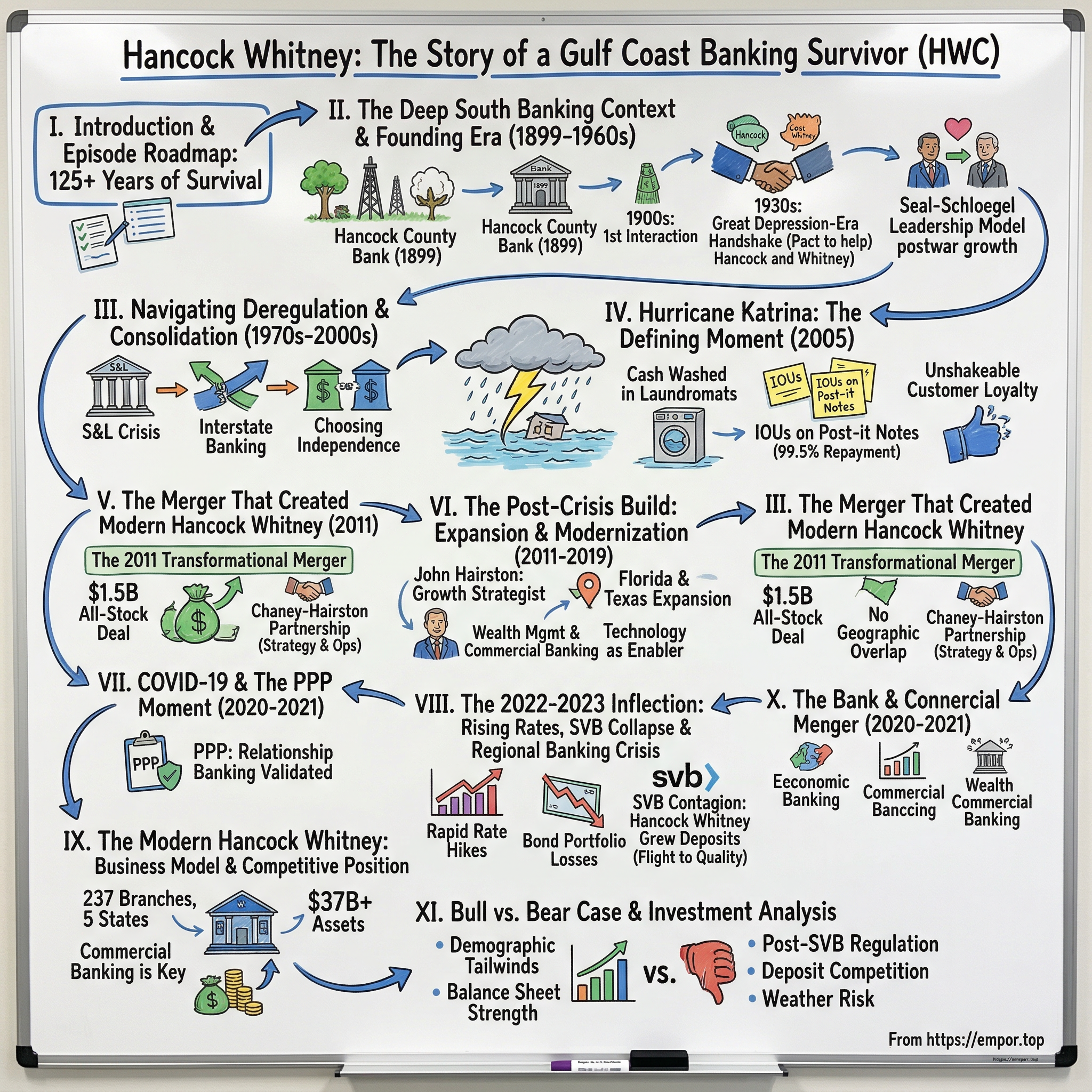

Hancock Whitney: The Story of a Gulf Coast Banking Survivor

I. Introduction & Episode Roadmap

Picture the Mississippi Gulf Coast on a sweltering August morning. The air is thick with salt and humidity, shrimp boats bob in the harbors of Gulfport and Biloxi, and the oak-lined streets of Bay St. Louis still carry the unhurried rhythm of the Deep South. Somewhere along this coastline sits a bank that has, against improbable odds, survived for more than 125 years.

It has outlasted two world wars, the Great Depression, the savings and loan crisis, Hurricane Katrina, the 2008 financial meltdown, a global pandemic, and the regional banking panic of 2023. Its name today is Hancock Whitney, and with more than $37 billion in assets, it stands as the largest independent bank headquartered in the Gulf South region of the United States.

That survival is not incidental. The central question of this deep dive is deceptively simple: How did a bank founded in a small Mississippi coastal town in 1899 avoid the fate of thousands of regional banks that were swallowed by larger competitors, destroyed by crises, or simply faded into irrelevance?

The answer involves a hurricane that nearly destroyed the institution but ultimately made it stronger, a century-old handshake between rival bankers that laid the groundwork for a transformational merger, and a leadership culture that prizes conservative underwriting and community loyalty above all else.

The Hancock Whitney story is really two stories converging into one. On one side, you have Hancock Bank, founded in the Mississippi Gulf Coast, a scrappy community institution built on personal relationships and local knowledge. On the other side sits Whitney National Bank, a New Orleans banking institution with roots dating to 1883, carrying the sophistication and gravitas of one of America's most storied cities. These two banks operated independently for over a century, survived Katrina separately, and then merged in 2011 to create something neither could have become alone.

What makes this story worth telling is not just the longevity. It is the strategic clarity that emerges when you study how Hancock Whitney navigated each crisis. Every existential threat became a strategic inflection point.

Katrina turned devastation into unshakeable customer loyalty. The 2011 merger turned geographic limitation into regional scale. The COVID-19 pandemic turned relationship banking from an anachronism into a competitive weapon. And the SVB-triggered regional bank panic of 2023 turned a well-run balance sheet into a flight-to-quality magnet.

Consider the broader context: since 1990, the number of FDIC-insured commercial banks in the United States has fallen from over twelve thousand to fewer than four thousand. The regional banking model, the idea that a mid-size bank can serve a specific geography better than either a massive national institution or a tiny community lender, has been under relentless pressure. Every year, more banks either fail, sell to larger acquirers, or simply decide the regulatory burden is not worth the fight.

Hancock Whitney did none of those things. Today, trading on NASDAQ under the symbol HWC, the company carries a market capitalization of approximately $5.5 billion on roughly 83.6 million shares outstanding. Its total deposits exceed $29 billion, its total loan book stands at approximately $23 billion, and its total assets approach $37 billion. The stock reached an all-time high near $74 in early February 2026 before settling in the mid-$60s, and the company pays a quarterly dividend of $0.50 per share. These are the numbers. But the story behind them is far more interesting than any balance sheet can convey. This is the story of a bank that mastered the art of turning survival into strategy.

II. The Deep South Banking Context & Founding Era (1899-1960s)

To understand Hancock Whitney, you first need to understand the world that created it. Mississippi at the turn of the twentieth century was a place of paradox. The state was rich in natural resources, cotton, timber, seafood, and oil, but desperately poor in financial capital.

Reconstruction had left the South economically isolated. Northern banks had little interest in lending to Mississippi enterprises, and the few local institutions that existed operated under severe geographic restrictions. Unit banking laws in many Southern states prohibited banks from opening branches beyond their home county. This created a landscape of tiny, hyperlocal banks, each serving a single community, each knowing every borrower by name.

It was in this environment that Peter Hellwege and seventeen other founders established the Hancock County Bank in Bay St. Louis, Mississippi, in the fall of 1899. The choice of location was deliberate. The Mississippi Gulf Coast was experiencing a boom as a port region and resort destination.

Gulfport, just miles down the coast, had recently been developed as a major lumber-shipping port. Hellwege saw an opportunity to provide banking services to a growing coastal economy that was chronically underserved by distant financial centers. The bank's original capitalization was modest, its ambitions local, its underwriting deeply personal. You lent to people you knew, and you knew everyone.

Hellwege was an ambitious connector. In 1904, he founded the Bank of Orleans in New Orleans, running both institutions simultaneously. When he died in December 1907, Eugene H. Roberts succeeded him at the helm of both banks.

But the dual-bank structure did not survive World War I. During the war and the recession that followed, the Bank of Orleans faced financial instability. Rather than risk the Hancock County Bank's capital to prop up its struggling sibling, the boards made a fateful decision: they sold the Bank of Orleans to Whitney Bank.

It was a decision rooted in a principle that would define Hancock for the next century: protecting depositors' money above all else. And it was the first recorded transaction between Hancock and Whitney, two institutions whose fates would intertwine across generations.

Whitney National Bank, meanwhile, occupied an entirely different stratum of Southern banking. Founded in 1883 in New Orleans, it had grown into one of Louisiana's most prestigious financial institutions.

New Orleans in the Gilded Age was the financial capital of the Gulf South, a cosmopolitan city with deep ties to international trade, cotton finance, and the maritime economy. Whitney became the bank of New Orleans business aristocracy, financing the port, the oil industry, and the city's commercial elite. By the early twentieth century, it was already operating more than a hundred locations across Louisiana, Alabama, Mississippi, and Florida, even maintaining offices in the Cayman Islands.

Both banks survived the Great Depression, and the story of how they did so contains a remarkable detail. During the 1930s, when banks were failing across the country at a rate of thousands per year, Leo W. Seal Sr., Hancock's cashier, and his Whitney counterparts, executives named Bouden and O'Keefe, made a private pact: they would always help each other in times of need, ensuring neither bank would fail.

This Depression-era handshake, a commitment between two rival community banks to serve as each other's backstop, is the kind of detail that only makes sense in the context of Deep South banking culture. These were not anonymous financial corporations. They were family-run institutions embedded in their communities, and their leaders understood that their survival was intertwined.

The postwar era brought transformative leadership to Hancock. Leo W. Seal Jr. joined the bank in 1947, when its assets totaled just $12 million. A graduate of Harvard Business School who had cut his teeth at Continental Illinois Bank in Chicago, Seal brought big-city financial sophistication back to the Mississippi coast.

He was named the bank's fifth president in 1963 and would lead Hancock for the next four decades, growing it from a small-town lender into a genuine regional franchise serving communities from south Louisiana to the Florida panhandle. His partnership with George Schloegel, who served as chairman, became the stuff of Gulf Coast banking legend. Over their fifty-year collaboration, Hancock's assets grew from less than $25 million to more than $6 billion.

The Seal-Schloegel partnership deserves attention because it established a leadership model that would persist at Hancock for generations: a duo structure where one leader focused on strategy and relationships while the other managed operations and risk. This complementary approach, later replicated in the Chaney-Hairston partnership that would execute the Whitney merger, became a defining characteristic of how Hancock developed its executive talent.

For investors, the founding era reveals the DNA that still defines Hancock Whitney today: conservative credit culture, deep local knowledge, generational leadership continuity, and an almost religious commitment to protecting depositors' money. These were not strategies invented in a boardroom. They were survival mechanisms forged in an era when a single bad loan could kill a bank, and they created compounding advantages that would prove decisive more than a century later.

III. Navigating Deregulation & Consolidation (1970s-2000s)

The comfortable world of hyperlocal Southern banking began to crack in the 1970s and accelerated into full upheaval in the 1980s. The savings and loan crisis devastated financial institutions across the Gulf Coast, as hundreds of thrifts loaded up on speculative real estate loans and collapsed when interest rates spiked.

Mississippi and Louisiana were not the hardest-hit states, Texas and Florida bore the worst of the S&L carnage, but the ripple effects were felt everywhere. The crisis demonstrated a brutal lesson: banks that strayed from their core competencies and chased yield into unfamiliar territory would pay a devastating price. It was a lesson that Hancock and Whitney absorbed deeply, and one that their less disciplined peers would fail to learn.

Then came interstate banking deregulation. Throughout the 1980s and 1990s, states progressively dismantled the legal barriers that had prevented banks from operating across state lines. For regional banks, this was simultaneously an existential threat and an unprecedented opportunity.

The threat was obvious: national banking giants like Bank of America, NationsBank, and Wells Fargo could now march into Gulf Coast markets, armed with massive balance sheets, national advertising budgets, and the latest technology. The opportunity was subtler: well-run regional banks could finally expand beyond their home states, building scale that had previously been impossible.

The consolidation that followed was savage. Between 1980 and 2000, the number of banks in the United States fell by roughly half. Across the South, storied regional names disappeared into larger entities. Many of Hancock and Whitney's peers made the rational economic choice: sell to a larger acquirer at a premium, cash out, and let someone else deal with the technology investments, regulatory compliance costs, and competitive pressures that were crushing smaller players.

BancorpSouth, TrustMark, AmSouth, and scores of others either merged, sold, or struggled to find their footing in this new landscape. The gravitational pull toward consolidation was powerful. Every year, the economics of independence became a little harder, the compliance costs a little steeper, the technology investments a little more daunting.

Hancock and Whitney each made the contrarian choice to remain independent. For Hancock, this reflected the Seal family's long-term orientation and the board's belief that the Gulf Coast economy had secular growth potential that outside acquirers would not understand or properly invest in.

For Whitney, the calculus was similar: its New Orleans franchise was a crown jewel, deeply embedded in a unique local economy, and any national acquirer would inevitably strip away the relationship-oriented culture that made it special. Both banks chose patience over liquidity, conviction over convenience.

This independence came at a cost. Neither bank could match the technology budgets of the emerging super-regionals. Neither could offer the breadth of products that national banks were bringing to market. But both invested methodically in building branch networks within their core geographies, developing expertise in specialized lending categories, commercial real estate, energy, and maritime finance, and cultivating the kind of banker-client relationships that could not be replicated by a centralized lending algorithm in Charlotte or San Francisco.

By the early 2000s, Hancock had built a respectable franchise across Mississippi, Alabama, and parts of Florida, with roughly $6 billion in assets. Whitney had grown to over $10 billion in assets, with its Louisiana stronghold supplemented by operations in Texas and Alabama. Both banks were profitable, both were conservatively managed, and both had survived when many of their peers had not.

But they were approaching a ceiling. Without further scale, they risked being perpetually stuck in the uncomfortable middle: too large to operate as true community banks, too small to compete effectively with the super-regionals and money-center giants. The question was not whether they needed to grow, but how, and with whom. The answer, when it came, arrived in the most dramatic possible fashion.

IV. Hurricane Katrina: The Defining Moment (2005)

On August 29, 2005, Hurricane Katrina made landfall near Buras, Louisiana, as a Category 3 storm with Category 5 storm surge. The impact on the Mississippi Gulf Coast was apocalyptic. Gulfport, Biloxi, Pass Christian, and Bay St. Louis were devastated. A storm surge reaching nearly thirty feet in some areas swept entire neighborhoods into the sea.

In New Orleans, the levees catastrophically failed, inundating eighty percent of the city in floodwater. More than 1,300 people died across the Gulf Coast. The property damage would ultimately be estimated at $125 billion, making Katrina the costliest natural disaster in American history at the time.

For Hancock Bank, the storm was an existential crisis. The bank's headquarters at One Hancock Plaza in downtown Gulfport took a direct hit. As Katrina's gales intensified, the building's windows began to bow from the pressure. Projectile debris from collapsing nearby structures shattered the glass, and white-capped storm surge flooded the granite first-floor lobby.

Approximately twenty-two members of Hancock's disaster recovery team had chosen to ride out the storm inside the headquarters building. They survived, but when the winds subsided, they emerged to a landscape of total destruction.

The numbers were staggering. Fifty-nine of Hancock's 155 properties across four states suffered damage totaling more than $49 million. Twenty-two locations were more than fifty percent destroyed. One hundred and ninety Hancock employees, more than ten percent of the entire workforce, lost their homes. Over four hundred employees and their immediate families suffered significant property damage.

What happened next became one of the most remarkable stories in American banking history. Within hours of the storm's passage, Hancock employees began setting up makeshift operations in parking lots, under tents, and in any structure that remained standing.

The challenge was immediate and visceral: tens of thousands of people needed cash, and the modern financial infrastructure, ATMs, electronic banking, credit card networks, had been completely destroyed. There was no electricity, no phone service, no internet. Banking had reverted to its most primitive form.

Hancock's response was extraordinary and, by the standards of modern banking risk management, borderline insane. Bank employees recovered cash from flooded ATMs, vaults, and night deposit boxes. The money was contaminated with sewage and debris.

In a detail that became legendary, employees took the cash to a functioning laundromat and literally washed the bills in washing machines to make them usable. They then set up folding tables in parking lots and began distributing cash to anyone who needed it, customers and non-customers alike. No account verification was possible. No identification was required in many cases. Employees tracked these emergency disbursements on scraps of paper and Post-it notes, writing IOUs by hand.

Over the following days and weeks, Hancock Bank distributed approximately $42 million in cash to storm victims across the Gulf Coast. The bank's chairman, George Schloegel, made a conscious decision that protecting the community took precedence over protecting the balance sheet.

It was a bet on human nature, a gamble that the people of the Gulf Coast would remember who showed up for them when everything was destroyed, and that they would pay the money back. Schloegel later explained the philosophy simply: "Basically, people are honest and want to do the right thing and they'll stand by you if you do the right thing by them."

The bet paid off spectacularly. Of the $42 million distributed through hand-scrawled IOUs and Post-it note accounting, only $200,000 was never recovered. That is a repayment rate of over 99.5 percent, a number so extraordinary it sounds fictional. But it was real, and it tells you everything you need to know about the depth of the relationship between Hancock Bank and its community.

In the four months following Hurricane Katrina, Hancock Bank grew by $1.6 billion in deposits, more than the bank had grown in its entire previous ninety-five years of existence. Thousands of new customers, people who had experienced firsthand how Hancock responded in the worst moment of their lives, opened accounts.

The national media picked up the story, and Hancock's Katrina response became a case study in corporate crisis management taught at business schools across the country. George Schloegel's personal reputation was so enhanced that in 2009, the people of Gulfport elected him mayor with nearly ninety percent of the vote.

Meanwhile, John Hairston, then a senior executive, spearheaded the company's operational recovery and the restoration of the downtown Gulfport headquarters. His leadership during the crisis positioned him as the natural successor to lead the next chapter of the bank's evolution.

Whitney National Bank faced a different but equally devastating challenge in New Orleans. The bank's branch network was concentrated in a city that was eighty percent underwater. Branches were flooded, employees were evacuated, and the future of the New Orleans economy itself was uncertain.

Whitney's recovery was quieter than Hancock's dramatic parking-lot operations, but the bank's commitment to remaining in New Orleans and continuing to serve its customers through the long, painful reconstruction earned similar loyalty. While several national banks scaled back their New Orleans presence after Katrina, deeming the city too risky and the recovery too uncertain, Whitney doubled down, becoming a lifeline for the city's recovery. Whitney bankers helped process SBA disaster loans, financed the rebuilding of homes and businesses, and maintained continuity for commercial clients who needed a banking partner that understood the unique complexities of operating in post-Katrina New Orleans. The loyalty earned during those years would prove every bit as durable as the loyalty Hancock earned on the Mississippi coast.

The Katrina experience fundamentally reshaped both banks' strategic thinking. Both recognized the imperative of geographic diversification, the danger of having a franchise concentrated in a single disaster-prone corridor. Both understood that the emotional bonds forged during the crisis were a form of competitive advantage that no amount of advertising or technology could replicate.

And both began to see each other not as competitors but as natural partners, institutions with complementary geographies, shared values, and a mutual understanding of what it meant to survive the worst. The storm that nearly destroyed them would ultimately bring them together.

V. The Merger That Created Modern Hancock Whitney (2011)

Six years after Katrina, the courtship that had been quietly developing between Hancock and Whitney became official. On December 22, 2010, the two companies announced a definitive merger agreement.

The deal was structured as an all-stock transaction in which Whitney shareholders would receive 0.418 shares of Hancock Holding Company stock for each Whitney share, valuing Whitney at approximately $1.5 billion. The implied price of roughly $15.48 per Whitney share represented a forty-two percent premium to Whitney's closing price of $10.87, a substantial premium that reflected Hancock's conviction about the strategic value of the combination.

The timing was not accidental. Whitney had been weakened by the financial crisis and Katrina's lingering effects on the New Orleans economy. Its stock was trading well below pre-crisis levels, and the bank faced the same scale challenges that plagued mid-size regionals everywhere.

For Hancock, the opportunity was unmistakable: acquire the premier banking franchise in New Orleans, Louisiana's financial capital, at a price that the crisis had made possible, and create a combined institution with the geographic breadth to compete effectively against larger rivals.

The strategic logic was elegant in its complementarity. Hancock's strength ran along the Mississippi coast, through Alabama, and into the Florida panhandle. Whitney dominated Louisiana, with a growing presence in Texas. There was almost no geographic overlap, meaning the merger would create genuine expansion rather than redundant coverage.

Combined, the entity would become the thirty-second largest bank holding company in the United States, with approximately $20 billion in assets, nearly 300 branches, and almost 400 ATMs. It would be the largest independent bank headquartered in the Gulf South. That distinction mattered enormously in a region where banking relationships are personal and local identity is a competitive asset.

Shareholders of both companies approved the deal at special meetings on April 29, 2011, and the merger closed on June 4, 2011. Where required by antitrust regulators, overlapping branches were divested. The First Bancshares acquired several Whitney branches on the Mississippi Gulf Coast and in Bogalusa, Louisiana, to resolve the geographic overlap.

The operational integration that followed was where the hard work began. The company initially maintained dual brand identities: Whitney Bank continued to operate in Louisiana and Texas, while Hancock Bank retained its name in Mississippi, Alabama, and Florida.

This two-brand approach was a deliberately cautious choice, acknowledging that both names carried deep emotional resonance in their respective markets and that forcing an immediate rebrand could alienate loyal customers on either side. In New Orleans, the Whitney name was woven into the city's identity. In Gulfport, Hancock was the bank that had washed dirty cash in laundromats to help its neighbors after Katrina. Neither brand could be casually discarded.

The CEO who executed the integration was Carl Chaney. Chaney was not a lifelong Gulf Coast banker. He was a University of Mississippi honor graduate who earned both a BBA in Banking and Finance and a Juris Doctorate from the Ole Miss School of Law. Before joining Hancock, he had spent his career as a bank mergers-and-acquisitions attorney, representing over a hundred financial institutions across thirteen states in the Southeast and Southwest.

That background was exactly what a complex integration demanded. Chaney brought to the CEO role a precision and process orientation born from having dissected scores of bank deals from the legal and regulatory side. Under his leadership from 2006 to 2014, Hancock's assets grew from $6 billion to $21 billion. He executed a $50 million efficiency and process improvement initiative that delivered results three quarters ahead of schedule.

When the integration milestones were achieved and the combined company was operating smoothly, Chaney retired on December 31, 2014, having accomplished what he was brought in to do. It was a clean, purposeful exit, rare in corporate America.

Working alongside Chaney was John Hairston, who served as co-CEO and chief operating officer. Hairston's background was strikingly unconventional for a bank executive. He graduated magna cum laude from Mississippi State University with a degree in chemical engineering and began his career not in banking but in management consulting, working as a financial consulting manager at Andersen Consulting, now Accenture.

It was through that consulting work that Hairston first encountered Hancock: in 1992, he was the project manager who implemented operating and technology practices across the Hancock franchise. He joined the bank full-time and never left, rising through the ranks to become one of the two executives who would lead the combined institution.

The Chaney-Hairston partnership echoed the Seal-Schloegel duo that had run Hancock for decades: one leader focused on strategy and deal execution, the other on operations and technology. The model worked because it paired complementary skill sets while maintaining a unified culture and vision.

The merger worked for a reason that defies the conventional wisdom about bank acquisitions: the two cultures, though different in style, were fundamentally aligned in values. Hancock brought an entrepreneurial, roll-up-your-sleeves culture forged in small-town Mississippi and tempered by Katrina. Whitney brought New Orleans sophistication, institutional depth, and deep expertise in energy and commercial lending.

But both shared a commitment to conservative underwriting, community service, and long-term relationship building. The Depression-era handshake between the Seal and Whitney families was not just a charming anecdote; it was an expression of genuine cultural compatibility that had been building for nearly a century.

Most bank mergers destroy value. Academic research consistently shows that the majority of bank acquisitions result in customer attrition, employee turnover, system integration failures, and culture clashes that erode the very franchise value the acquirer paid for. That this merger defied that pattern is perhaps the single most important fact about the modern company. It demonstrated something rare: a management team that could execute operationally complex transactions without destroying the intangible assets that make a bank franchise valuable.

VI. The Post-Crisis Build: Expansion & Modernization (2011-2019)

The years immediately following the merger were consumed by the unglamorous but essential work of integration. Systems had to be consolidated, branch overlap addressed, and the operating cultures of two distinct institutions harmonized.

From 2011 through roughly 2014, the combined company focused inward: converting core banking platforms, rationalizing branch networks where the two footprints overlapped, and building unified risk management and compliance frameworks. It was the kind of work that never makes headlines but determines whether a merger ultimately succeeds or fails.

When Carl Chaney retired at the end of 2014, John Hairston assumed sole leadership as president and CEO. The transition was seamless, a reflection of the co-CEO structure that had allowed Hairston to be deeply involved in every strategic decision since the merger.

But Hairston brought a subtly different emphasis. Where Chaney had been the integration architect, Hairston was the growth strategist. His background in technology consulting gave him an instinct for operational leverage and digital investment that would prove increasingly important as fintech competition intensified. The ABA Banking Journal would later profile him as an "All-American Banker," recognizing his ability to blend technology-forward thinking with deep community banking values.

Under Hairston's leadership, the geographic expansion strategy crystallized around what executives described as a "Gulf Coast to Gulf Coast" footprint. Florida became a major growth vector, with the bank pushing into attractive markets along the state's Gulf Coast and into the Tampa Bay area.

Texas, inherited from Whitney, became the other major growth frontier. The Lone Star State's booming economy, favorable business climate, and massive population growth made it impossible to ignore, even though Hancock Whitney would be competing against banking behemoths like JPMorgan Chase and Wells Fargo in markets like Houston and Dallas.

The business model evolved significantly during this period. Hancock Whitney moved beyond traditional community banking into a more diversified financial services platform. Wealth management became an area of deliberate investment, as the bank built out trust services, investment advisory, and private banking capabilities to serve the affluent clientele in its markets.

Commercial banking grew increasingly sophisticated, with specialized lending teams focused on energy, healthcare, maritime, and real estate. The bank also built its mortgage operation into a meaningful revenue contributor, though it remained a relationship-driven business rather than a volume origination machine.

Technology transformation was a persistent theme throughout the decade. Hancock Whitney invested in mobile banking platforms, digital account opening, commercial cash management tools, and cybersecurity infrastructure. These investments were necessary to remain competitive with both national banks and the wave of fintech startups that were beginning to challenge traditional banking models.

But the bank's approach to technology was distinctive: rather than trying to out-invest the money-center banks, it focused on using technology to enhance the relationship model. The goal was making it easier for customers to do business with their banker, not replacing the banker with an app. This philosophy, technology as enabler rather than substitute, became a defining element of the Hancock Whitney brand.

The energy portfolio became a significant test during this period. The collapse in oil prices from mid-2014 through early 2016, when crude fell from over $100 per barrel to below $30, hit Gulf Coast energy lenders hard. Hancock Whitney had meaningful exposure to the energy sector through Whitney's legacy Louisiana franchise.

Loan loss provisions rose, and the bank had to work through a painful period of credit deterioration in its energy book. But the experience reinforced the conservative underwriting culture: energy loans were structured with appropriate collateral coverage and covenant protections, and the losses, while painful, were manageable. The workout process demonstrated discipline and expertise that would serve the bank well in future credit cycles. And it prompted management to begin deliberately reducing energy concentration, a decision that would look wise in the years ahead.

By 2019, Hancock Whitney had digested the merger, established itself as a credible five-state franchise, and built a diversified business model capable of generating consistent returns through different economic environments. Assets had grown to approximately $30 billion, and the bank had earned the respect of investors and analysts as one of the better-managed regional banks in the Southeast.

But the two-brand approach that had served as a bridge during the integration was creating increasing confusion. In 2018, seven years after the merger, the company finally unified under a single name: Hancock Whitney Bank. CEO Hairston explained the decision with characteristic directness: "This is really about clarity and simplicity, eliminating the awkwardness of dealing with both brands."

The company tested the new combined logo on focus groups, and in a detail that delighted the design team, about half of participants at first glance saw the letter "H" in the logo, while the other half saw a "W." It was, perhaps, the perfect visual metaphor for a merger of equals. The bank entered the new decade with a unified identity, a proven leadership team, and a balance sheet about to be tested by forces no one saw coming.

VII. COVID-19 & The PPP Moment (2020-2021)

When the COVID-19 pandemic shut down the American economy in March 2020, the immediate fear for regional banks was a wave of small business failures that would decimate loan portfolios.

Hancock Whitney's franchise was heavily weighted toward exactly the kinds of businesses most vulnerable to lockdowns: restaurants, hotels, retail shops, and service businesses along the Gulf Coast, a region whose economy depends significantly on tourism and hospitality. The bank's commercial real estate portfolio was suddenly under stress as tenants could not make rent. Its energy book faced renewed pressure as oil prices briefly went negative. It was a moment that tested every element of the conservative credit culture that management had spent decades building.

The Paycheck Protection Program, or PPP, became an unexpected proving ground for relationship banks. The federal government's program to funnel emergency loans to small businesses was theoretically open to any SBA-approved lender, but in practice, the banks that moved fastest and served their customers most effectively were those with existing relationships and the institutional knowledge to navigate the chaotic rollout.

Hancock Whitney threw its entire organization into PPP processing. Bankers who had deep, personal relationships with small business owners across the Gulf Coast were able to move quickly because they already understood their clients' businesses, their payroll structures, and their financial needs. The bank processed thousands of PPP loans in the program's first rounds, keeping businesses alive that might otherwise have closed permanently.

The contrast with the fintech-driven approach was stark. Online lenders and platforms attempted to process PPP loans at scale, but they lacked the know-your-customer infrastructure and the personal relationships needed to navigate the program's complexities. Many small business owners who had moved their primary banking to digital platforms found themselves unable to get PPP loans processed in time. They came back to their community banks.

The PPP experience became a powerful validation of the relationship banking model at precisely the moment when conventional wisdom was declaring that model obsolete. It was, in many ways, a rhyme of the Katrina story: when crisis hit, the institutions that showed up for their communities earned loyalty that no marketing budget could buy.

The pandemic also unleashed a deposit surge across the banking industry. Federal stimulus payments, enhanced unemployment benefits, and the general contraction in consumer spending meant that households and businesses were accumulating cash at an unprecedented rate. Hancock Whitney, like its peers, saw deposits balloon.

This was a blessing and a curse: the bank had more liquidity than it knew what to do with, but the Federal Reserve had driven interest rates to near zero, compressing net interest margins to painful levels.

Think of net interest margin as the fundamental measure of a bank's profitability engine: it is simply the difference between what a bank earns on its loans and investments and what it pays to depositors and other funding sources, expressed as a percentage of earning assets. When rates are near zero, that spread shrinks, and banks have to work harder to make money on every dollar of assets they hold. It is the banking equivalent of a retailer seeing its gross margin compressed, the most basic indicator of business health.

But the bank's conservative balance sheet management during the zero-rate era would prove prescient in hindsight. Rather than reaching for yield by loading up on long-duration bonds or making aggressive credit bets, Hancock Whitney maintained a relatively short-duration securities portfolio and stuck to its underwriting standards in the loan book.

It was leaving money on the table in the short term, but building optionality for what would come next. By the fourth quarter of 2020, net income had recovered to $103.6 million with EPS of $1.17, up thirty-one percent from the third quarter. The bank emerged from the pandemic with strong credit quality, elevated capital ratios, a larger customer base, and a balance sheet positioned to benefit significantly when interest rates eventually rose.

VIII. The 2022-2023 Inflection: Rising Rates, SVB Collapse & Regional Banking Crisis

The turn came faster and harder than almost anyone anticipated. In March 2022, the Federal Reserve began raising the federal funds rate from near zero, and over the next eighteen months, it executed the most aggressive tightening cycle in four decades, pushing rates above five percent.

For banks, rising rates are generally a good thing, because they can reprice loans faster than they reprice deposits, widening that critical net interest margin spread. But the speed and magnitude of the rate increases created massive dislocations across the financial system.

The most immediate pain point was the bond portfolio. Banks hold large portfolios of government and agency securities as part of their liquidity management. When interest rates rise sharply, the market value of existing bonds falls, sometimes dramatically.

This is basic bond math: a bond paying two percent becomes less valuable when new bonds pay five percent. Think of it like a house with a locked-in low-rate mortgage in a world where everyone else is borrowing at high rates. The asset is still worth its face value at maturity, but its market value today has declined. Across the banking industry, unrealized losses on securities portfolios ballooned into the hundreds of billions of dollars.

For most banks, this was a paper loss: if they held the bonds to maturity, they would receive full face value. But the unrealized losses still reduced tangible book value on the balance sheet and created a vulnerability that savvy depositors and investors could see.

Hancock Whitney had positioned its securities portfolio with a shorter duration than many peers, meaning its bonds were less sensitive to rate changes. The bank also benefited from an asset-sensitive balance sheet structure, with a meaningful portion of its loan book tied to variable rates that repriced upward as the Fed hiked.

Net interest margin expanded from below three percent during the zero-rate trough to above 3.30 percent by mid-2024, and continued climbing toward 3.50 percent through 2025. This NIM expansion was a major earnings tailwind and validated the conservative positioning strategy that management had maintained through the easy-money years.

Then came March 2023, and everything changed. On March 10, Silicon Valley Bank, a $209 billion institution that served the technology and venture capital ecosystem, collapsed in a matter of hours after a bank run triggered by unrealized bond losses and concentrated, uninsured deposit flight.

Signature Bank followed days later. Within weeks, First Republic Bank, a wealth-management-focused institution with over $200 billion in assets, was seized by regulators and sold to JPMorgan Chase. The three largest bank failures in American history outside of the 2008 crisis happened in the span of two months.

The contagion was not limited to the banks that failed. Across the regional banking sector, stock prices cratered as investors feared that deposit runs could spread to any mid-size institution. Hancock Whitney's stock was not spared; shares of virtually every regional bank sold off sharply as the market struggled to distinguish between genuinely troubled institutions and well-run banks caught in the panic.

But the fundamentals beneath Hancock Whitney's stock price told a reassuring story. The bank's deposit base was diversified across five states and hundreds of thousands of individual and commercial accounts. Noninterest-bearing demand deposits represented approximately thirty-six percent of total deposits, a level of "free" funding that most banks would envy and that indicated deeply embedded customer relationships rather than rate-sensitive hot money.

The bank's capital ratios were well above regulatory minimums. And critically, Hancock Whitney's exposure to the kinds of concentrated, high-risk deposit bases that had killed SVB and Signature was essentially zero. There were no crypto deposits. There was no single-industry dependency. The deposit base reflected the diversified real economy of the Gulf Coast: shrimpers and surgeons, oil companies and restaurants, retirees and real estate developers.

Management's communication during the crisis was crucial. CEO Hairston and the leadership team conducted investor calls, communicated proactively with large depositors, and reinforced the message that the balance sheet was a fortress. As the panic subsided, a flight-to-quality dynamic emerged: depositors who were nervous about smaller or less well-capitalized institutions moved their money to banks perceived as safe and well-managed.

The aftermath of the SVB crisis left the regional banking sector permanently changed. Regulatory scrutiny intensified. Proposals for stricter capital requirements and enhanced liquidity standards for mid-size banks moved forward, increasing compliance costs for institutions in Hancock Whitney's size range.

But the crisis also thinned the competitive field and validated the conservative management philosophy that had been practiced for more than a century. Being "boring" in banking is not a weakness; it is a survival strategy.

The banks that failed in 2023 all shared a common characteristic: they had reached for growth, yield, or concentration in ways that made them fragile when conditions changed. Hancock Whitney, by contrast, had spent decades building a franchise that was resilient precisely because it was diversified in deposits, conservative in underwriting, adequate in capital, and deeply rooted in local relationships. The Katrina playbook, showing up when others retreated, was proving transferable to financial crises as well as natural disasters.

IX. The Modern Hancock Whitney: Business Model & Competitive Position

Hancock Whitney today operates 237 branches across five states: Mississippi, Louisiana, Alabama, Florida, and Texas. The footprint is deliberately concentrated in the Gulf South, stretching from the Florida panhandle through the Gulf Coast of Mississippi, Alabama, and Louisiana, and extending into the major Texas metropolitan areas.

This is not a bank that aspires to be everywhere. Its competitive advantage is rooted in being deeply embedded in specific markets where its local knowledge, relationship network, and century-plus history provide genuine differentiation.

The business model has four major components. Community banking serves consumers and small businesses with traditional deposit and lending products. Commercial banking provides more sophisticated services to middle-market companies, including term loans, lines of credit, treasury management, and specialized industry lending. Wealth management encompasses trust services, investment advisory, and private banking for affluent individuals and families. And the mortgage business originates residential loans, both for portfolio and for sale into the secondary market.

Of these, commercial banking is the largest earnings contributor, followed by community banking and wealth management. This mix matters because commercial banking relationships are stickier and more profitable than consumer accounts, providing the kind of recurring, relationship-driven revenue that insulates the bank from the commoditized end of the industry.

The customer segments reveal the franchise's character. Small and mid-size businesses form the backbone of the commercial lending book. Energy sector expertise, inherited from Whitney's Louisiana operations, remains a valuable specialization, though management has deliberately reduced energy concentration to less than two percent of total loans, a prudent hedge against oil price volatility.

Maritime and shipping clients, reflecting the Gulf Coast's port infrastructure, represent a niche that national banks struggle to serve. Affluent individuals, particularly retirees and business owners drawn to the Gulf Coast's climate and cost of living, anchor the wealth management and private banking businesses.

The Gulf Coast advantage is real and underappreciated. The Sun Belt migration trend, accelerated by the pandemic, has brought population and business growth to Hancock Whitney's markets. Florida's Gulf Coast has been among the fastest-growing regions in the country. Texas remains a magnet for corporate relocations and new business formation. Even Mississippi, long viewed as economically stagnant, has seen meaningful development in advanced manufacturing, military installations, and technology.

The Texas strategy deserves particular attention. In late 2025, Hancock Whitney opened three new financial centers in the Dallas area, including a Preston Center location, with two additional locations planned for the first half of 2026 in communities like Little Elm and Frisco. This represents a meaningful commitment to the state's largest metro area, complementing the bank's existing Houston presence.

The approach in Texas is not to compete head-to-head with Chase and Bank of America on consumer banking, but to target the commercial middle market: businesses large enough to need sophisticated banking services but small enough to value a dedicated relationship banker who knows their industry and their community. It is the same playbook that has worked in Mississippi and Louisiana for over a century, transplanted to higher-growth markets.

The wealth management business received a significant boost in May 2025 when Hancock Whitney completed the acquisition of Sabal Trust Company, a Florida-based wealth advisory firm headquartered in St. Petersburg with approximately $3 billion in assets under management and $22 million in annual revenue. The deal brought total trust assets under administration to nearly $40 billion and expanded capabilities in a fee-income business that is less sensitive to interest rate cycles than traditional banking.

Capital allocation has been shareholder-friendly and disciplined. The company completed a $251 million share buyback program by the fourth quarter of 2025, reducing the share count to approximately 83.6 million shares. The dividend has been raised twice in consecutive years: to $0.45 per share in January 2025, and to $0.50 in January 2026. The annualized dividend of $2.00 per share, combined with a payout ratio of approximately thirty-one percent, suggests meaningful room for further increases.

In a bold balance sheet move, the company executed a $1.5 billion bond portfolio restructuring in January 2026, selling lower-yielding securities at an average yield of 2.49 percent and reinvesting in higher-yielding instruments at approximately 4.35 percent. The repositioning involved a pre-tax charge of $99 million but was expected to add approximately $0.23 to annual earnings per share and roughly $24 million in additional net interest income.

The company also announced plans to hire up to fifty revenue-generating bankers during 2026, signaling that the organic growth engine is accelerating. These decisions, the bond swap, the banker hires, the Texas expansion, collectively paint a picture of a management team that is confident enough in the franchise to invest aggressively for growth while maintaining the conservative balance sheet that has defined the institution for 125 years.

X. Strategic Frameworks: Porter's Five Forces & Hamilton's Seven Powers Analysis

Understanding Hancock Whitney's competitive position requires examining the structural forces shaping the banking industry and the specific powers the company possesses to navigate them.

Starting with Michael Porter's five forces framework: the threat of new entrants into traditional banking remains relatively low, principally because of the regulatory barriers. Obtaining a bank charter, building the required capital base, and satisfying examiners is a multi-year, multi-million-dollar proposition.

But fintech companies and neobanks have found ways to nibble at the edges, offering checking accounts, payments, and lending products without the full burden of a bank charter. The key question is whether these digital challengers can replicate the full-service commercial banking relationship that anchors Hancock Whitney's franchise.

So far, the answer is largely no: a fintech can originate a simple consumer loan, but it cannot sit across the table from a business owner, structure a complex commercial credit facility, help navigate SBA lending, and provide treasury management services while sponsoring the local chamber of commerce dinner. Branch economics, far from being obsolete, remain defensible for relationship-oriented models.

The bargaining power of suppliers, meaning depositors in a banking context, has increased significantly in the rising rate environment. When rates were near zero, depositors had few alternatives. Now, money market funds, Treasury bills, and high-yield savings accounts at online banks offer attractive returns, and depositors have become more sophisticated about shopping for yield.

Hancock Whitney has navigated this by maintaining a deposit mix heavily weighted toward noninterest-bearing demand deposits, which represent sticky operating accounts for businesses rather than rate-sensitive savings. But the bank has had to compete on rates for time deposits and savings accounts, and the cost of deposits has risen across the industry.

The key metric to monitor is the deposit beta, which measures how much of each rate increase gets passed through to depositors. Think of it as a scorecard for the bank's pricing power over its own funding costs: a low deposit beta means the bank keeps more of the rate increase for itself, while a high beta means the benefit flows to depositors.

Buyer power in commercial banking is moderate. Large corporate clients have many banking options and can negotiate aggressively on pricing. But for the mid-market commercial clients that form Hancock Whitney's sweet spot, switching costs are meaningful. Moving a complex banking relationship involves changing treasury management systems, renegotiating credit facilities, transferring collateral documents, and, perhaps most importantly, losing the institutional knowledge that an experienced banker has accumulated about the client's business over years of interaction. Consumer banking has lower switching costs, though customer inertia remains surprisingly powerful. Studies consistently show that consumers are more likely to change spouses than change banks, a statistic that is both amusing and economically significant for franchise valuation.

The threat of substitutes is genuine but manageable. Fintechs, credit unions, non-bank lenders, and embedded finance platforms all offer pieces of what a full-service bank provides. But none of them can do everything simultaneously while maintaining the regulatory trust infrastructure, FDIC insurance, and community presence that define a bank.

Competitive rivalry is the most intense of the five forces. Hancock Whitney competes simultaneously against national banks like JPMorgan Chase and Bank of America, super-regionals like Regions Financial (roughly $157 billion in assets) and Truist, mid-size peers like Cadence Bank ($47 billion in assets) and the newly enlarged Renasant Corporation ($25 billion post-merger), and hundreds of community banks and credit unions.

Hancock Whitney's positioning is as a "Goldilocks" bank: large enough to offer sophisticated commercial banking and wealth management services, small enough to provide genuine relationship attention, and sufficiently well-capitalized to survive crises that eliminate less disciplined competitors.

Turning to Hamilton Helmer's seven powers framework, Hancock Whitney's most potent advantages are switching costs, counter-positioning, and process power.

Commercial clients with complex treasury management, lending, and advisory relationships face significant friction in switching banks. The counter-positioning advantage is subtle but real: Hancock Whitney's relationship model is fundamentally different from the efficiency-driven approach of fintechs and national banks. Attempting to match this model would require a fintech to build physical branches, hire experienced relationship bankers, and develop deep local market knowledge, all of which would undermine the low-cost, scalable business model that makes fintechs profitable.

Process power manifests in the conservative underwriting culture and crisis management capability that have been refined over 125 years and cannot be easily taught or replicated. This is the accumulated institutional knowledge of how to lend in hurricane-prone geographies, how to manage an energy portfolio through price collapses, and how to integrate a transformational acquisition without destroying franchise value.

Scale economies exist at the regional level but are not dominant. Branding power is strong within the five-state footprint, particularly given the Katrina narrative, but essentially non-existent outside it. Network effects are limited, as banking is not naturally a winner-take-all network business. And cornered resources, while meaningful in the form of deep Gulf Coast relationships and generational customer ties, are geographically bounded.

The investment case rests on continued execution of a proven playbook in growing markets, not on structural inevitability.

XI. Bull vs. Bear Case & Investment Analysis

The bull case for Hancock Whitney rests on three pillars: demographic tailwinds, balance sheet strength, and the optionality created by a conservative posture in a distressed sector.

The Sun Belt migration trend is not speculation; it is a documented reality that has been reshaping American geography for decades and accelerated after the pandemic. Population growth along the Gulf Coast, particularly in Florida and Texas, directly translates into demand for banking services: more homebuyers needing mortgages, more small businesses needing commercial credit, more affluent retirees needing wealth management. Hancock Whitney is positioned squarely in the path of these flows, and the recent Texas expansion demonstrates management's intent to capitalize on them.

The balance sheet is genuinely strong. As of year-end 2024, the CET1 capital ratio stood at 14.14 percent, well above the regulatory minimum and in the top tier among regional peers. Total risk-based capital was nearly sixteen percent. Tangible book value per share grew twelve percent year-over-year.

Credit quality remained solid, with net charge-offs in the range of eighteen to thirty-one basis points, manageable levels that reflect the conservative underwriting culture. The allowance for credit losses stood at approximately 1.45 to 1.49 percent of total loans, providing a meaningful cushion against potential deterioration. Management expects net charge-offs to settle in the upper teens to low twenties basis points range, consistent with well-managed peers.

Earnings momentum has been positive. Full-year 2024 EPS came in at approximately $5.28 on revenue of $2.06 billion, a nearly eight percent year-over-year increase. The 2025 quarterly earnings cadence, from $1.38 in the first quarter to $1.49 by the fourth quarter, showed consistent improvement.

The net interest margin expanded from around 3.32 percent to nearly 3.50 percent over this period, and the efficiency ratio improved to approximately 54.8 percent for 2025, indicating that the bank was generating more revenue per dollar of operating expense. Return on assets exceeded 1.40 percent, a strong showing for a bank of this size and profile.

The M&A optionality is worth noting. The regional banking sector continues to consolidate. Renasant Corporation's acquisition of The First Bancshares, which closed in April 2025, was just one example of the ongoing reshuffling. Hancock Whitney, with its strong currency (the stock reached an all-time high near $74 in early 2026) and ample capital, is well-positioned to be an acquirer if attractive opportunities emerge. Alternatively, the bank itself could become a target for a larger institution seeking a premier Gulf South franchise.

The bear case is equally worth understanding. The structural challenges facing regional banks are real. Post-SVB regulatory proposals could impose stricter capital and liquidity requirements on mid-size banks, increasing compliance costs without providing the offsetting revenue advantages that come with truly national scale. Hancock Whitney occupies the uncomfortable middle: too large to fly under the regulatory radar, too small to spread compliance costs across a massive balance sheet.

Deposit competition will not relent. Money market fund assets remain near record highs, Treasury yields offer risk-free returns above four percent, and online banks continue to offer savings rates that brick-and-mortar institutions struggle to match. Even with its strong noninterest-bearing deposit base, Hancock Whitney faces ongoing pressure to raise rates on interest-bearing deposits, which compresses margins.

Geographic concentration introduces weather risk that is genuinely difficult to quantify. Climate science suggests that Gulf Coast hurricanes are becoming more frequent and more intense. Insurance costs across the region have skyrocketed, affecting both the bank's customers and its own operating expenses. A major hurricane striking the core markets could cause massive operational disruption and credit losses. The bank's disaster preparedness capabilities are exceptional, but the underlying risk is structural and growing.

The technology gap relative to national banks is persistent. JPMorgan Chase spends more than $15 billion annually on technology, a figure that exceeds Hancock Whitney's total revenue. While the bank does not need to match this spending to remain competitive in its niche, the risk of falling behind on digital capabilities is real, particularly as younger customer cohorts increasingly expect banking experiences that rival the best consumer technology products.

Succession risk deserves mention. John Hairston has led the bank since 2014 and has been central to its strategic direction for two decades. The conservative, relationship-driven culture that defines Hancock Whitney is deeply personal, embedded in the behavior of specific leaders who model it daily. Whether that culture can survive leadership transitions without dilution is an open question that every long-tenured management team eventually faces.

The key KPIs that matter most for tracking Hancock Whitney's ongoing performance are net interest margin and the efficiency ratio. NIM is the single most important indicator of the bank's core profitability engine: it measures the spread between what the bank earns on its assets and what it pays for funding, and it reflects the interplay of rate positioning, deposit franchise strength, and loan pricing discipline.

The efficiency ratio measures operating expenses as a percentage of revenue: a declining ratio means the bank is generating more revenue without proportionally increasing costs, indicating operating leverage and management discipline. Together, these two metrics tell an investor whether the fundamental business is getting stronger or weaker, regardless of the noise created by credit cycles, one-time items, or stock market sentiment.

XII. Epilogue & The Future

In January 2026, Hancock Whitney's management team made two moves that crystallized the strategic direction for the years ahead. The $1.5 billion bond portfolio restructuring was designed to meaningfully boost net interest income by replacing low-yielding pandemic-era bonds with higher-yielding instruments. And the announcement of plans to hire up to fifty revenue-producing bankers, primarily in Texas and Florida growth markets, signaled that the bank's organic growth ambitions are accelerating.

The stock responded, reaching an all-time high near $74 in February 2026 before pulling back modestly to the mid-$60s, reflecting both confidence in the strategy and broader market volatility affecting regional bank valuations.

The full-year 2025 results confirmed the trajectory. Revenue came in at approximately $2 billion, with net income of roughly $486 million. The quarterly EPS progression from $1.38 to $1.49 demonstrated improving profitability throughout the year. Share repurchases reduced the outstanding count to approximately 83.6 million shares, amplifying per-share earnings growth.

The dividend increase to $0.50 per quarter, yielding approximately three percent at recent prices, established Hancock Whitney as a meaningful income generator for patient shareholders. Management guided for 2026 with expectations of five to six percent net interest income growth, mid-single-digit loan expansion, and an efficiency ratio target of 54 to 55 percent.

The question that hangs over every regional bank, and especially one as well-positioned as Hancock Whitney, is whether it will remain independent. The consolidation logic is compelling from both directions.

As a potential acquirer, Hancock Whitney has the currency, capital, and integration capability to absorb smaller Gulf South banks and bolt-on wealth management firms, as the Sabal Trust deal demonstrated. As a potential target, it represents exactly the kind of franchise that larger institutions covet: a well-run, relationship-rich, geographically desirable platform with strong earnings and clean credit quality.

Whether the bank remains independent, becomes a serial acquirer, or eventually joins a larger institution will depend on the strategic judgment of a leadership team that has thus far proven disciplined and patient.

The technological future presents both threat and opportunity. The emergence of artificial intelligence and embedded finance is beginning to reshape how banking services are delivered. AI-powered lending models can underwrite consumer loans in seconds. Embedded finance allows non-bank companies to offer banking products seamlessly within their own platforms.

For a bank that has staked its competitive identity on the human relationship, these technologies represent a genuine challenge. But they also offer the possibility of augmenting human bankers with AI-powered tools that enhance their productivity, improve their risk assessment, and free them to spend more time on the relationship activities that differentiate the franchise. The winners in the next era of banking will likely be institutions that successfully blend technology and human expertise, rather than choosing one over the other.

Climate risk remains the most significant unquantifiable threat on the horizon. The Gulf Coast has always been hurricane country, and Hancock Whitney has demonstrated, repeatedly, that it can survive and even thrive in the aftermath of catastrophic storms. But the insurance market is sending clear price signals that the risk profile is changing. Homeowners' insurance costs in Louisiana and Mississippi have doubled or tripled in recent years, straining household budgets and depressing real estate values in some markets. A bank cannot control the weather, but it must account for the possibility that climate change will fundamentally alter the economics of its core geography over the coming decades.

Perhaps the deepest lesson from the Hancock Whitney story is about the compounding power of institutional culture. The conservative credit standards established by Peter Hellwege in 1899 were maintained by Leo Seal Jr. through the postwar era, reinforced by George Schloegel during Katrina, institutionalized by Carl Chaney during the merger integration, and continued by John Hairston through the modern era.

Each generation of leadership inherited a culture and handed it to the next, slightly refined but fundamentally unchanged. In an industry where the pressure to reach for growth, take on risk, and chase short-term returns is constant and relentless, the ability to maintain disciplined underwriting through 125 years of temptation is itself a form of competitive advantage.

The Depression-era handshake between the Seal and Whitney families was more than a charming historical footnote. It was an expression of a principle that runs through every chapter of this story: when you do the right thing for your community, the community does the right thing for you.

The $42 million in Katrina cash distributed on Post-it note IOUs and repaid at a 99.5 percent rate was proof of that principle. The deposit growth that followed was the compounding return. And the 2011 merger was the culmination of a century of mutual respect between two institutions that always knew, on some level, that their destinies were intertwined.

In a financial world increasingly dominated by algorithms, platforms, and scale, Hancock Whitney represents something increasingly rare: a bank that knows its customers, knows its markets, and has proven, crisis after crisis, that it can survive anything the Gulf Coast throws at it.

XIII. Further Reading & Resources

Top 10 Resources:

-

Hancock Whitney Investor Relations - Annual reports, quarterly earnings releases, and investor presentations provide the most detailed view of the company's financial performance and strategic direction (HancockWhitney.com/investor-relations)

-

"The Storm: What Went Wrong and Why During Hurricane Katrina" by Ivor van Heerden and Mike Bryan - Essential context for understanding the catastrophe that defined both banks' modern identities

-

ABA Banking Journal, "All-American Banker" (2016) - Profile of CEO John Hairston that provides insight into his leadership style and strategic vision

-

Federal Reserve Bank of Atlanta - Regional economic analysis and banking sector research covering Hancock Whitney's core markets

-

"Why Regional Banks Matter" - American Banker series on the importance of regional banking institutions to local economies

-

FDIC Historical Banking Studies - Context on Southern banking history, consolidation trends, and the regulatory evolution that shaped the industry

-

"Bank Merger Motivations and Performance" - Academic research on what makes bank M&A succeed or fail, directly relevant to evaluating the 2011 transaction

-

"The End of Banking: Money, Credit, and the Digital Revolution" by Jonathan McMillan - Broader context for the technological disruption facing traditional banking models

-

Gulf Coast Economic Development Reports - State and regional economic data that illuminate the demographic and business trends driving growth in Hancock Whitney's markets

-

Post-SVB Banking Regulatory Analyses - Publications from the Brookings Institution, Federal Reserve, and industry groups examining the regulatory changes affecting regional banks

Key SEC Filings:

- 10-K annual reports, particularly the Management's Discussion and Analysis sections, provide the most comprehensive view of risk factors, credit quality trends, and strategic priorities

- Proxy statements detail executive compensation, governance structure, and board composition

- 8-K filings capture material events including the Sabal Trust acquisition and bond portfolio restructuring

- Quarterly investor presentation decks available on the investor relations website offer management's own framing of operating results and strategic initiatives

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube