Illumina: The Genomics Revolution - From Startup to Sequencing Monopoly

I. Introduction & Episode Roadmap

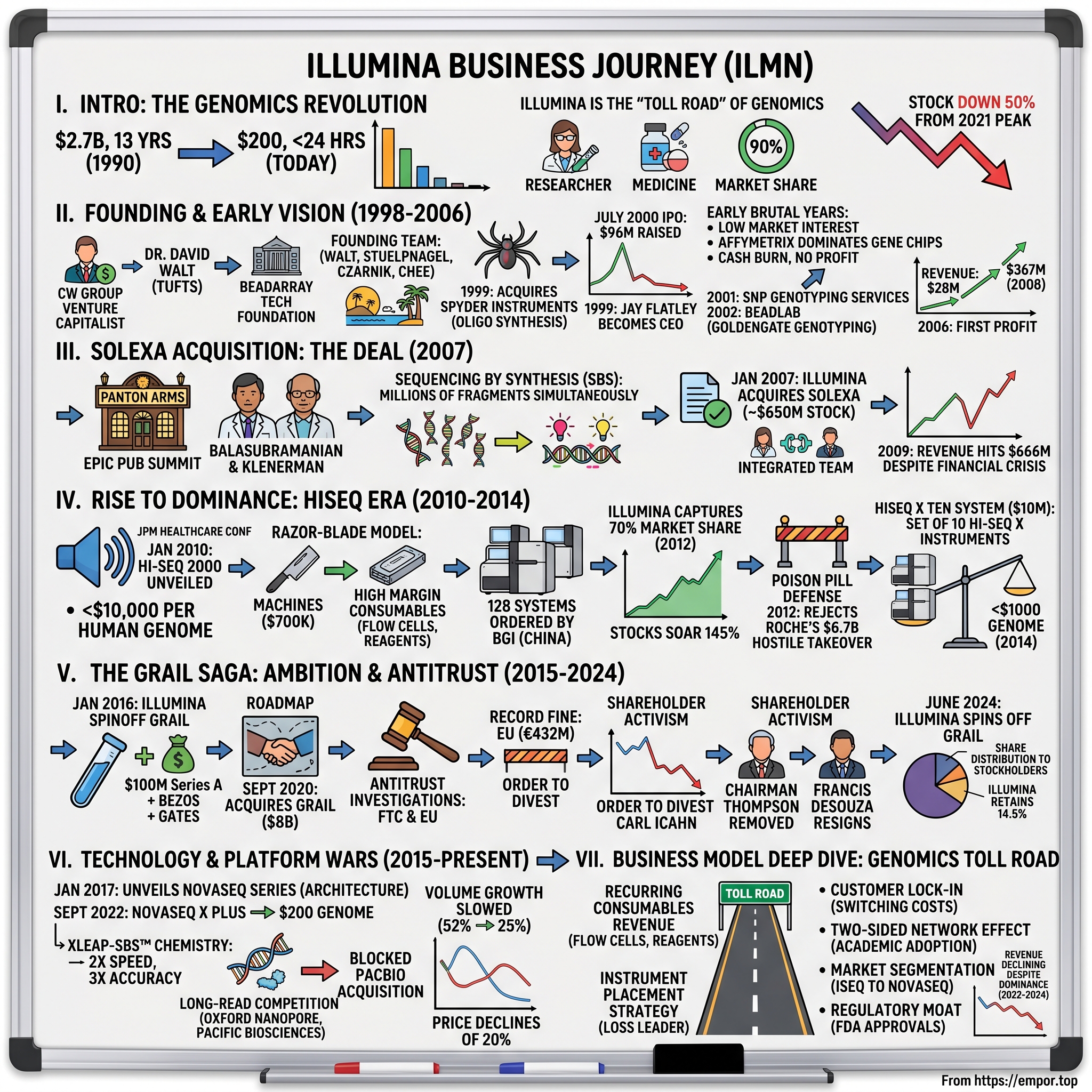

Picture this: In 1990, sequencing a single human genome cost $2.7 billion and took 13 years. Today, Illumina's machines can do it for $200 in under 24 hours. That's a 13-million-fold improvement—a cost reduction curve that makes Moore's Law look sluggish. Welcome to the story of how a San Diego startup achieved something that should be impossible in capitalism: a 90% market share that has persisted for over a decade.

Illumina isn't just another biotech success story. It's the company that built the toll road for the genomics revolution, then convinced everyone to drive on it. Founded in April 1998, when the Human Genome Project was still years from completion, Illumina has become the invisible infrastructure powering everything from COVID variant tracking to personalized cancer treatment. Every time researchers decode DNA to understand disease, develop new drugs, or trace human ancestry, there's a 9-in-10 chance they're using Illumina's machines.

The company's dominance rests on a technology called sequencing by synthesis (SBS)—a method so superior to alternatives that competitors have essentially given up trying to beat it head-on. Instead, they're looking for niches where Illumina doesn't play. It's the kind of moat Warren Buffett dreams about: high switching costs, network effects, and a razor-blade business model where the real money comes from consumables, not machines.

But here's where it gets interesting: Despite this seemingly unassailable position, Illumina's stock has been cut in half from its 2021 peaks. Growth has stalled. Activists are circling. The company that enabled the genomics revolution is now grappling with what happens when a revolution becomes routine.

How did a startup with borrowed technology from a British university lab become the Standard Oil of genomics? Why did they spend $8 billion trying to buy back a company they'd spun off, only to be forced by regulators to divest it? And most importantly—in an era where AI promises to transform drug discovery and personalized medicine becomes reality—is Illumina's monopoly a fortress or a prison?

This is the story of scientific breakthroughs, billion-dollar bets, antitrust battles, and the peculiar economics of selling shovels in a gold rush that never ends. It's about how five scientists built a company that would sequence billions of genomes, enable thousands of discoveries, and fundamentally change how we understand life itself.

II. The Founding Story & Early Vision (1998-2006)

The genomics revolution began, improbably, with a venture capitalist getting lost. In 1997, Larry Bock of CW Group was visiting Tufts University when he stumbled into the wrong lab. Instead of finding the professor he was scheduled to meet, he discovered David Walt working on something called BeadArray technology—tiny glass beads that could detect multiple biological targets simultaneously. Bock saw something Walt hadn't: this wasn't just clever chemistry. It was potentially the foundation for reading DNA at scale.

By April 1998, Bock had assembled a founding team that read like a biotech dream team. There was Walt himself, the Tufts professor with the core technology. John Stuelpnagel, a veterinarian-turned-biotech-executive who'd already built and sold companies. Anthony Czarnik and Mark Chee, both molecular biology pioneers. They set up shop in San Diego—not Boston or San Francisco—because Stuelpnagel insisted the year-round perfect weather would help recruit talent. "Why suffer through winters when you're trying to change the world?" he'd tell potential hires. The early years were brutal. In 1999, Illumina acquired Spyder Instruments for their technology of high-throughput synthesis of oligonucleotides—essentially buying the ability to make the DNA probes that would sit on their beads. But timing is everything in business, and Illumina completed its initial public offering in July 2000, raising $96 million just as the dot-com bubble burst spectacularly. The stock immediately tanked. Within months, the company was worth less than the cash it had raised.

The technology worked, but nobody cared. Wall Street had moved on from biotech promises. Competitors like Affymetrix dominated the market with their gene chip technology. Illumina's first commercial product, the Illumina BeadLab launched in 2002, using GoldenGate Genotyping technology, found few buyers. The company was burning through cash with no path to profitability. Enter Jay Flatley in late 1999. A former CEO of Molecular Dynamics who'd already built and sold one sequencing company, Flatley was exactly what Illumina needed: someone who understood both the science and the Street. During his tenure as CEO, he would take Illumina from $1.3 million in sales in 2000 to $2.2 billion in 2015, representing a compound annual growth rate of 64 percent. But in those early days, survival was the only metric that mattered.

Flatley's first move was brutal efficiency. He cut costs, focused the product line, and evangelized a simple message: Illumina's bead technology could do what Affymetrix's chips did, but cheaper and more flexibly. Slowly, customers started listening. In 1999, Illumina acquired Spyder Instruments for their technology of high-throughput synthesis of oligonucleotides. Illumina began offering single nucleotide polymorphism (SNP) genotyping services in 2001 and launched its first system, the Illumina BeadLab, in 2002, using GoldenGate Genotyping technology.

The numbers tell the story of a company clawing its way to relevance. Revenue grew from $28 million in 2003 to $367 million in 2008. The company achieved its first profit in 2006—eight years after founding. These weren't Silicon Valley hockey-stick growth rates. This was grinding, customer-by-customer progress in a market that didn't yet understand why it needed what Illumina was selling.

But Flatley knew something the market didn't: the real revolution wasn't in reading known genetic variations. It was in reading entire genomes. And halfway around the world, in a Cambridge pub, two scientists had already invented the technology that would make it possible.

III. The Solexa Acquisition: The Deal That Changed Everything (2007)

The legend of Solexa begins, as all great scientific breakthroughs should, in a pub. On an August evening in 1997, University of Cambridge chemists Shankar Balasubramanian and David Klenerman met at the Panton Arms pub for what would become one of the most consequential beer summits in scientific history. Shankar Balasubramanian's diary records the date as when "the pieces of the jigsaw came together".

They were working on single-molecule fluorescence spectroscopy—watching individual DNA polymerase enzymes copy DNA in real-time. But over pints that evening, they had an epiphany: if they could watch the enzyme copying a genome, they were inadvertently also reading the genome. They had discovered a radically new way to sequence DNA that could be fast, accurate, low-cost and scalable.

The genius was in the parallelization. Instead of analyzing one DNA molecule at a time, they fragmented the human genome into millions of tiny pieces, allowing for the simultaneous sequencing of millions of fragments. They color-coded the four different DNA bases using fluorescent markers. It was like going from reading one book at a time to reading an entire library simultaneously.

Within a year, Balasubramanian and Klenerman obtained seed funding from venture capital firm Abingworth Management to found Solexa in 1998. Solexa was eventually acquired by Illumina in 2007 for approximately $650 million.

Back in San Diego, Jay Flatley had been watching Solexa's progress with the intensity of a chess grandmaster studying an opponent. Illumina had built a solid business in genetic analysis, but Flatley knew the real prize was whole-genome sequencing. The Human Genome Project had taken 13 years and $2.7 billion to sequence a single genome. Whoever could bring that cost down by orders of magnitude would own the future of biology. In November 2006, Illumina announced it would acquire Solexa for approximately $600 million in stock. The deal closed on January 26, 2007. "We are excited to join the two companies, creating the only company with genome-scale technology for genotyping, gene expression, and sequencing, the three cornerstones of modern genetic analysis," Jay Flatley said at closing.

The integration wasn't seamless. Solexa had operations in both Hayward, California, and Cambridge, England. The cultures were different—academic British scientists meets aggressive California biotech. The technology needed refinement. Illumina had to merge Solexa's sequencing-by-synthesis with its own manufacturing expertise and commercial infrastructure.

But when it worked, it was magic. Solexa's technology could sequence 1 gigabase of data in a single run—a massive leap from anything else available. The Genome Analyzer, Illumina's first Solexa-based product, could do in days what had taken the Human Genome Project years.

The financial impact was immediate. Despite the 2008 financial crisis decimating markets globally, Illumina's revenue jumped 16% from 2008 to 2009, largely due to Genome Analyzer sales. In the midst of global economic turmoil, Illumina posted its highest revenue ever at $666 million in 2009.

The Solexa acquisition wasn't just a product purchase. It was Illumina buying the future of genomics—and with it, the keys to what would become a monopoly.

IV. The Rise to Dominance: HiSeq Era & Market Control (2010-2014)

In January 2010, at the annual J.P. Morgan Healthcare Conference—biotech's equivalent of the Oscars—Jay Flatley took the stage with news that would reshape the industry. Illumina unveiled the HiSeq 2000 sequencing system, and for the first time, took the cost of sequencing a human genome below $10,000.

The numbers were staggering. HiSeq 2000 could generate 200 gigabases of quality filtered data in a single run, allowing researchers to obtain 30-fold coverage of two human genomes simultaneously. What had cost $2.7 billion in 1990 now cost less than a luxury watch.

But the real genius wasn't just the technology—it was the business model. Illumina had learned from the printer industry: sell the machines at reasonable margins, then make the real money on consumables. Every sequencing run required flow cells, reagents, and other supplies that only Illumina could provide. Customers who bought a HiSeq 2000 for around $700,000 were locked into buying millions of dollars of consumables over the machine's lifetime.

The market response was immediate and overwhelming. Beijing Genomics Institute (BGI), then emerging as China's genomics powerhouse, placed an order for 128 HiSeq 2000 systems—the largest single order for sequencing systems ever. Over the next year and a half, Illumina stock soared 145%

The market capitulation was swift. By 2012, Illumina had captured 70% of the sequencing market. Academic labs, pharmaceutical companies, and emerging diagnostics firms all standardized on HiSeq. The competition wasn't just losing—they were becoming irrelevant.

Then came the test of monopoly power. In January 2012, Swiss pharmaceutical giant Roche launched a hostile takeover bid for Illumina, initially offering $5.7 billion at $44.50 per share. When Illumina's board unanimously rejected the offer as "grossly inadequate", Roche raised its bid to $51 in March.

The battle turned ugly. Illumina adopted a "poison pill" defense, granting investors the right to buy shares at half price, with shareholders receiving one preferred stock purchase right as a dividend for each common share held as of February 6, allowing them to purchase $550 in common shares for $275. Roche tried to install favorable board members at Illumina's annual meeting. The entire industry watched nervously—sequencing industry veterans predicted that Illumina would become a much less innovative company under Roche's management.

On April 18, 2012, Illumina shareholders delivered their verdict: no deal. Shareholders rebuffed Roche's efforts to install board members favorable to a merger at the San Diego-based gene sequencing technology company's annual meeting. Roche CEO Severin Schwan withdrew, stating that with access only to public information about Illumina's business, they didn't believe a price above $51 per share would be in Roche shareholders' interest.

Illumina had done something remarkable: it had rejected a 64% premium to its pre-offer stock price because management believed they were worth more. They were right. Free from Roche's grasp, Flatley unleashed the company's most audacious product yet.

At the January 2014 J.P. Morgan Healthcare Conference, Flatley took the stage with an announcement that would define genomics for the next decade: the HiSeq X Ten. Illumina broke the 'sound barrier' of human genomics by enabling the $1,000 genome, made possible by the new HiSeq X Ten Sequencing System.

The system wasn't just one machine—it was a set of 10 HiSeq X instruments that could deliver over 18,000 human genomes per year. The economics were revolutionary: the world's first platform to deliver full coverage human genomes for less than $1,000, inclusive of typical instrument depreciation, DNA extraction, library preparation, and estimated labor, purpose-built for population-scale human whole genome sequencing with the ability to sequence tens of thousands of samples annually.

The technical breakthrough came from patterned flow cells containing billions of nanowells at fixed locations, combined with new clustering chemistry delivering a significant increase in data density at 6 billion clusters per run. But the business model breakthrough was equally important: at $10 million for the full system, only the world's largest sequencing centers could afford it. This wasn't democratization—it was consolidation.

By the end of 2014, the dominance was complete. Illumina had achieved something that should be impossible in competitive markets: a sustainable monopoly built on continuous innovation. They controlled the technology roadmap, the pricing curve, and effectively, the future of genomics.

V. The GRAIL Saga: Ambition Meets Antitrust (2015-2024)

In January 2016, Illumina did something unprecedented for a monopolist: it gave birth to its own disruption. Illumina formed a spinoff company called GRAIL to experiment with a simple blood test for early detection of all types of cancer, with Illumina, whose instruments accounted for more than 90% of all DNA data collected worldwide in 2014, providing the foundational technology.

The vision was audacious: develop "a universal, direct measure of cancer," far more accurate than proxy tests like mammograms or PSA tests for prostate cancer. GRAIL was initially funded by over $100 million in Series A financing from Illumina and ARCH Venture Partners, with participating investments from Bezos Expeditions, Bill Gates and Sutter Hill Ventures.

"We hope today is a turning point in the war on cancer," said Jay Flatley, Illumina Chief Executive Officer and Chairman of the Board of GRAIL. "By enabling the early detection of cancer in asymptomatic individuals through a simple blood screen, we aim to massively decrease cancer mortality by detecting the disease at a curable stage."

The spinoff made strategic sense. Illumina could share the financial burden of developing an unproven technology while avoiding conflicts with customers who had their own liquid biopsy ambitions. By 2017, GRAIL was fully independent, having raised $2 billion from investors to develop its Galleri test—a blood test capable of detecting over 50 types of cancer before symptoms appear.

Then, in September 2020, with GRAIL preparing for an IPO, Illumina shocked the industry. The companies announced they had entered into a definitive agreement under which Illumina would acquire GRAIL for cash and stock consideration of $8 billion upon closing of the transaction. GRAIL stockholders, including Illumina, would receive $3.5 billion in cash and $4.5 billion in shares of Illumina stock.

The timing was curious. GRAIL hadn't proven its test could improve health outcomes. The liquid biopsy market was nascent. But Illumina CEO Francis deSouza saw something others didn't: the total NGS oncology opportunity was expected to grow at a CAGR of 27% to $75 billion in 2035. This wasn't just about selling sequencers—it was about owning the entire value chain from hardware to clinical diagnosis.

What happened next was a masterclass in corporate defiance. Both the Federal Trade Commission and European Commission launched investigations, arguing the deal would stifle competition. The concern was obvious: Illumina controlled the sequencing infrastructure that GRAIL's competitors needed. It would be like Standard Oil buying the railroads.

But on August 18, 2021, Illumina did something extraordinary: despite looming antitrust investigations on both sides of the Atlantic, Illumina pushed forward with finalizing its $8 billion deal to acquire Grail. The company completed the acquisition before regulators reached their conclusions, betting that possession would be nine-tenths of regulatory law.

The gamble backfired spectacularly. The EU's competition watchdog levied a record fine against Illumina of 432 million euros, or about $476 million, in addition to declaring that the company would have to unwind its ownership. The FTC followed up in April 2023 with an order of its own.

Meanwhile, activist investor Carl Icahn smelled blood. He launched a proxy battle arguing GRAIL was draining Illumina's finances. The pressure mounted from all sides. Shareholders ultimately voted out company Chairman John Thompson, and CEO Francis deSouza resigned weeks later.

By June 2024, the inevitable had happened. Illumina completed its spinoff of Grail, ending the company's attempted acquisition nearly four years after announcing the deal. Grail began trading on Nasdaq as an independent company, with Illumina distributing Grail shares to its stockholders and retaining a minority share of 14.5% in the business.

The GRAIL saga cost Illumina billions in acquisition costs, regulatory fines, and management upheaval. But more importantly, it revealed something fundamental about the limits of monopoly power: even with 90% market share and unlimited resources, there are some things money can't buy—especially when regulators are watching.

VI. Technology Evolution & The Platform Wars (2015-Present)

While Illumina was battling regulators over GRAIL, the company never stopped innovating on its core technology. In January 2017, at the J.P. Morgan Healthcare Conference, CEO Francis deSouza unveiled the NovaSeq series—a new and scalable sequencing architecture expected one day to enable a $100 genome. Speaking at the J.P. Morgan Healthcare Conference, Francis deSouza, President and CEO of Illumina, unveiled the NovaSeq series, a new and scalable sequencing architecture, comprised of two instruments: the NovaSeq 5000 and NovaSeq 6000.

The NovaSeq represented a complete departure from the HiSeq architecture. NovaSeq is the most powerful sequencer Illumina has ever launched and will open new horizons for more highly powered experiments at the depth required to discover rare genetic variants. It was designed from the ground up to allow a broad set of researchers to access next-generation sequencing technology and more easily conduct large-scale genomics projects with greater sample volumes, or more breadth and depth in the genome.

The business model was telling. Want a NovaSeq 6000? Get ready to shell out $985K, but you can save $135K by settling for a 5000 at only $850K. This wasn't democratization of sequencing—it was further consolidation at the high end. The strategy was clear: force customers to choose between Illumina's expensive but proven technology or risk falling behind.

But the real revolution came in September 2022. At Illumina's inaugural Genomics Forum in San Diego, the company unveiled the NovaSeq X Series, Using revolutionary new technology, NovaSeq X Plus can generate more than 20,000 whole genomes per year – 2.5 times the throughput of prior sequencers. Most importantly, the company announced it could sequence a human genome for $200.

The technical breakthrough was remarkable. Launch of a fundamentally new sequencing by synthesis (SBS) chemistry, formerly known as Chemistry X – now known as XLEAP-SBS™ – engineered for 2x higher speed and up to 3x greater accuracy. NovaSeq X series took five years to develop. Some 1,500 scientists, researchers and designers worked on the project, which is backed by 40 patents. "We set out to disrupt the status quo and build the technology from the ground up, introducing fundamentally new chemistry, higher-resolution optics, ultra-dense flow cells and more," said Aravanis.

The market reaction was mixed. Illumina's bombastic launch event yesterday, for a suite of new products including the high-end NovaSeq X Plus instrument and a long-read technology, left shareholders cold judging by the 4% fall in the group's stock. The problem wasn't the technology—it was the competition.

Oxford Nanopore and Pacific Biosciences had been chipping away at Illumina's monopoly with long-read sequencing technology that could read DNA fragments orders of magnitude longer than Illumina's short-read approach. While Illumina dominated in accuracy and throughput, long-reads were becoming essential for certain applications, particularly in understanding structural variations and complex genomic regions.

Illumina's response was telling. Rather than acquire the competition (their attempted $1.2 billion Pacific Biosciences acquisition was blocked by regulators), they developed their own long-read technology. But as interest in the company's new long-read technology was "muted", as this is seen as having read lengths well below the native long-read technologies produced by companies including Pacbio and Oxford Nanopore Technologies.

The deeper problem was structural. Illumina had built a business model on continuous price declines driving volume growth. But the math was breaking. Sequencing volume growth had slowed from 52% annually to 25% over the past five years. With annual price declines of 20%, the result was obvious: 25% volume growth minus 20% price declines equals 0% revenue growth.

The platform wars revealed an uncomfortable truth: Illumina's monopoly, while still dominant, was no longer absolute. They controlled the highways, but competitors were building the side roads. The question wasn't whether Illumina would remain the market leader—they would. The question was whether being the leader of a commoditizing market was still a prize worth having.

VII. Business Model Deep Dive: The Genomics Toll Road

To understand Illumina's dominance, you need to understand its business model—and it's brilliant in its simplicity. Like Gillette with razors or HP with printers, Illumina built a consumables empire disguised as a hardware company. The machines are just the gateway drug; the real addiction is the reagents.

The economics are seductive. Revenue of $1.09 billion for Q1 2023 might sound modest for a supposed monopolist, but the margins tell the real story. The company's CFO, Joydeep Goswami, noted a decrease in non-GAAP gross margin primarily due to product mix and lower manufacturing volumes—but even in decline, Illumina maintains gross margins that most hardware companies can only dream of.

The instrument placement strategy is pure financial engineering. Sell a NovaSeq X for $985,000 to $1.25 million—a price that seems astronomical until you realize it's a loss leader. The real money comes from the consumables: flow cells that cost thousands of dollars and can only be used once, reagents that expire and must be replenished, and software licenses that lock customers into annual contracts.

Consider the math on a single NovaSeq X installation. The instrument might generate $1 million upfront, but over its five-year lifetime, that same customer will spend $5-10 million on consumables. Every genome sequenced requires approximately $200 in reagents (at current prices), and a busy lab might sequence thousands of genomes annually. It's recurring revenue with 70%+ gross margins—the kind of business model that makes software companies jealous.

The customer lock-in is nearly absolute. Once a lab standardizes on Illumina, switching costs become prohibitive. It's not just the capital cost of new equipment—it's retraining staff, revalidating protocols, rewriting analysis pipelines, and risking research continuity. Academic labs with multi-year NIH grants literally cannot afford to switch mid-project. Clinical labs with FDA-approved workflows would need to repeat years of validation work.

This creates what economists call a "two-sided network effect." The more customers use Illumina, the more third-party developers create tools for Illumina platforms. The more tools available, the more attractive Illumina becomes to new customers. It's a virtuous cycle that compounds over time.

The market segmentation is equally strategic. Illumina offers instruments across the entire price spectrum: the iSeq at $20,000 for small labs, the MiSeq at $100,000 for clinical diagnostics, the NextSeq at $250,000 for mid-throughput applications, and the NovaSeq X series at $1 million+ for production facilities. This isn't product diversification—it's market saturation. Every possible customer, at every price point, has an Illumina option.

But the real genius is in the software layer. DRAGEN, Illumina's bioinformatics platform, processes the raw data from sequencing into usable genetic information. By integrating DRAGEN directly into the NovaSeq X hardware, Illumina created another switching barrier. Customers don't just rely on Illumina for sequencing—they rely on it for interpretation.

The clinical market represents the next frontier. Unlike research, where grants fund purchases, clinical applications tap into healthcare spending—a market measured in trillions, not billions. Every FDA-approved test that runs on Illumina equipment creates a regulatory moat. Competitors can't just offer better technology; they need to navigate years of clinical trials and regulatory approval.

Growth in sequencing consumables was driven by mid-teens growth in clinical, showing this transition is already underway. Clinical customers are stickier, more profitable, and less price-sensitive than academic researchers. They're also more likely to sign multi-year contracts and volume commitments.

The regulatory strategy is particularly clever. By working closely with the FDA to establish Illumina platforms as the de facto standard for clinical sequencing, the company created barriers that go beyond technology. New entrants don't just need better sequencers—they need to convince regulators to approve entirely new workflows, a process that can take years and millions of dollars.

Yet cracks are showing in this model. Illumina annual revenue for 2024 was $4.372B, a 2.93% decline from 2023. Illumina annual revenue for 2023 was $4.504B, a 1.75% decline from 2022. Illumina annual revenue for 2022 was $4.584B, a 1.28% increase from 2021. After decades of growth, revenue is declining despite maintaining market dominance.

The problem is fundamental: Illumina's business model depends on continuously declining prices driving volume growth that more than compensates. But there's a floor to pricing—the cost of goods sold—and a ceiling to volume—the total addressable market for sequencing. As both limits approach, the growth algorithm breaks.

The company commits to achieving Core Illumina non-GAAP operating margins of 25% in 2024 and 27% in 2025, but margin expansion without revenue growth is just financial engineering, not value creation. Cost cuts can only go so far before they impact innovation—the very thing that justified Illumina's monopoly in the first place.

The consumables model that built Illumina's empire may ultimately constrain it. High margins attract competition. Regulatory moats slow innovation. Customer lock-in reduces incentive to improve. The toll road is still profitable, but traffic has stopped growing.

VIII. Modern Challenges & Strategic Pivots (2020-Present)

COVID-19 should have been Illumina's finest hour. When a novel respiratory illness emerged in Wuhan in late 2019, it was next-generation sequencing—specifically on Illumina machines—that identified SARS-CoV-2 as the causative agent. Deep shotgun sequencing is unbiased and can be performed on nasal swabs and other samples to look for non-host genomic material, which can then be assembled into potential causative agents. The sequence rapidly identified the virus as one closely resembling a coronavirus endemic in bats, but also revealed a mutation in the protein involved in attaching to host cells that helped explain the ability of the virus to infect human cells.

As the pandemic exploded globally, Illumina rapidly developed the COVIDSeq Test, enabling high-throughput viral surveillance. Aegis began a partnership with the Centers for Disease Control (CDC) in April of 2021 to provide up to 480,000 sequences. "We moved from a single Illumina MiSeq™ to purchasing two NovaSeq™ 6000 platforms, and we have been off to the races ever since." They were able to install the instruments and then validate and launch the Illumina COVIDSeq™ assay in less than six weeks.

The numbers were staggering. In thirteen months, Illumina based SARS-CoV-2 sequencing laboratories contributed to public databases with 28,005 SARS-CoV-2 high-quality sequences and corresponding metadata, which is more than 86% of all genomes in GISAID from the Slovak Republic during the period. Countries worldwide launched genomic surveillance programs, tracking variants in real-time as Alpha gave way to Delta, then Omicron.

For Illumina, COVID represented both opportunity and challenge. Demand for sequencing instruments surged as governments funded surveillance programs. But it also exposed the limitations of centralized sequencing. Most of the existing genomic data comes from large genomic centers where labs have the capacity for high-throughput sample processing, and countries with limited resources to invest in high-throughput sequencers have low submissions to COVID surveillance. The COVIDSeq Assay provides low- and mid-throughput labs access to de-centralized surveillance at a smaller scale, to sequence and identify viral variants that can help public health agencies to manage the COVID-19 pandemic.

Illumina responded by developing the COVIDSeq Assay for smaller labs. The COVIDSeq Assay kit provides reagents to prep up to 96 samples for sequencing on the MiSeq™, MiniSeq™, and iSeq™ 100 Systems, a more manageable alternative to the 3,072 samples on the NovaSeq™ 6000 or even 384 samples on the NextSeq™ 500/550/550Dx/2000. This democratization of surveillance capabilities represented a strategic shift—acknowledging that not every application required Illumina's most expensive platforms.

But as quickly as the COVID boom arrived, it evaporated. By 2023, surveillance funding dried up globally. Growth in sequencing consumables driven by COVID surveillance reversed. The pandemic had given Illumina a taste of what truly widespread sequencing adoption could look like—and then taken it away.

The deeper challenge was strategic focus. While Illumina was building COVID surveillance infrastructure, competitors were advancing in areas that mattered more long-term. Oxford Nanopore's portable sequencers enabled real-time outbreak tracking in remote locations—something Illumina's lab-based instruments couldn't match. Chinese competitors used the pandemic to establish themselves in domestic markets previously dominated by Illumina.

The COVID experience also revealed uncomfortable truths about Illumina's business model. When governments were paying for surveillance, price was no object. But as funding disappeared, the high cost of Illumina's consumables became a barrier to continued monitoring. We slashed the library preparation cost by half by using 50% of recommended reagents at each step and normalizing the libraries before pooling to achieve uniform coverage. Reagent-only cost (∼$43.27/sample) for SARS-CoV-2 variant analysis with this normalized input protocol on MiniSeq instruments is comparable to what is achieved on high throughput instruments such as NextSeq and NovaSeq.

Meanwhile, other challenges mounted. The funding environment for academic research—Illumina's bread and butter—tightened dramatically. NIH budgets stagnated. Venture funding for genomics startups dried up. China, once a growth engine representing 10% of revenue, became increasingly hostile to foreign technology companies. Local competitors like BGI/MGI gained government support and market share.

The company responded with operational excellence initiatives—corporate speak for cost cuts. Building on the cost reduction steps announced in November 2022, Illumina would further reduce its annualized run rate expenses by more than $100 million beginning later in 2023. But cutting costs while maintaining innovation is a difficult balance. Every researcher laid off is potentially a breakthrough not discovered.

The strategic pivots were equally challenging. Illumina pushed into clinical markets, but regulatory approval cycles are long and expensive. They invested in single-cell and spatial biology, but these remain niche applications compared to bulk sequencing. They developed proteomics capabilities, but this put them in competition with established players like Thermo Fisher.

The fundamental problem was that Illumina had optimized for a world of exponentially growing sequencing demand—and that world no longer existed. Academic research budgets were flat. Clinical adoption was slower than expected. Population-scale sequencing remained a dream rather than reality. The growth algorithm that had powered Illumina for two decades—declining prices driving volume growth—had broken.

By 2024, the challenges were impossible to ignore. "Consumable sales remained solid as customers continued to increase their sequencing activity, but instrument demand has softened in a constrained funding environment," CEO Jacob Thaysen admitted. The company that had enabled the genomics revolution was discovering that revolutions, by definition, don't last forever.

IX. Playbook: Lessons from Building a Monopoly

The Illumina story offers a masterclass in building and maintaining market dominance—until it doesn't. The playbook that created a 90% market share contains both timeless principles and cautionary tales about the limits of monopoly power.

Platform Economics in Life Sciences

Illumina understood something fundamental: in life sciences, standards matter more than performance. Once researchers publish using your platform, they're locked in. Every paper citing Illumina sequencing creates pressure for the next researcher to use the same platform for comparability. It's a network effect measured in citations, not users.

The genius was recognizing that academic researchers, not companies, would drive adoption. While competitors chased commercial applications, Illumina subsidized academic access, knowing that today's graduate student becomes tomorrow's biotech founder. Every PhD trained on Illumina equipment became a future customer and evangelist.

R&D Investment Strategy and Innovation Cycles

Illumina's R&D strategy followed a counterintuitive principle: cannibalize yourself before someone else does. The progression from HiSeq to NextSeq to NovaSeq wasn't driven by competitive pressure—Illumina was replacing its own products before competitors could. This created a treadmill effect where customers perpetually upgraded, maintaining revenue growth even with declining unit prices.

But this strategy has a dark side. Constant platform changes mean constant validation costs for customers. Every new chemistry requires reoptimization of protocols. Every new instrument requires retraining. Eventually, upgrade fatigue sets in. Customers start asking whether the marginal improvement justifies the switching cost.

Managing Antitrust Risk While Maintaining Dominance

Illumina's approach to antitrust was to embrace the appearance of competition while ensuring it remained ineffective. They maintained open protocols, published specifications, and even helped potential competitors—knowing their head start and scale advantages were insurmountable. It's easier to defend a monopoly that doesn't look like one.

The GRAIL acquisition revealed the limits of this strategy. Regulators weren't fooled by Illumina's promises to treat all customers equally. When you control the roads, owning the destination creates unavoidable conflicts. The $8 billion GRAIL gamble became a $500 million fine and a forced divestiture—an expensive lesson in regulatory overreach.

Transitioning from Growth to Value

The hardest transition for any growth company is accepting maturity. Illumina's attempts to maintain growth multiples in a maturing market led to increasingly desperate moves: the failed PacBio acquisition, the GRAIL debacle, promises of market expansion that never materialized.

The playbook for mature markets is different: maximize cash generation, return capital to shareholders, and accept single-digit growth. But Illumina's culture, compensation structures, and investor expectations were all built for hypergrowth. Changing that DNA proved harder than sequencing it.

Capital Allocation in High-Margin Businesses

With gross margins above 70%, Illumina generated enormous cash flows. The temptation was to reinvest everything in growth—new platforms, new markets, new acquisitions. But high margins also attract competition. Every dollar spent defending yesterday's business is a dollar not spent inventing tomorrow's.

Illumina's capital allocation revealed a company caught between two strategies. They spent like a growth company—heavy R&D, aggressive expansion—while operating in an increasingly mature market. The result was declining returns on invested capital even as absolute spending increased.

Building Switching Costs Through Workflow Integration

The deepest moat isn't technology—it's workflow. Illumina understood that every touchpoint in the sequencing process was an opportunity to create lock-in. Sample prep, sequencing, analysis, interpretation, storage—each step integrated with the next, making it nearly impossible to switch just one component.

DRAGEN's integration into NovaSeq X hardware was the culmination of this strategy. Customers weren't just buying a sequencer; they were buying an entire workflow. The switching cost wasn't just capital; it was organizational transformation.

The Importance of Consumables in Recurring Revenue Models

The consumables model transformed Illumina from a capital equipment company to a recurring revenue business. Wall Street values predictable revenue streams, and nothing is more predictable than consumables for installed instruments. Every sequencer sold was an annuity stream locked in for years.

But consumables create their own challenges. High margins invite substitution. Customers constantly seek ways to reduce reagent use. Third-party suppliers offer compatible products. The very predictability that Wall Street loves makes the business vulnerable to disruption.

Lessons for Platform Businesses

-

Standards are more powerful than technology. Once established, they're nearly impossible to displace.

-

Academic adoption drives commercial success. Today's researchers are tomorrow's customers.

-

Cannibalize yourself strategically. But know when to stop—constant change exhausts customers.

-

Monopolies attract scrutiny. The more successful you are, the more constrained your strategic options become.

-

High margins are both blessing and curse. They fund innovation but attract competition and regulatory attention.

-

Workflow integration creates real lock-in. But it also creates complexity that becomes its own limitation.

-

Growth company tactics don't work in mature markets. Recognizing market maturity and adapting strategy accordingly is crucial.

-

Consumables models create predictable revenue but commodity risk. The same predictability that supports high valuations makes disruption more likely.

The Illumina playbook worked brilliantly for two decades. It built a monopoly in one of the most important technologies of the 21st century. But playbooks age. Markets mature. Competition evolves. The very strategies that built Illumina's dominance may now constrain its future.

X. Bear vs Bull Case & Investment Analysis

Bull Case: The Genomics Infrastructure Monopoly

The bull case for Illumina rests on a simple premise: they own the rails on which the entire genomics industry runs. With 90% market share after fifteen years of competition, Illumina has proven that their moat isn't just wide—it's nearly uncrossable.

The installed base alone justifies optimism. Thousands of NovaSeq, NextSeq, and MiSeq instruments worldwide represent locked-in consumables revenue for years. Each instrument is a toll booth, generating $200-500 per genome sequenced. With genomic medicine still in its infancy, the runway for growth remains enormous.

Clinical applications represent the next S-curve. As genomic testing moves from research curiosity to standard of care, the addressable market expands from billions to tens of billions. Every FDA-approved test running on Illumina equipment creates regulatory lock-in that competitors can't easily break. The transition from research to clinical transforms Illumina from a tools company to a healthcare infrastructure provider.

The NovaSeq X Series demonstrates continued innovation leadership. Achieving the $200 genome while improving accuracy and speed shows Illumina can still push the technological frontier. Their 1,500-person R&D team and 40 patents on NovaSeq X alone create barriers that capital alone can't overcome.

Operating leverage potential remains significant. After years of growth investments, Illumina is pivoting to margin expansion. Their commitment to 25% operating margins in 2024 and 27% in 2025 suggests substantial earnings growth even with modest revenue increases. Cost discipline could unlock value that growth obscurity has hidden.

The competitive landscape, while evolving, remains favorable. Oxford Nanopore and PacBio combined have less market share than Illumina's quarterly fluctuation. Chinese competitors face geopolitical barriers to Western markets. No one has Illumina's scale, scope, or switching costs.

Emerging markets in chronic disease and population health could dwarf current applications. As healthcare shifts from treatment to prevention, genomic screening becomes essential. Illumina is the only company with the scale to enable population-level sequencing. The $100 genome, when it arrives, won't just expand the market—it will create entirely new ones.

Bear Case: The Commodity Trap

The bear case sees Illumina as a high-multiple stock in a commoditizing industry. Growth has stalled, competition is intensifying, and the core business model is breaking down.

The numbers tell the story. Revenue declined 3% in 2024, 2% in 2023, and grew just 1% in 2022. This isn't a temporary blip—it's a trend. The exponential growth that justified premium valuations is over. Illumina is now a GDP-growth business trading at tech multiples.

Pricing pressure is relentless and structural. Every year, customers expect lower costs per genome. But Illumina has already captured most efficiency gains. The $200 genome might be an achievement, but the path to $100 or $10 requires fundamental breakthroughs that may not come from Illumina. Competitors don't need to match Illumina's performance—they just need to be good enough at a lower price.

Technology disruption is accelerating. Oxford Nanopore's portable sequencers enable applications Illumina can't match. Spatial biology and single-cell technologies are growing faster than bulk sequencing. AI-powered computational approaches might bypass sequencing altogether for some applications. Illumina's dominance in short-read sequencing might become like Kodak's dominance in film—unassailable until irrelevant.

China represents both competitive threat and lost opportunity. BGI/MGI compete globally with government backing and lower cost structures. The Chinese market, once 10% of Illumina revenue, is effectively closed. Every Chinese graduate student trained on BGI equipment is a future customer lost. The geopolitical decoupling of genomics technology creates a parallel ecosystem where Illumina doesn't compete.

Regulatory overhang persists. The GRAIL debacle cost over $500 million in fines plus billions in value destruction. Future antitrust action could limit strategic options. Clinical regulatory requirements slow innovation and increase costs. Every FDA approval is both a moat and a milestone that constrains future flexibility.

Management credibility is damaged. The GRAIL acquisition destroyed shareholder value. Growth promises haven't materialized. The activist investor battles revealed board dysfunction. New CEO Jacob Thaysen faces the impossible task of reigniting growth while cutting costs and rebuilding trust.

Market maturity is undeniable. Academic research funding is flat to declining. Clinical adoption is slower than projected. Population sequencing remains economically unviable. The Total Addressable Market (TAM) that justified growth investments may have been a mirage.

The Commodity Paradox

The core tension is that Illumina's monopoly created the conditions for its own commoditization. High margins attracted competition. Dominant market share triggered regulatory scrutiny. Technical leadership reduced customer urgency to upgrade. Success bred the very challenges now constraining growth.

The broken growth algorithm—where volume growth no longer exceeds price declines—fundamentally changes the investment thesis. Without revenue growth, multiple expansion is impossible. Without multiple expansion, returns depend entirely on cash generation. But cash generation requires the cost cuts that could undermine innovation, accelerating commoditization.

Risk-Reward Assessment

At current valuations, Illumina presents an asymmetric risk profile—but not in shareholders' favor. The bull case requires multiple expansions in currently declining markets. The bear case simply requires current trends to continue.

The downside scenarios are concrete: continued revenue pressure, margin compression from competition, multiple contraction to industrial conglomerate levels. A 30-50% decline from current levels wouldn't be unprecedented for a former growth stock facing maturity.

The upside requires breakthroughs: new markets that actually materialize, clinical adoption accelerating dramatically, or competitive threats failing to scale. These aren't impossible, but they're increasingly improbable given recent history.

Investment Conclusion

Illumina remains a remarkable company with genuine competitive advantages. But remarkable companies can be poor investments when priced for perfection in imperfect markets. The monopoly that seemed eternal now looks temporal. The moat that seemed unbreachable shows cracks.

For existing shareholders, the question isn't whether Illumina will remain dominant—it likely will. The question is whether dominance in a mature market justifies current valuations. History suggests it doesn't.

For potential investors, Illumina represents a value trap disguised as a growth story. The optical cheapness relative to historical multiples ignores the fundamental change in growth trajectory. This isn't a temporary cyclical downturn—it's a structural transition from growth to maturity.

The prudent approach may be to wait. Wait for management to prove they can grow revenue. Wait for margins to demonstrate sustainability. Wait for valuation to reflect reality rather than history. In a commoditizing market with declining growth, time favors patience over urgency.

Illumina built a monopoly that changed the world. But monopolies, like revolutions, carry the seeds of their own destruction. The question isn't if Illumina's dominance will end, but when—and whether shareholders will recognize it in time.

XI. Epilogue & Future Horizons

The path to the $10 genome seems inevitable until you examine the physics. Moore's Law worked because transistors could shrink. But DNA molecules can't get smaller. Chemistry has inherent limits. The exponential cost curve that brought us from $2.7 billion to $200 will flatten. The question isn't if, but when—and what happens after.

Population-scale sequencing remains the holy grail, forever just five years away. The UK's 100,000 Genomes Project became the 500,000 Genomes Project. China promises to sequence millions. But sequencing is the easy part. Storage, analysis, interpretation—these scale linearly with data volume. Every genome sequenced is 100 gigabytes stored forever, analyzed repeatedly, interpreted carefully. The infrastructure costs dwarf the sequencing itself.

The AI revolution promises to transform genomics, but it might also bypass it. Large language models trained on protein sequences predict structure better than decades of crystallography. Machine learning on electronic health records finds disease patterns without genomic data. The question becomes: do we need everyone's genome, or just better algorithms on existing data?

Precision medicine's promise remains largely that—a promise. Pharmacogenomics works for some drugs, some populations, some conditions. But most disease isn't monogenic. Most drug response isn't deterministic. The complexity that genomics revealed undermines the simplicity that precision medicine requires. We sequenced the book of life only to discover it's written in a language we don't fully understand.

China's emergence as a genomics power creates a bifurcated future. Two technology stacks, two regulatory regimes, two scientific communities increasingly isolated from each other. BGI sequences millions while Illumina fights for thousands. Chinese papers cite Chinese technology. Western research ignores Eastern advances. The global scientific enterprise fragments into regional franchises.

Competition from alternative technologies accelerates. Proteins, not DNA, drive biology. Metabolites, not genes, reflect real-time state. The microbiome, epigenome, transcriptome—each offers insights DNA alone cannot provide. Illumina's dominance in genomics might matter less if genomics itself matters less.

What would different leadership do differently? The question haunts Illumina's boardroom. Would fresh eyes see opportunities in maturity rather than fighting for growth? Would outsider perspective recognize that monopolies can be profitable prisons? Would new leadership accept what current management cannot: that Illumina's hypergrowth phase is over?

A private equity owner might strip costs, maximize cash generation, and distribute profits rather than chase dreams. A strategic acquirer might integrate Illumina into a broader diagnostics portfolio. A visionary founder might pivot entirely, using Illumina's infrastructure for something beyond sequencing. Each path requires admitting what current strategy denies: the old model is broken.

Key Lessons for Platform Businesses and Market Dominators

First, dominance is temporary, even when it seems permanent. Illumina's 90% market share felt unassailable until growth stopped. Monopolies don't gradually erode—they persist until suddenly they don't. The same network effects that create lock-in can reverse, creating spiral-out.

Second, customers remember monopolist behavior. Every time Illumina raised consumables prices, every time they forced an upgrade, every time they ignored customer feedback—these accumulated grievances wait for alternatives. Monopolists confuse customer retention with customer satisfaction until competition reveals the difference.

Third, technology transitions are discontinuous. Illumina optimized short-read sequencing to perfection, but perfect implementation of old technology loses to imperfect implementation of new technology. The next platform won't be a better Illumina—it will make Illumina irrelevant.

Fourth, regulation is the monopolist's shadow. Success attracts scrutiny. Scale triggers intervention. The very moats that protect the business become walls that constrain it. The GRAIL acquisition wasn't just a failed deal—it was a $8 billion lesson in the limits of monopoly power.

Fifth, financial engineering isn't strategy. Margin expansion through cost cuts works once. Share buybacks boost EPS until they don't. Multiple expansion requires growth, and growth requires investment, and investment pressures margins. The financial optimization that Wall Street rewards often undermines the innovation that built the monopoly.

Sixth, culture calcifies with dominance. The hunger that built Illumina differs from the entitlement that maintains it. Risk-taking becomes risk-avoidance. Innovation becomes iteration. The organizational antibodies that protect the core business reject the very changes needed to transcend it.

Finally, timing matters more than technology. Illumina succeeded not because they had the best technology—Solexa did. They succeeded because they had good-enough technology at the right time with the right business model for the right customers. That alignment of factors can't be engineered—only recognized and exploited.

The Ultimate Question

Standing in San Diego, looking out at Illumina's gleaming campus, you see a monument to scientific capitalism. Thousands of employees, billions in revenue, products that literally decode life itself. It's impossible not to be impressed. But monuments commemorate the past, not the future.

The ultimate question isn't whether Illumina will survive—it will. Large companies with monopoly positions and switching costs don't disappear; they fade into industrial conglomerate obscurity. The question is whether Illumina can transcend its origins, evolving from a sequencing company to something greater—or whether it will remain trapped in the monopoly it built.

History suggests the latter. Companies that define categories rarely transcend them. IBM dominated mainframes but missed PCs. Microsoft owned PCs but missed mobile. Google conquered search but struggles with social. The capabilities that create dominance become constraints on evolution.

Illumina's story isn't over, but its heroic chapter might be. What follows could be equally important—a lesson in how monopolies age, adapt, or atrophy. The genomics revolution Illumina enabled will continue, but whether Illumina continues to lead it remains uncertain.

The company that brought the $1,000 genome, then the $200 genome, might deliver the $10 genome. But by then, the world might have moved on to questions that sequencing can't answer. The ultimate irony would be Illumina achieving its technical goals just as they cease to matter.

In the end, Illumina's legacy won't be the monopoly it built but the industry it enabled. Every cancer detected early, every rare disease diagnosed, every agricultural advancement—these matter more than market share or margins. Illumina democratized reading DNA, even if it couldn't democratize understanding it.

The future belongs to companies we haven't heard of, solving problems we don't yet know exist, with technologies we can't imagine. Illumina's monopoly created the foundation for whatever comes next. That's both their greatest achievement and their fundamental limitation—they built the platform for their own disruption.

Whether that disruption comes from long-reads, proteins, AI, or something entirely unexpected, one thing seems certain: the next chapter of genomics won't be written in San Diego. Monopolies don't innovate themselves out of existence. They persist until they don't, replaced not by better versions of themselves but by different answers to different questions.

Illumina sequenced the genome. The question now is who will sequence what comes after genomics. That company, wherever it is, whatever it's doing, represents the future that Illumina's monopoly made possible but cannot itself become.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube