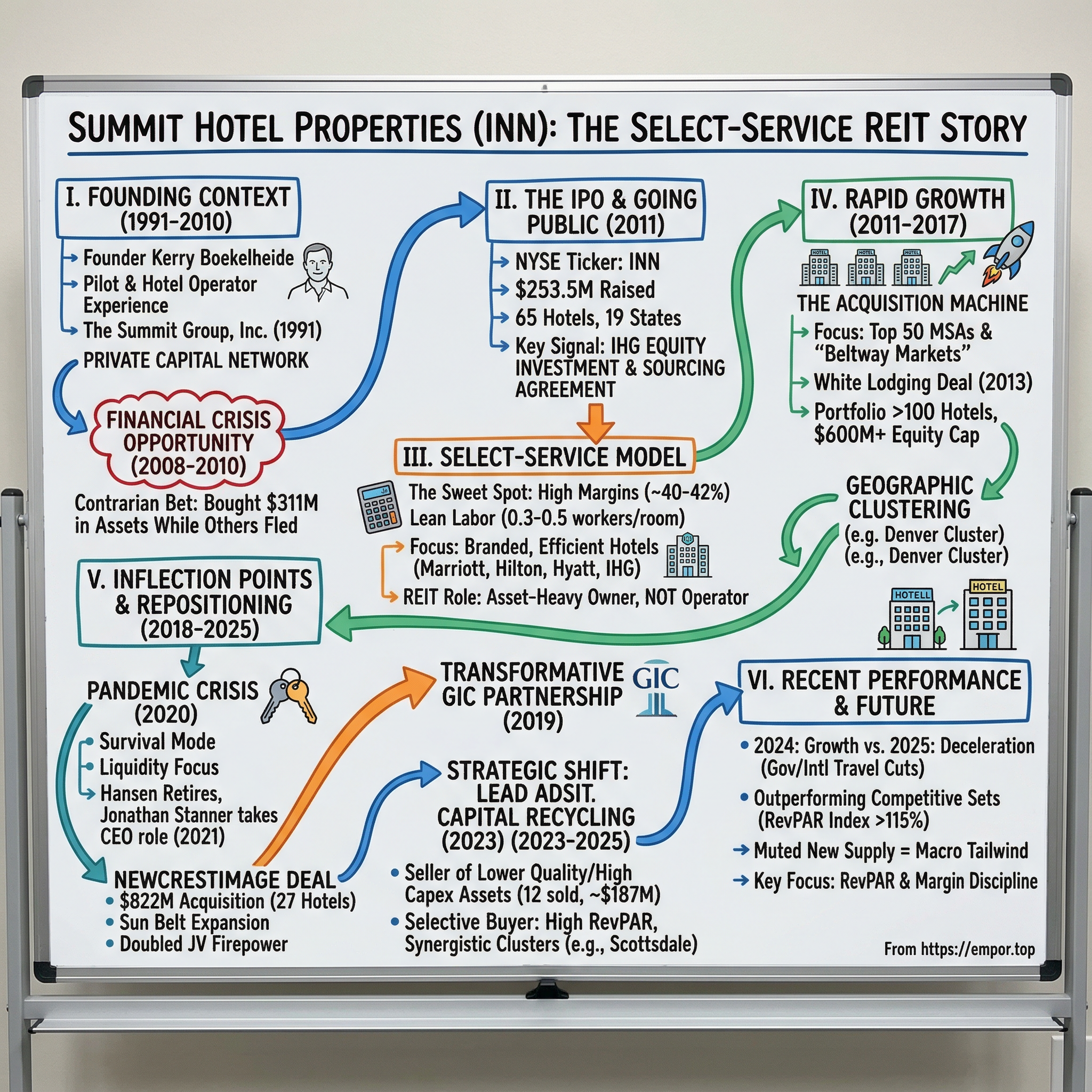

Summit Hotel Properties: The Select-Service REIT Story

I. Introduction & Episode Roadmap

Picture a stretch of highway outside Denver, Colorado, on a Tuesday evening in late 2025. Eight branded hotels sit within a few miles of each other along the beltway, each flying a different flag — a Hampton Inn here, a Courtyard by Marriott there, a Hyatt Place around the corner. They are not competitors in the traditional sense. They are all owned by the same company, a real estate investment trust based in Austin, Texas, that most retail investors have never heard of: Summit Hotel Properties, trading on the NYSE under the ticker INN.

As of late 2025, Summit owned interests in 95 lodging properties totaling more than 14,300 guestrooms spread across 24 states. The portfolio reads like a who's who of premium hotel brands — Marriott, Hilton, Hyatt, and IHG account for over 99 percent of guestrooms. Yet Summit does not operate a single one of these hotels. It does not employ the front desk clerks, manage the breakfast buffets, or set the room rates. It is a pure-play owner, a landlord in a franchise ecosystem, navigating one of the most capital-intensive and cyclically volatile corners of the real estate market.

The central question of this story is deceptively simple: how does a focused-service hotel REIT — one that does not even run its own buildings — compete against giants, survive multiple industry crises, and still find ways to create value? The answer involves a contrarian founder who learned the hotel business by flying Super 8 executives around in a Cessna, a perfectly timed IPO that caught the bottom of a real estate cycle, a sovereign wealth fund partnership that transformed the company's firepower, and a brutal pandemic that somehow became a springboard for the boldest acquisition in company history.

Summit's story sits at the intersection of real estate, hospitality, and capital allocation. It is a story about the power of focus, the discipline of knowing when to buy and when to sell, and the particular economics of a hotel segment that most people walk past without a second thought — the select-service tier. Not quite the Ritz-Carlton, not quite a Motel 6, but occupying a sweet spot that generates surprisingly attractive margins for those who understand how to operate in it.

This deep dive traces the arc from financial crisis origins through post-pandemic resilience, from a sixty-five-hotel IPO portfolio to nearly a hundred properties, through leadership transitions, strategic pivots, and the sobering realities of government travel cuts and rising insurance costs. For investors evaluating Summit today, the past fifteen years offer a masterclass in how a small REIT can punch above its weight — and the risks that come with playing in a capital-heavy industry where the next downturn is always around the corner.

II. Understanding the Select-Service Hotel Model & Industry Context

Before diving into Summit's story, it is worth pausing to understand the product it owns, because the select-service hotel model is one of the most fundamentally misunderstood segments in all of real estate investing. When people think of hotels, they tend to imagine two extremes: the grand full-service resort with its concierge desk, room service, spa, and ballroom — or the budget roadside motel with its outdoor corridors and vending machines. Select-service hotels occupy the substantial middle ground, and that middle ground turns out to be where some of the best economics in hospitality live.

A select-service hotel offers what most modern travelers actually want: a clean, well-designed room with a quality mattress, free high-speed Wi-Fi, a fitness center, and often a complimentary breakfast. What it strips away is everything that inflates the cost structure of a full-service property: bellmen, valet parking, elaborate conference facilities, high-priced restaurants and bars, room service, and the army of specialized staff required to operate all of it. Think of a Hilton Garden Inn, a Courtyard by Marriott, a Hyatt Place, or a Holiday Inn Express. These properties look and feel premium from a guest experience perspective, but they run with dramatically fewer employees per room.

The financial implications are significant. Select-service hotels have historically generated gross operating profit margins in the range of 40 to 42 percent, roughly six percentage points higher than comparable full-service properties. That margin advantage comes almost entirely from labor efficiency. A full-service hotel might employ 1.5 to 2 workers per room; a select-service property can operate with as few as 0.3 to 0.5. When labor costs are rising at mid-single-digit annual rates, as they have been since the pandemic, that structural advantage compounds.

The REIT structure adds another layer of complexity. Hotel REITs like Summit own the real estate but, to maintain their tax-advantaged REIT status, cannot directly operate the properties. Instead, Summit leases its hotels to taxable REIT subsidiaries, which in turn hire professional third-party management companies to handle day-to-day operations. This creates a triangular relationship: Summit as owner, the management company as operator, and the brand franchisor (Marriott, Hilton, etc.) as the flag that attracts guests through loyalty programs and reservation systems.

This structure means Summit's competitive advantage cannot come from running a better front desk or cooking a better omelet. It must come from capital allocation — buying the right hotels in the right markets at the right price, optimizing revenue management at the asset level, knowing when to renovate and when to sell, and managing a balance sheet through cycles. The brand franchisors hold enormous power in this ecosystem. Marriott International alone controls over 1.5 million rooms globally, and its loyalty program drives booking volume that no individual hotel owner could replicate. For Summit, the brand relationship is simultaneously its greatest asset and its most significant constraint — essential for attracting guests, but costly in franchise fees and renovation requirements.

The competitive landscape for hotel REITs is crowded and fragmented. Host Hotels and Resorts dominates the full-service end with a portfolio valued in the tens of billions. Pebblebrook Hotel Trust, Park Hotels and Resorts, and Sunstone Hotel Investors compete in various segments. Apple Hospitality REIT and Chatham Lodging Trust operate in select-service territory closer to Summit's sweet spot. In this arena, Summit has always been a relatively small player, which brings both vulnerability and agility — the ability to move quickly on deals that larger competitors might overlook, but without the scale advantages that come with a massive portfolio.

There is one more crucial aspect of the hotel REIT business model that outsiders often miss: the difference between a hotel REIT and a hotel company. When most people hear "Marriott" or "Hilton," they think of the building, the rooms, the experience. But modern Marriott International and Hilton Worldwide are primarily franchise and management companies — they make money by charging fees to property owners, not by owning hotels themselves. They are "asset-light." Hotel REITs like Summit are the opposite — they are "asset-heavy," owning the bricks and mortar while paying the franchisors for the right to use their brands. This creates a fascinating tension: the asset-light franchisors set the rules, control the loyalty programs, and collect their fees regardless of whether the hotel is profitable. The asset-heavy REITs bear the capital risk, the renovation obligations, and the operating volatility. In good times, the REIT model generates substantial returns because every dollar of incremental revenue flows through to the bottom line. In bad times, the franchisors keep collecting their fees while the REITs absorb the losses.

Understanding this context is essential because Summit's entire strategic history can be read as a series of answers to a single question: how do you build a durable competitive position in a business where you do not control the product, the brand, or the operations, and where the asset itself — a hotel room — is fundamentally commoditized?

III. Founding Context: The Financial Crisis Opportunity (2004-2010)

Kerry Boekelheide's path to founding Summit Hotel Properties began not in a boardroom, but in a cockpit. From 1980 to 1984, Boekelheide served as a certified commercial pilot and flight instructor for Super 8 Motels, Inc., flying the company's executives and ownership group around the country. But Boekelheide was not content to just fly the plane. Between flights, he was absorbing everything he could about the budget hotel business — how properties were selected, financed, developed, and managed.

By 1980, at a remarkably young age, Boekelheide had already risen to president and CEO of Super 8 Management, Inc., where he oversaw the management of more than 100 Super 8 Motels across the United States and Canada. Simultaneously, from 1983 to 1988, he partnered with a colleague in Boekelheide-Rivett Developers, Inc., personally handling site selection, financing, and construction oversight for eight new Super 8 properties. After a stint leading Super 8 Motels of Canada from 1988 to 1990, Boekelheide was ready to build something of his own.

What makes Boekelheide's story remarkable is the breadth of his early hotel experience. He was not a finance person who wandered into hospitality, nor a real estate developer who happened upon hotels. He was a hotel operator who understood every dimension of the business — from the cockpit view of site selection across the Great Plains to the ground-level reality of managing housekeeping schedules and continental breakfast logistics at a hundred properties simultaneously. That combination of strategic vision and operational granularity would prove essential in the decades ahead.

In 1991, he founded The Summit Group, Inc. in Sioux Falls, South Dakota — an unlikely headquarters for what would become a national hotel company, but a location that reflected Boekelheide's Upper Midwest roots and his ability to operate with lower overhead than competitors headquartered in expensive coastal markets. The thesis was straightforward but ambitious: acquire and develop premium-branded, focused-service hotels across the United States, targeting properties that offered the operating efficiency of budget hotels with the brand cachet and room rates of the upscale segment. Craig Aniszewski, who would become Summit's executive vice president and chief operating officer, joined Boekelheide in 1997, bringing operational rigor to complement Boekelheide's development instincts.

For the next decade, The Summit Group quietly built a portfolio, property by property, funded by private capital. Through Summit Capital Partners, LLC, which Boekelheide established in 2003, the team raised approximately $200 million from a private investor base exceeding 1,000 individuals. This was not institutional money or venture capital — it was a network of private investors, many of them from the Upper Midwest, who trusted Boekelheide's track record and deep knowledge of hotel economics.

Then came the financial crisis — and with it, the defining moment of Boekelheide's career.

When the credit markets seized up in 2008 and the economy plunged into recession, the hotel industry was devastated. Occupancy rates collapsed, RevPAR (revenue per available room, the industry's key metric) plummeted, and distressed hotel assets flooded the market. Many hotel owners were forced sellers, unable to service their debt or meet brand-mandated renovation requirements. For most players, the crisis was a catastrophe.

Boekelheide saw it differently. He saw opportunity.

In what the company would later describe as a contrarian bet, Summit invested roughly $311 million during the crisis period in development, strategic acquisitions, and property improvements. While competitors were retrenching, Summit was building its portfolio and preparing for a public market debut. The strategic logic was sound: buy when others cannot, improve the assets during the downturn when construction costs are low and contractors are hungry for work, and position the portfolio to ride the inevitable recovery in travel demand.

By 2010, Summit's predecessor entities had acquired 94 hotels and sold 28 that did not fit the long-term strategy. The remaining portfolio had been curated around a specific thesis: upscale, premium-branded, select-service hotels clustered in the top 50 U.S. metropolitan statistical areas. Not coastal gateway cities where prices were astronomical, but interior markets with reliable demand generators — corporate business parks, hospitals, universities, airports, and retail centers.

On January 12, 2004, Summit Hotel Properties, LLC had formally filed its Articles of Organization with the South Dakota Secretary of State, establishing the legal entity that would eventually become the publicly traded company. But the real founding moment was the decision to invest aggressively during the worst financial crisis in a generation. That contrarian instinct — the willingness to deploy capital when the market was paralyzed by fear — would define Summit's DNA for the next fifteen years.

The numbers tell the story. Between 1991 and 2010, Boekelheide's team acquired or developed 94 hotels and strategically sold 28 that did not fit the evolving thesis. Each sale refined the portfolio's focus, shedding properties in weaker markets or with lower-quality brand affiliations in favor of hotels that met increasingly stringent criteria for location quality, brand tier, and return on invested capital. By the time the team began preparing for a public offering, the remaining portfolio was not a random collection of crisis-era opportunistic buys — it was a curated set of assets that told a coherent investment story.

The question now was whether the public markets would agree with Boekelheide's bet.

The answer would come in February 2011, and the timing could not have been better.

IV. The IPO & Going Public: A Perfect Timing Play (2011)

The transition from private hotel company to publicly traded REIT required careful choreography. On June 30, 2010, Summit Hotel Properties, Inc. was organized as a Maryland corporation — the state of choice for most REITs due to its flexible corporate governance statutes. The plan was to merge Boekelheide's predecessor entities into a new operating partnership, contribute the hotel portfolio, and raise fresh capital through an initial public offering on the New York Stock Exchange.

The formation transactions were complex — a legal jigsaw puzzle that took months to assemble. The hotels had historically been owned through a web of limited liability companies, limited partnerships, and other entities, each managed by The Summit Group, Inc., which was wholly owned by Boekelheide himself. Some properties had individual mortgage debt; others were cross-collateralized. Some had different investor groups from different capital-raising rounds through Summit Capital Partners. The IPO would consolidate everything into a single, transparent public structure while bringing in institutional capital to fuel the next phase of growth. Getting there required merging multiple predecessor entities into a new operating partnership — Summit Hotel OP, LP — and contributing each hotel's ownership interest into the unified structure.

On February 14, 2011, Summit completed its IPO, pricing 26 million shares at $9.75 each. Valentine's Day proved to be an auspicious date. The offering raised $253.5 million, giving the company an initial equity market capitalization of roughly $364 million. The initial portfolio consisted of 65 hotels with 6,533 guestrooms located across 19 states — a significant subset of the nearly 70 properties Boekelheide's team had assembled over two decades.

The timing was exquisite.

The hotel industry was just beginning to emerge from its post-crisis trough, and industry forecasters were projecting strong recovery ahead. Colliers PKF projected RevPAR growth for upscale hotels at 8.4 percent in 2011 and 10.7 percent in 2012 — among the highest growth rates in any real estate segment. Summit was going public with a portfolio of exactly the type of hotels positioned to benefit most from this recovery.

But the IPO brought more than just capital. It brought a strategic partnership that would prove crucial. InterContinental Hotels Group, one of the world's largest hotel companies and the parent of brands like Holiday Inn, Crowne Plaza, and Staybridge Suites, purchased 1,274,000 shares of Summit common stock at the IPO — roughly a 4.7 percent stake — for $11.6 million. This was not a passive investment. Alongside the equity purchase, Summit and IHG entered into a sourcing agreement on December 2, 2010, granting IHG an exclusive five-year right of first offer to franchise or manage any unbranded hotel that Summit acquired and wished to brand.

The IHG relationship served as a powerful signal to the market. Here was one of the world's largest hotel franchisors putting real money behind Summit's strategy — essentially saying, "We believe in this team's ability to identify, acquire, and improve select-service properties, and we want to be their preferred brand partner." For a newly public REIT with a relatively small portfolio, that kind of endorsement was invaluable for attracting institutional investor attention.

The early months after the IPO were not without challenges. Managing the transition from a privately held collection of hotels to a publicly traded REIT required new governance structures, public reporting capabilities, and institutional-grade asset management processes. Some of the predecessor portfolio's hotels carried Choice Hotels brands — lower on the brand quality spectrum than Summit's target positioning — and would need to be converted or sold. Dan Hansen, who had joined the predecessor company in 2003 and had prior experience with Hyatt Hotels Corporation, served as president and CEO, bringing public-company leadership skills that complemented Boekelheide's entrepreneurial roots.

The IHG deal also brought practical benefits beyond signaling. Shortly after the IPO, IHG sold Summit two properties — the 121-room Staybridge Suites Denver Cherry Creek and the 143-room Holiday Inn Atlanta-Gwinnett Place — for a combined $17 million. IHG retained management of the Holiday Inn under a long-term agreement and continued the Staybridge Suites under a license arrangement. This was exactly the kind of mutually beneficial transaction the sourcing agreement was designed to facilitate: IHG shed owned assets (consistent with its own strategy of becoming more asset-light) while Summit acquired branded properties with built-in management continuity.

Beyond IHG, Summit also brought on board a seasoned management team for the public company era. Stuart Becker, who had joined as chief financial officer in 2007, brought the financial discipline needed for public reporting and capital markets access. Christopher Eng, serving as general counsel since 2004, handled the complex legal structuring of the REIT formation and ongoing regulatory compliance. Together with Hansen and Aniszewski, this was a team that combined entrepreneurial instincts with institutional capabilities.

There is an important footnote to the IPO story that is often overlooked. The $9.75 per share pricing valued Summit's 65-hotel portfolio at roughly $5.6 million per hotel in equity market cap terms — a fraction of the replacement cost of building a new select-service property. This deep discount to intrinsic value reflected the market's lingering skepticism about the hotel sector's recovery and about a relatively unknown South Dakota operator. But for Boekelheide and his team, it meant the IPO capital could be deployed into acquisitions at a time when hotel valuations were still depressed, creating a powerful arbitrage: raise equity at one valuation, buy hotels at a lower one, and let the gap close as the recovery matured.

The market's initial reception was cautious, but the stage was set for what would become a remarkably aggressive growth phase. Summit had the capital, the brand relationships, and the industry tailwinds. The only question was how fast they could deploy.

V. Rapid Growth Phase: The Acquisition Machine (2011-2017)

Walk into the lobby of a Hampton Inn in suburban Denver circa 2013, and nothing about the experience would suggest the property was owned by a South Dakota REIT that had been public for barely two years. The brand signage was Hilton's. The front desk staff worked for a third-party management company. The continental breakfast was served under brand-mandated specifications. But behind the scenes, Summit's asset management team was analyzing daily occupancy reports, competitor rate movements, and seasonal demand patterns to squeeze every possible dollar of RevPAR from each of the rooms upstairs. This invisible layer of optimization — happening simultaneously across dozens of properties — was where Summit was building its competitive advantage.

The two years following the IPO were a blur of deal-making. Summit moved with a speed and discipline that surprised even optimistic observers. Within 24 months of going public, the company acquired 24 upscale select-service hotels under Hilton, Hyatt, InterContinental, and Marriott banners, nearly doubling its portfolio's brand quality profile. Two subsequent stock offerings — in September 2012 and January 2013 — generated an additional $232.8 million in equity capital, pushing Summit's equity market capitalization to approximately $626 million by mid-January 2013.

The acquisition strategy was not scattershot. Every deal reflected a set of specific criteria that had been refined over Boekelheide's two decades in the business. The target: upscale, premium-branded, select-service hotels in top 50 U.S. metropolitan statistical areas, preferably in "beltway market" locations rather than downtown cores. Beltway markets offered a particular combination of lower acquisition costs, proximity to corporate demand generators, and less volatile occupancy patterns than urban center hotels that depended heavily on convention and tourism traffic.

The Denver cluster exemplified the approach. Summit assembled eight select-service hotels inside the Denver metropolitan beltway, each serving slightly different market segments but all benefiting from shared demand drivers — the corporate parks along the Interstate 25 corridor, Denver International Airport traffic, the University of Denver, and the area's growing technology and energy sectors. Clustering hotels in a single market created operational synergies: shared sales teams, coordinated revenue management across properties, and the ability to "walk" guests between properties during peak demand rather than losing them to competitors.

The White Lodging portfolio acquisition in 2013 was a signature deal of this era. Summit closed on four hotels containing 786 guestrooms from affiliates of White Lodging Services Corporation for approximately $153 million. Later that same year, the company acquired the newly completed 213-room Hyatt Place in downtown Minneapolis for $32.6 million. Each acquisition fit the template — premium brand, select-service format, strong market with reliable demand generators.

By mid-2013, the portfolio had swelled to 96 hotels with over 11,200 guestrooms across 24 states. Brand concentration was a deliberate choice: Hilton, Hyatt, InterContinental, and Marriott properties constituted 93 percent of the select-service portfolio. This brand discipline ensured that Summit's hotels were plugged into the most powerful loyalty programs and reservation systems in the industry — Marriott Bonvoy, Hilton Honors, World of Hyatt, and IHG One Rewards. These programs drive a significant share of direct bookings, reducing dependence on online travel agencies like Expedia and Booking.com that charge commissions of 15 to 25 percent per reservation.

Not every acquisition worked perfectly — and this is where Summit's story diverges from the typical growth narrative that public companies love to tell. The rapid expansion required transitioning properties between management companies, converting brands on some assets, and integrating hotels with varying quality levels and capital needs. In 2014, Summit transitioned several recently acquired properties to new management partners, acknowledging that the right operator was as important as the right location. Some deals brought hotels that would later be identified as non-core — properties in secondary markets or with brands that did not align with the evolving portfolio thesis.

But the overall trajectory was unmistakable. Summit had transformed from a modest, privately held hotel company into a publicly traded REIT with genuine scale and institutional credibility. The growth was funded through a combination of equity offerings, mortgage debt assumed in acquisitions, and operating cash flow. Each stock offering diluted existing shareholders but was immediately accretive as the proceeds were deployed into properties generating yields above the cost of capital.

The capital structure supporting this growth was carefully engineered. Rather than loading up on high-cost debt, Summit used a combination of equity offerings (which diluted existing shareholders but avoided excessive leverage), assumed mortgage debt on acquired properties, and operating cash flow. The September 2012 and January 2013 equity offerings raised $232.8 million at progressively higher share prices — a signal that the public market was validating the acquisition strategy with each deal. By 2014, the portfolio had been refined to approximately 90 hotels with over 11,350 guestrooms in 22 states, reflecting ongoing dispositions of non-core assets even as new acquisitions were being closed.

The early 2014 vintage illustrates the granular deal-making. In January alone, Summit closed on the 182-room Hilton Garden Inn in Houston for $37.5 million (including $17.9 million in assumed mortgage debt) and the 98-room Hampton Inn in Santa Barbara for $27.9 million (including $12 million in assumed mortgage debt and $3.7 million in operating partnership units). The use of OP units as partial consideration was a clever financing technique — it allowed sellers to defer capital gains taxes while giving Summit an alternative currency that conserved cash.

By 2017, the growth-at-all-costs mentality was beginning to show its limits. The hotel cycle was maturing, acquisition pricing was becoming less favorable, and the market was starting to reward operational excellence over deal volume. Summit needed a new playbook, and the transition would test whether the company could evolve from a growth story to a value story.

VI. Inflection Point #1: From Growth to Quality — Portfolio Optimization (2018-2019)

There is a moment in every growth company's life when management must make a difficult admission: the era of easy growth is over. For Summit, that moment arrived around 2018. The relentless acquisition pace that had defined the post-IPO years gave way to a more measured approach — one focused less on the number of hotels owned and more on the quality of each property's contribution to the portfolio. This was not a retreat; it was a maturation. The company began actively recycling capital, selling non-core assets and redeploying proceeds into either better-positioned properties or balance sheet strengthening.

The strategic logic was straightforward but required discipline to execute. After seven years of rapid acquisition, Summit's portfolio inevitably contained a range of quality levels. Some hotels were high-RevPAR, high-margin performers in growing markets. Others were lower-RevPAR properties in secondary locations that required disproportionate capital expenditure to maintain brand standards. The optimization strategy meant identifying the bottom of the portfolio — the properties dragging down returns — and having the discipline to sell them, even at modest premiums, to reinvest in better opportunities.

This period also saw significant leadership evolution. Kerry Boekelheide, the founder who had built the predecessor company from scratch, had retired from his Executive Chairman position on July 30, 2015, stepping back after more than two decades at the helm. His departure was more than a personal milestone — it marked the end of the founder era and the beginning of professional management. Boekelheide moved on to found KWB Hotel Partners, LLC in 2014, continuing to invest in hospitality through a smaller, privately held platform. The man who had started as a corporate pilot flying Super 8 executives around the Great Plains had built a publicly traded company worth hundreds of millions of dollars. Not bad for a kid from South Dakota.

Dan Hansen, who had served as president and CEO since the IPO and held the additional title of Chairman of the Board from 2016, led the company through the maturation phase. Hansen, with his background at Hyatt Hotels Corporation and his education at South Dakota State University, brought a public-company discipline that was essential for this transition — a shift from entrepreneurial deal-making to institutional portfolio management.

The discipline of saying no proved as important as the earlier discipline of saying yes. In a market where hotel transaction volumes remained healthy and pricing was elevated, it was tempting to keep acquiring. But Summit's management recognized that marginal acquisitions at cycle-high pricing would destroy value, not create it. Instead, the company focused on asset-level improvements — renovations, revenue management optimization, and operational efficiency programs at existing properties — to drive organic growth in RevPAR and margins.

This shift also reflected broader industry dynamics. The hotel sector was deep into a mature expansion, with RevPAR growth decelerating from the double-digit recoveries of 2011 and 2012 to low-single-digit gains. New supply was accelerating in many markets, putting pressure on occupancy rates and limiting rate growth. In this environment, the winners were not the fastest acquirers but the best operators — the companies that could squeeze incremental margin from their existing portfolios while maintaining balance sheet flexibility for opportunistic moves.

By the end of 2019, Summit had quietly positioned itself for whatever came next. The portfolio was cleaner, the balance sheet more conservative, and the management team more focused on returns per dollar invested rather than total rooms owned. And in July 2019, Summit had formed a joint venture with GIC, the Singapore sovereign wealth fund — a partnership that at the time seemed like a modest strategic enhancement but would soon prove to be one of the most important decisions in the company's history. None of them knew that "what came next" would be the most devastating crisis in the history of the modern hotel industry.

VII. Inflection Point #2: The Pandemic Crisis & The NewcrestImage Deal (2020-2022)

There is a photograph from April 2020 that captures the hotel industry's darkest moment better than any earnings report: the Las Vegas Strip at midnight, every major casino hotel dark, their towering signs turned off for the first time in living memory. Across the country, the scene was repeated in miniature at every select-service hotel, every business park Courtyard, every airport Hampton Inn. The lobbies were empty. The breakfast rooms were shuttered. The parking lots held nothing but delivery trucks.

When COVID-19 shut down global travel in March 2020, the hotel industry experienced a collapse that made the 2008 financial crisis look mild by comparison. Occupancy rates across the U.S. hotel industry fell below 25 percent in April 2020 — a number so far below breakeven that many hotels simply closed their doors. For hotel REITs, the crisis was existential. Revenue evaporated overnight, but fixed costs — mortgage payments, property taxes, insurance, brand franchise fees — continued unabated.

Summit's survival strategy centered on two priorities: preserving liquidity and maintaining the physical assets. The company drew down its credit facility, suspended its dividend, and implemented aggressive cost controls across the portfolio. Third-party management companies, operating under extreme duress, furloughed most of their hotel staff. Every discretionary capital expenditure was frozen. The goal was to emerge from the pandemic with the balance sheet intact and the properties in condition to capture the eventual recovery.

The select-service model proved its worth during this crisis in ways that full-service hotel owners could only envy. With fewer employees per room, lower food and beverage exposure, and simpler operations, Summit's hotels could operate at much lower occupancy levels before burning cash. Select-service properties maintained gross operating profit margins of approximately 26 percent even in the trough of 2020 — still painful, but 11 percentage points better than full-service hotels, which were hemorrhaging money on idle restaurant staff, empty banquet halls, and shuttered spas. This structural resilience confirmed the thesis Boekelheide had articulated decades earlier: in bad times, lean operating models survive while bloated ones collapse.

The pandemic also accelerated a leadership transition that had been in the works. In December 2020, Summit announced that Dan Hansen would step down as chairman, president, and CEO, transitioning to the role of Executive Chairman effective January 15, 2021. Jonathan P. Stanner, who brought expertise in strategic planning and financial management, took over as president and CEO. Hansen would serve as Executive Chairman until his retirement at the end of 2021, ensuring a smooth handoff during an extraordinarily challenging period.

Stanner's background was notably different from his predecessors. Before joining Summit in 2017 as executive vice president and chief investment officer (later becoming CFO and treasurer in 2018), he had served as CEO of Strategic Hotels and Resorts, a NYSE-listed hotel REIT that was acquired by Blackstone in 2015. At Strategic Hotels, Stanner had held progressively senior roles from 2005 to 2015, including CFO and SVP of Capital Markets and Acquisitions. He had also worked as an investment banking analyst at Banc of America Securities. A Purdue University graduate with both a bachelor's degree in management and an MBA from the Krannert School of Management, Stanner brought a capital markets sophistication and strategic planning rigor that would prove essential for the next phase of Summit's evolution.

Then came the move that would define Summit's post-pandemic identity.

In October 2021, Summit announced that it had entered into a definitive agreement to acquire a 27-hotel portfolio from affiliates of NewcrestImage, a Texas-based hotel development and management company. The deal was structured through Summit's existing joint venture with GIC, the Singapore sovereign wealth fund that had become Summit's strategic capital partner since forming the joint venture in July 2019.

The numbers were staggering by Summit standards.

Total consideration for the transaction was approximately $822 million — comprising $776.5 million for the 27 hotels (totaling 3,709 guestrooms), $24.8 million for two parking structures, and $20.7 million for various financial incentives. At roughly $209,000 per key, the pricing reflected the quality of the assets: a curated portfolio of Marriott, Hilton, and Hyatt-branded select-service hotels concentrated in Texas, Oklahoma, and Louisiana.

The initial closing occurred on January 13, 2022, covering 26 of the 27 hotels. The remaining property — a 176-room Canopy by Hilton New Orleans that was still under construction — closed shortly thereafter. The financing was anchored by a $410 million commitment from Bank of America and Wells Fargo, structured as a four-year interest-only term loan at SOFR plus 2.86 percent.

Why did this deal make strategic sense in the middle of a still-uncertain pandemic recovery? The timing looked risky from the outside — the Omicron variant was sweeping through the country, and hotel occupancy had only partially recovered. But several strategic reasons converged that made the risk worth taking. NewcrestImage had built a high-quality portfolio of newer-vintage, well-located hotels, but as a private developer, it was facing the same liquidity pressures that afflicted many hotel owners. The GIC joint venture structure gave Summit the firepower to execute a deal of this magnitude without overleveraging the REIT's balance sheet — GIC contributed 49 percent of the equity, with Summit putting up 51 percent and serving as the joint venture's asset manager.

The acquisition roughly doubled the GIC joint venture's hotel count and dramatically expanded Summit's footprint in the Sun Belt markets of Texas and the broader Southwest. These were markets benefiting from corporate relocations, population growth, and strong leisure demand — structural tailwinds that would persist regardless of pandemic recovery dynamics.

The GIC partnership structure deserves particular attention because it represents a genuinely innovative approach to capital sourcing for a small-cap REIT. In the joint venture, Summit serves as the general partner and asset manager, contributing 51 percent of the equity and earning management fees. GIC contributes the remaining 49 percent and provides access to its deep institutional network for financing. This structure allows Summit to participate in deals that would be far too large for its balance sheet alone, while giving GIC — which manages approximately $930 billion in assets — a platform for deploying capital into a segment of U.S. hospitality that the sovereign wealth fund views favorably. For Summit, the partnership means access to patient capital without the dilution of public equity offerings. For GIC, it means access to specialized asset management expertise without having to build an in-house team.

But the deal was not without risk.

Summit was taking on significant additional debt, adding properties in a geographically concentrated region, and betting that the pandemic recovery would sustain itself. The integration of 27 hotels simultaneously tested the company's asset management capabilities, and some properties would later be flagged for potential disposition as part of ongoing portfolio optimization.

The final piece of the deal fell into place on March 29, 2022, when the joint venture closed on the 176-room Canopy by Hilton New Orleans Downtown, completing the full 27-hotel portfolio acquisition. The Canopy, a lifestyle brand within Hilton's portfolio, represented a slight departure from Summit's traditional select-service focus — a signal that the company was willing to stretch its brand range for the right asset in the right market.

The NewcrestImage acquisition was the pivotal moment of the Stanner era — a transaction that signaled Summit's ambition to be more than a small-cap curiosity in the hotel REIT space. It roughly doubled the GIC joint venture's hotel count overnight and added significant scale in the Sun Belt markets of Texas, Oklahoma, and Louisiana — regions benefiting from corporate relocations, energy sector activity, and population growth. Whether it would prove to be a brilliantly timed contrarian move — echoing Boekelheide's financial crisis acquisitions a decade earlier — or an overreach at a challenging moment would depend on execution in the years ahead.

VIII. Inflection Point #3: Strategic Repositioning — Seller to Selective Buyer (2023-2025)

In a conference room in Austin, Texas, Jonathan Stanner spread out a portfolio map in early 2023 and drew two circles — one around the properties he wanted to keep, and another around those he wanted to sell. The exercise was simple in concept but agonizing in execution: every hotel on the sell list represented a community, a management team, a brand relationship, and a stream of cash flow. But Stanner had learned at Strategic Hotels, and then through the pandemic, that portfolio quality matters more than portfolio size. The pruning had to begin.

The ink was barely dry on the NewcrestImage integration before Summit pivoted again. This time, the shift was toward active capital recycling — selling lower-quality assets to fund higher-returning investments and reduce leverage. Since 2023, Summit has sold 12 hotels generating gross proceeds of approximately $187 million, with 10 of those hotels fetching a combined $150 million over an 18-month window.

The composition of the dispositions revealed the strategic logic. Four of the ten hotels sold over that period were Hyatt Place properties. The common thread was not the brand itself, but the financial profile: these were lower-RevPAR, lower-margin hotels that required significant near-term capital investment to meet brand renovation standards. In the calculus of a focused-service hotel REIT, pouring renovation dollars into a property generating below-average returns per room makes far less sense than selling it and redeploying the capital into a higher-yielding opportunity.

President and CEO Stanner was explicit about the logic. The goal was to sell the REIT's lower-performing hotels, concentrating the portfolio on properties with stronger RevPAR profiles, better market positions, and lower capital intensity. This is the classic "pruning the portfolio" approach that the best real estate investors employ, but executing it in practice requires the discipline to accept modest gains on sales while competing for acquisitions in a market where pricing is often aggressive.

If the sell side of the ledger reflected discipline, the buy side reflected precision.

The selective acquisition side of the strategy was equally revealing. Through the GIC joint venture, Summit completed the purchase of a two-hotel portfolio — the 250-room Hampton Inn Boston-Logan Airport and the 149-room Hilton Garden Inn Tysons Corner — for a combined $96 million, representing an 8.8 percent net capitalization rate. Both properties were well-established, premium-branded hotels in high-barrier-to-entry markets near major demand generators (Logan Airport and the Tysons Corner corporate corridor in Northern Virginia).

Perhaps the most strategically elegant acquisition was the purchase of the 120-room Residence Inn Scottsdale North for $29 million in June 2023. The property was fully renovated in 2019, requiring minimal near-term capital expenditure. But the real appeal was its location: directly across North Scottsdale Road from Summit's existing Courtyard and SpringHill Suites hotels, both already owned through the GIC joint venture. Adding a third Marriott-branded property to this cluster created a sales and revenue management synergy that exceeded what any of the three hotels could achieve independently. Adjacent to TPC Scottsdale — the annual venue for the PGA Tour's WM Open, which draws over 700,000 attendees — the location offered an embedded demand driver that few hotel investments can match.

This clustering strategy is a distinctly Summit approach. By owning multiple branded hotels in close proximity, the company can cross-sell between properties, coordinate pricing strategies to maximize market-wide revenue, and share operational resources. A business traveler whose preferred Courtyard is sold out can be walked to the Residence Inn across the street rather than lost to a competitor hotel down the road. This approach does not show up in headline acquisition metrics, but it compounds in the form of higher occupancy, better rate management, and lower per-property marketing costs.

The financial mechanics of these capital recycling transactions reveal the sophistication of Stanner's approach. The 10 hotels sold over 18 months fetched a combined $150 million at a blended capitalization rate below 5 percent after accounting for foregone capital expenditure needs — essentially, the company was selling assets where the required renovation spending would have depressed actual returns well below the headline cap rate. By eliminating approximately $47 million in near-term renovation obligations through these sales, Summit effectively boosted its free cash flow by avoiding non-discretionary spending. Meanwhile, the acquisitions were completed at cap rates of 8 to 9 percent — a roughly 300-basis-point positive spread that created immediate value for shareholders.

This spread between disposition cap rates and acquisition cap rates is the engine of the capital recycling strategy. Sell a lower-quality hotel at a 5 percent cap rate, buy a higher-quality hotel at an 8.5 percent cap rate, and you have transformed the same dollar of invested capital from a low-returning, high-maintenance asset into a high-returning, low-maintenance one. The cumulative effect over two years of disciplined execution was a portfolio that was smaller by count but meaningfully better by every quality metric.

By 2025, the company owned fewer hotels than at its peak, but the remaining properties were generating higher RevPAR per room, with better margins and lower deferred maintenance risk. The capital recycling program also facilitated nearly a full turn reduction in Summit's Net Debt to Adjusted EBITDAre leverage ratio — a critical improvement for a company operating in a cyclically volatile industry. For investors evaluating Summit, the key question was whether this quality improvement would translate into a re-rating of the stock — whether the market would begin to value Summit not as a small-cap hotel REIT with a bloated portfolio, but as a focused operator of premium select-service assets in well-chosen markets.

IX. The Business Model Deep Dive

To understand how Summit actually makes money, imagine a single hotel — say, a 150-room Hilton Garden Inn in a suburban market outside Atlanta. The property sits near a corporate office park, a regional medical center, and an interstate interchange. On any given night, business travelers from the nearby offices, visiting families of hospital patients, and road-tripping families heading south fill some portion of those 150 rooms at an average rate of roughly $140 per night. Multiply the rooms sold by the rate charged, and that is the top line. Everything below that line — the housekeeper who cleans the room, the electricity that powers it, the franchise fee paid to Hilton, the management fee paid to the operating company, the property taxes owed to the county — determines whether Summit earns a return on its investment.

At its core, Summit Hotel Properties operates a simple business: it owns hotels and collects the profits from their operation after paying management companies, brand franchise fees, and property-level expenses. Room revenue dominates the top line, accounting for the vast majority of hotel income. Ancillary revenue from parking, meeting rooms, and sundry operations contributes a smaller but growing share, particularly at properties with attached parking structures or in markets where event-driven demand creates opportunities.

The brand partnership is both the engine and the governor of the business model. Operating under flags like Marriott's Courtyard and Residence Inn, Hilton's Hampton Inn and Hilton Garden Inn, Hyatt Place and Hyatt House, and IHG's Holiday Inn Express and Staybridge Suites, Summit's hotels benefit from massive global reservation systems, loyalty programs with hundreds of millions of members, and national marketing campaigns that no independent hotel could replicate. In return, Summit pays franchise fees typically ranging from 10 to 12 percent of gross room revenue — a significant but unavoidable cost of doing business in branded hospitality.

The third-party management structure adds another dimension. Because hotel REITs cannot directly operate their properties under tax law, Summit contracts with professional management companies to run each hotel. These managers handle staffing, guest services, procurement, and day-to-day operations. Summit's role is that of asset manager: setting strategy, approving budgets, overseeing capital expenditure programs, monitoring performance metrics, and holding management companies accountable for execution. This creates a model where Summit's competitive advantage must reside in asset management expertise — the ability to identify operational improvements, implement revenue management strategies, and control costs more effectively than peers who own similar hotels with similar brands.

Revenue management is where much of the value creation happens — the hidden engine room of hotel economics.

Summit's asset management team analyzes demand patterns, competitor pricing, booking velocity, and market events to guide the third-party managers on rate-setting and inventory allocation. The goal is to maximize RevPAR — the product of occupancy rate and average daily rate — which is the single most important operating metric in hotel economics. Even modest improvements in RevPAR flow almost entirely to the bottom line because most hotel costs are fixed or semi-fixed. A hotel that increases RevPAR by three percent on a base of $120 per room generates an incremental $3.60 per room per night, and on a 150-room hotel operating 365 days a year, that translates to nearly $200,000 in additional revenue, most of which drops to operating profit.

Capital allocation is the other critical competency — and arguably the one that separates exceptional hotel REITs from mediocre ones.

Summit must continuously decide where to invest renovation dollars, which properties to acquire, which to sell, and how to finance the portfolio. The company has demonstrated a disciplined approach to this over the past decade, marked by accretive acquisitions at reasonable cap rates, timely divestitures of non-core assets, and proactive debt management. The decision to push significant debt maturities out to 2028 through a combination of refinancing and the repayment of $287.5 million in convertible notes using a delayed draw term loan reflects exactly the kind of balance sheet foresight that separates well-managed REITs from overleveraged ones.

Geographic and brand diversification serves as risk management. With properties in 24 states and exposure to all four major hotel brand families, Summit is not overly dependent on any single market or franchisor. The clustering strategy within individual markets adds a layer of operational synergy without creating geographic concentration risk at the portfolio level. With approximately 50 percent of the portfolio in urban markets and 25 percent in suburban locations, Summit has deliberately tilted toward markets with diverse demand generators — corporate headquarters, hospitals, universities, government facilities, and transportation hubs — rather than seasonal or tourism-dependent destinations. This demand diversity provides a natural hedge: when corporate travel softens, hospital visitation and university events provide a floor; when government travel declines, corporate and leisure segments help offset the loss.

A word on how franchise fees work, because this cost is often underappreciated by investors. A typical franchise agreement requires the hotel owner to pay an initial franchise fee, an ongoing royalty of 4 to 6 percent of gross room revenue, a marketing contribution of 2 to 3 percent, and a reservation system fee of 2 to 3 percent. Combined, these fees consume 10 to 12 percent of every dollar of room revenue before the hotel owner sees any operating income. In exchange, the hotel gains access to the brand's reservation system, loyalty program, quality assurance standards, and national marketing campaigns. For Summit, which operates over 99 percent of its rooms under premium brands, these fees represent one of the largest line items in the cost structure — a permanent drag on margins that is the price of admission to the branded hotel ecosystem.

The RevPAR obsession that drives this industry is not arbitrary. Because hotel rooms are a perishable inventory — an unsold room tonight cannot be sold tomorrow — the ability to maximize revenue per available room on a daily basis is the fundamental operating challenge. Unlike apartments or office buildings where leases provide long-term revenue visibility, hotels re-price their entire inventory every single night. This makes hotel REITs more volatile than most real estate subsectors but also creates the potential for faster organic growth when conditions are favorable.

To understand how dramatically this differs from other real estate sectors, consider the comparison. An office REIT with a 10-year lease knows its rental income for the next decade. A hotel REIT with the same square footage has no guaranteed revenue beyond tonight. Every morning, the revenue management team at each hotel wakes up to essentially an empty spreadsheet — all 150 rooms (or however many) are available, and the goal is to fill as many as possible at the highest possible rate before midnight. This daily repricing mechanism is why hotel REITs trade at wider valuation swings than apartment, industrial, or office REITs. It is also why asset management expertise — the ability to optimize this daily auction across dozens or hundreds of properties simultaneously — is the critical differentiator in the space.

Summit's sustainability initiatives also merit mention. As institutional investors and brand partners increasingly prioritize ESG performance, Summit benefits from a structural advantage: select-service hotels have inherently smaller environmental footprints than full-service properties. Less food and beverage waste, smaller buildings, lower energy intensity per room, and simpler mechanical systems all translate to a more favorable sustainability profile. As Marriott, Hilton, and IHG roll out increasingly stringent carbon reduction targets for their franchise networks, Summit's efficient property designs should require less incremental capital to meet these standards than older, more complex full-service assets.

X. Recent Performance & Current Challenges (2024-2025)

The numbers tell one story. The context tells another. To understand Summit's recent performance, one must hold both in mind simultaneously — because the headline figures mask significant operational outperformance that the stock market has stubbornly refused to recognize.

Summit's 2024 results offered a story of modest progress. Full-year operating income reached $103.5 million, with adjusted funds from operations — the key earnings metric for REITs — increasing 5.6 percent to $0.96 per diluted share. Pro forma RevPAR grew 1.8 percent to $124.13 for the full year, a respectable result in an environment where the broader hotel industry was seeing similar low-single-digit growth. The balance sheet as of December 31, 2024, showed outstanding debt of $1.1 billion with a weighted average interest rate of 4.55 percent and total liquidity of approximately $350 million.

Then 2025 brought a different reality.

The year was marked by a meaningful deceleration in performance driven by two factors largely outside Summit's control: a sharp decline in government-related travel demand and a pullback in international inbound visitors. Together, these segments represented approximately 10 to 15 percent of total room nights across the portfolio. When they declined by roughly 20 percent on a blended basis, the impact rippled through Summit's results.

Same-store RevPAR fell 1.8 percent for the full year 2025 to $121.73, with the sharpest decline in the third quarter when same-store RevPAR dropped 3.7 percent to $115.77. The RevPAR decline was driven predominantly by lower average daily rates as the company's hotels shifted toward lower-rated demand segments to backfill the lost government and international business. Total revenues slipped modestly to $729.5 million from $731.8 million in 2024, but the real pain showed in profitability: adjusted EBITDAre fell 9.0 percent to $174.9 million, and adjusted FFO declined to $103.6 million, or $0.85 per diluted share — an 11.5 percent decline from the prior year.

The government travel decline, which accelerated sharply in the fourth quarter amid federal budget uncertainty and workforce reductions, was particularly frustrating because it had nothing to do with Summit's operational execution. This is the challenge of owning hotels in an economy increasingly subject to policy-driven volatility. When federal agencies cut travel budgets or entire departments freeze non-essential travel, hotel owners in markets with significant government demand — Washington D.C. suburbs, military base communities, state capitals — feel the pain immediately. Summit's Hilton Garden Inn Tysons Corner, acquired just months earlier, sat in the heart of this weakness.

Yet there were important silver linings beneath the headline numbers.

The company's RevPAR Index — a measure of how Summit's hotels perform relative to their competitive sets — improved by 140 basis points during the third quarter to approximately 116 percent. This meant that even as the overall market softened, Summit's properties were gaining market share from local competitors. Excluding government and international inbound segments, fourth-quarter RevPAR actually increased roughly 60 basis points year over year. The operational efficiency discipline continued to deliver, with operating expense growth held to low single digits through careful labor management and non-rooms revenue initiatives.

On the balance sheet front, the company executed a critical — and often underappreciated — refinancing. The $287.5 million in convertible notes maturing in February 2026 were addressed through a $275 million delayed draw term loan closed in March 2025, combined with revolver draws. The result was transformative for the maturity profile: Summit exited 2025 with virtually no significant debt maturities until 2028, a weighted average debt maturity of approximately four years, and 75 percent of its pro rata debt at fixed interest rates with an average fixed SOFR rate of around 3 percent.

One notable bright spot amid the challenging 2025 results was Summit's continued outperformance versus its competitive sets. The company's proprietary revenue management platform — developed in-house and a point of particular pride for the Stanner management team — helped Summit's hotels capture a disproportionate share of available demand even as the overall pie was shrinking. This in-house revenue management capability represents a genuine operational differentiator relative to peers who rely entirely on third-party management companies for pricing decisions. Summit's asset management team can identify market-specific opportunities and implement pricing strategies faster than a distant third-party manager might, particularly during demand spikes around events, conventions, or seasonal patterns.

For 2026, management guided to RevPAR growth of zero to 3 percent, adjusted EBITDA of $167 million to $181 million, and adjusted FFO of $0.73 to $0.85 per share. The guidance incorporated expectations that government travel comparisons would ease, that strong special event demand — including FIFA World Cup matches in six of Summit's markets — would provide a boost, and that corporate transient and group demand would continue to strengthen.

The stock market's verdict on all of this has been harsh. Summit's shares traded in a 52-week range of $3.57 to $6.99, with the stock declining nearly 20 percent over the trailing twelve months. The lodging REIT sector as a whole returned negative 17.2 percent through March 31, 2025, reflecting broader concerns about lingering inflation, softening consumer sentiment, and economic uncertainty. Summit's small-cap status amplifies its vulnerability to these sector-wide headwinds.

The disconnect between operational execution and stock performance is worth dwelling on. Summit's hotels continued to gain market share — the RevPAR Index above 115 percent meant they were outperforming their competitive sets even as the absolute numbers declined. Operating expenses grew at less than 2 percent — a remarkable feat when the industry as a whole was grappling with labor cost increases of 9 percent on a per-available-room basis and insurance premium increases of 17 percent. In 2024, combined hotel industry expenses above gross operating profit increased 4.1 percent year-over-year, exceeding the 2.3 percent increase in total hotel revenue — a scissors effect squeezing profitability industry-wide. Summit managed this squeeze better than most, but the market rewarded none of it.

For long-term investors, the question is whether the stock's decline reflects a temporary mispricing driven by sector-wide sentiment, or a more fundamental re-rating of hotel REIT valuations in a world of structurally lower RevPAR growth and structurally higher operating costs.

XI. Porter's Five Forces Analysis

Porter's Five Forces framework reveals the structural dynamics that shape Summit's competitive environment — and some of the forces are more favorable than they might initially appear.

Threat of New Entrants: Moderate-High. Building or acquiring a portfolio of premium-branded select-service hotels requires substantial capital — a single property can cost $20 million to $50 million, and a meaningful portfolio demands hundreds of millions in equity and debt. Securing franchise agreements with top brands requires operational track records and financial credibility that new entrants may lack. The franchise approval process itself acts as a barrier: Marriott, Hilton, and Hyatt evaluate potential franchisees on financial strength, operational experience, and track record before granting a franchise license. A first-time hotel owner cannot simply buy a building and hang a Hilton flag. However, private equity firms and sovereign wealth funds have shown willingness to enter the space through platform acquisitions, as demonstrated by KSL Capital's $1.4 billion take-private of Hersha Hospitality Trust. The barriers are real but not insurmountable for well-capitalized entrants who can acquire an existing platform rather than building one from scratch.

Bargaining Power of Suppliers: Moderate. The most powerful suppliers in Summit's ecosystem are the brand franchisors themselves — Marriott, Hilton, Hyatt, and IHG. These companies control the franchise agreements, set brand standards (including mandatory renovation cycles), operate the loyalty programs that drive bookings, and charge franchise fees that typically consume 10 to 12 percent of gross room revenue. Summit has virtually no negotiating leverage on franchise fees or brand standards with these global giants. Third-party management companies represent another supplier category, though the market for hotel managers is competitive enough that Summit can negotiate reasonable terms and switch operators if performance lags. Labor is the wild card — wage rates have been growing at mid-single-digit annual rates since the pandemic, and the select-service segment's lower staffing levels offer only partial insulation. Rising property insurance premiums and aggressive property tax assessments add further cost pressure that Summit cannot easily pass through to guests.

Bargaining Power of Buyers: Moderate-High. Hotel guests in the select-service segment are notably price-sensitive. Corporate travel departments negotiate bulk rates and increasingly use data analytics to optimize hotel spending. Online travel agencies like Expedia and Booking.com provide price transparency that limits hotels' ability to extract premium pricing. Brand loyalty programs create some stickiness — a dedicated Marriott Bonvoy member may prefer the Courtyard over a competing brand — but switching costs for the average traveler are essentially zero. The rise of Airbnb and alternative accommodations has further empowered buyers by expanding the competitive set beyond traditional hotels.

Threat of Substitutes: Moderate. Airbnb and vacation rental platforms represent the most visible substitute threat, though their impact varies significantly by segment. For leisure travelers in resort and destination markets, short-term rentals offer a compelling alternative. For business travelers — Summit's core customer — the substitution threat is lower, as corporate travel policies typically require branded hotels with standardized safety, security, and billing capabilities. Extended-stay apartments, hybrid work arrangements that permanently reduce business travel frequency, and the growth of cruise vacations as an alternative leisure option all represent substitution pressures. The structural shift toward remote and hybrid work may be the most consequential long-term substitute threat, as companies that once booked hundreds of hotel room nights annually now manage with a fraction of that travel.

Competitive Rivalry: High. The hotel REIT landscape is crowded and intensely competitive. Host Hotels and Resorts, with a portfolio valued in the tens of billions, dominates the full-service segment. Pebblebrook Hotel Trust, Park Hotels and Resorts, Sunstone Hotel Investors, Apple Hospitality REIT, RLJ Lodging Trust, and Chatham Lodging Trust all compete for similar assets in similar markets. Apple Hospitality REIT, with its focus on premium-branded, select-service properties, is Summit's most direct public-market competitor and commands a significantly larger portfolio and market capitalization. RLJ Lodging Trust, with 94 hotels and approximately 21,000 rooms focused on premium-branded, high-margin properties, represents another formidable peer. In 2024, publicly listed hotel REITs actively pursued consolidation, collectively investing $1.5 billion in acquisitions. The select-service segment, while large, offers limited differentiation opportunities — a Hilton Garden Inn in Denver is functionally similar to a Hilton Garden Inn in Dallas. Competition plays out primarily through capital allocation skill, asset management execution, and balance sheet management rather than through product differentiation.

XII. Hamilton's 7 Powers Framework Analysis

Hamilton Helmer's 7 Powers framework provides a lens for evaluating where Summit's competitive advantages actually reside — and just as importantly, where they do not.

Scale Economies: Weak-Moderate. Summit's portfolio of 95 hotels, while substantial, is small relative to the largest hotel REITs. Host Hotels and Resorts, for example, owns roughly 80 properties but with dramatically higher total value due to its focus on luxury and upper-upscale assets. Scale advantages in hotel REIT ownership are modest — there are some benefits in corporate overhead leverage, brand negotiating power, and access to capital markets, but these diminish beyond a certain portfolio size. Summit's clustering strategy generates localized scale advantages within specific markets, but these are geographic rather than enterprise-wide. The company is large enough to be taken seriously by institutional investors and brand partners, but not so large that scale alone creates a meaningful cost advantage.

Network Effects: None. Hotel ownership does not generate network effects. Each additional hotel in Summit's portfolio does not make the existing hotels more valuable to guests. The brand loyalty programs that do create network-like dynamics — where more hotels in a system make the loyalty program more attractive — are owned by the franchisors, not by Summit. This is a fundamental structural limitation of the hotel REIT model.

Counter-Positioning: Moderate. This is perhaps Summit's most interesting power to analyze. Summit's exclusive focus on select-service hotels represents a form of counter-positioning against both full-service hotel REITs and asset-light hotel franchisors. Full-service REITs like Host Hotels carry much higher operating costs, more volatile revenue streams, and greater exposure to convention and group cancellation risk. Summit's lean cost structure provides resilience during downturns that full-service peers cannot match. Against asset-light operators like Wyndham Hotels, Summit's model offers direct operational control and the full economic upside of property ownership, whereas Wyndham benefits from wider market positioning and scalability without capital intensity. Neither model is universally superior — the advantage shifts depending on where in the cycle you are — but Summit's positioning gives it a distinctive risk-return profile.

Switching Costs: Low. For travelers, there are essentially no switching costs between hotels. Brand loyalty programs create some friction, but a Hilton Honors member will happily stay at a Marriott if the price or location is better. For Summit as a property owner, switching brands on a hotel is possible but costly — requiring franchise termination, renovation to meet the new brand's standards, and a period of revenue disruption during the transition. This creates modest lock-in to existing brand relationships but is not a source of competitive advantage.

Branding: Moderate. Summit's own brand — "Summit Hotel Properties" — has zero consumer recognition. No guest books a hotel because Summit owns it. The company's value proposition is entirely mediated through its brand partners. However, Summit has built a solid reputation among institutional investors, brand partners, and the hotel transaction community as a reliable, disciplined owner and asset manager. This reputational capital facilitates deal flow, brand franchise approvals, and access to capital markets — but it is not the kind of consumer-facing brand power that commands pricing premium.

Cornered Resource: Weak. Summit's assets — select-service hotels in top 50 MSAs — are valuable but not unique. Similar properties can be acquired, developed, or replicated by competitors with sufficient capital. The GIC partnership provides a capital access advantage that is relatively rare among small-cap hotel REITs, but GIC invests across the global hospitality sector and is not exclusive to Summit. Management expertise, while strong, is ultimately replicable through hiring.

Process Power: Moderate-Strong. If there is a single power that justifies Summit's existence as an independent company, this is it. Over 15 years as a public company and 30-plus years including the predecessor period, Summit has developed a highly refined operating model for select-service hotel asset management. The company's ability to consistently identify operational improvements, implement effective revenue management strategies, and control costs is demonstrated by its RevPAR Index consistently above 110 percent — meaning its hotels outperform their local competitive sets by a meaningful margin. The clustering strategy, the capital allocation discipline developed through multiple cycles, and the institutional knowledge embedded in the asset management team represent process advantages that competitors cannot simply copy by reading a playbook.

The dominant power in Summit's arsenal is Process Power — the accumulated operational wisdom and disciplined capital allocation that allows a small-cap REIT to consistently outperform larger peers on a per-asset basis. This is not a moat in the traditional Buffett sense; it can erode with management turnover or strategic drift. But it is the most durable advantage available to a company in Summit's structural position.

What is notably absent from Summit's 7 Powers profile is any power that creates enduring pricing advantage or customer lock-in. The company operates in a fundamentally commoditized space where its products are branded by others, managed by others, and chosen by guests who compare prices on their smartphones in seconds. The absence of network effects, strong branding, or significant switching costs means Summit must continually earn its returns through superior execution rather than relying on structural advantages that compound automatically. This reality makes the quality of management and the discipline of capital allocation even more critical — when you have no moat, you must run faster than everyone else.

XIII. Bull vs. Bear Case

The Bull Case

Every hotel REIT has a narrative about why its portfolio is better positioned than the competition. Summit's bull case is distinctive because it rests not on trophy assets or irreplaceable locations, but on operational execution and strategic positioning in a segment that many institutional investors underappreciate.

The optimistic thesis rests on several reinforcing pillars. First, operational efficiency: Summit has demonstrated best-in-class execution in the select-service segment, with hotel EBITDA margins remaining essentially flat year-over-year even during periods of low RevPAR growth. Pro forma RevPAR growth exceeded the industry average for three consecutive years through 2024, and the RevPAR Index consistently above 115 percent indicates genuine operational alpha rather than favorable market exposure.

Second, the balance sheet transformation: the strategic capital recycling program has simultaneously improved portfolio quality and reduced leverage. The repayment of $287.5 million in convertible notes and the extension of debt maturities to 2028 removed near-term refinancing risk from the story. With 75 percent of pro rata debt fixed at an average SOFR rate of around 3 percent, Summit is well-insulated against further interest rate increases.

Third, the GIC partnership provides patient capital and acquisition firepower that few small-cap hotel REITs can match. When the right acquisition opportunity emerges, Summit can move quickly through the joint venture without diluting public shareholders through equity offerings. This structural advantage becomes particularly valuable in distressed-pricing environments when smaller competitors lack access to capital.

Fourth, the select-service segment itself offers structural resilience. These hotels tend to outperform full-service properties during economic downturns because they cater to budget-conscious travelers and maintain lower cost structures. The segment has seen record-high RevPAR levels in recent years, and institutional investor interest in select-service and extended-stay properties remains strong.

Fifth, valuation: with the stock trading near multi-year lows and well below estimated net asset value, the bull case argues that the market is pricing in a recession scenario that may not materialize. If government travel normalizes, the FIFA World Cup drives demand in 2026, and the macro environment stabilizes, the stock has significant upside potential from current levels. The dividend yield at current prices exceeds 6 percent — an attractive income stream for yield-oriented investors who believe the dividend is sustainable at current FFO levels.

Sixth, new supply discipline: construction of new hotels remains muted across most U.S. markets, constrained by elevated building costs and tighter lending standards. This limited new supply should support occupancy rates and give existing owners like Summit greater pricing power during the next demand upswing.

The Bear Case

The bearish argument is equally compelling, and honest analysis requires grappling with it head-on. The most fundamental challenge is structural, and it is one that no amount of operational excellence can fully overcome: hybrid work may have permanently reduced business travel demand. Every Fortune 500 company that allows two or three days of remote work per week is, by definition, generating fewer hotel room nights than it did pre-pandemic. This is not a cyclical headwind that will reverse; it is a structural shift in how corporations operate. Summit's portfolio, heavily oriented toward corporate transient demand in beltway markets, is directly exposed to this trend.

The 2025 results laid bare the operational vulnerability. Even modest declines in demand — the 20 percent blended drop in government and international inbound segments — produced a 9 percent decline in adjusted EBITDA despite management's best cost-control efforts. In a true recession, the impact would be far more severe. Hotel REITs are among the most cyclically sensitive real estate sub-sectors because they re-price their inventory every night with no lease protection.

Rising operating costs represent another persistent headwind. Property insurance premiums have increased aggressively across the hospitality sector, with some markets seeing double-digit annual increases. Property tax assessments have risen in many jurisdictions as local governments seek revenue. Labor wage rates continue to grow at mid-single-digit annual rates. These costs cannot be easily passed through to guests when occupancy is declining and rate elasticity is constrained. The result is margin compression that even the best operators struggle to offset.

Summit's scale remains a concern. As a small-cap REIT with a market capitalization well under $1 billion, the company faces higher relative costs of capital, limited analyst coverage, and vulnerability to being overlooked by institutional investors. Larger competitors can absorb downturns more easily, access cheaper debt, and negotiate more favorable terms with brand partners.

The reliance on wholly-owned real estate — as opposed to the asset-light franchise models favored by companies like Marriott International and Hilton Worldwide — means Summit bears the full capital intensity of property ownership, including renovation cycles, environmental compliance costs, and periodic property improvement plans mandated by brand franchisors. These capital requirements are lumpy and non-discretionary, creating cash flow volatility that asset-light operators avoid entirely.

The Airbnb effect adds another competitive pressure that did not exist when Summit went public in 2011. Airbnb's share of the business travel market surged from 28 percent in 2019 to 44 percent in 2024, and quarterly demand growth for short-term rentals has consistently outpaced traditional hotels since early 2022. While select-service hotels in suburban and highway-adjacent locations face less Airbnb competition than urban full-service properties, the structural expansion of alternative accommodations represents a permanent broadening of the competitive set.

Finally, the broader lodging REIT sector has been punished by the market, returning negative 17.2 percent through March 31, 2025. Whether this reflects prescient pricing of an economic slowdown or an overreaction to temporary headwinds is the essential question for any investor considering Summit today.