IQVIA: The Data-Driven Revolution in Life Sciences

I. Introduction & Episode Roadmap

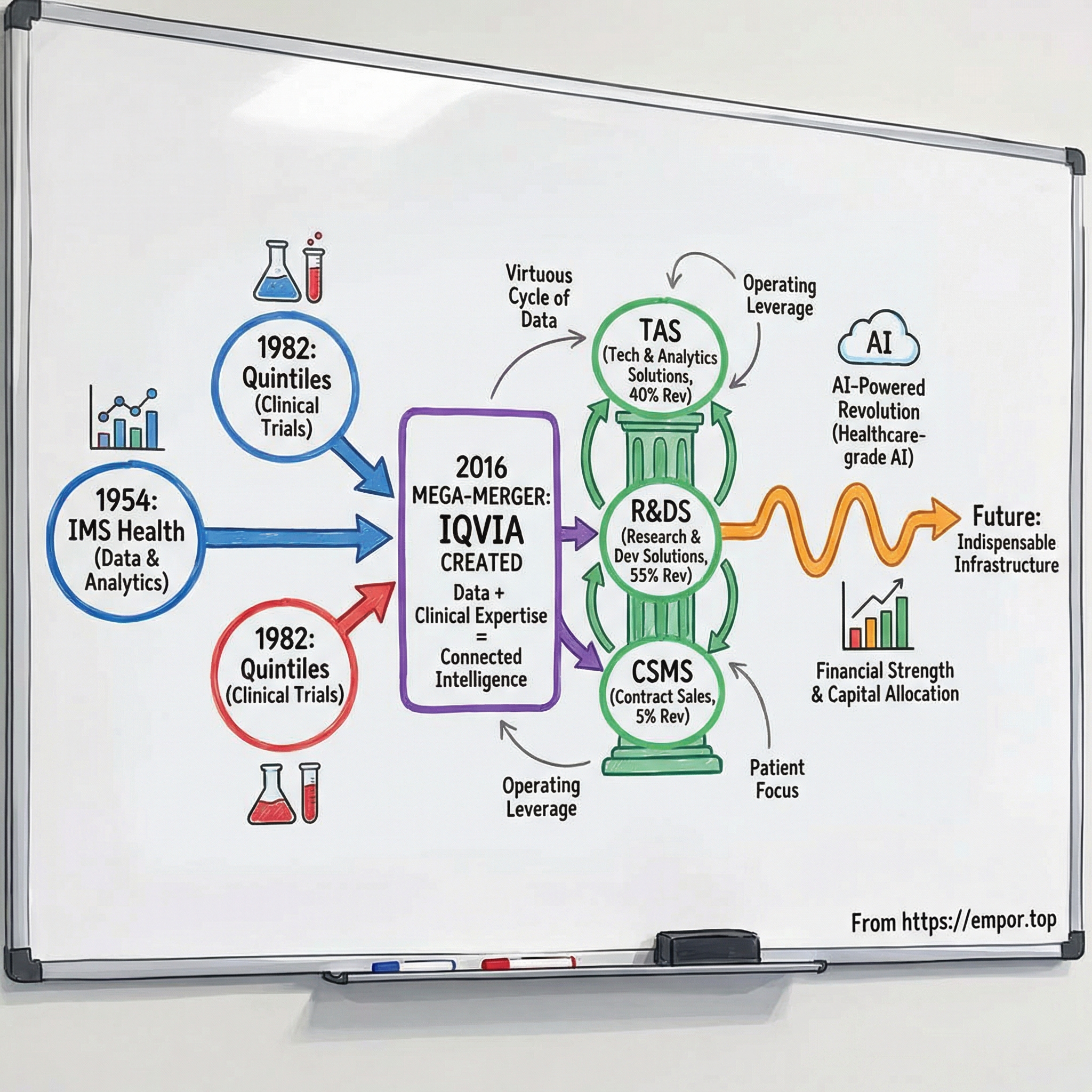

Picture this scene: It's 2016 in a Durham, North Carolina boardroom. Two CEOs are shaking hands on what will become one of healthcare's most transformative mergers. Tom Pike of Quintiles and Ari Bousbib of IMS Health have just agreed to combine their companies—one built on the messy, human work of clinical trials, the other on the pristine world of pharmaceutical data. Neither man could have predicted that within eight years, their merged entity would become a $15.4 billion revenue juggernaut, processing data on 1.2 billion patients while managing 9,000 active clinical trials across the globe.

This is the story of IQVIA—a company that most people have never heard of, yet touches nearly every prescription filled, every drug approved, and increasingly, every AI model trained on healthcare data. It's the ultimate picks-and-shovels play in the pharmaceutical gold rush, providing the essential infrastructure that powers modern drug development.

The narrative arc we're about to explore reads like a business school case study in strategic patience. How did a biostatistics professor's side hustle in 1982 and a data collection startup from 1954 converge to create what is arguably the most important company in healthcare that operates entirely behind the scenes? The answer involves parallel journeys of two companies that spent decades building complementary moats before recognizing they were stronger together.

IQVIA today stands as a three-legged stool: Technology & Analytics Solutions driving 40% of revenues through health information technology and that massive patient database; Research & Development Solutions contributing 55% through comprehensive clinical trial management; and Contract Sales & Medical Solutions adding the remaining 5% through targeted healthcare provider engagement. Each leg reinforces the others in ways competitors simply cannot replicate.

What makes this story particularly compelling for students of business strategy is how IQVIA has positioned itself as the indispensable middleman in an industry notorious for its inefficiencies. While pharmaceutical companies pour billions into R&D with notoriously low success rates, IQVIA profits regardless of which drugs succeed or fail. It's the house that always wins—except in this casino, the stakes are human lives and the chips are data points.

We'll trace this journey from those parallel founding stories through the mega-merger, examine how the company navigated COVID-19's disruption of clinical trials, and look ahead to an AI-powered future where IQVIA's data advantage might become insurmountable. Along the way, we'll unpack the business model that generates over $3.6 billion in adjusted EBITDA, explore why competitors struggle to replicate their success, and examine whether this healthcare data empire faces any real threats to its dominance.

The roadmap ahead takes us from post-war America's pharmaceutical boom through today's AI revolution, with stops at pivotal moments of strategic brilliance, operational excellence, and occasionally, regulatory controversy. It's a story about how information became as valuable as the medicines themselves, and how two companies recognized this truth before anyone else. As we dive into these parallel origins, remember: in healthcare, whoever controls the data controls the future.

II. Parallel Origins: IMS Health & The Data Revolution (1954-1990s)

The year was 1954, and post-war America was in the midst of a pharmaceutical revolution. Antibiotics had transformed medicine, psychotropics were emerging from laboratories, and drug companies were flush with cash but flying blind—they had no reliable way to track which drugs doctors were prescribing or how their sales compared to competitors. Into this information vacuum stepped three men whose partnership would remain hidden for decades: Bill Frohlich and David Dubow, with Arthur Sackler having a hidden ownership stake.

L.W. Frohlich, who had established his advertising agency in 1941, was dissatisfied with the limited market data about the new "wonder drugs." By forming IMS with David Dubow, they created the first market research syndicate for the pharmaceutical industry, providing information at a level of depth and objectivity not available at the time. The company's original name, Intercontinental Marketing Statistics, betrayed its global ambitions from day one.

What made IMS revolutionary wasn't just the data collection—it was the audacity of the business model. With Dubow as president, IMS began its pharmaceutical research in Europe. The company's first syndicated study, published in 1957, included a sales audit of the West German pharmaceutical market. The drug audit involved tracking sales invoices and monitoring inventory at select drugstores, at chain and discount stores, as well as at drug wholesalers and physicians' offices. Pharmacies were actually paid to share their prescription data, a practice that would later spark fierce privacy debates but at the time seemed like harmless market research.

The hidden hand behind IMS belonged to Arthur Sackler, whose involvement would only come to light after his death in 1987. When Arthur Sackler appeared under oath before the Kefauver Commission in January, 1962, he lied through his teeth, denying his ownership of IMS. This deception wasn't merely about avoiding scrutiny—Sackler understood that controlling data was the key to controlling the pharmaceutical market. This capability derived from Sackler's original hidden ownership stake in IMS – the data company that for decades had purchased the Physician Masterfile database from the AMA in order to package and sell physician prescription profiling data to eager pharmaceutical clients.

By 1969, company revenues reached $5 million and IMS was the leader in pharmaceutical market research in Europe and Asia. The company's expansion strategy was methodical and acquisitive. IMS began operations in North America through the acquisition of Davee, Koehnlein and Keating, a Chicago-based syndicate that conducted sales audits for markets in the United States and Canada. Each acquisition brought new capabilities: IMS acquired Lea Associates, known for developing the first National Disease and Therapeutic Index. Through the acquisition of Armbruster, Moore and MacKerell, IMS gained the Hospital Supply Index and Laboratory Diagnostic Audits. IMS obtained important products with the acquisition of Pharmatech, which developed the precursor to online delivery systems.

The 1970s marked a critical evolution as IMS went public in 1972 and began diversifying beyond pure data collection. In 1973 IMS established the Medical Communications division and the Life Sciences division to complement its market research activities. Medical Communications published informational materials, such as professional and trade journals, directories, and audiovisual training products. This wasn't just business expansion—it was the creation of an ecosystem where IMS could both collect data and influence the medical professionals generating that data.

The company introduced what would become its crown jewel in 1979: the Multinational Integrated Data Analysis (MIDAS) system. This platform allowed pharmaceutical companies to track drug sales across multiple countries in real-time, transforming how they allocated resources and made strategic decisions. For the first time, a Pfizer executive in New York could know exactly how their latest antibiotic was performing in Germany versus Japan, adjusting marketing spend accordingly.

Then came the corporate shuffle that would define IMS's next chapter. In 1988, Dun & Bradstreet (D&B) acquired IMS for $1.77 billion, seeing the value in healthcare information services. But D&B's ambitions proved too sprawling. In 1996, growth of healthcare industry-related businesses led D&B to spin off IMS Health as a subsidiary of Cognizant Corporation. During the first phase, IMS became a subsidiary of Cognizant Corporation along with Nielsen Marketing Research and the Gartner Group.

The Cognizant era was brief but transformative. In 1998, the parent company, Cognizant Corporation, split into two companies: IMS Health and Nielsen Media Research. After this restructuring, Cognizant Technology Solutions became a public subsidiary of IMS Health. This convoluted corporate structure—where the parent became the subsidiary—reflected the immense value locked in IMS's data assets. In 2003, IMS Health sold its entire 56% stake in Cognizant and both companies separated into two independent entities.

Throughout these ownership changes, IMS's core business model remained remarkably consistent: collecting information from more than 29,000 data sources, including drug manufacturers, wholesalers, retailers, pharmacies, hospitals, managed care providers, and long-term care facilities. The company had become the invisible infrastructure of the pharmaceutical industry, processing billions of transactions that no single drug company could replicate.

The controversies that would dog IMS for decades began emerging in this period. Throughout its history, IMS Health's business of collecting anonymized pharmaceutical sales data came under scrutiny from both the media and the legal system. Privacy advocates raised alarms about the company's ability to track individual physician prescribing patterns, even if patient data was supposedly anonymized. State legislatures attempted to restrict data sales, leading to landmark court cases that would ultimately reach the Supreme Court.

By the 1990s, IMS Health had evolved far beyond its origins as a simple data collector. The company was now offering sophisticated analytics, consulting services, and even software platforms that pharmaceutical companies used to manage their entire commercial operations. Compiling information into more than 10,000 reports, available on a regularly updated basis, IMS Health provided a wide variety of market knowledge to support strategic decision-making.

The internet revolution of the late 1990s transformed IMS once again. The company launched its i-squared portal, giving clients instant access to data that once took weeks to compile. Real-time analytics replaced quarterly reports. Predictive models began suggesting which doctors were most likely to prescribe a new drug based on their historical patterns—capabilities that would have seemed like science fiction when Frohlich and Dubow founded the company.

What's remarkable about IMS Health's journey through these decades is how it maintained its monopolistic position despite multiple ownership changes, technological disruptions, and regulatory challenges. The answer lay in the network effects of its business model: the more data IMS collected, the more valuable its insights became, which attracted more clients, which generated more data. It was a virtuous cycle that competitors found impossible to break.

As the 1990s drew to a close, IMS Health stood as the undisputed king of pharmaceutical data, operating in over 100 countries with revenues approaching $1.5 billion. But the company's leadership understood that data alone wouldn't be enough for the future. The next frontier would require combining IMS's information mastery with actual clinical expertise—setting the stage for a merger that would create an entirely new kind of healthcare company. The parallel story of Quintiles, developing just a few states away in North Carolina, would provide exactly what IMS needed.

III. Quintiles: The Clinical Trials Pioneer (1982-2000s)

The scene opens in Trailer 39 on the University of North Carolina campus in 1974. A British biostatistics professor named Dennis Gillings is hunched over stacks of German hospital charts, translating medical records for Hoechst pharmaceutical company. The German pharmaceutical giant was trying to bring a new diabetes drug to market and it was associated with deaths in what was then West Germany. Gillings was asked to do an expert statistical analysis, which he agreed to do as a consulting project. It worked out well because he determined that the drug was not being excreted properly, which caused low blood sugar.

This modest consulting project would spark something much larger. Dennis Gillings began providing statistical consulting and data management services to pharmaceutical clients in 1974 during his tenure as professor of biostatistics at the University of North Carolina at Chapel Hill. He founded Quintiles in 1982, which grew out of his consulting activities with the pharmaceutical industry. What started as a side hustle for extra income would revolutionize how drugs are developed globally.

Gillings wasn't your typical academic. Born in London to a fishmonger father, he had climbed the academic ladder through sheer mathematical brilliance—bachelor's and PhD in mathematics from Exeter, a diploma in mathematical statistics from Cambridge. In 1971, Gillings accepted a position to teach biostatistics at the University of North Carolina at Chapel Hill. But academia felt limiting. He was by now a full professor at the university, but in certain respects the achievement felt limiting. He started to entertain the notion of leaving: "I thought, 'If I stay here for the rest of my life, there's too much more of the same'".

The business model Gillings pioneered was radical for its time. The company was born from the idea that drug development is, in essence, an information science, and that patients benefit when all stakeholders are properly informed. Pharmaceutical companies were spending billions on R&D but lacked the specialized expertise to efficiently manage clinical trials. Why not outsource this to specialists who could do it better, faster, and cheaper?

The new enterprise was called Quintiles. It was housed originally in Trailer 39, "and that worked very well," Gillings says. "I would feed a lot of the work into projects for students. Papers would get published, and the students generated consulting income." The business grew. In February 1982, Gillings incorporated and moved the firm off campus with five full-time employees.

The timing was perfect. Drug makers had begun outsourcing clinical development work in the 1980s in order to rein in skyrocketing R&D costs. Quintiles wasn't just offering statistical analysis—it was creating an entirely new industry category: the Contract Research Organization (CRO). Quintiles started with statistical analysis, added data management, and soon offered a comprehensive clinical services package. "By about the late 1980s, I'd really built that model very successfully and built it internationally," Gillings says.

The international expansion was aggressive and methodical. Quintiles Transnational established Quintiles Pacific Inc. and Quintiles Ireland Ltd. in 1990. In 1991 Quintiles GmbH was established in Germany and Quintiles Laboratories Ltd. was established in Atlanta, Georgia. Each new office wasn't just a flag on the map—it represented the ability to run multi-national clinical trials, a capability pharmaceutical companies desperately needed as drug development became increasingly global.

By the mid-1990s, Quintiles was ready for its most audacious moves yet. Continuing its frenetic pace of growth and expansion, in 1996 the company opened offices in Pretoria, South Africa, Vienna, Austria, Helsinki, Finland, Madrid, Spain, and Buenos Aires, Argentina. Acquisitions included The Lewin Group, Inc., a Fairfax, Virginia-based healthcare policy research and consulting company with a global reputation, and PMC Contract Research AB located in Uppsala, Sweden.

The crown jewel acquisition came in September 1996. Quintiles purchased Innovex Ltd. of Britain for $747.5 million in stock. Innovex Ltd., located in Marlow, England, is one of the world's leading contract pharmaceutical firms that specializes in the sale and marketing of drugs for international pharmaceutical companies. This wasn't just another CRO acquisition—Innovex brought commercial capabilities, allowing Quintiles to support drugs not just through development but into the marketplace.

The reorganization that followed was strategic genius. Company operations were organized into three operating divisions: The Contract Research Division, which provides services such as those involved in clinical trials, regulatory affairs, and medical device consulting; The Innovex Division, which provides the company's marketing and sales services; and The Lewin-Benefit Division, which provides services in the areas of health economics and healthcare policy consulting. This reorganization enabled the company to provide full-service, vertically integrated, product development, sales, and marketing services to all of its clients worldwide.

Wall Street took notice. Gillings took Quintiles public on NASDAQ in 1994, and Quintiles went public in 1997 and completed a successful secondary stock offering. The numbers were staggering for a company that had started in a trailer just 15 years earlier. In 1998, Quintiles was the first company in industry to break the $1 billion mark, when it reported net revenues of $1.19 billion.

But public markets proved frustrating for Gillings, who felt quarterly earnings pressure constrained long-term strategic thinking. In a move that shocked Wall Street, in 2003, the Board of Directors agreed to merge with Pharma Services Holdings Inc; Quintiles became a private company. This privatization, led by Gillings himself, allowed the company to make bold investments without worrying about short-term stock price fluctuations.

The 2000s saw Quintiles continue its relentless expansion. The company wasn't just growing geographically—it was deepening its capabilities across the entire drug development spectrum. From early-stage toxicology studies to late-stage commercialization support, Quintiles positioned itself as the one-stop shop for pharmaceutical companies looking to outsource any aspect of drug development.

What made Quintiles different from other CROs wasn't just scale—it was the systematic approach to standardizing clinical research. By 1990, it was clear that the way forward was to address the full range of drug makers' clinical needs, and to do it efficiently by standardizing clinical research. Gillings moved to reorder the field through the introduction of new information technologies. This standardization created efficiencies that pharmaceutical companies couldn't achieve on their own.

The company's growth trajectory was remarkable. Gillings believed they grew faster than any of their peers, and that allowed them to gain the largest market share by the end of the 1990s. By 2013, when Quintiles returned to public markets trading on NYSE under ticker "Q", it had become the undisputed leader in the CRO industry, managing thousands of clinical trials across every therapeutic area imaginable.

Dennis Gillings had transformed from a professor doing statistical consulting on the side to the architect of an entire industry. He was founding chairman of the Association of Clinical Research Organizations, a Washington, D.C.-based trade group formed in 2002. He served for more than 15 years as a professor at the University of North Carolina at Chapel Hill. His contributions were recognized globally—honored by the Queen as Commander of the Most Excellent Order of the British Empire in 2004 for services to the pharmaceutical industry.

As Quintiles entered the 2010s, it was clear that data and clinical expertise alone wouldn't be enough for the future. The company needed something more—access to the real-world data that could inform not just how trials were designed, but which drugs should be developed in the first place. Meanwhile, just a few hundred miles north in Connecticut, IMS Health had been building exactly that capability for over 60 years. The stage was set for a merger that would reshape the entire life sciences industry.

IV. The Mega-Merger: Creating IQVIA (2016-2017)

May 3, 2016. The announcement dropped like a bombshell on the life sciences industry. Ari Bousbib, chairman and chief executive officer of IMS Health, will become chairman and chief executive officer of the merged organization. Tom Pike, chief executive officer of Quintiles, will become vice chairman. Two titans of healthcare services—one built on data, the other on clinical expertise—were joining forces in what would become a $17.6 billion merger.

The boardroom negotiations had been months in the making, but the strategic logic was instantly clear to both CEOs. Quintiles Chief Executive Officer, Tom Pike, said, "This combination addresses life-science companies' most pressing needs: to transform the clinical development of innovative medicines, demonstrate the value of these medicines in the real world, and drive commercial success. We are bringing together two best-in-class leaders." Pike understood that Quintiles' clinical trial expertise alone wasn't enough anymore—pharmaceutical companies wanted to know not just if a drug worked in controlled trials, but how it performed in the messy reality of everyday healthcare.

Bousbib saw the merger from a complementary angle. Ari Bousbib, chairman and chief executive officer of IMS Health, stated, "Together our solutions will enable differentiation in the CRO market, advance Real-World Evidence capabilities, and deliver comprehensive commercial solutions for our clients. This powerful combination brings together leading technology and analytics with deep scientific expertise delivered on a global scale by our 50,000 immensely talented professionals in more than 100 markets."

The structure of the deal reflected a careful balance of power. Both market leaders in their respective spaces, IMS and Quintiles are merging in an all-stock deal that will create a combined company currently with $17.6 billion in equity value (based on pre-announcement stock prices). After the merger, IMS stockholders will own 51.4% of the combined entity, giving IMS Health a slight majority despite calling it a "merger of equals."

The governance structure was equally balanced. The company's Board of Directors will be comprised of six directors appointed by the Quintiles Board of Directors and six directors appointed by the IMS Health Board of Directors. The lead director will be Dennis Gillings, CBE, Ph.D. Having Gillings, the founder of Quintiles, as lead director was a symbolic nod to Quintiles' heritage while Bousbib held operational control.

Wall Street's initial reaction was brutal. Shareholders greeted the news unenthusiastically, with both companies' share prices dropping by several percentage points over the day; speculation was that shareholders were looking for a substantial premium in stock repurchases. However, shares in both companies dropped sharply on Tuesday after the deal was announced, indicating that some shareholders were not satisfied with the combination. The share price of IMS Health was down 7.5% on the news in morning trading, while Quintiles was down more than 8%.

The skepticism wasn't just about price. But investors may be wary of the deal because "neither side is receiving a merger-related premium from the combination" and "integration risks are higher in a merger-of-equals," John Kreger, an analyst at William Blair, said in a research note. Mergers of equals have a notorious track record—without a clear acquirer and target, power struggles and cultural clashes often doom integration efforts.

But beneath the surface skepticism lay transformative potential. The deal will, in essence, merge the real-world clinical applications of Quintiles' business with IMS Health's data gathering and analysis, as well as its access to patient, prescription and other key healthcare data, giving the new company a pool of information for drugmakers. It will also likely encroach deeply into the offerings of Quintiles' main big CRO, North Carolina rivals, which have also been looking to expand into consultancy, digital and analytics in recent years.

The integration planning revealed the complexity of merging two industry giants. The combined company expects to maintain dual headquarters in Danbury, CT, and Research Triangle Park, NC. This decision to maintain both headquarters was partly practical—avoiding massive relocations—but also symbolic, showing neither company was being absorbed by the other.

By August 2016, the leadership structure was taking shape. Senior functional leaders reporting to Chairman and Chief Executive Officer Ari Bousbib will include Michael McDonnell, EVP and Chief Financial Officer; James Erlinger, EVP and General Counsel; and Trudy Stein, EVP and Chief Human Resources Officer. Global business leaders reporting to Mr. Bousbib will include, for the clinical research business, Tom Pike, Vice Chairman and President, Research & Development Solutions; and for the commercial business, Kevin Knightly, President, Information and Technology Solutions; José Luis Fernández, President, Global Services; Jon Resnick, President, Real-World Insights; and Scott Evangelista, President, Contract Sales Organization.

The strategic rationale went beyond simple synergies. Synergies from combined back office services and the like will generate $100 million in savings by the third year—a relatively small amount which implies that no broad layoffs are planned. The real value lay in creating something entirely new: a company that could follow a drug from early development through real-world performance, providing insights no competitor could match.

The transaction is subject to customary closing conditions, including regulatory approvals and approval by both IMS Health and Quintiles shareholders and is expected to close in the second half of 2016. Shareholders of IMS Health owning approximately 54 percent of the common stock of IMS Health and shareholders of Quintiles owning approximately 25 percent of the common stock of Quintiles have entered into agreements to vote in favor of the merger, essentially guaranteeing its approval.

The cultural integration challenges were immense. IMS Health's data scientists and technology experts in Connecticut had little in common with Quintiles' clinical operations teams in North Carolina. IMS employees were accustomed to selling insights and software; Quintiles staff managed complex multi-year clinical trials. The companies even spoke different languages—IMS talked about "data lakes" and "analytics engines" while Quintiles discussed "protocol amendments" and "site activation."

October 3, 2016, marked the official closing of the merger. The combined entity, initially called QuintilesIMS, brought together 50,000 employees across more than 100 countries. But the real work was just beginning. Integrating two companies with such different cultures, business models, and operational approaches would test even the most experienced management team.

The company faced immediate pressure to prove the merger's value. Pharmaceutical clients were watching closely—would this new entity deliver on its promises of seamlessly integrated services from molecule to market? Competitors were circling, looking for disgruntled clients or employees to poach during the integration chaos.

November 2017 brought the final piece of the transformation. On November 6, 2017, the company adopted the new name of IQVIA. The name itself told the story: The IQVIA name is a combination of: I (IMS Health), Q (Quintiles), and VIA (by way of). It was a deliberate break from the past, signaling that this wasn't just IMS Health with Quintiles bolted on, or vice versa—it was something genuinely new.

The rebranding wasn't just cosmetic. It reflected a fundamental reimagining of what a healthcare services company could be. IQVIA wasn't positioning itself as a CRO that also had data, or a data company that could run trials. It was presenting itself as the essential infrastructure for modern drug development—a company whose "Connected Intelligence" could accelerate every stage of the pharmaceutical value chain.

Ari Bousbib declared, "I am proud to be part of a leadership team with deep industry knowledge, a proven track record of success and a commitment to transforming healthcare for the better." His vision was ambitious: create a category of one, a company so differentiated that clients couldn't replicate its capabilities even if they tried.

Looking back, the merger's success hinged on recognizing that the future of healthcare wasn't about clinical trials or data analytics in isolation—it was about the integration of both. Every drug that reached patients would need to prove itself twice: first in the controlled environment of clinical trials, then in the chaotic reality of actual medical practice. IQVIA positioned itself as the only company that could provide visibility across this entire journey.

The merger also sent shockwaves through the competitive landscape. Other CROs scrambled to acquire data capabilities. Data companies rushed to add clinical services. But none could match the scale and scope of what IQVIA had assembled. The integration challenges were real—cultural clashes, system incompatibilities, client confusion—but the strategic logic proved sound. As we'll explore in the next section, this unique combination of capabilities would drive a business model unlike anything else in healthcare services.

V. Business Model Deep Dive: Three Pillars of Growth

The numbers tell a story of strategic precision. Revenue of $15,405 million for the full year of 2024 grew 2.8 percent on a reported basis and 3.4 percent at constant currency, compared to 2023. TAS revenue was $6,160 million, up 5.1 percent on a reported basis and 5.7 percent at constant currency. R&DS revenue was $8,527 million, up 1.6 percent on a reported basis and 2.0 percent at constant currency. CSMS revenue was $718 million, down 1.2 percent on a reported basis and up 1.4 percent at constant currency. But behind these figures lies a business model engineered to capture value at every stage of the pharmaceutical lifecycle.

Technology & Analytics Solutions (TAS): The Data Engine

TAS revenue was $6,160 million, up 5.1 percent on a reported basis and 5.7 percent at constant currency, representing 40% of IQVIA's total revenues. This segment is where the IMS Health DNA shines brightest—a vast repository of healthcare data that provides insights no competitor can match.

The scale is staggering: access to 1.2 billion unique non-identified patient records globally. To put this in perspective, that's roughly one in every seven humans on Earth whose anonymized health data flows through IQVIA's systems. This isn't just passive data collection—it's active intelligence generation that pharmaceutical companies depend on for critical decisions.

As Ari mentioned in his opening remarks, the 2024 growth trajectory in TAS played out as we anticipated with improvements every quarter. We had we experienced a softening growth rate throughout 2023 due to cautious customer discretionary spending and we predicted that 2024 would be a turnaround year based on our forward-looking indicators in recent history. In fact, that's what happened in 2024 TAS growth picked up significantly, finishing the second half with high single digit growth driven by strong mid-single digit organic growth.

The TAS business model operates on three core pillars. First, subscription-based analytics services provide recurring revenue streams as pharmaceutical companies pay for ongoing access to market intelligence. These aren't one-time purchases but essential infrastructure—like Bloomberg terminals for traders, IQVIA's platforms become indispensable once integrated into a client's workflow.

Second, cloud-based CRM and commercial solutions help pharmaceutical sales teams target the right doctors with the right messages. When a sales representative walks into a physician's office, they're armed with IQVIA data showing that doctor's prescribing patterns, patient demographics, and competitive dynamics. It's precision selling powered by comprehensive data.

Third, real-world evidence (RWE) capabilities are increasingly valuable as regulators and payers demand proof that drugs work outside controlled clinical trials. But we also had stronger organic demand than expected across all sub-segments with real-world actually returning to double digit growth. We finished the year with constant currency growth of 5.7% and about 6.5% excluding the COVID step down, which was at the high end of our guidance.

What makes TAS particularly attractive from a business perspective is its capital efficiency. Unlike clinical trials that require armies of personnel and physical infrastructure, data analytics scales beautifully. The marginal cost of serving an additional client with existing data is minimal, driving impressive operating leverage as the business grows.

Research & Development Solutions (R&DS): The Clinical Powerhouse

R&DS revenue was $8,527 million, up 1.6 percent on a reported basis and 2.0 percent at constant currency, making it IQVIA's largest segment at 55% of revenues. This is the Quintiles heritage—managing the complex, multi-year journey of drug development from first-in-human studies to post-market surveillance.

The business model here is fundamentally different from TAS. R&DS operates on a project basis with long-term contracts that can span 5-10 years for a single drug development program. As of December 31, 2024, R&DS contracted backlog, including reimbursed expenses, was $31.1 billion, growing 4.4 percent year-over-year and 5.5 percent at constant currency. This backlog provides remarkable revenue visibility—essentially three to four years of guaranteed work already contracted.

The R&DS value proposition goes beyond simple outsourcing. IQVIA manages every aspect of clinical trials: protocol design, site selection, patient recruitment, data management, statistical analysis, and regulatory submissions. For a pharmaceutical company developing a new drug, IQVIA becomes an extension of their organization, sometimes with more people working on a program than the sponsor company itself employs.

R&D Solutions quarterly bookings of over $2.5 billion, representing a book-to-bill ratio of 1.20x The 1.20x book-to-bill ratio is particularly telling—for every dollar of revenue recognized, IQVIA is booking $1.20 in new business, driving consistent backlog growth.

Patient recruitment has become a critical differentiator. Using TAS data capabilities, IQVIA can identify optimal trial sites, predict enrollment rates, and even use digital marketing to find eligible patients. This integration between segments creates competitive advantages that pure-play CROs simply cannot replicate.

The operational complexity of R&DS is immense. Managing thousands of clinical trials simultaneously across hundreds of countries requires sophisticated project management systems, regulatory expertise in every major market, and relationships with thousands of investigator sites. This operational moat takes decades to build and would cost billions to replicate.

Contract Sales & Medical Solutions (CSMS): The Commercial Catalyst

CSMS revenue was $718 million, down 1.2 percent on a reported basis and up 1.4 percent at constant currency, representing just 5% of revenues. While the smallest segment, CSMS plays a strategic role in IQVIA's integrated offering.

CSMS provides outsourced sales forces to pharmaceutical companies—particularly valuable for specialty drugs or orphan indications where maintaining a dedicated sales team isn't economical. But this isn't just body-shopping. IQVIA's sales representatives come armed with the company's data and analytics capabilities, making them more effective than traditional contract sales organizations.

The segment also includes medical affairs services, helping pharmaceutical companies engage with key opinion leaders, manage scientific communications, and handle medical information requests. In an era of increasing scientific complexity, having experts who can translate clinical data for practicing physicians is invaluable.

Finally, CSMS revenue is expected to be approximately $700,000,000 and flattish year over year. The flat growth reflects strategic choices rather than market weakness. IQVIA has been selective about CSMS contracts, focusing on higher-margin engagements that leverage the company's broader capabilities rather than competing on price for commodity sales force contracts.

The Power of Integration

What transforms these three segments from good businesses into a formidable competitive moat is their integration. Consider the journey of a single drug:

TAS data identifies an unmet medical need and market opportunity. R&DS designs and executes clinical trials to prove the drug's safety and efficacy, using TAS data to optimize site selection and patient recruitment. Post-approval, TAS analytics guide commercial strategy while CSMS deploys specialized sales forces. Throughout the lifecycle, TAS real-world evidence demonstrates the drug's value to payers and regulators.

This integration creates switching costs that lock in clients. A pharmaceutical company using IQVIA for clinical trials naturally turns to them for commercial analytics—the data flows seamlessly. A client using TAS for market intelligence finds it efficient to use R&DS for trials since IQVIA already understands their therapeutic area deeply.

The financial model reflects this integration. While R&DS generates the most revenue, TAS drives the highest margins due to its scalability. CSMS, though smallest, provides strategic touchpoints with commercial teams that often influence trial and analytics decisions. Cross-selling between segments is extensive—most large pharmaceutical companies use services from all three segments.

Operating Leverage and Financial Dynamics

Adjusted EBITDA for the full year of 2024 was $3,684 million, up 3.2 percent year-over-year. The 24% adjusted EBITDA margin reflects a business with significant operating leverage. As revenues grow, margins expand because much of the infrastructure—data systems, therapeutic expertise, operational platforms—already exists.

Operating Cash Flow of $885 million, bringing full-year Operating Cash Flow to $2,716 million, up 26 percent year-over-year Free Cash Flow of $721 million for Q4 alone demonstrates the cash-generative nature of the business model. Unlike capital-intensive industries, IQVIA converts a high percentage of earnings into free cash flow, enabling aggressive capital allocation.

The segment mix evolution tells a strategic story. TAS is growing fastest, which should drive margin expansion over time given its superior economics. R&DS growth has been muted by COVID-19 comp issues and pharmaceutical industry restructuring, but the massive backlog provides confidence in future growth. CSMS remains strategically important despite its small size, providing client touchpoints that facilitate cross-selling.

Competitive Moats in Action

The durability of IQVIA's business model stems from multiple reinforcing moats:

Data Network Effects: Every prescription filled, every clinical trial conducted, every sales call tracked adds to IQVIA's data advantage. Competitors starting today would need decades to build comparable historical datasets.

Switching Costs: Pharmaceutical companies integrate IQVIA systems deeply into their operations. Changing providers mid-trial is virtually impossible, and switching analytics platforms requires retraining entire commercial organizations.

Economies of Scale: The fixed costs of maintaining global clinical operations, regulatory expertise, and data infrastructure are massive. Spread across IQVIA's revenue base, these costs are manageable. For smaller competitors, they're prohibitive.

Regulatory Expertise: IQVIA's relationships with regulators worldwide, built over decades, cannot be replicated quickly. When a pharmaceutical company needs to navigate complex approval processes, IQVIA's expertise saves years and millions of dollars.

Looking ahead, the business model is evolving to capture new opportunities. Artificial intelligence is being embedded across all segments, from predictive analytics in TAS to patient matching in R&DS. The rise of precision medicine creates demand for new types of real-world evidence that only IQVIA can provide at scale. Cell and gene therapies require entirely new clinical trial approaches that IQVIA is pioneering.

The three-pillar structure isn't just organizational—it's a strategic framework that allows IQVIA to capture value wherever it's created in the pharmaceutical value chain. As we'll explore in the next section, this integrated model generates substantial cash flows that management deploys strategically to drive shareholder returns while investing in future growth.

VI. Financial Performance & Capital Allocation

For the full year of 2024, Operating Cash Flow was $2,716 million and Free Cash Flow was $2,114 million, growing 26 percent and 41 percent year-over-year, respectively. These aren't just numbers on a spreadsheet—they represent IQVIA's transformation into a cash flow machine that converts intellectual capital into shareholder value with remarkable efficiency.

The free cash flow story is particularly compelling. For the fourth quarter of 2024, Operating Cash Flow was $885 million and Free Cash Flow was $721 million. In a single quarter, IQVIA generated more free cash than many companies its size produce in a year. The 41% year-over-year growth in free cash flow dramatically outpaced revenue growth of 2.8%, demonstrating powerful operating leverage as the business scales.

After all reinvestments are considered, my calculations suggest that IQV is routinely throwing off $2 billion-$3 billion of free cash flow every rolling 12-month period, whilst comfortably investing surplus cash to grow the business. This cash generation enables aggressive capital allocation without compromising the balance sheet or growth investments.

The Capital Allocation Playbook

IQVIA's capital allocation strategy reflects a disciplined balance between returning cash to shareholders and investing in growth. During the fourth quarter of 2024, the company repurchased $1,150 million of its common stock, resulting in full-year share repurchases of $1,350 million. This represents over 60% of free cash flow returned to shareholders through buybacks alone.

The board's confidence is evident in their authorization expansion. On February 5, 2025, the IQVIA board of directors increased the share repurchase authorization by $2,000 million dollars, bringing the total remaining authorization to $3,013 million. This massive authorization—nearly 10% of the company's market cap—signals management's belief that the stock remains undervalued despite strong operational performance.

Share buybacks at IQVIA aren't just financial engineering—they're value creation. It also returned an average of $800 million-$900 million per rolling 12-month period from 2023 up to Q1 2024 in the form of buybacks to shareholders. With shares consistently repurchased below intrinsic value, each buyback increases the ownership stake of remaining shareholders in a growing, cash-generative business.

Leverage: A Strategic Tool, Not a Burden

As of December 31, 2024, cash and cash equivalents were $1,702 million and debt was $13,983 million, resulting in net debt of $12,281 million, and IQVIA's Net Leverage Ratio was 3.33x trailing twelve-month Adjusted EBITDA. A 3.33x leverage ratio might alarm some investors, but for IQVIA, this represents optimal capital structure rather than financial stress.

The company's approach to debt management is sophisticated. IQVIA's decision to issue $2 billion in senior notes due June 1, 2032, at a 6.25% interest rate is a strategic refinancing step. The funds will primarily repay borrowings under its revolving credit facility, which likely carried higher interest costs or shorter maturities. By extending debt maturity and locking in a fixed rate, IQVIA is shielding itself from rising interest rate risks—a prudent move as central banks globally remain cautious about monetary policy.

This isn't leveraging for leverage's sake—it's using debt strategically to enhance returns. As seen below, most of the company's trailing return on equity is driven from leverage, with the 4.2x equity multiplier. When a business generates consistent free cash flow with minimal capital requirements, moderate leverage amplifies returns to equity holders without materially increasing risk.

Margin Expansion: The Compounding Machine

Adjusted EBITDA of $996 million for the fourth quarter, $3,684 million for the full year The $3.684 billion in adjusted EBITDA represents a 23.9% margin, but the trajectory is more important than the absolute level. For the full year, we delivered margin expansion, high single-digit growth in Adjusted EPS, and outstanding free cash flow; we also repurchased $1.35 billion dollars of our shares while lowering our net leverage ratio year-over-year.

Margin expansion at IQVIA isn't accidental—it's engineered through multiple levers. Scale economics in TAS mean each additional dollar of revenue requires minimal incremental cost. Automation and AI deployment in R&DS reduce manual processes while improving quality. Strategic pruning of low-margin CSMS contracts improves mix. The cumulative effect: a business that becomes more profitable as it grows.

Earnings Power and Valuation Dynamics

GAAP Diluted Earnings per Share of $2.42 for the fourth quarter, $7.49 for the full year Adjusted Diluted Earnings per Share of $3.12 for the fourth quarter, $11.13 for the full year The gap between GAAP and adjusted earnings—$7.49 versus $11.13—reflects substantial non-cash charges from historical acquisitions. Focusing on adjusted earnings provides a clearer picture of economic reality.

Consensus is looking at 8.7% bottom-line growth in 2024. If there is no change in the P/E multiple, then the company is worth $249 to me today, with implied earnings of $7.97 per share (31.3 x $7.97 = $249). This valuation framework suggests significant upside from current levels, particularly given IQVIA's consistent execution and improving fundamentals.

Working Capital Efficiency

One underappreciated aspect of IQVIA's financial model is working capital management. Unlike many service businesses that must fund growth with working capital, IQVIA often receives cash upfront for multi-year clinical trial contracts. This negative working capital dynamic means growth actually generates cash rather than consuming it.

The R&DS backlog structure illustrates this beautifully. Clients commit to multi-billion dollar contracts spanning years, often with upfront payments or milestone-based funding that arrives before work is complete. This creates a float that IQVIA can deploy for acquisitions, buybacks, or organic investments while earning returns on client money.

Return on Invested Capital: The Ultimate Scorecard

Last time, I commented on the company's strengths in unlocking risk capital for shareholders, namely via 1) exceptional net operating profit after tax relative to the capital invested to produce these numbers, 2) decompression of post-tax margins with increasing capital turnover, and 3) the company's propensity to throw off stable, high amounts of free cash flow to its owners.

IQVIA's return on invested capital consistently exceeds 10%, remarkable for a people-intensive business. This isn't achieved through capital intensity—IQVIA has minimal fixed assets relative to revenues. Instead, it's driven by intellectual capital: proprietary data, therapeutic expertise, operational know-how, and client relationships that generate returns without requiring proportional capital investment.

Strategic Acquisitions: Buying vs. Building

While organic growth drives most value creation, IQVIA deploys capital strategically for acquisitions that enhance capabilities or accelerate market entry. The company typically spends $200-400 million annually on tuck-in acquisitions—small enough to integrate easily but meaningful enough to move the needle in specific therapeutic areas or geographies.

These aren't transformational deals seeking synergies through cost cuts. Instead, IQVIA acquires specialized capabilities that would take years to build organically: a real-world evidence platform in oncology, a patient recruitment technology, a regional CRO with local expertise. Each acquisition is evaluated on its ability to enhance IQVIA's competitive moat rather than just financial metrics.

The Dividend Question

Notably absent from IQVIA's capital allocation is a dividend. This isn't oversight—it's strategy. With returns on invested capital exceeding 10% and ample reinvestment opportunities, paying dividends would be value-destructive. Every dollar retained and reinvested compounds at high rates, creating more value than returning cash to shareholders who might struggle to find similar returns elsewhere.

The buyback-focused strategy also provides more flexibility than dividends. Buybacks can be accelerated when shares are cheap and paused when prices are dear. Dividends, once initiated, become quasi-obligations that limit financial flexibility. For a business with IQVIA's growth profile and capital efficiency, buybacks are the optimal choice.

2025 Guidance: Conservative or Sandbagged?

Looking ahead, management's guidance reveals their capital allocation priorities. The guidance also assumes $2 billion of cash deployment split between acquisitions and share repurchase. This balanced approach—roughly $1 billion each for M&A and buybacks—maintains optionality while returning substantial capital to shareholders.

The guided free cash flow generation of approximately $2.3-2.5 billion for 2025 (implied from EBITDA guidance less interest and capital expenditures) suggests another year of robust cash generation. With the business requiring minimal capital for organic growth, virtually all free cash flow is available for deployment at management's discretion.

The financial performance story at IQVIA isn't just about growing revenues or expanding margins—it's about converting intellectual capital into shareholder value through disciplined capital allocation. As we'll explore next, this financial strength provides the foundation for maintaining competitive advantages in an increasingly crowded marketplace.

VII. Competition & Market Position

The global contract research organization (CRO) services market is projected to reach USD 129.8 billion by 2029 from an estimated USD 82.0 billion in 2024, at a CAGR of 9.6% during the forecast period. In this rapidly expanding market, IQVIA Inc. (US) held the largest share in the global CRO services market in 2023. This is mainly due to its strong presence in the biopharmaceutical services industry and wide geographical reach.

The Competitive Landscape

IQVIA's dominance isn't just about size—it's about strategic positioning that competitors struggle to replicate. The company holds a strategic position in the market mainly supported by its wide range of service offerings along with significant partnerships with large industry players operating in the pharmaceutical and biopharmaceutical industry. While competitors focus on specific niches, IQVIA offers the full spectrum from molecule to market.

The competitive set reads like a who's who of healthcare services:

ICON plc - Following their 2021 acquisition of PRA Health Sciences, ICON has emerged as IQVIA's most formidable competitor. In 2024, ICON generated full-year revenues of $8,282 million, a year-on-year increase of 2.0%. ICON's strength lies in therapeutic expertise, particularly in oncology and rare diseases. However, they lack IQVIA's data assets and commercial capabilities, forcing them to compete primarily on clinical excellence and price.

Syneos Health - Formed through the merger of inVentiv Health and INC Research, Syneos attempted to replicate IQVIA's integrated model. With approximately $5 billion in revenue, they offer both clinical and commercial services. But Syneos lacks the scale and data infrastructure that makes IQVIA's integration truly powerful. Their recent financial struggles and leadership changes highlight the difficulty of executing this integrated strategy without sufficient scale.

Parexel - Now owned by private equity, Parexel focuses on biotech and emerging biopharma clients. Their "patients first" positioning and expertise in complex trials for rare diseases has carved out a profitable niche. But with revenues around $3 billion, they lack the resources to compete across IQVIA's full spectrum of services.

Covance (LabCorp subsidiary) - LabCorp's $7.2 billion acquisition of Covance in 2015 created a unique competitor combining laboratory services with clinical trials. Their central lab capabilities give them advantages in certain trial types, but they lack IQVIA's commercial services and real-world data assets. The integration with LabCorp's diagnostic business has been slower than expected, limiting synergies.

Charles River Laboratories - Focused on preclinical services with $4 billion in revenue, Charles River dominates early-stage drug development. While not a direct competitor across IQVIA's full range, they compete intensely for early-phase work and have been expanding into clinical services through acquisitions.

Unique Market Position

What sets IQVIA apart isn't just scale—it's the company's unique positioning at the intersection of data and services. IQVIA was formed in 2016 from the merger of Quintiles, a contract research organization, and IMS Health, a healthcare data and analytics provider and the largest vendor of U.S. physician prescribing data. This combination created capabilities no competitor can match.

Consider a pharmaceutical company developing a new diabetes drug. ICON or Parexel could run the clinical trials. Syneos could provide the sales force. Various data vendors could offer market analytics. But only IQVIA can: - Use historical data to identify optimal trial sites and predict enrollment rates - Manage the entire clinical development program from Phase I through approval - Provide real-world evidence to support reimbursement negotiations - Deploy analytics to optimize commercial launch strategy - Offer contract sales teams armed with proprietary market intelligence

This integrated offering creates powerful lock-in effects. Once a client uses IQVIA for clinical trials, the data naturally flows into commercial planning. Once they rely on IQVIA's analytics, extending into real-world evidence studies becomes seamless.

Market Dynamics and Growth Drivers

The CRO market's robust growth—projected at 9.6% CAGR through 2029—benefits all players, but IQVIA captures a disproportionate share. According to IQIVIA's Global Trends in R&D 2024 report, oncology remains the largest therapeutic area of R&D activity, with 2,143 Phase I to III trials started or planned to start in 2023. IQVIA's deep oncology expertise and comprehensive data on cancer patients positions them perfectly for this growth.

The market is being reshaped by several trends that favor IQVIA's integrated model:

Complexity Escalation - Of these trials, 25% are focused on novel oncology mechanism, including cell and gene therapies, antibody drug conjugates, and multi-specific antibodies. These complex modalities require sophisticated trial designs and real-world evidence generation—areas where IQVIA's data-service integration provides unique value.

Geographic Expansion - Asia Pacific dominated the market globally with a revenue share of 46.40% in 2024. The region's high share is due to an increased number of actively functioning CROs, especially in China and Japan. IQVIA's early investments in Asia, including strategic partnerships with local players, give them advantages competitors struggle to replicate.

Precision Medicine - Growing demand for precision/ personalized medicine is a key opportunity area for players in CRO Services market. IQVIA's vast patient data enables identification of specific patient populations for targeted therapies, a capability pure-play CROs cannot match.

Competitive Advantages in Action

IQVIA's competitive moats manifest in tangible ways:

Win Rates - IQVIA wins a higher percentage of RFPs than competitors, particularly for large, complex programs requiring integrated services. Pharmaceutical companies value the simplicity of a single vendor managing data, trials, and commercialization.

Pricing Power - While CRO services are increasingly commoditized, IQVIA maintains premium pricing for integrated offerings. Clients pay more for the convenience and risk reduction of working with a proven partner across the development lifecycle.

Customer Stickiness - IQVIA Holdings Inc (NYSE:IQV) successfully renewed all large pharma strategic partnerships and expanded the scope of work in several partnerships. These multi-year, multi-billion dollar partnerships create switching costs that lock in revenue for years.

Innovation Leadership - IQVIA Holdings Inc (NYSE:IQV) was recognized with several awards, including the 2024 Global Customer Value Leadership Award for excellence in AI quality and regulatory solutions in healthcare. This innovation leadership attracts clients seeking cutting-edge capabilities.

Emerging Competitive Threats

While IQVIA's position appears secure, several trends could reshape competition:

Technology Disruption - Companies like Veeva Systems are building cloud platforms that could disintermediate parts of IQVIA's business. If pharmaceutical companies can access integrated data and trial management through software platforms, the value of IQVIA's integration diminishes.

Chinese CROs - WuXi AppTec and other Chinese CROs are expanding globally with significantly lower cost structures. While they currently lack IQVIA's sophistication and data assets, they're investing heavily in capabilities and winning share in price-sensitive segments.

Big Tech Entry - Amazon, Google, and Microsoft are all eyeing healthcare. Their cloud infrastructure, AI capabilities, and deep pockets could enable them to build or acquire competitive positions. IQVIA's collaboration with NVIDIA shows they're aware of this threat and partnering proactively.

Consolidation - Further consolidation among mid-tier CROs could create stronger competitors. If ICON merged with Syneos, or if private equity rolled up several smaller players, the resulting entity might achieve sufficient scale to challenge IQVIA more effectively.

Defensive Strategies

IQVIA isn't standing still. The company undertakes development initiatives in order to maintain its position in this market. These developments include collaborations, partnerships, and acquisitions along with expansion. Their defensive playbook includes:

Capability Expansion - Continuous investment in new therapeutic areas, technologies, and geographies prevents competitors from finding undefended niches.

Partnership Lock-in - Multi-year strategic partnerships with major pharmaceutical companies create switching barriers and provide revenue visibility.

Technology Investment - Heavy investment in AI, automation, and digital capabilities maintains IQVIA's innovation edge and improves operational efficiency.

Selective M&A - Strategic acquisitions of specialized capabilities or regional players prevents competitors from acquiring these assets while enhancing IQVIA's offerings.

The Verdict on Competition

In the near term, IQVIA's competitive position appears unassailable. The combination of scale, scope, and switching costs creates formidable barriers to competition. Competitors can nibble at the edges—ICON winning a large oncology program, Syneos taking a commercial contract—but they cannot replicate IQVIA's integrated value proposition.

The real competitive risk isn't from traditional CROs but from business model disruption. If pharmaceutical R&D shifts dramatically—perhaps through AI-driven drug discovery or regulatory changes—IQVIA's current advantages might become less relevant. But given the company's track record of adaptation and innovation, they're likely to evolve with the industry rather than be disrupted by it.

As we'll explore next, IQVIA's technology and innovation initiatives aren't just about maintaining competitive advantage—they're about redefining what's possible in pharmaceutical development.

VIII. Technology & Innovation: The AI Revolution

Introduced 60 innovations in 2024, including 39 AI-enabled applications. This staggering pace of innovation—more than one AI application launched per week—demonstrates IQVIA's transformation from a data and services company into an AI-powered healthcare intelligence platform. The recent collaboration between IQVIA and NVIDIA will help accelerate IQVIA Healthcare-grade AI™, enabling new levels of agentic automation of complex and time-consuming workflows across the therapeutic life cycle with the precision, scalability, and trust required by IQVIA's customers.

Healthcare-grade AI: A New Standard

Building on a rich history of developing AI for healthcare, IQVIA AI connects the right data, technology, and expertise to address the unique needs of healthcare. It's what we call Healthcare-grade AI. This isn't marketing fluff—it's a fundamental reimagining of how AI should be deployed in life sciences.

Healthcare-grade AI™ represents IQVIA's commitment to using AI responsibly, with AI-powered capabilities built on best-in-class approaches to privacy, regulatory compliance and patient safety, and delivering AI to the high standards of trust, scalability and precision demanded by the industry. In an industry where a single error can delay drug approval by years or harm patients, "healthcare-grade" means AI that pharmaceutical companies can trust with billion-dollar decisions.

The distinction matters. While tech companies tout general-purpose AI models, IQVIA is trained on high-quality data and deep domain expertise. A large language model trained on internet text might hallucinate drug interactions; IQVIA's models are trained on decades of validated clinical data, ensuring outputs that meet regulatory standards.

The NVIDIA Partnership: Accelerating the Future

"This represents a significant leap forward in how we apply AI to healthcare and life sciences," said Bhavik Patel, president, Commercial Solutions, IQVIA. "We are excited to combine our industry-leading capabilities and a decade of experience in artificial intelligence with NVIDIA's advanced AI technologies."

The partnership isn't just about accessing NVIDIA's GPUs—it's about co-creating purpose-built solutions. The collaboration will combine IQVIA's unparalleled information assets, analytics, and domain expertise, known as IQVIA Connected Intelligence™, with the NVIDIA AI Foundry service to help transform life science processes from R&D through commercialization.

IQVIA will benefit from NVIDIA's NIM microservices, NeMo, the DGX Cloud platform, and direct support from NVIDIA's research and engineering teams. This deep technical integration allows IQVIA to deploy AI at unprecedented scale while maintaining the precision required for healthcare applications.

Agentic AI: From Automation to Intelligence

The most transformative development is IQVIA's move into agentic AI—systems that don't just analyze but act. Deployed in its healthcare-grade AI platform, IQVIA's AI orchestrator agents are designed to accelerate every step of the pharmaceutical lifecycle, including clinical trials.

Consider the clinical trial startup process. Clinical trials represent a major accomplishment in the research and development process for pharmaceutical companies, but planning and executing a trial typically takes years. The start-up process, alone, often takes about 200 days and is manually intensive. IQVIA's clinical trial start-up AI orchestrator agent addresses the growing need for acceleration in clinical trial timelines.

These AI agents act as supervisors for a group of sub-agents that each specialize in different tasks, like a conductor managing strings, woodwinds, bass and percussion sections. The orchestrator agent routes any necessary actions — like speech-to-text transcription, clinical coding, structured data extraction and data summarization — to the appropriate sub-agent.

Real-World Applications Transforming Drug Development

IQVIA AI Assistant wins 2024 PM360 Innovation Award. Launched in September 2024, IQVIA AI Assistant revolutionizes insight generation by providing rapid, relevant and precise answers to complex business questions. Using a conversational interface with advanced data science, it makes complex analytics accessible to a wide variety of users and provides near real-time insights.

This isn't a chatbot—it's a domain expert. Pharmaceutical executives can ask complex questions like "Which oncology trials in Europe are struggling with enrollment?" and receive actionable insights drawn from IQVIA's vast data repositories, analyzed through proprietary algorithms, and presented with regulatory-compliant documentation.

Another game-changing application: the clinical data review agent, uses a set of automated checks and specialized agents to catch data issues early, reducing the data review process from seven weeks to as little as two weeks. In clinical trials where every day of delay costs millions, this acceleration translates directly to faster drug approvals and earlier patient access.

The Human Data Science Cloud: Infrastructure for Innovation

The IQVIA Human Data Science Cloud is our unique capability designed to enable healthcare-grade analytics, tools, and data management solutions to deliver fit-for-purpose global data at scale. This isn't just cloud storage—it's a purpose-built platform processing 64 petabytes of healthcare information with the security, compliance, and computational power required for AI at scale.

The platform's architecture enables something previously impossible: real-time analysis of global health trends. During COVID-19, IQVIA could track infection patterns, treatment outcomes, and vaccine effectiveness across continents in near real-time, providing insights that shaped public health responses worldwide.

Democratizing AI Across the Organization

For example, we introduced IQVIA AI Assistant, our first ever gen AI interface. It allows customers to interact with a growing number of our products and get answers to their questions almost instantly. This democratization of AI means a sales representative in Brazil can access the same sophisticated analytics as a data scientist in Boston, breaking down silos and accelerating decision-making.

We launched a number of AI-enabled patient offerings, including our Patient Relationship Manager, which has already been deployed at eight clients including three top 10 pharma. This system uses AI to predict which patients are most likely to discontinue therapy, enabling proactive interventions that improve outcomes while reducing healthcare costs.

Real-World Evidence Revolution

The convergence of AI and real-world data is perhaps IQVIA's most significant innovation frontier. IQVIA orchestrator agents can provide a comprehensive understanding of how a treatment will reach patients by analyzing patient records, prescriptions and lab results in just a few days instead of weeks.

This capability is transforming how drugs are approved and reimbursed. Regulators increasingly demand real-world evidence showing drugs work outside controlled trials. IQVIA's AI can analyze millions of patient records to demonstrate effectiveness in diverse populations, supporting regulatory submissions and reimbursement negotiations.

Commercial AI: Precision Selling at Scale

The IQVIA field companion orchestrator agent delivers tailored insights to pharmaceutical sales teams before each engagement with healthcare providers. By integrating physician demographics, digital behavior, prescribing patterns and patient dynamics, the agent helps field teams prepare for each meeting using near real-time insights, leading to more engaging and impactful discussions.

This isn't just about selling more drugs—it's about ensuring the right patients get the right treatments. AI identifies physicians whose patients would most benefit from a new therapy, enabling targeted education that improves patient outcomes while optimizing commercial resources.

The Competitive Moat of AI

IQVIA's AI advantage creates a competitive moat that grows stronger over time. Every AI model trained improves the next one. Every client interaction generates data that enhances algorithms. Every successful prediction builds trust that attracts more clients. It's a virtuous cycle competitors cannot replicate without IQVIA's data foundation.

The initial AI solutions from this partnership are expected to reach the market within the calendar year. But this is just the beginning. As AI capabilities expand, IQVIA's role evolves from service provider to intelligence partner, embedded so deeply in pharmaceutical operations that separation becomes unthinkable.

Challenges and Responsibilities

With great power comes great responsibility. IQVIA is committed to using artificial intelligence responsibly, with AI-powered capabilities built on best-in-class approaches to privacy, regulatory compliance and patient safety. This commitment isn't just ethical—it's existential. A single privacy breach or biased algorithm could destroy decades of trust.

The company faces technical challenges too. Healthcare data is notoriously messy, with different standards across countries, inconsistent coding, and massive volumes. Training AI on this data requires sophisticated cleaning, standardization, and validation processes that IQVIA has spent years perfecting.

The Future of Healthcare Intelligence

Everything we do in our industry ultimately has an impact on patients, so it's imperative that we deliver AI that's built on a foundation of unparalleled data, expertise, and trust. With IQVIA Healthcare-grade AI®, we're building on our rich history of deploying AI to connect the right data, technology, and expertise to address the unique needs of each challenge we help our customers solve.

The vision is ambitious: AI that doesn't just analyze but anticipates, doesn't just report but recommends, doesn't just process but truly understands healthcare. It's a future where drug development accelerates from decades to years, where treatments are personalized to individual genetics, where healthcare becomes predictive rather than reactive.

IQVIA isn't just participating in this AI revolution—it's leading it. With unmatched data, deep domain expertise, and now cutting-edge AI capabilities, the company is positioned to define how artificial intelligence transforms healthcare. As we'll see in the next section, even this technological leadership faces challenges that test IQVIA's adaptability and resilience.

IX. Recent Challenges & Strategic Responses

The path from $14 billion to $15 billion in revenue should have been straightforward for a company of IQVIA's caliber. Instead, 2024 became a masterclass in navigating industry turbulence. The company faced significant challenges in 2024 due to the Inflation Reduction Act, leading to delayed customer decision-making and reduced discretionary spending. IQVIA Holdings Inc (NYSE:IQV) experienced a high level of cancellations, nearly 50% higher than the average of the previous three years.

The IRA Disruption: Unintended Consequences

The Inflation Reduction Act's drug pricing provisions sent shockwaves through the pharmaceutical industry that reverberated directly to IQVIA. While the legislation aimed to reduce drug costs for Medicare beneficiaries, its impact on pharmaceutical R&D decisions was immediate and severe. Large pharmaceutical companies began reassessing their entire portfolios, questioning which drugs to advance and which to abandon.

In total, large pharmaceutical companies spent more than $161 billion on R&D efforts in 2023, indicating an increasingly competitive global marketplace. But the IRA changed the calculus. Drugs that might have been profitable under previous pricing regimes suddenly looked marginal. The result: a wave of trial cancellations and delays that hit IQVIA's R&DS segment particularly hard.

The R&D Solutions segment saw a decline in revenue, down 1.3% reported and 1% at constant currency for the fourth quarter. This might seem modest, but for a business accustomed to steady growth, it represented a significant disruption. More concerning was the forward-looking impact—pharmaceutical companies weren't just canceling current trials but delaying decisions on future programs.

COVID's Long Shadow

While the acute phase of the pandemic has passed, its effects continue to ripple through IQVIA's business. Excluding all COVID-related work growth in constant currency in R&DS was over 5%. The company faces a $100 million COVID revenue stepdown in 2025, entirely in R&DS, creating a significant headwind to reported growth.

But the COVID challenge goes beyond declining revenues. The pandemic fundamentally changed how clinical trials are conducted, accelerating the adoption of decentralized trials and remote monitoring. While IQVIA was well-positioned for this shift, the transition created operational complexity and required significant investment in new capabilities.

The pandemic also distorted year-over-year comparisons, making underlying business trends harder to discern. Was the slowdown in traditional trials due to COVID disruptions or structural changes in pharmaceutical spending? These questions complicated investor communications and strategic planning.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube