IDEX Corporation: The Silent Fluidics Compounder

I. Introduction & Episode Roadmap

Here is the paradox at the center of this episode. IDEX is, by any honest definition, a rollup — a serial acquirer that grows by buying other companies. And rollups, as a species, are where investor capital goes to die. The graveyard is enormous: Tyco, Valeant, roll-ups of funeral homes, of dental practices, of trucking firms. The pattern is almost always the same. A company buys aggressively, promises synergies, jams the acquisitions together, destroys the thing that made each target special, and eventually collapses under the weight of its own goodwill and debt.

The word to hold onto is fluidics. IDEX is, at its core, a company that moves, measures, filters, focuses, and controls the flow of liquids, gases, and light. Ashleman himself boils the whole sprawling portfolio down to a single sentence: the company moves "fluids, gas or light." That is a surprisingly precise description of an $8-billion-plus-in-market-value collection of businesses that most investors could not describe in a sentence at all. And the reason the description matters is that it is the thread connecting a 1911 gear pump to a 2024 porous-metal filter — the same fundamental problem, moving something precisely from here to there where failure is not an option, solved with ever more exotic technology.

IDEX did the opposite of almost everything on the rollup graveyard list, and it worked. The company runs more than fifty distinct operating businesses, keeps most of their brand names and management teams intact, and still produces gross margins in the mid-40% range and adjusted EBITDA margins in the high-20s.12 In 2024 it turned roughly $3.27 billion of revenue into about $505 million of net income; in 2025, revenue grew to about $3.46 billion.3 For most of its life the stock quietly outran the broad industrial index, the kind of chart that makes people ask, after the fact, how they never noticed.

So how does a maker of gear pumps, stainless-steel clamps, and microscopic glass filters become one of the most consistent compounding engines in industrial history? That is the question this episode exists to answer — and, just as importantly, to stress-test, because the machine that built IDEX may be running into the mathematical limits of its own success.

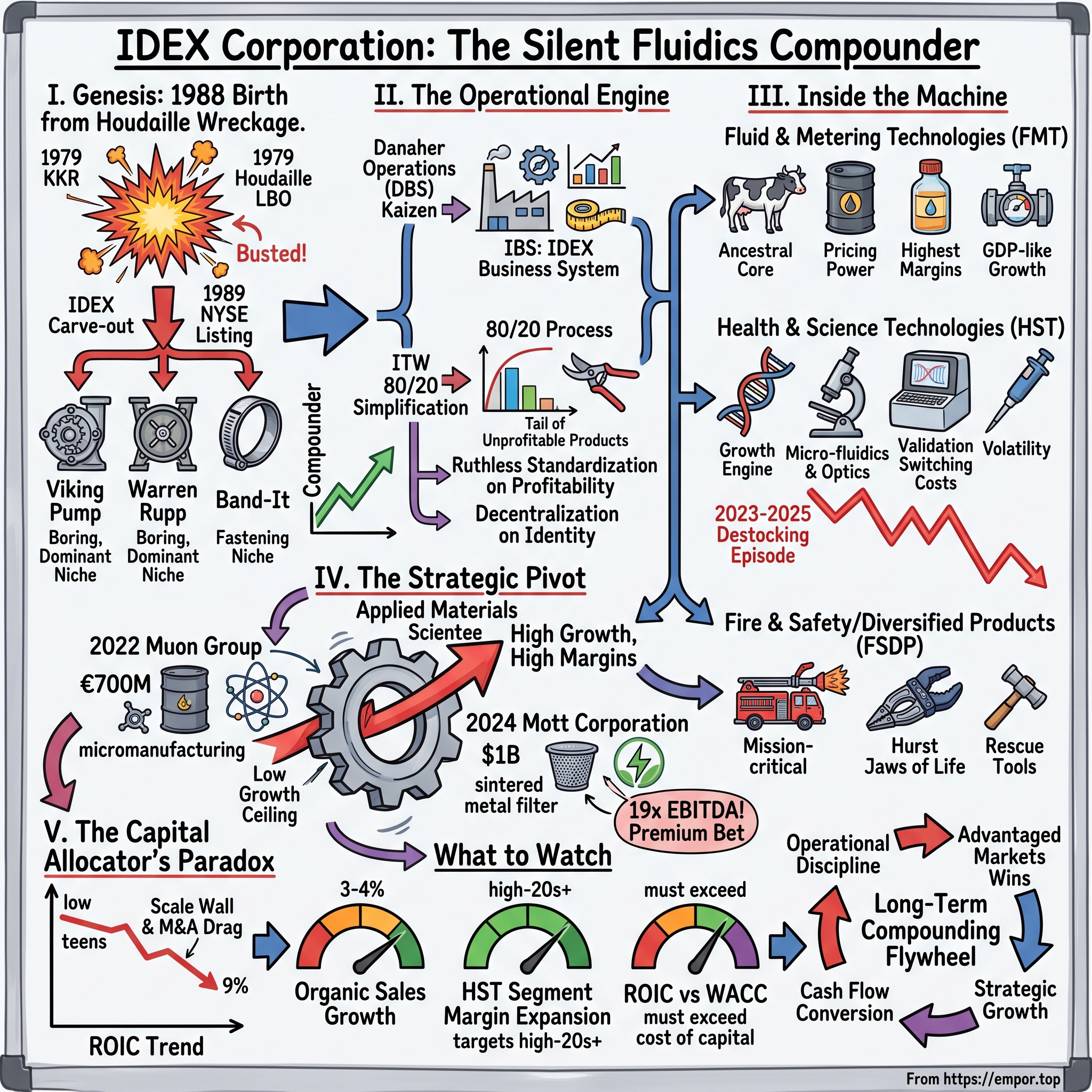

The roadmap runs like this. First, the genesis: how KKR's historic 1979 buyout of Houdaille Industries — the first true mega-LBO of a public company — blew up, and how the salvage operation gave birth to IDEX in 1988. Second, the operational secret: the unusual fusion of Danaher-style continuous improvement with Illinois Tool Works' legendary "80/20" simplification discipline. Third, the machine itself: where the cash is actually made across three segments with very different economics. Fourth, the pivot: IDEX's deliberate march away from cheap industrial iron toward high-margin applied materials science, capped by the roughly $1 billion purchase of Mott Corporation in 2024. And finally, the skeptical case: why the same growth that built the company has quietly compressed its return on invested capital from the low-to-mid teens down toward 9%, and whether current management has an answer.

To understand any of it, you have to start with a bankruptcy-adjacent disaster that most of Wall Street has chosen to forget.

II. The Houdaille Wreckage & The Birth of IDEX

In May 1979, a New York firm barely three years old and staffed by a handful of former Bear Stearns bankers did something that had never been done at scale. Kohlberg Kravis Roberts took Houdaille Industries — a publicly traded, half-century-old maker of machine tools, industrial pumps, chrome car bumpers, and vibration dampers — completely private in a $380 million leveraged buyout.4 The mechanics were audacious to the point of absurdity. Of that $380 million, roughly $300 million was borrowed from a syndicate of banks and insurance companies, and only about $1 million came directly out of KKR's own pocket.4 A tiny sliver of equity, mountains of debt, and a public company disappears into private hands. This was the template. Every LBO that followed — the whole private-equity industry, the RJR Nabisco circus a decade later, the entire language of "financial engineering" — traces its lineage to Houdaille.

To grasp why this deal mattered so much, you have to appreciate what the three founders of KKR — Jerome Kohlberg, Henry Kravis, and George Roberts — were actually selling. Their insight, developed in the 1960s and 1970s, was that a stable, cash-generative company was in effect an under-leveraged balance sheet. If you could borrow against its predictable cash flows to buy it, use that cash flow to pay down the debt, and hand management a slug of equity to align their interests, you could turn a modest sliver of your own capital into an enormous return — provided nothing went wrong. Houdaille, with its diversified industrial cash flows and its conservative balance sheet, looked like the perfect proof of concept. The banks agreed, and history was made. Before Houdaille, the leveraged buyout was a cottage technique used on small private companies. After Houdaille, it was a force that would reshape corporate America for the next forty years.

For a few years it looked brilliant. And then it looked like a case study in what debt does to a cyclical industrial company when the world turns against it. The early-1980s recession hammered demand. Worse, Houdaille's crown-jewel machine-tool business — the very engine of cash flow the deal had been underwritten against — ran straight into a wall of Japanese competitors who were better, cheaper, and relentless. Companies like Yamazaki and Mori Seiki were flooding the American market with computer-controlled machine tools at prices Houdaille could not match, and a company that desperately needed to reinvest to compete instead had to funnel its cash into servicing a crushing debt load. It is the fundamental fragility of the LBO in a single example: leverage magnifies returns on the way up and magnifies ruin on the way down, and it leaves no margin for a business that suddenly needs to fight for its life. Houdaille was slowly dismembered — divisions sold, plants closed, thousands of jobs gone. Critics would later use it as Exhibit A in the argument that the LBO boom hollowed out American manufacturing; one widely read 1989 op-ed simply titled the post-mortem "How to Kill a Company."5 By the mid-1980s the once-proud conglomerate was a carcass being picked apart.

In 1987, the British engineering group TI Group (Tube Investments) bought what was left of Houdaille, mainly for its industrial products.[^6] But TI had its own priorities, and after the October 1987 stock-market crash it wanted cash and focus, not a grab-bag of small American niche manufacturers. That created an opening — and KKR, which knew these assets intimately, walked back through the door it had opened eight years earlier.

Here is where the story pivots from tragedy to something more interesting. In 1988, KKR and a management team led by Donald Boyce carved three unglamorous, cash-generative divisions out of the Houdaille estate — Viking Pump, Warren Rupp, and Band-It — and packaged them into a brand-new company incorporated in September 1988.[^6] They named it IDEX, a coined word meant to evoke Innovation, Diversity, and Excellence, though the name mattered far less than the assets. In 1989 IDEX listed on the New York Stock Exchange.[^6]

There is a delicious irony worth pausing on. IDEX — a company that would go on to become one of the most durable value-creators in industrial history — was assembled by KKR from the debris of the deal that first taught Wall Street how leverage could destroy value. The same firm, the same assets, the same financiers; opposite outcome. The difference was not the tools of finance but what got built with them. Where the Houdaille LBO had loaded a fragile, competitively exposed machine-tool business with debt it could not survive, the IDEX carve-out did the reverse: it isolated the three most stable, least cyclical, most defensible little businesses in the whole estate and gave them room to breathe.

What made those three businesses special was not size or growth or technology. It was dominance of tiny markets no one else wanted. Viking Pump, founded in 1911 in Cedar Falls, Iowa, made internal gear pumps — devices that move thick, sticky, difficult fluids like asphalt, chocolate, resin, and adhesives, the substances that would gum up or destroy an ordinary centrifugal pump — and had held a commanding share of that obscure niche for the better part of a century.6 Warren Rupp made air-operated double-diaphragm pumps, the workhorses used to move slurries and corrosive liquids where reliability matters more than elegance. Band-It made stainless-steel clamping and banding systems used to fasten things in the harshest environments on earth, from oil rigs to utility poles. None of them would ever appear in a headline. All of them threw off cash with the reliability of a utility, precisely because they sold mission-critical components into markets too small for larger competitors to bother attacking.

Under CEO Donald Boyce, IDEX spent the 1990s doing methodically what it would do for the next thirty years: using the cash from these founding franchises to acquire more small, dominant, niche businesses, one careful bolt-on at a time. The portfolio grew — fluid handling, dispensing equipment, fire and rescue tools — but the philosophy stayed fixed. That was the founding insight, and it never really changed: own the boring, essential thing that a customer cannot easily replace and will not shop hard on price. Everything IDEX became — the acquisition machine, the margin profile, the operating philosophy — is an elaboration of a lesson learned in the ruins of Houdaille. What the company needed next was a system to run it, a way to make the machine repeatable and not merely lucky. That arrived, imported wholesale, from two of the most admired operating cultures in American industry.

III. The Lineage of the Engine: Danaher Operations Meets ITW 80/20

For its first decade and a half, IDEX was a competent, acquisitive, mid-cap industrial — good, not legendary. The transformation into a genuine compounding machine began in 2005, when the board hired a Danaher man.

To understand why that mattered, you have to understand Danaher, the company that quietly reprogrammed how a generation of industrial executives think. Danaher had adapted the Toyota Production System into something called the Danaher Business System — DBS — a relentless, almost religious culture of continuous improvement, or kaizen. In a DBS company, managers run structured "kaizen events," measure everything, cut waste obsessively, and treat operational excellence not as a project but as a permanent way of life. Danaher used DBS to turn ordinary acquisitions into extraordinary cash machines, and its alumni scattered across corporate America carrying the gospel.

Larry Kingsley, who became IDEX's CEO in 2005, was one of them. He took the DBS philosophy and rebuilt it inside IDEX as the IDEX Business System (IBS) — the same insistence on lean manufacturing, data-driven decision-making, and continuous improvement, now aimed at IDEX's collection of niche pump and component businesses. IBS was not a binder of slogans; it was a set of habits. Managers learned to map the flow of value through a factory and hunt for waste in it, to run rapid-improvement events that reorganized a production cell in a week, and to hold themselves to hard metrics on quality, delivery, and cost. The point was cultural as much as mechanical: to make the pursuit of a slightly better process next month a permanent condition rather than a periodic campaign. IBS gave the company a common operating language across dozens of otherwise unrelated businesses and a repeatable way to squeeze more profit out of each acquisition. It was the first half of the formula, and it is why Kingsley — who later left to run Pall Corporation — is remembered inside IDEX as the man who professionalized the machine.

The second half arrived in 2011, when another Danaher alumnus, Andy Silvernail, succeeded Kingsley as CEO. Silvernail was a different kind of executive — a capital-allocation obsessive who talked, more openly than most CEOs dare, about the CEO's real job being the deployment of every incremental dollar to its highest return. He would run IDEX for nearly a decade, and his imprint on the company's intellectual DNA is arguably deeper than anyone's since the founders. Silvernail — intense, cerebral, unusually willing to talk publicly about capital allocation as the core job of a CEO — added an ingredient that would define the modern IDEX. He layered onto IBS the 80/20 simplification process, the operating religion of Illinois Tool Works. This was not an accident of osmosis; it was deliberately imported at the board level, guided in part by David Parry, a former vice chairman of ITW who joined the IDEX board in 2012.

So what is 80/20, and why does it matter so much? The Pareto principle — the observation that roughly 80% of results come from 20% of causes — is old and familiar. ITW's genius, developed over decades under leaders like John Nichols and refined into a company-wide religion, was to turn that observation into a hard manufacturing discipline practiced by thousands of managers. In an 80/20 company, managers are pushed to confront a brutal truth about most industrial businesses: a small minority of customers and products generate the overwhelming majority of the profit, while a long tail of small orders, oddball SKUs, and marginal accounts quietly consumes cash, factory floor space, engineering time, and management attention while earning almost nothing — and often losing money once you honestly load in the cost of complexity.

Picture a pump factory that makes a thousand product variants for two thousand customers. An 80/20 analysis will typically reveal that a couple of hundred variants sold to a few hundred customers produce nearly all the profit, and that the remaining sprawl is a hidden tax — it lengthens production runs, bloats inventory, distracts the sales force, and slows the whole plant down. The 80/20 answer is heretical to a traditional sales culture that measures itself by revenue and treats every order as sacred: deliberately walk away from the unprofitable tail. Raise prices on the marginal accounts until they either pay their way or leave. Fire the customers who cost more to serve than they pay. Kill the low-volume product lines and simplify the catalog. Concentrate people, capital, and inventory on the profitable core — what ITW veterans call "quadrant one." Done right, revenue may dip slightly while profit, cash flow, and factory throughput all jump, because the business is finally spending its finite resources only where they earn a return.

Now combine that with IDEX's founding structure, and you get the real secret. Most rollups fail because the corporate center tries to integrate — merging back offices, consolidating sales forces, standardizing products — and in doing so severs the customer relationships and technical know-how that made each target valuable in the first place. IDEX refuses to do this. Its fifty-plus businesses keep their own names, their own leaders, and their own customer relationships. There is no grand plan to merge Viking Pump into Warren Rupp.

Instead of structural integration, IDEX applies operational discipline. It does not touch the brand or the customer list from the outside; it hands each subsidiary manager the 80/20 toolkit and the IBS playbook and lets them prune their own business from the inside. The result is decentralization with a spine — autonomy on identity and customer intimacy, ruthless standardization on how you think about profitability. That combination is genuinely rare, and it is the analytical heart of why IDEX's margins hold up where other acquirers' collapse.

A note of independence is warranted here, because this is exactly the kind of narrative a company loves to tell about itself. The mechanism is real and visible in the margins. But it is worth remembering what 80/20 also does: it grows the bottom line partly by shrinking the top line, pruning revenue that does not pay. That is a wonderful tool in a mature, low-growth business. It is a more complicated one when a company needs to find growth — a tension that becomes the central drama of the second half of IDEX's story. First, though, we need to see where the money actually comes from.

IV. Inside the Machine: Segment Economics & Niche Dominance

Walk into a Viking Pump facility and you will not see anything that looks like the future. You will see machined metal, castings, assembly benches, and engineers who can tell you exactly what happens to a pump when it has to move molten chocolate at one temperature and roofing tar at another. This is the unglamorous physical reality beneath IDEX's financial elegance, and it is organized into three segments that behave like three different companies.

The first is Fluid & Metering Technologies (FMT) — the ancestral core, the businesses that came out of Houdaille and their descendants. In 2024, FMT generated roughly $1.23 billion of net sales at an adjusted EBITDA margin of about 32.9%, the fattest margins in the company.67 This is the cash cow: positive-displacement pumps, flow meters, valves, and dispensing equipment sold under names like Viking Pump, Warren Rupp, Banjo, and Corken. The end markets are the plumbing of the industrial economy — agricultural chemical transfer, fuel and propane handling, sanitary food-and-beverage processing, water and wastewater. In most of these sub-markets IDEX holds the number one or number two position, and the reason it can charge what it charges is worth dwelling on.

Consider the economics from the customer's point of view. A Viking pump might cost a few hundred to a few thousand dollars, and it sits inside a chemical processing line worth millions. If that pump fails, the line stops, and the cost of an hour of downtime dwarfs the price of the pump many times over. So the customer does not buy on price; they buy on reliability, on the specific engineering fit, and on the certainty that the replacement will be identical to the one that has run flawlessly for fifteen years. This is the "mission-critical but low cost-to-value" dynamic, and it is the single most important idea in the entire IDEX story. It shows up as pricing power, as customer stickiness, and ultimately as margin.

There is a second, subtler moat inside FMT that investors often miss: distribution. Many of these products are not sold directly but through networks of specialized industrial distributors who stock IDEX parts, know the applications, and recommend them to end users. Once a brand like Banjo — the standard in agricultural chemical transfer fittings — is embedded in that distributor channel, a competitor has to dislodge not just the customer's preference but an entire ecosystem of intermediaries who have built their businesses around carrying it. That is why FMT's margins are the fattest in the company and also the most stable: the demand is unglamorous and GDP-like, but the competitive position is close to unassailable, and the pricing is set by value rather than by a spot market. The trade-off, as we will see, is that all this durability comes with a low natural growth rate — a chemical plant does not need twice as many fuel-transfer pumps next year — and that ceiling is the strategic problem that eventually drove IDEX to reinvent itself.

The second segment, Health & Science Technologies (HST), is where IDEX has been reinventing itself. In 2024, HST was the largest segment by revenue at roughly $1.30 billion, but at a structurally lower adjusted EBITDA margin of about 26.7%.67 The lower margin is the point: this is higher-technology, faster-growing, more competitive territory. HST makes high-precision micro-fluidics, optical filters, specialized valves, and sealing technologies for life-sciences instruments, analytical and diagnostic equipment, and semiconductor manufacturing.

It helps to make this concrete, because "micro-fluidics" is the kind of phrase that slides past the ear. Think of a laboratory analyzer — a machine in a hospital or a drug-discovery lab that runs blood or reagents through a maze of tiny channels to identify what is in a sample. The performance of that entire machine depends on the ability to move nanoliter volumes of fluid through those channels with perfect precision, no leaks, no contamination, no dead space where one sample could taint the next. The valves, pumps, fittings, and degassing components that do that work are the invisible plumbing of modern science, and IDEX brands like Rheodyne and Sapphire are longtime leaders in supplying them. Similarly, an optical filter — a precisely coated piece of glass that lets exactly one color of light through and blocks the rest — is the component that lets a fluorescence microscope or a genetic sequencer read its signal; IDEX's Semrock brand is a benchmark name there. When a mass spectrometer or a DNA sequencer needs to move a microscopic, precisely metered volume of fluid or split light into exact wavelengths, the component doing that work is often an IDEX product.

The switching costs here are, if anything, even more extreme than in FMT, because these parts are designed into instruments that must be validated and, in medical uses, regulatory-certified. An instrument maker that has spent years and millions qualifying an IDEX component into its platform is not going to swap it out to save a few dollars; ripping out a qualified part and re-validating the whole system can take months and trigger fresh regulatory review. So once IDEX is designed in, it tends to stay in for the entire commercial life of the instrument — often a decade or more of recurring component and consumable revenue. That is a beautiful annuity when instrument volumes are growing. It is also, as the 2023–2025 destocking episode painfully demonstrated, a source of volatility when the customers who buy those instruments abruptly stop reordering.

The third segment, Fire & Safety/Diversified Products (FSDP), is the smallest at about $744 million of 2024 net sales and roughly 28.8% adjusted EBITDA margin.67 It is a collection of niche leaders where failure is literally a matter of life and death: Akron Brass, which makes the nozzles and valves on fire trucks; Hurst Jaws of Life, the hydraulic rescue tools that firefighters use to cut people out of wrecked cars; and Band-It, the founding stainless-steel clamping business that holds things together in the harshest environments imaginable. Also here sits the dispensing business — the equipment that mixes and tints paint at hardware stores and industrial suppliers — which is more cyclical and project-driven than the rescue franchises.

FSDP is instructive precisely because its economics blend the sublime and the ordinary. The buyer of a Jaws of Life tool is not price-shopping; they are betting a trapped person's survival on the tool working the first time, every time, which is about as pure a mission-critical purchase as exists and commands correspondingly durable pricing. But the paint-dispensing equipment sells into home-improvement and retail cycles that ebb and flow with construction and consumer spending, and in early 2026 it was a visible drag even as the fire-and-rescue franchises grew high single digits.13 The segment is a useful reminder that "IDEX quality" is not uniform across all fifty-plus businesses — it is a spectrum, and part of the 80/20 discipline is knowing which businesses to feed and which to prune. Demand in these fragmented, quick-turn markets can also shift fast, which is why management treats their order rates as a real-time diagnostic of industrial health rather than a source of committed backlog.

Put the three together and a pattern emerges that maps neatly onto the frameworks investors use to think about durable advantage. In the language of Hamilton Helmer's 7 Powers, IDEX's primary edge is switching costs — the validation cycles, re-engineering, and re-certification that make customers deeply reluctant to change a working component. Layered on top is something like a cornered resource: decades of accumulated, hard-to-copy know-how in metallurgy, porous-metal filtration, precision micro-machining, and optics. In Porter's terms, the threat of new entrants is low because the markets are too small and too specialized to attract scale competitors, and buyer power is muted because the component is cheap relative to the cost of it failing.

None of this means IDEX operates unopposed. In FMT it fights direct, brand-versus-brand battles against Dover Corporation's pump businesses (Blackmer, Wilden) and Ingersoll Rand's Precision and Science Technologies division, competing on customization and distributor relationships rather than price. These are war-games fought account by account, application by application, and IDEX generally wins where the specification is tight, the customer is loyal to a proven design, and the distributor relationship is entrenched — and cedes ground where a product has drifted toward commodity status, which is precisely the kind of tail business 80/20 is designed to prune away.

In HST the competitive picture is more sobering. Here IDEX runs up against far larger players — Parker Hannifin, Nordson, and Danaher's Pall filtration business — in a fight where scale, R&D budgets, and the ability to co-develop with the world's biggest instrument makers matter more than niche dominance. That is a quiet but important warning embedded in the strategy: as IDEX has pushed deeper into high-technology fluidics and materials science, it has moved from markets where it is the biggest fish in tiny ponds toward markets where it is a respected but mid-sized fish swimming alongside giants with far deeper pockets. The switching-cost moat still protects the installed base, but winning new platform designs against a Danaher or a Parker is a genuinely harder contest than defending a gear-pump niche. Which is exactly the strategic gamble the company made when it decided to spend a billion dollars remaking itself — a gamble that only makes sense against the low-growth ceiling of the legacy business it was trying to escape.

V. The Pivot to applied Materials: The Mott & Muon Bets

Somewhere in the last decade, IDEX's leadership confronted an uncomfortable arithmetic. A gear pump is a magnificent business, but it is a low-organic-growth business. The chemical plants and fuel terminals that buy them grow with GDP, slowly and cyclically. You can compound value on top of that with 80/20 and bolt-on acquisitions for a very long time — IDEX did — but you cannot escape the ceiling. To grow faster, the company would have to move to a different curve. It chose to climb toward the frontier of applied materials science, and it did so with two large, expensive, revealing acquisitions.

The first was Muon Group, announced in September 2022 and completed that November for cash consideration of €700 million.89 Muon, based in the Netherlands and sold by the private-equity firm Rivean Capital, was not a pump company at all. It was a collection of miniaturization specialists — brands like Veco, LouwersHanique, and others — with mastery of exotic manufacturing techniques: electroforming, photo-chemical etching, precision laser and thermal processing, and micromechanical fabrication.89 Translated into plain English: Muon makes microscopic, absurdly precise flow paths and structures in metal, glass, and ceramic — the kind of components that let fluids and gases move through medical diagnostics, semiconductor tools, and digital printers at a scale measured in microns.

Electroforming is worth a sentence, because it captures why IDEX wanted this. Instead of cutting a part down from a block of metal, electroforming grows the part atom by atom onto a mold using an electrochemical bath, which allows features finer and more precise than machining can achieve. It is the kind of proprietary, hard-won process knowledge that takes decades to accumulate and cannot be replicated by throwing money at a problem — the "cornered resource" made physical. A year later, in October 2023, IDEX bolted on STC Material Solutions for about $206 million, adding technical-ceramics manufacturing expertise and folding it into the Muon platform.10 Around the same period it also acquired Micro-LAM, a laser-based precision manufacturing specialist, rounding out what management would come to call its Material Science Solutions platform — a deliberately assembled toolbox for making the tiniest, most precise flow paths and optical components in the world.

Then came the statement acquisition. In July 2024, IDEX announced it would acquire Mott Corporation for $1 billion in cash — the largest acquisition in company history.11 It closed in September 2024.12 Mott is the gold standard in sintered porous metal filtration: it takes metal powder and fuses it into precisely engineered porous structures that filter, distribute, and control the flow of gases and liquids at extraordinary tolerances.11 Its parts sit inside advanced semiconductor fabrication equipment, medical devices, aerospace and defense systems, and emerging clean-energy applications like hydrogen electrolysis. This is not a component that competes on price; it is a proprietary materials-science platform embedded in the most demanding manufacturing processes on earth.

And here is where an independent investor has to sit up, because Mott is where IDEX broke its own rules on valuation. For most of its history, IDEX bought overlooked bolt-ons at roughly 8 to 12 times EBITDA — the disciplined multiples of a buyer picking up businesses no one else was chasing. For Mott, IDEX paid a net transaction value of about $900 million after adjusting for roughly $100 million of expected tax benefits, which the company itself acknowledged worked out to approximately 19 times Mott's forecasted 2024 EBITDA.11 Nineteen times. That is not a distressed-seller, no-one-else-wanted-it price. That is a fully competitive, top-of-market price for a prized asset in a contested auction.

The strategic argument for paying it is coherent. Mott gives IDEX a defensible, high-margin, proprietary platform plugged directly into the secular growth stories that industrial investors most want exposure to: advanced semiconductor nodes, space and defense, and hydrogen. Management's framing, repeated across investor materials, is that Mott is "strategic to the core" — a foundational capability, not a financial trade. On the Q1 2026 earnings call, CEO Eric Ashleman offered an unusually candid reflection on the whole applied-materials push, noting that these mission-critical markets have longer adoption cycles that "delayed some things out of the gate," but arguing that the very slowness is the point: "that actually becomes the moat for us once we get through it," because customers who are that risk-averse do not switch once they trust you.13

The skeptical argument is equally coherent, and it is not refuted by management's optimism. At 19 times EBITDA, IDEX paid a price that leaves essentially no margin for error. To see why that number should give an investor pause, compare it to IDEX's own history: buying at 8 to 12 times means you are paying for roughly a decade of current earnings and letting the business's growth and your operational improvements do the rest. Buying at 19 times means you are paying for nearly two decades of current earnings up front, so the deal only works if you can grow those earnings substantially and quickly. If Mott's end markets grow as hoped, the deal looks visionary in hindsight. If they disappoint, or if integration takes longer than planned — and management has openly admitted the newly acquired businesses are still earning below the segment's margin average — IDEX will have parked a billion dollars of capital at a return that dilutes the whole company's historic efficiency for years.

There is also an honest question about consistency of narrative here. For a decade, IDEX told investors its edge was disciplined, patient acquisition of overlooked assets at attractive prices. Mott is the opposite trade: a fully-valued, hotly-contested prize bought at a premium. Management's defense is that the nature of the business changed — that a proprietary materials-science platform plugged into semiconductors and defense is worth a price a gear-pump bolt-on never would be — and that defense is reasonable. But it is exactly the kind of reasoning that every acquirer uses to justify paying up right before the cycle turns, and an independent observer should hold it to the evidence rather than the logic. Paying a premium multiple does not create value on its own; it borrows against future execution. Whether that bet pays off is not a matter of narrative — it is a matter of arithmetic that will play out over years. And that arithmetic is precisely where the case for IDEX gets uncomfortable.

VI. The Capital Allocator's Paradox: The Skeptical Stress Test

Every great serial acquirer eventually meets the same enemy, and it is not a competitor. It is size. This is the problem an activist or a skeptical long-short investor would put at the very center of the IDEX debate, and it deserves to be stated plainly rather than smoothed over.

For most of its history, IDEX earned a return on invested capital comfortably in the low-to-mid teens — the mark of a business that turned each dollar of capital into a healthy stream of after-tax profit. By the financial data of 2024 and 2025, that figure had compressed toward roughly 9%.146 The trend line is unmistakable: capital efficiency that was once a defining strength has quietly eroded.

The mechanism is not mysterious, and it is not primarily a story of operational failure. It is a story of scale colliding with math. As IDEX has grown to well over $3 billion in revenue, small bolt-on deals no longer move the needle. To grow meaningfully, the company has to buy bigger businesses — and bigger, higher-technology businesses like Mott and Muon are sold in competitive, well-banked auctions where the price gets bid up. Every one of those premium acquisitions loads the balance sheet with goodwill and intangible assets. That inflates the denominator of the ROIC equation — invested capital — faster than the newly acquired operating profit can grow the numerator. The result is exactly what the numbers show: a company that is larger, arguably higher quality, and less capital-efficient than it used to be. This is the "growth wall" that every rollup eventually hits, and IDEX has hit it in slow motion.

Layered on top of the capital-efficiency problem was a demand problem. Across roughly 2023 to 2025, IDEX's organic growth ran flat to negative for stretches — a jarring change for a company that had trained investors to expect steady expansion. The main culprit was not IDEX-specific; it was a violent inventory correction. During the pandemic, life-sciences and medical-instrument customers had over-ordered components to protect against shortages. When the shortages passed, they stopped ordering and worked down their stockpiles — a phenomenon called destocking that battered the entire life-sciences supply chain, from Danaher to Agilent to Thermo Fisher. IDEX's HST segment, so carefully built up as the growth engine, took the brunt of it, compounded by cyclical softness in chemicals and semiconductors.

It is worth explaining the destocking mechanism in plain terms, because it is the key to understanding why a high-quality company posted such disappointing numbers through this stretch. During the pandemic, when supply chains were breaking and lead times stretched to absurd lengths, IDEX's instrument-maker customers did the rational thing: they ordered far more components than they immediately needed and stockpiled them, terrified of being caught without a critical part. That artificial over-ordering flattered IDEX's revenue on the way up. Then the shortages eased, and those same customers looked at their overflowing warehouses and simply stopped ordering, drawing down inventory they already owned. IDEX's sales fell not because end demand for scientific instruments had collapsed but because the channel was digesting a stockpile — a whipsaw that hit the entire life-sciences supply chain, from Danaher to Agilent to Thermo Fisher, at roughly the same time. IDEX's HST segment, so carefully built up as the growth engine, took the brunt of it, compounded by genuine cyclical softness in chemicals and semiconductors.

This is where reading the actual earnings calls matters, because they reveal how management handled adversity — and management credibility is built or destroyed in exactly these moments. Across the destocking period, IDEX's leadership was consistent in a specific and testable way: rather than chase revenue with defensive, dilutive M&A or abandon the strategy, they leaned harder into 80/20, using the downturn to prune tail products and protect margins even as sales stagnated. The proof is in the margin line — adjusted EBITDA margins stayed in the high-20s through a period of negative organic growth, which is genuinely hard to do and speaks well of operational discipline. It is one thing to protect margins when volumes are rising and leverage does the work for you; it is another to hold them when volumes are falling, because that requires actively cutting cost and complexity fast enough to offset the lost leverage. IDEX did the latter, and it is the strongest single piece of evidence that the operating system is real rather than a fair-weather story.

But an independent read also has to note where analysts pushed back, because they pushed hard. On recent calls, the sharpest questions were not about the macro; they were about IDEX's own acquisitions. On the Q1 2026 call, Stifel's Nathan Jones pressed on why the incremental margins in HST — the profit dropping through on each new dollar of sales — were stuck in the low-30s when history and long-term expectations would put them closer to 40%. The answer went straight to the acquisitions: those recently bought businesses, Mott, Muon, and Micro-LAM, are still earning margins below the HST segment average, diluting the very profitability IDEX is famous for. CFO Sean Gillen conceded the point directly — they "are below the segment EBITDA margins of kind of 26%, 27%" — and said lifting them requires "some 8020 actions," pruning and refocusing, before the flow-through can climb back toward 40%, likely into 2027.13 TD Cowen's Joe Giordano probed the same nerve from a different angle, asking essentially whether the whole applied-materials detour had been worth the pain of slow starts; Ashleman's reply reframed the slowness as the moat itself, arguing the very caution of these risk-averse customers is what makes them impossible to dislodge once won.13

Both exchanges are revealing. The premium assets IDEX paid up for are, so far, a drag on the metric that made IDEX special, and management's answer is to apply the same operational medicine it applies to everything else — on a timeline it can describe but cannot precisely promise. An investor's job is to hold that promise to the tape. The mechanism is credible and the early order data is encouraging, but "we will get the margins up with 80/20" is, until it shows up in the segment margin line, an assertion rather than an achievement.

That is the honest state of the stress test: a high-quality company that has paid up to buy growth, temporarily surrendered some capital efficiency to do it, and is now asking investors to trust that its operating system will convert expensive assets into the returns of old. Whether that trust is warranted comes down, in large part, to the people running the machine.

VII. Management & Governance Audit

When Eric Ashleman talks on an earnings call, he does not sound like a promoter. He sounds like an operator — a plant guy who happens to run a public company — and that is more or less exactly what he is. Ashleman became CEO of IDEX in December 2020, taking the reins from Andy Silvernail, but he was no outsider: he had joined IDEX in 2008 and, before that, had run operations and general management across three different divisions of Danaher.13 The lineage, once again, runs straight back to DBS. IDEX has now been led for two decades by executives steeped in the same operating philosophy, which is part of why the strategy has been so consistent across CEO transitions.

The predecessor matters to the story too. Andy Silvernail left IDEX in 2020 not because he faltered but because he had built the machine to run without him; he went on to become chairman and CEO of API Group, taking his capital-allocation gospel elsewhere. That IDEX handed the wheel to a fellow operator from the same Danaher school, and that the strategy did not lurch afterward, is a governance data point in its own right. Succession is where many great compounders quietly break — the founder-genius leaves and the discipline dissolves. IDEX has now navigated two CEO handoffs, Kingsley to Silvernail and Silvernail to Ashleman, without abandoning the operating system, which suggests the system is genuinely institutional rather than personal.

The current CFO is Sean Gillen, who partners with Ashleman on the capital-allocation discipline that is, for a serial acquirer, the whole ballgame.13 The framing the two of them return to, again and again, is control: focus relentlessly on the operational levers the company can actually pull — productivity, price/cost, portfolio pruning — and treat macro headwinds as an occasion to do more 80/20 rather than an excuse. On the Q1 2026 call, Ashleman used the word "trust" to describe the culture and returned repeatedly to the idea of "focus on what we can control," while Gillen walked analysts through leverage held near 2 times, liquidity of roughly $1.1 billion, and a buyback pace the company intended to keep steady all year.13 It is a low-drama, low-ego communication style, and across multiple calls it has stayed notably consistent, which is itself a form of credibility. Management that tells the same story in good quarters and bad, and explains its misses in concrete operational terms rather than blaming the weather, earns more benefit of the doubt than management that reinvents its narrative every quarter.

The behavioral record supports a reasonably favorable read on discipline, with caveats. Through the destocking downturn, IDEX did not panic-buy revenue or abandon its buyback-and-bolt-on cadence. In the first quarter of 2026, with results improving, the company repurchased $76 million of its own shares and signaled it would keep that pace all year, paid $53 million in dividends, and held gross leverage at roughly 2 times EBITDA — a conservative balance sheet that preserves optionality.13 It also raised full-year 2026 organic-growth guidance from an initial 1–2% range to 3–4% and lifted its adjusted EPS outlook, a rare instance of a management team under-promising and then delivering enough to walk guidance up rather than down.13 Crucially, Ashleman and Gillen were explicit that the raise came from internal growth initiatives and recent M&A rather than a cyclical rebound they could not control — a distinction that, if it holds, matters for how durable the improvement is.13

An activist would still find things to poke at, and honesty requires naming them. Portfolio complexity is the obvious one: running fifty-plus decentralized businesses is a feature when it works and a governance risk when it does not, because problems in a small subsidiary can fester unseen beneath a corporate center that deliberately keeps a light touch. The very autonomy that preserves each unit's customer intimacy also means the parent relies heavily on culture and metrics rather than direct control — and culture is invisible until it fails. Disclosure at the individual-business level is thin by design; IDEX reports three segments, not fifty units, which asks investors to take a great deal of the operating story on trust and makes it genuinely hard to see where value is being created or destroyed inside the machine.

And the central capital-allocation question hangs over everything: after years of preaching discipline, management paid 19 times EBITDA for Mott. That is not necessarily a governance failure — a great asset can be worth a great price — but it is a decision a skeptical board member should be interrogating, and shareholders are right to watch whether it becomes a pattern or remains an exception. The tell will be the next few large deals: if IDEX keeps reaching up the multiple ladder to feed its growth, the bear's capital-efficiency thesis strengthens; if Mott proves to be a one-time strategic exception and the company returns to disciplined bolt-ons and buybacks, the bull's case holds. The company's own investor materials describe management incentives as heavily weighted toward long-term, performance-based equity, which is the right structure in principle. The test, as always, is whether the performance metrics actually reward genuine capital efficiency — returns above the cost of capital — rather than merely rewarding growth in revenue and earnings that a serial acquirer can always manufacture by simply buying more. On that question, the ROIC line is the honest scoreboard, and right now it is telling a cautionary story.

On balance, the management read is that of a credible, consistent, operationally excellent team that has made one large, expensive, unresolved bet. Which sets up the real question for any investor: from here, does IDEX win, and what would prove the bulls wrong?

VIII. Bull vs. Bear Case & What to Watch

Let us war-game both sides honestly, because IDEX is a company where the bull and bear cases are unusually well-matched and rest on the same set of facts interpreted through opposite lenses.

The bull case begins with the durability of the machine. The 80/20 operating system is intact and, if anything, evolving — on recent calls management described increasingly using 80/20 not just to cut costs but as a growth tool, deliberately concentrating capital and talent on the fastest-growing "advantaged" applications: data-center power and cooling, semiconductor manufacturing, space and defense, and municipal water.13 Ashleman described this as a "flywheel": as the company doubles down on winning customers in advantaged markets, it can prune and simplify elsewhere, which frees resources to double down further — growth and margin reinforcing each other rather than trading off. It is a genuinely different use of a tool that, for a decade, was mostly about defense and cost.

In the first quarter of 2026, the strategy showed real signs of working. Organic sales grew 5%, organic orders grew about 10%, and HST — the segment that had been ground zero for destocking — grew orders 17% and revenue 11%, building a backlog that management said improves visibility into 2027.13 More telling than the headline numbers was where the strength came from: the exact advantaged markets IDEX had spent the prior three years pivoting toward. Management highlighted its optics feeding secure data transmission and Mott's filtration supporting propulsion and thermal management in space and defense systems; valves positioned around liquid cooling for AI data centers; broad semiconductor exposure spanning consumables, metrology, and lithography; and a water platform, focused on storm-water monitoring and high-purity water for chip fabs, that grew high single digits.13 These are not GDP-plus industrial markets; they are the secular growth stories of the decade, and IDEX is now genuinely plugged into them. The bull argues that once the life-sciences correction fully clears and the Mott/Muon platforms get the 80/20 treatment, both organic growth and HST margins inflect upward together — and that the multiyear "tails" on these program wins, which Ashleman stressed repeatedly, mean the growth is more durable and more visible than anything in IDEX's cyclical past.

The bull case also rests on cash and pricing. IDEX consistently converts more than 100% of net income into free cash flow, a sign of high earnings quality and modest capital intensity, which hands management a durable war chest to fund bolt-ons, buybacks, and dividends without straining the balance sheet.13 That capital-light quality is not incidental; management stressed on the Q1 2026 call that none of its businesses is particularly capital-intensive, and that even the recent uptick in growth capital spending remains low relative to the size of the company — with 80/20 itself acting as an internal funding source, because pruning a low-value product line frees up the very equipment and floor space needed to run a faster-growing one.13 A business that grows without consuming much capital is the mathematical foundation of compounding, and IDEX has it.

And the switching-cost moat translates into genuine pricing power: through the recent inflationary and tariff turbulence, IDEX was able to raise prices to offset cost increases without triggering the volume pushback that a commodity supplier would face — a direct, observable proof point of the mission-critical thesis rather than a management assertion.13 Gillen made the point explicitly, framing the tariff episode as evidence that IDEX's businesses "have the ability to move price in accordance with what they're seeing in cost."13 For a long-term investor, that pricing behavior is worth more than any single quarter's growth rate, because it is the mechanism by which a business protects its real returns against inflation over decades — and it is the clearest evidence that the moat described throughout this story is not a slide-deck abstraction but something customers demonstrate with their wallets.

The bear case does not dispute the quality; it disputes the price and the math. Start with valuation: IDEX has long traded at a premium multiple to the broad industrial sector, the classic "quality compounder" rating. A premium multiple is a promise — it prices in years of above-average execution — and it leaves the stock exposed if growth or returns disappoint. This is the "quality trap": a wonderful business can still be a mediocre investment if you overpay for it, and the bear argues IDEX is priced for a perfection that its own ROIC trend is quietly undermining.

The second bear pillar is the M&A drag already dissected: if IDEX must keep paying 15–20 times EBITDA to buy the growth its size demands, return on invested capital may stay anchored near 9% rather than recovering toward the mid-teens, structurally eroding the capital efficiency that made the stock a long-term winner in the first place. The third is complexity risk — the possibility that a portfolio swollen past fifty disparate businesses eventually overwhelms even a decentralized control model, producing localized failures that are invisible until they are not.

There is also a live risk radar worth naming without overstating. IDEX's short-cycle industrial businesses — much of FMT and FSDP — turn over inventory in weeks and give management visibility only about halfway into any given quarter, which means demand can shift under the company faster than it can see coming; on the Q1 2026 call, Ashleman described order rates that were weak in January, better in February, and strong in March, then explicitly declined to extrapolate the improvement because of "the overhang of the geopolitical situation."13 Tariffs are a genuine but so-far-manageable overhang: management noted that new tariffs had largely replaced repealed ones, leaving little net financial impact, and that IDEX's pricing power let it pass through tariff-driven costs — a real-time demonstration of the switching-cost moat, but also a reminder that the company operates global supply chains exposed to trade policy.13 The life-sciences end market carries its own specific headwinds that have nothing to do with inventory: pressure on Chinese demand and constraints on U.S. academic research funding tied to the NIH, both of which management expects to persist.13 None of these is existential. Together they explain why even a raised 2026 outlook still embeds a deliberately conservative, flattish assumption for the legacy industrial segments.

Running both cases through the strategic frameworks sharpens the verdict rather than resolving it. Through Helmer's 7 Powers, IDEX's switching-cost and cornered-resource advantages are real and, in HST, arguably strengthening as the applied-materials platforms deepen. Through Porter's five forces, the threat of substitutes and new entrants remains low in the legacy niches but rises in the high-technology markets where IDEX now competes against Parker Hannifin, Nordson, and Danaher's Pall — larger rivals with deeper R&D. The moat, in other words, is not weakening, but the terrain IDEX has chosen to expand into is more contested than the ponds it used to dominate. That is the trade the company has consciously made: more growth, more competition, more capital at stake.

For an investor trying to cut through all of this, the number of things worth actually tracking is small. Three KPIs carry most of the signal:

- Organic net sales growth. This is the single cleanest test of whether IDEX is genuinely growing its core businesses or merely buying revenue. Management's own guidance walked up to 3–4% for 2026; sustained, broad-based organic growth above that would validate the pivot, while a relapse to flat-to-negative would reignite every bear concern.13

- The ROIC-versus-cost-of-capital spread. This is where the Mott and Muon bets are ultimately settled. If returns on invested capital grind back up toward the mid-teens as acquired businesses get the 80/20 treatment, the premium acquisitions will have been vindicated. If ROIC stays stuck around 9%, the growth wall will have won.

- Adjusted HST segment EBITDA margin. The specific proof point to watch is whether HST margins expand back toward the high-20s and beyond as the 80/20 playbook is applied to Mott, Muon, and Micro-LAM. Management has explicitly promised this; the margin line will show, quarter by quarter, whether they deliver.13

Everything else — the tariff noise, the quarterly order wiggles, the macro headlines — is secondary to those three questions. Which brings us to what the whole story teaches.

IX. Epilogue & Playbook Lessons

Step back from the numbers and IDEX resolves into a small number of durable lessons — the kind that outlast any single quarter or acquisition.

The first is that operational simplification can beat structural integration. The conventional rollup destroys value by merging its acquisitions into a homogenized whole and severing the relationships that made them worth buying. IDEX proved, over three decades, that you can achieve world-class margins without touching a target's identity at all — that the leverage comes not from consolidating back offices but from importing a rigorous, data-driven way of thinking about which customers and products actually deserve the company's attention. Autonomy on the outside, discipline on the inside. It is a genuinely counterintuitive model, and IDEX is one of the few companies that has run it for long enough to prove it is not luck. It is also worth noting how few imitators have managed to copy it, despite the playbook being no secret. The reason is that the hard part is not the concept but the culture — a decades-long habit of managerial honesty about which parts of a business are quietly unprofitable, and the discipline to act on that honesty even when it means shrinking. That is difficult to install and easy to let slip, which is exactly why it functions as a moat around the operating model itself.

The second lesson is that mission-criticality is the ultimate source of pricing power. The through-line from Viking's gear pumps in 1911 to Mott's porous-metal filters in 2024 is a single obsessive focus: own the cheap component whose failure is catastrophically expensive. When the cost of the part is trivial next to the cost of it not working, the customer stops caring about price and starts caring only about trust — and trust, once earned through validation cycles and years of flawless performance, is the deepest and most defensible moat an industrial company can have. It cannot be bought with a lower bid.

The third lesson is the one the market is watching in real time, and it is the least comfortable: every successful serial acquirer eventually hits a scale wall. The very success that makes a compounder famous forces it to buy larger, pricier, more-contested businesses to keep growing — and that arithmetic can quietly dilute the capital efficiency that made it great. IDEX's transition from mechanical components to high-technology applied materials is not just a growth strategy; it is a live experiment in whether a compounder can jump to a new curve without breaking the machine that got it there. The pivot has bought real exposure to genuinely exciting markets — space, semiconductors, hydrogen, AI-driven data-center demand — and the early 2026 order trends suggest the strategy is finding traction.13 But the price of admission was a compressed return on capital and a billion-dollar bet that is still, by management's own admission, working its way toward the returns IDEX expects of itself.

There is a final, more philosophical lesson buried in all of this, one that applies well beyond IDEX. The market prizes "quality compounders" — businesses that reinvest at high returns and grow relentlessly — and it prices them at premium multiples on the assumption that the compounding will continue indefinitely. But compounding is not a law of nature; it is a rate that decays as a business grows, because scale forces a company to deploy ever-larger sums into an ever-thinner set of high-return opportunities. IDEX is a near-perfect case study in that decay happening in real time to a genuinely excellent company. Nothing about the operating system has broken. The margins are intact, the moat is real, the management is disciplined, and the cash flow is pristine. And yet the return on each incremental dollar has quietly fallen by roughly a third, not because IDEX got worse but because it got bigger. That is the tax that success eventually levies on every compounder, and the interesting question is never whether it arrives but how gracefully a management team handles it — whether it keeps paying up for growth to flatter the top line, or accepts a slower, more disciplined path that protects returns.

Whether that bet pays off will not be settled by narrative or by management conviction. It will be settled by three numbers — organic growth, return on invested capital, and HST margins — grinding out their answer over the next several years. IDEX has earned the benefit of the doubt through thirty-odd years of disciplined compounding. It has not yet earned a verdict on the most expensive decision it has ever made. That verdict is still being written, one quarter at a time, inside the quietest empire in American industry.

References

-

IDEX Corporation Form 10-K, Fiscal Year 2024 (segment margins, gross margin) — SEC EDGAR ↩

-

IDEX Corporation FY2024 Annual Report (Form ARS) — SEC EDGAR ↩

-

This Day In Market History: The First Modern Leveraged Buyout (KKR–Houdaille, 1979, $380M) — Yahoo Finance/Benzinga ↩↩

-

Opinion: How to Kill a Company (Houdaille post-mortem) — The Washington Post, 1989-04-23 ↩

-

IDEX Corporation Form 10-K, Fiscal Year 2024 (segment net sales and adjusted EBITDA) — SEC EDGAR ↩↩↩↩↩

-

IDEX Corporation FY2024 Annual Report (Form ARS) — SEC EDGAR ↩↩↩

-

IDEX Corporation to Acquire Muon Group for €700 million — Business Wire, 2022-09-12 ↩↩

-

IDEX Corporation Completes Acquisition of Muon Group — IDEX Corporation, 2022-11-18 ↩↩

-

STC Material Solutions Joins the Muon Group, an IDEX Corporation Organisation — Business Wire, 2023-10-03 ↩

-

IDEX Corporation to Acquire Mott Corporation (~$1B; ~19x forecasted 2024 EBITDA; ~$100M tax benefit) — SEC EDGAR Form 8-K Exhibit 99.1, 2024-07-23 ↩↩↩

-

IDEX Corporation Completes Acquisition of Mott Corporation — Business Wire, 2024-09-05 ↩

-

IDEX Corporation (IEX) Q1 2026 Earnings Call Transcript, 2026-04-29 — Seeking Alpha Earnings Transcripts Library ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

IDEX Corporation SEC Filings (return on invested capital and financial data, FY2020–FY2025) — SEC EDGAR, CIK 0000832101 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube