Intuit: The Platform Revolution in Financial Software

I. Introduction & Episode Roadmap

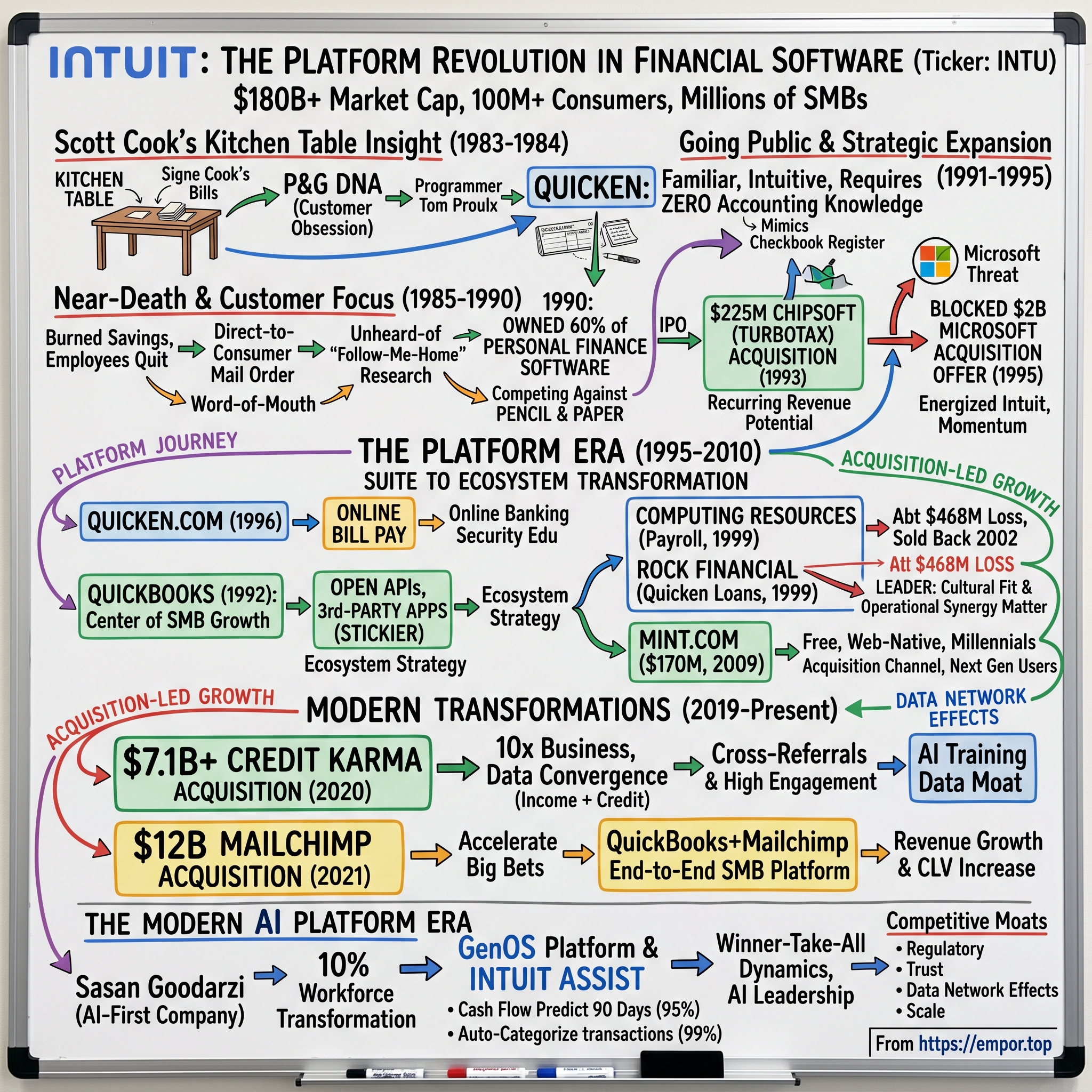

Picture this: It's August 2024, and Intuit just reported quarterly earnings that would make any CFO jealous—revenue up 17% year-over-year, operating income surging 24%, and the stock hovering near all-time highs around $650 per share. The company that started at a kitchen table in Palo Alto now commands a market capitalization north of $180 billion, making it more valuable than Goldman Sachs, American Express, or Charles Schwab. Not bad for a company that almost died in its infancy when employees worked without pay for six months.

But here's what's truly remarkable: Intuit isn't just another software success story. It's a masterclass in platform evolution, having transformed from a single personal finance product into the financial operating system for 100 million consumers and millions of small businesses worldwide. Today, if you're an American filing taxes, there's a 40% chance you're using TurboTax. If you're running a small business, the odds are even higher you're touching QuickBooks. Add in Credit Karma's 130+ million members and Mailchimp's marketing automation empire, and you have a company that has become as essential to America's financial infrastructure as the banks themselves. The overarching question we're tackling today isn't just how Intuit grew—plenty of software companies grow. It's how a company founded to solve one person's checkbook-balancing frustration evolved into the definitive platform for financial life management, survived multiple existential threats from Microsoft, and emerged as one of the most durable franchises in software history. This is a story of relentless customer obsession, strategic acquisitions that actually worked (a rarity in tech), and the counterintuitive power of serving markets that enterprise software ignored.

Our journey spans four decades of transformation: from boxed software to cloud platforms, from single products to ecosystem thinking, from serving individuals to powering the entire small business economy. Along the way, we'll uncover how Intuit pioneered the "follow-me-home" customer research method, why they turned down Microsoft's $2 billion acquisition offer, and how two massive bets—Credit Karma for $7.1 billion and Mailchimp for $12 billion—positioned them to dominate the AI era of financial services.

The themes we'll explore resonate far beyond Intuit: How do you build switching costs without becoming the villain? Can you maintain startup velocity at enterprise scale? And perhaps most importantly, what happens when you treat financial software not as a tool, but as a trusted advisor? Let's dive into one of Silicon Valley's most underappreciated success stories.

II. The Kitchen Table Insight (1983-1984)

The year was 1983, and Scott Cook was watching his wife Signe wrestle with their monthly bills at the kitchen table of their Palo Alto home. She had spread out checkbooks, receipts, and calculator across the wooden surface—a monthly ritual that consumed hours and generated visible frustration. Cook, a Harvard MBA who'd spent five years at Procter & Gamble learning the gospel of consumer marketing, saw something his wife didn't: a massive market opportunity hiding in plain sight.

"Why isn't there software for this?" he asked, more to himself than to Signe. Personal computers were just beginning to penetrate American homes—the Apple II had been out for six years, the IBM PC for two. Yet while businesses had accounting software, consumers were still balancing checkbooks with pencil and paper, just as their parents had done in the 1950s.

Cook's P&G training had taught him to obsess over consumer pain points. At P&G, he'd learned that great products don't come from technology innovation but from deep understanding of customer frustration. He'd managed Crisco shortening and Duncan Hines cake mixes—decidedly unglamorous products that generated billions because they solved real problems for real people. Now, sitting in Silicon Valley's epicenter, he saw the same opportunity in personal finance.

But Cook had a problem: he couldn't code. He was a marketer with an idea but no technical ability to execute it. So he did what any resourceful Stanford neighbor would do—he posted a note on the university's computer science bulletin board. "Programmer wanted to help create personal finance software," it read, with his phone number at the bottom.

The call that changed everything came from Tom Proulx, a Stanford student who'd been programming since high school. Their first meeting was almost comically mismatched—Cook in his business casual, armed with market research and consumer insights; Proulx in jeans and a t-shirt, skeptical that anyone would pay for software to balance a checkbook. But Proulx needed the money, and Cook's enthusiasm was infectious. They shook hands on a partnership that would eventually be worth billions.

Proulx retreated to his dorm room and began coding what would become Quicken. His approach was radically different from existing financial software, which mimicked professional accounting systems with debits, credits, and double-entry bookkeeping. Proulx thought like a consumer, not an accountant. The interface looked like a checkbook register—familiar, intuitive, requiring zero accounting knowledge. You entered checks like you wrote them, deposits like you made them. The software did the math and categorization behind the scenes.

By early 1984, they had a prototype. Cook incorporated Intuit—a portmanteau of "intuitive" and "compute"—and set up shop in his basement. Their first employee was Cook's wife Signe, who handled customer service from the kitchen where the idea was born. The irony wasn't lost on anyone.

Cook's initial go-to-market strategy reflected his P&G DNA but proved disastrously wrong. He approached banks, thinking they'd want to offer Quicken to customers as a value-add service. The banks were interested but wanted to white-label the product, removing Intuit's branding entirely. Worse, they moved at glacial speed—months of meetings that went nowhere. Cook pivoted to retail, approaching software stores and computer retailers. The response was crushing: "Nobody wants to do accounting at home," they said. "This is a solution looking for a problem."

By late 1984, Intuit was burning through Cook's savings with no revenue in sight. They'd printed 50,000 copies of Quicken based on Cook's optimistic projections. The boxes sat in the basement, a monument to entrepreneurial overconfidence. Three of their first seven employees quit when Cook couldn't make payroll. The remaining four, including Cook and Proulx, worked without salary for six months. Cook later called this period "the valley of death," when lesser companies—and founders—would have given up.

The competitive landscape offered little comfort. Managing Your Money, created by tax attorney Andrew Tobias, had first-mover advantage and better functionality. It could do tax planning, portfolio management, and financial planning—Quicken just balanced checkbooks. Dollars and Sense from Monogram had corporate backing and retail distribution. Even smaller players like Home Accountant had more traction. Intuit was dead last in a market that retailers insisted didn't exist.

But Cook noticed something the competition missed. When he did get Quicken into customers' hands—through direct sales at computer user groups or the rare retail placement—something magical happened. Users didn't just like Quicken; they evangelized it. They told friends, brought it to work, demanded their spouses use it. The net promoter score, had it existed then, would have been off the charts. The product was simple where competitors were complex, friendly where others were forbidding. Cook realized he didn't have a product problem; he had a distribution problem.

This insight would lead to one of the most important strategic decisions in Intuit's history—but not before the company nearly died. As 1984 turned to 1985, Intuit had less than $100,000 in revenue and was weeks from bankruptcy. Thirty venture capitalists had rejected Cook's funding pitches, including his Harvard Business School roommate. The feedback was consistent: the market was too small, the competition too established, and Cook had no technical background. One VC literally laughed him out of the office.

Cook's response revealed the trait that would define Intuit's culture for decades: maniacal customer focus. Instead of pivoting the product or pursuing enterprise sales like VCs suggested, he doubled down on understanding why those few Quicken users loved the product so much. He started calling customers personally, visiting their homes, watching them use the software. This "follow-me-home" research, unheard of in 1980s software, would become Intuit lore. Cook discovered that users didn't want financial planning or investment tracking—they wanted to stop bouncing checks and know where their money went. Quicken did exactly that, nothing more, nothing less.

The kitchen table insight had evolved into something more profound: software should solve human problems, not computer problems. While competitors built features for reviewers and retail buyers, Intuit built for Signe Cook and millions like her—people who just wanted their financial life to be a little less painful. This philosophy would carry Intuit through its darkest period and into an unexpected renaissance that nobody—least of all Scott Cook—saw coming.

III. The Near-Death Experience & Customer Obsession (1985-1990)

January 1985 found Scott Cook staring at a balance sheet that told a story of impending doom. Intuit had $125,000 in debt, virtually no revenue, and 47,000 unsold copies of Quicken gathering dust. The four remaining employees—Cook, Proulx, and two others—hadn't been paid in six months. Cook's father-in-law, who'd loaned them money, asked pointedly when he might see a return. Even Signe was beginning to question whether this software dream was worth destroying their financial security.

Then came the moment that nearly ended everything. Cook approached employee number three, a programmer who'd been working without pay, to discuss equity compensation instead of salary. The programmer looked at Cook with a mixture of pity and disgust. "Scott, this company is going nowhere. I'm done working for free." He walked out, taking specialized knowledge with him. Within a week, two more employees followed. Intuit was down to Cook, Proulx, and a part-time contractor.

But desperation breeds innovation. Unable to afford traditional advertising or secure retail distribution, Cook made a radical decision: sell directly to consumers through mail order. This wasn't how software was sold in 1985—you went to ComputerLand or Egghead Software, browsed boxes on shelves, maybe read a review in Byte magazine. Mail order was for vitamins and collectible plates, not serious software.

Cook scraped together $125,000—maxing out credit cards, borrowing from anyone who'd listen—for a direct marketing campaign. He bought mailing lists of personal computer owners and placed small ads in computer magazines. The ads were simple, even crude by today's standards: "End financial hassles." But they included something revolutionary: a money-back guarantee. No software company offered this. It was insane, potentially suicidal. Cook figured he had nothing left to lose.

The first responses trickled in slowly—five orders one day, seven the next. Then something unexpected happened. Return rates were essentially zero. Customer service calls, handled by Signe from their kitchen, revealed why: users loved Quicken's simplicity. More importantly, they were telling friends. Cook discovered that each customer generated, on average, 2.5 additional sales through word-of-mouth. The customer acquisition cost math suddenly worked.

Cook's obsession with customer service became legendary, bordering on pathological. He instituted a policy that every employee, including engineers and executives, had to work customer support regularly. This wasn't token gesture—Cook himself spent hours on the phone, troubleshooting printer problems and walking users through reconciliation. He kept a notebook of every complaint, every confusion, every feature request. These weren't just data points; they were product roadmap.

One call changed Quicken's trajectory forever. A customer complained that entering transactions was tedious—typing the same payees repeatedly, remembering exact category names. Proulx implemented "memorized transactions" in the next version, where Quicken remembered previous entries and auto-completed them. This feature, born from a single customer complaint, became Quicken's killer differentiator. Competitors had more features; Quicken saved time.

The direct marketing numbers improved dramatically. By mid-1985, response rates hit 3%—astronomical for direct mail. Customer satisfaction scores approached 90%. But Cook wanted more. He started including surveys with every shipment, offering discounts for responses. The data revealed something counterintuitive: customers didn't want more features. They wanted existing features to work better, faster, more intuitively. While competitors chased reviews by adding investment tracking and tax planning, Intuit obsessed over shaving seconds off transaction entry.

The advertising breakthrough came from an unlikely source. Cook hired a freelance copywriter who'd never written software ads. Instead of focusing on features or technology, she wrote about outcomes: "Throw away your calculator." "Never bounce another check." "Know where your money goes." The ads didn't mention computers or software specifications. They sold peace of mind.

By late 1985, Quicken was selling 1,000 copies a month through direct mail. Revenue hit $500,000. It wasn't profitable yet, but Cook could finally pay salaries. He hired back two employees who'd left, promising them equity that might actually be worth something. The retail doors that had been slammed shut began creaking open. Egghead Software agreed to carry Quicken in five stores as a test.

The retail test revealed Cook's marketing genius. Instead of relying on box art and shelf placement, Intuit created something unprecedented: in-store demos run by Intuit employees. Not retail staff who barely knew the product, but true believers who used Quicken themselves. They set up computers, showed real checkbook balancing, answered questions for hours. Conversion rates hit 70%—if someone watched a demo, they usually bought. Egghead expanded Quicken to all stores within three months.

But competition intensified. Microsoft announced Microsoft Money, scheduled for 1991 release. Managing Your Money added features monthly. New entrants appeared, funded by VCs who now saw personal finance software as viable. Cook's response was counterintuitive: ignore them all. "We don't compete against other products," he told employees. "We compete against pencil and paper." This wasn't corporate spin—it shaped every decision. Features were evaluated not against competitors but against manual methods. If something wasn't dramatically better than paper, it didn't ship.

The customer obsession border on cultish. Engineers were required to watch customers use Quicken in their homes—Cook's famous "follow-me-home" program. These weren't focus groups or usability labs but real-world observation. Engineers watched customers struggle with unclear terminology, hunt for menu items, abandon tasks in frustration. Every observation generated a bug report or feature request. One engineer watched a customer spend ten minutes trying to void a check, a process that required three non-obvious steps. The next version: one-click voiding.

By 1990, Quicken owned 60% of the personal finance software market. Revenue hit $33 million. The company that nearly died in 1985 was now profitable, growing 50% annually, and had 100 employees. But Cook knew the real test was coming. Microsoft Money would launch with Windows integration, unlimited marketing budget, and bundling deals with PC manufacturers. The scrappy startup phase was over. Intuit would need to evolve or die.

The near-death experience left permanent marks on Intuit's culture. The customer service obsession became institutionalized—even today, every Intuit employee must work customer support. The focus on simplicity over features became product dogma. The preference for customer feedback over competitive analysis shaped strategy. Most importantly, the experience taught Cook that in software, distribution and customer love matter more than technical superiority. Quicken wasn't the best personal finance software in 1985. By 1990, it was the only one that mattered.

IV. Going Public & The ChipSoft Acquisition (1991-1995)

Microsoft Money launched in October 1991 with the subtlety of a Sherman tank. Full-page ads in the Wall Street Journal. Bundling deals with Compaq and Dell. A retail price of $29.95—half of Quicken's $59.95. The message was clear: Microsoft intended to own personal finance software just as it owned operating systems and productivity suites. Industry analysts gave Intuit 18 months before capitulation.

Scott Cook convened an emergency executive session that would define Intuit's next decade. The conference room whiteboard filled with sobering facts: Microsoft had unlimited resources, Windows integration advantages, and a proven playbook for crushing competitors. But Cook identified one critical weakness: Microsoft didn't understand consumers. Their Money product, despite technical superiority, felt like enterprise software—powerful but intimidating. Cook bet the company on a simple thesis: customers would choose ease over features, even from Microsoft.

The Windows transition proved this bet right. While Microsoft optimized Money for Windows 3.1's technical capabilities, Intuit focused on preserving Quicken's simplicity in the new environment. The first Windows version of Quicken, released in 1991, looked almost identical to the DOS version—deliberately. Cook resisted engineers' desire to use every Windows widget and whistle. "Our users aren't computer enthusiasts," he reminded them. "They're parents balancing checkbooks after the kids are asleep."

But Cook knew defensive strategies don't win wars. Intuit needed offensive weapons—new products, new markets, new revenue streams. The board, now including venture capitalists who'd finally invested after years of rejection, pushed for acquisition-led growth. Cook resisted initially, believing in organic product development. That philosophy changed when he discovered ChipSoft.

ChipSoft, based in San Diego, had created TurboTax—the number two tax preparation software behind Intuit's own MacInTax. But ChipSoft dominated Windows while Intuit ruled Macintosh. Together, they'd own 70% of the consumer tax software market. More importantly, Cook saw strategic synergy: tax and personal finance were adjacent problems for the same customer. Quicken users became TurboTax prospects every January.

The 1993 IPO provided acquisition currency. Intuit went public at $15 per share, raising $81 million. The stock popped 25% on day one—validation after a decade of struggle. Cook used the proceeds immediately, acquiring ChipSoft for $225 million in stock just three months post-IPO. Wall Street gasped at the price—10x revenue for a seasonal business. Cook saw something analysts missed: recurring revenue potential. Tax customers returned annually, creating a subscription business before SaaS existed.

The ChipSoft integration revealed Cook's evolving management philosophy. Rather than imposing Intuit's culture, he preserved ChipSoft's entrepreneurial spirit. The San Diego office remained independent, keeping their development processes and brand identity. Cook was building a portfolio of products, not a monolithic corporation. This decentralized approach would define Intuit's acquisition strategy for decades.

1994 brought a transition Cook had been planning for years. He recruited Bill Campbell as CEO, moving himself to Executive Chairman. Campbell was Silicon Valley royalty—former Apple executive, GO Corporation CEO, and coach to Steve Jobs. Where Cook was thoughtful and analytical, Campbell was charismatic and decisive. He brought operational discipline to Intuit's creative chaos. Revenue hit $233 million. Employee count surpassed 700. Intuit wasn't a startup anymore.

Then came the phone call that shocked Silicon Valley.

In October 1994, Bill Gates personally called Bill Campbell with an acquisition offer: $2 billion for Intuit. The number was staggering—20x revenue, unprecedented for a software company. Microsoft wanted to eliminate its most persistent consumer software competitor and gain TurboTax's tax preparation dominance. Campbell and Cook faced an existential decision: sell for a fortune or bet they could build something even bigger independently.

The board meeting was contentious. Some directors saw $2 billion as validation of a decade's work—take the money, let Microsoft deal with competition. Others worried about employee morale and customer trust. Cook, surprisingly, was ambivalent. He'd built Intuit to solve problems, not maximize exit value. But $2 billion could fund countless new ventures. Campbell provided clarity: "Do we believe Intuit can become a $10 billion company independently?" The answer, after heated debate, was yes.

They accepted Microsoft's offer with one condition: regulatory approval. Both companies knew the Department of Justice would scrutinize the deal, but Microsoft's lawyers expressed confidence. Intuit began integration planning, employees received retention packages, and Cook started thinking about his next venture. For six months, Intuit existed in corporate limbo—technically independent but practically Microsoft's.

The DOJ's decision in April 1995 was swift and brutal: the acquisition was anticompetitive and blocked. Microsoft plus Intuit would control over 90% of personal finance software—monopolistic by any measure. The press release was embarrassing for Microsoft, validating for Intuit. David had been deemed too dangerous for Goliath to absorb.

Campbell's post-Microsoft speech to employees became Intuit legend. "Microsoft just validated our strategy. They tried to buy us because they couldn't beat us. Now we're going to show them what a massive mistake they made." The near-acquisition energized rather than demoralized. Engineers worked harder, salespeople pushed more aggressively, and customer service became even more obsessive. Microsoft renewed Money development with vengeance, but Intuit had momentum.

The ChipSoft acquisition proved prescient. TurboTax revenue grew 40% annually post-integration. Cross-selling between Quicken and TurboTax exceeded projections—30% of TurboTax customers came from Quicken referrals. The Windows version dominated despite Microsoft's bundling attempts. By 1995's tax season, TurboTax processed 2 million returns. The seasonal spike smoothed Intuit's revenue, making quarterly earnings predictable—Wall Street loved it.

Campbell's operational excellence showed in the numbers. 1995 revenue hit $384 million, up 65% year-over-year. Operating margins expanded from 8% to 15%. The stock price doubled from IPO levels. Intuit was generating enough cash to fund R&D and acquisitions without dilution. The company Microsoft tried to buy for $2 billion would be worth $5 billion within three years.

But the real victory was strategic positioning. The failed Microsoft acquisition forced Intuit to think bigger. Instead of being the best personal finance software company, why not own the entire consumer financial software category? QuickBooks for small business launched in 1992 but had been a side project. Campbell made it a priority. The payroll processing acquisition followed. The platform strategy was emerging.

The period from 1991 to 1995 transformed Intuit from successful startup to category leader. The Microsoft threat catalyzed innovation rather than paralysis. The ChipSoft acquisition proved Cook could buy and integrate successfully. Campbell's operational leadership freed Cook to think strategically about the next decade. Most importantly, surviving Microsoft's assault—both competitive and acquisitive—gave Intuit confidence that would fuel ambitious expansion.

As 1995 ended, Intuit stood at an inflection point. The desktop software era was maturing, the internet was emerging, and customer expectations were evolving. The next chapter would require reimagining Intuit's products for a connected world—a transformation that would test every lesson learned in the company's first decade.

V. The Platform Expansion Era (1995-2010)

The Netscape IPO in August 1995 changed everything. Suddenly, the internet wasn't just for academics and techies—it was the future of computing. At Intuit's Menlo Park headquarters, Scott Cook watched employees trade Netscape stock and realized his carefully built desktop software empire might become obsolete overnight. The question wasn't whether to embrace the internet, but how fast they could transform without destroying what worked.

QuickBooks, launched quietly in 1992, had been Campbell's first major strategic bet as CEO. While Quicken dominated personal finance, small business accounting remained fragmented among dozens of complex, expensive solutions. Campbell saw opportunity in simplification—apply Quicken's consumer-friendly approach to business accounting. The initial reception was tepid. Accountants dismissed it as too simple. Small businesses found it too complex. It was classic innovator's dilemma: too advanced for non-users, too basic for power users.

The breakthrough came from an unexpected source: Intuit's own sales data. They discovered QuickBooks wasn't replacing existing accounting software—it was converting businesses that used no software at all, just paper ledgers and shoeboxes of receipts. This wasn't a market share play but market creation. Campbell immediately refocused marketing from "better than Peachtree" to "better than paper." Sales exploded. By 1998, QuickBooks had 1 million users, generating $200 million annually.

The internet transition proved more challenging than anyone anticipated. Cook created Quicken.com in 1996, offering online bill pay and account aggregation. The technology was groundbreaking—securely pulling data from hundreds of banks—but consumer adoption lagged. Only 20% of Quicken users had internet access. Those who did were terrified of online banking security. Intuit spent millions educating customers about SSL certificates and encryption, essentially funding internet banking adoption for the entire industry.

Then came the acquisition spree that would transform Intuit from product company to platform.

Computing Resources Corporation in 1999 for $200 million brought payroll processing—a $15 billion market Intuit had completely ignored. The synergy was obvious: every QuickBooks customer needed payroll. But execution proved difficult. Payroll required regulatory compliance across 50 states, thousands of tax jurisdictions, and constant updates. Intuit's engineers, accustomed to annual software releases, struggled with daily tax table changes. Customer service calls quadrupled. Campbell brought in payroll industry veterans, created a separate division, and accepted that payroll would require different operational rhythms than software.

The Rock Financial acquisition in 1999 was Cook's boldest bet—and biggest failure. Intuit paid $532 million for the mortgage company, renaming it Quicken Loans. The thesis was compelling: Quicken users were prime mortgage customers, already trusting Intuit with financial data. Cross-selling mortgages through software seemed natural. But Intuit fundamentally misunderstood the mortgage business. Software companies sell products; mortgage companies sell relationships. The cultures clashed immediately. Quicken engineers in Silicon Valley couldn't relate to mortgage brokers in Detroit. Regulatory compliance across states was nightmarish. When the dot-com bubble burst in 2000, mortgage demand evaporated.

Dan Gilbert, Rock Financial's founder who'd stayed on post-acquisition, proposed a management buyout in 2002. Intuit, exhausted from mortgage industry battles, agreed to sell Quicken Loans back to Gilbert for $64 million—an $468 million loss. Gilbert would later build Quicken Loans into America's largest mortgage lender, worth $25 billion by 2020. The failure taught Cook a crucial lesson: adjacency isn't enough for successful acquisition. Cultural fit and operational synergy matter more than strategic logic.

The 2000s brought new leadership and renewed focus. Steve Bennett replaced Campbell as CEO in 2000, bringing General Electric operational discipline. Bennett was everything Silicon Valley wasn't—process-oriented, metrics-obsessed, allergic to waste. He implemented Six Sigma, laid off 500 employees, and killed dozens of unprofitable initiatives. Engineers rebelled against process documentation. Marketing chafed at ROI requirements. But Bennett's discipline worked: operating margins expanded from 15% to 25%.

Bennett's masterstroke was recognizing QuickBooks' platform potential. Rather than building every feature, Intuit opened APIs for third-party developers. Within two years, 500 applications integrated with QuickBooks—point-of-sale systems, inventory management, e-commerce platforms. Each integration made QuickBooks stickier, harder to leave. Customer churn dropped from 20% to 12% annually. The ecosystem strategy that would define modern Intuit was born.

The 2006 Digital Insight acquisition for $1.35 billion seemed like another Rock Financial disaster in the making. Digital Insight provided online banking software to financial institutions—enterprise sales to conservative banks, antithetical to Intuit's consumer DNA. But Bennett saw strategic value: Digital Insight connected 700 banks to 10 million consumers. Those connections could feed Intuit's products with real-time financial data, enabling features competitors couldn't match.

Integration took three years and nearly failed multiple times. Bank executives distrusted Intuit's consumer focus. Intuit engineers struggled with enterprise reliability requirements—99.999% uptime was different from annual desktop releases. But persistence paid off. By 2009, Quicken and Mint could instantly sync with thousands of banks. Competitors had to negotiate individual bank relationships; Intuit had wholesale access. The data network effect became Intuit's deepest moat.

The boldest acquisition of this era almost didn't happen. Mint.com, founded in 2006, was everything Intuit wasn't—free, web-native, beloved by millennials. By 2009, Mint had 1.5 million users and was adding 1,000 daily. Their business model was radical: free software monetized through financial product recommendations. Young users who'd never buy Quicken were flocking to Mint. Cook saw an existential threat.

The September 2009 acquisition for $170 million was controversial internally. Why buy a free competitor with no revenue? Bennett's successor, Brad Smith (who became CEO in 2008), understood: Mint wasn't a product but a acquisition channel for the next generation. Mint users were 15 years younger than Quicken users on average. They'd eventually need TurboTax, maybe QuickBooks. The $170 million bought not current revenue but future customer relationships.

Mint's founder Aaron Patzer joined Intuit, bringing Silicon Valley credibility the company desperately needed. Intuit had become corporate, bureaucratic, uncool. Patzer's presence signaled transformation. He reimagined Quicken for the web, launched mobile apps, and pushed free offerings. The cultural clash was intense—Patzer's team worked in hoodies and sneakers while Intuit executives wore collared shirts. But Smith protected Patzer, understanding that Intuit needed disruption.

By 2010, the platform expansion was complete. Intuit offered products across the financial lifecycle: Mint for budgeting, Quicken for wealth building, TurboTax for compliance, QuickBooks for business. The products shared data, customers, and infrastructure. Revenue hit $3.5 billion. Market cap exceeded $15 billion. The desktop software company had become a financial services platform.

But transformation came with costs. Intuit was now complex—dozens of products, thousands of employees, millions of customers with divergent needs. Innovation slowed under operational burden. Startups like Square and Stripe were reimagining financial services while Intuit optimized existing products. The next decade would require another reinvention—from desktop-first to mobile-native, from software to services, from products to artificial intelligence.

The platform expansion era proved Intuit could evolve beyond its origins. The failed Rock Financial acquisition taught valuable lessons about strategic discipline. The successful Mint acquisition showed Intuit could disrupt itself. Most importantly, the period established Intuit's modern identity: not just a software company but a financial platform powering prosperity for millions. That platform would soon face its biggest test—and opportunity—in the mobile and AI revolution ahead.

VI. The Credit Karma Transformation (2019-2020)

Ken Lin was nursing a beer at a San Francisco bar in October 2018 when his phone buzzed with a text that would change his life: "Scott Cook wants to meet. Tomorrow. Can you make it?" Lin, founder and CEO of Credit Karma, had built his company into a financial powerhouse with 100 million members and $1 billion in revenue. He'd turned down acquisition offers from banks, credit card companies, even Google. But Intuit was different. This wasn't about selling out—it was about scaling up.

The next morning, Cook arrived at Credit Karma's Oakland headquarters with a simple question: "What would it take for Credit Karma to reach a billion users?" Lin was stunned. Most acquirers wanted to harvest Credit Karma's revenue or eliminate competition. Cook wanted to 10x the business. They talked for four hours—about financial inclusion, data-driven insights, the convergence of tax and credit. Cook left without mentioning acquisition. But Lin knew negotiations had begun.

Credit Karma's origin story resonated with Cook because it mirrored Intuit's. Lin had started the company in 2007 after being denied a credit card despite good credit—he simply didn't know his score. Credit scores were hidden behind paywalls, controlled by bureaus that charged $15 per peek. Lin's radical idea: give credit scores away free, monetize through targeted financial product recommendations. Banks would pay for qualified customer leads. Consumers would get transparency. Everyone wins.

By 2019, Credit Karma had become the largest free credit platform globally. Members checked their scores 37 times per year on average. The platform recommended credit cards, loans, and insurance based on approval likelihood—eliminating the application anxiety that plagued financial services. Revenue per member hit $35 annually through affiliate commissions. The business model was brilliant: help consumers understand their finances, then connect them with appropriate products. The February 2020 announcement stunned Silicon Valley: Intuit would acquire Credit Karma for approximately $7.1 billion—$3.55 billion in cash and $3.55 billion in stock. The deal represented Intuit's largest acquisition ever, dwarfing the Mailchimp purchase that would come a year later. But what made the acquisition truly remarkable wasn't the price—it was the strategic vision it revealed.

Sasan Goodarzi, who'd become CEO in January 2019, had identified Credit Karma as the missing piece in Intuit's consumer finance puzzle. "Credit Karma set out to do exactly what we're trying to do—they're just 10 years ahead of us," Goodarzi explained. The synergies were compelling: TurboTax users needed credit monitoring, Credit Karma members needed tax filing, and both needed financial products. The combined entity would touch consumers at every major financial decision point.

But the real genius lay in the data convergence. Credit Karma's value wasn't just its 110 million members but the data those members generated—credit scores, spending patterns, loan applications. Combined with TurboTax's income data and Mint's transaction history, Intuit could now see the complete financial picture of tens of millions of Americans. This wasn't just cross-selling opportunity; it was the foundation for AI-driven financial advice that no competitor could match.

The regulatory gauntlet proved more challenging than anticipated. The Department of Justice scrutinized the deal for anti-competitive concerns, particularly around tax preparation where both companies competed. In November 2020, Intuit and Credit Karma entered a consent decree with the DOJ and an Assurance of Discontinuance with the New York State Attorney General, agreeing to divest Credit Karma Tax to Square for $50 million. It was a small price for regulatory clearance—Credit Karma Tax had less than 1% market share versus TurboTax's 40%.

The integration philosophy reflected lessons from past acquisitions. Rather than absorbing Credit Karma into Intuit's infrastructure, Goodarzi maintained it as an autonomous subsidiary. Ken Lin remained CEO, the Oakland headquarters stayed open, and the freemium model continued unchanged. This wasn't corporate imperialism but strategic federation—preserve what works while enabling synergies.

When the deal closed in December 2020, the final price had increased to approximately $8.1 billion—$3.4 billion in cash and $4.7 billion in stock. Intuit's stock appreciation during the nine-month regulatory review had boosted the equity portion's value. The combined company now served over 147 million customers globally, creating what Intuit called "a new consumer finance platform".

The immediate impact validated the acquisition thesis. Within six months, cross-referrals between platforms exceeded projections by 40%. TurboTax users who connected to Credit Karma increased their engagement 3x. Credit Karma members who filed taxes with TurboTax had 25% higher lifetime value. The data feedback loop created compound advantages—better credit recommendations led to more successful applications, which generated more affiliate revenue, which funded product improvements.

Ken Lin articulated the strategic breakthrough: "One of the biggest frustrations for consumers is the lack of certainty around whether you're qualified for a product. While Credit Karma could predict someone's eligibility for a personal loan using credit reports, credit worthiness is only 60% to 80% of the final approval decision. Now obviously with Intuit and TurboTax, we're able to increase our certainty much higher" by incorporating income data.

The financial performance exceeded even optimistic projections. Credit Karma contributed $1.4 billion in revenue in its first full year under Intuit, growing 35% year-over-year. More importantly, it transformed Intuit's business model. The traditional software company now had a significant advertising revenue stream—Credit Karma generated money not from software licenses but from financial institution partnerships. This diversification proved prescient as software pricing pressure intensified.

Cultural integration proved surprisingly smooth. Credit Karma's mission—"championing financial progress for all"—aligned perfectly with Intuit's "powering prosperity." Both companies obsessed over net promoter scores, conducted extensive user research, and prioritized simplicity. The main cultural clash came from business models: Intuit charged for premium features while Credit Karma gave everything away free. The solution was elegant—maintain both models, let customers choose.

The Credit Karma acquisition also accelerated Intuit's AI ambitions. With 110 million members generating billions of data points monthly, Credit Karma provided the training data necessary for sophisticated machine learning models. These models could predict cash flow crunches, identify savings opportunities, and recommend financial products with unprecedented accuracy. The AI wasn't just analyzing numbers but understanding financial behavior patterns across demographics, geographies, and economic cycles.

By late 2021, the strategic value was undeniable. Credit Karma members who used other Intuit products had 40% higher retention rates. The platform processed over $10 billion in loan applications monthly. Customer acquisition costs dropped 30% through cross-platform referrals. Most importantly, Intuit now had a relationship with consumers year-round, not just during tax season or when paying bills.

The acquisition transformed Intuit's competitive position. Traditional banks couldn't match the user experience. Fintech startups lacked the scale and data. Even tech giants like Google and Apple lacked the specialized financial expertise. Intuit had built what Cook envisioned decades earlier—a trusted financial companion for every consumer's journey from their first paycheck to retirement.

VII. The Mailchimp Mega-Deal (2021)

Ben Chestnut was pacing the conference room at Mailchimp's Atlanta headquarters in March 2021, wrestling with a decision that would define his legacy. The email marketing platform he'd bootstrapped from zero to $800 million in annual revenue had received acquisition interest from multiple strategic buyers. But only one suitor understood Mailchimp's true potential: Intuit, offering $12 billion—a valuation that made even Chestnut's wildest dreams seem conservative.

The courtship had begun a year earlier, not with bankers and term sheets but with a simple phone call from Scott Cook. "I'm not calling to buy your company," Cook had said. "I'm calling to learn from you." They talked for two hours about bootstrapping, customer obsession, and the loneliness of founder-CEOs. Cook became an informal advisor, offering counsel on international expansion and platform strategy. Only after six months of relationship-building did acquisition enter the conversation.

Mailchimp's origin story resonated with Cook because it mirrored Intuit's bootstrapped beginnings. Chestnut and co-founder Dan Kurzius had started in 2001 as a web design agency, building Mailchimp as a side project for clients who needed email newsletters. For eight years, they ran it as a lifestyle business—profitable but unambitious. The 2009 freemium launch changed everything. Small businesses that couldn't afford ConstantContact's $30 monthly fee flocked to Mailchimp's generous free tier. Growth exploded: 100,000 users in 2009, 1 million by 2011, 15 million by 2021.The September 2021 announcement sent shockwaves through Silicon Valley: Intuit would acquire Mailchimp for approximately $12 billion in cash and stock, making it Intuit's largest acquisition ever and the biggest exit for a bootstrapped company in history. The total consideration included approximately $300 million of assumed Mailchimp employee transaction bonuses that would be issued in the form of restricted stock units, expensed over three years.

What made Mailchimp unique wasn't just its size but its philosophy. This was a company that had famously rejected venture capital for 20 years, growing entirely on revenue and profits. Chestnut and Kurzius owned 100% of the company—no dilution, no board seats, no quarterly earnings calls. They'd built a $800 million revenue business answering to nobody but customers. The culture reflected this independence: quirky marketing campaigns, generous employee benefits, and a commitment to serving small businesses that VCs would have considered too small to matter.

Goodarzi understood that Mailchimp wasn't just an email marketing tool but a small business operating system. Beyond the 12 million users sending billions of emails monthly, Mailchimp had evolved into a comprehensive marketing platform—landing pages, social media ads, customer journeys, e-commerce integration. Small businesses used Mailchimp not just to send newsletters but to understand customers, drive sales, and compete with larger rivals. This aligned perfectly with Intuit's QuickBooks ecosystem vision.

The strategic rationale was compelling. With the acquisition of Mailchimp, Intuit would accelerate two of its previously-shared strategic Big Bets: to become the center of small business growth; and to disrupt the small business mid-market. QuickBooks helped businesses manage finances; Mailchimp helped them grow revenue. Together, they created an end-to-end platform that no competitor could match. A small business could now manage books, process payroll, send invoices, run email campaigns, and analyze customer behavior—all within the Intuit ecosystem.

The synergies emerged immediately. The companies began testing a one-way integration between QuickBooks Online and Mailchimp in July 2021, and QuickBooks customers imported more than 400,000 customer contacts into their Mailchimp accounts to use for customer segmentation and marketing. This was just the beginning—deeper integration would enable purchase data syncing, automated campaign triggers based on invoice status, and AI-driven marketing recommendations based on financial performance.

The cultural fit surprised skeptics who expected a clash between Intuit's corporate structure and Mailchimp's irreverent independence. But both companies shared foundational values: customer obsession, product simplicity, and small business advocacy. Goodarzi promised to maintain Mailchimp's Atlanta headquarters as a hub, preserve the brand identity, and keep the freemium model that had driven growth. Intuit would add about 1,200 employees to Mailchimp, and the company planned to turn Atlanta, where Mailchimp is based, into a new hub.

The financial structure reflected confidence in the combination. When the deal closed in November 2021, Intuit paid approximately $5.7 billion in cash and 10.1 million shares of Intuit common stock with a fair value of approximately $6.3 billion. Intuit funded the cash consideration through cash on hand and a $4.7 billion term loan under a new credit agreement.

The integration philosophy learned from Credit Karma—autonomy with synergy—guided Mailchimp's absorption. Rather than forcing Mailchimp onto Intuit's technology stack, teams identified specific integration points that created customer value. QuickBooks invoice data enhanced Mailchimp's segmentation. Mailchimp's engagement metrics improved QuickBooks' customer health scores. The platforms remained distinct but interconnected, giving customers choice while encouraging ecosystem adoption.

By mid-2022, the results validated the acquisition premium. Mailchimp revenue grew 25% year-over-year, accelerating from pre-acquisition rates. Cross-sell metrics exceeded targets—15% of new QuickBooks customers added Mailchimp within six months. Customer lifetime value increased 35% for businesses using both platforms. The combined data set—financial performance plus marketing engagement—enabled AI models that could predict customer churn, recommend optimal pricing, and identify growth opportunities with unprecedented accuracy.

The Mailchimp deal also transformed Intuit's market position. No longer just a financial software company, Intuit now competed across the entire small business stack. Competitors like Salesforce, HubSpot, and Square found themselves facing an integrated platform they couldn't replicate without similar massive acquisitions. The moat wasn't just features but data network effects—every QuickBooks transaction made Mailchimp smarter, every Mailchimp campaign improved QuickBooks insights.

Ben Chestnut's post-acquisition reflection captured the strategic alignment: "We spent 20 years helping small businesses look bigger. Intuit spent 40 years helping them run smarter. Together, we're building something neither could achieve alone—a platform that doesn't just manage business but actively drives growth."

The Mailchimp acquisition proved that Intuit had evolved beyond its desktop software roots into something more ambitious: a platform company willing to pay premium prices for strategic assets that accelerated its vision. The $12 billion price tag that seemed excessive to some analysts looked prescient as the small business economy digitized post-pandemic. Intuit hadn't just bought an email marketing company—it had secured its position as the operating system for millions of small businesses worldwide.

VIII. The Modern AI Platform Era (2020-Present)

The Zoom call in July 2024 lasted exactly 12 minutes. Sasan Goodarzi, speaking from Intuit's Mountain View headquarters, delivered news that would reshape the company: 1,800 employees—10% of the global workforce—would be leaving Intuit. But this wasn't a typical layoff driven by financial pressure. Revenue was growing double-digits, profits were at record highs, and the stock price had tripled during Goodarzi's tenure. This was something different: a deliberate transformation to become an AI-first company, even if it meant letting go of talented people who didn't fit the new vision.

"We're not trying to save money," Goodarzi explained to stunned employees. "We're reshaping our workforce for the AI era. The employees leaving are not poor performers in their current roles—they simply don't have the skills we need for where we're going." It was brutally honest, strategically bold, and classically Goodarzi—an executive who'd risen through Intuit's ranks by challenging sacred cows and pushing uncomfortable changes. Goodarzi's vision for AI wasn't incremental improvement but fundamental reimagination. "Companies that aren't prepared to take advantage of this AI revolution will fall behind and, over time, will no longer exist," he wrote in the memo. The centerpiece of this transformation was Intuit Assist, an AI-powered financial assistant that would evolve from answering questions to actually completing tasks—filing taxes, categorizing expenses, creating marketing campaigns, all with minimal human intervention.

The AI strategy reflected a profound shift in how Intuit viewed its role. For 40 years, the company had built tools that helped people manage finances. Now, Goodarzi envisioned AI that would manage finances for people—a "done-for-you" experience rather than "do-it-yourself" software. This wasn't just about adding chatbots or automating workflows; it was about reimagining every product from first principles with AI at the core.

TurboTax Live exemplified this transformation. Launched in 2017 as human tax experts available via video chat, it had grown to represent 30% of Consumer Group revenue by 2024, with 17% year-over-year growth. But the real innovation wasn't the human experts—it was how AI augmented them. Machine learning models pre-filled forms, identified deductions, and flagged audit risks. Experts focused on complex situations and customer confidence. The result: higher customer satisfaction, increased average selling prices, and improved expert productivity.

The QuickBooks evolution was even more dramatic. What started as desktop accounting software had become an AI-driven business command center. Intuit's GenOS platform—the AI infrastructure underlying all products—could now predict cash flow 90 days out with 95% accuracy, automatically categorize transactions with 99% precision, and identify expense anomalies that might indicate fraud or inefficiency. Small businesses weren't just tracking finances; they were receiving CFO-level insights previously available only to large corporations.

The Mailchimp integration showcased AI's cross-platform potential. By combining QuickBooks financial data with Mailchimp marketing metrics, Intuit could predict which customers were likely to churn, which marketing campaigns would generate highest ROI, and when businesses should adjust pricing. One restaurateur described the impact: "It's like having a consultant who knows my business better than I do, available 24/7, for the cost of software subscription."

The market rewarded this transformation spectacularly. Intuit's market cap soared from around $50 billion when Goodarzi became CEO in 2019 to approximately $198-200 billion by August 2025. Revenue growth accelerated despite mature markets—fiscal 2024 revenue hit $16.3 billion, up 13% year-over-year. More impressively, operating margins expanded even while investing heavily in AI, reaching 35% by 2024.

The competitive moat deepened through data network effects. With 100 million consumers and millions of small businesses generating billions of transactions annually, Intuit possessed training data that no competitor could replicate. Every tax return filed improved tax prediction algorithms. Every invoice sent enhanced revenue forecasting models. Every marketing email opened refined customer engagement predictions. This wasn't just big data—it was relevant, real-time, financial data with clear monetization paths.

International expansion accelerated under the AI strategy. Rather than rebuilding products for each geography, Intuit could train AI models on local tax codes, accounting standards, and business practices. QuickBooks launched in France, Germany, and Brazil with minimal localization effort. Credit Karma expanded to Canada and the UK by partnering with local financial institutions. The platform approach—build once, deploy globally—finally worked.

But challenges emerged alongside opportunities. Privacy concerns intensified as AI models required more personal data. Regulators questioned whether Intuit's AI-driven tax advice constituted unauthorized practice of law. Some customers resented AI automation replacing human bookkeepers and tax preparers—professions Intuit had historically supported. The company walked a tightrope between innovation and disruption of its own ecosystem.

The July 2024 layoffs revealed another challenge: talent transformation. Of the 1,800 employees departing, 1,050 were "not meeting expectations"—not in their current roles but for the AI-first future Goodarzi envisioned. The company needed machine learning engineers, not traditional software developers. Data scientists, not financial analysts. AI product managers, not feature managers. The workforce transformation was as radical as the product transformation.

Goodarzi's boldest bet was on "Big Bets"—strategic initiatives that would define Intuit's next decade. Big Bet 1, "Revolutionize Speed to Benefit," focused on Intuit Assist delivering instant, personalized financial guidance. Big Bet 2, "Connecting People to Experts," combined AI with human expertise for complex situations. Big Bet 3, "Unlock Smart Money Decisions," leveraged Credit Karma's data for proactive financial recommendations. Big Bet 4, "Become the Center of Small Business Growth," positioned QuickBooks plus Mailchimp as the growth engine for SMBs. Big Bet 5, "Disrupt the Small Business Mid-market," targeted larger businesses traditionally served by enterprise software.

The fiscal 2025 guidance reflected confidence in this strategy: revenue of $18.2-18.3 billion (12-13% growth), operating income growth of 13-14%, and earnings per share growth of 13-14%. These weren't startup growth rates, but for a 40-year-old company with dominant market positions, they were remarkable. The market agreed—analysts raised price targets, institutional ownership increased, and the stock hit all-time highs.

By August 2025, Intuit's transformation was nearly complete. The company that started with Quicken balancing checkbooks now operated one of the world's most sophisticated AI platforms for financial services. The ecosystem spanning tax preparation, accounting, marketing, and credit had become self-reinforcing—each product made others more valuable. The data moat was essentially unassailable. The brand trust, built over four decades, provided permission to expand into new financial services.

Yet Goodarzi remained paranoid about disruption. In every employee meeting, he reminded teams that Intuit's greatest risk wasn't competition but complacency. The AI revolution was just beginning. Large language models were improving exponentially. Startups were attacking niche problems with AI-first solutions. Even tech giants like Apple and Google were eyeing financial services. Intuit's response was continuous transformation—not just adopting AI but reimagining what financial software could be in an AI-native world.

IX. Playbook: Platform & Acquisition Lessons

At a Stanford Graduate School of Business lecture in 2019, Scott Cook was asked the question every entrepreneur wants answered: "What's the secret to Intuit's longevity?" Cook's response was unexpected. "We've survived because we've been willing to kill our own products before competitors could." He then detailed how Intuit had cannibalized Quicken with Mint, desktop QuickBooks with cloud versions, and traditional TurboTax with Live assisted filing. This wasn't disruption theory—it was disruption practice, executed repeatedly over four decades.

The power of customer obsession from Day 1 became Intuit's foundational lesson. While competitors focused on features, Intuit focused on outcomes. The "follow-me-home" program, where employees observed customers in their natural environment, revealed insights that focus groups never could. Engineers watched small business owners balance books at 11 PM after putting kids to bed. Product managers observed taxpayers gathering receipts from shoebox "filing systems." These observations drove product decisions more than competitive analysis or technical capabilities.

This customer obsession institutionalized into measurable metrics. Net Promoter Score became religion—not just tracked but tied to compensation. Every product team had customer contact requirements. Even the CEO spent hours monthly on customer support calls. When Goodarzi became CEO, his first action wasn't strategy revision but spending a week visiting small businesses. The message was clear: customers determine success, not competitors or investors.

The platform evolution from Products to Suite to Ecosystem to AI Platform represented four distinct strategic eras, each requiring different capabilities. The Products era (1983-1995) focused on solving specific problems exceptionally well—Quicken for checkbooks, TurboTax for taxes. The Suite era (1995-2005) connected related products—QuickBooks integrated with payroll, TurboTax imported from Quicken. The Ecosystem era (2005-2020) opened APIs, acquired adjacent services, and built network effects. The AI Platform era (2020-present) reimagined everything with machine learning at the core.

Each transition was painful. Moving from products to suite required standardizing data formats across independent teams. Building an ecosystem meant cannibalizing license revenue for subscription models. The AI platform demanded firing 10% of employees who couldn't adapt. But each transformation was necessary—companies that stayed in previous eras became irrelevant. Cook's willingness to endure short-term pain for long-term positioning became organizational DNA.

The M&A philosophy—"buy time to market, not just technology"—shaped acquisition strategy. Intuit rarely bought companies for their code or patents. Instead, they bought customer relationships, market position, and most importantly, time. Credit Karma would have taken five years to build internally—if it could be built at all, given Intuit's premium pricing DNA conflicting with Credit Karma's free model. Mailchimp represented a decade of email marketing evolution. Even failed acquisitions like Rock Financial taught valuable lessons about market adjacency limits.

The "5-year rule" became Intuit's acquisition heuristic: If building internally would take more than five years, or if the probability of success was below 50%, acquire instead. This rule justified paying premium prices—$170 million for Mint (100x revenue), $7.1 billion for Credit Karma (7x revenue), $12 billion for Mailchimp (15x revenue). Critics called these prices excessive, but Intuit measured value differently: years of development saved, competitive threats neutralized, new customer segments accessed.

Cultural integration proved more important than technical integration. Intuit's biggest acquisition failures—Rock Financial, certain Digital Insight components—stemmed from cultural misalignment, not technical challenges. Successful acquisitions like Mint, Credit Karma, and Mailchimp maintained founder involvement, preserved brand identity, and retained separate offices. This federated approach sacrificed some efficiency for entrepreneurial energy.

The integration playbook evolved through trial and error. First 30 days: Preserve everything, change nothing, just observe. First quarter: Identify quick wins—simple integrations that demonstrate value without disruption. First year: Deep technical integration on select high-value connections. Years 2-3: Full platform integration while maintaining product independence. This patient approach contrasted with typical acquisition integration that forced rapid consolidation.

Network effects and data advantages created compounding value at scale. Every QuickBooks customer made the product more valuable through aggregated benchmarking data. Every TurboTax return improved tax calculation algorithms. Every Credit Karma member enhanced credit prediction models. These network effects were subtle—users didn't see them directly—but they created switching costs that competitors couldn't overcome. A small business might consider leaving QuickBooks, but they'd lose access to industry benchmarks, cash flow predictions, and integrated services that no standalone product could match.

Capital allocation philosophy balanced growth investment with shareholder returns. Despite spending $20+ billion on acquisitions over two decades, Intuit maintained consistent dividends and share buybacks. The company funded acquisitions through a combination of cash generation ($5+ billion annually by 2024), debt (maintaining investment-grade ratings), and stock (using high valuation multiples as currency). This balanced approach avoided dilution while maintaining financial flexibility.

The platform playbook's greatest insight was recognizing that financial services aren't discrete products but interconnected needs. Taxes connect to bookkeeping. Bookkeeping connects to payroll. Payroll connects to payments. Payments connect to lending. Lending connects to credit scores. Credit scores connect back to taxes. This circular relationship meant that owning multiple touchpoints created exponential value—not just cross-selling opportunities but data insights that improved every product.

Intuit's approach to competition evolved from direct confrontation to ecosystem absorption. Rather than competing with every startup, Intuit opened APIs and created partnership programs. Thousands of apps integrated with QuickBooks. Hundreds of financial institutions connected to Mint. This openness created a gravitational pull—startups built on Intuit's platform rather than competing against it. When startups gained traction, Intuit could acquire them with existing technical integration already complete.

The timing lesson proved crucial: being too early was as dangerous as being too late. Intuit's 1990s online banking push was premature—customers weren't ready. The 2000s mobile efforts initially flopped—screens were too small for financial software. But when markets matured, Intuit was positioned to move quickly. The company maintained "scout" teams exploring emerging technologies without full commitment, ready to accelerate when timing aligned.

Risk management balanced bold bets with careful hedging. Every major acquisition had a Plan B: if Credit Karma integration failed, it could operate independently; if Mailchimp culture clashed, it could remain autonomous. Product innovations followed similar patterns—TurboTax Live complemented rather than replaced self-service; QuickBooks Online ran parallel to desktop for a decade. This portfolio approach meant no single bet could destroy the company.

The organizational structure enabled platform thinking while maintaining product excellence. Business units operated independently with P&L responsibility, preventing bureaucratic slowdown. But platform teams—data, AI, infrastructure—served all units, ensuring coherence. This matrix structure was complex but necessary, balancing autonomy with integration. Regular rotation programs moved talent across units, spreading best practices and preventing silos.

The lesson for other companies was clear but difficult to execute: platform success requires patient capital, cultural flexibility, and willingness to cannibalize existing products. Most companies fail at one of these requirements. They lack patience for multi-year integrations. They force cultural conformity that kills innovation. They protect legacy products too long. Intuit succeeded by accepting these tensions rather than resolving them prematurely.

X. Analysis & Investment Case

The numbers tell a compelling story, but the moats tell a better one. Intuit's competitive advantages aren't just traditional software switching costs—though those certainly exist when a small business has seven years of QuickBooks data or a consumer has a decade of TurboTax returns. The real moats are more subtle and more durable: regulatory complexity that takes decades to master, trust earned through billions of successful transactions, and network effects that compound with every customer interaction.

Consider the regulatory moat first. TurboTax doesn't just calculate taxes—it embodies decades of accumulated knowledge about IRS rules, state variations, and edge cases that would take competitors years to replicate. The product handles military combat pay differently than foreign earned income, understands Arkansas's border city exemptions, and knows which Vermont towns have local option taxes. This isn't software development; it's institutional knowledge crystallized into code. When tax laws change—as they do constantly—Intuit's relationships with regulators and army of tax experts enable rapid updates that smaller competitors can't match.

The trust moat runs deeper than brand recognition. When consumers enter their Social Security numbers into TurboTax or connect their bank accounts to Mint, they're expressing profound trust earned over decades. Credit Karma members share their complete financial picture—debts, income, credit history—because they believe Intuit will protect their data and provide valuable insights. This trust can't be purchased through marketing or replicated through technology. It's earned through millions of successful interactions and destroyed by a single breach. Intuit's security infrastructure, with billions invested in protection, creates a barrier that startups can't afford to match.

The financial profile reveals a business with exceptional unit economics improving over time. Fiscal 2024 operating margins reached 35%, up from 25% five years prior, despite heavy AI investment. This margin expansion during transformation is rare—most companies sacrifice profitability while pivoting. But Intuit's subscription model, with 85% recurring revenue, provides stability for investment. Customer acquisition costs continue declining through cross-platform referrals, while lifetime values increase through ecosystem lock-in.

The capital efficiency metrics impress even more. Return on invested capital exceeds 20%, remarkable for a company making multi-billion dollar acquisitions. Free cash flow conversion approaches 30% of revenue, funding both growth investment and shareholder returns. The balance sheet remains conservative with net debt/EBITDA below 2x despite recent acquisitions. This financial strength provides flexibility for opportunistic moves while maintaining dividend growth—16% increase in 2024, the 13th consecutive annual raise.

Yet risks lurk beneath the surface strength. AI disruption presents both opportunity and threat—while Intuit leads in financial AI, new large language models could enable competitors to leapfrog current capabilities. Regulatory changes pose constant challenges: IRS Direct File threatens TurboTax's free-file funnel, open banking regulations could commoditize Mint's aggregation advantage, and small business lending regulations might limit Credit Karma's recommendation revenue. Consumer privacy concerns intensify as Intuit collects more data for AI training, creating tension between personalization and protection.

The competitive landscape is evolving rapidly. Block (formerly Square) attacks from payments, expanding into accounting and tax. PayPal pushes into small business services. Even Microsoft, after failing with Money, sees opportunity in financial services through AI. But Intuit's response demonstrates resilience—rather than defending narrow products, they're expanding the battlefield through platform breadth that point-solution competitors can't match.

The bull case rests on three pillars. First, platform dominance creates winner-take-all dynamics in SMB financial software. As switching costs increase and network effects compound, Intuit's market share grows despite competition. Second, AI leadership accelerates competitive advantages. With more financial data than any competitor, Intuit's AI models improve faster, creating a virtuous cycle. Third, SMB digitization remains early—only 30% of small businesses use cloud accounting, suggesting years of growth ahead.

International expansion offers untapped potential. While Intuit generates 90% of revenue in North America, global SMB software markets are growing faster. The AI platform strategy enables easier localization than traditional software. Credit Karma's UK launch and QuickBooks' European expansion demonstrate early success. If Intuit captures even modest international share, it could add billions in revenue.

The bear case focuses on three vulnerabilities. Valuation appears stretched at 35x forward earnings, well above historical averages and software peer medians. Any execution stumble—integration delays, AI disappointments, security breaches—could trigger multiple compression. Second, platform complexity increases execution risk. Managing distinct businesses with different models (subscription, advertising, transaction) while maintaining integration requires exceptional operational excellence. Third, competitive threats multiply as financial services boundaries blur. Every tech giant, bank, and fintech startup sees opportunity in Intuit's markets.

The cyclical exposure through Credit Karma adds volatility previously absent. During recessions, lending partners pull back, reducing Credit Karma's recommendation revenue. Small businesses—QuickBooks' core market—suffer disproportionately in downturns. While subscription revenue provides stability, usage-based components (payments, payroll) would decline. This cyclicality wasn't present when Intuit was purely desktop software, making financial modeling more complex. The recent fiscal 2025 guidance paints an optimistic picture: revenue of $18.723-18.760 billion (15% growth), GAAP operating income of $4.898-4.918 billion (35% growth), non-GAAP operating income of $7.543-7.563 billion (18% growth), GAAP diluted EPS of $13.19-13.24 (26-27% growth), and non-GAAP diluted EPS of $20.07-20.12 (18-19% growth). These aren't just beats against consensus—they're acceleration during supposed maturity.

The segment performance reveals strategic success. Total revenue grew to $16.3 billion (up 13% year-over-year), with combined platform revenue—including Small Business Online Ecosystem, TurboTax Online, and Credit Karma—growing 14% to $12.5 billion. The Global Business Solutions Group (formerly Small Business and Self-Employed) continues as the growth engine, while Consumer Group benefits from mix shift toward higher-value assisted offerings.

The capital return framework balances growth investment with shareholder returns. The $3 billion share buyback authorization announced in 2024, combined with the 16% dividend increase, signals confidence in cash generation. Yet management maintains flexibility for opportunistic acquisitions, suggesting the M&A playbook isn't finished. The balance sheet strength—investment-grade rating, moderate leverage, substantial cash generation—provides options regardless of market conditions.

Valuation remains the primary debate among investors. Bulls argue the premium multiple reflects quality—predictable revenue, expanding margins, secular growth tailwinds. Bears counter that any disappointment—integration delays, AI development challenges, competitive pressure—could trigger multiple compression from elevated levels. The truth likely lies between: Intuit deserves a premium for execution excellence, but perfection is increasingly priced in.

The investment case ultimately depends on time horizon and risk tolerance. Short-term investors face valuation risk and potential volatility from quarterly results. Long-term investors can look through near-term fluctuations to focus on structural advantages: dominant market positions, increasing switching costs, accelerating data network effects, and management that's successfully navigated multiple technology transitions. Few companies combine Intuit's scale, growth, profitability, and competitive moats.

XI. Epilogue & Reflections

Standing in Intuit's Mountain View headquarters today, you can still find remnants of the company's scrappy origins—a framed copy of the first Quicken manual, handwritten by Tom Proulx; a photo of Scott Cook's kitchen table where the idea was born; the rejection letters from 30 venture capitalists, now displayed like trophies. These artifacts aren't just corporate memorabilia but reminders of an improbable journey from personal frustration to $200 billion market value.

The transformation from solving personal pain points to reaching this scale wasn't linear or inevitable. At every inflection point—the Microsoft assault, the internet transition, the mobile revolution, the AI transformation—Intuit could have faltered. Many contemporaries did. Broderbund, Peachtree, even Microsoft Money are footnotes in software history. Yet Intuit not only survived but thrived through four decades of technological upheaval.

What separated Intuit wasn't technical superiority—competitors often had better features. It wasn't first-mover advantage—Intuit was rarely first to market. It wasn't capital—the company bootstrapped for years while competitors had corporate backing. The differentiator was something more fundamental: an obsessive focus on customer problems rather than technology solutions. While competitors built what was possible, Intuit built what was useful.

This customer obsession manifested in countless small decisions that compounded over time. The follow-me-home program that revealed how real people actually used software. The money-back guarantee when software was sold as-is. The insistence on simple interfaces when complexity signaled sophistication. The willingness to cannibalize profitable desktop software for uncertain cloud futures. Each decision prioritized long-term customer value over short-term optimization.

The enduring power of focus on customer problems becomes clearer in retrospect. Every successful Intuit product solved a visceral pain point: Quicken eliminated checkbook balancing frustration, TurboTax removed tax filing anxiety, QuickBooks simplified small business accounting, Credit Karma democratized credit scores, Mailchimp made email marketing accessible. The products succeeded not because they were technologically advanced but because they addressed genuine human needs.

Platform thinking in the age of AI represents Intuit's latest evolution, but the principles remain unchanged. AI isn't deployed for its own sake but to solve customer problems better—predicting cash flow crunches before they occur, identifying tax deductions customers miss, recommending marketing strategies that actually work. The technology is revolutionary; the mission—powering prosperity—remains constant.

What founders can learn from 40+ years of evolution extends beyond software or financial services. First, solving real problems matters more than building cool technology. Second, customer obsession must be genuine, measured, and institutionalized—not just claimed in mission statements. Third, platform transitions require accepting short-term pain for long-term gain. Fourth, successful acquisitions preserve entrepreneurial energy rather than forcing conformity. Fifth, and perhaps most importantly, longevity requires constant reinvention while maintaining core values.

The Intuit story also illustrates the compounding power of trust. Every successful tax filing, every accurate bookkeeping entry, every helpful credit recommendation builds trust that competitors can't quickly replicate. This trust becomes permission to expand—customers who trust TurboTax with taxes are willing to try QuickBooks for business. The network effects aren't just technical but emotional.

Yet challenges loom that will test these principles. Generative AI could enable competitors to leapfrog current capabilities. Younger consumers may reject traditional financial software for embedded fintech. Regulators might restrict data usage that powers AI insights. International expansion requires adapting to different financial cultures. Each challenge echoes previous transitions—different in specifics but similar in requiring fundamental rethinking.

The final thoughts on financial software's future extend beyond Intuit to the entire category. Financial services are becoming invisible, embedded in daily activities rather than discrete tasks. AI will increasingly handle routine financial decisions, freeing humans for strategic thinking. The winners won't be those with the best algorithms but those who best understand human financial anxiety and aspiration. Technology will be table stakes; empathy will be the differentiator.

Intuit's journey from kitchen table to AI platform demonstrates that transformative companies aren't built through single innovations but through decades of consistent execution, strategic evolution, and unwavering focus on customer value. The company that helped millions balance checkbooks now helps them navigate complex financial lives. The tools have changed dramatically; the mission remains remarkably consistent.