Samsara: The Connected Operations Story

I. Introduction & The Big Picture

Picture this: It's 2015, and while Silicon Valley obsesses over consumer apps and social networks, two MIT engineers are sitting in a nondescript office, sketching out plans for technology that would power garbage trucks, construction sites, and refrigerated trailers. Not exactly the sexiest pitch deck material. Yet today, Samsara commands a market cap north of $20 billion, generates over $1.3 billion in annual recurring revenue, and has become the digital nervous system for organizations that literally keep the world running—from the trucks delivering your Amazon packages to the utilities maintaining your power grid.

The company trades on the NYSE under the ticker "IOT"—a wonderfully literal choice that signals exactly what they do: Internet of Things for the physical world. But Samsara's story isn't just about sensors and software. It's about two founders who already had their exit—a $1.2 billion sale to Cisco—and could have retired to become venture capitalists or angel investors. Instead, Sanjit Biswas and John Bicket chose to tackle an even bigger challenge: digitizing the operations of industries that technology had largely ignored.

The hook that makes Samsara fascinating isn't just the numbers, though they're impressive: 39% year-over-year growth, over 2,300 customers paying more than $100,000 annually, and a recent milestone of positive adjusted free cash flow. It's that they've built this empire by focusing on what Biswas calls "the organizations that keep our world running and yet have been overlooked by the technology industry." These aren't sexy SaaS startups or tech giants—they're trucking companies, construction firms, utilities, and municipalities. The unglamorous backbone of the economy.

What we're about to explore is a masterclass in second-time founder execution, platform timing, and the power of solving boring but massive problems. We'll trace the journey from an MIT research project that became Meraki, through its acquisition by Cisco, to the founding of Samsara and its evolution into what might become the Salesforce of physical operations. Along the way, we'll unpack the strategic decisions, the near-death experiences during COVID, and the aggressive bets on AI and computer vision that have positioned Samsara at the intersection of several massive trends.

This is also a story about patience and conviction. While other IoT companies rushed to build broad platforms hoping something would stick, Samsara started narrow—really narrow—with vehicle gateways for trucking companies. They resisted the temptation to be everything to everyone, instead following a disciplined land-and-expand strategy that would make any enterprise software executive jealous. The result? They've built switching costs so high that their net retention rate consistently exceeds 115%, meaning existing customers not only stick around but spend significantly more each year.

But perhaps most intriguingly, this is a story about timing. The founders launched Samsara just as several trends converged: cellular connectivity became ubiquitous and cheap, computer vision moved from research labs to production, and industries facing labor shortages became desperate for efficiency gains. They caught the wave at exactly the right moment—not too early like many IoT pioneers who crashed and burned in the 2000s, and not too late to establish themselves as the platform of record.

So buckle up. We're about to dive deep into how two engineers built a company that's digitizing the physical world, one fleet, one construction site, one factory at a time. And we'll explore whether Samsara can maintain its torrid growth while navigating the challenges of being a public company in an increasingly competitive market. The road ahead isn't without potholes—pun intended—but if history is any guide, betting against Biswas and Bicket has rarely been profitable.

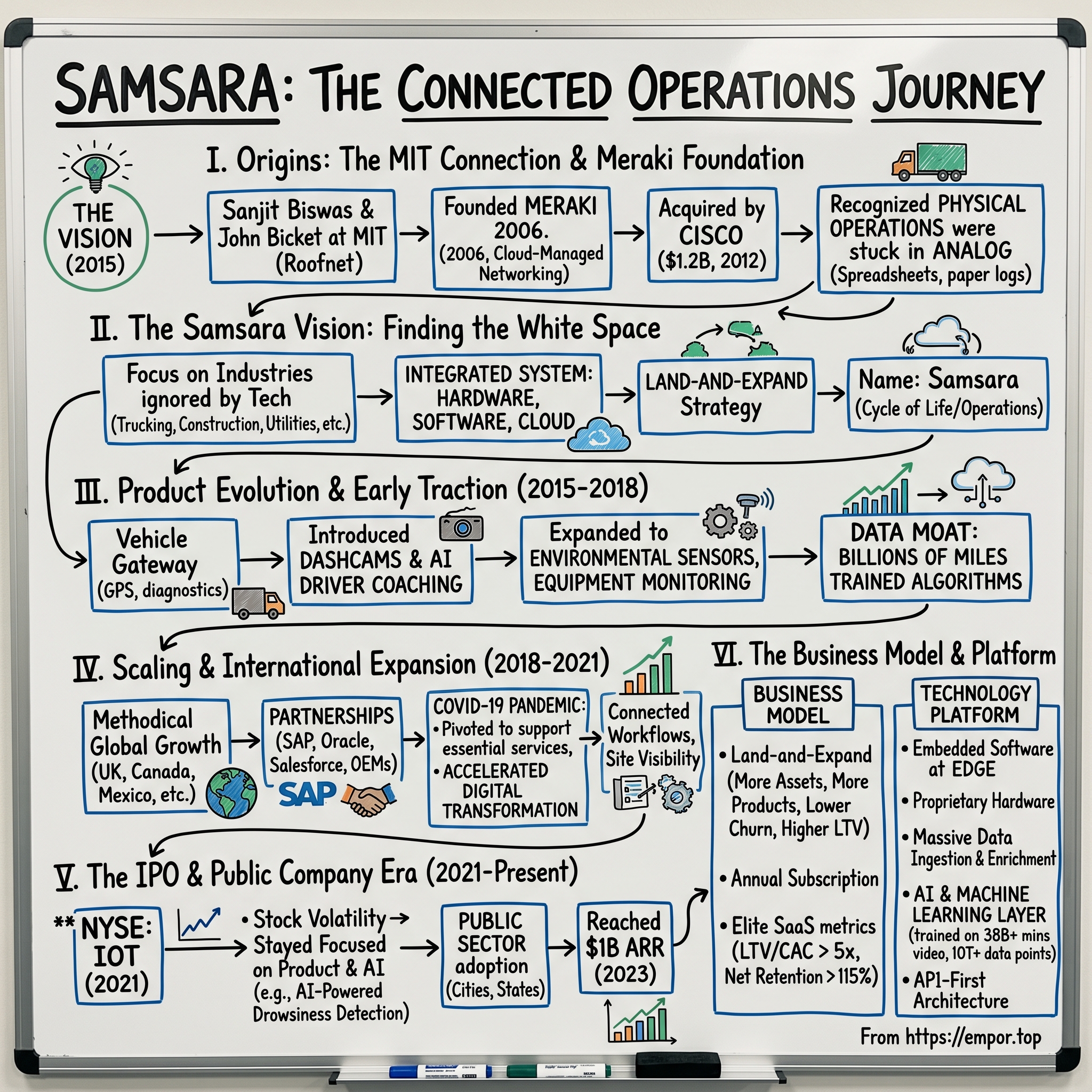

II. Origins: The MIT Connection & Meraki Foundation

The year is 2003, and in a cramped MIT computer science lab, two graduate students are hunched over circuit boards and routers, trying to solve a problem that seems almost quaint by today's standards: how to provide cheap, reliable internet access to underserved communities. Sanjit Biswas, a cerebral engineer with a knack for systems thinking, and John Bicket, a networking wizard who could make packets dance, were working on something called Roofnet—a mesh networking project that would let anyone share their internet connection with neighbors wirelessly.

This wasn't their first collaboration. The two had bonded over late-night coding sessions and a shared frustration with how complicated networking equipment was. Enterprise networking in the early 2000s was dominated by Cisco's command-line interfaces and required specialized training just to configure a simple access point. Biswas and Bicket thought there had to be a better way. Their Roofnet project, which eventually covered much of Cambridge, Massachusetts, proved that mesh networking could work at scale. But more importantly, it planted the seed for something bigger.

In 2006, armed with their MIT research and a vision for democratizing enterprise networking, they founded Meraki. The name came from a Greek word meaning "doing something with soul, creativity, or love"—a philosophy that would permeate their approach to building products. Along with Hans Robertson, who brought hardware expertise, they set out to build networking equipment that was so simple to use that any IT admin could manage it from anywhere.

The innovation that made Meraki special wasn't just the hardware—it was the cloud management layer. This was 2006, remember. Amazon Web Services had just launched, and the idea of managing physical infrastructure through a web browser was borderline heretical in enterprise IT. Yet Biswas and Bicket built exactly that: a dashboard where you could configure access points, switches, and security appliances from anywhere in the world. No command line. No specialized training. Just point, click, deploy.

The growth was explosive. Meraki doubled revenues every year, expanding from wireless access points to switches, security appliances, and eventually mobile device management. They raised $80 million from investors including Sequoia Capital and grew to over 500 employees. By 2012, they were processing over 2 billion network requests per day and had deployed equipment in over 10,000 networks across 100 countries.

Then came the offer they couldn't refuse. In November 2012, Cisco announced it would acquire Meraki for $1.2 billion in cash. For a company that was less than seven years old, it was a stunning exit. But what happened next was even more unusual. Instead of taking their money and running, Biswas and Bicket stayed. They integrated Meraki into Cisco, grew the team to over 700 employees, and turned it into one of Cisco's fastest-growing and most profitable business units.

The Meraki team had a front-row seat to Cisco's vast enterprise customer base, and they noticed something interesting. While IT infrastructure was becoming increasingly sophisticated and cloud-managed, the physical operations side of these businesses—their vehicle fleets, manufacturing equipment, facilities—remained largely analog. Spreadsheets. Phone calls. Clipboard inspections. Paper logs. It was as if the digital transformation had stopped at the server room door.

By 2015, after successfully scaling Meraki within Cisco and proving that their vision for cloud-managed infrastructure could work at enterprise scale, Biswas and Bicket were ready for their second act. They had learned invaluable lessons: the power of starting simple and expanding, the importance of beautiful user interfaces in enterprise software, and most crucially, that combining hardware, software, and cloud services into an integrated system could create magical user experiences.

They also had something most founders don't: pattern recognition from having done it before. They knew how to hire, how to scale, how to manage the delicate balance between product simplicity and feature completeness. They understood the enterprise sales cycle, the importance of channel partnerships, and the value of patient capital. All of this would prove invaluable in their next venture.

The decision to leave Cisco wasn't easy. They were running a successful business unit, had golden handcuffs in the form of retention packages, and enjoyed the resources of a $150 billion company. But the itch to build something new, something even bigger, was too strong to ignore. They saw an opportunity in physical operations that was orders of magnitude larger than enterprise networking. And this time, they wouldn't be starting from zero. They had credibility, capital, and most importantly, clarity on what they wanted to build. The foundation was set for Samsara.

III. The Samsara Vision: Finding the White Space (2015)

In early 2015, Biswas and Bicket found themselves in a series of conversations that would define their next decade. They were meeting with operations managers at trucking companies, construction firms, and utilities—industries that collectively represented trillions in GDP but had been largely ignored by Silicon Valley. One conversation stood out: a fleet manager at a mid-sized trucking company showed them his "technology stack"—a cluttered desk covered in paper logs, Excel printouts, and three different GPS tracking systems that didn't talk to each other. "We're running a $100 million operation," he said, "and our most sophisticated tool is a spreadsheet I built myself."

This was the white space they had been looking for. While consumer technology had revolutionized how we communicate, shop, and entertain ourselves, and enterprise software had transformed back-office operations, the physical operations that literally keep the world running were stuck in the dark ages. These companies weren't behind because they were luddites—they simply hadn't been offered solutions built for their unique needs.

The insight that crystallized Samsara's founding thesis was deceptively simple: "No one was building products the way we did at Meraki, by combining hardware, software and cloud into an easy-to-use system." The IoT industry at the time was fragmented between hardware companies that made sensors, software companies that built analytics platforms, and systems integrators who charged millions to stitch it all together. Nobody was delivering an integrated, plug-and-play solution that just worked.

They chose the name Samsara deliberately. In Sanskrit, it means the eternal cycle of life, death, and rebirth—a fitting metaphor for second-time founders starting fresh, but also for the continuous, cyclical nature of physical operations. Trucks constantly moving goods, equipment perpetually cycling through job sites, the endless flow of materials through supply chains. The name signaled both philosophical depth and practical focus on continuous, repeating processes.

The funding came quickly. Marc Andreessen had watched Meraki's journey from afar and immediately understood the vision. In April 2015, Andreessen Horowitz led a $25 million Series A, with Marc himself joining the board. His presence sent a signal to the market: this wasn't just another IoT startup; this was a platform play with the potential to transform entire industries.

But raising money was the easy part. The hard part was deciding where to start. The physical operations space was vast—transportation, manufacturing, energy, construction, agriculture, utilities. Each had its own unique requirements, regulations, and buying patterns. The temptation was to build a horizontal platform that could serve everyone, but they had learned from Meraki the power of starting narrow and expanding methodically.

After months of customer research, they made a crucial decision: they would start with fleet management, specifically focusing on small and mid-sized trucking companies. Why trucking? First, the pain was acute—regulations like the ELD mandate were forcing digitization. Second, the ROI was clear and measurable—fuel savings, safety improvements, compliance avoided. Third, and perhaps most importantly, vehicles were mobile endpoints that generated rich, continuous data streams perfect for showcasing the power of an integrated IoT platform.

The initial product wasn't revolutionary on paper—a vehicle gateway that plugged into the diagnostic port and tracked location, speed, and engine diagnostics. But the execution was everything. While competitors required professional installation, complex configuration, and clunky software, Samsara's gateway could be installed by drivers in minutes and started streaming data immediately to an intuitive cloud dashboard. They obsessed over tiny details: the magnetic mounting system, the cellular antenna placement, the way data visualized on the dashboard.

Within months of launching, they discovered something interesting. Customers kept asking for more. Could you add temperature sensors for our refrigerated trucks? What about cameras to see what really happened in that accident? Can you help us with driver coaching? Rather than seeing these as distractions, Biswas and Bicket recognized them as the roadmap to building a platform. Each request revealed a new pain point, a new opportunity to expand the relationship.

By the end of 2015, they had their first dozen customers and a clear product-market fit signal: customers were calling them, not the other way around. Word was spreading through the tight-knit trucking community that there was finally a technology company that understood their needs. The foundation was set, but the real test would be whether they could scale without losing the simplicity and focus that made them special. As they would soon learn, building for physical operations brought challenges that made enterprise networking look simple by comparison.

IV. Product Evolution & Early Traction (2015–2018)

The first Samsara Vehicle Gateway looked deceptively simple—a small black box about the size of a deck of cards. But inside that unassuming device was years of hard-won wisdom about how to build hardware that could survive in the harsh environment of commercial vehicles. It had to work in Phoenix summers and Minneapolis winters, survive the vibrations of long-haul trucks, and maintain cellular connectivity in remote areas. The team spent months testing prototypes, literally throwing them against walls and submerging them in water to ensure reliability.

The gateway launched in late 2015 with a focused feature set: real-time GPS tracking, engine diagnostics, and fuel consumption monitoring. But what really set it apart was the software layer. While competitors offered cluttered interfaces that looked like they were designed in the 1990s, Samsara's dashboard was clean, intuitive, and—critically—fast. Data appeared in real-time, not with the 5-10 minute delays common in the industry. Fleet managers could finally see their entire operation on a single screen.

The first major product evolution came from an unexpected source: customer support tickets. In early 2016, several customers reported accidents where drivers claimed they weren't at fault, but had no way to prove it. The team's response was to develop a dashcam that integrated seamlessly with the Vehicle Gateway. But instead of just recording video, they added intelligence: the camera could detect harsh events like sudden braking or collisions and automatically upload relevant footage to the cloud. No more scrolling through hours of video to find an incident.

This was where Samsara's integrated approach really shone. Competitors sold standalone dashcams that required separate installation, different software, and usually stored video locally on SD cards that could mysteriously "disappear" after accidents. Samsara's camera plugged directly into their gateway, used the same cellular connection, and uploaded everything to the same dashboard. It was elegant in its simplicity.

The introduction of cameras unlocked something unexpected: driver coaching opportunities. Fleet managers started noticing patterns in the footage—drivers texting, eating, or looking drowsy. In response, Samsara added an inward-facing camera option with AI that could detect distracted driving behaviors in real-time. This was controversial—many drivers saw it as Big Brother surveillance—but safety-conscious fleets saw dramatic reductions in accidents. One early customer reported a 50% decrease in accidents within six months of deploying the cameras.

By mid-2017, Samsara had expanded beyond pure fleet tracking into adjacent areas. They launched environmental monitoring sensors for refrigerated trucks, allowing companies to prove their cold chain was never broken. They added equipment monitoring for construction companies, tracking usage hours and location of expensive assets like excavators and generators. Each new product followed the same playbook: start simple, integrate deeply, expand based on customer feedback.

The platform approach was working. Customers who started with basic GPS tracking were adding cameras, then sensors, then driver apps. The average customer was using 2.3 products by the end of 2017, up from 1.2 just a year earlier. This land-and-expand motion drove net retention rates above 115%, meaning the cohort of customers from one year would be paying 15% more the following year even accounting for churn.

Customer acquisition was equally impressive. While enterprise software companies typically required expensive sales teams and long sales cycles, Samsara was seeing something unusual: organic growth through word-of-mouth. Trucking companies talk to each other at truck stops, industry conferences, and online forums. When one company saw their competitor getting real-time visibility into operations, they wanted it too. The product was essentially selling itself.

The traction caught Silicon Valley's attention. In March 2018, Samsara raised a $100 million Series C that valued the company at over $1 billion, officially making it a unicorn. The round was led by existing investor Andreessen Horowitz, with participation from General Catalyst. But unlike many unicorns that burned cash in pursuit of growth, Samsara was remarkably capital efficient. They were growing over 100% year-over-year while maintaining reasonable burn rates.

The key to this efficiency was their customer-centric development process. Instead of building features they thought customers might want, they built exactly what customers were asking for. Every product manager spent time riding along in trucks, visiting construction sites, and sitting in dispatch offices. This wasn't just lip service to customer obsession—it was baked into the company culture. Engineers had metrics not just on system uptime but on customer satisfaction scores.

By the end of 2018, Samsara had over 5,000 customers and was processing billions of data points daily. They had expanded from their initial focus on trucking to serve construction companies, utilities, and even local governments. The platform was proving its versatility—the same core technology that tracked delivery trucks could monitor school buses, garbage trucks, and emergency vehicles.

But perhaps the most important development during this period was less visible: the data moat they were building. Every mile driven, every harsh braking event, every minute of video footage was training their algorithms to be smarter. They were learning what normal looked like across thousands of different operations, which would prove invaluable as they moved into more sophisticated AI applications. The foundation was set for explosive growth, but first, they would have to navigate the challenge every successful startup faces: scaling without losing their soul.

V. Scaling & International Expansion (2018–2021)

In the summer of 2018, Samsara faced a classic startup dilemma. They had product-market fit in the United States, customers were pulling the product faster than they could onboard them, and investors were throwing money at them. The temptation was to pour gasoline on the fire—hire aggressively, expand everywhere, grow at all costs. But Biswas and Bicket had seen this movie before. They knew that undisciplined scaling was where good companies went to die.

Their approach to international expansion was methodical, almost cautious by Silicon Valley standards. Instead of launching in 20 countries simultaneously, they picked one: the United Kingdom. Why the UK? Similar regulatory environment to the US, English-speaking, and most importantly, customers were already asking for it. Several US-based logistics companies had UK operations and wanted to standardize on Samsara globally. Following customer pull rather than pushing into new markets—classic Samsara.

The London office opened in September 2018 with just five people. Within months, they had signed major UK brands and proved the model could work internationally. But they discovered something interesting: while the core platform translated well, each market had unique requirements. UK companies needed tachograph integration for compliance. European markets required GDPR-compliant data handling. These weren't just features to add; they required deep understanding of local regulations and business practices.

The expansion continued deliberately: Canada in early 2019, then Mexico, leveraging NAFTA trade routes where customers already operated cross-border. The first East Coast office in Atlanta opened in mid-2019, recognizing that selling to traditional industries required local presence. You couldn't convince a construction company in Georgia to buy enterprise software from a salesperson in San Francisco who'd never set foot on a job site.

Meanwhile, the product suite was expanding beyond vehicles into what Samsara called "Connected Operations"—a broader vision for digitizing all physical operations. They launched Equipment Monitoring for tracking non-vehicle assets, Site Visibility for monitoring facilities and yards, and Connected Workflows for digitizing paper processes. Each expansion followed the same pattern: start with a specific customer pain point, build a simple solution, then expand based on feedback.

The partnership ecosystem became crucial during this period. Samsara integrated with major enterprise systems like SAP, Oracle, and Salesforce, allowing customers to pipe IoT data directly into their existing workflows. They partnered with insurance companies who offered discounts to fleets using Samsara's safety features. They even worked with OEMs like Ford and Navistar to pre-install compatibility. The platform was becoming sticky not just through its own features but through its connections to everything else in the enterprise stack.

Then came March 2020. COVID-19 hit, and suddenly the world shut down. For a company focused on physical operations—trucking, construction, field services—this could have been catastrophic. Fleet miles plummeted. Construction projects halted. Samsara's customer base was directly in the crosshairs of the pandemic's economic impact.

The company's response revealed its operational maturity. Within days, they implemented a hiring freeze and reduced discretionary spending. But critically, they didn't panic. They kept their entire engineering team and customer support staff, betting that their customers would need them more than ever during the crisis. They rolled out features to help customers adapt: contact tracing for driver interactions, sanitation verification workflows, and route optimization for the suddenly crucial last-mile delivery sector.

The bet paid off. While some sectors like passenger transportation struggled, others exploded. E-commerce drove unprecedented demand for delivery fleets. Construction resumed quickly as an essential service. Food and beverage companies needed cold chain monitoring more than ever. By the third quarter of 2020, Samsara was growing again, and growing fast. They ended the year with nearly $400 million in ARR, up from $250 million at the start of 2020.

The pandemic also accelerated digital transformation in industries that had been resistant to change. Companies that had delayed IoT adoption for years suddenly needed real-time visibility into their operations. A construction company executive told them: "COVID made us realize we were flying blind. We needed to know where every piece of equipment was, who was using it, and whether our sites were compliant with safety protocols. Samsara gave us that overnight."

International expansion continued even during the pandemic, with offices opening in Paris, Amsterdam, and Munich in 2021. But perhaps more interesting than geographic expansion was the vertical depth they were achieving. They weren't just selling to more companies; they were becoming more embedded in the ones they had. Customers that started with 10 vehicles were expanding to their entire fleet. Companies that began with GPS tracking were adding cameras, sensors, and workflow automation.

By mid-2021, Samsara had over 20,000 customers and was approaching $500 million in ARR. They had weathered the pandemic, expanded internationally, and broadened their platform—all while maintaining the disciplined execution that defined them. The foundation was set for the next chapter: going public. But taking a company public during one of the most volatile market periods in history would require nerves of steel and perfect timing.

VI. The IPO & Public Company Era (2021–Present)

The Samsara S-1 dropped on November 19, 2021, and it was a revelation. While most of Silicon Valley had heard of the company, few understood the scale they had achieved. The numbers were staggering: $378 million in ARR growing 97% year-over-year, 21,000 customers, and most remarkably, founders who still owned over 50% of the company despite raising hundreds of millions in venture capital. Biswas and Bicket had maintained control through dual-class shares and disciplined dilution management—a masterclass in founder-friendly capitalization.

The IPO roadshow happened during one of the strangest periods in market history. The Fed was printing money, tech valuations were at all-time highs, and investors were desperate for growth stories. But Samsara wasn't just another money-losing unicorn riding the wave. They had a clear path to profitability, improving unit economics, and most importantly, they were selling to the real economy—trucking companies, construction firms, utilities—not other tech companies.

On December 15, 2021, Samsara began trading on the NYSE under the ticker "IOT." The stock opened at $24.41, well above the $23 IPO price, valuing the company at $11.5 billion. They raised $805 million, selling 35 million shares, with strong demand from institutional investors who understood the long-term potential of digitizing physical operations. The first day ended with the stock up 17%, a strong debut in an increasingly volatile market.

But the honeymoon was short. By January 2022, the tech selloff had begun. The Fed signaled rate hikes, inflation spiked, and suddenly growth at any cost was out of fashion. Samsara's stock, along with most recent tech IPOs, got crushed. By May 2022, it was trading below $10, less than half the IPO price. The financial media was brutal, lumping Samsara in with other "pandemic darlings" that had lost their luster.

What happened next separated Samsara from the pack. While other companies panicked—laying off staff, cutting R&D, desperately trying to show profitability—Samsara stuck to their plan. They continued investing in product development, particularly in AI and computer vision. They kept hiring engineers, though more selectively. Most importantly, they maintained their customer-first focus, knowing that retention and expansion were more important than new logo acquisition in a downturn.

The discipline showed in the numbers. Despite the macro headwinds, Samsara continued growing at 40%+ rates while improving margins. They reached $750 million in ARR by the end of fiscal 2023, then crossed the magical $1 billion mark in December 2023. This wasn't just a vanity metric—it proved that digitizing physical operations wasn't a nice-to-have but a necessity, even in tough economic times.

The product innovation during this period was remarkable. In 2023, they launched AI-powered Drowsiness Detection, trained on 38 billion minutes of video footage—one of the largest real-world computer vision datasets ever assembled. The system could detect micro-sleeps and alert drivers before accidents happened. One customer reported preventing three likely fatal accidents in the first month of deployment. This wasn't theoretical AI; it was AI saving lives.

The international expansion accelerated post-IPO, with offices opening in Mexico City, Poland, and Tokyo. But more interesting than geographic expansion was their push into new verticals. They signed major wins in passenger transit (city bus systems), education (school districts), and healthcare (medical equipment tracking). The platform was proving its versatility beyond the initial trucking focus.

Public sector adoption became a major growth driver. The cities of New Orleans, Boston, and Houston standardized on Samsara for their municipal fleets. The states of New Jersey and Tennessee deployed it across thousands of vehicles. These weren't just big deals financially; they were validation that Samsara had achieved enterprise-grade reliability and security. When a city trusts you with their emergency vehicles, you know you've arrived.

The 2024 launch of Asset Tags—Bluetooth-based trackers for high-value equipment—showed Samsara's continued innovation. While the technology wasn't groundbreaking (Apple had popularized it with AirTags), the integration was. Asset Tags leveraged Samsara's existing vehicle network as mobile gateways, creating a mesh network that could track equipment across job sites without requiring cellular connectivity for each asset. Elegant, practical, and perfectly aligned with customer needs.

By late 2024, Samsara had transformed from a scrappy startup to a legitimate enterprise platform. They had 2,303 customers paying over $100,000 annually, up from 1,663 the year before. The public markets had finally recognized the value, with the stock recovering to trade above $40, giving the company a market cap exceeding $20 billion. The volatility of the public markets had tested them, but they emerged stronger, more focused, and with a clear path to long-term value creation.

The public company era also brought new challenges. Quarterly earnings calls meant constant scrutiny. Competitors could see their metrics and strategy. Employees with stock options watched the daily fluctuations. But Biswas and Bicket managed it with characteristic calm, focusing on long-term value over short-term stock movements. As Biswas said on an earnings call: "We're building a generational company. Quarterly noise doesn't change that mission."

VII. The Business Model & Go-to-Market Strategy

At the heart of Samsara's success lies a deceptively simple philosophy, articulated by Biswas in an early interview: "Make a few people really, really happy, rather than make something that's kind of useful for a tonne of people." This focus on depth over breadth shaped every aspect of their go-to-market strategy and created a business model that venture capitalists dream about but rarely see executed successfully.

The land-and-expand motion at Samsara is a thing of beauty. A typical customer journey might start with a small trucking company buying 10 Vehicle Gateways to track their delivery trucks. Six months later, they add dashcams after an accident dispute. A year in, they're using driver apps for electronic logging. By year two, they've added temperature sensors for refrigerated trucks and Equipment Monitoring for their forklifts. What started as a $10,000 annual contract has grown to $50,000, and the customer can't imagine operating without Samsara.

The numbers tell the story: customers using multiple products have 30% lower churn rates and generate 2.5x the revenue of single-product users. By late 2024, the average enterprise customer was using 3.7 different Samsara products, up from 2.1 just three years earlier. This isn't accidental—the entire platform is designed to make adding new capabilities as frictionless as possible. Same login, same dashboard, same billing. The marginal cost of trying a new product is essentially zero.

The sales motion evolved from founder-led selling to a sophisticated multi-channel approach. In the early days, Biswas and Bicket personally sold to the first hundred customers, learning their pain points and refining the pitch. As they scaled, they built three distinct sales channels: inside sales for smaller accounts, field sales for enterprise deals, and increasingly, a partner channel for international and vertical markets. The beauty is that each channel reinforces the others—partners bring leads that inside sales qualifies for field sales to close.

Customer segmentation at Samsara is remarkably sophisticated. They've identified that companies with 20-200 vehicles represent the sweet spot—large enough to need sophisticated tools but small enough to make decisions quickly. These mid-market customers don't have the IT resources to build their own solutions or integrate multiple point products, making Samsara's integrated platform invaluable. The proof is in the penetration: over 40% of for-hire trucking companies in this segment use Samsara.

The pricing model is elegant in its simplicity: annual subscriptions based on the number of assets monitored, with additional charges for premium features like AI-powered safety coaching or advanced analytics. This aligns pricing with value—the more assets you track, the more value you get, the more you pay. Importantly, they've resisted the temptation to nickel-and-dime customers. API access, unlimited users, and basic reporting are all included, reducing friction for expansion.

The public sector strategy deserves special attention. While most B2B software companies struggle with government sales—long cycles, complex procurement, tight budgets—Samsara cracked the code. They focused on ROI metrics that resonated with budget-conscious municipalities: fuel savings, reduced accidents, overtime reduction. They made pricing transparent and predictable, crucial for government budgeting. Most cleverly, they enabled success stories to spread organically—when one city saw another reducing accidents by 40%, they wanted in.

Key customer wins read like a who's who of American industry. Ford uses Samsara across their commercial fleet. DHL tracks packages and vehicles globally. Sysco monitors their food distribution network. XPO Logistics manages their complex supply chain operations. Each of these logos doesn't just represent revenue; they represent validation and create a flywheel effect. When the world's largest companies trust you with their operations, smaller companies follow.

The customer success motion is where Samsara really differentiates. They don't just sell software and disappear. Every customer gets an onboarding specialist who ensures successful deployment. Quarterly business reviews track ROI metrics. A dedicated support team responds to issues in minutes, not hours. This isn't cheap—customer success represents a significant portion of operating expenses—but it drives the net retention rates that make the business model work.

The competitive moat is multi-layered. First, there's the data network effect—the more vehicles and equipment on the platform, the better the AI models become. Second, switching costs are enormous—not just in terms of hardware replacement but in retraining staff and rebuilding workflows. Third, the integration depth makes Samsara sticky. When your IoT platform is piping data into your ERP, transportation management system, and maintenance software, ripping it out becomes almost impossible.

The unit economics have improved dramatically over time. Customer acquisition cost (CAC) payback periods have dropped from 24 months in 2018 to under 15 months by 2024. Gross margins have expanded from 60% to over 75% as hardware costs decreased and software revenue mix increased. The lifetime value to CAC ratio now exceeds 5x for enterprise customers, putting Samsara in elite company among SaaS businesses.

But perhaps the most impressive aspect of the business model is its resilience. During COVID, when vehicle miles dropped 40%, Samsara's revenue kept growing. Why? Because the value proposition—visibility, safety, efficiency—becomes even more critical during uncertainty. Companies couldn't afford to operate blindly when margins were tight. This countercyclical dynamic provides a buffer that pure software companies lack. The model isn't just working; it's getting stronger over time.

VIII. Technology & Platform Architecture

Under the hood of Samsara's platform lies one of the most sophisticated IoT architectures ever built for physical operations. The Connected Operations Cloud is a platform that enables organizations that depend on physical operations to harness Internet of Things (IoT) data to develop actionable insights and improve their operations. But calling it just an "IoT platform" undersells the technical complexity and elegant design that makes it work at massive scale.

The architecture starts at the edge with Samsara's proprietary hardware—vehicle gateways, cameras, sensors, and asset tags—each running embedded software capable of real-time processing. The platform stack has a localized edge component for gathering vital data, pre-analyzing it (via on-device AI), and using a cellular connection to transmit it to the cloud platform. This edge computing capability is crucial: instead of streaming raw video or sensor data continuously, the devices process information locally and only transmit relevant events, dramatically reducing bandwidth costs and latency.

The data ingestion layer is where things get impressive. Using data points from over 80 billion miles driven annually and 120+ billion API calls, their AI-based solutions are built with — and for — the world's largest and most complex operations. The platform processes this torrent of information through a sophisticated pipeline that cleanses, normalizes, and enriches the data in real-time. Once the data is ingested into the platform, that data is enriched with other data sources (such as maps, routing, and weather info), and is then run through cloud-based AI/ML layers that perform analytics and predictions.

The scale of video processing alone is staggering. Samsara's models are trained on more than 38 billion minutes of video footage to ensure accurate detection. This isn't just stored footage—it's actively analyzed, labeled, and used to train increasingly sophisticated computer vision models. The Drowsiness Detection feature, for instance, doesn't just look for yawning; it considers several behaviors, such as head nodding, slouching, prolonged eye closure, and yawning. An analysis among early adopters found that approximately 77% of drowsy driving events were detected by behaviors other than yawning alone.

The platform's modularity deserves special attention. The platform then evolved over the next 6 years into 5 separate products built upon the same core architecture stack. Each product—Vehicle Telematics, Equipment Monitoring, Site Visibility, Mobile Experience Management, and Apps & Workflows—shares the same underlying infrastructure but exposes different capabilities. This isn't accidental; it's architectural genius. Customers can start with one product and seamlessly add others without integration headaches.

The API-first architecture enables deep integration with enterprise systems. In September 2022, the company added its 200th partner integration on the Samsara App Marketplace. These aren't superficial integrations—they're bi-directional data flows that embed Samsara data directly into ERP systems, transportation management platforms, and maintenance software. The APIs handle billions of calls annually, maintaining sub-second response times even under massive load.

What makes the technology particularly impressive is how it handles the unique challenges of physical operations. Unlike typical SaaS platforms dealing with structured data in controlled environments, Samsara's platform must handle: vehicles moving through cellular dead zones, sensors operating in extreme temperatures, cameras capturing footage in low light conditions, and equipment generating data in proprietary formats. The platform gracefully handles intermittent connectivity, caching data locally and syncing when connections restore.

The AI and machine learning layer represents years of investment and innovation. Samsara's petabyte-scale dataset collects more than 10 trillion data points each year and is used to train AI models that automate workflows, accelerate time to value, and provide personalized, actionable insights for customers. These models power everything from route optimization to predictive maintenance, getting smarter with every mile driven and every hour of equipment operation.

The security architecture is enterprise-grade, with end-to-end encryption, SOC 2 Type II compliance, and granular access controls. Data residency requirements for international customers are handled through regional data centers, ensuring compliance with GDPR and other regulations. The platform maintains 99.9%+ uptime, critical when customers depend on it for real-time operations.

Recent innovations show the platform's continued evolution. The 2024 launch of Asset Tags demonstrates clever system design— The Asset Tag utilizes Bluetooth technology and Samsara's network of cloud-connected devices to track unpowered assets without requiring cellular connectivity for each item. Vehicles act as mobile gateways, creating a mesh network that can track tools and equipment across job sites.

But perhaps the most impressive aspect is what users don't see: the platform's ability to maintain simplicity despite underlying complexity. A fleet manager can log in and immediately understand their operation's status without knowing anything about the terabytes of data being processed behind the scenes. This abstraction of complexity—making the sophisticated appear simple—is the hallmark of great platform architecture. It's what allows a small trucking company and a Fortune 500 enterprise to use the same platform successfully, each getting exactly what they need without complexity they don't.

IX. Financial Analysis & Growth Metrics

The financial story of Samsara reads like a playbook for efficient growth at scale—a rare combination in the world of enterprise software. The top-line numbers are impressive: fiscal 2025 revenue of $1.249 billion, up 33% year-over-year, building on fiscal 2024's $937 million (44% growth) and fiscal 2023's $653 million (52% growth). But it's the underlying unit economics and the path to profitability that reveal the true strength of the business model.

The gross margin evolution tells a story of a maturing platform. Starting in the low 60s when hardware represented a larger portion of revenue, gross margins have steadily expanded to 75-76% as the software mix increased and hardware costs declined through scale and engineering improvements. This isn't just margin expansion for its own sake—it reflects the increasing value customers place on the software and services layer versus the commodity hardware.

The ARR trajectory is even more compelling. The company added over 1,000 core customers in the quarter and also saw its number of customers with annual recurring revenue of $100,000 or more grow to 2,303 as of the end of the quarter, up from 1,663 as of the same time last year. This 38% growth in large customers outpacing overall revenue growth signals that Samsara is successfully moving upmarket while maintaining its mid-market stronghold.

The path to profitability inflection happened faster than many expected. In Q4 fiscal 2024, Samsara posted its first positive non-GAAP operating income of $13.5 million and adjusted free cash flow of $16 million. This wasn't a one-time achievement—the company has maintained positive adjusted free cash flow since, proving that growth and profitability aren't mutually exclusive. The improvement came from disciplined spending, improved sales efficiency, and the natural leverage in the model as the platform scales.

Customer acquisition costs have improved dramatically. CAC payback periods dropped from 24 months in 2018 to under 15 months by 2024, driven by improved sales efficiency and faster time-to-value for customers. The lifetime value to CAC ratio now exceeds 5x for enterprise customers, putting Samsara in the top tier of SaaS metrics. This efficiency allows them to invest aggressively in growth while maintaining a path to profitability.

The net retention rate consistently above 115% is perhaps the most important metric. It means that even if Samsara never added another new customer, the business would still grow 15% annually just from existing customer expansion. This expansion comes from multiple vectors: adding more vehicles or equipment, adopting additional products, and increasing usage of premium features like AI-powered coaching. The beauty is that expansion requires minimal sales cost—customers pull additional products rather than needing to be pushed.

R&D investment remains robust at approximately 25% of revenue, higher than many mature SaaS companies but appropriate given the technical complexity and competitive dynamics. This investment drives the continuous innovation in AI, computer vision, and platform capabilities that maintain Samsara's technical edge. Importantly, R&D efficiency has improved—they're getting more innovation per dollar as the platform matures and they can build on existing infrastructure.

Sales and marketing efficiency deserves special attention. At roughly 35% of revenue, it's in line with best-in-class SaaS companies but remarkable given the complexity of selling to traditional industries. The efficiency comes from the land-and-expand model—it's cheaper to sell a small initial deployment and expand than to sell a large enterprise deal upfront. The channel partnership strategy also helps, with partners bringing qualified leads that close faster and at lower cost.

The balance sheet is fortress-like, with over $1 billion in cash and no debt. This financial strength provides strategic flexibility—they can weather economic downturns, invest countercyclically, and pursue acquisitions without dilution. During the 2022-2023 tech downturn, while competitors pulled back, Samsara continued investing in product and go-to-market, gaining share.

Working capital dynamics are favorable. Customers typically pay annually upfront, providing negative working capital that funds growth. Hardware is increasingly drop-shipped directly from manufacturers, reducing inventory requirements. The combination means that growth actually generates cash rather than consuming it—a rare dynamic in hardware-software businesses.

International expansion is still early but accelerating. International revenue represents less than 15% of total revenue but is growing faster than the overall business. The unit economics in international markets are rapidly improving as they achieve scale and localize go-to-market strategies. Europe, in particular, shows promise with its focus on sustainability and regulatory compliance driving adoption.

The stock-based compensation burden is meaningful at roughly 20% of revenue, but it's declining as a percentage as the business scales. More importantly, it's enabling them to attract world-class talent in a competitive market. The dual-class structure ensures founders maintain control, allowing them to focus on long-term value creation rather than quarterly earnings management.

Looking forward, the financial model has significant room for improvement. Gross margins could expand to 80%+ as software becomes an even larger portion of revenue. Operating margins could reach 20-25% at maturity, in line with best-in-class SaaS companies. The combination of durable growth, expanding margins, and positive cash flow generation creates a powerful compounding machine. While the GAAP losses ($123 million operating loss in the most recent year) grab headlines, the underlying unit economics tell a story of a business that's not just growing but strengthening with scale.

X. Playbook: Lessons for Founders & Investors

The Samsara story offers a masterclass in second-time founder advantages. Biswas and Bicket didn't just bring technical expertise from Meraki—they brought pattern recognition about how to build and scale an enterprise technology company. They knew to start narrow and expand methodically, to obsess over customer experience even in B2B, and most crucially, when to push the accelerator and when to tap the brakes.

The platform timing lesson is profound. As Biswas noted in an early interview: "IoT platforms are really interesting, but to get broadly adopted, you have to build applications on top." Too many IoT companies built platforms hoping others would build the applications. Samsara built both, ensuring customers got immediate value while maintaining platform extensibility. They caught the wave just as cellular connectivity became cheap and ubiquitous, compute power enabled edge processing, and industries faced pressure to digitize. Earlier would have been too expensive; later would have meant entrenched competition.

Building for overlooked markets with massive TAMs is perhaps the most underappreciated aspect of Samsara's strategy. While Silicon Valley chased sexy consumer apps and enterprise software for knowledge workers, Samsara focused on trucking companies, construction firms, and utilities. These industries represent trillions in GDP but had been largely ignored by technology companies. The lack of competition meant less pricing pressure, faster sales cycles, and grateful customers who became evangelists.

The power of founder-led sales in the early days cannot be overstated. Biswas and Bicket personally sold to the first hundred customers, sitting in truck cabs, visiting construction sites, and riding along on delivery routes. This wasn't just about closing deals—it was about deeply understanding customer pain points and building credibility in industries naturally skeptical of Silicon Valley. Even today, with a sophisticated sales organization, the founders regularly meet with customers and prospects.

Product development at Samsara follows a disciplined process of customer collaboration. Every major feature comes from specific customer requests, validated across multiple customers before building. They resist the temptation to build speculative features or chase competitor capabilities. This discipline ensures high adoption rates for new features and prevents feature bloat that could compromise the platform's simplicity.

Managing through market cycles—from COVID to supply chain disruptions to macroeconomic headwinds—revealed the resilience of both the business model and the leadership team. While others panicked and cut deeply, Samsara made surgical adjustments while continuing to invest in critical areas. They understood that downturns are when market share is won, not by being reckless but by being strategically aggressive when competitors retreat.

Capital efficiency while maintaining growth is perhaps Samsara's most impressive achievement. They've raised significant capital but used it judiciously, achieving more with less than most venture-backed companies. The key was focusing on sustainable unit economics from day one rather than growth at any cost. Every dollar of burn had to drive measurable ROI, whether in product development, customer acquisition, or market expansion.

The cultural elements are subtle but crucial. Samsara maintains a builder culture despite being a public company with thousands of employees. Engineers still ride in trucks, product managers visit job sites, and customer feedback drives the roadmap. They've avoided the bureaucracy that typically comes with scale by maintaining small, autonomous teams with clear ownership and metrics.

The acquisition strategy—or lack thereof—is notable. Unlike many successful companies that grow through M&A, Samsara has remained focused on organic growth. They've made small talent acquisitions but avoided large deals that could disrupt culture or distract from core execution. This discipline requires confidence that you can build better than you can buy—confidence earned through consistent execution.

Network effects in the business are subtle but powerful. Every vehicle and piece of equipment on the platform makes the AI models smarter. Every integration makes the platform stickier. Every customer success story makes the next sale easier. These compound over time, creating increasing returns to scale that make it harder for competitors to catch up.

The lesson on pricing strategy is instructive. Rather than complex enterprise pricing with hidden fees and long negotiations, Samsara kept pricing simple and transparent: pay for what you monitor, get unlimited users and basic features included. This reduced sales friction and made expansion natural—add more assets, pay more, simple. No painful repricing negotiations that poison customer relationships.

For investors, Samsara demonstrates the power of betting on large, underpenetrated markets with clear digitization catalysts. The combination of massive TAM, strong unit economics, and proven execution creates the conditions for sustained, profitable growth. The dual-class structure and founder control might concern some governance purists, but it's enabled long-term thinking that's created tremendous value.

Perhaps the most important lesson is about solving unglamorous problems. Samsara didn't try to change the world with revolutionary technology—they applied proven technology to practical problems. They made trucks safer, equipment more efficient, and operations more visible. It's not sexy, but it's valuable. And in the end, creating real value for real customers in the real economy is the ultimate playbook for building an enduring company.

XI. Competition & Market Dynamics

The competitive landscape in connected operations and fleet management is fragmented, complex, and rapidly evolving. Legacy telematics providers like Geotab, Verizon Connect, and Trimble have been in the market for decades, built on older technology stacks and business models. New entrants like Motive (formerly KeepTruckin) and Convoy are attacking from different angles. Yet Samsara has managed to carve out a leadership position by threading the needle between these various competitive threats.

The legacy players brought scale and customer relationships but suffered from technical debt. Their platforms were built in the pre-cloud era, requiring complex on-premise installations and clunky user interfaces. Many grew through acquisition, resulting in a patchwork of poorly integrated products. Their enterprise sales motions, while effective for large deals, couldn't compete with Samsara's product-led growth and land-and-expand strategy. Most critically, they viewed hardware as the product rather than a means to deliver software value—a fundamental misunderstanding of where the industry was heading.

New entrants posed a different challenge. Motive, Samsara's closest competitor, started with electronic logging devices (ELDs) and expanded into broader fleet management. They raised significant capital and grew aggressively, but their focus on owner-operators and small fleets limited their enterprise potential. Other startups attacked specific verticals or use cases but lacked the platform breadth to compete for larger customers. The capital requirements to build hardware, software, and go-to-market capabilities simultaneously created a significant barrier to entry.

Why did Samsara succeed where other IoT providers failed? The answer lies in their narrow initial focus driving mass adoption rather than building broad platforms hoping something would stick. While competitors tried to be everything to everyone, Samsara obsessed over fleet management for mid-sized trucking companies. Only after dominating that segment did they expand to adjacent verticals and use cases. This focused approach created a virtuous cycle: deep product-market fit drove word-of-mouth growth, which generated cash for R&D, which funded expansion into new areas.

The vertical versus horizontal expansion debate is fascinating. Samsara chose horizontal expansion—taking their platform to new industries rather than going deeper into transportation. This strategy leveraged their core platform capabilities while diversifying revenue sources. Competitors who went vertical, building deep transportation-specific features, found themselves trapped in a single industry with limited growth potential. Samsara's approach required more product flexibility but created a larger addressable market.

International dynamics add another layer of complexity. Each geography has local competitors with regulatory expertise and customer relationships. In Europe, companies like Webfleet and Masternaut have strong positions. In Latin America, local players understand the unique security and infrastructure challenges. Samsara's approach has been pragmatic: compete where their product advantages matter most (enterprise, multi-geography deployments) while potentially partnering or acquiring local players for specific market access.

The AI and computer vision capabilities have become a significant competitive moat. In one year alone, Samsara's Video-Based Safety solutions have helped prevent more than 200,000 crashes among customers worldwide. Competitors simply don't have access to the training data—38 billion minutes of video footage—needed to build comparable AI models. This data advantage compounds over time, making it increasingly difficult for competitors to catch up even with unlimited capital.

The enterprise platform dynamics favor Samsara. Once a large enterprise standardizes on Samsara across multiple use cases—fleet, equipment, facilities—switching costs become prohibitive. It's not just about replacing hardware; it's about retraining thousands of employees, rebuilding integrations, and losing historical data. This creates winner-take-most dynamics in enterprise accounts, where the platform provider captures an increasing share of the customer's IoT spending.

Channel partnerships have become a critical battleground. Insurance companies, equipment dealers, and systems integrators influence billions in technology spending. Samsara's partnerships with major insurers who offer discounts for using their safety technology create powerful distribution leverage. Competitors are forced to match these partnerships or risk being locked out of significant distribution channels.

The threat from adjacent players is real but manageable. Enterprise software companies like Salesforce or ServiceNow could theoretically enter the market, leveraging their customer relationships and platform capabilities. Cloud providers like AWS or Azure have IoT ambitions. However, the hardware component, vertical expertise, and specialized go-to-market requirements create significant barriers. More likely, these players become partners rather than competitors.

Price competition has remained surprisingly rational. While there's always pressure on hardware pricing, the software and services layer maintains healthy margins across the industry. Customers make decisions based on total value rather than lowest cost, especially for mission-critical operations. Samsara's premium pricing relative to basic telematics is justified by superior product experience, reliability, and ROI.

The market dynamics suggest continued consolidation. Subscale players will struggle to fund the R&D necessary to remain competitive. Private equity-owned assets will seek exits. Strategic buyers will look for capability acquisitions. Samsara is well-positioned to be a consolidator, with the financial strength and platform scale to integrate acquisitions successfully. However, their organic growth focus suggests they'll be selective, acquiring only when it accelerates strategic objectives.

Looking forward, the competitive dynamics will likely shift from feature competition to ecosystem competition. The winner won't be who has the best individual product but who builds the most comprehensive platform with the strongest network effects. Samsara's early lead, combined with their execution capabilities and financial resources, positions them well for this next phase of competition. But the market is large enough for multiple winners, and competition will keep everyone honest and innovative.

XII. Bear vs. Bull Case

Bull Case: The Path to $100 Billion

The optimistic case for Samsara rests on several powerful trends converging. First, the TAM is genuinely massive and mostly untapped. Physical operations represent over 40% of global GDP, yet less than 10% have adopted modern IoT solutions. Samsara is capturing a tiny fraction of a giant market that's in the early innings of digital transformation. As regulations tighten, labor shortages worsen, and sustainability pressures mount, adoption will accelerate from nice-to-have to must-have.

The unit economics are best-in-class and improving. Net retention rates above 115% mean the existing customer base is a growth engine by itself. Gross margins expanding toward 80% provide enormous operating leverage. CAC payback under 15 months enables aggressive but profitable growth. These aren't theoretical metrics—they're proven at scale and getting better each quarter.

Platform network effects are creating an insurmountable moat. Every mile driven makes the AI smarter. Every integration makes switching harder. Every customer success story makes the next sale easier. Competitors can't replicate 38 billion minutes of video training data or thousands of enterprise customer relationships. The rich get richer dynamic in platform businesses strongly favors the incumbent leader.

The AI and computer vision opportunity is still early. Samsara's capabilities in drowsiness detection, predictive maintenance, and route optimization are just the beginning. As models improve and edge computing advances, the platform could enable autonomous operations, predictive logistics, and zero-accident fleets. The company that owns the data and customer relationships will capture most of this value.

Second-act founders with proven execution significantly de-risk the investment. Biswas and Bicket have done this before, know the playbook, and learn from mistakes. They've maintained culture while scaling, balanced growth with profitability, and navigated public markets successfully. The dual-class structure ensures they can execute their long-term vision without short-term pressure.

International expansion is just beginning. Less than 15% of revenue comes from outside North America, yet the international opportunity is larger than the domestic market. Europe's sustainability regulations, Asia's manufacturing growth, and emerging markets' infrastructure development all drive demand for connected operations. Samsara could triple their addressable market through geographic expansion alone.

The M&A optionality provides additional upside. With over $1 billion in cash and a valuable currency in their stock, Samsara could accelerate growth through strategic acquisitions. Buying regional leaders, vertical solutions, or complementary technologies could drive step-function growth while leveraging their platform scale.

Bear Case: The Risks Are Real

The skeptical view starts with the financial reality: despite impressive growth, Samsara is still posting significant GAAP losses. Operating losses of $123 million and negative earnings per share of $0.21 aren't trivial. While adjusted metrics look better, the path to GAAP profitability remains uncertain, especially if growth slows and stock-based compensation remains elevated.

Competition is intensifying from multiple directions. Motive is growing aggressively with significant funding. Legacy players are modernizing their platforms. New entrants are attacking specific verticals with focused solutions. Chinese competitors could enter with lower-cost alternatives. The comfortable competitive position of today could evaporate quickly if execution stumbles.

Macro sensitivity is a fundamental risk. Samsara's customers—trucking, construction, manufacturing—are cyclical industries hit hard during recessions. When fleet miles drop and construction projects halt, Samsara's growth could decelerate rapidly. The COVID resilience was impressive but might not predict performance in a traditional recession.

Hardware components and supply chain risks remain significant. While software generates most gross profit, customers need hardware to use the platform. Component shortages, supply chain disruptions, or manufacturing issues could constrain growth. The China dependency for electronics manufacturing creates geopolitical risk that's difficult to mitigate.

The valuation multiple relative to growth raises questions. Trading at over 10x forward revenue while growing 30-35% implies continued execution perfection. Any growth deceleration, margin compression, or competitive pressure could trigger multiple compression. The high valuation leaves little room for error.

Customer concentration in traditional industries could limit growth. While diversification is improving, transportation and construction still dominate revenue. These industries aren't known for rapid technology adoption or high growth. Samsara might hit penetration ceilings sooner than expected, forcing them into less attractive markets.

Technical disruption is always possible. A breakthrough in autonomous vehicles could eliminate the need for driver monitoring. Advances in synthetic data could erode Samsara's data advantage. New connectivity technologies could obsolete their hardware approach. While these seem unlikely near-term, technology markets can shift suddenly.

The stock-based compensation dilution is meaningful. At 20% of revenue, it's a real cost that shareholders bear. If the stock price stagnates, retaining talent becomes harder, potentially triggering a negative spiral. The dual-class structure, while enabling long-term thinking, reduces shareholder influence if performance deteriorates.

The Balanced View

Reality likely lies between these extremes. Samsara has built a strong business with attractive economics and significant competitive advantages. The market opportunity is real, execution has been impressive, and the platform is becoming increasingly sticky. However, the valuation reflects much of this optimism, competition is real, and macro risks can't be ignored.

For long-term investors, the key question isn't whether Samsara will face challenges—they will—but whether the fundamental business quality and market opportunity are sufficient to overcome them. The evidence suggests yes, but the path won't be linear. Volatility should be expected, but the destination—becoming the system of record for physical operations—seems achievable given current trajectory and execution capabilities.

XIII. The Future: What's Next for Samsara

The roadmap ahead for Samsara is both ambitious and grounded in customer reality. The AI and computer vision opportunities are perhaps most exciting. Having proven the value with drowsiness detection and safety coaching, the next frontier is predictive operations. Imagine AI that predicts equipment failures days before they happen, routes that automatically optimize based on real-time conditions, or cameras that can assess cargo damage instantly. The 10 trillion data points collected annually provide the raw material for AI applications we're only beginning to imagine.

International expansion will accelerate, but thoughtfully. Europe presents immediate opportunity with its regulatory environment favoring digital transformation—think sustainability reporting, driver hours regulations, and safety requirements. Asia's manufacturing and logistics boom creates massive demand, though competition from local players will be fierce. Latin America's infrastructure development and Africa's leapfrogging of legacy technology both offer longer-term potential. The playbook will vary by region, but the core value proposition—simple, integrated, powerful—translates globally.

Adjacent market opportunities abound. Healthcare logistics managing critical medical supplies, agriculture optimizing farming equipment, energy companies monitoring remote infrastructure—each represents billions in potential revenue. The beauty of Samsara's horizontal platform is that expansion requires minimal product changes, mainly vertical-specific features and go-to-market expertise. They could address dozens of new verticals without fundamental architecture changes.

The M&A strategy will likely remain disciplined but opportunistic. Small technology acquisitions that accelerate product roadmaps, regional players that provide market access, or vertical solutions that bring domain expertise all make sense. Large, transformative deals seem unlikely given the founders' preference for organic growth and cultural preservation. The integration track record from Meraki suggests they know how to acquire successfully when strategically necessary.

The long-term vision is becoming clearer: Samsara as the operating system for physical operations. Just as Salesforce became the system of record for customer relationships and Workday for human resources, Samsara aims to be the default platform for managing physical assets and operations. This isn't just about tracking vehicles—it's about orchestrating the entire physical value chain from manufacturing through delivery.

Could Samsara become the Salesforce of physical operations? The parallels are striking. Both started with a focused application (fleet management, sales force automation) and expanded into platforms. Both prioritized ease of use in industries accustomed to complex software. Both built ecosystem strategies that create lock-in through integrations and partner applications. Both maintained high growth while improving unit economics.

The differences matter too. Salesforce operated in a pure software world; Samsara must manage hardware complexity. Salesforce sold to tech-forward sales teams; Samsara sells to traditional operations managers. Salesforce rode the initial SaaS wave; Samsara must convince industries still using paper and spreadsheets. These challenges are real but surmountable with continued execution.

The autonomous vehicle implications deserve consideration. While full autonomy might seem threatening—no drivers to monitor—it could actually accelerate Samsara's opportunity. Autonomous fleets will need sophisticated monitoring, coordination, and optimization. The company managing today's human-driven fleets is well-positioned to manage tomorrow's autonomous ones. The platform architecture and customer relationships matter more than specific features.

Sustainability and ESG reporting are becoming growth drivers. Companies need to track carbon emissions, optimize routes for fuel efficiency, and prove sustainable operations to stakeholders. Samsara's platform provides the data foundation for comprehensive sustainability reporting. As regulations tighten and stakeholder pressure increases, this capability transforms from nice-to-have to business-critical.

The edge computing evolution will enable new capabilities. As processing power at the edge increases and 5G enables faster connectivity, Samsara's devices will become even smarter. Real-time video analytics, predictive maintenance algorithms, and autonomous coordination could all run locally, with only insights and exceptions sent to the cloud. This architectural evolution maintains Samsara's relevance as computing paradigms shift.

Platform extensibility through low-code/no-code tools could unlock customer-driven innovation. Allowing customers to build custom workflows, create specialized reports, or develop vertical-specific applications would accelerate adoption and increase stickiness. The Connected Workflows feature is a step in this direction, but the potential is much greater.

The financial services opportunity is intriguing. With deep operational data on thousands of businesses, Samsara could enable better insurance underwriting, equipment financing, or working capital loans. They might not become a financial services provider directly, but the data and insights they provide could transform how financial services are delivered to physical operations businesses.

Looking ahead five years, Samsara could be a very different company—larger, more international, more diversified across verticals, with AI capabilities we can barely imagine today. Yet the core mission—increasing the safety, efficiency, and sustainability of physical operations—will remain constant. The founders' track record suggests they can navigate this evolution while maintaining the cultural DNA and execution excellence that got them here. The future isn't guaranteed, but the foundation is solid, the opportunity is massive, and the team has proven they can execute. For a company named after the eternal cycle of rebirth, the next incarnation promises to be even more interesting than the last.

XIV. Epilogue & Key Takeaways

Standing back from the detailed analysis, Samsara's journey illuminates several profound truths about building transformational technology companies. The power of solving unglamorous but critical problems cannot be overstated. While Silicon Valley chased consumer unicorns and enterprise software for knowledge workers, Biswas and Bicket focused on garbage trucks, delivery vans, and construction equipment. They understood that the least sexy problems often represent the biggest opportunities—precisely because they've been overlooked.

The second-company advantage is real and powerful. Most successful entrepreneurs struggle to replicate their initial success, but Biswas and Bicket leveraged every lesson from Meraki. They knew to start narrow, expand methodically, prioritize customer experience, and maintain technical excellence. They avoided the common second-time founder trap of trying to build something too ambitious too quickly. Instead, they applied proven patterns to a new domain, de-risking execution while maintaining ambition.

Customer obsession in B2B isn't just rhetoric at Samsara—it's operational reality. Engineers ride in trucks, product managers visit construction sites, and customer success managers know their clients' businesses intimately. This isn't efficient in the short term, but it creates a product-market fit so strong that customers become evangelists. In industries where word-of-mouth matters more than marketing, this organic growth is priceless.

Timing matters enormously in platform businesses. Samsara launched just as multiple trends converged: ubiquitous cellular connectivity, cheap sensors, cloud computing maturity, and regulatory pressure for digitization. Five years earlier would have been too expensive; five years later would have meant entrenched competition. Recognizing and riding these waves requires both insight and luck, but mostly the wisdom to know when conditions are right.

The integrated hardware-software-cloud model that Samsara pioneered in IoT is becoming the standard across industries. Pure software companies are adding hardware components (see Amazon's devices), while hardware companies are desperately trying to add software services. Samsara proved that starting with integration from day one creates competitive advantages that are nearly impossible to replicate through acquisition or partnership.

Building for the real economy—the trucks, factories, and construction sites that power global GDP—is both a responsibility and an opportunity. These industries have been underserved by technology not because they're small or unprofitable, but because they're complex, regulated, and require deep domain expertise. Companies willing to do the hard work of understanding these industries can capture enormous value while making genuine societal impact.

The discipline to maintain simplicity while adding capability is perhaps Samsara's greatest achievement. As the platform expanded from fleet tracking to equipment monitoring to workflow automation, they resisted feature creep and interface complexity. This isn't easy—every customer wants their specific feature, every product manager has ideas, every engineer wants to build cool stuff. Saying no to maintain simplicity requires tremendous organizational discipline.

Financial discipline and growth aren't mutually exclusive, despite what many venture-backed companies suggest. Samsara proved you can grow 40%+ while improving margins and generating cash flow. The key is focusing on unit economics from day one, expanding existing customers rather than just acquiring new ones, and maintaining pricing discipline even when competitors discount.

The platform network effects in physical operations are subtle but powerful. Unlike social networks where effects are obvious, Samsara's compound quietly: better AI from more data, stronger ecosystem from more integrations, easier sales from more success stories. These take years to build but once established, create sustainable competitive advantages that pure software companies can't match.

Culture can survive scale if deliberately maintained. Despite growing from dozens to thousands of employees, from startup to public company, Samsara maintains its builder culture. This isn't accident—it's the result of careful hiring, consistent communication, and leaders who model the values they preach. The founders' continued involvement in product decisions and customer meetings signals that excellence remains paramount.

The public markets can be navigated successfully by focusing on long-term value over short-term stock movements. Samsara's stock has been volatile, but the business has steadily strengthened. By maintaining strategic focus despite market gyrations, they've proven that public companies can still think in years rather than quarters.