Humana: The Vertical Integration of American Aging

I. Introduction: The Medicare Advantage Pure-Play (0:00 – 10:00)

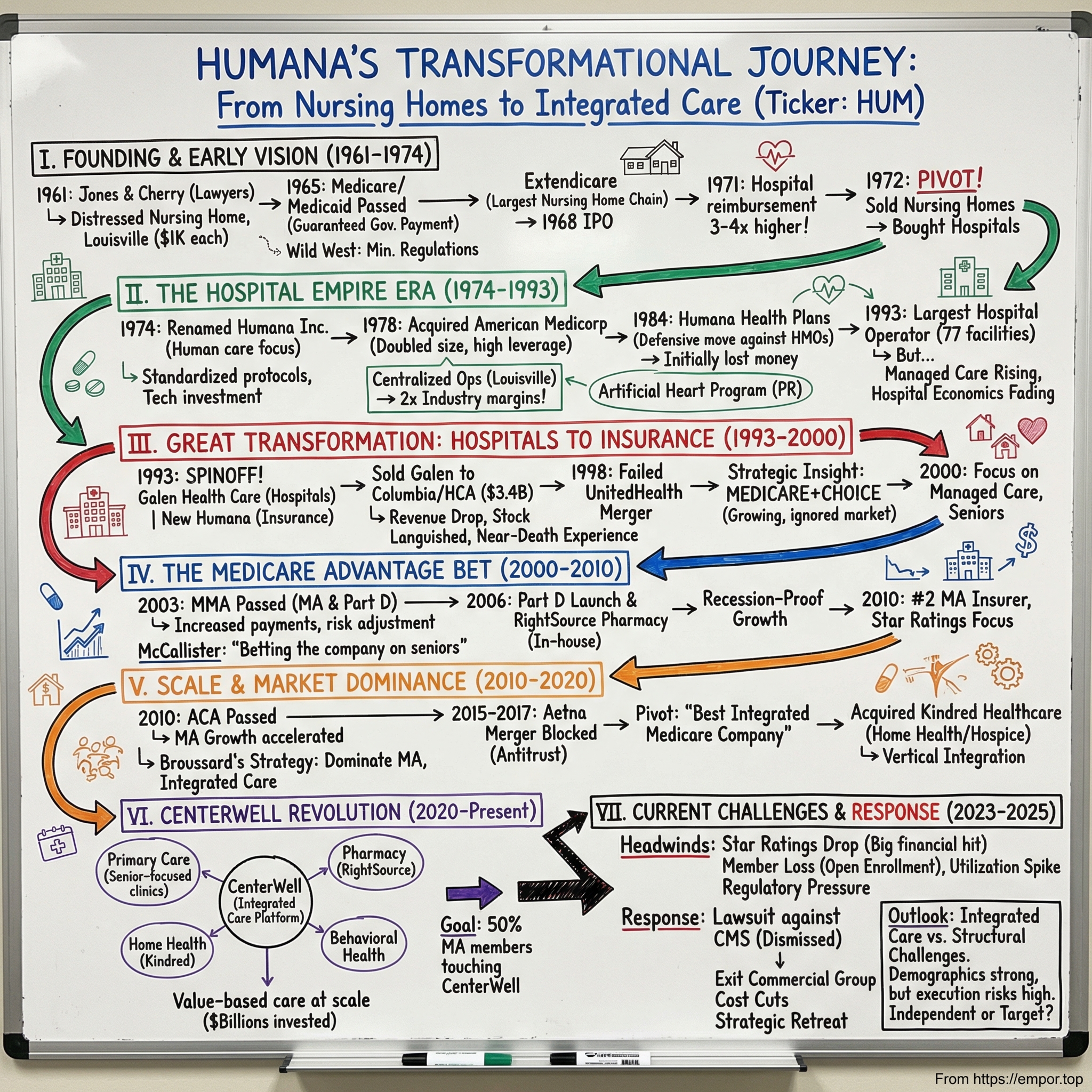

Picture a boardroom in Louisville, Kentucky, February 2023. The executives of Humana Inc. are about to make one of the most counterintuitive moves in American healthcare: they are going to fire their own customers. Not the unprofitable ones. Not the difficult ones. All of them — every employer-sponsored commercial health plan member the company serves. In an industry where scale is gospel, where every insurer from Cigna to Elevance chases the massive employer market like it is oxygen, Humana looked at a business representing millions in premium revenue and said: we do not want this anymore.

That decision — to exit the Employer Group Commercial Medical Products business entirely — was not a retreat. It was the final punctuation mark on a thirty-year strategic sentence. Humana was not shrinking. It was finishing a transformation that began when two Louisville lawyers pooled a thousand dollars each in 1961 to open a nursing home, continued through a stint as the world's largest hospital company, detoured through a failed mega-merger, and arrived at something the healthcare industry had never quite seen before: a company that decided its entire reason for existing was the American senior citizen.

Most health insurers try to be everything to everyone. UnitedHealth Group covers commercial employees, Medicaid recipients, military families, and Medicare beneficiaries across forty-seven million members. CVS Health bought Aetna and then bolted on a pharmacy chain and a benefits manager. Elevance Health spans commercial, government, and specialty lines across forty-eight million lives. They are conglomerates, hedged against the political winds of any single payer source. Humana chose the opposite path. By early 2025, the company derived essentially all of its insurance revenue from government-funded programs: Medicare Advantage, Medicaid, and military TRICARE contracts. It serves roughly six million Medicare Advantage members, making it the second-largest MA insurer in the country behind only UnitedHealthcare.

But here is the thesis that makes Humana more than just a big Medicare insurer. Calling Humana an insurance company is like calling Amazon a bookstore. The insurance arm — the part that collects premiums from the Centers for Medicare and Medicaid Services and pays out claims — is the visible surface. Beneath it sits CenterWell, a rapidly growing healthcare delivery platform that includes the largest senior-focused primary care network in the United States, one of the largest home health operations in the country, and a pharmacy business processing prescriptions for millions. The strategic logic is disarmingly simple: instead of collecting a premium and then paying a hospital across town to treat your member, why not own the doctor, own the home health nurse, own the pharmacy — and keep the money inside your own ecosystem while delivering better outcomes?

This is the story of how a nursing home company became a hospital empire, burned that empire down, rebuilt as an insurer, nearly got swallowed by Aetna, survived, and then spent eight billion dollars buying its way into the living rooms and medicine cabinets of America's seniors. The market currently values Humana at roughly twenty-one billion dollars — down from a peak above sixty billion — because the near-term financials are ugly, tangled in Star Ratings downgrades and regulatory headwinds. But whether you are a bull or a bear, you cannot understand the opportunity or the risk without understanding the full arc. So let us start at the beginning.

II. Origins & The Strategic Pivot (10:00 – 25:00)

Louisville, Kentucky, 1961. Two young lawyers — David A. Jones Sr. and Wendell Cherry — each put up one thousand dollars, recruited four friends to chip in as well, and incorporated a company called Heritage House of America. Their business plan was modest: build and operate nursing homes. The timing was not accidental. Medicare and Medicaid were being debated in Congress and would become law in 1965, creating for the first time a federal payment stream for elderly and low-income healthcare. Jones and Cherry saw the coming wave of government money and positioned themselves to catch it.

Their first facility opened in 1962 on Liverpool Lane in Louisville — seventy-eight beds, nothing fancy. But Jones and Cherry were not content to run a single building. They were operators with an appetite for growth. The company reincorporated as Extendicare Inc. and by 1968 had expanded to more than forty nursing home facilities, making it the largest nursing home chain in the nation. The playbook was straightforward: standardize operations, replicate the model, and ride the demographic and regulatory tailwind of government-funded elder care.

Then came the first great pivot. In late 1968, Extendicare acquired its first hospital. By 1970, the company had added nine more. The logic was economic: hospitals had higher revenue per bed, better margins, and more prestige than nursing homes. By 1972, Jones and Cherry had made the extraordinary decision to divest every single nursing home and go all-in on hospitals. They renamed the company Humana Inc. in January 1974 — a name chosen to signal "humane" care and shed the warehousing stigma that clung to the nursing home industry.

What followed was one of the most aggressive hospital rollups in American history. In 1978, Humana acquired American Medicorp, the second-largest hospital chain in the country, instantly doubling in size. By the early 1980s, Humana operated ninety-one hospitals with approximately eighteen thousand beds across twenty-two states, plus facilities in England, Switzerland, and Mexico. It was the world's largest hospital company. Jones and Cherry had developed an innovative "double corridor" hospital design that reduced construction costs, and they ran their facilities with the operational discipline of a hotel chain. The company even funded a high-profile artificial heart program at the Humana Heart Institute in 1985, recruiting the renowned surgeon Dr. William DeVries to perform implants using the Jarvik-7 device — partly for the medical advancement, partly for the publicity.

But the hospital business was about to hit a wall. Government cost-containment efforts, particularly the introduction of the Medicare Prospective Payment System — which paid hospitals fixed amounts per diagnosis rather than reimbursing whatever they charged — began squeezing margins industry-wide. Full-paying patient admissions were declining. The economics that had made hospital ownership so attractive in the 1970s were deteriorating.

So Humana pivoted again. In 1984, the company launched Humana Health Care Plans, entering the managed care insurance business. The early years were brutal — premiums were underpriced by at least twenty percent, only forty-six percent of members used Humana's own hospitals, and the health plan division did not post its first operating profit until 1989, after five straight years of losses. But Jones saw where the puck was heading. The future was not in owning hospital beds; it was in controlling the flow of patients and dollars through insurance contracts.

The decisive break came in March 1993, when Humana spun off seventy-six hospitals into a new entity called Galen Health Care. Humana kept the insurance business and emerged with six hundred eighty-five million dollars in cash and almost no long-term debt — Galen took the leverage. Within six months, Galen merged with Columbia Hospital Corp., and by 1994 those hospitals were absorbed into what became HCA, the hospital giant that still dominates today. Humana had effectively built the world's largest hospital company, then given it away to focus on something it believed was more valuable: the insurance wrapper around those hospitals.

The post-spinoff years were a frenzy of insurance acquisitions. Group Health Association in 1994 for one hundred eighty million. EMPHESYS Financial Group in 1995 for six hundred fifty million, adding 1.3 million members. Physician Corporation of America and ChoiceCare in 1997. By the end of the decade, Humana had nearly four million plan participants and was generating close to five billion in revenue. A proposed merger with United HealthCare in 1998 — which would have created a behemoth with over ten million members — collapsed when United's stock cratered. Humana was on its own.

Then came the moment that created the modern company. The Medicare Prescription Drug, Improvement, and Modernization Act of 2003 did two things that changed Humana's trajectory forever. First, it rebranded and turbocharged the old Medicare+Choice program into Medicare Advantage, creating richer financial incentives for private insurers to offer managed care plans to seniors. Second, it created Medicare Part D, the prescription drug benefit, which launched on January 1, 2006. Humana was among the first insurers approved to offer the new Medicare Advantage Regional PPO plans. The company had found its calling: the government was going to outsource the risk and management of America's aging population to private enterprise, and Humana was going to be standing at the front of the line.

The co-founders did not live to see the full flowering of what they had planted. Wendell Cherry died of cancer in July 1991 at age fifty-five, before the hospital spinoff was even complete. David Jones retired as chairman in 2005 after forty-four years at the helm, and passed away in September 2019 at eighty-eight. But their DNA — the willingness to build an asset, recognize when its best days are behind it, and ruthlessly pivot to the next thing — became the defining characteristic of the company they built. Nursing homes to hospitals to insurance to Medicare Advantage: each pivot was a bet that the higher-margin, more defensible business lay one step further up the value chain.

The question that would consume the next decade was whether that chain had one more link.

III. The Near-Death Experience: The Aetna Merger Failure (25:00 – 40:00)

July 2015. The American health insurance industry was in a frenzy of consolidation. In a single extraordinary month, two mega-mergers were announced that would have reduced the "Big Five" insurers to three. Anthem proposed to buy Cigna. And Aetna, led by its charismatic CEO Mark Bertolini, announced it would acquire Humana for approximately thirty-seven billion dollars.

For Humana shareholders, the Aetna offer looked like a triumph. The stock had been trading in the one-hundred-seventy-dollar range before merger speculation began, and Aetna was offering a substantial premium. Bruce Broussard, Humana's CEO since 2013, had built a fast-growing Medicare Advantage franchise — membership was approaching three million individual MA members — and Aetna wanted that franchise badly. Bertolini's vision was to create a diversified healthcare giant that could compete with UnitedHealth Group across every line of business: commercial, Medicare, Medicaid, specialty.

But the Department of Justice saw it differently. In July 2016, the DOJ filed suit to block the merger, arguing it would substantially reduce Medicare Advantage competition in more than three hundred fifty counties across twenty-one states, affecting over 1.5 million MA customers. The trial revealed something remarkable: federal judge John Bates found that Aetna had attempted to leverage its participation in the Affordable Care Act exchanges to pressure the DOJ into approving the deal. Aetna had threatened to withdraw from the exchanges if the merger was blocked — and then did exactly that. The judge was not impressed.

On January 23, 2017, Judge Bates ruled the merger would violate antitrust law. Three weeks later, Aetna and Humana officially terminated the agreement. Aetna paid Humana a one-billion-dollar breakup fee — about six hundred thirty million after taxes. Bertolini issued a statement about "the current environment," and that was that.

Here is why this failed merger is arguably the most important event in Humana's modern history — more important than any acquisition the company has ever made.

If the deal had closed, Humana would have disappeared. Its Medicare Advantage members would have been folded into Aetna's sprawling portfolio alongside commercial employer plans, Medicaid contracts, dental, vision, disability, and life insurance. The senior-focused strategy would have been diluted into a generalist playbook. The vertical integration moves that came later — the Kindred acquisition, the CenterWell buildout — almost certainly would not have happened, because Aetna's management had different priorities and a different philosophy.

Instead, the failure forced a reckoning. Broussard and his team had to answer a hard question: if horizontal integration — buying or merging with other insurers to get bigger — was effectively blocked by antitrust regulators, what was the growth strategy? The answer that emerged was vertical integration. If you cannot buy another insurer's members, buy the doctors and nurses who treat your own members. If the government will not let you get wider, get deeper.

The billion-dollar breakup fee was not just consolation money. It was seed capital for a completely different strategic vision. Within months of the merger's collapse, Humana began assembling the pieces of what would become CenterWell. The company had tried the horizontal path and been rebuffed. Now it would go vertical — and the results would be far more transformative than any merger with Aetna could have been.

The irony is rich. Aetna, seeking to strengthen itself by absorbing Humana, instead ended up being absorbed itself — by CVS Health in 2018, becoming a division of a pharmacy chain. Humana, the would-be acquisition target, emerged independent and began building something genuinely new. Sometimes the best thing that can happen to a company is the deal that falls apart.

IV. The Kindred Bet & Capital Deployment (40:00 – 1:00:00)

In December 2017, less than a year after walking away from the Aetna wreckage, Humana announced it was joining a consortium with TPG Capital and Welsh, Carson, Anderson & Stowe to acquire Kindred Healthcare for approximately four billion dollars, including debt. The deal closed in July 2018. On the surface, this looked nothing like the blockbuster Aetna merger. Kindred was a troubled operator of long-term acute care hospitals, rehabilitation facilities, and — crucially — the nation's largest home health and hospice business. It was the kind of company that made Wall Street analysts wrinkle their noses: low-margin, operationally messy, heavily regulated.

But Humana was not buying Kindred for its hospitals. The consortium split Kindred into two pieces. TPG and Welsh Carson took the institutional facilities — the LTAC hospitals and rehab centers. Humana took a forty percent stake in Kindred at Home, the home health and hospice division, for approximately eight hundred million dollars. The private equity partners held the remaining sixty percent.

Why home health? Because the most expensive thing that happens to a Medicare patient is a hospital admission. If you can keep a seventy-eight-year-old with congestive heart failure stable in her own home — with a nurse visiting three times a week, a physical therapist coming on Tuesdays, and a pharmacist managing her medications remotely — you avoid a fifteen-thousand-dollar hospital stay. The math is elegant: spend two thousand dollars on home-based care to prevent fifteen thousand in hospital costs. The patient is happier, the outcomes are better, and the insurer's medical costs drop. But to make it work at scale, you need to own the home health infrastructure. You cannot rely on a patchwork of independent agencies with inconsistent quality and no data integration with your insurance platform.

Humana paid roughly ten to twelve times EBITDA for its stake in the home health business — a price that seemed rich at the time. Skeptics pointed out that home health was a notoriously difficult business to scale, plagued by clinician shortages, regulatory complexity, and thin margins. But Humana was not buying a standalone business; it was buying a strategic asset that would fundamentally change the economics of its insurance book. And by 2021, when home health multiples had skyrocketed as every major player in healthcare suddenly discovered the value of in-home care, Humana's early move looked prescient.

In April 2018, the consortium made a second move: acquiring Curo Health Services, one of the largest hospice operators in the country, with two hundred forty-five locations across twenty-two states, for approximately 1.4 billion dollars. Curo was merged with Kindred at Home's hospice operations to create the nation's largest hospice provider. The total enterprise value of the Kindred and Curo acquisitions exceeded five and a half billion dollars — a massive bet on the "last mile" of healthcare, the patient's own home.

Then in April 2021, Humana took the decisive step: it acquired the remaining sixty percent of Kindred at Home from its private equity partners, valuing the total enterprise at 8.1 billion dollars. This was no longer a toe-in-the-water investment. Humana now owned the whole thing. The following year, the company made a sophisticated portfolio move — divesting a sixty percent majority stake in the hospice and personal care divisions to Clayton, Dubilier & Rice for approximately 2.8 billion dollars, reflecting an enterprise valuation of 3.4 billion for those segments. The divested entity was renamed Gentiva. Humana retained forty percent of the hospice business and kept full ownership of the home health division, which became CenterWell Home Health.

The logic of what stayed and what went reveals the strategic thinking. Home health — sending nurses and therapists into a patient's home to manage chronic conditions and prevent hospitalizations — is directly synergistic with the Medicare Advantage insurance business. Humana controls the insurance plan, identifies high-risk members through its data systems, and then deploys its own home health clinicians to intervene before a crisis. The data loop is closed: the insurer knows exactly what the patient needs, and the provider delivers it. Hospice, by contrast, is an important service but less directly tied to the "keep them healthy and out of the hospital" value proposition. Selling a majority stake monetized the asset while retaining upside.

The final act of capital discipline came in February 2023, when Humana announced it would exit the Employer Group Commercial Medical Products business entirely — all fully insured, self-funded, and Federal Employee Health Benefit medical plans. The commercial business accounted for less than six percent of total membership but consumed management attention, required different infrastructure, and operated at lower margins than the government-focused segments. The exit was phased over eighteen to twenty-four months. When it was complete, Humana had achieved something remarkable in the insurance industry: pure-play focus. Every dollar of insurance premium now came from either Medicare, Medicaid, or military contracts. Every clinical investment was oriented toward seniors.

Think about the capital allocation arc from 2017 to 2023: receive a billion-dollar breakup fee, spend eight billion-plus buying home health and hospice assets, divest the hospice majority for 2.8 billion, and exit the commercial insurance business entirely. The company was sculpting itself, chipping away everything that did not serve the core thesis: own the full care continuum for America's aging population. Whether that sculpture turns out to be a masterpiece or a monument to overreach depends on execution — which brings us to the people now running the show.

V. Current Management: The Rechtin Era (1:00:00 – 1:15:00)

Bruce Broussard was the architect. He arrived at Humana in 2011 as President, was promoted to CEO in 2013 succeeding Michael McCallister, and over the next eleven years transformed the company from a traditional health insurer into an integrated care platform. The numbers under Broussard were staggering: revenue more than doubled from thirty-nine billion to over ninety-two billion, net income doubled to 2.8 billion, and the stock price climbed from roughly sixty-three dollars to above five hundred. He navigated the Aetna merger's collapse, led the Kindred and Curo acquisitions, launched the CenterWell brand, and made the decision to exit commercial insurance. His background — finance and accounting from Texas A&M, CPA, stints as CFO at Sun Healthcare Group and at US Oncology before coming to Humana — made him the right person to engineer the financial and strategic architecture.

But architecture is not the same as operations. By 2024, Humana's challenge had shifted. The grand strategy was in place: own the insurance, own the primary care, own the home health, own the pharmacy. Now the company needed someone who could make all those pieces actually work together — who could walk into a CenterWell clinic and understand the workflow, who could look at a home health staffing model and know whether it was efficient, who could bridge the cultural gap between insurance executives who think in actuarial tables and clinicians who think in patient encounters.

Enter Jim Rechtin. He assumed the CEO role in July 2024, and his biography reads like a deliberate casting choice for this exact moment. Rechtin grew up in Indianapolis, earned his BA from DePauw University and his MBA from Harvard Business School, and then did something unusual for a future healthcare CEO: he spent over two years in the Peace Corps. He began his career at Horizon House, an Indianapolis nonprofit serving people with mental health and developmental challenges. Then came fourteen years at Bain & Company, rising to partner, where he developed the consulting toolkit for analyzing complex operations. But the defining stretch came in healthcare delivery: he joined DaVita Medical Group in 2014, overseeing four thousand clinicians and eleven thousand employees across the California market. He had a brief stint as President of OptumCare — UnitedHealth's provider subsidiary, giving him an inside view of the competitor's playbook — before becoming CEO of Envision Healthcare, one of the country's largest physician staffing companies.

The pattern is clear. Rechtin is a provider guy, not an insurance guy. He has run physician groups, managed clinical operations, and navigated the messy human complexity of actually delivering healthcare. The board chose him because the next chapter of Humana's story is not about buying more assets — it is about making the assets Humana already owns perform at the level that justifies the billions spent acquiring them.

His compensation structure tells the story of what the board expects. Rechtin's total 2024 compensation was approximately 15.6 million dollars, with a base salary of 1.25 million. But the critical detail is in the performance metrics: his incentive compensation is weighted heavily toward Total Shareholder Return and, notably, toward Value-Based Care penetration — meaning the percentage of Humana's members who receive care through value-based arrangements where providers are paid for outcomes rather than volume. This is not a metric you tie to an insurance CEO. It is a metric you tie to someone whose job is to make the clinical delivery engine work.

Broussard, for his part, moved on to new challenges. In February 2026, he was appointed interim CEO of HP Inc. after Enrique Lores stepped down — a testament to his reputation as a transformation executive. His departure from Humana was clean, and Rechtin inherited both the strategic vision and the operational headaches that come with it. Chief among those headaches: a Star Ratings crisis that was about to wallop the company's financials like a Louisville Slugger.

VI. Hidden Business: CenterWell (1:15:00 – 1:35:00)

Walk into a CenterWell Senior Primary Care clinic in Houston or Tampa or Kansas City, and you will notice something different from a typical doctor's office. The waiting room is quieter, designed for an older population. The exam rooms are configured for longer visits — thirty to forty-five minutes, not the seven-minute sprint that defines most primary care in America. The physicians are salaried, not paid per procedure, which means they have no financial incentive to order unnecessary tests or referrals. And critically, the clinic's electronic health records are integrated with Humana's insurance data, so the doctor can see not just the patient's medical history but their pharmacy claims, their home health visits, their emergency room utilization — the full picture of how this particular seventy-two-year-old is interacting with the healthcare system.

This is CenterWell, and it is the business that most investors overlook when they think about Humana. The CenterWell segment generated more than eighteen billion dollars in revenue in 2023 — a number that tends to surprise people who think of Humana as "just" an insurance company. It operates across three major verticals, each with its own competitive dynamics and growth trajectory.

The first is primary care. CenterWell Senior Primary Care and its sister brand Conviva now serve approximately 390,000 seniors across more than 340 centers. That makes it the largest provider of senior-focused primary care in the United States. The company planned to add twenty to thirty new centers in 2025, including an innovative partnership to open twenty-three clinics inside Walmart locations across Florida, Georgia, Missouri, and Texas — leveraging Walmart's foot traffic and real estate in exactly the communities where Medicare-eligible seniors live. A second joint venture with Welsh Carson was announced to develop additional value-based primary care clinics. The expansion is methodical: identify markets where Humana has high MA membership density, open a clinic, staff it with physicians who understand geriatric medicine, and begin migrating members from external providers into the CenterWell ecosystem.

The second vertical is home health. Following the full acquisition of Kindred at Home and the subsequent divestiture of the hospice business, CenterWell Home Health operates more than 350 locations serving patients in thirty-eight states. This is the operational heart of Humana's "keep them at home" strategy. When a CenterWell primary care physician identifies a patient at risk for a hospital admission — perhaps their blood pressure has been creeping up, or they missed a medication refill, or they just had a fall — the physician can order home health services from within the same system. A CenterWell nurse shows up at the patient's house, sometimes within twenty-four hours. No referral to an outside agency, no fax machines, no information gaps. The data flows seamlessly because the insurer, the doctor, and the home health nurse are all part of the same organization.

The third vertical is pharmacy. CenterWell Pharmacy and CenterWell Specialty Pharmacy process prescriptions for Humana's millions of members, particularly through the Medicare Part D benefit. This is a high-volume, high-margin business with powerful retention characteristics — once a senior's medications are being managed through a particular pharmacy, switching is both inconvenient and potentially risky. The pharmacy operation also provides a data advantage: Humana can see in real time whether members are filling their prescriptions, and can intervene when adherence drops — a leading indicator of future health deterioration and expensive hospital visits.

The flywheel connecting these three pieces is what makes CenterWell strategically powerful. A Humana MA member visits a CenterWell primary care clinic. The doctor manages their chronic conditions and prescribes medications filled by CenterWell Pharmacy. When the patient needs home-based care, CenterWell Home Health provides it. At every step, the money that would have flowed out to a third-party hospital system, an independent physician practice, or a retail pharmacy instead stays within the Humana ecosystem. The company captures the margin at every node of the care continuum, and because it controls each node, it can optimize for the thing that actually reduces total cost: keeping the patient healthy.

But perhaps the most interesting strategic development is CenterWell's "Open Access" evolution. Increasingly, CenterWell clinics and home health services are available to non-Humana members — seniors on UnitedHealthcare or Aetna MA plans, even those on traditional fee-for-service Medicare. This transforms CenterWell from an internal cost center serving only Humana members into a merchant-scale services business that generates revenue from the broader market. If CenterWell can demonstrate superior outcomes and lower costs, it becomes attractive to any payer — and the economics shift from "captive subsidiary" to "independent platform." Some analysts have begun to speculate that CenterWell, if it were a standalone public company, might eventually command a higher valuation than Humana's insurance arm. That remains speculative, but the trajectory is real, and the open-access strategy is the mechanism that could get it there.

For investors tracking this business, CenterWell is where the long-term optionality lives. The insurance arm is mature, regulated, and increasingly subject to the vagaries of CMS rate-setting and Star Ratings. CenterWell is where the margin expansion story resides — and where the distinction between "Humana the insurer" and "Humana the healthcare delivery platform" will ultimately be tested.

VII. The 7 Powers & Porter's 5 Forces (1:35:00 – 1:55:00)

To understand whether Humana's position is durable or fragile, it helps to run the company through two classic strategic frameworks. Hamilton Helmer's Seven Powers identifies the sources of persistent competitive advantage. Michael Porter's Five Forces maps the structural pressures on profitability. Together, they paint a nuanced picture of a company with genuine moats in some areas and alarming vulnerabilities in others.

Start with Helmer's framework. The most powerful force working in Humana's favor is switching costs. Think about what it means for a seventy-five-year-old to change their Medicare Advantage plan. It is not like switching car insurance. Their primary care doctor at a CenterWell clinic may not be in the new plan's network. Their home health nurse, who knows exactly how to manage their twice-daily insulin, works for CenterWell. Their prescriptions are auto-filled by CenterWell Pharmacy. Their health records, care coordination notes, and clinical history are all in Humana's system. Switching means disrupting every one of those relationships simultaneously — for a population that, by definition, has complex health needs and values continuity above almost everything else. This is not an abstract theoretical advantage. It shows up in retention rates that are among the highest in the industry. Once a senior is in the Humana-CenterWell ecosystem, leaving is extraordinarily high-friction.

The second power is scale economies, specifically data scale. Humana has been operating Medicare Advantage plans since the program's earliest incarnation. It possesses roughly two decades of longitudinal health data on senior populations — millions of patient-years of claims history, clinical encounters, pharmacy utilization, and outcomes data. This dataset allows Humana to price risk with a precision that is extremely difficult for new entrants to replicate. When Humana bids on a Medicare Advantage contract in a given county, it knows the historical cost patterns of that population at a granular level. A new entrant is essentially guessing. Over time, this data advantage compounds: better pricing leads to better margins, which fund better benefits, which attract more members, which generate more data.

The third power is what Helmer calls "cornered resource" — a valuable asset that competitors cannot easily acquire. In Humana's case, this is the home health clinician workforce. There is a severe and worsening shortage of home health nurses, physical therapists, and occupational therapists in the United States. The aging population is growing, the number of clinicians trained in geriatric home care is not keeping pace, and the work is physically demanding and emotionally taxing. Humana, through CenterWell Home Health's 350-plus locations, has already recruited, trained, and retained one of the largest home health workforces in the country. Competitors — CVS Health, Amazon, Walmart — can announce home health strategies, but actually assembling the clinical workforce to execute those strategies takes years and enormous investment. You cannot download nurses from the cloud.

Now flip to Porter's Five Forces, which reveal where the vulnerabilities lie.

The bargaining power of buyers is perhaps the single most important force acting on Humana. In most industries, "buyers" are the customers. In Medicare Advantage, the "buyer" is effectively the federal government, acting through CMS. CMS sets the benchmark payment rates that determine how much revenue MA insurers receive per member. CMS designs the Star Ratings system that determines bonus payments. CMS controls the risk adjustment model — the formula that adjusts payments based on how sick a plan's members are. And CMS can change any of these levers at any time, for any reason, with enormous financial consequences for companies like Humana. This is "stroke of the pen" risk in its purest form. A single regulatory decision — like the 2024 transition from the V24 to V28 risk adjustment model, which reduced the revenue insurers could claim from aggressive diagnosis coding — can erase billions of dollars in expected revenue overnight. Humana's stock has swung by double-digit percentages on CMS rate announcements. No amount of operational excellence can fully hedge against a regulator that controls the revenue spigot.

The intensity of rivalry is the other force that demands attention. UnitedHealthcare, with approximately thirty percent of the MA market compared to Humana's roughly nineteen percent, is not just a larger competitor — it is a qualitatively different kind of threat. Through Optum, UnitedHealth Group operates one of the world's largest healthcare services businesses, with more than two hundred fifty billion dollars in annual revenue. Optum's provider network, data analytics capabilities, and pharmacy benefits operation dwarf what CenterWell has built to date. UnitedHealthcare offered MA plans in 2,709 of 3,143 U.S. counties in 2024, with the largest market share in forty-one percent of all counties. When Humana enters a new county or tries to grow in an existing one, it is almost always fighting United for the same members. The competitive dynamics resemble a chess match between a grandmaster and a very talented amateur: Humana can win specific positions through superior local execution, but the overall resource disparity is real.

The combined market share of the top five national MA carriers grew from forty-six percent in 2012 to sixty-six percent in 2023, and UnitedHealthcare and Humana together account for nearly half of all MA enrollment. This concentration means the two companies are locked in a duopoly dynamic in many local markets — which is good for pricing power but also means regulators are watching closely for any sign that competition is being stifled.

For investors, the strategic framework yields a clear conclusion: Humana has genuine competitive advantages in switching costs, data scale, and clinical workforce — but all of those advantages exist within a regulatory construct that a government agency can reshape at will. The company's fate is inextricably linked to the political and budgetary decisions made about Medicare spending. Understanding that duality — real operational moats inside a fundamentally government-controlled market — is essential to valuing the business correctly.

VIII. The Playbook: Lessons for Investors (1:55:00 – 2:10:00)

There is a myth on Wall Street that focus is risky — that a company concentrated in one market or one customer segment is more vulnerable than a diversified conglomerate. Humana's history offers a powerful counterargument. In complex regulated markets, where the rules change constantly and deep expertise is required to navigate them, the focused operator tends to outperform the generalist. UnitedHealth Group is the obvious exception — a conglomerate that dominates — but UnitedHealth's success comes precisely because its individual business units (UnitedHealthcare insurance, Optum Health services, Optum Rx pharmacy, Optum Insight analytics) each operate with the depth and focus of standalone companies. For everyone else in the industry, trying to be excellent at commercial insurance, Medicare, Medicaid, dental, vision, disability, and international operations simultaneously tends to produce mediocrity across the board.

Humana's decision to exit commercial insurance was a recognition of this reality. The employer market requires different infrastructure, different sales channels, different regulatory expertise, and different competitive positioning than Medicare Advantage. Every dollar of management attention spent on the commercial business was a dollar not spent on deepening the Medicare moat. By walking away, Humana did not just save money — it freed up institutional focus, which in a business as complex as senior healthcare, may be the scarcest resource of all.

The deeper lesson is about the transition from middleman to value creator. A traditional health insurer is, at its core, a financial intermediary. It collects premiums, manages a pool of risk, and pays claims to providers. The value it adds is actuarial: pricing risk accurately and managing the administrative machinery of claims processing. This is a legitimate business, but it is a commodity business with limited pricing power and thin differentiation. Humana's vertical integration strategy is an attempt to escape that commodity trap. By owning the clinical delivery infrastructure — the doctors, the nurses, the pharmacies — Humana shifts from being a company that pays for healthcare to a company that produces healthcare. The economics are fundamentally different. An insurer earns a spread between premiums collected and claims paid. A vertically integrated care platform earns that spread plus the margin on every clinical service delivered internally.

There is a concept in competitive strategy called counter-positioning, where a smaller player adopts a business model that the dominant incumbent cannot easily replicate without cannibalizing its existing business. Humana's home health bet has elements of this. UnitedHealth Group, through Optum, certainly has the resources to build a comparable home health infrastructure. But Optum's existing provider business is heavily weighted toward ambulatory surgery centers, physician practices, and large medical groups — high-revenue, facility-based care. Shifting aggressively toward low-cost, home-based care models would cannibalize the revenue generated by those higher-acuity settings. Humana, with its smaller and more focused asset base, could make the home health bet without that internal conflict. Whether this counter-positioning advantage persists as Optum inevitably builds its own home health capabilities remains to be seen, but Humana's multi-year head start in integrating home health with insurance data is a real and compounding advantage.

The narrative shift that investors should track is subtle but profound: from "EBITDA from premiums" to "EBITDA from clinical outcomes." If Humana succeeds in its value-based care transformation, the income statement will increasingly reflect margin earned by delivering care efficiently — not just by underwriting insurance risk correctly. That is a structurally different and potentially more durable earnings stream. But it requires flawless execution in clinical operations, which is far harder than managing an actuarial spreadsheet.

For those tracking Humana's ongoing performance, two KPIs matter more than any others. The first is the Medicare Advantage benefit expense ratio — what the insurance industry calls the medical loss ratio, or MLR. This is the percentage of premium revenue that goes out the door to pay medical claims. A lower ratio means Humana is keeping more of each premium dollar, either because its members are healthier, its care management is more effective, or its provider contracts are more favorable. This ratio has been trending in the wrong direction — from the high-eighties in early 2023 to nearly ninety-two percent by late 2024 — and is the single best real-time indicator of whether the integrated care model is actually bending the cost curve. The second KPI is Star Ratings — specifically, the percentage of members enrolled in plans rated four stars or above. This determines whether Humana receives the five percent quality bonus from CMS, which on a base of six million members translates to billions of dollars. The collapse from ninety-four percent of members in four-star plans in 2024 to roughly twenty-five percent in 2025 was the financial earthquake that cratered the stock. Tracking the recovery trajectory of Star Ratings is essential to understanding when — or whether — the earnings power returns.

IX. The Bear vs. Bull Case (2:10:00 – 2:25:00)

The bear case for Humana is not a whisper. It is a scream, and it is playing out in real time.

Start with Star Ratings, the quality scoring system that determines whether a Medicare Advantage plan receives bonus payments from CMS. In 2024, ninety-four percent of Humana's MA members were enrolled in plans rated four stars or above — meaning the company received the full five percent quality bonus on almost its entire membership base. Then the roof caved in. For the 2025 payment year, that number plummeted to approximately twenty-five percent. One of Humana's largest contracts, covering roughly forty-five percent of its MA members, dropped a full point from 4.5 to 3.5 stars. The financial impact was staggering: a 3.5-billion-dollar net revenue headwind for 2026, which forced the company to issue guidance of "at least nine dollars" in adjusted earnings per share — barely half of the 16.21 dollars it earned in 2024. The stock, which had traded above five hundred forty dollars in late 2022, cratered to the low one-seventies. Humana has sued the Department of Health and Human Services challenging the lower ratings, and management has stated it plans to regain four-star ratings by 2028 — but that is two years away, and the financial damage in the interim is severe.

Layer on the V28 risk adjustment model transition. CMS is phasing in a new formula for calculating how sick a plan's members are, which determines payment adjustments. The old V24 model allowed insurers to generate higher payments through aggressive diagnosis coding — documenting every minor ailment to make the member population appear sicker than it actually was. V28 tightens these rules significantly and reached full implementation in 2026. For Humana, which derived substantial revenue from coding intensity, this represents a permanent reduction in per-member revenue that cannot be recovered through operational improvements.

Then there is the medical loss ratio trend. Humana's benefit expense ratio climbed from the high-eighties to nearly ninety-two percent by the fourth quarter of 2024. In an industry where the ACA mandates a minimum MLR of eighty to eighty-five percent, operating at ninety-two percent leaves almost no room for administrative costs, investment in CenterWell, or shareholder returns. The culprit is a combination of factors: rising utilization as post-COVID deferred care continues to flow through the system, higher acuity among new MA members attracted by rich benefits during the growth years, and the challenge of managing costs for a population that is, by definition, aging and becoming more expensive every year.

And hovering over all of this is the political dimension. Medicare is the third rail of American politics, and Medicare Advantage — the privatized version — has drawn increasing scrutiny from both parties. Progressives argue that MA plans generate excess profits for private insurers at taxpayers' expense. Fiscal conservatives eye Medicare spending as a target for budget reduction. Either direction creates downward pressure on the payment rates that drive Humana's revenue. The company's financial performance is, in a very real sense, an appendage of the federal budget.

The bull case requires stepping back from the near-term carnage and asking a different question: what does the world look like in 2030?

The answer starts with demographics. Approximately ten thousand Americans turn sixty-five every single day. The Baby Boomer generation — seventy-six million people — is in the heart of its aging-in period. By 2030, every Boomer will be at least sixty-five, and an estimated sixty-seven million Americans will be enrolled in Medicare, up from roughly forty million a decade earlier. Medicare spending is projected to exceed 1.2 trillion dollars annually. This is not a cyclical trend that will reverse. It is a structural demographic reality that will persist for decades, and it is the single most powerful tailwind in American healthcare.

Within that growing Medicare population, the shift toward Medicare Advantage continues to accelerate. MA enrollment has grown from roughly a quarter of Medicare beneficiaries in 2010 to over half today. Seniors prefer MA plans because they typically offer lower out-of-pocket costs, dental and vision benefits, and integrated care coordination that traditional Medicare does not provide. The government prefers MA because it outsources administrative complexity and, in theory, incentivizes private-sector efficiency. Barring a dramatic policy reversal, MA penetration will continue to rise, and the total addressable market will expand.

Within that market, Humana's CenterWell platform represents a genuinely differentiated asset. The primary care clinics, the home health infrastructure, the pharmacy operation — these are physical, clinical assets that take years and billions of dollars to build. CVS Health has been trying to make its MinuteClinic and Oak Street Health acquisitions work. Amazon acquired One Medical and is experimenting with home health. Walmart partnered with CenterWell and others to put clinics in its stores. But none of these competitors has what Humana has: the insurance data integrated with the clinical delivery, the closed-loop economics, and the twenty years of experience managing senior populations at scale. If CenterWell continues to expand its open-access strategy — serving non-Humana members and proving its outcomes are superior — it could eventually be valued as a standalone healthcare services platform worth more than the insurance arm.

The Star Ratings headwind, as painful as it is, is also temporary. Humana has a clear path back to four-star ratings by 2028, and the company's quality infrastructure — the clinical workflows, the member engagement programs, the data systems — has not been dismantled. The 2025-2026 period looks like a valley, not a cliff.

The tension between these two cases — between a company drowning in near-term headwinds and one riding the most powerful demographic wave in American history — is what makes Humana one of the more intellectually interesting investments in healthcare. The bears see a regulated utility trapped in a political vice. The bulls see a platform company being valued at a cyclical trough during a temporary quality hiccup, with decades of demographic growth ahead.

X. Epilogue (2:25:00 – End)

In 1961, two lawyers in Louisville, Kentucky pooled two thousand dollars to build a nursing home. They grew it into the largest nursing home chain in America, then decided nursing homes were not the future. They built the largest hospital company in the world, then decided hospitals were not the future. They created one of the country's largest health insurers, nearly sold it to Aetna, watched that deal collapse, and then decided that plain insurance was not the future either. At each inflection point, the company did something that most large corporations find almost impossible: it let go of what it had built and bet on what it believed came next.

That willingness to destroy value in order to create it — to spin off seventy-six hospitals, to walk away from a thirty-seven-billion-dollar acquisition, to fire every commercial insurance customer — is either the mark of exceptional strategic clarity or reckless reinvention addiction. The answer probably depends on the time horizon. In the near term, Humana faces the most challenging operating environment it has encountered in decades: Star Ratings downgrades, V28 implementation, rising medical costs, a stock price that has lost more than sixty percent from its peak, and a new CEO who must execute a complex operational turnaround. In the long term, the company sits at the intersection of the most durable growth trend in American society — the aging of the Baby Boom generation — with a vertically integrated platform that no competitor has fully replicated.

David Jones and Wendell Cherry started with seventy-eight nursing home beds. Their successors now oversee an enterprise with over a hundred billion dollars in revenue, six million Medicare Advantage members, 340 primary care clinics, 350 home health locations, and a pharmacy operation that touches millions of prescriptions annually. The form has changed beyond recognition. The underlying bet has not. From the very first day, this has been a company that wagers on the American senior — on the certainty that the population will age, that the government will pay for their care, and that whoever manages that care most effectively will build an extraordinarily valuable franchise.

Whether the current management team can navigate through the Star Ratings valley, prove the CenterWell economics, and emerge on the other side with restored earnings power will determine whether the Humana story is remembered as a masterclass in corporate reinvention or a cautionary tale about regulatory dependence. The next two years will tell us which.

Top References for Further Reading:

- "The Healing of America" by T.R. Reid — Essential context on the structure of U.S. health systems and how Medicare fits within the global landscape.

- Humana's 2023 Investor Day Presentation — The most detailed public articulation of the CenterWell strategy and value-based care economics.

- DOJ vs. Aetna/Humana (2017) Court Documents — Judge Bates's ruling contains the most thorough publicly available analysis of competitive dynamics in the Medicare Advantage market.

- "7 Powers" by Hamilton Helmer — The strategic framework used in this analysis to evaluate the durability of Humana's competitive position.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube