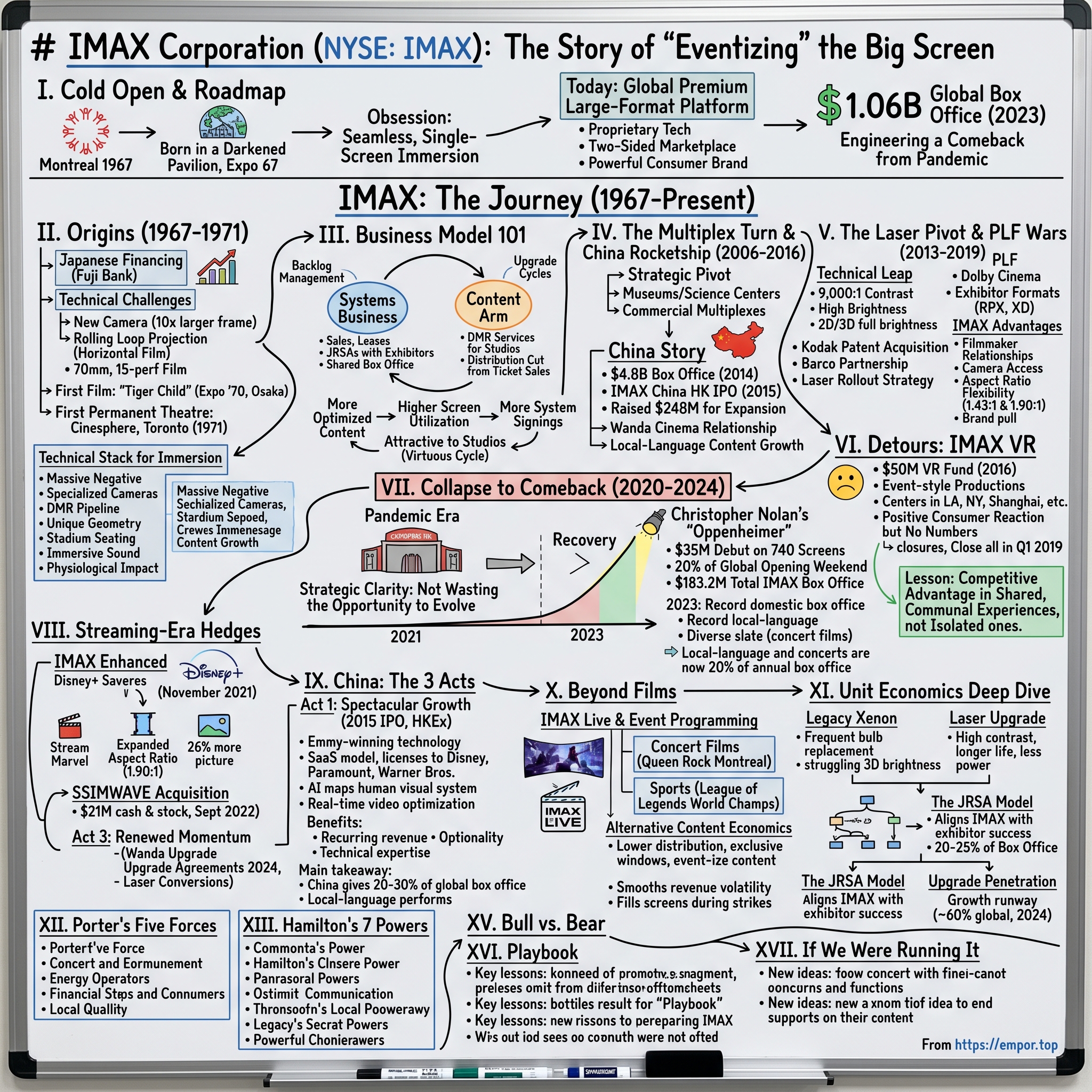

IMAX Corporation (NYSE: IMAX): The Story of "Eventizing" the Big Screen

I. Cold Open & Roadmap

Picture this: Montreal, 1967. The world's fair buzzes with innovation, and in a darkened pavilion, three Canadian filmmakers witness something that will change cinema forever. Roman Kroitor, Graeme Ferguson, and Robert Kerr stand transfixed as multi-screen projections engulf audiences in ways standard cinema never could. They leave with a singular obsession: create a seamless, single-screen experience that delivers the impossible—total immersion.

Today, IMAX Corporation stands as more than just big screens and booming sound. It's a global premium large-format platform that masterfully blends proprietary technology, operates a two-sided marketplace connecting studios with exhibitors, and maintains one of entertainment's most powerful consumer brands. With $1.06 billion in global box office in 2023, near to its highest grossing year ever, the company has engineered a remarkable comeback from the pandemic's devastation.

The central question isn't whether IMAX survived streaming's assault on theatrical exhibition—it clearly has. The real puzzle is how a niche museum format transformed into a global network of over 1,700 theaters and became more profitable in the streaming era than almost anyone predicted. What follows is the story of relentless technical innovation, strategic pivots into China, the laser revolution, failed VR experiments, and ultimately, how IMAX turned "going to the movies" into an event that streaming simply cannot replicate.

II. Origins: What IMAX Actually Is

The IMAX origin story reads like a classic tale of Canadian innovation meeting Japanese financing at the perfect moment. In 1967, Fuji Bank of Japan asked Kroitor to produce a film for Expo '70 in Osaka, with partial financing provided by Fuji. This wasn't just another film commission—it was the catalyst for creating entirely new technology.

The company would have to create new technology for it, including a new camera to shoot images on a film frame ten times larger than the normal 35mm format, new equipment to project those larger frame images onto a six-story-high screen. The technical challenge was staggering. William Shaw, the fourth co-founder and engineering genius behind the projection system, developed the breakthrough "Rolling Loop" technology that allowed horizontal film movement—a radical departure from traditional vertical feed systems.

The film "Tiger Child," directed by Donald Brittain in 1970, became the first IMAX film, premiering at Expo '70 in Osaka. But the real milestone came in 1971 when the first permanent IMAX theatre opened in the Cinesphere at Ontario Place, Toronto. The technology itself was revolutionary: standard IMAX film uses 70mm film stock, turned on its side, with 15 perforations designating the size of each frame, creating images ten times larger than conventional 35mm when projected.

The technical stack that makes IMAX "feel" different isn't just about size. It's the combination of massive negative area (65mm/15-perforation film), specialized cameras that few filmmakers have access to, the DMR (Digital Media Remastering) pipeline that can upconvert standard films, unique projection geometry with steep stadium seating that fills peripheral vision, and a sound system designed specifically for the format's scale. Every element works together to create physiological immersion—your brain literally processes the experience differently than standard cinema.

III. Business Model 101

IMAX operates two distinct but synergistic revenue engines that create a powerful platform dynamic. The Systems business sells, leases, or enters joint revenue-sharing agreements (JRSAs) with exhibitors. These JRSAs are particularly clever: IMAX provides the technology and brand, while sharing in box office revenues, aligning incentives perfectly. The company carefully manages its backlog of system signings and the perpetual upgrade cycle as theaters transition from film to digital to laser technologies.

The Content arm operates as both service provider and distributor. IMAX charges studios for DMR services to convert their films to the IMAX format, then takes a distribution cut from every ticket sold in its global network. Local-language films have emerged as a critical growth vector—Chinese blockbusters, Bollywood epics, and Japanese anime now regularly play in IMAX, diversifying revenue beyond Hollywood tentpoles.

The platform dynamics are elegant: more IMAX-optimized content drives higher screen utilization, which improves exhibitor ROI, which drives more system signings, which makes IMAX more attractive to studios, completing the virtuous cycle. Unlike traditional exhibitors who simply rent movies, IMAX sits at the nexus of technology, content, and distribution, extracting value from each node.

IV. The Multiplex Turn and China Rocketship (2006–2016)

The mid-2000s marked IMAX's great strategic pivot from museums to multiplexes. The strategic shift from institutional venues (museums, science centers) towards commercial multiplexes in the mid-1990s was crucial. This required adapting the technology and business model but opened up a vastly larger market. No longer would IMAX be confined to hour-long documentaries about sharks and space—it would showcase the latest blockbusters.

The China story deserves its own Hollywood treatment. China's box-office revenues surged approximately 36% year over year to $4.8 billion in 2014, and IMAX positioned itself perfectly to capture this growth. The masterstroke came in 2015 when IMAX China raised HK$1.922 billion (US$248 million) through its Hong Kong IPO, with shares priced at HK$31 apiece.

The timing seemed audacious—IMAX went forward with the IPO at a time when China was undergoing economic turmoil—but management's conviction in the Chinese movie market proved prescient. The IPO funded massive expansion: IMAX China had 239 theaters in Greater China at the end of March, with commitments to build another 219. The relationship with Wanda Cinema, China's largest exhibitor chain, became particularly crucial, with Wanda theaters comprising nearly half of all IMAX locations in the country.

By the mid-2010s, China wasn't just another market for IMAX—it was becoming the growth engine. Local-language content flourished, exclusive territorial agreements locked in expansion, and Chinese audiences demonstrated an insatiable appetite for premium experiences. The network effects were powerful: more screens attracted more local content, which drove more attendance, which justified more screens.

V. The Laser Pivot and the PLF Wars (2013–2019)

The laser revolution began quietly in 2013 with a series of demonstrations that would reshape IMAX's technological foundation. In early November 2013, Imax Corporation and Laser Light Engines, Inc., hosted demonstrations of laser-illuminated projectors. Imax invited select members of the giant-screen and Hollywood movie industries to their headquarters in Santa Monica to see 2K images projected with the prototype laser projector developed by Eastman Kodak.

The technical leap was massive. The laser projection system would be capable of a contrast ratio of almost 9,000:1, which is almost double the clarity of even the best film projectors. But this wasn't just about raw specifications. A laser light source provides substantially more brightness than a xenon bulb, allowing IMAX to fill its largest screens with even sharper and more lifelike images. With IMAX's laser, audiences experience full brightness in both 2D and 3D.

IMAX acquired critical intellectual property to make this happen, licensing more than 50 patent families covering fundamental laser projection technology from Eastman Kodak. The company then partnered with Barco for the actual projector development, throwing out conventional wisdom about how digital cinema projectors should work. They weren't retrofitting existing technology—they were building from scratch.

The competitive landscape was heating up. In late 2014, Dolby announced Dolby Cinema as an IMAX competitor with super-vivid image mainly in High Dynamic Range. Exhibitors launched their own premium formats—AMC's Prime, Regal's RPX, Cinemark's XD—all trying to capture premium pricing without paying IMAX's fees. But IMAX had advantages competitors couldn't replicate: filmmaker relationships, exclusive camera access, aspect ratio flexibility (1.43:1 or 1.90:1 versus standard formats), and most importantly, a consumer brand that meant something.

The laser rollout strategy was surgical. Start with flagship institutional locations to prove the technology, then scale to multiplexes through major partnership deals. The AMC and Regal/Cineworld agreements from 2018-2019 committed hundreds of screens to upgrade to laser, essentially standardizing IMAX as the premium offering across North America's largest chains.

VI. Detours That Didn't Work: IMAX VR

The VR venture stands as IMAX's most public failure, but also demonstrates the company's ability to recognize mistakes quickly and cut losses. In 2016, IMAX partnered with a handful of investors for a $50 million VR fund with the aim of creating "event-style productions". The vision was compelling: leverage IMAX's brand and prime multiplex real estate to become the gateway for mainstream VR adoption.

By early 2017, IMAX VR centers opened in Los Angeles, New York, Shanghai, Toronto, and Bangkok. The centers featured pods with HTC Vive headsets, premium content including exclusive experiences, and price points starting at just $10. Early reviews were positive—praising the quality, variety, and staff support.

But the numbers told a different story. "The consumer reaction was extremely positive, but the numbers just weren't there," Gelfond said during an earnings call. By mid-2018, closures began cascading. The writing was on the wall when IMAX's 'New Business' sector posted less than half the sales numbers in 2018 in comparison to 2017.

IMAX decided to conclude the IMAX VR center pilot program and close the remaining three locations in Q1 2019. The lesson was expensive but clear: IMAX's competitive advantage lay in shared communal experiences, not isolated individual ones. VR might be the future, but it wasn't IMAX's future. The discipline to walk away from a hyped technology that didn't fit the core business model would prove crucial as the company faced its next existential challenge.

VII. Collapse to Comeback: Pandemic to "Oppenheimer" (2020–2024)

The pandemic should have killed IMAX. Theaters shuttered globally, Hollywood studios pushed everything to streaming, and industry observers wrote obituaries for theatrical exhibition. IMAX's response revealed the strategic clarity that separates survivors from casualties.

First, management refused to panic about streaming's permanence. Gelfond perceived another chance to change the IMAX model: "We said we're not going to waste this opportunity to look at how to further evolve the business". Instead of hunkering down, IMAX accelerated international expansion, particularly in markets recovering faster than North America.

The comeback trajectory was steep. From pandemic lows, IMAX generated $1.06 billion in global box office in 2023, near to its highest grossing year ever with $1.1 billion in pre-pandemic 2019. The catalyst? Christopher Nolan's "Oppenheimer."

The Oppenheimer phenomenon validated everything IMAX had been building toward. The film delivered a $35 million debut on 740 screens worldwide, representing the biggest share ever of a film's global opening weekend box office with 20% of total receipts. Total IMAX box office for the film reached $183.2 million globally. This wasn't just about one movie—it demonstrated that audiences would pay premium prices for differentiated experiences.

The 2023 success extended beyond Oppenheimer. The year featured the largest-ever domestic IMAX box office, record local-language performance, and a diverse content slate including concert films like Taylor Swift's Eras Tour. IMAX expanded offerings to include concert experiences and foreign language content, which now accounts for 20% of annual box office revenue.

The geographic mix shift proved prescient. China's recovery, India's explosion, Middle Eastern expansion—IMAX was capturing growth wherever it emerged. The company's global footprint, built over decades, became its salvation. When one market struggled, others compensated.

VIII. Streaming-Era Hedges: IMAX Enhanced + SSIMWAVE

Rather than fight streaming, IMAX chose to embrace it—on its own terms. The IMAX Enhanced initiative with Disney+ launched in November 2021 marked a watershed moment. For the first time ever, fans would be able to stream some of their favorite Marvel titles in IMAX's Expanded Aspect Ratio at home.

The technical implementation was clever: IMAX's Expanded Aspect Ratio is 1.90:1, which offers up to 26% more picture for select sequences. This wasn't about competing with theaters—it was about extending the brand into the home while maintaining theatrical superiority. Disney+ became the exclusive streaming home for this enhanced format, starting with 13 Marvel titles.

The real strategic coup came in September 2022 with the acquisition of SSIMWAVE Inc. for $21 million in cash and stock. SSIMWAVE wasn't just another tech acquisition—it was a gateway to recurring SaaS revenue. The company had won a Technology & Engineering Emmy Award (2020) and was honored as Best New Streaming Technology winner in the NAB Show Product of the Year Awards in both 2022 and 2021.

SSIMWAVE licenses their AI-driven video quality technology to media companies including Disney, Paramount Global, and Warner Bros. The technology addresses a critical streaming pain point: Its 30-person engineering team has mapped the human visual system to produce one of the most accurate measures of perceptual quality, which its AI-driven software applies to enhance video streams and files in real time.

For IMAX, SSIMWAVE provides three strategic benefits: immediate recurring revenue from existing streaming clients, technical expertise to enhance IMAX's own quality standards across platforms, and optionality for future home entertainment initiatives. The acquisition philosophy echoes the company's DNA— Gelfond noted "the similarities between this company and IMAX when we acquired it nearly 30 years ago are uncanny".

By 2024, this streaming hedge was bearing fruit. The IMAX Enhanced footprint on Disney+ expanded with new titles and functionality. SSIMWAVE's client base grew. Most importantly, these initiatives generated revenue without cannibalizing theatrical attendance—streaming became a marketing funnel for the theatrical experience, not a replacement.

IX. China: IPO, Take-Private Attempt, and Re-acceleration (2015–2025)

The China subsidiary story plays like a three-act drama: spectacular growth, attempted take-private, and renewed expansion. Act One saw IMAX China begin trading on the Hong Kong Stock Exchange on October 8, 2015, with the IPO raising critical expansion capital at precisely the right moment.

The structure was elegant: IMAX Corporation retained 80% ownership while bringing in local investors who understood the market's nuances. The company was valued at $400 million when IMAX Corp sold a 20% stake to two private equity firms in 2014, setting the stage for the public offering.

Act Two brought drama in 2023 when IMAX Corporation attempted to take the China subsidiary private, seeking to recapture full ownership of its fastest-growing market. But minority shareholders balked at the offer, ultimately rejecting the privatization scheme. The failed attempt could have poisoned relationships, but instead demonstrated the subsidiary's independence and value.

Act Three, still unfolding, shows renewed momentum. Despite geopolitical tensions and economic uncertainty, Wanda Film signed major upgrade agreements in 2024, committing to laser conversions across their network. The message was clear: China's appetite for premium experiences remained robust, and IMAX was the preferred partner.

The numbers tell the story: China consistently delivers 20-30% of global IMAX box office, local-language content performs increasingly well, and the pipeline of new signings remains strong. The subsidiary structure, initially a financing mechanism, evolved into a strategic advantage—providing local credibility while maintaining technological and operational control.

X. Beyond Films: IMAX Live and Event Programming

The transformation of IMAX from pure cinema to experiential platform accelerated post-pandemic. Live events emerged as a new content category with different economics and audience dynamics than traditional films. Concert films like Queen Rock Montreal demonstrated the model: capture legendary performances, distribute globally through the IMAX network, then extend to streaming with IMAX Enhanced.

Sports represented another frontier. In 2024, almost 200 IMAX theaters across China live-streamed the world championships of the multiplayer online game League of Legends to near sold-out crowds. This wasn't traditional cinema—it was communal viewing of live events that benefited from IMAX's scale and quality.

The economics of alternative content are compelling. Lower distribution costs than Hollywood films, often exclusive windows, and the ability to event-ize content that might otherwise go straight to streaming. A filmed Broadway show, a playoff game, a K-pop concert—each becomes an event when presented in IMAX.

The programming strategy also smooths revenue volatility. When Hollywood struggles with strikes or release delays, IMAX can fill screens with alternative content. This flexibility proved crucial during the 2023 actors' strike, when concert films and international content kept screens busy and revenues flowing.

XI. Unit Economics Deep Dive

The laser upgrade cycle fundamentally altered IMAX's unit economics. Legacy xenon systems required frequent bulb replacements, significant power consumption, and struggled with 3D brightness. Laser systems deliver contrast levels substantially higher than ever before, last longer, and consume less power—improving both exhibitor ROI and viewing quality.

The JRSA (Joint Revenue Sharing Agreement) model deserves particular attention. Unlike selling systems outright, JRSAs align IMAX with exhibitor success. IMAX typically receives 20-25% of box office revenues from JRSA screens, providing recurring revenue tied directly to performance. Exhibitors get lower upfront costs and ongoing technical support. The model creates stickiness—once an exhibitor sees IMAX driving higher per-screen averages, they're incentivized to add more screens.

Geographic exclusivity zones protect exhibitor investments while ensuring optimal market coverage. IMAX won't oversaturate a market, maintaining scarcity value. This discipline contrasts sharply with other PLF formats that proliferated without regard for economics.

The upgrade penetration metric reveals the growth runway. With laser systems in roughly 60% of the global network as of 2024, significant upgrade opportunity remains. Each upgrade not only generates installation revenue but typically extends contract terms and increases IMAX's box office share. The installed base becomes an annuity-like revenue stream requiring minimal incremental investment.

XII. Strategy Frameworks – Porter's Five Forces

Threat of New Entrants: Low The barriers are formidable. Beyond the hundreds of millions in R&D investment, new entrants face the challenge of convincing both exhibitors and studios simultaneously. IMAX's 50-year head start in technology development, coupled with exclusive filmmaker relationships and consumer brand recognition, creates a moat that money alone cannot cross. The proprietary camera systems, with only a handful in existence, represent a physical barrier competitors cannot quickly replicate.

Supplier Power: Moderate Barco partnership on laser light sources represents a key dependency, though IMAX owns critical IP and could potentially switch suppliers. The company's acquisition of Kodak's laser patents provides negotiating leverage. Camera components, sound systems, and screen materials come from various suppliers, reducing single-source risk. The SSIMWAVE acquisition brought critical technology in-house, reducing external dependencies.

Buyer Power: High but Tempered Large exhibitor chains (AMC, Regal, Wanda, PVR INOX) wield significant negotiating power through volume. However, IMAX's proven ability to drive 20-40% premium pricing and higher concession sales moderates this power. The exclusive territorial agreements mean exhibitors can't easily switch to alternatives without losing the IMAX advantage in their markets. Exhibitor consolidation increases buyer power, but IMAX's brand pull with consumers provides counter-leverage.

Threat of Substitutes: High but Differentiated Home entertainment, gaming, and rival PLFs all compete for consumer entertainment dollars. Dolby Cinema offers comparable technical quality. Exhibitor-owned formats like RPX and XD provide cheaper alternatives. Yet IMAX maintains differentiation through filmmaker partnerships, exclusive aspect ratios, and brand prestige. The "filmed for IMAX" designation has become a quality marker that substitutes cannot replicate.

Industry Rivalry: Intensifying but Advantaged The PLF space has become increasingly competitive, but IMAX's first-mover advantages compound over time. While Dolby Cinema offers superior contrast and sound in some metrics, IMAX's larger screen real estate, filmmaker relationships, and global footprint maintain its premium position. Regional PLF formats struggle to achieve the scale necessary for studio support. IMAX's answer to rivalry: make the pie bigger through market education rather than fight for pieces.

XIII. Strategy Frameworks – Hamilton's 7 Powers

Scale Economies IMAX's global network of 1,700+ theaters amortizes massive R&D investments across a broad base. DMR conversion costs decrease per film as volume increases. Marketing efficiency improves as the brand strengthens globally. Studios can justify IMAX-specific content creation knowing the global distribution reach. Smaller PLF formats cannot match this scale math.

Network Economies The two-sided network effects are powerful and compounding. More screens attract more studio content and filmmaker interest. More exclusive content drives consumer demand and exhibitor ROI. Higher exhibitor returns justify more screen installations. This flywheel has been spinning for decades and accelerates with each revolution. The Oppenheimer phenomenon—where IMAX captured 20% of global box office with 1% of screens—exemplifies these network dynamics.

Counter-positioning IMAX positioned itself as the "event" layer above commodity movie-going. While others compete on price or convenience, IMAX competes on experience. This counter-positioning means IMAX benefits from the very streaming trend that threatens traditional exhibition—as home viewing becomes ubiquitous, the desire for differentiated theatrical experiences increases. Exhibitors' in-house PLF formats cannot counter-position against themselves, giving IMAX structural advantage.

Switching Costs For exhibitors, switching costs are substantial: specialized room geometry designed for IMAX, exclusive territorial agreements with penalties, staff training on proprietary systems, and marketing investments in the IMAX brand locally. For filmmakers, switching costs include learning new camera systems, establishing new post-production workflows, and risking audience expectations. These costs compound over time, creating deep moats.

Branding IMAX achieved something rare: consumer pull in a B2B2C model. Moviegoers actively seek out IMAX screenings and pay premiums for them. "See it in IMAX" has become cultural shorthand for the ultimate viewing experience. The brand transcends rational attributes—it's emotional, experiential, and aspirational. Competitors can match technical specifications but cannot replicate decades of brand building.

Cornered Resource Multiple cornered resources reinforce IMAX's position: scarce 65mm/15-perf cameras (fewer than 10 in circulation), deep post-production expertise that takes years to develop, exclusive long-term filmmaker relationships (Nolan, Villeneuve, Marvel Studios), and unique ability to project at 1.43:1 and 1.90:1 aspect ratios. The TCL Chinese Theatre and other flagship locations serve as cornered resources for premieres and marketing.

Process Power Decades of accumulated know-how create process power that's nearly impossible to replicate: DMR algorithms refined over thousands of films, color science that preserves director intent while optimizing for large-format presentation, theater calibration processes ensuring consistent global quality, and embedded workflows with major studios' post-production pipelines. This isn't just technology—it's organizational knowledge that compounds annually.

XIV. Key Inflection Points of the Last 10–15 Years

2013–2018: The Laser Revolution The 2013 demonstrations of laser-illuminated projectors initiated IMAX's most significant technical transition since digital conversion. The subsequent Kodak patent acquisition, Barco partnership, and massive exhibitor upgrade agreements with AMC and Regal reset industry standards. This wasn't incremental improvement—laser technology doubled contrast ratios, eliminated lamp replacements, and enabled consistent 3D brightness. The multi-year rollout required precise orchestration of R&D, manufacturing, installation, and training across hundreds of locations globally.

2015: China IPO as Growth Catalyst The HK$1.922 billion IPO of IMAX China provided capital at exactly the right moment to capture China's theatrical boom. This wasn't just fundraising—it was a strategic masterstroke that provided local credibility, government relations advantages, and alignment with Chinese partners. The subsidiary structure allowed IMAX to navigate geopolitical complexities while maintaining technology control.

2019: VR Exit and Focus Closing the remaining VR centers in Q1 2019 marked a crucial strategic inflection—the discipline to abandon a hyped technology that didn't fit IMAX's core competencies. This wasn't failure but strategic clarity. Resources redirected from VR accelerated laser rollout and content partnerships.

2020–2023: Pandemic Resilience to Record Performance The pandemic created an existential crisis that became a strategic opportunity. While competitors retreated, IMAX expanded internationally, diversified content, and prepared for the inevitable theatrical return. The $1.06 billion 2023 global box office, powered by Oppenheimer's record performance, validated the strategy. IMAX emerged stronger, with higher market share and clearer differentiation than pre-pandemic.

2021–2024: Platform Extension Strategy The Disney+ IMAX Enhanced launch in November 2021 and SSIMWAVE acquisition in 2022 represent IMAX's evolution from pure theatrical to multi-platform premium experiences. These aren't defensive moves but offensive expansion—capturing value across the entire content consumption chain while protecting theatrical primacy.

2023–2024: China Independence and Renewal The failed take-private attempt paradoxically strengthened IMAX China by demonstrating its independence and value. The 2024 Wanda upgrade agreements signal continued confidence despite macroeconomic uncertainty. China remains central to IMAX's global strategy, contributing 25-30% of revenues with significant expansion runway remaining.

XV. Bull vs. Bear, and What to Watch

Bull Case:

The structural shift toward premium experiences accelerates post-pandemic. Audiences demonstrate willingness to pay 40-60% premiums for IMAX, validating the eventization thesis. The laser upgrade cycle provides multi-year revenue visibility with improving unit economics. System signings remain robust globally, particularly in emerging markets where modern multiplexes are still being built.

The filmmaker alignment strengthens with each cycle. Directors increasingly design shots specifically for IMAX cameras and aspect ratios. "Filmed for IMAX" becomes a production standard for blockbusters, creating switching costs for studios. The expanded content slate—local language films, concerts, sports, gaming—smooths revenue volatility and increases screen utilization.

SSIMWAVE adds recurring SaaS revenue with 50 patents and Emmy-winning technology serving Disney, Paramount, and Warner Bros. This isn't just diversification—it's leveraging core competencies in image quality across platforms. IMAX Enhanced on streaming platforms extends brand reach without cannibalization, potentially driving theatrical attendance through increased awareness.

Geographic diversification continues with India, Southeast Asia, and Middle East expansion offsetting any China slowdown. The installed base of 1,700+ screens generates predictable upgrade revenue for the next decade as laser penetration remains below 70%.

Bear Case:

Rival PLFs proliferate and improve, compressing IMAX's premium over time. Dolby Cinema offers superior technical specifications in some dimensions. Exhibitor-owned formats avoid revenue sharing, improving theater economics at IMAX's expense. As these alternatives mature, IMAX's differentiation erodes.

Macro headwinds intensify: recession reduces discretionary entertainment spending, China's box office volatility increases amid economic uncertainty, and geopolitical tensions complicate international expansion. Film slate concentration risk remains high—a few weak blockbusters significantly impact annual results.

The hardware upgrade cycle naturally slows as laser penetration increases. Once the low-hanging fruit of upgrades completes, growth must come from new installations in increasingly marginal markets. System sales face longer sales cycles and lower IRRs in emerging markets.

Streaming's convenience and improving home theater technology gradually erode the theatrical value proposition for all but the biggest event films. Younger audiences, raised on mobile consumption, may not value the theatrical experience enough to sustain premium pricing.

KPIs to Track:

-

Global box office indexation: IMAX's percentage of global box office for its films (currently 11-20% for blockbusters on 1% of screens). This single metric captures brand strength, content quality, and pricing power.

-

Laser penetration percentage: Currently ~60% globally, with each percentage point representing $15-20M in upgrade revenue. The pace of penetration indicates both exhibitor confidence and IMAX's execution capability.

-

SSIMWAVE customer additions and recurring revenue growth: New streaming/broadcast clients validate the technology's value beyond IMAX's ecosystem, while recurring revenue provides stability against box office volatility.

XVI. Playbook: Lessons for Builders and Investors

Own the End-to-End Experience IMAX's control from camera to projection creates insurmountable competitive advantages. Partial solutions fail—Dolby has great projection but no cameras; exhibitor PLFs have screens but no content partnerships. Full-stack ownership enables rapid innovation and quality control impossible in fragmented value chains.

Be the Category Name When consumers say "let's see it in IMAX," value accrues throughout the chain. This requires decades of consistent brand investment and discipline to maintain premium positioning. The temptation to dilute for growth must be resisted—every compromised installation weakens the brand promise.

Upgrade Cycles as Strategy Technology transitions, properly managed, create predictable multi-year revenue streams. The film-to-digital-to-laser progression wasn't just technical evolution but strategic orchestration. Each cycle deepens relationships, extends contracts, and raises switching costs. The key: time upgrades to coincide with exhibitor capital cycles and technological step-changes consumers notice.

Partner Where It Compounds, Prune Experiments Fast The Disney+ partnership compounds because both parties benefit—Disney gets differentiation, IMAX gets brand extension without infrastructure investment. The Barco partnership leverages specialized expertise while maintaining IP control. Conversely, the VR experiment was identified as non-core and terminated quickly, preserving capital and focus. Strategic discipline means saying no to attractive opportunities that don't reinforce core advantages.

XVII. If We Were Running It

The eventization flywheel needs aggressive acceleration. Live sports represent a massive untapped opportunity—imagine NBA Finals, World Cup matches, or Super Bowl parties in IMAX. The technology exists; the challenge is content rights and scheduling flexibility. Gaming tournaments, particularly in Asia, could fill off-peak hours while attracting younger demographics.

Filmmaker services should expand beyond cameras and post-production to become a full creation platform. IMAX Studios could co-finance films shot entirely with IMAX cameras, ensuring exclusive windows and deeper creative partnerships. Provide free camera training programs for emerging directors, creating the next generation of IMAX advocates. Document and share technical knowledge through an IMAX Film School, cementing thought leadership.

The software layer via SSIMWAVE needs aggressive expansion. Every streaming platform, broadcaster, and content creator needs video quality optimization—IMAX should become the Dolby of video, licensing technology broadly while maintaining the premium theatrical brand. Develop AI-powered tools that automatically optimize any content for any screen, from mobile to theatrical. The recurring revenue potential dwarfs current projections.

Geographic expansion should follow a barbell strategy: accelerate in high-growth emerging markets (India, Indonesia, Nigeria) while selectively adding flagship locations in mature markets. The next Burj Khalifa or Mumbai airport needs an IMAX. These prestige locations serve as brand billboards while generating solid returns.

Capital allocation should remain disciplined. Share buybacks make sense when the stock trades below intrinsic value, but growth investments in laser upgrades and emerging markets generate higher IRRs. Maintain the dividend as a signal of stability while preserving flexibility for opportunistic investments.

XVIII. Epilogue

IMAX transformed "going to the movies" from commodity consumption into premium experience. This wasn't luck or timing—it was five decades of relentless focus on a simple idea: make audiences feel something they cannot feel anywhere else.

The next decade will test whether IMAX can maintain its moat as technology democratizes and attention fragments. The company's answer seems clear: widen the moat through deeper filmmaker relationships, broader content categories, and selective platform expansion. The theatrical experience remains the crown jewel, but IMAX increasingly becomes a quality standard that transcends any single screen.

The $1.06 billion 2023 box office proves something important: in an era of infinite content and viewing options, scarcity and differentiation become more valuable, not less. IMAX doesn't compete with Netflix any more than Rolex competes with Apple Watch—they solve different problems for different occasions.

The ultimate bull case for IMAX isn't about screens or technology. It's about human nature. We are social creatures who crave communal experiences. We want to feel small in the presence of something magnificent. We desire escape that's more than distraction. IMAX delivers all three in ways that no algorithm or convenience can replicate. In eventizing the big screen, IMAX discovered something profound: the future of entertainment might be more human than we think.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube