Hubbell: The 136-Year Infrastructure Backbone Nobody Talks About

I. Introduction & Cold Open

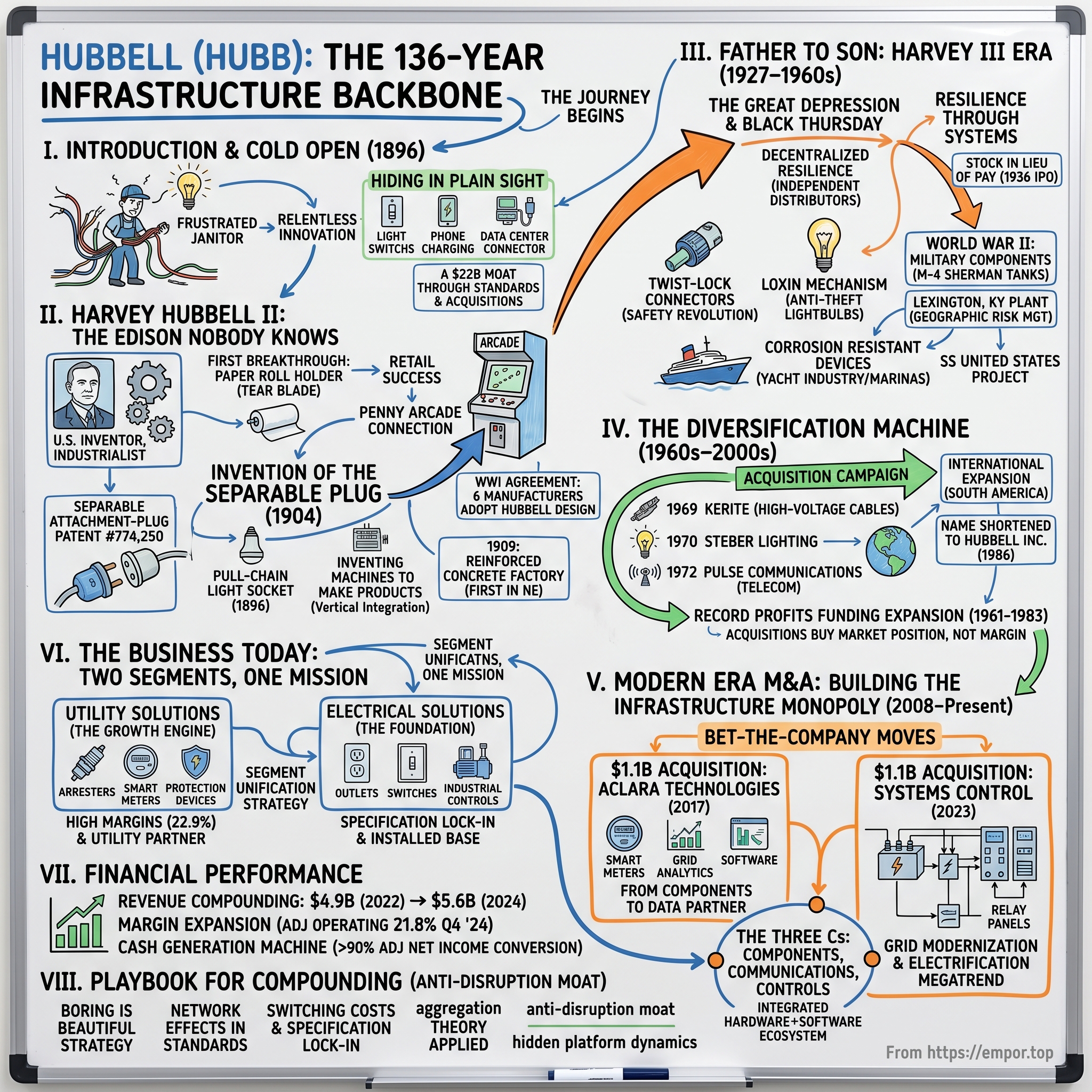

Picture this: It's 1896 in Bridgeport, Connecticut. A frustrated janitor at a local penny arcade is on his hands and knees, disconnecting and reconnecting dozens of electrical wires every night just to sweep the floor. Each connection risks a spark, a short circuit, maybe worse. Harvey Hubbell II, a 39-year-old inventor with a knack for spotting inefficiency, watches this nightly ritual and thinks: "There has to be a better way."

That moment of observation would birth one of the most ubiquitous inventions in modern life—the electrical plug and socket. Today, you probably touched a Hubbell product within the last hour without knowing it. The light switch you flipped this morning? The outlet charging your phone? The industrial connector powering a data center somewhere? There's a decent chance Hubbell made it, or invented the standard it follows.

Yet mention Hubbell to most investors and you'll get blank stares. This is a company with a $22 billion market cap, $5.6 billion in annual revenue, and products embedded in virtually every piece of electrical infrastructure in North America. It's the ultimate "hiding in plain sight" story—a 136-year-old business that has quietly become the picks-and-shovels provider for the entire electrical age.

The puzzle at the heart of Hubbell is fascinating: How does a company that started by inventing the electrical outlet evolve into a diversified infrastructure giant? How do you build a moat around products that seem utterly commoditized? And why, in an era obsessed with software and platforms, is this old-line manufacturer trading at near all-time highs?

The answer lies in a playbook that's been executed across five generations of leadership—a combination of relentless innovation, strategic acquisitions, and the quiet genius of becoming the standard itself. When you invent the plug, you don't just make a product. You create a system that the entire world must adopt.

This is the story of how Harvey Hubbell II's simple observation in a penny arcade spawned an infrastructure empire. It's about the power of boring businesses, the compounding effects of setting standards, and why the least sexy companies often make the best investments. From that first pull-chain light socket to today's smart grid technologies, Hubbell has been the infrastructure backbone nobody talks about—until now.

II. Harvey Hubbell II: The Edison Nobody Knows

Born in Connecticut in 1857, Harvey Hubbell II wasn't supposed to become the Edison nobody knows. He was a U.S. inventor, entrepreneur, and industrialist, but unlike Edison's celebrity status, Hubbell would build his empire quietly, almost invisibly. After graduating from high school, he began working for companies that manufactured marine engines and printing machinery—the kind of unglamorous industrial apprenticeship that teaches you how things actually work.

By 1888, at age 31, Hubbell had seen enough. He quit his job as a manager of a manufacturing company and founded Hubbell Incorporated in Bridgeport, Connecticut, opening what he called a "small manufacturing facility." But this wasn't some grand venture-backed startup. This was a craftsman with ideas, setting up shop in an era when electricity was still more novelty than necessity.

His first breakthrough had nothing to do with electricity. Hubbell's first product was taken from his own patent for a paper roll holder with a toothed blade for use in stores that sold wrapping paper. Think about every time you've watched a retail clerk tear wrapping paper against that metal edge—that was Hubbell's invention. This cutter stand became a tremendous success; it was a common feature of retail stores that used wrapping paper in the early 1900s and remained in wide use into the late 20th century.

But it was electricity that would make Hubbell's fortune. The story that changed everything happened in the early 1890s during a visit to New York City. Hubbell happened upon a penny arcade, featuring several electrically operated games that, although popular with customers, caused maintenance headaches. Every day, the janitor had to detach each of the power supply wires for the games from separate terminals in the wall so that he could move them and sweep the floor underneath. After he was done, he faced the tedious task of reconnecting the wires, making sure that each one went into the proper terminal--the consequence of not doing so being a short circuit. Watching the janitor gave Hubbell the idea for an electrical plug in which the wires were permanently attached in their proper sequence, so that devices could be easily detached and reattached to their power sources.

This wasn't just observation—it was empathy engineering. Hubbell built a prototype, which he tested with the help of the janitor, and later patented it. The two-pronged electrical plug that became standard for electrical appliances is a direct descendant of this innovation. The janitor, probably unaware of his role in history, had just helped birth the modern electrical age.

But before the plug came another fundamental invention. In August 1896, Hubbell received what would become one of his most important patents: the electric light socket with a pull-chain switch. Think about the simplicity: before this, turning on a light meant either unscrewing the bulb or dealing with complicated wall switches. The pull chain gave ordinary people control over light itself—convenience, safety, and that satisfying click that would echo through the 20th century.

The pace of innovation was staggering. In 1901, Hubbell published a 12-page catalogue that listed 63 electrical products of his company's manufacture. This wasn't a guy tinkering in a garage—this was systematic innovation at industrial scale. Four years later he incorporated his enterprise as Harvey Hubbell, Incorporated.

What set Hubbell apart wasn't just inventing products—it was inventing the machines to make them. Some of the equipment he designed included automatic tapping machines and progressive dies for blanking and stamping. One of his most important industrial inventions, still in use today, is the thread rolling machine. He quickly began selling his newly devised manufacturing equipment alongside his commercial products. This vertical integration before anyone called it that—controlling not just what you make, but how you make it.

The separable plug patent came in 1904. On November 8, 1904, Harvey Hubbell II patented the first detachable electric plug in the United States. The patent number 774,250 for the "Separable Attachment-Plug" would become the foundation for billions of electrical connections worldwide. Hubbell devised a two-part device that would allow portable appliances to quickly pull away from light sockets. The base of the device screwed into the light socket, and a two-pronged plug cap that was connected to the appliance cord would allow the two to be easily separated.

The genius was in the standardization. Hubbell's first plug cap device was patented in 1904, but it wasn't until 1931 that wall plug receptacles had become common enough that the conversion was effectively complete. Milestones during this process were an agreement during World War I by six manufacturers to adopt the Hubbell design. When you create the standard, you don't just win the market—you become the market.

By 1909, Hubbell was building for the ages. The company began constructing a four-floor factory and office building that would become the first building in New England made of reinforced concrete. This wasn't just a factory; it was a statement. While others built in wood and brick, Hubbell built in the material of the future.

The numbers tell the story of relentless expansion. Between 1896 and 1909, he was granted 45 patents on a wide variety of electrical products. By 1917, the transformation was complete: Catalogue No. 17 was published in March 1917. The catalogue had more than 100 pages and listed more than a thousand products. In bulb sockets alone, the company manufactured 277 different types and sizes.

Consider that last number: 277 types of bulb sockets. This wasn't diversification for its own sake—it was solving every conceivable use case, becoming indispensable to an electrifying nation. Every streetcar, every factory, every home being wired for the first time needed Hubbell products.

The innovation never stopped. Hubbell's toggle action light switch which incorporated a "quick make or break" feature to meet the rigid requirements of Underwriters' Laboratories (UL) was replacing the former two button type push switch. When safety standards emerged, Hubbell didn't just meet them—his designs helped define them.

Even problems others ignored became opportunities. Hubbell designed a "Loxin" mechanism which fit into any standard socket and locked the bulb in place. Falling lightbulbs no longer endangered streetcar passengers, and overly thrifty commuters had to find a new source of replacement bulbs for home use. Vibrations from new electric streetcars were loosening bulbs? Hubbell had a product for that. Light bulb theft on public transport? There's a Hubbell solution.

Harvey Hubbell II died on December 17, 1927, three days before his 70th birthday. He left behind not just a company, but an entire electrical ecosystem—products, standards, manufacturing techniques—that would outlive him by centuries. While Edison got the glory for inventing the light bulb, Hubbell invented the infrastructure that made Edison's invention useful. Without Hubbell's pull chain, his plug, his socket, electricity remains a laboratory curiosity rather than the foundation of modern civilization.

The transition was ready: a 26-year-old son trained in the family business, a company with dominant market position, and an America about to face its greatest economic crisis. The stage was set for Harvey Hubbell III to prove whether this empire could survive its founder.

III. Father to Son: The Harvey III Era (1927–1960s)

December 17, 1927. The date hit Bridgeport like a thunderbolt. Harvey Hubbell II was dead, just three days shy of his 70th birthday. The company that bore his name faced an existential question: Could an enterprise built on one man's inventive genius survive without him?

He was succeeded as president of the company by his son, Harvey Hubbell III. Twenty-six years old when he succeeded his father, Harvey Hubbell III had already spent years working in the business. This wasn't nepotism—this was apprenticeship. That early experience with electrical equipment engineering and learning the discipline of production was to stand the company in good stead in the decades to come.

The timing couldn't have been worse. Or perhaps, in retrospect, better. Young Harvey III took the helm less than two years before Black Thursday would crater the American economy. While other companies were caught flat-footed, Harvey III had the advantage of fresh eyes and no sacred cows. He would need both.

Harvey Hubbell III soon showed that he had inherited his father's twin acumen for product innovation and business development. But where his father had been the lone inventor-genius, Harvey III understood systems. His first major innovation wasn't a product—it was a process. He also proved his business acumen by establishing a network of independent distributors to help market and disseminate the company's products, a system that would help offset the low profile that the company has traditionally kept.

Think about the brilliance of this move. In 1929, as credit markets froze and businesses collapsed, Hubbell had already built a distribution network that didn't require massive capital outlays. Independent distributors carried inventory, extended credit to customers, and absorbed local market risks. It was decentralized resilience before anyone had a name for it.

Then came the masterstroke that would define Depression-era Hubbell. Under Harvey Hubbell III, the company went public in 1936, a timely move considering that, during the later years of the Great Depression, some employees occasionally had to accept company stock in lieu of pay. This wasn't just financial engineering—it was social engineering. When cash ran short, employees became owners. The workers who kept the lights on literally owned pieces of the company making the lights work.

Imagine the factory floor in 1936: Workers accepting stock certificates instead of paychecks, not knowing if they were being cheated or given a lottery ticket. Those who held on would discover they'd been handed generational wealth. It's the kind of aligned incentives that modern Silicon Valley thinks it invented.

Product innovation never stopped, even in the depths of economic collapse. He devised the company's lines of twist-lock industrial connectors with new 2-,3- and 4-wire devices of various ratings, designed a whole new series of locking connectors for industrial use which he named "hubbellock", and introduced heavy-duty, circuit-breaking devices. The Twist-Lock wasn't just a product—it was a safety revolution. In industrial settings where accidental disconnection could mean death, the Twist-Lock created certainty. Turn and lock. Simple. Foolproof. Essential.

The toggle light switch story exemplifies Harvey III's approach. His father had mentioned the basic concept, but Harvey III perfected it, incorporating a "quick make or break" feature that met Underwriters' Laboratories' rigid requirements. This wasn't invention for invention's sake—it was innovation guided by standards, regulations, and real-world needs.

There was also the "Loxin" mechanism—a device that locked lightbulbs in place to prevent theft on streetcars. In the Depression, people were stealing lightbulbs from public transport. Harvey III's response wasn't moral outrage—it was a product that made theft physically impossible. Solve the problem, don't complain about it.

Then came December 7, 1941. Pearl Harbor transformed American industry overnight, and Hubbell was ready. During World War II, much of the company's capacity was devoted to manufacturing electrical components for the military, including battery-charging systems for the M-4 Sherman tank. Every Sherman tank rolling through Europe carried Hubbell components. The company that started with penny arcade observations was now helping win the war.

Hubbell also opened a plant in Lexington, Kentucky, in part to meet demand for its military products and also because its original factory in Connecticut was considered vulnerable to air attack. Think about that calculation: In 1942, American industrialists were planning for potential bombing raids on Connecticut. The Kentucky plant wasn't just capacity expansion—it was geographic risk management in an age before anyone used such terms.

The post-war boom found Hubbell perfectly positioned. They had production capacity, technical expertise, a national distribution network, and a workforce that literally owned the company's success. The first Safety Receptacle was designed and produced as were the original "grounding only" devices which helped to set the standards for the industry. And while Hubbell was busy on land, the company found new opportunities at sea. In 1952, the ocean liner "SS United States" was launched in Newport News, Virginia. Queen of the seas for many years, the ship was completely fitted with Hubbell wiring devices designed expressly for narrow stateroom partitions and to withstand the effects of salt air. An ardent yachtsman himself, Harvey Hubbell III designed a complete family of corrosion resistant devices including both on-board and dockside equipment for the expanding pleasure boat industry. Familiar sights at marinas today, these first products were so successful that alternative designs were produced for many industrial applications where corrosive atmospheres and materials posed challenges for standard wiring devices.

The SS United States project reveals Harvey III's genius. He didn't just supply components—he solved for specific constraints: narrow partitions, salt air corrosion, marine safety standards. Then he took those solutions and created an entire marina infrastructure business. Every yacht club in America became a Hubbell customer.

By the late 1950s, the transformation was complete. The company's sales in new products and continuing lines increased proportionately to these successes, but more was to come as Harvey Hubbell Incorporated added diversification. Beginning in 1960, the company entered a new period of rapidly expanding growth in both sales and income. Much of the growth resulted from the company's internal product development, a longstanding Hubbell tradition, and a source that expanded under the industry leadership of Harvey Hubbell III and other Hubbell engineers.

The numbers tell the story: From a company that nearly paid employees in stock during the Depression to a diversified industrial giant entering the go-go 1960s. Harvey III had done more than preserve his father's legacy—he'd institutionalized innovation itself. The company was no longer dependent on a single inventive genius. It had become an innovation machine.

Harvey Hubbell III died in 1968 and was succeeded as CEO by George Weppler, who became the first non-Hubbell to run the company in its 80 years of existence. For the first time, Hubbell would be run by someone whose name wasn't on the building. The family business was about to become something else entirely: a modern conglomerate with acquisition appetite and global ambitions.

IV. The Diversification Machine (1960s–2000s)

The 1960s marked a seismic shift in American business. Conglomerates were the rage, stock multiples soared for anything that could show growth through acquisition, and old-line manufacturers suddenly discovered they could be empire builders. For Hubbell, this era would transform a focused electrical products company into something entirely different—and set the stage for everything that followed.

Beginning in 1960, the company entered a new period of rapidly expanding growth in both sales and income. Much of the growth resulted from the company's internal product development, a longstanding Hubbell tradition, and a source that expanded under the industry leadership of Harvey Hubbell III and other Hubbell engineers. But organic growth was no longer enough. The company embarked on what one correspondent for Forbes admonished his readers in 1977 that 'unless you are reading this on safari, there is probably a Harvey Hubbell invention within six feet of you right now.' Yet despite this ubiquity, the company had remained strongly focused on such products until the 1960s, when it embarked on a diversification program.

The timing was perfect. The post-war industrial boom created thousands of small, specialized electrical companies—perfect acquisition targets for a company with Hubbell's balance sheet and distribution network. Each acquisition wasn't just buying revenue; it was buying a customer list, specialized knowledge, and often critical patents or manufacturing techniques.

Harvey Hubbell III died in 1968 and was succeeded as CEO by George Weppler, who became the first non-Hubbell to run the company in its 80 years of existence. Under Weppler, the pace of Hubbell's acquisition campaign was maintained. In 1969 the company acquired Kerite, a Connecticut-based manufacturer of high-voltage electrical cables used mainly by utility companies and railroads.

The Kerite acquisition was particularly strategic. Founded in 1854 by Austin Goodyear Day, nephew of Charles Goodyear, Kerite had invented the first crosshead extruder for insulated telegraph wire—essentially creating the cable industry. In 1969, Kerite was purchased by the Hubbell Company, an electrical equipment manufacturer with a long history, known for patenting the ubiquitous duplex receptacle and the electric light pull socket. For the next 30 years, Kerite prospered as part of Hubbell, which invested heavily in new manufacturing facilities and revised plant layouts, replacing some buildings that dated back to the Civil War era.

The next year, it acquired Steber Lighting to augment its light fixtures business. Then came the move into telecommunications. In 1972 Hubbell entered the telecommunications equipment field when it purchased Pulse Communications, a Virginia-based manufacturer of voice and data signal processing components. Also that year Hubbell acquired Southern Industrial Diecasting.

The international expansion began almost immediately. Moreover, the company established a presence in South America with its Brazilian subsidiary, Harvey Hubbell do Brasil, after acquiring H.K. Porter do Brasil in 1973 and Metal-Arte Industrias Sao Paolo in 1974.

The numbers tell the story of transformation. In 1961, the company posted a relatively modest $22 million in sales; by 1981 sales had reached $445.8 million. Robert Dixon retired as CEO in 1983 and was succeeded by Fred Dusto, who presided over the final acquisitions of Hubbell's long spree: Miller Lighting and Killark Electric Manufacturing, both purchased in 1985. Twenty years, twenty-fold growth. That's not organic expansion—that's empire building.

But here's where it gets interesting. By this time, Hubbell's diversifications had produced mixed results. On the one hand, the company's original wiring and light fixture business accounted for a disproportionate share of profits into the 1980s, a sign that acquired companies were not proving terribly lucrative despite the fact that Hubbell had made few outright missteps. On the other hand, Hubbell generated record profits every year from 1961 to 1983.

Think about that paradox: Record profits every year for 22 straight years, yet the acquisitions weren't the profit drivers. What was happening? The core business—those boring outlets, switches, and connectors invented by Harvey Hubbell II—was throwing off so much cash that it could fund an acquisition spree while still delivering consistent profit growth. The acquisitions were buying market position, not margin.

In 1986 the company shortened its name to its current form. From "Harvey Hubbell, Incorporated" to just "Hubbell Inc." The founder's first name disappeared, signaling the complete transition from family enterprise to modern corporation.

Dusto retired in 1987 and was succeeded by George Ratcliffe, who had once served as the company's chief counsel. Under Ratcliffe, Hubbell spent aggressively on upgrading and automating its capital equipment as well as on research and development. This reinvestment produced profit margins higher than those of its competitors during the 1980s, as the company was able to cut labor costs and also sell innovative products that commanded relatively high returns.

The 1990s brought more strategic acquisitions. In 1991 it purchased Westinghouse's Bryant Electric division, which made wiring devices for industrial applications. In 1993 Hubbell acquired Hipotronics, a manufacturer of high-voltage cables and test and measurement equipment, and E.M. Weigmann and Co., Inc., a manufacturer of industrial enclosures.

By the turn of the millennium, Hubbell had transformed into something unrecognizable from Harvey Hubbell II's workshop. Hubbell has manufacturing facilities in the United States, Canada, Switzerland, Puerto Rico, Mexico, China, Italy, the United Kingdom, Brazil and Australia and maintains sales offices in Singapore, China, India, Mexico, South Korea, and countries in the Middle East. The company that started with a paper roll holder now spanned the globe.

The 2000s brought a new challenge: integration. Having assembled dozens of companies, brands, and product lines, Hubbell needed to make them work together. In April of that year, Hubbell added U.S. Industries Inc.'s domestic lighting group, LCA Group, to its arsenal in a $250 million deal. Hubbell jumped at the chance to buy the unit, which had secured $575 million in sales in 2001. Management believed the addition of LCA would prove lucrative and expected sales in its lighting products segment to climb to more than $800 million as a result of the deal. Overall, sales during 2002 increased by 21 percent over the previous year.

But not everything worked. During this time period, the company shed several businesses that had proved unprofitable in the long term. With the sale of The Kerite Company, Hubbell exited the insulated cable business. After 30 years, even successful acquisitions could be divested if they no longer fit the strategy.

The diversification era had created a paradox. Hubbell was now everywhere in electrical infrastructure—from the outlet in your wall to the high-voltage lines bringing power to your city. Yet it remained virtually unknown to the public. This anonymity wasn't a bug; it was a feature. While flashier companies captured headlines and volatile stock prices, Hubbell quietly compounded, acquisition by acquisition, product line by product line.

The stage was set for the next transformation. The company had the scale, the distribution, the manufacturing expertise. What it needed was a strategy for the 21st century—one that would transform this collection of electrical businesses into something more valuable than the sum of its parts. The era of financial engineering was ending. The era of strategic focus was about to begin.

V. Modern Era M&A: Building the Infrastructure Monopoly (2008–Present)

December 26, 2017. The day after Christmas, when most of corporate America was still on holiday, Hubbell dropped a bombshell. Hubbell Incorporated (NYSE: HUBB) today announced that it has entered into a definitive agreement to acquire Aclara Technologies LLC ("Aclara"), an affiliate of Sun Capital Partners, Inc. ("Sun Capital") for approximately $1.1 billion in an all-cash transaction.

This wasn't the Hubbell of old, buying small bolt-on acquisitions to round out product lines. This was a bet-the-company move into the future of the electrical grid. Aclara reported revenues of $500 million and adjusted EBITDA of $90 million for the fiscal year ended September 30, 2017. At 12.2x EBITDA, Hubbell was paying up for growth—and signaling a fundamental shift in strategy.

"This is an exciting transaction that is consistent with our long-standing acquisition strategy. Aclara participates in attractive markets that complement our core with high quality products and talented people," said David G. Nord, Chairman, President and Chief Executive Officer. But this wasn't really consistent with the old strategy at all. This was transformation.

What Hubbell was really buying was the future. Aclara offers a comprehensive suite of solutions, including advanced metering infrastructure, meters and edge devices, software, and installation services. Smart meters. Grid analytics. Software. These weren't Harvey Hubbell II's pull chains and outlets. This was data infrastructure for the 21st-century grid.

The strategic logic was compelling. With approximately 1,200 people working with more than 800 electric, water and gas utilities worldwide, Aclara provides actionable insights to help utilities predict, plan and respond to conditions, improve operational efficiency and promote resource conservation to customers. In one acquisition, Hubbell gained relationships with 800 utilities globally—not as a components supplier but as a technology partner.

In 2016, Aclara won a landmark deal to participate in the largest project undertaken by Con Edison, working with Silver Spring and IBM. This was validation at the highest level—Con Edison, serving New York City, doesn't take chances with unproven technology. If Aclara could handle Manhattan, it could handle anywhere.

The integration playbook revealed Hubbell's sophistication. The addition of Aclara's software and analytics solutions, along with its robust and flexible communications networks, to Hubbell Power Systems' performance-critical components, will provide a differentiated solution for a broader set of utility customers to meet their "next gen" needs. This wasn't just adding products—it was creating an ecosystem where hardware and software reinforced each other.

Fast forward to October 30, 2023. Lightning strikes twice. Hubbell Incorporated (NYSE: HUBB) today announced that it has entered into a definitive agreement to acquire Northern Star Holdings, Inc. (commercially known as Systems Control), a portfolio company of Comvest Partners, for $1.1 billion in cash, subject to customary adjustments.

Same price tag, different target, but the strategic thread was clear. Systems Control is a leading manufacturer of substation control and relay panels, as well as turnkey substation control building solutions. Systems Control estimates 2024 sales of approximately $400 million.

Do the math: $1.1 billion for $400 million in revenue. That's 2.75x sales for an industrial manufacturer. In the old Hubbell playbook, this would be insanity. But These highly engineered offerings are mission-critical to grid reliability, enabling utility customers to protect and control substation infrastructure while detecting faults and controlling the flow of electricity.

The CEO's comments revealed the strategy. Gerben Bakker, Hubbell's Chairman, President and Chief Executive Officer said, "This acquisition enhances Hubbell Utility Solutions' industry-leading franchise across utility components, communications and controls. Components, communications, controls—the three Cs of modern grid infrastructure. Hubbell was assembling the full stack.

Greg Gumbs, President, Utility Solutions said, "Substation automation is critical to upgrading aged infrastructure and enabling the integration of renewables and electrification on the grid. There it was—the megatrend play. Renewable integration. Grid modernization. Electrification. Every electric vehicle, every solar panel, every wind farm makes the grid more complex. Complexity requires intelligence. Intelligence requires Systems Control's products.

The financing tells its own story. Hubbell financed the acquisition and related transactions with net proceeds from borrowings under a new unsecured term loan facility in the aggregate principal amount of $600 million, cash on hand, and issuances of commercial paper. This was leverage, but controlled leverage. Investment-grade leverage for infrastructure-grade returns.

Between these two bookend deals, the transformation accelerated. 2008 saw a triple acquisition—USCO Power Equipment, CDR Systems, ElectroComposites. Each one strategic, each one filling a gap in the utility solutions portfolio. $1.1 billion purchase price represents ~12x projected 2024 EBITDA multiple for Systems Control—aggressive but not reckless in a world where infrastructure multiples keep expanding.

The geographic footprint of these acquisitions matters. The company's manufacturing operations are based in Iron Mountain, where about 750 people are employed in a 400,000-square-foot facility. Iron Mountain, Michigan—not Silicon Valley, not Austin. This is American manufacturing in the heartland, the kind of facilities that become impossible to replicate once they're gone.

What's remarkable is the consistency of approach across different management teams. From David Nord to Gerben Bakker, the playbook remained the same: Buy critical infrastructure, pay fair prices, integrate carefully, and trust in the inexorable growth of electrical demand. Total of 14 acquisitions, including 5 in last 5 years, 6 from private equity firms—this wasn't opportunistic M&A. This was systematic empire building.

The private equity angle deserves attention. Six acquisitions from PE firms in recent years—these aren't distressed assets. These are companies that private equity has already optimized, professionalized, and prepared for exit. Hubbell was buying pre-cleaned, pre-packaged growth machines and plugging them into its distribution network.

Not everything stayed. 2021 saw the divestiture of the C&I Lighting business—a tacit admission that not all electrical markets are created equal. The future was in utility and electrical T&D markets, not in commercial lighting where LED disruption and Chinese competition had permanently changed the game.

The modern M&A machine at Hubbell represents something unique in American industry: patient capital deployed aggressively. Each billion-dollar bet is really a 20-year bet on electrical infrastructure. While software companies chase monthly recurring revenue and consumer brands optimize for TikTok virality, Hubbell is betting that substations built today will still need control systems in 2050.

The irony is delicious. Harvey Hubbell II invented the plug to solve a janitor's daily annoyance. His corporate descendants are spending billions to solve utilities' existential challenges. Same DNA—see a problem, build a solution, own the standard—just at continental scale.

VI. The Business Today: Two Segments, One Mission

Strip away the corporate structure, the acquisitions, the global footprint—at its core, Hubbell today is elegantly simple. Two segments, one mission: power the infrastructure that powers everything else.

With 2024 revenues of $5.6 billion, Hubbell solutions electrify economies and energize communities. The company operates two segments: the utility solutions segment, which produces items such as arresters, insulators, connectors, anchors, bushings, enclosures, cutoffs and switches and the electrical solutions segment, which produces application wiring device products, rough-in electrical products, connector and grounding products, and lighting fixtures, as well as other electrical equipment.

But those dry descriptions hide the strategic genius. This isn't random product aggregation—it's systematic control of the electrical value chain from generation to consumption.

Electrical Solutions: The Foundation

The Electrical Solutions segment is Harvey Hubbell II's direct descendant. This is where the outlets, switches, and connectors live—the unsexy backbone of every building in America. In Q4 2024, the segment generated $487 million in revenue, down from prior periods but with expanding margins.

The product portfolio reads like an electrician's shopping list: wiring devices, rough-in electrical products, connector and grounding products, lighting fixtures, industrial controls, communication systems. But focus on what's not said: These are all specification products. Once an architect specs Hubbell, once a contractor learns Hubbell, once a building code requires Hubbell-compliant products, switching becomes almost impossible.

In Electrical Solutions segment, where electrification drove broad-based strength across industrial markets and continued execution on our segment unification strategy drove operating profit growth and margin expansion. The unification strategy is key—instead of competing brands cannibalizing each other, Hubbell is creating a unified go-to-market approach. One sales force, multiple products, total wallet share.

The brand portfolio tells the story of 60 years of acquisitions now working as one: Hubbell, Kellems, Bryant, Burndy, CMC, Bell, TayMac, Wiegmann, Killark, Hawke. Each brand carries its own customer loyalty, its own specifications, its own installed base. Together, they create a web of switching costs that competitors can't untangle.

Electrical Segment Operating Profit Growth: 10% in Q4 2024, with 3.5 points of margin expansion. This is the power of the installed base. Even as revenue fluctuates with construction cycles, margins expand because the business has pricing power. When you're specified into a $100 million building project, nobody quibbles over a 3% price increase on electrical components.

Utility Solutions: The Growth Engine

If Electrical Solutions is the cash cow, Utility Solutions is the rocket ship. The Utility Solutions segment saw net sales increase 4% to $847 million in Q4 2024, but that modest top-line growth masks a fundamental transformation.

This segment makes the equipment that utilities can't operate without: distribution products, transmission equipment, substation products, smart meters, protection devices. When a utility builds a substation, when they upgrade transmission lines, when they install smart meters—Hubbell gets paid.

The recent acquisitions—Aclara for smart meters, Systems Control for substation automation—weren't just adding revenue. They were completing the stack. Now Hubbell can offer utilities everything from the physical infrastructure to the software that manages it. In Utility Solutions, sales growth was driven by acquisitions, as well as strength in grid protection and controls products and continued backlog conversion in AMI and smart meters.

Utility Segment Operating Margin: 22.9% in Q4 2024, with 1.5 points of margin expansion. Think about that margin profile. Nearly 23% operating margins selling to utilities—entities notorious for squeezing suppliers. How? Because when the grid fails, when a transformer explodes, when a storm knocks out power to millions, utilities don't shop for the cheapest solution. They buy what works, what's proven, what's already in their system.

Greg Gumbs, President, Utility Solutions said, "Substation automation is critical to upgrading aged infrastructure and enabling the integration of renewables and electrification on the grid. Systems Control has a proven value proposition, with leading manufacturing quality and engineering expertise driving labor savings for utility customers while enabling them to operate critical infrastructure reliably and efficiently."

The Geographic Manufacturing Moat

Hubbell has manufacturing facilities in the United States, Canada, Switzerland, Puerto Rico, Mexico, China, Italy, the United Kingdom, Brazil and Australia and maintains sales offices in Singapore, China, India, Mexico, South Korea, and countries in the Middle East.

This isn't just global reach—it's strategic redundancy. When COVID shut down Chinese factories, Hubbell's Mexican plants kept running. When tariffs hit Chinese imports, Hubbell's U.S. facilities absorbed demand. Each facility isn't just capacity; it's optionality.

The company's manufacturing operations are based in Iron Mountain, where about 750 people are employed in a 400,000-square-foot facility. Iron Mountain, Michigan. Not a tech hub, not a coastal city. A place where manufacturing knowledge passes from generation to generation, where the workforce shows up, where real estate costs allow for 400,000-square-foot facilities.

The Channel Strategy

Distribution is where Hubbell's strategy crystallizes. They don't sell direct to consumers. They sell through electrical distributors, industrial distributors, utilities directly, and specialty channels. Each channel relationship is decades old, carefully cultivated, impossible to replicate quickly.

The genius is in the coverage model. A contractor working on a hospital in Dallas doesn't call Hubbell directly. They call their local electrical distributor, who has Hubbell products in stock, who has a Hubbell rep on speed dial, who can get specialty products delivered tomorrow. This distribution density creates convenience that becomes dependence.

The Financial Architecture

For the full year 2025, Hubbell anticipates total sales growth and organic sales growth of 4-5%. Hubbell expects 2025 GAAP diluted earnings per share from continuing operations in the range of $16.00 to $16.50 and adjusted diluted earnings per share from continuing operations ("Adjusted EPS") in the range of $17.35 to $17.85. Adjusted EPS excludes amortization of acquisition-related intangible assets, which the Company expects to be approximately $1.35 per share for the full year. The Company believes Adjusted EPS is a useful measure of underlying financial performance in light of our acquisition strategy.

Those numbers tell a story. 4-5% organic growth in a GDP-plus business. But $1.35 per share in intangible amortization—that's the price of empire building. Every acquisition brings intangibles that must be amortized, depressing GAAP earnings but not cash flow. The adjusted numbers strip this out, showing the real economic engine.

Net cash provided by operating activities was $432 million in the fourth quarter of 2024 versus $346 million in the comparable period of 2023. Free cash flow was $364 million in the fourth quarter of 2024 versus $284 million reported in the comparable period of 2023.

Cash generation is accelerating even as the company invests heavily. This is the beauty of the installed base model—once the products are specified, once the relationships are built, the cash flows are remarkably predictable.

The Integration Symphony

What's happening beneath the surface is more interesting than segment reporting. Hubbell is quietly integrating capabilities across segments. Smart meters from Aclara talk to substation controls from Systems Control. Electrical components from the core business get specified alongside utility solutions. The company that started with separate products is becoming a systems provider.

We made strong progress in unifying our HES segment to compete collectively, achieved attractive growth across key utility and electrical verticals, proactively managed price/cost/productivity and drove significant shareholder value creation through portfolio transformation and strategic capital allocation.

"Unifying to compete collectively"—that's corporate speak for creating a monster. Instead of 20 companies selling different products, it's becoming one company selling complete solutions. The customer doesn't want to coordinate between vendors. They want one throat to choke, one number to call, one company to trust.

This is the Hubbell of 2024: Not the most exciting business, not the fastest growing, not the highest margins. But possibly the most entrenched, the most essential, the most impossible to displace. Two segments, thousands of products, millions of connection points—all adding up to one simple mission: be the infrastructure layer that nobody thinks about but everybody depends on.

VII. Financial Performance & Unit Economics

The numbers tell a story of relentless compounding, the kind that makes value investors salivate and growth investors yawn. But beneath the steady progression lies a financial architecture that's more sophisticated than it appears.

The Revenue Trajectory

Start with the headline numbers. Revenue growth: $4.948B (2022) → $5.373B (2023) → $5.629B (2024). That's 14% growth over two years—not explosive, but inexorable. As of May 2025 Hubbell has a market cap of $20.89 Billion USD. This makes Hubbell the world's 959th most valuable company according to our data.

Do the math: $20.89 billion market cap on $5.63 billion in revenue. That's a 3.7x revenue multiple for an industrial manufacturer. For context, most industrial companies trade at 1-2x revenue. The market is paying for something beyond the current numbers.

The company is ranked 651st on the Fortune 500 list of the largest United States corporations by total revenue. Position 651 might not sound impressive until you realize that's out of all U.S. companies, across all industries. For a company nobody's heard of, that's remarkable penetration.

Margin Evolution

The real story is in the margins. Q4 2024 adjusted diluted EPS of $4.10, up 11% YoY despite organic sales being down. How? Margin expansion. Operating margin reached 19.3% with adjusted operating margin at 21.8%, up 240bps year-over-year.

Think about what 240 basis points of margin expansion means. Every dollar of revenue throws off 2.4 cents more profit than a year ago. On $5.6 billion in revenue, that's $134 million of additional profit from operational improvement alone. No growth required.

Utility Segment Operating Margin: 22.9% in Q4 2024. Electrical Segment operating margins expanding 350 basis points. These aren't software margins, but for industrial manufacturing, they're extraordinary. The average S&P 500 industrial company operates at 10-12% margins. Hubbell doubles that.

Cash Generation Machine

Net cash provided by operating activities was $432 million in the fourth quarter of 2024 versus $346 million in the comparable period of 2023. A 25% increase in operating cash flow while revenue was essentially flat. This is the beauty of the model—as the installed base grows, the cash generation accelerates.

Free cash flow was $364 million in the fourth quarter of 2024 versus $284 million reported in the comparable period of 2023. That's a 28% increase. 2025 Outlook - Free Cash Flow Conversion: At least 90% of adjusted net income. When a company commits to 90% cash conversion, they're telling you the earnings are real, not accounting fiction.

Annual free cash flow is approaching $1.5 billion on a $21 billion market cap. That's a 7% free cash flow yield. In a world of 5% Treasury yields, a growing industrial company throwing off 7% cash yields starts to look interesting.

The Acquisition Math

Here's where it gets sophisticated. Adjusted EPS excludes amortization of acquisition-related intangible assets, which the Company expects to be approximately $1.35 per share for the full year. On expected GAAP EPS of $16.00-16.50, that's about 8% of earnings being consumed by acquisition amortization.

But this is non-cash. The $1.35 per share in amortization doesn't reduce cash flow, doesn't require reinvestment, doesn't impact the business operations. It's an accounting artifact of the acquisition strategy. Strip it out, and the real earnings power emerges: $17.35 to $17.85 in adjusted EPS for 2025.

At current prices around $380 per share, that's a P/E of 21-22x on adjusted earnings. Not cheap for an industrial, but remember what you're buying: a tollbooth on electrical infrastructure with 90% cash conversion and expanding margins.

Capital Allocation Framework

The capital allocation tells you everything about management's confidence. Hubbell financed the acquisition and related transactions with net proceeds from borrowings under a new unsecured term loan facility in the aggregate principal amount of $600 million, cash on hand, and issuances of commercial paper.

They're using debt to fund acquisitions while maintaining an investment-grade rating. This is financial engineering at its most conservative—lever up slightly to buy strategic assets, pay down debt with superior cash flow, repeat. Each cycle, the company gets bigger, the moat gets wider, the returns compound.

The dividend story completes the picture. Hubbell has paid dividends continuously since going public in 1936. Through the Depression, through wars, through recessions—the dividend never stopped. Current yield around 1.5%, growing mid-single digits annually. Not exciting, but relentless.

Unit Economics Decoded

The unit economics are deceptively simple. Take a $10 electrical outlet. Hubbell manufactures it for maybe $3 in materials and labor. It sells to a distributor for $6. The distributor sells to a contractor for $8. The contractor bills the end customer $10 plus installation.

Hubbell makes $3 gross profit on $6 revenue—50% gross margins. After SG&A, R&D, and corporate overhead, they net about 20% operating margins. The distributor makes $2 on minimal capital investment. The contractor makes $2 plus labor charges. Everyone wins, nobody has an incentive to disrupt the chain.

Now multiply that by millions of SKUs, thousands of distributors, tens of thousands of contractors. The complexity becomes the moat. A new entrant can't just make a better outlet—they need to infiltrate this entire ecosystem.

Comparative Valuation

Look at the peers. Eaton trades at 25x earnings with similar growth. Emerson trades at 22x with lower margins. Schneider Electric trades at 24x with more cyclicality. Hubbell at 21-22x starts to look reasonable, even cheap given the quality.

The market doesn't fully appreciate what Hubbell has built. This isn't a cyclical industrial that will crater in the next recession. It's an infrastructure provider with 60%+ recurring revenue from maintenance, replacement, and regulatory-driven upgrades.

The Inflation Hedge

Here's what the market really misses: Hubbell is a perfect inflation hedge. Pricing was positive in both segments in Q4, with more than 1 point overall. When copper prices rise, Hubbell passes it through. When labor costs increase, prices adjust. When transportation gets expensive, surcharges appear.

The pricing power comes from the specification lock-in. When you're specified into a $100 million project, nobody changes vendors to save 2% on electrical components. The switching costs—reengineering, respecifying, retraining—dwarf any savings.

Return on Invested Capital

The ROIC story is where Hubbell shines. With $5.6 billion in revenue generating $1+ billion in EBITDA, on a total asset base that's heavily depreciated, the returns on incremental capital are extraordinary. Each dollar invested in the business generates returns far exceeding the cost of capital.

This is why the acquisition strategy works. Buy a company for 12x EBITDA, integrate it into the Hubbell system, expand margins by 300-500 basis points through operational improvements and purchasing power, and suddenly that 12x purchase multiple looks like 8x. Do this repeatedly, and you're creating value with every deal.

The Untold Story

The financial performance reflects something deeper: Hubbell has solved the industrial company paradox. How do you grow steadily in a cyclical world? How do you expand margins in a commoditized industry? How do you generate premium returns on mundane products?

The answer is positioning. By becoming the standard, by owning the specifications, by controlling the channels, Hubbell transcends the limitations of its industry. It's not really selling electrical products—it's selling certainty, reliability, and compliance. And those, it turns out, have pricing power that never goes away.

The numbers prove it works. From $22 million in sales in 1961 to $5.6 billion today. From a family workshop to a Fortune 500 company. From making outlets to owning the infrastructure layer. The financial performance isn't just good—it's the validation of a century-long strategy that's still playing out.

VIII. Power Laws & Playbook

The Hubbell playbook isn't complicated, but it's nearly impossible to replicate. Like compound interest, the strategy seems boring until you zoom out and see the exponential curve. This is how you build a monopoly nobody notices.

The "Boring is Beautiful" Strategy

Warren Buffett once said he likes businesses that are so boring they have no competition. Hubbell took this to an extreme. Who dreams of disrupting the electrical outlet industry? What venture capitalist gets excited about substation control panels? Which MBA graduate wants to revolutionize pull-chain sockets?

Nobody. And that's the point.

The boring nature of the business creates a talent moat. The best engineers at MIT aren't joining Hubbell—they're going to SpaceX or OpenAI. Investment bankers aren't pitching rollups in electrical components—they're chasing software multiples. This lack of attention from smart, ambitious people means less competition for decades.

But boring doesn't mean simple. A Hubbell catalog has thousands of SKUs, each with different voltages, amperages, configurations, and certifications. The complexity is fractal—zoom in on any product category and you find endless variations, each serving a specific use case, each requiring deep expertise.

Network Effects in Electrical Standards

Here's the genius nobody talks about: Hubbell doesn't just follow standards—it helps write them. When you invent the plug, you define what "standard" means. When your engineers sit on the committees that write the National Electrical Code, your products become the reference design.

Every electrician trained in America learns on Hubbell products. Every electrical engineering textbook shows Hubbell diagrams. Every building code references specifications that Hubbell helped write. This isn't regulatory capture—it's something more subtle: expertise capture.

The network effects compound. The more electricians who know Hubbell, the more architects who specify Hubbell. The more Hubbell gets specified, the more distributors stock Hubbell. The more distributors stock it, the more contractors use it. The more contractors use it, the more electricians learn it. The wheel keeps turning.

Switching Costs and Specification Lock-in

Once Hubbell is specified into a project, switching is almost impossible. Consider a hospital being built with Hubbell components. The electrical drawings specify Hubbell part numbers. The contractor bid the job based on Hubbell prices. The electricians trained on Hubbell products.

To switch vendors, you'd need to: Re-engineer the entire electrical design. Get new approvals from the architect and engineer. Retrain the installation crew. Risk compatibility issues between components. Accept liability for any failures from non-standard parts. Face potential code compliance issues.

For what? To save 5% on components that represent 2% of the total project cost? No rational actor makes that trade.

The lock-in extends beyond initial installation. When that hospital needs replacement parts in 10 years, they'll buy Hubbell. When they expand the building, they'll specify Hubbell. When the electrical contractor bids the next hospital, they'll recommend Hubbell. The specification becomes self-perpetuating.

M&A Integration Excellence

Hubbell's acquisition playbook is deceptively simple: Buy companies with strong market positions. Keep the brand and customer relationships. Integrate the back office and manufacturing. Leverage Hubbell's distribution network. Apply Hubbell's operational excellence. Expand margins by 300-500 basis points.

What makes this work is patience. Hubbell doesn't slash costs day one. They don't force product consolidation. They don't alienate customers with aggressive integration. Instead, they play the long game—gradually improving operations, slowly cross-selling products, steadily expanding margins.

The Systems Control acquisition exemplifies this. Keep the Iron Mountain facility. Keep the local workforce. Keep the brand identity. But plug it into Hubbell's purchasing power for raw materials. Use Hubbell's shipping contracts. Apply Hubbell's quality systems. Share Hubbell's customer relationships. The company stays the same but becomes more profitable.

Grid Modernization and Electrification Megatrends

Every Tesla sold makes the grid more complex. Every solar panel installed requires grid upgrades. Every wind farm built needs new transmission infrastructure. Every data center opened demands more reliable power. Every electric vehicle charger needs upgraded electrical service.

Hubbell sells the picks and shovels for all of it.

The beauty is that Hubbell wins regardless of which technology wins. Solar or wind? Both need Hubbell transformers. Hydrogen or batteries? Both need Hubbell electrical infrastructure. Centralized or distributed generation? Both need Hubbell components.

Climate change accelerates the opportunity. More extreme weather means more grid hardening. More hurricanes mean more rebuild opportunities. More heat waves mean more electrical demand. More floods mean more elevated equipment. Every climate scenario drives infrastructure investment, and infrastructure investment drives Hubbell revenue.

The Infrastructure Investment Thesis

The Infrastructure Investment and Jobs Act allocated $1.2 trillion for infrastructure. The Inflation Reduction Act added hundreds of billions more. The CHIPS Act drives semiconductor facility construction. Each requires massive electrical infrastructure investment.

But here's what's missed: Government infrastructure spending has a multiplier effect. Every federal dollar spent on transmission lines triggers state spending on distribution. Every utility upgrade triggers commercial building upgrades. Every commercial upgrade triggers residential upgrades. Hubbell captures value at every level.

The timeline favors patient capital. Infrastructure projects take 5-10 years from planning to completion. Hubbell gets specified in year 1, ships products in years 3-5, and supplies replacement parts for decades after. Today's infrastructure bill becomes next decade's revenue stream.

Why This Business Compounds

Compounding requires three things: Durability, reinvestment opportunities, and time. Hubbell has all three in abundance.

Durability comes from the installed base. Products last 20-50 years, creating decades of replacement demand. Standards change slowly, protecting existing designs. Customer relationships span generations of buyers.

Reinvestment opportunities are endless. Every acquisition expands the addressable market. Every new standard creates product opportunities. Every infrastructure trend drives growth. The company can deploy capital at high returns indefinitely.

Time is Hubbell's friend. Unlike technology companies racing against obsolescence, Hubbell's products become more entrenched over time. The longer a standard exists, the harder it becomes to change. The bigger the installed base, the stronger the replacement cycle. The more complex the grid, the more valuable Hubbell's expertise.

The Aggregation Theory Applied

Ben Thompson's Aggregation Theory usually applies to digital platforms, but Hubbell has built an analog version. By aggregating demand from thousands of contractors and distributors, Hubbell gains power over suppliers. By aggregating supply from hundreds of acquired companies, Hubbell gains power over customers.

The aggregation creates a two-sided network. Manufacturers want access to Hubbell's distribution. Distributors want access to Hubbell's products. Neither side can easily defect because the other side depends on Hubbell's network. It's a platform business disguised as a manufacturing company.

The Anti-Disruption Moat

Clay Christensen's disruption theory suggests incumbents get displaced by simpler, cheaper alternatives that gradually move upmarket. But Hubbell has structured itself to be disruption-proof.

Electrical products can't start simple and move upmarket—they must meet code from day one. There's no "minimum viable outlet" that's good enough for early adopters. Every product must be safe, certified, and reliable from the start. This eliminates the disruptor's usual entry point.

The distributed customer base prevents disruption from another angle. Hubbell doesn't depend on a few large customers who might defect. Instead, it serves thousands of contractors, distributors, and utilities. A disruptor would need to convert the entire ecosystem simultaneously—an impossible coordination problem.

The Hidden Platform Dynamics

What Hubbell has really built is a platform, but not in the software sense. It's a physical platform where different players in the electrical ecosystem can interact efficiently.

Manufacturers use Hubbell's platform to reach customers. Distributors use it to access products. Contractors use it to source materials. Utilities use it to maintain infrastructure. Each participant makes the platform more valuable for others.

The platform dynamics create winner-take-all effects in narrow niches. Once Hubbell dominates hospital-grade outlets, competitors can't achieve the scale to compete. Once Hubbell owns substation automation, rivals can't match the R&D investment. Each niche becomes a defensible kingdom within the empire.

This is the power law at work: small advantages compound into insurmountable leads. A 10% market share advantage becomes 20%, then 40%, then 80%. The winner doesn't just win—they win everything worth winning. And in the boring world of electrical infrastructure, Hubbell keeps winning by default.

IX. Bear Case & Risks

Every investment thesis needs a pre-mortem—what could kill this story? For Hubbell, the risks aren't existential, but they're real enough to temper expectations.

Cyclical Exposure to Construction and Utility Spending

The bear case starts with the cycle. Construction spending drives 40% of Hubbell's revenue. When construction stops, Hubbell's growth stops. We saw this in 2008-2009 when revenue dropped 20% as construction projects froze. The installed base provides ballast, but it can't offset a construction collapse.

Utility spending, another 40% of revenue, seems stable until it isn't. Utilities are regulated monopolies, but regulators can deny rate increases, defer capital projects, or mandate spending cuts. California's PG&E bankruptcy showed that even essential utilities can face financial distress. When utilities cut capital spending, Hubbell's backlog evaporates.

The current environment masks this cyclicality. Infrastructure spending is booming, interest rates are stabilizing, and reshoring drives industrial construction. But cycles turn. When they do, Hubbell's premium multiple could compress violently. A company trading at 22x earnings could quickly trade at 15x if growth disappears.

Competition from Low-Cost Manufacturers

Chinese manufacturers have destroyed margins in countless industries. Why not electrical components? The threat is real and growing. Chinese companies already dominate consumer electrical products. They're moving upstream into commercial and industrial markets.

The standard defense—"our products meet U.S. codes"—is weakening. Chinese manufacturers now build to U.S. specifications. They're getting UL certifications. They're establishing U.S. distribution. They're hiring American engineers. The quality gap that protected Hubbell is narrowing.

Price becomes the battleground, and Hubbell can't win on price. A Chinese manufacturer with 60% lower labor costs and government subsidies can undercut Hubbell by 30% and still make money. Once price becomes the only differentiation, margins collapse.

The tariff protection is temporary. Political winds change, trade deals get negotiated, and tariffs fade. When 25% tariffs on Chinese electrical products disappear, Hubbell faces a wave of competition it hasn't seen in decades.

Technology Disruption Risks

Wireless power transmission sounds like science fiction until it isn't. Multiple companies are developing ways to transmit power without wires. If successful, it obsoletes billions in electrical infrastructure. Every outlet, every wire, every connector becomes unnecessary.

DC power grids represent another disruption vector. Modern devices run on DC power. Solar panels generate DC power. Batteries store DC power. Yet we convert everything to AC for transmission, then back to DC for use. Emerging DC grid technologies could bypass traditional AC infrastructure entirely.

Smart buildings with integrated electrical systems could eliminate discrete components. Instead of thousands of outlets and switches, buildings could have unified power management systems. Software replaces hardware. Intelligence replaces infrastructure. Hubbell's mechanical products become anachronisms.

Even within traditional infrastructure, technology threatens margins. 3D printing enables on-demand part production. IoT sensors enable predictive maintenance, reducing replacement cycles. Software-defined power systems reduce hardware complexity. Each innovation chips away at Hubbell's moat.

Integration Risks from Aggressive M&A

Hubbell has acquired 14 companies in recent years, including two $1.1 billion deals. Integration risk compounds with each acquisition. Cultural clashes, system incompatibilities, customer defections, key employee departures—any could derail the strategy.

The Aclara acquisition brings particular risk. Smart meters and software are different from mechanical components. Software requires continuous updates, cybersecurity vigilance, and rapid innovation. Hubbell's deliberate, engineering-driven culture might struggle with software's pace of change.

Systems Control represents different integration challenges. Keeping the Iron Mountain facility sounds strategic until you realize it's 600 miles from any other Hubbell facility. Maintaining separate operations increases costs and complexity. But consolidating risks losing the local expertise that made the acquisition valuable.

Debt levels are rising to fund acquisitions. While still investment-grade, the balance sheet isn't as fortress-like as it was. If acquisitions disappoint, if synergies don't materialize, if multiples were too high, Hubbell could face a debt-driven reckoning.

Valuation Concerns at Current Multiples

At 22x earnings and 3.7x revenue, Hubbell trades at premium multiples for an industrial company. The valuation assumes continued growth, margin expansion, and successful acquisitions. Any disappointment could trigger multiple compression.

Compare to historical valuations. Hubbell traded at 12-15x earnings for most of the 2000s. The current premium reflects infrastructure enthusiasm and low interest rates. When enthusiasm fades or rates rise further, multiples could revert to historical means. That's 30-40% downside from multiple compression alone.

The market might be extrapolating temporary trends. Infrastructure spending won't last forever. Grid modernization will eventually modernize. Electrification will reach saturation. When growth slows to GDP-plus, does Hubbell deserve a premium multiple?

Regulatory and Standards Changes

Hubbell benefits from electrical standards, but standards can change. The transition from Type A to Type B outlets in Europe shows how new standards can obsolete entire product lines. If the U.S. adopted European electrical standards, Hubbell's installed base advantage evaporates.

Environmental regulations pose rising risks. Electrical products contain copper, plastics, and rare earth elements. Mining restrictions, recycling mandates, or material bans could increase costs or force product redesigns. The EU's aggressive environmental regulations often become global standards.

Grid modernization might bypass traditional infrastructure. If regulators mandate microgrids, distributed generation, or alternative technologies, Hubbell's transmission and distribution products lose relevance. The regulatory push for resilience might favor new technologies over traditional infrastructure upgrades.

Labor regulations and union dynamics add complexity. Many Hubbell facilities are unionized. Labor disputes, strikes, or organizing drives could disrupt production. Rising minimum wages and benefit costs pressure margins. The tight labor market gives workers unprecedented bargaining power.

ESG and Sustainability Pressures

The electrical industry faces increasing ESG scrutiny. Mining for copper and rare earth elements causes environmental damage. Manufacturing processes consume energy and generate emissions. End-of-life disposal creates waste. Activist investors and regulators demand accountability.

Climate change paradoxically threatens the infrastructure Hubbell builds. More extreme weather damages electrical equipment faster. Flooding destroys substations. Heat waves stress transformers. Ice storms topple transmission lines. Climate adaptation might require entirely new infrastructure approaches that obsolete current products.

The sustainability transition might reduce electrical demand. Energy efficiency improvements reduce consumption. Distributed generation reduces transmission needs. Demand response systems reduce peak loads. Each efficiency gain reduces the infrastructure investment required.

The Hidden Fragility

The biggest risk might be complacency. Hubbell has succeeded for 136 years by doing the same things well. But past success doesn't guarantee future results. The company's culture, optimized for stability and quality, might struggle to adapt to rapid change.

The distributed business model that provides resilience also prevents rapid transformation. Thousands of SKUs across dozens of facilities serving fragmented markets—it's a system optimized for stability, not agility. When change comes, Hubbell might move too slowly.

The bear case isn't that Hubbell fails dramatically. It's that Hubbell fades gradually. Growth slows. Margins compress. Multiples contract. The stock becomes dead money for a decade. Not a catastrophe, but not the compound machine investors expect.

These risks are real, but they're also why the opportunity exists. If Hubbell were risk-free, it would trade at 30x earnings. The risks create the discount that makes the investment interesting. The question isn't whether risks exist—it's whether you're being paid enough to bear them.

X. Bull Case & Opportunity

But here's why the bears are wrong, or at least early. The bull case for Hubbell isn't about explosive growth or disruption—it's about inexorable trends that play out over decades, not quarters.

Infrastructure Spending Tailwinds

The Infrastructure Investment and Jobs Act isn't just big—it's transformational. $1.2 trillion over 10 years, with $73 billion specifically for power infrastructure. That's before counting the Inflation Reduction Act's $370 billion in clean energy incentives or the CHIPS Act's semiconductor facility buildout.

But the real story is the multiplier effect. Federal infrastructure spending triggers state matching funds. State projects trigger local upgrades. Public investment crowds in private capital. A dollar of federal spending becomes three dollars of total investment. Hubbell captures value at every level.

The spending is also sticky. Infrastructure projects, once started, rarely stop. They're too visible, too political, too essential. Even in recessions, infrastructure spending continues because it's seen as stimulus. This isn't discretionary spending that disappears in downturns—it's countercyclical investment that accelerates in weakness.

Grid Modernization Imperative

America's electrical grid is ancient. The average substation is 40 years old. Most transmission lines were built in the 1960s. Distribution infrastructure dates from the post-war boom. It all needs replacement, regardless of economic cycles or political changes.

The Texas freeze of 2021 exposed the grid's fragility. California's rolling blackouts highlighted capacity constraints. Hurricane damage grows more severe annually. Each failure accelerates investment in grid hardening, redundancy, and modernization. Hubbell supplies the components for all of it.

Grid modernization isn't optional—it's existential. Without reliable electricity, the modern economy stops. Data centers go dark. Hospitals lose power. Manufacturing halts. The cost of grid failure now exceeds the cost of grid investment by orders of magnitude. This dynamic ensures decades of spending regardless of other factors.

Electrification of Everything

Every electric vehicle adds electrical load equivalent to an entire house. Every heat pump replaces a gas furnace. Every data center demands megawatts of reliable power. Every bitcoin mined consumes electricity. The electrification megatrend is really dozens of trends converging.

Transportation electrification alone drives massive infrastructure investment. Not just EV chargers, but upgraded service panels, distribution transformers, and transmission capacity. A typical gas station becoming an EV charging hub requires the electrical capacity of a small factory. Multiply that by 150,000 gas stations.

Building electrification is accelerating. Cities are banning natural gas in new construction. Heat pumps are replacing furnaces. Induction cooktops are replacing gas stoves. Each conversion requires electrical upgrades—new panels, circuits, and components. Hubbell makes them all.

Industrial electrification represents the biggest opportunity. Electric arc furnaces replacing blast furnaces. Electric heating replacing steam systems. Electrified processes replacing combustion. Each industrial conversion is a multi-million-dollar electrical infrastructure project.

Pricing Power from Critical Infrastructure Position

When ConEd needs a substation component, they don't shop on Amazon. When a hospital needs code-compliant outlets, they don't buy the cheapest option. When a data center needs reliable power infrastructure, price is secondary to reliability. This is Hubbell's pricing power—selling to customers who can't afford to fail.

Pricing was positive in both segments in Q4, with more than 1 point overall. We expect favorable pricing to continue across the portfolio. In an inflationary environment, Hubbell passes through costs plus margin. Customers accept it because the alternative—system failure—is unthinkable.

The pricing power compounds. Each year's price increases become the new baseline. Over a decade, 2% annual price increases compound to 22% higher prices. Meanwhile, manufacturing efficiency improves, scale economies develop, and margins expand. It's a beautiful business model hidden in boring products.

Revenue Forecast Growth Acceleration

Revenue forecast to grow 5.9% p.a. over next 3 years vs 8.6% for electrical industry. This apparent underperformance is actually conservative guidance that Hubbell consistently beats. Management sandbagging creates opportunity for those who understand the business.

The organic growth drivers are accelerating. Grid investment cycles last 10-20 years, and we're in year 2. Electrification is in the first inning. Infrastructure spending has barely begun. Reshoring of manufacturing is creating new industrial demand. Each trend supports mid-to-high single-digit growth for years.

Acquisition-driven growth adds another layer. With $1.5 billion in annual free cash flow and modest leverage, Hubbell can do a major acquisition annually. Each deal adds 5-10% to revenue while expanding margins through synergies. Organic plus acquired growth could sustain 8-10% top-line expansion.

Consolidation Opportunities Remain

The electrical equipment industry remains fragmented. Hundreds of small manufacturers serve niche markets. Family-owned companies lack succession plans. Private equity portfolios need exits. Hubbell is the natural acquirer for all of them.

The acquisition pipeline is robust. Every month, investment bankers pitch Hubbell on potential targets. The company can be selective, choosing only deals that fit strategically and financially. With patient capital and operational expertise, Hubbell can pay fair prices and still create value through integration.

The consolidation endgame is powerful. As Hubbell approaches dominant share in key categories, its bargaining power increases exponentially. Suppliers must prioritize Hubbell's orders. Customers have fewer alternatives. Pricing power expands. Margins widen. The strong get stronger.

Resilience Through Cycles

Hubbell generated record profits every year from 1961 to 1983—through Vietnam, oil crises, stagflation, and recessions. The resilience comes from diversity—geographic, product, and customer. When one area weakens, others compensate.

The installed base provides ballast. Even in severe recessions, electrical infrastructure needs maintenance. Outlets fail. Transformers age. Storms damage equipment. Code changes mandate upgrades. This replacement demand provides a revenue floor that pure construction companies lack.

Counter-cyclical dynamics help too. When the economy weakens, government infrastructure spending often increases as stimulus. Utilities, with regulated returns, maintain capital programs through cycles. The non-residential construction that drives Hubbell is less volatile than residential construction.

The Hidden AI and Data Center Boom

Every ChatGPT query consumes electricity. Every AI model training run demands megawatts. Every autonomous vehicle requires edge computing. The AI revolution is really an electrical infrastructure revolution, and Hubbell provides the picks and shovels.

Data center construction is exploding. Microsoft alone is spending $50 billion annually on data centers. Each facility requires sophisticated electrical infrastructure—switchgear, transformers, backup power systems, specialized cooling. Hubbell supplies much of it, often sole-sourced due to specifications and reliability requirements.

The edge computing buildout multiplies the opportunity. Instead of a few massive data centers, we're building thousands of edge facilities. Each needs electrical infrastructure. Each represents a Hubbell sales opportunity. The distributed nature plays to Hubbell's strength in serving fragmented markets.

The Inflation Beneficiary Paradox

While most companies fear inflation, Hubbell benefits from it. Higher copper prices? Pass them through with a markup. Rising labor costs? Justify price increases. Supply chain inflation? Add surcharges. Hubbell's essential products allow it to stay ahead of inflation.

The replacement cost dynamic amplifies this. As inflation drives up the cost of new infrastructure, the value of existing infrastructure rises. Utilities earn regulated returns on asset values. Higher asset values mean higher allowed earnings. Higher earnings mean more capital investment. More investment means more Hubbell sales.

Operational Leverage at Inflection Point

After years of investment in systems, processes, and integration, Hubbell is hitting an operational inflection point. The unified go-to-market strategy is reducing sales costs. Shared manufacturing is improving utilization. Integrated supply chains are reducing working capital.

Each margin improvement drops directly to the bottom line. A 100 basis point margin improvement on $5.6 billion in revenue is $56 million in additional profit. At a 20x multiple, that's $1.1 billion in market value creation. The operational improvements already underway could add $3-5 billion in market capitalization.

The ESG Tailwind Nobody Sees

While ESG creates challenges, it also creates opportunities. Grid modernization to support renewable energy is an ESG imperative. Electrification to reduce emissions is an ESG goal. Resilient infrastructure for climate adaptation is an ESG necessity. Hubbell enables all of it.