HubSpot: The Inbound Revolution and the Platform Play

I. Introduction

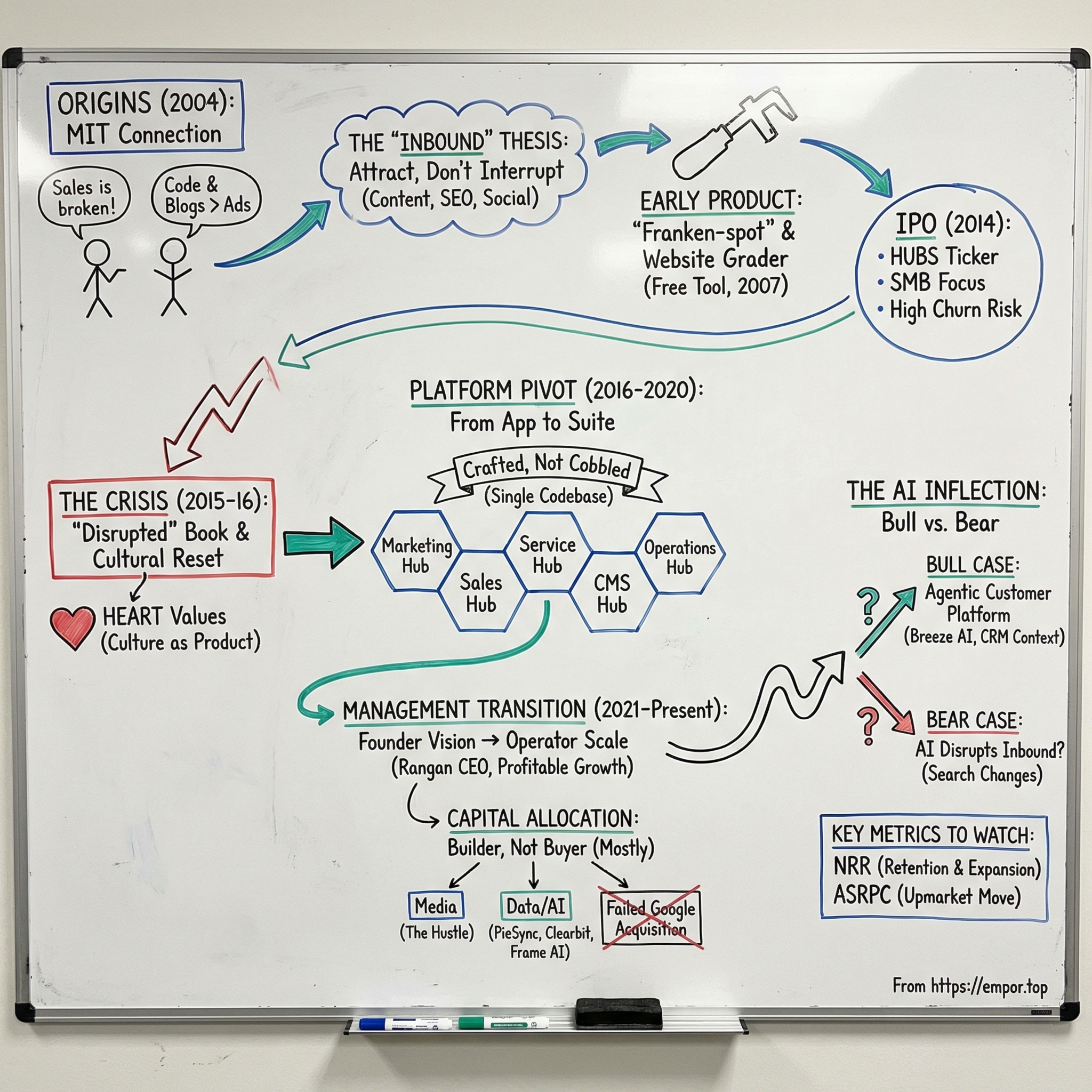

Picture a conference room at MIT Sloan in the fall of 2004. Two graduate students, about as different as two people could be, are arguing about why marketing is broken.

One is a fast-talking Irish-American sales veteran who spent a decade selling enterprise CAD software in Tokyo and then ran a venture fund's portfolio. The other is a quiet Indian-born coder who sold his first company for millions but still writes blog posts at two in the morning for fun.

Between them, they are about to coin a term that will reshape an entire industry, build a company worth tens of billions of dollars, survive a public scandal involving the FBI, fend off an acquisition attempt by Google, and ultimately face the existential question of whether artificial intelligence will destroy the very marketing philosophy they invented.

This is the story of HubSpot.

Today, HubSpot sits at a fascinating inflection point.

The company reported $3.13 billion in revenue for fiscal year 2025, growing 19% year-over-year. It serves nearly 289,000 customers across 135 countries. Its board just authorized a $1 billion share buyback program, the first major capital return in the company's history.

Net new annual recurring revenue grew 24% in 2025, outpacing headline revenue growth by 600 basis points, a signal that the economic engine is actually accelerating even as the top-line growth rate moderates from its post-COVID peaks.

And yet the stock trades roughly 48% below its 52-week highs, caught in a brutal SaaS selloff that has punished even the best-executing software companies.

The central tension is the same one that has defined HubSpot for two decades: can a company built on simplicity and small business love successfully move upmarket into the enterprise without becoming the bloated, complex software behemoth it was designed to replace?

And now there is a second, even more urgent question: in a world where AI agents can write emails, qualify leads, and answer customer questions autonomously, does the traditional CRM even need to exist?

To understand where HubSpot is going, you have to understand where it came from. And that story begins with a blog, a thesis advisor, and a very compelling observation about the death of interruption marketing.

The themes that run through HubSpot's story are category creation, culture as product, the founder-to-professional-CEO transition, and the AI platform shift. Each of these themes is playing out simultaneously in the current chapter.

And each one will determine whether HubSpot's next decade resembles a compounding machine or a cautionary tale about what happens when the paradigm you invented gets disrupted by the next paradigm.

II. Origins: The MIT Connection and the "Inbound" Thesis

Dharmesh Shah was born in 1967 in Ankleshwar, a small industrial town in Gujarat, India, a place with no paved streets, no traffic lights, and no hospitals. He was delivered at his grandmother's house with the help of a midwife. His family moved frequently, from India to the United States to Canada and back again, before finally settling near Purdue University in Indiana. Shah never touched a computer in high school. At Purdue, he took a summer "Introduction to Computers" course on a whim, and the experience was transformative. He pivoted to computer science and never looked back.

By his late twenties, Shah had founded Pyramid Digital Solutions, an enterprise software company serving the financial services sector, bootstrapped with less than ten thousand dollars. Pyramid became a three-time Inc. 500 honoree, grew to over $15 million in annual revenue, and was acquired by SunGard Data Systems in 2005. Shah was already a successful entrepreneur when he enrolled in the MIT Sloan Fellows Program in Innovation and Global Leadership. He did not need an MBA. He wanted intellectual stimulation. What he got instead was a co-founder.

Brian Halligan took a very different path to that same MIT classroom. A University of Vermont electrical engineering graduate, Halligan started his career in 1990 at Parametric Technology Corporation, one of the iconic enterprise software companies of the nineties. He began as an administrative secretary to the VP of channel sales, a job that sounds unglamorous but gave him a ground-floor education in how enterprise software gets sold. Over the next decade, he rose to SVP of Sales, and in his mid-twenties, PTC shipped him off to Japan to build out its entire Asian sales operation during the company's hypergrowth phase. This experience was formative: Halligan learned how to sell complex software across cultural boundaries, how to build sales organizations from scratch, and how to think about market expansion as a system rather than a series of individual deals.

After PTC, Halligan ran sales at Groove Networks, a collaboration startup founded by Ray Ozzie that Microsoft eventually acquired in 2005. Between stints, he served as a venture partner at Longworth Ventures, where he sat on boards and watched portfolio companies spend millions of dollars on television ads, trade show booths, and cold-calling campaigns, all with increasingly diminishing returns.

What Halligan noticed at Longworth was fascinating but troubling. The companies he was advising were spending fortunes on traditional marketing and getting almost nothing back. Meanwhile, his classmate Dharmesh had started a blog called OnStartups as part of his MIT thesis work. Shah's thesis advisor had demanded real data and industry perspective, not just opinions, so Shah started blogging about startup lessons to gather feedback from actual entrepreneurs. The thing was, the blog took off. OnStartups generated more traffic, more engagement, and more leads than any of the venture-backed companies Halligan was working with, companies spending millions on advertising. Shah was spending zero. He was just writing useful content and letting Google deliver the readers.

That observation was the seed. Halligan, the sales guy, saw the implication immediately: people had developed what he called "ad blindness." Think about your own behavior. When was the last time you clicked on a banner ad? When was the last time you answered an unknown number on your phone?

Interruption marketing, cold calls, pop-up ads, direct mail, all the traditional outbound tactics that had powered the advertising and sales industries for decades, was dying. The internet had fundamentally shifted power from the seller to the buyer. People now researched products on their own, read reviews, consulted blogs, asked questions on social media. They did not want to be interrupted; they wanted to be educated.

If you could build tools that helped businesses get found rather than forcing them to buy attention, you would have something genuinely new.

They coined the term "inbound marketing" to describe this philosophy. And then they did something strategically brilliant that deserves its own spotlight: they named the category before they built the product.

This is a classic category-creation playbook. By defining "inbound marketing" as a concept through content, blog posts, speaking engagements at conferences, and eventually a best-selling book, Halligan and Shah created demand for a solution that only they were positioned to provide. They were not selling software; they were selling a worldview. The software was just how you enacted it.

In October 2009, they published "Inbound Marketing: Get Found Using Google, Social Media and Blogs," which became the manifesto for an entire movement. The book was itself the ultimate piece of inbound marketing, a demonstration of the thesis within the thesis. It attracted customers who were already believers by the time they signed up.

HubSpot was officially founded in June 2006 in Cambridge, Massachusetts. The early product was, by all accounts, rough. Internally, some called it "Franken-spot," a clunky collection of tools for SEO analysis, blogging, social media management, and email, stitched together by vision more than engineering elegance. But the vision sold it. Customers were not buying a polished tool; they were buying the promise of a new way to grow their business.

HubSpot's first genius product was not software at all; it was Website Grader, a free online tool launched in 2007 that let anyone type in their website URL and get a report card on their site's performance across SEO, social media presence, mobile readiness, and blogging activity. Website Grader was named one of PC Magazine's Top 100 Undiscovered Websites that year. Within its first twelve months, it analyzed over 400,000 URLs and generated millions of leads.

The tool was, of course, the ultimate piece of inbound marketing: a free, genuinely useful product that demonstrated the value of the paid platform and simultaneously captured contact information from every user who ran it. It was HubSpot eating its own cooking, and it worked spectacularly. A small business owner types in their URL, gets a report showing they are scoring 42 out of 100, sees specific recommendations for improvement, and thinks: "I need help with this." HubSpot is right there with the paid product to help. The flywheel was already spinning, years before they would formalize it as a model.

The revenue numbers tell the story of a company selling a philosophy as much as software. In 2007, HubSpot generated just $255,000 in revenue. By 2010, that number had exploded to $15.6 million, roughly a 60x increase in three years. That kind of growth gets noticed by venture capitalists.

General Catalyst led a $5 million Series A in July 2007. Matrix Partners, one of Boston's most prestigious venture firms, put in $12 million in a Series B a year later. Scale Venture Partners led a $16 million Series C in October 2009. And in March 2011, Sequoia Capital, Google Ventures, and Salesforce itself invested $32 million in a Series D round. In total, HubSpot raised approximately $101 million in venture capital before going public.

The fact that Salesforce invested in HubSpot's Series D is a delicious irony given that the two companies would soon be positioned as direct competitors: one as the disruptive upstart, the other as the enterprise incumbent. For investors who study competitive dynamics, Salesforce's early investment was essentially paying to observe a company that was building a playbook to steal its lower-end customers. It is also worth noting that Google Ventures' participation in the same round adds another layer of irony, given that Google would attempt to acquire the entire company thirteen years later.

III. The Early Years and the IPO (2006-2014)

By 2014, HubSpot had matured from a scrappy startup into a real company with real revenue. From $15.6 million in 2010, revenue grew to approximately $116 million by the time the IPO paperwork was filed. The growth rate was extraordinary, roughly 50% annually, but the business model faced deep skepticism from Wall Street. The core concern was churn.

Here is why churn matters so much in SaaS, explained simply. A SaaS company is essentially a subscription business, like a gym membership or a newspaper subscription. The company's revenue in any given year is the sum of all its active subscribers paying their monthly or annual fees. "Churn" is the percentage of subscribers who cancel in a given period.

If a company has a million dollars in recurring revenue and 20% annual churn, it needs to sell $200,000 in new business just to stay flat. That is the "leaky bucket" problem.

Enterprise software companies like Salesforce tend to have very low churn, often 5-8%, because their products become deeply embedded in business processes and switching is painful. SMB software companies historically had churn rates of 20-30% or even higher, because small businesses go out of business, they run out of budget, they find cheaper alternatives, or they simply forget why they were paying for the software in the first place.

HubSpot sold to small and medium-sized businesses, a customer segment notorious for exactly this kind of turnover. Many investors believed that an SMB-focused SaaS model was structurally unable to compound because the customer base churned too fast to build durable revenue.

The skeptics had a point: HubSpot's S-1 filing would reveal a net revenue retention rate of just 88.6%, meaning that the cohort of customers from a year ago was paying nearly 12% less in aggregate. That is well below the 100%+ threshold that SaaS investors typically worship. At 100%+ net retention, the existing customer base grows on its own even if the company adds zero new customers, which is the hallmark of a truly compounding business model.

HubSpot's response to the churn challenge was strategic and came in two parts.

First, at the INBOUND14 conference in September 2014, the company announced a free CRM product. This was a bold move that drew skepticism internally and externally. Giving away the core product for free seemed counterintuitive. Why would a company that needed to demonstrate revenue durability to public market investors make its most important product free?

But Halligan and Shah understood something profound: the biggest barrier to adoption for small businesses was not features or functionality; it was the decision to start paying at all. A twenty-person marketing agency that has never used a CRM is not going to commit $500 per month to software they have never tried. But they will sign up for a free tool, especially one that lets them organize their contacts and track their deals with zero financial risk. By offering a genuinely useful free CRM, HubSpot removed that barrier entirely.

The free CRM was not just a marketing gimmick; it was the top of a carefully engineered conversion funnel. Users would start with the free CRM, get their contacts and deals organized, build workflows around the platform, and then discover the tool's limitations as their business grew. They would need marketing automation, so they upgrade to Marketing Hub. They need sales sequences, so they add Sales Hub. They need a helpdesk, so they add Service Hub. Each upgrade is a natural extension of a tool they are already using and dependent on.

HubSpot formally adopted what it called the "flywheel" model, replacing the traditional marketing funnel in its vocabulary. The flywheel worked like this: free adoption drives product familiarity, which drives paid upgrades, which improves customer experience, which generates referrals and word-of-mouth, which brings in more free users. Each revolution of the flywheel builds on the last, creating compounding momentum. The critical insight was that the flywheel replaced the linear funnel, where customers fall in at the top and drop out at every stage, with a circular model where every satisfied customer accelerates the next customer's journey.

Second, on October 9, 2014, HubSpot went public on the New York Stock Exchange under the ticker symbol HUBS. The company priced 5 million shares at $25 each, above the already-upwardly-revised range of $22 to $24, raising $125 million. On the first day of trading, shares opened at $32.95 and closed at $30.10, a roughly 20% gain that briefly pushed the market capitalization above $1 billion. At the closing price, the market cap settled at around $900 million.

The IPO was significant beyond the numbers. It was a validation of the SMB SaaS model at a time when conventional wisdom held that only enterprise-focused software companies could generate the low-churn, high-expansion revenue profiles that public market investors demanded.

Consider the context of 2014. The dominant SaaS narrative was that small business software was a graveyard: high churn, low contract values, expensive customer acquisition. Companies like Salesforce, Workday, and ServiceNow were celebrated precisely because they sold to enterprises with sticky, multi-year contracts. HubSpot's pitch to public market investors was essentially: "We know SMB churn is high, but we are going to solve it with product-led growth, freemium conversion, and multi-product expansion." Many investors were skeptical.

The market was betting that the free CRM, the expanding product suite, and the inbound marketing movement would overcome the inherent challenges of the SMB customer base. That bet would prove extraordinarily prescient: over the next eleven years, HubSpot's net revenue retention would climb from 88.6% to 105%, and the company would grow revenue from $116 million to over $3 billion. But before the flywheel could fully spin up, HubSpot had to survive a crisis that nearly defined the company in all the wrong ways.

IV. The "Disrupted" Crisis and Cultural Reset (2015-2016)

In 2013, HubSpot hired Dan Lyons, a fifty-two-year-old journalist who had been laid off from Newsweek, to serve as a marketing fellow. Lyons was a well-known tech writer, perhaps best remembered for his satirical blog "Fake Steve Jobs," in which he impersonated Apple's co-founder with biting wit. What nobody at HubSpot anticipated was that Lyons was effectively embedding himself as an anthropologist in a tech startup, taking notes on everything he saw, and preparing to write a book about it.

To understand why this mattered, you have to picture what HubSpot looked like from the inside in 2013-2014. The company was growing fast, had a young workforce, and operated with the kind of startup culture that Silicon Valley celebrates and outsiders find bewildering. There were nerf gun battles, beer fridges, a candy wall, and an internal social hierarchy that Lyons would later describe in unflattering terms. For a fifty-two-year-old journalist accustomed to the culture of serious newsrooms, the experience was jarring.

In July 2015, before the book was even published, the situation exploded. HubSpot's CMO, Mike Volpe, was fired for cause. VP of Content Joe Chernov resigned. The reason: an internal attempt to obtain an advance copy of Lyons' manuscript through what the FBI would investigate as potentially involving unauthorized access to electronic communications and extortion-like tactics aimed at stopping the book's publication.

The Boston FBI office opened a formal investigation. CEO Brian Halligan, who knew about Volpe's actions but failed to bring the ethical violation to the board's attention in a timely fashion, was sanctioned with a pay cut. The SEC also took notice, as the company had failed to disclose the investigation promptly.

The FBI investigation was ultimately closed with no criminal charges filed, but the reputational damage was done.

In April 2016, Lyons' book hit shelves: "Disrupted: My Misadventure in the Start-Up Bubble." It painted HubSpot as a frat house masquerading as a tech company, with allegations of ageism, cult-like behavior among a group Lyons dubbed "The Capones," an orange-obsessed internal culture team, and a product that he described as little more than glorified spam.

The book became a bestseller and, for a moment, threatened to define HubSpot's narrative in the public imagination.

It raised legitimate questions: was the "inbound" philosophy just a marketing trick? Was the culture genuinely healthy or merely performative? Were the metrics sustainable or a house of cards? For a company whose entire brand was built on transparency and authenticity, the accusations cut directly at the foundation.

What happened next is arguably the most important chapter in HubSpot's history, even though it received almost no media attention. Halligan and Shah did not fight the book publicly. They did not hire crisis PR firms or launch counter-narratives. Instead, they turned inward. Dharmesh Shah published a thoughtful Medium post titled "Undisrupted: HubSpot's Reflections on a Scathing Book," in which he acknowledged lessons learned while defending the company's core mission. He pointed to HubSpot's ranking as fourth on Glassdoor's Best Places to Work list and expressed genuine disappointment that Lyons' experience diverged so sharply from that of most employees.

But the real work happened behind the scenes. Dharmesh Shah, who had already spent hundreds of hours crafting the HubSpot Culture Code, a 128-slide deck that would accumulate over 5.7 million views on SlideShare, doubled down on culture as an engineering problem. The Culture Code was treated not as a static manifesto but as a living product, updated over thirty times based on employee feedback, company evolution, and the painful lessons of the Disrupted era. The company codified its values in the acronym HEART: Humble, Empathetic, Adaptable, Remarkable, and Transparent. Notably, the "E" originally stood for "Effective" and was later changed to "Empathetic," a modification HubSpot itself described as fixing a "critical bug" in its cultural operating system.

The crisis forced HubSpot to mature from a startup that happened to be public into a public institution that operated with the discipline and accountability that status demands.

Think of it as a crucible moment: the fire that burns away the startup bro culture and leaves behind a company capable of scaling to thousands of employees across dozens of countries without losing its identity. Companies that fail to navigate these moments, Uber under Travis Kalanick being perhaps the most prominent cautionary tale, pay an enormous price in talent attrition, regulatory scrutiny, and customer distrust. HubSpot navigated it by treating culture as a product requiring the same rigor, iteration, and intentionality that it applied to its software.

For investors, the key insight is that HubSpot's culture moat, the thing that drives its consistently high Glassdoor ratings and its ability to attract top engineering and sales talent in a fiercely competitive market, was forged in this period of crisis. It was not organic; it was deliberately engineered in response to failure. And that is precisely why it has proven durable.

There is a broader lesson here about how companies handle existential reputational threats. The instinct in Silicon Valley is to go on offense: attack the critic, discredit the narrative, hire the best PR firm money can buy. HubSpot did the opposite. They absorbed the blow, acknowledged what was true, fixed what needed fixing, and let the results speak for themselves. Revenue in 2016, the year Disrupted was published, grew 49% to $271 million. The stock, after an initial dip, recovered and kept climbing. The market ultimately cared more about the flywheel than the book reviews. But that only happened because HubSpot did the hard internal work that most companies, when put in the same position, refuse to do.

V. The Pivot to Platform: From "App" to "Suite" (2016-2020)

If the cultural reset was about the soul of the company, the platform pivot was about its body. Between 2016 and 2020, HubSpot executed one of the more ambitious product transformations in SaaS history, evolving from a single-product marketing automation tool into a multi-hub CRM platform that touches every aspect of how a business interacts with its customers.

The strategic decision at the heart of this transformation was deceptively simple to articulate but operationally grueling to execute: build everything on a single codebase.

To appreciate why this matters, consider the alternative approach, which is exactly what Salesforce did. Salesforce grew primarily through acquisition: buying ExactTarget for $2.5 billion in 2013 and inheriting Pardot in the process, then adding Tableau for $15.7 billion in 2019 and Slack for $27.7 billion in 2021.

Each acquired product came with its own database, its own user interface, its own login system, and its own data model. Integrating these products into a coherent platform requires years of engineering work, and the integration is often incomplete. Pardot, for example, existed as a standalone platform for years after Salesforce acquired it before beginning a painful piece-by-piece transition onto the core Salesforce platform. Tableau still operates as a functionally separate application.

Marc Benioff declared after the Slack acquisition, "We're going to rebuild all of our technology to become Slack-first," an admission that even within one of the world's most valuable software companies, the products existed in varying states of integration.

For a large enterprise with a dedicated IT team, a full-time Salesforce administrator, and a budget for consultants, this complexity is manageable. For a fifty-person marketing agency or a two-hundred-person SaaS startup, it is a nightmare. And that is precisely the gap HubSpot targeted.

HubSpot's internal tagline for the single-codebase approach was "crafted, not cobbled." Every new hub would be built natively on the same underlying CRM platform, sharing the same data model, the same user interface patterns, and the same architecture.

What this meant in practice was that a sales rep using Sales Hub and a marketer using Marketing Hub were looking at the same customer record, the same properties, the same activity timeline. No data replication, no field mapping, no integration maintenance.

If a marketing lead became a sales opportunity, the handoff was seamless because both teams were working in the same system. If a customer who bought the product then filed a support ticket, the service rep could see the entire history: every marketing email they received, every sales call logged, every page on the website they visited. The entire customer journey, from the first anonymous website visit through the sales close to the post-sale support ticket, lived in a single container.

The hub-by-hub expansion unfolded in carefully staged phases. Marketing Hub was the founding product. The free CRM and early sales tools arrived in 2014 and evolved into a full Sales Hub with pipeline management, email sequences, and meeting scheduling.

Service Hub launched in 2018, providing helpdesk ticketing, knowledge base management, and customer feedback tools. CMS Hub, for website content management integrated directly with CRM data so that website content could be personalized based on who was visiting, arrived in 2020. And Operations Hub, focused on data sync, data quality automation, and programmable workflows, launched in April 2021.

Each hub was additive and interconnected: a customer that started with Marketing Hub could add Sales Hub, then Service Hub, each time increasing both the value they extracted from the platform and the pain they would experience if they tried to leave.

To build the ecosystem around the platform, HubSpot invested heavily in its App Marketplace. By early 2022, the marketplace had surpassed 1,000 integrations. By February 2026, that number exceeded 2,000, with 76 new apps added in Q4 2025 alone. The average HubSpot customer now has nine or more apps installed from the marketplace, and over half have five or more. Each installed integration adds another layer of switching cost, because replacing HubSpot means replacing not just the CRM but also reconfiguring every integration that connects to it.

The financial impact of the platform strategy was dramatic and directly addressed the churn concern that had haunted the IPO. Revenue grew from $271 million in 2016 to $883 million in 2020, a tripling in four years. More importantly, the multi-hub adoption drove net revenue retention from the 88.6% reported in the S-1 toward and eventually past the 100% threshold, peaking at approximately 115% in 2021. The company was not just acquiring new customers; it was extracting meaningfully more revenue from existing ones as they adopted additional hubs and upgraded to higher tiers.

To put the net revenue retention improvement in context: moving from 88.6% to 115% fundamentally transforms the economics of a subscription business. At 88.6%, HubSpot needed to grow new bookings by more than 11% of existing revenue just to stay flat. At 115%, the existing customer base generated 15% growth on its own, before a single new customer was acquired. This is the difference between running on a treadmill and riding an escalator. Every new customer acquired at 115% NRR is additive to a base that is already growing autonomously. This was the mathematical engine behind HubSpot's acceleration from sub-$1 billion to over $3 billion in revenue.

For investors who had worried about SMB churn, this was the definitive answer: you solve churn by making the platform so central to the customer's operations that leaving becomes almost unthinkable. The platform strategy did not just add revenue lines; it fundamentally changed the character of the business from a leaky bucket into a compounding machine.

VI. The Management Transition: Founder to Operator (2021-Present)

In February 2021, Brian Halligan was seriously injured in a snowmobile accident, breaking twenty bones and requiring thirty-four surgical screws to put himself back together. He took a leave of absence to recover. What was initially a temporary arrangement became permanent when, on September 7, 2021, HubSpot announced that Yamini Rangan would become CEO and Halligan would transition to Executive Chairman.

Rangan was not a random hire plucked from the talent market in the wake of a crisis. She had been carefully recruited as HubSpot's first-ever Chief Customer Officer in January 2020, more than a year before Halligan's accident. Her appointment to that newly created role was itself a signal that the board was preparing for the eventual transition from founder-led to professionally managed, and Rangan was being groomed for the top job regardless of Halligan's accident.

Her background explains why she was chosen. Born in India, Rangan holds a B.S. in Electronics Engineering from Bharathiar University, an M.S. in Computer Engineering from Clemson University, and an MBA from UC Berkeley's Haas School of Business.

Her career reads like a syllabus for enterprise Go-to-Market leadership: Lucent Technologies, Siebel Systems (one of the original CRM pioneers), SAP, Workday, and Dropbox. At Workday, she served as VP of Sales Strategy and Operations and helped quadruple revenue while scaling the sales organization. At Dropbox, she rose from VP of Business Strategy to Chief Customer Officer, overseeing sales, marketing, customer experience, partnerships, and strategy.

She is, in the purest sense, a GTM operator: someone who understands the mechanics of acquiring, retaining, and expanding customers with the precision of an engineer, someone who thinks in terms of pipeline velocity, conversion rates, and cohort analysis.

The shift from Halligan to Rangan represented a clear change in leadership archetype. Halligan was the product visionary, the Deadhead who co-authored "Marketing Lessons from the Grateful Dead" with a Berklee professor, who believed that the personality of the perfect founder mirrored Jerry Garcia: authentic, humble, obsessed with craft, unconventional. His leadership style centered on hiring great people and getting out of their way.

Rangan is the operational executor, the person who brings discipline, margin expansion, and the kind of operating rigor that public market investors reward. Her compensation is heavily weighted toward stock-based pay tied to total shareholder return, which aligns her incentives directly with Wall Street performance.

The financial results under Rangan have been striking. Non-GAAP operating margin expanded from 9.8% in 2022 to 15.2% in 2023, an improvement of 540 basis points in a single year. It expanded further to 17.5% in 2024. Non-GAAP operating income nearly doubled from $169 million in 2022 to $330 million in 2023.

Free cash flow grew from $191 million in 2022 to $595 million in 2025. And in 2024, HubSpot achieved GAAP profitability for the first time in its history, recording $4.6 million in net income after years of GAAP losses. In 2025, GAAP net income expanded tenfold to $45.9 million.

The story shifted from "growth at all costs" to "profitable growth," and the margin expansion has been among the most impressive in the mid-cap SaaS universe.

Meanwhile, Dharmesh Shah remains as CTO, though his role is unlike that of any other CTO in enterprise software. His LinkedIn title reads "Chief Thought Officer," not Chief Technology Officer, and the distinction is intentional. He has no direct reports.

His focus is on product vision, culture stewardship, AI strategy, and thought leadership. He still owns approximately 1.27 million shares of HubSpot common stock, representing roughly a 3.5% stake worth several hundred million dollars. His ownership ensures deep founder alignment even as professional management runs the day-to-day operation.

Halligan served as Executive Chairperson until May 2025, when Lorrie Norrington was appointed Chair of the Board. Halligan remains a co-founder and board member, while also working with Sequoia Capital, his venture firm Propeller, and continuing to teach at MIT. The transition is now complete: HubSpot is a professionally managed public company with founder oversight through board seats and significant equity ownership.

For investors evaluating management quality, this bifurcated model, a product and culture founder maintaining strategic influence alongside an execution-focused professional CEO, is a repeatable pattern seen at several high-performing technology companies, including Snowflake under Frank Slootman and Palo Alto Networks under Nikesh Arora. The risk is that the operational CEO optimizes for margin and Wall Street metrics at the expense of the product magic that built the franchise. The opportunity is that the combination of visionary oversight and operational discipline creates a more durable compounding machine. So far, the evidence favors the latter interpretation: revenue has grown from $1.3 billion in 2021 to $3.13 billion in 2025, while margins have expanded dramatically and net revenue retention has stabilized in a healthy range.

One important nuance on the incentive structure: Rangan's compensation is heavily weighted toward stock-based pay tied to total shareholder return. This means she is directly incentivized to grow both the top line and the stock price, which creates strong alignment with long-term shareholders but also introduces the risk of short-term optimization for Wall Street metrics. Shah's massive equity stake provides a counterbalance, ensuring that product quality and culture do not get sacrificed for quarterly earnings beats. The tension between these two incentive structures, one driven by operational performance metrics and the other by ownership and product pride, is actually a feature, not a bug. It creates a natural check-and-balance system that pure professional management teams often lack.

VII. Capital Allocation and M&A Strategy

HubSpot has historically been a builder, not a buyer. The "crafted, not cobbled" philosophy extended to its M&A strategy: if a capability could be built in-house on the unified codebase, it was built in-house. Acquisitions were rare and small, typically talent acquisitions like Kemvi, an AI and machine learning startup acquired in 2017 to bring natural language processing capabilities in-house, and Motion.ai, a visual chatbot builder acquired the same year. This restraint was itself a strategic choice, preserving the architectural coherence that differentiated HubSpot from Salesforce's acquisition-assembled platform.

But starting in 2019, HubSpot's acquisition strategy shifted in two important directions: media and data.

The media play came first and was unconventional. In February 2021, HubSpot acquired The Hustle for approximately $27 million, roughly $17.2 million in cash plus equity according to SEC filings. The Hustle was a media company with 1.5 million newsletter subscribers, a popular podcast called "My First Million," and a premium research arm called Trends. The audience skewed heavily toward founders, growth operators, and early-stage investors, precisely the demographic that HubSpot wanted to convert into customers of its "HubSpot for Startups" program.

Brian Halligan articulated the vision bluntly: "The goal is to build the largest business content network in the world."

The strategic logic was elegant: owning the media channel, rather than renting attention from Google and Facebook through paid ads, provided zero-marginal-cost lead generation. Every newsletter send was a free impression to 1.5 million warm prospects who had opted in. Every podcast episode was brand awareness that HubSpot did not have to pay for on a per-click basis.

The Hustle also cross-promoted HubSpot tools, Academy courses, and product launches directly to an engaged audience. For a company built on the philosophy that attracting customers is superior to interrupting them, buying a media company was not a diversification; it was the ultimate expression of the inbound thesis.

The data and AI acquisition strategy was even more consequential, and it unfolded in three carefully sequenced steps.

First came PieSync in November 2019, a Belgium-based data synchronization startup that was the highest-reviewed data syncing platform on the market at the time of acquisition. The price was not disclosed. PieSync solved a specific but critical problem: when a business uses HubSpot for CRM but also uses Mailchimp for email, QuickBooks for accounting, and Zendesk for support, customer data gets fragmented across all those systems. PieSync provided real-time, bidirectional data sync across hundreds of applications, ensuring that if a contact's phone number changed in one system, it automatically updated everywhere else. Post-acquisition, PieSync's technology became the backbone of Operations Hub's native Data Sync feature, enabling HubSpot's CRM to stay in sync with over 100 third-party apps without manual imports, exports, or CSV files. This was the plumbing layer, invisible but essential.

Second came Clearbit in November 2023, HubSpot's largest and most strategically significant acquisition to date: a B2B intelligence platform acquired for $150 million in cash as confirmed in the company's 10-K filing. Clearbit brought 400,000 users and a database covering 20 million companies and 500 million decision-makers, enriching customer records with over 100 firmographic, demographic, and technographic data points. To put it simply: if PieSync connected HubSpot's data to other systems, Clearbit enriched HubSpot's data with external intelligence about who those companies and contacts actually are.

The Clearbit acquisition operated on multiple strategic layers simultaneously.

First, it provided the structured data foundation needed to train and power HubSpot's AI models. You cannot build intelligent AI features without high-quality data to feed them, and Clearbit's database provided exactly that raw material.

Second, it directly challenged ZoomInfo, then a roughly $4.2 billion market cap company selling B2B data as a standalone product, by bundling that same intelligence natively into the CRM at no additional cost for many tiers. This was a classic counter-positioning move: ZoomInfo sells data for $15,000 to $40,000+ per year; HubSpot gives it away as a platform feature.

Third, it gave HubSpot the data quality and enrichment capabilities that enterprise clients demand, fueling the upmarket push.

At roughly 3-4x Clearbit's estimated annual recurring revenue of $40-50 million, versus ZoomInfo's 6-8x revenue multiple at the time, the deal appeared disciplined. Clearbit was subsequently rebranded as "Breeze Intelligence" and integrated natively across HubSpot's Smart CRM, providing automatic data enrichment, buyer intent scoring, and form shortening.

Third came Frame AI in December 2024, a conversational intelligence platform that transforms unstructured data, emails, phone calls, meeting transcripts, and chat conversations, into actionable insights using AI. If Clearbit gave HubSpot structured B2B data, Frame AI gave it unstructured conversational intelligence. Together, the three acquisitions create a complete data architecture: PieSync connects the data across systems, Clearbit enriches it with external intelligence, and Frame AI extracts meaning from the messy, unstructured conversations that happen between businesses and their customers every day. It is a data trifecta, and each piece was acquired in sequence as the strategic vision clarified.

The most dramatic M&A event in HubSpot's history, however, was a deal that never happened.

In April 2024, Reuters reported that Alphabet was considering acquiring HubSpot and had met with investment bankers to discuss an offer price and regulatory risk. Over the following weeks, Bloomberg reported continuing talks, and HubSpot's stock spiked to approximately $587 per share, implying a market cap north of $35 billion.

Then in July 2024, Bloomberg reported that Alphabet had shelved the effort. The stock plummeted 21% from its rumor-driven peak. The dominant reason was antitrust risk: Google was already under active DOJ investigation and European Commission scrutiny. Adding a dominant CRM and marketing platform to Google's advertising empire would have triggered years of regulatory review. The two sides reportedly never even reached detailed due diligence discussions.

After walking away, Alphabet pivoted to acquiring Wiz, the cybersecurity company, for $32 billion, a sector with far fewer antitrust complications.

For investors, the failed Google deal was informative in several ways. It validated HubSpot's strategic value: the world's largest advertising company saw it as a key asset for competing with Salesforce and Microsoft in enterprise Go-to-Market. It confirmed that HubSpot's independent path was not for lack of acquirer interest but rather a consequence of today's regulatory environment. And it created a natural ceiling on the stock price: once the $587 acquisition rumor price evaporated, the shares had to find a new equilibrium based on fundamentals rather than takeout speculation. That process of re-pricing took the stock down substantially and contributed to the broader compression in HubSpot's valuation multiple.

The most recent capital allocation signal came on February 7, 2026, when HubSpot's board authorized a $1 billion share buyback program over 24 months, the company's first-ever significant capital return. For a company that spent its first twelve years as a public company reinvesting every dollar into growth, the buyback represented a maturation milestone. It signaled three things: management's confidence that free cash flow generation is now durable and predictable, a belief that the stock is undervalued at current levels, and a recognition that the company has moved past the phase where every marginal dollar needs to be plowed into customer acquisition. The $1 billion authorization represents roughly 1.7 years of free cash flow at 2025 levels, suggesting it is sized to be meaningful without constraining growth investment.

VIII. Hidden Businesses and Growth Engines

Three businesses within HubSpot receive almost no attention in analyst reports or media coverage, but each has the potential to meaningfully alter the company's trajectory. These are the hidden engines worth understanding.

The first is HubSpot Payments and Commerce Hub.

HubSpot has quietly built a native quote-to-cash solution that embeds payments directly into quotes, invoices, and payment links within the CRM. Powered by Stripe's infrastructure, Commerce Hub charges 2.9% per credit card transaction and 0.5% per ACH transaction, capped at $500 per transaction, with no monthly fees.

In 2025 alone, Commerce Hub received over 58 product updates, including enhanced billing automation, recurring payment management, and AI-powered configure-price-quote capabilities.

To understand why this matters, think about the Shopify Payments analogy. Shopify started as a software platform for building online stores, charging a monthly subscription fee. Then it added Shopify Payments, which takes a small percentage of every transaction processed through the platform. Today, Shopify's Merchant Solutions segment, which is primarily payments and financial services, generates more revenue than its subscription software. HubSpot is running a similar playbook but applied to B2B transactions rather than e-commerce. Every transaction processed through HubSpot Payments creates a payments-based switching cost that goes far beyond software: if your invoicing, your payment processing, your CRM, and your sales pipeline all live in the same system, the pain of switching becomes prohibitive. HubSpot does not yet disclose payments GMV or transactional revenue as a separate line item, which is itself telling: the business may still be too small to warrant disclosure, but with 289,000 customers on the platform, even modest adoption rates could create a meaningful transactional revenue stream that compounds independently of software subscription growth.

The second hidden business is HubSpot Academy.

On the surface, it looks like a training platform that offers free certifications in inbound marketing, sales methodology, content strategy, and CRM administration. But the real moat is deeper and more structural.

Over 500,000 professionals held active HubSpot certifications as of 2023, a number that has almost certainly grown substantially since. "HubSpot Certified" has become a resume line item, a credential listed as a preferred or required qualification in job postings on LinkedIn, Glassdoor, and Indeed for roles ranging from Inbound Marketing Manager to VP of Customer Success.

Northeastern University accepts HubSpot Academy certifications as transfer credits toward a master's degree. That is a remarkable signal: an accredited university treating a software vendor's training as equivalent to graduate coursework. It is the kind of institutional validation that money cannot buy.

The genius of making all certifications free is that it removes the barrier to adoption and creates a massive trained workforce that functions as HubSpot's distribution moat. Every certified professional is, in effect, a HubSpot advocate embedded inside a company that might not yet be a customer. When that professional is hired by a new company and asked "what CRM should we use?", the answer is almost always the one they are already certified in. Every hiring manager who lists "HubSpot Certified" as a job requirement is reinforcing the platform's centrality in the Go-to-Market technology stack. This is a self-reinforcing loop: more certified professionals drive more company adoptions, which creates more demand for certified professionals, which drives more people to get certified.

The third hidden engine is the Solutions Partner ecosystem.

HubSpot now has over 7,000 Solutions Partners globally, consisting of agencies, consultancies, and system integrators organized into Gold, Platinum, Diamond, and Elite tiers with revenue sharing on deals sourced and managed.

IDC projects that the HubSpot partner ecosystem is on pace to surpass $30 billion in potential partner revenue globally by 2028. Nearly one-third of solutions partner revenue now comes from technical services like integrations and data migrations, indicating deepening platform dependency.

In 2025, HubSpot launched a Partner Development Fund, providing marketing development funds to higher-tier partners for pipeline creation.

This partner ecosystem creates a powerful network effect: more partners means more implementation support, which means more customers can adopt HubSpot, which attracts more partners. It also creates a constituency of thousands of independent businesses that actively sell and recommend HubSpot, distributing the customer acquisition burden far beyond HubSpot's own sales organization.

To appreciate the scale of this hidden asset, compare it to the Salesforce partner ecosystem. Salesforce has over 150,000 implementation consultants and thousands of partners generating an estimated $6.19 in ecosystem revenue for every $1 of Salesforce revenue. HubSpot's ecosystem is much smaller in absolute terms, but it is growing faster and is more tightly coupled to the platform. A Salesforce partner typically builds custom solutions on top of the platform, which creates value but also complexity. A HubSpot partner typically implements the standard platform and trains users, which creates value through adoption velocity rather than customization depth. Both models work, but HubSpot's is arguably more scalable and less prone to the technical debt that accumulates in heavily customized Salesforce implementations.

Taken together, these three hidden businesses, Commerce Hub's payments, Academy's certification ecosystem, and the Solutions Partner network, represent optionality that is largely unpriced in the current stock. Each operates as a flywheel within the larger flywheel, compounding in ways that do not show up cleanly in quarterly revenue figures but that fundamentally strengthen the platform's competitive position.

IX. Framework Analysis: Power and Moats

To rigorously assess HubSpot's competitive position, it is worth applying two classic strategic frameworks that sophisticated investors use: Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces.

Through the lens of Helmer's 7 Powers, HubSpot possesses at least three identifiable sources of durable competitive advantage.

The most potent is switching costs. A CRM is the system of record for customer relationships, the digital spine of a business's revenue engine. It stores every contact, every deal, every email exchange, every marketing campaign, every support ticket.

Once a company has its marketing automation, sales pipeline, service tickets, website, and commerce workflows running through HubSpot, with data flowing between those hubs in real time, the cost of migrating to a different platform is enormous. The cost is not just financial; it is organizational disruption, data migration risk, retraining hundreds of employees, and the potential for months of reduced productivity during the transition.

With the average HubSpot customer now using nine or more marketplace integrations, the tentacles of the platform extend deep into the customer's broader technology stack. Pulling HubSpot out is not like canceling a subscription; it is more like performing open-heart surgery on the business's operations.

The second power is network effects, operating through two channels. The App Marketplace, now exceeding 2,000 integrations, becomes more valuable to each customer as more integrations are added, while each new integration makes HubSpot more attractive to potential customers. If you are a SaaS company deciding where to build your next integration, you build it for the platform with the most potential users, which means you build it for HubSpot, which makes HubSpot more useful, which attracts more users. The Solutions Partner network of 7,000-plus agencies creates a similar dynamic: more partners means better implementation support, which drives more customer adoption, which attracts more partners.

The third power is counter-positioning, specifically against Salesforce. This is worth explaining carefully because it is one of the most powerful dynamics in enterprise software.

Salesforce is powerful, complex, and expensive. A Salesforce implementation typically costs $150+ per user per month, requires dedicated administrators, consultants, and custom development, and takes months to fully deploy. HubSpot's pitch is the inverse: easy, crafted, and lovable.

HubSpot won the SMB and mid-market segments because Salesforce structurally cannot simplify down to compete without cannibalizing its own business. Salesforce's acquisition-assembled architecture, its enterprise pricing models, and its organizational DNA all pull toward complexity. Its army of 150,000+ implementation consultants generates revenue from that complexity.

For Salesforce to truly compete with HubSpot in the SMB market, it would have to cannibalize its premium pricing, simplify its product architecture, shrink its professional services ecosystem, and potentially alienate its existing enterprise customer base. This is the classic counter-positioning dynamic: the incumbent cannot respond to the disruptor without damaging its own business model.

HubSpot also has a nascent counter-positioning dynamic against ZoomInfo. With Clearbit rebranded as Breeze Intelligence, HubSpot now bundles B2B data intelligence natively into the CRM. ZoomInfo, with roughly $1.2 billion in revenue, sells data as a standalone product at premium prices. HubSpot gives similar data away as a platform feature included in higher tiers, directly threatening ZoomInfo's standalone pricing power.

Porter's 5 Forces paint a more nuanced picture. The threat of new entrants is moderate to high. AI is making software cheaper and faster to build, and new AI-native CRM startups are emerging regularly. But distribution remains the bottleneck. HubSpot's nearly 289,000 customers, 7,000-plus partners, 500,000-plus certified professionals, and 2,000-plus integrations create a distribution moat that a startup cannot replicate with better technology alone. Technology is the easy part; building the ecosystem is the hard part.

The threat of substitutes is real, particularly from vertical-specific CRMs built for industries like real estate, healthcare, and construction that offer deeper domain-specific workflows. ServiceTitan for home services trades, Veeva for life sciences, and Procore for construction all compete by offering industry-tailored functionality that a horizontal platform like HubSpot cannot match in depth.

Monday.com competes as a simpler, cheaper CRM alternative for project-centric SMBs at roughly $12 per user per month, but lacks the full-funnel integration across marketing, sales, and service that HubSpot provides.

The bargaining power of buyers remains low to medium: SMBs have very few all-in-one alternatives at HubSpot's price and usability combination. Salesforce is too complex and expensive for most of them, Monday.com lacks depth, and Zoho, while affordable, is less polished. Microsoft Dynamics 365 is strong for companies already deep in the Microsoft stack but has never gained significant traction in the SMB segment.

The competitive battleground worth watching most closely is the mid-market, companies with roughly $10 million to $500 million in revenue, where HubSpot is pushing upmarket and Salesforce is trying to push down. In 2025, HubSpot deals exceeding $10,000 in monthly recurring revenue grew 41%, a strong signal that the upmarket push is gaining traction.

There is also a supplier power dimension worth noting. HubSpot's AI strategy depends heavily on OpenAI's GPT models, with the recent upgrade to GPT-5 across Breeze Studio agents. This creates a supplier dependency: if OpenAI raises prices, restricts access, or changes its API terms, HubSpot's AI cost structure and capabilities could be materially affected. Salesforce, by contrast, has invested in building more of its AI infrastructure in-house with its Einstein platform and has diversified across multiple model providers. This supplier concentration risk is a legitimate concern in the Porter's framework analysis, though HubSpot could presumably switch to alternative large language model providers if the economics shifted unfavorably.

Finally, the rivalry among existing competitors is intensifying. Salesforce launched its "Agentforce" AI agent platform in late 2024, directly competing with HubSpot's Breeze Agents for the "agentic CRM" positioning. Microsoft is embedding Copilot capabilities across Dynamics 365. And a new generation of AI-native CRM startups is emerging, built from the ground up around AI agents rather than bolting AI onto traditional CRM architectures. The question for investors is whether HubSpot's installed base, ecosystem, and AI investments create sufficient defensibility against both the incumbents pushing down and the startups pushing up.

X. Playbook: Lessons for Builders and Investors

Four lessons from HubSpot's journey stand out as broadly applicable, not just to software companies, but to any business navigating platform competition and market expansion.

First, ecosystem beats product.

HubSpot does not necessarily have the best feature in any single category. Its marketing automation is not as deep as what was once offered by Marketo, now owned by Adobe. Its CRM is not as customizable as Salesforce's. Its helpdesk is not as mature as Zendesk's or Freshdesk's.

But HubSpot wins because its ecosystem, the Academy with 500,000-plus certified professionals, the 7,000 Solutions Partners, the 2,000-plus marketplace integrations, creates gravitational pull that no individual feature can match.

Builders should invest in ecosystems early, even before the product is fully mature, because ecosystems compound in ways that features do not. A better feature can be copied in months; an ecosystem takes years to build and is nearly impossible to replicate.

Second, culture is technical debt. If you do not manage it intentionally, you pay exponentially higher interest later.

HubSpot's Disrupted crisis in 2015-2016 could have been fatal. Instead, it became the catalyst for a systematic cultural engineering effort that has paid dividends for a decade. The lesson is not that culture happens naturally at good companies. The lesson is that culture must be treated with the same intentionality, iteration, and rigor as a software product.

Shah's Culture Code has been updated over thirty times. That is not a one-time exercise; that is continuous deployment applied to organizational values. Most companies write a culture deck once, put it on the website, and never touch it again. HubSpot treats its culture like software: versioned, tested against real-world feedback, and patched when bugs appear.

Third, the bifurcated CEO model works when the roles are clearly delineated.

The split between a product and culture founder maintaining strategic influence, in HubSpot's case Shah and to a lesser extent Halligan, and an execution-focused professional CEO like Rangan, is a repeatable pattern for scaling. The key is that both parties genuinely respect each other's domain and resist the temptation to micromanage across the boundary.

When this model fails, it usually fails because of ego, not structure. The founder feels sidelined, or the professional CEO feels second-guessed on every operational decision. HubSpot has so far avoided this trap because Shah genuinely does not want to run the company day-to-day and Rangan genuinely respects the product and cultural vision that built the franchise.

Fourth, media plus software is a defensible combination that most software companies undervalue.

HubSpot's acquisition of The Hustle was not a vanity project. It was a recognition that in a world where paid customer acquisition costs relentlessly increase, owning the audience directly is a structural advantage.

Every Hustle newsletter subscriber who converts to a HubSpot customer was acquired at effectively zero marginal cost, compared to the $500 to $2,000 per customer that typical B2B SaaS companies spend on paid digital acquisition.

For companies building in categories where content marketing is a natural fit, the integration of owned media and software distribution deserves serious strategic consideration. It is no coincidence that the most successful SaaS companies of the last decade, HubSpot, Atlassian, Shopify, have all invested heavily in content-driven distribution rather than relying solely on enterprise sales teams. The pattern is clear: companies that own their distribution channels outperform those that rent them.

XI. The AI Inflection: Bull Case, Bear Case, and What to Watch

The bull case and bear case for HubSpot both hinge on the same force: artificial intelligence. This is what makes the current moment so fascinating for investors. The same technology that threatens HubSpot's foundational marketing philosophy also represents perhaps its greatest growth opportunity.

The bear case begins with an uncomfortable truth: HubSpot's own marketing philosophy is under direct assault from AI. "Inbound marketing" was built on the premise that businesses could attract customers by creating useful content that ranks highly in search engines. A prospect searches "how to improve my email open rates," finds a HubSpot blog post with helpful advice, downloads a free template, enters their email address, gets nurtured through a sequence of educational emails, and eventually becomes a customer. The entire system depended on Google sending traffic to content.

But what happens when the search engine itself provides the answer? Google's AI Overviews, which now appear in 13 to 16 percent of all queries, provide AI-generated answers directly in search results, reducing click-through rates to underlying websites by up to 47 percent. The user gets the answer without ever visiting the website.

HubSpot has felt this pain firsthand, and the numbers are stark. The company's own organic blog traffic declined from 24.4 million monthly visits in March 2023 to just 6.1 million by January 2025, a staggering 75 percent decline in under two years.

This collapse was driven not only by AI Overviews but also by Google algorithm updates that penalized the kind of broad, generic content HubSpot had published for years: topics far outside its core CRM business like resignation letter templates, cover letter examples, and famous quotes. HubSpot had been playing an SEO volume game, publishing content on anything that attracted search traffic regardless of relevance, and AI disrupted exactly that type of content strategy.

The bear case extends beyond SEO. If AI agents can autonomously research prospects, write personalized outreach emails, qualify leads, and even handle initial sales conversations, then the sales development representatives who constitute a significant share of HubSpot's user base might no longer need a CRM in the traditional sense. Why log activities in a database when an AI agent can manage the entire top-of-funnel process end to end?

And if AI can generate marketing content, build landing pages, write email sequences, and optimize ad campaigns, does a mid-market company even need Marketing Hub? These are real questions, and bears argue that AI is not a feature to add to HubSpot but rather an existential threat to the category itself.

The bull case, however, is equally compelling and arguably more grounded in HubSpot's recent execution. Start with the most important data point: despite the 75 percent organic traffic decline, HubSpot's revenue grew 19 percent in the same period. This disconnect reveals something crucial. Organic blog traffic was never the primary revenue driver. It was a top-of-funnel awareness channel, the equivalent of a billboard on the highway. The actual conversion engine, the free CRM, Academy certifications, partner channel, word-of-mouth referrals, and product-led growth flywheel, remained intact and continued to accelerate. Net new ARR grew 24 percent in 2025, outpacing revenue growth by 600 basis points, a signal that the economic engine is actually accelerating even as the SEO traffic channel shrinks.

HubSpot's AI strategy, branded Breeze, is ambitious and comprehensive.

Breeze Copilot serves as an AI assistant embedded across all hubs for conversational queries, content generation, and task automation. Breeze Intelligence, the rebranded Clearbit, provides AI-powered data enrichment using the combined database of 20 million company profiles and 500 million decision-maker records.

And Breeze Agents, a suite of four specialized AI agents, represent HubSpot's bid to become the "agent control center" for business operations.

The Breeze Customer Agent already resolves over 50 percent of support tickets autonomously, with customers spending roughly 40 percent less time closing tickets. The Breeze Prospecting Agent researches target accounts and personalizes outreach using CRM context and intelligence data.

The Content Agent generates blog posts, landing pages, case studies, and social media content aligned with the company's brand voice. And the Knowledge Base Agent, launched in 2025, automatically expands and enhances knowledge base articles using data extracted from existing support tickets and conversations, powered by Frame AI's conversational intelligence technology.

At INBOUND 2025, HubSpot introduced "The Loop," a new continuous growth methodology designed for hybrid human-AI teams. This represented the company's most significant strategic shift since coining "inbound marketing" over a decade earlier, a pivot from SEO-dependent inbound to what the industry is calling Answer Engine Optimization and Generative Engine Optimization, optimizing content to be cited by AI models rather than just ranked by search engines. In January 2026, HubSpot upgraded its default AI model from GPT-4.1 to GPT-5 across all Breeze Studio agents, and added audit cards for AI action transparency.

The bull thesis can be stated simply: the companies that survive platform shifts are the ones that own the customer relationship. CRMs do not go away when AI arrives; they become more important, because AI agents need structured data to operate on, context to personalize their actions, and a system of record to log their outputs.

Think of it this way. An AI agent that can write a personalized sales email is useful. But an AI agent that can write a personalized sales email based on the prospect's complete interaction history, their company's firmographic data, the sentiment of their last three support conversations, and the context of where they are in the buying journey, that is transformative. And all of that context lives in the CRM. The AI agent without a CRM is like a brilliant new hire on their first day: talented but blind to context. The CRM is what gives the agent eyes.

HubSpot is positioning itself as the platform that orchestrates the AI agents, not the platform that gets displaced by them. CEO Yamini Rangan, on the Q4 2025 earnings call, cited "real outcomes for customers" from Breeze agents as a key growth driver and described the company as an "agentic customer platform." The early data supports this positioning: the Breeze Customer Agent resolves over half of support tickets autonomously, and customers using it spend 40% less time per ticket. That is not a demo; that is production-grade AI delivering measurable ROI.

The enterprise question adds a final layer of complexity. Deals over $10,000 in monthly recurring revenue grew 41 percent in 2025, and net revenue retention rose to 105 percent in Q4, the highest level in recent years. These are encouraging signals. But the fundamental tension remains: moving upmarket requires adding complexity, permissions layers, customization options, and enterprise-grade security and compliance features. Every feature added for a Fortune 500 customer is a feature that risks overwhelming the fifty-person startup that made HubSpot lovable in the first place. This is the classic innovator's dilemma in reverse: instead of being disrupted from below, HubSpot risks over-engineering itself as it reaches upward.

The resolution of this tension will likely determine the next five years of stock performance. If HubSpot can successfully serve both the 20-person startup and the 5,000-person enterprise on the same platform, with AI abstracting away the complexity for smaller customers while providing the depth that larger customers demand, it will have achieved something that very few software companies have ever accomplished. If it cannot, it risks getting stuck in the mid-market, a profitable but not spectacular position that would compress the stock's valuation multiple toward the low-growth SaaS peer group.

XII. Key Metrics to Track

For investors following HubSpot's ongoing performance, two KPIs rise above the noise as the most important signals to monitor.

The first is net revenue retention.

This single metric captures both churn and expansion in one number, telling you whether the installed base is growing in value or shrinking. Think of it as the heartbeat of the subscription business.

If NRR is above 100%, the existing customer base is generating more revenue this year than last year, even before you count new customer additions. If it is below 100%, the bucket is leaking.

HubSpot's NRR journey has been a story in three acts: 88.6% at IPO in 2014, which was the key bear case; a peak of approximately 115% in 2021 during the COVID-driven digital transformation boom, which validated the multi-hub platform strategy; and a trough near 101-102% in 2024 as macro headwinds hit SMB budgets, before recovering to 103.5% for full-year 2025 and 105% in Q4 2025.

Management expects NRR to grow an additional one to two percentage points year-over-year in 2026. If NRR sustains above 105% and trends toward 110-plus, it will signal that the multi-hub strategy and AI monetization are successfully driving expansion within the installed base. If NRR stalls or declines, it may indicate that the SMB customer base is hitting a spending ceiling or that competitive pressures from vertical CRMs and AI-native startups are intensifying.

The second key metric is average subscription revenue per customer, currently around $11,600 annually.

This number captures the upmarket push in a single figure. If ASRPC is growing faster than inflation, it means customers are adopting more hubs, upgrading to higher tiers, or adding Breeze AI capabilities, all of which indicate that HubSpot is successfully expanding its wallet share within each customer.

Conversely, if ASRPC growth flattens while customer count still rises, it suggests HubSpot is adding more low-value freemium-to-entry customers without successfully migrating them to higher-value relationships, which would be a warning sign for long-term unit economics.

Management has guided for low-to-mid single-digit ASRPC growth in constant currency for 2026, which is modest but reflects the tension between adding high-value enterprise customers and continuing to expand the freemium funnel at the bottom.

These two metrics, NRR and ASRPC, together tell the complete story of HubSpot's strategic execution.

NRR tells you whether the platform is sticky and expansive. ASRPC tells you whether the customer mix is moving upmarket.

If both are trending up simultaneously, the compounding thesis is intact. If NRR rises but ASRPC falls, HubSpot is winning on retention but losing the upmarket battle. If ASRPC rises but NRR falls, the company is landing bigger customers but failing to retain and expand them.

A third metric worth tracking as a secondary indicator is the ratio of stock-based compensation to revenue. This ratio has been declining from elevated levels but still represents a meaningful gap between GAAP and non-GAAP profitability. A company generating $595 million in free cash flow but running $700 million in annual SBC is effectively paying a significant portion of its workforce in equity dilution rather than cash. As long as this ratio continues declining, the GAAP earnings trajectory will improve. If it reverses, it would signal that HubSpot is struggling to retain talent without escalating equity grants, a common challenge in competitive software labor markets.

Watch these numbers quarter by quarter and they will tell you everything you need to know about whether the strategy is working.

XIII. Recent Developments

On February 11, 2026, HubSpot reported Q4 and full-year 2025 results that exceeded expectations across every key metric.

Q4 revenue reached $846.7 million, up 20 percent year-over-year, beating the consensus estimate of $830.8 million. Full-year revenue hit $3.13 billion. Customer count grew 16 percent to 288,706, and net revenue retention rose to 105 percent in Q4, up sequentially from 103 percent in Q3.

Most notably, full-year net new ARR grew 24 percent, outpacing constant currency revenue growth by 600 basis points, indicating that the company is accelerating its monetization trajectory even as headline revenue growth moderates from its post-COVID peaks.

The company's 2026 guidance was equally strong and notably above consensus. Management guided for full-year revenue of $3.69 to $3.70 billion, representing 18 percent as-reported growth and 16 percent in constant currency, well above the consensus estimate of $3.61 billion. Q1 2026 revenue guidance of $862 to $863 million similarly exceeded the $836 million consensus. Earnings per share guidance of $12.38 to $12.46 for the full year dwarfed the consensus estimate of $11.46, reflecting continued margin expansion and operational discipline.

The $1 billion share buyback authorization represented a milestone in HubSpot's capital allocation evolution. For a company that had never returned capital to shareholders in its twelve-year history as a public company, it was a statement of confidence in free cash flow durability and a signal that management considered the stock undervalued. With $595 million in free cash flow generated in 2025 and expectations for further expansion in 2026, the buyback program appears well-funded without compromising the company's ability to invest in growth or pursue strategic acquisitions.

Despite the strong results, the stock remains under pressure from the broader SaaS selloff.

Shares surged 9.4 percent to $228.95 on the earnings release but remain roughly 70 percent below their all-time highs above $800 reached during the pandemic-era tech boom.

Analyst price targets have been cut broadly amid the SaaS downdraft, with RBC cutting to $400, Morgan Stanley to $405, Truist to $300, and UBS to $325. But all four maintained Buy or Outperform ratings, reflecting a consensus view that the business fundamentals are stronger than the stock price suggests.

The disconnect between operating performance and stock price is itself a story about the SaaS sector broadly. Across the industry, multiples have compressed from the 20-30x forward revenue common in 2021 to the 8-12x range that prevails in early 2026. HubSpot trades at roughly 9x forward revenue, a multiple that would have been considered absurdly cheap just three years ago for a company growing 19 percent with expanding margins and a $1 billion buyback. The market is effectively pricing in a scenario where growth decelerates meaningfully from current levels, which means that if HubSpot delivers on its guidance, there is significant room for multiple re-expansion.

CEO Yamini Rangan highlighted the "agentic customer platform" as HubSpot's next growth vector on the earnings call, citing "real outcomes for customers" from Breeze agents as a key driver.

The company continues to invest heavily in AI capabilities, with over 200 product updates unveiled at INBOUND 2025, the majority AI-related, and the upgrade to GPT-5 across all Breeze Studio agents in January 2026.

One material accounting and regulatory consideration worth flagging: HubSpot's stock-based compensation remains significant, running at approximately $700 million annually, which creates a meaningful gap between GAAP and non-GAAP profitability metrics. While the company achieved $45.9 million in GAAP net income in 2025, non-GAAP earnings are substantially higher due to the stock-based compensation add-back. Investors should monitor the ratio of stock-based compensation to revenue, which has been declining but remains elevated relative to mature software companies. Additionally, the company's international revenue, which reached 49% of total revenue in Q3 2025, introduces foreign exchange translation risk, which management addresses by providing constant currency growth rates alongside as-reported figures.

Whether AI proves to be the existential threat that bears fear or the growth accelerant that bulls anticipate remains the defining question for HubSpot's next chapter.

What is clear is that the company is not standing still: it is rebuilding its growth methodology, its product architecture, and its competitive positioning around AI with the same urgency that it once brought to defining inbound marketing itself.

Twenty years ago, two MIT grad students looked at a broken marketing landscape and asked: what if businesses could attract customers instead of chasing them? Today, a new generation of leaders at the same company is asking an equally fundamental question: what if AI agents could handle the customer relationship while humans focus on strategy and creativity?

The answer to that question will determine whether HubSpot's next twenty years are as remarkable as its first.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube