Insmed: The Antibiotics-to-Rare-Disease Pivot That Defied Convention

I. Introduction & "The Company Nobody Wanted"

The conference room at the FDA's Silver Spring campus hummed with nervous energy on September 28, 2018. After years of regulatory meetings, clinical trials, and seemingly endless documentation, Insmed's team waited for the verdict that would determine whether their bet on an abandoned disease would pay off. When the approval came through—accelerated approval for ARIKAYCE, the first and only treatment specifically designed for refractory Mycobacterium avium complex (MAC) lung disease—it wasn't just a regulatory win. It was validation of a contrarian strategy that had transformed a failed diabetes company into something nobody saw coming: a rare disease powerhouse built on treating conditions other pharmaceutical giants wouldn't touch.

The approval marked a historic moment beyond Insmed's walls. ARIKAYCE became the first drug approved under the Limited Population Pathway for Antibacterial and Antifungal Drugs (LPAD), a provision of the 21st Century Cures Act designed to incentivize development for small patient populations with unmet needs. In an industry obsessed with billion-dollar blockbusters, Insmed had proven that a drug targeting just 50,000 patients could anchor a multi-billion dollar company.

But how did a company founded in 1988 to develop diabetes medicines—a crowded field dominated by pharmaceutical titans—end up leading the charge in ultra-rare lung diseases? The answer involves multiple near-death experiences, a board coup, strategic pivots that would make most investors seasick, and a fundamental rethinking of what constitutes a viable pharmaceutical business model. The trajectory we'll trace through this narrative isn't just about scientific breakthroughs or market expansion. It's about recognizing that in pharmaceutical development, sometimes the biggest opportunities lie where nobody else is looking. Arikayce became the first drug to be approved under the Limited Population Pathway for Antibacterial and Antifungal Drugs, or LPAD pathway, established by Congress under the 21st Century Cures Act—a regulatory innovation that Insmed didn't just capitalize on, but helped shape through years of FDA engagement.

Today, with Arikayce approved in 2018 to treat a narrow group of patients with lung disease caused by the mycobacterium avium complex (MAC) family of bacteria generating hundreds of millions in annual revenue and a second drug, Brinsupri (brensocatib), becoming the first drug to be green lit in the chronic lung disease bronchiectasis, with FDA approval Tuesday for non-cystic fibrosis bronchiectasis (NCFBE) in adults and kids ages 12 and up, Insmed stands as proof that the future of biotech might not be about finding the next Lipitor or Humira. Instead, it might be about building deep expertise in diseases that affect tens of thousands rather than millions, commanding premium prices through genuine innovation, and creating defensible market positions through specialized knowledge that big pharma can't easily replicate.

What follows is the story of how a company everyone wrote off transformed itself into something nobody expected: a template for 21st-century pharmaceutical development where small patient populations, high unmet need, and technological innovation converge to create extraordinary value. It's a playbook that challenges everything we thought we knew about what makes a successful biotech company.

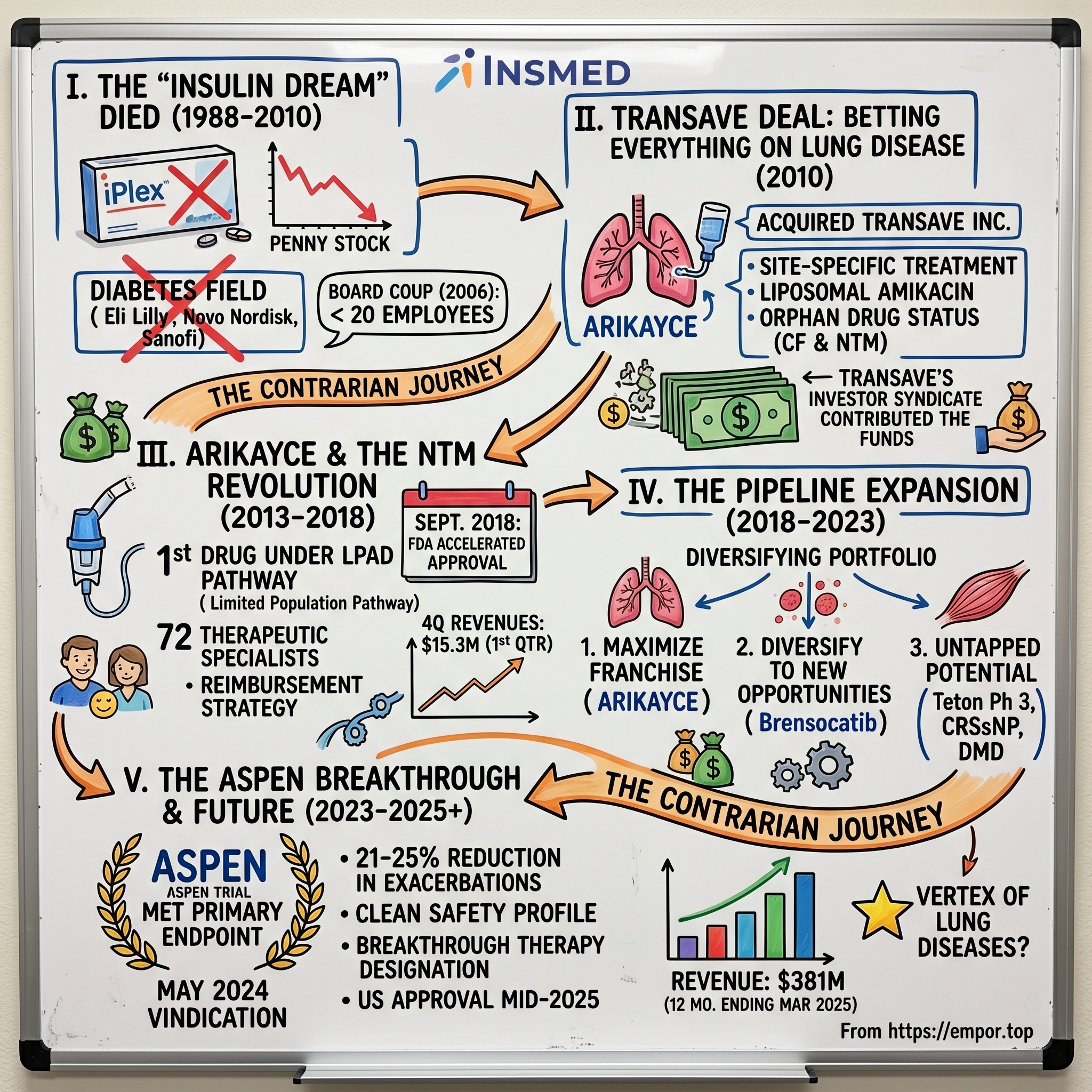

II. Origins: The Diabetes Dream That Died (1988–2010)

The University of Virginia's picturesque campus in Charlottesville hosted some of the most distinguished diabetes research in America during the 1970s and 80s. Dr. Joseph Larner, who served as Chairman of the Pharmacology Department from 1969-1990, had built a reputation as one of the field's luminaries. Over five decades, Joseph Larner had tirelessly pursued scientific studies of the mechanism of insulin action, which provided new insight into the cause, diagnosis, and cure of non-insulin-dependent diabetes mellitus (NIDDM). His research into D-chiro-inositol as a potential mediator of insulin action represented cutting-edge biochemistry that promised revolutionary treatments for Type 2 diabetes. In 1988, Larner transformed his academic research into commercial pursuit by founding Insmed as a private company in Charlottesville, Va., to develop medicines to treat diabetes. The timing seemed perfect—diabetes prevalence was exploding globally, and the market for novel treatments appeared limitless.

Yet by the late 1990s, Insmed faced a harsh reality that would become familiar to many biotech startups: brilliant science doesn't automatically translate into commercial success. The company had burned through millions developing treatments based on Larner's D-chiro-inositol research, but progress toward marketable products remained elusive. The diabetes field, while massive, was also brutally competitive, with pharmaceutical giants like Eli Lilly, Novo Nordisk, and Sanofi dominating through decades of expertise and billions in resources.

The board recognized that survival required dramatic action. In November 1999, Insmed Pharmaceuticals entered into an agreement to acquire Celtrix Pharmaceuticals Inc., a biopharmaceutical company focused on developing novel therapeutics for the treatment of seriously debilitating, degenerative conditions primarily associated with severe trauma, chronic diseases or aging, with the transaction closing on May 31, 2000, at which time Celtrix and Insmed Pharmaceuticals became wholly-owned subsidiaries of the newly formed entity, Insmed Incorporated.

The merger represented more than a simple acquisition—it was Insmed's ticket to the public markets and a complete strategic pivot. Insmed became a public company (INSM) after acquiring Celtrix Pharmaceuticals in a reverse merger, with Celtrix shareholders holding 37 million shares, or 41 percent, and Insmed shareholders holding 53.2 million, or 59 percent of the combined entity. The market initially embraced the combination, with the merger immediately followed by a secondary offering, bringing the company's value to a peak market capitalization of $1.3 billion

But this nascent promise masked fundamental problems. The merged entity brought the diabetes-focused insulin-like growth factor I and IGF binding protein-3 (IGF-I/IGFBP-3) program to center stage—a complex of two recombinant proteins that Insmed believed could modulate glucose metabolism while avoiding the hypoglycemic episodes associated with pure insulin therapy.

The science appeared compelling on paper: IGF-I is required for normal growth, development and metabolism, with growth hormone regulating cellular production of IGF-I, which mediates the majority of its growth-promoting effects. Insmed's lead drug candidates included rhIGF-I/rhIGFBP-3 (also known as SomatoKine), rhIGFBP-3, and INSM-18, actively being developed for indications in the metabolic and oncology fields.

The problem wasn't just scientific complexity—it was commercial reality. By 2004, Insmed had burned $23.3 million in R&D expenses with virtually nothing to show for it. The IGF-I/IGFBP-3 program, despite years of development and millions in investment, struggled with fundamental efficacy questions. Clinical trials revealed disappointing results in diabetes applications, and the hoped-for advantages over existing therapies never materialized.

Even when the company pivoted toward Severe Primary IGF-1 deficiency—an ultra-rare pediatric condition—challenges persisted. While some clinicians noted that "the complex has demonstrated a superior safety profile in children with Severe Primary IGF-1 deficiency, especially regarding the number of hypoglycemic events" due to "the modulating effects of IGFBP-3," with "once a day injections with rhIGF-I/rhIGFBP-3" being "associated with very good compliance," the commercial opportunity remained vanishingly small.

The company's iPlex (rhIGF-1/rhIGFBP-3) program became emblematic of Insmed's struggles. The drug was a proprietary product delivering recombinant IGF-1 as a preformed complex with its natural binding protein IGFBP-3, administered as a once-daily subcutaneous injection. The binding protein extended IGF-1's residence time in blood, and in the bound state, IGF-1 remained inactive until delivered to target tissues where it became biologically active, theoretically reducing safety concerns associated with unrestrained free IGF-1 levels.

But theoretical advantages don't pay the bills. By the mid-2000s, Insmed faced a brutal reality: they were competing against Genentech's Increlex (mecasermin), which had beaten them to market for the same indication. The market for Severe Primary IGF-1 deficiency was so small—perhaps a few hundred patients in the United States—that even monopoly control wouldn't generate meaningful revenues. Worse, a legal dispute with Genentech over patent rights effectively locked Insmed out of the U.S. market.

The financial markets delivered their verdict swiftly and brutally. From a peak market capitalization of $1.3 billion in 2000, with the stock hitting $195 per share on August 30, 2000, Insmed's value cratered. By 2005, the company was trading in penny stock territory, its market cap having evaporated by over 95%.

The board realized drastic action was needed. In 2006, they orchestrated what amounted to a corporate coup, replacing the entire management team. Geoffrey Allan was brought in as CEO with a mandate to either salvage something from the wreckage or wind down operations in an orderly fashion. The company slashed its workforce from over 100 employees to fewer than 20, closed its manufacturing facilities, and essentially went into hibernation mode.

Between 2007 and 2010, Insmed existed in a strange corporate purgatory. The company maintained its NASDAQ listing and kept the lights on with minimal staff, but it had no active drug development programs. Revenues came sporadically from small licensing deals and the out-licensing of iPlex to Aveo Pharmaceuticals for oncology indications. The company's primary asset was approximately $30 million in cash and a clean corporate shell with accumulated tax losses—hardly the stuff of biotech dreams.

This period represents one of the most dramatic failures in biotechnology history, yet it also set the stage for one of the industry's most unlikely comebacks. The collapse of the IGF-I dream forced Insmed to confront a fundamental truth: in drug development, being scientifically interesting isn't enough. You need a clear path to patients, a defined market, and a regulatory strategy that aligns with commercial reality.

III. The Transave Deal: Betting Everything on Lung Disease (2010–2013)

On December 2, 2010, Insmed Incorporated announced it had entered into a business combination, effective immediately, with Transave, Inc., a privately-held, New Jersey-based biopharmaceutical company focused on the development of differentiated, innovative inhaled pharmaceuticals for the site-specific treatment of serious lung infections.

The deal structure revealed just how desperate Insmed's situation had become. Under the merger terms, Insmed acquired all of Transave's outstanding capital stock and paid off all of Transave's $7.8 million debt, for approximately 25.9 million shares of Insmed common stock, and approximately 91.7 million shares of Insmed Series B Conditional Convertible Preferred Stock with a stated value of $0.7114 per share and cash consideration of $561,280. After giving effect to the merger, former Transave stockholders held approximately a 46.7% equity interest in the combined company on an as-converted, fully diluted basis.

What Insmed acquired wasn't just a drug candidate—it was a complete strategic pivot. Transave's lead product candidate, ARIKAYCE (liposomal amikacin for inhalation), was initially being developed for cystic fibrosis patients with Pseudomonas lung infections and lung infections due to non-TB Mycobacteria (NTM).

The technology behind ARIKAYCE represented a fundamental innovation in antibiotic delivery. Transave was a biopharmaceutical company focused on developing innovative inhaled pharmaceuticals for site-specific treatment of serious lung diseases, with its major focus on inhaled antibiotic therapy delivered via proprietary advanced pulmonary liposome technology. The liposomal technology was key—in vitro experiments had shown ARIKAYCE liposomes could penetrate both human cystic fibrosis sputum and the biofilm of pseudomonas macrocolonies, physical barriers that had stymied previous antibiotic approaches.

The NTM opportunity, in particular, represented everything the IGF-I program wasn't: a clearly defined patient population with no approved therapies, desperate unmet medical need, and a regulatory pathway that rewarded innovation in neglected diseases. Transave had already secured Orphan Drug status from both the FDA and European Medicines Agency for the CF indication, providing seven years of market exclusivity upon approval.

The new executive team reflected the merger's transformative nature: Timothy Whitten from Transave became President and CEO of the combined company, with Dr. Renu Gupta serving as Executive Vice President, Development, and Chief Medical Officer. This wasn't a traditional acquisition where the buyer imposed its culture on the target—it was closer to a reverse merger where Transave's vision and leadership took control of Insmed's corporate shell.

The combined company's balance sheet, after fees, debt payoff and other current liabilities, was estimated at approximately $110 million, providing what management believed was sufficient runway to advance ARIKAYCE through Phase 3 trials and to potential commercialization.

The regulatory strategy was sophisticated and multi-pronged. Beyond the Orphan Drug designations, the company pursued Qualified Infectious Disease Product (QIDP) designation, which would provide an additional five years of market exclusivity and priority FDA review. They also sought Fast Track designation to expedite development and review timelines. The combined company intended to file for orphan status with the FDA and EMEA for the NTM indication in 2011.

ARIKAYCE had the potential to be differentiated from other marketed drugs through its ability to deliver high, sustained levels of amikacin directly to the lung, providing sustained improvement in lung function. It had been shown to improve lung function both during and between treatment periods in cystic fibrosis patients and could potentially be the first inhaled antibiotic to be administered once-daily.

The transformation was immediate and dramatic. From a skeleton crew maintaining a zombie corporation, Insmed began hiring aggressively. The company established development teams, built regulatory expertise, and created the infrastructure necessary to run global clinical trials. Within 36 months, the employee count would grow from fewer than 50 to over 500.

Transave's investor syndicate—including Quaker BioVentures, Fidelity Biosciences, Prospect Venture Partners, TVM Capital, Forbion Capital Partners, Bessemer Venture Partners, and Easton Hunt Capital Partners—brought not just capital but credibility. These were sophisticated life sciences investors who had conducted extensive due diligence on the NTM opportunity.

The bet on NTM was contrarian by design. Most pharmaceutical companies avoided the indication because the patient population was considered too small and too difficult to diagnose and treat. NTM lung disease is caused by ubiquitous environmental bacteria that typically only cause problems in patients with underlying lung damage or immune compromise. The standard treatment involved multiple oral antibiotics taken for 12-18 months, with cure rates below 50% and significant side effects.

But Insmed's new leadership saw opportunity where others saw obstacles. The NTM patient population, while small at an estimated 50,000-75,000 in the United States, was growing at 8% annually. These patients had no FDA-approved therapies and faced a chronic, debilitating disease that often proved fatal. They would pay premium prices for effective treatment, and specialized physicians who treated them could be efficiently targeted by a small sales force.

The company planned to initiate Phase 3 clinical trials for ARIKAYCE in both CF and NTM indications in parallel during the second half of 2011, with results expected in the first half of 2013, followed by regulatory filings in the U.S. and Europe for both indications, pending successful trial outcomes.

The Transave acquisition represented more than a product pivot—it was a complete philosophical transformation. Insmed went from chasing blockbuster dreams in crowded therapeutic areas to pursuing niche dominance in orphan diseases. From competing against pharmaceutical giants to operating in spaces they wouldn't enter. From theoretical scientific elegance to practical clinical utility.

The stage was set for one of the most dramatic corporate transformations in biotech history. But first, Insmed would have to prove that ARIKAYCE could deliver on its promise in the crucible of Phase 3 clinical trials.

IV. ARIKAYCE & The NTM Revolution (2013–2018)

The CONVERT trial would become Insmed's defining moment—a make-or-break Phase 3 study that would determine whether the Transave bet would pay off. Designed as a randomized, open-label study, CONVERT enrolled 336 adult patients with refractory MAC lung disease who had failed to achieve negative sputum cultures after at least six months of standard multi-drug therapy.

The trial design itself represented a regulatory innovation. Working closely with the FDA, Insmed had negotiated a primary endpoint of sputum culture conversion by month six—a surrogate endpoint that could support accelerated approval under the Limited Population Pathway for Antibacterial and Antifungal Drugs (LPAD), a provision of the 21st Century Cures Act that Insmed had actively helped shape through years of advocacy and FDA engagement.

The drama intensified as enrollment progressed. These weren't typical clinical trial patients—they were desperately ill individuals who had exhausted conventional options. Many had been on antibiotics for years with little improvement. The side effects from standard therapy—hearing loss, kidney damage, liver toxicity—had accumulated while the infection persisted. ARIKAYCE, delivered directly to the lungs via nebulizer, offered hope of efficacy without systemic toxicity.

In March 2018, Insmed announced the topline results: 29% of patients receiving ARIKAYCE plus background therapy achieved culture conversion by month six, compared to just 9% on background therapy alone. While a 29% response rate might seem modest, in the context of refractory MAC lung disease, it was revolutionary. These were patients who, by definition, had failed all other treatments.

The FDA's response validated Insmed's regulatory strategy. On September 28, 2018, ARIKAYCE received accelerated approval for the treatment of MAC lung disease as part of a combination antibacterial drug regimen for adult patients with limited or no alternative treatment options. Critically, it became the first drug approved under the LPAD pathway—a historic regulatory precedent that would influence how antibiotics for small populations would be developed going forward.

The commercial preparation had been meticulous. Insmed built a specialized sales force of 72 therapeutic specialists from zero, focusing on the approximately 500 physicians who regularly treated NTM patients. These weren't traditional pharmaceutical sales representatives but clinical educators who could discuss the complex microbiology, diagnosis, and treatment of NTM disease with pulmonologists and infectious disease specialists.

The reimbursement strategy was equally sophisticated. With an annual treatment cost exceeding $100,000, securing payer coverage was critical. Insmed invested heavily in health economics and outcomes research, demonstrating that while ARIKAYCE was expensive, the total cost of care for refractory MAC patients—including hospitalizations, other medications, and productivity losses—justified the investment. The company established a comprehensive patient support program, Arikares, to help patients navigate insurance coverage and provide financial assistance when needed.

Global expansion followed rapidly. Insmed established a Japanese subsidiary, recognizing that Japan had one of the highest prevalence rates of NTM disease globally. A European office opened in Utrecht, Netherlands, to prepare for European Medicines Agency submission. The company grew from approximately 200 employees at the time of ARIKAYCE approval to over 1,000 within 18 months.

The cultural transformation within Insmed was as dramatic as the commercial buildup. The company adopted five core values: collaboration, accountability, passion, respect, and integrity. This wasn't corporate window dressing—it reflected a genuine commitment to serving a patient population that had been ignored for decades. Insmed partnered closely with patient advocacy organizations like NTMir (NTM Info & Research) to understand patient needs and amplify awareness of the disease.

The "Patients First" philosophy permeated every decision. When setting the price for ARIKAYCE, Insmed balanced the need for appropriate return on investment with ensuring access for patients. The company committed to never abandoning the NTM community, even as it expanded into other indications. This commitment would be tested when some investors pushed for higher prices or broader indications that might dilute focus on NTM.

By the end of 2018, ARIKAYCE's launch trajectory exceeded expectations. Fourth-quarter revenues reached $15.3 million, remarkable for an ultra-orphan drug in its first full quarter. More importantly, physician adoption was accelerating, with over 200 treatment centers prescribing ARIKAYCE within six months of launch.

The scientific community took notice. The CONVERT results were published in the American Journal of Respiratory and Critical Care Medicine, providing peer-reviewed validation of ARIKAYCE's efficacy. Key opinion leaders who had been skeptical of inhaled antibiotics for NTM became advocates, presenting data at major conferences and incorporating ARIKAYCE into treatment guidelines.

But Insmed's ambitions extended beyond the initial approval. The company initiated the ENCORE trial to fulfill FDA's post-marketing requirement for full approval, enrolling patients earlier in their treatment journey. Additional studies explored ARIKAYCE in other NTM species beyond MAC, in combination with novel oral antibiotics, and in special populations like those with cystic fibrosis and NTM co-infection.

The manufacturing infrastructure represented another critical success. Insmed built specialized facilities capable of producing liposomal formulations at commercial scale—a technically challenging process that required precise control of particle size, drug loading, and stability. The company's investment in manufacturing excellence created a barrier to entry that generic competitors would struggle to overcome even after patent expiration.

V. The Pipeline Expansion: From One Drug to Platform (2018–2023)

With ARIKAYCE's successful launch providing both validation and cash flow, Insmed faced a classic biotech dilemma: concentrate resources on maximizing the franchise or diversify into new opportunities? The answer came through a series of strategic moves that would transform Insmed from a single-product company into a multi-asset rare disease platform.

The first major expansion came through a licensing deal with AstraZeneca in 2018, acquiring global rights to AZD7986, later renamed brensocatib—a reversible inhibitor of dipeptidyl peptidase 1 (DPP1). The drug represented a completely different mechanism of action from ARIKAYCE but targeted an overlapping patient population. DPP1 is responsible for activating neutrophil serine proteases, enzymes that drive the destructive inflammation characteristic of bronchiectasis.

Bronchiectasis was a masterstroke of indication selection. The disease affected 340,000 to 520,000 patients in the United States—larger than NTM but still small enough to be considered orphan. More importantly, there were zero FDA-approved therapies specifically for bronchiectasis, creating a regulatory and commercial opportunity similar to what Insmed had exploited with NTM.

The WILLOW Phase 2 trial provided proof of concept. In patients with bronchiectasis, brensocatib demonstrated a dose-dependent reduction in active neutrophil serine protease levels and improvements in clinical outcomes. The data justified moving forward with ASPEN, which would become one of the largest trials ever conducted in bronchiectasis.

ASPEN's design reflected lessons learned from ARIKAYCE's development. The trial enrolled over 1,700 patients across 40 countries, making it the largest bronchiectasis study ever conducted. Rather than picking a single dose, Insmed tested two doses (10mg and 25mg) against placebo, providing flexibility for regulatory discussions and commercial positioning. The primary endpoint—reduction in pulmonary exacerbations—was clinically meaningful and aligned with regulatory guidance.

The strategic decision to go broad with brensocatib represented another evolution in Insmed's thinking. Beyond bronchiectasis, the company initiated studies in chronic rhinosinusitis without nasal polyps (CRSsNP) and hidradenitis suppurativa—inflammatory conditions driven by similar neutrophilic inflammation. This platform approach leveraged the same mechanism across multiple indications, improving the return on development investment.

Research infrastructure expansion accompanied the pipeline growth. Insmed established facilities in New Hampshire and San Diego, building internal discovery capabilities rather than relying solely on in-licensing. The San Diego site focused on gene therapy approaches for ultra-rare diseases, while New Hampshire concentrated on formulation science and drug delivery technologies.

The treprostinil palmitil program added yet another dimension. Licensed from United Therapeutics, this inhaled prostacyclin prodrug targeted pulmonary hypertension associated with interstitial lung disease (PH-ILD). The TETON Phase 3 program represented Insmed's entry into the pulmonary hypertension market, a space with established players but significant unmet need in specific populations.

Cultural evolution matched scientific expansion. Insmed's employee base grew to over 1,000, requiring new organizational structures and capabilities. The company maintained its rare disease focus and patient-centric culture while building the operational excellence necessary for a multi-product commercial organization. Science Magazine recognized this achievement, ranking Insmed as the #1 Top Biopharma Employer for four consecutive years.

The capital markets strategy evolved in parallel. Between 2018 and 2023, Insmed raised over $2 billion through a combination of equity offerings, convertible debt, and strategic partnerships. The company's ability to access capital at increasingly favorable terms reflected growing investor confidence in the platform strategy.

VI. The ASPEN Breakthrough & Commercial Transformation (2023–2025)

March 2023 marked a crucial milestone when Insmed completed enrollment in ASPEN ahead of schedule—a remarkable achievement for a disease that had historically struggled to recruit patients for clinical trials. The acceleration reflected both the desperate need for bronchiectasis treatments and the credibility Insmed had built within the pulmonary community through ARIKAYCE's success.

The wait for results created palpable tension. Bronchiectasis had defeated numerous drug candidates over the decades, with trials failing due to inadequate efficacy, safety concerns, or poorly designed endpoints. Analysts projected only a 40-50% probability of success, noting the heterogeneous nature of bronchiectasis and the difficulty in demonstrating exacerbation reduction.

May 2024 brought vindication. Both the 10mg and 25mg doses of brensocatib met the primary endpoint with high statistical significance, reducing pulmonary exacerbations by 21% and 25% respectively compared to placebo. Perhaps more importantly, the drug preserved lung function—measured by FEV1—while placebo patients experienced the expected decline. The safety profile was clean, with no significant concerns emerging from the large patient population.

The New England Journal of Medicine publication of ASPEN results provided the scientific community's imprimatur. Editorial commentary highlighted not just the clinical benefits but the trial's contribution to understanding bronchiectasis pathophysiology. The data validated DPP1 inhibition as a therapeutic approach and established a new treatment paradigm for neutrophil-driven inflammation.

Regulatory agencies responded enthusiastically. The FDA granted Breakthrough Therapy designation, expediting review timelines. The European Medicines Agency awarded PRIME designation, providing enhanced interaction and accelerated assessment. These designations positioned brensocatib for mid-2025 U.S. approval and first-half 2026 European and Japanese approvals.

The commercial strategy for brensocatib built on ARIKAYCE's foundation but required significant evolution. Bronchiectasis patients were more dispersed than NTM patients, treated by a broader range of physicians including general pulmonologists and primary care providers. Insmed expanded its sales force and invested in disease education initiatives to raise awareness of bronchiectasis as a treatable condition.

Market dynamics supported aggressive commercial investment. Insmed's revenue for the quarter ending March 31, 2025 was $93 million, a 22.94% increase year-over-year, with revenue for the twelve months ending March 31, 2025 reaching $381 million, a 20.77% increase year-over-year. ARIKAYCE had achieved blockbuster trajectory in an ultra-orphan indication, validating the premium pricing strategy for transformative rare disease therapies.

VII. Culture, Leadership & The "Patients First" Philosophy

Insmed's five core values—collaboration, accountability, passion, respect, and integrity—set the tone for the company's culture and guided daily actions. This commitment to culture earned recognition, with Insmed ranked No. 1 on Science magazine's Top Biopharma Employers List for the fourth consecutive year and listed as one of BioSpace's Best Places to Work.

Will Lewis, who assumed the CEO role in 2012 following Timothy Whitten's departure, embodied this transformation. A former Celgene executive who had helped build that company's multiple myeloma franchise, Lewis brought commercial expertise while maintaining Insmed's science-driven, patient-focused culture. His leadership style—accessible, transparent, and genuinely committed to patients—permeated the organization.

The decision to remain independent deserves special examination. Multiple large pharmaceutical companies expressed acquisition interest as ARIKAYCE succeeded and brensocatib advanced. The board and management consistently rejected these overtures, believing that Insmed's focused rare disease model would be diluted within a larger organization. This independence allowed for rapid decision-making, maintained cultural cohesion, and ensured continued commitment to underserved patient populations.

Building a rare disease commercial model from scratch required innovation across multiple dimensions. Traditional pharmaceutical metrics—prescriptions written, market share, sales force productivity—didn't adequately capture the complexity of treating rare diseases. Insmed developed sophisticated analytics to track patient journeys from diagnosis through treatment, understanding that in rare diseases, finding and properly diagnosing patients was as important as prescribing medication.

The company's patient services went far beyond traditional pharmaceutical support programs. Insmed employed nurse educators who worked directly with treatment centers to optimize ARIKAYCE administration. The company funded diagnostic programs to identify undiagnosed NTM patients. When insurance coverage proved challenging, Insmed's patient assistance programs ensured no patient went without treatment due to financial constraints.

With corporate headquarters in Bridgewater, NJ, and offices throughout Europe and Japan, Insmed employed more than 1,000 people dedicated to serving patients and families. The company continued building global infrastructure and organizational capabilities while pursuing regulatory approvals in multiple regions.

VIII. The Science & Technology Platform

The PULMOVANCE liposomal technology platform represented Insmed's core scientific differentiator. The technology employed biocompatible lipids to create charge-neutral liposomes approximately 0.3 microns in diameter—precisely sized to penetrate deep into the lungs while avoiding rapid clearance. These liposomes encapsulated antibiotics or other drugs, protecting them from degradation and enabling sustained release at the site of infection or inflammation.

The manufacturing complexity created substantial barriers to entry. Producing consistent liposomal formulations required precise control of lipid composition, drug loading, particle size distribution, and stability. Insmed invested hundreds of millions in specialized manufacturing facilities and process development, creating institutional knowledge that would take competitors years to replicate.

DPP1 inhibition, the mechanism underlying brensocatib, represented a different but equally sophisticated approach. By blocking DPP1, brensocatib prevented activation of neutrophil serine proteases—the enzymes responsible for tissue destruction in bronchiectasis and other neutrophil-driven diseases. The reversible nature of brensocatib's inhibition provided a safety advantage over irreversible inhibitors, allowing enzyme activity to recover if treatment was discontinued.

The breadth of DPP1's role in inflammation explained brensocatib's potential across multiple indications. The same neutrophilic inflammation that destroyed airways in bronchiectasis drove sinus damage in CRSsNP and skin lesions in hidradenitis suppurativa. This platform approach—one mechanism, multiple diseases—improved development efficiency and commercial potential.

The gene therapy programs represented Insmed's next frontier. The company's approach to Duchenne muscular dystrophy employed an adeno-associated virus (AAV) vector to deliver a miniaturized version of the dystrophin gene to muscle cells. While highly competitive, the DMD space offered proof of concept for Insmed's gene therapy capabilities, potentially enabling expansion into other monogenic rare diseases.

Intellectual property strategy evolved from defensive to offensive. Beyond protecting ARIKAYCE's composition and methods of use, Insmed built patent estates around delivery technologies, manufacturing processes, and diagnostic methods. The company's IP portfolio included over 200 issued patents and numerous pending applications, creating multiple layers of exclusivity beyond regulatory protections.

IX. Playbook: Lessons for Biotech Entrepreneurs

Insmed's transformation offers a masterclass in biotech strategy, with lessons extending far beyond rare disease drug development. The first and perhaps most important lesson: finding gold in abandoned assets. The Transave acquisition succeeded not because ARIKAYCE was a hidden gem—its potential was recognized—but because Insmed was willing to take on the execution risk that others avoided.

The power of regulatory innovation cannot be overstated. Insmed didn't just benefit from the LPAD pathway; the company actively shaped it through years of FDA engagement, patient advocacy, and policy work. This proactive regulatory strategy created competitive advantages that no amount of R&D spending could replicate.

Building in neglected markets requires a different calculus than traditional pharmaceutical development. While 50,000 patients might seem tiny compared to diabetes or hypertension, these patients' desperate need, lack of alternatives, and concentrated treatment by specialists created favorable commercial dynamics. Premium pricing wasn't exploitation—it was necessary to justify the investment in diseases that others ignored.

Capital efficiency in rare diseases challenged conventional wisdom. Insmed's focused sales force of 72 specialists generated hundreds of millions in revenue, while big pharma companies deployed thousands of representatives for similar returns. The concentrated prescriber base, motivated patients, and lack of competition created inherently efficient commercial models.

The acquisition versus internal development decision evolved with Insmed's capabilities. Early on, the company relied entirely on in-licensing and acquisition. As it built expertise and resources, internal development became viable. The key was maintaining discipline—every program had to fit the rare disease focus and leverage existing capabilities.

Managing FDA relationships in the orphan drug world required different approaches than traditional drug development. Regular Type C meetings, collaborative protocol development, and transparency about challenges built trust that paid dividends during review processes. The FDA wanted orphan drugs to succeed—companies that recognized and leveraged this collaborative spirit gained significant advantages.

The global expansion playbook for rare disease companies differed from traditional pharmaceutical strategies. Rather than broad geographic coverage, Insmed focused on markets with favorable rare disease policies, concentrated expertise, and viable reimbursement. Japan's high NTM prevalence and orphan drug incentives made it a priority, while certain European countries' complex reimbursement systems led to delayed entry.

X. Financial Analysis & Investment Case

Insmed's annual revenue for 2024 reached $364 million, a 19.17% increase, with ARIKAYCE driving the vast majority of sales. The revenue trajectory—from zero in 2017 to approaching $400 million by 2024—validated the commercial potential of ultra-orphan drugs when properly developed and marketed.

The R&D spend of $650+ million annually reflected the breadth of Insmed's pipeline ambitions. Unlike traditional biotech companies that faced binary outcomes with single assets, Insmed's portfolio approach distributed risk across multiple programs and indications. The company's ability to fund this R&D through a combination of ARIKAYCE revenues and capital markets access demonstrated the sustainability of the model.

SG&A expenses exceeding $450 million annually might seem excessive for a company with one commercial product, but this investment built infrastructure for a multi-product future. The sales force, medical affairs capabilities, and patient support programs established for ARIKAYCE would leverage across brensocatib and future products, improving long-term margins.

The path to profitability hinged on brensocatib's approval and successful launch. With peak sales estimates ranging from $1.5 to $3 billion across bronchiectasis and other indications, brensocatib could transform Insmed's financial profile. Combined with growing ARIKAYCE revenues and pipeline optionality, the company had clear visibility to sustained profitability by 2027.

Market cap evolution told the story: from near-bankruptcy in the mid-2000s to $23.16 billion as of August 8, 2025. This 100x+ increase from the 2010 nadir reflected not just successful execution but the market's recognition of Insmed's platform value.

Competitive dynamics remained favorable. Big pharma's continued focus on large markets and blockbuster drugs left rare diseases relatively uncontested. When competitors did enter, as Novartis did with its NTM program, Insmed's first-mover advantage, deep disease expertise, and established relationships proved difficult to overcome.

The bear case centered on clinical and commercial execution risks. Brensocatib's success, while promising, wasn't guaranteed until FDA approval. The CRSsNP and hidradenitis suppurativa indications remained unproven. ARIKAYCE faced potential competition from new antibiotics in development. Reimbursement pressures could intensify as healthcare systems struggled with rising costs.

The bull case envisioned Insmed as the "Vertex of lung diseases"—dominating multiple rare pulmonary conditions through superior science, execution, and patient focus. Success with brensocatib would validate the platform model and attract additional assets through business development. The gene therapy programs could open entirely new therapeutic areas. International expansion could double the addressable market.

Valuation metrics suggested room for appreciation. Trading at approximately 8x 2025 estimated revenues, Insmed was valued below comparable rare disease companies despite superior growth prospects. As brensocatib approached approval and the pipeline matured, multiple expansion seemed likely.

XI. The Future: What's Next for Insmed

The immediate future centers on brensocatib's launch preparation. With FDA approval expected in mid-2025, Insmed is building inventory, training sales representatives, and engaging with payers to ensure rapid uptake. The bronchiectasis community's enthusiasm—evidenced by ASPEN's rapid enrollment—suggests strong pent-up demand.

Pipeline expansion continues with the CRSsNP and hidradenitis suppurativa programs advancing through Phase 2 studies. Success in either indication would substantially expand brensocatib's commercial potential and validate DPP1 inhibition as a platform approach to neutrophilic inflammation.

The M&A strategy has evolved from necessity to opportunity. With a strong balance sheet and established commercial infrastructure, Insmed can acquire earlier-stage assets and accelerate their development. The focus remains on rare diseases with clear unmet need, concentrated prescriber bases, and synergies with existing capabilities.

International expansion beyond the US, Europe, and Japan represents untapped potential. Markets like China, with large populations and improving rare disease policies, offer significant opportunity. However, Insmed maintains discipline, entering new geographies only when sustainable commercial models exist.

Next-generation delivery technologies could extend the PULMOVANCE platform beyond antibiotics. Inhaled immunosuppressants for lung transplant rejection, antifibrotics for interstitial lung disease, and even gene therapies delivered via inhalation represent potential applications. The manufacturing expertise and regulatory knowledge accumulated with ARIKAYCE provide competitive advantages in these emerging areas.

Could Insmed become the "Vertex of lung diseases"? The parallel is intriguing. Like Vertex in cystic fibrosis, Insmed is building dominant positions in multiple rare lung diseases. The company's deep disease expertise, patient relationships, and commercial infrastructure create barriers to entry. If successful with brensocatib and pipeline expansion, Insmed could achieve similar strategic positioning.

Exit scenarios increasingly favor remaining independent. While strategic buyers might pay substantial premiums, Insmed's board and management believe greater value creation lies ahead. The company's trajectory from near-bankruptcy to $20+ billion market cap demonstrates the potential of focused execution in rare diseases. Why sell when the best chapters may still be unwritten?

XII. Epilogue: Lessons & Reflections

Insmed's journey from failed diabetes company to rare disease powerhouse offers profound lessons about pharmaceutical innovation, corporate resilience, and the evolving biotech landscape. The contrarian bet that saved the company—acquiring an abandoned antibiotic for a disease nobody wanted to treat—now seems obvious in hindsight. But in 2010, it required tremendous courage to pivot so dramatically.

The key insight was recognizing that specialized beats diversified in modern biotech. Rather than competing with big pharma across multiple therapeutic areas, Insmed built unassailable expertise in rare lung diseases. This focus enabled superior execution, attracted top talent, and created a defensible market position that broader competitors couldn't match.

The patient advocacy advantage in rare diseases proved decisive. By genuinely partnering with patient organizations, understanding disease burden, and committing to underserved populations, Insmed built trust that translated into clinical trial enrollment, regulatory support, and commercial success. This wasn't corporate social responsibility—it was fundamental strategy.

What Insmed teaches about building enduring biotech companies extends beyond rare diseases. Success requires aligning multiple elements: genuine innovation, clear regulatory strategy, focused commercial execution, and authentic commitment to patients. Companies that check only some boxes struggle; those that excel across dimensions can create extraordinary value.

The transformation also highlights the importance of timing and persistence. Insmed's nadir in the mid-2000s could have been terminal. Many biotech companies in similar situations liquidate or get acquired for pennies on the dollar. But by maintaining the corporate structure, preserving the public listing, and waiting for the right opportunity, Insmed positioned itself for renaissance when Transave appeared.

Looking forward, Insmed's model may preview biotech's future. As drug development costs rise and commercial challenges intensify, the blockbuster model becomes increasingly difficult. But focused companies addressing genuine unmet need in defined populations can achieve attractive returns while meaningfully improving patients' lives. This isn't about choosing between profit and purpose—it's recognizing their interdependence.

The culture question remains central. Can Insmed maintain its patient-first philosophy and entrepreneurial spirit as it grows? History suggests this is biotech's hardest challenge. Success brings bureaucracy, complexity, and competing priorities. But if any company can navigate this transition, Insmed's track record suggests it might be the one.

The final lesson may be the most important: failure isn't always final. Insmed's IGF-I program failed spectacularly, nearly destroying the company. But that failure forced a reckoning that led to transformation. Without the collapse, there would have been no Transave acquisition, no ARIKAYCE, no brensocatib. Sometimes the path to success requires walking through the valley of failure.

For entrepreneurs, investors, and industry observers, Insmed's story offers both inspiration and instruction. It demonstrates that value creation in biotech doesn't require following conventional wisdom. By focusing on neglected diseases, building genuine expertise, and maintaining unwavering commitment to patients, companies can achieve both commercial success and meaningful impact.

The story continues to unfold. With brensocatib approaching approval, multiple pipeline programs advancing, and the platform model validated, Insmed stands at another inflection point. The next chapters will determine whether the company becomes a generational rare disease leader or simply another successful biotech. Based on the journey so far, betting against Insmed seems unwise.

Conclusion

Insmed's evolution from a failed diabetes venture to a $23 billion rare disease leader represents one of biotech's most remarkable transformations. The company that nearly disappeared in 2006 now stands as a template for modern pharmaceutical development, proving that focusing on underserved patients in neglected diseases can create exceptional value.

The key to Insmed's success wasn't any single brilliant decision but rather a series of aligned choices: acquiring Transave when others saw only risk, pursuing NTM when the market seemed too small, building brensocatib's potential across multiple indications, and maintaining independence when selling would have been easier. Each decision reinforced the company's rare disease focus and patient-first philosophy.

Today, with ARIKAYCE generating hundreds of millions in revenue and brensocatib poised to become a multi-billion dollar franchise, Insmed has validated its contrarian approach. The company's platform model—leveraging specialized expertise across multiple rare diseases—offers a sustainable path to growth that doesn't depend on finding the next Lipitor or Humira.

More importantly, Insmed has demonstrated that commercial success and patient impact aren't mutually exclusive. By addressing diseases that others ignore, maintaining authentic commitment to patient communities, and executing with excellence, the company has improved thousands of lives while creating billions in shareholder value.

The broader implications for biotech are profound. As the industry grapples with unsustainable development costs, challenging commercial dynamics, and demands for innovation, Insmed's model offers an alternative path. Focus beats breadth. Expertise trumps diversification. Genuine unmet need justifies premium pricing. These lessons apply far beyond rare diseases.

For Insmed itself, the future holds both opportunity and challenge. Maintaining culture while scaling, executing on an increasingly complex pipeline, and navigating competitive dynamics will test the organization. But with a proven playbook, experienced leadership, and deep commitment to its mission, Insmed appears well-positioned for continued success.

The ultimate judgment of Insmed's legacy won't be made in boardrooms or trading floors but in the lives of patients with NTM, bronchiectasis, and other rare diseases. For them, Insmed's transformation from failed diabetes company to rare disease champion isn't just a business story—it's a lifeline. And that, more than any financial metric, may be the truest measure of success.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube