling a new compressor is a competitive, price-sensitive fight; buyers get multiple quotes, and margins on the iron itself are ordinary. The equipment is better understood as the gateway — the razor that necessitates a lifetime of blades. Once a compressor is installed and wired into a customer's critical process, the economics invert. That machine needs filters, lubricants, and spare parts. It needs scheduled service to avoid unplanned downtime. It often runs under a service agreement in which Ingersoll Rand's technicians keep it healthy. And crucially, the customer has almost no incentive to switch brands, because ripping out a working, validated machine to save a few percent on the next one risks exactly the downtime that would cost far more than the savings.

There is a second, underappreciated hook in the machine itself, and it turns on energy. A compressor is, in effect, a device for converting electricity into pressurized air, and it is a thirsty one — over a typical machine's life, the electricity to run it dwarfs the purchase price, sometimes by a factor of five or more. That makes the compressor one of the largest single electricity consumers in many plants, which means efficiency is not a green talking point but a hard line on the customer's utility bill. Ingersoll Rand's salespeople have learned to sell on this: replace an old, inefficient machine with a modern variable-speed one, and the energy savings can pay back the entire purchase in a year or two. On the Q1 2026 call, Reynal described a customer saving roughly $15,000 a month at a single location, with a payback measured in about a year, and framed rising European energy prices as a potential long-term tailwind precisely because expensive power makes efficient compressors an easier sell.1 It is a reminder that even in a commodity, there is room to compete on total cost of ownership rather than sticker price — a theme management returns to whenever analysts worry about pricing.

This is the aftermarket annuity, and it is the beating heart of the investment case. On the Q1 2026 earnings call, management pegged aftermarket at roughly 40% of enterprise revenue — recurring parts, consumables, and service that arrive year after year largely independent of whether customers are buying new equipment.1 That stream carries structurally higher margins than the original equipment, and it behaves defensively: even when factories stop buying new compressors in a downturn, the compressors they already own still need parts and service. The installed base, in other words, is a shock absorber. It is why a company selling into cyclical manufacturing can throw off remarkably steady cash. Management has been explicit that it is trying to grow this deliberately — building recurring-revenue offerings that exceeded roughly $450 million and targeting a $1 billion run-rate by the end of 2027, a goal it repeated on the most recent call.1

A brief word on what these machines actually do, because the PST side in particular can sound like alphabet soup. A progressive-cavity pump — the technology Ingersoll Rand deepened with Seepex — works like a corkscrew turning inside a rubber sleeve, carrying fluid forward in sealed pockets; that gentle, pulse-free action is what lets it move things ordinary pumps mangle, from toothpaste to sewage sludge to shear-sensitive biological fluids. A liquid-ring vacuum pump — the Nash specialty — spins a ring of liquid to trap and compress gas, prized in paper mills and chemical plants because it shrugs off wet, dirty, corrosive vapors that would destroy a dry pump. A dosing pump meters a precise squirt of chemical — a disinfectant into drinking water, an additive into a drug batch — to tolerances where a small error means a ruined product or a safety incident. The common thread is criticality: in each case the pump is small relative to the process it serves, but the process cannot run correctly without it, and the cost of failure dwarfs the cost of the pump. That is why these niches carry higher margins than compressors, and why they behave defensively — the customer's incentive is reliability, not thrift.

The analytical takeaway is that the moat here is not the machine; it is the position. The switching cost is created by the customer's own fear of downtime and, in regulated industries, by validation requirements that make swapping a qualified piece of equipment a bureaucratic ordeal. That is a genuine competitive advantage, and it is why the aftermarket earns what it earns. The limitation worth holding in mind is that the moat protects the installed base, not necessarily new placements — to keep the annuity growing, Ingersoll Rand has to keep winning new equipment slots against Atlas Copco and the rest, and that front-end battle is as competitive as ever. The company's answer to sharpening both ends of that fight — winning more placements and squeezing more cash from each one — is a management system it treats almost as a proprietary technology in its own right.

VI. Evolving the Playbook: The "IRX" Operating System

Every great industrial compounder has a religion, and its scripture is an operating system. For Danaher it is DBS; for Roper it is a decentralized capital-allocation discipline; for Ingersoll Rand it is a home-grown framework called IRX — Ingersoll Rand Execution Excellence. On virtually every earnings call, Reynal returns to it like a refrain. On the Q1 2026 call he called IRX "the backbone of the organization," the thing that lets the company "stay focused on what we can control."1 Strip away the corporate branding and IRX is what a Danaher alumnus builds when he is handed a company of his own: a centralized, repeatable machine for making high-mix, low-volume industrial manufacturing run faster, cleaner, and more profitably, and — critically — for absorbing acquired companies into that discipline quickly.

The mechanics are deliberately concrete, because vague operating systems are just slogans. When Ingersoll Rand buys a business, it runs it through structured 100-day sprints — intense, time-boxed pushes to align the new operation on a handful of the highest-value improvements before old habits reassert themselves. Day-to-day, the company runs on daily and weekly management standups (its version of what many industrials call daily management), where teams track scrap rates, on-time delivery, safety, and cash conversion on visible metrics boards, surfacing problems in hours rather than quarters. On the commercial side, it layers what it calls demand-generation tools — a systematized approach to finding and converting new sales opportunities rather than waiting for orders to arrive. The point of all of it is to make performance a process rather than an act of heroism, so that results survive the departure of any individual manager.

The manufacturing context is worth understanding, because it explains why the system has to be so disciplined. Ingersoll Rand does not run a few giant plants stamping out millions of identical widgets, where automation and volume do the work. It runs high-mix, low-volume production: a given factory might build hundreds of configurations of compressor, blower, or pump, many of them semi-customized to a specific customer's plant, in small batches. That is the hardest kind of manufacturing to make efficient, because you cannot simply buy a faster machine and amortize it over a huge run. The gains have to come from process — from cutting the time a job waits between steps, from reducing the defects that force rework, from getting parts to the line exactly when needed. That is exactly the terrain a Danaher-style system is built for, which is why importing it, rather than inventing something new, made sense. IRX is less a novel invention than a faithful, well-executed adaptation of a proven method to a portfolio of businesses that badly needed one.

Does it work? The honest evaluation is that the evidence is suggestive rather than airtight, but it is not nothing. The clearest proof point is margin. Ingersoll Rand has repeatedly bought businesses at industrial multiples and expanded their margins meaningfully within a year or two, which is the observable signature of a genuine operating system as opposed to financial engineering. The counter-consideration is that a rising post-COVID industrial cycle and aggressive pricing also flattered margins during the same years, so IRX cannot claim sole credit. The most useful way to think about it: IRX is real and it is a competitive advantage in Helmer's Process Power sense — an embedded, hard-to-copy way of operating — but its value is easiest to see specifically at the moment of acquisition, which is exactly why the company has organized itself around buying things.

That advantage shows up in the shape of the portfolio, which the company reports in two segments of very different character. The larger by far is Industrial Technologies & Services (ITS) — the compressors, vacuum pumps, blowers, and power-and-lifting systems that are the historical core. In fiscal 2024 ITS generated on the order of $5.8 billion in revenue, roughly 80% of the company, and it is the engine that produces the bulk of the cash.5 Within ITS, compressors alone are about 65% of the segment's revenue, with blowers and vacuum making up much of the rest.1 This is the cyclical, cash-generative heavy-metal base of the business — steady, defensive through the aftermarket, but tied to the rhythm of global manufacturing.

The smaller, faster, higher-margin segment is Precision & Science Technologies (PST) — roughly $1.4 billion in 2024, about 20% of revenue.5 PST makes highly precise fluid-handling equipment: dosing pumps, liquid-transfer systems, progressive-cavity pumps, and niche environmental and life-science gear under brands like Milton Roy and Seepex. These products meter chemicals and fluids to exacting tolerances in applications — biopharma, water treatment, chemical processing — where getting the dose slightly wrong is catastrophic, which is precisely why they command structurally higher margins. Management has, over the past few years, begun describing PST in two pieces, a "Precision Technologies" side and a fast-growing "Life Science Technologies" platform, the latter built around a large 2024 acquisition we are about to examine.1 PST is the part of the company that looks least like a compressor maker and most like a life-sciences tools business — and that resemblance is the whole strategic point. The question is how Ingersoll Rand keeps feeding both segments, and the answer is a capital-allocation machine that runs almost without pause.

VII. The Roll-Up Machine & Capital Allocation

Here is the flywheel, in Reynal's own framing: the business throws off durable free cash flow; that cash is redeployed into acquisitions; the acquisitions are run through IRX to lift their margins and cash generation; and the enlarged cash flow funds the next round of deals.1 It is self-funding growth, and it is the mechanism that turns a mediocre commodity into a compounder. The scale of the ambition is easy to underappreciate until you hear the numbers management uses to describe its pipeline. On the Q1 2026 call, the company said it had more than 200 companies in its acquisition funnel, with ten transactions at the letter-of-intent stage, and — the detail that reveals how the machine actually works — more than 90% of those opportunities were internally sourced rather than shopped by bankers.1 Internally sourced deals mean less competition and lower prices, which is the difference between a disciplined acquirer and a serial overpayer.

It is worth making the value-creation arithmetic concrete, because it is the crux of the whole enterprise. Imagine a family-owned pump maker earning $10 million of EBITDA, bought at 9x for $90 million. It runs at, say, a 15% margin because it has never had a real procurement function, its factory flow is chaotic, and it under-prices its aftermarket parts. Run it through IRX for eighteen to twenty-four months — consolidate purchasing into Ingersoll Rand's scale, tighten the plant, professionalize pricing, and push the service attach-rate — and lift that margin by three to five points. Suddenly the same revenue throws off materially more EBITDA, and the effective purchase multiple on the new earnings has quietly compressed from 9x toward 6-7x, before a single dollar of growth. Layer on cross-selling the acquired product through Ingersoll Rand's global channel, and the returns compound further. That is the engine, and when it works it is genuinely powerful. The risk it hides is that it depends on a steady supply of under-managed targets at reasonable prices; the day those run scarce, the arithmetic that makes the flywheel spin starts to grind.

The template is specific. Ingersoll Rand hunts small, often family-owned regional industrial businesses — the kind that trade at single-digit EBITDA multiples precisely because they are subscale and lack a professional operating system. It buys them, typically in the range of 8 to 10 times EBITDA, and then runs them through the integration pipeline, aiming to expand margins by several hundred basis points within the first year or two. The math is elegant: buy at 8-10x, improve the economics, and the effective purchase multiple on the improved earnings drops meaningfully, creating value even before any growth. The company reaffirmed on the most recent call that it expects to add roughly 400 to 500 basis points of annualized inorganic revenue in 2026, a steady mechanical contribution to the top line year after year.1

It is important to see that M&A is the first priority in the capital-allocation stack, not the only one. Management describes an order of operations that starts with reinvesting in the business, then acquisitions as the primary use of surplus cash, with share repurchases and a quarterly dividend rounding out the rest — a framework it reaffirmed as "unchanged" on the Q1 2026 call.1 The logic is coherent: if you genuinely can buy businesses at 8-10x and improve them, that is a better use of a dollar than buying back your own stock at a much higher multiple, so acquisitions should come first as long as the pipeline is full and the returns hold. Buybacks then serve as a pressure-release valve for cash the deal funnel cannot absorb, and the dividend signals discipline without consuming much of the firepower. The signing of a small Italian maker of hydropneumatic accumulators and dampeners, Fox s.r.l., announced alongside the Q1 2026 results, is a perfect miniature of the everyday machine at work — an on-strategy tuck-in that enhances the pump portfolio, the kind of deal that individually moves nothing but collectively compounds.1

The bolt-ons rarely make headlines individually, but a few larger moves map the strategy's evolution. In 2021, Ingersoll Rand acquired the German maker Seepex for about €431.5 million, deepening its progressive-cavity-pump capability inside PST — pumps that move thick, abrasive, or shear-sensitive fluids that ordinary pumps cannot handle.[^5] In 2023 it acquired the Howden Roots blower and compressor business for roughly $300 million, consolidating its position in industrial blowers and vacuum.[^4] These were classic, on-strategy consolidations — expanding franchises the company already understood, at prices that fit the disciplined template.

Then came the deal that tested whether the discipline was real. In March 2024, Ingersoll Rand agreed to acquire ILC Dover — a specialist in single-use solutions for biopharma, including powder and liquid containment systems and bioprocess components — for an upfront cash price of about $2.325 billion, plus an earnout.2 This was not a bolt-on; it was a step-out, a deliberate move deeper into life sciences and a new center of gravity for the Life Science Technologies platform. And the price was the point of controversy. ILC Dover was struck at roughly 17 times its 2024 estimated adjusted EBITDA — nearly double the 8-to-10x the company pays for ordinary industrial tuck-ins.2 For a management team that had built its credibility on valuation discipline, paying a life-sciences multiple was a genuine departure that demanded a justification.

The defense management offered was that ILC Dover is not an industrial business wearing a lab coat but a genuinely different animal: mid-30s percent EBITDA margins, a mid-teens historical organic growth rate, and roughly 75% of revenue coming from consumable, recurring, single-use products bought again and again by the world's largest biopharma companies.2 By that logic, the relevant comparison is not other compressors but pure-play life-science tools peers — the Danahers, Sartoriuses, and Repligens of the world — which have historically traded at 20x to 30x EBITDA or more. Against that benchmark, 17x for a recession-resistant, consumables-heavy franchise reads less like overpaying and more like buying a coveted asset class at an industrial discount. That is a coherent argument. The unresolved risk, which we will press on shortly, is whether an operator bred on heavy metal can actually run an FDA-regulated consumables business as well as the specialists — and whether the recurring-revenue and growth assumptions that justify 17x hold up once the cycle turns.

It is worth sitting with the ILC Dover valuation a beat longer, because it is the single clearest test of whether "disciplined acquirer" is a description or a slogan. Pay 17x for anything and you are, by definition, no longer buying at the 8-10x that made the roll-up math so forgiving. The premium only creates value in two ways. Either the acquired business grows fast enough and long enough that the entry multiple shrinks into the rear-view mirror — plausible if ILC Dover really does compound in the mid-teens with recession-resistant consumables — or the market chooses to value those earnings inside Ingersoll Rand at a higher multiple than the 17x paid, effectively re-rating industrial cash into life-sciences cash. That second path is the seductive one: if investors come to see a growing slice of Ingersoll Rand as a biopharma-consumables business deserving the 20-30x its pure-play peers command, the arbitrage between what IR paid and what the market will capitalize is enormous. But that re-rating is a hope, not a fact, and it depends on management proving it can run the asset as well as the specialists — the very thing it has not yet demonstrated over a full cycle. The tell to watch is whether Ingersoll Rand ever starts breaking out Life Science Technologies as its own reported segment; doing so would invite exactly the peer comparison the bull case needs, and management's continued reluctance to disaggregate it, noted on the most recent call, cuts modestly against the most optimistic read.1

There is also a scale question lurking. Reynal let slip on the Q1 2026 call that beyond the ten deals at letter-of-intent, the funnel contained at least one transaction of "a little bit more than $1 billion" — smaller than ILC Dover but far larger than a tuck-in.1 That is the roll-up's central tension made concrete: to keep moving the needle on a company approaching $8 billion in revenue, the deals have to get bigger, and bigger deals are pricier, harder to integrate, and less forgiving of error. The disciplined-acquirer thesis works beautifully at $50 million a deal; it is a different and more dangerous game at $1-2 billion a deal, where a single misjudgment can dent the whole company. Investors who love the flywheel should be clear-eyed that its next revolutions carry more weight than its last.

On management's own skin in the game, the alignment is real and above the industry norm. Reynal operates under a stock-ownership requirement of 10 times his base salary — a stringent bar even among large-cap CEOs — and beneficially owns well over a million shares when trusts and exercisable options are counted, so his personal wealth rises and falls with the stock rather than merely with his salary. Combined with the broad-based grants pushed down to the factory floor, the ownership philosophy is at least internally consistent from the CEO to the line worker. Consistency, however, is not the same as being right, and the most recent quarter handed the skeptics some ammunition. To evaluate the story fairly, you have to look hard at where the growth is actually coming from — and where it is not.

VIII. The Stress Test: Risk Radar & The Skeptic's Case

Every compelling growth story eventually meets a quarter that tests it, and for Ingersoll Rand the Q1 2026 results, reported at the end of April 2026, were that quarter — not a disaster, but a set of numbers that forced management to defend the machine.[^1] On the surface the headline looked healthy: total revenue grew about 8% year over year, adjusted earnings per share rose roughly 7% to $0.77, and adjusted EBITDA came in around $469 million.1 Dig one layer down, though, and the picture complicated. That 8% growth was substantially inorganic — propped up by acquisitions like ILC Dover — while the underlying organic business was soft, and the softness was concentrated in the historical core.

The pressure point was ITS. The flagship industrial segment saw organic revenue decline about 2% year over year, and its adjusted EBITDA margin contracted by roughly 210 basis points to 26.7%.[^1]1 Management attributed the margin squeeze to three things: the natural deleverage of running lower volumes through a high-fixed-cost manufacturing base, the dilutive effect of tariffs (where the company raised prices to offset tariff costs dollar-for-dollar, which recovers the cost but mathematically compresses the margin percentage), and continued spending on commercial initiatives to drive future growth. On the call, CFO Vik Kini acknowledged that ITS margins had now been down year over year for five straight quarters — an unusually candid admission for a company that prefers to talk about long-term expansion.1

This is where the analytical discipline matters, because the same facts support two very different stories, and the earnings call became a live contest between them. Analysts pushed hard. Barclays' Julian Mitchell pressed on the five-quarter margin decline and asked what gave management confidence in a second-half recovery. UBS's Amit Mehrotra asked the sharpest question of the day: with so much price taken over recent years and short-cycle activity supposedly improving, why wasn't that momentum "piercing its way through" to organic growth — was there a demand-elasticity problem, where customers balked at higher prices?1 Reynal's answer leaned on the argument that Ingersoll Rand sells on total cost of ownership and payback rather than sticker price, and that the short-cycle order book was in fact improving beneath the surface. Management framed the ITS weakness as largely transitory — a mix of a roughly $40 million slug of Middle East project orders delayed by regional conflict (about a third of which it said had already been recovered in April), tariff noise that would lap and normalize, and customers taking longer to finalize long-cycle decisions without actually canceling projects.1

A few exchanges on that call are worth surfacing because they reveal how management thinks under pressure, and whether its answers are concrete or evasive. When Stifel's Nathan Jones drew the parallel to 2022 — the last time a European energy shock sent customers rushing to buy efficient compressors — Reynal was careful rather than promotional, conceding that gas prices were "not at the same level as what it was back then" and that the tailwind would "take a little bit of time," while insisting the demand-generation tools were already being pointed at the opportunity.1 On China, where many industrials were bleeding, Reynal claimed Ingersoll Rand had posted positive organic order growth for roughly three straight quarters by taking share with localized technology, while candidly acknowledging he did not expect the underlying Chinese market itself to grow.1 And on Life Sciences — the segment that has to justify the ILC Dover price — management pointed to double-digit organic order growth and a visibly improving funnel tied to U.S. biopharma reshoring and domestic active-ingredient production.1 These are specific, falsifiable claims rather than hand-waving, which is a point in management's favor on the credibility ledger; the answers can be checked against future quarters.

That explanation may well prove correct — book-to-bill above 1.0x and improving short-cycle orders lend it some support. But an independent reader should notice the shape of the bear case forming underneath it, and it has three prongs. The first is the roll-up trap: if the organic core is flat-to-declining and total growth is being carried by acquisitions, is Ingersoll Rand a secular compounder or an acquisition treadmill that must keep buying — and keep buying bigger, as the ILC Dover step-out suggests — to sustain the appearance of growth? A roll-up can create enormous value right up until the moment cheap targets run out or integration stumbles, and the market re-rates hard when it decides a "compounder" is really a "serial acquirer." The second prong is integration and complexity risk: a team trained on compressors is now selling FDA-regulated, single-use biopharma consumables, a world with different customers, longer qualification cycles, and different competitors; management insists ILC Dover is executing well and that Life Science orders grew double digits, but by its own admission it will not break out the asset's specific performance, so investors are asked to take the integration on faith.1

The third prong is valuation. Ingersoll Rand trades at a premium to traditional industrial peers — the kind of forward earnings and EV/EBITDA multiple that only makes sense if the compounding continues. Premium multiples are an asset when growth is delivering and a liability when it stalls, because they price in success and punish disappointment asymmetrically. If organic growth stays negative, or if the M&A engine sputters — cheap targets dry up, an integration disappoints, or a large deal like the "little bit more than $1 billion" transaction Reynal hinted was in the funnel goes wrong — the multiple has a long way to fall.1 None of this means the bear case is right; management has a credible, specific plan for the second-half margin recovery (pricing actions fully implemented, restructuring benefits landing, productivity in the seasonally strong fourth quarter), and it has generally delivered against its guidance in prior years, which counts for something on the credibility ledger.1 But the honest framing is that the Q1 2026 print moved the story from "proven" toward "prove it again," and the burden is now on management to show that the core can grow without a bolt-on doing the heavy lifting. With the risks named, it is worth stepping back to weigh the durable advantages against them.

IX. Playbook: The 7 Powers & Core Investing Lessons

Strip the story down to its load-bearing walls and Ingersoll Rand's competitive position rests on a handful of Hamilton Helmer's 7 Powers, some of them sturdier than others. The most distinctive — and the one management would put first — is the Cornered Resource of culture: the broad-based employee-ownership model that turns line workers and field technicians into equity holders. The theory is that owners work more safely, waste less, and stay longer, and that this is nearly impossible for a competitor to replicate, because the grant is easy to copy but the decade of cultural reinforcement behind it is not. Treat this one as plausible but not fully proven — the mechanism is sound and genuinely differentiated, but the hard evidence linking it to superior financial outcomes is largely company-supplied, and a skeptic is entitled to ask for independent proof.

The sturdiest power is Switching Costs, examined earlier through the aftermarket: once a compressor or a dosing pump is embedded in a mission-critical, sometimes regulated process, the cost of switching — downtime risk, re-validation, re-qualification — is prohibitively high, which is what lets the aftermarket earn its outsized margins. Sitting alongside it is Scale Economies in a specific, physical form: a dense, localized network of service technicians. A factory that loses air needs someone on-site within hours, not days, and only a competitor with comparable geographic density can promise that. That service footprint is a real barrier to the small regional players Ingersoll Rand spends its time acquiring, though against a peer of Atlas Copco's scale it is a source of parity rather than dominance. And finally there is Process Power in IRX — the repeatable, documented operating system that is most valuable at the moment of acquisition.

One more power belongs on the list, quieter than the others: Branding, in the narrow, Helmer-specific sense of a name that lets a seller charge more because buyers attach durable, affective trust to it. In consumer goods that means luxury logos; in industrial equipment it means a mill manager who will pay a premium for the Nash or Gardner Denver name because thirty years of uptime have taught him it will not fail at 3 a.m. That trust is not transferable — a low-cost rival cannot manufacture forty years of reliability reputation — and it is one reason the portfolio-of-brands strategy holds together commercially rather than just financially. It is a modest power, easily overstated, and it does nothing against a customer buying purely on price. But in the aftermarket, where the buyer's real fear is downtime rather than cost, it quietly reinforces the switching-cost moat that does the heavy lifting.

Run the same picture through Porter's Five Forces and the industry looks structurally attractive but not impregnable. Rivalry is real and rational: Atlas Copco is a formidable, disciplined leader, and the two behave more like an oligopoly that competes on technology and service than a knife-fight on price — though at the low end, and increasingly in China, price competition is fierce. The threat of new entrants is low; building a global compressor franchise with a service network and a trusted brand portfolio takes decades and enormous capital. Buyer power is diffused across thousands of industrial customers, none of them large enough to dictate terms, and the fear of downtime blunts their leverage on the aftermarket. Supplier power is moderate, though with direct materials at roughly 70% of cost of goods sold, input-cost and tariff swings clearly matter, as the 2026 margin squeeze demonstrated.1 The threat of substitutes is limited — there is no replacing compressed air in most of its uses — which is exactly what makes the fourth-utility framing more than a marketing line.

Two investing lessons generalize beyond this one company. The first is that business culture can be a cold-blooded financial instrument, not just an HR slogan — if the ownership thesis is even partly right, Ingersoll Rand is proof that aligning incentives all the way down to the factory floor can show up in warranty rates, safety, and turnover, and therefore in cash flow. The lesson for investors is to take culture seriously as a potential source of durable advantage while demanding evidence rather than accepting it on faith. The second is the power of focus over sprawl: the 2020 split that freed the compressor business from the shadow of HVAC, and simultaneously created a pure-play climate champion in Trane Technologies, unlocked value in both directions. Conglomerate discounts are real, and the pure-play template — a focused operator with a disciplined acquisition engine — has been one of the most reliable value-creation formulas of the modern era. The open question, always, is whether the acquisition engine can keep running when the cheap fuel gets scarce.

X. Epilogue & Key KPIs to Track

So where does this leave the modern Ingersoll Rand — the six-year-old company wearing a century-old name? At an inflection worth watching honestly. Management's ambition is unmistakable: to evolve from a cyclical maker of industrial air compressors into a diversified flow-control and life-sciences platform, using the aftermarket annuity for defense, IRX for execution, and a relentless bolt-on machine for growth. The ILC Dover step-out is the clearest signal of that ambition, and also its clearest risk — the moment the company stopped buying more of what it knew and started paying up for a new kind of business it will have to prove it can run. The bull case is that the flywheel keeps turning, the core stabilizes, and the life-sciences pivot re-rates the whole company toward its higher-multiple peers. The bear case is that organic growth is quietly stalling, the roll-up must keep getting bigger and pricier to mask it, and a premium multiple leaves no room for the machine to skip a beat.

The next act genuinely hangs on whether Ingersoll Rand can grow the organic business, not just the acquired one — whether it remains fundamentally bound to the cyclicality of global manufacturing PMI, or whether the aftermarket, the recurring-revenue push, and the life-sciences platform can lift it above the cycle. Nothing in the most recent numbers settles that question; they merely sharpen it. For readers following the story from here, three metrics will reveal, quarter by quarter, which case is winning.

The first is organic revenue growth, especially in ITS. This is the cleanest test of whether the core franchise is a secular grower or a cyclical one dressed up by M&A. The Q1 2026 organic decline of roughly 2% in ITS is the number to watch: if it inflects back to positive through 2026 as management insists it will, the "transitory" explanation holds; if it lingers, the roll-up-treadmill worry gains weight.[^1]1 The second is the adjusted EBITDA margin split between ITS and PST. Watch whether ITS can recover the roughly 210 basis points it shed — management has staked its credibility on a second-half rebound driven by pricing, restructuring, and productivity — and whether PST can sustain margins in the 30s as it digests ILC Dover.[^1]1 The margin line is where the operating system, IRX, either proves itself or does not.

The third is free-cash-flow conversion and leverage. The entire flywheel depends on the business converting earnings into cash — management guides to roughly 95% conversion — and on keeping the balance sheet, currently levered below 2x with nearly $4 billion of liquidity, healthy enough to keep feeding the acquisition machine after large cash outlays like ILC Dover.1 If conversion holds and leverage stays low, the roll-up has fuel; if either deteriorates, the growth engine loses its self-funding character and the story changes. Track those three — organic growth, the segment margins, and cash conversion — and you will know, well before the headline EPS does, whether the heavy-metal compounding machine is still compounding.

References

-

Ingersoll Rand (IR) Q1 2026 Earnings Call Transcript — The Motley Fool, 2026-04-29 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Ingersoll Rand to Acquire ILC Dover to Expand Presence in Life Sciences — Ingersoll Rand (irco.com), 2024-03-25 ↩↩↩

-

KKR-Backed Gardner Denver Gives Over $100 Million In Stock Grants To Employees In Market Return — Forbes, 2017-05-12 ↩↩↩

-

Reverse Morris Trust Merger of Gardner Denver and Ingersoll Rand Industrial Closed — Baird, 2020-03-01 ↩↩

-

Ingersoll Rand Inc. SEC Filings (10-K, 10-Q, Proxy) — SEC EDGAR ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube